© the mcgraw-hill companies, inc., 2004 slide 3-1 mcgraw-hill/irwin chapter three consolidations...

TRANSCRIPT

© The McGraw-Hill Companies, Inc., 2004

Slide 3-1

McGraw-Hill/Irwin

Chapter Three

Consolidations Consolidations – Subsequent – Subsequent to the Date of to the Date of AcquisitionAcquisition

© The McGraw-Hill Companies, Inc., 2004

Slide 3-2

McGraw-Hill/Irwin

Consolidation - The Effects of the Passage of Time

In Chapter 2, we looked at consolidation on the date of the combination was created.

As time passes, the investment account changes, and the consolidation process becomes more complex.

In Chapter 2, we looked at consolidation on the date of the combination was created.

As time passes, the investment account changes, and the consolidation process becomes more complex.

© The McGraw-Hill Companies, Inc., 2004

Slide 3-3

McGraw-Hill/Irwin

SFAS No. 142 - Goodwill and Other Intangible Assets

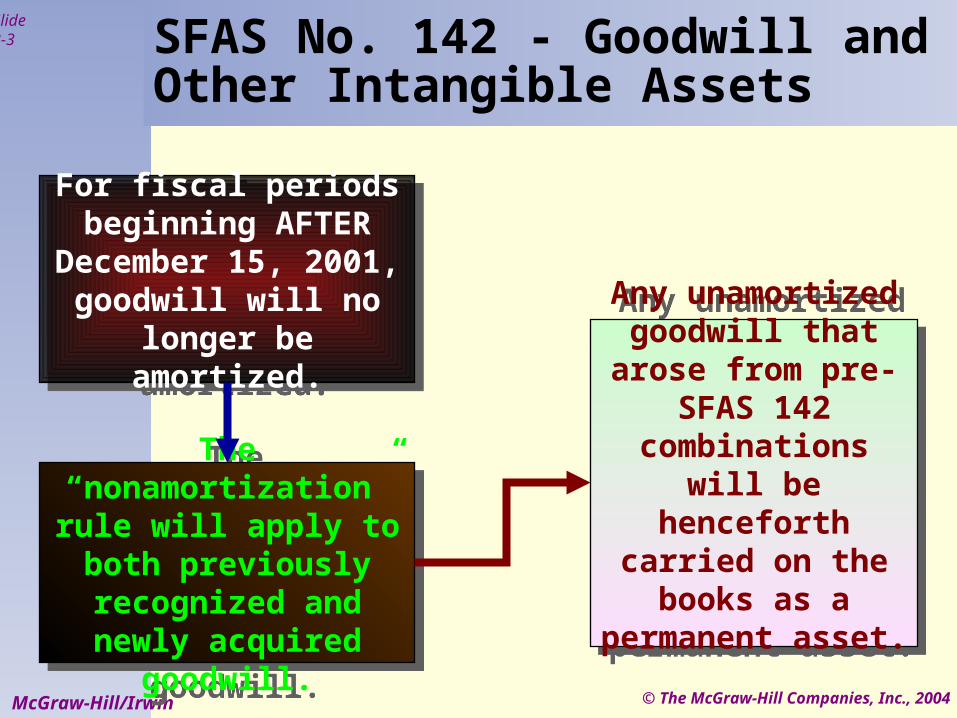

For fiscal periods beginning AFTER

December 15, 2001, goodwill will no longer

be amortized.

For fiscal periods beginning AFTER

December 15, 2001, goodwill will no longer

be amortized.

The “nonamortization” rule will apply to both previously recognized

and newly acquired goodwill.

The “nonamortization” rule will apply to both previously recognized

and newly acquired goodwill.

Any unamortized goodwill that arose from pre-SFAS 142 combinations will

be henceforth carried on the

books as a permanent asset.

Any unamortized goodwill that arose from pre-SFAS 142 combinations will

be henceforth carried on the

books as a permanent asset.

© The McGraw-Hill Companies, Inc., 2004

Slide 3-4

McGraw-Hill/Irwin

SFAS No. 142 - Goodwill and Other Intangible Assets

Generally, once goodwill has been recorded, the value will remain unchanged.

Generally, once goodwill has been recorded, the value will remain unchanged.

Sale of all or part of therelated subsidiary.

Any impairm ent in the valueof goodw ill should be reported

as an extraordinary item.

A determ ination that goodw illhas experienced a permanent

im pairm ent of value.

Tw o circum stances exist thatw ill result in adjusting the am ount

of goodw ill on the consolidated balance sheet.

© The McGraw-Hill Companies, Inc., 2004

Slide 3-5

McGraw-Hill/Irwin

Consolidation - The Effects of the Passage of Time

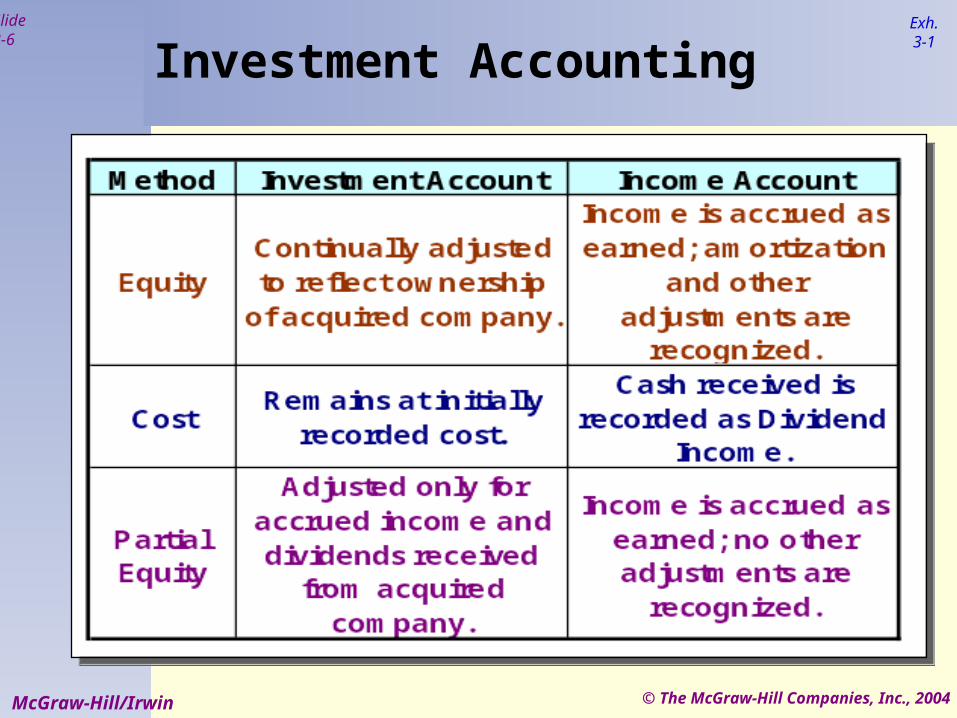

The parent can account for its investment one of three ways:

Equity MethodCost MethodPartial Equity

The parent can account for its investment one of three ways:

Equity MethodCost MethodPartial Equity

Let’s compare the three methods briefly.

© The McGraw-Hill Companies, Inc., 2004

Slide 3-6

McGraw-Hill/Irwin

Investment AccountingExh.3-1

© The McGraw-Hill Companies, Inc., 2004

Slide 3-7

McGraw-Hill/Irwin

Before the consolidation balances can be determined, the Parent’s investment account must be adjusted to reflect the

application of the equity method.

Subsequent Consolidation - Equity Method

Record the Investment in Sub on the acquisition date.

Recognize the receipt of dividends from the sub.

Recognize a share of the sub’s income (loss).

FMV adjustments and other intangible assets.

Record the Investment in Sub on the acquisition date.

Recognize the receipt of dividends from the sub.

Recognize a share of the sub’s income (loss).

FMV adjustments and other intangible assets.

© The McGraw-Hill Companies, Inc., 2004

Slide 3-8

McGraw-Hill/Irwin

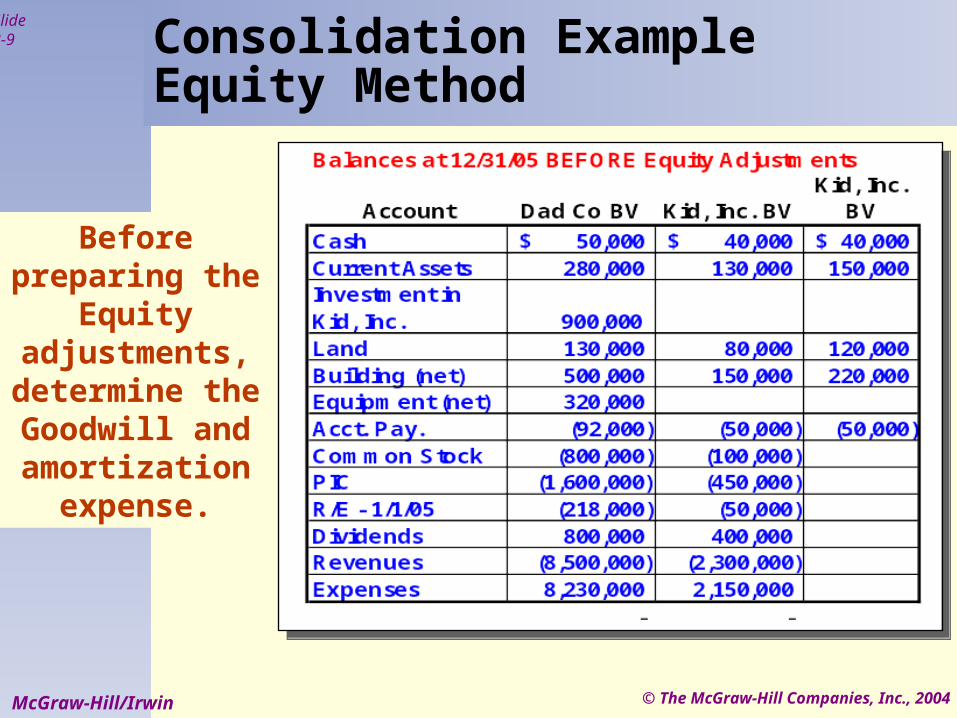

On 1/1/05, Dad Co. purchases 100% of Kid,

Inc. for $900,000 cash.

Kid’s net assets on 1/1/05 was

$600,000.

Consolidation ExampleEquity Method

© The McGraw-Hill Companies, Inc., 2004

Slide 3-9

McGraw-Hill/Irwin

Consolidation ExampleEquity Method

Before preparing the

Equity adjustments, determine the Goodwill and amortization

expense.

© The McGraw-Hill Companies, Inc., 2004

Slide 3-10

McGraw-Hill/Irwin

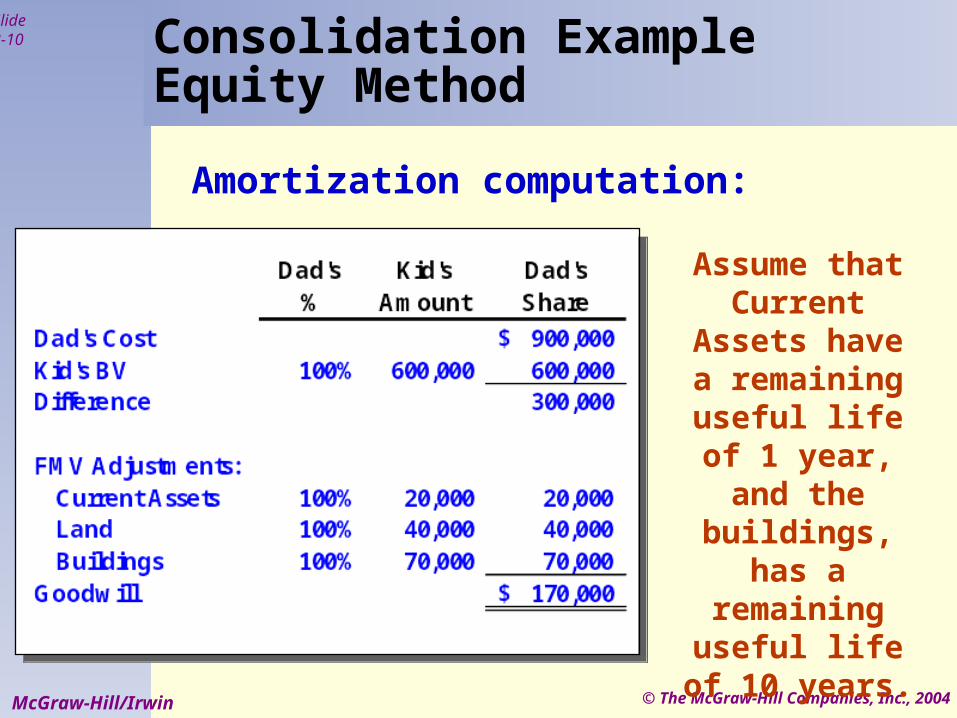

Assume that Current Assets

have a remaining

useful life of 1 year, and the

buildings, has a remaining

useful life of 10 years.

Consolidation ExampleEquity Method

Amortization computation:

© The McGraw-Hill Companies, Inc., 2004

Slide 3-11

McGraw-Hill/Irwin

Amortization computation:

Consolidation ExampleEquity Method

© The McGraw-Hill Companies, Inc., 2004

Slide 3-12

McGraw-Hill/Irwin

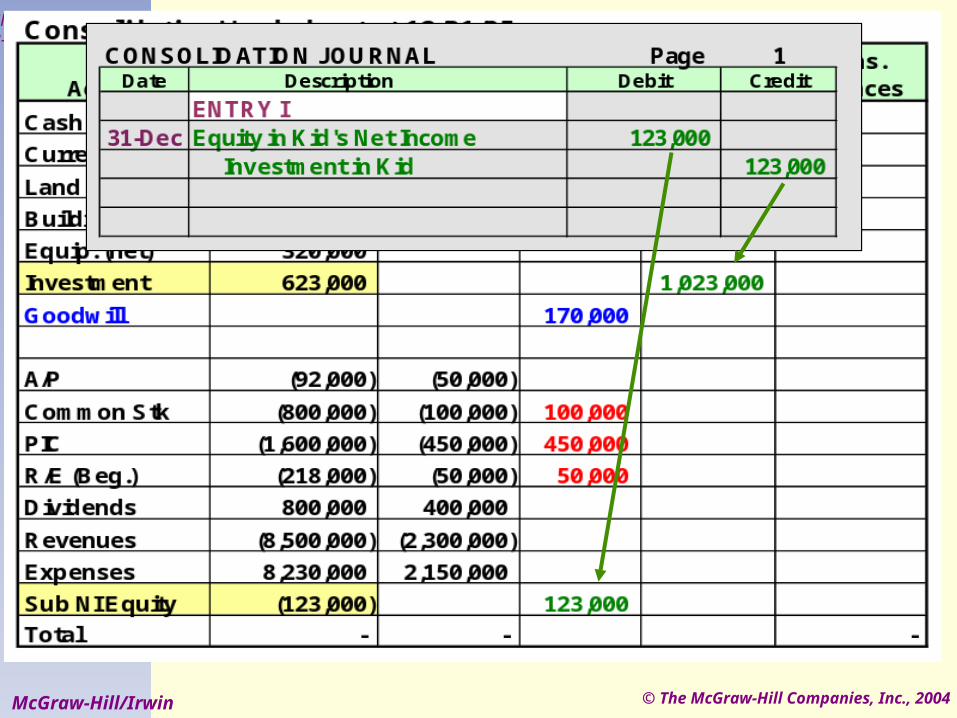

First, prepare the entry to recognize First, prepare the entry to recognize Dad’s share of Kid’s net income.Dad’s share of Kid’s net income.

Dad owns 100% of Kid.Dad owns 100% of Kid.Kid’s Net Income = $150,000Kid’s Net Income = $150,000

First, prepare the entry to recognize First, prepare the entry to recognize Dad’s share of Kid’s net income.Dad’s share of Kid’s net income.

Dad owns 100% of Kid.Dad owns 100% of Kid.Kid’s Net Income = $150,000Kid’s Net Income = $150,000

Consolidation ExampleEquity Method

© The McGraw-Hill Companies, Inc., 2004

Slide 3-13

McGraw-Hill/Irwin

Consolidation ExampleEquity Method

Kid's Net Income for 2005 150,000$ % of Kid owned by Dad 100%Equity Adjustment 150,000$

Kid's Net Income for 2005 150,000$ % of Kid owned by Dad 100%Equity Adjustment 150,000$

© The McGraw-Hill Companies, Inc., 2004

Slide 3-14

McGraw-Hill/Irwin

Consolidation ExampleEquity Method

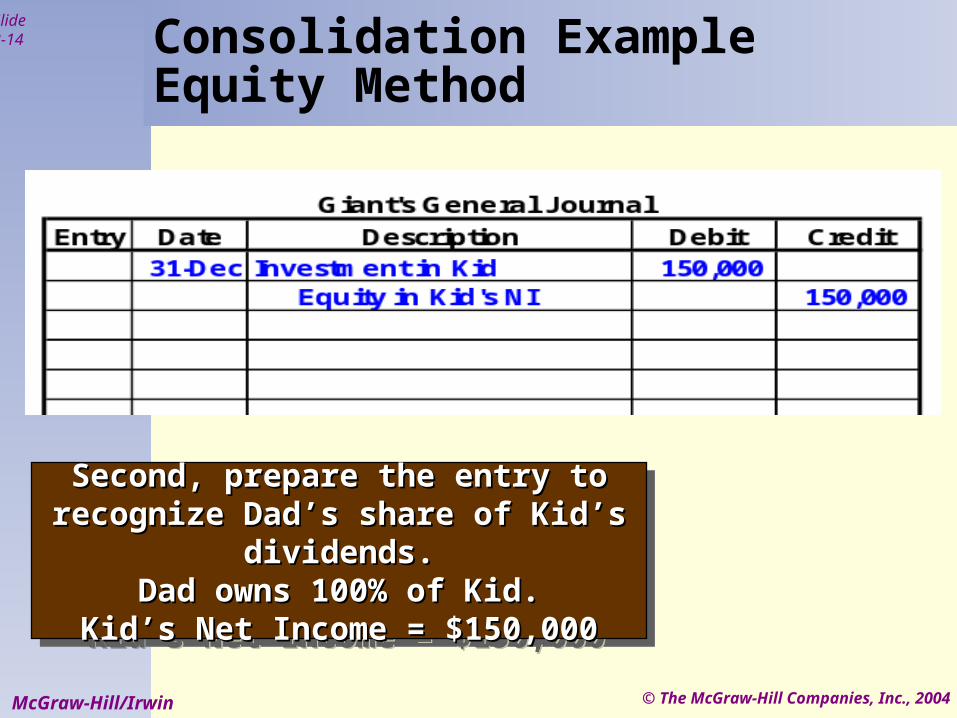

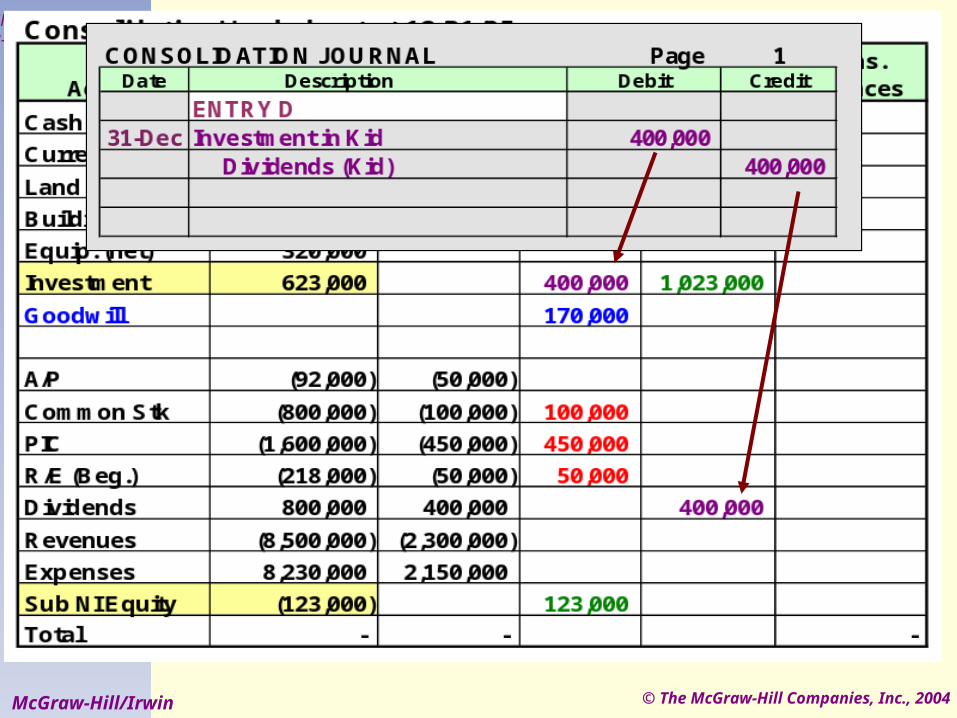

Second, prepare the entry to recognize Second, prepare the entry to recognize Dad’s share of Kid’s dividends.Dad’s share of Kid’s dividends.

Dad owns 100% of Kid.Dad owns 100% of Kid.Kid’s Net Income = $150,000Kid’s Net Income = $150,000

Second, prepare the entry to recognize Second, prepare the entry to recognize Dad’s share of Kid’s dividends.Dad’s share of Kid’s dividends.

Dad owns 100% of Kid.Dad owns 100% of Kid.Kid’s Net Income = $150,000Kid’s Net Income = $150,000

© The McGraw-Hill Companies, Inc., 2004

Slide 3-15

McGraw-Hill/Irwin

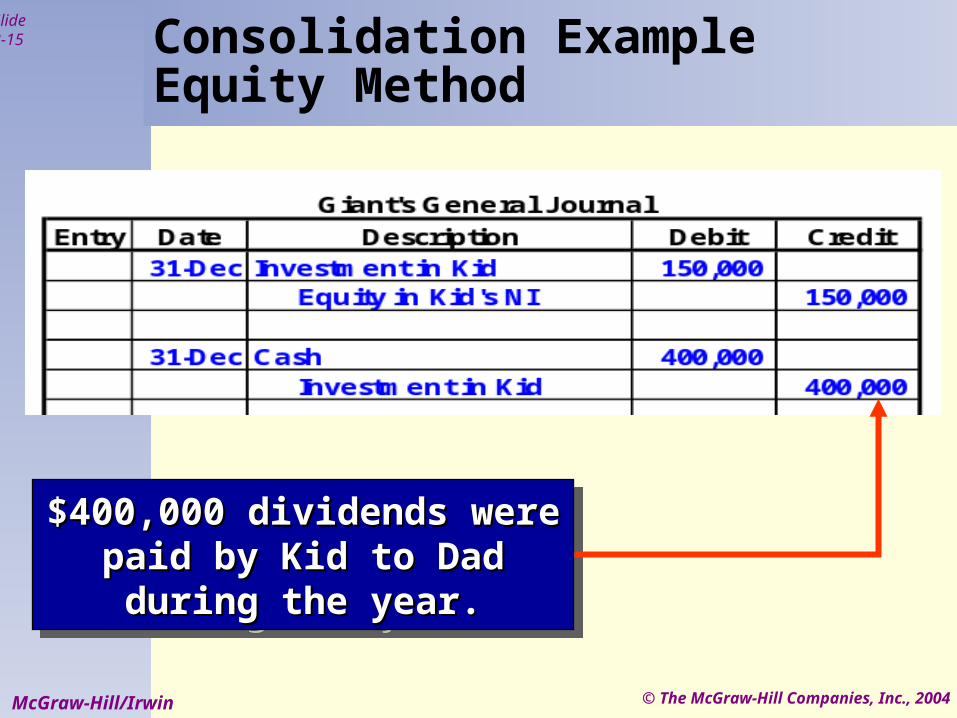

$400,000 dividends were paid $400,000 dividends were paid by Kid to Dad during the by Kid to Dad during the

year.year.

$400,000 dividends were paid $400,000 dividends were paid by Kid to Dad during the by Kid to Dad during the

year.year.

Consolidation ExampleEquity Method

© The McGraw-Hill Companies, Inc., 2004

Slide 3-16

McGraw-Hill/Irwin

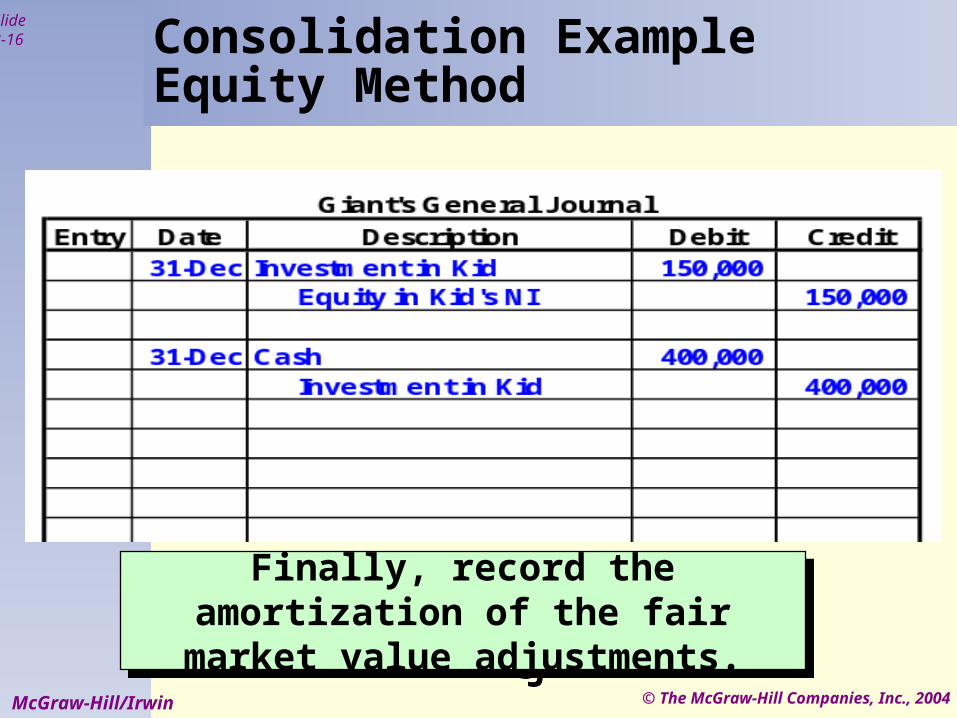

Finally, record the amortization of the fair market value adjustments.

Finally, record the amortization of the fair market value adjustments.

Consolidation ExampleEquity Method

© The McGraw-Hill Companies, Inc., 2004

Slide 3-17

McGraw-Hill/Irwin

The Amortization Expense from the earlier computation = $27,000

The Amortization Expense from the earlier computation = $27,000

Consolidation ExampleEquity Method

© The McGraw-Hill Companies, Inc., 2004

Slide 3-18

McGraw-Hill/Irwin

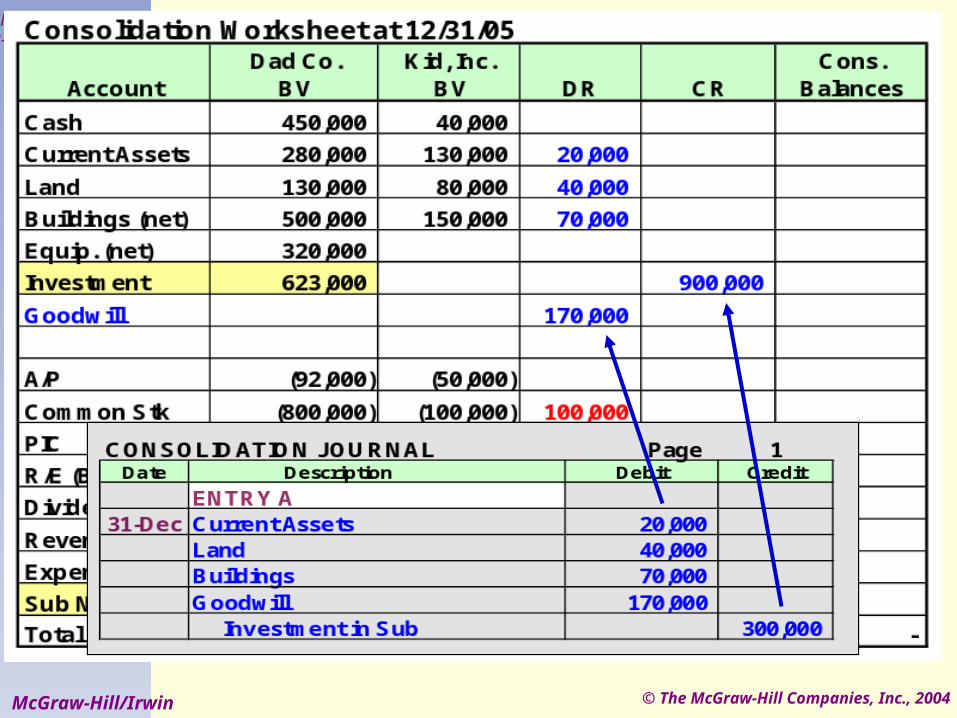

Subsequent Consolidation - Worksheet Entries

5 basic entries are posted to the worksheet. The Sub’s equity accounts are eliminated. The other intangible assets are recorded and

the Sub’s assets are adjusted to FMV. The Equity in Sub Income account is

eliminated. The Sub’s dividends are eliminated. Amortization Expense is recorded for the

FMV adjustments and other intangible assets associated with the consolidated entity.

5 basic entries are posted to the worksheet. The Sub’s equity accounts are eliminated. The other intangible assets are recorded and

the Sub’s assets are adjusted to FMV. The Equity in Sub Income account is

eliminated. The Sub’s dividends are eliminated. Amortization Expense is recorded for the

FMV adjustments and other intangible assets associated with the consolidated entity.

© The McGraw-Hill Companies, Inc., 2004

Slide 3-19

McGraw-Hill/Irwin

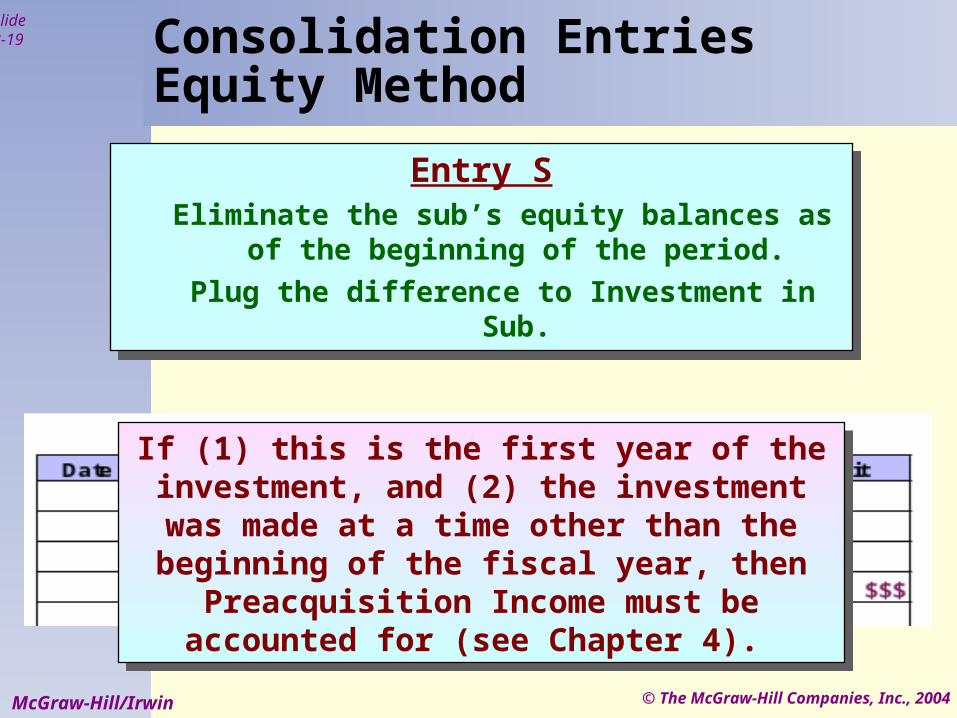

Consolidation EntriesEquity Method

Entry SEliminate the sub’s equity balances as of

the beginning of the period.

Plug the difference to Investment in Sub.

Entry SEliminate the sub’s equity balances as of

the beginning of the period.

Plug the difference to Investment in Sub.

If (1) this is the first year of the investment, and (2) the investment was made at a time other than the beginning of the fiscal year,

then Preacquisition Income must be accounted for (see Chapter 4).

If (1) this is the first year of the investment, and (2) the investment was made at a time other than the beginning of the fiscal year,

then Preacquisition Income must be accounted for (see Chapter 4).

© The McGraw-Hill Companies, Inc., 2004

Slide 3-20

McGraw-Hill/Irwin

Consolidation EntriesEquity Method

Entry AAdjust sub’s assets and liabilities to FMV.

Set up the Goodwill account and the other intangible assets. The difference is a reduction of the

Investment in Subsidiary account.

Entry AAdjust sub’s assets and liabilities to FMV.

Set up the Goodwill account and the other intangible assets. The difference is a reduction of the

Investment in Subsidiary account.

In the first year of the investment, the FMV adjustments for this entry will be identified during

the computation of Goodwill. In subsequent years, the FMV adjustments and the other

intangible assets identified must be reduced by any depreciation taken in prior periods.

In the first year of the investment, the FMV adjustments for this entry will be identified during

the computation of Goodwill. In subsequent years, the FMV adjustments and the other

intangible assets identified must be reduced by any depreciation taken in prior periods.

© The McGraw-Hill Companies, Inc., 2004

Slide 3-21

McGraw-Hill/Irwin

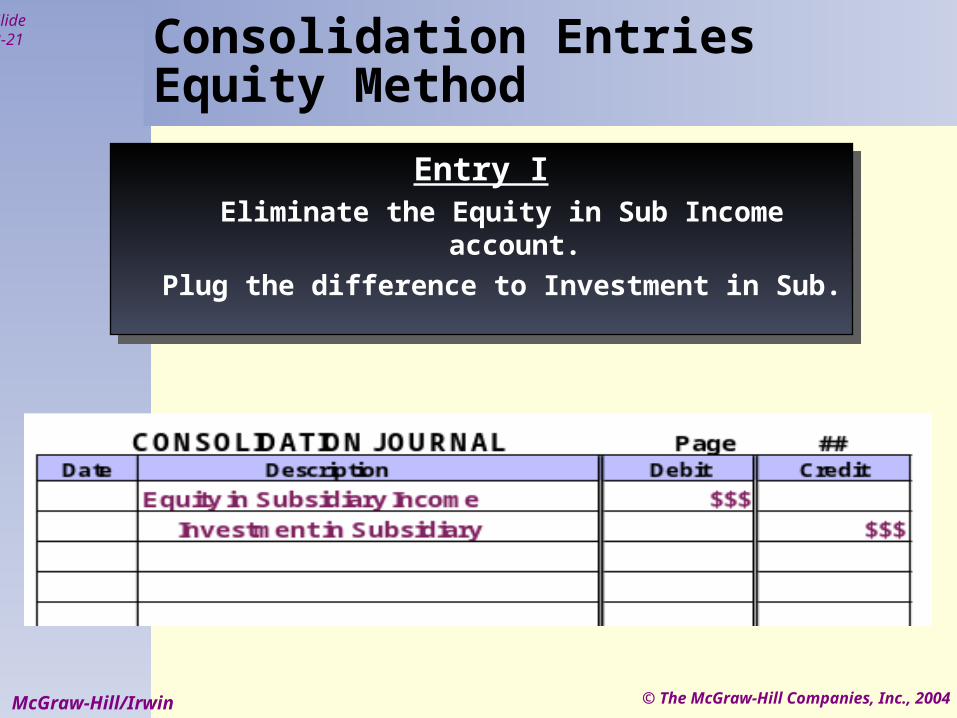

Consolidation EntriesEquity Method

Entry IEliminate the Equity in Sub Income account.

Plug the difference to Investment in Sub.

Entry IEliminate the Equity in Sub Income account.

Plug the difference to Investment in Sub.

© The McGraw-Hill Companies, Inc., 2004

Slide 3-22

McGraw-Hill/Irwin

Consolidation EntriesEquity Method

Entry DEliminate sub’s Dividends.

Plug the difference to Investment in Sub.

Entry DEliminate sub’s Dividends.

Plug the difference to Investment in Sub.

© The McGraw-Hill Companies, Inc., 2004

Slide 3-23

McGraw-Hill/Irwin

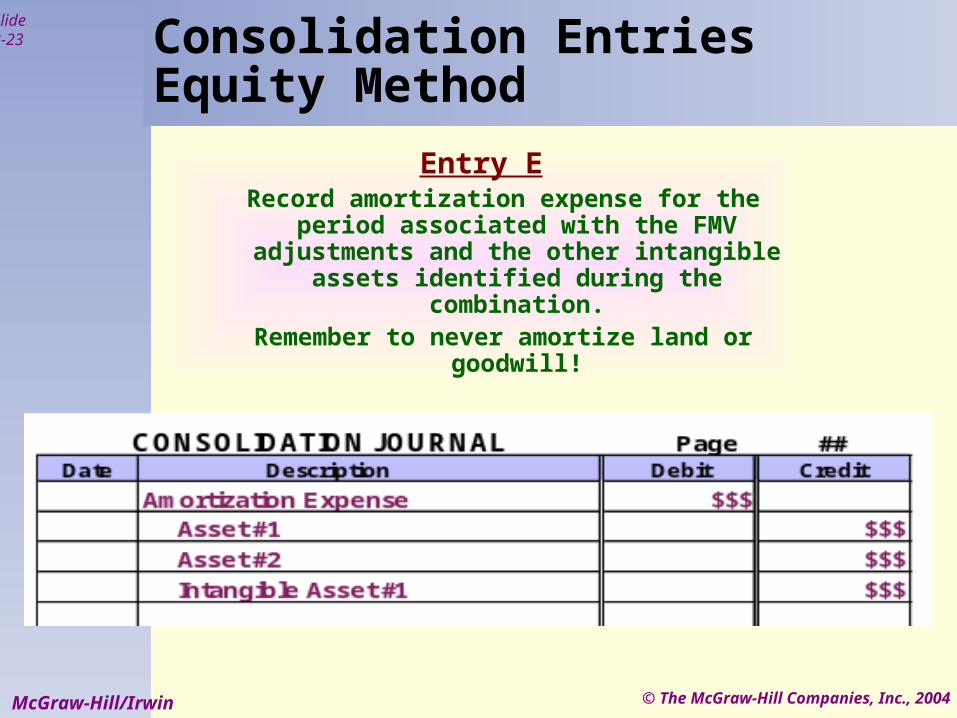

Consolidation EntriesEquity Method

Entry ERecord amortization expense for the period

associated with the FMV adjustments and the other intangible assets identified

during the combination.Remember to never amortize land or

goodwill!

© The McGraw-Hill Companies, Inc., 2004

Slide 3-24

McGraw-Hill/Irwin

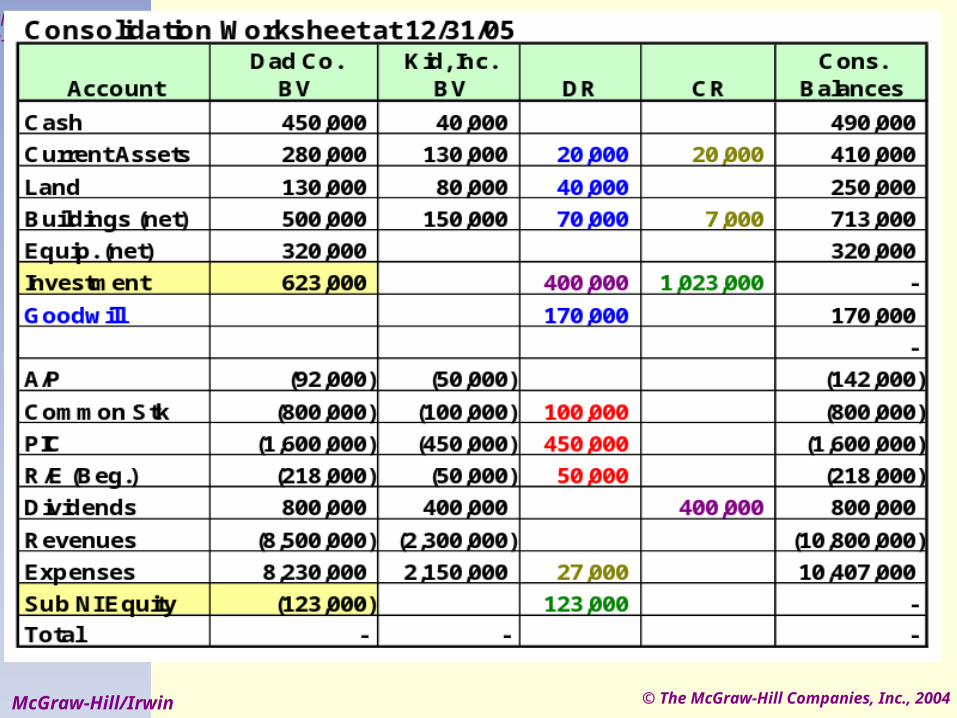

Consolidation at 12/31/05Equity Method Example

Using the 12/31/05 adjusted balances,

prepare the consolidation at

12/31/05.

© The McGraw-Hill Companies, Inc., 2004

Slide 3-25

McGraw-Hill/Irwin

Note Dad’s updated

numbers.Now, post the consolidation entries to the worksheet.

Note Dad’s updated

numbers.Now, post the consolidation entries to the worksheet.

© The McGraw-Hill Companies, Inc., 2004

Slide 3-26

McGraw-Hill/Irwin

© The McGraw-Hill Companies, Inc., 2004

Slide 3-27

McGraw-Hill/Irwin

© The McGraw-Hill Companies, Inc., 2004

Slide 3-28

McGraw-Hill/Irwin

© The McGraw-Hill Companies, Inc., 2004

Slide 3-29

McGraw-Hill/Irwin

© The McGraw-Hill Companies, Inc., 2004

Slide 3-30

McGraw-Hill/Irwin

© The McGraw-Hill Companies, Inc., 2004

Slide 3-31

McGraw-Hill/Irwin

© The McGraw-Hill Companies, Inc., 2004

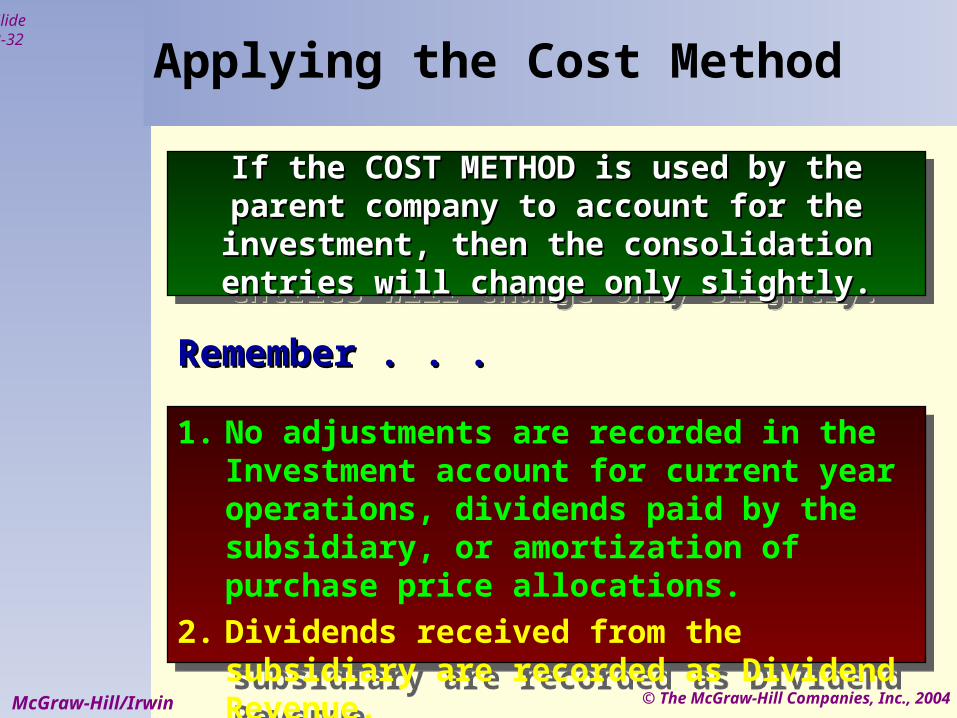

Slide 3-32

McGraw-Hill/Irwin

Applying the Cost Method

If the COST METHOD is used by the parent If the COST METHOD is used by the parent company to account for the investment, then the company to account for the investment, then the consolidation entries will change only slightly.consolidation entries will change only slightly.

If the COST METHOD is used by the parent If the COST METHOD is used by the parent company to account for the investment, then the company to account for the investment, then the consolidation entries will change only slightly.consolidation entries will change only slightly.

Remember . . . Remember . . .

1. No adjustments are recorded in the Investment account for current year operations, dividends paid by the subsidiary, or amortization of purchase price allocations.

2. Dividends received from the subsidiary are recorded as Dividend Revenue.

1. No adjustments are recorded in the Investment account for current year operations, dividends paid by the subsidiary, or amortization of purchase price allocations.

2. Dividends received from the subsidiary are recorded as Dividend Revenue.

© The McGraw-Hill Companies, Inc., 2004

Slide 3-33

McGraw-Hill/Irwin

Consolidation EntriesCost Method

Entry SEliminate the sub’s equity balances as of the

beginning of the period.

Plug the difference to Investment in Sub.

This entry is the same under both the Equity Method and the Cost Method.

Entry SEliminate the sub’s equity balances as of the

beginning of the period.

Plug the difference to Investment in Sub.

This entry is the same under both the Equity Method and the Cost Method.

© The McGraw-Hill Companies, Inc., 2004

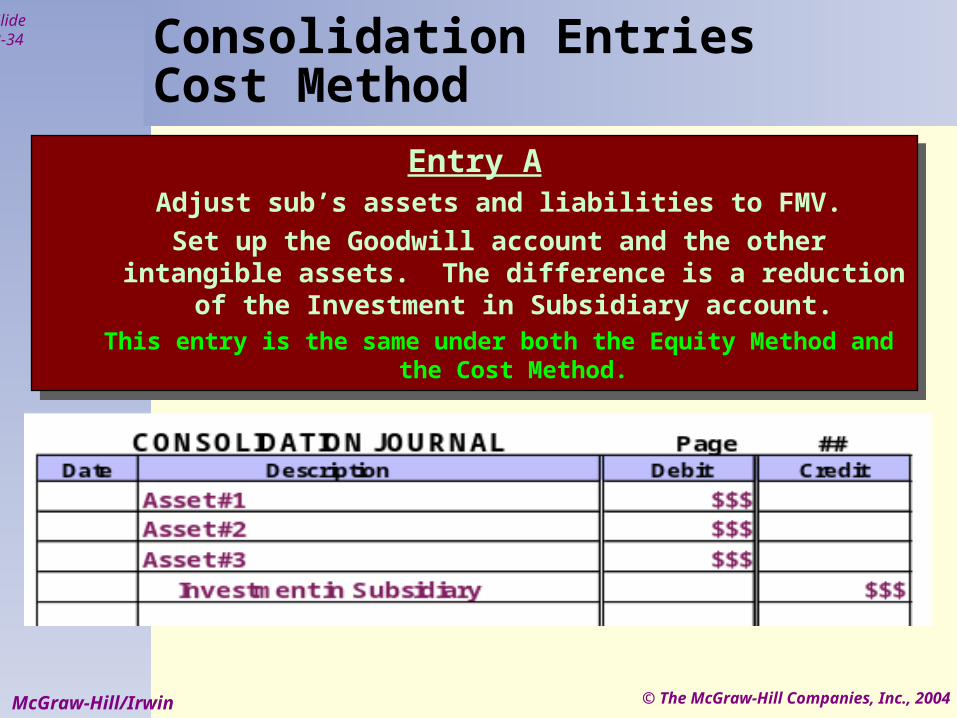

Slide 3-34

McGraw-Hill/Irwin

Consolidation EntriesCost Method

Entry AAdjust sub’s assets and liabilities to FMV.

Set up the Goodwill account and the other intangible assets. The difference is a reduction of the Investment in Subsidiary

account.This entry is the same under both the Equity Method and the Cost

Method.

Entry AAdjust sub’s assets and liabilities to FMV.

Set up the Goodwill account and the other intangible assets. The difference is a reduction of the Investment in Subsidiary

account.This entry is the same under both the Equity Method and the Cost

Method.

© The McGraw-Hill Companies, Inc., 2004

Slide 3-35

McGraw-Hill/Irwin

Consolidation EntriesCost Method

Entry IThis entry is different under the Cost Method.

Eliminate the Parent’s Dividend Income account.

Also, eliminate the Sub’s Dividends Paid account.

Entry IThis entry is different under the Cost Method.

Eliminate the Parent’s Dividend Income account.

Also, eliminate the Sub’s Dividends Paid account.

© The McGraw-Hill Companies, Inc., 2004

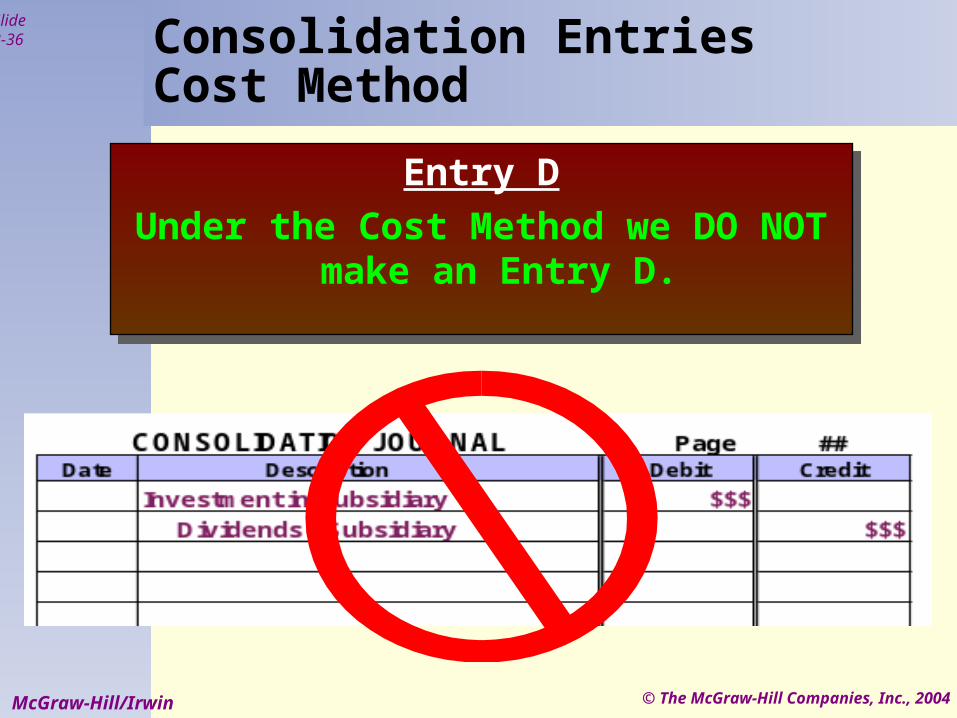

Slide 3-36

McGraw-Hill/Irwin

Consolidation EntriesCost Method

Entry D

Under the Cost Method we DO NOT make an Entry D.

Entry D

Under the Cost Method we DO NOT make an Entry D.

© The McGraw-Hill Companies, Inc., 2004

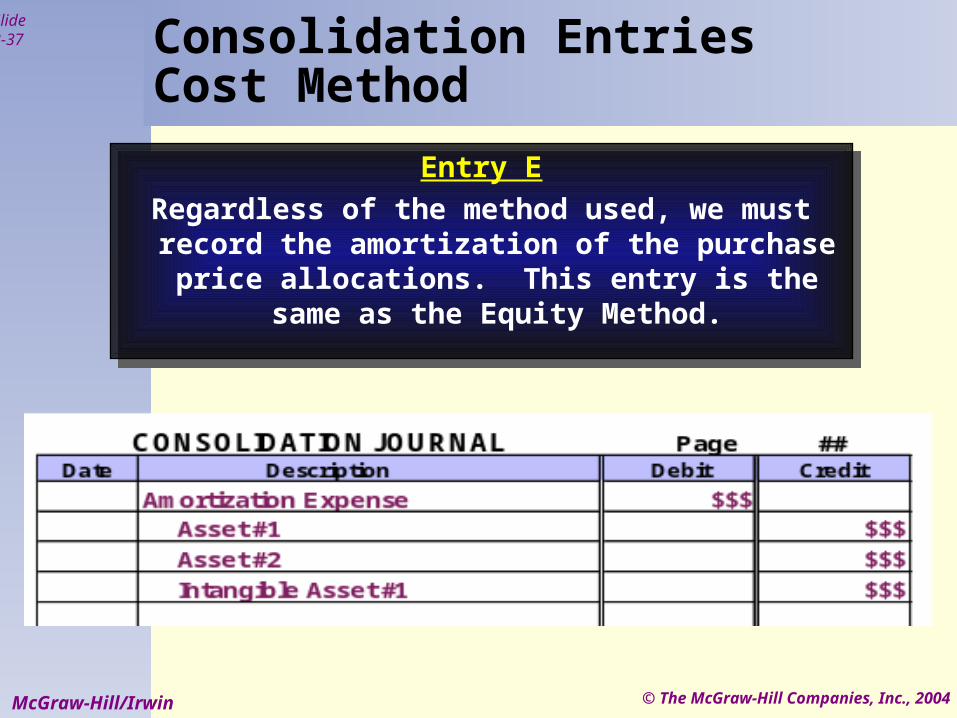

Slide 3-37

McGraw-Hill/Irwin

Consolidation EntriesCost Method

Entry E

Regardless of the method used, we must record the amortization of the purchase price

allocations. This entry is the same as the Equity Method.

Entry E

Regardless of the method used, we must record the amortization of the purchase price

allocations. This entry is the same as the Equity Method.

© The McGraw-Hill Companies, Inc., 2004

Slide 3-38

McGraw-Hill/Irwin

Other Consolidation Entries

In addition to the Entries S, A, I, D, & E, you must also eliminate intercompany payables or receivables.

So far, we have assumed that the parent acquired 100% of the subsidiary in the combination. If control acquired is < than 100%, an additional adjustment must be made (see Chapter 4).

In addition to the Entries S, A, I, D, & E, you must also eliminate intercompany payables or receivables.

So far, we have assumed that the parent acquired 100% of the subsidiary in the combination. If control acquired is < than 100%, an additional adjustment must be made (see Chapter 4).

© The McGraw-Hill Companies, Inc., 2004

Slide 3-39

McGraw-Hill/Irwin

Goodwill Impairment

Goodwill is not amortized. It is assigned an

“indefinite” useful life. Generally, goodwill

will be carried at it’s acquisition cost.

At some future point in time, the goodwill may become permanently impaired.

Goodwill is not amortized. It is assigned an

“indefinite” useful life. Generally, goodwill

will be carried at it’s acquisition cost.

At some future point in time, the goodwill may become permanently impaired.

SFAS No. 142 calls

for an annual test

of impairment

for Goodwill.

© The McGraw-Hill Companies, Inc., 2004

Slide 3-40

McGraw-Hill/Irwin

Goodwill Impairment ExamplesExh.3-15

2002 Goodwill Impairment Write-downs

Company 2002 Write-DownAOL Time Warner 54,000,000,000$ Boeing 1,800,000,000$ Blockbuster 1,800,000,000$ SBC Communications 1,800,000,000$ General Electric 1,000,000,000$ Coca-Cola 926,000,000$ AT&T 856,000,000$ Safeway 700,000,000$ Verizon Communications 500,000,000$

© The McGraw-Hill Companies, Inc., 2004

Slide 3-41

McGraw-Hill/Irwin

Goodwill Impairment Test

Step 1 Compare fair value of

REPORTING UNIT to carrying value of the REPORTING UNIT

Step 2 Compare fair value of

GOODWILL to carrying value of GOODWILL

Step 1 Compare fair value of

REPORTING UNIT to carrying value of the REPORTING UNIT

Step 2 Compare fair value of

GOODWILL to carrying value of GOODWILL

© The McGraw-Hill Companies, Inc., 2004

Slide 3-42

McGraw-Hill/Irwin

Goodwill Impairment Test - Step 1Is the Fair Value of a Reporting Unit Less Than Carrying Value?

Compare the Reporting Unit’s Fair Value to its

Carrying Value. If Fair Value of the

Reporting Unit is < Carrying Value, GO TO

STEP 2. Recompute Fair Value

if the previous Fair Value can not be used?

Compare the Reporting Unit’s Fair Value to its

Carrying Value. If Fair Value of the

Reporting Unit is < Carrying Value, GO TO

STEP 2. Recompute Fair Value

if the previous Fair Value can not be used?

© The McGraw-Hill Companies, Inc., 2004

Slide 3-43

McGraw-Hill/Irwin

Goodwill Impairment Test - Step 1Is the Fair Value of a Reporting Unit Less Than Carrying Value?

Use the most recent Fair Value if: The net assets of the reporting unit have not

changed significantly since the most recent fair value determination.

AND The most recent fair value determination >

the carrying amount of the reporting unit by a substantial margin.

AND It is remote that computing a new fair value

would result in an amount < the current carrying amount of the reporting unit.

© The McGraw-Hill Companies, Inc., 2004

Slide 3-44

McGraw-Hill/Irwin

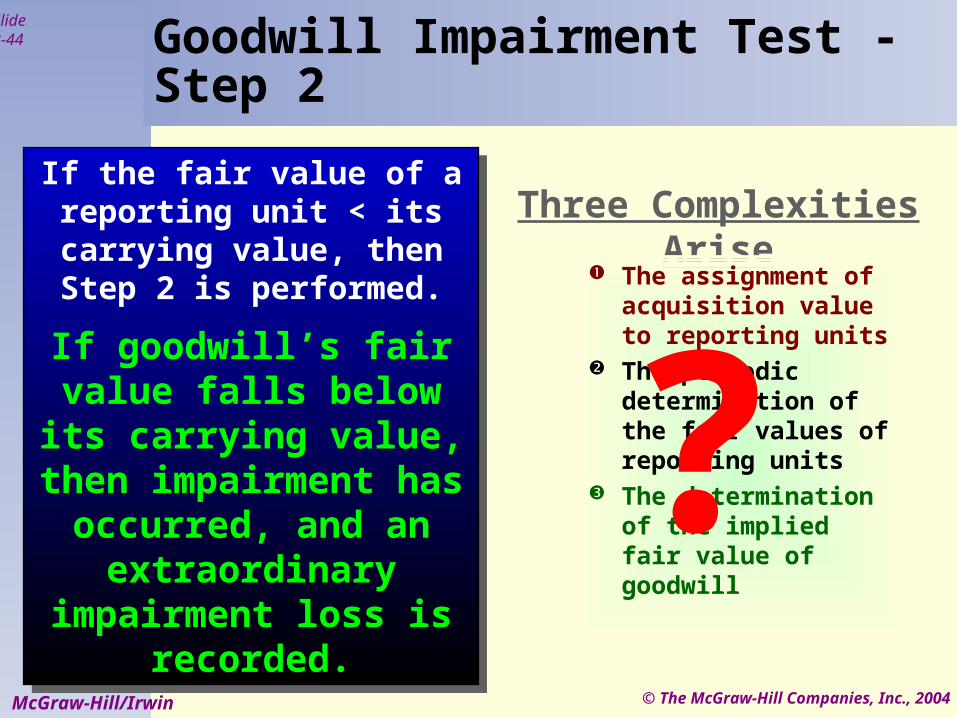

Goodwill Impairment Test - Step 2

If the fair value of a reporting unit < its carrying

value, then Step 2 is performed.

If goodwill’s fair value falls below its carrying value, then impairment has occurred, and an

extraordinary impairment loss is

recorded.

If the fair value of a reporting unit < its carrying

value, then Step 2 is performed.

If goodwill’s fair value falls below its carrying value, then impairment has occurred, and an

extraordinary impairment loss is

recorded.

Three Complexities Arise

The assignment of acquisition value to reporting units

The periodic determination of the fair values of reporting units

The determination of the implied fair value of goodwill

?

© The McGraw-Hill Companies, Inc., 2004

Slide 3-45

McGraw-Hill/Irwin

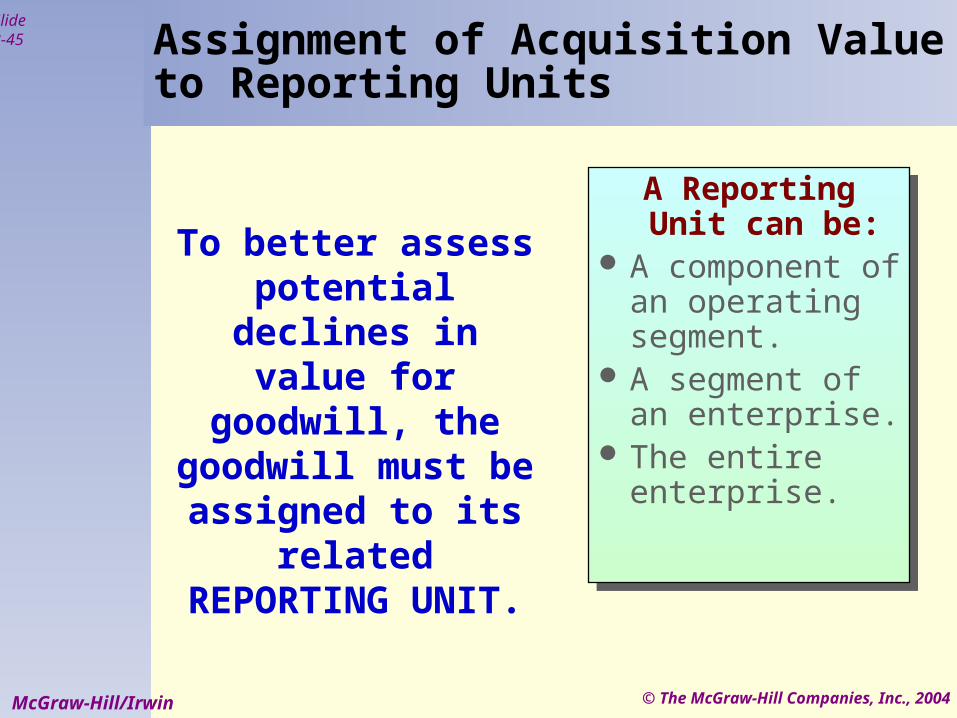

A Reporting Unit can be:

A component of an operating segment.

A segment of an enterprise.

The entire enterprise.

A Reporting Unit can be:

A component of an operating segment.

A segment of an enterprise.

The entire enterprise.

Assignment of Acquisition Value to Reporting Units

To better assess potential declines in value for goodwill,

the goodwill must be assigned to its

related REPORTING UNIT.

© The McGraw-Hill Companies, Inc., 2004

Slide 3-46

McGraw-Hill/Irwin

Basis for determining fair value:

Market price, if the reporting unit is publicly traded.

Market price of comparable businesses.

Business valuation techniques using PV.

Basis for determining fair value:

Market price, if the reporting unit is publicly traded.

Market price of comparable businesses.

Business valuation techniques using PV.

Periodic Determination of the Fair Value of a Reporting Unit

© The McGraw-Hill Companies, Inc., 2004

Slide 3-47

McGraw-Hill/Irwin

Use the fair value of the reporting unit as the “purchase price”.

Allocate the “purchase price” to all identifiable assets and liabilities of the reporting unit.

Compare the resulting “implied goodwill” to the goodwill on the books.

If “implied goodwill” < recorded goodwill, impairment has occurred.

Use the fair value of the reporting unit as the “purchase price”.

Allocate the “purchase price” to all identifiable assets and liabilities of the reporting unit.

Compare the resulting “implied goodwill” to the goodwill on the books.

If “implied goodwill” < recorded goodwill, impairment has occurred.

Determination of the Implied Fair Value of Goodwill

The “impliedimplied” fair value of Goodwill is

calculated in a similar manner

as the determination of

goodwill in a business

combination.

© The McGraw-Hill Companies, Inc., 2004

Slide 3-48

McGraw-Hill/Irwin

Closing Observations Related to the Testing of Goodwill for Impairment

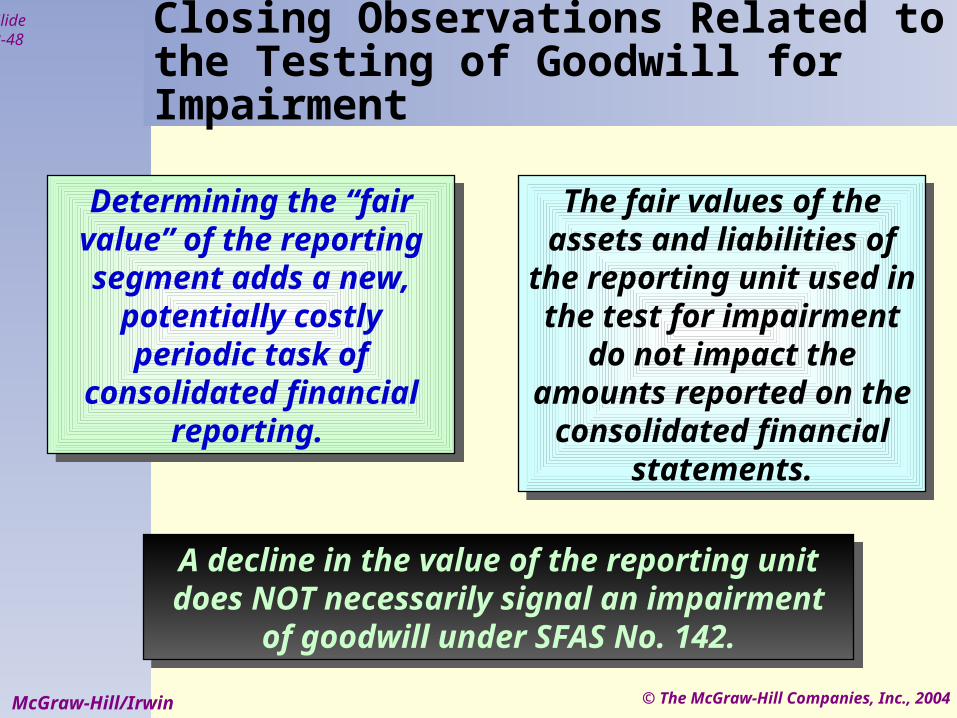

Determining the “fair value” of the reporting segment adds a new,

potentially costly periodic task of

consolidated financial reporting.

Determining the “fair value” of the reporting segment adds a new,

potentially costly periodic task of

consolidated financial reporting.

The fair values of the assets and liabilities of

the reporting unit used in the test for impairment

do not impact the amounts reported on the

consolidated financial statements.

The fair values of the assets and liabilities of

the reporting unit used in the test for impairment

do not impact the amounts reported on the

consolidated financial statements.

A decline in the value of the reporting unit does NOT necessarily signal an impairment

of goodwill under SFAS No. 142.

A decline in the value of the reporting unit does NOT necessarily signal an impairment

of goodwill under SFAS No. 142.

© The McGraw-Hill Companies, Inc., 2004

Slide 3-49

McGraw-Hill/Irwin

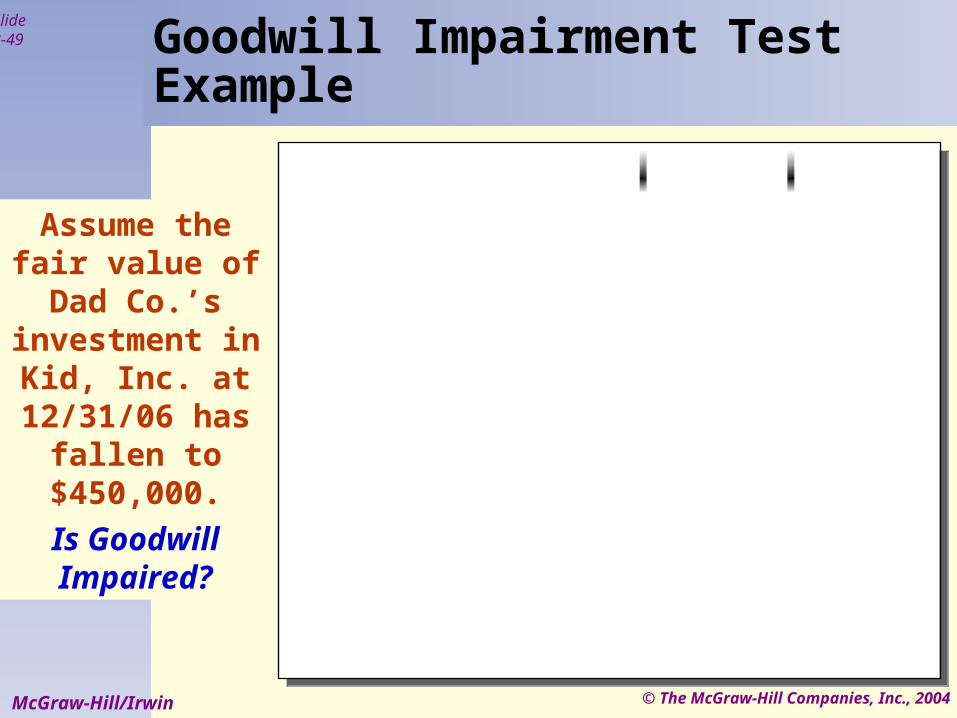

Goodwill Impairment TestExample

Assume the fair value of Dad

Co.’s investment in

Kid, Inc. at 12/31/06 has

fallen to $450,000.

Is Goodwill Impaired?

© The McGraw-Hill Companies, Inc., 2004

Slide 3-50

McGraw-Hill/Irwin

Goodwill Impairment TestExample

STEP 1STEP 1

Fair value of the investment < the carrying

amount of the investment, so go to Step 2.

© The McGraw-Hill Companies, Inc., 2004

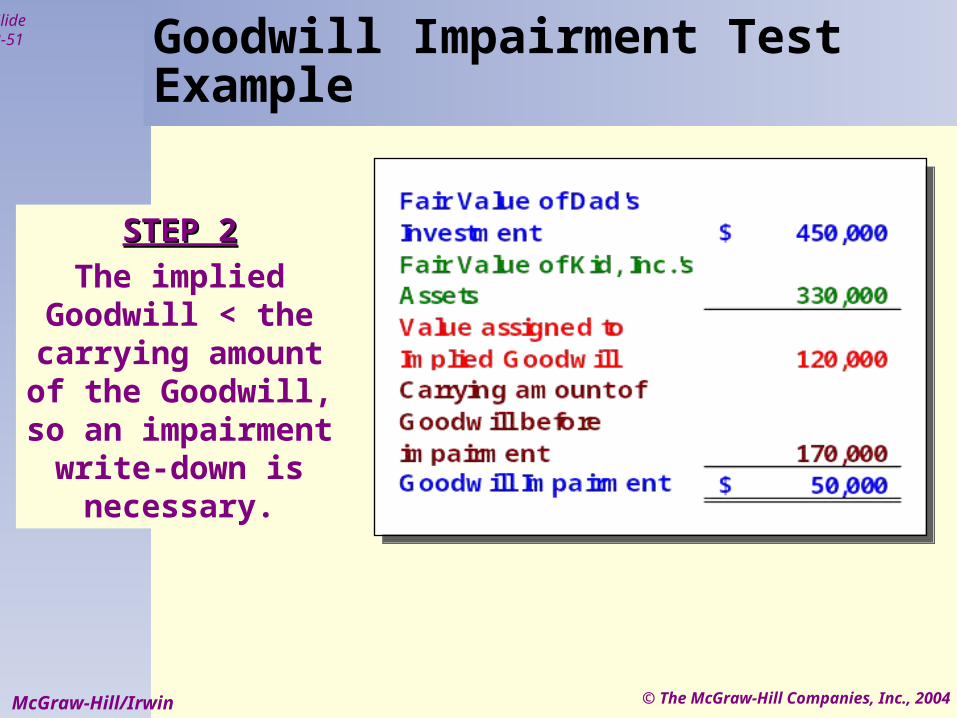

Slide 3-51

McGraw-Hill/Irwin

Goodwill Impairment TestExample

STEP 2STEP 2

The implied Goodwill < the

carrying amount of the Goodwill, so an impairment write-

down is necessary.

© The McGraw-Hill Companies, Inc., 2004

Slide 3-52

McGraw-Hill/Irwin

Goodwill Impairment TestExample

Goodwill Impairment EntryThe Goodwill needs to be written down by $50,000. The entry should be recorded as an extraordinary item on the consolidated

financial statements, if it is material.

Goodwill Impairment EntryThe Goodwill needs to be written down by $50,000. The entry should be recorded as an extraordinary item on the consolidated

financial statements, if it is material.

© The McGraw-Hill Companies, Inc., 2004

Slide 3-53

McGraw-Hill/Irwin

This stuff This stuff is a is a

breeze, breeze, ain’t it?ain’t it?

End of Chapter 3