© 2007 independent communications authority of south africa all rights reserved 1 “ competitive...

TRANSCRIPT

© 2007 Independent Communications Authority of South AfricaAll Rights Reserved

1

““Competitive Platforms for the Delivery of Digital Competitive Platforms for the Delivery of Digital Content”Content”

EBU

21-22 June 2007, Geneva

Dr. Tracy Cohen, Councillor, ICASA

© 2007 Independent Communications Authority of South AfricaAll Rights Reserved

2

Disclaimer

The views expressed in this presentation are not necessarily those of ICASA, its Council,

management or staff.

© 2007 Independent Communications Authority of South AfricaAll Rights Reserved

3

The business case for mobile

Voice continues to be dominant in Africa

Segmented approach to the mobile business case• “Emerging markets” are not uniform markets

Africa can be split into 2 categories• Markets nearing maturity (Egypt, Morocco, South Africa)

Data becoming increasingly important for mature markets

Markets with growth potential (other African markets) are still based on voice

© 2007 Independent Communications Authority of South AfricaAll Rights Reserved

4

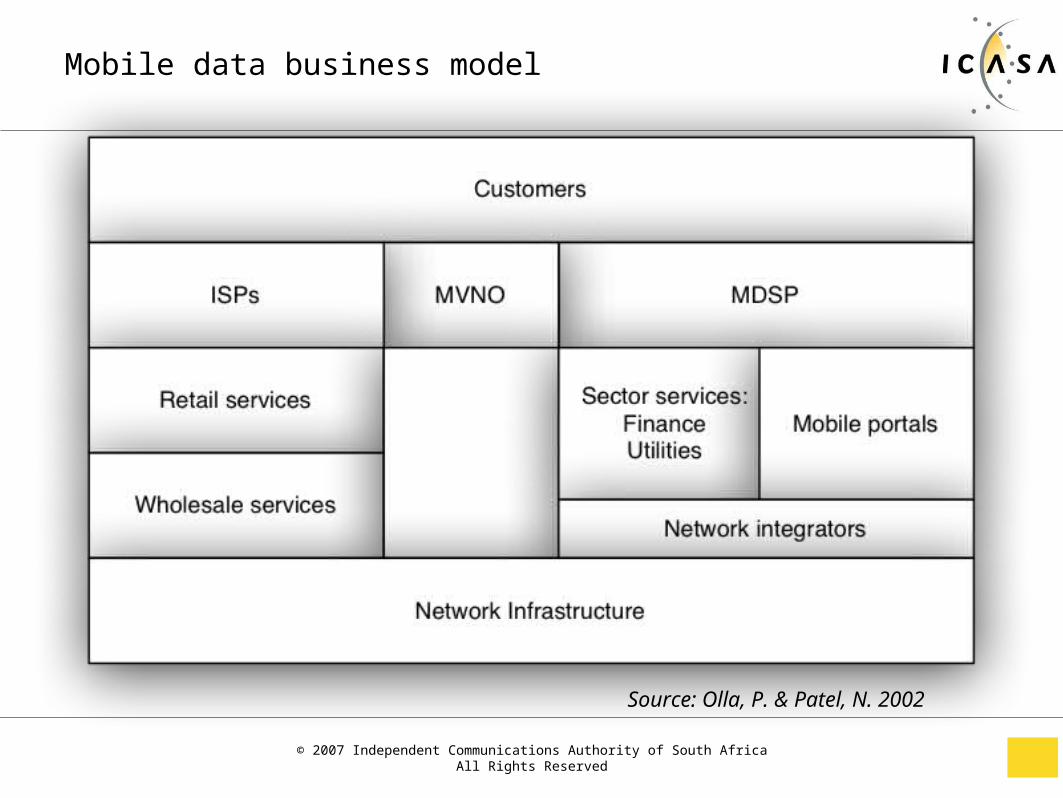

Mobile data business model

Source: Olla, P. & Patel, N. 2002

© 2007 Independent Communications Authority of South AfricaAll Rights Reserved

5

Mobile subscriber growth

© 2007 Independent Communications Authority of South AfricaAll Rights Reserved

6

Declining ARPUs

2004 2005 2006

Nigeria DRC Tanzania Lesotho Mozambique South Africa

© 2007 Independent Communications Authority of South AfricaAll Rights Reserved

7

Mobile data

Operators see data as a growth area– "Take advantage of opportunities within the value chain [such as] data

opportunities" (MTN)

"The alliance with Vodafone Group Plc is expected to provide further impetus to revenue growth from innovative products, which will also support the group's growth strategy for new technologies ..... where the focus remains on growing data revenues" (Vodacom)

Operators seeking new sources of revenue and enhanced user experience

Fixed –data Mobile broadband (data, gaming, entertainment…) Mobile TV (DVB-H) IPTV CAPEX to NGN Exploit success of pre-paid model

366%78%

© 2007 Independent Communications Authority of South AfricaAll Rights Reserved

8

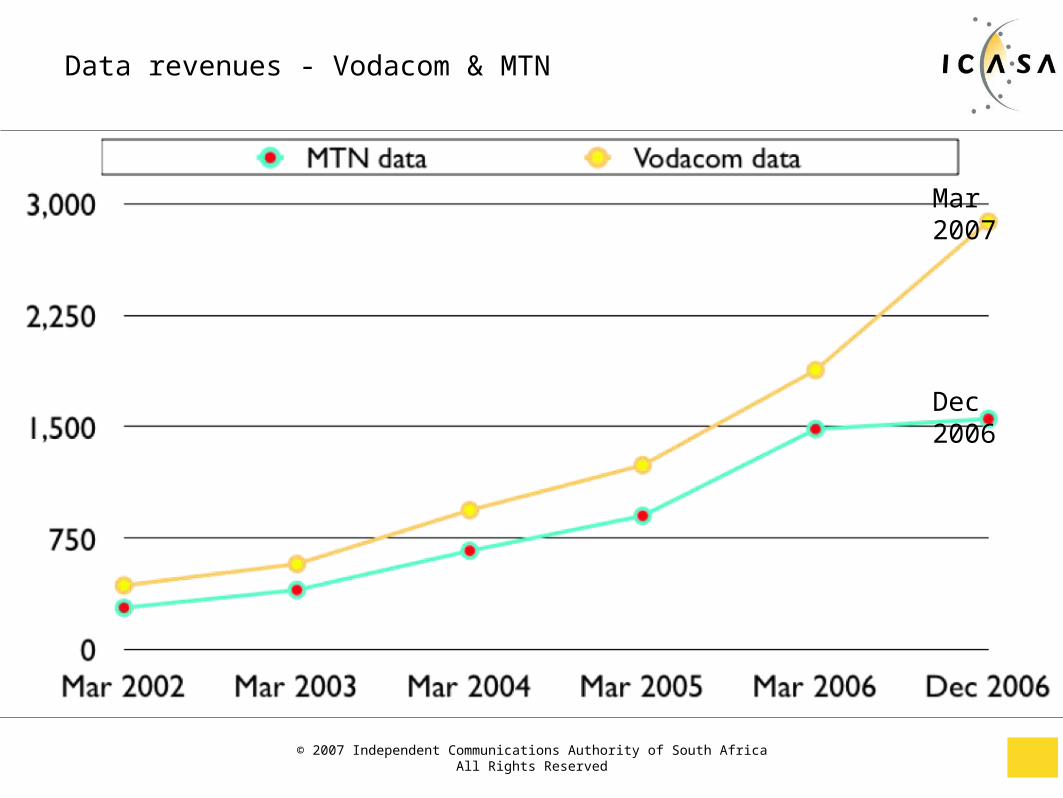

Data revenues - Vodacom & MTN

Dec 2006

Mar 2007

© 2007 Independent Communications Authority of South AfricaAll Rights Reserved

9

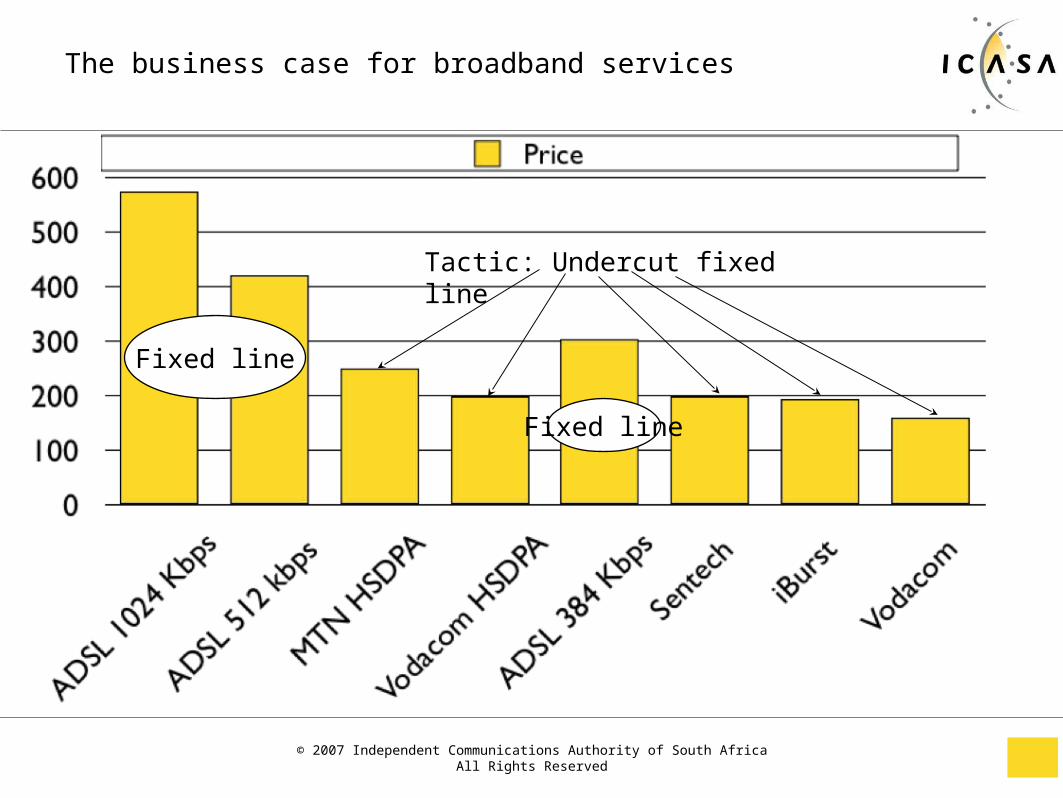

The business case for broadband services

Tactic: Undercut fixed line

Fixed line

Fixed line

© 2007 Independent Communications Authority of South AfricaAll Rights Reserved

10

The business case for mobile TV in SA

2m pay TV subscribers

10m TV sets

33m mobile phones

Declining ARPU

Increased delivery platforms

2010 World Cup Football

Maturing market

Success of prepaid model

Increased data spend

© 2007 Independent Communications Authority of South AfricaAll Rights Reserved

11

The changing/cyclical nature of regulation

Noam suggests that all regulation will converge around a single platform – the Internet - changing the nature of all regulation to become, in essence, telecom regulation.

Eli M. Noam, “Why TV Regulation will become telecom regulation” OFCOM, http://www.ofcom.org.uk/research/commsdecade/

Media players

Regulators/ policy makers

New media

© 2007 Independent Communications Authority of South AfricaAll Rights Reserved

12

SA market - vertical to horizontal

D ep t o f C om m u n ica tion s

M ob ile D a ta (1 )R ad io Tru n k in g (3 )

P ag in g (2 3 )

V A N S /IS P s1 2 0 +

P TNTran sn e t (ra il)E skom (e lec )

C e llu la r: G S MV od acom ; M TN ; C e ll-C

F ixedTe lkom S A

M u lt ip le tech n o log ies

G M P C S

U S A L> 5 %

G S M 1 8 0 03 G

S N OF ixed , fixed m ob ile

(n o t ce llu la r)Incl. T ransnet and Eskom

S en techM M an d C C

R eg u la to rICASA

M in is te r o f C om m u n ica tion s P P C C om m u n ica tion s

© 2007 Independent Communications Authority of South AfricaAll Rights Reserved

13

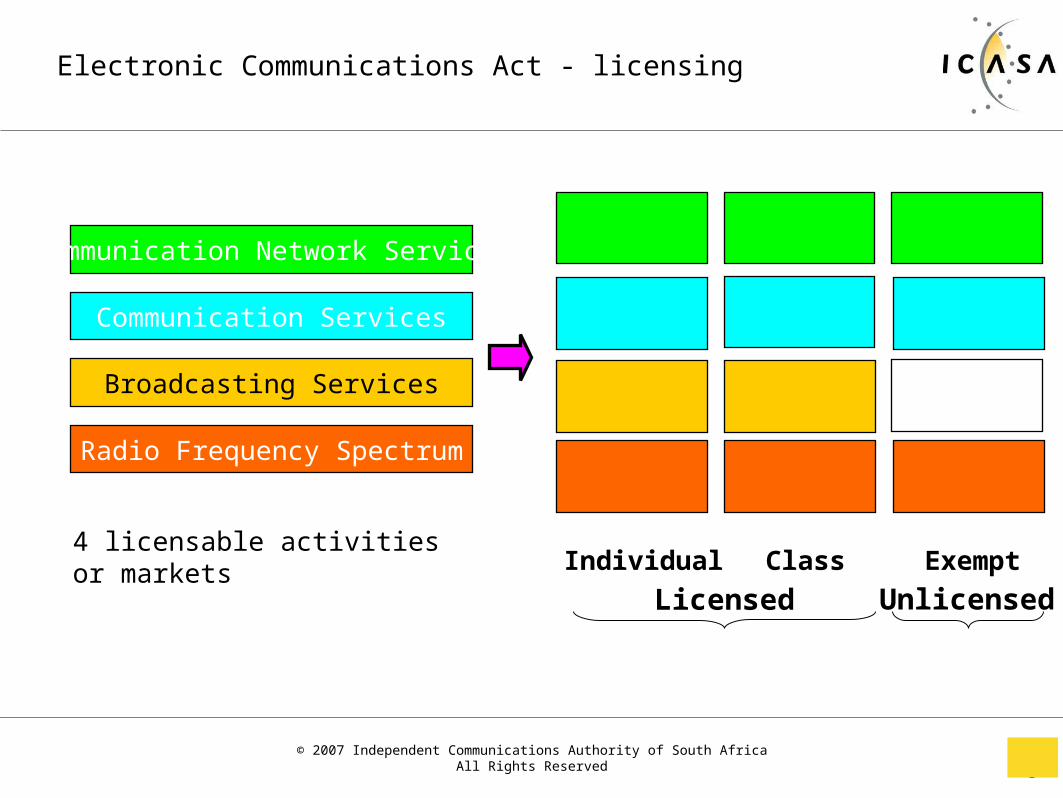

Electronic Communications Act - licensing

Radio Frequency Spectrum

Broadcasting Services

Communication Services

Communication Network Services

Individual Class Exempt

Licensed

4 licensable activities or markets

Unlicensed

© 2007 Independent Communications Authority of South AfricaAll Rights Reserved

14

Converged approach to licensing

Generic provisions of the Bill apply to all relevant activities

Standard licence conditions commonto Individual and Class licenses

Standard LicenceConditions common

to Individual Licenses

Special conditions

Undertakings

ExemptIndividual Class

© 2007 Independent Communications Authority of South AfricaAll Rights Reserved

15

Conclusion

Legal and market convergence underway

Supplementary revenue through data and mobile broadcasting

NGN capex commitments confirm

User experience sought to be enhanced

Business case for mobile TV is untested

2010 world cup football – major driver of DVB-H in SA

Legal and regulatory framework not an impediment

Implications for competition (regulation)