zalewski - employee classification: defining the employment relationship

TRANSCRIPT

Defining the Employment Relationship

2010 J. J. Keller & Associates, Inc.®

Employee Classification

Basics of classifications

• Employees (legal or internal designations)

• Legal classification: Exempt & non-exempt

• Internal (part time, seasonal) — usually

defines benefit eligibility

• Employees by any

other name…

• Non-Employees (interns,

independent contractors,

volunteers)

Part I: Exempt classifications

• Wrongful classification can be costly,

especially if many employees are affected

• Back pay for two years

• Three years for willful,

plus damages

• Award of legal fees

• Example case

• Employee got $4,000 back pay, and

over $55,000 to cover his legal fees

Exemptions: Primary duty

• To qualify for a ―white collar‖ exemption:

(Executive, Administrative, Professional, etc.)

• Primary duty must meet the criteria for the

exempt classification

• Some employees may perform a

combination of exempt duties

• Employee must be paid on a salary basis

Exemptions: Salary basis

• Same salary each week, regardless of:

• Payday frequency

• Days or hours worked

• Limited deductions

• Minimum $455 per week

• Not based on 40 hours (cannot pro-rate)

• Can reduce salary with hours reduction

Executive exemption

• Claims often based on the degree of authority

• Primary duty must be management

• Customarily and regularly direct the work of at

least two full-time employees or equivalent

• Authority to hire or fire, or recommendations on

hiring, firing, or other change in status must be

given particular weight (job duty, frequency)

Executive exemption case

• ―Managers‖ did no hiring, firing, or promoting;

were closely supervised with little discretion

• Worked 60 to 70 hours per week, stocking

shelves, cashiering, and janitorial duties

• Violation was found to be willful;

1,400 employees awarded $35 million

• Job description may not reflect the actual duties

• Morgan v. Family Dollar Stores (11th Cir., 2008)

Executive exemption case

• Employees failed to show willful violation

• Company failed to show good-faith efforts;

no expert consultation — documentation

• Issue is not whether employer

could have won, but whether

it could have lost (and it was)

• Evidence did not favor either

side, so the jury ruling in favor

of employees was upheld

• Rodriguez v. Farm Stores Grocery (11th Cir., 2008)

Administrative exemption

Primary duty:

• Office or non-manual work directly related to

management or business operations

• Accounting, budgeting, HR, marketing,

safety, regulatory compliance, etc.

• Include the exercise of:

• Discretion and independent judgment with

respect to matters of significance

Administrative exemption case

• Employee sold advertising space in a magazine

• Direct sales vs. promoting sales in general

• The employee‘s primary duty was making sales,

so she was not exempt

• Employees in retail might ―promote‖ sales, but

are not engaged in marketing

• Reiseck v. Universal Communications of Miami

(2nd Circuit, 2010)

Administrative exemption case

• Bachelor‘s degree and knowledge of accounting,

financial, and administrative services

• Coordinates meetings and interviews with clients,

medical providers, and investment advisors

• Develops procedures, recommends action

• Spends 95% of his time on client services or

support of executives

• Exemption did not apply

• Opinion Letter FLSA 2003-1NA

Learned professional exemption

• Primary duty which requires:

• Advanced intellectual knowledge, and

• Consistent exercise of discretion and

independent judgment

• Advanced knowledge must be:

• In a field of science or learning (includes

accountants and even chefs), and

• Customarily acquired by a prolonged course

of specialized intellectual instruction

Learned professional exemption

• Employee uses the advanced knowledge to

analyze, interpret or make deductions from

varying facts or circumstances

• Not for positions attained through general

knowledge acquired by a degree in any field

• Not for positions where most employees

acquired their skill by experience rather than by

advanced specialized intellectual instruction

• Usually challenged on educational requirement

Learned professional case

• Offered exempt job;

let go after three years

• Position requires 12 years

experience, but no specific

degree (had 20 years)

• Duties qualified, but did not justify exempt status

without the educational requirement

• Young v. Cooper Cameron Corp. (2nd Cir., 2009)

Creative professional exemption

• Primary duty must be work requiring invention,

imagination, originality, or talent in an artistic or

creative field

• Available for actors, musicians, composers,

painters, cartoonists, novelists, and persons

creative writers or graphic designers

• Status depends on the extent of the invention,

imagination, originality, or talent exercised

(not merely following a template)

Computer employee exemption

• Salary rule does not apply (can be hourly)

• Systems analysts, programmers, engineers

• Primary duty is designing or creating systems

• Does not include ―help desk‖

positions

• Opinion Letter FLSA 2006-42

Outside sales exemption

• Salary rule does not apply (often commission)

• Primary duty is making sales or obtaining orders

or contracts for services

• Customarily and regularly engaged away from the

employer‘s place of business

• Inside sales?

Certain commissioned sales of ―big ticket‖ items

Part II: Duties, deductions, and

expectations

• Each exemption has specific duties

• Employees who perform other duties

may question their classification

• Be wary of assigning non-exempt work

• Certain deductions from salary may threaten the

exempt classification — what you cannot do

• Options to keep timesheets, manage vacation,

and change compensation

Related or occasional tasks

• Most exempts perform minor, related tasks

29 CFR 541.703, Directly and closely related

• Occasional non-exempt tasks may be ―exempt‖

29 CFR 541.707, Occasional tasks

1) Are they performed by subordinates?

2) Can they be assigned to non-exempts?

3) Are they performed frequently?

4) Is performing them an industry practice?

Remember Morgan v. Family Dollar

Emergencies

• Non-exempt tasks during emergencies (which

threaten safety or property damage in situations

that cannot be anticipated) can be ―exempt‖ work

• Routine non-exempt

work may threaten the

exempt classification

• 29 CFR 541.706,

Emergencies

Training periods

• Exemptions do not apply to

trainees who don‘t perform the

duties of the exempt position

• Short periods should be okay,

especially if the employee does

not work overtime hours

• 29 CFR 541.705, Trainees

Prohibited salary deductions

• Making improper deductions may threaten the

exemption if the employer did not intend to pay

employees on a salary basis. (29 CFR 541.603,

Effect of improper deductions from salary)

• Partial day absences (except FMLA)

• Absences initiated by the employer or by the

operating requirements of the business

• Unpaid disciplinary suspension

• Damage or loss (Opinion Letter FLSA2006-7)

What does not threaten status?

• Salary deductions for:

• Full-day absences

initiated by employee

• Full-week absences

(including furloughs)

• Vacation advances

(for full days)

• Deductions for the employee‘s benefit

(insurance, retirement, charity contributions)

What does not threaten status?

• Employers ―may require exempt employees to

record and track their hours and to work a

specified schedule‖ (Opinion Letter FLSA 2005-5)

• Employers ―may require an exempt employee to

make up work time lost due to a personal absence

of less than a day without loss of the exemption‖

(Opinion Letter FLSA 2006-6)

• Mandatory use of vacation or PTO, even if the

company initiates the absence

(Opinion Letter FLSA 2009-2)

What does not threaten status?

• Additional compensation may be paid on any

basis (bonus, straight-time hourly, time and

one-half, or any other basis), and may include

paid time off (29 CFR §541.604, Minimum

guarantee plus extras)

• Example: Safety manager gets recertification

• Be careful not to create a direct relationship

between compensation and hours worked

• Comp time is not allowed for private employers

Part III: Internal classifications

and non-employees

• Employees may challenge other classifications:

• Part-time, seasonal, etc.

• Based on your policies or plan documents

• An ―employee‖ might be wrongly classified as a

non-employee (contractor, volunteer)

• Based on specific legal criteria

• Employer has the burden of proof

Internal status changes

• When does part-time becomes full-time?

• Based on the expected annual hours, or

• Based on your policy or plan definitions

• Claims normally fall under contract law

(if unclear, rule in favor of employees)

• No legal obligation to change status to full-time;

your only duty is to follow your policies

Non-employee classifications

• Volunteers

• Interns — paid or unpaid?

• Independent contractors

• Classification suits for overtime, taxes, or benefits

Volunteers

• Employees cannot ―volunteer‖ for their employer

• Any service for the employer must be paid

• Employees cannot ―decline‖ the protections of the

FLSA by performing duties the employer and

employee have characterized as volunteer work

• Opinion Letter FLSA 2001-18

Unpaid interns

• The internship is similar to educational training

• The experience is for the benefit of the intern

• The intern does not displace regular employees

• The employer gets no immediate advantage,

and operations may be impeded

• The intern is not entitled to a job

• Both parties understand that wages are not paid

• Fact Sheet #71, Internship programs

Independent contractors

• Behavioral control (outcome vs. methods)

• Financial control (profit, hiring, equipment)

• Type of relationship (contract, nature of work)

• Potential risk of an ―employment‖ relationship:

• Dependency, duties, and duration

• Proposed rule to document justification

• IRS and DOL criteria vs. state laws

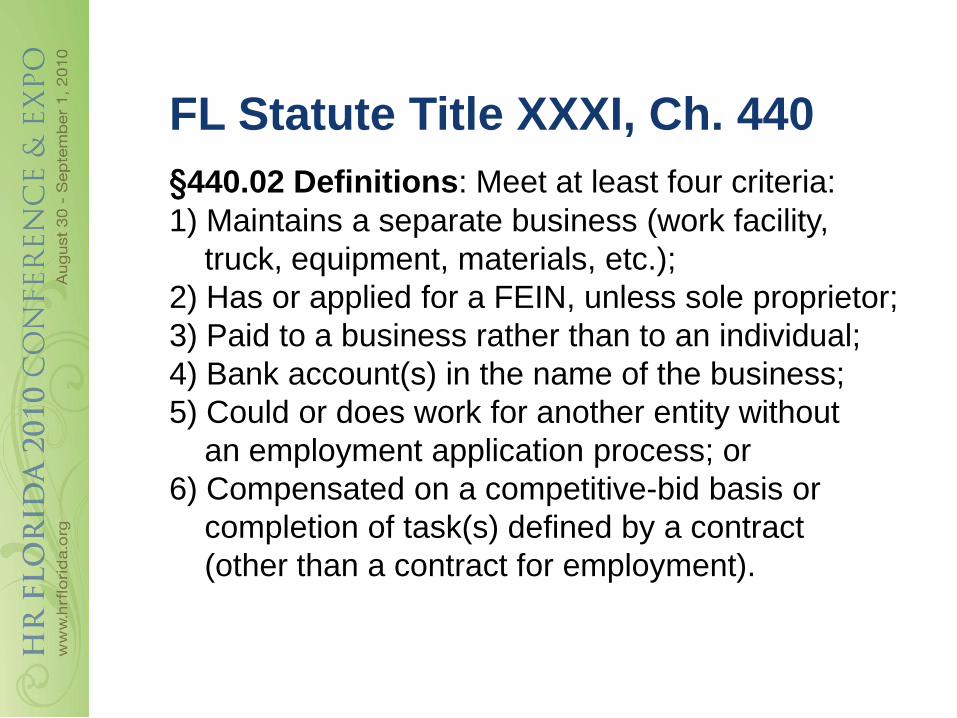

FL Statute Title XXXI, Ch. 440

§440.02 Definitions: Meet at least four criteria:

1) Maintains a separate business (work facility,

truck, equipment, materials, etc.);

2) Has or applied for a FEIN, unless sole proprietor;

3) Paid to a business rather than to an individual;

4) Bank account(s) in the name of the business;

5) Could or does work for another entity without

an employment application process; or

6) Compensated on a competitive-bid basis or

completion of task(s) defined by a contract

(other than a contract for employment).

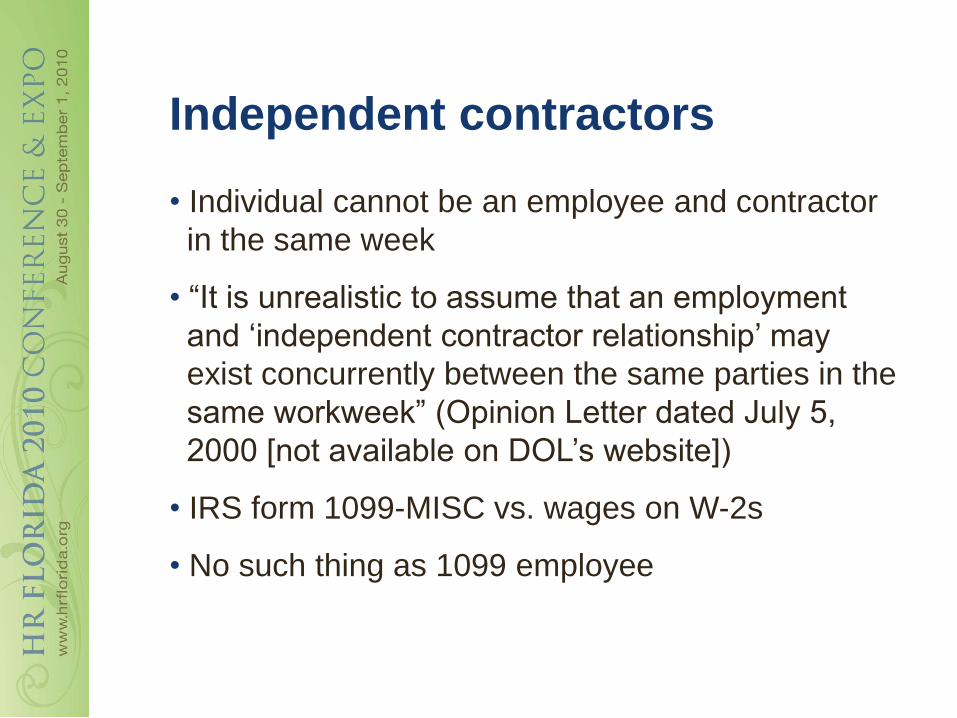

Independent contractors

• Individual cannot be an employee and contractor

in the same week

• ―It is unrealistic to assume that an employment

and ‗independent contractor relationship‘ may

exist concurrently between the same parties in the

same workweek‖ (Opinion Letter dated July 5,

2000 [not available on DOL‘s website])

• IRS form 1099-MISC vs. wages on W-2s

• No such thing as 1099 employee

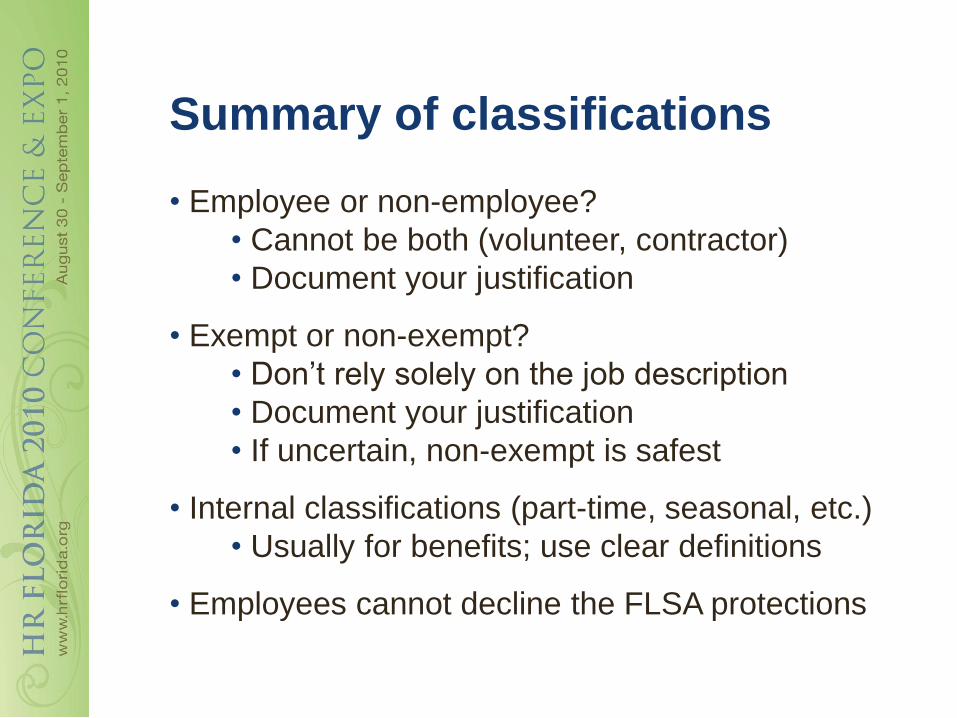

Summary of classifications

• Employee or non-employee?

• Cannot be both (volunteer, contractor)

• Document your justification

• Exempt or non-exempt?

• Don‘t rely solely on the job description

• Document your justification

• If uncertain, non-exempt is safest

• Internal classifications (part-time, seasonal, etc.)

• Usually for benefits; use clear definitions

• Employees cannot decline the FLSA protections

Resources

• Opinion Letters from the Wage and Hour Division

www.dol.gov/whd/opinion/opinion.htm

• Fact Sheets from the Wage and Hour Division

www.dol.gov/whd/fact-sheets-index.htm

• Regulations of the Wage and Hour Division

www.dol.gov/dol/allcfr/Title_29/Chapter_V.htm

Part 541 (white collar exemptions)

Part 779 (―inside sales‖ exemption)

• Florida statutes

www.leg.state.fl.us/statutes/

Edwin Zalewski

Editor – Human Resources

J. J. Keller & Associates, Inc.

www.jjkeller.com

(920) 722-2848

[email protected], regulations, and best practices change. The observations and comments drawn

today may not apply to laws, regulations, or best practices as they may be in the future.

J. J. Keller & Associates, Inc. does not assume responsibility for omissions, errors, or

ambiguity contained in this presentation. Individuals needing legal or other professional

advice should seek the assistance of a licensed professional in that field.

2010 J. J. Keller & Associates, Inc.®

Questions?