0 33rd apec transportation working group tokyo, japan october 10-14 2010 what actions to be taken on...

TRANSCRIPT

1

33rd APEC Transportation Working Group Tokyo, JapanOctober 10-14 2010

What actions to be taken on Japanese international shipping

~ Towards Restoration of Maritime Nation Japan~

Maritime BureauMinistry of Land, Infrastructure, Transport and Tourism

Japan

ContentsContents

1

I Current Issues II Growth Strategy on Maritime Sector III Taxation system request for the next fiscal year -Tonnage tax, -Special depreciation, -Exemption on a property replaced by purchase, etc.

IV Budgetary request for the next fiscal year -Maritime environment initiative, -Offshore wind power, -Securing and training seafarers

-海上荷動きの予測-

19951997

19992001

20032005

20072009

20112013

20152017

20192021

20232025

2027

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

1,178 1,413 1,710 2,192 2,441

2,907 3,413

3,984 4,641

181 195

209 258

262 279

294

310

326

383 462

507

644 742

791

830

868

907

190 367

398

656 821

917

989

1,061

1,135

470 526

671

853

949

1,042

1,109

1,173

1,237

1,518

1,713

1,850

1,809

2,062

2,211

2,316

2,413

2,509

497

564

742

1,100

1,781

2,177

2,523

2,894

3,289

鉄鋼石 ( 2008→2028 年で約 3 倍) 原油 (〃約 1.4 倍) 石炭 (〃約 1.5 倍) 天然ガス (〃約 1.7 倍) 石油精製品 (〃約 1.4 倍) 穀物 (〃約 1.3 倍) その他 (コンテナ含む)(〃約 2 倍)

( million metric tons )

(Source) Global Insight 3

International marine transport is a growth industryInternational marine transport is a growth industry

- Global seaborne trade volume and Japan’s merchant fleet share of that -

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

1989 1994 2001 2002 2003 2004 2005 2006 2007 2008

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

Global marine cargo volumeJapan’s merchant fleet share of transport

Global share of Japan’s merchant fleet

Year

(million tons )

15.5%

11.3%

Declining share of Japan‘s

merchant fleet

Increase of the marine cargo volume due to economic globalization

(Source) Global marine cargo volume according to Fernleys“REVIEW 2008.” Japan’s merchant fleet share of transport compiled by the Maritime Bureau of the Ministry of Land, Infrastructure, Transport and Tourism.

- Volume of the world ocean cargo movement -

Iron oreCrude oilCoalnatural gasPetroleum productsGrainOther(including container)

・ The volume of world ocean cargo movement has a tendency to increase. It is growth of 49% for the past ten years. ・ The future ocean cargoes are expected to continue increasing mainly among emerging countries like China and India.

I Current Issues

CargoCargo ratio of

Japanesemerchant fleet

Major cargoowners

Ships(special ships)

Major types of contracts

Iron ore almost 100%Iron and steel

companiesBulker

Rawcharcoal

almost 100%Iron and steel

companiesBulker

Generalcharcoal(Electriccharcoal)

over 95%Electricity/

other industriesBulker

Raw oil about 75% Oil Tankers

mostly long-termcontracts

(partly some contracts ofevery journey)

LNG about 50% Electricity/gas LNG shipslong-term contracts in

principle

Chips 100%Paper

manufacturingships only for

chipsall long-term contracts in

principle

Cars almost all Carsships only for

carshalf a year to one year

contracts

Source: Research on future international maritime transport policy by Nittsu ResearchInstitute & Nomura Research Institute (2005)

long-term contracts inprinciple

Japan’s dependence on maritime trade Ocean-going shipping has supported the industrial development of Japan

Japanese fleet has been providing services respond to needs for Japanese industries. It has borne most of imported resources and supported overseas development of Japan’s industries.

40% of domestic distribution of goods (about 80% of basic industrial goods) depends on coastal shipping

Japan ~The Maritime Nation~Japan ~The Maritime Nation~I Current Issues

Source:Trade statistics by Ministry of Finance (2008), Port and harbor statistics (2007), and Survey on trend of logistics of import/export cargoes by Ministry of Finance (September 2008)

Maritime(Containers)

11.3%

Maritime(Non-containers)

88.4%

Aviation0.3% Aviation

25.9%

Maritime(Containers)

34.6%Total tradeabout 160 trillion yen

Maritime(Non-containers)

39.4%

Total tradeabout 1.3billion tons

99.7% of Japan’s trade volume was martime trade through ports

Types of contracts specific to Japan that are not seen in Europe

4

Declining International Competitiveness of Japan’s Port ServicesDeclining International Competitiveness of Japan’s Port Services

0.86 0.94 1.0 1.1

1.3 1.4 1.5 1.6 1.7

2.0

2.3 2.4

2.8 3.0

3.5

3.9

4.3

4.8

5.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

'90 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08

億TEU

その他

欧州

北米

日本

アジア

Asia: China, Hong Kong, Indonesia, The Republic of Korea, Malaysia, Philippines, Singapore, Taiwan and Thailand North America: The United States and Canada Europe: Belgium, Denmark, Finland, France,Germany, Greece, Ireland, Italy, Netherlands, Spain, Sweden and the United Kingdom Others: Japan and other countries/regions not mentioned above

2008

World

Japan

Asia(excluding Japan)

169,640,000 TEU 502,390,000 TEU

10,520,000 TEU 18,790,000 TEU

65,270,000 TEU 233,800,000 TEU

3.0 times

1.8 times

3.6 times

Asian ports233,800,000 TEUAsian ports

65,270,000 TEU

1998

Source: Port and Harbours Bureau of MLIT, based on “Containerisation International Yearbook”

※Provisional data

※

I Current Issues

Japanese ports have lost their competitiveness compared to neighboring countries in terms of cost and convenience, etc.

Change in the volume of cargo container handled at ports

Others

Europe

North America

Japan

Asia

100 million TEU

5

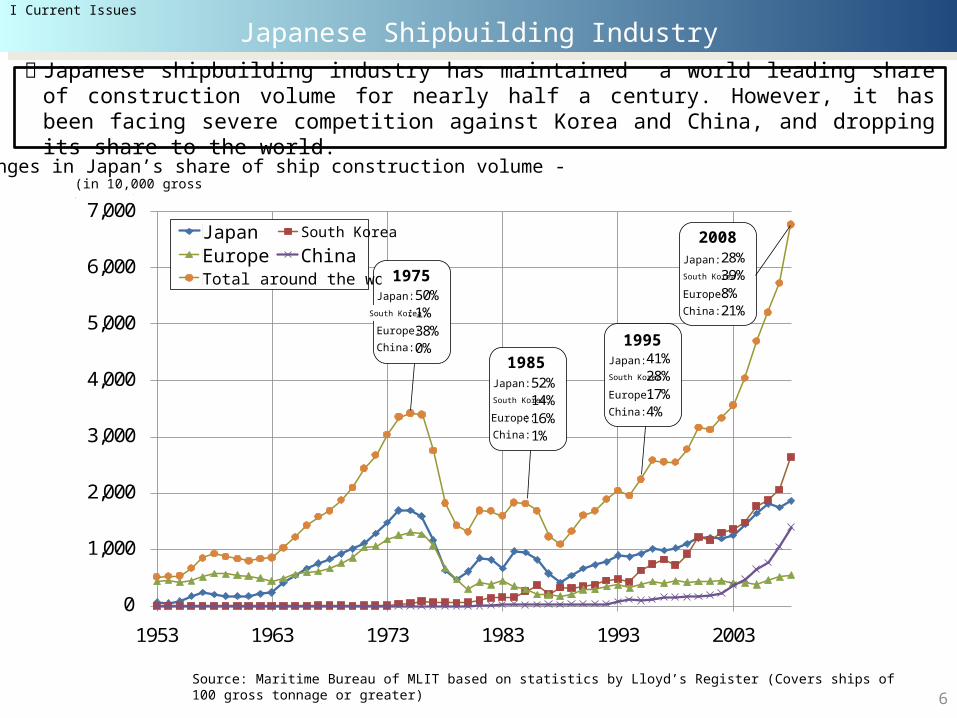

Japanese shipbuilding industry has maintained a world leading share of construction volume for nearly half a century. However, it has been facing severe competition against Korea and China, and dropping its share to the world.

- Changes in Japan’s share of ship construction volume -

Japanese Shipbuilding IndustryJapanese Shipbuilding Industry

Source: Maritime Bureau of MLIT based on statistics by Lloyd’s Register (Covers ships of 100 gross tonnage or greater)

(in 10,000 gross tonnage)

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

1953 1963 1973 1983 1993 2003

日本 韓国欧州 中国世界計 1975年

日本:50%韓国:1%欧州:38%中国:0%

1985年日本:52%韓国:14%欧州:16%中国:1%

1995年日本:41%韓国:28%欧州:17%中国:4%

2008年日本:28%韓国:39%欧州:8%中国:21%

JapanEuropeTotal around the world

South Korea

China

Japan:

Europe:

China:

Japan:South Korea:

Europe:

China:

Japan:South Korea:

Europe:

China:

Japan:South Korea:

Europe:

China:

1975

19851995

2008

South Korea:

I Current Issues

6

SeafarersJapanese seafarers:

approx. 2,600 personsForeign seafarers:

approx. 48,000 persons

Ship managementManning, Management of employees, Maintenance and repair of ships, Operation control, etc.* Required appropriate number of person commensurate with the scale of Japanese fleet.

Maritime insuranceInsurance revenue :

230 billion yen

Financial institutionLocal banks, Credit unions, commercial

banks, etc.

Market Scale:

approx. 9 trillion yen

Coastal shipping industry:

710 companies

Charterer for coastal shipping:

1,786 companies

International shipping company(Operator)approx. 210 companies (incl. owner-operator)

approx. 6,000 employeesBusiness profit : 5.1 trillion yen

Charterer for international shipping(Owner)approx. 1,100 companies (incl. owner-operator)

approx. 1,400 employees (estimated)

Provision of ships(Charter contract)

60% for domestic consumption *1

40% forexports

29% forexports

88% of the fleet are procured domestically

12%Overseas

procurement

Shipbuilding industryapprox. 1,200 companiesapprox. 85,000 employees

Business profit: approx. 2.3 trillion yen

Ship machinery industryapprox. 650 companies

approx. 42,000 employeesBusiness profit: approx. 1.3 trillion yen

*1 Completion volume basis*2 Production value basis

Seafarers for coastal shipping:

22,000 persons

Transport of goods(Carriage contract)

7

Ripple effect on maritime cluster from growth of international shipping industryRipple effect on maritime cluster from growth of international shipping industry- Market scale of international shipping industry in Japan is approximately five trillion yen. It

forms a maritime cluster by closely connecting with shipbuilding and ship-machinery industries, etc.

- It is expected that growth of Japanese international shipping industry, which procures 90% of its fleet from domestic ship-building industry, will bring great ripple effect on them.

Shippers

71% for domestic consumption *2

95% of ship equipment are procured domestically

I Current Issues

● The scope of Tonnage Tax ●taxation system on vessel acquisition / possession

8

The competitive condition being less advanced on Maritime TransportThe competitive condition being less advanced on Maritime Transport

・ Shipping companies depend on the taxation system of the main office located in a country. The taxation system of each country influences directly with the competitiveness of the national merchant fleet. ・ European countries have introduced tonnage tax for enhancing the international competitiveness conditions for national merchant fleets and adopted the taxation systems with the aim of securing a certain national flag vessels as the core of shipping policy.

I Current Issues

fixed asset taxregistration

license tax/charge

The depreciation system for vessels

The scope of depreciation for 5 years (including ratio of special depreciation)

Japan Impose 100 67.5%(including special depreciation18%)

United Kingdom no tax 0.7 76.00%

France no tax 0 80.82%

United States Impose * (different by State) 0.1 ~ 0.3 84.00%

Norway no tax 14.35 53.00%

Netherlands no tax 0 100.00%

Denmark no tax 59.5 47.23%

Germany Impose 30.1 76.00%

China no tax 1.54 100%

Singapore no tax 28.5 100%

Korea no tax 8 81.18%

(Source) Japanese Shipowners' Association

Tonnage tax Taxation by the normal profit

Tonnage tax

National flagged vessel

Foreign flagged vessel

Japan, US

Countries which has introduced Tonnage tax, excluding Japan, US

*The ratio of Japan-flagged vessel of Japanese merchant fleet is around 4%. (as of the middle of 2009)*Under certain conditions, tonnage tax has been adopted for foreign-flagged vessels as well as national flagged vessels in the countries which has introduced tonnage tax excluding Japan and US.

- Progress of the oligopoly by European container shipping companies -

Background of the progressing European oligopoly includes M&A and in the EU the tonnage tax system (for all merchant fleets) as the standard (gradual introduction in the late 1990s).In Japan the tonnage tax system was introduced for Japanese-flagged vessels only in 2008 (for approximately 4% of the total fleet).

The capital-asset ratio of Japan’s shipping companies is lower than that of the overseas major companies

Debt –to-net assets ratio constitution ratio ( 2008 )

Maersk Group

Evergreen Marine Corporation

China Shipping Container Lines

日本郵船商船三井

川崎汽船

0%10%20%30%40%50%60%70%80%90%

100%

46.2% 50.8%

79.3%

28.1%38.5% 36.7%

34.3% 28.3%

4.5%

44.2%37.1% 44.0%

19.5% 21.0% 16.3%27.8% 24.4% 19.3%

流動負債計 固定負債計 純資産計

9

Results from less advanced competitive conditionsResults from less advanced competitive conditions

・ Japanese shipping industry has struggled in a severe competition in the world market. Its capital-asset ratio has been lower than other overseas industry. Ships registered in Japan and Japanese sailors have also decreased, while European majors have proceeded the oligopoly.

Ranking Operational shipping company Ranking Operational shipping company

1 Sea-Land (USA) 197,625 ( 6% ) 1 Maersk Line (Denmark) 1,915,563 ( 16% )

2 Maersk (Denmark) 196,510 ( 5% ) 2 MSC (Switzerland) 1,403,210 ( 12% )

3 Evergreen (Taiwan) 165,864 ( 5% ) 3 CMA-CGM (France) 921,027 ( 8% )

4 COSCO (China) 156,263 ( 4% ) 4 Evergreen (Taiwan) 630,899 ( 5% )

5 Hanjin Shipping (South Korea) 118,896 ( 3% ) 5 Hapag-Lloyd (Germany) 476,187 ( 4% )

6 NYK Line (Japan) 107,968 ( 3% ) 6 COSCO (China) 458,172 ( 4% )

7 P&OCL (UK) 102,485 ( 3% ) 7 NOLAPL (Singapore) 445,083 ( 4% )

8 Hyundai Merchant Marine (South Korea) 101,706 ( 3% ) 8 CSCL (China) 425,820 ( 3% )

9 Osaka Mitsui O.S.K. Lines (Japan) 100,542 ( 3% ) 9 NYK Line (Japan) 422,765 ( 3% )

10 Nedlloyd (Netherlands) 96,240 ( 3% ) 10 Mitsui O.S.K. Lines (Japan) 373,385 ( 3% )

13 Kawasaki Kisen (Japan) 80,104 ( 2% ) 13 Kawasaki Kisen (Japan) 298,547 ( 2% )

3,584,416 ( 100% ) 12,180,125 ( 100% )

(出典)日本郵船調査グループ「世界のコンテナ船隊及び就航状況」に基づき海事局作成。

World Total World Total

November 1996 January 2009

TEU (market share) TEU (market share)

The total share of the world’s top three 15.6% 34.8%

- Changes in the number of Japan-flagged vessels and Japanese seafarers in Japan’s merchant fleet -

S47 S55 S60 H 1 6 11 16 18 19 20 0

500

1,000

1,500

2,000

2,500

3,000

0

10,000

20,000

30,000

40,000

50,000

60,000

1,580 1,176 878 532 280 154 99 95 92 98

655 1,329 1,557

1,470 1,710 1,842 1,797 2,128 2,214 2,555

56,833

38,425

30,013

11,167 8,781 5,573 3,008 2,650 2,649 2,621

2,621 seafarers

98 ships

The number of Japan-flagged vessels, and Japanese seafarers has dropped sharply due to tough international competition.

Source: Maritime Bureau, MLIT

(ships)(seafarers)

■ Vessels other than Japan-flagged■ Japan-flagged vessels■ the number of Japanese seafarers for ocean-going vessels

1972 1980 1985 1989 1994 1999 2004 2006 2007 2008

I Current Issues

Net assetfixed liabilitycurrent liability

NYK MOL K-Line

Promote competitiveness for shipbuilding through leading developments of international treaties as well as developing and disseminating innovative energy-saving technology for ships

Strengthen public-private sector collaboration to further upgrade shipbuilding technology and foster marine industries that can contribute to EEZ management, development and use

1) Enhance the competitiveness of Japanese merchant fleets centered on Japan-flagged ships. Even out competitive conditions including the strategic reform of Japan’s taxation systems on maritime transport

Improve procedures related to ships’ equipment and seafarers’ qualifications on Japan-flagged ships

2) Develop platform for securing or training superior seamen (officers) Provide effective incentives for promoting the hiring of Japanese seamen (officers) Improve recognition of the significance and attraction of the profession of seaman

Economic growth and development of the Japanese economy

Enhance the strengths of maritime transport

10

Towards “Japan’s Restoration as a Maritime Nation”Towards “Japan’s Restoration as a Maritime Nation”Brief summary of “MLIT’s Growth strategy “

1) Strengthen international competitiveness through “selection” and “concentration”2) Carry out comprehensive measures and take steps to centralize cargoes in selected strategic ports for international containers3) Achieve safe and reliable port entry by passenger ships and respond to tourism promotion measures

Enhance the Strengths of Ports

Strengthen shipbuilding and develop it for Ocean Sector

1. Taxation System to promote growth of Japanese economy

2. Taxation System to prevent global warming and protect environment related

3. Taxation System for safety and security including safety net

(1) The improvement of Japanese standard tonnage taxation system (International shipping)(2) Wide revision of exemptions for taxations to improve competitiveness on international transportation (Special depreciation for international shipping and property tax )

(3) The extension and improvement of exemptions to the tax property replaced by purchase (International shipping)(4) The expansion of reduction for registration and license tax for possession and mortgage of a vessel in International Ship System in Japan (International shipping)(5) The establishment of exemption systems for domestic feeder boats (Domestic, oil and coal tax, property tax)

(1) The extension and improvement of special depreciation for domestic low environmental load ships and extension of exemptions to the tax on a property replaced by purchase (Domestic shipping)(2) The establishment of exemption systems to the tax in order to encourage a modal shift or/and promote utilization of public transportation tax for preventing global warming ( Domestic, horizontal issue on transport modes)

・ Improvement of relevant taxation system on securing and improving local public transportation (property tax of remote islands routes, horizontal issue on transport modes)

11

Outline of request for tax modifications in FY2011 (Maritime Bureau, MLIT)Outline of request for tax modifications in FY2011 (Maritime Bureau, MLIT)III Taxation system request for the next fiscal year

To involve growth of world shipping into Japanese economy through providing good quality and mass services with competitiveness

Japanese standard tonnage taxation system ( Applied to Ship operators )

OthersIncluding not only national flagged vessels also a certain non-national flagged vessels in the taxation scheme

( Up to three times of national flagged vessels in UK, Germany, France and Netherland, and five times in Korea )

JapanApplied to national flagged vessels

( The number accounts for only 4% of Japanese fleet )

Policy Developme

nt in a package

The expansion of applied vessels(Japanese flagged vessels plus up to three times of them not more than total of time chartered vessels from subsidiaries abroad)

Expansion of Japanese fleet by securing cash flow like foreign major operatorsGrowth

Strategies

○ To secure the targeted 450 number of Japanese flagged vessels earlier, which is essential for ensuring economic security in emergency , by accelerating the increase of Japanese flagged vessels . Plus to secure stable seaborne transport by Japanese fleet including foreign flag vessels near Japanese one

○ To grow the scale of Japanese fleet just as global expansion by encouraging industry to get competitiveness and involve growth of world shipping.

※Marine Transportation Law will be amended to implement improved Japanese standard tonnage taxation.

Present

12

Strengthening international competitiveness of Japan’s fleet centered on Japanese flagged vessels (International Shipping) (1)

Strengthening international competitiveness of Japan’s fleet centered on Japanese flagged vessels (International Shipping) (1)

III Taxation system request for the next fiscal year

To provide fleet with competitiveness centered on Japanese flag to ship operators from Japan’s owners

Special depreciation and exemptions on a property replaced by purchase( Applied to Ship owners )

Property tax( Japanese

flagged ships )

Registration on and license tax

( Japanese flagged ships )

Others Higher depreciation rates than Japan No taxVery low rates

( 1/5-1/100 compared to Japan )

JapanSpecial depreciation: 18% of acquisitionAdvanced depreciation: 80% of the gain from transfer of property

1/6-1/15 compared to

standard rates

Rate: 3/1000( \20M at 160Ttonnage

tanker

Policy Developme

nt in a package

Preferential treatment to national flagSpecial depreciation: 30% for national flag 16% for others Advanced depreciation: 90% for national flag 70% for others

No tax like other nations

Exemptions for flagging back(1/1000)

Smooth supply of vessels by improvement of owners’ cash flow

Cost reduction for holding vessels

Cost reduction for vessel registration

Growth Strategie

s

Continued

Present

13

Strengthening international competitiveness of Japan’s fleet centered on Japanese flagged vessels (International Shipping) (2)

Strengthening international competitiveness of Japan’s fleet centered on Japanese flagged vessels (International Shipping) (2)

III Taxation system request for the next fiscal year

○ The amount of GHG emission from international shipping is 870 million tons and comparable to 3% of the world total emission (euqal to that from Germany)

Current condition○ Growth of ocean-going shipping continues to push up GHG emission ⇒ 2.7 times in 2020 from1990 levels ( in case no measures )

International movement toward GHG emission from ships

○ IMO discusses GHG emission from international shipping as Kyoto Protocol doesn’t apply to it

○ Development of Treaty such as the introduction of mileage regulation to ships・ Regulation of energy efficiency of new ships Mileage regulation to ships on the basis of innovation ⇒ Enforced from January 2013 at the earliest

Development at IMO

< Japan leads discussions on the environmental regulation in IMO* and take initiatives >

・ Market mechanisms ( Levying, Emission trading scheme etc. )

Japan’s contribution to IMO

Market measures : Accelerate all possible measures to be taken for energy-saving shipping Fuel levy : Proposal to establish “Leveraged incentive scheme” to evaluate fuel consumption at actual sea conditions in addition to Levy from bunker ⇒ To be discussed in conjunction with other proposals (Emission trading scheme, Ship efficiency and credit trading)

Promote international strategy in cooperation with technology development

Technical measures : Energy Efficiency Design Index ○ Assessment of energy efficiency of new ships ○ Assessment of energy efficiency of ships’ operation

Positive proposal on the basis of innovation by technology development

Japan has led discussions at IMO

Development of high efficient energy saving technologies (1) Development of high efficient energy saving technologies (1)For 30% reduction in GHG emission from international shipping, MLIT takes measures to support researches and developments for new technology and develop international standards strategy to spread energy saving technologies.

IV Budgetary request for the next fiscal year

*International Maritime Organization

14

Engine(Machinery, Electronics,

etc.)

Operation(Electronics,

IT, etc.)

Hull(Shipbuilding,

Material, etc.)

Thrust(Material,

Machinery, etc.)

30% reduction of CO2 emissions from ships

Advance of heat efficiency by wasted heat recovery system

Advance of energy-efficiency by technology development for converting wasted heat into onboard electrical power.

Advance of thrust efficiency by new type propeller

Next-generation operation control system

Friction resistance reduction

Air lubrication method

New typeConventional type

Technology Development

High-efficiency propeller

Development of advanced operation control system with IT.Control propellers/motors in response to weather/hydrographic conditions.

Development of high-efficiency propeller resolving energy loss factors.

Development of air lubrication method (covering hull with air bubbles),etc.

Development of high efficient energy saving technologies (2) Development of high efficient energy saving technologies (2)IV Budgetary request for the next fiscal year

Promote and support advanced R&D by private sectors for improvement of new ships’ fuel-efficiency(targeted 30% improvement). Achieve a good balance between global warming prevention and strengthening competitiveness of Japanese maritime industry through technological innovation in the wide-range shipbuilding-related industries.

15

Develop “safety guideline” on the basis of research and development

● Promotion of the maritime industry● Expansion of marine renewable energy

● Promotion of the maritime industry● Expansion of marine renewable energy

◆Background

◆The number of offshore windmills

◆Challenges for broad use

◆Background

◆The number of offshore windmills

◆Challenges for broad use

( 1 ) Risk assessment for becoming a large scale ( 2 ) Sympathetic vibration between Windmill and floating substruction

( 3 ) Securing safety of upset

( 1 ) Risk assessment for becoming a large scale ( 2 ) Sympathetic vibration between Windmill and floating substruction

( 3 ) Securing safety of upset

improvement for safety environment

● Technical issues on safety for floating system

● Needs

16

Research and development on the safety of Offshore Wind PowerResearch and development on the safety of Offshore Wind Power

828 in Europe, 14 in Japan (the end of 2009)

・ Wind energy is expected to be effective renewable energy, as well as solar energy. Less and less land area is available for windmills because of low-frequency noise, etc.

・ Offshore is available for windmills on the grounds of satisfying very large space and stable wind

・ In Japan, verification test to enhance durability and to increase the capacity of windmill, and the research on floating wind power system will be promoted.

・ Selection of sites apt for windmills including wind conditions, coordination among stakeholders, cost reduction, etc.

country generation capacity( Wind

Power) (MW)

generation capacity (Offshore Wind Power) (MW)

UK 3,331 598

Denmark 3,163 423

Netherlands 2,214 228

Sweden 1,047 133

Japan 1,880 11

IV Budgetary request for the next fiscal year

- 94% of seafarers aboard Japanese merchant fleet are from Asian countries. It is essential for safety, stability and strengthening competitiveness of international maritime transport in Japan to secure and train highly-qualified Asian seafarers.

- Japan intends to support seafarers’ training in Asian region.

Instructors in Asian countries

technical transfer of onboard training system

Measures

・ Development of training curriculum

・ Dispatch of NIST1) instructors

Education for instructors

・ Secure safety and stability of ocean-going marine transport

・ Strengthen the international competitiveness of ocean-going maritime transport

Effect

Training for seafarers

・ Lecture・ Onboard training

Onboard Japanese commercial ships Development of onboard training system

Acceptance Dispatch

17

Securing and training highly-qualified Asian seafarersSecuring and training highly-qualified Asian seafarers

Resolution of bottleneck of seafarers supplyTraining prospective Asian seafarers into highly qualified seafarers

IV Budgetary request for the next fiscal year

1)National Institute for Sea Training

◇Japanese international maritime transport industry heavily depends on foreign seafarers. → approx. 94% from Asian region(Philippines, etc)◇Increasing seaborne trade volume → Global shortage of seafarers → 27 thousand persons shortage (estimated in 2015)◇Scrambling for highly-qualified Asian seafarers → approx. 44% of global seafarers are from Asia.

◇Japanese international maritime transport industry heavily depends on foreign seafarers. → approx. 94% from Asian region(Philippines, etc)◇Increasing seaborne trade volume → Global shortage of seafarers → 27 thousand persons shortage (estimated in 2015)◇Scrambling for highly-qualified Asian seafarers → approx. 44% of global seafarers are from Asia.

◇Circumstances of seafarers training in Asia - Poor training facility - Less opportunities for onboard training → Bottleneck of seafarers supply

Current situations

Seafarers of International maritime transport in Japan

94%94%

フィリピンでの乗船訓練で指導

日本商船隊における船舶職員

航海訓練所・海技大学校での研修

ソフト面の支援実施【新事業】

教 官

練習船実 習

社 船実 習

【現行事業】 新人(学生)

現現 状状

◇ 日本外航はアジア人船員に大きく依存(約94%がフィリピン他アジア諸国)

◇ →海上輸送量増大 世界的な船員不足△ 2.7万人の見込み(2015年)

◇ 欧州との間で優秀なアジア人船員の囲い込み激化(世界船員の約44%がアジア人船員)

◇ 日本外航はアジア人船員に大きく依存(約94%がフィリピン他アジア諸国)

◇ →海上輸送量増大 世界的な船員不足△ 2.7万人の見込み(2015年)

◇ 欧州との間で優秀なアジア人船員の囲い込み激化(世界船員の約44%がアジア人船員)

◇ アジアの船員教育の現状-船員供給のボトルネック

・貧弱な船員教育機関・乗船実習機会の不足

◇ アジアの船員教育の現状-船員供給のボトルネック

・貧弱な船員教育機関・乗船実習機会の不足

我が国として、優秀なアジア人船員の確保に積極的に関与することが急務

日本

フィリピン

その他アジア

アジア以外

日本 3.2%

我が国外航商船船員

アジア人船員 94%アジア人船員 94%

現現 状状

◇ 日本外航はアジア人船員に大きく依存(約94%がフィリピン他アジア諸国)

◇ →海上輸送量増大 世界的な船員不足△ 2.7万人の見込み(2015年)

◇ 欧州との間で優秀なアジア人船員の囲い込み激化(世界船員の約44%がアジア人船員)

◇ 日本外航はアジア人船員に大きく依存(約94%がフィリピン他アジア諸国)

◇ →海上輸送量増大 世界的な船員不足△ 2.7万人の見込み(2015年)

◇ 欧州との間で優秀なアジア人船員の囲い込み激化(世界船員の約44%がアジア人船員)

◇ アジアの船員教育の現状-船員供給のボトルネック

・貧弱な船員教育機関・乗船実習機会の不足

◇ アジアの船員教育の現状-船員供給のボトルネック

・貧弱な船員教育機関・乗船実習機会の不足

我が国として、優秀なアジア人船員の確保に積極的に関与することが急務

日本 3.2%

我が国外航商船船員

アジア人船員 94%アジア人船員 94%

具体的施策

効果・海上輸送の安全性・安定性確保・我が国外航海運の国際競争力確保

日本

フィリピン

その他アジア

アジア以外

フィリピンでの乗船訓練で指導

日本商船隊における船舶職員

航海訓練所・海技大学校での研修

ソフト面の支援実施【新事業】

教 官

練習船実 習

社 船実 習

【現行事業】 新人(学生)

現現 状状

◇ 日本外航はアジア人船員に大きく依存(約94%がフィリピン他アジア諸国)

◇ →海上輸送量増大 世界的な船員不足△ 2.7万人の見込み(2015年)

◇ 欧州との間で優秀なアジア人船員の囲い込み激化(世界船員の約44%がアジア人船員)

◇ 日本外航はアジア人船員に大きく依存(約94%がフィリピン他アジア諸国)

◇ →海上輸送量増大 世界的な船員不足△ 2.7万人の見込み(2015年)

◇ 欧州との間で優秀なアジア人船員の囲い込み激化(世界船員の約44%がアジア人船員)

◇ アジアの船員教育の現状-船員供給のボトルネック

・貧弱な船員教育機関・乗船実習機会の不足

◇ アジアの船員教育の現状-船員供給のボトルネック

・貧弱な船員教育機関・乗船実習機会の不足

我が国として、優秀なアジア人船員の確保に積極的に関与することが急務

日本

フィリピン

その他アジア

アジア以外

日本

フィリピン

その他アジア

アジア以外

日本 3.2%

我が国外航商船船員

アジア人船員 94%アジア人船員 94%アジア人船員 94%アジア人船員 94%

現現 状状

◇ 日本外航はアジア人船員に大きく依存(約94%がフィリピン他アジア諸国)

◇ →海上輸送量増大 世界的な船員不足△ 2.7万人の見込み(2015年)

◇ 欧州との間で優秀なアジア人船員の囲い込み激化(世界船員の約44%がアジア人船員)

◇ 日本外航はアジア人船員に大きく依存(約94%がフィリピン他アジア諸国)

◇ →海上輸送量増大 世界的な船員不足△ 2.7万人の見込み(2015年)

◇ 欧州との間で優秀なアジア人船員の囲い込み激化(世界船員の約44%がアジア人船員)

◇ アジアの船員教育の現状-船員供給のボトルネック

・貧弱な船員教育機関・乗船実習機会の不足

◇ アジアの船員教育の現状-船員供給のボトルネック

・貧弱な船員教育機関・乗船実習機会の不足

我が国として、優秀なアジア人船員の確保に積極的に関与することが急務

日本 3.2%

我が国外航商船船員

アジア人船員 94%アジア人船員 94%

具体的施策

効果・海上輸送の安全性・安定性確保・我が国外航海運の国際競争力確保

日本

フィリピン

その他アジア

アジア以外

日本

フィリピン

その他アジア

アジア以外Asian seafarers 94%

Securing highly-qualified seafarers is an urgent matter for Japan

Japanese seafarers 3.2%

JapanPhilippinesOther AsiaOthers

・ Lecture・ Onboard training

Thank you for your attention!

18