© etphones.com ltd 2004. all rights reserved. the real world of sip a business perspective trefor...

TRANSCRIPT

© ETphones.com Ltd 2004. All rights reserved. www.purplepacket.com

The Real World of SIPA Business Perspective

Trefor Davies – ETphones.net

Board of Directors, SIP Forum.

Co-chair Certification Working Group

Sip:[email protected] [email protected]+44 1522 533 888

© ETphones.com Ltd 2004. All rights reserved. www.purplepacket.com

Agenda

• Where have we come from? Review of market

• Phones• Service providers• Enterprise

• The anatomy of a real SIP system

• Where do we go?

© ETphones.com Ltd 2004. All rights reserved. www.purplepacket.com

SIP Phones 2001

© ETphones.com Ltd 2004. All rights reserved. www.purplepacket.com

SIP Phones 2002

© ETphones.com Ltd 2004. All rights reserved. www.purplepacket.com

SIP Phones 2003

© ETphones.com Ltd 2004. All rights reserved. www.purplepacket.com

SIP Phones 2004

© ETphones.com Ltd 2004. All rights reserved. www.purplepacket.com

SIP Service Providers

• BlueWin

• eAccess Broadband Services

• WorldCom

• BT

• Telus

• Telstra

• TalkingNets

• bConvergent

• Callserve

• Deltathree/iConnect Here

• Exario

• Level 3

• iBasis

• Telia

• Denwa

• Vonage

• BroadSIP

• Song Networks

• Sonera

• CoolCall

• Korea telecom

• Peerlinx (wireless)

• GoBeam

© ETphones.com Ltd 2004. All rights reserved. www.purplepacket.com

SIP Service Providers

• BlueWin

• eAccess Broadband Services

• BT

• Telus

• Telstra

• bConvergent

• Callserve

• Deltathree/iConnect Here

• Exario

• Level 3

• iBasis

• Telia Sonera

• Vonage

• BroadSIP

• Song Networks

• Korea Telecom

• Peerlinx (wireless)

• GoBeam

© ETphones.com Ltd 2004. All rights reserved. www.purplepacket.com

SIP Service Providers

• BlueWin• eAccess Broadband

Services• MCI• BT• Telus• Telstra• Voice Pulse• Voz Telecom• Fordyce• Bredbandsbolaget• Xtraphone• KDDI• IAXTEL• TeleSIP.net• Free World Dialup• Net2Phone

• ETphones.net

• bConvergent

• CallServe

• Delta3 iConnect Here

• Exario

• Level3

• Telia Sonera

• iBasis

• Packet8

• CallUK

• Japan Telecom

• Telio

• Most US ILECs in process

• Vonage

• SIPphone.com

• BroadSIP

• Song Networks

• Addaline

• DialPad

• KT

• Peerlinx

• GoBeam

• SIPTel

• NTT

• Iptel

• Primus

• Mobitus

© ETphones.com Ltd 2004. All rights reserved. www.purplepacket.com

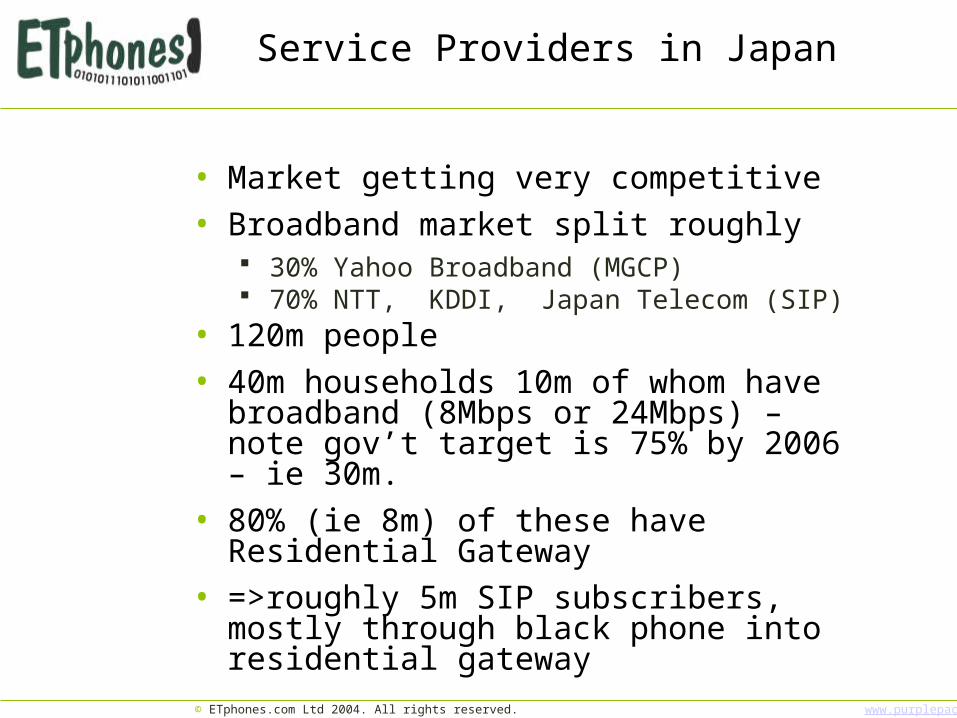

Service Providers in Japan

• Market getting very competitive• Broadband market split roughly

30% Yahoo Broadband (MGCP) 70% NTT, KDDI, Japan Telecom (SIP)

• 120m people• 40m households 10m of whom have

broadband (8Mbps or 24Mbps) – note gov’t target is 75% by 2006 – ie 30m.

• 80% (ie 8m) of these have Residential Gateway

• =>roughly 5m SIP subscribers, mostly through black phone into residential gateway

© ETphones.com Ltd 2004. All rights reserved. www.purplepacket.com

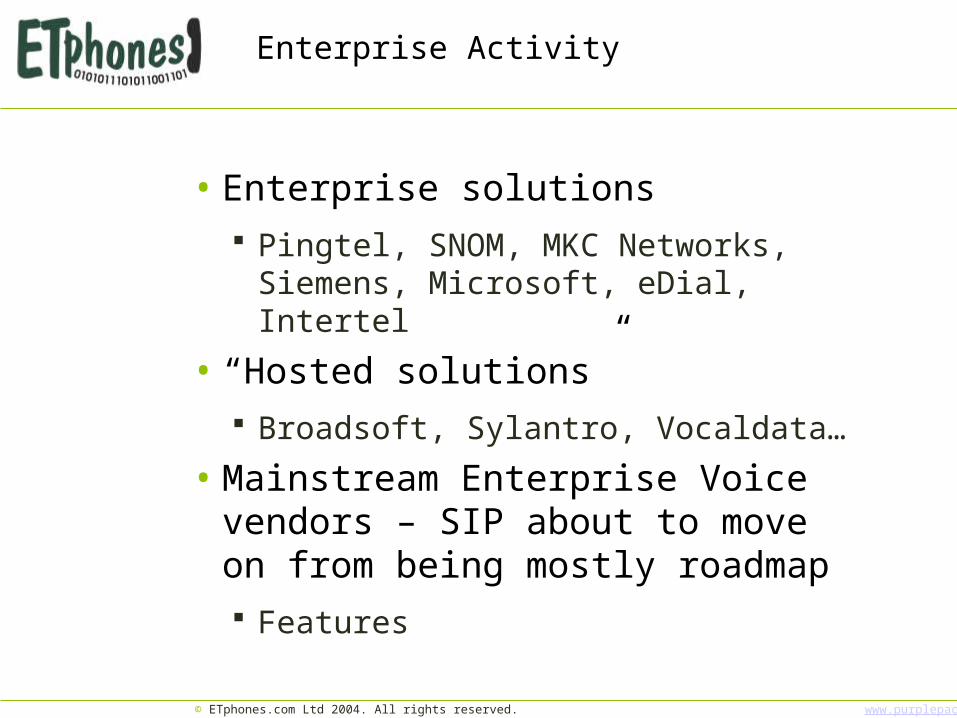

Enterprise Activity

• Enterprise solutions Pingtel, SNOM, MKC Networks,

Siemens, Microsoft, eDial, Intertel

• “Hosted solutions” Broadsoft, Sylantro, Vocaldata…

• Mainstream Enterprise Voice vendors – SIP about to move on from being mostly roadmap Features

© ETphones.com Ltd 2004. All rights reserved. www.purplepacket.com

Some Enterprise Implementation Examples

• Yale University -16k users

• IBM – stated aim to have entire worldwide workforce using SIP by 2006 (600,000< people)

• Reuters

• University British Columbia

© ETphones.com Ltd 2004. All rights reserved. www.purplepacket.com

Anatomy of a SIP service Easy for new players to get in the market

• Drivers• Regulatory• Local Numbers & ENUM • SIP server• The NAT issue • Applications• Conferencing• PSTN connectivity• Billing• Marketing• Dollars

© ETphones.com Ltd 2004. All rights reserved. www.purplepacket.com

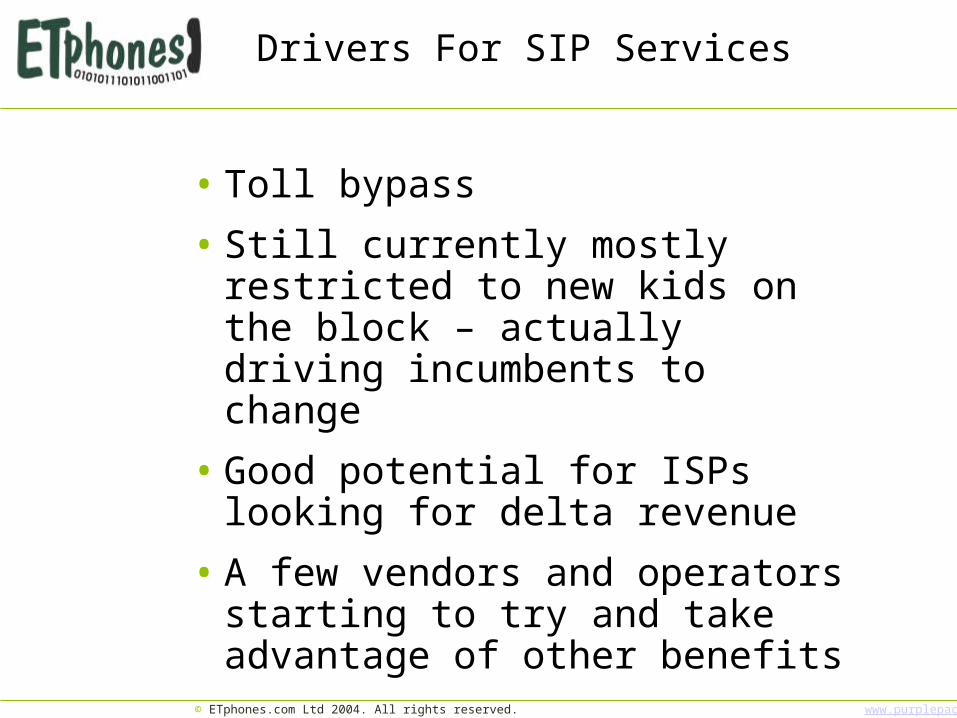

Drivers For SIP Services

• Toll bypass

• Still currently mostly restricted to new kids on the block – actually driving incumbents to change

• Good potential for ISPs looking for delta revenue

• A few vendors and operators starting to try and take advantage of other benefits

© ETphones.com Ltd 2004. All rights reserved. www.purplepacket.com

Regulatory

• High Profile in the USA Pulver, - very careful not to call it a

telephony service Vonage/Packet 8

-Minnesota/California et al

• Much less of an issue in Europe UK completely deregulated –

anyone can set up a service

• Emergency services Typically either not supported or

via local PSTN gateway

© ETphones.com Ltd 2004. All rights reserved. www.purplepacket.com

© ETphones.com Ltd 2004. All rights reserved. www.purplepacket.com

PSTN Hook-Up

• Termination is easy

• Choices global players (iBasis Level 3 etc) smaller CLEC or doing it yourself

• Origination has been harder to find. Dearth of numbers Was a shortage of people offering it

outside of USA

© ETphones.com Ltd 2004. All rights reserved. www.purplepacket.com

ENUM

• ENUM trials at different stages of maturity around the world

• Australia, Austria, Brazil, Canada, China, Denmark, Finland, France, Germany, Hungary, Ireland, Japan, Korea, Malaysia, Netherlands, Poland, Singapore, Slovenia, Sweden, Switzerland, Taiwan, UAE, UK, USA

© ETphones.com Ltd 2004. All rights reserved. www.purplepacket.com

Billing

• Whole range of billing options available

• Servers typically provide CDR data that can easily be interfaced to billing software of choice

• Billing can be expensive - pricing pitched as % of revenues (3 – 4%)

• Some server vendors provide integrated billing solutions

© ETphones.com Ltd 2004. All rights reserved. www.purplepacket.com

The NAT issue

• Mix of solutions out there Stand alone Solutions integrated with other

features eg DSL modem/ SIP comms server/firewall

Session Border Control Softphones sold with STUN

server hookup Intelligent solution with STUN

& RTP relay options

© ETphones.com Ltd 2004. All rights reserved. www.purplepacket.com

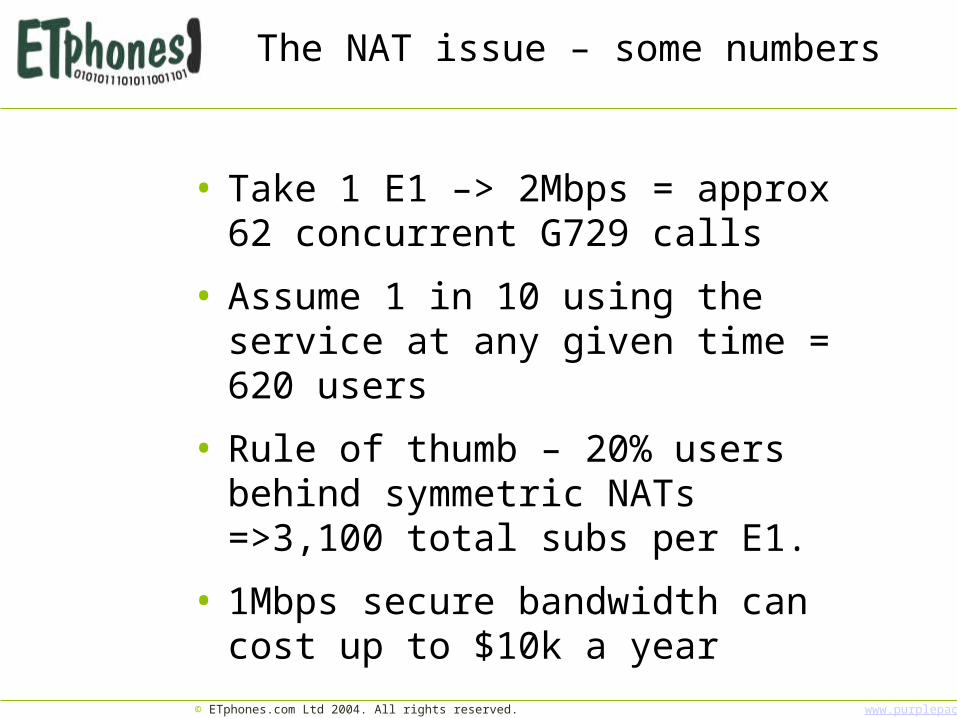

The NAT issue – some numbers

• Take 1 E1 –> 2Mbps = approx 62 concurrent G729 calls

• Assume 1 in 10 using the service at any given time = 620 users

• Rule of thumb – 20% users behind symmetric NATs =>3,100 total subs per E1.

• 1Mbps secure bandwidth can cost up to $10k a year

© ETphones.com Ltd 2004. All rights reserved. www.purplepacket.com

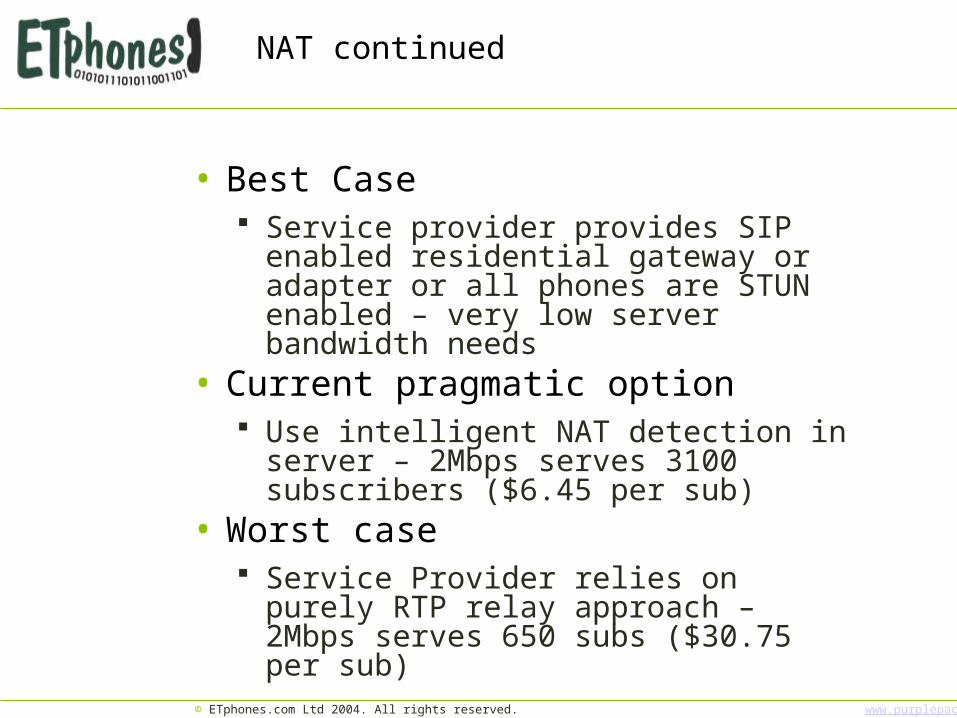

NAT continued

• Best Case Service provider provides SIP

enabled residential gateway or adapter or all phones are STUN enabled – very low server bandwidth needs

• Current pragmatic option Use intelligent NAT detection in

server – 2Mbps serves 3100 subscribers ($6.45 per sub)

• Worst case Service Provider relies on purely

RTP relay approach – 2Mbps serves 650 subs ($30.75 per sub)

© ETphones.com Ltd 2004. All rights reserved. www.purplepacket.com

SIP Server

• Most SIP server vendors had to change strategy - server alone was not saleable during hard times

• Now just seen as an essential commodity - part of a wider portfolio (eg as a key part of a systems

integration activity or applications offering)

• Performance should still be viewed as a differentiator

© ETphones.com Ltd 2004. All rights reserved. www.purplepacket.com

Conferencing & media servers

• 3 Basic Choices: “Carrier class” hardware

based solutions – typically a partnership between media server and apps company

Software only – runs on standard platforms – big benefit is scalability and economic price points

Open source products – experience to date suggests some way to go on quality

© ETphones.com Ltd 2004. All rights reserved. www.purplepacket.com

Other Applications

• Big thrust is presence and collaboration aka Openscape, Windows Messenger etc Disappointingly few presence

based services out there at the moment other than the traditional ones (non SIP) and specific enterprise product rollouts.

• SMS ringback Easy to do with SIP

© ETphones.com Ltd 2004. All rights reserved. www.purplepacket.com

Marketing

• Most important driver of business success & very cash dependant Vonage advertising on TV in USA

• Estimate 250k customers by end 2004, 1m by 2006. Just raised $35m

Free World Dial Up• Approx 125k? subs. Uses resources

of pulver.com. Free PSTN calls promotions

© ETphones.com Ltd 2004. All rights reserved. www.purplepacket.com

Dollars

• ITSP setup costs €40 - €60 per subscriber in first year (assumes own hosting)

• For an ISP typical delta revenues of €8 a month brings fast recovery of investment

© ETphones.com Ltd 2004. All rights reserved. www.purplepacket.com

© ETphones.com Ltd 2004. All rights reserved. www.purplepacket.com

Conclusions

• 2004 is the year SIP companies start making profit

• Service Providers everywhere coming off the fence – often against their will.

• With basic infrastructure in place road is clear to start taking advantage of what SIP can really offer