─ xbma ─ cross-border m&a data points beijing, june 12-13, 2008

TRANSCRIPT

─xbma─

Cross-Border M&A Data Points

Beijing, June 12-13, 2008

2─xbma─

Global M&A Volume: 1995-2007

• Steady growth of global M&A volume from 2003 (under US$2 trillion) through mid-2007 (US$5.1 trillion), fueled by the availability of vast amounts of cheap debt, growing pools of investment capital across the globe, and confidence in the markets.

• US$5.1 trillion M&A volume in 2007 represented a new high water mark, beating prior high watermark of US$4.3 trillion in 1999.

• Generally three- to four-year cycles historically.

0

1

2

3

4

5

6

US

$tr

illio

ns

1995 1997 1999 2001 2003 2005 2007

Global M&A Dollar Volume

Source: Dealogic Thomson

$4.3T

$5.1T

$1.5T

3─xbma─

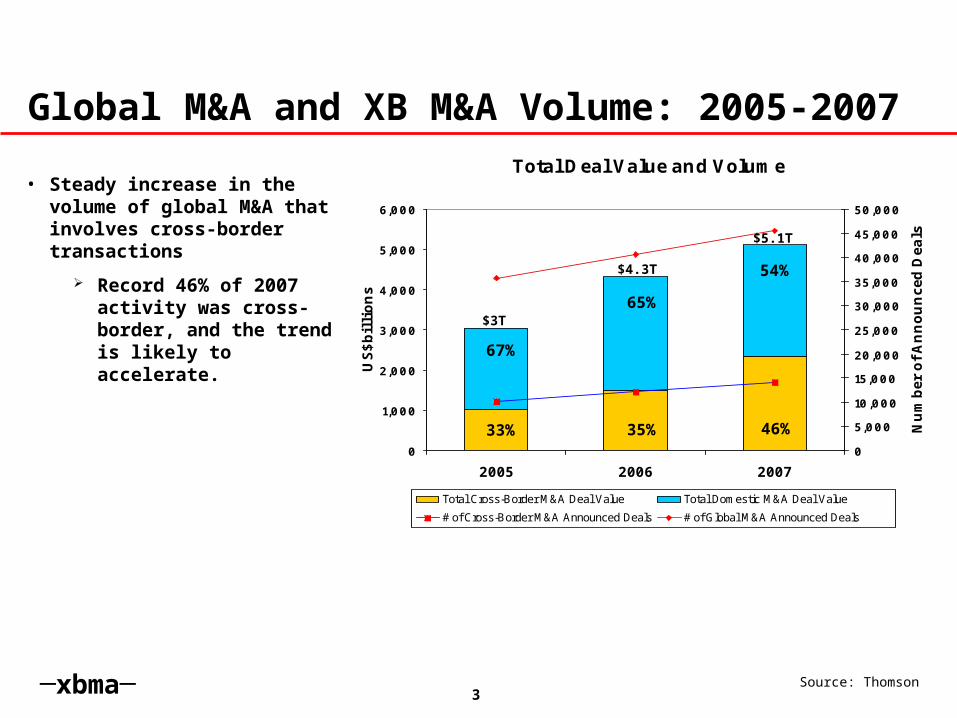

Global M&A and XB M&A Volume: 2005-2007

• Steady increase in the volume of global M&A that involves cross-border transactions

Record 46% of 2007 activity was cross-border, and the trend is likely to accelerate.

Total Deal Value and Volume

0

1,000

2,000

3,000

4,000

5,000

6,000

2005 2006 2007

US$bil

lions

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

Num

ber

of A

nnounce

d D

eals

Total Cross-Border M&A Deal Value Total Domestic M&A Deal Value

# of Cross-Border M&A Announced Deals # of Global M&A Announced Deals

46%

54%

65%

35%

67%

33%

$3T

$4.3T

$5.1T

Source: Thomson

4─xbma─

Total Deal Value and Volume

0

1,000

2,000

3,000

4,000

5,000

6,000

2005 2006 2007 2008

US$bil

lions

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

Num

ber

of A

nnounce

d D

eals

Total Cross-Border M&A Deal Value Total Domestic M&A Deal Value

# of Cross-Border M&A Announced Deals # of Global M&A Announced Deals

Global M&A: Current Conditions

46%

54%

65%

35%

67%

33%

$3T

$4.3T

$5.1T

*2008 figures projected based on 2008 Q1 and estimated Q2 data

Est. $3T?

Source: Thomson

• Sub-prime and credit crises of mid-2007 marked the beginning of a down-cycle – 2008 YTD volume down significantly

• Key determining factors for activity in the second half of 2008 are likely to be:

Restoration of liquidity; re-emergence of private equity deals

Restoration of confidence in the markets; acceleration of strategic deals

Acquisition activity from China, India and oil-rich countries (including the growing SWFs)

~47%

~53%

5─xbma─

M&A Volume by Target’s Region – 2007

South & Central America

2%

Western Europe

40%

Eastern Europe

4%

Asia-Pacific (Ex-Japan)

10%

Japan2%

Africa/Middle East2%

North America

40%

Breakdown of $5.1 Trillion of 2007

Transactions

• M&A markets in North America and Western Europe are significantly more developed and liquid than those of the rest of the world

80% of global M&A occurred in North America and Western Europe (which represent 60% of the world’s GDP)

12% of global M&A occurred in Asia (which represents 22% of the world’s GDP)

• But the M&A volume involving China, India and oil-rich countries (including SWFs) is growing fast

Source: Thomson

6─xbma─

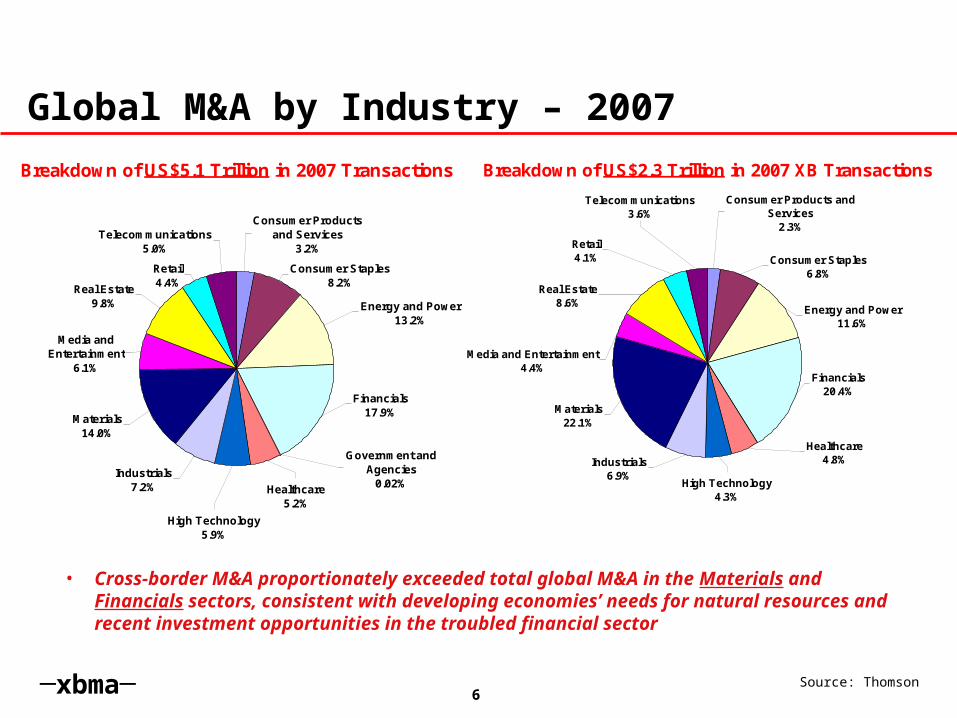

Global M&A by Industry – 2007

• Cross-border M&A proportionately exceeded total global M&A in the Materials and Financials sectors, consistent with developing economies’ needs for natural resources and recent investment opportunities in the troubled financial sector

Source: Thomson

Breakdown of US$5.1 Trillion in 2007 Transactions

Consumer Products and Services

3.2%

Consumer Staples8.2%

Retail4.4%

Telecommunications5.0%

Real Estate9.8%

Media and Entertainment

6.1%

Materials14.0%

Industrials7.2%

Government and Agencies

0.02%Healthcare5.2%

High Technology5.9%

Financials17.9%

Energy and Power13.2%

Breakdown of US$2.3 Trillion in 2007 XB Transactions

Retail4.1%

Telecommunications3.6%

Consumer Products and Services

2.3%

Consumer Staples6.8%

Energy and Power11.6%

Financials20.4%

High Technology4.3%

Healthcare4.8%Industrials

6.9%

Materials22.1%

Media and Entertainment4.4%

Real Estate8.6%

7─xbma─

Asia-Pacific (ex-Japan): M&A Volume – 2005-2007

Asia-Pacific (ex-Japan) M&A and Cross-Border M&A Total Deal Value

0

100

200

300

400

500

600

2005 2006 2007

US$bil

lions

Total Cross-Border M&A Deal Value Total Domestic M&A Deal Value

40% 41% 41%

60%

59%

59%

$267B

$427B

$533B

Source: Thomson

• Steady increase in volume throughout the region – US$533B of domestic and inbound M&A in 2007.

• China accounts for a growing component of the total, representing about US$20B of the 2006 total and about US$30B of the 2007 total.

† Asia-Pacific (ex-Japan) region includes India

8─xbma─

China Inbound and Outbound M&A and Investment, by Industry – 2007

• Chinese investors and acquirers have been most active in outbound investments/acquisitions in the financial, mining and oil sectors. The trend of buying natural resources offshore is continuing in 2008, with more than $21B worth of transactions in those sectors already announced in 2008 YTD

• Inbound investments highest in financial and real estate sectors

Source: Thomson

Inbound M&A/Investments by IndustryBreakdown of US$25 Billion in 2007 Inbound M&A

Retail1.3%

Consumer Products and Services

3.9%Consumer Staples

3.3%

Telecommunications0.8%

Energy and Power2.6%

Financials53.3%

High Technology7.7%

Healthcare2.0%

Industrials5.8%

Materials4.9%

Media and Entertainment

1.6%

Real Estate12.8%

Outbound M&A/Investments by IndustryBreakdown of US$37 Billion in 2007 Outbound M&A

Consumer Staples0.7%

Telecommunications1.0%

Energy and Power1.9%

Financials75.2%

High Technology2.1%

Industrials0.6%

Materials18.1%

Real Estate0.3%

9─xbma─

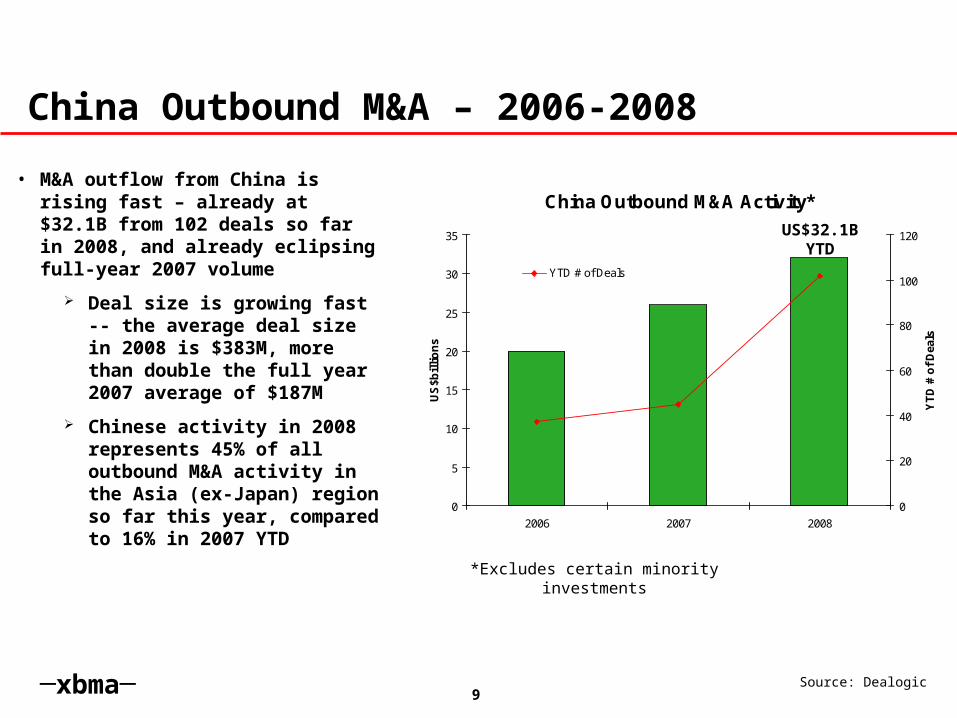

China Outbound M&A – 2006-2008

• M&A outflow from China is rising fast – already at $32.1B from 102 deals so far in 2008, and already eclipsing full-year 2007 volume

Deal size is growing fast -- the average deal size in 2008 is $383M, more than double the full year 2007 average of $187M

Chinese activity in 2008 represents 45% of all outbound M&A activity in the Asia (ex-Japan) region so far this year, compared to 16% in 2007 YTD

Source: Dealogic

China Outbound M&A Activity*

0

5

10

15

20

25

30

35

2006 2007 2008

US

$bil

lio

ns

0

20

40

60

80

100

120

YT

D #

of

Dea

ls

$ YTD # of Deals

US$32.1BYTD

*Excludes certain minority investments

10─xbma─

China Inbound M&A – 2006-2008

Source: Dealogic

China Inbound M&A Activity

0

5

10

15

20

25

30

2006 2007 2008

US

$bil

lio

ns

0

50

100

150

200

250

300

YT

D #

of

Dea

ls

$ YTD # of Deals

US$6.5BYTD

• China inbound activity rose through 2007, but would appear to be at a lower pace so far in 2008, perhaps reflecting the downturn in the West.

$18.3B

$25.1B

11─xbma─

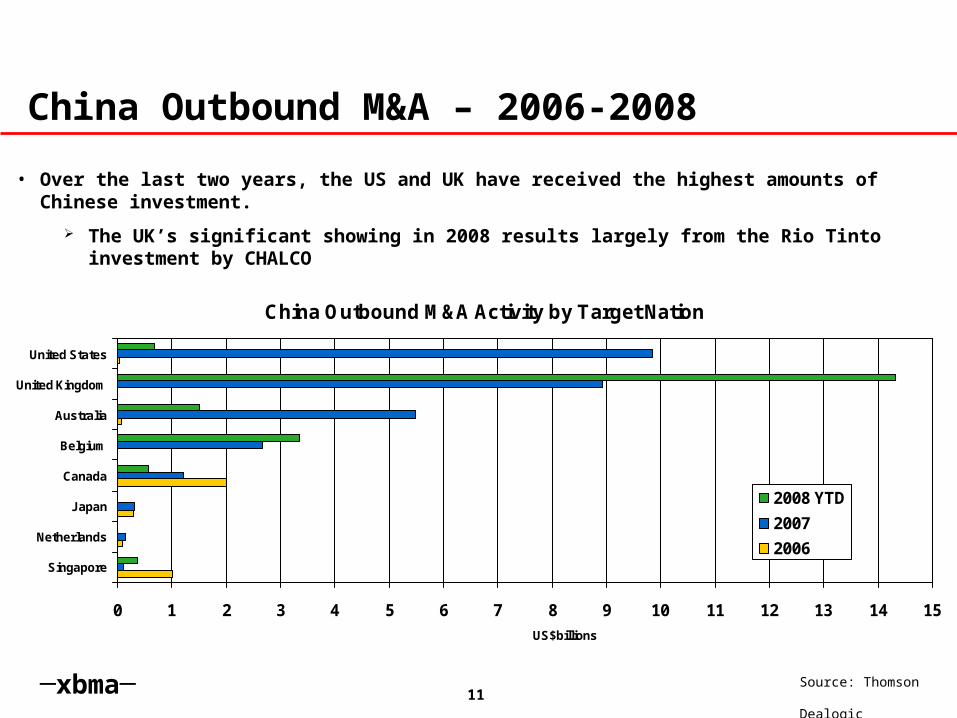

China Outbound M&A Activity by Target Nation

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Singapore

Netherlands

Japan

Canada

Belgium

Australia

United Kingdom

United States

US$billions

2008 YTD

2007

2006

China Outbound M&A – 2006-2008

• Over the last two years, the US and UK have received the highest amounts of Chinese investment.

The UK’s significant showing in 2008 results largely from the Rio Tinto investment by CHALCO

Source: Thomson Dealogic

12─xbma─

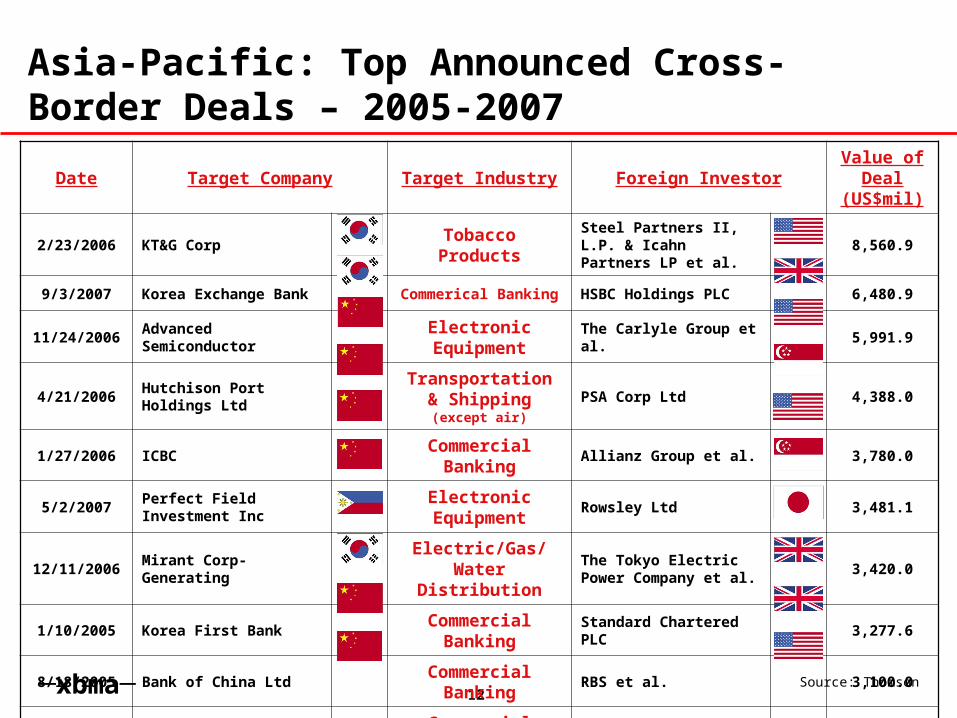

Asia-Pacific: Top Announced Cross-Border Deals – 2005-2007

Date Target Company Target Industry Foreign InvestorValue of

Deal (US$mil)

2/23/2006 KT&G CorpTobacco Products

Steel Partners II, L.P. & Icahn Partners LP et al.

8,560.9

9/3/2007Korea Exchange Bank

Commerical Banking

HSBC Holdings PLC 6,480.9

11/24/2006Advanced Semiconductor

Electronic Equipment

The Carlyle Group et al.

5,991.9

4/21/2006Hutchison Port Holdings Ltd

Transportation & Shipping

(except air)

PSA Corp Ltd 4,388.0

1/27/2006 ICBCCommercial

BankingAllianz Group et al. 3,780.0

5/2/2007Perfect Field Investment Inc

Electronic Equipment

Rowsley Ltd 3,481.1

12/11/2006Mirant Corp-Generating

Electric/Gas/Water

Distribution

The Tokyo Electric Power Company et al.

3,420.0

1/10/2005 Korea First BankCommercial

BankingStandard Chartered PLC

3,277.6

8/18/2005 Bank of China LtdCommercial

BankingRBS et al. 3,100.0

11/16/2006Guangdong Development Bank

Commercial Banking

Citigroup et al. 3,100.0

Source: Thomson

13─xbma─

China: Top Announced Inbound Cross-Border Deals – 2007

Date Target CompanyTarget

IndustryForeign Investor

Value of Deal

(US$mil)

5/2/2007Perfect Field Investment Inc

High Technology

Rowsley Ltd 3,481.1

9/2/2007China Eastern Airlines Corp

Industrials Temasek et al. 923.8

12/6/2007Kerry (Shenyang) Real Estate Development Co Ltd

Real EstateAllgreen Properties Ltd

650.7

9/10/2007China National Chemical Corp

MaterialsBlackstone Group LP

600.0

7/10/2007City Centre Development Phases

Real EstateChina Real Estate Opp

548.1

9/25/2007China Fortune Securities Co Ltd

Financials Morgan Stanley 533.0

1/28/2007Guangzhou Hengda Industrial Group Co

Financials Investor Group 400.0

2/13/2007 C-BONS Hair CareConsumer Staples

Beiersdorf AG 381.4

12/12/2007

Shenzhen ExcelStor LtdHigh Technology

Iomega Corp 323.1Source: Thomson

14─xbma─

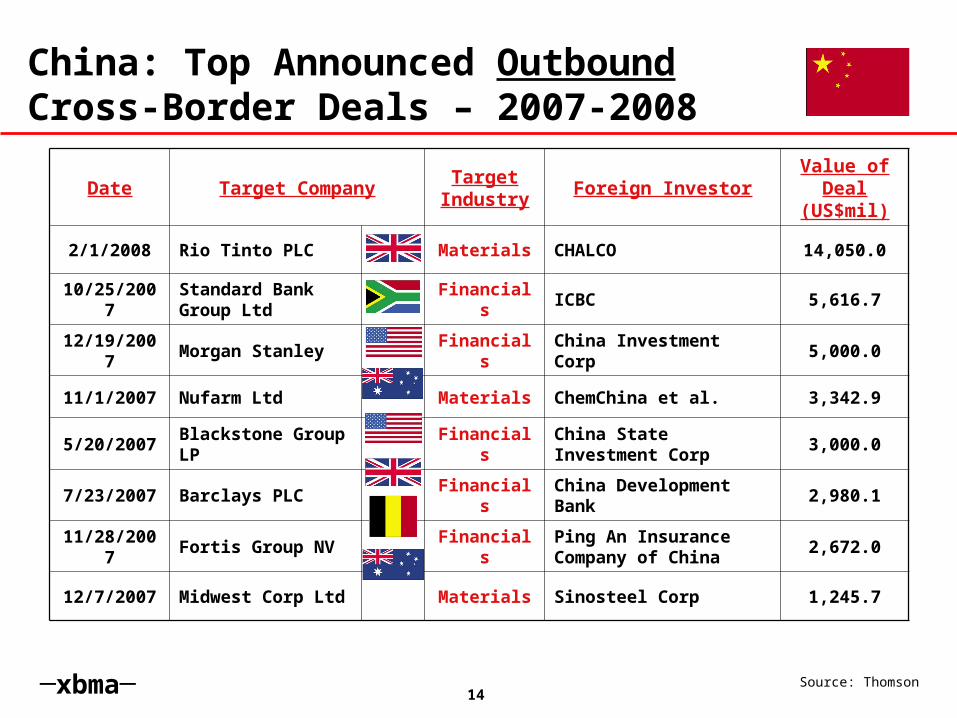

China: Top Announced Outbound Cross-Border Deals – 2007-2008

Date Target CompanyTarget

IndustryForeign Investor

Value of Deal

(US$mil)

2/1/2008 Rio Tinto PLC Materials CHALCO 14,050.0

10/25/2007

Standard Bank Group Ltd

Financials ICBC 5,616.7

12/19/2007

Morgan Stanley FinancialsChina Investment Corp

5,000.0

11/1/2007 Nufarm Ltd Materials ChemChina et al. 3,342.9

5/20/2007Blackstone Group LP

FinancialsChina State Investment Corp

3,000.0

7/23/2007 Barclays PLC FinancialsChina Development Bank

2,980.1

11/28/2007

Fortis Group NV FinancialsPing An Insurance Company of China

2,672.0

12/7/2007 Midwest Corp Ltd Materials Sinosteel Corp 1,245.7

Source: Thomson

15─xbma─

Sovereign Wealth Fund Assets

CIC $200B

~$8B

~$20B

$33B

$50-$60B

$213B

$380B

$489B

$500-$875B

$1.7 trillion

0 200 400 600 800 1000 1200 1400 1600 1800

Oman

Dubai

Russia

Qatar

Kuwait

Norway

Singapore

Abu Dhabi

China

(US$ billions)

SAFE

SWFs manage approximately US$3 trillion in assets, including:

16─xbma─

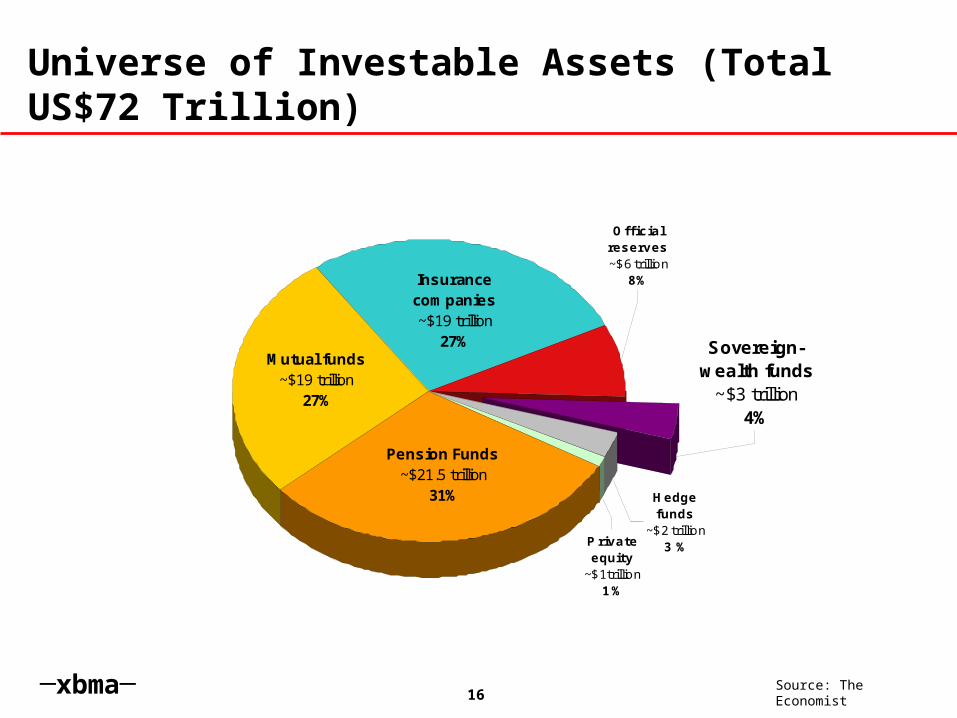

Universe of Investable Assets (Total US$72 Trillion)

Source: The Economist

Hedge funds

~$2 trillion3 %Private

equity~$1 trillion

1 %

Sovereign-wealth funds

~$3 trillion4%

Official reserves~$6 trillion

8%Insurance companies~$19 trillion

27%Mutual funds

~$19 trillion27%

Pension Funds~$21.5 trillion

31%