© 2011 financial operations networks llc the power of e-payments! harness it now! david w. hay...

TRANSCRIPT

© 2011 Financial Operations Networks LLC

The Power of e-Payments! Harness It Now!

David W. HayFinancial Operations Networks

Tuesday, April 12, 2011

www.TheAPNetwork.com Page 2

THE ACCOUNTS PAYABLE

Leadership ConferenceA Word About Checks

• Checks have their roots in the bill of exchange which has been in use for centuries

• The earliest checks were issued in the U.K. in the early 1700s

www.TheAPNetwork.com Page 3

THE ACCOUNTS PAYABLE

Leadership ConferenceChecks

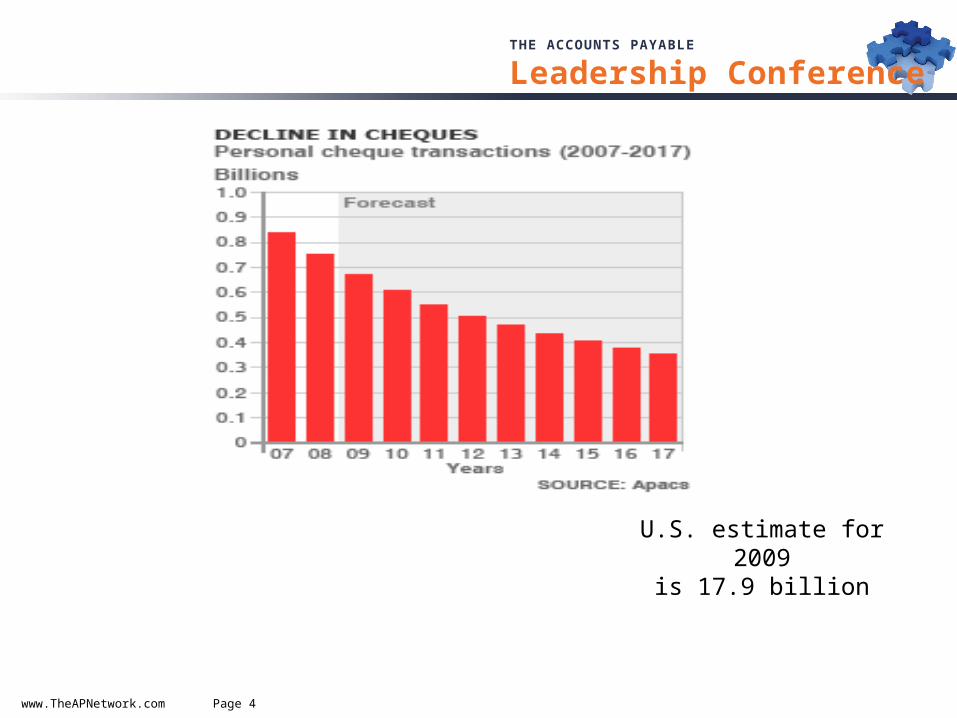

• However, it is almost time to say “RIP” to checks – at least in the U.K.

• The U.K. plans to phase out personal checks by Oct. 31, 2018

• The U.S. still has a long way to go; with a GDP 6.5 times larger than the U.K., the U.S. issues 28 times as many checks

www.TheAPNetwork.com Page 4

THE ACCOUNTS PAYABLE

Leadership Conference

U.S. estimate for 2009is 17.9 billion

www.TheAPNetwork.com Page 5

THE ACCOUNTS PAYABLE

Leadership Conferencee-Payments

Key reasons for switching to e-payments:• Discount recovery

— Ability to offer dynamic discounting

• Cost— As check volume declines, unit processing costs rise

• Fraud prevention—Millions of paper checks are “intercepted” each year

www.TheAPNetwork.com Page 6

THE ACCOUNTS PAYABLE

Leadership Conference

• e-payments include:― Credit and debit cards― Portal systems such as PayPal and CheckFree― ACH payments― Wire payments― Cross-border payments― And soon your phone, iPad, etc.

e-Payments (Cont’d.)

www.TheAPNetwork.com Page 7

THE ACCOUNTS PAYABLE

Leadership Conference

www.TheAPNetwork.com Page 8

THE ACCOUNTS PAYABLE

Leadership Conference

www.TheAPNetwork.com Page 9

THE ACCOUNTS PAYABLE

Leadership ConferenceP-Cards

Card providers are beginning to offer new and effective

payment methods

www.TheAPNetwork.com Page 10

THE ACCOUNTS PAYABLE

Leadership ConferenceCard Types

• Procurement card―Can be physical or ghost card

• T&E cards―Used for travel – usually physical

• Fleet cards―Used specifically for fleet management

• One card―Combines the functions of a procurement and a

travel card

www.TheAPNetwork.com Page 11

THE ACCOUNTS PAYABLE

Leadership ConferenceBasic Card Information from Merchants• Level 1

― Similar to personal card, • Date, supplier and total amount

• Level 2― Includes level 1 data plus

• Sales tax• Variable data field that includes an order number and employee name

• Level 3 – line item detail― Includes level 1 and 2 data plus

• Product number• Quantity• Unit of measure• Product description• Price

www.TheAPNetwork.com Page 12

THE ACCOUNTS PAYABLE

Leadership ConferenceProcurement Card • Benefits

― Introduced in the early 1990s as a feature to reduce the amount of low-value invoices

― Many companies report that the average savings using a p-card is in excess of 50% per transaction

• Card-issuing banks charge vendors a per transaction fee on card purchases averaging 2%–2.5%

• Issues― Cultural change is an important factor in successfully

implementing a p-card program― Most companies do not allow use of a p-card to purchase

hazardous materials, capital equipment or for personal charges― Suppliers need to have an agreement with a merchant

service company

www.TheAPNetwork.com Page 13

THE ACCOUNTS PAYABLE

Leadership ConferenceGhost Card or AP Card• A ghost card is a single card that can be used by

multiple users

• The number is given to a single supplier, or multiple suppliers with similar NAICS codes

• The requestors do not know the account number, reducing the chance of fraud and misuse

• No physical card exists

• Monitoring and control resides with the department responsible for the account

www.TheAPNetwork.com Page 14

THE ACCOUNTS PAYABLE

Leadership ConferenceP-Card as aPayment Method

The merchant charges the p-card for the transaction and then creates and mails an invoice marked as paid• Benefits

— Payment cost reduced— Reduced chance of check fraud— Level 2 and 3 data not required

• However!— Care must be taken that the invoice is not paid twice— Invoice must contain CC or Credit Card in the “Terms” box on

the invoice— May still require merchant service provider

www.TheAPNetwork.com Page 15

THE ACCOUNTS PAYABLE

Leadership Conference

www.TheAPNetwork.com Page 16

THE ACCOUNTS PAYABLE

Leadership ConferenceBuyer InitiatedPayments (BIP)New offering from credit card issuers completely reverses the normal card transaction flow• In a normal card transaction, the card holder

presents his card to the supplier who initiates the payment process as soon as the card is “swiped”

• With BIP, the buyer initiates the payment which is electronically remitted to the supplier

• Supplier does not need a point of sale terminal

www.TheAPNetwork.com Page 17

THE ACCOUNTS PAYABLE

Leadership Conference

• Benefits― Supplier receives payment usually within 48 hours from invoice approval― Buyer benefits from float― Rebate potential for the buyer― Lower cost than a check― No card number is given to the supplier for the ultimate in security― Buyer can use one provider for traditional p-card, e-payments and

payables financing― Normal invoice approval process still applies― Benefit from online payment status and reporting portal― Complete remittance data is passed to supplier― Most providers help or completely conduct vendor enrollment― Some providers offer selective acceptance so a supplier is not forced

to accept this form of payment from all of their buyers

Buyer InitiatedPayments (BIP) (Cont’d.)

www.TheAPNetwork.com Page 18

THE ACCOUNTS PAYABLE

Leadership ConferenceACH Payment Documents• CCD+

―Cash Concentration and Disbursements plus Addenda Entry• Commonly used for business transactions• Has an 80-character addenda record

• CTX―Corporate Trade Exchange

• Contains complete RA details

• PPD―Prearranged Payment or Deposit

• Primary consumer-to-business transaction

www.TheAPNetwork.com Page 19

THE ACCOUNTS PAYABLE

Leadership ConferenceACH Volumes

www.TheAPNetwork.com Page 20

THE ACCOUNTS PAYABLE

Leadership ConferenceACH Transactions

www.TheAPNetwork.com Page 21

THE ACCOUNTS PAYABLE

Leadership ConferenceEDI

• EDI systems can be used to send both remittance data to the supplier and the payment instructions to the bank

• Can handle all types of payment transactions including check, ACH, SWIFT, wire, etc.

• Key document used is the ANSI 820 which can act as both the Remittance Advice and the Payment Instruction

www.TheAPNetwork.com Page 22

THE ACCOUNTS PAYABLE

Leadership ConferenceInternet

• Banks― Banks offer Internet services on their own platforms or

through a service provider such as CheckFree

• Service providers― Such as Xign (now owned by JPMorgan Chase)― Trade card― EDI vans (for EDI payments)

www.TheAPNetwork.com Page 23

THE ACCOUNTS PAYABLE

Leadership ConferenceInternational Payments• Wire

― Similar to domestic wire• Higher priced, except if transmitted through CHIPS

• ACH― As of Sept. 2009, all International ACH transactions must be

in the form of an IAT

• SWIFT― Service used by banks to remit payments cross-border

• Letter of Credit― Transaction guaranteed by banks, used for trade transactions

• OFAC― Office of Foreign Asset Control. All transactions must be

checked against OFAC SDN list

www.TheAPNetwork.com Page 24

THE ACCOUNTS PAYABLE

Leadership Conference

www.TheAPNetwork.com Page 25

THE ACCOUNTS PAYABLE

Leadership ConferenceIs My Transaction an IAT?

Payment transaction? IAT

Yes Yes Yes

MessageDomestic

ACHForeign/

Proprietary

No No No

Instruction + settlement

Location of originator & receiver not

relevant

At any point

Not an IAT

Still subject to OFAC

rules!

Financial agencyoutside U.S.?

U.S. ACHnetwork?

www.TheAPNetwork.com Page 26

THE ACCOUNTS PAYABLE

Leadership ConferenceEuropean Payments

• All payments going to—or crossing borders within—Europe must contain the International Bank Account Number (IBAN)

• IBAN is up to 28 digits plus a 2-digit country code― For example, a U.K. IBAN would look like this when printed: GB99 RBOS 1234 5612 3456 78― IBAN consists of country code and check digits, bank name

sort, or routing code and account number. A currency code can be added after the IBAN i.e. (USD)

www.TheAPNetwork.com Page 27

THE ACCOUNTS PAYABLE

Leadership Conference

27

GLOBALCUSTOMER

Global GatewayBank Architecture

LOCAL CLEARING

Branch

LOCAL CLEARING

Branch

LOCAL CLEARING

Partner Bank A

LOCAL CLEARING

Partner Bank Z

LOCAL CLEARING

Branch

LOCAL CLEARING

Branch

LOCALREGIONAL

EMEA

NA Hub

ASPAC Hub

LATAM Hub

GlobalGatewayHub

GlobalGateway File

GlobalGateway WEB

www.TheAPNetwork.com Page 28

THE ACCOUNTS PAYABLE

Leadership ConferenceU.S. E-Payment Providers

• The ACH is the backbone of all low value payments in the U.S. Go to www.nacha.org for details

• Credit card providers

• Non-bank entities such as the EDI vans and Web players offer solutions for the very smallest businesses to the largest

• Banks – increasing the range of their services through their own systems, or by partnering or purchasing non-bank providers

www.TheAPNetwork.com Page 29

THE ACCOUNTS PAYABLE

Leadership ConferenceWeb Players (Sample List)

• Probably the best known is PayPal owned by eBay. There is an “App for That”

• CheckFree: used by many billers in the B2C and smaller B2Bs

• Fresh Books: Web-based solution targeted at small business, uses PayPal or credit card for payment

• Vendoran: a trading partner network that facilitates the move from paper to electronic B2B payments.

www.TheAPNetwork.com Page 30

THE ACCOUNTS PAYABLE

Leadership ConferenceBanks

Most large banks offer services ranging from standard ACH payments to a complete order-to-pay service. These include:• JPMorgan Chase – purchased Xign and can offer full

order-to-pay

• Citi – partnered with Ariba for procure-to-pay

• U.S. Bank through their PowerTrack division – full P2P

• Bank of America

www.TheAPNetwork.com Page 31

THE ACCOUNTS PAYABLE

Leadership Conference

Directly Supports Our Clients’ Goals for Achieving Electronic Payment Transformation:

Comprehensive Payables

Paymode-X for Reimbursement Convert costly paper expense

reimbursements to electronic payments E-mail notification of expense payment and

expense report details

The Payment Network®

Global high-value (Wires) and low-value (ACH) payments

Bulk FX payment and draft processing Additional file upload and vendor remittance

delivery options

e-Payables AP payments using the p-card network No implementation or per transaction fees Incentive cash payouts based on spend Increase float when compared to other

payment types, allowing for improved cash flow

Paymode-X®

AP payments leveraging a proven ACH vendor network

Increase processing efficiency and reduce payment processing costs

Ability to include multiple payment types including card, ACH, checks and wires in a flexible single file, turn-key solution

PayMode e-Invoicing Enable the receipt, routing, approval and/or

dispute of electronic invoices Lower administrative costs and provide greater

visibility into your procure-to-pay process

Paymentsto Suppliers/

Vendors

Client Access — Transaction & Information ServicesComprehensive Payables’ Web-based tools allow for real-time management of payment and remittance data

CashPro® Online Works®

Paymode-X

Bank, Sample Offering (B of A)

Source: Bank of America

www.TheAPNetwork.com Page 32

THE ACCOUNTS PAYABLE

Leadership Conference

Easy-to-implement and cost-effective – Designed to reduce the administrative and IT effort typically required to start an e-Payments program

Fully integrated end-to-end payment process – Uses your preferred format Single point of origination – Send instructions for all payment types in one file: card, ACH, wire

and check printing and distribution Accelerates enrollment program – Multiphase campaign enrolls your vendors Consultative services – Adds value to both the payer and receiver by going deeper into the

supply chain Expense savings – reduces per check costs and increases card rebate potential Enhances reporting – Includes supplier-friendly remittance and online access

Easily migrate from paper to electronic payments:

Bank, Sample Offering (B of A) (Cont’d.)

Source: Bank of America

www.TheAPNetwork.com Page 33

THE ACCOUNTS PAYABLE

Leadership ConferenceTrends in Payment Options

• Banks and p-card providers merging traditional payments with card options

• Payables financing offerings are replacing factoring

• P-card use extending to non-traditional purchases by state and local government

© 2011 Financial Operations Networks LLC

Thank You!