enpard.geenpard.ge/.../agrocredit-project-assessment_eng.docx · web viewthe farmer-led...

TRANSCRIPT

Assessment of the Preferential Agro Credit ProjectFrom Farmers' Needs and Requirements Perspective

2016

The present publication has been produced with the support of ENPARD. Implementing partners of the Project ‘Enhancing Small Farmers’ Cooperatives’ Productivity in Imereti and Racha-Lechkhumi Regions’ are solely responsible for the content of the publication.

The views expressed in the publication do not represent the position of ENPARD.

The Project Is Sponsored By ENPARD

Project Partner

Content

Study Methodology...............................................................................................................................1

Study Objectives and Instruments.........................................................................................................2

Preferential Agro Credit Project Overview............................................................................................4

Project overview................................................................................................................................4

Preferential Agro Credit for current assets.........................................................................................4

Preferential Agro Credit for Fixed Assets..........................................................................................5

Preferential Agro Leasing..................................................................................................................6

Agricultural Part of the State Programme ‘Produce in Georgia’........................................................7

Agro Credits in Statistics.......................................................................................................................8

Assessment of the Preferential Agro Credit Project.............................................................................11

Assessment of the project purpose and implementation process......................................................11

Project Impact on Agro Business.....................................................................................................19

Project Sustainability and Performance Risks.....................................................................................22

Assessment of Farmer’s Expectations, Attitudes and Needs Towards the Preferential Agro Credit Project.................................................................................................................................................24

Concluding Findings and Recommendations.......................................................................................28

Appendix 1. Focus Group Guidelines..................................................................................................30

Appendix 2. In-Depth Interview Guidelines........................................................................................33

Study Methodology

The farmer-led assessment of the Preferential Agro Credit Project1 is conducted in the framework of the project “Enhancing Small Farmers’ Cooperatives’ Productivity in Imereti and Racha-Lechkhumi Regions”. The project is implemented with the financial support of the European Neighbourhood Programme for Agriculture and Rural Development (ENPARD).

The target municipalities of the project are: Oni, Ambrolauri, Kharagauli, Tkibuli, Zestaponi, Bagdati, Terjola, Tskaltubo and Khoni.

The aim of the study was to perform qualitative assessment of the preferential agro credit project from the perspective of farmers’ expectations, attitudes and needs.

The research was implemented in the target municipalities of the project “Enhancing Small Farmers’ Cooperatives’ Productivity in Imereti and Racha-Lechkhumi Regions and involved farmers, local government authorities, agronomists and representatives of municipal information and consulting centres.

Hereby it should be emphasized that the study focuses on the identification of the issues and needs stated by the farmers.

The Preferential Agro Credit Project is a national project that is being implemented by the Ministry of Agriculture of Georgia. The scope of the study was defined within the scopes of nine municipalities targeted by the project “Enhancing Small Farmers’ Cooperatives’ Productivity in Imereti and Racha-Lechkhumi Regions”. Qualitative research methods used for the present study allow for the generalisation of the finding and recommendations and thus can be considered as relevant for the overall assessment of the Agro Credit Project.

1 The Preferential Agro Credit Project is the official name of the project as used by the Government of Georgia and throughout the present report in capital letters and without quotation marks. The word project refers to the Preferential Agro Credit Project.

1

Study Objectives and Instruments

The following qualitative research tools were used:

(1) Focus groups with the participation of farmers

A total of 10 focus groups: one group per each target municipality (nine in total) and one joint focus group with the participation of active cooperatives in the region.

The number of participants were 10-12 farmers. Sectoral and geographical differentiation was ensured in the process of selection of the farmers. Additionally, the participants had at least generally information about the agro credit project.

Additional requirements: a minimum of 2 and maximum of 8 farmers / cooperative representatives, who applied for agro loan, was selected (regardless of the response received by them).

Focus group discussions were conducted as per guidelines (Appendix 1), audio recordings and relevant transcripts were prepared.

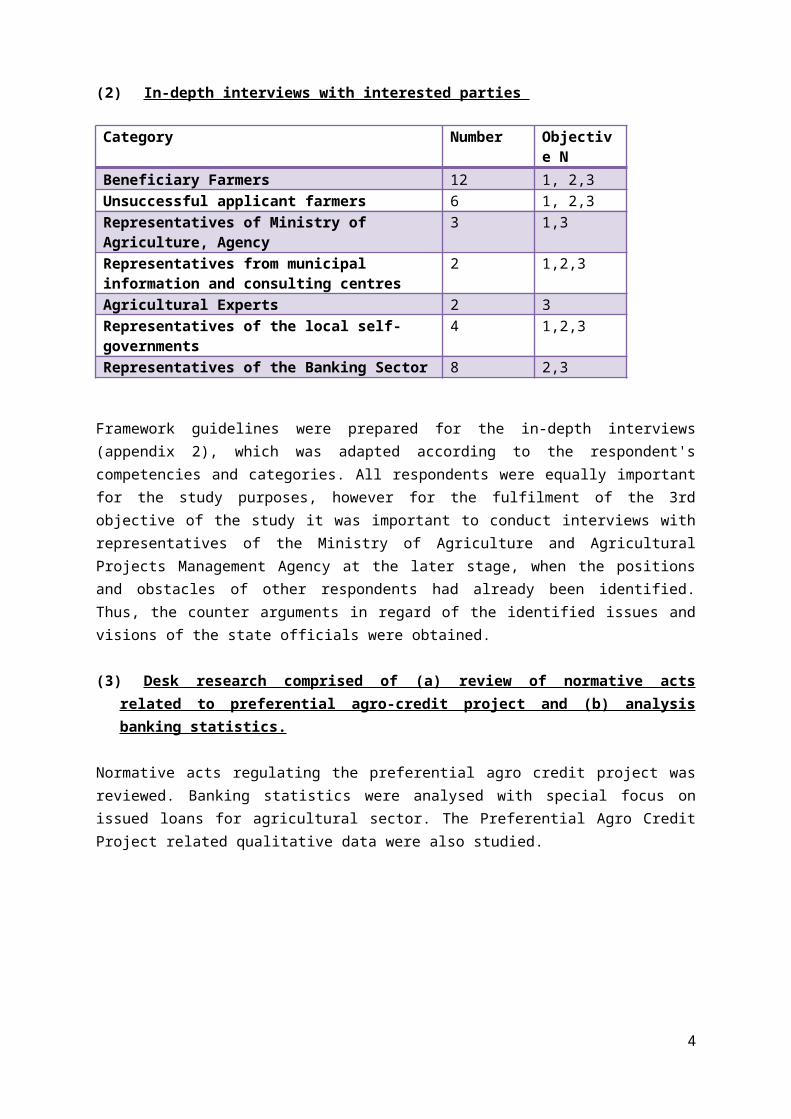

(2) In-depth interviews with interested parties

Category Number Objective NBeneficiary Farmers 12 1, 2,3Unsuccessful applicant farmers 6 1, 2,3Representatives of Ministry of Agriculture, Agency 3 1,3Representatives from municipal information and consulting centres

2 1,2,3

Agricultural Experts 2 3

2

Screening of the relevant legislative documents In-depth interviews with the representatives of the Ministry of Agriculture In-depth interviews with beneficiaries Focus groups discussions with farmers

Objective 1: Assessment of the project procedures and

aims

In-depth interviews with representatives of banking sector Focus group discussions with farmersIn-depth interviews with beneficiaries, experts and representatives of local self-government bodies

Objective 2: Identifiction of awareness, expectations,

attitudes and needs of farmers on agricultural loans

In-depth interviews with the representatives from the Ministry of Agriculture In-depth interviews with representatives of banking sectorIn-depth interviews with beneficeries and experts

Objective 3: Development of recommendations for

improvement

Representatives of the local self-governments 4 1,2,3Representatives of the Banking Sector 8 2,3

Framework guidelines were prepared for the in-depth interviews (appendix 2), which was adapted according to the respondent's competencies and categories. All respondents were equally important for the study purposes, however for the fulfilment of the 3rd objective of the study it was important to conduct interviews with representatives of the Ministry of Agriculture and Agricultural Projects Management Agency at the later stage, when the positions and obstacles of other respondents had already been identified. Thus, the counter arguments in regard of the identified issues and visions of the state officials were obtained.

(3) Desk research comprised of (a) review of normative acts related to preferential agro-credit project and (b) analysis banking statistics.

Normative acts regulating the preferential agro credit project was reviewed. Banking statistics were analysed with special focus on issued loans for agricultural sector. The Preferential Agro Credit Project related qualitative data were also studied.

3

Preferential Agro Credit Project Overview

Project overview

The project has been initiated by the Ministry of Agriculture of Georgia and has been implemented by the Agricultural Projects Management Agency since 27 th March 2013 under ‘The United Agro Project’.

The purpose of the project is to improve the processes of primary agricultural production, processing, storage and sale by providing farmers and entrepreneurs engaged in agriculture with cheap, long-term and preferential funds.

The project focuses on enterprises that use local raw materials and local labour for their manufacturing processes.

Within the framework of the project primary agricultural production, processing, storage and sale facilities receive preferential agro credit from financial institutions for fixed assets and current assets. During the years 2013-2015, current assets for primary agricultural production purposes were financed. However, the stated component is no longer financed within the framework of the project. In addition, the lower limit of the loan amount was raised from 5,000 GEL to 20,000 GEL.

Under the ‘Preferential agro credit’ project, credits are granted by commercial banks and financial institutions participating in the project according to the conditions determined by the Agricultural Project Management Agency. The Agricultural Project Management Agency is not engaged in the process of reviewing credit applications and allocating credits.

The Preferential Agro Credit Project consists of the following financial products:

1. The Preferential Agro Credit Project2. For current assets3. For fixed assets4. Preferential Agro Leasing5. The state programme ‘Produce in Georgia’

Preferential Agro Credit for current assets

Preferential agro credit for current assets is a seasonal component of the project. The Preferential Agro Credit for current assets includes financing certain part of the interest rate of loans, allocated by the financial institutions for the current assets of the enterprises producing and processing agricultural products, by the Agency.

The Agency ensures co-financing of the loan interests on the basis of the agreement concluded with beneficiaries. In order to obtain a Preferential Agro Credit, a potential beneficiary must fulfil the preconditions determined by financial institutions for granting such type of credits, and the requirements of this project.

Under the component of Preferential Agro Credit for Current Assets loans will be given for financing current assets of the enterprises purchasing and/or processing agricultural products, namely:

4

purchasing grapes for processing; purchasing tangerine for sale and/or processing; purchasing peach for sale and/or processing; purchasing substandard apples for processing; purchasing grapes for producing alcohol.

In case of financing current assets of primary agricultural enterprises, the amount of Preferential Agro Credit shall be 15 000 000 GEL or its equivalent amount in USD for one beneficiary.

The period of the credit depends on its purpose and is determined as follows:

for purchasing tangerine for sale - maximum period is 6 months; for purchasing tangerine for processing – maximum period is 12 months; for purchasing peach for sale and/or processing - maximum period is 6 months; for purchasing substandard apples for processing - maximum period is 12 months; for purchasing grapes for producing alcohol – maximum period is 36 months; for purchasing grapes for processing - maximum period is 15 months.

The lower limit of credit for the component of current assets per beneficiary amounts 20,000 GEL. The loan amount shall not exceed 10,000,000 GEL or its equivalent in US Dollars. The exception includes grape processing enterprises, which buy their grapes to produce the spirit (alcohol). In this case, the upper limit for the amount of the agro credit constitutes GEL 15,000,000 or its equivalent amount in US Dollars.

The Agency will co-finance the loan interest in the amount of 8% of the principal amount of the loan to be paid by the Agency according to the loan repayment schedule, parallel the repayment of the loan by the borrower.

The agency establishes the maximum volumes for loan interest rates, in accordance with the different loan amounts. Co-financing for loan interest rates on the part of the agency will be issued only in cases when the bank loan interest rates meet the Agency's restrictions.

Preferential Agro Credit for Fixed Assets Under the component of ‘Preferential Agro Credit for Fixed Assets’ the Agency shall finance certain part of the loan interests, allocated by the financial institutions for the fixed assets of the enterprises producing and processing agricultural products.

This component is available to the following individuals: An individual, who is a citizen of Georgia – only in case of the loans in the amount of 20,000

GEL - 30,000 USD; An individual, who is a citizen of Georgia (a sole proprietor) and a legal person registered

under the legislation of Georgia (except for the enterprises established with the partial participation of the state), including agricultural cooperatives - total amount under this component shall be 20,000 GEL – 600,000 USD, or its equivalent in GEL, and the term will not be more than 84 months.

5

The interest rate of the credit is determined according to its amount. The following interest rates must be determined by the financial institutions:

From 20,000 Gel to 30,000 USD inclusive or its equivalent in GEL Not more than 15% From 30,001 USD to 100,000 USD inclusive or its equivalent in GEL Not more than 14% From 100,001 USD to 200,000 USD inclusive or its equivalent in GEL Not more than 13% From 200,001 USD to 600,000 USD inclusive or its equivalent in GEL Not more than 12%

The same component provides different approach in benefit of grape processing enterprises, which belong to alcohol beverage category.

Under the present subcomponent frame, according the Preferential Agro-Credit amount, the grape processing enterprises can be divided into two categories:

Grape processing enterprises, out of which the total current remaining balance of Preferential Agro-Credits under the present subcomponent frame constitutes from the 20,000 USD and up to 600,000 USD (or equivalent in Georgian GEL) – If the loan is issued in GEL currency, the co-financing of the Agency shall be granted simultaneously with the amount of the money paid by the borrower, based on the annual 11% of principal amount of the loan, not more than within the term of 84 months from the moment when the loan has been issued. If loan is issued in USD currency, the Agency co-financing would be granted simultaneously to the amount paid by the borrower, with the amount of annual 8 % of principal amount of the Loan, not more than within the 84 months from the moment when the loan has been issued.

Grape processing enterprises, out of which the total current remaining balance of Preferential Agro-Credits under the present subcomponent frame accounts from USD 600,001 up to USD 2,000,000 (or equivalent in GEL) - In case when loan is issued in GEL currency, the Agency co-financing shall be granted simultaneously to the amount paid by the borrower within the 24 months’ percentage, at the amount of annual 11 % of principal amount of the loan. In case a loan is issued in national currency GEL, the Agency co-financing shall be granted simultaneously to the amount paid by the borrower within 24 months’ percentage, at the amount of annual rate of 11 % of principal amount of the loan.

Preferential Agro Leasing

The agro leasing component has the aim of further developing infrastructure, which increases the value of agricultural products.

A lessor may allocate Preferential Agro Leasing for the following purposes: An import of a new or preowned equipment and machinery; Purchase of the equipment and machinery of foreign or local production in Georgia; The secondary equipment and machinery existing on the balance of the lessor shall be given

to the lessee on condition that the lease subject is not purchased from the lessee or a related person.

The amount of the investment of the lessor determined for one beneficiary shall not be less than 12,000 USD and more than 600,000 USD, and the maximum term of the leasing is 84 months.

6

The purposeful co-financing of the Agency shall be 12% of the investment of the lessor that will be paid by the lessor to the lessee in accordance with the leasing fee payment scheme determined by the agreement, after payment of the leasing fee.

Agricultural Part of the State Programme ‘Produce in Georgia’

The nation-wide programme ‘Produce in Georgia’ is implemented by the Ministry of Economy and Sustainable Development of Georgia and the Ministry of Agriculture of Georgia.

Goals of the programme is to facilitate development of industries focused on production and facilitate establishment of new enterprises and extensions units as well as upgrade of the existing ones.

Under the programme the amount of one loan/lease must not be less than 600,000 USD and must not exceed 2,000,000 USD or its equivalent in GEL. In case of requesting more than 2,000,000 USD or its equivalent GEL the decision of allocating the funding will be made by the Government of Georgia.

Within the scopes the project loan / leasing may not be given for the production of wine and alcoholic beverages made from processing grapes.

The grace period of the issued loans/leasing on the principal amount is: For fixed assets – not less than 24 months; For current assets – not less than 18 months.

Under the program the following interest rates are determined for the loans for the first 24 months: from 600,000 USD to 1,000,000 USD inclusive (or equivalent in GEL) – not more than 12%; from 1,000,000 USD to 2,000,000 USD inclusive (or equivalent in GEL) – not more

than 11%.

The Agency will co-finance the interest rate by annual 10% only during the first 24 months from allocating the loan.

The interest rate determined by the programme for leasing is – not more than 13%. The Agency will co-finance the interest rate of the leasing by annual 12% for not more than 24 months from allocating the lease.

7

Agro Credits in Statistics

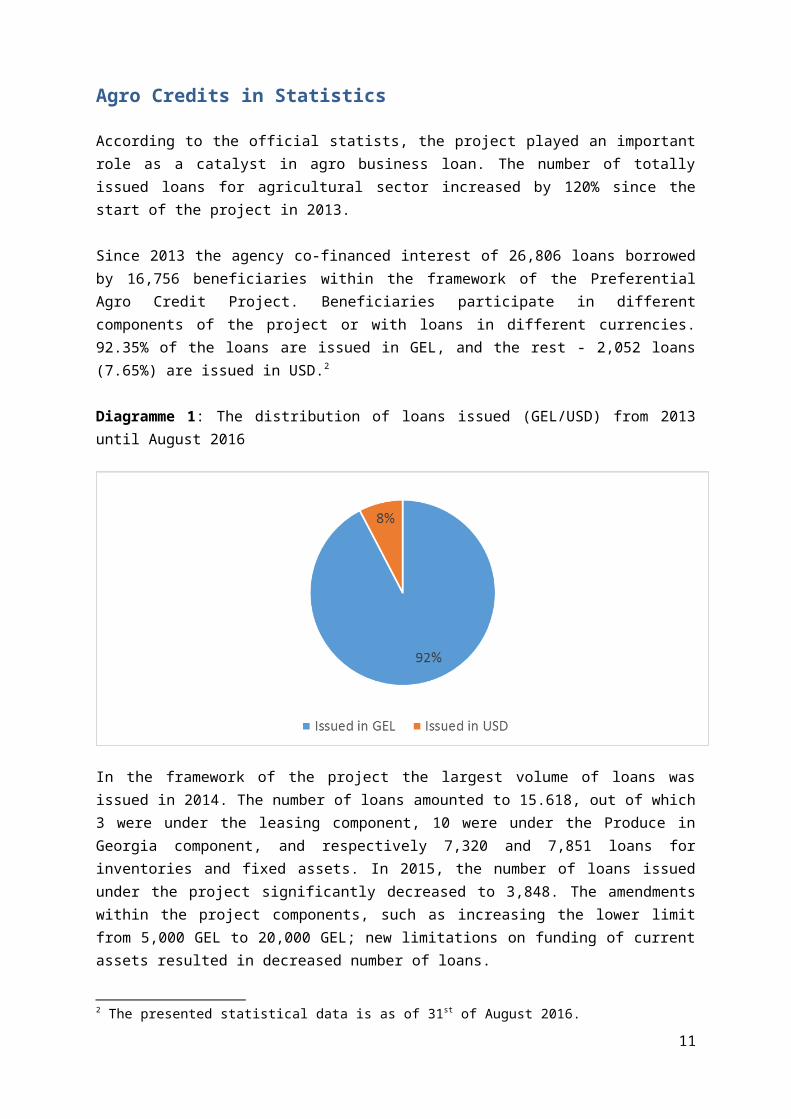

According to the official statists, the project played an important role as a catalyst in agro business loan. The number of totally issued loans for agricultural sector increased by 120% since the start of the project in 2013.

Since 2013 the agency co-financed interest of 26,806 loans borrowed by 16,756 beneficiaries within the framework of the Preferential Agro Credit Project. Beneficiaries participate in different components of the project or with loans in different currencies. 92.35% of the loans are issued in GEL, and the rest - 2,052 loans (7.65%) are issued in USD.2

Diagramme 1: The distribution of loans issued (GEL/USD) from 2013 until August 2016

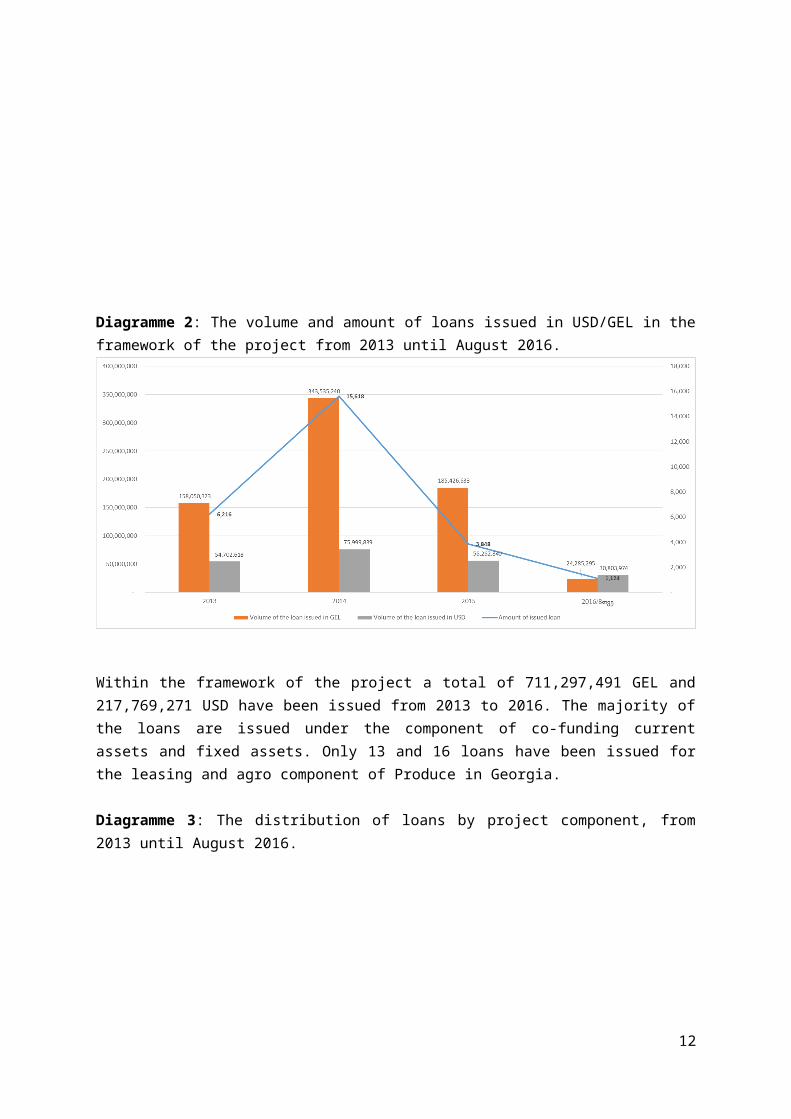

In the framework of the project the largest volume of loans was issued in 2014. The number of loans amounted to 15.618, out of which 3 were under the leasing component, 10 were under the Produce in Georgia component, and respectively 7,320 and 7,851 loans for inventories and fixed assets. In 2015, the number of loans issued under the project significantly decreased to 3,848. The amendments within the project components, such as increasing the lower limit from 5,000 GEL to 20,000 GEL; new limitations on funding of current assets resulted in decreased number of loans.

Diagramme 2: The volume and amount of loans issued in USD/GEL in the framework of the project from 2013 until August 2016.

2 The presented statistical data is as of 31st of August 2016.

8

Within the framework of the project a total of 711,297,491 GEL and 217,769,271 USD have been issued from 2013 to 2016. The majority of the loans are issued under the component of co-funding current assets and fixed assets. Only 13 and 16 loans have been issued for the leasing and agro component of Produce in Georgia.

Diagramme 3: The distribution of loans by project component, from 2013 until August 2016.

11,523

15,256

Current Assets component Fixed Assets component

The Agency spent 120,231,600 GEL with the purpose of co-financing of loan interests. The largest share of loans (45.7%) was allocated for Kakheti region. Kvemo Kartli region (22.2%) came second, while Shida Kartli region (13.8%) was third. In all other regions the loans were much less than the above-mentioned regions, for example, Samtskhe-Javakheti region accounts for a total amount of 6.3% of the loans, Imereti region 5.4%, Samegrelo 3.2%, Mtskheta-Mtianeti 1.4%, Tbilisi 1%, the rest of the regional indicators are less than 1 %.

Diagramme 4: Distribution of loans issued within the scopes of the project according to regions from 2013 until August 2016.

9

AdjaraGuria TbilisiImereti

Kakheti

Mtskheta-MtianetiRacha-LechkhumiSamegrelo

Samtskhe-Javakheti

Kvemo-Kartli

Shida-Kartli

The amount of agriculture loans issued throughout Georgia is quite low. Compared to 2006 the amount of loans issued in agricultural sector increased by 37% in 2007. In 2008 this indicator decreased by 16%, and in 2009 decreased by 20%. In 2013 there was a rise of 17% in agriculture loans, while this indicator increased to by 32% in 2014, and in 2015 it increased by 42%, in comparison to the previous year. There is a growth of 120% in the number of issued loans in agriculture loans before its start in 2012 and in 2015.

The figures are quite impressive, however, there is no current data on the current status of the financed enterprises / farmers’ businesses. Therefore, making a statistical comparison on efficiency is difficult. At the same time, the most crucial period for the lenders will be when the period of state co-financing ends. Only after co-financing ends will it be possible to see unbiased picture of the actual development of the financed businesses.

10

Assessment of the Preferential Agro Credit Project

The preferential agro credit project has been implemented by the Agricultural Projects Management Agency since 27 March 2013 under ’The United Agro project. During its implementation process the project has been modified significantly. Up to now 14 packages of changes was made to the project by the relevant resolutions of the Government of Georgia. The conducted research did not imply differentiated approach for assessing the project by its amendments. Therefore, all major components, including those which are revoked or suspended, are still analysed in this assessment. These include, for example, preferential credits starting with the lower threshold of 5,000 GEL, financing of current assets for primary sources etc.

Assessment of the project purpose and implementation process

The declared purpose of the preferential agro credit project is to support the initial production, processing and storage and sales processes by agricultural facilities through providing affordable and accessible cash funds to physical and legal entities. The project also aims to support the process of consolidation of farmers into bigger units or associations and facilitation of cooperation.

Despite the fact that the project focus has lately been fully directed towards financing the processing enterprises respective changes have not been reflected in the project aims.

At the same time, it cannot be claimed that the project aims on the support of primary production of agricultural products has been met and exhausted. Increasing the lower loan limit can be considered as an instrument for the creation of cooperatives and consolidation of them into bigger units. However, this component alone cannot provide the required support to cooperatives.

It should be noted here that in addition to the Preferential Agro Credit Project, the Ministry also implements a number of projects which contribute to the above-mentioned objectives. These include: Plant the Future, Agro Production Support Programme, Processing and Storage Facility Co-Financing Programme, Spring Works Support Project, etc.

One of the aims of the project is to facilitate the process of consolidation of farmers into bigger units or associations and supporting cooperation among them. This is one of the most challenging objectives not only for this project but also for the development of the agricultural sector as a whole. The study also focused on the issue of cooperatives. A lot is yet to be done to achieve proper development of cooperation. Increasing the lower threshold of the loan limits clearly contributes to the process of facilitation of cooperation as well as unification of the farmers into bigger units however this is not sufficient to reach the objective. Representatives of the surveyed cooperatives believe that only the accessibility to financial means is not sufficient. The main problem according to them is among the farmers since they find it difficult to reach an agreement even on smallest issues:

‘Theoretically everyone knows what agricultural cooperatives are for, however, cooperating in practice is a real issue. Our municipality has scarce land and agriculture cannot be developed without cooperation. If we were to start planning creation of some cooperative unit, then we would have difficulty choosing one supervising person. The government should consider these issues” (A quote by a representative of a cooperative).

11

Overall, it can be concluded that the declared aim of the project has only partially been met. The changes in the project shold be accompanied by reflecting these changes in the project objectives as well.

The respondents said that additional conditions should be created for cooperatives if the project aims to support creation of cooperative units. It also seems that banks find it difficult to make a positive decision on cooperatives. There were instances when certaing cooperative units met bank requirements but the members of these cooperative units had problematic individual loans that created additional obstacles. Members of cooperative units also find it difficult to reach common agreement. Some of the cooperative members are motivated and active while others are hesitant. Below are some of the quotes on similar cases:

‘I am a chairman of a cooperative. Our cooperative applied for a loan to TBC Bank. The bank told us to put our property, our houses and land in mortgage as a bank guarantee. We registered our land and after two months we received a negative response from the bank. First the problem was that out of 8 members of our cooperative union 2 were already guarantors of the borrowers outside of our cooperative. This issue was resolved, but our loan we still not approved. They just wasted our time’. ‘We applied to Kartu Bank where we were told to increase our turnover to 2 million GEL in order for us to receive 20,000 GEL loan. Only those who already possess money and capital can benefit from the project. There are no cooperatives in Zestaponi while there are 5 in Terjola. People know that there is no point to participate since they will still be unable to take loans’.

‘Of course we know that there are some advantages in uniting into cooperative unions, but there are clear issues in creating a cooperative; neither the Government nor non-governmental organisations can fully understand this. There are 20 members in our cooperative union but 10 of them are uninterested to be a part of the cooperative. They only care about receiving grants. We cannot get a loan from a bank, since we as group are unable to access loans because majority of our cooperative union members already owe individuals loans to banks’.

‘There are three main reasons why banks do not issue loans to cooperative. Firstly, some members of cooperative unions are in a bank’s so-called black lists. Secondly, they already have individual or consumer loans. And thirdly majority of cooperative members do not want to have their signatures under a loan agreement’.

Therefore, is important that the issue of cooperative be discussed separately and the whole situation be analysed and diagnosed. It is important to establish financial and non-financial needs for the development of cooperatives. Active members of cooperatives consider is necessary to have a common platform through which communication with the government would be possible:

‘It is important to hold a working meeting (throughout Imereti region) between interested cooperative unions and bank representatives, public sector, agricultural specialists, and Ministry representatives in order to discuss and establish the needs of cooperatives and the ways of solution’.

12

The most popular component of the project was loan for inventories with a lower limit set at 5,000 GEL. There is still high demand for this type of loans and some small farmers especially in mountainous regions request decrease of the lower limit:

‘Representatives of VTB Bank visited us from Kutaisi and offered a very low interest rate of 3%, but the minimum amount we could borrow was 20,000 GEL. The population does not always need such a large amount of money and the bank will not issue smaller amounts. Loans to the amount of 3,000 GEL or 5,000 GEL would be of better use for us’.

However, the survey revealed a high number of instances where these types of loans were not used in a non-target manned and in bad faith, both from side of farmers and banks.

It should be noted here that a 5,000 GEL loan cannot provide a sufficient ground for starting or building on an agricultural business. This component is more of a social impact character rather than economic. Beneficiary farmers also indirectly confirm this, when they say that loan gave them opportunity to improve their household food consumption.

With regard to terms and conditions of the Preferential Agro Credit Project and its implementation, both beneficiary and non-beneficiary name the following issues:

Non-existence of a grace period; Lack of access to loans without significant collateral; USD and GEL exchange rate fluctuations (for those who have loans in USD); Difficulties in communicating with banks and absence of agro experts in banks; The project does not target small farmers.

The surveyed farmers, experts and other field representatives positively assess the project and believe that these types of programmes create conducive environment for the development of agricultural sector. However, according to them, it is important to take into account interests and possibilities of farmers of all sizes. Below are some of the comments from respondents assessing the project:

‘It is a great programme, with realistic timeframes. The only negative side was that it did not provide agricultural insurance and the snow destroyed my greenhouse that year. I still pay my loan and this month is my last payment’ (a beneficiary farmer).

‘It is a good programme but you need to have high value assets, income to access it. Otherwise there is no chance to take a loan’ (non-beneficiary farmer).

‘The programme idea is good, but not tailored to the needs of specific regions’ (a beneficiary farmer).

‘The goal has not been reached. The farmers were unable to acquire the loans since they do not have sufficient assets. We conduct our own evaluation based on the feedback from the beneficiaries. The property and land in our region do not provide sufficient value for banks. Also the timeframes are very short. The timeframe should be until at least the planted crops start to show signs of growth’ (a local self-government representative).

‘The program is excellent and it provides great benefits. But the problem is that the farmers are unable to clearly communicate with bank representative, they do not understand each

13

other and this often leads to miscommunication (an agricultural advisory service representative).

The study has revealed that farmers had unrealistic expectations concerning the loan procedures and prerequisites for accessing the loan. Thus, after thei applications were declined by the banks their negative attitude was directed towards the banks. The attitude of farmers towards banks deserve separate discussion during the assessment of the project.

Very few non-beneficiary farmers felt that their application for loan was turned down because they were unable to properly formulate their idea. They acknowledged that they lacked specialised knowledge on issues such as preparation of financial calculations. Bank representatives on the other hand, said that there were some farmers who might have good knowledge of agricultural issues but did not possess any business-oriented skills and thus had incorrect calculations in their loan applications.

‘When we go to a bank a credit officer provides detailed information. Many people want to participate in the project, but it is difficult for us to write a loan application with financial calculations. That is why banks are hesitant to provide loans. Dealing with banks is difficult, but at the same time, the population is not adequately informed, we lack specific knowledge and skills to write a full loan application. This is what causes discontent’ (a quote of a farmer).

The majority of the farmers have a very negative attitude towards the banking sector in general due to some of the following factors:

Majority of farmers believe that the project is good and designed for their needs but the banks try to offer them loans with higher interest rates;

Farmers often are not informed about the grounds for rejecting a loan application therefore majority of them blame banks for turning down their applications;

Farmers have difficulty to understand bank procedures and think that they intentionally complication their their participation procedures.

Majority of the surveyed farmers who have above-mentioned opinion are not the project beneficiaries and their loan applications were turned down. Majority of them also think that it is necessary to have some connections in order to deal with banks. These people have negative attitude towards all banks. Below are some of the quotes from these beneficiaries:

‘The banks do not issue loans even after you provide all documentation or they offer you a loan with a very high repayment interest rate of 24 – 32%’.

‘All banks have the same answer: come back in a month, issuing of loans is suspended for the time being and meanwhile you can apply for a consumer loan’.

‘Some banks tell us that issuing of loans has been suspended for a year instead of telling us that they do not want to finance our business ideas’.

‘We wanted to get out a loan to develop our hazelnut small business. I already purchased the relevant agricultural tools and machinery and they are being installed now. We do not have

14

sufficient funds to purchase hazelnuts and wanted to get out a low interest rate loan for current assets. We applied to TBC Bank, Bank Republic and Bank of Georgia. TBC told us that they temporarily suspended issuing loans. The other two banks offered loans on very high interest rates’.

‘The bad thing is that loans were not issued in a targeted way for what they were designed for, but rather based on connections. Then these people used the received loans for other non-agricultural purposes. I could receive a loan from any bank but at a very high interst rate of 34% and would be unable to repay it’.

On the other hand, the project beneficiary farmers acknowledge that they did not face any significant procedural or administrative barrier and were easily included into the project. There were some farmers who applied for loans in several banks and received loans eventually. Below are some of the quotes from them:

‘I no connections in the bank but my loan application was easily approved by the Bank of Georgia. Before that my application was rejected by three banks’.

‘As for procedures, it was the same as when you would acquire a loan with a high interest rate. I put my assets in the bank as a guarantee. I wanted to renovate my building and this building was encumbered with mortgage’.

‘I went through the procedures very easily. The procedures were the same as during application of a standard high-interest loan. I wanted to get a loan for repairs work of my small enterprise premises and the property was used as a collateral to secure my loan’.

‘I wanted to build a greenhouse. I made applied for a loan at the bank and was included in the project. I did not have any connections’.

‘The whole process was very swift. The bank gave me the total loan amount and it is up to the lender how to use it. The grace period is 3-4 years after which you should start repaying the loan. In our case the interest rate was further decreased and I pay approximately 2%. Some banks issue loans even for 0,5%. Accessing loans becomes easier after the first successful loan application. The bank representatives periodically visit us to monitor the progress and see whether we use the loan as stated in loan application’.

The project had a significant impact on the policies of the banking sector towards the financing agricultural projects and initiatives. If the banking sector had fully ignored communication with farmers in the past they now realise that the agricultural sector could be profitable thus they have stepped up agricultural direction.

Bank representatives say that the volumes of agricultural loans have increased by 30%.

‘The volume of agricultural loans has dramatically increased by 30%. The project got many lenders interested in starting agricultural activities since half of the agricultural loan interest is paid by the government, thereby decreasing the loan burden on businesses’ (a bank representative).

15

Bank representatives have their own counterarguments on the accusations of unhappy applicants. According to them, most frequently the reason for denial to issue a loan is low creditworthiness, negative credit history, lack of security etc.:

‘The most important factor for banks issuing loans is solvency, or the lenders’ ability to repay the loan. Therefore we check the creditworthiness of the clients. Some of them have no business, are not engaged in agriculture in any way. We cannot finance pure start ups. If lenders have no experience in the agriculture and have no income from other sources either then we have to turn down their loan applications’ (a bank representative).

‘All approved loan applications included some collaterals. All successful start-up project ideas requested loans for fixed assets, not current assets. These included construction, renovation of the existing premises, etc. Therefore, in all such applications there were some basis for collateral. I cannot recall a single case when project proposal was rejected for non-existence of collateral’ (a bak representative).

‘There were frequent cases when a farmer comes just wanting to get some money withyout any financial calculations or a project idea, with no documentations or a plan how to repay the loan. We had to turn down these cases’ (a bank representative).

The study also focused on farmers’ opinions on how to improve or modify the project. Several key issues have been revealed summarised below that might have an impact on achieving the project aims.

Increasing farmers’ knowledge on modern technologies and give preference to the existence oif these skills during the evaluation of agricultural loan applications:

‘Agricultural practices have not changed in my village. Farmers still use the same methods to look after their land as they did years ago. There are advanced technological developments technology in other countries. Our farmers need to acquire new technologies and knowledge on innovative productions’.

‘I own two hectaires of agricultural land. Recently I paid 1,600 GEL for fencing of the landplot. Now I need an expert opinion on how to use my land more productively, which agricultural products to plant’.

Additionally, it should be noted that the agricultural advisory services under the Ministry of Agriculture are quite efficient. However, the present study revealed that it is difficult to bring these new methods and technologies to farmers and even harder to implement them in practice.

Agro loans should have grace periods: Both project beneficiaries and non-beneficiaries agree on this:

‘If we aim to develop small businesses then some time should be given to lenders to develop and expand their businesses and only after that to start repaying loan interests. It is unreasonable for me to acquire money for inventories and have to return it in the next month’.

16

‘My loan application was approved easily. But if we want to see the long-term impact, then the issued loans should also be longer-term, with longer grace period’.

An overwhelming majority of the respondents feel that at least 8-months grace period would make a significant difference to farmers and would be a better use of the accessible financial resources.

Agricultural experts in banks: Majority of the surveyed respondents believe that the banks should expand recruitment of agricultural experts if they plan to expand this direction. According to them, the issue of solvency is one thing but equally important is the sound project idea, especially when it is related to innovation.

‘A bank should employ an expert agronomist. I once dealt with a bank representative from Kutaisi and realised that he did not understand the subject matter I was discussing. A bank should have at least one agronomist in order to be able to make unbiased and realistic evaluation of the agricultural projects. For example, there is a certain species of strawberries that can produce 20 tonnes of harvest per hectare. Because of the technical nature of this issue I was not able to convince the bank representative that I was telling him the truth. Thus my application was rejected’.

The government cannot oblige banks to employ specialised expertsm, however, this should be in the interest of banks themselves so that they could make objective assessment of a business idea proposal.

Promotion of the concept of agro insurance projects: farmers either are not fully aware of the benefits of agricultural insurance concept or do not use the opportunity. Some of them have a vague understanding of the importance of agricultural insurance especially during having an agricultural credit, but at the same time they undertake no practical steps in this direction.

‘This project is very useful but it is essential for insurance to be one of its components. It could be the case that I take out a loan, develop my business and due to natural disasters I loose all of my harvest. How will I repay the loan?’ (a farmer).

‘Agriculture is a very unique and specific field that requires special understanding. There are cases when an honest farmer with sound ability to repay his loan is put in a difficult situation when as a result of natural disasters loses his/her harvest s/he cannot repay his/her loan. Therefore, agricultural insurance is crucial. As far as I know the Ministry has an agricultural insurance programme, but its scope is limited. It would be good to expand the insurance programme’ (a bank representative).

There is a separate set of problems faced by beneficiaries who have loans issued in US dollars. High inflation rate of national currency in relation to US dollars is a heavy burden on lenders, whose income is in national currency and high rate of inflation of national currency results for them in higher loan repayment amount. The project does not limit applicants to access loans only in national currency. But there were a number of instances when banks gave preference to loans requiring US dollars.

‘The amount of my loan is 230,000 USD and I pay 4,002 USD each month. When I initially started repaying my loan I used to pay around 6,000 GEL a month. This amount has now increased up to 10,000 GEL a month’ (a project beneficiary).

17

Clearly, significant inflation of the national currency has a negative impact on business activity. On the other hand, the loan applicants are free to choose the currency of the loan, therefore no additional remedial steps could be taken in this regard to mitigate the negative impact of national currency devaluation on the lenders.

18

Project Impact on Agro Business

Official statists indicate that the project played an important role as a catalyst in the process of development of agro business financing. The overall number of issued loans for agricultural sector since the start of the project in 2013 has increased by 120%.

The numbers are rather promising although there is no data on the present status of the financed business projects and ideas. Therefore, it is difficult to make a quantitative judgment on the project’s effectiveness. The crucial period will be when state funding ends since only then will it be possible to see the real picture of the efficiency of the project and how much it contributed to the development of agricultural sector, business activities and what financial impact it made.

The study also focused on the farmers’ evaluations and visions on the impact of the project. Most of them share a belief that these types of programme can make a real difference to rural communities. However, they also pointed out that the project targets the existing businesses or individuals who already have income from other sources.

Overall, the beneficiaries think that the project enabled them to implement their business ideas and expand on the existing businesses in a much shorter time that would have achieved the same result without the project.

‘One lender expanded on the existing onion business, purchased agricultural equipments with the loan and expects harvest of at least 200 tons. Another groups of lenders built a cattle farm with the agro loan but they would have built it anyway, since they are a group of businessmen, they have money and business turnover. But these are still some separate singular cases, seven to eight successful businesses are not sufficient enough for the development of a whole region. The positive impact is there, but not its scope is limited’.

‘I accessed a preferential loan in 2013, received 100,000 USD. Initially, my repayment interest rate was 3% which has now been reduced to 0%. I have greenhouses. This project was a big relief for me. I would have probably still been able to expand my business but it would have taken me much longer to achieve the same results’.

‘I am not engaged only on this project. I plann to expand my business further once I repay the loan. The result is that I have a well-functioning farm. It would have taken me much longer to get these results without the project’.

However, there are some farmers who started thinking about the expansion of their business, only after they received information about the poject. According to bank representatives many loan applicants had businesses in the city and started agricultural activities only because of the project with the hope to receive the preferential loan.

‘I would have been unable to make the harvest without this project since I would not be able to pay a high-interest loan. I have a greenhouse and my yield has increased by about 50%’.

‘I would not have dreamed about expansion without the preferential low-interest rate loan’.

19

‘I owned a farm of 70 cattle and their number have now increased to 140. I have a shelter for all 140. Without the loan, I would not be able to build the shelter or I would have to sell my cattle’.

Therefore, we can conclude that the project has increased the motivation of farmers and businessmen. There were cases when farmers started thinking about creating new farms but were unable to obtain loans and still put their ideas into practice using their own resources or by finding alternative sources. This will doubtlessly have a positive effect on the development of agriculture.

Regardless of whether a farmer is a project beneficiary or not, everyone agrees that the project has a positive impact on agricultural production. But the respondents also agree that the marketing and sales part still remain especially problematic:

‘Agricultural production has increased but the problem is its sales since the market it very small’.

Additionally, some of the respondents feel that, although the influence of the project has been positive so far, a certain period of time must pass to see the real results.

‘A large farm has been financed in our area and still operates successfully. It has been connected to a milk processing facility. Another large greenhouse farm has been funded, which provides its products to supermarkets in Tbilisi. However, agriculture development does not get immediate results. The farmers who owne these financed enterprises have increased their profits. The project contributed to the development of agribusiness for the moment but the real impact and long-term results will be seen in five years’ time’.

On the one hand, the farmers are asking for decrease of 5,000 GEL loan threshold on current assets but at the same time they also say that that this component had no any impact on agribusiness at the time. Mainly small farmers are interested in these types of loans, which pursue agricultural activities mainly for their own household purposes and not as a regular economic activity. Bank representatives also say that the usage of loans for non-approved purposes was highest among the low amount loans.

One of the most important indirect economic results of the project is the creation of a precedent of a successful agricultural business, which is a good example for other potential entrepreneurs.

‘The positive side of this project is that those people who can start or develop a successful business can serve as an example for other farmers. Others also become interested, those who have starting capital and would benefit by receiving additional support through this project. Nevertheless, it should be taken into consideration that this project is not for the masses’ (a farmer).

‘The project has provided motivation for the development of agriculture in the country. Business groups operating in a totally different field of work suddenly expressed interest to participate. Many individuals, who live in the city and have businesses invested money in agriculture in order to receive the preferential loans and create start-ups. This supported the development of agriculture’ (a bank representative).

20

The study also revealed a number of cases when farmers’ applications were rejected but they still started business with their own resources. Therefore, one of the indirect results of the project is the increase of awareness and change of approach among rural population. After receiving information about the project these individuals started thinking about business ideas and regardless of the fact how well the idea was formulated this type of change in awareness should be considered as a positive effect.

Statements such as ‘I grew up in a village and I understand agriculture, I hoped to use this opportunity to start my own business but sadly I was not given a loan since I did not own an already existing business. But nevertheless I found other opportunities together with my friend and now we are getting ready to create our own start-up’ and ‘I know some people who received financing from the bank, but I could not take a loan, and this was disappointing. However, I still plan to find financial means from a different source and realize my plans’ were made by the farmers participating in the focus group discussions.

21

Project Sustainability and Performance Risks

All respondents agree on the significance of the project on the development of agricultural sector and that it should be continued. Morover, the farmers also believe that without such projects development of agriculture in the country would not be possible. They frequently bring examples of other developed countries and underline the importance of longer-term loans with respective grace periods.

While assessing the project sustainability one of the biggest challenges named by the farmers is the existence of grace period that matches the whole agricultural cycle required for an agricultural business. Access to current assets is also named as an important condition:

‘The second, third, fourth months are very challenging. Therefore, grace periods for each financed business idea should be determined on a case by case basis’.

‘Farmers are always in need for current assets and farm input in spring. These include seeds, pesticides, chemicals’.

‘A minimum of a 5-6 months’ grace period should be given to the lenders. Plowing season starts in April. If I get a loan in April I would need a grace period until at least August so that I can use the loan, get a bigger harvest, and this will ease the burden on farmers’.

‘It would be good if the project requirements are adjusted, if it becomes loner-term and mer easily accessible for farmers. Interest rates should be repaid only after the end of the grace period’.

Naturally, there is a constant demand for preferential loans especially in the field of agriculture. With time supporting specific direction of agricultural sector and stimulating competition will become even more important.

The study learnt risks associated with both project format as well as farmers’ the so-called ‘mentality’ as perceived by the project respondents.

One of the biggest programme risks is the utilisation of loans for non-approved purposes. This risk was slightly decreased by raising the lower threshold of the loan although it still persists. This is also associated with the lack of a rigorous monitoring practices of the spending of the issued loans for the approved aims:

‘The biggest risk is an absence of proper monitoring. Monitoriung of the project is being done both by the Agency and the banks. In the absence of rigorous monitoring over the approved spending of the loans there are riskts that the issued loans will not be spent according to the approved purpose (a bank representative).

Natural disasters pose a serious risk not only to this project but to the whole agriculture in general. There is an agro insurance project in place but both the farmers and the bank representatives highlighted the greater need for insurance projects. We can only speculate what is the reason for these, whether there is a lack of information disseminated among the farmers on the availability of insurance projects or the farmers hesitate to make practical steps in this direction.

22

‘There is always a risk that natural disasters could destroy our crops leaving us unable to repay our loans. That is why it is important that insurance is a part of the loan’.

‘When a farmer becomes unable to repay a loan due to the damaged crops as a result of natural disaster, either banks should take this into account and offer grace period for repayment or the issued loans should include agricultural insurance’.

The side effects and risks associated with the preferential agro credit project and other similar projects should also be mentioned. These are unrealistically high expectations of the farmers towards the government summarised below.

Unrealistically high expectations that each farmer will be receive the so-called ‘free money’. Various state subsidy programmes that were not properly communicated to the population have created an illusion among some farmers that they will be given the so-called ‘free money’:

‘This type of mind-set among farmers has to change or it will always lead to false expectations’.

The farmers have become too dependent on the government and hold the government responsible for the development of their business, including sales of crops. A part of the focus group participant farmers said that that there is no point in the government financing of the project if it fails to help them in the sales process of their harvest, crops and production at the prices acceptable to farmers. They also believe that the government should cover the agro insurance, agro innovations etc. The governmet support in the form of agricultural projects for the development of agriculture is important but at the same time this should not be a demotivator for farmers.

Low level of knowledge among the farmers on business processes. At this stage, the experienced farmers admit that most of the individuals engaged in agriculture do not possess necessary knowledge and skill to plan and manage agricultural enterprises and projects. Hence, their communication with banks is problematic, they are unable to estimate and forecast costs. They need to develop basic marketing skills to sell the produce. They have no access to any type of information database where they would be able to see who could be potential buyers of their products.

As the assessment results of the project impact, risks and project aims show the project sustainability is not sufficiently rigorous but rather of a medium level. To increase the impact of such projects, as well as achieve higher level of sustainability and maximum results of the subsidised loans projects it is necessary to make further steps in the direction of agricultural development. Possible actions could include but not limited to inittiatives such as the expansion of farming enterprises, building on farmers’ knowledge and skill, initiation of modern technologies and methods etc.

23

Assessment of Farmer’s Expectations, Attitudes and Needs Towards the Preferential Agro Credit Project

Farmers provide an ovcerall positive evaluation of the agricultural projects financed by the Ministry of Agriculture, including the Preferential Agro Credit Project and believe that such initiatives support the development of rural population. However, there is a negative attitude towards the banks especially among those farmers whose loan applications were rejected.

Some farmers who received loans provide overall negative feedback on banks. The following possible reasons have been revealed by the study in the farmers’ attitudes towards banks:

Exessively high expectations from the very beginning as a result of poor understanding; Lack of / insufficient experience of working with documentation; Lack of skills for financial calculations; Lack of understanding some basics of operations of financial sector; A stereotype of a ‘robber’ towards the banks.

Farmers have difficulty differentiating between the state and private sectors. Majoity of them do not have full understanding of what interest rate co-financing means very often they would express an opinion about creating a ‘government-owned agricultural bank’. They do not fully understand why the private banks participate in the preferential agro credit project. At the same time, they believe that the banks participating in the project are fully independent in the decision making processes and that the government does not have any control over them. Below are some of the assessments made by the farmers, showing their attitudes towards the banking sector:

‘If farmers are accountable to everyone, how come the banks are not liable for their actions? The interest rates are so high that there is no point in even discussing this whole project’ (a non-beneficiary farmer).

‘I pay 3% and the government finances the remaing 12%. I think that a 15% loan is already not a preferential loan. The banks act in an unfair way. Why should the government have to pay such a large amount of money? It would have been much acceptable if the total interest rate were 8%’ (a beneficiary farmer)

‘Let us assume that a cooperative union makes a certain payment, say an equity fund is created worth of 100,000 GEL. The government should contribute to securing at least 20% of its collateral. A cooperative is a union and will be able to make the payments. But in reality, we are not able to convince banks and neither is the government since banks are a huge structure’ (a cooperative representative).

‘A maximum amount of of 50,000 GEL will be sufficient for a cooperative. Instead of making banks even richer, the government should give this money directly to us, and we will repay this money as soon as we start receiving a yield’ (a cooperative representative)

Bank representatives are also informed about these kind of attitudes of farmers. They also confirm that especially at the initial stages of the project there were many farmers who would come to the bank without any documentation just with a desire to receive a loan.

24

‘Some farmers trule believed that they would receive a loan just by coming to the regardless of the fact whether they owned a farm or had any relevant experience. We explained the details to them. It took a lot of work on our part. They had an illusion that everyone would be just given money for free’ (a credit officer).

Expectations of farmers are very high and unrealistic regarding the responsibilities of the government. Ecept for the tight oversight of the banking sector majority of them also believes that the government should ensure sales of that the farmers harves at the prices that are acceptable for the farmers.

Thus we assume that this is one of the side effects of recent state initiated projects or international programmes in agriculture. Farmers avoid full ownership and decisions maiking and feel that ‘someone else’ should overcome challenges faced by them. Among other things, farmers feel that it is a direct responsibility of the government to take care of the sales of their produce:

‘The farmers’ work should be more appreciated. The government has to purchase the crops or help the farmers in the sales process’ (a farmer).

‘The project helped me increased production of organic wine but I have to compete with low quality cheap wine producers. The government should help me sell my product at a good price’ (a farmer).

In connection with the above, it is very important to undertake all relevant actions to raise awareness among the farmers and contribute to changing their attitudes so that they are able to take on initiative. This is a long-term process but because the farmers do not have basic marketing skills and understanding of how the sales processes work they try to take the blame on someone else. It is thus very important to equip the farmers with basic marketing skills.

There were cases when farmers simple did not seem to comprehend why would anyone want to buy imported goods whilst their produce is all organic and of high quality. Farmers find it difficult to understand that all-natural does not necessarily translate into higher demand for their goods. At the same time, majority of the surveyed farmers do not make an effort to increase the sales of their produce.

Another widely-spread stereotype among the farmers is that it is essential to have the so-called ‘connections’ to receive a preferential loan. The format of the study does not allow to either confirm or reject these assumptions. At the focus group discusasions even those farmers that had not applied for the preferential loan said that participating in the project does not make sense unless one has connections. Opinions similar to the following are often expressed at focus group meetings:

‘Such projects are conducive to the development of agriculture, however, they should be accessible for everyone and not only for those individuals who have connections that can help them receive loans’.

Therefore, many farmers did not even try to apply for preferential loans because of the above stereotype. This should be targeted by enhanced communication and information component. Addressing this issue is important in order not to overshadow the project reputation but more importantly not to demotivate actively engaged farmers.

25

Some farmers ask for tight monitoring of the financed projects and the beneficiaries . They say that many bad faith farmers received loans for some reason.

‘For example, there is a person who received 10,000 GEL in grant and believes that he will not be asked to repay the sum after 5 years. As for me, my application was denied by the bank’.

‘There should be a strict monitoring of the project ideas implementation in order to see whether the loans are used for the approved purpose. It should be strictly studied which farmers are applying for loans with honest intentions and which ones want the money for something else’.

‘The government’s money should be given to farmers who are really motivated to get the work done and should not be handed out to all farmers equally’.

It is important to disseminate information about the monitoring methods, processes and the positive results and practices in order to avoid spread of negative attitudes.

Farmers also expect the government to fight against falsified products and dishonest farmers. This issue was brought up frequently among wine producers:

‘The project is very good but one of the problems I encounter is that my product is unable to compete on the market since it is natural and there are so many falsified products for a lower price. I was told by the food safety agency that they checked many stores but no wine matched the quality of my wine. Although no stores were shut down, I guess there is no point to have these inspections’.

Naturally, agricultural entities cannot and should not regulate market prices or consumers’ choices which product to buy. But it is important that all entrepreneurs and retail shop owners to be under the control of the system.

Official or informal information spread among farmers has a big influence on their attitudes and expectations. Therefore, the communication strategy of such projects have a big impact on its results. The study found the following:

The information was not disseminated in an accurate manner and therefore it failed to be interpreted correctly and wrong expectations were created;

It is important that an intensive informational campaign to be conducted not only during the project initiation phase but during its implementation process. It is important for the farmers to be correctly informed about issues such as the suspension or initiation of a component; change in the funding limits, etc.

It is equally important to spread information on successful cases as well as discontinued components, for existing stereotypes to be slowly diminished;

It is important the information to be disseminated at a regional level on the financed enterprises so that farmers and the community can see the real entrepreneurs financed by the project.

26

The local population gets information from the television, ICC / RCC and bank representatives. Information disseminated among farmers themselves also plays a big role. Farmers have more or less similar opinions on receiving the relevant information:

‘The project achievements should receive wider coverage with more detailed and clear information. For example, approximately 2 million USD’s worth of agro credit has been issued in my region. I know that there have been established 3 or 4 cooperative unions and up to 10 small enterprises within the project. But I am interested to know the impact of these financed business projects on the economic development’ (local population representative).

‘Information about the project is not always easily available and transparent. This needs to be improved. I find it difficult to understand whom to address for more detailed information, what is the project about, how you can participate in the project etc.’.

‘Expectations towards the project were and are still high but I still do not know whether my understanding of the project is correct. We have no answers and ask each other questions to get information’.

It is important to revise the information and communication strategy of agricultural projects in general and to ensure adequate awareness raising among farmers towards such initiatives. Information dissemination only through mass media is not sufficient since the farmers have a tendency to interpret the information in their own way. Therefore, consulting services and the local government representative have a crucial role in this.

27

Concluding Findings and Recommendations

One of the important indirect effects of the project has been promotion of successful agricultural business activities and nation-wide success stories. Such examples facilitate the process of getting other potential entrepreneurs interested in taking up such activities.

It is thanks to this project that banks had to change their approaches towards the financing of agricultural projects. In the past the banking sector would avoid farmers’ proposals but not having seen the positive results of their agricultural activities they realise that agriculture can be profitable. Thus the banks have stepped up agricultural direction. According to the official statistics, the number of agricultural loans issued from the start of the project in 2013 have increased by 120 %.

The beneficiary farmers are partially unsatisfied with issues such as lack of a grace period, low availability of unsecured loans, exchange rate fluctuations in those case when loans are issued in USD; difficulty in communicating with banks and the absence of qualified agro experts in bank offices. The project is not designed to target small farmers specifically as there were expectations at the initial stage of the project.

Expansion of farms and supporting cooperation is one of the most challenging objectives not only for this project but for the development of the overall agricultural sector. In order to achieve a desired level of cooperation there is a lot of work to be yet done.

Increasing lower limit threshold of loans is a stimulus to achieve expansion of cooperative into bigget units, but this is not sufficient for achieving the stated goal. The surveyed cooperative representatives believe that only accessibility to loans is not sufficient and that the main problem is in the inability among the farmers to reach an agreement. Banks also find it difficult to reach decisions on cooperatives.

Farmers have a negative attitude towards the banking sector which is mainly caused by the following reasons. Most of the farmers believe that the project is well-designed and targets them but the banks offer them loans with higher interest rates. Oftentimes the farmers do not have information about the discontinuation of a project component and think that these are banks’ own decisions. The farmers find it difficult to understand bank standards and procedures and feel that banks intentionally created artificial barriers to complicate the process of participation in the project.

Agricultural experts in banks. Many respondent farmers feel that the banks should recruit agriculture experts if they intend to continue financing agriculture direction. They feel that solvency is an important factor while evaluating the project ideas, but equally important are other factors, such as the content of the project proposal and ability of the banks to evaluate the project idea impartially and professionally, especially if it deals with agriculture innovations. The government cannot interfere in the internal organisational structure of the banks and oblige them to recruit agriculture experts. This should be within the interst of banks themselves.

Targeted dissemination of information on the project to avoid misinterpretation. The study found that many of the assumptions of farmers were simply not true but nevertheless the farmers held firm views. The information spread among the farmers significantly impacts the farmers’ attitudes and expectations. Therefore, the project information strategy has a big impact on the project results. Extensive information campaign is essential not only at the initial stage of the project

28

launch but also during its implementation period. Farmers should be informed of the issues such as initiation and suspension of project components, changes in funding limit thresholds etc. Spreading information on the successful cases and the discontinued components are equally significant in order to eliminate biased attitudes of farmers. Information should be disseminated at the regional level regarding the financed projects so that the interested parties and the public in general can see the positive impact.

Product marketing and sales support. It is without any doubt that the government should not provide the farmers with the direct marketing services. This will only have a very negative effect on the farmers’ mind-sets and behaviour as well as the development of the sector. However, supporting processing enterprises will be conducive to sales of agricultural products. The study showed that farmers have no information on potential clients or methods of selling their products. Their sales experience is mostly limited only to selling their products to wholesale buyers and on the agricultural markets. It would be beneficial to have an information database so that the farmers can have access to it. It would also be good to support knowledge provision to farmers on sales strategies. Farmers view the market as their local area and might not consider some other alternatives.

Increase farmers’ knowledge and skills. ICC / RCC of the Ministry of Agriculture are working very actively in this direction. But the study results show that it is very difficult to provide the farmers with new methods and even harder to implement them. At the same time, it is a priority to acknoiwledge that there are gaps in this and therefore there is a need of further knowledge and skills development.

Promotion of agro insurance programmes and other insurance-related ideas. Although there is an ongoing agro insurance programme, the farmers are not informed about it or are unable to take advantage of it. Some farmers acknowledge the need of agro insurance but fail to take any real steps in this direction.

Provision of information (agricultural sector specific information as well as agricultural information according to geographical regions) on the agricultural sector to farmers.

This information would play an important role for farmers. This could include information about what agricultural products have better prospects for development according to geographical areas; what are the price dynamics of agricultural produts; information on consumers’ interest etc.

29

Appendix 1. Focus Group Guidelines

Focus Group Guidelines

Study aim: The qualitative assessment of the preferential agro credit project implementation process and impact, the reveal of the tendencies of the farmers’ attitudes, expectations and needs regarding the agro credit project and the development of relevant recommendations.

The specific objective of the guidelines: to receive information regarding the evaluation, opinions, attitudes, subjective perception and expectations of the farmers participating in the Preferential Agro Credit Program, as well as identification of new criteria and directions, if any.

Moderators: Introduce the objectives of the study to the group members. Ask them to introduce themselves shortly and state in what way they participated in the program, whether they are applicants, beneficiaries or plan to apply. Additionally, they should state the field or component where they already are/ or want to participate in.

Components1. Preferential agro-credit for inventories2. Preferential agro-credit for fixed assets”3. Preferential agro-leasing4. The agricultural part of the state program "Produce in Georgia".

Task #1. General assessment of the preferential agro credit state program. Main purpose, strengths and weaknesses.

Important: to indicate actual examples, explain/justify their opinions; try to obtain evaluative information, epithets, reveal their attitudes and expectations. Ask them to describe specific examples (cases). # Question/Issue

1Generally, in what way did you participate in the agro credit program and how would you assess it and its importance in developing agriculture in your municipality?

In your opinion, what is the main purpose of this program and what should be its purpose in optimal conditions?

2 How important is the program for your specific agricultural activities? (Moderator: If the individual is a beneficiary, try to obtain information in relation to data, e. g. the turnover increased by %, purchase of new machinery, etc.)

3 How did you hear about the agro credit program? In your opinion to what extent, do you have information about the processes and conditions of the program? Please tell us how easily you can obtain information about the program, to what extent and where?

4 In your opinion, how well managed is the program participation process? What positive sides does it have and what would you change?

5 (Moderator: Ask the question if you have beneficiaries): Please tell us about the path you went through in order to participate in the program. Which stages/conditions were sufficient and what obstacles did you run into? What would be your recommendation and what

30

changes would you make?6 In your opinion, what are the main strengths and weaknesses of this program

7 In your opinion, what are the main flaws and weaknesses of the program

Moderator notes:

Task #2 Farmers’ expectations and attitudes # Question/issue1 What expectations did you develop when you heard about this program and how much did

they differ from the real procedures?

2 In your opinion, what component should be added and which should be canceled for the program to meet the farmers needs better?

3 Please numerate the fields in which preferential agro loans are needed for the development of agriculture in your region (regardless of the fact this field is included in the program or not at this stage)

4 Besides preferential agro loans what can be done on the part of government for quick and effective development of agriculture (do not suggest answers: for example, trainings, demonstration land plots, land registration, etc.)

Moderator Notes:

Task#3 Program needs, main risks and improvement ideas