winning strategies for mitigating risk - deloitte.com · winning strategies for mitigating risk...

TRANSCRIPT

Winning strategies for mitigating risk

2018 Engineering and Construction ConferenceJune 20-22, 2018

Presentation title[To edit, click View > Slide Master > Slide master1]

Copyright © 2017 Deloitte Development LLC. All rights reserved. 2

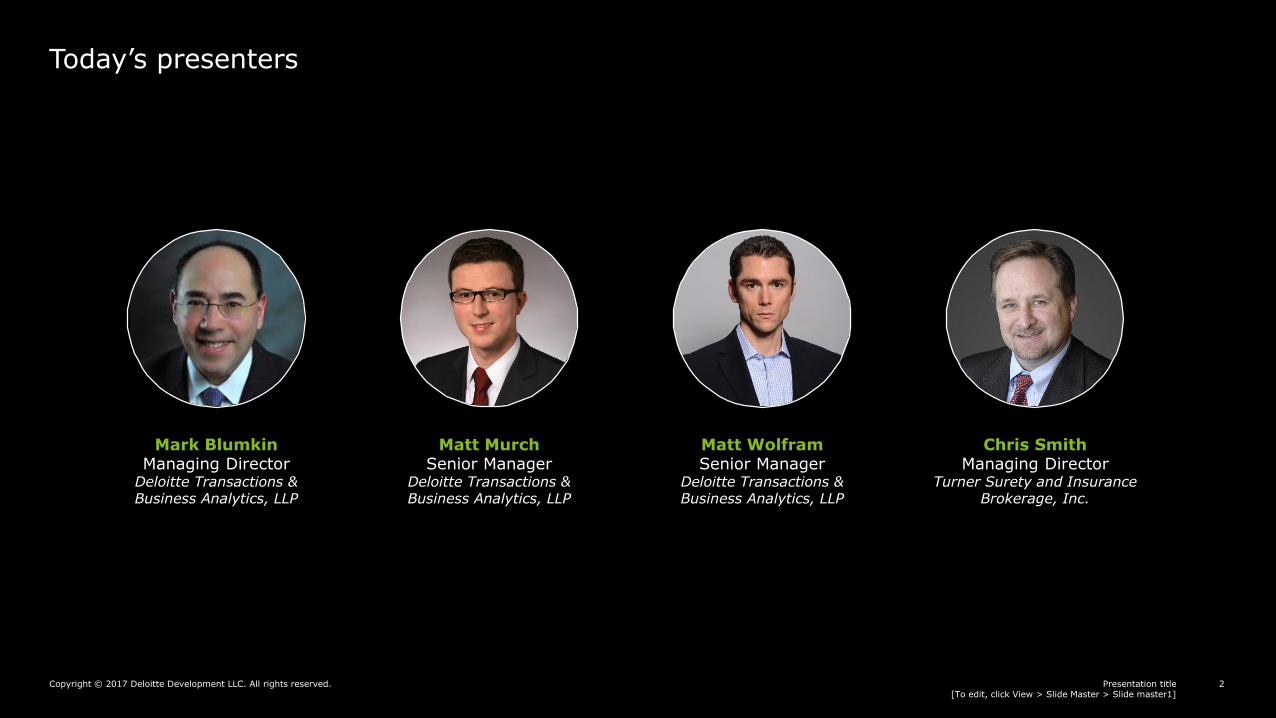

Today’s presenters

Mark BlumkinManaging Director

Deloitte Transactions & Business Analytics, LLP

Chris SmithManaging Director

Turner Surety and Insurance Brokerage, Inc.

Matt MurchSenior Manager

Deloitte Transactions & Business Analytics, LLP

Matt WolframSenior Manager

Deloitte Transactions & Business Analytics, LLP

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 3

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 4

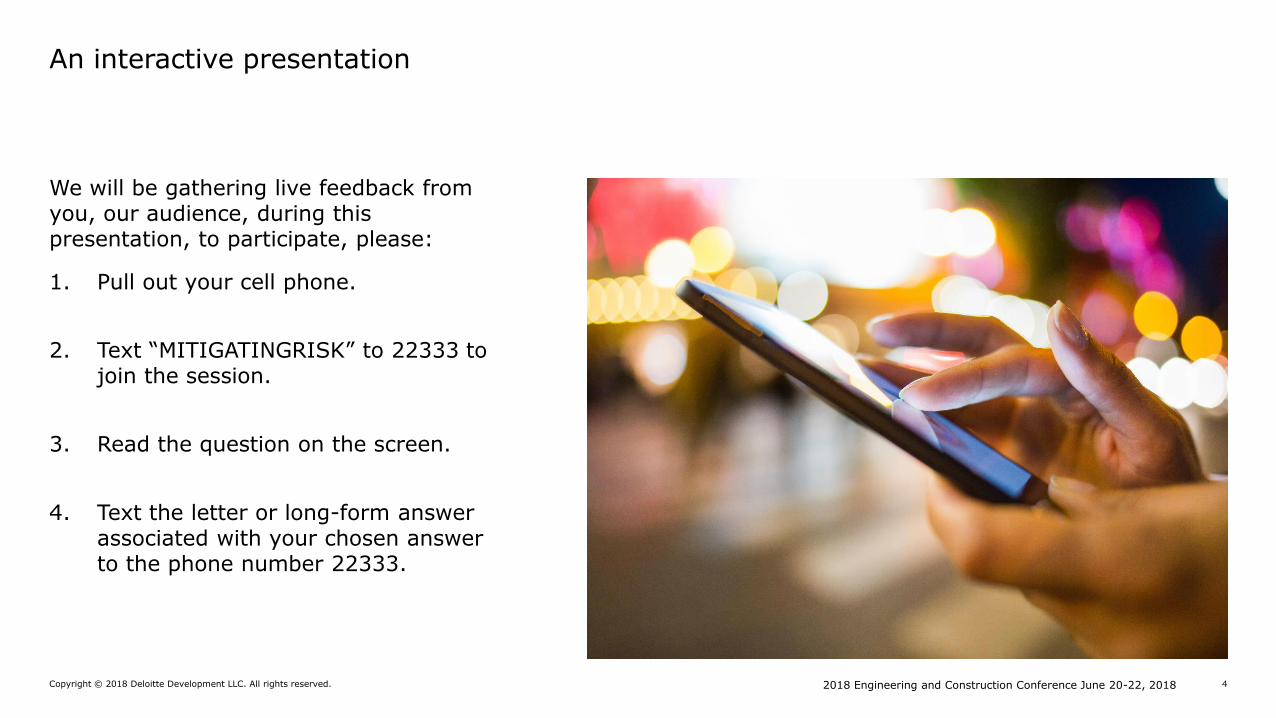

We will be gathering live feedback from you, our audience, during this presentation, to participate, please:

1. Pull out your cell phone.

2. Text “MITIGATINGRISK” to 22333 to join the session.

3. Read the question on the screen.

4. Text the letter or long-form answer associated with your chosen answer to the phone number 22333.

An interactive presentation

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 5

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 6

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 7

• Financial Risk & Mitigation Strategy

• Owner Construction Audit Risk

• Captive Insurance

• Culture of Risk

• Game Time

Presentation overview

Financial Risk & Mitigation Strategy Matt Murch, Senior ManagerDeloitte Transactions and Business Analytics, LLP

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 9

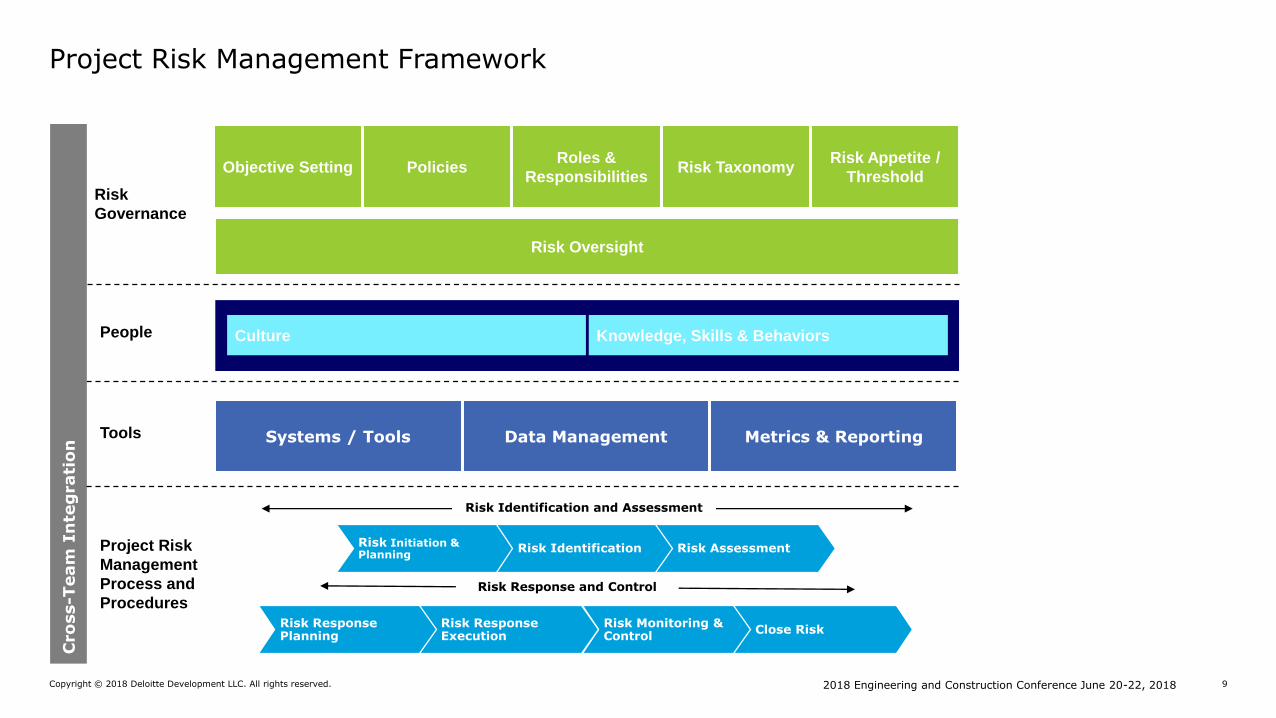

Project Risk Management Framework

Risk Oversight

Risk

Governance

People

Systems / Tools Data Management Metrics & ReportingTools

Risk Initiation & Planning

Risk Identification Risk Assessment

Objective Setting PoliciesRoles &

ResponsibilitiesRisk Taxonomy

Risk Appetite /

Threshold

Cro

ss-T

eam

In

teg

rati

on

Project Risk

Management

Process and

Procedures

Risk Monitoring & Control

Risk Response Planning

Risk Response Execution

Close Risk

Risk Identification and Assessment

Risk Response and Control

Culture Knowledge, Skills & Behaviors

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 10

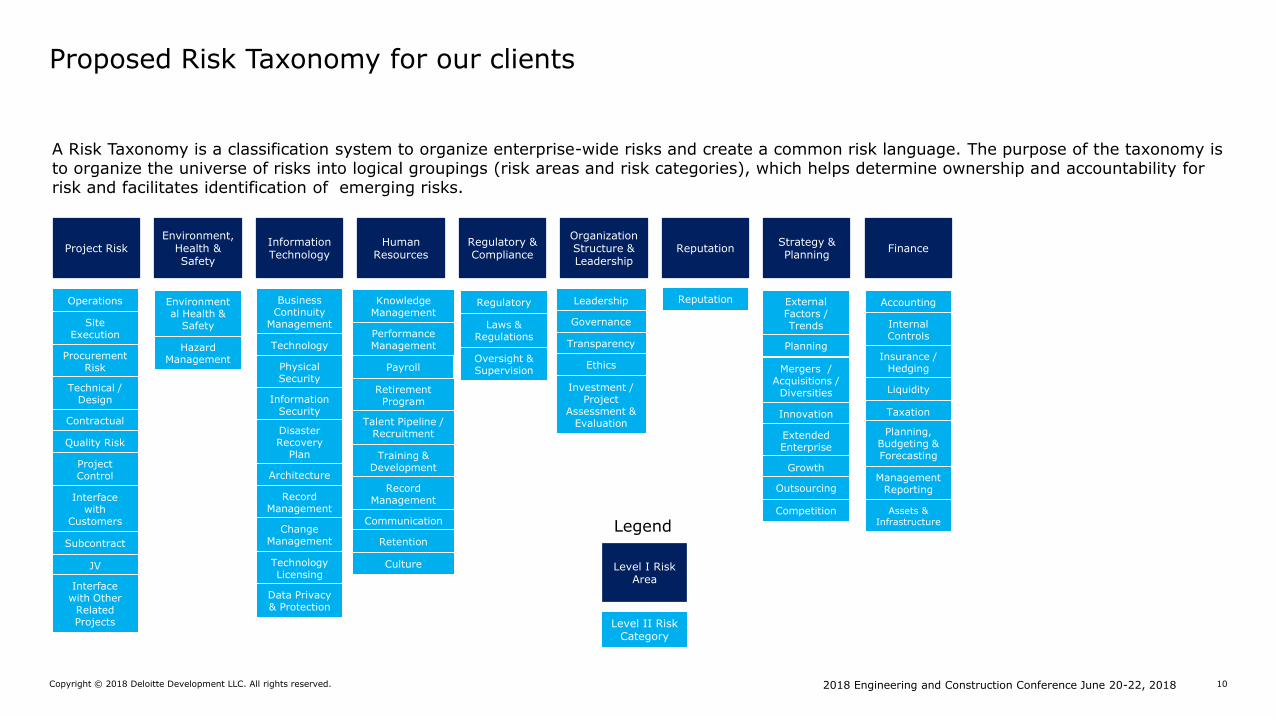

A Risk Taxonomy is a classification system to organize enterprise-wide risks and create a common risk language. The purpose of the taxonomy is to organize the universe of risks into logical groupings (risk areas and risk categories), which helps determine ownership and accountability for risk and facilitates identification of emerging risks.

Proposed Risk Taxonomy for our clients

Project RiskEnvironment,

Health & Safety

Information Technology

Human Resources

Regulatory & Compliance

Organization Structure & Leadership

Reputation

Operations

Site Execution

Procurement Risk

Technical / Design

Contractual

Quality Risk

Project Control

Interface with

Customers

Subcontract

JV

Interface with Other

Related Projects

Strategy & Planning

Finance

Environmental Health &

Safety

Hazard Management

Business Continuity

Management

Technology

Physical Security

Information Security

Disaster Recovery

Plan

Architecture

Record Management

Change Management

Technology Licensing

Data Privacy & Protection

Knowledge Management

Performance Management

Payroll

Retirement Program

Talent Pipeline / Recruitment

Training & Development

Record Management

Communication

Retention

Culture

Regulatory

Laws & Regulations

Oversight & Supervision

Leadership

Governance

Transparency

Ethics

Investment / Project

Assessment & Evaluation

Reputation External Factors / Trends

Planning

Mergers / Acquisitions /

Diversities

Innovation

Extended Enterprise

Growth

Outsourcing

Competition

Accounting

Internal Controls

Insurance / Hedging

Liquidity

Taxation

Planning, Budgeting & Forecasting

Management Reporting

Assets & Infrastructure

Level I Risk Area

Level II Risk Category

Legend

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 11

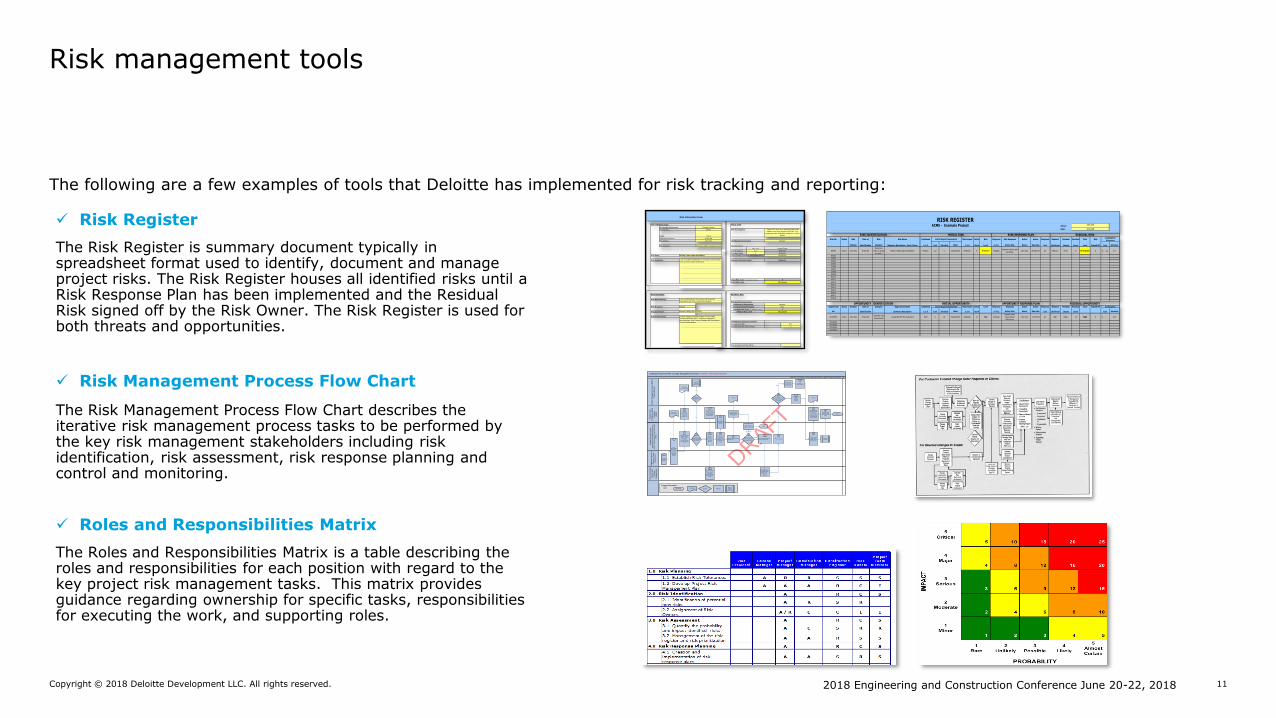

The following are a few examples of tools that Deloitte has implemented for risk tracking and reporting:

Risk management tools

Risk Information Form

RISK IDENTIFICATION INITIAL RISK

Risk Assumptions

Risk Category Potential Impact

Most Likely

Cost ($ millions) $2.2

Schedule (days) 8

Risk Name

Risk Symptoms

Initial Risk Level

RISK RESPONSE RESIDUAL RISK

Risk Root Cause(s)

Risk Response Maximum Potential Impact

Residual Risk Score (= Likelihood x Impact)

Response Name Residual Risk Level

Action Plan Details

Contingency allowance provided

Residual cost ($M)

Residual schedule impact (days)

Risk Accepted and Sign Off By

Signature and Date:

Action Details

Action Owner Comments / Remarks / Attachments

Action Due date

Action Cost ($M)

Develop enhaced training program for key trades

requiring additional labor. Implement aggressive

recruiting plan. See Training Strategy and Recruitment

Plan for further details.

Of Concern

Lack of available skilled labor is resulting increased labor

costs and may impact productivity.

Medium

Residual Risk Assessment

Likelihood of Occurrence

6

Of Concern

3

Minor

Moderate

John Doe

20-Sep-08

Initial Risk Score (= Likelihood x Impact)

Improve training and recruiting.

$0.1

Trades XZY have been impacted and trends

indicate costs may increase by $2.2M. See

supporting Labor Availability Analysis for further

details.

Moderate

Moderate

9

Impact Score

Medium

Insignificant

Active

John Doe

EX001

Resources (Who is doing the work)

Likelihood of Occurrence

Maximum Potential Impact

Date of Identification

Skilled Trades Labor Availability Other (Quality, Customer Satisfaction, etc.)

Example ProjectResponsible Organization

$1.2

Lack of skilled labor in local areas and increased

completition with other construction projects.

Mitigate

Risk Number

8-Sep-08

Risk Initiator

Status

RISK REGISTERACME - Example Project Owner:

Date:

Risk No. Status Risk Date of Risk Risk Name Likelihood Max Impact Initial Risk Response Risk Response Action Action Response Residual Residual Residual Risk Risk

Initiator Identification Category Summary Description - Root Causes L:1-5 Cost Schedule Other I:1-5 Score Level (4 T's) Action Plan Owner Due Date Cost Likelihood Impact Score Level Signed Off Cost Schedule

EX001 Active John Doe 8-Sep-08

Resources

(Who is doing

the work)

Skilled Trades Labor Availability Medium 2.2 8 Insignificant Moderate 9 Of Concern MitigateImprove training and

recruiting.John Doe 20-Sep-08 $0 Medium Minor 6 Of Concern 0 1.2$ 3.0

EX002

EX003

EX004

EX005

EX006

EX007

EX008

EX009

EX010

EX011

EX012

EX013

EX014

EX015

EX016

EX017

EX018

Opportunity Status Initiator Date of Category Opportunity Name Likelihood Max Impact Initial Level Response Response Action Action Response Residual Residual Residual Level Signed Off

No. Identification Summary Description L:1-5 Cost Schedule Other I:1-5 Score (4 T's) Action Plan Owner Due Date Cost Likelihood Impact Score Cost Schedule

EX-OP001 Active John Doe 8-Sep-08Interface with

ProcurementAccelerate RFP for Equipment High 0 10 Insignificant Moderate 12 High Enhance

Identify other

procurement

efficiencies

John Doe 15-Oct-08 $0 High Major 16 High 0 -$ 10.0

EX-OP001

EX-OP001

EX-OP001

EX-OP001

Contingency

John Doe

8-Sep-08

Initial Impact AssessmentContingency

Allowance

RESIDUAL RISK

INITIAL OPPORTUNITY OPPORTUNITY RESPONSE PLAN RESIDUAL OPPORTUNITY

RISK IDENTIFICATION INITIAL RISK RISK RESPONSE PLAN

Initial Impact Assessment

OPPORTUNITY IDENTIFICATION

✓ Risk Register

The Risk Register is summary document typically in spreadsheet format used to identify, document and manage project risks. The Risk Register houses all identified risks until a Risk Response Plan has been implemented and the Residual Risk signed off by the Risk Owner. The Risk Register is used for both threats and opportunities.

✓ Risk Management Process Flow Chart

The Risk Management Process Flow Chart describes the iterative risk management process tasks to be performed by the key risk management stakeholders including risk identification, risk assessment, risk response planning and control and monitoring.

✓ Roles and Responsibilities Matrix

The Roles and Responsibilities Matrix is a table describing the roles and responsibilities for each position with regard to the key project risk management tasks. This matrix provides guidance regarding ownership for specific tasks, responsibilities for executing the work, and supporting roles.

Enbridge Proposed PMT Change Management Process – DRAFT FOR DISCUSSION

Valid for all Phases of the Proposed Major Capital Project Lifecycle

Pro

ject M

anager

/ Lead

(Bu

sin

ess D

eve

lop

me

nt E

ng

ine

erin

g

(BD

E)

/ E

ng

ine

erin

g &

Pro

ject E

xe

cu

tio

n

(EP

E))

DRAFT

Origin

ato

r (I

de

ntifie

r o

f

Ch

an

ge

or

Ch

an

ge

Re

qu

ire

me

nt)

Pro

ject C

ost/

Schedule

Contr

ol

Engin

eer

(PM

T)

Pro

ject M

anagem

ent T

eam

(P

MT

)

Pro

ject D

irecto

r

Oth

er

Functional

Gro

ups a

nd

Exte

rnal

Sta

kehold

ers

Potential

Change

Identified

Initial

identification

Root Cause,

Cost, Schedule

and Scope

impact of

potential

change

Informed of

Potential Change

Originate Potential

Change Notice

(PCN) Document

and record

Potential Change

in Project Change

Log

Review

Potential

Change Notice

& Project

Change Log

PMT

Contingency

Management

Process

Informed of

Potential Change

Does

urgency / Impact

warrant Exception

Sub-process

Review

Potential

Change with

Functional

Groups

Review Potential

Change identify

any related

changes /impacts

due to potential

change

Determine Total

Impacts to

Scope, Cost,

Schedule, Cost

of Schedule &

Funding

Update PCN and Project

Change Log

Review Potential

Change Notice &

Project Change

Log

Merit Assessment

of Potential Change

& Supporting Info.

Convert Updated PCN to a

Project Change Order

Update PCN and

Project Change LogEnd

Endorse Change

Finalize Change

Order and

Update Project

Change Log

Review Change

Order and Project

Change Log

Ensure Budget /

Schedule / Scope

and Contingency

Log are updated

InformedChange

within PD Authorization

Limits & Funding

Available

Review with

Customer via BD

(If Required)

Endorse or

Reject Change

No

NO MERIT

MERIT

YES

Seek AFE and/

or Higher

Approval

Authority

NO

Review / ensure

Functional Group

and Stakeholder

contact and input.

(As Required)

Informed

See PMT

Exception

Sub-process

Approve

Exception Sub-

process

Yes

Yes

Involved

Functional Group

and Stakeholder

Endorsement –

Sign off on

Change

Ensure Change

implemented in

accordance with

PCO

Implement

Change

1

2

3

4

56

7

8

9

10

1112 13

1415

16

17

18

19

End

6a

# Process

defined

elsewhere

ProcessDocument

TerminatorNote Number

Decision

Process Flow Legend:

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 12

Monte Carlo 101As part of this engagement, Deloitte will help the UN utilize the Monte Carlo simulation to assess project risks.

• Quantitative risk analysis enables the client to identify and mitigate “high impact” risks inherent in traditional cost estimates and schedule projections

• Traditional cost estimating and CPM scheduling does not account for risk or uncertainty

• Monte Carlo simulation and scenario analysis accounts for both risk and uncertainty related to cost estimates and project schedules

• Cost and schedule confidence: Monte Carlo simulation and scenario analysis will help to evaluate the range of expected costs or schedule completion dates as well as the confidence levels associated with achieving certain cost or schedule objectives

• Enhanced ability to assess key drivers of risk and uncertainty utilizing statistical information collected during the simulation process

Quantitative Risk Management – Approach

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 13

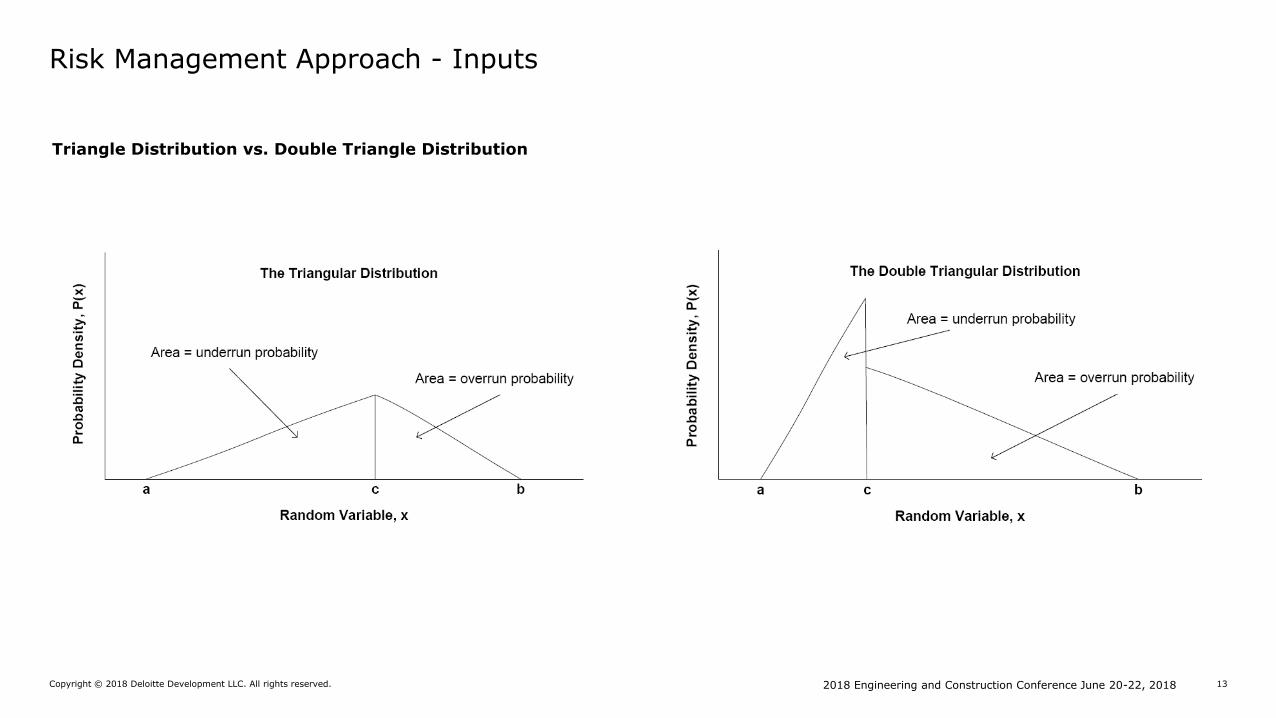

Triangle Distribution vs. Double Triangle Distribution

Risk Management Approach - Inputs

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 14

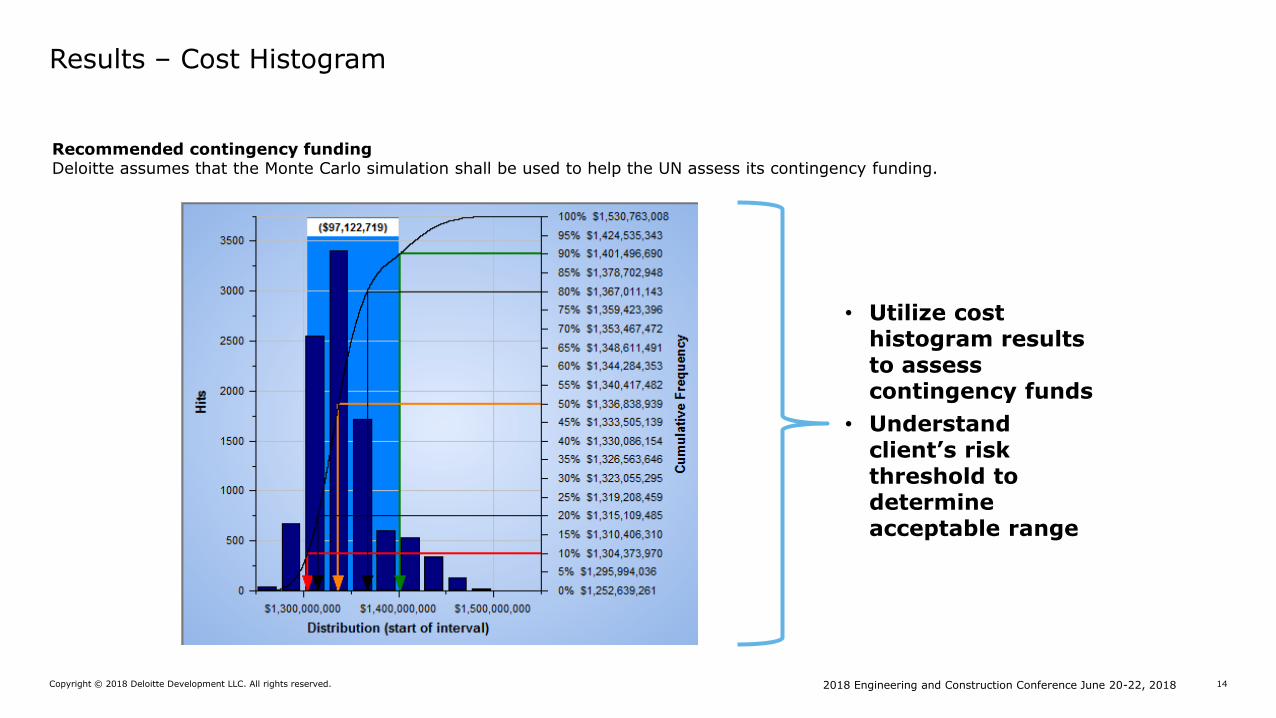

Recommended contingency fundingDeloitte assumes that the Monte Carlo simulation shall be used to help the UN assess its contingency funding.

Results – Cost Histogram

• Utilize cost histogram results to assess contingency funds

• Understand client’s risk threshold to determine acceptable range

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 15

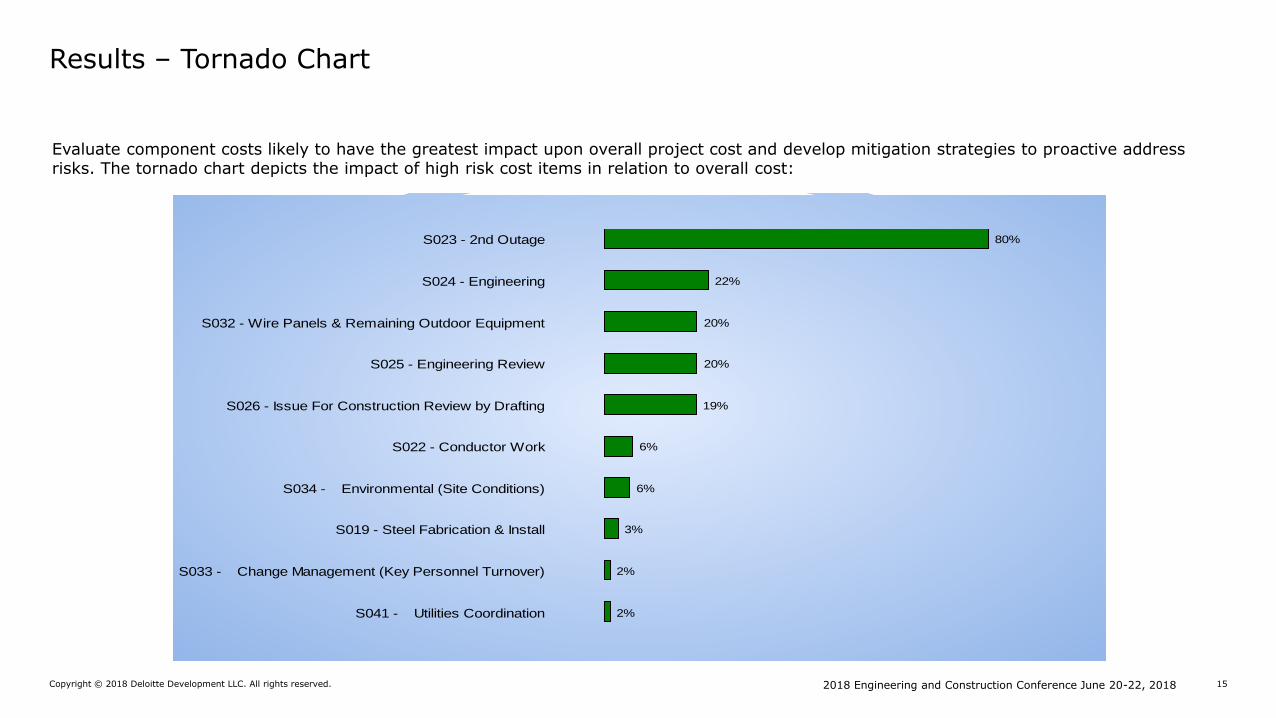

Evaluate component costs likely to have the greatest impact upon overall project cost and develop mitigation strategies to proactive address risks. The tornado chart depicts the impact of high risk cost items in relation to overall cost:

Results – Tornado Chart

2%

2%

3%

6%

6%

19%

20%

20%

22%

80%S023 - 2nd Outage

S024 - Engineering

S032 - Wire Panels & Remaining Outdoor Equipment

S025 - Engineering Review

S026 - Issue For Construction Review by Drafting

S022 - Conductor Work

S034 - Environmental (Site Conditions)

S019 - Steel Fabrication & Install

S033 - Change Management (Key Personnel Turnover)

S041 - Utilities Coordination

ConEd Feeder 76 - 7-2-2015 v01.mppSchedule Sensitivity Index: Entire Plan - All tasks

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 16

Project scope:

• Client has been contracted by two large utility providers to design, procure, manufacture, and construct hydroelectric turbine generators.

• Utilize Monte Carlo to determine if contingency amounts are adequate.

• Review risk register information in risk workshops to develop Monte Carlo inputs and results

Process:

• Conducted numerous risk workshops with project stakeholders

• Collect Monte Carlo inputs to run simulation software and generate results in the form of histograms and tornado charts

Benefits

• Probabilistic range of contingency amounts required to cover identified risks not included in the Estimate-At-Completion (EAC).

• Monte Carlo results used as support in external audit of client’s financial statement

Case Study – Monte Carlo & Financial Reporting

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 17

Project scope:

• Assess the reasonable basis for change orders;

• Assess compliance with contracts, internal procedures and revenue recognition accounting standards IAS 11 and IFRS 15;

• Assess the reasonableness of the order of magnitude of change orders; and,

• Identify opportunities to improve the change management practices.

Process:

• Assessment of the Project change orders for entitlement, prioritization, strengths and weaknesses and alignment with revenue recognition policies and accounting standards

Benefits

• Analyzed risks associated with potential change orders and impacts upon financials

• Worked with client’s financial team and external auditors to support revenue recognition

Case Study – Change Order Risk & Financial Reporting

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 18

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 19

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 20

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 21

Owner Construction Audit RiskMatt Wolfram, Senior ManagerDeloitte Transactions and Business Analytics, LLP

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 23

A look at where the industry is heading

The evolving owner

▪ Owners are becoming more sophisticated and shifting from providing oversight to managing projects

▪ Owners increasingly are commissioning construction audits

▪ What drives that decision?

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 24

The first step of the capital projects specialist is to anticipate the audit:

What is the auditor looking for?

Mitigating audit risk

Types of Audits

Timing of the Audit Audit Accelerators

Questions to Ask

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 25

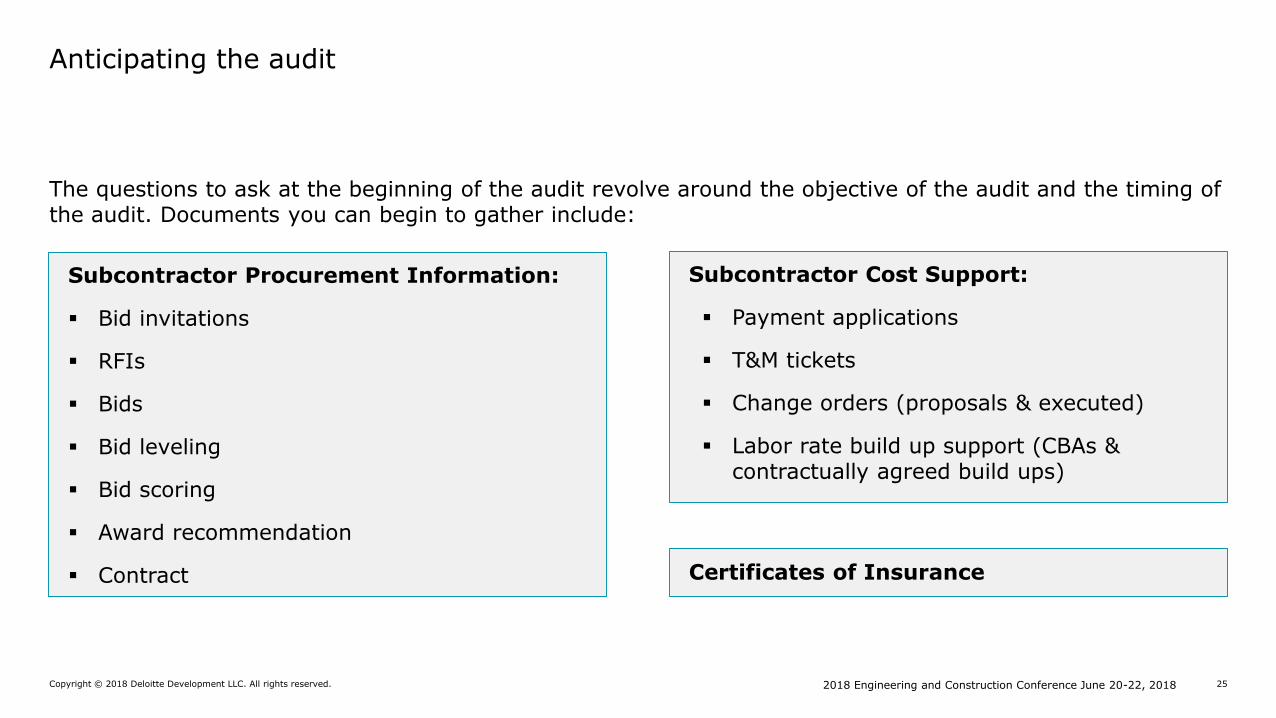

The questions to ask at the beginning of the audit revolve around the objective of the audit and the timing of the audit. Documents you can begin to gather include:

Anticipating the audit

Subcontractor Procurement Information:

▪ Bid invitations

▪ RFIs

▪ Bids

▪ Bid leveling

▪ Bid scoring

▪ Award recommendation

▪ Contract

Subcontractor Cost Support:

▪ Payment applications

▪ T&M tickets

▪ Change orders (proposals & executed)

▪ Labor rate build up support (CBAs & contractually agreed build ups)

Certificates of Insurance

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 26

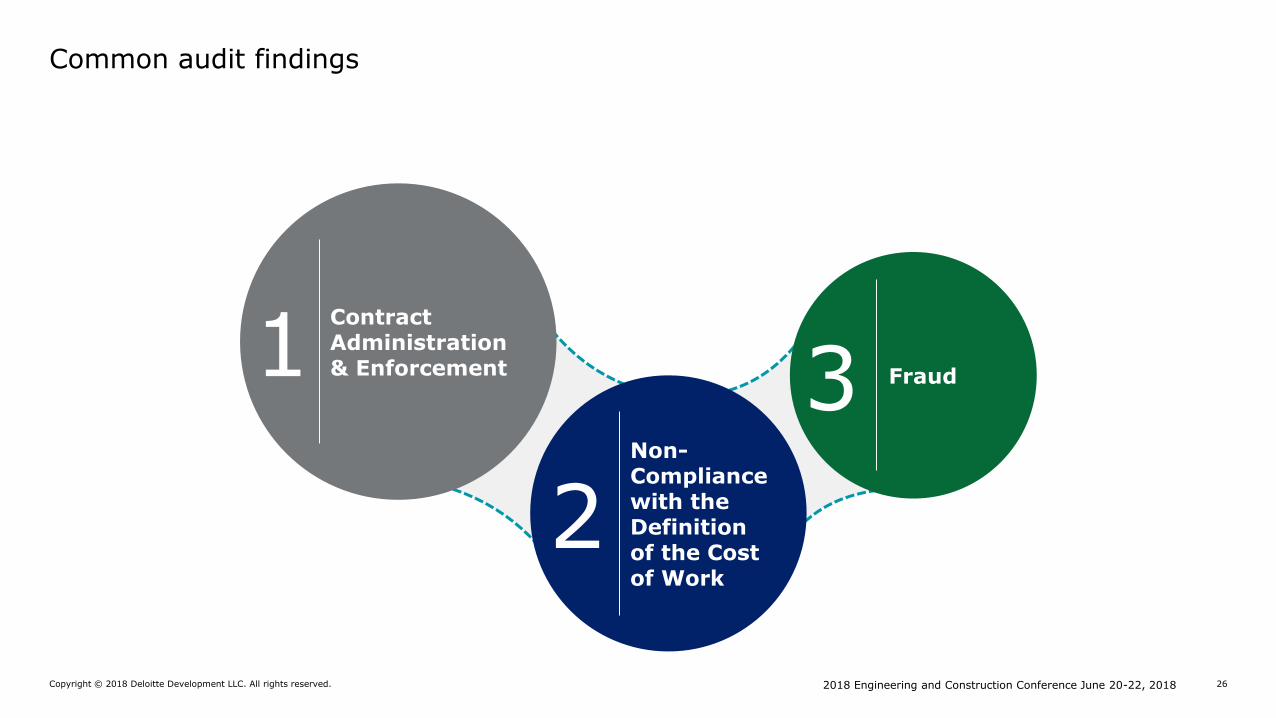

Common audit findings

Contract Administration & Enforcement1

Non-Compliance with the Definition of the Cost of Work

2

Fraud3

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 27

“At any given moment, there is a certain percentage of the population that’s up to no good.”

- J. Edgar Hoover

A Statistical Certainty

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 28

▪ Construction is consistently rated as the most corrupt industry worldwide

▪ 30% of mega-firms express little or no confidence in corporate controls over construction

▪ Fraud/waste/abuse accounts for at least 10% loss of project value globally

▪ Cost of corruption is more than just wasted money; can lead to shoddy workmanship, which in turn can damage the environment and even cost lives

Fraud and Construction

Source: Transparency International 2009 Global Corruption Report

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 29

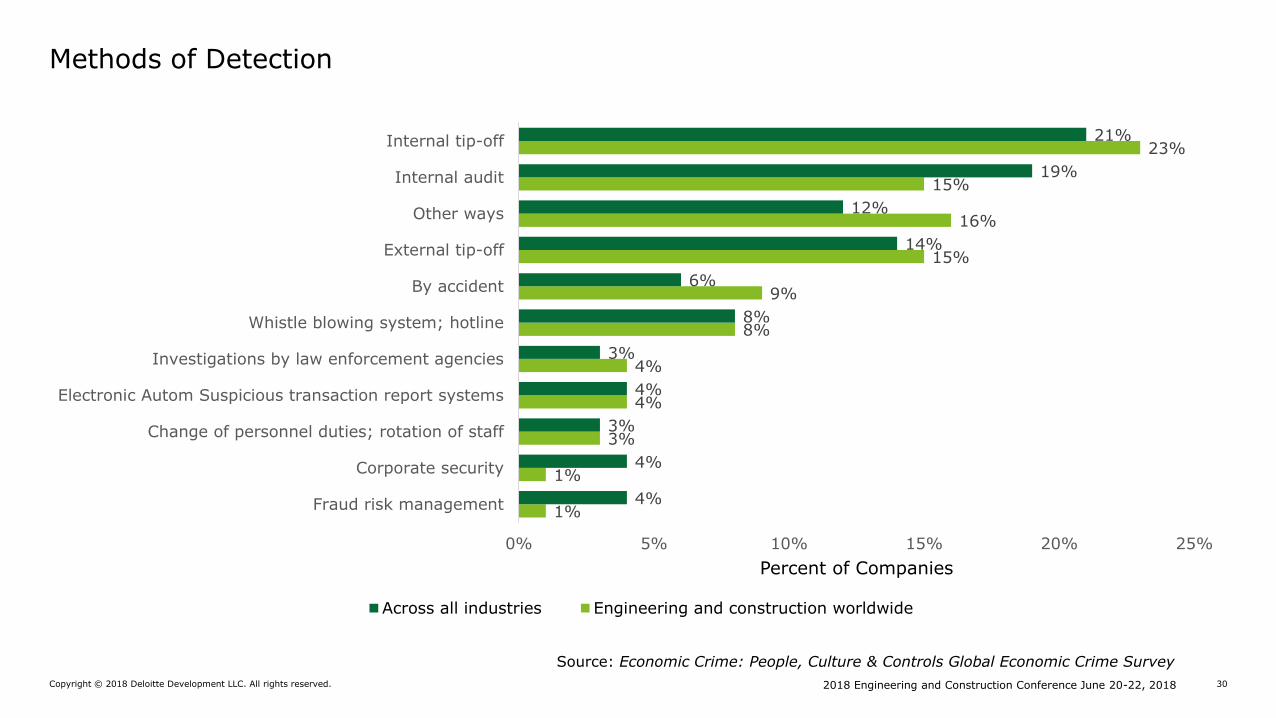

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 30

1%

1%

3%

4%

4%

8%

9%

15%

16%

15%

23%

4%

4%

3%

4%

3%

8%

6%

14%

12%

19%

21%

0% 5% 10% 15% 20% 25%

Fraud risk management

Corporate security

Change of personnel duties; rotation of staff

Electronic Autom Suspicious transaction report systems

Investigations by law enforcement agencies

Whistle blowing system; hotline

By accident

External tip-off

Other ways

Internal audit

Internal tip-off

Percent of Companies

Across all industries Engineering and construction worldwide

Methods of Detection

Source: Economic Crime: People, Culture & Controls Global Economic Crime Survey

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 31

The most effective methods of detection:

▪ Internal/External Tip-off

▪ “The fact that tips continue to be the most effective means of detecting fraud suggests that organizations could improve their detection efforts by establishing formal structures to receive reports about possible fraudulent conduct.” (2008 ACFE Report to the Nation on Occupational Fraud and Abuse)

▪ Whistleblowing, primarily through the False Claims Act, has resulted in over $2 billion in recoveries and over $177 million in awards (2007 Department of Justice Civil Fraud Division)

▪ Internal Audit

▪ Recurring audits and testing project transactions

▪ Internal Controls

▪ Periodic reviews and testing of the efficiency and adequacy of internal controls

Methods of Detection

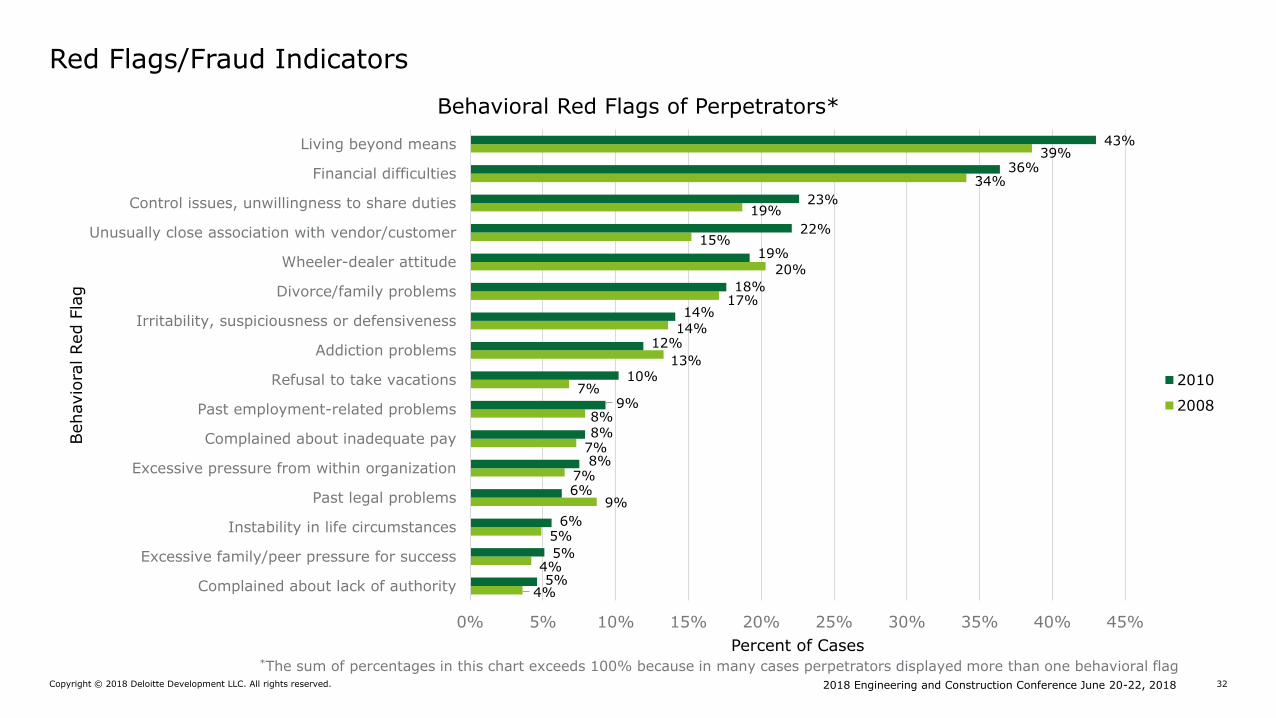

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 32

4%

4%

5%

9%

7%

7%

8%

7%

13%

14%

17%

20%

15%

19%

34%

39%

5%

5%

6%

6%

8%

8%

9%

10%

12%

14%

18%

19%

22%

23%

36%

43%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

Complained about lack of authority

Excessive family/peer pressure for success

Instability in life circumstances

Past legal problems

Excessive pressure from within organization

Complained about inadequate pay

Past employment-related problems

Refusal to take vacations

Addiction problems

Irritability, suspiciousness or defensiveness

Divorce/family problems

Wheeler-dealer attitude

Unusually close association with vendor/customer

Control issues, unwillingness to share duties

Financial difficulties

Living beyond means

Percent of Cases

Behavio

ral Red F

lag

Behavioral Red Flags of Perpetrators*

2010

2008

Red Flags/Fraud Indicators

*The sum of percentages in this chart exceeds 100% because in many cases perpetrators displayed more than one behavioral flag

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 33

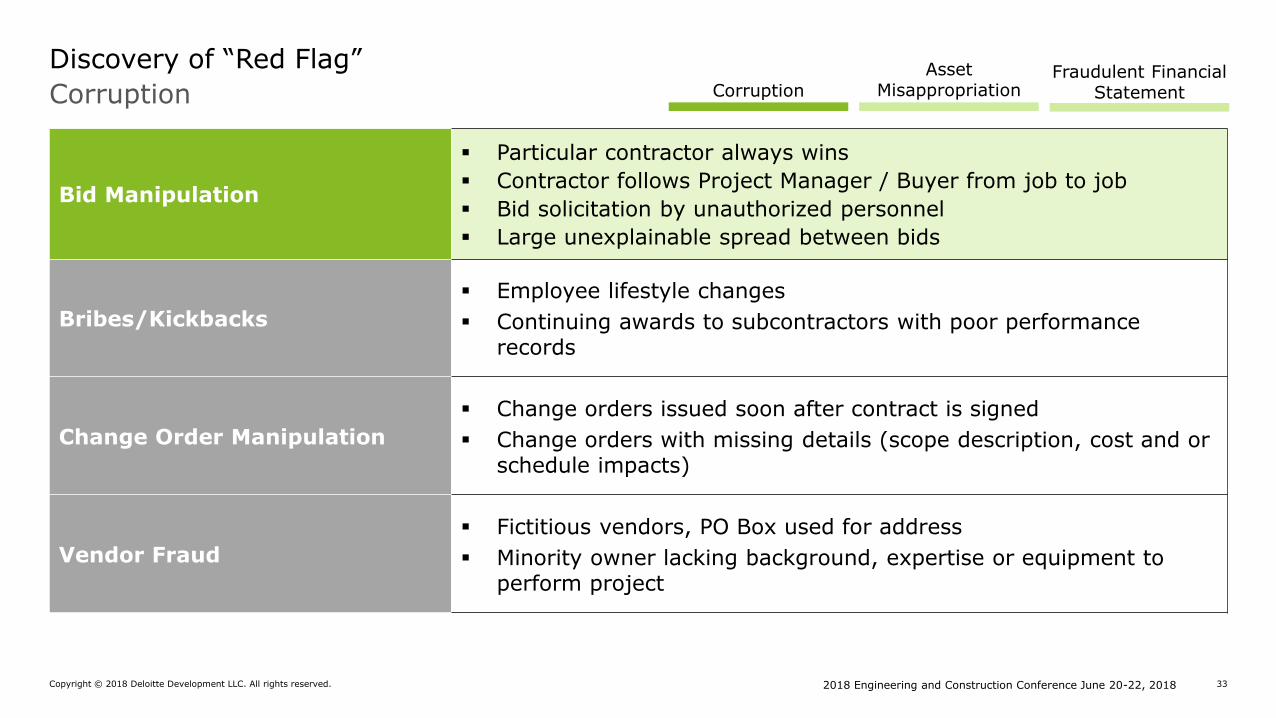

Corruption

Discovery of “Red Flag”

Bid Manipulation

▪ Particular contractor always wins

▪ Contractor follows Project Manager / Buyer from job to job

▪ Bid solicitation by unauthorized personnel

▪ Large unexplainable spread between bids

Bribes/Kickbacks

▪ Employee lifestyle changes

▪ Continuing awards to subcontractors with poor performance records

Change Order Manipulation

▪ Change orders issued soon after contract is signed

▪ Change orders with missing details (scope description, cost and or schedule impacts)

Vendor Fraud

▪ Fictitious vendors, PO Box used for address

▪ Minority owner lacking background, expertise or equipment to perform project

Corruption

Asset Misappropriation

Fraudulent Financial Statement

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 34

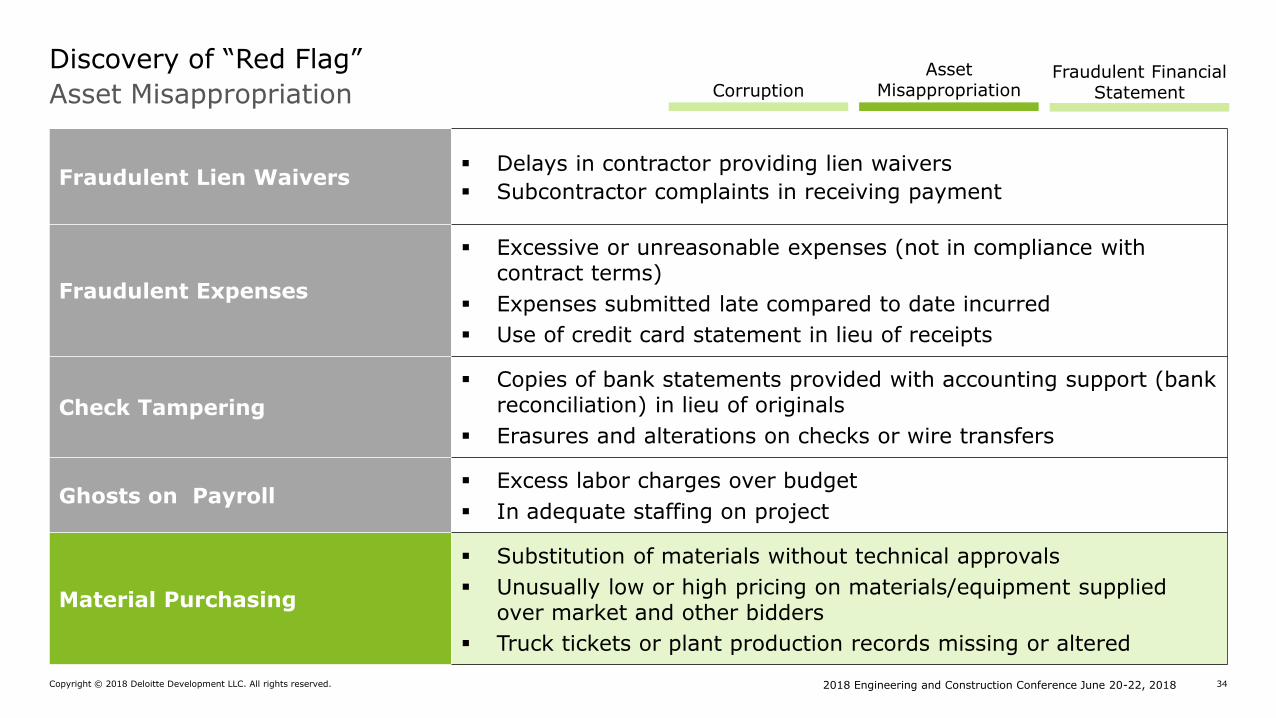

Asset Misappropriation

Discovery of “Red Flag”

Fraudulent Lien Waivers▪ Delays in contractor providing lien waivers

▪ Subcontractor complaints in receiving payment

Fraudulent Expenses

▪ Excessive or unreasonable expenses (not in compliance with contract terms)

▪ Expenses submitted late compared to date incurred

▪ Use of credit card statement in lieu of receipts

Check Tampering

▪ Copies of bank statements provided with accounting support (bank reconciliation) in lieu of originals

▪ Erasures and alterations on checks or wire transfers

Ghosts on Payroll▪ Excess labor charges over budget

▪ In adequate staffing on project

Material Purchasing

▪ Substitution of materials without technical approvals

▪ Unusually low or high pricing on materials/equipment supplied over market and other bidders

▪ Truck tickets or plant production records missing or altered

Corruption

Asset Misappropriation

Fraudulent Financial Statement

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 35

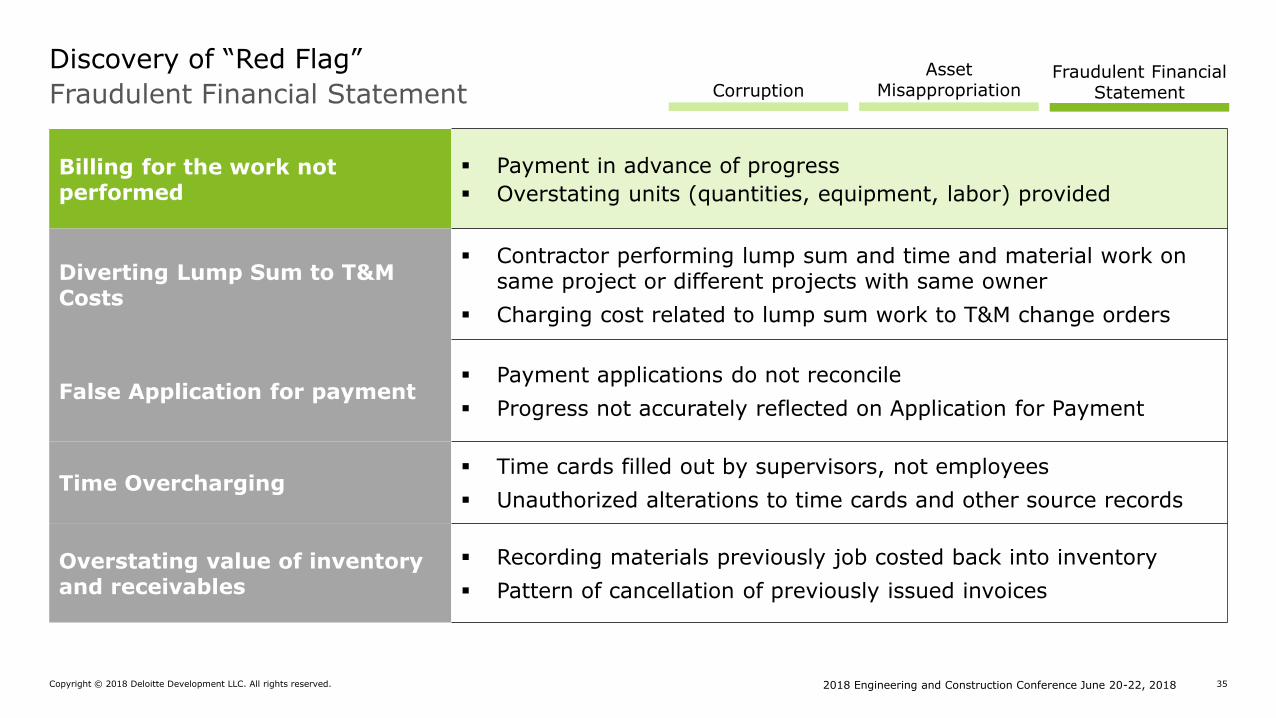

Fraudulent Financial Statement

Discovery of “Red Flag”

Billing for the work not performed

▪ Payment in advance of progress

▪ Overstating units (quantities, equipment, labor) provided

Diverting Lump Sum to T&M Costs

▪ Contractor performing lump sum and time and material work on same project or different projects with same owner

▪ Charging cost related to lump sum work to T&M change orders

False Application for payment▪ Payment applications do not reconcile

▪ Progress not accurately reflected on Application for Payment

Time Overcharging▪ Time cards filled out by supervisors, not employees

▪ Unauthorized alterations to time cards and other source records

Overstating value of inventory and receivables

▪ Recording materials previously job costed back into inventory

▪ Pattern of cancellation of previously issued invoices

Corruption

Asset Misappropriation

Fraudulent Financial Statement

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 36

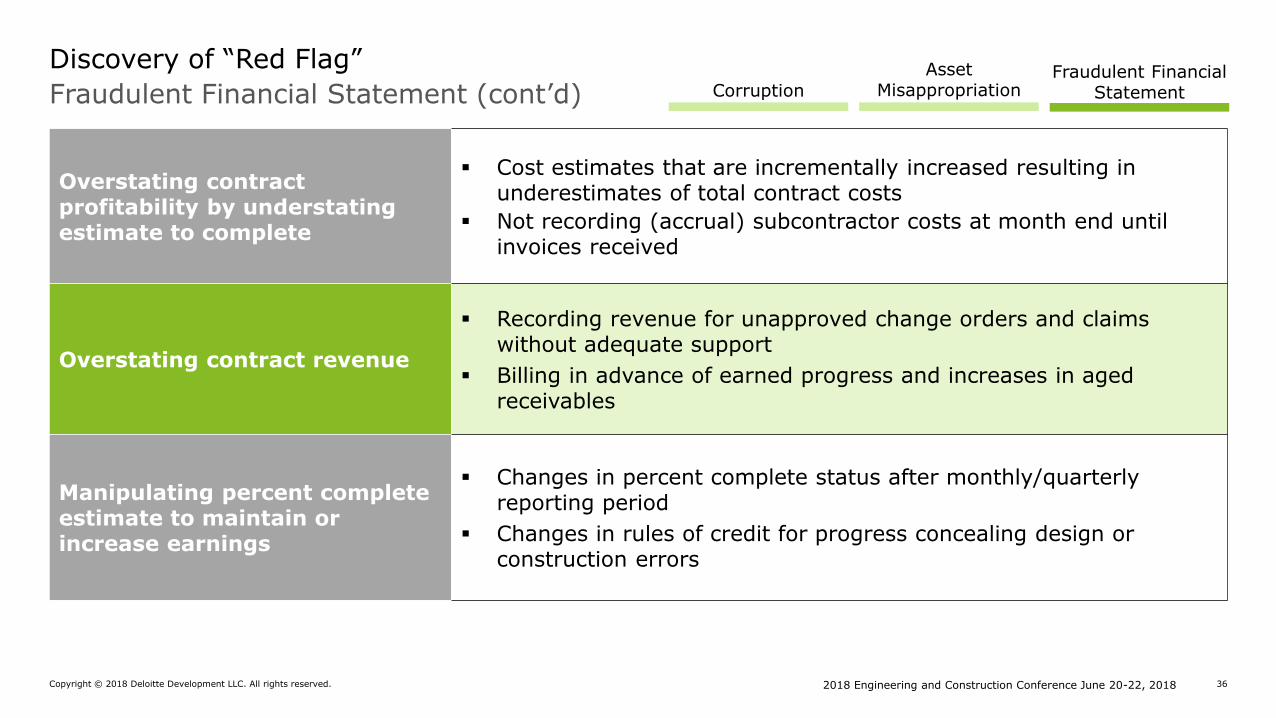

Fraudulent Financial Statement (cont’d)

Discovery of “Red Flag”

Overstating contract profitability by understating estimate to complete

▪ Cost estimates that are incrementally increased resulting in underestimates of total contract costs

▪ Not recording (accrual) subcontractor costs at month end until invoices received

Overstating contract revenue

▪ Recording revenue for unapproved change orders and claims without adequate support

▪ Billing in advance of earned progress and increases in aged receivables

Manipulating percent complete estimate to maintain or increase earnings

▪ Changes in percent complete status after monthly/quarterly reporting period

▪ Changes in rules of credit for progress concealing design or construction errors

Corruption

Asset Misappropriation

Fraudulent Financial Statement

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 37

Fraudulent Financial Statement (cont’d)

Discovery of “Red Flag”

Understanding accounts payable

▪ Unexpected increase or decrease in liabilities between reporting periods

▪ Under-accrual for material in transit

Crediting and rebilling receivables to affect aged balances

▪ Invoice numbers that are out of sequence based on invoice date

▪ Unusual debit transactions to revenue account

Overstating/understating Property, Plant & Equipment (PPE)

▪ Job charging PPE in lieu of capitalization and depreciation

▪ Resale of fully depreciated assets to related entity

Corruption

Asset Misappropriation

Fraudulent Financial Statement

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 38

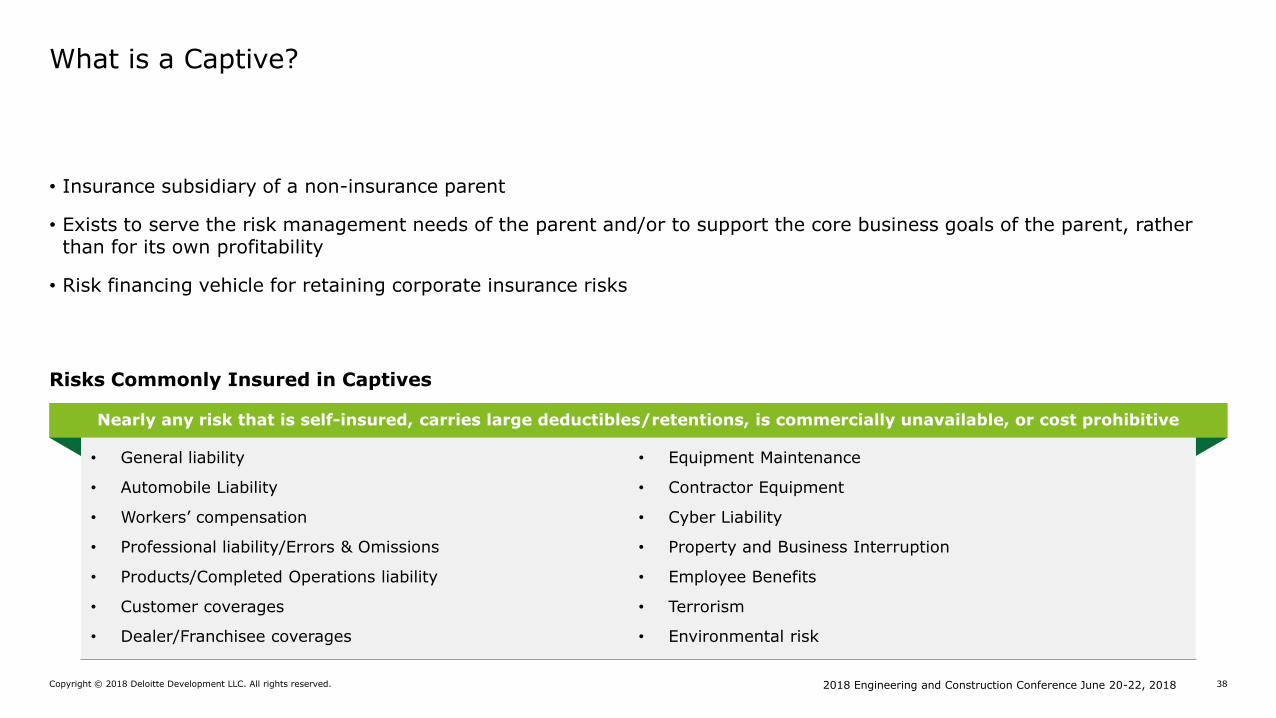

• Insurance subsidiary of a non-insurance parent

• Exists to serve the risk management needs of the parent and/or to support the core business goals of the parent, rather than for its own profitability

• Risk financing vehicle for retaining corporate insurance risks

What is a Captive?

Risks Commonly Insured in Captives

• General liability

• Automobile Liability

• Workers’ compensation

• Professional liability/Errors & Omissions

• Products/Completed Operations liability

• Customer coverages

• Dealer/Franchisee coverages

• Equipment Maintenance

• Contractor Equipment

• Cyber Liability

• Property and Business Interruption

• Employee Benefits

• Terrorism

• Environmental risk

Nearly any risk that is self-insured, carries large deductibles/retentions, is commercially unavailable, or cost prohibitive

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 39

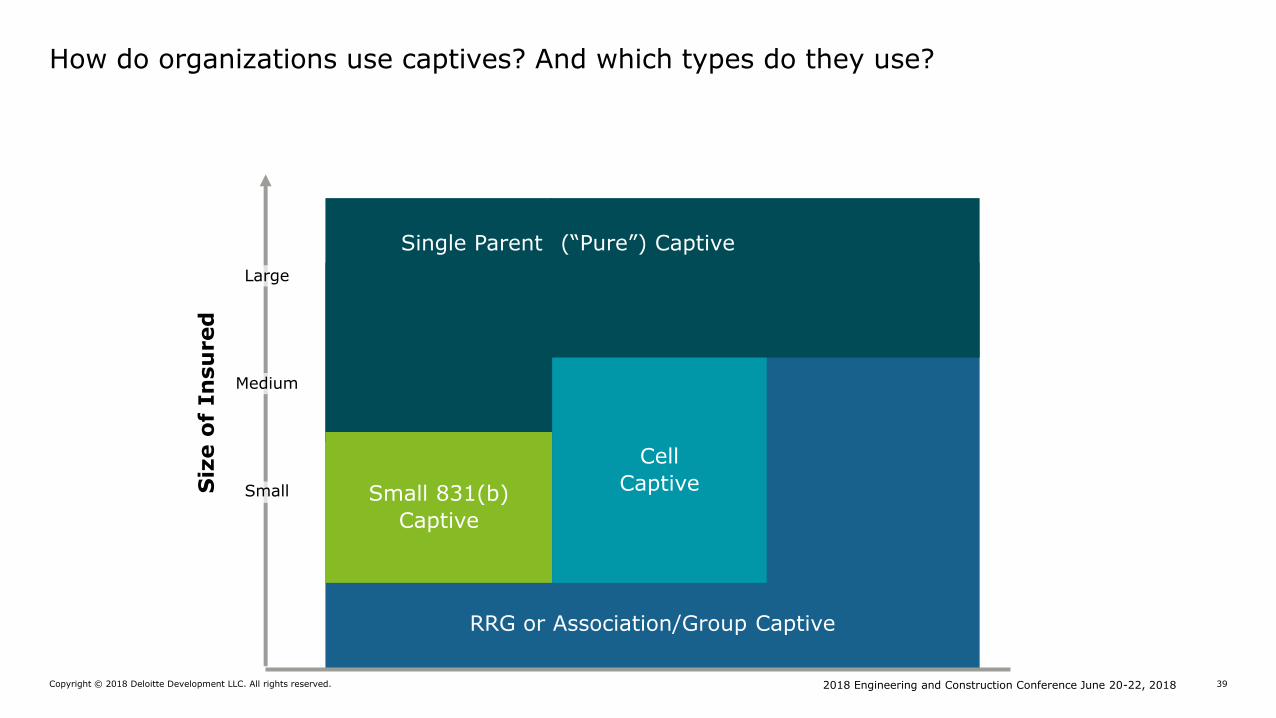

How do organizations use captives? And which types do they use?

RRG or Association/Group Captive

Single Parent

Small 831(b)

Captive

Large

Medium

Small

(“Pure”) Captive

Cell

CaptiveSiz

e o

f In

su

red

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 40

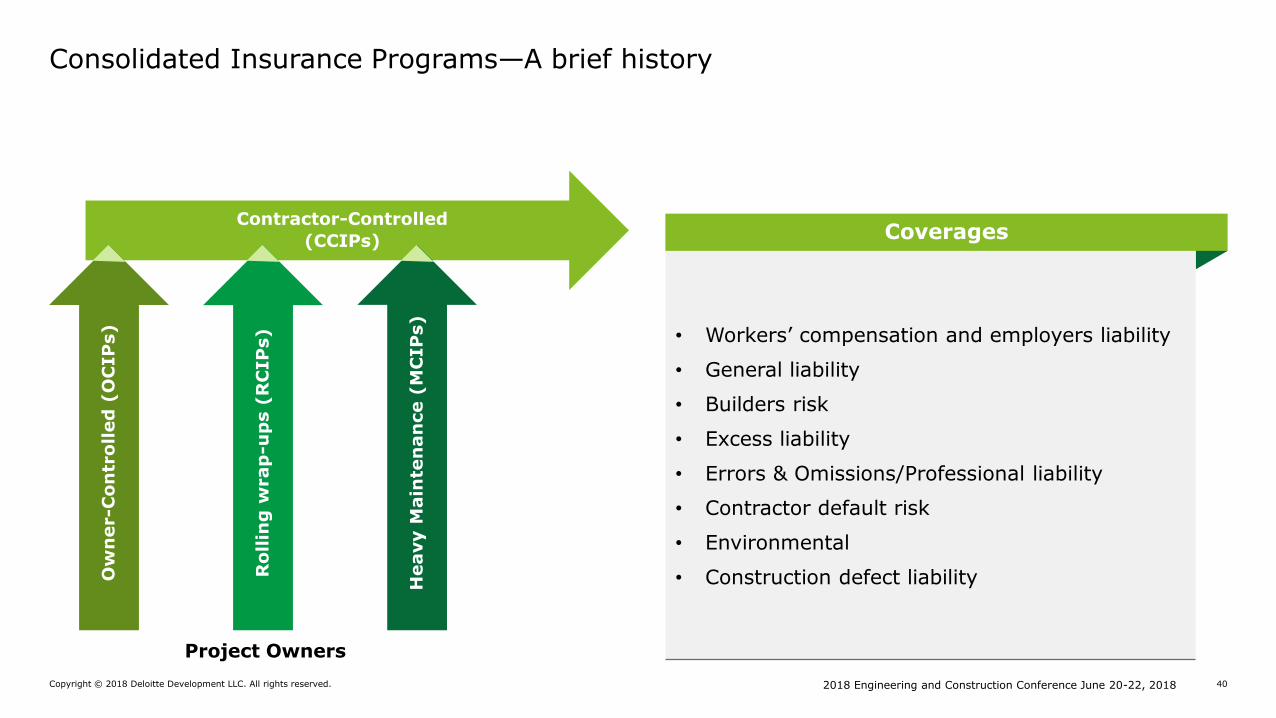

Consolidated Insurance Programs—A brief history

• Workers’ compensation and employers liability

• General liability

• Builders risk

• Excess liability

• Errors & Omissions/Professional liability

• Contractor default risk

• Environmental

• Construction defect liability

CoveragesContractor-Controlled

(CCIPs)

Project Owners

Heavy M

ain

ten

an

ce (

MC

IP

s)

Ow

ner-C

on

tro

lled

(O

CIP

s)

Ro

llin

g w

rap

-up

s (

RC

IP

s)

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 41

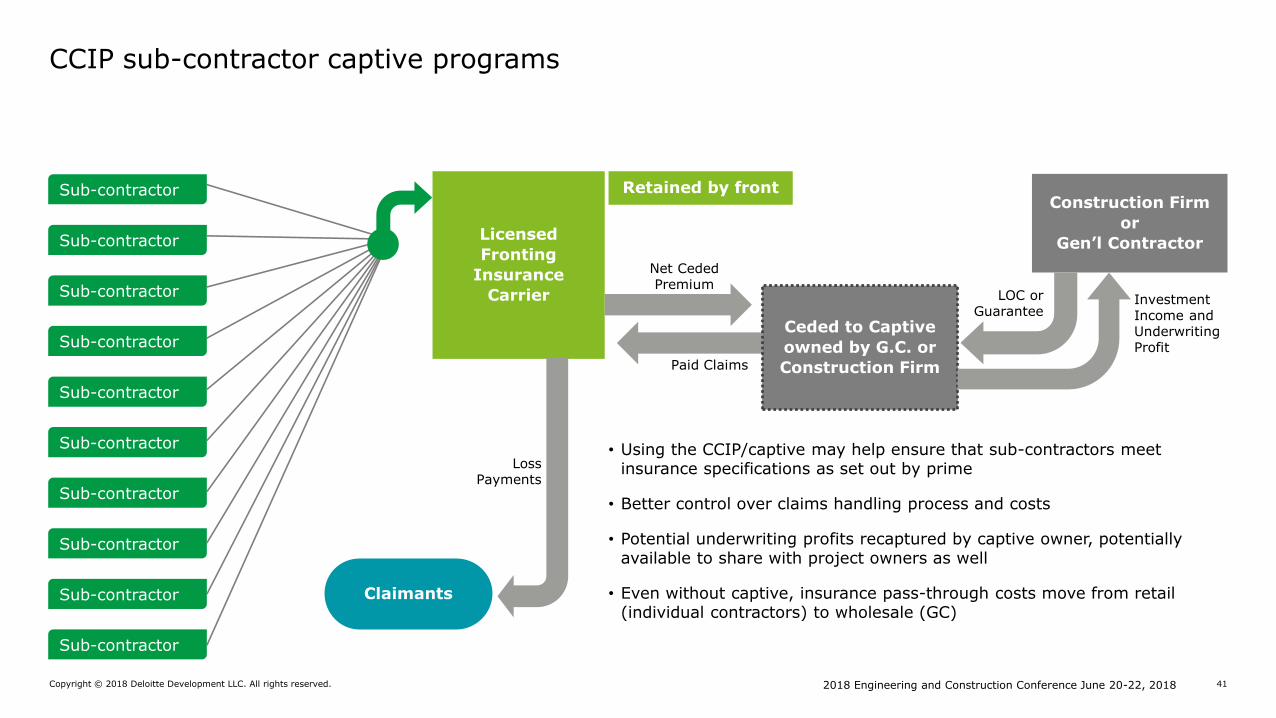

CCIP sub-contractor captive programs

Sub-contractor

Sub-contractor

Sub-contractor

Sub-contractor

Sub-contractor

Sub-contractor

Sub-contractor

Sub-contractor

Sub-contractor

Sub-contractor

• Using the CCIP/captive may help ensure that sub-contractors meet insurance specifications as set out by prime

• Better control over claims handling process and costs

• Potential underwriting profits recaptured by captive owner, potentially available to share with project owners as well

• Even without captive, insurance pass-through costs move from retail (individual contractors) to wholesale (GC)

Paid Claims

LOC orGuarantee

InvestmentIncome andUnderwritingProfit

LossPayments

Licensed

Fronting

Insurance

Carrier

Retained by front

Net CededPremium

Ceded to Captive

owned by G.C. or

Construction Firm

Construction Firm

or

Gen’l Contractor

Claimants

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 42

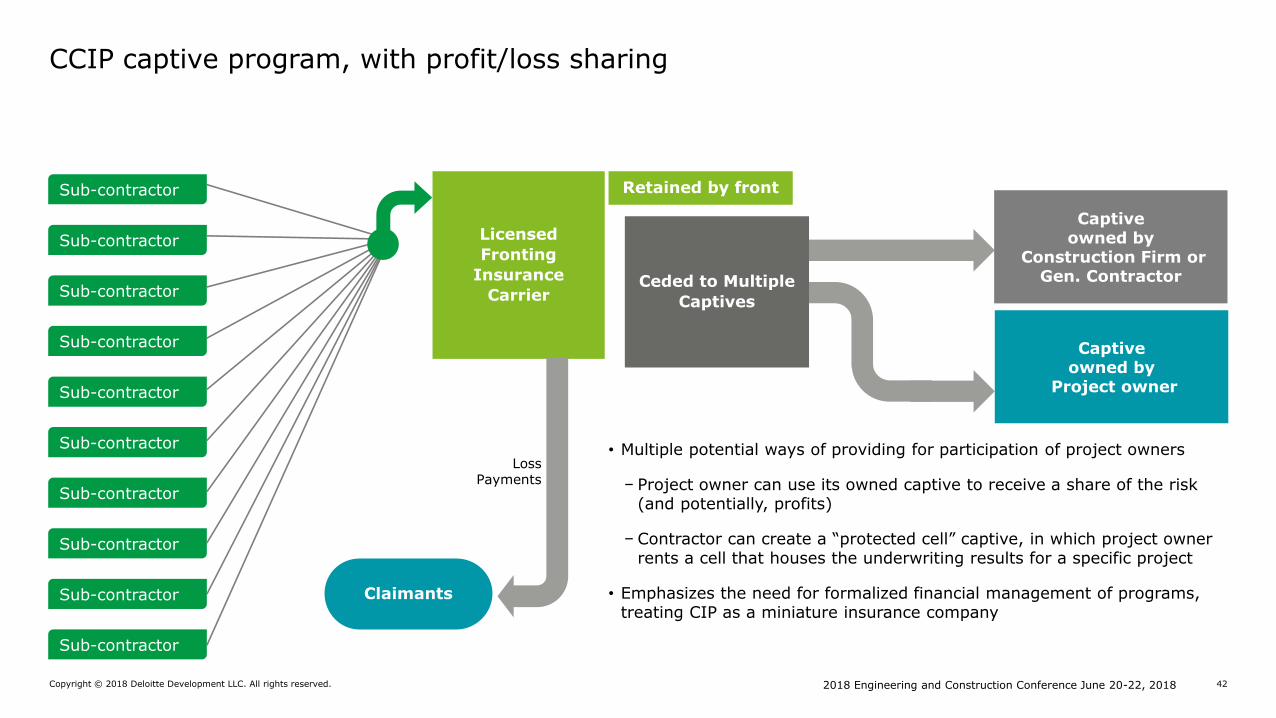

CCIP captive program, with profit/loss sharing

Sub-contractor

Sub-contractor

Sub-contractor

Sub-contractor

Sub-contractor

Sub-contractor

Sub-contractor

Sub-contractor

Sub-contractor

Sub-contractor

Licensed

Fronting

Insurance

Carrier

Retained by front

Captive owned by

Construction Firm orGen. Contractor

Captive owned by

Project owner

• Multiple potential ways of providing for participation of project owners

− Project owner can use its owned captive to receive a share of the risk (and potentially, profits)

− Contractor can create a “protected cell” captive, in which project owner rents a cell that houses the underwriting results for a specific project

• Emphasizes the need for formalized financial management of programs, treating CIP as a miniature insurance company

Ceded to Multiple

Captives

LossPayments

Claimants

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 43

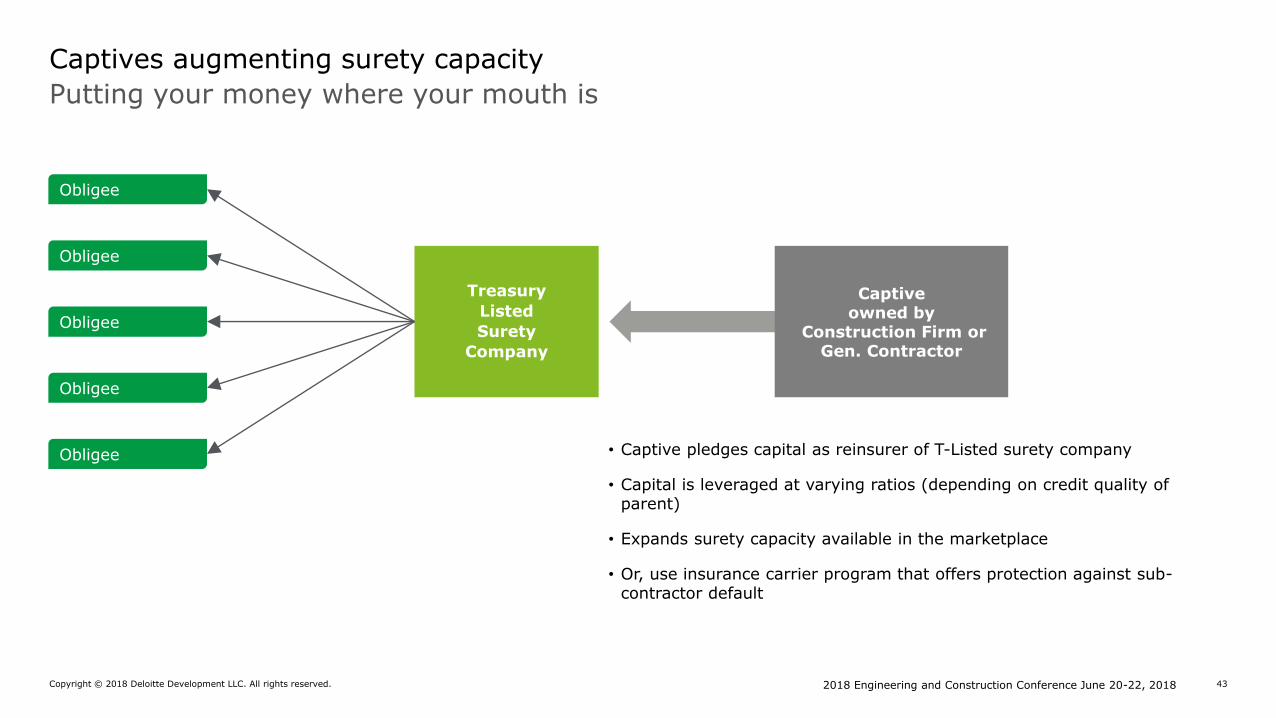

Putting your money where your mouth is

Captives augmenting surety capacity

Captive owned by

Construction Firm orGen. Contractor

Treasury

Listed

Surety

Company

• Captive pledges capital as reinsurer of T-Listed surety company

• Capital is leveraged at varying ratios (depending on credit quality of parent)

• Expands surety capacity available in the marketplace

• Or, use insurance carrier program that offers protection against sub-contractor default

Obligee

Obligee

Obligee

Obligee

Obligee

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 44

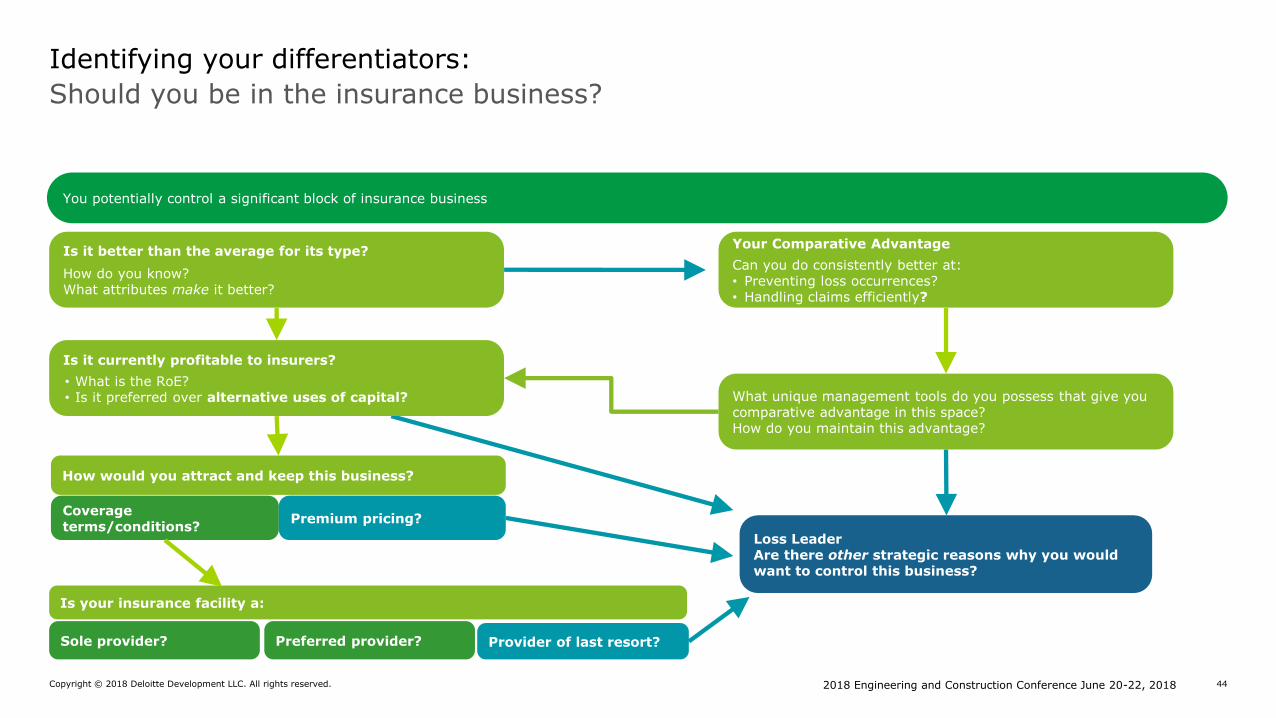

Should you be in the insurance business?

Identifying your differentiators:

You potentially control a significant block of insurance business

Is it better than the average for its type?

How do you know?What attributes make it better?

Sole provider? Preferred provider?

Coverage terms/conditions?

Premium pricing?

Provider of last resort?

Is your insurance facility a:

How would you attract and keep this business?

Is it currently profitable to insurers?

• What is the RoE?• Is it preferred over alternative uses of capital?

Your Comparative Advantage

Can you do consistently better at: • Preventing loss occurrences?• Handling claims efficiently?

What unique management tools do you possess that give you comparative advantage in this space?How do you maintain this advantage?

Loss LeaderAre there other strategic reasons why you would want to control this business?

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 45

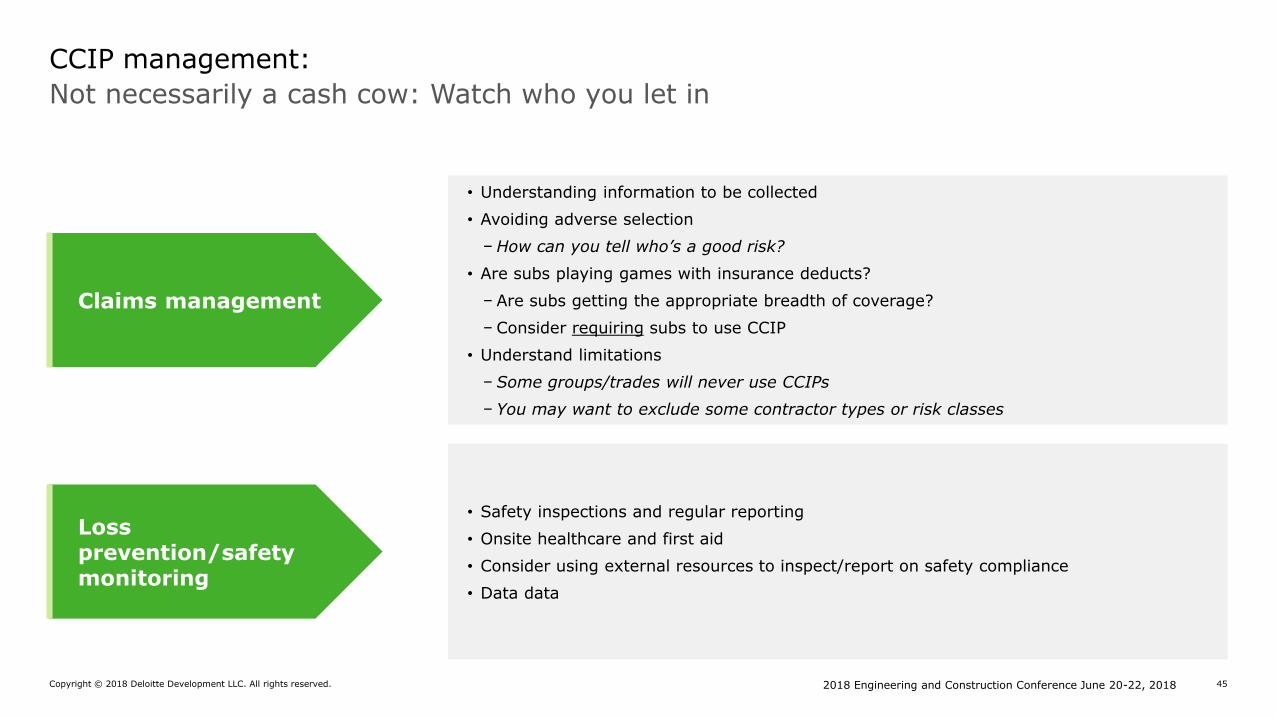

Not necessarily a cash cow: Watch who you let in

CCIP management:

• Understanding information to be collected

• Avoiding adverse selection

− How can you tell who’s a good risk?

• Are subs playing games with insurance deducts?

− Are subs getting the appropriate breadth of coverage?

− Consider requiring subs to use CCIP

• Understand limitations

− Some groups/trades will never use CCIPs

− You may want to exclude some contractor types or risk classes

Claims management

• Safety inspections and regular reporting

• Onsite healthcare and first aid

• Consider using external resources to inspect/report on safety compliance

• Data data

Loss prevention/safety monitoring

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 46

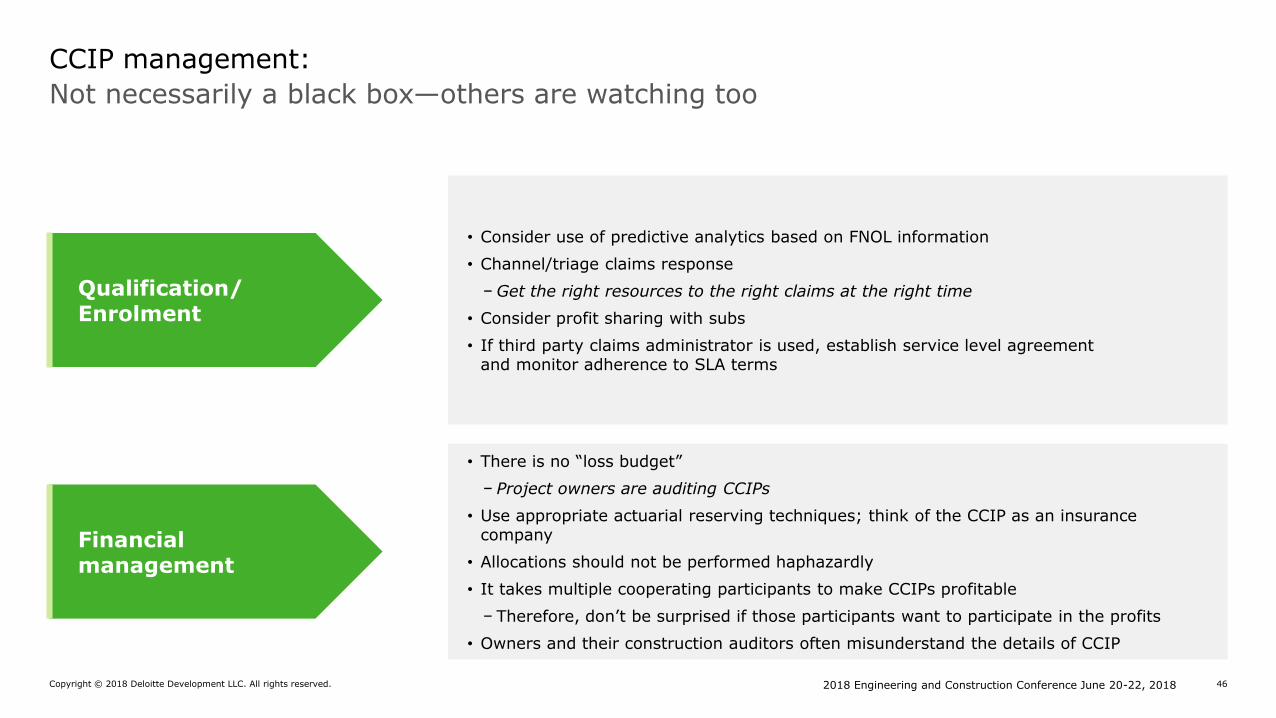

Not necessarily a black box—others are watching too

CCIP management:

• Consider use of predictive analytics based on FNOL information

• Channel/triage claims response

− Get the right resources to the right claims at the right time

• Consider profit sharing with subs

• If third party claims administrator is used, establish service level agreement and monitor adherence to SLA terms

Qualification/Enrolment

• There is no “loss budget”

− Project owners are auditing CCIPs

• Use appropriate actuarial reserving techniques; think of the CCIP as an insurance company

• Allocations should not be performed haphazardly

• It takes multiple cooperating participants to make CCIPs profitable

− Therefore, don’t be surprised if those participants want to participate in the profits

• Owners and their construction auditors often misunderstand the details of CCIP

Financial management

Culture of RiskChris Smith, Vice PresidentTurner Surety and Insurance Brokerage, Inc.

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 48

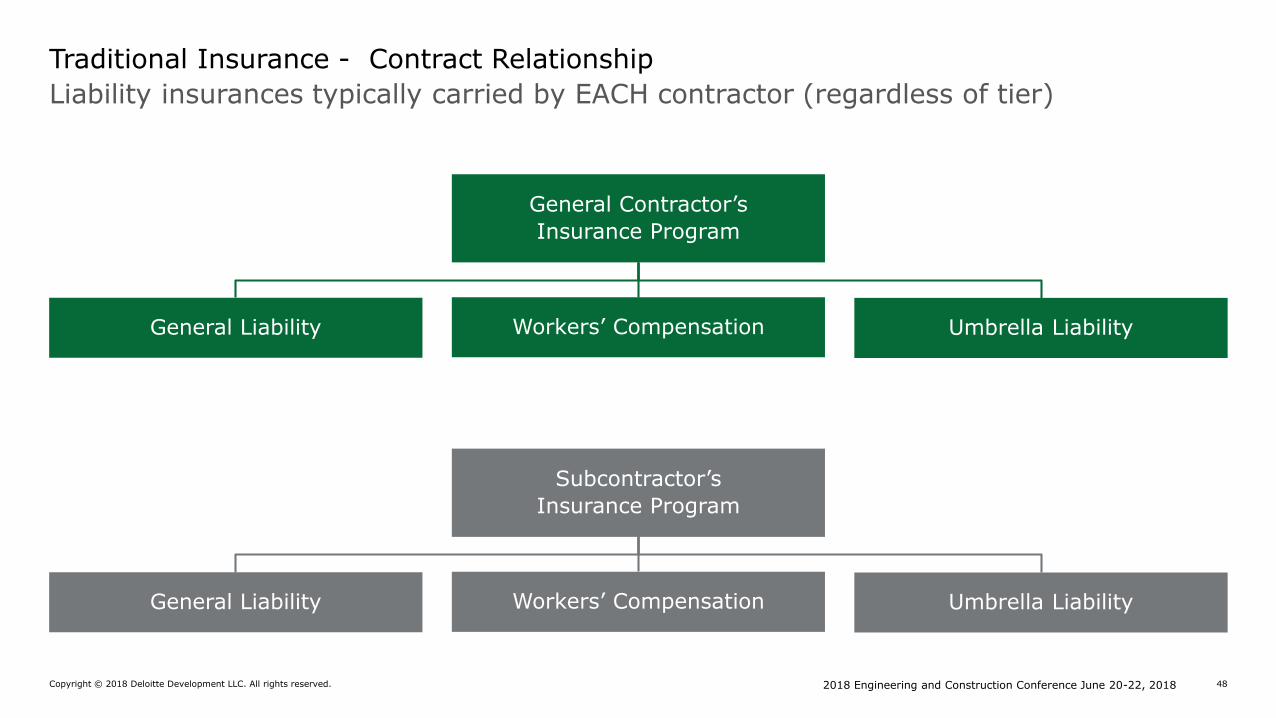

Liability insurances typically carried by EACH contractor (regardless of tier)

Traditional Insurance - Contract Relationship

General Contractor’s

Insurance Program

Workers’ CompensationGeneral Liability Umbrella Liability

Subcontractor’s

Insurance Program

Workers’ CompensationGeneral Liability Umbrella Liability

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 49

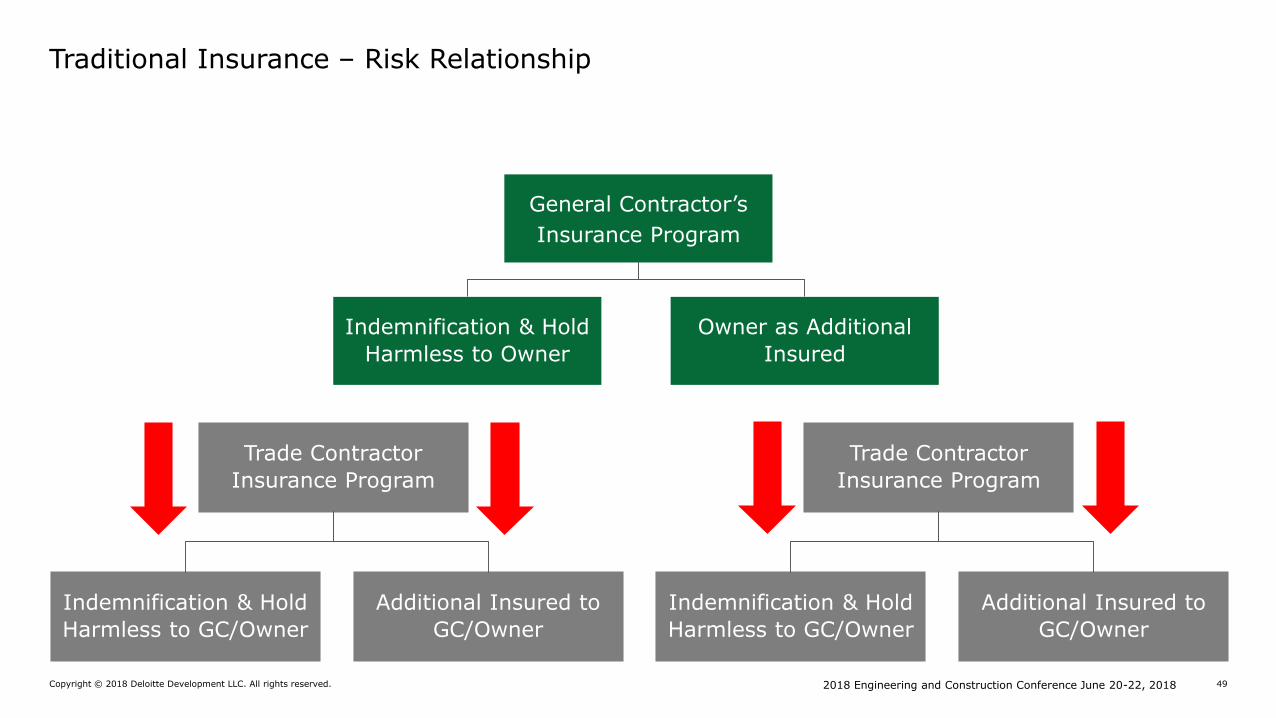

Traditional Insurance – Risk Relationship

Owner as Additional

Insured

Indemnification & Hold

Harmless to Owner

General Contractor’s

Insurance Program

Trade Contractor

Insurance Program

Trade Contractor

Insurance Program

Indemnification & Hold

Harmless to GC/Owner

Additional Insured to

GC/Owner

Additional Insured to

GC/Owner

Indemnification & Hold

Harmless to GC/Owner

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 50

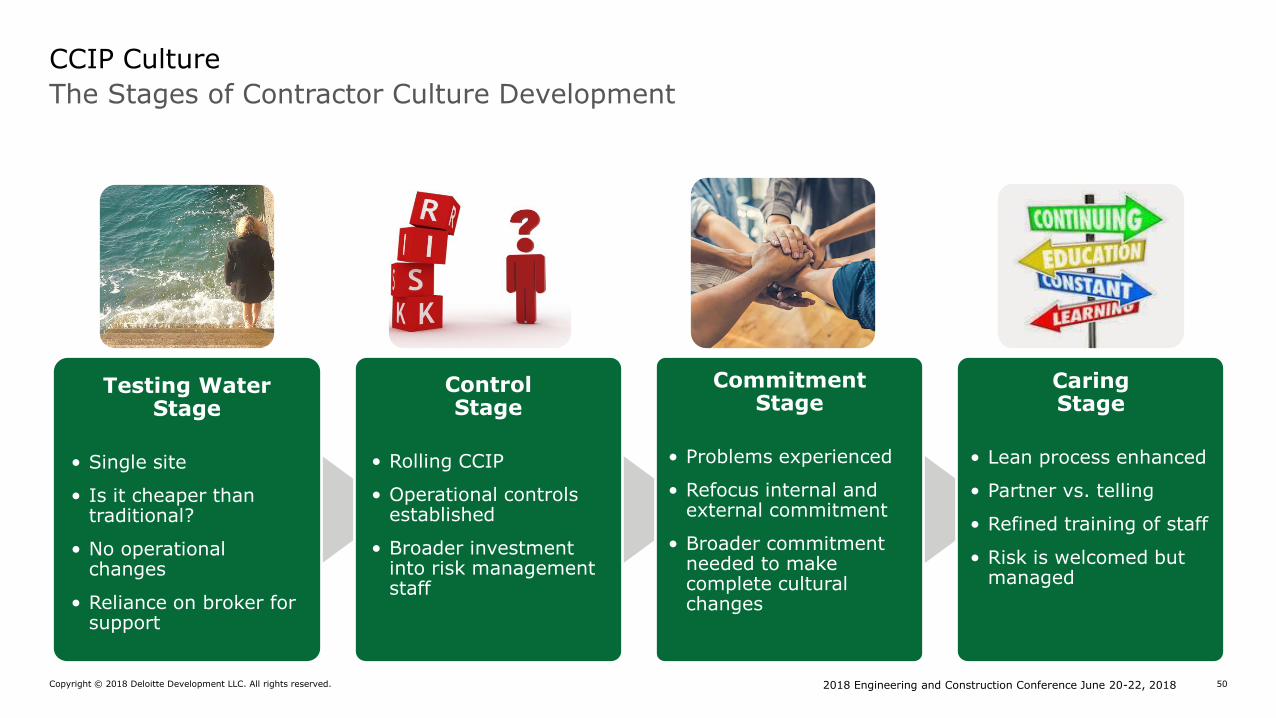

The Stages of Contractor Culture Development

CCIP Culture

Testing Water Stage

• Single site

• Is it cheaper than traditional?

• No operational changes

• Reliance on broker for support

ControlStage

• Rolling CCIP

• Operational controls established

• Broader investment into risk management staff

CommitmentStage

• Problems experienced

• Refocus internal and external commitment

• Broader commitment needed to make complete cultural changes

CaringStage

• Lean process enhanced

• Partner vs. telling

• Refined training of staff

• Risk is welcomed but managed

Game TimeMark Blumkin, Managing DirectorDeloitte Transactions and Business Analytics, LLP

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 52

If you would like the opportunity to play along, please:

1. Pull out your cell phone.

2. Text “MITIGATINGRISK” to 22333 to join the session.

3. Read the question on the screen.

4. Text the letter or long-form answer associated with your chosen answer to the phone number 22333.

It’s game time.

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 53

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 54

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 55

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 56

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 57

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 58

2018 Engineering and Construction Conference June 20-22, 2018Copyright © 2018 Deloitte Development LLC. All rights reserved. 59

Questions?

This presentation contains general information only and Deloitte is not, by means of this presentation, rendering accounting, business, financial, investment,

legal, tax, or other professional advice or services. This presentation is not a substitute for such professional advice or services, nor should it be used as a

basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should

consult a qualified professional advisor.

Deloitte shall not be responsible for any loss sustained by any person who relies on this presentation.

About Deloitte

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and

their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not

provide services to clients. In the United States, Deloitte refers to one or more of the US member firms of DTTL, their related entities that operate using the

“Deloitte” name in the United States and their respective affiliates. Certain services may not be available to attest clients under the rules and regulations of

public accounting. Please see www.deloitte.com/about to learn more about our global network of member firms.

Copyright © 2018 Deloitte Development LLC. All rights reserved.