zoroastrian bank bank annual report...zoroastrian bank (the zoroastrian co ... mrs. dhanoo h....

TRANSCRIPT

ZOROASTRIAN BANK(The Zoroastrian Co-operative Bank Ltd.)

1

Registration No: MSCS /CR/881/2013 dated 11th November, 2013, under the Multi State Co-operative Societies Act, 2002.

Reserve Bank of India Licence No. UBD.MH.1065p dated 16th February, 1994

BOARD OF DIRECTORS

Ms. Homai A. Daruwalla – Chairperson Mr. Yazdi B. Tantra – Vice Chairman

Mrs. Shernaz D. Mehta Mr. Homa D. Petit

Mrs. Dhanoo H. Khusrokhan Mr. Jimmy N. Panthaky

Dr. Firdos T. Shroff Mr. Saroosh C. Dinshaw

Mr. Phillie D. Karkaria Mr. Mehrab N. Irani

Mr. Farhad S. Choksey Mr. Manek J. Kalyaniwalla

Mr. Aspi A. Kathawalla

MANAGING DIRECTOR & CEOMr. Uday A. Shetye

STATUTORY AUDITORSM. P. Chitale & CompanyChartered Accountants

90th Annual Report 2016-2017

2

Dear Shareholders,

I have immense pleasure in welcoming you all to the 90th Annual General Meeting of the Bank.

I am proud that I am at the helm of the Bank when we are celebrating 90 year of operations.

Though small in size of business, we had the privilege of having experienced bankers at the helm for quite some time, and I am confident, I will be able to carry on the tradition.

Our Capital and Reserves are at robust levels, with Total Paid Up Capital at Rs.1412.36 lakhs and Reserve Funds at Rs.13310.24 lakhs as on 31/03/2017. The Total Reserve Funds as of March 2017 stand at over 9.42 times your capital.

The past year has been quite eventful for the banking industry.

• Demonetization of high value currency notes of Rs.500/- and Rs.1000/- on 8th November 2016 paused a big challenge to all banks during the year. Many of the co-operative banks were forced to keep the cash counters shut for many days due to non-availability of legal tender. Your bank has come out of the crisis with flying colours as not a single branch in Mumbai had kept the cash counters closed.

• We have seen one of the biggest consolidations in banking sector with State Bank of India merging with it 5 subsidiary Banks and Bharatiya Mahila Bank with effect from 1st April, 2017.

• Global rating agency Moody’s has upgraded its outlook for the Indian banking system to ‘Stable’ from ‘Negative’, based on its assessment of five drivers including improvement in the operating environment and stable asset risk and capital scenario.

• The Reserve Bank of India (RBI) has released the Vision 2018 document, aimed at encouraging greater use of electronic payments by all sections of society by reducing paper-based transactions, increasing the usage of digital channels, and boosting the customer base for mobile banking.

• The Rajya Sabha has passed the major economic reform Bill moved by the Government i.e. ‘Insolvency and Bankruptcy Code, 2016. The Act aims at consolidating the laws relating to insolvency of companies and limited liability entities (including limited liability partnerships and other entities with limited liability), unlimited liability partnerships and individuals, presently contained in a number of legislations, into a single legislation. Such consolidation will provide for a greater clarity in law and facilitate the application of consistent and coherent provisions to different stakeholders affected by business failure or inability to pay debt.

The effect of demonetization was a mixed bag for our Bank on the business front. While the Deposits grew by 21.77% from Rs.887.14 crores as of 31st March, 2016 to 1080.25 crores as of 31st March, 2017, the Advances portfolio registered a decline of 9.36% from Rs.585.24 crores to Rs.530.45 crores for the corresponding period.

The Net Profit remained more or less at the same level, i. e. Rs.10.87 crores as of 31st March, 2017 compared to Rs.10.76 crores as of 31st March, 2016, with a marginal growth of 1.02%.

Though the share of NPAs to total advances grew from 1.48 % as on 31st March, 2016 to 1.58% as of 31st March, 2017, the perceived growth is only on account of the decline in Total Advances. The Gross NPAs have

From the Chairperson’s Desk

ZOROASTRIAN BANK(The Zoroastrian Co-operative Bank Ltd.)

3

actually declined from Rs.865.18 lakhs as on 31st March, 2016 to Rs.840.21 lakhs as on 31st March, 2017 despite addition of 4 accounts to NPAs category during the year.

With a view to improve the advances portfolio of the Bank, we have introduced a slew of Retail Loan Products with very liberal terms and rate of interest comparable with the peers. Different marketing strategies are chalked out for marketing of these products and also the progress is closely monitored by the Senior Executives at the Corporate Office. I request all of you to avail of these facilities for you and your family members, and also recommend the same to your friends and business associates.

We are also making all attempts to bring in the Technology Advancements and New Products linked to such advanced technology. All efforts are made to bridge the gap in comparison to similar sized banks. I may add a word of caution at this stage, no technology can replace the human touch and personal care. We are fortunate in this respect as the feedbacks I have received from our constituents generally reflect appreciation of the customer service rendered by our staff members.

We have a relatively young HR force. Wherever necessary, we are planning recruitment of personnel with specialized qualifications and skills to strengthen the Management structure at different levels.

I am aware that we have to look beyond our community for growth and offer universal banking to all regardless of caste or creed. However, I firmly believe that our community is rich enough to contribute much more to the growth of the organisation. This can materialize by each director, shareholder and member of the community opening more accounts and also introducing more accounts for the Bank.

While the Board of Directors and the Management are working in tandem to take the organisation to higher levels, I also seek your co-operation and efforts as ambassadors of ZCBL to increase the customer base and business of the Bank.

I will be failing in my duties if I do not acknowledge and appreciate the efforts and contributions from different individuals and agencies in the working of the Bank. Notable among them are:

• M/s. M. P. Chitale & Co – Chartered Accountants appointed as Statutory Auditors for timely completion of the Statutory Audit.

• Mr. Homiyar Madan of H.F.K. Madan & Co. for the support and suggestions made during the course of audit of the Bank.

• The Officers of the Reserve Bank of India, especially the Urban Banks Department, The Central Registrar of Co-operative Societies, New Delhi, The Commissioners for Co-operation and Registrar of Co-operative Societies for the State of Maharashtra and Gujarat and National Federation of Urban Co-operative Banks for their support and contribution from time to time.

• The shareholders and constituents and for their patronage, involvement and support in the overall development of the Bank.

• Last but not the least, the Management Executives and Staff at all levels for their dedication and devotion to duty and involvement in Business Development.

H. A. DARUWALLACHAIRPERSON

90th Annual Report 2016-2017

4

NOTICE OF ANNUAL GENERAL MEETING

NOTICE is hereby given that the Ninetieth Annual General Meeting of the members of the Bank will be held on 19th September, 2017, at 4.00 p.m at The Homi J. H. Taleyarkhan Memorial Hall, Indian Red Cross Society, Town Hall Compound, Opp. Horniman Circle, Fort, Mumbai – 400 001 to transact the following business: -

(1) To read and confirm the Minutes of the Annual General Meeting held on September 23, 2016.

(2) To adopt the Annual Report placed by the Board of Directors for the Financial Year ended March 31, 2017, Balance Sheet and Profit and Loss Account and take note of Statutory Auditor’s report.

(3) To declare dividend and allocation of profit for the financial year 2016-17.

(4) To appoint Statutory Auditors for the Financial Year 2017-18 and to authorize Board of Directors to fix their remuneration.

(5) To grant leave of absence to members who have not attended this Annual General Meeting.

(6) Any other business with the permission of the Chair.

By Order of the Board of Directors

U. A. Shetye Managing Director& CEO

Mumbai, August 2, 2017

In the event, a quorum is not formed within half an hour of the appointed time for the meeting, the meeting shall stand adjourned. Thereafter, the adjourned meeting shall be re-convened and conducted on the same day and at the same place as specified in this Notice to transact the business on the agenda, irrespective of the required quorum but within seven days from the date of the adjourned meeting in terms of Bye-law No.25.

ZOROASTRIAN BANK(The Zoroastrian Co-operative Bank Ltd.)

5

NOTES

1. Members desiring any information relating to the accounts are requested to do so in writing to the Bank on or before 5th September, 2017, to enable the Management to make available the required information at the Annual General Meeting.

2. Dividend for the year ended March 31, 2017, if approved at the Annual General Meeting, will be paid from 21st September, 2017 to those Shareholders whose names appear on the Register of Members as on March 31, 2017.

3. It is recommended that Shareholders avail of the facility of crediting dividend amount due to them to their respective Current/Savings accounts with the Bank’s Branches, and for the purpose, they are requested to send their mandate in writing to the Bank.

4. Members are requested to bring a copy of the Annual Report and the attendance slip sent herewith at the Annual General Meeting.

5. Attention of the Members is invited to Bye-law No.47, in terms of which, any dividend remaining undrawn for three years after having been declared, shall be forfeited and transferred to the Reserve Fund of the Bank. The Shareholders who have not collected dividend for the previous three years are requested to do so on or before September 30, 2017 failing which, the dividend for the year ended March 31, 2014 will be forfeited and credited to the Reserve Fund Account.

6. Shareholders, Depositors and Safe Deposit Locker holders are requested to avail of the nomination facility provided by the Bank. Prescribed nomination forms are available at all our Branches.

7. Deposits upto Rs. 1.00 lakh in the case of each individual depositor is insured by the Bank with the Deposit Insurance Credit Guarantee Corporation and the Bank has effected up-to-date payment of the corresponding Insurance premium.

90th Annual Report 2016-2017

6

DIRECTORS’ REPORT

GLOBAL ECONOMIC SCENARIO:Amidstthereportsofterrorism,religiousintoleranceandconflictsallovertheworld,increasingnuclearexperimentsandthreatsbyNorth Korea, re-emergence of cold waves between the USA and Russia, heightening of tensions between India and its neighbours, conflictsinArabcountries,etc.,twoeventsstoodoutintheglobalscenarioduring2016-17i.e.PresidentialelectionsintheUSAand Brexit in the European countries. While the debates on these events will continue, the effects of these developments on the global economic scenario cannot be underestimated. The economic as well as political decisions of the new US administration will have far reaching implications on the US economy as well as on global economy. Similarly, the decision of the UK to exit European UnionandconsequentfinancialsettlementwillnotonlyaffecttheUKandothercountriesintheEuropeanUnion,butwillhaveserious impacts on the global economy.Given the uncertainties surrounding the policy stance of the U.S. administration, UK exit from European Union and its global ramifications,theemergingeconomicstudiesandreportspointstowardsfirmingupofpaceoftheeconomicgrowthin2017and2018aftera lacklusteroutturn in2016.TheWorldEconomicOutlook (WEO) forecastalso incorporatesafirmingofoilpricesfollowing the agreement among OPEC members and several other major producers to limit supply. Long-term nominal and real interest rates have risen substantially since August 2016(the reference period for the October 2016 WEO), particularly in the United Kingdom and in the United States since the November 2016 election. Advanced economies are now projected to grow by 1.9 percent in 2017 and 2.0 percent in 2018. World economic growth is expected to rise from 3.1 percent in 2016 to 3.5 percent in 2017 and 3.6 percent in 2018.

INDIAN ECONOMIC SCENARIO :Indiawitnessedseveralfarreachingdecisionsanddevelopmentsintheeconomicscenarioduringthefinancialyear2016-17.Themajor such events are:yy Decision by the Government of India on 8th November 2016 to demonetize old high value currencies in the denomination of

Rs.500/- and Rs.1000/- yy Accelerated push for the implementation of GST, bringing most of the indirect taxes under one uniform tax system, with roll

out date pegged at 1st July, 2017 yy Rajya Sabha passing “Insolvency and Bankruptcy Code, 2016”.yy Amendment to Banking Regulation Act giving powers to the Reserve Bank of India to intervene and decide on resolutions

ofspecificstressedloanaccounts.yy The Government of India is looking to set a special fund as part of National Investment and Infrastructure Fund to deal with

stressed assets.yy Setting up of Monetary Policy Committee with 6 members to raise transparency in rate setting by the Reserve Bank of India.yy The Reserve Bank of India has released Vision 2018 document aimed at encouraging greater use of electronic payments

by all sections of the society.While the expected gains from the above policies are yet to set in fully, the overall economic outlook remains positive. India’s real Gross Value Added (GVA) growth was projected at 6.7%, down from 7% earlier projected. Agriculture expanded robustly year on year with food grains production touching an all-time-high of 272 million tonnes, with record production of rice, wheat and pulses. ActivityintheServiceSectorappearedtobeimprovingwiththenegativeimpactsofdemonetizationwearingoff.TheCPIInflationcamedownto3.81%asofMarch2017from5.39%atthebeginningoftheyearandtheCPIinflationisexpectedtoremainwithinthe target of 2% to 6% set by the Reserve Bank of India.A major cause of worry is the further slowing down of industrial output to -1.25% as of February 2017 from -0.8% in April 2016.

INDIAN BANKING SCENARIO :In addition to the economic factors discussed hereinabove, some of the other developments directly impacting the Indian Banking scenario are as under:yState Bank of India merging with it 5 subsidiary Banks and Bharatiya Mahila Bank with effect from 01/04/2017, making State

Bank of India one among the top 50 banks in the world.yRoll out of innovative banking models such as Payment Banks and Small Finance Banks.yGlobal rating agency, Moody’s, has upgraded its outlook for the Indian Banking System to ‘Stable’ from ‘Negative’, based

onitsassessmentoffivedriversincludingimprovementinoperatingenvironmentandstableassetriskandcapitalratio.A key concern is the health of the Indian Banking system, which is still dealing with large amounts of bad loans, and also heightened corporate vulnerabilities in several key sectors of the economy.

ZOROASTRIAN BANK(The Zoroastrian Co-operative Bank Ltd.)

7

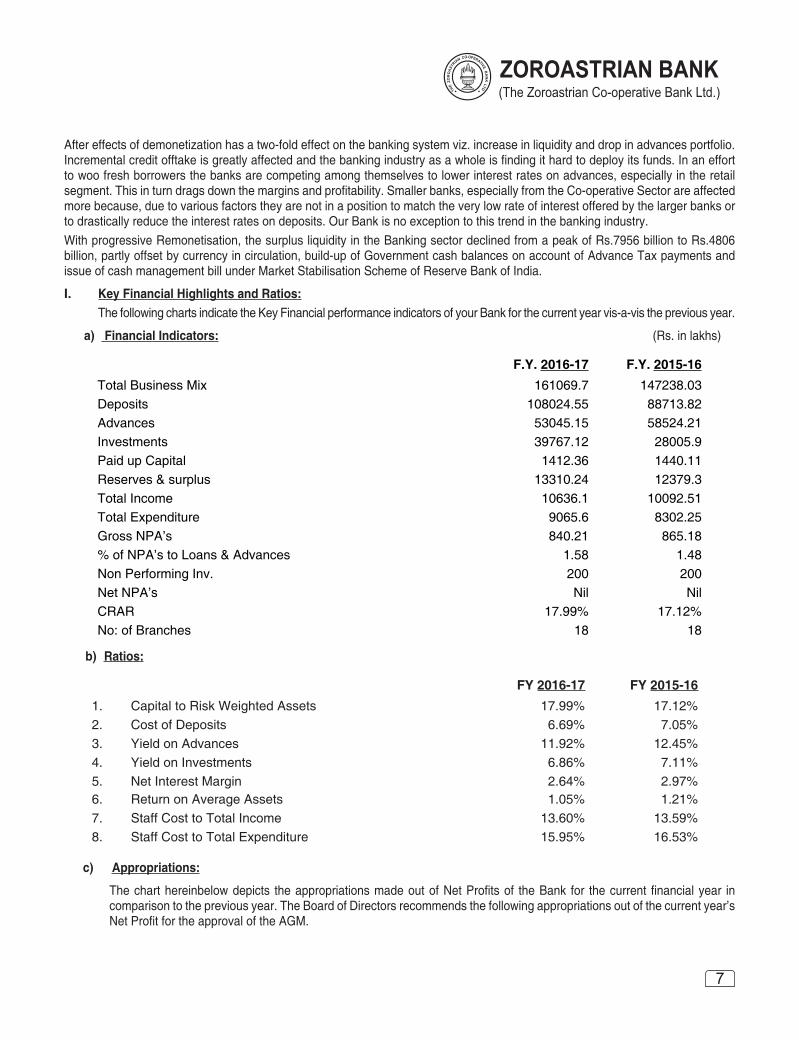

After effects of demonetization has a two-fold effect on the banking system viz. increase in liquidity and drop in advances portfolio. Incrementalcreditofftakeisgreatlyaffectedandthebankingindustryasawholeisfindingithardtodeployitsfunds.Inaneffortto woo fresh borrowers the banks are competing among themselves to lower interest rates on advances, especially in the retail segment.Thisinturndragsdownthemarginsandprofitability.Smallerbanks,especiallyfromtheCo-operativeSectorareaffectedmore because, due to various factors they are not in a position to match the very low rate of interest offered by the larger banks or to drastically reduce the interest rates on deposits. Our Bank is no exception to this trend in the banking industry.With progressive Remonetisation, the surplus liquidity in the Banking sector declined from a peak of Rs.7956 billion to Rs.4806 billion, partly offset by currency in circulation, build-up of Government cash balances on account of Advance Tax payments and issue of cash management bill under Market Stabilisation Scheme of Reserve Bank of India.

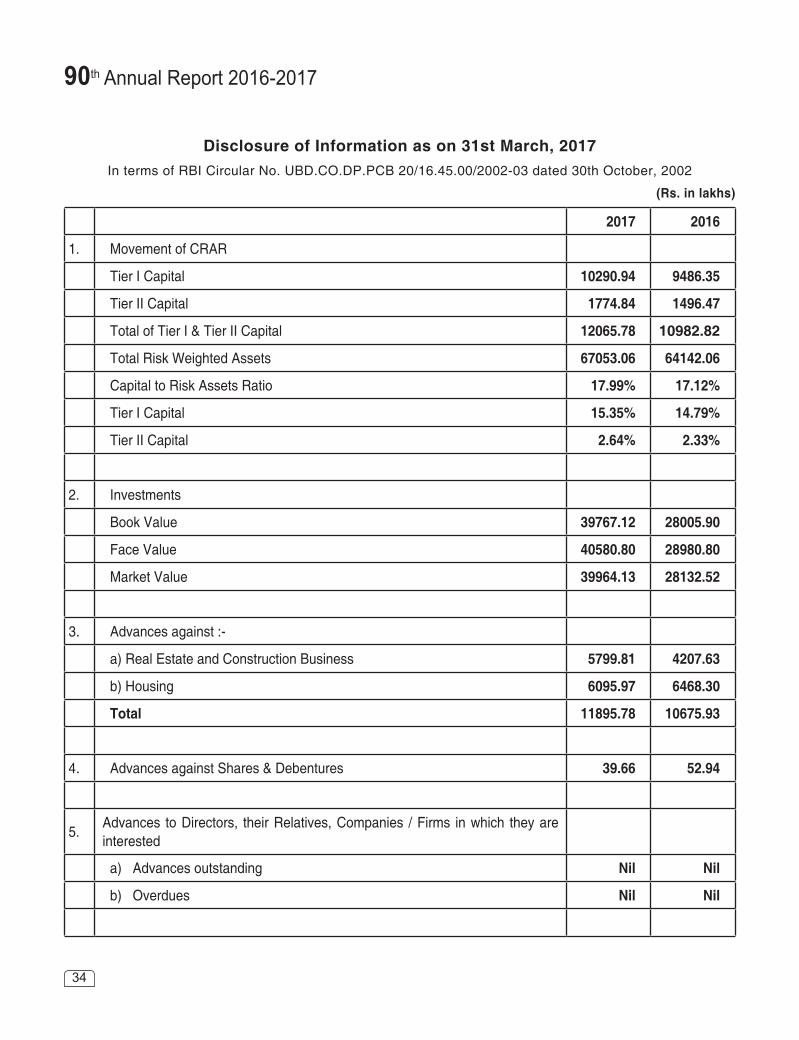

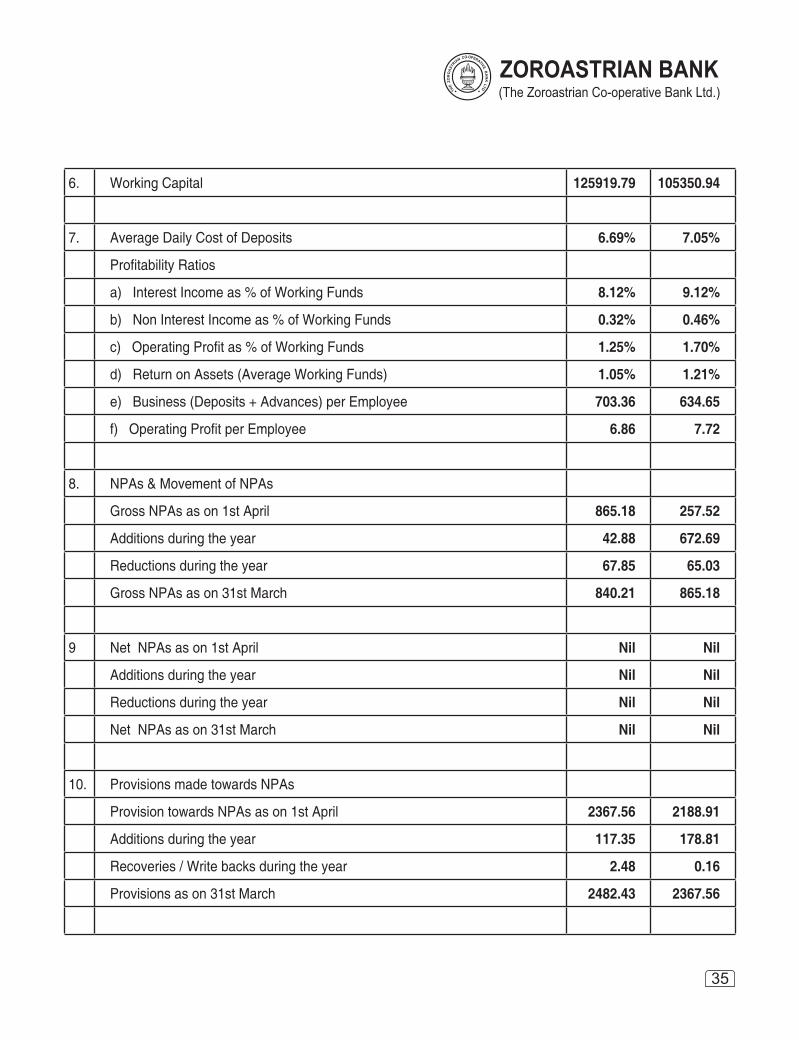

I. Key Financial Highlights and Ratios:The following charts indicate the Key Financial performance indicators of your Bank for the current year vis-a-vis the previous year.

a) Financial Indicators: (Rs. in lakhs)

F.Y. 2016-17 F.Y. 2015-16Total Business Mix 161069.7 147238.03Deposits 108024.55 88713.82Advances 53045.15 58524.21Investments 39767.12 28005.9Paid up Capital 1412.36 1440.11Reserves & surplus 13310.24 12379.3Total Income 10636.1 10092.51Total Expenditure 9065.6 8302.25Gross NPA’s 840.21 865.18% of NPA’s to Loans & Advances 1.58 1.48Non Performing Inv. 200 200Net NPA’s Nil NilCRAR 17.99% 17.12%No: of Branches 18 18

b) Ratios:

FY 2016-17 FY 2015-161. Capital to Risk Weighted Assets 17.99% 17.12%2. Cost of Deposits 6.69% 7.05%3. Yield on Advances 11.92% 12.45%4. Yield on Investments 6.86% 7.11%5. Net Interest Margin 2.64% 2.97%6. Return on Average Assets 1.05% 1.21%7. Staff Cost to Total Income 13.60% 13.59%8. Staff Cost to Total Expenditure 15.95% 16.53%

c) Appropriations:

Thecharthereinbelowdepicts theappropriationsmadeoutofNetProfitsof theBank for thecurrentfinancialyear incomparison to the previous year. The Board of Directors recommends the following appropriations out of the current year’s NetProfitfortheapprovaloftheAGM.

90th Annual Report 2016-2017

8

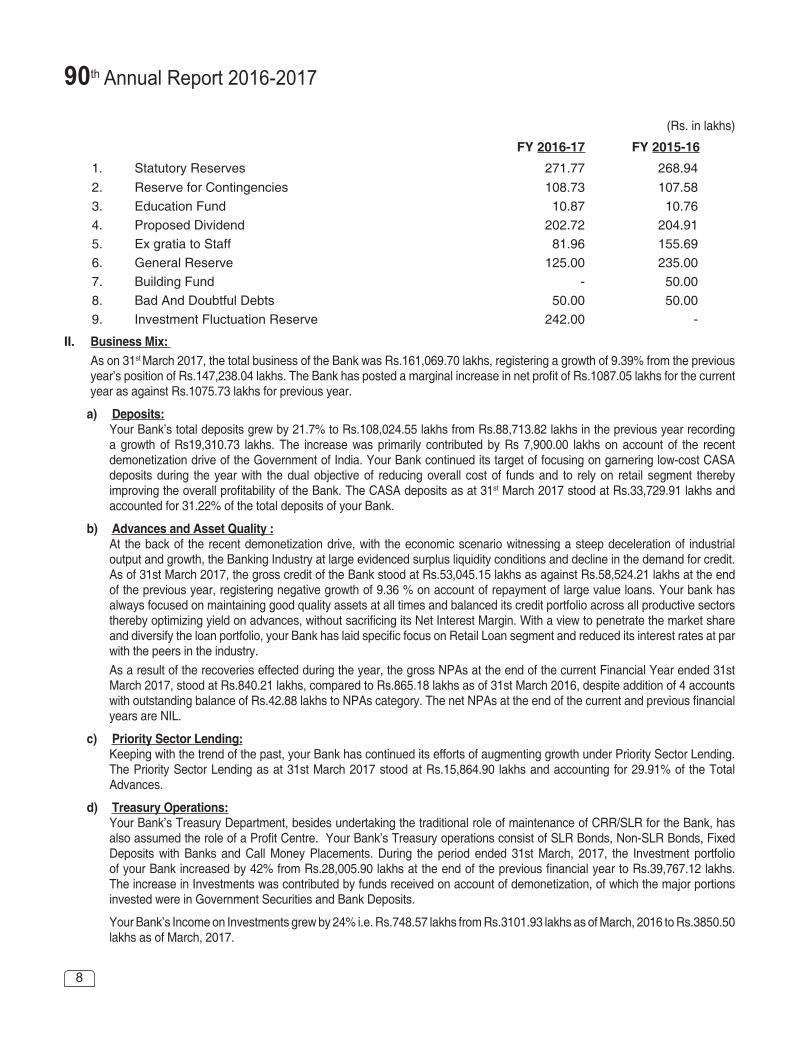

(Rs. in lakhs)

FY 2016-17 FY 2015-161. Statutory Reserves 271.77 268.942. Reserve for Contingencies 108.73 107.583. Education Fund 10.87 10.764. Proposed Dividend 202.72 204.915. Ex gratia to Staff 81.96 155.696. General Reserve 125.00 235.007. Building Fund - 50.008. Bad And Doubtful Debts 50.00 50.009. Investment Fluctuation Reserve 242.00 -

II. Business Mix: As on 31st March 2017, the total business of the Bank was Rs.161,069.70 lakhs, registering a growth of 9.39% from the previous year’spositionofRs.147,238.04lakhs.TheBankhaspostedamarginalincreaseinnetprofitofRs.1087.05lakhsforthecurrentyear as against Rs.1075.73 lakhs for previous year.

a) Deposits:Your Bank’s total deposits grew by 21.7% to Rs.108,024.55 lakhs from Rs.88,713.82 lakhs in the previous year recording a growth of Rs19,310.73 lakhs. The increase was primarily contributed by Rs 7,900.00 lakhs on account of the recent demonetization drive of the Government of India. Your Bank continued its target of focusing on garnering low-cost CASA deposits during the year with the dual objective of reducing overall cost of funds and to rely on retail segment thereby improvingtheoverallprofitabilityoftheBank.TheCASAdepositsasat31st March 2017 stood at Rs.33,729.91 lakhs and accounted for 31.22% of the total deposits of your Bank.

b) Advances and Asset Quality :At the back of the recent demonetization drive, with the economic scenario witnessing a steep deceleration of industrial output and growth, the Banking Industry at large evidenced surplus liquidity conditions and decline in the demand for credit. As of 31st March 2017, the gross credit of the Bank stood at Rs.53,045.15 lakhs as against Rs.58,524.21 lakhs at the end of the previous year, registering negative growth of 9.36 % on account of repayment of large value loans. Your bank has always focused on maintaining good quality assets at all times and balanced its credit portfolio across all productive sectors therebyoptimizingyieldonadvances,withoutsacrificingitsNetInterestMargin.Withaviewtopenetratethemarketshareanddiversifytheloanportfolio,yourBankhaslaidspecificfocusonRetailLoansegmentandreduceditsinterestratesatparwith the peers in the industry. As a result of the recoveries effected during the year, the gross NPAs at the end of the current Financial Year ended 31st March 2017, stood at Rs.840.21 lakhs, compared to Rs.865.18 lakhs as of 31st March 2016, despite addition of 4 accounts withoutstandingbalanceofRs.42.88lakhstoNPAscategory.ThenetNPAsattheendofthecurrentandpreviousfinancialyears are NIL.

c) Priority Sector Lending:Keeping with the trend of the past, your Bank has continued its efforts of augmenting growth under Priority Sector Lending. The Priority Sector Lending as at 31st March 2017 stood at Rs.15,864.90 lakhs and accounting for 29.91% of the Total Advances.

d) Treasury Operations:Your Bank’s Treasury Department, besides undertaking the traditional role of maintenance of CRR/SLR for the Bank, has alsoassumedtheroleofaProfitCentre.YourBank’sTreasuryoperationsconsistofSLRBonds,Non-SLRBonds,FixedDeposits with Banks and Call Money Placements. During the period ended 31st March, 2017, the Investment portfolio ofyourBankincreasedby42%fromRs.28,005.90lakhsattheendofthepreviousfinancialyeartoRs.39,767.12lakhs.The increase in Investments was contributed by funds received on account of demonetization, of which the major portions invested were in Government Securities and Bank Deposits.

Your Bank’s Income on Investments grew by 24% i.e. Rs.748.57 lakhs from Rs.3101.93 lakhs as of March, 2016 to Rs.3850.50 lakhs as of March, 2017.

ZOROASTRIAN BANK(The Zoroastrian Co-operative Bank Ltd.)

9

The debt market yields softened on account of consistent monetary intervention by RBI during the year by reduction of Repo andRevReporates,toboostmarketsentimentsandeaseliquiditypressures,onthebackdropofeasinginflation.Your Bank takes investments decisions looking at the market scenario and with a view to optimize the overall earnings on the investment portfolio. Your Bank has in place an Investment Policy which is reviewed in accordance with the guidelines issued by RBI and the Treasury Department of your Bank functions within the framework of RBI policy guidelines and the Treasury and Risk policy framework of your Bank.

III. Profit and Profitability:Notwithstandingtheslowdowninthebusinessgrowth,yourBankhasregisteredanoperatingprofitofRs.1570.49lakhsfortheFinancial Year ended 31stMarch,2017asagainsttheoperatingprofitofRs.1790.26lakhsinthepreviousyear.

IV. Dividend :Your Directors are pleased to recommend maximum permissible dividend @15% (i. e @ Rs 3.75 per share of Rs 25 each) involving a total outlay of Rs.2,02,71,860/- for the year under review.

V. Net Worth and Capital Adequacy : The Net Worth of your Bank improved to Rs.14,727.26 lakhs in the current year as against Rs.13,823.58 lakhs in the previous year which works out to an increase of Rs.903.68 lakhs i. e. 6.54% growth over the previous year. TheCapitalAdequacyratioofyourBankwasreflectedatalevelof17.99%comparedto17.12%inthepreviousyearasagainstRBI’s stipulation of 9%. TierIandTierIICapitalforthelasttwoyearsarereflectedasunder:

Particulars 2016-17 2015-16Tier I Capital 15.35% 14.79%

Tier II Capital 2.64% 2.33%

VI. Risk Management :Risk Management systems are well established in your Bank. Your Bank has given due importance to managing and mitigating riskinclusiveofOperational,CreditandMarketrisksinachievinglongtermfinancialstabilityandsuccess.YourBank’srisksphilosophy involves developing and maintaining a healthy Balance Sheet. Risk Management at your Bank includes risk identification, risk assessment, riskmeasurement and riskmitigation and itsmain objective is tominimise negative impactonProfitabilityandCapital.YourBankhaslaiddownpoliciesandprocedurestomeasure,assess,monitorandmanageriskssystematically across all portfolios. The Board of Directors of your Bank regularly reviews the Bank’s Risk Management policies/practices under Credit, Market and Operational risks. The Credit Committee of the Board of Directors regularly monitors the Non-Performing and Slow Moving accounts at periodic intervals, where the progress account-wise in recovery and legal steps for recovery are reported. Your Bank also has a separate monitoring cell to closely monitor the operations and identify delinquencies in the borrowers’ accounts, and to initiate suitable remedial measures. Under Operational Risks, your Bank has a dedicated KYC/AML Department for effective transaction monitoring with a view to prevent misuse of banking channels. Your Bank periodically monitors the risk categorization for its clientele, ensures that correct risk categories are applied and submits periodical statements to the Board. Also, transaction of higher values are thoroughly monitored and reported to Financial Intelligence Unit (FIU) by way of Cash Transaction Reports (CTR) and Suspicious Transaction Reports(STR).AllaccountsareopenedwiththoroughverificationofKYCdocumentsandyourBankadherestoallKYC/AMLguidelines issued by Reserve Bank of India from time to time.

VII. Asset and Liability Management:Asset and Liability Management occupy prime focus in the overall management of Financial Institutions. ALM practices require specializedknowledgeandskillstoefficientlyhandledynamicandevolvingchallengesintheFinancialSector.YourBankhasaneffectiveAssetLiabilityCommittee(ALCO))toreviewonaregularbasistheassetsandliabilitiesprofile,liquidity management and interest rate sensitivity and due importance is given to Asset Liability Management reports and remedialactionisinitiatedfromtimetotime.YourBankhasinplaceawelldefinedcreditpolicywithexplicitrulesandguidelinesrelating to grant of credit, which aims at following sound lending practices.The Asset Liability Management Committee of your Bank oversees the Interest Rate and Liquidity Risks, reviews the components ofBalanceSheetsandsetsupbenchmarks forefficientmanagementof theserisks.TheCommittee reviews thepatternofgrowth of liability products vis-a-vis credit growth and liquidity management and approves appropriate pricing of Bank’s products.

90th Annual Report 2016-2017

10

VIII. Foreign Exchange AD –II License :Your Bank undertakes foreign exchange transactions as a money changer i.e. Sale and Purchase of Foreign Exchange, Remittances, etc. Your Bank has initiated tie-ups with renowned Private Sector and Public Sector Banks to simplify and expedite the remittances thereby helping existing clients and also enabling your Bank to widen its client base. Your Bank, in addition to the above facilities also has tie-up arrangements with Private and Public Sector Banks for issuance of Bank Guarantees and establishing Letters of Credit on behalf of your Bank’s clientele engaged in imports and exports.

IX. Audit and Inspection :The Audit and Inspection Department of the Bank is instrumental in undertaking audit across all the branches and departments of the Bank. The audit process is evaluated every year to ensure that all new RBI guidelines and statutory requirements as also technological enhancements taking place in the banking industry are taken care of, by incorporating the required changes in the audit and inspection process. Your Bank also undertakes Information Systems (IS) audit to mitigate IT risks and to ensure that Information Systems in use are being managed prudently.Your Bank has a sound system in place for internal/concurrent audit. It provides the management with accurate information on the effectiveness of risk management and internal controls including regulatory compliance by the Bank. Your Bank has a dedicatedInternalAuditdepartmentwithateamofqualifiedandexperiencedindividuals.TheInternalAuditteamundertakesacomprehensive risk based audit of all operating units of your Bank in line with regulatory guidelines. The Audit Committee of the Board of Directors oversees and provides directions to the internal audit/inspection machinery and to the executives of the Bank. The Audit Committee of the Board of Directors also reviews the implementation of the guidelines issued by RBI and submits information to the Board of Directors at periodic intervals. Further, as per the requirements of RBI, theInvestmentportfolioofyourBankisauditedbytheinternalauditorofyourBankandaquarterlycertificateofverificationisforwarded to RBI.Your Bank also ensures timely submission of various returns to the concerned authorities. During the year, RBI carried out on-site inspection of the Bank under Section 35 of the Banking Regulation Act with respect to thefinancialpositionasonMarch31,2016.ThereportfromRBIisreceivedandisbeingattendedtoforcompliance.

X. Human Resource Management :The HRD Department plays a key role of nurturing and developing the Bank’s manpower, synergizing between individual aspirations of employees and the Bank’s business goals and thus ensuring effective utilization of the Bank’s Human Resources. Recruitingtherighttalentfortherightposition,recognizingandrewardingperformers,fixingstaffaccountabilityincasesoflapses/negligence, initiating corrective action against non-performers and maintaining harmonious industrial relations are some of the areas necessitating intervention of the HRD Department.Your Bank’s H.R. vision is built around the principles of inclusiveness, empowerment and development. Its people are its strength and accordingly your Bank constantly pursues effectively to ensure its key personnel are provided adequate encouragement and the required motivation in developing a second line of Management and succession planning. In line with its Vision, your Bank repeatedly arranges for training programs for employees at all levels covering training programs on specialized bankingfields.YourBankalsoorganizestrainingprograms,bothin-houseandbyoutsourcing,envelopingallfacetsofbankingoperations regularly, including workshops for development of soft skills.

XI. Information Technology :Your Bank has been offering innovative products to customers with the objective of enabling smooth banking transactions for its customers. Your Bank’s technology strategies have evolved in line with the customer expectations from time to time. Your Bank provides robust and customer friendly Core Banking platform to its customers, which is periodically upgraded in line with the evolving customer requirements. YourBanklayssignificantemphasisonDigitalizationandexcellenceinoperationsthrougheffectiveI.T.products,resultingintoreductionintheturnaroundtimeandextendedbenefitstoyourBank’scustomers.

XII. Digital Initiatives:Realising the importance of technology in today’s era, changing customer expectations and competition from peers, your Bank has applied to Reserve Bank of India for Internet Banking (Transaction facility) as well as Mobile Banking. Decision from RBI is awaited. Your Bank also has a robust I.T. tool for timely and accurate management information data.

ZOROASTRIAN BANK(The Zoroastrian Co-operative Bank Ltd.)

11

XIII. Customer Relationship Management :Customer Relationship Management has always been integral to your Bank. Your Bank has always been the frontrunner in catering to the needs of customers from time to time. Your Bank constantly ensures that the customer’s demands are served with high quality service across all branches. YourBankhasaGeneralManagerdesignatedas“NodalOfficerforCustomerServiceandGrievanceRedressal”providingabetteravenueforredressalofgrievancesofCustomers.ThenameofthedesignateNodalOfficerforCustomerGrievanceshas been displayed on the Bank’s website as well as displayed on the notice boards of your Bank’s respective branches for quick redressal of grievances of the customers in terms of the recommendations of Damodaran Committee on Customer Service w. e. f. 21/08/2012. The average grievance redressal period is 14 days within which grievances, if any, are redressed to the complete satisfaction of the customers.

XIV. Ethics and Business Conduct :Your Bank has been showing its commitments with the highest professional and ethical standards regardless of its growth and reach. The idea is to anchor, promote, nurture and institutionalize the Bank’s positive ethical culture of being “The Bank that is Big on Tradition and Trust.”

XV. Branch Expansion:With a view to expanding your Bank’s services, market recognition and reaching a wide range of customers and stakeholders, your Bank has applied to Reserve Bank of India to accord approval for opening of 10 new branches. RBI approval in the matter is awaited.

XVI. Awards and Accolades:During the year under review, your Bank has been awarded the Second Prize in the segment of Deposits amongst the Co-operative Banks in the category of Rs.300.00 Crores to Rs.1500.00 Crores for the Financial Year 2015-16. The Award was presented by The Brihan Mumbai Nagari Sahakari Bank Association Ltd.

XVII. Marching Towards Centenary Year:You are aware that your Bank has completed 90 Glorious Years of its existence and is marching towards the Centenary Year. With its humble beginnings on 17th June, 1927 as a Co-operative Credit Society, your Bank has come a long way since, to emerge as one of the leading Co-operative Bank amongst the peers in the industry. With the total business mix at around Rs.43,245.82 lakhs in March 2005, your Bank’s business has grown manifold to Rs.161,069.70 lakhs on 31st March, 2017, which is an increase of nearly 272.45% in last twelve years. Inthisjourney,yourBankhasgrownfromstrengthtostrengthandtrulyreflectstheimageofasoundandawellmanagedBank.

XVIII. Auditors:Your Board of Directors is thankful to M/s. M P Chitale & Co – Chartered Accountants appointed as Statutory Auditors and to Mr. Homiyar Madan of H.F.K. Madan & Co. for their support and suggestions made during the course of audit of the Bank.

XIX. Acknowledgements:YourBoardofDirectors records itsappreciation for theunstintedco-operationextendedby theOfficersof theReserveBank of India, especially the Urban Banks Department, The Central Registrar of Co-operative Societies, New Delhi, The Commissioners for Co-operation and Registrar of Co-operative Societies for the State of Maharashtra and Gujarat and National Federation of Urban Co-operative Banks for their contribution from time to time.Your Board of Directors appreciates the deep involvement of its shareholders and clientele and for their ongoing support and loyalty and their active participation and contribution.Your Board of Directors is thankful to the Management and Staff at all levels for their dedication and devotion to duty with sincerity.

For and on behalf of the Board of Directors

HOMAI A. DARUWALLACHAIRPERSON

90th Annual Report 2016-2017

12

CORPORATE GOVERNANCE REPORT

I. Bank’s Philosophy on Corporate Governance:

Your Bank believes in adopting and adhering to best recognized Corporate Governance Policies right from its inception. Your Bank shall continue its endeavour to enhance its shareholders’ value by protecting their interest by ensuring performance at all levels, and maximizing returns with optimal use of resources in its pursuit of excellence.

Your Bank understands and respects its role and responsibility to stake holders comprising shareholders, customers and society at large by enhancing its good governance practices, based on fairness, transparency and accountability along with a disciplined approach to achieving excellence in all spheres of activities. Your Bank complies with not only the statutory requirements, but also voluntarily formulates and adheres to a set of strong Corporate Governance practices.Your Bank seeks assistance from a few Directors / their relatives in the nature of Legal reference, Computer systems as well as allotting printing jobs. Your Bank also occupies premises for its back office which belongs to a Trust where a Director is a Trustee.

II. Board of Directors:

Your Bank has a broad based Board of Directors, constituted in compliance with the Multi State Co-operative Societies Act, 2002. The Board consists of eminent persons with considerable professional expertise and experience in Banking, Finance, Law, Information Technology and other fields. Your Board of Directors is committed to adopt good Corporate Governancepractices in letter and spirit.

Your Bank is committed to ensuring that the Bank’s Board of Directors meets regularly, provides effective leadership and insight in business and functional matters and monitors the Bank’s performance.

Your Board of Directors is collectively responsible for the growth of your bank and confirms as under:

1. that in the preparation of the annual accounts, the applicable accounting standards and policies have been followed along with proper explanation; so as to give a true and fair view of the state of affairs of the bank at the end of the financial year and of the profit of the bank for that period.

2. that proper care for the maintenance of adequate accounting records, in accordance with the provisions of the Banking Regulation Act, 1949 for safeguarding the assets of the Bank and for preventing and detecting fraud and other irregularities;

3. that they have prepared the annual accounts on a going concern basis;

4. that they have laid down internal financial controls to be followed by the Bank and that such internal financial controls are adequate and were operating effectively; and

5. that they have devised proper systems to ensure compliance with the provisions of all applicable laws and that such systems were adequate and operating effectively.

III. Composition of Committees of Directors:

Your Board has constituted various Committees of Directors to take informed decisions in the best interests of your Bank. These committees monitor the activities falling within their terms of reference.

The Board has constituted the following Committees of Directors for effective control and supervision of operations of your Bank.

ZOROASTRIAN BANK(The Zoroastrian Co-operative Bank Ltd.)

13

1. The Enrolment of Members and Redressal of Grievances of Share-holders/Customers Committee of Board of Directors.

2. The Audit and Risk Management Committee of Board of Directors.

3. The Information Technology Committee of Board of Directors.

4. The Board Governance and Human Resources Committee of Board of Directors.

5. The Credit Committee of Board of Directors.

6. The Investment Committee of Board of Directors

The Board of Directors met regularly during the financial year 2016-17. The Board met 13 times during the year, with an average attendance of over 84% of the Directors. The various Committees of the Board of Directors as mentioned above also met regularly. There were in all 11 meetings of The Enrolment of Members and Redressal of Grievances of Share-holders / Customers Committee, 4 meetings of the Audit and Risk Management Committee, 4 meetings of Information Technology Committee, 4 meetings of The Board Governance and Human Resources Committee, 13 meetings of Credit Committee and 4 meetings of The Investment Committee.

IV. Shareholders Information:

Your Bank is a Multi-state Scheduled Urban Co-operative Bank with its Corporate Office at Mumbai and its area of operation is now Greater Mumbai, Municipal limits of Pune City, Thane District, and Municipal areas of Navi Mumbai in the State of Maharashtra and the whole of Surat District including the Municipal Corporation areas of Surat, Bharuch, Baroda, Anand, Nadiad, Ahmedabad, Navsari and Valsad in the State of Gujarat. As on March 31, 2017, your Bank has 9708 number of Members.

V. Means of Communication:

Your Bank strongly believes that all stakeholders should have access to complete information on the Bank’s activity, performance and product initiatives. Annual results of the Bank are published in English and Regional newspapers as well as also displayed on the Bank’s Website (www.zoroastrianbank.com). Each year, the Annual Report is sent to all Shareholders. The Bank’s Website displays, inter alia, official news releases of the Bank, Financial highlights and details of various product offerings.

For and on behalf of the Board of Directors

HOMAI A. DARUWALLA

CHAIRPERSON

90th Annual Report 2016-2017

14

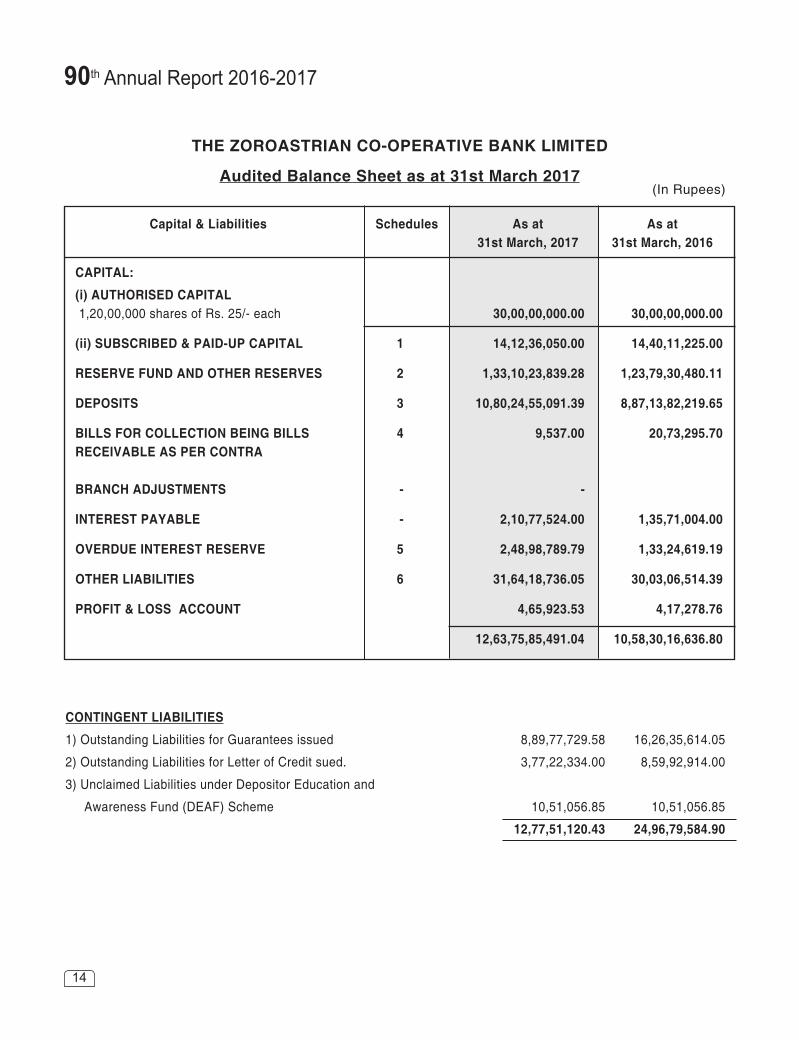

THE ZOROASTRIAN CO-OPERATIVE BANK LIMITED

Audited Balance Sheet as at 31st March 2017

Capital & Liabilities Schedules As at As at 31st March, 2017 31st March, 2016

CAPITAL:

(i) AUTHORISED CAPITAL 1,20,00,000 shares of Rs. 25/- each 30,00,00,000.00 30,00,00,000.00

(ii) SUBSCRIBED & PAID-UP CAPITAL 1 14,12,36,050.00 14,40,11,225.00

RESERVE FUND AND OTHER RESERVES 2 1,33,10,23,839.28 1,23,79,30,480.11

DEPOSITS 3 10,80,24,55,091.39 8,87,13,82,219.65

BILLS FOR COLLECTION BEING BILLS 4 9,537.00 20,73,295.70 RECEIVABLE AS PER CONTRA

BRANCH ADJUSTMENTS - -

INTEREST PAYABLE - 2,10,77,524.00 1,35,71,004.00

OVERDUE INTEREST RESERVE 5 2,48,98,789.79 1,33,24,619.19

OTHER LIABILITIES 6 31,64,18,736.05 30,03,06,514.39

PROFIT & LOSS ACCOUNT 4,65,923.53 4,17,278.76

12,63,75,85,491.04 10,58,30,16,636.80

CONTINGENT LIABILITIES

1) Outstanding Liabilities for Guarantees issued 8,89,77,729.58 16,26,35,614.05

2) Outstanding Liabilities for Letter of Credit sued. 3,77,22,334.00 8,59,92,914.00

3) Unclaimed Liabilities under Depositor Education and

Awareness Fund (DEAF) Scheme 10,51,056.85 10,51,056.85

12,77,51,120.43 24,96,79,584.90

(In Rupees)

ZOROASTRIAN BANK(The Zoroastrian Co-operative Bank Ltd.)

15

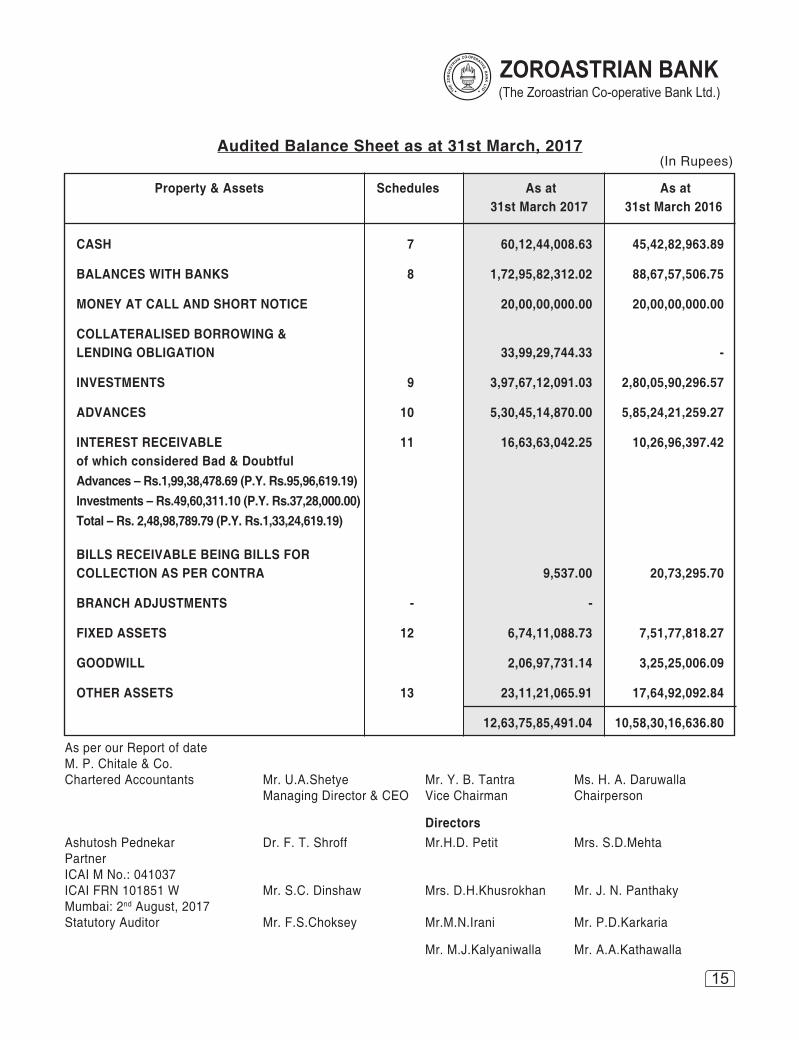

Audited Balance Sheet as at 31st March, 2017(In Rupees)

Property & Assets Schedules As at As at 31st March 2017 31st March 2016

CASH 7 60,12,44,008.63 45,42,82,963.89

BALANCES WITH BANKS 8 1,72,95,82,312.02 88,67,57,506.75

MONEY AT CALL AND SHORT NOTICE 20,00,00,000.00 20,00,00,000.00

COLLATERALISED BORROWING &LENDING OBLIGATION 33,99,29,744.33 -

INVESTMENTS 9 3,97,67,12,091.03 2,80,05,90,296.57

ADVANCES 10 5,30,45,14,870.00 5,85,24,21,259.27

INTEREST RECEIVABLE 11 16,63,63,042.25 10,26,96,397.42of which considered Bad & Doubtful Advances – Rs.1,99,38,478.69 (P.Y. Rs.95,96,619.19) Investments – Rs.49,60,311.10 (P.Y. Rs.37,28,000.00) Total – Rs. 2,48,98,789.79 (P.Y. Rs.1,33,24,619.19)

BILLS RECEIVABLE BEING BILLS FORCOLLECTION AS PER CONTRA 9,537.00 20,73,295.70

BRANCH ADJUSTMENTS - -

FIXED ASSETS 12 6,74,11,088.73 7,51,77,818.27

GOODWILL 2,06,97,731.14 3,25,25,006.09

OTHER ASSETS 13 23,11,21,065.91 17,64,92,092.84

12,63,75,85,491.04 10,58,30,16,636.80

As per our Report of dateM. P. Chitale & Co.Chartered Accountants Mr. U.A.Shetye Mr. Y. B. Tantra Ms. H. A. Daruwalla Managing Director & CEO Vice Chairman Chairperson

DirectorsAshutosh Pednekar Dr. F. T. Shroff Mr.H.D. Petit Mrs. S.D.MehtaPartnerICAI M No.: 041037ICAI FRN 101851 W Mr. S.C. Dinshaw Mrs. D.H.Khusrokhan Mr. J. N. PanthakyMumbai: 2nd August, 2017Statutory Auditor Mr. F.S.Choksey Mr.M.N.Irani Mr. P.D.Karkaria

Mr. M.J.Kalyaniwalla Mr. A.A.Kathawalla

90th Annual Report 2016-2017

16

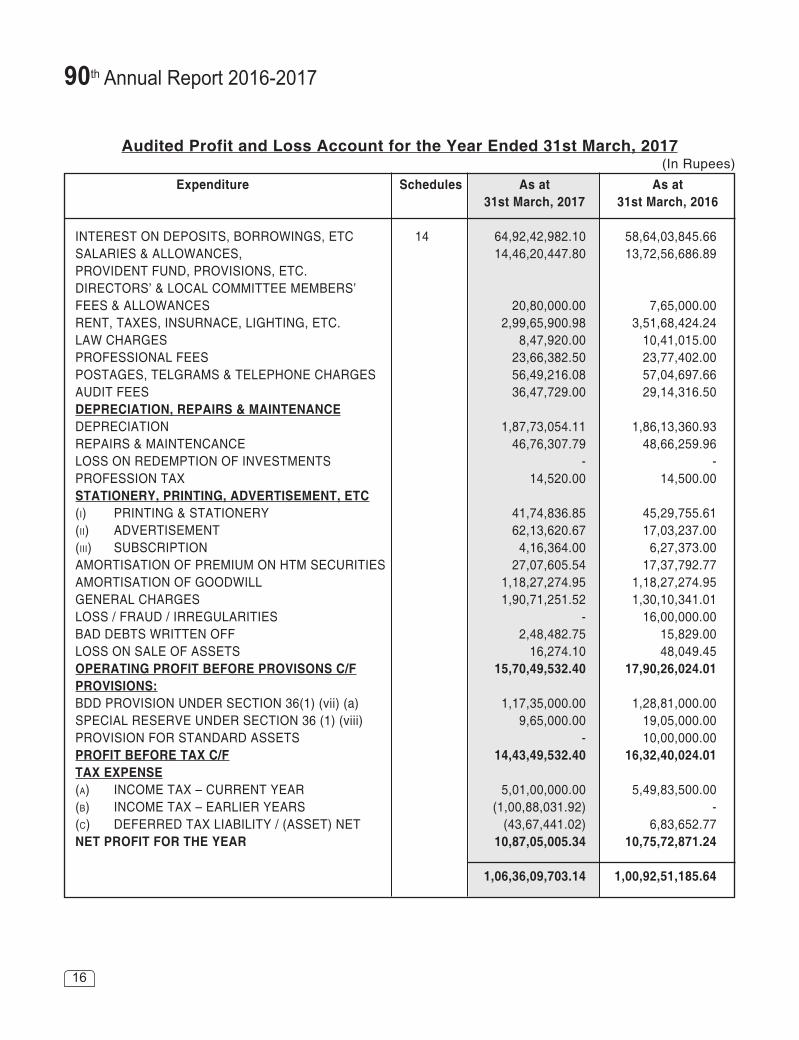

Audited Profit and Loss Account for the Year Ended 31st March, 2017

Expenditure Schedules As at As at 31st March, 2017 31st March, 2016

INTEREST ON DEPOSITS, BORROWINGS, ETC 14 64,92,42,982.10 58,64,03,845.66SALARIES & ALLOWANCES, 14,46,20,447.80 13,72,56,686.89PROVIDENT FUND, PROVISIONS, ETC. DIRECTORS’ & LOCAL COMMITTEE MEMBERS’ FEES & ALLOWANCES 20,80,000.00 7,65,000.00RENT, TAXES, INSURNACE, LIGHTING, ETC. 2,99,65,900.98 3,51,68,424.24LAW CHARGES 8,47,920.00 10,41,015.00PROFESSIONAL FEES 23,66,382.50 23,77,402.00POSTAGES, TELGRAMS & TELEPHONE CHARGES 56,49,216.08 57,04,697.66AUDIT FEES 36,47,729.00 29,14,316.50DEPRECIATION, REPAIRS & MAINTENANCE DEPRECIATION 1,87,73,054.11 1,86,13,360.93REPAIRS & MAINTENCANCE 46,76,307.79 48,66,259.96LOSS ON REDEMPTION OF INVESTMENTS - -PROFESSION TAX 14,520.00 14,500.00STATIONERY, PRINTING, ADVERTISEMENT, ETC (I) PRINTING & STATIONERY 41,74,836.85 45,29,755.61(II) ADVERTISEMENT 62,13,620.67 17,03,237.00(III) SUBSCRIPTION 4,16,364.00 6,27,373.00AMORTISATION OF PREMIUM ON HTM SECURITIES 27,07,605.54 17,37,792.77AMORTISATION OF GOODWILL 1,18,27,274.95 1,18,27,274.95GENERAL CHARGES 1,90,71,251.52 1,30,10,341.01LOSS / FRAUD / IRREGULARITIES - 16,00,000.00BAD DEBTS WRITTEN OFF 2,48,482.75 15,829.00LOSS ON SALE OF ASSETS 16,274.10 48,049.45OPERATING PROFIT BEFORE PROVISONS C/F 15,70,49,532.40 17,90,26,024.01PROVISIONS: BDD PROVISION UNDER SECTION 36(1) (vii) (a) 1,17,35,000.00 1,28,81,000.00SPECIAL RESERVE UNDER SECTION 36 (1) (viii) 9,65,000.00 19,05,000.00PROVISION FOR STANDARD ASSETS - 10,00,000.00PROFIT BEFORE TAX C/F 14,43,49,532.40 16,32,40,024.01TAX EXPENSE (A) INCOME TAX – CURRENT YEAR 5,01,00,000.00 5,49,83,500.00(B) INCOME TAX – EARLIER YEARS (1,00,88,031.92) -(C) DEFERRED TAX LIABILITY / (ASSET) NET (43,67,441.02) 6,83,652.77NET PROFIT FOR THE YEAR 10,87,05,005.34 10,75,72,871.24

1,06,36,09,703.14 1,00,92,51,185.64

(In Rupees)

ZOROASTRIAN BANK(The Zoroastrian Co-operative Bank Ltd.)

17

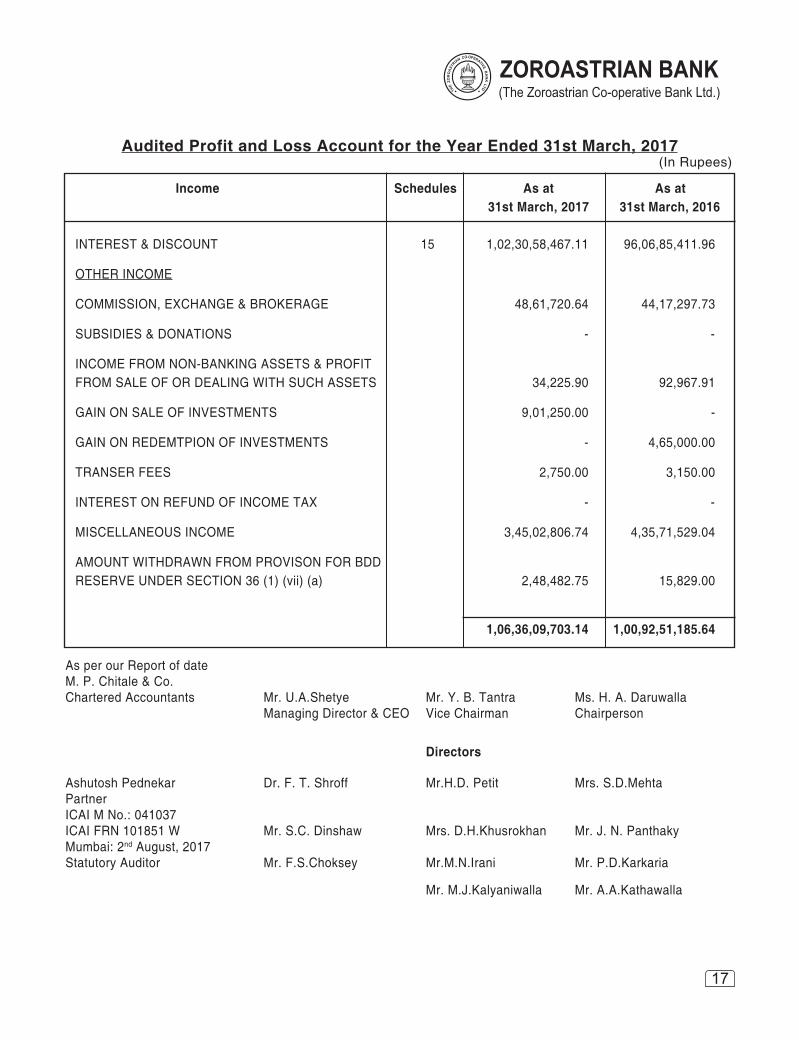

Audited Profit and Loss Account for the Year Ended 31st March, 2017

Income Schedules As at As at 31st March, 2017 31st March, 2016

INTEREST & DISCOUNT 15 1,02,30,58,467.11 96,06,85,411.96

OTHER INCOME

COMMISSION, EXCHANGE & BROKERAGE 48,61,720.64 44,17,297.73

SUBSIDIES & DONATIONS - -

INCOME FROM NON-BANKING ASSETS & PROFIT FROM SALE OF OR DEALING WITH SUCH ASSETS 34,225.90 92,967.91

GAIN ON SALE OF INVESTMENTS 9,01,250.00 -

GAIN ON REDEMTPION OF INVESTMENTS - 4,65,000.00

TRANSER FEES 2,750.00 3,150.00

INTEREST ON REFUND OF INCOME TAX - -

MISCELLANEOUS INCOME 3,45,02,806.74 4,35,71,529.04

AMOUNT WITHDRAWN FROM PROVISON FOR BDD RESERVE UNDER SECTION 36 (1) (vii) (a) 2,48,482.75 15,829.00

1,06,36,09,703.14 1,00,92,51,185.64

(In Rupees)

As per our Report of dateM. P. Chitale & Co.Chartered Accountants Mr. U.A.Shetye Mr. Y. B. Tantra Ms. H. A. Daruwalla Managing Director & CEO Vice Chairman Chairperson

Directors

Ashutosh Pednekar Dr. F. T. Shroff Mr.H.D. Petit Mrs. S.D.MehtaPartnerICAI M No.: 041037ICAI FRN 101851 W Mr. S.C. Dinshaw Mrs. D.H.Khusrokhan Mr. J. N. PanthakyMumbai: 2nd August, 2017Statutory Auditor Mr. F.S.Choksey Mr.M.N.Irani Mr. P.D.Karkaria

Mr. M.J.Kalyaniwalla Mr. A.A.Kathawalla

90th Annual Report 2016-2017

18

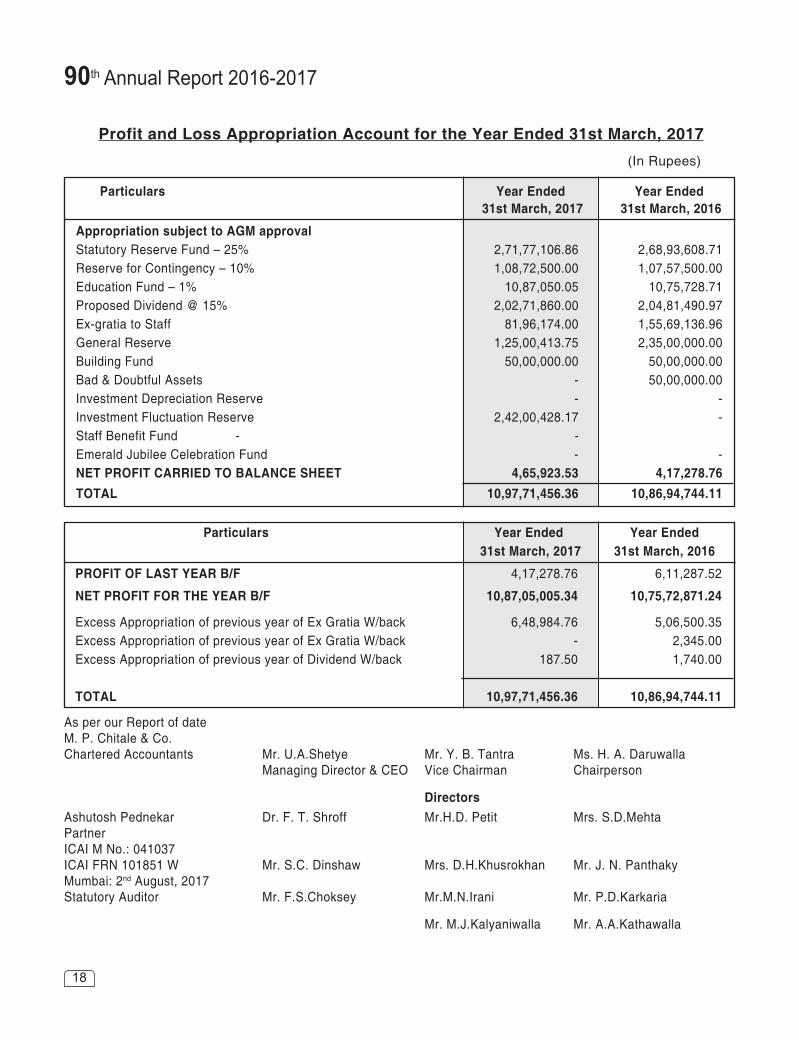

Profit and Loss Appropriation Account for the Year Ended 31st March, 2017 (In Rupees)

Particulars Year Ended Year Ended 31st March, 2017 31st March, 2016

Appropriation subject to AGM approval Statutory Reserve Fund – 25% 2,71,77,106.86 2,68,93,608.71Reserve for Contingency – 10% 1,08,72,500.00 1,07,57,500.00Education Fund – 1% 10,87,050.05 10,75,728.71Proposed Dividend @ 15% 2,02,71,860.00 2,04,81,490.97Ex-gratia to Staff 81,96,174.00 1,55,69,136.96General Reserve 1,25,00,413.75 2,35,00,000.00Building Fund 50,00,000.00 50,00,000.00Bad & Doubtful Assets - 50,00,000.00Investment Depreciation Reserve - -Investment Fluctuation Reserve 2,42,00,428.17 -Staff Benefit Fund - -Emerald Jubilee Celebration Fund - -NET PROFIT CARRIED TO BALANCE SHEET 4,65,923.53 4,17,278.76TOTAL 10,97,71,456.36 10,86,94,744.11

Particulars Year Ended Year Ended 31st March, 2017 31st March, 2016

PROFIT OF LAST YEAR B/F 4,17,278.76 6,11,287.52

NET PROFIT FOR THE YEAR B/F 10,87,05,005.34 10,75,72,871.24

Excess Appropriation of previous year of Ex Gratia W/back 6,48,984.76 5,06,500.35Excess Appropriation of previous year of Ex Gratia W/back - 2,345.00Excess Appropriation of previous year of Dividend W/back 187.50 1,740.00

TOTAL 10,97,71,456.36 10,86,94,744.11

As per our Report of dateM. P. Chitale & Co.Chartered Accountants Mr. U.A.Shetye Mr. Y. B. Tantra Ms. H. A. Daruwalla Managing Director & CEO Vice Chairman Chairperson

DirectorsAshutosh Pednekar Dr. F. T. Shroff Mr.H.D. Petit Mrs. S.D.MehtaPartnerICAI M No.: 041037ICAI FRN 101851 W Mr. S.C. Dinshaw Mrs. D.H.Khusrokhan Mr. J. N. PanthakyMumbai: 2nd August, 2017Statutory Auditor Mr. F.S.Choksey Mr.M.N.Irani Mr. P.D.Karkaria

Mr. M.J.Kalyaniwalla Mr. A.A.Kathawalla

ZOROASTRIAN BANK(The Zoroastrian Co-operative Bank Ltd.)

19

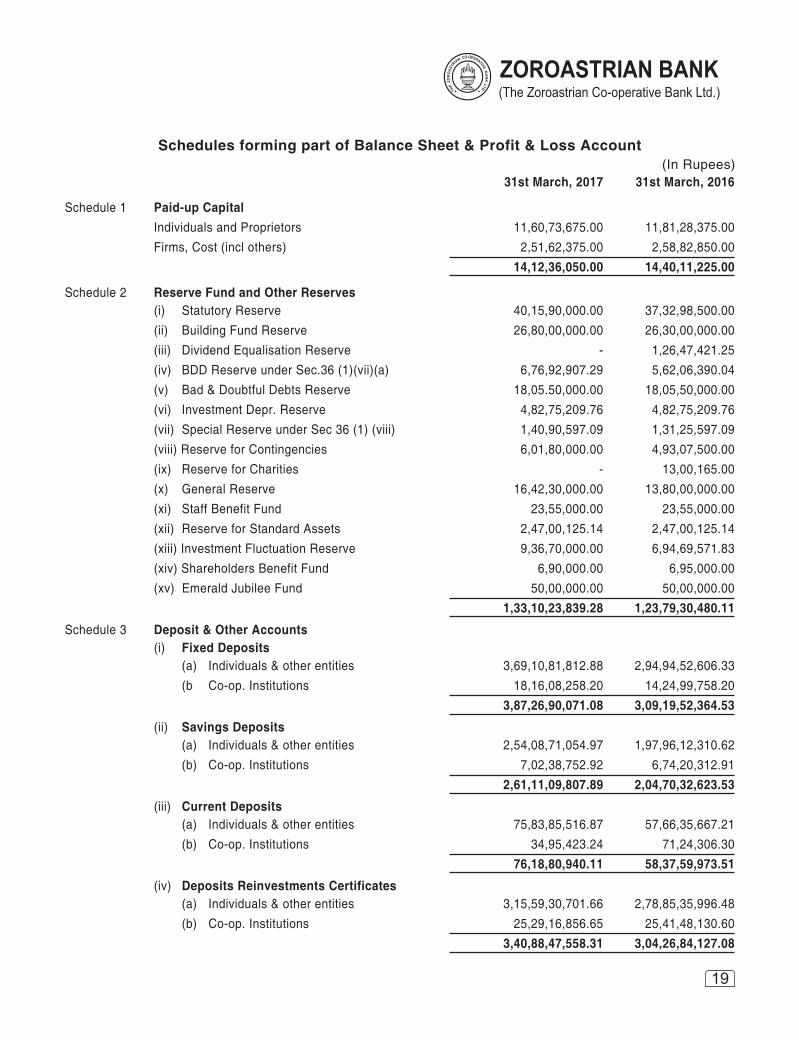

Schedules forming part of Balance Sheet & Profit & Loss Account(In Rupees)

31st March, 2017 31st March, 2016

Schedule 1 Paid-up Capital Individuals and Proprietors 11,60,73,675.00 11,81,28,375.00 Firms, Cost (incl others) 2,51,62,375.00 2,58,82,850.00 14,12,36,050.00 14,40,11,225.00

Schedule 2 Reserve Fund and Other Reserves (i) Statutory Reserve 40,15,90,000.00 37,32,98,500.00 (ii) Building Fund Reserve 26,80,00,000.00 26,30,00,000.00 (iii) Dividend Equalisation Reserve - 1,26,47,421.25 (iv) BDD Reserve under Sec.36 (1)(vii)(a) 6,76,92,907.29 5,62,06,390.04 (v) Bad & Doubtful Debts Reserve 18,05.50,000.00 18,05,50,000.00 (vi) Investment Depr. Reserve 4,82,75,209.76 4,82,75,209.76 (vii) Special Reserve under Sec 36 (1) (viii) 1,40,90,597.09 1,31,25,597.09 (viii) Reserve for Contingencies 6,01,80,000.00 4,93,07,500.00 (ix) Reserve for Charities - 13,00,165.00 (x) General Reserve 16,42,30,000.00 13,80,00,000.00 (xi) Staff Benefit Fund 23,55,000.00 23,55,000.00 (xii) Reserve for Standard Assets 2,47,00,125.14 2,47,00,125.14 (xiii) Investment Fluctuation Reserve 9,36,70,000.00 6,94,69,571.83 (xiv) Shareholders Benefit Fund 6,90,000.00 6,95,000.00 (xv) Emerald Jubilee Fund 50,00,000.00 50,00,000.00 1,33,10,23,839.28 1,23,79,30,480.11

Schedule 3 Deposit & Other Accounts (i) Fixed Deposits (a) Individuals & other entities 3,69,10,81,812.88 2,94,94,52,606.33 (b Co-op. Institutions 18,16,08,258.20 14,24,99,758.20 3,87,26,90,071.08 3,09,19,52,364.53

(ii) Savings Deposits (a) Individuals & other entities 2,54,08,71,054.97 1,97,96,12,310.62 (b) Co-op. Institutions 7,02,38,752.92 6,74,20,312.91 2,61,11,09,807.89 2,04,70,32,623.53

(iii) Current Deposits (a) Individuals & other entities 75,83,85,516.87 57,66,35,667.21 (b) Co-op. Institutions 34,95,423.24 71,24,306.30 76,18,80,940.11 58,37,59,973.51

(iv) Deposits Reinvestments Certificates (a) Individuals & other entities 3,15,59,30,701.66 2,78,85,35,996.48 (b) Co-op. Institutions 25,29,16,856.65 25,41,48,130.60 3,40,88,47,558.31 3,04,26,84,127.08

90th Annual Report 2016-2017

20

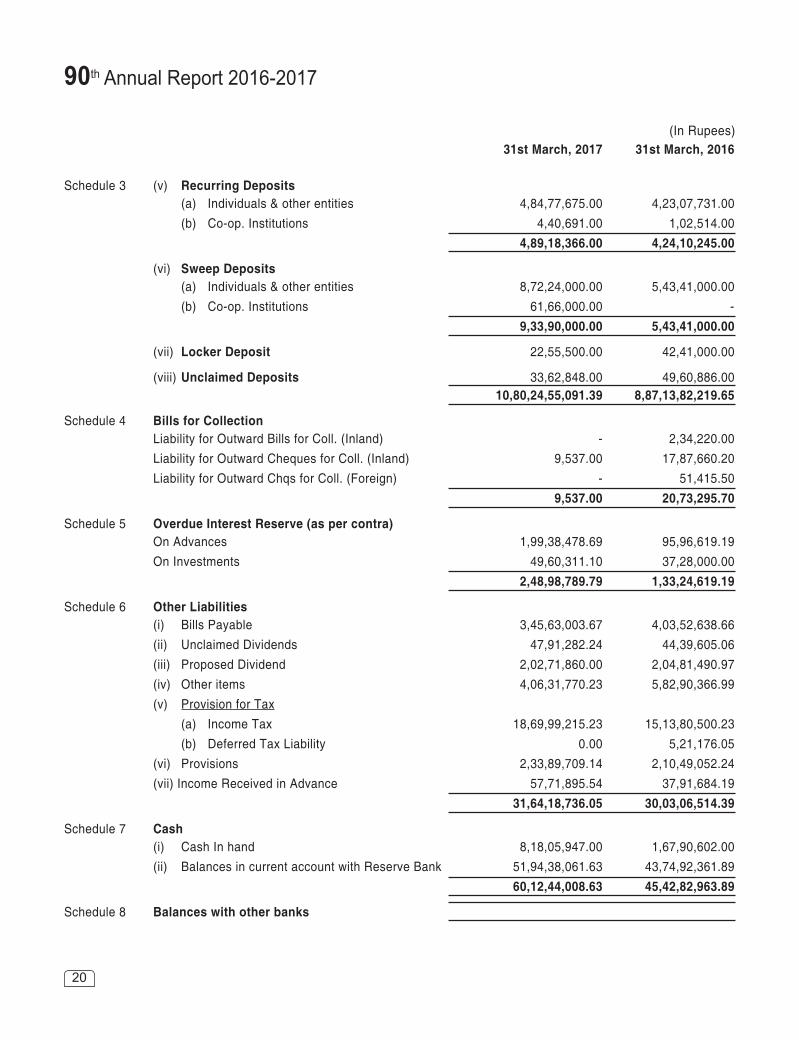

(In Rupees) 31st March, 2017 31st March, 2016

Schedule 3 (v) Recurring Deposits (a) Individuals & other entities 4,84,77,675.00 4,23,07,731.00 (b) Co-op. Institutions 4,40,691.00 1,02,514.00 4,89,18,366.00 4,24,10,245.00

(vi) Sweep Deposits (a) Individuals & other entities 8,72,24,000.00 5,43,41,000.00 (b) Co-op. Institutions 61,66,000.00 - 9,33,90,000.00 5,43,41,000.00

(vii) Locker Deposit 22,55,500.00 42,41,000.00

(viii) Unclaimed Deposits 33,62,848.00 49,60,886.00 10,80,24,55,091.39 8,87,13,82,219.65

Schedule 4 Bills for Collection Liability for Outward Bills for Coll. (Inland) - 2,34,220.00 Liability for Outward Cheques for Coll. (Inland) 9,537.00 17,87,660.20 Liability for Outward Chqs for Coll. (Foreign) - 51,415.50 9,537.00 20,73,295.70

Schedule 5 Overdue Interest Reserve (as per contra) On Advances 1,99,38,478.69 95,96,619.19 On Investments 49,60,311.10 37,28,000.00 2,48,98,789.79 1,33,24,619.19

Schedule 6 Other Liabilities (i) Bills Payable 3,45,63,003.67 4,03,52,638.66 (ii) Unclaimed Dividends 47,91,282.24 44,39,605.06 (iii) Proposed Dividend 2,02,71,860.00 2,04,81,490.97 (iv) Other items 4,06,31,770.23 5,82,90,366.99 (v) Provision for Tax (a) Income Tax 18,69,99,215.23 15,13,80,500.23 (b) Deferred Tax Liability 0.00 5,21,176.05 (vi) Provisions 2,33,89,709.14 2,10,49,052.24 (vii) Income Received in Advance 57,71,895.54 37,91,684.19 31,64,18,736.05 30,03,06,514.39

Schedule 7 Cash (i) Cash In hand 8,18,05,947.00 1,67,90,602.00 (ii) Balances in current account with Reserve Bank 51,94,38,061.63 43,74,92,361.89 60,12,44,008.63 45,42,82,963.89

Schedule 8 Balances with other banks

ZOROASTRIAN BANK(The Zoroastrian Co-operative Bank Ltd.)

21

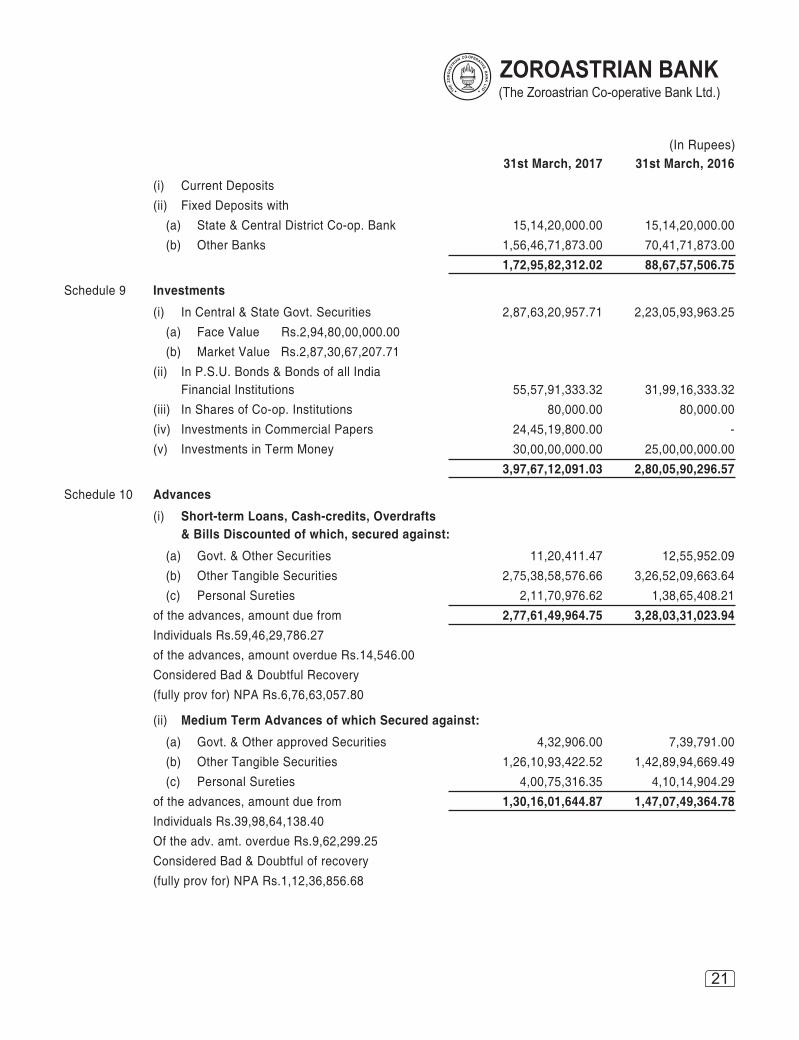

(In Rupees) 31st March, 2017 31st March, 2016

(i) Current Deposits 1,34,90,439.02 3,11,65,633.75 (ii) Fixed Deposits with (a) State & Central District Co-op. Bank 15,14,20,000.00 15,14,20,000.00 (b) Other Banks 1,56,46,71,873.00 70,41,71,873.00 1,72,95,82,312.02 88,67,57,506.75

Schedule 9 Investments

(i) In Central & State Govt. Securities 2,87,63,20,957.71 2,23,05,93,963.25 (a) Face Value Rs.2,94,80,00,000.00 (b) Market Value Rs.2,87,30,67,207.71 (ii) In P.S.U. Bonds & Bonds of all India

Financial Institutions 55,57,91,333.32 31,99,16,333.32 (iii) In Shares of Co-op. Institutions 80,000.00 80,000.00 (iv) Investments in Commercial Papers 24,45,19,800.00 - (v) Investments in Term Money 30,00,00,000.00 25,00,00,000.00 3,97,67,12,091.03 2,80,05,90,296.57

Schedule 10 Advances

(i) Short-term Loans, Cash-credits, Overdrafts & Bills Discounted of which, secured against:

(a) Govt. & Other Securities 11,20,411.47 12,55,952.09 (b) Other Tangible Securities 2,75,38,58,576.66 3,26,52,09,663.64 (c) Personal Sureties 2,11,70,976.62 1,38,65,408.21 of the advances, amount due from 2,77,61,49,964.75 3,28,03,31,023.94 Individuals Rs.59,46,29,786.27 of the advances, amount overdue Rs.14,546.00 Considered Bad & Doubtful Recovery (fully prov for) NPA Rs.6,76,63,057.80

(ii) Medium Term Advances of which Secured against:

(a) Govt. & Other approved Securities 4,32,906.00 7,39,791.00 (b) Other Tangible Securities 1,26,10,93,422.52 1,42,89,94,669.49 (c) Personal Sureties 4,00,75,316.35 4,10,14,904.29 of the advances, amount due from 1,30,16,01,644.87 1,47,07,49,364.78 Individuals Rs.39,98,64,138.40 Of the adv. amt. overdue Rs.9,62,299.25 Considered Bad & Doubtful of recovery (fully prov for) NPA Rs.1,12,36,856.68

90th Annual Report 2016-2017

22

(In Rupees) 31st March, 2017 31st March, 2016

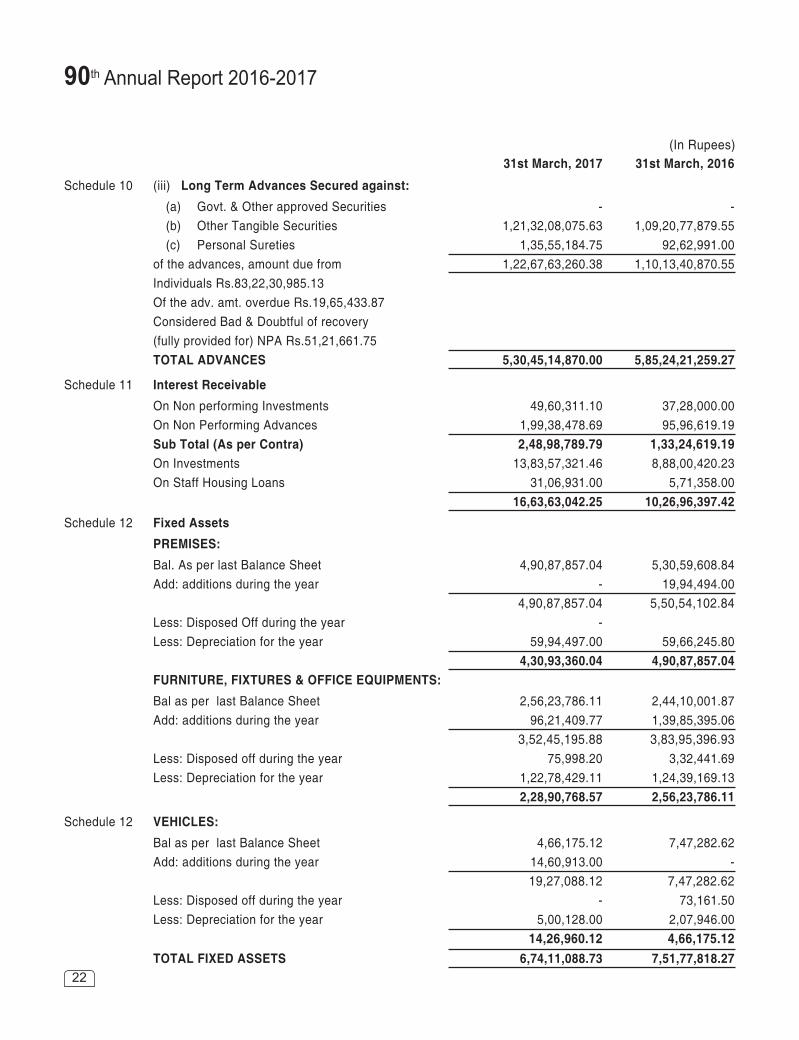

Schedule 10 (iii) Long Term Advances Secured against:

(a) Govt. & Other approved Securities - - (b) Other Tangible Securities 1,21,32,08,075.63 1,09,20,77,879.55 (c) Personal Sureties 1,35,55,184.75 92,62,991.00 of the advances, amount due from 1,22,67,63,260.38 1,10,13,40,870.55 Individuals Rs.83,22,30,985.13 Of the adv. amt. overdue Rs.19,65,433.87 Considered Bad & Doubtful of recovery (fully provided for) NPA Rs.51,21,661.75 TOTAL ADVANCES 5,30,45,14,870.00 5,85,24,21,259.27

Schedule 11 Interest Receivable

On Non performing Investments 49,60,311.10 37,28,000.00 On Non Performing Advances 1,99,38,478.69 95,96,619.19 Sub Total (As per Contra) 2,48,98,789.79 1,33,24,619.19 On Investments 13,83,57,321.46 8,88,00,420.23 On Staff Housing Loans 31,06,931.00 5,71,358.00 16,63,63,042.25 10,26,96,397.42Schedule 12 Fixed Assets PREMISES:

Bal. As per last Balance Sheet 4,90,87,857.04 5,30,59,608.84 Add: additions during the year - 19,94,494.00 4,90,87,857.04 5,50,54,102.84 Less: Disposed Off during the year - Less: Depreciation for the year 59,94,497.00 59,66,245.80 4,30,93,360.04 4,90,87,857.04 FURNITURE, FIXTURES & OFFICE EQUIPMENTS:

Bal as per last Balance Sheet 2,56,23,786.11 2,44,10,001.87 Add: additions during the year 96,21,409.77 1,39,85,395.06 3,52,45,195.88 3,83,95,396.93 Less: Disposed off during the year 75,998.20 3,32,441.69 Less: Depreciation for the year 1,22,78,429.11 1,24,39,169.13 2,28,90,768.57 2,56,23,786.11

Schedule 12 VEHICLES:

Bal as per last Balance Sheet 4,66,175.12 7,47,282.62 Add: additions during the year 14,60,913.00 - 19,27,088.12 7,47,282.62 Less: Disposed off during the year - 73,161.50 Less: Depreciation for the year 5,00,128.00 2,07,946.00 14,26,960.12 4,66,175.12 TOTAL FIXED ASSETS 6,74,11,088.73 7,51,77,818.27

ZOROASTRIAN BANK(The Zoroastrian Co-operative Bank Ltd.)

23

(In Rupees) 31st March, 2017 31st March, 2016

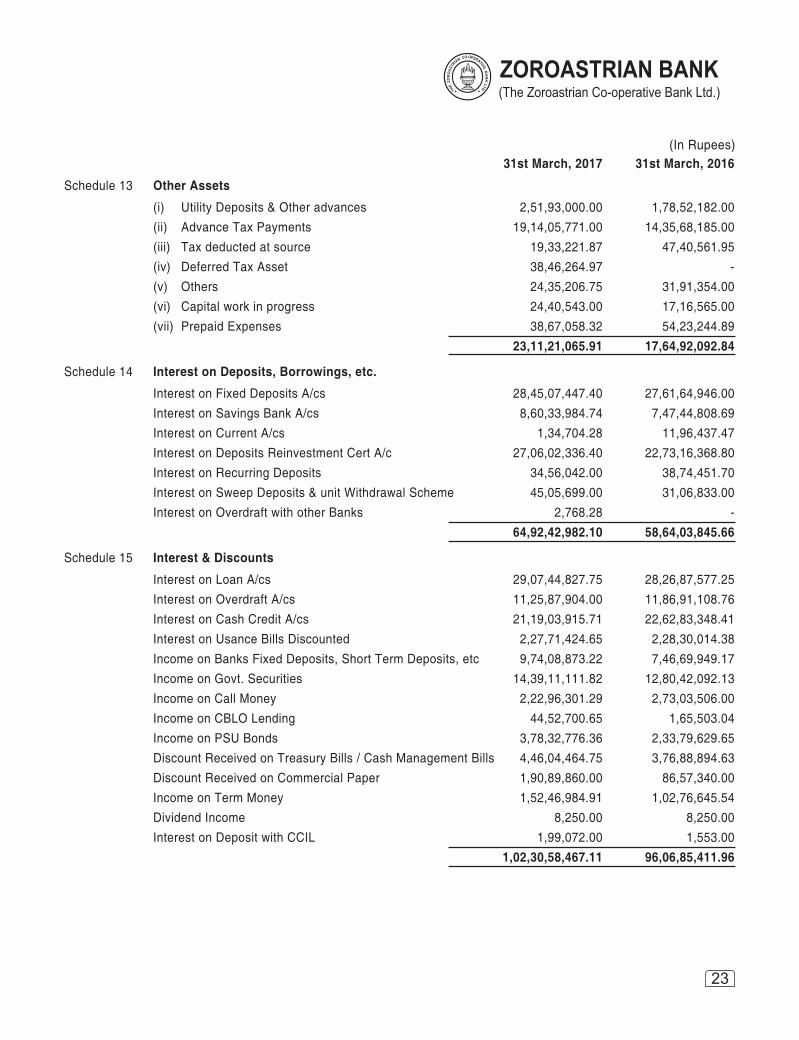

Schedule 13 Other Assets

(i) Utility Deposits & Other advances 2,51,93,000.00 1,78,52,182.00 (ii) Advance Tax Payments 19,14,05,771.00 14,35,68,185.00 (iii) Tax deducted at source 19,33,221.87 47,40,561.95 (iv) Deferred Tax Asset 38,46,264.97 - (v) Others 24,35,206.75 31,91,354.00 (vi) Capital work in progress 24,40,543.00 17,16,565.00 (vii) Prepaid Expenses 38,67,058.32 54,23,244.89 23,11,21,065.91 17,64,92,092.84

Schedule 14 Interest on Deposits, Borrowings, etc.

Interest on Fixed Deposits A/cs 28,45,07,447.40 27,61,64,946.00 Interest on Savings Bank A/cs 8,60,33,984.74 7,47,44,808.69 Interest on Current A/cs 1,34,704.28 11,96,437.47 Interest on Deposits Reinvestment Cert A/c 27,06,02,336.40 22,73,16,368.80 Interest on Recurring Deposits 34,56,042.00 38,74,451.70 Interest on Sweep Deposits & unit Withdrawal Scheme 45,05,699.00 31,06,833.00 Interest on Overdraft with other Banks 2,768.28 - 64,92,42,982.10 58,64,03,845.66

Schedule 15 Interest & Discounts

Interest on Loan A/cs 29,07,44,827.75 28,26,87,577.25 Interest on Overdraft A/cs 11,25,87,904.00 11,86,91,108.76 Interest on Cash Credit A/cs 21,19,03,915.71 22,62,83,348.41 Interest on Usance Bills Discounted 2,27,71,424.65 2,28,30,014.38 Income on Banks Fixed Deposits, Short Term Deposits, etc 9,74,08,873.22 7,46,69,949.17 Income on Govt. Securities 14,39,11,111.82 12,80,42,092.13 Income on Call Money 2,22,96,301.29 2,73,03,506.00 Income on CBLO Lending 44,52,700.65 1,65,503.04 Income on PSU Bonds 3,78,32,776.36 2,33,79,629.65 Discount Received on Treasury Bills / Cash Management Bills 4,46,04,464.75 3,76,88,894.63 Discount Received on Commercial Paper 1,90,89,860.00 86,57,340.00 Income on Term Money 1,52,46,984.91 1,02,76,645.54 Dividend Income 8,250.00 8,250.00 Interest on Deposit with CCIL 1,99,072.00 1,553.00 1,02,30,58,467.11 96,06,85,411.96

90th Annual Report 2016-2017

24

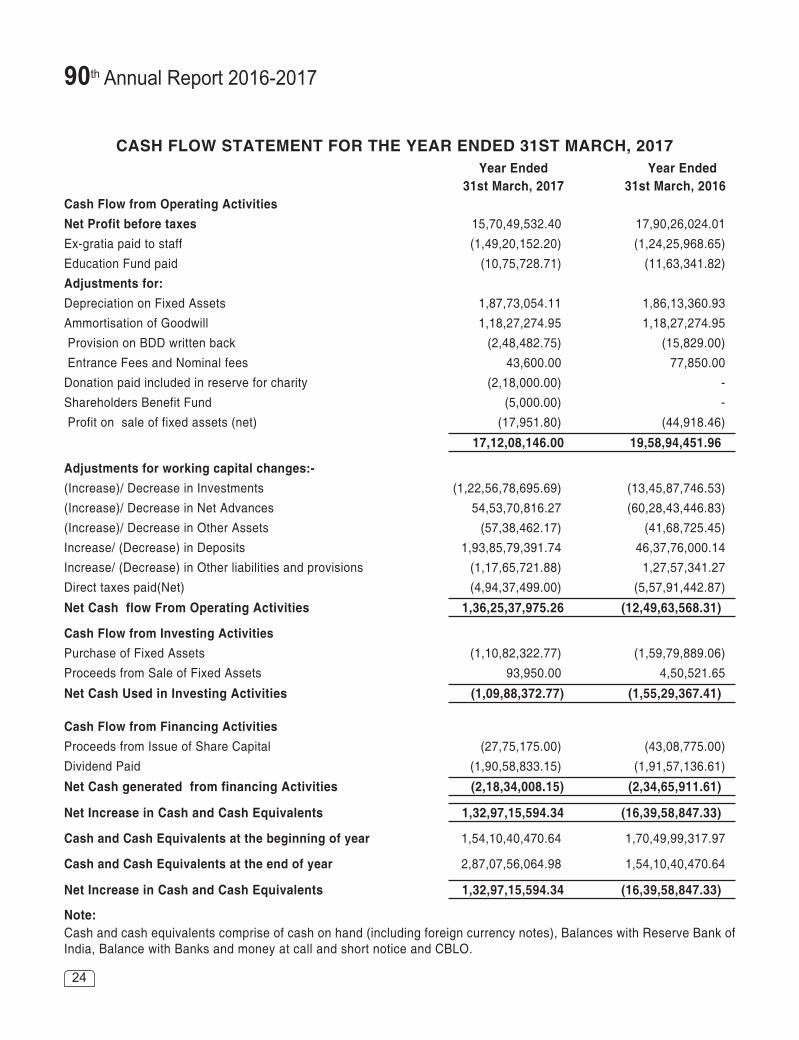

CASH FLOW STATEMENT FOR THE YEAR ENDED 31ST MARCH, 2017 Year Ended Year Ended 31st March, 2017 31st March, 2016Cash Flow from Operating Activities Net Profit before taxes 15,70,49,532.40 17,90,26,024.01Ex-gratia paid to staff (1,49,20,152.20) (1,24,25,968.65)Education Fund paid (10,75,728.71) (11,63,341.82)Adjustments for: Depreciation on Fixed Assets 1,87,73,054.11 1,86,13,360.93Ammortisation of Goodwill 1,18,27,274.95 1,18,27,274.95 Provision on BDD written back (2,48,482.75) (15,829.00) Entrance Fees and Nominal fees 43,600.00 77,850.00Donation paid included in reserve for charity (2,18,000.00) -Shareholders Benefit Fund (5,000.00) - Profit on sale of fixed assets (net) (17,951.80) (44,918.46)

17,12,08,146.00 19,58,94,451.96

Adjustments for working capital changes:- (Increase)/ Decrease in Investments (1,22,56,78,695.69) (13,45,87,746.53)(Increase)/ Decrease in Net Advances 54,53,70,816.27 (60,28,43,446.83)(Increase)/ Decrease in Other Assets (57,38,462.17) (41,68,725.45)Increase/ (Decrease) in Deposits 1,93,85,79,391.74 46,37,76,000.14Increase/ (Decrease) in Other liabilities and provisions (1,17,65,721.88) 1,27,57,341.27Direct taxes paid(Net) (4,94,37,499.00) (5,57,91,442.87)

Net Cash flow From Operating Activities 1,36,25,37,975.26 (12,49,63,568.31)

Cash Flow from Investing Activities Purchase of Fixed Assets (1,10,82,322.77) (1,59,79,889.06)Proceeds from Sale of Fixed Assets 93,950.00 4,50,521.65

Net Cash Used in Investing Activities (1,09,88,372.77) (1,55,29,367.41)

Cash Flow from Financing Activities Proceeds from Issue of Share Capital (27,75,175.00) (43,08,775.00)Dividend Paid (1,90,58,833.15) (1,91,57,136.61)

Net Cash generated from financing Activities (2,18,34,008.15) (2,34,65,911.61)

Net Increase in Cash and Cash Equivalents 1,32,97,15,594.34 (16,39,58,847.33)

Cash and Cash Equivalents at the beginning of year 1,54,10,40,470.64 1,70,49,99,317.97

Cash and Cash Equivalents at the end of year 2,87,07,56,064.98 1,54,10,40,470.64

Net Increase in Cash and Cash Equivalents 1,32,97,15,594.34 (16,39,58,847.33)

Note:Cash and cash equivalents comprise of cash on hand (including foreign currency notes), Balances with Reserve Bank of India, Balance with Banks and money at call and short notice and CBLO.

ZOROASTRIAN BANK(The Zoroastrian Co-operative Bank Ltd.)

25

SIGNIFICANT ACCOUNTING POLICIES & NOTES FORMING PART OF ACCOUNTSFOR THE YEAR ENDED 31ST MARCH, 2017

1. ACCOUNTING POLICIES

1.1 Accounting Convention:

The financial statements have been prepared and presented under the historical cost convention on accrual basis of accounting, and comply with the generally accepted accounting principles, statutory requirements prescribed under the Banking Regulation Act, 1949, and the Multi State Co-operative Societies Act, 2002 (the Act), the circulars and guidelines issued by the Reserve Bank of India ('RBI') from time to time and the Accounting Standards issued by the Institute of Chartered Accountants of India to the extent applicable and current practices prevailing within the Co-operative Banking industry in India.

Use of estimates :

The preparation of the financial statements in conformity with the generally accepted accounting principles requires the Management to make estimates and assumptions that affect the reported amount of assets and liabilities, revenues and expenses and disclosure of contingent liabilities at the date of the financial statements. Actual results could differ from those estimates. The Management believes that the estimates used in the preparation of the financial statements are prudent and reasonable. Any revision to the accounting estimates is recognised prospectively in the current and future periods.

1.2 Investments:

1.2.1 Investment portfolio of the Bank is categorised in accordance with the guidelines issued by Reserve Bank of India as under:-

a) ‘Held to Maturity’ comprising investments acquired with the intention to hold them till maturity.

b) ‘Held for Trading’ comprising investments acquired with the intention to trade within 90 days.

c) ‘Available for Sale’ comprising investments not covered (a) and (b) above i.e. those which are acquired neither for trading purposes nor for being held till maturity.

For presentation in the Balance Sheet, Investments are classified under Central & State Government Securities, Other Approved Trustee Securities, Reserve Fund, Investments, Other Investments (PSU Bonds & Bonds of all India Financial Institutions, Fixed Deposits with State / District Central Co-op. Banks, etc.)

1.2.2 Valuation of Investments is as per directives issued by Reserve Bank of India from time to time.

1.2.3 Investments in ‘Available for Sale’ & ‘Held for Trading’ categories are valued scrip-wise at lower of cost or market value. Appreciation / Depreciation are aggregated for each class of securities and net depreciation, in aggregate for each category, is provided for, while net appreciation, if any, is ignored.

Investments in ‘Held to Maturity’ category are valued at cost and the premium paid in individual security is amortized over the life of that security.

1.2.4 Market value is taken on the basis of the Yield to Maturity as indicated by Fixed Income, Money Market and Derivatives Association of India (FIMMDA).

90th Annual Report 2016-2017

26

1.2.5 Broken period interest accrued at the time of acquisition of securities is recognised as expenses.

1.2.6 Investments where principal / interest remain overdue for more than 90 days are classified as Non Performing and provision is made in line with the guidelines of Reserve Bank of India.

1.2.7 Interest on Investments of all earmarked funds are credited to the Profit and Loss Account.

1.2.8 The Statutory Reserve Fund is augmented to the extent required by earmarking additional funds as approved by the Board.

1.3 Advances:

1.3.1 In terms of guidelines issued by Reserve Bank of India, advances to borrowers are classified into “Performing” or Non-performing” assets based on recovery of Principal / Interest. Non Performing Assets (NPA) is further classified as sub-standard, doubtful and loss assets and provisions thereon are made in accordance with the prudential norms prescribed by the RBI.

1.3.2 Specific provisions in respect of NPAs are made subject to the minimum provisioning norms prescribed by the RBI. The Bank also makes additional provisioning over and above the specific minimum provisioning as per RBI norms as a matter of prudence. Provision on Standard Advances is made at a rate ranging between 0.25% and 1.00% as prescribed by RBI.

1.3.3 Overdue Interest Reserve represents unrecovered interest on all NPA advances& investments, which is correspondingly shown under interest receivable.

1.3.4 For the purpose of presentation, Advances are classified as Short term Advances up to 12 months, Medium term Advances from 1 to 5 years and Long term Advances above 5 years.

1.4 Fixed Assets & Depreciation:

1.4.1 Premises and other fixed assets are stated at historical cost, net of accumulated depreciation, thereon. Cost includes cost of purchase and all expenditure like freight, duties , taxes and incidental expenses related to the acquisition and installation of the asset.

1.4.2 Capital work-in-progress includes cost of fixed assets that are not ready for their intended use and also includes advances paid to acquire fixed assets.

1.4.3 Bank has not re-valued any of its Fixed Assets.

ZOROASTRIAN BANK(The Zoroastrian Co-operative Bank Ltd.)

27

1.4.4 Depreciation :

1.4.4.1 Assets purchased and put to use are depreciated on the basis of Straight Line Method as under:

a) Furniture & Fixtures 15%

b) Electrical Equipments 15%

c) Vehicles 20%

d) Premises 5%

e) Computer Hardware 33.33%

f) Computer Software 33.33%

1.4.4.2 Depreciation on additions to assets is provided for the full year if the assets are purchased on or before 30th September and for the half year, if the assets are purchased after 30th September. No depreciation is provided on assets sold/disposed off during each of the half year.

1.5 Revenue Recognition ( AS -9) :

Items of Income and Expenditure are accounted for on accrual basis except for certain items of Income and Expenditure, mentioned below, which are accounted for on cash basis:

a) Interest on Non-Performing Assets in accordance with RBI guidelines

b) Rent on Safe Deposit Lockers

c) Commission on Insurance Business on referral basis.

d) Interest on Refund of Income Tax.

e) Dividend on shares of Co-operative Banks.

1.6 Employee Benefits( AS -15):

1.6.1 Provident Fund is Defined Contribution Plan and contributions made to the Commissioner of Provident Fund at rates prescribed in the Employees Provident Fund and Misc. Provisions Act, 1952 are accounted for on accrual basis and deposited within the stipulated time.

1.6.2 The Bank operates defined benefit plan for its employees, viz. gratuity liability. The cost of providing benefits under these plans is determined on the basis of actuarial valuation at each year-end. The Bank is maintaining fund under Trust Deed with Life Insurance Corporation of India (LIC) for gratuity payments to employees and annual premium is paid based on the demand from LIC.

1.6.3 Provision for Leave Encashment is made on an actuarial basis.

1.6.4 Ex-Gratia is appropriated out of net profit in accordance with the Multi-State Co-operative Societies Act, 2002.

90th Annual Report 2016-2017

28

1.7 Segment Reporting (AS - 17) :

The business segment is considered as primary reporting format and Bank does not have any geographical segment. In accordance with the guidelines issued by RBI, Bank has adopted following business segments :-

(a) Treasury includes all investment portfolio, profit / loss on sale of investments (Bonds and government securities) . The expenses of this segment consist of interest expenses on funds borrowed from external sources as well as internal sources and depreciation / amortization of premium on Held to Maturity investments.

(b) Other banking operations include all other operations not covered under Treasury Operations.

1.8 Lease Payment (AS - 19):

Operating lease payments are recognized as an expense in the Profit and Loss account during the year as per lease agreement.

1.9 Taxes on Income (AS -22):

Provision for current tax is made after taking into consideration benefits admissible under the provisions of the Income-Tax Act, 1961. A Deferred Tax Asset / Liability resulting from timing differences between taxable and accounting income is accounted for, using the tax rates and laws that are enacted or substantially enacted as on the Balance Sheet date. A deferred tax asset/ liability is recognised and carried forward only to the extent that there is a reasonable certainty or a virtual certainty as the case maybe that the asset will be realised in future

1.10 Provisions & contingencies(AS -29) :

1.10.1 In conformity with AS- 29 relating to “Provisions, Contingent Liabilities and Contingent Assets”, the Bank recognises by way of provision only when it has a present obligation as a result of past event. It is probable that an outflow of resources embodying economic benefits may be required to settle the obligations as and when a reliable estimate of the amount of the obligation can be made.

1.10.2 Acceptance, endorsements and other obligations including guarantees are disclosed as Contingent Liabilities at the face value of the commitments undertaken.

2. NOTES TO ACCOUNTS:

2.1 The Bank has a Borrowing Arrangement of Funds under ‘Collateralised Borrowing and Lending Obligations’ (CBLO).

2.2 In accordance with Reserve Bank of India guidelines, Investment Fluctuation Reserve @ 5% of the investment in AFS category of Rs. 18719.46 lakhs should be Rs.935.97 lakhs. As against this, the Bank has a balance under Investment Fluctuation Reserve of Rs. 936.70 lakhs.

2.3 There is depreciation in Government Securities amounting to Rs.32.54 lakhs and appreciation in Non SLR investments amounting to Rs. 229.55 lakhs. Net Appreciation in investments as at the Balance Sheet date was Rs. 197.01 lakhs which has been ignored. The Bank already has provision of Rs. 482.75 lakhs under Investment Depreciation Reserve. The excess balance in the Investment Depreciation Reserve is continued on a conservative basis.

ZOROASTRIAN BANK(The Zoroastrian Co-operative Bank Ltd.)

29

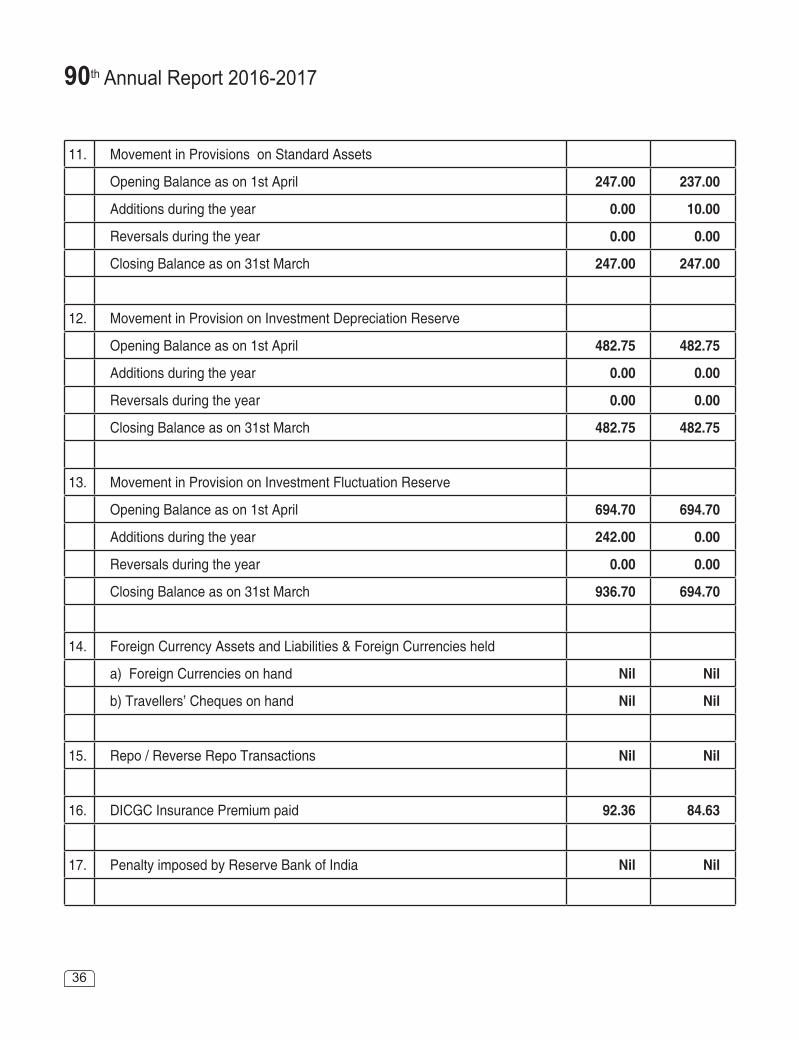

2.4 The requirement of provision against Standard &Non Performing Assets in terms of Reserve Bank of India guidelines are as follows:

(Rs in lakhs)

Provision required Provision Held Excess Provision

Standard Assets 227.96 247.00 19.04

Non Performing Assets

- Advances 348.432482.43 2074.00

- Investments 60.00

Total 408.43 2482.43 2074.00

In view of provisions already held in place, no further provision is required.

2.5 The Bank has not restructured any account during the period under review.

2.6 An amount of Rs. 67.85 lakhs has been recovered from Non Performing Advances during the financial year. Rs. 2.48 lakhs has been written-off during the year.

2.7 Claims against Bank not acknowledged as debt is Rs NIL.

2.8 Employee Benefits- Accounting Standard 15 (Revised):-

• Bank’s Contribution to Provident Fund for the current year – Rs. 1,27,96,234.00 (Previous year- Rs. 1,26,72,867.00 )

• Gratuity(fundedwithLIC)&LeaveEncashment(unfunded).

• ThefollowingtablegivesdisclosuresforthecurrentyearasrequiredunderAS15asfurnishedbyActuaries Messrs K .A. Pandit& Associates and is in accordance with the financial statements.

I) Table showing discounting rates / expected return / salary escalation rate:-

Sr. No. Particulars Gratuity (Funded) Leave Encashment (Unfunded)

31.03.17 31.03.16 31.03.17 31.03.16

1 Discount rate 7.34% 8.07% 7.34% 8.07%

2 Salary Escalation rate 3.00% 3.00% 3.00 3.00%

90th Annual Report 2016-2017

30

II) Changes in present value of obligations :- (Amount in Rs.)

Sr. No. Particulars Gratuity (Funded) Leave Encashment (Unfunded)

31.03.17 31.03.16 31.03.17 31.03.161 Liability at the beginning of the

current period3,35,99,000 3,64,05,521 1,86,94,419 1,67,60,379

2 Interest cost 27,11,439 29,08,801 15,08,640 13,39,1543 Current service cost 21,54,044 24,35,837 12,38,835 16,09,5384 Benefits paid (1,10,634) (6,56,750) (16,59,343) (17,49,000)5 Actuarial (gain)/loss on obligations 28,64,193 (74,94,409) 9,43,577 7,34,3486 Liability at the end of the current

period 4,12,18,042 3,35,99,000 2,07,26,128 1,86,94,419

III) Changes in fair value of Plan Assets:- (Amount in Rs.)

Sr. No. Particulars Gratuity (Funded) Leave Encashment (Unfunded)

31.03.17 31.03.16 31.03.17 31.03.16

1Fair value of plan assets at the beginning of the year

3,99,23,752 3,10,06,293 - -

2 Expected return on plan assets 32,21,847 24,77,403 - -

3 Contributions 37,92,649 64,80,923 - -

4 Benefits paid (1,10,634) (6,56,750) - -

5 Actuarial gain/ (loss) on plan assets (2,78,362) 6,15,883

6Fair value of plan assets at the end of the year

4,65,49,252 3,99,23,752 - -

IV) Amount recognized in Balance Sheet:- (Amount in Rs.)

Sr. No. Particulars Gratuity (Funded) Leave Encashment (Unfunded)

31.03.17 31.03.16 31.03.17 31.03.16

1Fair value of plan assets at the end of the period.

4,65,49,252 3,99,23,752 - -

2 Liability at the end of the period (4,12,18,042) (3,35,99,000) (2,07,26,128) (1,86,94,419)

3 Amount recognized in the Balance Sheet - (2,17,89,709) (1,94,49,052)

ZOROASTRIAN BANK(The Zoroastrian Co-operative Bank Ltd.)

31

V) Expenses recognized in income statement:- (Amount in Rs.)

Sr. No. Particulars Gratuity (Funded) Leave Encashment (Unfunded)

31.03.17 31.03.16 31.03.17 31.03.16

1 Current service cost 21,54,044 24,35,837 12,38,835 16,09,538

2 Interest cost (5,10,408) 4,31,398 15,08,640 13,39,154

3 Expected return on plan assets - - - -

4 Net actuarial gain/ (loss) 31,42,555 (81,10,292) 9,43,577 7,34,348

5 Expenses recognised in P&L account. 47,86,191 (52,43,057) 36,91,052 36,83,040

* The Bank has been consistently debiting to the Profit & Loss Account the amount demanded by LIC towards the Group Gratuity Fund. The difference in the liability as assessed by actuaries K.A. Pandit& Associates and LIC is on account of differential discounting rates as well as service cost. The fair value of plan assets available with the Fund is in excess of the liability towards gratuity. This excess amount has not been recognized as an asset on a conservative basis.On completion of reconciliation between the actuarial valuation determined by the actuaries. K APandit& Associate and the actuarial valuation determined by the LIC, appropriate amounts will be recognized in the Balance Sheet.

2.9 Accounting Standard 17 Segment Reporting as at March 31, 2017: (Rs.in lakhs)

Financial year 2016-17

Business Segments TreasuryOther Banking

OperationsTotal

Revenue 3859.52 6776.55 10636.07

Expenses 3354.95 5719.38 9074.33

Result 504.57 1057.17 1561.74

Unallocated expenses 118.24

Operating profit 1443.50

Income Tax 356.45

Net Profit 1087.05

Other Information -

Segment assets 69095.47 55101.55 124197.02

Unallocated assets 2178.83

Total assets 126375.85

Segment liabilities 55136.28 54642.32 109778.60

Unallocated liabilities 1874.65

Share Capital & Reserves 14722.60

Total Liabilities 126375.85

90th Annual Report 2016-2017

32

2.10 Accounting Standard 18 Related Party Transactions :

The Bank is a Co-operative Society under the Multi State Co-operative Societies Act, 2002 and there are no Related Parties requiring a disclosure under Accounting Standard 18 issued by the Institute of Chartered Accountants of India read with Master Circular on Disclosure in Financial Statements – Notes to Accounts dated July 1, 2014 issued by Reserve Bank of India, other than one Key Management Personnel viz. Mr. U. A. Shetye, the Managing Director of the Bank. However, in terms of Reserve Bank of India circular dated March 29, 2003, the Managing Director being a full time employee of the bank, no further details need to be disclosed.

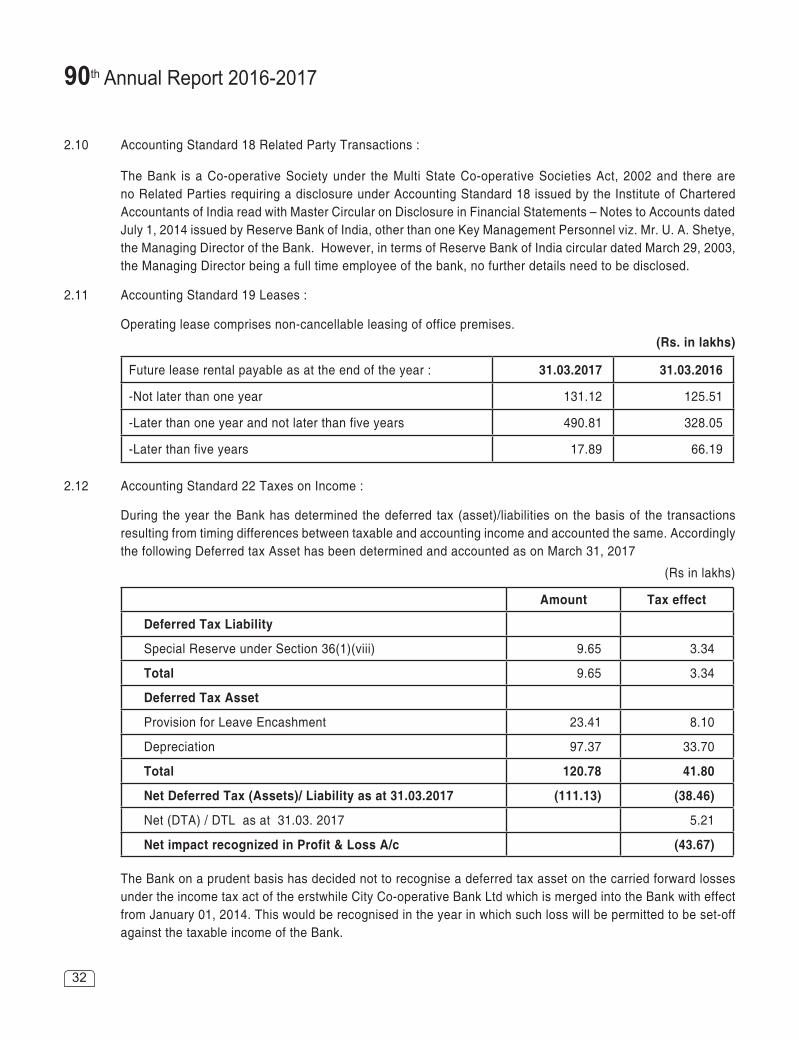

2.11 Accounting Standard 19 Leases :

Operating lease comprises non-cancellable leasing of office premises. (Rs. in lakhs)

Future lease rental payable as at the end of the year : 31.03.2017 31.03.2016

-Not later than one year 131.12 125.51

-Later than one year and not later than five years 490.81 328.05

-Later than five years 17.89 66.19

2.12 Accounting Standard 22 Taxes on Income :

During the year the Bank has determined the deferred tax (asset)/liabilities on the basis of the transactions resulting from timing differences between taxable and accounting income and accounted the same. Accordingly the following Deferred tax Asset has been determined and accounted as on March 31, 2017

(Rs in lakhs)

Amount Tax effect

Deferred Tax Liability

Special Reserve under Section 36(1)(viii) 9.65 3.34

Total 9.65 3.34

Deferred Tax Asset

Provision for Leave Encashment 23.41 8.10

Depreciation 97.37 33.70

Total 120.78 41.80

Net Deferred Tax (Assets)/ Liability as at 31.03.2017 (111.13) (38.46)

Net (DTA) / DTL as at 31.03. 2017 5.21

Net impact recognized in Profit & Loss A/c (43.67)

The Bank on a prudent basis has decided not to recognise a deferred tax asset on the carried forward losses under the income tax act of the erstwhile City Co-operative Bank Ltd which is merged into the Bank with effect from January 01, 2014. This would be recognised in the year in which such loss will be permitted to be set-off against the taxable income of the Bank.

ZOROASTRIAN BANK(The Zoroastrian Co-operative Bank Ltd.)

33

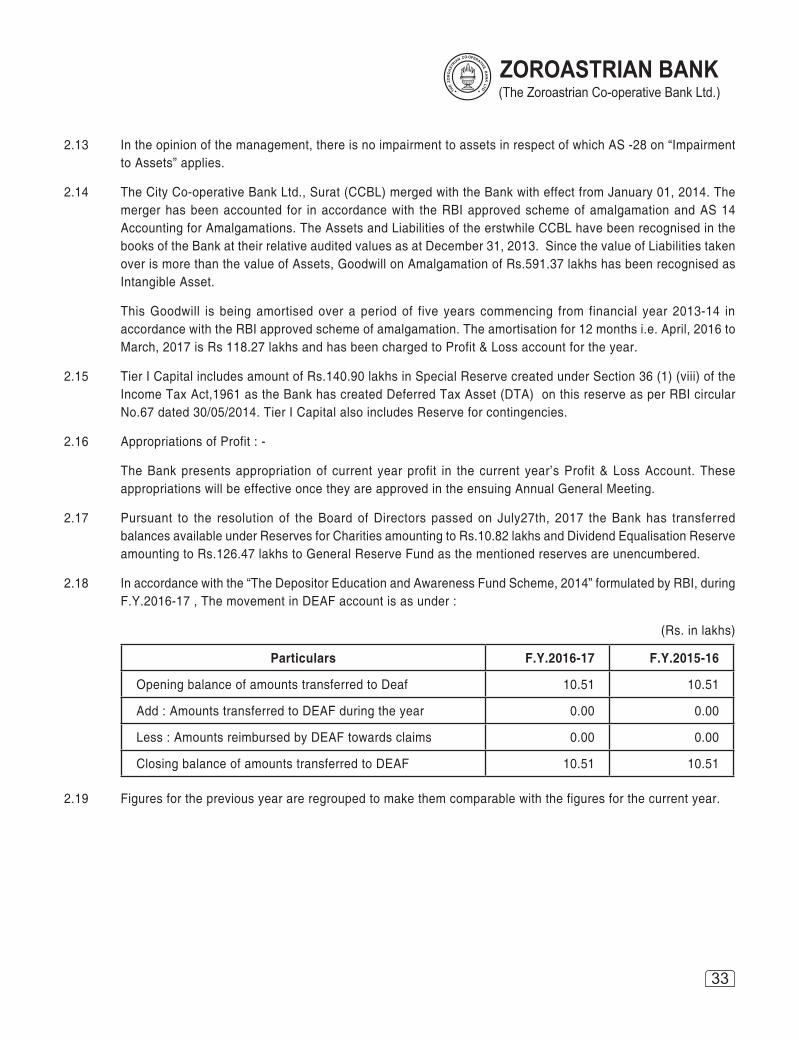

2.13 In the opinion of the management, there is no impairment to assets in respect of which AS -28 on “Impairment to Assets” applies.

2.14 The City Co-operative Bank Ltd., Surat (CCBL) merged with the Bank with effect from January 01, 2014. The merger has been accounted for in accordance with the RBI approved scheme of amalgamation and AS 14 Accounting for Amalgamations. The Assets and Liabilities of the erstwhile CCBL have been recognised in the books of the Bank at their relative audited values as at December 31, 2013. Since the value of Liabilities taken over is more than the value of Assets, Goodwill on Amalgamation of Rs.591.37 lakhs has been recognised as Intangible Asset.

This Goodwill is being amortised over a period of five years commencing from financial year 2013-14 in accordance with the RBI approved scheme of amalgamation. The amortisation for 12 months i.e. April, 2016 to March, 2017 is Rs 118.27 lakhs and has been charged to Profit & Loss account for the year.