benefits · help and support this booklet is intended to provide a summary of benefits offered to...

TRANSCRIPT

2018BENEFITS

................. Welcome

................. What to Do and What to Expect

................. What's New in 2018?

................. Benefits in Review

................. Eligibility

................. Enrollment – How

................. Help and Support

This booklet is intended to provide a summary of benefits offered to employees. In determining actual benefit coverage and eligibility, the official text of company plan documents and summary plan descriptions is the governing source.

03

04

05

06

22

25

26

22018 Benefits

What’sINSIDE

Welcome

We are committed to offering choices that provide quality benefits for you and your dependents. We are also responsible for maintaining the competitiveness of our business. A successful business is the key to creating opportunity and security for our employees.

Both the company and our employees have a critical role in managing health care costs. That involves shared responsibility, shared risk-taking and you taking an active role in understanding, utilizing and purchasing health care services.

Your benefit choices are important decisions and affect how you receive your benefits and what you pay for them. Take the time to make sure you fully understand the plans available.

Welcome What to Do What's New Benefits Eligibility Enrollment Help

Welcome 3

What to doWithin 30 Calendar Days• Enroll in your benefits within 30 days of hire date. Your date of hire counts as day 1.

1. Study your options—read through this guide or visit taylorcorp.com/enrollment

2. Know the difference—make sure you understand how the plans work and how you can manage your health

care expenses all year long.

3. Decide what plans you will elect.

4. Decide who to cover—yourself, your legal spouse, your eligible children or your entire family

The company reserves the right to audit dependents at any point in time.

Within 60 Calendar Days• Complete your wellness screening* AFTER you enroll in benefits. If you choose to participate

in the wellness screenings, this must be complete within 60 days of your hire date.

What to expectMedical/Dental/VisionIf you enroll in Medical, Dental, and/or Vision, you will receive ID cards as follows:

• Medical ID card from BCBS of MN

• Prescription card from CVS/Caremark

• A Dental ID card from Delta Dental

• You will NOT get an ID card for vision – you will use your employee ID as your Vision ID

Pre-Tax AccountsIf you enroll in one of the Pre-tax accounts, you can expect to receive the following:

• If you enroll in the HSA, you will receive a Welcome Kit and Debit Card from HSA Bank.

• If you enroll in the Health Care Flexible Spending Account, you will receive a Payment Card from Optum.

• If you participate in the commuter expense reimbursement account, you will receive a Payment Card from Optum.

Retirement• You will receive a packet of materials on the 401(k) Plan from Merrill Lynch

*Wellness screenings are optional and give you and your spouse the opportunity to earn wellness dollars if you enroll in one of the company's health plans. Learn more about your wellness options on page 10.

What to Do and What to Expect

Welcome What to Do What's New Benefits Eligibility Enrollment Help

What to Do and What to Expect 4

What's New in 2018?MedicalWe will continue to offer you and your family choice in your medical plans. In 2018, you will be able to choose from three

new medical plans options. Two of these plans will offer copays for office visits, urgent care and telehealth visits.

WellnessYour health is important to us and we want you to have low costs and great access to providers. We have expanded our

wellness benefit offering for 2018 and wellness dollars will now apply to all of our medical plans. If you can’t meet the

initial requirements, we will provide you with a reasonable alternative to earn wellness dollars.

Commuter Expense Reimbursement Account (CERA)All benefit eligible employees can now elect to participate in a Commuter Expense Reimbursement Account (CERA)

through Optum. A CERA allows you to pay for qualified parking, mass transit and vanpooling expenses using money you

have set aside pre-tax.

Long Term Disability Benefit PlanLong-Term Disability (LTD) Benefit Plan Effective January 2018, the maximum benefit period (how long benefits will be

paid) for the current employer provided long-term disability (LTD) benefit will change to 5-years; this plan will be called

the Core LTD plan. A buy-up LTD plan will be made available to all eligible employees that extends this period to a date

based on the employee’s age when they become disabled and on a reducing benefit duration table.

CarrierTo enhance our benefits and manage costs we will be changing our life and disability carrier to Voya Financial, as well as

our Flexible Spending Account, COBRA and Commuter Expense Reimbursement Account administration to Optum.

Welcome What to Do What's New Benefits Eligibility Enrollment Help

What's New in 2018? 5

Benefits in Review MedicalMedical coverage is one of your most important and valuable benefits. You have the choice of three new medical plans:

All three plans help you stay well by providing 100 percent coverage for in-network preventive care and help you

when you are not well by covering a portion of your costs.

All three plans are administered by Blue Cross Blue Shield of MN and include prescription coverage through CVS/Caremark.

PPO PLUS PPO HSA

Welcome What to Do What's New Benefits Eligibility Enrollment Help

Benefits in Review 6

Employee Employee+1 Family Employee Employee+1 Family Employee Employee+1 Family

Employee-Bi-Weekly* Contribution $74.37 $171.06 $223.12 $41.05 $94.43 $123.16 $34.92 $80.33 $104.77

Employer-Bi-Weekly* Contribution

$157.72 $362.75 $473.15 $175.02 $402.54 $525.06 $148.89 $342.44 $446.67

Wellness Eligible Yes Yes Yes

Annual Deductible• Individual• Family

In-Network$1,500$3,000

In-Network$2,500$5,000

In-Network$6,600$13,200

Annual Out of Pocket Maximum• Individual• Family

In-Network $6,600$13,200

In-Network$6,600$13,200

In-Network $6,600$13,200

Coinsurance (what the plan pays after deductible) Plan pays 80% after deductible Plan pays 80% after deductible Plan pays 100% after deductible

Physician Office Visits• Primary Care Physician Visit• Specialist Visit• Retail Clinic Visit• Doctor On Demand Medical• Doctor On Demand Psychology/Psychiatry• X-ray/Lab (what plan pays after deductible)• Routine Preventive Care• Well Child Care

You pay $25 copayYou pay $35 copay You pay $20 copay

$0 copay; 100% You pay $25 copay

80% after deductible100%100%

You pay $40 copayYou pay $60 copayYou pay $40 copay

$0 copay; 100%You pay $40 copay

80% after deductible100%100%

Plan pays 100% after deductible

Plan pays 100% after deductible

Plan pays 100% after deductible

Plan pays 100% after deductible

Plan pays 100% after deductible

Plan pays 100% after deductible

100%100%

Prescription Drugs

Retail Pharmacy

• Generic Drugs

• Preferred Brand Name

• Non-Preferred Brand Name

• Specialty

You pay:

$10 copay

Greater of $40 copay or 20% to a max of $80

Greater of $60 copay or 50% to a max of $120

Greater of $75 copay or 20% to a max of $150

You pay:

$10 copay

Greater of $40 copay or 20% to a max of $80

Greater of $60 copay or 50% to a max of $120

Greater of $75 copay or 20% to a max of $150

Plan pays 100% after deductible

Plan pays 100% after deductible

Plan pays 100% after deductible

Plan pays 100% after deductible

PPO Plus

PPO Plus

PPO

PPO

HSA

HSAMedical Premiums

The medical plan comparison below gives a side-by-side comparison of covered In-Network services and plan features.

*To calculate a weekly amount, divide by 2.

Welcome What to Do What's New Benefits Eligibility Enrollment Help

Benefits in Review 7

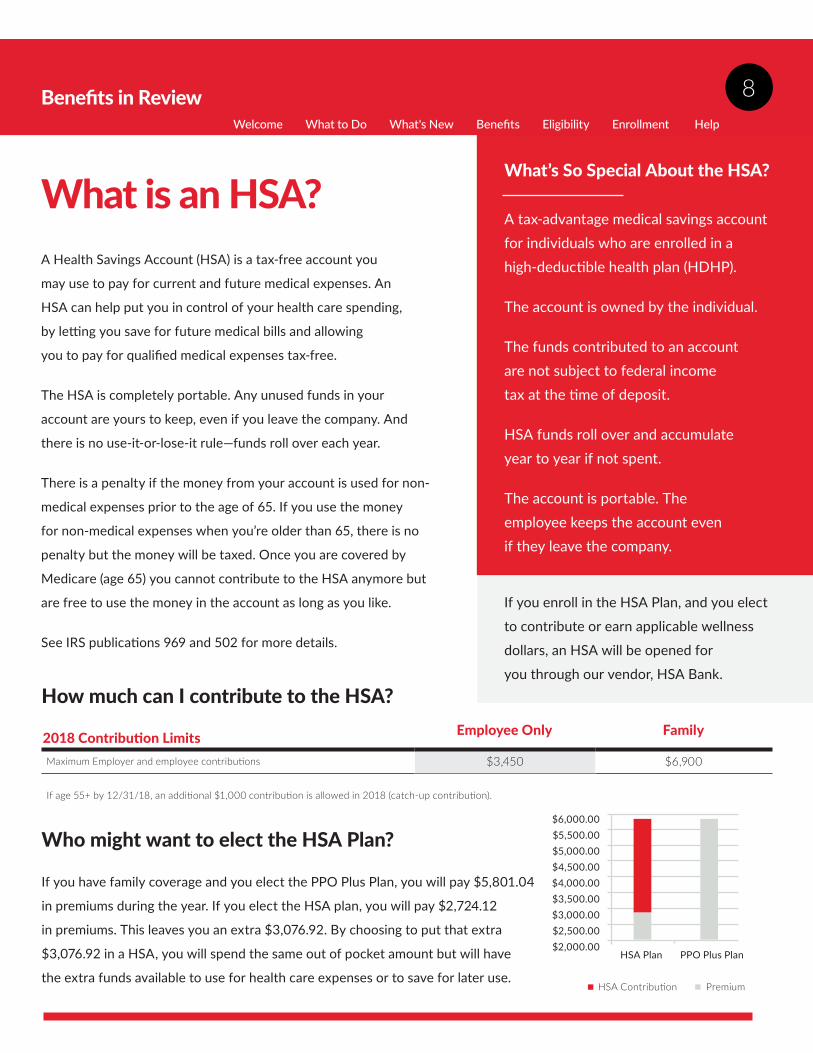

A Health Savings Account (HSA) is a tax-free account you

may use to pay for current and future medical expenses. An

HSA can help put you in control of your health care spending,

by letting you save for future medical bills and allowing

you to pay for qualified medical expenses tax-free.

The HSA is completely portable. Any unused funds in your

account are yours to keep, even if you leave the company. And

there is no use-it-or-lose-it rule—funds roll over each year.

There is a penalty if the money from your account is used for non-

medical expenses prior to the age of 65. If you use the money

for non-medical expenses when you’re older than 65, there is no

penalty but the money will be taxed. Once you are covered by

Medicare (age 65) you cannot contribute to the HSA anymore but

are free to use the money in the account as long as you like.

See IRS publications 969 and 502 for more details.

If you enroll in the HSA Plan, and you elect

to contribute or earn applicable wellness

dollars, an HSA will be opened for

you through our vendor, HSA Bank.

A tax-advantage medical savings account for individuals who are enrolled in a high-deductible health plan (HDHP).

The account is owned by the individual.

The funds contributed to an account are not subject to federal income tax at the time of deposit.

HSA funds roll over and accumulate year to year if not spent.

The account is portable. The employee keeps the account even if they leave the company.

What’s So Special About the HSA?

What is an HSA?

How much can I contribute to the HSA?

Who might want to elect the HSA Plan?

If you have family coverage and you elect the PPO Plus Plan, you will pay $5,801.04

in premiums during the year. If you elect the HSA plan, you will pay $2,724.12

in premiums. This leaves you an extra $3,076.92. By choosing to put that extra

$3,076.92 in a HSA, you will spend the same out of pocket amount but will have

the extra funds available to use for health care expenses or to save for later use.

Maximum Employer and employee contributions $3,450 $6,900

2018 Contribution Limits Employee Only Family

If age 55+ by 12/31/18, an additional $1,000 contribution is allowed in 2018 (catch-up contribution).

HSA Contribution Premium

$6,000.00$5,500.00$5,000.00$4,500.00$4,000.00$3,500.00$3,000.00$2,500.00$2,000.00

HSA Plan PPO Plus Plan

Welcome What to Do What's New Benefits Eligibility Enrollment Help

8Benefits in Review

Coverage for prescription drugs is included in all three health plans through CVS/Caremark. CVS/Caremark has over 64,000

pharmacies. These include retail pharmacies such as CVS, Kroger, Meijer, Walmart, and Walgreens as well as on line and mail

order options. To locate an in-network pharmacy, go to caremark.com or call CVS/Caremark. at (800) 405-6432.

What you pay for your prescriptions will depend on which medical plan you choose and what type of prescriptions you need.

The plan classifies drugs by four levels; generic, preferred brand, non-preferred brand and specialty. Each level of drug is a

different cost. Generic medications are the lowest cost options. Preferred brand, non-preferred brand and specialty are higher

priced medications, but your doctor may be able to prescribe a similar drug from another level with a lower cost.

Participants in the PPO Plus and PPO Plans will pay a copayment for generic drugs and a coinsurance payment for drugs from

the other three levels with minimum and maximum amounts depending on the level of drug.

Participants in the HSA plan pay the full discounted price of the drug until the deductible is met. After the deductible is met,

the plan works a little differently; in the HSA plan, the plan pays all expenses once the deductible/out-of-pocket maximum

are met.

Prescription Benefits

ID cards for prescription drugs

CVS will send a welcome packet and an ID card specific to the

prescription coverage. Upon receipt of your prescription ID card,

you will be able to go to caremark.com and register for online

access.

90-day Rx Program

If you take certain medications on a regular basis you can save

time and money with the 90-day Rx Program. You will have

lower copayments when you take part in the program. You pay

2.5 times the monthly copayment or coinsurance for a 3-month

drug supply instead of a full 3-month copayment or coinsurance-

this is like receiving two months of free medications each year.

You can take advantage of the 90-day program at participating

retail pharmacies or use mail order.

What is a Formulary?

A formulary is a list of prescription drugs, both generic and

brand name, that are preferred by the health plan. The plan will

pay for medications that are on this “preferred” list at a higher

level of reimbursement than those not on the list.

The purpose of the formulary is to direct you to the least costly

medications that are effective for treating your health condition.

You will pay more if you and your doctor choose a medication

that is not covered on the formulary.

CVS will review whether or not a doctor is using the formulary.

If not, CVS may communicate with the doctor and encourage

them to use medications on the formulary. You can find the

formulary listing by using the resources available on

caremark.com.

Welcome What to Do What's New Benefits Eligibility Enrollment Help

Benefits in Review 9

We all know how important it is to proactively manage you and your family’s health. Our company is committed to helping you achieve optimal health—encouraging you to be active, live a healthy lifestyle and make good health decisions. Our plan options offer you the flexibility to select the plan that best fits your needs, with the option to be rewarded for healthy behaviors through wellness dollars.

Once you have a health plan expense that can be paid with your wellness dollars, BlueCross will apply your dollars—no

forms to file.

1. Go to the doctor.

2. Claim is processed by BlueCross BlueShield of MN and forwarded to the SelectAccount area within BlueCross.

After you pay the threshold amount ($250 – single, $500 – single + 1 or family), the wellness dollars are applied and you

receive payment in the form of a check or direct deposit from your HRA account.

Wellness dollars are applied to your HRA if you are enrolled in the PPO Plus or PPO Plan. Wellness dollars are applied to your HSA if you are enrolled in the HSA Plan. *Based on the results of your Wellness Screening.

Employees and their spouse who enroll in the company's health plans have the opportunity to earn wellness dollars based on

the results of their wellness screenings.

If you think you might be unable to meet certain wellness program standards required to receive the incentives, you might qualify for an opportunity to receive the incentive by meeting an alternative requirement such as completing other activities that may be available to you under the wellness program. Please contact Bravo at (877) 662-7286 if you have any questions about the wellness program and/or determine whether you may be eligible to receive an incentive by meeting an alternative requirement.

As a new hire, you have 60 days to complete your wellness screening.* Once you have enrolled in a health plan, get started and visit bravowell.com/taylor, then click "Create an Account." Enter your first name, last name, date of birth and SSN and select "continue". You will be able to schedule a screening. Or download a form for your doctor to complete. If you and your spouse are both participating, you must each set up your own account with separate emails.

*Screenings for newly hired employees end on 7/31 for the current plan year.

ACTION!

Wellness Dollars

Wellness Dollars in the PPO Plus and PPO plans

Body Mass Index• Less than 30• Less than 25

$100/$200$200/$400

$25/$50$50/$100

Blood Pressure• Less than 140/90• Less than 120/80

$100/$200$200/$400

$25/$50$50/$100

Cholesterol LDL• Less than 130mg/dl $200/$400 $50/$100

Tobacco Status• Negative for Nicotine $200/$400 $50/$100

Total Dollars Possible $800/$1,600 $200/$400

Health IndicatorPPO Plus and PPO

Employee/EE + SpouseHSA

Employee/EE + Spouse

Earn wellness dollars* for your Health Reimbursement Account (HRA) or Health Savings Account (HSA)

Welcome What to Do What's New Benefits Eligibility Enrollment Help

10Benefits in Review

Your dental plan is designed to encourage you to visit the dentist and help ensure your basic dental needs are met in a timely,

cost-effective manner.

Access to regular checkups and sound preventive care are key to long-term oral

health. In addition to visiting your dentist for regular preventive care, talk to your

dentist about your specific oral health needs.

Dental coverage is offered through Delta Dental.

When you enroll in the Dental Plan, you may visit any provider in either Delta

Dental network (Premier or PPO). The same benefit levels apply in each of these

two networks.

If you choose to use an out-of-network dentist, your out-of-pocket cost will be

higher because those providers can charge amounts which would otherwise be

disallowed by Delta Dental.

Find out more about your potential cost savings with the Delta Dental network.

For more information on your dental benefits, see the Dental Plan highlights

below or visit deltadental.com.

Dental

Dentists who participate in our

Delta Dental PPO or Delta Dental

Premier networks have agreed not

to charge more than our maximum

allowable amount. This can result

in lower out-of-pocket costs.

Choosing a dentist in the Delta

Dental PPO network may save

you even more money. As an

added convenience, you never

have to file a claim when you

use a participating dentist—the

dentist files the claim for you.

Deductible (does not apply to diagnostic/preventive and orthodontics)

• Individual• Family

$50$150

Annual Maximum $1,250/person

Preventive Care: Exams, X-rays 100%

Basic: Fillings, Endodontics, Periodontics 80%

Major: Crowns, Prosthetics 50%

Orthodontia (Adults & Children)• Co-Insurance• Lifetime Maximum

50%$1,750/person

Plan Highlight Benefit

Employee-Bi-Weekly* Contribution

Employer-Bi-Weekly* Contribution

$7.55 $16.23 $21.51

$7.55 $16.23 $21.51

Employee Employee+1 Family

Dental PremiumsThe table below shows your pay period (bi-weekly)* cost for the Dental Plan.

*To calculate a weekly amount, divide by 2.

Welcome What to Do What's New Benefits Eligibility Enrollment Help

Benefits in Review 11

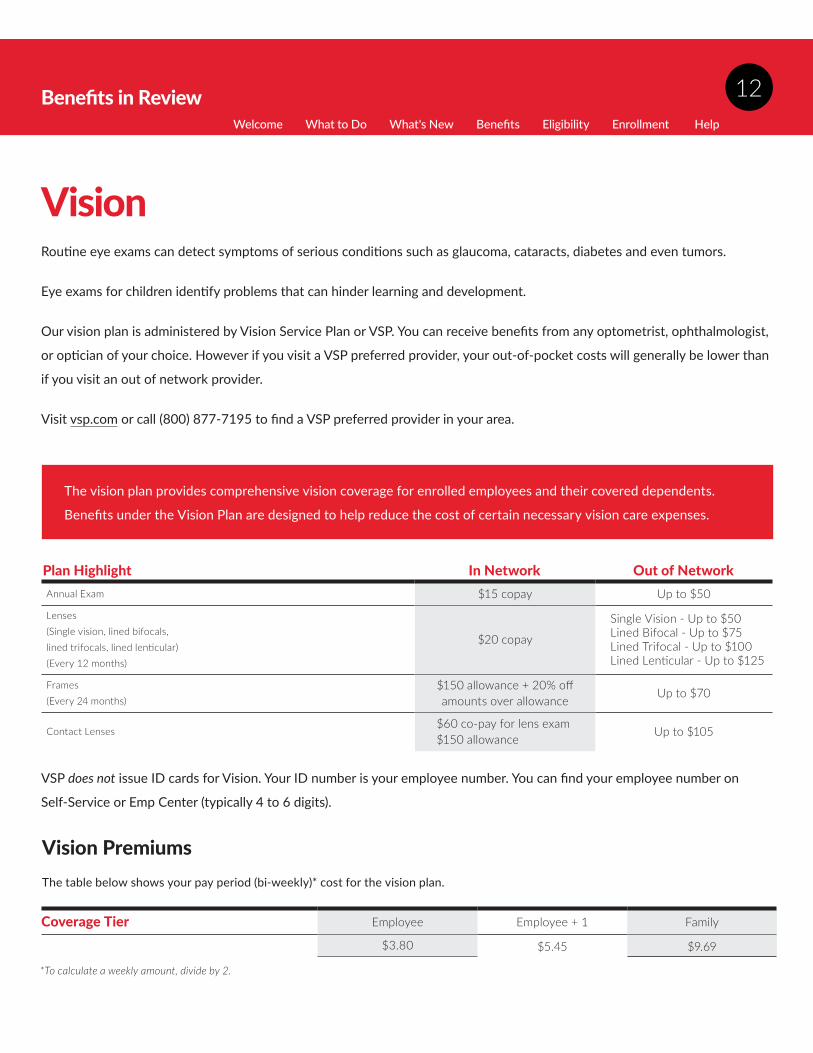

Employee Employee + 1 Family

$3.80 $5.45 $9.69

Routine eye exams can detect symptoms of serious conditions such as glaucoma, cataracts, diabetes and even tumors.

Eye exams for children identify problems that can hinder learning and development.

Our vision plan is administered by Vision Service Plan or VSP. You can receive benefits from any optometrist, ophthalmologist,

or optician of your choice. However if you visit a VSP preferred provider, your out-of-pocket costs will generally be lower than

if you visit an out of network provider.

Visit vsp.com or call (800) 877-7195 to find a VSP preferred provider in your area.

Vision

The vision plan provides comprehensive vision coverage for enrolled employees and their covered dependents.

Benefits under the Vision Plan are designed to help reduce the cost of certain necessary vision care expenses.

Annual Exam $15 copay Up to $50

Lenses(Single vision, lined bifocals, lined trifocals, lined lenticular)(Every 12 months)

$20 copay

Single Vision - Up to $50 Lined Bifocal - Up to $75 Lined Trifocal - Up to $100 Lined Lenticular - Up to $125

Frames(Every 24 months)

$150 allowance + 20% off amounts over allowance

Up to $70

Contact Lenses $60 co-pay for lens exam $150 allowance

Up to $105

Plan Highlight In Network Out of Network

VSP does not issue ID cards for Vision. Your ID number is your employee number. You can find your employee number on

Self-Service or Emp Center (typically 4 to 6 digits).

Coverage Tier

Vision PremiumsThe table below shows your pay period (bi-weekly)* cost for the vision plan.

*To calculate a weekly amount, divide by 2.

Welcome What to Do What's New Benefits Eligibility Enrollment Help

12Benefits in Review

Far Left:Image Description Image Location

Flexible Spending Accounts (FSAs) let you set aside pre-tax money to help pay for eligible expenses. Both a Health Care FSA

and a Dependent Care FSA are available as part of your benefits. The differences are shown below.

Flexible Spending Accounts (FSA)

Eligible Expenses Copayments, co-insurance, deductibles, dental expenses, vision expenses, prescription drugs See IRS Publication 502 for a complete list

Eligible child (under 13) and adult care expenses such as day care, before and after-school care, preschool, nursery school, summer day camps See IRS Publication 503 for a complete list

Annual MaximumContribution*

$2,600 (min. of $100) $5,000 ($2,500 per year if you are married and file a separate tax return.)

Funds availability Funds are available to you as of the beginning of the plan year.

Works on a “dollar in - dollar out” process. You are only eligible to be reimbursed for monies that have been withheld as of the date of your request.

Portability No No

Forfeiture IRS rules require you to forfeit any unused money in your Health Care FSA if you do not submit expenses by March 31 of the following plan year.

IRS rules require you to forfeit any unused money in your Dependent Care FSA if you do not submit expenses by March 31 of the following plan year.

Grace Period Medical claims incurred in the first 75 days following the plan year can be covered by outstanding funds from the previous year.

N/A

Health Care FSA Dependent Care FSA

*Subject to change based on IRS guidelines.

Important

If you elect to participate in the HSA Medical Plan, you will not be eligible to participate in the Healthcare Flexible Spending

Account. You may however still participate in the Dependent Care Flexible Spending Account.

Welcome What to Do What's New Benefits Eligibility Enrollment Help

Benefits in Review 13

Who is eligible? Employees in the HSA Plan Employees in the PPO Plus Plan and PPO Plan

Employees in the PPO Plus and PPO Plan

Will I be automatical-ly enrolling in a savings plan?

Yes, only if you participate in the wellness screening and earn dollars to activate it

Yes, only if you participate in the wellness screening and earn dollars to activate it

No - You must elect the plan if you are in either the PPO Plus or PPO Plans

Who opens the account? Employee Employer Employee

Who can contribute? Employee and Employer Employer Employee

Do I keep the account if I leave? Yes No, unless you elect COBRA for the remainder of the calendar year

No, unless you elect COBRA for the remainder of the calendar year

What can be reimbursed by the account?

Qualified Health Care Expenses Qualified Health Care Expenses Qualified Health Care Expenses

Tax status of the contributions Pre-tax N/A Pre-tax

Tax status of the payments Pre-tax N/A Pre-tax

Who controls the payments? You do Plan does You do

Use with other account based plans No. Health Care FSA prohibited FSA HRA. HSA prohibited

The Optum Health Care FSA payment card allows you to get faster access to your pre-tax FSA dollars. Pay for eligible health

and pharmacy expenses with your card, instead of paying cash. You can even use your card to pay for eligible over-the counter

health care expenses—bandages, contact lens solution and more.**

Note: Claims you submit through your FSA payment card may require supporting documentation, so always keep your

receipts! Optum will make every effort to electronically verify your card transactions, as required by the IRS. If Optum is not

able to verify a transaction, you will receive a letter requesting an itemized receipt or Explanation of Benefits (EOB). If the

required documentation is not received within the stated time period, your card will be suspended. If you are not able to

provide appropriate documentation, any unverified card purchases will be reported as taxable income.

**For a complete list, see IRS Publication 502

Optum Payment Card

HSA vs. HRA vs. FSA - Making sense of the different accounts

All of the letters can be confusing. Here is a closer look at the three types of reimbursement plans that are available.

After you know more, you can make better decisions about which plan is right for you.

Health Savings Account (HSA)

Health Reimbursement Account (HRA)

Health CareFSA

Welcome What to Do What's New Benefits Eligibility Enrollment Help

14Benefits in Review

The Commuter Expense Reimbursement Accounts (CERA) allow you to pay for qualified transit and parking expenses

using money you have set aside pre-tax. You can elect to contribute what you expect to spend on your commute per

month, that elected amount will be taken out pre-tax and put into your account at Optum. Funds are available for

disbursement once they have been deposited into your account. Unused amounts can be carried over.

The IRS sets maximum monthly pre-tax deduction and spending limits. The maximum allowed pre-tax contribution and

reimbursement amounts per calendar month are:

• Transit Passes or Commuter Highway Vehicle - $260/month

• Parking - $260/month

Optum Payment Card

If you enroll in the Commuter Benefits, you will receive an Optum Payment Card. If you are already a participant in the

company FSA through Optum, you can use the same card. You can use the card for parking and transit expenses.

Using the Card for Parking

When the participant uses the Card for parking expenses, there’s no paying cash up front, no claim forms to fill out and

no waiting for reimbursements. The card helps with qualified CERA expenses such as parking expenses for any type of

vehicle at or near the participant’s work location or at or near a location from which the participant commutes using

mass transit.

Using the Card for Transit

The Card can be used for mass transit passes, tokens, or fare cards purchased at a valid transit fare terminal.

Commuter Expense Reimbursement Accounts (CERA)

Welcome What to Do What's New Benefits Eligibility Enrollment Help

15Benefits in Review

Life insurance can help provide financial protection in the event of your death. All eligible employees are automatically covered by Basic Life and AD&D insurance at no cost. In addition to your basic life insurance, you have the option to enroll in different levels of supplemental coverage for yourself, as well as coverage for your eligible family members.

Supplemental Life Insurance coverage is paid by the employee with post-tax dollars.

Employees can add (if previously waived), or increase their current coverage amount by two increments (total of $20,000) every open enrollment period with no Evidence of Insurability (EOI) up to $350,000. Once the coverage level reaches $350,000, any requested increase would require EOI. Spouses can add (if previously waived) or increase their current coverage amount by one coverage level ($0-$5,000 or $5,000-$10,000 or $10,000-$25,000, and you can elect up to $10,000 for dependents) every open enrollment period with no EOI.

How to calculate your Supplemental Life Insurance cost.

The cost for this coverage is shown in the table below. The cost for this coverage is shown in the table below.

Amount Electedx = $

Life and AD&D Rate Above(based upon your age on January 1st)

Your Bi-Weekly Cost*

Life Insurance

Basic Life InsuranceThe Basic Life Insurance Plan automatically provides Life and AD&D

insurance of your salary, up to $400,000, at no cost.

Dependent Life InsuranceDependent Life Insurance provides a benefit to you in the case of the death of your spouse or your dependent child(ren)

(less than age 26).

Coverage Choices and Rates

Supplemental Life InsuranceOptional coverages include:

• Employee Life and AD&D insurance

• Spouse life insurance

• Child life insurance

How much can I elect?

Newly eligible employees have a one time opportunity to elect the following without providing Evidence of lnsurability (EOI). Supplemental Life—5x salary up to $350,000Spouse-up to $25,000 Dependent -up to $10,000

Age <25 25-29 30-34 35-39 40-44 45-49 50-54 55-59 60-64 65-69 70+

Bi-weekly* Rate/$10,000

0.27 0.30 0.38 0.42 0.512 0.73 1.12 1.93 2.55 4.62 7.44

$5,000 $10,000 $25,000

Bi-weekly* Rate $0.64 $1.27 $3.18

$5,000 $10,000

Bi-weekly* Rate $0.81 $1.62

Supplemental Life Insurance Rates

Spouse Life Insurance Child(ren) Life Insurance

10,000 =

Welcome What to Do What's New Benefits Eligibility Enrollment Help

Benefits in Review 16

Disability benefits provide income if you cannot work due to an illness or injury. Eligibility is the first of the month coinciding

with or next following 180 days of continuous service in an eligible status.

All full-time employees are automatically covered by short-term and Core long-term disability plans which are paid for by the

company. You have the ability to purchase additional long-term disability insurance. You do not need to enroll.

Disability Insurance

Short-Term Disability (company paid)

Short-term disability insurance provides income protection if you cannot work due to your own non-work-related illness or

injury, including maternity. Short-term disability begins to pay benefits after you cannot work for 7 consecutive calendar

days. After 7 days, short-term disability will pay 67 percent of your pre-disability earnings, once approved.

Benefits will continue for up to 25 weeks following the 7 day waiting period, as long as you remain disabled. When

short-term disability benefits end, you may be eligible to receive long-term disability benefits.

Core Long-Term Disability (company paid)

Long-term disability replaces 60% of your monthly earnings if you are disabled and cannot work, up to a maximum benefit of

$12,000 per month. Once approved, these benefits begin after short-term disability benefits end.

During the first 24 months of disability, you are deemed disabled if unable to perform the material duties of your own

occupation. After 24 months, to be considered disabled, you must not be able to perform the duties of any occupation for

which you are suited by prior training, education and experience.

As long as you remain disabled, the Core Long Term Disability Plan will continue to pay benefits for up to five years.

Buy Up Long-Term Disability (voluntary)

The Buy Up Long-Term Disability plan is paid by the employee with pre-tax dollars and extends the long-term disability

payments past the Core plan's 5-years up to Reducing Benefit Duration (refer to plan document for details). Employees are

automatically enrolled in the Buy Up Long-Term Disability plan and must actively opt-out via Self-Service if they do not want

the benefit.

Buy Up Long-Term Disability is paid by the employee with pre-tax dollars. Long-term disability rate: $0.068 per $100 of

covered payroll.

Monthly Earnings* Your Bi-Weekly Cost

100 x .0314 = $

*See plan document for definition of earnings

Welcome What to Do What's New Benefits Eligibility Enrollment Help

17Benefits in Review

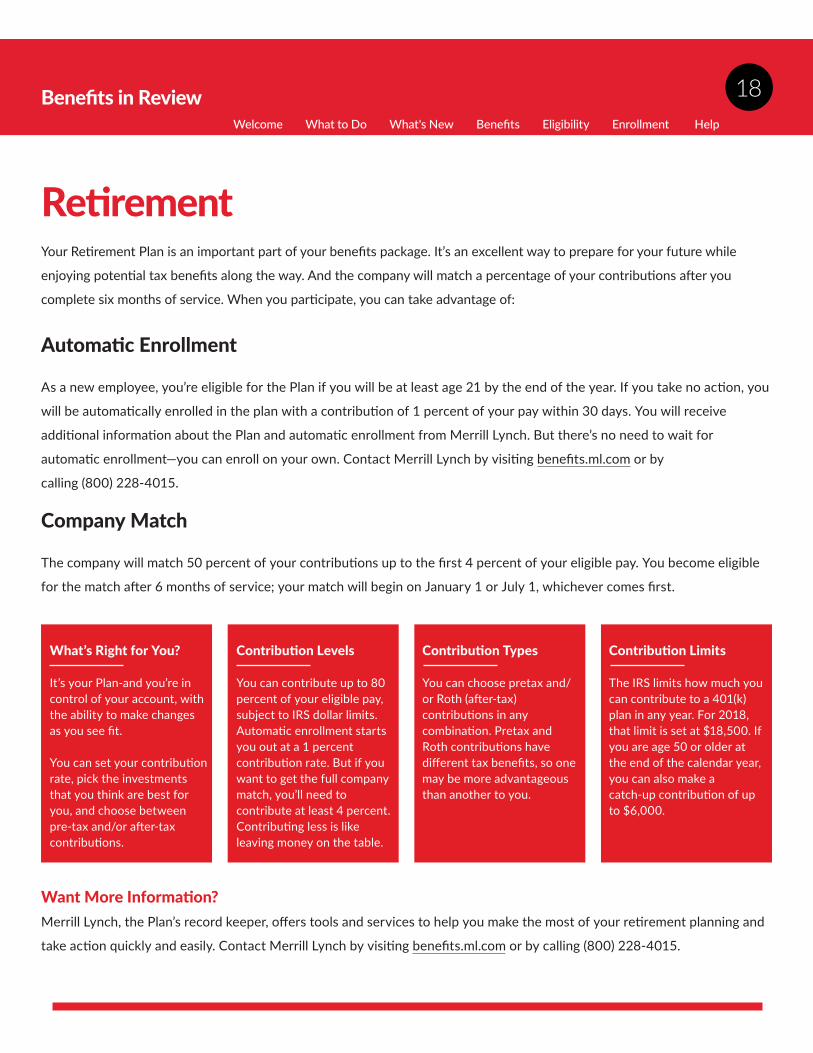

Your Retirement Plan is an important part of your benefits package. It’s an excellent way to prepare for your future while

enjoying potential tax benefits along the way. And the company will match a percentage of your contributions after you

complete six months of service. When you participate, you can take advantage of:

Retirement

Automatic Enrollment

As a new employee, you’re eligible for the Plan if you will be at least age 21 by the end of the year. If you take no action, you

will be automatically enrolled in the plan with a contribution of 1 percent of your pay within 30 days. You will receive

additional information about the Plan and automatic enrollment from Merrill Lynch. But there’s no need to wait for

automatic enrollment —you can enroll on your own. Contact Merrill Lynch by visiting benefits.ml.com or by

calling (800) 228-4015.

Company Match

The company will match 50 percent of your contributions up to the first 4 percent of your eligible pay. You become eligible

for the match after 6 months of service; your match will begin on January 1 or July 1, whichever comes first.

What’s Right for You?

It’s your Plan-and you’re in control of your account, with the ability to make changes as you see fit.

You can set your contribution rate, pick the investments that you think are best for you, and choose between pre-tax and/or after-tax contributions.

Contribution Levels

You can contribute up to 80 percent of your eligible pay, subject to IRS dollar limits. Automatic enrollment starts you out at a 1 percent contribution rate. But if you want to get the full company match, you’ll need to contribute at least 4 percent. Contributing less is like leaving money on the table.

Contribution Types

You can choose pretax and/or Roth (after-tax) contributions in any combination. Pretax and Roth contributions have different tax benefits, so one may be more advantageous than another to you.

Contribution Limits

The IRS limits how much you can contribute to a 401(k) plan in any year. For 2018, that limit is set at $18,500. If you are age 50 or older at the end of the calendar year, you can also make a catch-up contribution of up to $6,000.

Want More Information?Merrill Lynch, the Plan’s record keeper, offers tools and services to help you make the most of your retirement planning and

take action quickly and easily. Contact Merrill Lynch by visiting benefits.ml.com or by calling (800) 228-4015.

Welcome What to Do What's New Benefits Eligibility Enrollment Help

Benefits in Review 18

Employee Assistance Program (EAP)The Employee Assistance Program (EAP) provides 24/7 confidential, professional counseling and referral services to help you and your

family with personal, job or family issues. The program is no-cost, completely confidential and available to all benefit eligible employees

insured under the Basic Life Insurance and their families. The EAP provides unlimited phone support and up to five confidential

counseling sessions per person, per issue, per year. Some common concerns the EAP can help with include:

The EAP also provides financial counseling, legal consultations and more. Additional charges may apply. Call (866) 682-6047 or visit

guidanceresources.com for more information (web ID: EAP4TCC).

Additional Benefits

Employee DiscountsOur employee discount site is available to all employees offering substantial savings from a variety of online merchants ranging from

apparel to electronics to financial services and health and wellness, every day shopping needs, movie and theme park tickets and more!

Access our affiliate company product discounts as well via Compass - Offers and Discounts. We offer 15-50% discount opportunities

from our Taylor Companies for virtually any occasion; party supplies, decorations, holiday gifts and cards, invitations, personalized items

and office products and more. This perk can be shared with family and friends too!

Visit perksatwork.com for more information. You can register with your work email address or your employee ID as found in Self-Service.

Online Will PreparationDrafting a will ensures that your assets pass on to your loved ones and your children are protected by a guardian of your choosing.

EstateGuidance® makes it easy with online tools that walk you through the process in minutes. In addition, you can draft a living will to

ensure you get the end-of-life care you desire and a final arrangements document expressing your wishes for your funeral services. To get

started call 866.682.6047 or visit guidanceresources.com (Web ID: EAP4TCC).

Travel AssistanceWhen traveling more than 100 miles from home, Voya Travel Assistance offers you and your dependents four types of services: Pre-trip information, emergency personal services, medical assistance services and emergency transportation services.

Contact Voya Travel Assistance 24 hours a day, 365 days a year at 800.859.2821 (U.S. Toll Free) or 202.296.8355 (Worldwide) or email ops@suroassistance_usa.com.

Pre-trip informationThese valuable services help you start your trip the right way. Voya Travel Assistance can provide you with important, up-to-date travel information including:• Immunization requirements• Visa & passport requirements• Foreign exchange rates• Travel/tourist advisories• Temperature & weather conditions• Culture information

Emergency personal servicesIn the event of an unexpected situation of a non-medical nature, Voya Travel Assistance offers access to several valuable services, including:• Urgent message relay• Interpretation/translation services• Emergency travel arrangements• Recovery of lost or stolen luggage or personal posessions• Legal assistance and/or bail bond

Stress, anxiety,and depression

Grief and lossConflict

resolutionWork/life counseling

Divorce or separation

Life transitions Substance abuse

Welcome What to Do What's New Benefits Eligibility Enrollment Help

19Benefits in Review

Take Charge – Managing Your Health Care CostsYou have the power to help control our health care costs. The healthier you are and the better you manage your health care spending, the less the company has to spend and in the long run-the less you have to pay. We are all “consumers” of health care. In many instances you can control purchases with advanced planning. Here are some basic areas you might consider when “shopping” for your health care needs.

GenericsUsing generic drugs instead of their brand-name counterparts is a proven cost-saver for you and your health plan. You benefit from low copays and your health plans costs are far lower. On average, generics cost 85 percent less than brand-name drugs.

At present, our employees opt for generics 85 percent of the time, which is a great number. However, for every 1 percent increase in the use of generics, the health care plans can save $225,000. We can raise that percentage easily. It justtakes you. In fact, our pharmacy vendor estimates almost $1.4M in savings by increasing generic utilization for ADHD,

diabetes, pain, and cholesterol medications. We recommend you discuss generic options with your doctor/pharmacy.

90-Day Rx ProgramIf you take certain medications on a regular basis, you can save time and money with the 90-day Rx Program. You will have lower copayments when you take part in the program. You pay 2.5 times the monthly copayment or co-insurance for a 3-month drug supply instead of a full 3-month copayment or co-insurance—this is like receiving two months of free medications each year. You can take advantage of the 90-day program at participating retail pharmacies or use mail order.

Alternate Sources of Covered CareUrgent care centers, walk-in clinics, and Doctors on Demand are effective alternatives to emergency room care. These facilities can effectively treat serious but non life-threatening conditions, such as the flu, earaches, respiratory infections, small cuts, sprains and minor broken bones. They charge less and offer shorter wait times than an emergency room. Our medical plans provide coverage for urgent care centers, walk-in clinics and telemedicine. If you have any questions as to whether you should seek care in one of these alternate facilities, contact your physician for advice.

Doctor on DemandDoctor on Demand is a market leader in telemedicine which allows you to visit with a doctor remotely to treat common issues and prescribe medications, all at a lower cost than a traditional office visit. No need to schedule an appointment, travel to your doctor’s office and wait for your appointment, you can do it all through the Doctor on Demand application, which is available for download on iPhone or Android devices.

Emergency Room vs. Urgent Care VisitsThe average cost of an emergency room visit is $1,600 while the average cost of an urgent care visit is $135. If you have a situation that doesn’t require an ER visit, you might consider saving money and time by choosing urgent care.

Welcome What to Do What's New Benefits Eligibility Enrollment Help

Benefits in Review 20

And Let’s Not Forget the Biggest Cost Impact of All – Taking Care of Yourself!A healthy lifestyle can make a difference in your life - and in your health care costs. You can’t control every possibility that

impacts your health, but you can give yourself a leg up by doing things that help prevent diseases or control chronic

conditions. In fact, the five simple actions listed below can have an immediate impact on your health.

• Eat healthy

• Exercise

• Lose weight

• Follow preventive care guidelines

• Stop using nicotine

Partner with your physician to see how you can improve your health risks. Even small changes can have big results. You are

likely to see a difference in the way you feel, and, you may find yourself in better health and in need of a lot less care.

Throughout the coming year we will share ways in which you can become a more informed and active health care consumer.

Look for information on disease management programs and other initiatives as a way for you to take charge of your health

and avoid unnecessary expenditures.

Welcome What to Do What's New Benefits Eligibility Enrollment Help

21Benefits in Review

EligibilityBenefit EligibilityEligibility for these benefits varies. This section is

intended to provide a summary of benefits offered to

employees. In determining actual benefit coverage and

eligibility, the official text of company Plans Documents

and Summary Plan Descriptions are the governing source.

Generally, the following individuals may be eligible

dependents for our benefit plans. The company

reserves the right to audit dependent elections at any

point in time.

Spouse• Legally Married for purposes of federal law.

• Common Law when recognized by the state

of residence.

Dependent Children to Age 26• Natural born

• Adopted

• Stepchildren and/or foster children

• Eligible dependents include adopted children,

disabled dependents, dependent grandchildren

(who meet the plan’s eligibility requirement) and

children under legal guardianship. Dependents such

as Grand/Disabled/ Adopted Child(ren) are subject to

review/approval by the insurance carrier. Children or

spouses of the dependent are not eligible.

Note:No person can be insured as a dependent of more than one employee under the Policy. If both parents work for

the company, then only one parent can cover their child(ren) under the insurance.

Welcome What to Do What's New Benefits Eligibility Enrollment Help

Eligibility 22

Eligibility Requirements and Benefit BeginsThese benefits are governed by the applicable insurance policy, contract or plan document (“Governing Documents”). The

eligible criteria and benefit summaries contained in this Benefits Guide are only partial explanations; complete details are set

forth in the Governing Documents. In the event of a conflict between the content of this Benefits Guide and Governing

Documents, the Governing Documents will prevail over the terms of this Benefits Guide as relates to these benefits.

For purposes of the following benefits, your eligibility will be determined by your current Employee Status as described in

your Handbook. Please refer to the Note under “Health” below.

Eligibility for the following benefits will be determined at the time of a claim based on the average hours for the prior 12

months worked:

• Full-time benefits = an average of 35 hours or more.

• Part-time benefits = an average of 20 hours or more.

Health Available on date of hire. Note: Required to work an average of 30 hours per week in the prior 12-month Look Back Measurement period.

Dental Available on date of hire for full-time and part-time employees.

Vision Available on date of hire for full-time and part-time employees.

Flexible Benefits For full-time and part-time employees. Available on date of hire.

Short-Term Disability For full-time employees, effective first of a month following 180 days of service.

Long-Term Disability For full-time employees, effective first of a month following 180 days of service.

Basic Life Insurance Available on date of hire for full-time and part-time employees.

Supplemental Life Insurance Available on date of hire for full-time and part-time employees.

Employee Assistance Plan Available on date of hire for full-time and part-time employees.

Benefits(Insurance, pension, and related benefits)

Benefits

Eligibility Requirements

Eligibility Requirements

Welcome What to Do What's New Benefits Eligibility Enrollment Help

23Eligibility

Special Enrollment Provisions

Loss of Other CoverageIf you decline enrollment for yourself or for an eligible dependent because you had other group health plan coverage or

other health insurance, you may be able to enroll yourself and your dependents in the Plan if you or your dependents lose

eligibility for that coverage, or if the other employer stops contributing toward your or your dependents’ other coverage. You

must request enrollment within 30 days after you or your dependents’ other coverage ends, or after the employer stops

contributing toward the other coverage.

New Dependent by Marriage, Birth, Adoption, or Placement for Adoption If you gain a new dependent as a result of a marriage, birth, adoption or placement for adoption, you may be able to enroll

yourself and your new dependents in the Plan. You must request enrollment within 30 days after the marriage, birth,

adoption or placement for adoption. In the event you acquire a new dependent by birth, adoption or placement for adoption,

you may also be able to enroll your spouse in the Plan, if your spouse was not previously covered.

Enrollment Due to Medicaid/CHIP Events If you or your eligible dependents are not already enrolled in the Plan, you may be able to enroll yourself and your eligible

dependents in the Plan if: (1) you or your dependents lose coverage under a state Medicaid or children’s health insurance

program (CHIP); or (2) you or your dependents become eligible for premium assistance under state Medicaid or CHIP.

You must request enrollment within 60 days from the date of the Medicaid/CHIP event.

Notice AvailabilityA copy of this notice is available at our internal website at http://newcompass.tc.inet, Compass - HRConnect - Benefits -

Summary Plan Documents page. Additional information regarding your rights to enroll in the Plan are found in the applicable

Summary Plan Description(s) for the Plan, or you may contact HRConnect as provided above.

Contact Information If you have any questions about this Notice or about how to enroll in the Plan, please contact HRConnect at

(877) 252-9861, [email protected], or by writing to:

HRConnect

1725 Roe Crest Drive

P.O. Box 3728

North Mankato, MN 56002-3728

Life Events

Welcome What to Do What's New Benefits Eligibility Enrollment Help

24Eligibility

Enrollment – HowBefore you begin your enrollment:

1. Study your options—read through this guide or visit taylorcorp.com/enrollment.

2. Know the difference—make sure you understand how the plans work and how you can manage your health care

expenses all year long.

3. Decide what plans you will elect.

4. Decide who to cover—yourself, your legal spouse, your eligible children or your entire family. The company

reserves the right to audit dependents at any point in time.

5. Make your elections.

• Go to http://newcompass.tc.inet and click on Self Service under My Tools and login (or from home, go to

http://compass.taylorcorp.com).

• First, review and update the dependents and beneficiaries under the Benefits menu. Legal names, accurate

dates of birth and dependent social security numbers must be on file.

• Click on Benefit Enrollment/Change.

Making Changes/Life Events

You can only change your benefit elections if you have a qualified change in status, such as a birth, marriage, or divorce.

Changes must be made no later than the 30th day of the event. Make changes by logging into Self Service.

Questions?

HRConnect is available to answer your questions. Feel free to contact us by phone: 1 (877) 252-9861 or by email:

Welcome What to Do What's New Benefits Eligibility Enrollment Help

Enrollment - How 25

Help and SupportYou have lots of help and support when it comes to benefits. Use this page to find the support you need. Remember,

HRConnect should be your first stop regarding general enrollment and eligibility questions.

HRCONNECT I (877) 252-9861 I [email protected] I taylorcorp.com/enrollment

Contact the specific plan administrators listed for questions regarding claims or information specific to coverage,

providers, etc.

Medical BCBS of MN (866) 289-5154 www.bluecrossmnonline.com

Pharmacy CVS (800) 405-6432 www.caremark.com

Dental Delta Dental (800) 448-3815 www.deltadental.com

Doctor on Demand www.doctorondemand.com/bluecrossmn

Vision VSP (800) 877-7195 www.vsp.com

Life Insurance Voya (877) 882-9567 www.voya.com

Disability Insurance Voya (877) 882-9567 www.voya.com

Flexible Spending Accounts Optum (800) 243-5543 www.optumhealthfinancial.com

Health Savings Account HSA Bank (800) 357-6246 www.hsabank.com

Retirement Merrill Lynch (800) 228-4015 www.benefits.ml.com

Employee Assistance Program ComPsych (866) 682-6047 www.guidanceresources.com

COBRA Optum (866) 301-6681 www.optumhealthfinancial.com

Wellness Bravo Wellness (877) 662-7286 www.bravowell.com/taylor

HRA Select Account (800) 859-2144 www.selectaccount.com

Program PhoneProvider Web

26Welcome What to Do What's New Benefits Eligibility Enrollment Help

Help and Support