yume ir deck-mar2015

TRANSCRIPT

©2013 YUME. ALL RIGHTS RESERVED. 1

YuMe. Digital Video Audience Platform. March 2015.

FORWARD-LOOKING STATEMENTS

This presentation contains forward-looking statements. All statements other than statements of historical fact contained in this presentation are forward-looking statements. These statements are only current predictions and are subject to known and unknown risks, uncertainties, assumptions, and other factors that may cause our results or our industry’s actual results, levels of activity, performance or achievements to be materially different from those anticipated by the forward-looking statements. These forward-looking statements are subject to a number of risks, including those described under the heading “Risk Factors” in our periodic reports filed with the U.S. Securities and Exchange Commission, including our annual report on Form 10-K for the year ended December 31, 2014 and our quarterly report on Form 10-Q for the quarter ended September 31, 2014, and in our future filings and reports with the SEC. Moreover, new risks emerge periodically. It is not possible for us to predict all risks, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements we may make. Actual results could differ materially and adversely from those anticipated or implied in the forward-looking statements. You should not rely upon forward-looking statements as predictions of future events. Except as required by law, we are under no duty to update or revise any of the forward-looking statements, whether as a results of new information, future events or otherwise, after the date of this presentation.

In addition to the U.S. GAAP financials, this presentation includes certain non-GAAP financial measures. These non-GAAP financial measures are in addition to, and not a substitute for or superior to measures of financial performance prepared in accordance with U.S. GAAP. See reconciliations between each non-GAAP measure and the most comparable GAAP measure contained in our prior reports filed with or furnished to the SEC. This presentation also contains statistical data that we obtained from industry publications and reports generated by third parties. Although we believe that the publications and reports are reliable, we have not independently verified this statistical data.

©2015 YUME. ALL RIGHTS RESERVED. 2

LEADING END-TO-END DIGITAL VIDEO AD PLATFORM COMPANY

Delivering Audiences That Matter to TV Brands

3

Unlocking Audience Value

Combining the reach and frequency of TV with the software of digital Embedded Software + Data Sciences = Cross-screen,

brand-safe campaigns to attentive & receptive audiences

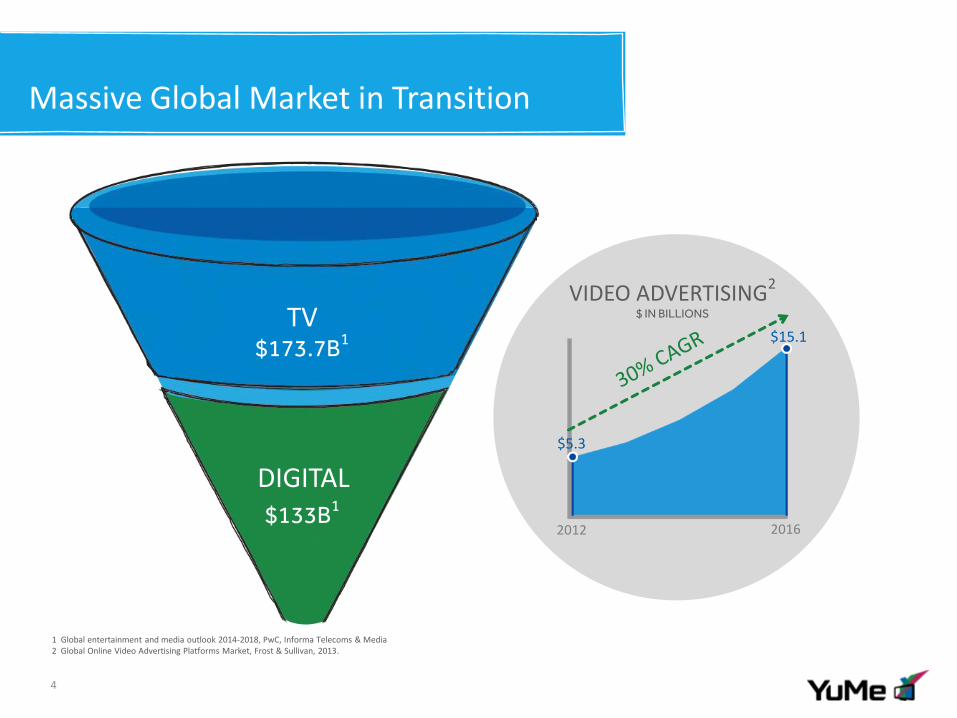

Massive Global Market in Transition

4

2012 2016

$15.1

VIDEO ADVERTISING

2

$ IN BILLIONS

$5.3

1 Global entertainment and media outlook 2014-2018, PwC, Informa Telecoms & Media 2 Global Online Video Advertising Platforms Market, Frost & Sullivan, 2013.

TV $173.7B

1

$133B1

DIGITAL

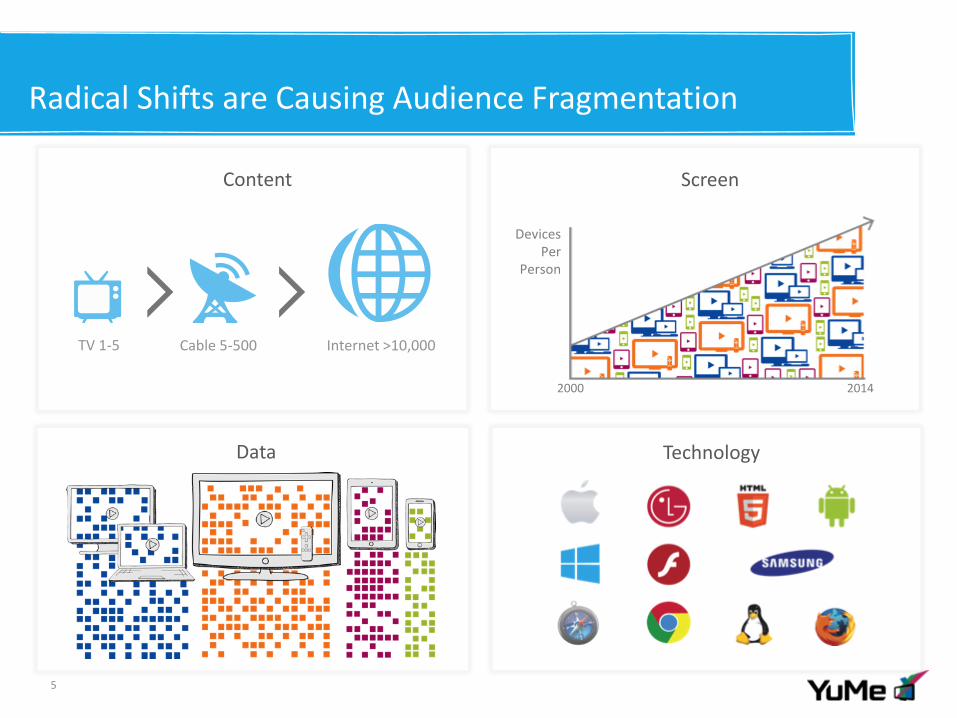

Content

TV 1-5 Cable 5-500 Internet >10,000

Technology

Radical Shifts are Causing Audience Fragmentation

5

Screen

Devices Per

Person

2000 2014

Data

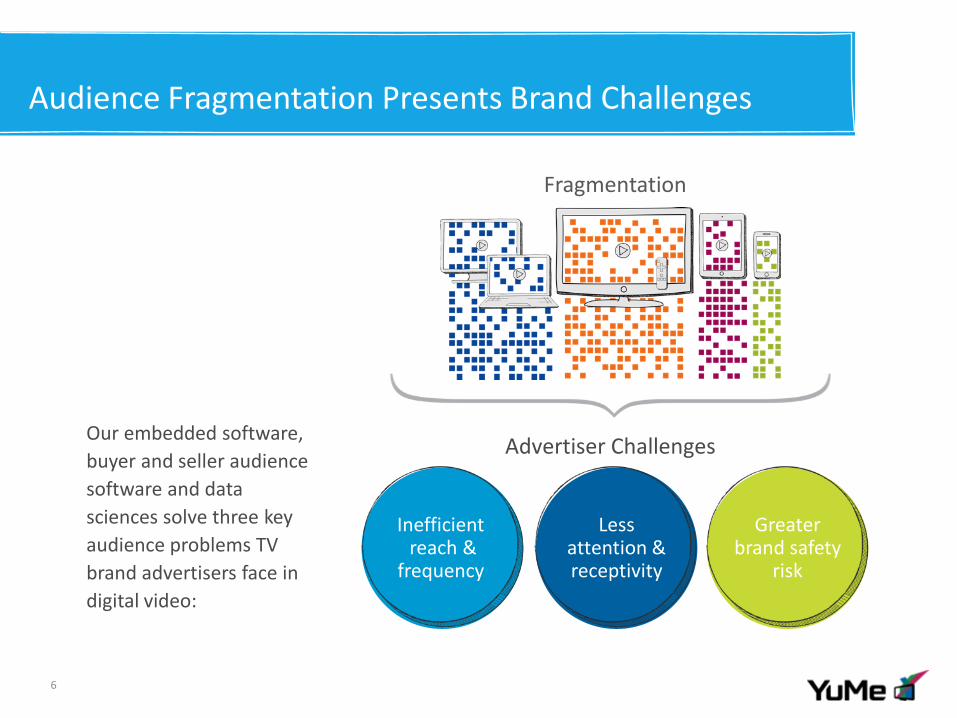

Audience Fragmentation Presents Brand Challenges

6

Advertiser Challenges

Greater brand safety

risk

Inefficient reach &

frequency

Less attention & receptivity

Fragmentation

Our embedded software,

buyer and seller audience

software and data

sciences solve three key

audience problems TV

brand advertisers face in

digital video:

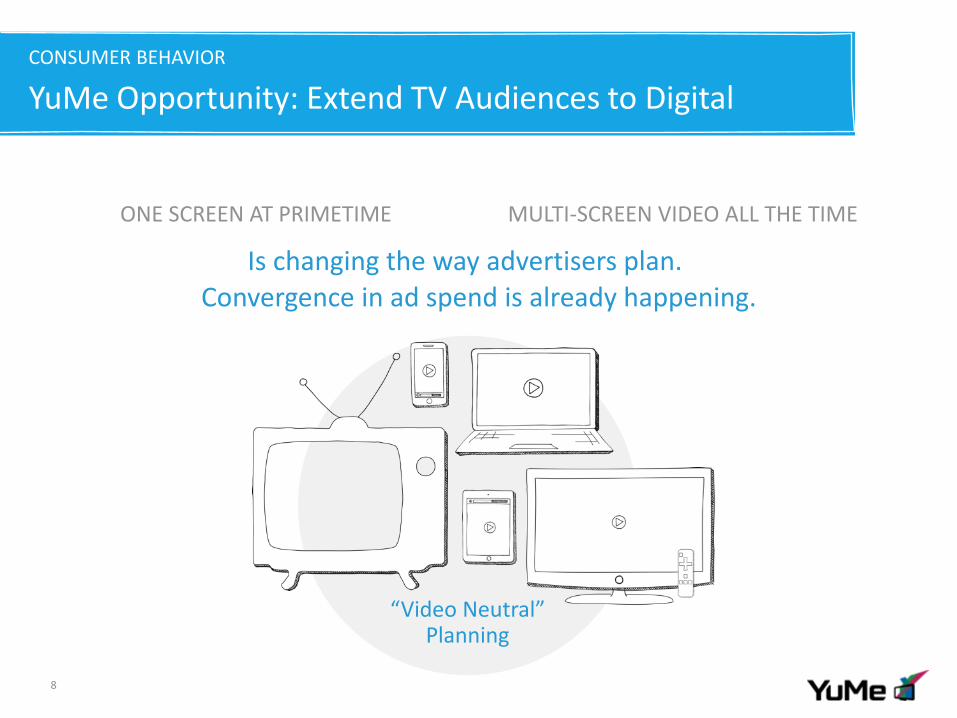

CONSUMER BEHAVIOR

YuMe Opportunity: Extend TV Audiences to Digital

7

ONE SCREEN AT PRIMETIME MULTI-SCREEN VIDEO ALL THE TIME

CONSUMER BEHAVIOR

YuMe Opportunity: Extend TV Audiences to Digital

8

ONE SCREEN AT PRIMETIME MULTI-SCREEN VIDEO ALL THE TIME

Is changing the way advertisers plan. Convergence in ad spend is already happening.

“Video Neutral” Planning

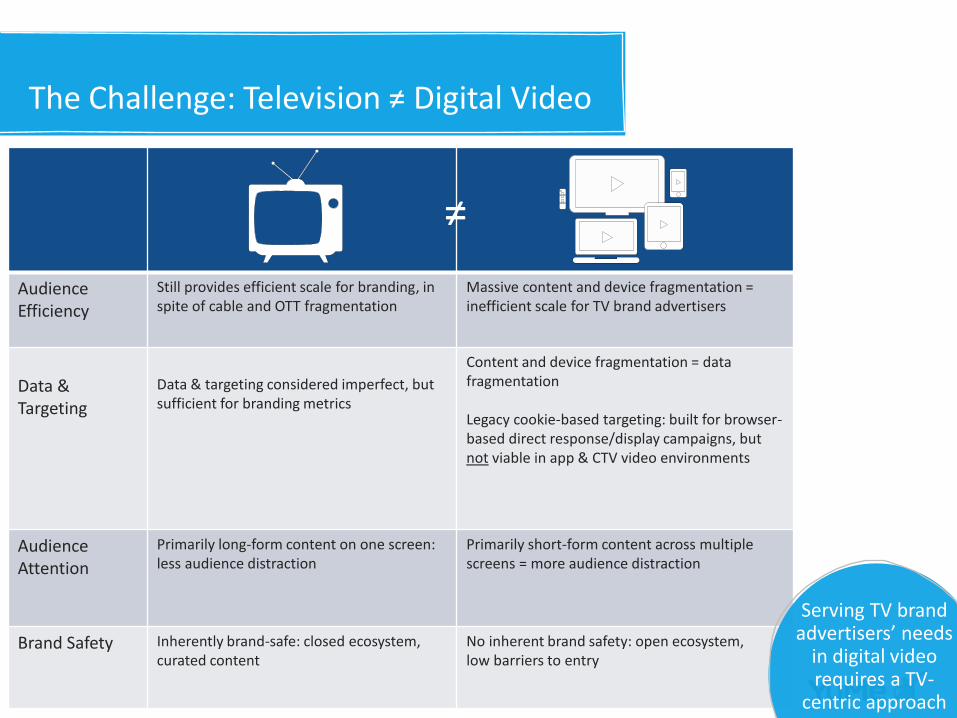

The Challenge: Television ≠ Digital Video

Audience Efficiency

Still provides efficient scale for branding, in spite of cable and OTT fragmentation

Massive content and device fragmentation = inefficient scale for TV brand advertisers

Data & Targeting

Data & targeting considered imperfect, but sufficient for branding metrics

Content and device fragmentation = data fragmentation Legacy cookie-based targeting: built for browser-based direct response/display campaigns, but not viable in app & CTV video environments

Audience Attention

Primarily long-form content on one screen: less audience distraction

Primarily short-form content across multiple screens = more audience distraction

Brand Safety Inherently brand-safe: closed ecosystem, curated content

No inherent brand safety: open ecosystem, low barriers to entry

≠

Serving TV brand advertisers’ needs

in digital video requires a TV-

centric approach

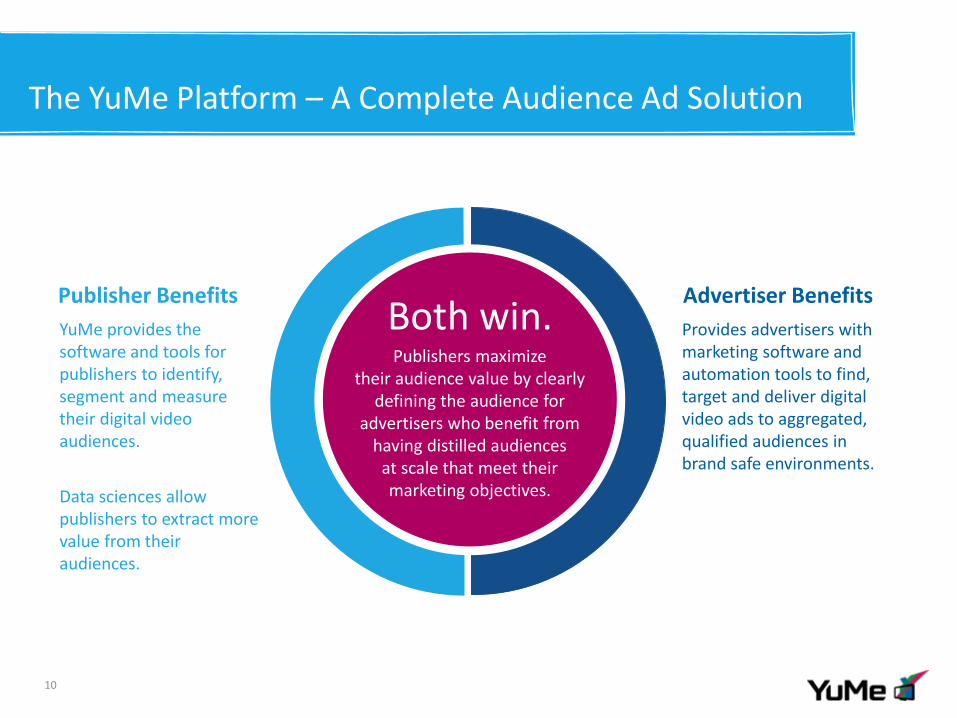

The YuMe Platform – A Complete Audience Ad Solution

10

Publisher Benefits Advertiser Benefits

Provides advertisers with marketing software and automation tools to find, target and deliver digital video ads to aggregated, qualified audiences in brand safe environments.

YuMe provides the software and tools for publishers to identify, segment and measure their digital video audiences.

Data sciences allow publishers to extract more value from their audiences.

Both win. Publishers maximize

their audience value by clearly defining the audience for

advertisers who benefit from having distilled audiences

at scale that meet their marketing objectives.

Purpose Built Video Audience Tech Stack

11

YuMe Supply Platform

YuMe Demand Platform

• Multiple buying channels – Direct, programmatic, private marketplaces, exchanges

• DSP enabling programmatic procurement of YuMe SDK-enabled inventory as well as third-party SSP inventory

• Deal ID management

• RTB 2.2 Support

• Bidding engine to optimize deals

• RFP/IO Workflow Automation

• 450+ brand advertisers: global, regional, local

• 150+ Ad Sales & Ad operations people in NA, APAC and Europe

• Ad serving: Online, Mobile and Smart TV

• SSP Integrated with RTB 2.2 compliant exchanges and demand side platforms

• Full suite of campaign management, creative, targeting and reporting capabilities

• Universal SDKs - Support for AS3, iOS, Android, HTML5 and Embedded C SDKs, MRAID, VPAID and VAST standard compliant

• Targeting and reporting across all screens

YuMe

Data Platform

First Party data collection through embedded

SDK in video delivery environment

Targeting and reporting across all screens.

Integration with advertisers and publishers DMP

Audience Modeling and Targeting Capability

TURNKEY PLATFORM + SERVICES

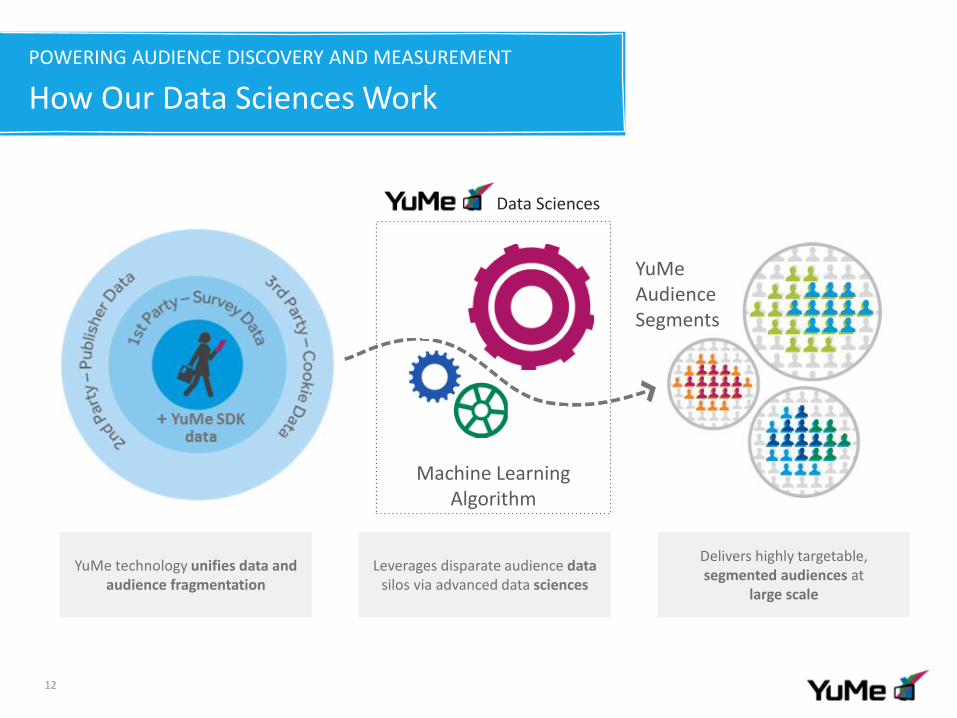

POWERING AUDIENCE DISCOVERY AND MEASUREMENT

How Our Data Sciences Work

12

YuMe technology unifies data and audience fragmentation

Machine Learning Algorithm

Data Sciences

Leverages disparate audience data silos via advanced data sciences

YuMe Audience Segments

Delivers highly targetable, segmented audiences at

large scale

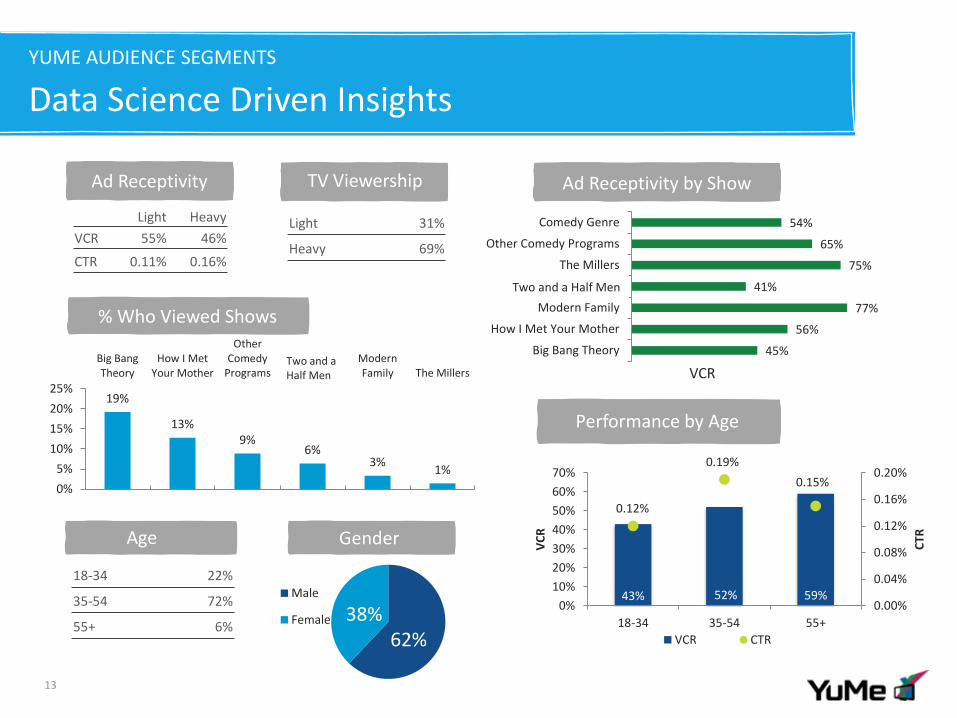

YUME AUDIENCE SEGMENTS

Data Science Driven Insights

13

18-34 22%

35-54 72%

55+ 6%

Gender Age

Light 31%

Heavy 69%

Light Heavy

VCR 55% 46%

CTR 0.11% 0.16%

Performance by Age

TV Viewership Ad Receptivity Ad Receptivity by Show

VCR

43% 52% 59%

0.12%

0.19%

0.15%

0.00%

0.04%

0.08%

0.12%

0.16%

0.20%

0%

10%

20%

30%

40%

50%

60%

70%

18-34 35-54 55+

CTR

VC

R

VCR CTR

45%

56%

77%

41%

75%

65%

54%

Big Bang Theory

How I Met Your Mother

Modern Family

Two and a Half Man

The Millers

Other Comedy Programs

Comedy Genre

% Who Viewed Shows

19%

13% 9%

6% 3%

1%

0%

5%

10%

15%

20%

25%

Big BangTheory

How I MetYour Mother

OtherComedy

ProgramsTwo and aHalf Man

ModernFamily The Millers

62% 38%

Male

Female

Two and a Half Men

Two and a Half Men

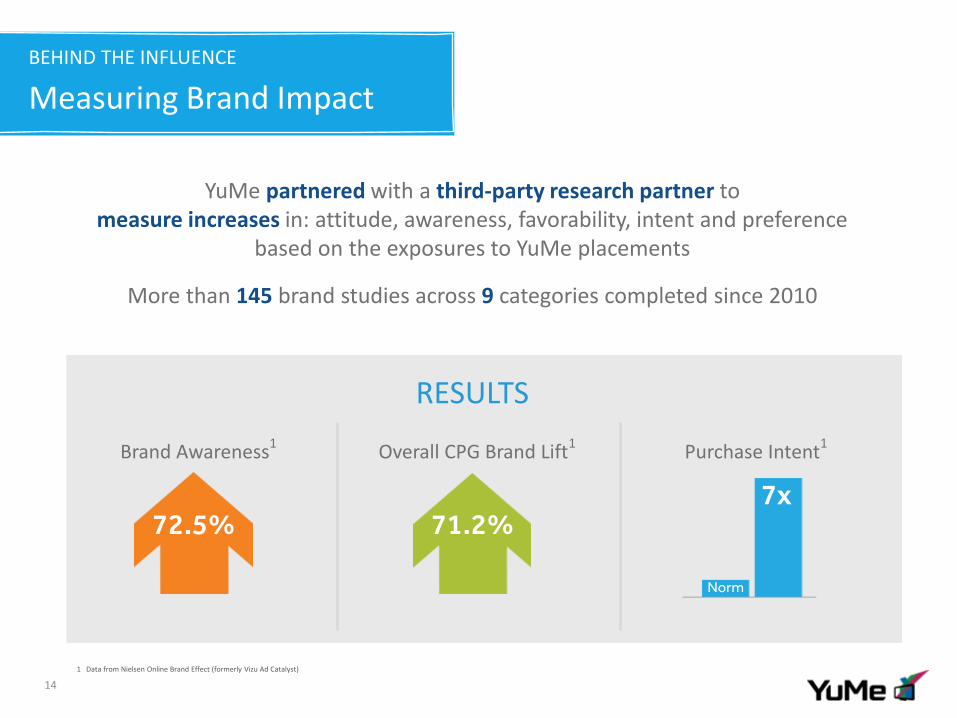

BEHIND THE INFLUENCE

Measuring Brand Impact

YuMe partnered with a third-party research partner to measure increases in: attitude, awareness, favorability, intent and preference

based on the exposures to YuMe placements

More than 145 brand studies across 9 categories completed since 2010

14

RESULTS

Brand Awareness1 Overall CPG Brand Lift

1 Purchase Intent

1

71.2% 72.5% 7x

Norm

1 Data from Nielsen Online Brand Effect (formerly Vizu Ad Catalyst)

100%

100% 67%

60%

26%

The Power of Television – Magnified

Cross-platform exposure drives superior brand-lift compared to TV alone for AdAge 100 Advertisers.

15

43%

24%

20%

15% 12%

34%

15%

10% 9% 6%

General Recall Brand Recall Message Recall Likeability Purchase Intent

Exposed To YuMe Campaign + TV Exposed to TV Ads Only

Source: Nielsen TV Brand Effect, A21+ Norm data from January 1, 2011 – January 1, 2012 Data is limited to same brands on TV & Online: Data is based on viewers exposure to the brand in the prior 7 days. Data is limited to exposure to video ads only on non-full episode player sites. Purchase intent is top 2 box. Same brands include: Hornitos Premium Tequila, Jim Beam Bourbon, Kahlua Coffee Liqueur, Maker's Mark Bourbon, & Pucker Flavored Vodka )

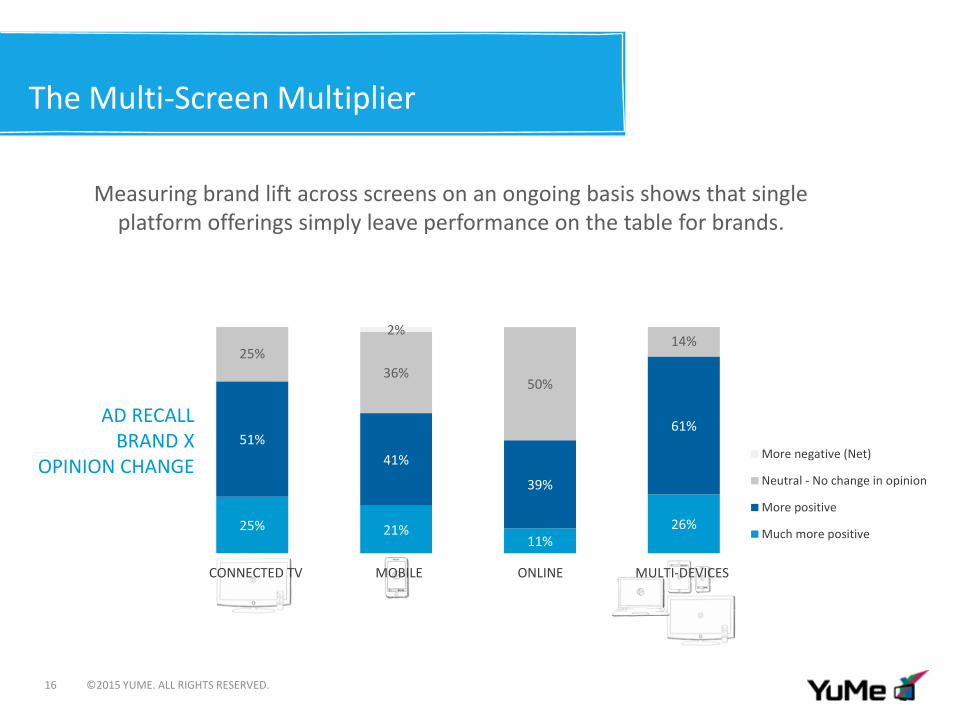

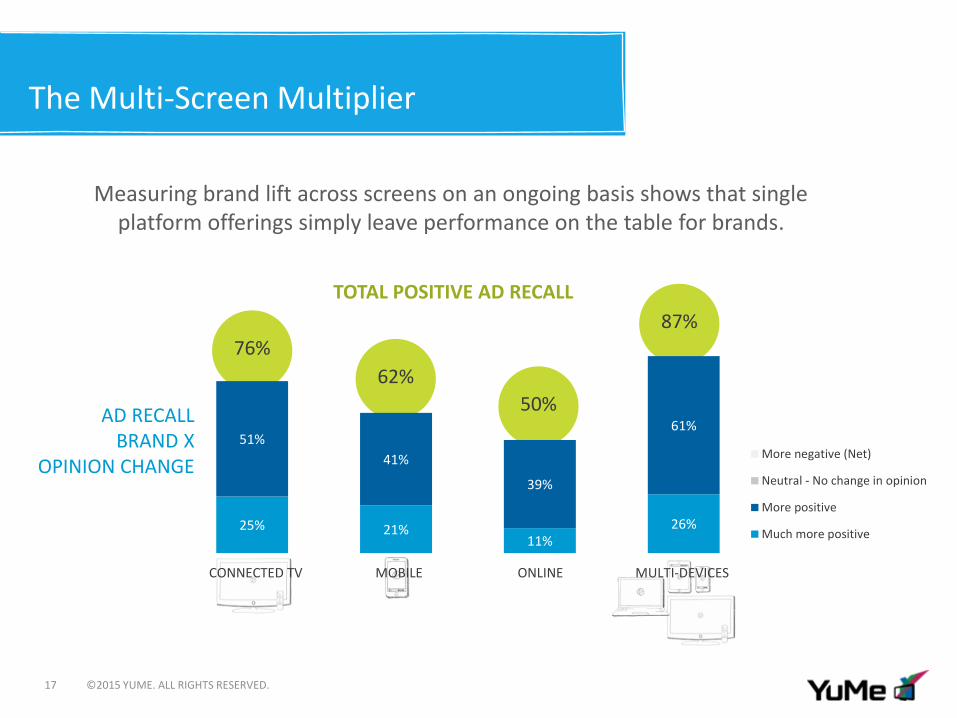

The Multi-Screen Multiplier

©2015 YUME. ALL RIGHTS RESERVED. 16

AD RECALL BRAND X

OPINION CHANGE

25% 21% 11%

26%

51%

41%

39%

61%

25%

36% 50%

14% 2%

More negative (Net)

Neutral - No change in opinion

More positive

Much more positive

CONNECTED TV MOBILE ONLINE MULTI-DEVICES

Measuring brand lift across screens on an ongoing basis shows that single platform offerings simply leave performance on the table for brands.

25% 21% 11%

26%

51%

41%

39%

61%

25%

36% 50%

14% 2%

More negative (Net)

Neutral - No change in opinion

More positive

Much more positive

The Multi-Screen Multiplier

©2015 YUME. ALL RIGHTS RESERVED. 17

AD RECALL BRAND X

OPINION CHANGE

CONNECTED TV MOBILE ONLINE MULTI-DEVICES

Measuring brand lift across screens on an ongoing basis shows that single platform offerings simply leave performance on the table for brands.

76%

62%

50%

87%

25% 21% 11%

26%

51%

41%

39%

61%

TOTAL POSITIVE AD RECALL

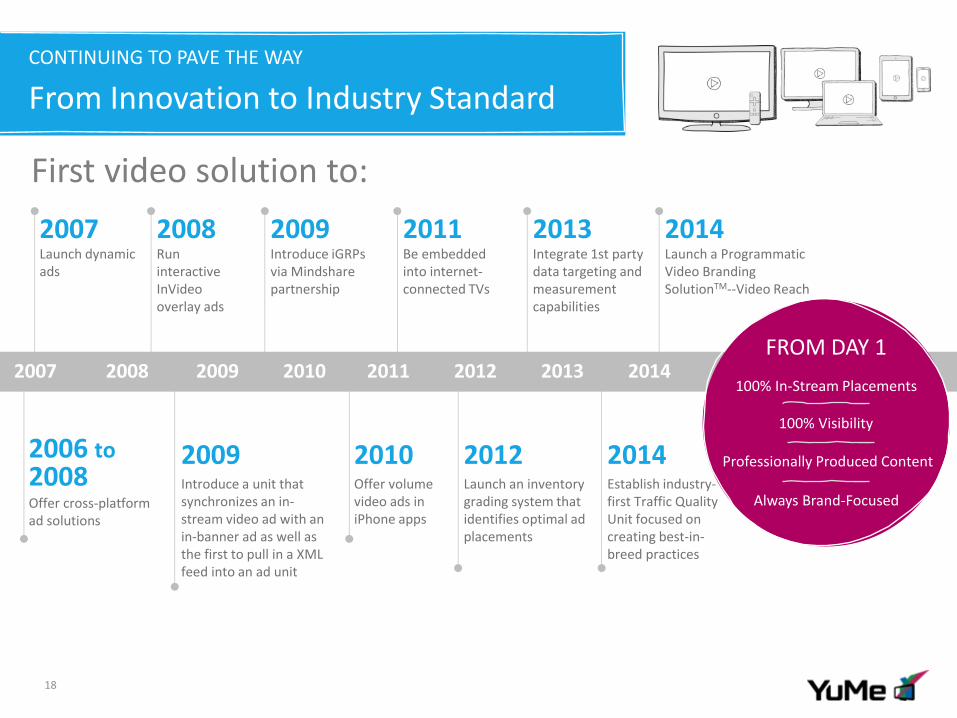

Launch an inventory grading system that identifies optimal ad placements

2012

CONTINUING TO PAVE THE WAY

From Innovation to Industry Standard

18

Offer cross-platform ad solutions

2006 to 2008 Introduce a unit that

synchronizes an in-stream video ad with an in-banner ad as well as the first to pull in a XML feed into an ad unit

2009

Launch dynamic ads

2007 Introduce iGRPs via Mindshare partnership

2009 Integrate 1st party data targeting and measurement capabilities

2013

First video solution to:

FROM DAY 1

100% In-Stream Placements

Professionally Produced Content

Always Brand-Focused

100% Visibility

Launch a Programmatic Video Branding SolutionTM--Video Reach

2014 Run interactive InVideo overlay ads

2008 Be embedded into internet-connected TVs

2011

Offer volume video ads in iPhone apps

2010 Establish industry-first Traffic Quality Unit focused on creating best-in-breed practices

2014

2008 2007 2009 2010 2013 2012 2011 2014

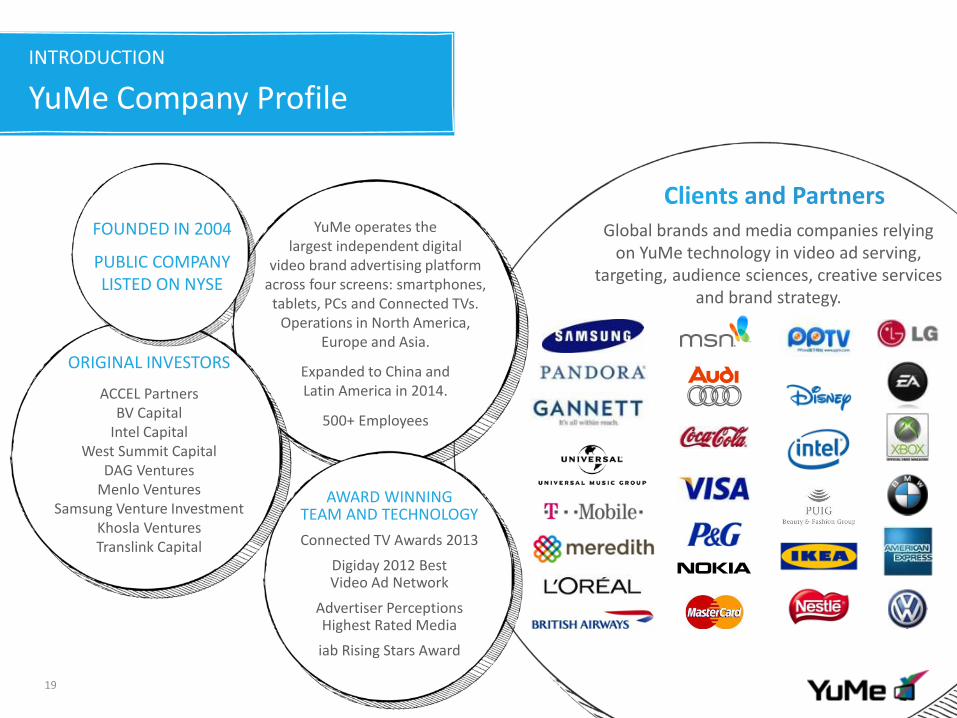

INTRODUCTION

YuMe Company Profile

19

Clients and Partners FOUNDED IN 2004

PUBLIC COMPANY LISTED ON NYSE

ORIGINAL INVESTORS

ACCEL Partners BV Capital

Intel Capital West Summit Capital

DAG Ventures Menlo Ventures

Samsung Venture Investment Khosla Ventures Translink Capital

YuMe operates the largest independent digital

video brand advertising platform across four screens: smartphones,

tablets, PCs and Connected TVs. Operations in North America,

Europe and Asia.

Expanded to China and Latin America in 2014.

500+ Employees

Global brands and media companies relying on YuMe technology in video ad serving,

targeting, audience sciences, creative services and brand strategy.

AWARD WINNING TEAM AND TECHNOLOGY

Connected TV Awards 2013

Digiday 2012 Best Video Ad Network

Advertiser Perceptions Highest Rated Media

iab Rising Stars Award

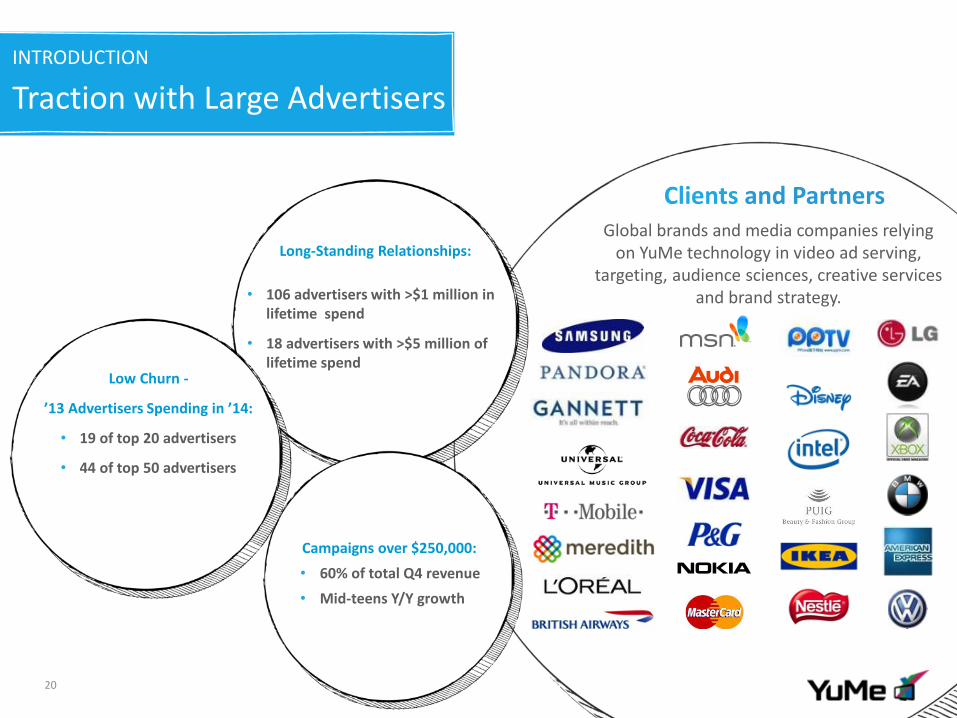

INTRODUCTION

Traction with Large Advertisers

20

Clients and Partners Global brands and media companies relying

on YuMe technology in video ad serving, targeting, audience sciences, creative services

and brand strategy.

Long-Standing Relationships:

• 106 advertisers with >$1 million in lifetime spend

• 18 advertisers with >$5 million of lifetime spend

Campaigns over $250,000:

• 60% of total Q4 revenue

• Mid-teens Y/Y growth

Low Churn -

’13 Advertisers Spending in ’14:

• 19 of top 20 advertisers

• 44 of top 50 advertisers

21

COMPANY OVERVIEW

Global Offices and Ongoing Expansion

2014 Total Headcount: 500+ Employees

Offices: Redwood City HQ New York, Chicago, Los Angeles, Boston, Dallas, Detroit, Atlanta, Miami, Toronto, Mexico City, Pune, Chennai, London, Paris, Madrid, Hamburg, Stockholm, Hong Kong, Shanghai

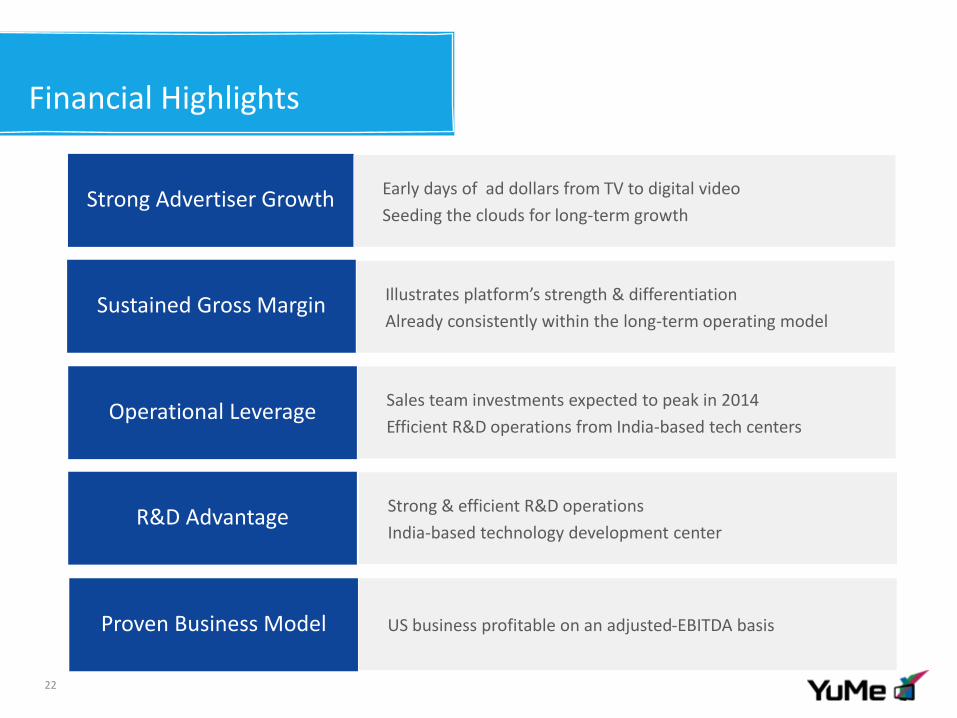

Financial Highlights

22

Proven Business Model US business profitable on an adjusted-EBITDA basis

Operational Leverage Sales team investments expected to peak in 2014

Efficient R&D operations from India-based tech centers

R&D Advantage Strong & efficient R&D operations

India-based technology development center

Sustained Gross Margin Illustrates platform’s strength & differentiation

Already consistently within the long-term operating model

Strong Advertiser Growth Early days of ad dollars from TV to digital video

Seeding the clouds for long-term growth

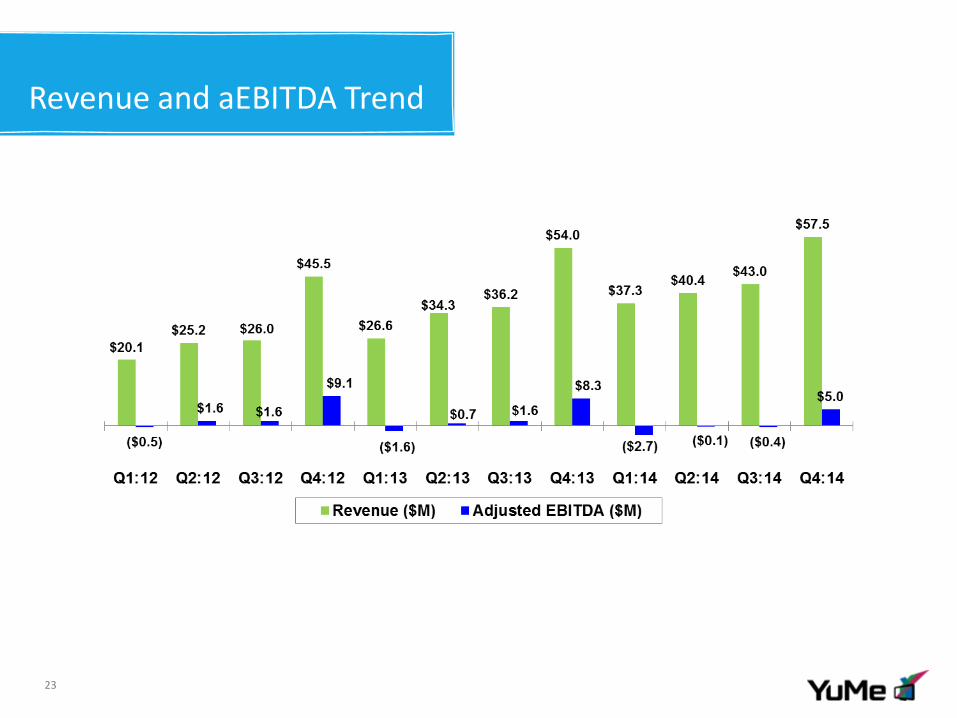

Revenue and aEBITDA Trend

23

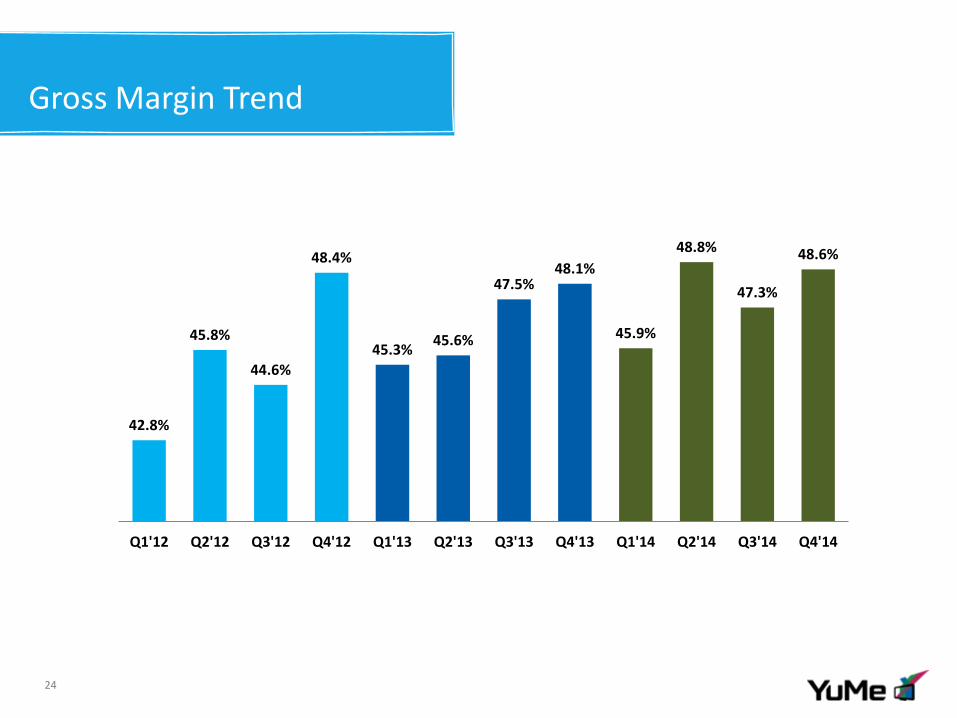

Gross Margin Trend

24

42.8%

45.8%

44.6%

48.4%

45.3% 45.6%

47.5% 48.1%

45.9%

48.8%

47.3%

48.6%

Q1'12 Q2'12 Q3'12 Q4'12 Q1'13 Q2'13 Q3'13 Q4'13 Q1'14 Q2'14 Q3'14 Q4'14

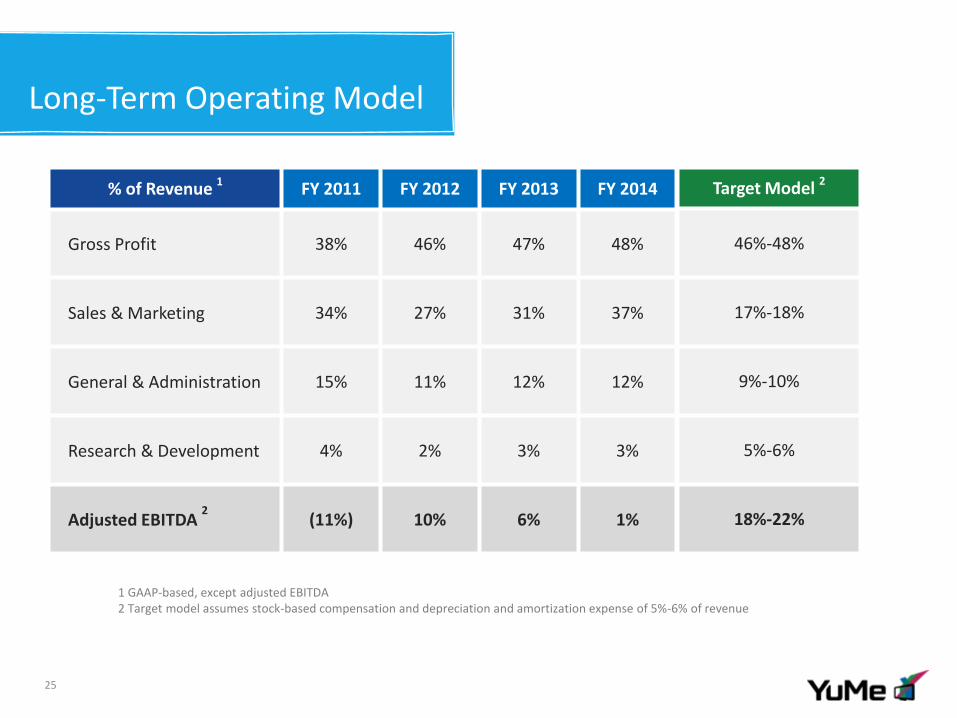

Long-Term Operating Model

25

Target Model 2

46%-48%

17%-18%

9%-10%

5%-6%

18%-22%

% of Revenue 1 FY 2011 FY 2012 FY 2013 FY 2014

Gross Profit 38% 46% 47% 48%

Sales & Marketing 34% 27% 31% 37%

General & Administration 15% 11% 12% 12%

Research & Development 4% 2% 3% 3%

Adjusted EBITDA 2

(11%) 10% 6% 1%

1 GAAP-based, except adjusted EBITDA 2 Target model assumes stock-based compensation and depreciation and amortization expense of 5%-6% of revenue

©2013 YUME. ALL RIGHTS RESERVED. 26

Thank you.