- 0 - presentation on indian economy february 2010

TRANSCRIPT

- 1 -

PRESENTATION ON INDIAN ECONOMY

February 2010

- 2 -

STRONG MACRO FUNDAMENTALS

World’s fourth-largest economy in terms of PPP* and ranked 12th in US$ terms.

GDP has increased rapidly over the past 15 years from $250 billion to over US$ 1 trillion currently.

Per Capita Income in 2008-09:- US$ 2,563 in PPP terms- US$ 831 in nominal terms

0

100

200

300

400

500

600

700

800

900

19

92

-93

19

93

-94

19

94

-95

19

95

-96

19

96

-97

19

97

-98

19

98

-99

19

99

-00

20

00

-01

20

01

-02

20

02

-03

20

03

-04

20

04

-05

20

05

-06

20

06

-07

20

07

-08

20

08

-09

0

200

400

600

800

1000

1200

1400

Per capita income GDP

US$ US$ bn

* PPP : Purchasing Power Parity terms

–

–

–

- 3 -

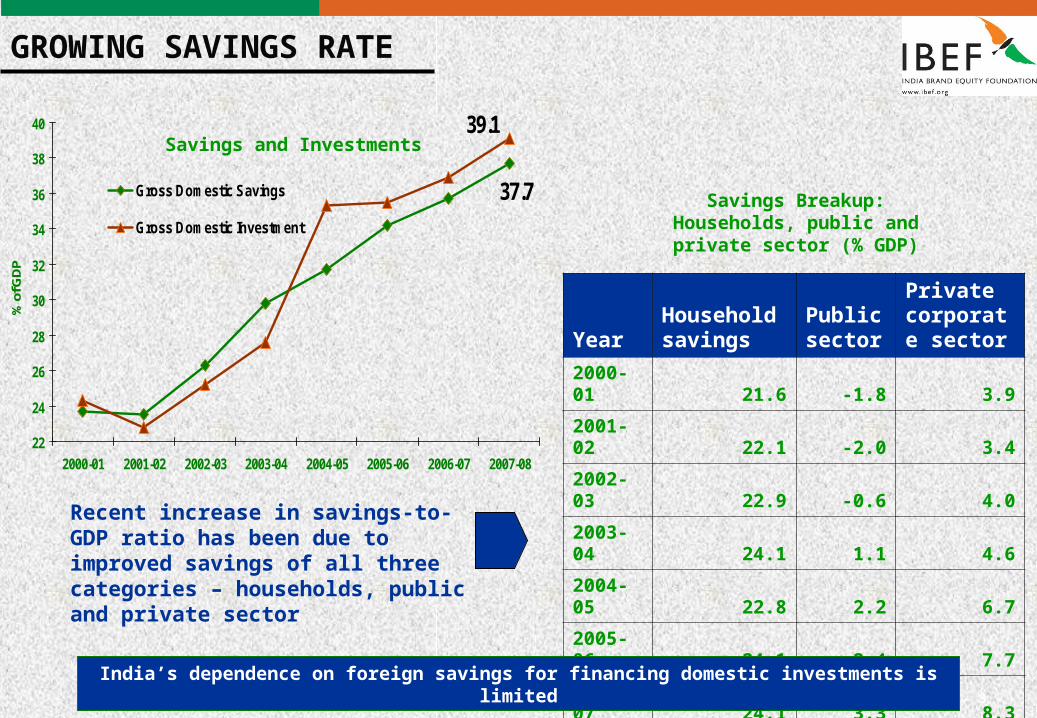

GROWING SAVINGS RATE

37.7

39.1

22

24

26

28

30

32

34

36

38

40

2000-01 2001-02 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08

% o

f GD

P

Gross Domestic Savings

Gross Domestic Investment

YearHouseholdsavings

Public sector

Private corporate sector

2000-01 21.6 -1.8 3.9

2001-02 22.1 -2.0 3.4

2002-03 22.9 -0.6 4.0

2003-04 24.1 1.1 4.6

2004-05 22.8 2.2 6.7

2005-06 24.1 2.4 7.7

2006-07 24.1 3.3 8.3

2007-08 24.3 4.5 8.8

Savings and Investments

Savings Breakup: Households, public and private sector (%

GDP)

Recent increase in savings-to-GDP ratio has been due to improved savings of all three categories – households, public and private sector

India’s dependence on foreign savings for financing domestic investments is limited

- 4 -

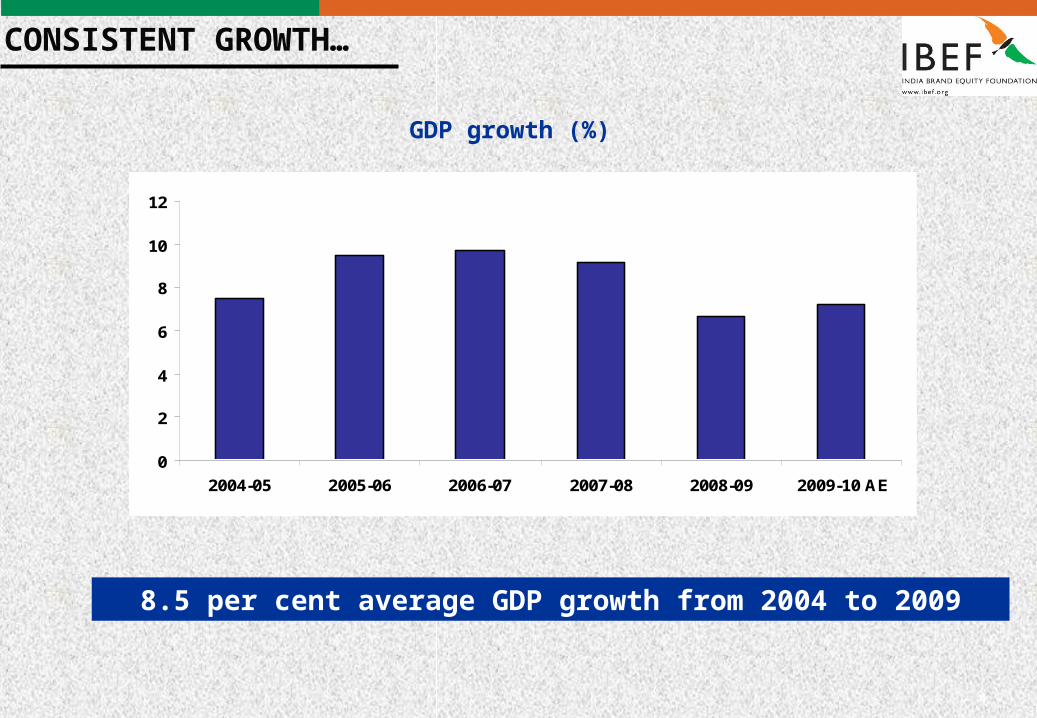

GDP growth (%)

CONSISTENT GROWTH…

0

2

4

6

8

10

12

2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 AE

8.5 per cent average GDP growth from 2004 to 2009

- 5 -Source: IMF

India is set to grow faster than other regions (Annual Percentage change)

Economies 2008 2009 Projections

2010 2011

World 3.0 -0.8 3.9 4.3

Advanced Economies 0.5 -3.2 2.1 2.4

United States 0.4 -2.5 2.7 2.4

Euro Area 0.6 -3.9 1.0 1.6

Japan -1.2 -5.3 1.7 2.2

Developing Asia 7.9 6.5 8.4 8.4

China 9.6 8.7 10.0 9.7

India 7.3 5.6 7.7 7.8

Brazil 5.1 -0.4 4.7 3.7

…OUTPACING THE WORLD

- 6 -

GDP Composition: 1990-91 and 2009-10

1990-91

32%

27%

41%

Agriculture Industry Services

2009-1015%

28%

57%

RISE OF SERVICES AND INDUSTRY

- 7 -

FDI and Portfolio Inflows (US$ bn)

8.9

22.7

34.2 35.0

26.5

12.57.1

29.623.7

-14.0

2005-06 2006-07 2007-08 2008-09 2009-10*

Inward FDI Portfolio

*Apr-Dec 2009

CAPITAL INFLOWS ARE RISING

• Foreign Direct Investment (FDI) in Jan 2010 grew 13.2 per cent over the previous month, to touch US$ 1.54 billion

• Private equity investments in India doubled in Jan 2010, with deals of over US$ 386 mn being announced.

• The recent recovery in capital inflows has lead to a 5-6% recovery in the value of the Rupee, which is currently trading at levels of Rs 46-47 /US$.

- 8 -

RESILIENT ECONOMY

OPPORTUNITY INDIA

TRENDS

- 9 -

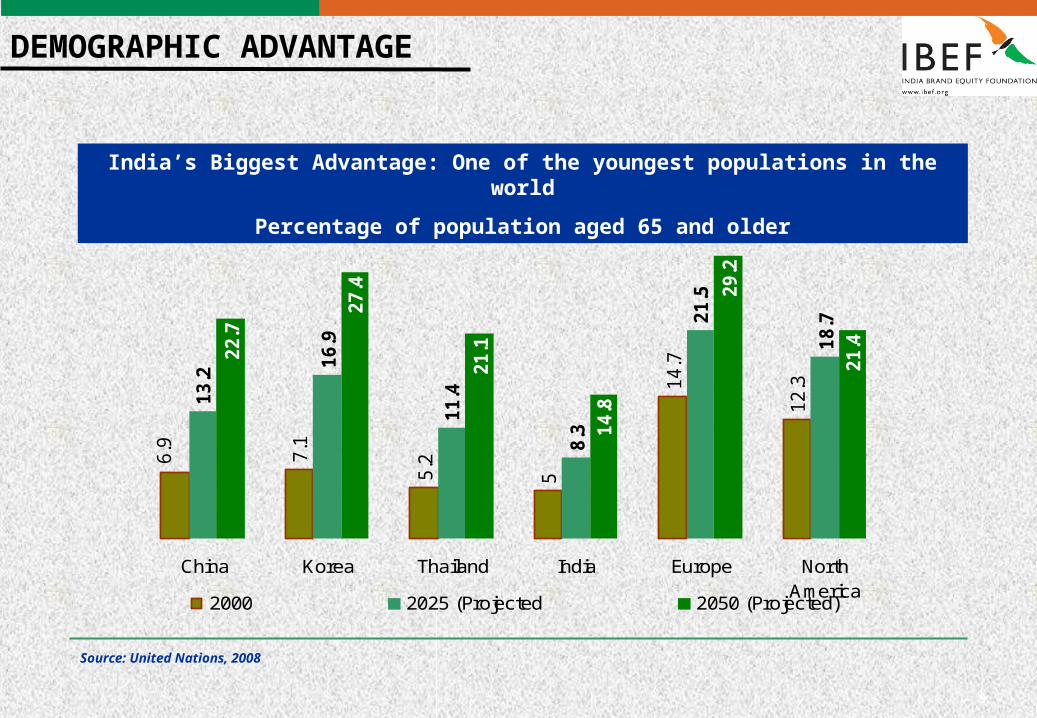

DEMOGRAPHIC ADVANTAGE

7.1

5

14.7

12.3

13.2

16.9

11.4

8.3

18.7

22.7

21.1

14.8

21.4

5.26

.9

21.5 2

9.2

27.4

China Korea Thailand India Europe NorthAmerica

2000 2025 (Projected 2050 (Projected)

India’s Biggest Advantage: One of the youngest populations in the world

Percentage of population aged 65 and older

Source: United Nations, 2008

- 10 -

• 50 per cent of the population under 25

• Among top three of 30 nations in availability of skilled labour

• 7.7 mn new entrants to the workforce every year

• Dependency ratio expected to fall from current 60 per cent to 48 per cent by 2025

STRONG DEMOGRAPHIC DIVIDEND

BOOSTING INCREDIBLE ASPIRATIONS

- 11 -

Market capitalisation

0

20

40

60

80

100

120

140

160

Oil

& g

as &

PO

L

pro

ducts

Banks a

nd

Fin

ancia

l

serv

ices

Energ

y

Constr

uction

Meta

ls a

nd

meta

l pro

ducts

IT /

ITE

S

Tele

com

Engin

eering

Consum

er

dis

cre

tionary

Dru

gs &

pharm

aceuticals

Min

ing

Tra

din

g

Auto

/ A

uto

ancill

iary

US$ billion

RELENTLESS ENTREPRENEURSHIP

Emergent Indian enterprises across sectors ranging from engineering to financial services.

Market capitalisation of top-500 companies in excess of $800 bn or about 70% of GDP

- 12 -12

INDIA INC. GOING GLOBAL

US$ 2.8 billion US$ 2.8 billion ONGC acquired Imperial Energy PLC in 2008ONGC acquired Imperial Energy PLC in 2008

US$ 44.44 million

US$ 44.44 million

Spice Group acquired 20 per cent stake in MediaRing Ltd. in 2009

Spice Group acquired 20 per cent stake in MediaRing Ltd. in 2009

US$ 82 millionUS$ 82 millionShree Renuka Sugars Ltd. acquired Vale Do Ivai

S.A. Acucar E Alcool sugar and ethanol company in Brazil in 2009

Shree Renuka Sugars Ltd. acquired Vale Do Ivai S.A. Acucar E Alcool sugar and ethanol

company in Brazil in 2009

Sources: 1. Tribune India

2. The First Reporter

Bharti Airtel has acquired a 70 per cent stake in Warid Telecom in 2010

Bharti Airtel has acquired a 70 per cent stake in Warid Telecom in 2010

Planned investment -

US$ 300 million

Planned investment -

US$ 300 million

- 13 -13

Abundant Natural Resources

Fifth-largest bauxite reserves in the world, fourth-largest coal reserves, sixth-largest iron ore deposits

Low-cost Skilled Talent

India offers skilled and trained human resource at low cost

Huge Demand

Large population base and surging middle class with high disposable income

Easy Access to Other Markets

India’s strategic geographical location offers an opportunity to access neighboring South Asian markets

Gains in Productivity

India's productivity growth was 5.5 per cent in 2008, as compared with 2.3 per cent globally

India: Manufacturing

Hub

Sources: The Conference Board; CIA

INDIA: GROWING MANUFACTURING HUB

- 14 -

INDIA: FAVOURED R&D HUB

Sources:: 1. Asia Times; 2. Business Standard

Vast pool of manpower

According to the IMD World Competitiveness Year Book, India ranks among the top three of 30 nations in terms of availability of skilled labour

Higher productivity

Indian graduates, on an average, work 2,350 hours a year as compared with 1,900–1,700 hours in the US

Tax benefits

Companies engaged in scientific R&D projects in India are entitled to a 100 per cent tax relief on profits for 10 years

Growing domestic market

The growing demand for technologically-advanced products in the Indian market is increasingly drawing MNCs to set up R&D centres here

India: R&D Hub

- 15 -

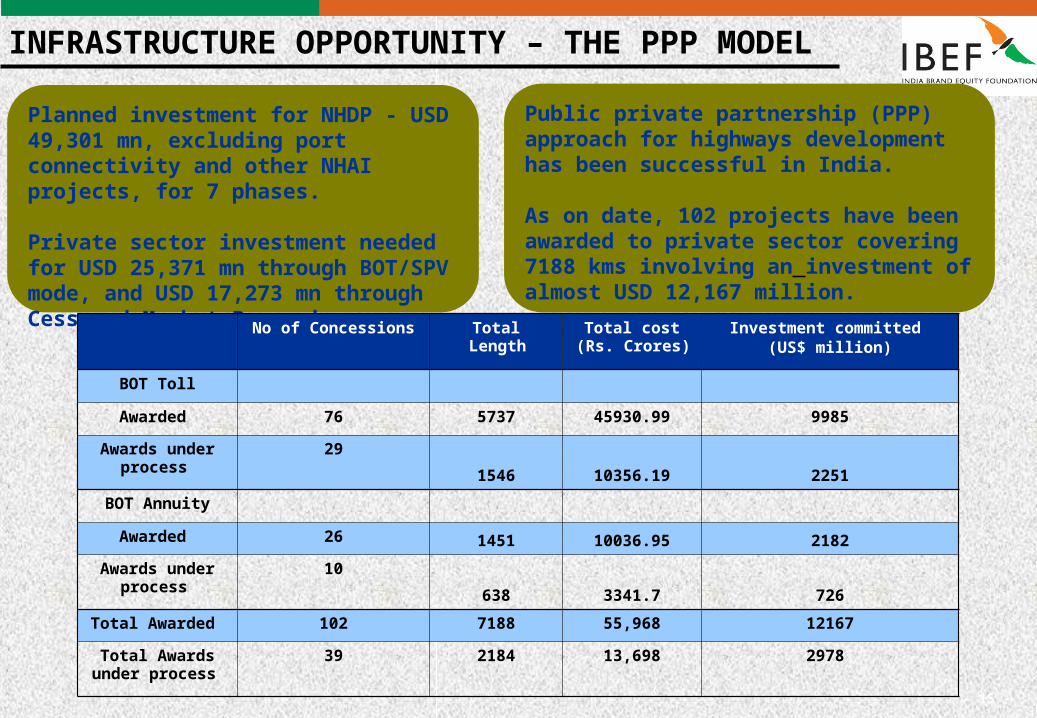

INFRASTRUCTURE OPPORTUNITY – THE PPP MODEL

Planned investment for NHDP - USD 49,301 mn, excluding port connectivity and other NHAI projects, for 7 phases.

Private sector investment needed for USD 25,371 mn through BOT/SPV mode, and USD 17,273 mn through Cess and Market Borrowings.

Public private partnership (PPP) approach for highways development has been successful in India.

As on date, 102 projects have been awarded to private sector covering 7188 kms involving an investment of almost USD 12,167 million.

No of Concessions Total Length Total cost (Rs. Crores)

Investment committed (US$ million)

BOT Toll

Awarded 76 5737 45930.99 9985

Awards under process

29

1546 10356.19 2251

BOT Annuity

Awarded 26 1451 10036.95 2182

Awards under process

10

638 3341.7 726

Total Awarded 102 7188 55,968 12167

Total Awards under process

39 2184 13,698 2978

- 16 -

BIOTECHNOLOGY

India is among the top-12 biotech markets globally.

India ranks third in the Asia-Pacific region, after Japan and Korea.

Expected to touch US$ 5 billion by 2010 and US$ 25 billion by 2015.

*Source: Top 20 biotech companies, Biospectrum industry survey, June 2009, p.14; Ernst & Young analysis

Segment 2008-09 Revenue (in US$ mn)

Contribution (in per cent)

Biopharma 1734.26 64.95

Bioservices 453.64 16.99

Bioagri 328.68 12.31

Bioindustrial 105.16 3.94

Bioinformatics 48.4 1.81

- 17 -

Low-cost operations

• Significantly lower R&D costs; outsourcing to India can save up to US$ 200 million.

• Cost of clinical trials 50 percent lower in phase I and 60 percent lower in phase II compared to global markets.

• Clinical trials take significantly lesser time.

BIOTECHNOLOGY - ADVANTAGE INDIA

Large pool of talented human resources

• Large talent pool of science students pursuing higher education.

• 5000 PhDs and 1000 post-doctorals in biosciences-related fields.

• Top-notch life science education and research institutes.

Favourable IP climate

Adherence to the TRIPS agreement with regard to the Patent Protection Act implemented in 2005 has increased the confidence of innovator companies in India.

- 18 -

PHARMACEUTICALS

Among the fastest growing pharmaceutical markets in the world; worth US$ 16.6 billion in 2007–08

Domestic retail market expected to cross US$ 10 billion mark in 2010 and reach an estimated US$ 12 billion to US$ 13 billion by 2012.

Outsourcing opportunity set to grow to US$ 53 billion in 2010 from US$ 26 billion in 2006.

Key Multinational Companies in India

- 19 -

PHARMACEUTICALS - ADVANTAGE INDIA

The basic production cost in India is almost 50 per cent lower than costs in the US.

85 per cent to 90 per cent

manpower cost savings

40 per cent to 50 per cent savings in raw materials

30 per cent to 50 per cent lower depreciation

Around 1,000 biotech and biochemistry postgraduates pass out every year

Around 10,000 chemistry postgraduate students graduate every year

India: Growing pharma market

- 20 -

IT & ITeS

India topped the A.T. Kearney Global Services Location Index 2009,

beating 49 other countries of the world, emerging to be the destination of

choice as an offshoring location of global IT/ITeS powerhouses

Revenues by segment – Indian IT industry

- 21 -

• India’s share in the global market has increased to four per cent in the IT segment and close to 12 per cent in ITeS in 2008-09.

• India has maintained its position as the preferred outsourcing destination; Indian IT/ITeS companies are now offering a global delivery model, at par with leading global standards.

• India offers low costs, technical and language skills, abundant skilled pool, mature industry players and supportive government policies.

Sources: ITeS: Industry profile, April 2009, CRIS INFAC

IT & ITeS - ADVANTAGE INDIA

Financial attractiveness of top 5 global services locations

Country Index on a scale of 4

India 3.13

China 2.59

Malaysia 2.76

Thailand 3.05

Indonesia 3.23

Source: A T Kearney Global Service Location index 2009

- 22 -

The processed food market in India

is at an early stage with low

penetration and offers huge

opportunities.

In the 2004-2007 period:

– Value of food processing

grew from US$57 bn to US$75 bn

– Number of registered operating

units increased from 24,000 to

25,725.

Source: Flavors of incredible India, Ernst & Young, 2009

FOOD PROCESSING

Growth in output of processed food (US$ billion)

- 23 -

FOR INFORMATION ON INDIAN BUSINESS AND ECONOMY, PLEASE VISIT

www.ibef.org