why do firms voluntarily have interim financial statements ...iri/papers/gpliu.pdf · 2 why do...

TRANSCRIPT

1

Why Do Firms Voluntarily Have Interim Financial Statements Reviewed by Auditors?

J. Efrim. Boritz School of Accountancy University of Waterloo

Waterloo, On N2L 3G1

Guoping Liu School of Business Management

Ryerson University Toronto, On M5B 2K3

August 01, 2006

2

Why Do Firms Voluntarily Have Interim Financial Statements Reviewed by Auditors?

Abstract This study investigates firm characteristics that are associated with firms’ voluntary decisions to have their quarterly financial statements reviewed by their auditor, utilizing a sample of Canadian public companies. We find that interim financial statements are more likely to be reviewed for firms with high complexity than for firms with low complexity. We also find that firms with high growth opportunities are less likely to be reviewed than those with low growth opportunities, presumably because they may be associated with higher information and litigation risks. However, we document mixed evidence that the likelihood of having interim financial statements reviewed increases in firms’ audit assurance and insurance needs.

3

Why Do Firms Voluntarily Have Interim Financial Statements Reviewed by Auditors?

Introduction

Reporting on interim financial statements originated in the US, where public

accounting firms required an interim review engagement as a condition for undertaking

the year-end audit. Subsequently, the US stock exchanges mandated the engagement

(Krishnan and Zhang, 2004). The reporting problems at Enron and other such scandals

triggered a review of the US interim review standard, resulting in a more focused

engagement, including some audit-oriented procedures. Currently, US SEC registrants

must have timely reviews of their interim financial information except for SEC

registrants that qualify as “foreign private issuers” that are not subject to these mandatory

review requirements.

The Canadian Securities Administrators’ (CSA) optional auditor review regime

results in companies being able to elect whether to have a review engagement on a

quarter by quarter basis. Canadian practices in this area differ from US standards where

US SEC registrants must have timely reviews performed. However, despite the absence

of a requirements to have a review performed, a number of Canadian public companies

have their interim financial statements reviewed.1 Public companies must disclose when

1 A review of SEDAR filings for 400 public companies (100 in each of four categories, as follows) found that 14% of TSX-SEC registrants, 31% of TSX-non-SEC companies, 66% of TSXV-SEC registrants and

4

there has been no review performed and they typically do this by a one line disclosure on

the cover of the financial statements that the financial statements were not reviewed by

the company’s auditor.2

The decision to have a review engagement is a joint decision of the client and

auditor (Krishnan and Zhang 2004). That is, the client may want a review done to reduce

information risk for potential investors but the auditor could recommend that the client not

include the review during a quarter, using the threat of higher fees to discourage the client

from asking for it. Alternatively, the client may not wish to have a review done in order

to avoid incurring the cost or to avoid questions about discretionary accruals or other

estimates made during the quarter but the auditor may use the threat of withdrawing from

the annual financial statement audit engagement to require the client to have a quarterly

review performed. Thus, a review would be performed when the benefits to the auditor and

to the client exceed the costs to both parties.

We investigate the reasons that companies and auditors jointly choose to have

quarterly reviews performed. Our paper is the first to gather data on voluntary quarterly

reviews, as contrasted with voluntary public reports on mandatory reviews as investigated

by Krishnan and Zhang (2004) and studies of review timeliness by Ettredge et al. (1994,

2000a, b).

68% of TSXV-non-SEC companies did not have reviews of their interim financial statements for Q1 of 2005. 2 This disclosure may not adequately distinguish entities that have had a review from those that have not. Because even reviewed financial statements carry the “unaudited” disclaimer, readers may not realize that an additional one-line disclosure, saying that the statements “were not reviewed by the auditor,” implies additional risk.

5

Interim Reporting Practices

While practices vary throughout the world, there is a general trend toward more

frequent disclosure of financial information and continuing disclosure of price-sensitive

information. In Japan, quarterly financial statements are being phased in over a three-year

period (2004-2007). In Europe, although supported by a vast majority of European

investment professionals,3 the introduction of mandatory US style quarterly reporting for

all 7,000 listed companies has been delayed in certain jurisdictions such as the UK, which

gives more weight to continuing disclosure requirements of price-sensitive information.

Instead, listed companies are able to issue general trading statements every quarter and

financial statements twice a year.4,5,6

In Canada, quarterly financial statements must be filed with securities regulators

within 45 days after the end of the quarter (60 days for venture exchange companies).

3 http://www.cfainstitute.org/pressroom/03releases/03quarterly_reporting.html, accessed September 8, 2005. 4 The European Commission’s proposal to have the EU’s 7,000 public companies adopt a quarterly reporting approach similar to that of the US met opposition from several countries such as the UK, the Netherlands and Denmark. Although the form of reporting adopted is different (i.e., companies may file quarterly “trading statements” with a general description of their financial position rather than full-blown financial statements), there is a clear move toward more frequent periodic reporting in addition to the requirements for continuing disclosure of price-sensitive information. 5 The UK Listing Authority requires, as part of the Listing Rules (Section 9.9), companies to prepare a half-yearly report. (www.fsa.gov.uk). Quarterly financial statements are not currently required. The half-yearly report does not require an OFR. All it requires is an explanatory statement including: (a) any significant information enabling investors to make an informed assessment of the trend of the group's activities and profit or loss; (b) information of any special factor that has influenced the group's activities and the profit or loss during the period in question; (c) enough information to enable a comparison to be made with the corresponding period of the preceding financial year; and (d) to the extent possible, a reference to the group's prospects in the current financial year. 6 The EU’s Transparency Directive, which has to be implemented by Member States from 2007, will require more comprehensive half-yearly reports, including an interim “management report” (more like an annual directors’ report than an OFR). This will also require “interim management statements,” providing: an explanation of material events and transactions that have taken place during the relevant period and their impact on the financial position of the issuer and its controlled undertakings; and a general description of the financial position and performance of the issuer and its controlled undertakings during the relevant period.

6

The typical process for interim reporting involves closing off, preparation of

subsidiary/divisional information, preparation of checklists and, where applicable, sub-

certification at divisional/subsidiary level, consolidation, review with disclosure

committee, preparation of package for audit committee/board, review with the audit

committee and, generally, the board. Many companies use checklists to document this

process and assist the business unit/subsidiary. Such checklists can run from 5-18 pages.

Once the quarterly financial package is available, auditors spend three to five days

reviewing it (if engaged to do so). Then, the financial package is brought to the audit

committee for its review and to the board for its approval. Some companies have the

audit committee and board meetings on the same day, while others have the board

meeting the next day so that any issues raised by the audit committee can be addressed

before the board meeting.

The amount of time taken to complete the quarterly reporting process varies

dramatically, even among large sophisticated organizations. Some companies complete

the process in as little as 15 days, while others use the whole 45 days allowed by the

securities regulators (60 days for venture companies).

Under current regulatory requirements (MI 52-109), a company’s CEO and CFO

each must certify that the filings do not contain any untrue statement of a material fact or

omit to state a material fact and that the financial statements, together with the MD&A,

present fairly the issuer’s financial condition, results of operations and cash flows. Under

7

MI 52-110, the audit committee7 must review the interim financial statements, MD&A

and earnings press release before the issuer publicly discloses this information.

Assurance Practices

Canadian securities regulators do not require auditors to conduct a review

engagement on interim financial statements. If a review is not performed, however, they

do require that this be disclosed in a notice accompanying the financial statements.8 Our

review of a sample of public company filings on SEDAR indicates that most TSX-listed

public companies have interim review engagements, although some SEC registrants that

qualify as foreign private issuers opt out of having such a review performed. Overall, we

found the following exception rates: 14% of TSX SEC registrants; 31% of non-SEC

TSX; 66% of non-TSX SEC registrants;9 and 68% of TSXV non-SEC registrants (68%).

It is noteworthy that the opt-out rate is so high for entities that could benefit from

having reviews performed. Such benefits include a more reliable quarterly financial

reporting process and more reliable quarterly financial statements, especially in terms of

the quality of estimates, accruals and earnings, which are key contributors to information

risk. In addition to benefits for the interim reports, there would be flow-through benefits

for the reliability of the annual financial statements and a potential reduction in the

7 While securities regulations permit the board to delegate approval of the interim financial statements and MD&A to the audit committee, some companies require both the board and audit committee to approve these documents. 8 This requirement came into effect in March 2004. Prior to that, it was impossible to distinguish which companies had a review and which ones did not. A review of a sample of interim financial statements for Q1 of 2003 indicated that virtually none of them reported that no review was performed. 9 These include both TSXV-listed and other Canadian companies that are not listed on a Canadian exchange but are listed solely on a US exchange or traded in the US over the counter.

8

frequency of both quarterly and annual financial statement restatements. For many

companies, the additional cost of having quarterly reviews could probably be offset by

potential cost reductions derived from improved financial reporting processes, better

distribution of audit effort and other efficiency gains.

CICA Handbook Section 7050 sets out requirements for a review of interim

financial statements that are very similar to the US standards. Section 7050 sets out the

procedures to be undertaken and provides for an oral or written report to the audit

committee. The work effort prescribed by Section 7050 suggests various procedures,

including some audit procedures associated with an annual audit (e.g., reading

shareholder and director minutes). When auditors conduct a review of interim financial

statements, they must also comply with CICA Handbook Section 7500, which includes a

requirement to read the MD&A to see whether any information is inconsistent with the

financial statements.

Some audit firms exceed the work effort required by the review standard, the

scope being determined by the audit committee and the audit firm. Common issues that

involve additional audit work at quarter ends include revenue recognition, legal claims

and other contingencies, inventory valuations, taxes, accounts receivable allowances,

derivatives, foreign exchange and consolidation issues. The nature and extent of the

additional procedures appears to vary significantly among the firms and, perhaps, among

clients of the same firm. In some cases, the additional work is restricted to enquiry-based

review procedures. In others, however, auditors execute some audit procedures at the

same time as they conduct the review engagement. These could include examination of

9

material transactions undertaken in the period or in respect of the initial application of

accounting policies. When audit procedures are undertaken, documentation is usually

segregated between that required for the review engagement and that prepared as a result

of the procedures conducted as part of the annual audit. When major transactions are

examined, this activity may occur within the reporting period, rather than at its

conclusion.

The time auditors spend at quarter ends varies according to the nature of the

assignment and the extent to which they are involved with the audit committee’s review.

When a client wants a formal report for its audit committee, additional time is required,

as is the case when an audit or additional review procedures are performed. The range

appears to be 2-10 days.

Enquiries that extend to assessing changes in internal control over disclosures

(ICOD) and internal control over financial reporting (ICOFR) could add one to six days

to an engagement (CICA Handbook paragraph 7050.35 requires enquiry about internal

control and changes in internal control). This large range reflects the need for firms to

call in their systems group when there are changes in the IT-based internal control

processes.

Form of reporting

In both Canada and US, the results of the auditor’s reviews are communicated

privately to audit committees. No public reports are issued except in unusual

circumstances. Those communications can be oral or written, although we understand

10

that most are written. Also, when an auditor performs extended procedures during an

interim period, the extent of the procedures and the findings of those procedures are not

required to be communicated to the audit committee.

Overall, auditors report whether, based on their review, they have become aware

of any material modification that needs to be made for the financial statements to be in

accordance with GAAP. This is in contrast to the negative assurance contemplated in the

general review engagement standards. A written report would normally conclude that the

auditor is not aware of any material modification that needs to be made for the interim

financial statements to be in accordance with GAAP. Before that, however, it would

explain that an interim review does not provide assurance that the auditor would become

aware of any or all significant matters that might be identified in an audit. To some, this

appears to be a convoluted, responsibility-avoiding message. Others counter that it is

designed to protect the auditor against litigation driven by unreasonable expectations. A

public report is not contemplated and is specifically precluded via restrictions on the use

of the auditor’s report.

Benefits of Voluntary Review of Interim Financial Statements

Interim financial statements are often not viewed as reliable, discrete, standalone

documents. There are good reasons for this, including seasonality factors that can

produce highly variable quarterly financial results, the lumpy structure of certain

revenues and costs that are received or paid in one quarter but apply to other quarters, and

uncertainties about costs that are not known until the fiscal year end. These factors result

11

in estimations of accruals and deferrals that can make interim financial statements

irrelevant or unreliable as standalone documents. Performing review engagements on

such documents might not appeal to decision makers.

An alternative view is that interim financial statements should be viewed as

discrete documents that should stand on their own (with interim MD&A), with controls

and audit procedures in place to tie down material transactions and events and prevent

shifting income from quarter to quarter through the abuse of accruals, deferrals and

estimates. About a third of the restatements reported by US public companies are

attributable to restatements of interim financial statements.10 Notorious “fourth quarter

adjustments” of accruals made during the previous three quarters can undermine the

credibility of the quarterly reports and the financial reporting system.

A 2004 study by the Huron Consulting Group11 of restatements due to errors

covering both interim and annual financial statements indicates that the overall frequency

of restatements is increasing, with “quarterly restatements” unrelated to annual

restatements being fairly stable but annual restatements rising dramatically. The

implication of this study is that quarterly reviews are not sufficiently rigorous to tie down

key financial statement results so that restatements are not necessary. The Huron

Consulting Group found that, over the five-year period ending in 2004, 75% of

restatements arose in smaller public companies (i.e., those with revenues of less than

10 Huron Consulting Group, 2004 Report on Financial Reporting Matters (February 28, 2005), www.huronconsultinggroup.com, 1-866-229-8700. 11 Huron Consulting Group, 2004 Report on Financial Reporting Matters.

12

$500 million, with more than half of these companies having revenues under $100

million).12

On the surface, it appears that smaller public companies often have limited

financial expertise in-house and should benefit from a review of their quarterly financial

statements as the auditor could keep in touch with the company’s accounting issues

throughout the year. Some commentators question the need for additional credibility in

the Venture exchange, however. A study carried out on behalf of the Ontario Securities

Commission by Charles River Associates suggests that, due to a form of “branding” of

stock exchanges, investors may compensate for the financial reporting risks associated

with venture exchange companies when making their investment and may suffer no harm

as a result of financial statement restatements that are not really representative of an

entity’s value.13

The quality of interim financial statements is a joint result of interim financial

reporting standards, the preparer’s financial expertise and integrity and the rigour of the

review process. Interim reviews of public company financial statements are based on

audit-based knowledge but require only enquiry, discussion and analysis. Such

procedures may not be sufficient to establish that material transactions, such as business

combinations, restructuring provisions, major contracts, lawsuits and other such material

events are accounted for properly in the quarter. That could result in fourth-quarter

adjustments, when more focused audit procedures are actually performed on those events

12 Huron Consulting Group, 2004 Report on Financial Reporting Matters. 13 Charles River Associates Canada Ltd., The Cost and Benefits of Management Reporting and Auditor Attestation on Internal Controls over Financial Reporting (April 2004).

13

and transactions. Such adjustments can cast doubt on the integrity of the financial

reporting system and the value of quarterly reports.14

The minimum review procedures under section 7050 might not add sufficient

value to the interim reporting of entities that currently are not having reviews done and

some securities regulators in Canada would like to see the work effort prescribed in the

current review engagement standard expanded. This is consistent with many companies’

existing practices. To avoid surprise fourth-quarter restatements, they often request that

auditors perform more than the minimum effort required by Section 7050. Since there are

no established standards for the extended procedures, however, the extent of the

additional procedures can vary from auditor to auditor and even from client to client for

the same auditor.

Research Question

Why do some firms voluntarily choose to have a review performed by their

auditor, while others do not? We hypothesize that firm complexity, economic prospects,

auditor pressure and cost would contribute to firms’ choices.

14 A study by Joshua Livnat and Christine Tan (“Restatements of Quarterly Earnings: Evidence on Earnings Quality and Market Reactions to the Originally Reported Earnings” Unpublished Manuscript Stern School of Business Administration, 2004) of restatements of quarterly earnings by US companies between 1988 and 2002 reports a quarterly restatement rate of 3.4%. (Note that companies with mergers and acquisitions, discontinued operations and fiscal-year changes were specifically excluded.) Quarterly restatements are typically smaller than annual restatements and are often not announced in press releases, becoming known only when a Form 8-K is filed with earnings that differ from those released in the quarterly earnings announcement. The restating companies are generally smaller. Most (62%) of the restatements are downward to correct previously overstated earnings. The most frequently restated components of earnings were cost of goods sold and tax expense. The fourth quarter had noticeably fewer restatements than the other quarters, presumably due to the auditor’s involvement in that quarter. (Note that, during most of the period of the study, auditors were not required to perform a “timely” quarterly review (i.e., at the end of the quarter the financial statements were issued), but could do it “in retrospect” as part of their annual/fourth quarter audit. This was changed starting March 15, 2000.)

14

(Hypothesis 1) Complexity of firms: Auditor review may provide information for

managers of firms with high complexity to better manage and control their business

operations. Moreover, the complexity of firms increases agency costs, thus enhancing

owners’ and creditors’ demand for auditor assurance (Simunic and Stein 1987; Abdel-

khalik 1993; Hay and Davis 2004). So, we predict that the demand for auditor review is

positively associated with the complexity of a firm.

(Hypothesis 2) Growth opportunities: Corporate governance research argues that the cost

of monitoring firms with high growth opportunities is relatively higher because outsiders

are ineffective in monitoring such firms (Gaver and Gaver 1993; Lehn, Patro and Zhao

2003; Yang, Linck and Netter 2004 ). Managers use accounting discretion for

opportunistic manipulation (i.e., opportunism) or communicating private inside

information (i.e., signalling). Since the information asymmetry between auditors and

clients is high for such firms, the value of audit review would be lower. So, we predict

that the demand for auditor review is negatively associated with the growth opportunities

of a firm.

(Hypothesis 3) Assurance and insurance needs: Auditing can provide not only assurance

services but also a type of insurance service (Doogar, Sougiannis and Xie 2003; Asthana,

Balsam and Krishnan 2003). We predict that the demand for auditor review is positively

associated with the assurance and insurance needs of a firm.

15

We consider leverage, auditor, US cross-listing and Venture exchange and industry as

control variables in the model.

Research Design

Model

We run the following logistic regression to test H1 to H3: Review = b0+b1Size+b2Invrec+b3MB+ b4Chgtac +b5FCF+b6ROA+ b7Lev +b8Auditor + b9Uslist + b10TSXV+Industry Dummies + error (1) where,

Review = 1 if the interim financial statements are reviewed by auditors and 0 otherwise;

Size = the log of total assets; Invrec = (inventory + receivables) / total assets; MB = the market value of equity / the book value of equity; Chgtac = change in total accruals for the latest two fiscal years prior to the interim

financial statements, where total accruals are calculated by (Income before extraordinary items – net cash flows from operating activities) / Total assets;

FCF = (Net cash from operating activity + interest paid + net cash flow from investing activity – capitalized interest )/Total assets;

ROA = Income before extraordinary items / Total assets; Lev = long-term debt / total assets; Auditor = 1 if the auditor is Big 4 and 0 otherwise; Uslist = 1 if the company’s shares are publicly traded in US and 0 otherwise; TSXV = 1 if the company is a TSE Venture company and 0 otherwise; Industry dummies = the dummies for two-digit SIC industries in which there are at

least 10 observations in the sample.

Following Knechel, Niemi and Sundgren (2005), we use firm size (Size) and the

ratio of inventory and receivables to total assets (Invrec) to proxy for complexity of a

firm.

16

Based on corporate governance research (e.g., Lehn, Patro and Zhao 2003; Yang,

Linck and Netter 2004), we use the ratio of market value of equity to book value of

equity (MB) to reflect the extent of growth opportunities.

Following DeAngelo (1986), we use the change in total accruals (Chgtac) to

reflect the extent of assurance needs for audit. Following Doogar, Sougiannis, and Xie

(2003), we use free cash flow (FCF) to reflect the extent of either insurance or assurance

value of audit.

We include the variables: ROA, Lev, Auditor, Uslist, and TSXV in the model to

control for the potential effects of firm performance, corporate financing policy, auditor

type, and listing status on companies’ incentives to have their interim financial statements

reviewed. We also add industry dummies in the model to control for industry effects.

Given that the demand for audit review is higher for firms with high complexity

(H1), we expect that both b1, the coefficient on firm size, and b2, the coefficient on the

ratio of inventory and receivables to total assets, would be positive and significant.

We also expect a negative and significant coefficient (b3) for the market-book

ratio as our H2 predicts that the demand for audit review is higher for firms with high

growth opportunities.

The coefficient on the change in total accruals, b4, would be positive and

significant and the coefficient on free cash flows, b5, would also be positive and

significant given that the demand for audit review is higher for firms with high audit

assurance and insurance value (H3).

17

Sample selection

The sample selection started with 400 randomly selected Canadian companies that

publicly filed their 2005 Q1 financial statements on SEDAR. We randomly select 100

companies from each of four segments or layers of Canadian public companies: (Layer1)

TSX-listed companies that are SEC registrants; (Layer2) TSX-listed companies that are

not SEC registrants; (Layer3) Canadian companies that are SEC registrants but are not

listed on the TSX; (Layer4) Other Canadian public companies that are not TSX

companies and are not SEC registrants. Next, we merged the sample of 400 companies

with the Canadian portion of Compustat North American, and generated a sample of 353

companies with data available on Compustat for the fiscal year of 2004. Since the audit

review of quarterly financial statements is mandatory for SEC 10-Q filers, we deleted 26

companies, reducing the sample to 327 companies. Finally, we deleted 61 companies

that had missing data in Compustat for the calculation of variables used in the analysis.

The final sample consists of 266 Canadian firms. We reviewed the interim

financial statements published on SEDAR to identify whether these firms’ 2005 Q1

financial statements had been reviewed by the company’s auditor.15 Table1, Panel A,

reports that 110 (41.4%) companies disclosed that their 2005 Q1 financial statements

were not reviewed by the company’s auditor, compared to 156 (58.6%) companies that

voluntarily had their 2005 Q1 financial statement reviewed by the company’s auditor.

15 Oral reporting as contemplated by Section 7050 can lead to vagueness as to whether or not a complete review in accordance with Section 7050 was conducted. This can lead to anomalies in situations where a company that has not had a formal Section 7050 review sends the interim financial statements to its auditor to read. In some such cases, companies may not include a notice in their interim filings to the effect that no review was performed because they believe that any auditor involvement with interim financial statements constitutes a review, taking comfort in the fact that the statement are marked “unaudited.”

18

Table 1, Panel B, shows that our sample consists of 75 (28.2%) TSX-listed/SEC registrants,

88 (33.1%) TSX-listed/non-SEC registrants firms, 22 (8.3%) non-TSX-listed/SEC registrants,

and 81 (30.4%) non-TSX-listed/non-SEC registrants firms. Table 1, Panel C, reports the

frequency and percent of the sample firms across each SIC industry division. Overall,

our sample includes firms from a variety of industries, including Manufacturing (35%),

Mining (29.3%), Services (11.3%), Transportation (9%), Finance, insurance, and real

estate (7.9%), among many others.

Analysis

Descriptive statistics and comparisons

Table 2, Panel A, presents descriptive statistics on continuous variables and their

comparisons between firms with audit review and firms without audit review. The mean

(median) log of total assets (Size) (million $ amount) is 5.21 (5.34) for reviewed firms

and 2.50 (2.56) firms not reviewed, respectively. T-test and Wilcoxon rank-sum test

show that reviewed firms are significantly larger than firms not reviewed (t=8.53,

z=7.64).

We find that the mean (median) free cash flows (FCF) is -0.16 (-0.06) for

reviewed firms and -0.34 (-0.17) for firms without audit review. The mean and median

FCF for reviewed firms are significantly greater than firms not reviewed (t=2.50,

z=2.82), suggesting that firms with audit review have less difficulty in generating cash

flows than firms without audit review.

19

Furthermore, the mean (median) of return on assets (ROA) is -0.13 (0.01) for

reviewed firms and -1.93 (-0.10) for firms not reviewed. The differences in mean

(median) ROA are also significant between reviewed and not reviewed firms (t=2.30,

z=4.53). Thus, reviewed firms seem to have better earnings performance than firms not

reviewed.

Table 2, Panel B, presents the frequency distributions of Big 4 auditors versus

non-Big 4 auditors, cross-listing firms versus non-cross listing firms, and TSX venture

firms versus non-TSX venture firms. Overall, 182 (68%) of our 266 sample firms have

Big 4 auditors, 97 (36%) firms are cross-listed in both Canadian and US stock markets,

and 103 (39%) firms are TSX Venture firms. We find that roughly 2/3 (68%) of our Big

4 client firms chose to purchase quarterly review of financials statements, whereas a

similar percentage of non-Big 4 clients (61%) chose not to do so. We also find that a

majority of cross-listed firms (69%) have auditor reviewed quarterly reports, although

non-US listed Canadian firms are not much different on whether to purchase quarterly

review (53% vs. 47%). Moreover, 76% of our TSX firms had their financial statements

reviewed by auditors, compared to only 31% of TSX Venture firms who made the same

decision.

In summary, we document that firms with audit review and those without audit

review are different in some characteristics using descriptive analysis. Next, we use

regression analysis to test our hypotheses.

20

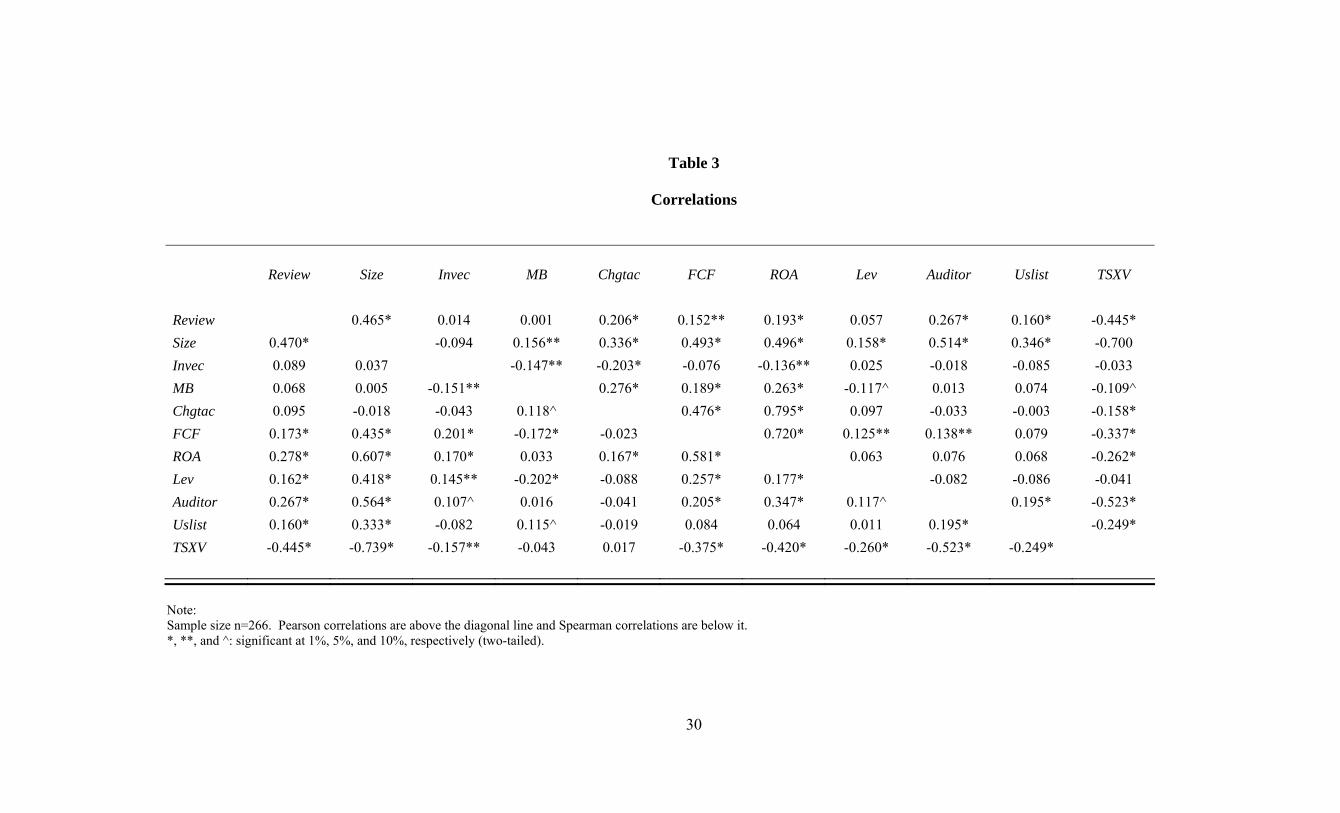

Correlations

Table 3 presents the correlations among all variables. We find that audit review

and firm size are significantly correlated using both parametric and nonparametric

correlation statistics (Pearson=0.465, Spearman=0.470).

Likewise, audit review is also significantly correlated with free cash flows

(Pearson=0.152, Spearman=0.173), return on assets (Pearson=0.193, Spearman=0.278),

auditor type (Pearson=0.267, Spearman=0.267), US listing (Pearson=0.160,

Spearman=0.160), and TSX venture status (Pearson=-0.445, Spearman=-0.445),

respectively. These findings are similar to the results in the descriptive analysis.

In addition, we find significant correlations between ROA and Chgtac

(Pearson=0.795, Spearman=0.167), and between ROA and FCF (Pearson=0.720,

Spearman=0.581), indicating that Chagtac and FCF are both highly correlated with ROA.

Thus, we will consider the multicollinearity issue for ROA in the following regression

analysis.

Regression analysis

We run logistic regressions to test the three hypotheses. Unlike the descriptive

analysis and the correlation analysis, the regression analysis controls for the potential

effects of various firm characteristics including industry dummies.

Table 4 presents results from the regression. First, we run a logistic regression

including ROA as a control variable (Specification 1). Column 3 and 4 in Table 4 report

the coefficients and Wald-statistics for Specification 1. We find that the coefficients on

21

firm size (Size) and the ratio of inventory and receivables to total assets ( Invrec) are 0.47

(Wald-statistics=15.85, p<0.01) and 1.02 (Wald-statistics=1.67, p<0.10) respectively.

This evidence is consistent with H1, suggesting that the demand for audit review is higher

for firms with high complexity than for firms with low complexity.

We also find that consistent with H2, the coefficient on the ratio of market value

to book value of equity (MB) is -0.05 and significant at 10% level (Wald-statistic=2.43).

Hence, the demand for audit review is higher for firms with high growth opportunities

than for firms with low growth opportunity when MB is used as a proxy for growth

opportunity.

Moreover, we document that the coefficient on the change in total accruals

(Chgtac) is 1.45 and significant at 1% level (Wald-statistic=6.39), consistent with the

conjecture (H3) that the demand for audit review is higher for firms with high audit

value. However, we find that the coefficient on free cash flows (FCF) is -0.74 and is

significant at 5% level (Wald-statistic=3.33), inconsistent with H3. Additionally, we also

find that the coefficient on TSX venture variable (TSXV) is -1.03 and significant at 1%

(Wald-statistic=5.60), suggesting that TSX venture firms are less likely to have their

interim financial statements reviewed by auditors.

By considering the potential multicollinearity effects due to the high correlations of

ROA with Chagtac and FCF respectively, we run the regression again after dropping

ROA from the model (Specification 2). Column 5 and 6 in Table 4 report the coefficients

and Wald-statistics for Specification 2. Our findings are consistent with those obtained

from Specification 1. Specifically, we document that the coefficients on Size and Invrec

22

are 0.46 and 1.01 respectively, and significant at 1% and 10% levels (Wald-

statistics=15.80 and 1.65, respectively). Similarly, we find a significant negative

coefficient on MB (b3=-0.05, Wald-statistic=2.50, p<0.10) that supports H2. Likewise,

we find mixed evidence on H3. The coefficients on Chgtac and FCF are 1.412 and -

0.798 respectively, and significant at 1 % and 5 % levels (Wald-statistics=6.19 and 4.63,

respectively). In addition, we also find that the coefficient on TSXV is -1.042 and

significant at 1% (Wald-statistic=5.71).

Concluding Remarks

Our study provides descriptive information about Canadian public companies that

voluntarily choose to have review engagements performed on their quarterly financial

statements. In addition, we provide evidence supporting our hypotheses that the

complexity of a firm and its growth opportunities affect the incentives of the firm to have

its interim financial statements reviewed by its auditors and for the auditors to perform

such a review.

Currently, Canadian regulators object to the absence of a published review

engagement report on the grounds that assurance engagements should communicate the

scope of work done and assurance provided. Some auditors agree that a written report

attached to the interim financial statements would be preferable; however, because it

tends to add rigour to the engagement, encouraging compliance with, and documentation

of, all suggested procedures, including management’s representations, it may add costs

and time to the review process. Discussions with preparers indicate that the full 45-day

23

period between the end of the quarter and the filing deadline is often required to complete

the pre-filing review process.

Some auditors fear that publicly reporting the results of reviews of interim financial

statements can lead to a new expectation gap, especially if managements and audit

committees believe that interim engagements with public reporting will result in lower

annual audit fees and will guarantee that no errors in the first three quarters will be

detected during the year-end audit. Thus some audit firms are concerned about litigation

risk if the interim review report becomes a public report. The concerns are based on the

limited nature of the work performed in a review and the difficulty of conveying the

nature of the review engagement to users removed from the entity’s management and

governance processes. They worry about the prospect of an expectation gap that could

lead to blaming the auditor for failing to identify accounting problems discovered after

the financial statements are filed. Regulators counter that the liability cap results in little

potential financial penalty for the auditor.

While currently there is no public reporting of interim reviews in the US, the

recently approved international standard requiring such reporting met with no opposition

from the major firms and professional associations such as the AICPA and CICA.16 The

International Auditing and Assurance Standards Board has approved a standard that

would require auditors to provide a written published report similar to the report to the

audit committee set out in Section 7050 of the CICA Handbook and the AICPA’s SAS

100. Evidence provided by Krishnan and Zhang (2004) for US public companies

16 http://www.ifac.org/IAASB/ProjectHistory.php?ProjID=0011.

24

indicates that currently very few choose to voluntarily provide review engagement

reports, presumably due to concerns about litigation risk. However, this is in the context

of mandatory review of quarterly financial statements. The proposed international

standards do not assume mandatory review requirements. They merely mandate public

reporting when a review engagement is performed. Thus, a natural extension to this

study, once new reporting requirements are in place, would be to determine their impact

on voluntary adoption of review engagements.

In addition, formal public reporting on quarterly financial statements could

introduce delays in reporting as auditors seek to mitigate any risks related to such

reporting. Presumably, delays could reflect on the quality of the companies’ financial

reporting processes. However, regardless of the reason, delays could be undesirable to

investors and analysts seeking timely reports and this could lead management to choose

to forego a review in the interest of preserving timely reporting. Thus, another extension

of this study could be to explain observed delays in reporting by companies that provide

voluntary reviews of quarterly financial statements compared with those that opt out.

25

References Abdel-khalik, A. R. 1993. Why do private companies demand auditing? A case for

organizational loss of control. Journal of Accounting, Auditing & Finance, 8(1): 31-52.

Asthana, S. C., S. Balsam, and J. Krishnan. 2003. Audit firm reputation and client stock

price reactions: Evidence from the Enron experience. Working paper, Temple University, Philadelphia, FA.

Charles River Associates Canada Ltd., The Cost and Benefits of Management Reporting

and Auditor Attestation on Internal Controls over Financial Reporting (April 2004). DeAngelo, L. 1986. Accounting numbers as market valuation substitute: A study of

management buyouts of public stockholders. The Accounting Review, 61(July): 400-420.

Doogar, R., T. Sougiannis, and H. Xie. 2003. The impairment of auditor credibility:

Stock market evidence from the Enron-Andersen saga. Working paper, University of Illinois at Urbana-Champaign.

Ettredge, M., D. Simon, D. Smith, and M. Stone. 1994. Why do companies purchase

timely quarterly reviews? Journal of Accounting and Economics, 18 (September): 131-156.

Ettredge, M., D. Simon, D. Smith, and M. Stone. 2000a. The effect of the external

accountant's review on the timing of adjustments to quarterly earnings. Journal of Accounting Research, 38 (Spring): 195-207.

Ettredge, M., D. Simon, D. Smith, and M. Stone. 2000b. Would switching to timely reviews

delay quarterly and annual earnings releases? Review of Quantitative Finance and Accounting, 14 (March): 111-130.

Gaver, J. J., and K. M. Gaver. 1993. Additional evidence on the association between

investment opportunity set and corporate financing, dividend, and compensation polices. Journal of Accounting & Economics, 16: 125-160.

Hay, D., and D. Davis. 2004. The voluntary choice of an auditor of any level of quality.

Auditing: A Journal of Practice and Theory, 23(2): 37-53. Huron Consulting Group, 2004 Report on Financial Reporting Matters (February 28,

2005), www.huronconsultinggroup.com, 1-866-229-8700.

26

Knechel, R., L. Niemi, and S. Sundgren. 2005. Attributes affecting auditor choice. Working paper (presented at 2005 AAA Annual Meeting), University of Florida.

Krishnan, J., and Y. Zhang. 2004. Auditor Litigation Risk and Corporate Disclosure of

Quarterly Review Report. Unpublished manuscript, Department of Accounting, Fox School of Business and Management, Temple University.

Lehn, K., S. Patro, and M. Zhao. 2003. Determinants of the size and structure of

corporate boards: 1935-2000. Working paper, University of Pittsburgh. Livnat, J., and C. Tan. 2004. Restatements of Quarterly Earnings: Evidence on Earnings

Quality and Market Reactions to the Originally Reported Earnings. Unpublished manuscript, Stern School of Business Administration.

Simunic, D. A., and M. T. Stein. 1987. Product Differentiation in Auditing: Auditor

Choice in the Market for Unseasoned New Issues. Vancouver, BC, CGA Research Foundation.

Yang, T., J. S. Linck, and J. M. Netter. 2004. A large sample study on board changes

and determinants of board structure. Working paper, University of Georgia.

27

Table 1

Sample Descriptions

Panel A: Frequencies and percents of firms whose 2005 Q1 financial statements were

reviewed or not reviewed by auditors Frequency Percent Audit Review Firms 156 58.6% Non-Audit Review Firms 110 41.4% Total 266 100.0% Panel B: Frequencies and percents of firms in each sample layer Frequency Percent Layer1: TSE-listed/SEC registrants 75 28.2% Layer2: TSE-listed/non-SEC registrants 88 33.1% Layer3: non-TSX-listed/SEC registrants 22 8.3% Layer4: non-TSX-listed/non-SEC registrants 81 30.4% Total 266 100.0% Panel C: Frequencies and percents of firms across SIC industry divisions Frequency Percent Manufacturing 93 35.0% Mining 78 29.3% Services 30 11.3% Transportation 24 9.0% Finance, insurance, and real estate 21 7.9% Wholesale trade 8 3.0% Retail trade 7 2.6% Public administration 3 1.1% Agriculture, forestry, and fishing 1 0.4% Construction 1 0.4% Total 266 100.0%

28

Table 2

Descriptive Statistics and Comparisons Panel A: Descriptive statistics and comparisons on continuous variables between firms with

and without audit review

Variable Group N Mean Median Std.

Deviation t score z score Size Reviewed 156 5.21 5.34 2.70 8.53* 7.64* Not reviewed 110 2.50 2.56 2.33 Invec Reviewed 156 0.21 0.14 0.21 0.22 1.45 Not reviewed 110 0.21 0.12 0.24 MB Reviewed 156 1.82 2.00 4.49 0.01 1.11 Not reviewed 110 1.81 1.55 7.49 Chgtac Reviewed 156 0.04 0.00 0.23 3.42* 1.55 Not reviewed 110 -0.35 0.01 1.39 FCF Reviewed 156 -0.16 -0.06 0.47 2.50** 2.82* Not reviewed 110 -0.34 -0.17 0.72 ROA Reviewed 156 -0.13 0.01 0.53 2.30** 4.53* Not reviewed 110 -1.93 -0.10 9.74 Lev Reviewed 156 0.17 0.11 0.22 0.92 2.63* Not reviewed 110 0.15 0.01 0.26

29

Table 2 (Continued) Panel B: Frequency distributions and chi-square tests on dummy variables between firms with

and without audit review Big 4 auditor Non-Big 4 auditor Total χ2

Reviewed 123(68%) 33(39%) 156(59%) 18.98* Non-reviewed 59(32%) 51(61%) 110(41%) Total 182(100%) 84(100%) 266(100%) US listed Non-US listed Total χ2

Reviewed 67(69%) 89(53%) 156(59%) 6.84* Non-reviewed 30(31%) 80(47%) 110(41%) Total 97(100%) 169(100%) 266(100%) TSX TSX venture Total χ2

Reviewed 124(76%) 32(31%) 156(59%) 52.71* Non-reviewed 39(24%) 71(69%) 110(41%) Total 163(100%) 103(100%) 266(100%)

Note: *, **: significant at 1% and 5%, respectively (two-tailed).

30

Table 3

Correlations

Review Size Invec MB Chgtac FCF ROA Lev Auditor Uslist TSXV Review 0.465* 0.014 0.001 0.206* 0.152** 0.193* 0.057 0.267* 0.160* -0.445* Size 0.470* -0.094 0.156** 0.336* 0.493* 0.496* 0.158* 0.514* 0.346* -0.700 Invec 0.089 0.037 -0.147** -0.203* -0.076 -0.136** 0.025 -0.018 -0.085 -0.033 MB 0.068 0.005 -0.151** 0.276* 0.189* 0.263* -0.117^ 0.013 0.074 -0.109^ Chgtac 0.095 -0.018 -0.043 0.118^ 0.476* 0.795* 0.097 -0.033 -0.003 -0.158* FCF 0.173* 0.435* 0.201* -0.172* -0.023 0.720* 0.125** 0.138** 0.079 -0.337* ROA 0.278* 0.607* 0.170* 0.033 0.167* 0.581* 0.063 0.076 0.068 -0.262* Lev 0.162* 0.418* 0.145** -0.202* -0.088 0.257* 0.177* -0.082 -0.086 -0.041 Auditor 0.267* 0.564* 0.107^ 0.016 -0.041 0.205* 0.347* 0.117^ 0.195* -0.523* Uslist 0.160* 0.333* -0.082 0.115^ -0.019 0.084 0.064 0.011 0.195* -0.249* TSXV -0.445* -0.739* -0.157** -0.043 0.017 -0.375* -0.420* -0.260* -0.523* -0.249*

Note: Sample size n=266. Pearson correlations are above the diagonal line and Spearman correlations are below it. *, **, and ^: significant at 1%, 5%, and 10%, respectively (two-tailed).

31

Table 4

Logistic Regressions

Specification 1 Specification 2

Variable Predicted sign Coefficient Wald-stat Coefficient Wald-stat Constant ? -1.55 4.69** -1.53 4.60

Size + 0.47 15.85* 0.46 15.80*

Invec + 1.02 1.67^ 1.01 1.65^

MB - -0.05 2.43^ -0.05 2.50^

Chgtac + 1.45 6.39* 1.41 6.19*

FCF + -0.74 3.33** -0.80 4.63**

ROA ? -0.06 0.21 n/a n/a

Lev ? -0.26 0.13 -0.24 0.11

Auditor ? -0.22 0.27 -0.21 0.26

Uslist ? -0.07 0.04 -0.06 0.03

TSXV ? -1.03 5.60* -1.04 5.71*

Industry dummies Included Included

N 266 266 -2 Log likelihood 266.78 266.87

Chi-square 93.98* 93.89*

Note: *, **, and ^: significant at 1%, 5%, and 10%, respectively (one-tailed).