000801 understanding asset swapped convertible option transactions msdw

TRANSCRIPT

Global ConvertiblesProduct Guide

MORGAN STANLEY DEAN WITTER

This Memorandum is based upon information available to the public. No representation is made that it is accurate or complete. This Memorandum is not an offer to buy or sell or a solicitation of an offer to buy or sell the securities mentioned herein. Morgan Stanley &Co International and others associated with it may have positions in, and may effect transactions in, securities of companies mentioned herein and may also perform or seek to perform investment banking services for those companies.

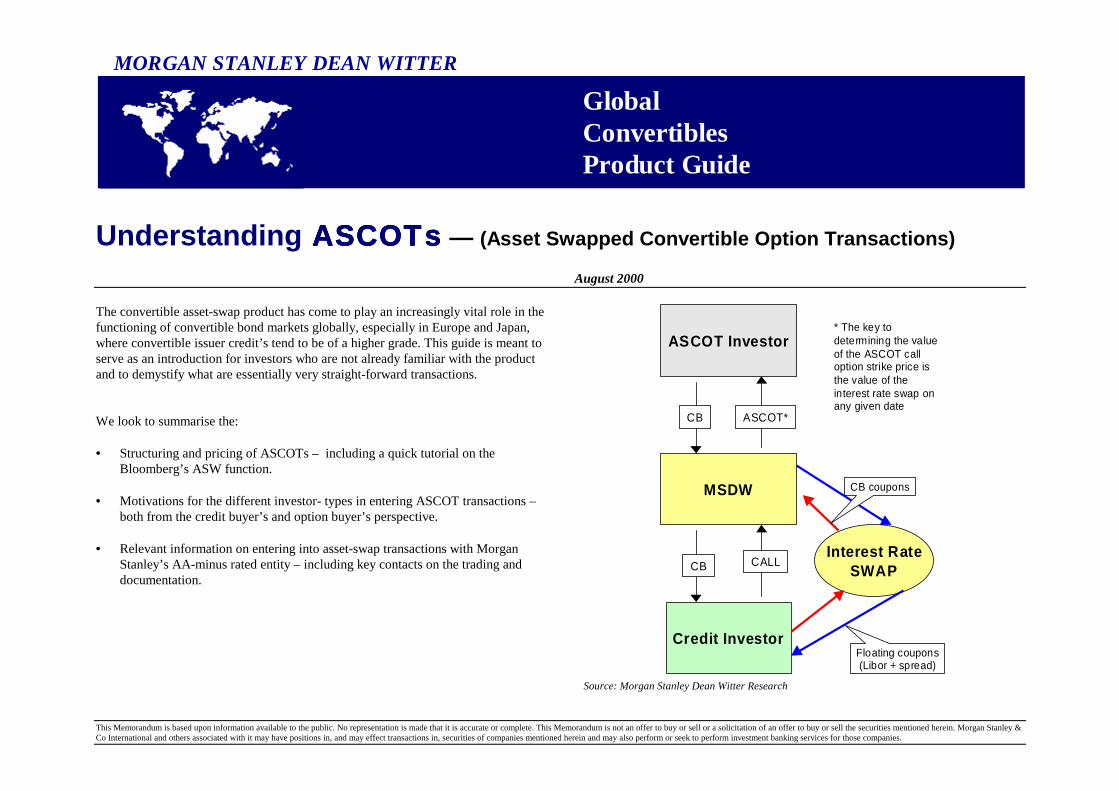

Understanding ASCOTsASCOTsASCOTsASCOTs — (Asset Swapped Convertible Option Transactions)

August 2000

The convertible asset-swap product has come to play an increasingly vital role in thefunctioning of convertible bond markets globally, especially in Europe and Japan,where convertible issuer credit’s tend to be of a higher grade. This guide is meant toserve as an introduction for investors who are not already familiar with the productand to demystify what are essentially very straight-forward transactions.

We look to summarise the:

• Structuring and pricing of ASCOTs – including a quick tutorial on theBloomberg’s ASW function.

• Motivations for the different investor- types in entering ASCOT transactions –both from the credit buyer’s and option buyer’s perspective.

• Relevant information on entering into asset-swap transactions with MorganStanley’s AA-minus rated entity – including key contacts on the trading anddocumentation.

Credit Investor

MSDW

Interest RateSWAP

ASCOT*

* The key todetermining the valueof the ASCOT calloption strike price isthe value of theinterest rate swap onany given date

ASCOT Investor

CALL

CB

CB

CB coupons

Floating coupons(Libor + spread)

Source: Morgan Stanley Dean Witter Research

MORGAN STANLEY DEAN WITTER

This Memorandum is based upon information available to the public. No representation is made that it is accurate or complete. This Memorandum is not an offer to buy or sell or a solicitation of an offer to buy or sell the securities mentioned herein. Morgan Stanley &Co International and others associated with it may have positions in, and may effect transactions in, securities of companies mentioned herein and may also perform or seek to perform investment banking services for those companies.

2

Index of Contents

Section Topic Page1. Development of the Market 22. Splitting a Convertible Bond 33. Who are the Investors ? 34. What does the Credit Investor get ? 45. What does the ASCOT Investor get ? 46. Mechanics of the Transaction 57. Option Call Features 68. Strike Price Features 69. The Bloomberg Calculator 710. The Leverage Effect – Example 711. Protection against Credit Widening – Example 812. Documentation 813. Sample Confirmation 914. Morgan Stanley Contacts 10

Appendix – Indicative Swap Levels

1. Development of the Market

Asset swaps within the fixed income markets experienced explosive growth duringthe 1990’s due to a surge in investor appetite for bonds packaged with swaps tocreate synthetic floating rate securities. They are now an established part of theworld’s credit markets. The global convertible market has taken advantage of thisand convertibles now form a significant part of the corporate asset swap sector.

Convertible bond asset swaps involve the restructuring of convertible bonds intosynthetic debt securities and equity call options. In this way they offer theopportunity for different investors to participate in the separate attractivecharacteristics embedded in convertible bonds and have, by implication, widenedthe appeal of this asset class to a broader group of investors.

Asset swaps play an important role in the pricing and sizing of convertible bondsin both the primary and secondary markets. No pricing discussion of a potentialnew issue occurs nowadays without a thorough assessment of the appetite for theasset swapped bonds. Spread discussion is referenced to the relevant swap curves(LIBOR EurIBOR etc.), therefore it is no longer practical to value convertibles ona spread-to-government bonds basis, particularly as swap/government spreadshave become increasingly volatile themselves.

The development of the asset swap market has contributed greatly to ability ofcompanies to issue large sized deals into the market and has also been partlyresponsible for the explosive growth in hedge funds investing in convertible bondswhose ability to run large positions has been enhanced by the risk reduction thatthis product offers.

There are no official statistics, but we estimate that in excess of $50 billionnotional has been asset swapped over the past 3 years alone in the Japanese,European, Asian and American convertible bond markets.

This guide offers a summary of some of the reasons why investors participate inthis product. It looks at the mechanics of the transactions and highlights some ofthe key issues to be aware of. Included in the appendix, we provide indicativelevels, across a wide spectrum of convertibles, of credit spreads based on ouractual experience in the marketplace, both recent and historical.

MORGAN STANLEY DEAN WITTER

This Memorandum is based upon information available to the public. No representation is made that it is accurate or complete. This Memorandum is not an offer to buy or sell or a solicitation of an offer to buy or sell the securities mentioned herein. Morgan Stanley &Co International and others associated with it may have positions in, and may effect transactions in, securities of companies mentioned herein and may also perform or seek to perform investment banking services for those companies.

3

2. Splitting a Convertible Bond

Asset swapping is the splitting of a convertible bond into it’s two separatecomponents. These are then purchased by investors seeking separate return profiles.These two components can be reassembled at any time at the option of the equitycomponent holder.

Exhibit 1Hellenic Finance/National Bank of Greece 2% due 07/2003

0

20

40

60

80

100

120

140

5,000 10,000 15,000 20,000 25,000

Convertible Value

Nat'l Bank of Greece (Stock Price)

Conversion Price = Drachma 19,937

The optionality of convertibles ensures that the equity drives valuation as the stock price rises above the fixed CB conversion price

Hellenic/NBG CBcurrently tradesat 101, with the stock @ 17,000

Credit Component

EquityComponent

Credit Component: Equity Component:• = Pure Bond Value = Call Option = the ASCOT• The credit investor buys Synthetic

Floating Rate NoteThe equity investor buys CB call option(ASCOT)

• Benefits to investor include access to awider choice of credits as well astypically higher spreads than in othercorporate bond markets.

Benefits to investor include off-balancesheet treatment and ability to eliminatecredit risk exposure to the issuer.

3. Who are the Investors?

The Credit Component – Convertible bond asset swaps offer the corporate creditbuyer greater spreads than are available in the FRN, Bank Finance and SyndicatedLoan Markets and give access to a more diverse range of borrowers.

� Bank Corporate Lending Departments� Corporate Treasuries� Bond & Money Market Funds� Insurance Companies

The Equity Component – Convertible bond asset swaps offer the ASCOT buyera pure and leveraged play on the underlying equity of a convertible bond whileeliminating credit risk and giving an improved interest rate risk profile

� Hedge Funds� Convertible Funds� Institutional Equity Investors� Retail Investors

MORGAN STANLEY DEAN WITTER

This Memorandum is based upon information available to the public. No representation is made that it is accurate or complete. This Memorandum is not an offer to buy or sell or a solicitation of an offer to buy or sell the securities mentioned herein. Morgan Stanley &Co International and others associated with it may have positions in, and may effect transactions in, securities of companies mentioned herein and may also perform or seek to perform investment banking services for those companies.

4

4. What does the Credit Investor Get?

The credit investor receives a higher spread than is normally available on moretraditional investments. He also gains access to a wider range of corporate creditswhere there may be limited opportunity in the market to purchase conventionalproducts. In return he accepts the feature which allows the ASCOT holder to recallthe asset swap package at any time. He also accepts the lower liquidity inherent withthis being a structured package.

Exhibit 2Current Euribor-plus Spreads Available on Different Forms of Vivendi Credit(May 2000)

+ 85bp

+ 75bp

+ 65bp

+ 35bp

0

10

20

30

40

50

60

70

80

90

Bank Debt Straight Debt Credit Derivative CB Asset Swap

bp over Euribor

Source: Morgan Stanley Dean Witter Research

5. What does the ASCOT Investor get?

� Leverage – ASCOTs give the same upside exposure to direct investment inconvertible bonds but with a smaller initial outlay. This is particularly attractive toleveraged hedge funds.

� Zero Credit Risk – There have been many examples of convertible bondswhose theoretical bond floors have failed to hold due to deteriorating creditcircumstances. ASCOTs lock in the bond floor.

� Off Balance Sheet Financing – Transferring the ownership of convertiblebonds but retaining the ASCOT successfully achieves an off-balance sheetposition financed at a rate defined by LIBOR plus the recall spread

� Improved Interest Rate Risk Profile – Convertible bond positions havenegative Rho. If rates rise the pure bond value falls but with ASCOTs the strikeprice declines thereby offsetting the fall in value of the bond.

� Purer Access to Cheap Pricing Volatility – ASCOTs provide the final pieceof the hedging jigsaw. Hedging equity, interest rate and credit risk allows investorsto capture effectively the cheap implied volatility of a convertible bond with noloss in liquidity.

MORGAN STANLEY DEAN WITTER

This Memorandum is based upon information available to the public. No representation is made that it is accurate or complete. This Memorandum is not an offer to buy or sell or a solicitation of an offer to buy or sell the securities mentioned herein. Morgan Stanley &Co International and others associated with it may have positions in, and may effect transactions in, securities of companies mentioned herein and may also perform or seek to perform investment banking services for those companies.

5

6. Mechanics of the Transaction

The Credit Buyer is effectively buying a callable synthetic floating rate note:-

� The investor purchases from Morgan Stanley an asset swap package whichcomprises a notional amount of convertible bonds, the asset, coupled with an interestrate swap. The price paid is typically 100% of notional.

� The interest rate swap agreement is for the investor to pay Morgan Stanley thefixed coupons of the convertible bond (2% from Exhibit 3) in return for receivingquarterly floating rate coupons set at EurIBOR (or LIBOR) + the agreed spread(EurIBOR +40bp from Exhibit 3).

� The future cash flows on the fixed leg of the swap (CB coupons) are typicallylower than those on the floating leg. By discounting all these future cash flows bythe zero coupon curve implied in the swap curve we can calculate the Net PresentValue of the swap (in this illustration, that comes to 6.60% of the notional). ThisNPV typically has a negative value to Morgan Stanley reflecting the excess in valueof payments owing over receivable payments.

� Morgan Stanley retains an option to repurchase the entire package, bonds plusswap, from the credit investor at 100% plus accrued interest.

The ASCOT Buyer is effectively buying an OTC call option to purchase aConvertible Bond:-

� Assuming the ASCOT investor already owns convertible bonds, he will sell thosebonds at a price which is calculated by subtracting the NPV of the interest rate swapfrom 100% of the notional value of the bonds. This can be viewed as the pure bondfloor.

� Morgan Stanley has therefore purchased bonds at one price and sold them to thecredit buyer at 100%. The difference between these two is the swap NPV (6.60%)and by keeping this Morgan Stanley is able to meet its obligation on the swappayments i.e. it pays for the shortfall of the payments made on the floating legversus the payments received on the fixed leg.

Exhibit 3Typical Asset-Swap Transaction Flowchart:Illustrates the Hellenic Finance/National Bank of Greece 2% due 07/2003

Credit Investorbuys CBs @ 100%

MSDWsells ASCOT @ 0%

MSDWbuys ASCOT @ 0%

Equity Investorsells CBs @ 93.10

(€uribor +50bp)

Fixed 2% Coupon

Floating Coupons of 3 month €uribor +40bp

Market Value of CBs(currently 101%)

ASCOT Intrinsic Valueof 7.60%*

(with €uribor +40bp strike)

* The ASCOT buyer sells CBs @ 93.10 (euribor +50) but his strike price immediately becomes 93.40 (euribor +40). Th is reflects the bid/offer spread of entering into the transaction. The intrinsic value of the ASCOT becomes 7.60 (101 less 93.40)

Source: Morgan Stanley Dean Witter

� The ASCOT investor simultaneously purchases at zero cost from MorganStanley an option to repurchase the convertible bonds. The strike price is set at100% minus the unwind value of the associated interest rate swap on the date ofexercise.

� The option strike price is therefore floating rather than fixed. The unwind valueof the swap is the Net Present Value of the remaining fixed and floating cash flowsof the interest rate swap. The strike price thus increases/decreases as interest ratesfall/rise. At maturity however the strike price is 100%

� The ASCOT is an individually negotiated contract with Morgan Stanley and hasno public secondary market. It can however be reassigned to a third party subjectto consent.

MORGAN STANLEY DEAN WITTER

This Memorandum is based upon information available to the public. No representation is made that it is accurate or complete. This Memorandum is not an offer to buy or sell or a solicitation of an offer to buy or sell the securities mentioned herein. Morgan Stanley &Co International and others associated with it may have positions in, and may effect transactions in, securities of companies mentioned herein and may also perform or seek to perform investment banking services for those companies.

6

7. Option Call Features

� An ASCOT is an American-style over-the-counter call option to repurchase aconvertible bond.

� The holder may exercise at any time but there may be restrictions for exercisingwithin the first six months.

� Bonds will be delivered back to the ASCOT holder for value date a maximum 10(but typically less) days following exercise.

� The expiry date of the option is set to match either the maturity date or the putdate of the underlying convertible bond.

� If the Issuer calls the convertible bonds for early redemption under the terms andconditions of the bonds then automatic exercise of the ASCOT is triggered wherebythe holder must repurchase the bonds. This avoids the potential scenario of missingthe final date for conversion of bonds to equity.

� If the Issuer of the bonds defaults, the ASCOT will expire 10 days later.

8. Strike Price Features

� The strike price can be viewed as the pure bond value and is therefore subject tointerest rate movements. In a stable interest rate environment the strike price risessteadily towards the convertible bond redemption price over time.

� The spread of the reference swap which determines the strike price is agreed atthe opening of the ASCOT position. This spread is typically 10-20bp tighter thanthe spread used to determine the initial sale price of the bonds to Morgan Stanleyand should be viewed as the Bid/Offer cost of the transaction.

� The floating strike is by no means the only structure employed in creatingASCOTs. Options can also be structured with fixed strikes or strike pricesreferenced to a fixed yield to maturity. Such structures are subject to acceptanceby the credit investor.

� The ‘ASW’ security specific function on Bloomberg for each individualconvertible bond provides an accurate tool for calculating the strike price (see thefollowing page).Exhibit 4: Illustration of the Interest Rate/Strike Price Relationship

96.2

94.8

92

90.6

93.4

90

91

92

93

94

95

96

97

4.0 4.5 5.0 5.5 6.0 6.5 7.0 7.5

Effective Strike Price (@ Euribor +40bp)

3 month Euribor Rates (%)

As rates rise,the strike price will fall

Source:Morgan Stanley Dean Witter Research

MORGAN STANLEY DEAN WITTER

This Memorandum is based upon information available to the public. No representation is made that it is accurate or complete. This Memorandum is not an offer to buy or sell or a solicitation of an offer to buy or sell the securities mentioned herein. Morgan Stanley &Co International and others associated with it may have positions in, and may effect transactions in, securities of companies mentioned herein and may also perform or seek to perform investment banking services for those companies.

7

9. The Bloomberg Calculator

The ‘ASW’ function on Bloomberg for a single convertible bond allows the user tocalculate the strike price of an ASCOT from a given credit spread. In the case of theHellenic Finance / National Bank of Greece bond, by entering the 50bp spread, wederive 93.1 as the effective level at which the ASCOT buyer sells the CBs. Thestrike is calculated on the offer spread (40bp), equating to a strike of 93.4, using thesame methodology.

Exhibit 4: Illustration of the ASW Function on Bloomberg

10. The Leverage Effect

Leveraged gains are attractive to all types of investors so long as they do notassume extra risk. For a considerably smaller outlay the same exposure to aconvertible bond position can be achieved through ASCOTs.Take the following example of ASCOTs in the Japanese electronics companyNEC purchased by some of our clients at a timely moment in June 1999. Bypaying less than 4 points for ASCOTs the buyer had an option on a convertiblewith a 60 % premium. The subsequent rise in NEC’s fortunes have provided ahandsome return to the ASCOT holder.

Exhibit 5NEC #6 1.8% 2002

June 1st May 1st1999 2000 Return

Stock Price 1336 3090 +131%

CB Price 104.00 156.00 +52%

Premium 60% 4% -

Implied Vol . 24% 46% -

STRIKE (+80bp) 100.60 101.00 -

ASCOT Price 3.40 55.00 +1,518%

Source: Morgan Stanley Dean Witter Research

Change the floatingleg to quarterly

payments(by entering 4)

Ensure that the Defaultswap curve is set to

#45 if EUR; #23 if USD#13 if JPY; #22 if GBP

Set the calculationmode to 1 (to Calculate

Bond Price)

The ASCOT buyereffectively sells the CBsat this interpolated price

(93.1 in this case)

Enter the spreadat which the

swap is beingexecuted

Set the Bid/Ask side ofthe curve to use;

A – for initial set upB – for recalling bonds

MORGAN STANLEY DEAN WITTER

This Memorandum is based upon information available to the public. No representation is made that it is accurate or complete. This Memorandum is not an offer to buy or sell or a solicitation of an offer to buy or sell the securities mentioned herein. Morgan Stanley &Co International and others associated with it may have positions in, and may effect transactions in, securities of companies mentioned herein and may also perform or seek to perform investment banking services for those companies.

8

11. Protection against Credit Widening

ASCOTs not only provide convertible investors with protection against the ultimatecredit risk of issuer default, but also protect against any credit widening which canhave a significant impact on the valuation of a convertible bond.

The following is an example of how a holder of ASCOTs fared relative to a holderof the Fullerton/Singapore Telecom 0% 2003 exchangeable bonds during the latestAsian crisis in 1998.

Exhibit 6Fullerton / Singapore Telecom 0% 2003

Issue Date: March 1998STOCK Price: S$ 3.2CB Price: 100CB Premium: 8%Strike (L+50): 94ASCOT Purchase Price: 6

A few months later: Sept. 1998(in the height of the Asian crisis)Stock Price: S$ 2.5CB Price: 86 (L+200)CB Premium: 18%Strike (L+50): 94.5ASCOT Intrinsic Price: 0ASCOT Market Price*: 4

Loss on CB: 14 pointsIntrinsic Loss on ASCOT: 6 pointsReal Loss on ASCOT: 4 points

Source: Morgan Stanley Dean Witter Research

The holder of the exchangeable bonds lost 14 points during the period underreview while the ASCOT holder suffered less. The bond price declined to 86,which was an implied credit spread of +200, proving convincingly that the debtspread assumptions used in convertible bond models should not be viewed as astatic input. The intrinsic loss on the ASCOT was its full 6 points if valued only asthe difference between the strike price and the CB price. Obviously an ASCOT ofa bond which only carries an 18% premium has to have a value greater than zero.Based on option models and conservative volatility assumptions the market pricedthese ASCOTs to have a real value of 4 points; thus the decline in ASCOT valuewas limited to only 2 points.

12. Documentation

� Transactions are negotiated with MSIL, Morgan Stanley’s operating entity,under ISDA guidelines for swaps & OTC options.

� MSIL (Morgan Stanley International Ltd.) is a member of the UK regulatingbody, the Financial Services Authority (FSA).

� All new counterparties are required to have capacity & authority documentsapproved by MSIL before a transaction can be executed.

� All counterparties are required to enter into an ISDA Master Agreement withMSIL.

� MSIL is guaranteed by Morgan Stanley Dean Witter & Co. (Aa3/AA-).

� MSIL dispatches ISDA confirmations for each transaction which need to besigned and returned.

� Morgan Stanley Prime Brokerage offers equity financing services for hedgedASCOT positions.

MO

RGAN

STANLEY D

EAN W

ITTER

Convertible Bond Asset Swap - Draft Confirm

ation – ASCOT Buyer

To:

Attn.:

Fax No:

From:

Morgan Stanley + C

o. International Lim

ited, London. M

ember of FSA

.

Date:

Our File R

ef:O

ur Swap R

ef:Taps R

ef:

Re:

Convertible Bond C

all and Notional Sw

ap Transaction between M

organ Stanley + Co.

International Lim

ited and

The purpose of this facsimile (this ''C

onfirmation'') is to confirm

the terms and conditions of the

bond option transaction and notional swap transaction entered into betw

een Morgan Stanley + C

o.International Lim

ited and you on the Trade Date specified below

(respectively, the ''Bond O

ptionTransaction'' and the ''N

otional Swap Transaction''; together the ''Transaction''). This C

onfirmation

constitutes a ''Confirm

ation'' as referred to in the ISDA

Master A

greement specified below

.

The definitions and provisions contained in the 1991 ISDA

Definitions (as supplem

ented by the1998 Supplem

ent, and as amended and supplem

ented by the 1998 ISDA

EUR

O D

efinitions) (the''Sw

ap Definitions'') and in the 1997 ISD

A G

overnment B

ond Option D

efinitions (the ''Bond

Definitions'', and together w

ith the Swap D

efinitions, the ''Definitions''), in each case as published

by the International Swaps and D

erivatives Association, Inc., are incorporated into this

Confirm

ation. The Bond D

efinitions apply in relation to the Bond O

ption Transaction (paragraphs2 and 3(1) below

). For purposes of the Bond D

efinitions, the Bond O

ption Transaction will be

deemed to be a G

overnment B

ond Option Transaction. The Sw

ap Definitions apply in relation to

the Notional Sw

ap Transaction (paragraph 4 below). In the event of any inconsistency betw

eeneither set of D

efinitions and this Confirm

ation, this Confirm

ation will govern.

This Confirm

ation supplements, form

s part of and is subject to, the ISDA

Master A

greement dated

as of ,as amended and supplem

ented from tim

e to time (the ''A

greement''), betw

een Morgan Stanley

+ Co. International Lim

ited and you. All provisions contained in the A

greement govern this

Confirm

ation except as expressly modified below

).

The Terms of the Transaction to w

hich this Confirm

ation relates are as follows:

1.G

eneral Term

s:

Party A:

Morgan Stanley + C

o. InternationalLim

ited

Party B:

Trade Date:

Time of execution of the transaction is

available upon request.

2.Term

s of Bond Option Transaction:

Terms of B

ond Option Transaction as follow

s:

Option Style:

Am

erican

Option Type:

Call

Seller:Party A

Buyer:

Party B

Bonds:

Stock Redem

ption:Should the Redem

ption be for Stock, as provided in the Terms

and Conditions of the B

onds, Party B w

ill pay to Party A a

USD

amount equal to the R

edemption A

mount of the

Bonds, and Party A

will deliver to Party B

the Redeem

edBonds. This is providing Party A

notify Party B of the StockR

edemption by at least Three (3) London and N

ew Y

orkB

usiness Days Prior to the 25 A

ugust 2003 Bond M

aturityD

ate.

Bond M

aturityD

ate:

Investor PutD

ate:

Num

ber ofO

ptions:

Option

Entitlement:

Option Strike

Price:100.00 PC

T.

Option

Penalty:If the O

ption is Exercised for a Settlement D

ate prior to thenParty B

will m

ake an Additional Paym

ent to Party A of the

present value of X basis points on the notional am

ountaccruing from

the Settlement D

ate until

Premium

:U

SD 1.00 (R

eceipt of which is hereby acknow

ledged)

Premium

Payment

Date:

Procedure for Exercise:

Multiple

Exercise:A

pplicable

Exercise Period:A

ny Seller Business D

ay during the period comm

encing onand including the Prem

ium Paym

ent Date and ending on and

including the Expiration Date betw

een 8.30 a.m. and 4.00

p.m. (London tim

e).

Seller Business

Day:

Any day on w

hich comm

ercial banks are open for business(including dealings in foreign exchange and foreign currencydeposits) in

Expiration Date:

The first to occur of:

(a) The date on w

hich notice is first given to the Holder

of the Bonds by the issuer of the B

onds that any ofthe B

onds which are the subject of this B

ond Option

Transaction are for any reason called or redeemed by

the issuer of the Bonds (expiration is lim

ited to theN

umber of O

ptions proportionate to the percentageof B

onds called or redeemed by the issuer of the

Bonds), and

(b) The Investor Put D

ate, and

(c) The B

ond Maturity D

ate, and

(d) D

efault Date

''Holder of the B

onds'' means, at any given tim

e, the holderas determ

ined by the Calculation A

gent in its sole discretion,

of a nominal am

ount of the Bonds equal to the O

ptionEntitlem

ent.

''Event of Default'' m

eans that in the event that (i) either theTrustee for the H

older of the Bonds, notified the issuer of

the Bonds of the occurrence of a default w

hich with the

giving of notice or the lapse of time or both, w

ould become

an Event of Default (as defined in the term

s of the Bonds),

and he issuer does not cure such default within the tim

especified after receipt or (ii) there is an Event of D

efault (asdefined in the term

s of the Bonds), and either the Trustee forthe H

older of the Bonds, or the H

older of the Bonds, by

notice to the issuer declares the Bonds to be due and payableim

mediately or (iii) there is an Event of D

efault (as definedin the term

s of the Bonds), and the B

onds become

imm

ediately due and payable without any declaration or

other act on the part of the Trustee for the Holder of the

Bonds, or the H

older of the Bonds, B

uyer must w

ithin thirty(30) B

usiness Days of such Event of D

efault, and subject toany restrictions on transfer thereunder, deliver irrevocablenotice of exercise to Seller, otherw

ise this Option w

ill expirethirty (30) B

usiness Days follow

ing such Event of Default

such thirtieth Business D

ay, the''D

efault Date''

Expiration Time:

4.00 p.m. (London tim

e)

Exercise Date:

The Seller Business D

ay (which shall also be a C

learanceSystem

Business D

ay) during the Exercise Period on which

Buyer

exercises the

Option,

subject to

The notice

requirements and other term

s specified in or pursuant to thisC

onfirmation

Notice of Exercise

and Written

Confirm

ation:A

pplicable, provided that Buyer must give notice of exercise

in writing addressed to A

lexandra MacG

regor (Derivatives

Products Group) at least ten (10) Seller B

usiness Days prior

to Exercise Date betw

een the hours of 8.30 a.m. and 4.00

p.m. (London tim

e).

Autom

aticExercise:

The applicable Options w

ill be deemed to be autom

aticallyexercised on the date w

hich notice is first given to theH

older of the Bonds by the issuer of the B

onds that any ofthe B

onds which are the subject of this B

ond Option

Transaction are for any reason (except for tax reasons) calledor redeem

ed bythe issuer of the B

onds in accordance with the term

s andconditions of the B

onds.

Autom

atic Exercise will be lim

ited to a Num

ber of Options

proportionate to the percentage of Bonds called or redeemed

by the Issuer for each early redemption date.

3.Settlem

ent Term

s:

(1)In relation to the B

ond Option Transaction, Physical

Settlement w

ill be applicable. For the purpose of thisparagraph 3(1), the follow

ing terms shall apply:

Settlement D

ate:The Exercise D

ate; provided, however, if the B

ond Option

Transaction is automatically exercised, the Settlem

ent Date

shall be ten (10) Seller Business Days follow

ing the ExerciseD

ate.

Clearance System

:M

organ Stanley + Co. International Lim

ited will notify youseparately regarding settlem

ent details.

Clearance System

Business D

ay:A

ny day on which the C

learance System is (or, but for the

occurrence of a Settlement D

isruption Event, would have

been) open for the acceptance and execution of settlement

instructions.

(2)In addition to the foregoing, the C

alculation Agent w

illdeterm

ine the Swap C

ash Settlement A

mount, as provided

below. If the Sw

ap Cash Settlem

ent Am

ount is a positiveam

ount, Party B w

ill pay such amount to Party A

on theExercise D

ate. If the Swap C

ash Settlement A

mount is a

negative amount, Party A

will pay the absolute value of such

amount to Party B

on the Exercise Date.

Swap C

ashSettlem

entA

mount:

An am

ount determined by the C

alculation Agent as the

amount that w

ould be payable under Section 6(e)(ii)(2) ofthe A

greement if the Settlem

ent Date had been designated as

an Early Termination D

ate in respect of a Swap Transaction

or portion thereof on the terms set out in paragraph 4 below

as a result of a Termination Event, in respect of w

hich theSw

ap Transaction was the sole A

ffected Transaction, PartiesA

and B are the A

ffected Parties and the Termination

Currency w

as, provided that (a) Market Q

uotations will be

determined by the C

alculation Agent using its estim

ates ofthe

amounts

that w

ould be

paid for

Replacem

entTransactions (as that term

is defined in the definition of''M

arket Quotation'') and (b) in the event of a dispute as to

the amount so determ

ined, the Calculation Agent shall obtain

quotations from three m

utually acceptable Reference Market

Makers w

hich will be averaged.

(3) For purposes of settlem

ent, if the Swap C

ash Settlement

Am

ount is payable by Party B, it w

ill be aggregated with the

Bond Paym

ent due from Party B

to Party A on the Exercise

Date. If the Sw

ap Cash Settlem

ent Am

ount is payable byParty A

, then the Swap C

ash Settlement A

mount w

ill bededucted from

the Bond Paym

ent due from Party B

to PartyA

on the Exercise Date, provided that if the Sw

ap Cash

Settlement A

mount exceeds the B

ond Payment, the excess

shall be payable by Party A to Party B

on the Exercise Date.

(4)The definition of ''B

ond Payment'' contained in the B

ondD

efinitions shall be amended for the purposes of this

Transaction by including the word ''zero'' in place of the

words ''accrued interest, if any, on the O

ption Entitlement

computed in accordance w

ith customary trade practices

employed w

ith respect to the Bonds''.

4.Term

s of the Notional Sw

ap Transaction:

Notional A

mount:

Effective Date:

Settlement D

ate

Termination D

ate:The Investor Put D

ate /the Bond M

aturity Date, subject to

adjustment in accordance w

ith the Following /Preceding

Modified Follow

ing / Business D

ay Convention.

Fixed Am

ounts:

Fixed Rate Payer:

Party B

Fixed Rate Payer Paym

ent Dates:

On and in each year, from

and including the first of or tooccur

after the

Effective D

ate to

and including

theTerm

ination Date, subject to adjustm

ent in accordancewith

the Following / Preceding M

odified Following / B

usinessD

ay Convention.

Fixed Am

ount: Floating A

mounts:

Floating Rate

Payer:Party A

Floating Rate Payer Paym

ent Dates:

On and in each year, from

and including the first of or tooccur

after the

Effective D

ate to

and including

theTerm

ination Date, subject to adjustm

ent in accordance with

the Modified Follow

ing Business D

ay Convention.

Floating Rate O

ption:U

SD-LIB

OR-B

BA

Designated M

aturity:3 M

onths

Spread:Plus X

PCT.

Floating Rate

Day C

ount Fraction:A

ctual/360

Reset D

ates:The first day of each Calculation Period, except for the ResetD

ate with respect to the first C

alculation Period which w

illbe the day w

hich precedes the first day of the secondC

alculation Period by the number of m

onths equal to theD

esignated Maturity.

Additional Paym

ent:The A

dditional Payment of U

SD / JPY

from Party B to Party

A should be w

ired to the Account detailed below

for value

5. C

alculation Agent:

The Calculation A

gent is Party A. A

ll determinations by the

Calculation A

gent are subject to agreement by Party A

andParty B

. If the parties are unable to agree on a particularcalculation another M

utually Acceptable C

alculation Agent,

who is a leading dealer in the relevant m

arket, will be

appointed to determine such calculation (the ''M

utuallyA

cceptable Calculation A

gent''). The expense of theM

utually Acceptable Calculation A

gent shall be borne by theparties equally.

6.A

ccount Details:

Account for Paym

ents to Party A:

Account for paym

ents to Party B:

Account for paym

ents in USD

:Please supply details

7.Party A

Docum

entation and Operation C

ontacts:

Docum

entation:Telephone Num

ber: ((0) 207) 513 7762

Operations:

Telephone Num

ber: ((0) 207) 677 7699

8.C

onfirmation:

Please confirm that the foregoing correctly sets forth the term

s of ouragreem

ent by sending to us a return facsimile substantially to the

following effect:

Quote

To:M

organ Stanley + Co. International

Limited, London

Attn.:

Alexandra M

acGregor, Lisa C

onway

Fax No:

London ((0) 207) 513 7988Telex N

o:London 8812564

From:

Date:

Your File R

ef:Y

our Swap R

ef:

Re:C

onvertible Bond C

all and Notional Sw

ap Transaction between

Morgan Stanley + C

o. International Limited and

We acknow

ledge receipt of your facsimile dated w

ith respect to theabove

referenced transaction

between

Morgan

Stanley +

Co.

International Limited and w

ith a Trade Date of and a Term

inationD

ate of and confirm that such facsim

ile correctly sets forth the terms

of our agreement relating to the transaction described therein.

Account details:

Signed:

By:

Nam

e:

Title:

Unquote

We are delighted to have entered into the above referenced transaction w

ith you, and we look

forward to w

orking with you again.

Yours faithfully,

Jack InglisA

nnabel Littlewood

Morgan Stanley + C

o. International Limited

MORGAN STANLEY DEAN WITTER

This Memorandum is based upon information available to the public. No representation is made that it is accurate or complete. This Memorandum is not an offer to buy or sell or a solicitation of an offer to buy or sell the securities mentioned herein. Morgan Stanley &Co International and others associated with it may have positions in, and may effect transactions in, securities of companies mentioned herein and may also perform or seek to perform investment banking services for those companies.

9

14. Morgan Stanley Contacts

Trading

London Jack Inglis +44 (0)20 7425 5994Annabel Littlewood +44 (0)20 7425 7763Ross Webster +44 (0)20 7425 6144 Ermes Caramaschi +44 (0)20 7425 8466

New York Jim Bedell +1 212 761 5830Tanya Ferencko +1 212 761 2654

Tokyo Jackson Chou +81 3 5424 7814Kenichi Ii +81 3 5424 7816Taro Goto +81 3 5424 7845Gavin Connor +81 3 5424 5633

Documentation

London Tracy Northey +44 (0)20 7425 5639Alexandra MacGregor +44 (0)20 7425 7762

New York Craig Abruzzo +1 212 761 5365

MORGAN STANLEY DEAN WITTER

This Memorandum is based upon information available to the public. No representation is made that it is accurate or complete. This Memorandum is not an offer to buy or sell or a solicitation of an offer to buy or sell the securities mentioned herein. Morgan Stanley &Co International and others associated with it may have positions in, and may effect transactions in, securities of companies mentioned herein and may also perform or seek to perform investment banking services for those companies.

10

Appendix – Indicative Spreads

The following is a list of indicative asset swap credit spread levels based on recent business we have seen in the marketplace or else where no recent business has beentransacted, the spreads shown are historical for illustrative purposes (notably in the Asian market). They are not firm bids nor should they be viewed as totally representativeof the spreads currently trading in the market. This is not an exhaustive list and there are inevitably a large number of issues in the convertible market for which we haveomitted to provide an indicated a credit spread. There may also be names on this list where there is no longer a credit bid available due to investors having exhausted theircredit lines or due to changing market conditions. Credit spreads are subject to supply and demand considerations as well as market sentiment. They are therefore not static.Readers should recognise that Morgan Stanley cannot find a credit bid for all the known names in the convertible universe although we will use our best endeavours to doso. Sub-investment grade issues do not typically find ready interest from credit buyers and this is particularly so in the US and Pacific Rim convertible markets which arecharacterised predominantly by such issues. Please contact your sales representative for an update on particular issues or for a general market overview.

MO

RGAN

STANLEY D

EAN W

ITTER

IssuerIssue #

Issue C

cyC

ouponM

aturityN

ext PutSpread

SectorC

ountryR

egionH

uaneng Power

USD

1.7521-M

ay-0421-M

ay-02380.00

Utilities

China

AsiaBank of East Asia

USD

2.0019-Jul-03

19-Jul-0185.00

Banks, Savings & Loan H

ong KongAsia

Far Eastern TextilesU

SD0.00

26-Jan-0526-Jan-01

175.00

Hong Kong

AsiaFirst Pacific

USD

2.0027-M

ar-02175.00

Conglom

erate H

ong KongAsia

Guangnan H

oldingsU

SD1.75

30-Jun-00310.00

Food & Beverages H

ong KongAsia

HD

FinanceU

SD6.75

01-Jun-00185.00

Real Estate

Hong Kong

AsiaH

ong Kong LandU

SD4.00

23-Feb-01136.00

Real Estate

Hong Kong

AsiaH

SH O

verseasU

SD5.00

06-Jan-01310.00

Leisure H

ong KongAsia

Hutchinson D

elta FinanceU

SD7.00

25-Nov-01

170.00

Hong Kong

AsiaKerry Properties

USD

2.0015-Jun-07

25-Mar-02

400.00R

eal Estate H

ong KongAsia

New

World D

evelopment

USD

3.0009-Jun-04

600.00R

eal Estate H

ong KongAsia

New

World Infrastructure

USD

5.0015-Jul-01

150.00Infrastructure

Hong Kong

AsiaPeregrine

USD

4.5001-D

ec-00200.00

Financial Services H

ong KongAsia

Shanghai IndustrialU

SD1.00

12-Jun-02425.00

Conglom

erate H

ong KongAsia

Shangri-La AsiaU

SD2.88

16-Dec-00

150.00Leisure

Hong Kong

AsiaSino Land

USD

4.0018-Apr-02

18-Apr-02260.00

Real Estate

Hong Kong

AsiaZhenhai R

efiningU

SD3.00

19-Dec-03

19-Dec-01

375.00O

il & Energy H

ong KongAsia

Polymax

USD

2.0027-Feb-06

27-Feb-01200.00

Housing & C

onstructionIndonesia

AsiaD

aewoo C

orpC

HF

0.1331-D

ec-0190.00

Trading Korea

AsiaKorea Electric Pow

erU

SD5.00

01-Aug-01140.00

Utilities

KoreaAsia

LG Electronics

USD

0.2531-D

ec-0708-Jul-02

100.00Sem

iconductors Korea

AsiaR

ashid Hussain

USD

1.5030-Jun-07

30-Jun-02375.00

Banks, Savings & Loan M

alaysiaAsia

Telekom M

alaysiaU

SD4.00

03-Oct-04

60.00Telecom

munications

Malaysia

AsiaYTL

USD

0.0015-Aug-02

15-Aug-00225.00

Infrastructure M

alaysiaAsia

JG Sum

mit

USD

3.5023-D

ec-03175.00

Real Estate

PhilippinesAsia

DBS Land

USD

2.0031-D

ec-01150.00

Real Estate

SingaporeAsia

Fullerton Global

USD

0.0002-Feb-03

130.00Telecom

munications

SingaporeAsia

Keppel Corp

USD

2.0012-Aug-03

175.00C

onglomerate

SingaporeAsia

Natsteel

USD

3.0030-Jun-02

200.00C

onglomerate

SingaporeAsia

Wing Tai

USD

1.5015-Jul-02

200.00R

eal Estate Singapore

AsiaAD

I Corp

USD

1.5008-Jul-03

08-Jul-01175.00

Com

puter Peripherals Taiw

anAsia

China Petrochem

icalU

SD1.00

08-May-08

08-May-03

300.00O

il & Energy Taiw

anAsia

CM

C M

agneticsU

SD1.00

06-Oct-04

06-Oct-02

350.00Electronics

Taiwan

AsiaD

elta ElectronicsU

SD0.00

15-Feb-0515-Feb-01

185.00C

omputer Peripherals

Taiwan

AsiaFirst International C

omputer

USD

0.0016-O

ct-0218.00

Com

puter Peripherals Taiw

anAsia

Formosa C

hemical

USD

1.7519-Jul-01

125.00C

hemicals

Taiwan

AsiaG

VC C

orpU

SD0.00

21-May-02

20.00C

omputer Peripherals

Taiwan

AsiaPou C

henU

SD1.50

15-Jun-0615-Jun-02

300.00R

etail Taiw

anAsia

Siliconware Precision

USD

0.5021-Jul-04

21-Jul-02225.00

Electronics Taiw

anAsia

Robinson D

epartment Store

USD

3.2527-Jul-00

25.00R

etail Thailand

AsiaTotal Access C

omm

unicationsU

SD2.00

31-May-06

31-May-01

140.00Telecom

munications

ThailandAsia

United C

omm

unicationsU

SD7.78

15-Dec-03

165.00Telecom

munications

ThailandAsia

Bank AustriaEU

R0.00

14-Oct-04

15-Oct-01

25.00Banks, Savings & Loan

AustriaEurope

ArbedD

EM3.25

30-Oct-04

70.00M

etals Belgium

EuropeG

BLD

EM2.50

09-Jul-0340.00

Financial Services Belgium

EuropeKBC

DEM

2.5010-D

ec-0575.00

Banks, Savings & Loan Belgium

EuropeM

etsa SerlaU

SD4.38

15-Oct-02

100.00Paper & Packaging

FinlandEurope

AccorEU

R1.00

29-Mar-02

53.00Leisure

FranceEurope

Artemis

EUR

1.5022-Feb-05

87.50R

etail France

EuropeBouygues

EUR

1.7001-Jan-06

80.00H

ousing & Construction

FranceEurope

Carrefour

EUR

2.5001-Jan-04

40.00Food & Beverages

FranceEurope

Financiere AgacheEU

R0.00

23-Apr-0467.00

Food & Beverages France

EuropeFrance Telecom

EUR

2.0001-Jan-04

50.00Telecom

munications

FranceEurope

France TelecomEU

R4.13

29-Nov-04

50.00Telecom

munications

FranceEurope

PinaultEU

R1.50

01-Jan-0365.00

Retail

FranceEurope

ScorEU

R1.00

01-Jan-0542.00

Insurance France

EuropeST M

icroelectronicsU

SD0.00

22-Sep-0922-Sep-04

105.00Electronics

FranceEurope

Suez Lyonnaise des EauxEU

R0.00

01-Jan-0450.00

Utilities

FranceEurope

Suez Lyonnaise des EauxEU

R2.88

12-Jan-0461.00

Utilities

FranceEurope

Usinor

EUR

3.8801-Jan-05

95.00M

etals France

EuropeVivendi

EUR

1.5001-Jan-05

80.00U

tilities France

EuropeVivendi

EUR

1.2501-Jan-04

70.00U

tilities France

EuropeVivendi

EUR

1.0005-Jul-03

115.00U

tilities France

EuropeAllianz

DEM

3.0004-Feb-03

21.00Insurance

Germ

anyEurope

AllianzEU

R2.00

23-Mar-05

22.00Insurance

Germ

anyEurope

Deutsche Bahn

DEM

1.1302-Apr-03

40.00Transportation

Germ

anyEurope

Deutsche Bank

EUR

2.0022-D

ec-0325.00

Banks, Savings & Loan G

ermany

EuropeD

eutsche BankC

HF

1.0026-Jul-01

18.00Banks, Savings & Loan

Germ

anyEurope

Deutsche Bank

USD

0.0012-Feb-17

12-Feb-0228.00

Banks, Savings & Loan G

ermany

EuropeD

usseldorf Stadtwerke

DEM

2.5025-Aug-03

40.00M

unicipalG

ermany

EuropeKam

psEU

R0.00

17-Mar-15

17-Mar-03

205.00Food & Beverages

Germ

anyEurope

Metro

DEM

0.0009-Jul-13

09-Jul-0350.00

Retail

Germ

anyEurope

Nordrhein-W

estfalenD

EM2.13

03-Dec-02

15.00M

unicipalG

ermany

EuropeEFG

EUR

2.0004-M

ay-0560.00

Banks, Savings & Loan G

reeceEurope

National Bank of G

reeceEU

R2.00

15-Jul-0338.00

Banks, Savings & Loan G

reeceEurope

Matav

USD

0.7502-Jul-01

10.00Telecom

munications

Hungary

Europe

MO

RGAN

STANLEY D

EAN W

ITTER

IssuerIssue #

Issue C

cyC

ouponM

aturityN

ext PutSpread

SectorC

ountryR

egionAutogrill

EUR

0.0016-Jun-14

15-Jun-04105.00

Restaurants

ItalyEurope

Banca di Rom

aITL

3.5002-Jan-01

52.50Banks, Savings & Loan

ItalyEurope

EdizioneITL

2.0008-Jul-03

84.00C

onsumer Products

ItalyEurope

Finmeccanica

EUR

2.0008-Jun-05

130.00Italy

EuropeM

ediobancaITL

0.0018-D

ec-0135.00

Banks, Savings & Loan Italy

EuropeM

ediobancaITL

1.5018-D

ec-0345.00

Banks, Savings & Loan Italy

EuropeAhold

NLG

3.0030-Sep-03

150.00Food & Beverages

Netherlands

EuropeC

regem Finance

USD

2.7506-Jan-04

18.00Banks, Savings & Loan

Netherlands

EuropeFortis

NLG

2.6306-N

ov-0336.00

Financial Services N

etherlandsEurope

FortisEU

R1.50

29-Jul-0460.00

Financial Services N

etherlandsEurope

VNU

NLG

2.7515-Apr-05

150.00Publishing

Netherlands

EuropeVN

UEU

R1.75

15-Nov-04

115.00Publishing

Netherlands

EuropePortugal Telecom

EUR

1.5007-Jun-04

35.00Telecom

munications

PortugalEurope

Banco SantanderEU

R2.00

06-Aug-0350.00

Banks, Savings & Loan Spain

EuropeBBV

EUR

0.0030-Jul-02

25.00Banks, Savings & Loan

SpainEurope

TelefonicaU

SD2.00

15-Jul-0555.00

Telecomm

unications Spain

EuropeAventis

EUR

2.7529-Jul-03

52.00C

hemicals

Switzerland

EuropeAventis

EUR

3.2522-O

ct-0365.00

Chem

icals Sw

itzerlandEurope

Ciba Speciality C

hemicals

USD

1.2524-Jul-03

55.00C

hemicals

Switzerland

EuropeC

lariantC

HF

1.0019-Aug-02

80.00C

hemicals

Switzerland

EuropeH

olderbankC

HF

0.0028-Jul-14

28-Jul-0260.00

Housing & C

onstructionSw

itzerlandEurope

Holderbank

CH

F1.00

14-May-04

40.00H

ousing & Construction

Switzerland

EuropeM

eridianEU

R1.50

25-Nov-04

25-Nov-01

60.00H

uman R

esources Sw

itzerlandEurope

Moevenpick

DEM

0.0011-Feb-13

11-Feb-0350.00

Leisure Sw

itzerlandEurope

Roche

JPY0.25

25-Mar-05

45.00D

rugs & Biotechnology Sw

itzerlandEurope

Roche

USD

0.0019-Jan-15

19-Jan-0435.00

Drugs & Biotechnology

Switzerland

EuropeSw

iss AirC

HF

0.1307-Jul-05

64.38Air Transportation

Switzerland

EuropeSw

iss AirU

SD2.25

10-Jun-0418.00

Insurance Sw

itzerlandEurope

Swiss Life

USD

2.0020-M

ay-0330.00

Insurance Sw

itzerlandEurope

Swiss Life

CH

F1.00

20-May-05

35.00Insurance

Switzerland

EuropeSw

iss LifeEU

R2.00

20-May-03

40.00Insurance

Switzerland

EuropeSw

iss Re

NLG

1.2523-Jun-03

23.00Insurance

Switzerland

EuropeU

BSU

SD2.75

16-Jun-0225.00

Banks, Savings & Loan Sw

itzerlandEurope

AirtoursG

BP5.75

05-Jan-04220.00

Leisure U

KEurope

BAAG

BP4.88

29-Sep-0440.00

Air Transportation U

KEurope

British LandG

BP6.50

17-Nov-07

80.00R

eal Estate U

KEurope

Capital Shopping

GBP

6.2531-D

ec-06150.00

Real Estate

UK

EuropeD

aily Mail & G

eneral TrustG

BP2.50

05-Oct-04

90.00M

edia U

KEurope

Ham

merson

GBP

6.5012-Jun-06

175.00R

eal Estate U

KEurope

National G

ridG

BP4.25

17-Feb-0863.00

Utilities

UK

EuropeP & O

USD

6.0010-M

ay-0475.00

Transportation U

KEurope

PatheEU

R3.00

24-Nov-03

125.00M

edia U

KEurope

Railtrack

GBP

3.5018-M

ar-0960.00

Transportation U

KEurope

Standard Chartered

EUR

4.5030-M

ar-10130.00

Banks, Savings & Loan U

KEurope

United N

ews & M

ediaG

BP6.13

03-Dec-03

90.00Publishing

UK

EuropeAcom

euroJPY

0.0031-M

ar-0290.00

Financial Services Japan

JapanAjinom

oto9

JPY1.90

29-Mar-02

51.00Food & Beverages

JapanJapan

All Nippon Air

euroJPY

0.7531-M

ar-1531-M

ar-03100.00

Air Transportation Japan

JapanAlps Electric

2JPY

2.0029-M

ar-02170.00

Electronics Japan

JapanAsahi Brew

eries10

JPY1.00

26-Dec-03

95.00Food & Beverages

JapanJapan

Asahi Glass

5JPY

1.9026-D

ec-0889.00

Industrial Products Japan

JapanBank of Fukuoka

2JPY

1.1028-Sep-07

161.00Banks, Savings & Loan

JapanJapan

Bank of Tokyo-Mitsubishi

euroJPY

4.2531-M

ar-03160.00

Banks, Savings & Loan Japan

JapanBank O

f Tokyo-Mitsubishi

euroU

SD3.00

30-Nov-02

30.00Banks, Savings & Loan

JapanJapan

Best Denki

4JPY

1.9028-Feb-02

70.00R

etail Japan

JapanC

apcom2

JPY0.80

28-Sep-01173.00

Electronics Japan

JapanC

hiba Bank3

JPY0.00

30-Mar-03

60.00Banks, Savings & Loan

JapanJapan

Chiyoda Fire and M

arine3

JPY0.80

31-Mar-03

48.00Insurance

JapanJapan

Chiyoda Fire and M

arine4

JPY0.70

30-Mar-01

25.00Insurance

JapanJapan

Chubu Electric Pow

er4

JPY1.00

31-Mar-06

31.00U

tilities Japan

JapanC

hugai Pharm5

JPY1.10

30-Mar-06

80.00H

ealth & Personal Care

JapanJapan

Chugai Pharm

6JPY

1.0530-Sep-08

100.00H

ealth & Personal Care

JapanJapan

Chugai Pharm

3JPY

1.7028-Jun-02

52.00H

ealth & Personal Care

JapanJapan

CM

K3

JPY0.70

30-Sep-05142.00

Electronics Japan

JapanD

ai Nippon Printing

5JPY

1.5031-M

ay-0230.00

Publishing Japan

JapanD

ai Nippon Printing

8JPY

1.8030-Sep-03

83.00Publishing

JapanJapan

Daiichi Kangyo Bank

euroU

SD3.88

30-Sep-04120.00

Banks, Savings & Loan Japan

JapanD

aiichi Pharmaceutical

4JPY

1.8029-Sep-00

34.00H

ealth & Personal Care

JapanJapan

Dainippon Screen

1C

HF

0.2530-Sep-00

130.00Electronics

JapanJapan

Daiw

a Securities11

JPY1.40

29-Aug-0370.00

Financial Services Japan

JapanD

aiwa Securities

16JPY

0.5029-Sep-06

145.00Financial Services

JapanJapan

Ebaraeuro

JPY0.13

30-Sep-0445.00

Industrial Products Japan

JapanFuji C

o.1

JPY0.90

31-Aug-01100.00

Retail

JapanJapan

Fuji Heavy

4JPY

0.9030-Sep-03

179.00Autom

otive Japan

JapanFutaba

3JPY

0.3030-Sep-03

48.00Industrial Products

JapanJapan

Gunm

a Bank4

JPY0.45

28-Sep-0154.50

Banks, Savings & Loan Japan

Japan

MO

RGAN

STANLEY D

EAN W

ITTER

IssuerIssue #

Issue C

cyC

ouponM

aturityN

ext PutSpread

SectorC

ountryR

egionH

ankyu Corp

euroJPY

1.5030-Sep-06

30-Sep-03150.00

Transportation Japan

JapanH

ankyu Departm

ent Store1

JPY2.00

30-Sep-0041.00

Retail

JapanJapan

Hanshin Electric

7JPY

4.8030-M

ar-0140.00

Transportation Japan

JapanH

iroshima Bank

3JPY

0.4030-Sep-03

72.00Banks, Savings & Loan

JapanJapan

Hitachi

5JPY

1.7029-Sep-02

40.00C

onsumer Electronics

JapanJapan

Hitachi

6JPY

1.3030-Sep-03

41.00C

onsumer Electronics

JapanJapan

Hitachi

7JPY

1.4030-Sep-04

46.00C

onsumer Electronics

JapanJapan

Hitachi M

etals12

JPY1.90

29-Mar-02

30.00M

etals Japan

JapanH

oriba2

JPY0.85

17-Mar-06

153.50Instrum

entation Japan

JapanItochu

1JPY

0.0030-M

ar-01140.00

Trading Japan

JapanKagaw

a1

JPY0.00

28-Sep-0185.00

Banks, Savings & Loan Japan

JapanKanegafuchi C

hemical

6JPY

1.8031-M

ar-0362.00

Chem

icals Japan

JapanKanegafuchi C

hemical

7JPY

1.8028-Sep-01

43.00C

hemicals

JapanJapan

Kanegafuchi Chem

ical8

JPY1.80

30-Sep-0463.00

Chem

icals Japan

JapanKansai Electric Pow

er2

JPY2.00

29-Mar-02

15.00U

tilities Japan

JapanKansai Electric Pow

er3

JPY1.40

31-Mar-05

17.00U

tilities Japan

JapanKaw

asaki Heavy

3JPY

0.8028-Sep-01

38.00Autom

otive Japan

JapanKaw

asaki Heavy

4JPY

0.9030-Sep-03

37.00Autom

otive Japan

JapanKeihan Electric R

ailway

6JPY

1.0031-M

ar-0333.00

Transportation Japan

JapanKeihin Electric Express

18JPY

1.5029-Sep-02

90.00Transportation

JapanJapan

Keisei Electric Rail

31JPY

0.9030-Sep-02

134.00Transportation

JapanJapan

Keisei Electric Rail

32JPY

0.4530-Sep-04

109.50Transportation

JapanJapan

Kinki Nippon R

ailway

6JPY

1.0031-M

ar-0870.00

Transportation Japan

JapanKinki N

ippon Railw

ay5

JPY0.70

31-Mar-03

47.00Transportation

JapanJapan

Kokusai Securitieseuro

JPY0.25

30-Sep-1430-Sep-04

70.00Financial Services

JapanJapan

Koyo Seiko7

JPY0.50

03-Mar-03

150.00Industrial Products

JapanJapan

Kubota Corp

4JPY

1.5029-Sep-00

36.50Industrial Products

JapanJapan

Kubota Corp

5JPY

1.5528-Sep-01

40.00Industrial Products

JapanJapan

Kubota Corp

6JPY

1.6030-Sep-02

41.00Industrial Products

JapanJapan

Kubota Corp

7JPY

0.8030-Sep-03

38.00Industrial Products

JapanJapan

Kuraray6

JPY2.20

29-Sep-0257.00

Consum

er Products Japan

JapanLintec

3JPY

0.2031-M

ar-0575.00

Instrumentation

JapanJapan

Marubeni

8JPY

0.8531-M

ar-06170.00

Trading Japan

JapanM

arui7

JPY1.40

31-Jan-0399.00

Retail

JapanJapan

Matsom

oto2

JPY1.20

30-Mar-01

145.00Trading

JapanJapan

Matsushita Electric Industrial

5JPY

1.3029-M

ar-0233.00

Consum

er Electronics Japan

JapanM

atsushita Electric Industrial6

JPY1.40

31-Mar-04

37.00C

onsumer Electronics

JapanJapan

Matsushita Electric W

orks8

JPY2.70

31-May-05

59.00H

ousing & Construction

JapanJapan

Matsushita Electric W

orks9

JPY1.00

30-Nov-05

48.00H

ousing & Construction

JapanJapan

Matsushita Electric W

orks7

JPY4.30

30-Nov-00

70.00H

ousing & Construction

JapanJapan

Minebea

3JPY

0.8031-M

ar-0383.00

Industrial Products Japan

JapanM

inebea4

JPY0.65

31-Mar-05

90.00Industrial Products

JapanJapan

Mitsubishi Electric

4JPY

2.0030-Sep-03

57.00Electrical Equipm

ent Japan

JapanM

itsubishi Logistics3

JPY1.90

31-Mar-03

75.00Transportation

JapanJapan

Mitsubishi M

otor1

JPY0.40

31-Mar-03

35.50Autom

otive Japan

JapanM

itsui & Co

6JPY

1.0530-Sep-09

58.50Trading

JapanJapan

Mitsui M

arine & Fire1

JPY2.10

29-Mar-02

12.00Insurance

JapanJapan

Mitsui M

arine & Fire3

JPY0.70

31-Mar-03

82.00Insurance

JapanJapan

Mitsui M

ining & Smelting

euroJPY

0.0030-Sep-03

135.00Instrum

entation Japan

JapanM

itsui Mining & Sm

elting1

JPY0.40

30-Sep-03114.00

Mining

JapanJapan

Mitsum

i Electric3

JPY0.40

31-Mar-03

225.00Electronics

JapanJapan

Mizuno C

orp7

JPY0.55

28-Sep-0150.00

Consum

er Products Japan

JapanN

agoya Bank2

JPY0.35

30-Sep-0383.50

Banks, Savings & Loan Japan

JapanN

agoya Rail

7JPY

1.0531-M

ar-0671.00

Transportation Japan

JapanN

ankai Electric Rail

1JPY

2.7030-M

ar-0177.00

Transportation Japan

JapanN

EC C

orp6

JPY1.80

29-Mar-02

43.00Electrical Equipm

ent Japan

JapanN

EC C

orp7

JPY1.90

31-Mar-04

56.00Electrical Equipm

ent Japan

JapanN

EC C

orp9

JPY1.90

30-Mar-01

114.00Electrical Equipm

ent Japan

JapanN

EC System

seuro

JPY0.38

31-Mar-02

135.00Electrical Equipm

ent Japan

JapanN

GK Insulator

3JPY

4.5029-Sep-00

60.00Industrial Products

JapanJapan

NG

K Spark Plug4

JPY1.30

29-Mar-02

93.00Industrial Products

JapanJapan

Nichido Fire & M

arine4

JPY0.90

30-Mar-01

45.00Insurance

JapanJapan

Nichido Fire & M

arine5

JPY1.00

31-Mar-03

50.00Insurance

JapanJapan

Nichiei

euroJPY

1.7531-M

ar-1431-M

ar-04200.00

Financial Services Japan

JapanN

idec Corp

2JPY

0.8031-M

ar-06208.00

Electrical Equipment

JapanJapan

Nidec C

orp3

JPY0.50

31-Mar-04

115.00Electrical Equipm

ent Japan

JapanN

idec Corp

euroJPY

0.1331-M

ar-03110.00

Electrical Equipment

JapanJapan

Nippon D

enso4

JPY1.60

20-Dec-02

56.00Electrical Equipm

ent Japan

JapanN

ippon Express4

JPY1.00

31-Mar-04

45.00Transportation

JapanJapan

Nippon M

ining & Metals

JPY0.00

30-Sep-04175.00

Mining

JapanJapan

Nippon Yusen

9JPY

2.0029-Sep-00

80.00Transportation

JapanJapan

Nishim

atsu8

JPY0.35

31-Mar-04

99.14Infrastructure

JapanJapan

Nishi-N

ippon Bank1

JPY0.20

30-Sep-0375.00

Banks, Savings & Loan Japan

JapanN

isshin Fire & Marine

1JPY

0.6531-M

ar-0474.92

Insurance Japan

JapanN

isshin Oil M

ills3

JPY1.00

30-Mar-01

50.00Food & Beverages

JapanJapan

Nissho Iw

ai1

JPY0.65

30-Sep-0340.50

Trading Japan

Japan

MO

RGAN

STANLEY D

EAN W

ITTER

IssuerIssue #

Issue C

cyC

ouponM

aturityN

ext PutSpread

SectorC

ountryR

egionN

TN C

orp5

JPY0.85

31-Mar-04

45.00Industrial Products

JapanJapan

Odakyu Electric R

ail18

JPY1.60

30-Sep-0258.00

Transportation Japan

JapanO

ki Electric17

JPY2.20

31-Mar-04

122.00Telecom

Equipment

JapanJapan

Oki Electric

19JPY

1.8028-Sep-01

88.00Telecom

Equipment

JapanJapan

Okinaw

a Bank1

JPY0.30

29-Mar-02

78.00Banks, Savings & Loan

JapanJapan

Orix

euroJPY

0.3831-M

ar-0575.00

Financial Services Japan

JapanR

engo10

JPY0.45

30-Jul-07115.50

Paper & Packaging Japan

JapanR

icoh8

JPY1.50

29-Mar-02

85.00O

ffice Products Japan

JapanR

icoh9

JPY0.35

31-Mar-03

76.75O

ffice Products Japan

JapanR

iso Kagaku3

JPY1.88

31-Mar-02

120.00O

ffice Products Japan

JapanSankyo

3JPY

0.7030-M

ar-0157.00

Health & Personal C

areJapan

JapanSeino Transport

euroJPY

0.1331-M

ar-0470.00

Transportation Japan

JapanSekisui C

hemical

7JPY

0.1028-Sep-01

46.00C

hemicals

JapanJapan

Sekisui House

16JPY

0.3031-Jul-03

26.00H

ousing & Construction

JapanJapan

Sekisui House

12JPY

2.5031-Jan-02

70.00H

ousing & Construction

JapanJapan

Sekisui House

13JPY

2.4031-Jul-00

60.00H

ousing & Construction

JapanJapan

Sekisui House

15JPY

0.8031-Jul-01

53.00H

ousing & Construction

JapanJapan

Sekisui House

14JPY

0.9031-Jul-03

125.00H

ousing & Construction

JapanJapan

Sharp12

JPY1.60

30-Sep-0461.00

Semiconductors

JapanJapan

Shiga Bank2

JPY0.40

30-Sep-0369.00

Banks, Savings & Loan Japan

JapanShim

adzu13

JPY0.95

30-Sep-0560.00

Industrial Products Japan

JapanShin M

eiwa

4JPY

4.7029-Sep-00

47.00Industrial Products

JapanJapan

Showa C

orpeuro

JPY0.50

31-Mar-04

110.00Autom

otive Japan

JapanSum

itomo C

hemical

8JPY

4.7029-D

ec-0037.00

Chem

icals Japan

JapanSum

itomo C

orp2

JPY1.60

29-Mar-02

32.00Trading

JapanJapan

Sumitom

o Corp

3JPY

1.5031-M

ar-0480.00

Trading Japan

JapanSum

itomo Electric

6JPY

0.2530-Sep-08

58.00Electronics

JapanJapan

Sumitom

o Electric4

JPY2.00

28-Sep-0150.00

Electronics Japan

JapanSum

itomo M

arine & Fire4

JPY1.20

31-Mar-04

47.00Insurance

JapanJapan

Sumitom

o Marine & Fire

3JPY

1.1029-M

ar-0212.00

Insurance Japan

JapanSum

itomo W

arehouse4

JPY1.00

31-Mar-05

110.00Transportation

JapanJapan

Sysmex

1JPY

0.2031-M

ar-0489.14

Japan

JapanTanabe Seiyaku

9JPY

0.3031-M

ar-0643.00

Health & Personal C

areJapan

JapanTH

K3

JPY0.30

30-Sep-03138.00

Industrial Products Japan

JapanTokyo Electron

2JPY

0.9030-Sep-03

65.00Trading

JapanJapan

Tomy

euroJPY

0.2530-Sep-03

145.00R

etail Japan

JapanToppan Printing

7JPY

1.4031-M

ar-0544.00

Publishing Japan

JapanToyam

a Chem

ical1

JPY1.00

31-Mar-05

180.00Electronics

JapanJapan

Toyo Com

munications

2JPY

1.4030-Sep-04

194.00Electrical Equipm

ent Japan

JapanToyo Trust & Banking

euroJPY

0.7530-Sep-02

225.00Banks, Savings & Loan

JapanJapan

Toyoda Auto Loom

2JPY

0.3530-Sep-03

48.50Autom

otive Japan

JapanU

be industries3

JPY1.25

30-Sep-05172.50

Conglom

erateJapan

JapanYasuda Fire & M

arine3

JPY0.60

30-Mar-01

86.00Insurance

JapanJapan

Yasuda Trust & Bankingeuro

USD

1.7530-Sep-02

90.00Banks, Savings & Loan

JapanJapan

Yasuda Trust & Bankingeuro

USD

2.8830-Sep-03

90.00Banks, Savings & Loan

JapanJapan

Anadarko PetroleumU

SD0.00

07-Mar-20

07-Mar-03

100.00O

il & Energy U

SAU

SABell Atlantic

USD

5.7501-Apr-03

50.00Telecom

munications

USA

USA

Bell AtlanticU

SD4.25

15-Sep-0555.00

Telecomm

unications U

SAU

SAC

endant Corp

USD

3.0015-Feb-02

80.00Leisure

USA

USA

Clear C

hannel Com

ms

USD

1.5001-D

ec-02153.00

Media

USA

USA

Clear C

hannel Com

ms

USD

2.6301-Apr-03

150.00M

edia U

SAU

SAC

omm

scopeU

SD4.00

15-Dec-06

240.00Telecom

Equipment

USA

USA

Costco W

holesaleU

SD0.00

19-Aug-1719-Aug-02

75.00R

etail U

SAU

SAC

ox Com

ms

USD

0.4319-Apr-20

19-Apr-05160.00

Telecom Services

USA

USA

Elan FinanceU

SD0.00

14-Dec-18

14-Dec-03

225.00D

rugs & Biotechnology U

SAU

SAG

enerU

SD6.00

01-Mar-05

310.00U

tilities U

SAU

SAH

ealthsource Corp

USD

3.2501-Apr-03

125.00H

ealthcare U

SAU

SAH

eartportU

SD7.50

01-Oct-03

180.00R

EIT - Healthcare

USA

USA

Ingram M

icroU

SD0.00

09-Jun-1809-Jun-01

375.00Electronics

USA

USA

InterpublicU

SD1.87

01-Jun-06155.00

Advertising U

SAU

SAKerr-M

cGee

USD

5.2515-Feb-10

165.00O

il & Energy U

SAU

SALennar C

orpU

SD0.00

29-Jul-1829-Jul-03

175.00H

ousing & Construction

USA

USA

Loews

USD

3.1315-Sep-07

118.00O

il Services U

SAU

SAM

agna InternationalU

SD4.88

15-Feb-05175.00

Automotive

USA

USA

Magna International

USD

5.0015-O

ct-02150.00

Automotive

USA

USA

Mattell

USD

5.5001-N

ov-0040.00

Consum

er Products U

SAU

SAM

errill LynchU

SD2.00

14-Apr-0445.00

Food & Beverages U

SAU

SAM

errill LynchU

SD1.00

03-Mar-03

50.00D

rugs & Biotechnology U

SAU

SAO

ffice Depot

USD

0.0011-D

ec-0711-D

ec-02200.00

Office Products

USA

USA

Om

nicareU

SD5.00

11-Dec-07

175.00D

rug Distribution

USA

USA

Pep BoysU

SD0.00

20-Sep-1120-Sep-01

125.00Autom

otive U

SAU

SAR

ite AidU

SD5.25

15-Sep-02200.00

Drug D

istribution U

SAU

SASolectron

USD

0.0008-M

ay-2008-M

ay-03180.00

Electronics U

SAU

SASolectron

USD

0.0027-Jan-19

27-Jan-02195.00

Electronics U

SAU

SATelm

exU

SD4.25

15-Jun-04255.00

Telecomm

unications U

SAU

SATransocean Sedco

USD

0.0024-M

ay-2024-M

ay-03110.00

Oil & Energy

USA

USA

MO

RGAN

STANLEY D

EAN W

ITTER

IssuerIssue #

Issue C

cyC

ouponM

aturityN

ext PutSpread

SectorC

ountryR

egionU

S Cellular

USD

0.0015-Jun-15

15-Jun-00120.00

Telecomm

unications U

SAU

SAW

ellpointU

SD0.00

02-Jul-1920-Jul-02

175.00H

ealthcare U

SAU

SAXerox

USD

0.5721-Apr-18

21-Apr-0375.00

Office Products

USA

USA

Young & Rubicam

USD

3.0015-Jan-05

150.00Advertising

USA

USA

MORGAN STANLEY DEAN WITTER

This Memorandum is based upon information available to the public. No representation is made that it is accurate or complete. This Memorandum is not an offer to buy or sell or a solicitation of an offer to buy or sell the securities mentioned herein. Morgan Stanley &Co International and others associated with it may have positions in, and may effect transactions in, securities of companies mentioned herein and may also perform or seek to perform investment banking services for those companies.

11

Morgan Stanley & Co. International Limited and/or its affiliates ("Morgan Stanley Dean Witter") prepared the information and opinions accessible herein.

Morgan Stanley Dean Witter does not undertake to advise you of changes in the opinions or information contained herein. You should note the date of each report. Other Morgan Stanley Dean Witter clients mayreceive research or other information, including rating changes, before they are made available to the users of this service. Morgan Stanley Dean Witter may discontinue or suspend coverage (for legal, policy orother reasons) of any issuer without advance notice and has no obligation to inform you of such discontinuance or suspension.

Morgan Stanley Dean Witter may make markets or specialise in, have positions in and effect transactions on a principal basis in securities and other instruments mentioned and may also perform or seek toperform investment banking services for issuers of these securities and other instruments.