© 2011 financial operations networks llc unclaimed property: avoid escheatment hassles &...

TRANSCRIPT

© 2011 Financial Operations Networks LLC

Unclaimed Property: Avoid Escheatment Hassles

& Headaches!Carla T. McGlynnUnclaimed Property Consulting & Reporting LLC

Tuesday, April 12, 2011

www.TheAPNetwork.com Page 2

THE ACCOUNTS PAYABLE

Leadership ConferenceObjectives

• Brief overview of unclaimed property fundamentals & compliance responsibilities

• Case studies —Accounting decision—Successor liability

• Practical suggestions for policy, procedure, and process establishment and improvement

• Takeaway – current state audit and legislative trends

www.TheAPNetwork.com Page 3

THE ACCOUNTS PAYABLE

Leadership ConferenceUP FundamentalsUnclaimed property is property that is held, issued or owing in the ordinary course of business and has remained unclaimed by the apparent owner for a specified period of time.

Wages, Payroll, Salary & Commissions

Disbursement Checks (Including Voids & Stop-Pays) Vendor Checks & Customer Refund Employee Travel & Expense Employee Benefit & Health

Suspense Accounts Unapplied Cash Unidentified Receipts

Rebates

Accounts Receivable Credit Balances Credit Memos Pre-pay Accounts Deposits

Third Party Administrated Accounts Equity Related Items

Stocks Bonds Dividends

Successor Liability - Acquisitions

Common Property Types

www.TheAPNetwork.com Page 4

THE ACCOUNTS PAYABLE

Leadership Conference

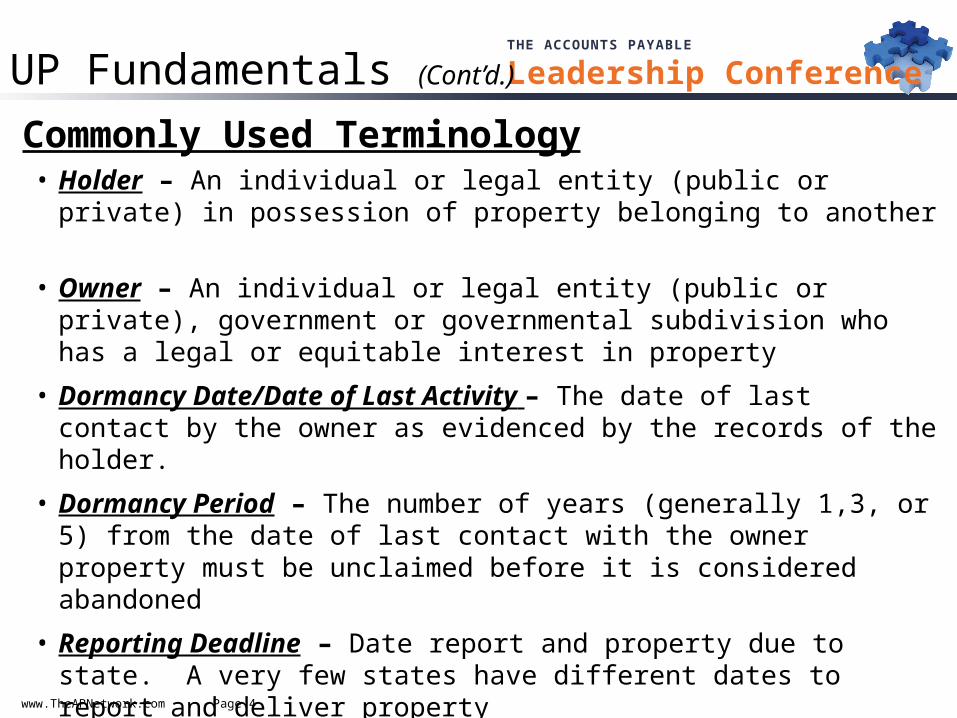

Commonly Used Terminology• Holder – An individual or legal entity (public or private) in possession of

property belonging to another

• Owner – An individual or legal entity (public or private), government or governmental subdivision who has a legal or equitable interest in property

• Dormancy Date/Date of Last Activity – The date of last contact by the owner as evidenced by the records of the holder.

• Dormancy Period – The number of years (generally 1,3, or 5) from the date of last contact with the owner property must be unclaimed before it is considered abandoned

• Reporting Deadline – Date report and property due to state. A very few states have different dates to report and deliver property

• Indemnification – Refers to the protection from subsequent claims (whether made by an owner or by another state) that may be provided by a state to a holder that remits property to a state

UP Fundamentals (Cont’d.)

www.TheAPNetwork.com Page 5

THE ACCOUNTS PAYABLE

Leadership Conference

Holder obligations & responsibilities• Records review

—Internal review & research—Determining eligibility for reporting—Applying the applicable state law—Determining the dormancy period

• Due diligence

• Reporting and remitting

• Retaining supporting records

UP Fundamentals (Cont’d.)

www.TheAPNetwork.com Page 6

THE ACCOUNTS PAYABLE

Leadership Conference

Internal review & research• Conduct a review of the appropriate financial

accounts and ledgers to identify accounts holding items subject to escheat

• Accounts to review:—AP disbursement: (ie. vendor, customer refund, travel

& expense, and TPA checks)—Payroll disbursement —AR aged trial balance

UP Fundamentals (Cont’d.)

www.TheAPNetwork.com Page 7

THE ACCOUNTS PAYABLE

Leadership Conference

Determining eligibility for reporting• Records review

—Identifying unclaimed property• Is the owner really lost?• Is the property really unclaimed?• Is the property exempt from reporting?

UP Fundamentals (Cont’d.)

www.TheAPNetwork.com Page 8

THE ACCOUNTS PAYABLE

Leadership ConferenceBe Proactive!!!

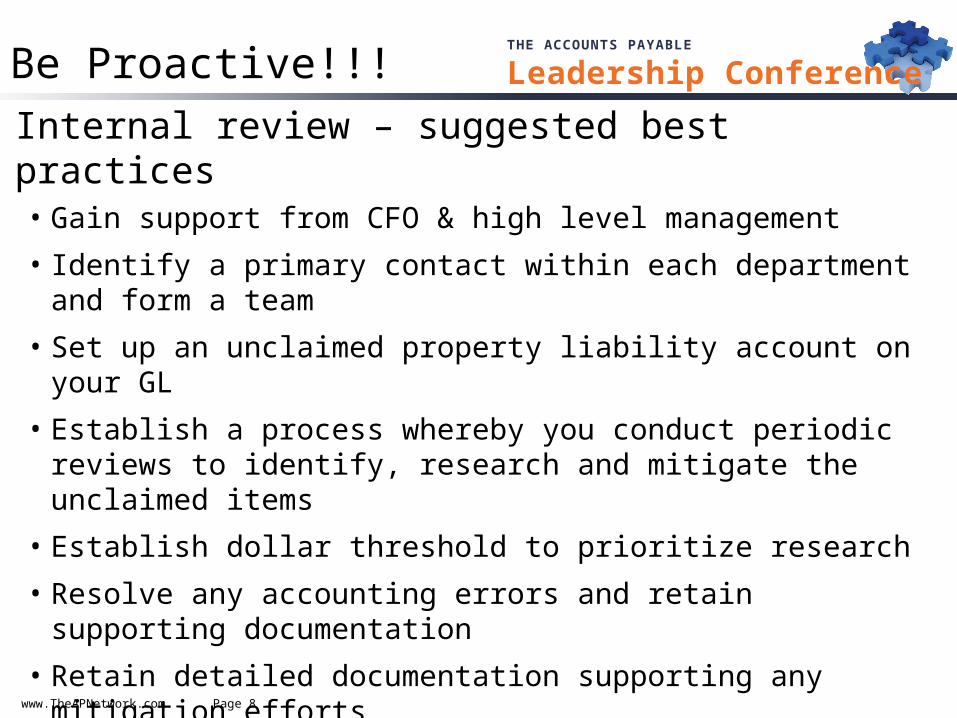

Internal review – suggested best practices• Gain support from CFO & high level management

• Identify a primary contact within each department and form a team

• Set up an unclaimed property liability account on your GL

• Establish a process whereby you conduct periodic reviews to identify, research and mitigate the unclaimed items

• Establish dollar threshold to prioritize research

• Resolve any accounting errors and retain supporting documentation

• Retain detailed documentation supporting any mitigation efforts

• Maintain written procedures for record review and make them a part of your company’s policy or manual

www.TheAPNetwork.com Page 9

THE ACCOUNTS PAYABLE

Leadership Conference

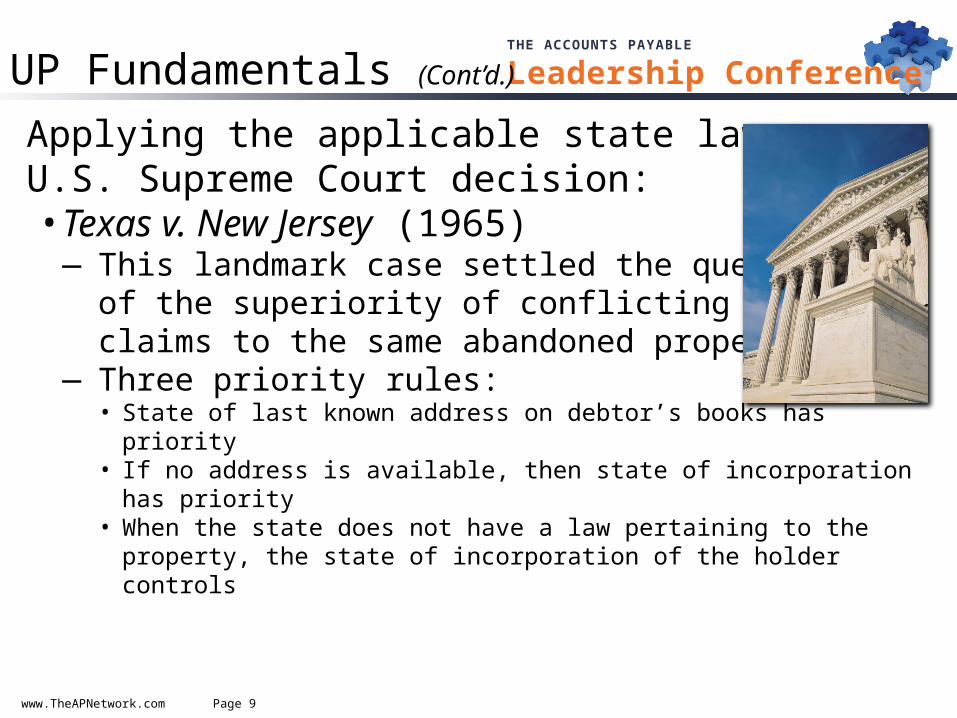

Applying the applicable state lawU.S. Supreme Court decision:• Texas v. New Jersey (1965)

—This landmark case settled the questionof the superiority of conflicting state claims to the same abandoned property

—Three priority rules:• State of last known address on debtor’s books has priority• If no address is available, then state of incorporation has priority• When the state does not have a law pertaining to the property, the state of

incorporation of the holder controls

UP Fundamentals (Cont’d.)

www.TheAPNetwork.com Page 10

THE ACCOUNTS PAYABLE

Leadership Conference

StateAP – Vendor

Checks (CK13/ MS08)

PayrollChecks(MS01)

Credit Balances(MS09)

Annual Reporting Deadline

As of/End Date

Illinois 3 years 1 year 3 years 5/01 12/31

California 3 years 1 year 3 years 11/01 06/30

Delaware 5 years 5 years 5 years 03/01 12/31

Florida 5 years 1 year 5 years 04/30 12/31

New York3 years

(2G)3 years

(8A) 3 years

(5E) 3/10 12/31

Michigan ** 3 years 1 year 3 years 7/01 03/31

Texas 3 years 1 year 3 years 11/01 06/30

** Recent Legislative Change for 2011 and forward

State dormancy periods & reporting deadlines

UP Fundamentals (Cont’d.)

www.TheAPNetwork.com Page 11

THE ACCOUNTS PAYABLE

Leadership Conference

Due diligence• Final effort to contact and reunite the owner/payee

with its property prior to reporting and remitting the unclaimed property to the applicable state

• Compliance requirement in all jurisdictions, except DE & PA

• Benefits:—Opportunity to reestablish

relationship with lost vendors & customers

—Create goodwill—Reduce escheatable property

to states

UP Fundamentals (Cont’d.)

www.TheAPNetwork.com Page 12

THE ACCOUNTS PAYABLE

Leadership Conference

Due diligence (Cont’d.)

Important considerations• Method of notification – generally, a notification

letter is mailed to the owner at the last known address on the holder’s records —First Class mail, Certified mail and/or publication

• Letter content – generally, the letter should include enough information to enable the recipient to verify the status of the property —check number, check amount, and check date—description of property—communicate to owner that it appears he/she is entitled

to the property & that it is at risk of being escheated to the state

—owner response instructions (preferably in writing)

UP Fundamentals (Cont’d.)

www.TheAPNetwork.com Page 13

THE ACCOUNTS PAYABLE

Leadership Conference

Payee Name,CompanyStreet AddressCity, State Zip

Dear Payee:

Our records indicate that your company may be the owner of property or have an interest in funds represented by the items listed below. No transaction or other activity has occurred for a significant period of time. If you have an interest in the funds and wish to prevent the funds from being reported and remitted as unclaimed property to the State of ________, please indicate the disposition of the items listed below. After you complete the form, please fax it to us immediately at XXX-XXX-XXXX or mail it to us in the enclosed self-addressed envelope. Please reply by __________.

Nature of FundsDate Issued Amount Description/Reference

Check #XXXX XX/XX/XX $XXXX Invoice No. XXX-

Disposition of Items (Check the blank next to one of the following.)

____ The above check was cashed on ________.

____ Check was received but not cashed. (If you still possess the check, please return it/them along with this letter indicating if you are still entitled to these funds.

____ Check is no longer required. There are no outstanding invoices for this amount and the obligation has been satisfied.

____ This check was not received and our records indicate the amount is still due. Please issue another check.

____ Other: ____________________________________________________________________________________________

Name: ___________________________ Signature:________________________________

Address (if different from above)__________________________________________

SSN/Federal ID No. __________________________________ Date: _____________

Sincerely,

Sample Due Diligence Letter

UP Fundamentals (Cont’d.)

www.TheAPNetwork.com Page 14

THE ACCOUNTS PAYABLE

Leadership ConferenceUP Fundamentals (Cont’d.)

Due diligence (Cont’d.)

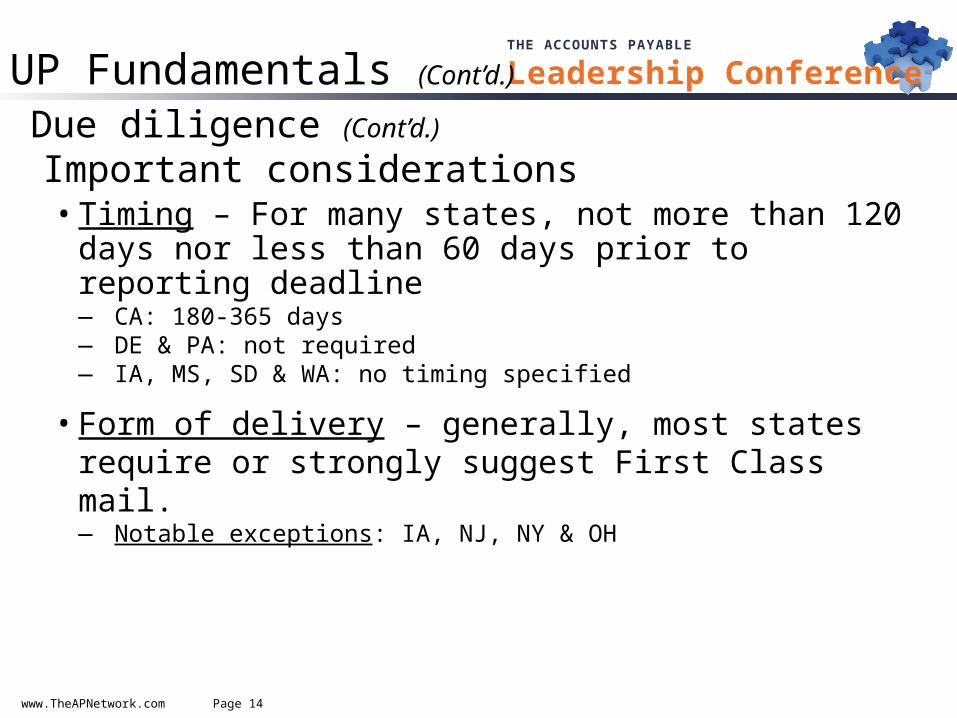

Important considerations• Timing – For many states, not more than 120 days nor less

than 60 days prior to reporting deadline— CA: 180-365 days — DE & PA: not required — IA, MS, SD & WA: no timing specified

• Form of delivery – generally, most states require or strongly suggest First Class mail.— Notable exceptions: IA, NJ, NY & OH

www.TheAPNetwork.com Page 15

THE ACCOUNTS PAYABLE

Leadership ConferenceUP Fundamentals (Cont’d.)

Due diligence (Cont’d.)

Important considerations• Thresholds:

— Minimums: by Item Amount/Value • $50: most States• Notable other states: $10 – IL; $25 – NE; $75 – WA; $100 – AK, KS, KY, MA, MD,

MN, OR, VA; $250 – TX • No minimum: AL, CT, IA, MS, NE, NY, PR

• Allowable deductions:— CA: banks and financial organizations may impose a service charge for the notice

in an amount not to exceed $2.00 on items over $50— DE & PR: may deduct expenses incurred for advertising — IL, IA, OH: may deduct first class mailing costs (i.e. postage, stationary,

and envelopes)— NV: limit $2.00 may be deducted on items over $50 and must be itemized

on report — NY: may deduct cost of certified mail and return receipt as a service charge. Also,

may deduct costs of publication on a pro rata basis (using a specified formula.)— OH: deductions are allowed up to $20.00 for certified mail

www.TheAPNetwork.com Page 16

THE ACCOUNTS PAYABLE

Leadership ConferenceUP Fundamentals (Cont’d.)

Reporting and remittingImportant processing considerations• Type of report – most states accept diskette or CD, online

internet reporting (mandatory – IN)

• Report format – most states accept NAUPA II standard electronic format. NY does not use NAUPAII format, but will accept. CA now accepts only NAUPA II format

• Negative reporting – required by many states (29). IN and OH allow online negative reporting

www.TheAPNetwork.com Page 17

THE ACCOUNTS PAYABLE

Leadership ConferenceUP Fundamentals (Cont’d.)

Reporting and remitting (Cont’d.)

Important processing considerations• Report Aggregate Limits – most states allow holders

to report items in aggregate if value is below a certain dollar amount— $25, $50, & $100 are typical limits— Most states do not permit aggregate reporting of dividends or

mineral interests

• Form of Remittance – checks or EFT— Most states accept checks. Some states require EFT if sum

of reportable property is greater than a specific dollar amount (i.e. CA, TX)

www.TheAPNetwork.com Page 18

THE ACCOUNTS PAYABLE

Leadership ConferenceUP Fundamentals (Cont’d.)

Reporting and remitting (Cont’d.)

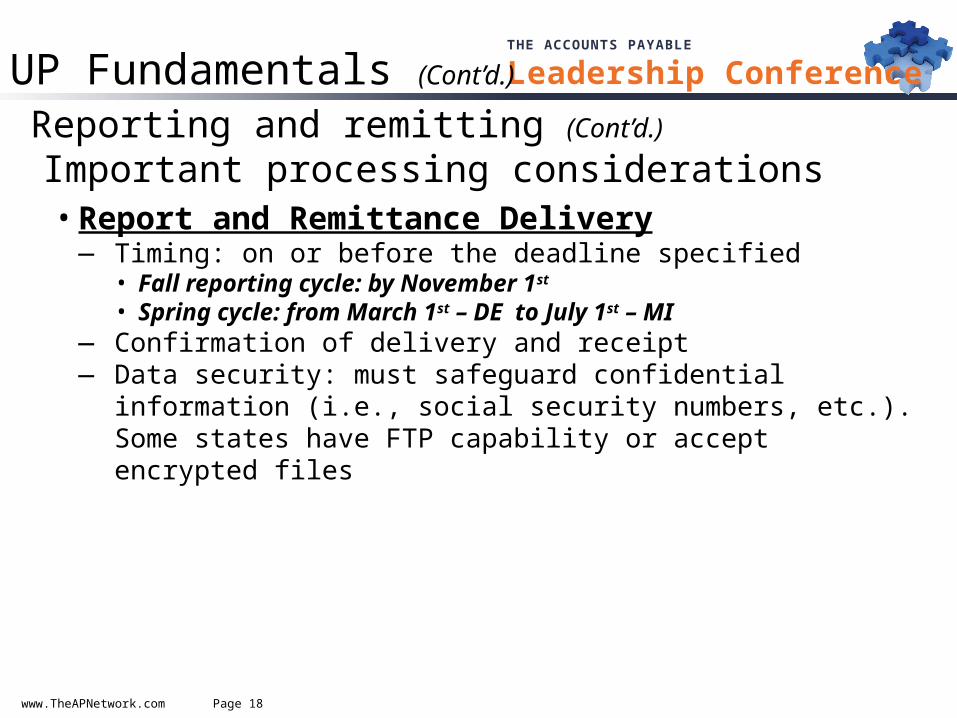

Important processing considerations• Report and Remittance Delivery

— Timing: on or before the deadline specified• Fall reporting cycle: by November 1st

• Spring cycle: from March 1st – DE to July 1st – MI— Confirmation of delivery and receipt— Data security: must safeguard confidential information (i.e., social

security numbers, etc.). Some states have FTP capability or accept encrypted files

www.TheAPNetwork.com Page 19

THE ACCOUNTS PAYABLE

Leadership ConferenceUP Fundamentals (Cont’d.)

Reporting and remitting (Cont’d.)

Important processing considerations• Filing extensions

— Notification/request of state administrator• Request made via holder letterhead• State provided forms – some states forms available on state websites

— Provide reason for request— Estimated payment may be required (i.e. NY, NJ, TX)

www.TheAPNetwork.com Page 20

THE ACCOUNTS PAYABLE

Leadership ConferenceReporting Red Flags!

Prevention tips: Report All Property Types when it is reportable! Prepare and complete all forms correctly and accurately! Sign and date the reports! Have them notarized, if required! Confirm report totals and payment match! File negative reports—only if required! Don’t wait to the last minute to request a filing

extension (best to allow 15 to 30 days prior to the filing deadline)! Confirm receipt with states, maintain document in one location

and create a calendar File reports by the new granted report due date

Complete all state unique report forms (i.e. holders information forms)!

www.TheAPNetwork.com Page 21

THE ACCOUNTS PAYABLE

Leadership Conference

Retaining supporting records & documentation• States require retention of unclaimed property report(s) and

supporting documentation for a period of years— Time period differs by state—usually 7 to 10 years

• Provides indemnification for property remitted and proof of claim

• Critically important in the event of audit• Records retained should include, but not limited to:

— Copies of the annual state unclaimed property reports— Supporting detail of property reported by legal entity— Copies of all due diligence letter responses and actions taken as a

result of the responses— Primary source documentation, including: GL reports, bank

statements, bank reconciliations, outstanding check lists, void/stop pay lists, aged trial balance reports and reconciliation reports

UP Fundamentals (Cont’d.)

www.TheAPNetwork.com Page 22

THE ACCOUNTS PAYABLE

Leadership Conference

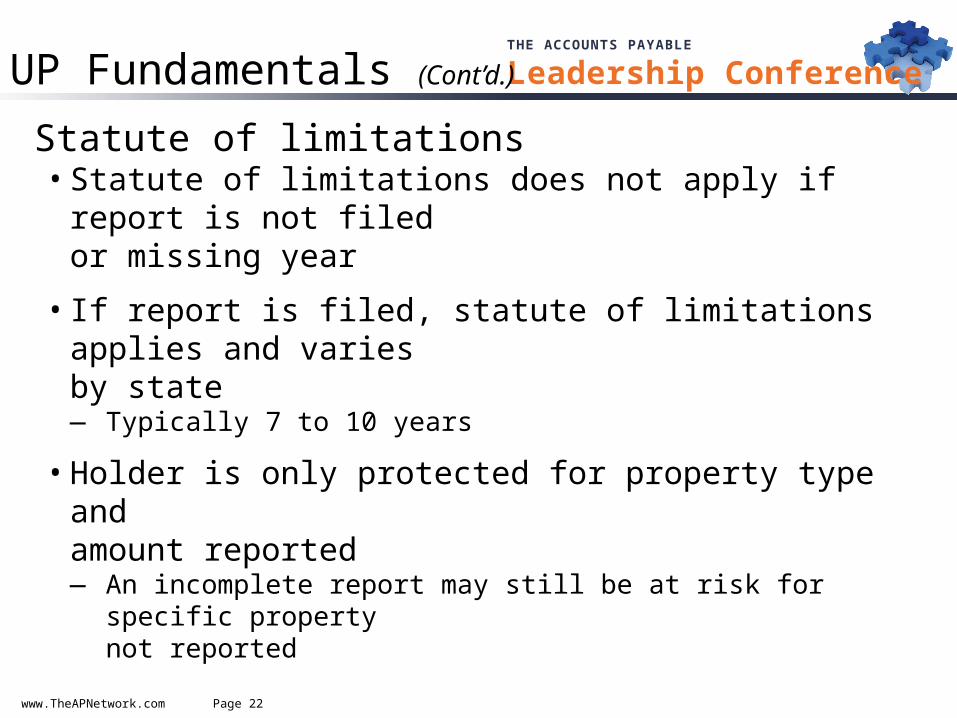

Statute of limitations• Statute of limitations does not apply if report is not filed

or missing year

• If report is filed, statute of limitations applies and varies by state— Typically 7 to 10 years

• Holder is only protected for property type and amount reported— An incomplete report may still be at risk for specific property

not reported

UP Fundamentals (Cont’d.)

www.TheAPNetwork.com Page 23

THE ACCOUNTS PAYABLE

Leadership ConferenceCase Study: Accounting Decision

Scenario:• Cash Management (CM) is responsible for reconciling monthly

bank reconciliations for accounts payable disbursements• CM identifies numerous stale-dated checks each month• CM maintains stale-dated check listing on bank account for

several years back to 2002, totaling more than $150,000• CM advises upper management of the accumulation

of checks• Manufacturer has never reported unclaimed property to states

What does management decide to do? Let’s find out…

www.TheAPNetwork.com Page 24

THE ACCOUNTS PAYABLE

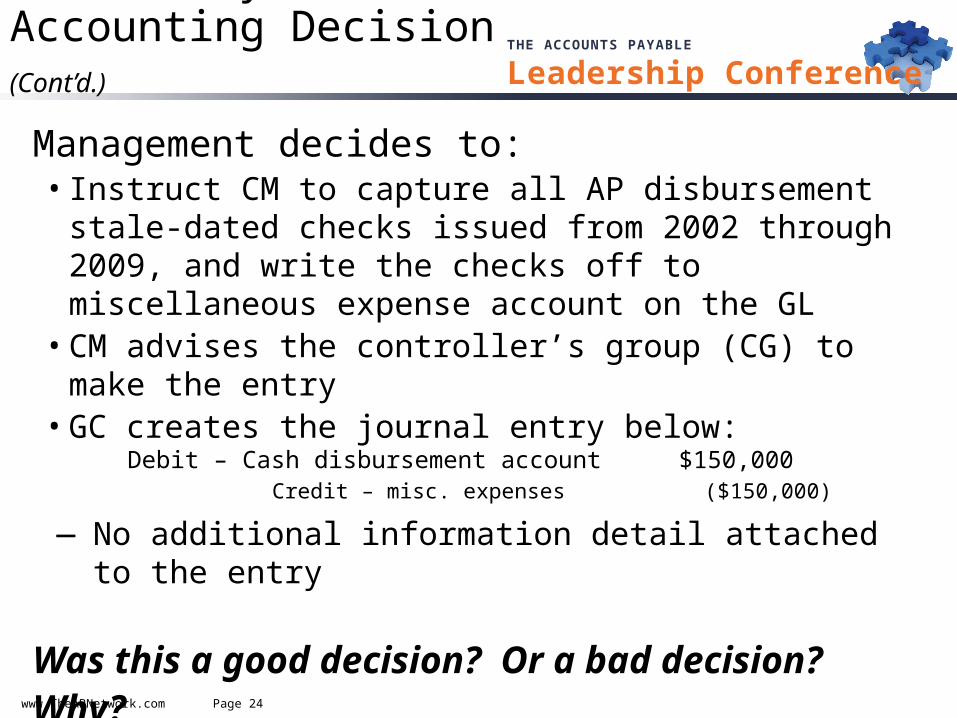

Leadership ConferenceCase Study: Accounting Decision (Cont’d.)

Management decides to:• Instruct CM to capture all AP disbursement stale-dated

checks issued from 2002 through 2009, and write the checks off to miscellaneous expense account on the GL

• CM advises the controller’s group (CG) to make the entry• GC creates the journal entry below:

Debit – Cash disbursement account $150,000Credit – misc. expenses ($150,000)

― No additional information detail attached to the entry

Was this a good decision? Or a bad decision? Why?

www.TheAPNetwork.com Page 25

THE ACCOUNTS PAYABLE

Leadership Conference

Capture the detail and have a journal entry made to reclass the property to an unclaimed liability account

Retain all of the check detail for future research and due diligence efforts

Research checks for name and addressConduct research of all state dormant checks for

ultimate dispositionProcess statutory due diligenceReport all unclaimed property to appropriate states

when due

The better decision…

Case Study: Accounting Decision (Cont’d.)

www.TheAPNetwork.com Page 26

THE ACCOUNTS PAYABLE

Leadership ConferenceCase Study: Successor Liability

Scenario:• Retailer acquires the stock of a distribution business

(Distributor) that has been doing business for over 15 years nationwide

• Distributor has never reported unclaimed property to states• Retailer rolls in the distributor’s AP processing into its

accounting process, including disbursements• Retailer identifies a significant population of outstanding

checks on the distributor’s old bank statement• Retailer closes the bank account and writes-off checks for

the entire outstanding bank balance to misc. income

Does the retailer have Successor Liability? YES!!

www.TheAPNetwork.com Page 27

THE ACCOUNTS PAYABLE

Leadership Conference

How should the retailer handle this matter?• Meets its reporting responsibilities

― Review and research― Due diligence― Report― Retain records

• If the liability is significant, consider filing a voluntary disclosure (VDA) effort with applicable states

• Conduct a review of the retailer’s financial operations to determine if there are any additional potential underreported liabilities on its accounts

Case Study: Successor Liability (Cont’d.)

www.TheAPNetwork.com Page 28

THE ACCOUNTS PAYABLE

Leadership ConferenceConsider a VDA

• Ability to perform self-review of financial issues and methodologies to employ

• Limited “look-back” period

• Waiver/reduction of interest and/or penalty

• Obtain closing/release agreement

• Understand and address areas of risk & weakness in compliance process

VDA Benefits:

www.TheAPNetwork.com Page 29

THE ACCOUNTS PAYABLE

Leadership ConferenceInitiating Voluntary Compliance Efforts• Formal vs. informal

― Formal VDA terms provide:• Limited look-back, completion time (6 months), penalty and/or interest

abatement/reduction and indemnification

• Holders eligible to participate, if:— Not under audit or contacted by state or a third-party auditor— Not previously reported or omitted/underreported property

• VDA look-back period— Generally between 5 to 10 report years (plus dormancy period), varies

by state

• vs. audit look-back period— Generally between 10 to 20+ report years (plus dormancy period); date of

incorporation; varies by state; audits are lengthy, time consuming, burdensome and intrusive

www.TheAPNetwork.com Page 30

THE ACCOUNTS PAYABLE

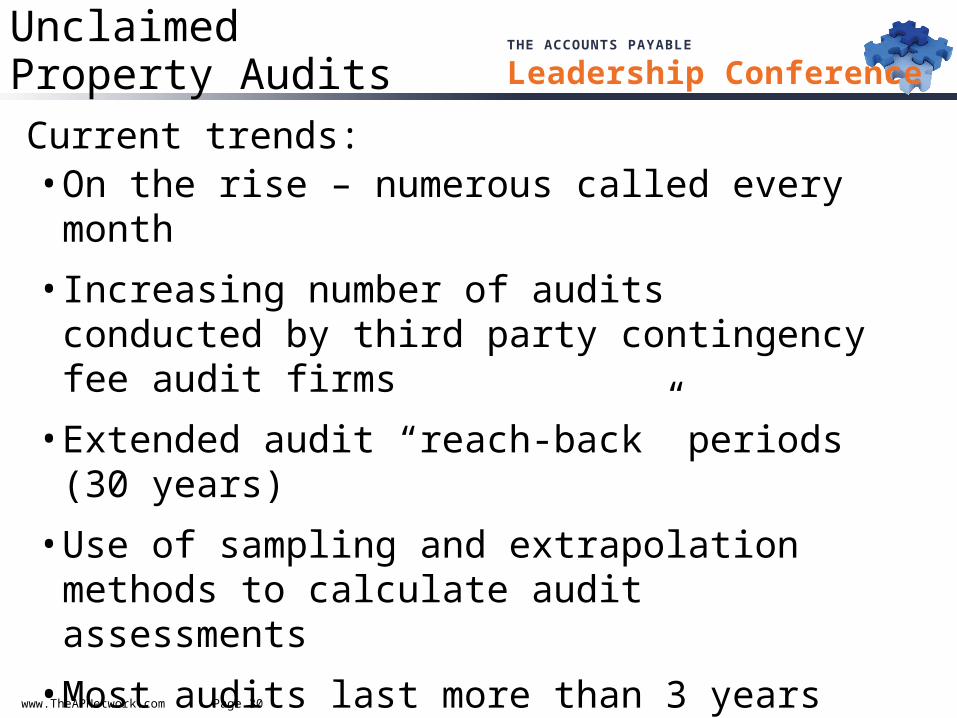

Leadership ConferenceUnclaimedProperty AuditsCurrent trends:• On the rise – numerous called every month

• Increasing number of audits conducted by third party contingency fee audit firms

• Extended audit “reach-back” periods (30 years)

• Use of sampling and extrapolation methods to calculate audit assessments

• Most audits last more than 3 years

• Multi-million dollar assessments

• Holders charged for audit costs (i.e. IN)

www.TheAPNetwork.com Page 31

THE ACCOUNTS PAYABLE

Leadership ConferenceMitigate Risk

Establish Effective

Escheat Processes

www.TheAPNetwork.com Page 32

THE ACCOUNTS PAYABLE

Leadership Conference

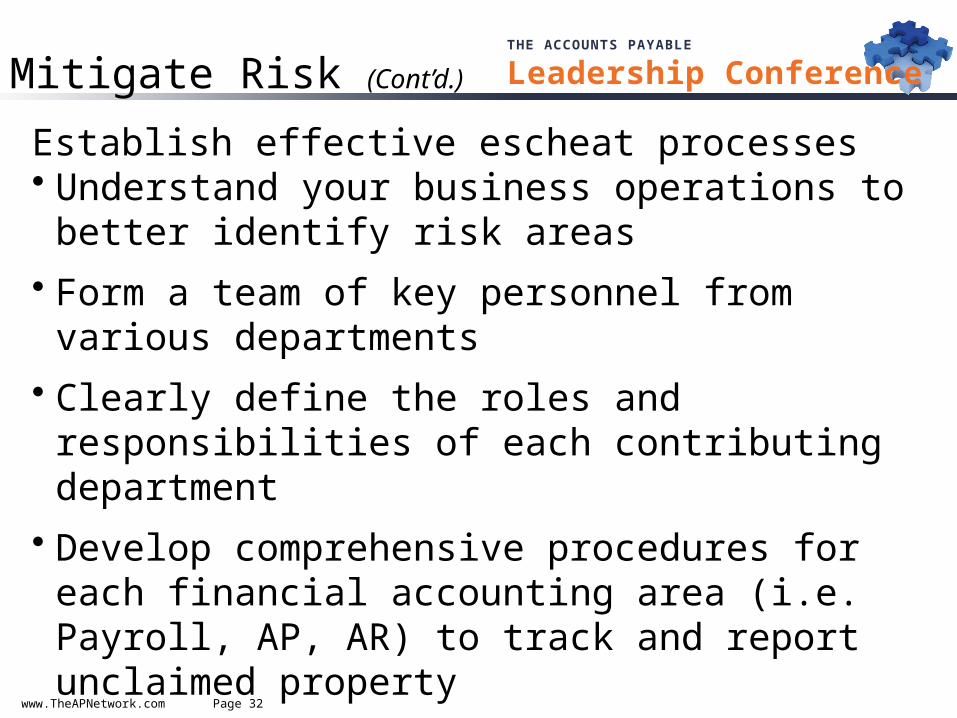

Establish effective escheat processes • Understand your business operations to better

identify risk areas

• Form a team of key personnel from various departments

• Clearly define the roles and responsibilities of each contributing department

• Develop comprehensive procedures for each financial accounting area (i.e. Payroll, AP, AR) to track and report unclaimed property

Mitigate Risk (Cont’d.)

www.TheAPNetwork.com Page 33

THE ACCOUNTS PAYABLE

Leadership Conference

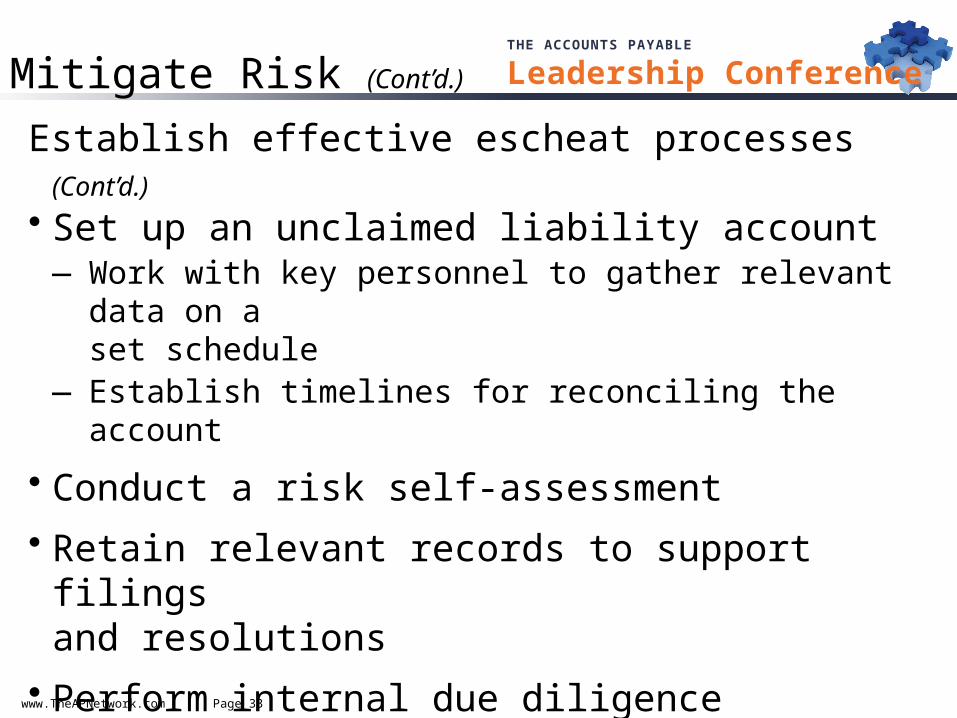

Establish effective escheat processes (Cont’d.) • Set up an unclaimed liability account

― Work with key personnel to gather relevant data on a set schedule

― Establish timelines for reconciling the account

• Conduct a risk self-assessment

• Retain relevant records to support filings and resolutions

• Perform internal due diligence routinely

• Perform statutory due diligence according to state statutory requirements

Mitigate Risk (Cont’d.)

www.TheAPNetwork.com Page 34

THE ACCOUNTS PAYABLE

Leadership Conference

Establish effective escheat processes (Cont’d.)

• Test your procedures annually to ensure continued effectiveness

• Perform a high level liability risk assessment of acquisitions (successor liability – it’s your headache now!)

• If underreported property is identified to state(s), consider voluntary compliance

• Encourage the direct deposit, EFT’s, wires and alternative forms of payments

Mitigate Risk (Cont’d.)

www.TheAPNetwork.com Page 35

THE ACCOUNTS PAYABLE

Leadership Conference

Establish effective escheat processes (Cont’d.)

• Review and revise contractual language on invoices and POs that may support positions of no liability due

• Retain documentation relating to settlement agreements with customers

• Invest more time and resources in researching unidentified payments and suspense accounts

• State UP laws change frequently – check state websites for updates, join educational trade associations, reach out to an expert, etc.

Mitigate Risk (Cont’d.)

www.TheAPNetwork.com Page 36

THE ACCOUNTS PAYABLE

Leadership Conference

Recent Legislative Developments

www.TheAPNetwork.com Page 37

THE ACCOUNTS PAYABLE

Leadership ConferenceState Legislative Developments

• Delaware – law changes

• Michigan – spring filing state & dormancy period reductions

• Indiana – dormancy period reduction

• New York – dormancy period reduction

• New Jersey – gift card & other changes

www.TheAPNetwork.com Page 38

THE ACCOUNTS PAYABLE

Leadership Conference

Delaware – Legislative Changes in 2010• Administrative Review Process: Provide for an administrative review process at the

conclusion of an unclaimed property examination. This review process may be invoked at the option of the holder

• Limited Uninvoiced Payables (UIP) Exemption: Create a limited exemption from the definition of abandoned property for transactions between merchants covered by the Uniform Commercial Code where, for whatever reason, a merchant holder receives and accepts goods in the ordinary course of business for which the holder was never invoiced by the seller

• Estimation Techniques Authorized: Clarify that in accordance with established accounting and industry practice, the State may employ estimation techniques when records do not exist or are insufficient to determine a holder’s liability for abandoned or unclaimed property

• Reporting Date & Due Diligence Changes: Changed the reporting date for banking organizations to 11/10 from 8/1 (negative reports were 8/10) and for life insurance corporations to 12/20 from 5/1. Organizations that are required to publish notice are no longer required to publish a statement that the entity holds such reports for public inspection in their headquarters. Banking organizations are required to publish at least 60 days prior to reporting and remitting property

State Legislative Developments (Cont’d.)

www.TheAPNetwork.com Page 39

THE ACCOUNTS PAYABLE

Leadership Conference

Michigan – spring filing state & dormancy reductions• In 2011, property reaching dormancy as of March 31,

2011 must be remitted to Treasury by July 1, 2011

• Dormancy periods for most property types, including money orders, uncashed checks, and accounts receivable credit balances reduced to three years

• Michigan now requires negative reporting attestation form

State Legislative Developments (Cont’d.)

www.TheAPNetwork.com Page 40

THE ACCOUNTS PAYABLE

Leadership Conference

Indiana – dormancy period reductions • Savings, checking & timed deposits – 5 to 3 years

• AP and AR – 5 to 3 years

• Any other property types not specifically mentioned in the IN unclaimed property law – 5 to 3 years

• Effective – Fall 2011 report deadlines

State Legislative Developments (Cont’d.)

www.TheAPNetwork.com Page 41

THE ACCOUNTS PAYABLE

Leadership Conference

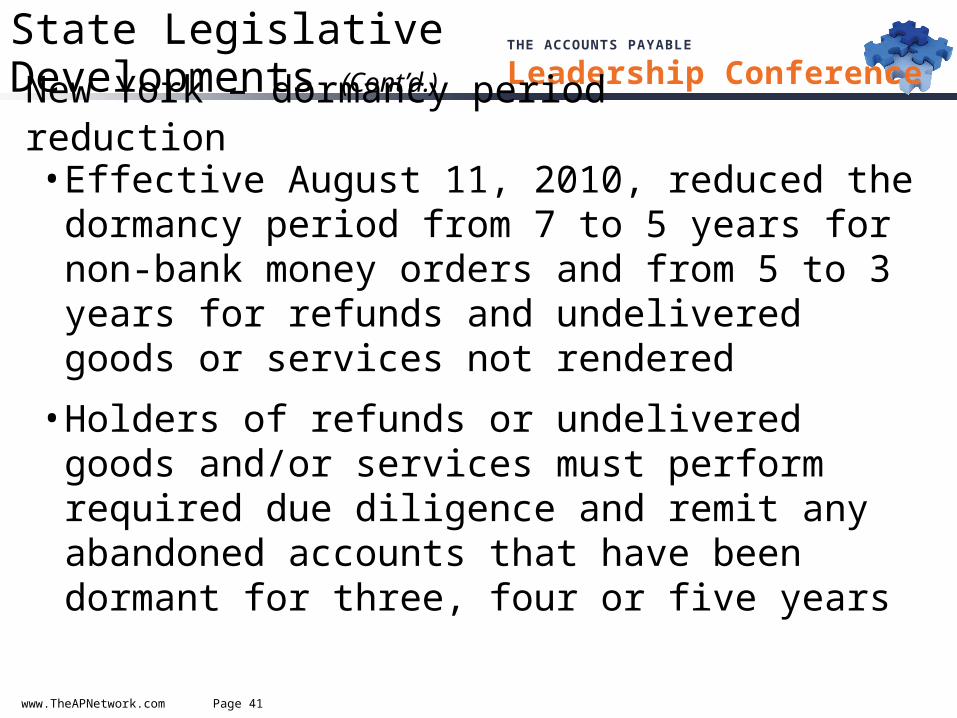

• Effective August 11, 2010, reduced the dormancy period from 7 to 5 years for non-bank money orders and from 5 to 3 years for refunds and undelivered goods or services not rendered

• Holders of refunds or undelivered goods and/or services must perform required due diligence and remit any abandoned accounts that have been dormant for three, four or five years

New York – dormancy period reduction

State Legislative Developments (Cont’d.)

www.TheAPNetwork.com Page 42

THE ACCOUNTS PAYABLE

Leadership Conference

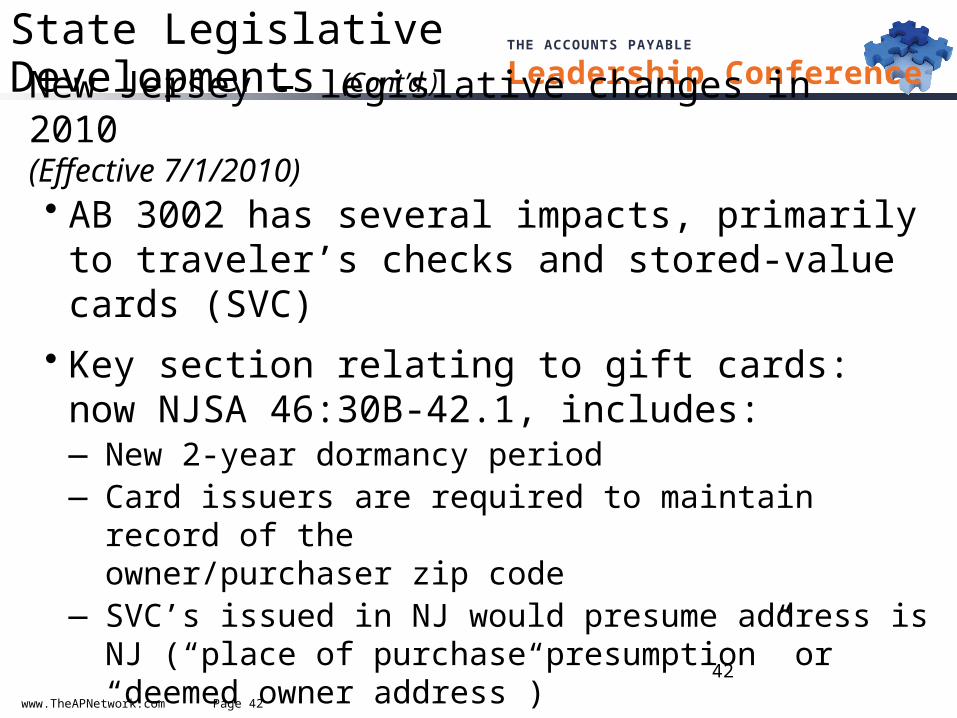

• AB 3002 has several impacts, primarily to traveler’s checks and stored-value cards (SVC)

• Key section relating to gift cards: now NJSA 46:30B-42.1, includes:― New 2-year dormancy period― Card issuers are required to maintain record of the

owner/purchaser zip code― SVC’s issued in NJ would presume address is NJ (“place

of purchase presumption” or “deemed owner address”)

42

New Jersey – legislative changes in 2010 (Effective 7/1/2010)

State Legislative Developments (Cont’d.)

www.TheAPNetwork.com Page 43

THE ACCOUNTS PAYABLE

Leadership Conference

New Jersey – SVC legal progress continues into 2011• During Sept. to Oct 2010 various groups/retail associations sued NJ in

U.S. District Court seeking enjoinment of law• Nov. 13, 2010 – Judicial Decision

― NJ enjoined from enforcing the “place of purchase” presumption, which violates Priority Rules in Texas line of U.S. Supreme Court cases

― NJ enjoined from escheating cards that were sold before enactment of AB 3002, but only if those cards are redeemable solely for merchandise/services (contract was for merchandise/services, and “lost profit” argument applies)

• Jan. 14, 2011 – the judge issues judicial opinion that clarifies Nov. 13, 2010 opinion—New Jersey can require card issuer to collect zip code of card owner/purchaser

• Jan. 19, 2011 – the Nov. 13, 2010 decision is on appeal to Third Circuit• Jan. 31, 2011 – Third Circuit Enjoins Enforcement of NJ zip code

collection requirement

State Legislative Developments (Cont’d.)

www.TheAPNetwork.com Page 44

THE ACCOUNTS PAYABLE

Leadership Conference

Unclaimed Property Resources – Websites and Links• Unclaimed Property Professionals Organization

(UPPO): www.uppo.org

• National Association of Unclaimed Property Administrators (NAUPA): www.unclaimed.org

• NAUPA II Standard Reporting Format: http://www.nast.org/NAUPA/Electronicreportstandard.htm (click on “new reporting standard”)

Resources

© 2011 Financial Operations Networks LLC

Thank You!

If you have further questions:

Carla McGlynnPartnerUnclaimed Property Consulting & Reporting LLC(732) [email protected]