what is your interest? discover the impact and power of interest

TRANSCRIPT

What is Your Interest?Discover the impact and power of interest

How does monetary policy influence inflation and employment?

Let’s look at the article at federalreserve.gov• Inflation – the overall increase in the price of goods and services that we buy•Monetary policy influences inflation and the economy-wide demand for goods and services in the short run (not long term)• The Fed sets the interest rates that banks pay to borrow; this affects

The interest rates banks pay depositors

The rate banks charge on loans

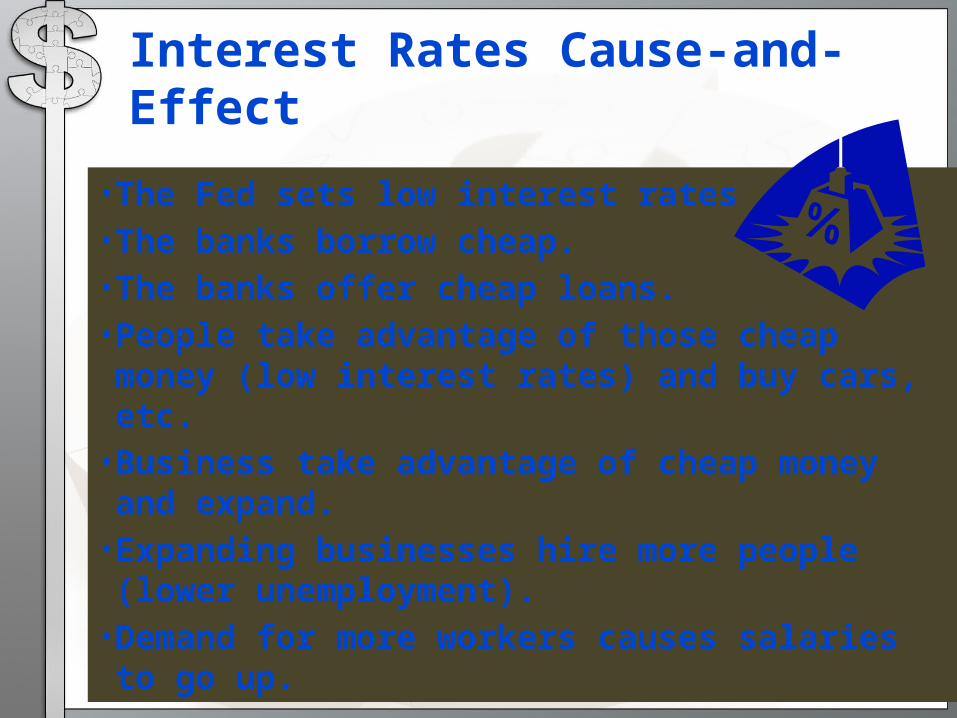

Interest Rates Cause-and-Effect

• The Fed sets low interest rates• The banks borrow cheap.• The banks offer cheap loans.•People take advantage of those cheap money (low interest rates) and buy cars, etc.•Business take advantage of cheap money and expand.• Expanding businesses hire more people (lower unemployment).•Demand for more workers causes salaries to go up.

What do Banks do with that Money?

Matching Savers and BorrowersIt is hard to match up savers’ goals and borrowers’ requests directly. Financial institutions do this job; for example:

Banks pool savers’ money together and lend from the pool.

Life insurance companies use policyholders’ funds to build up a pool from which survivors can be paid.

Pension funds use workers’ saved money to lend and invest, using the returns to finance the workers’ retirements.

• Financial institutions provide ways for people to save and invest.Without offering incentives like interest payments to depositors, it is difficult for depository institutions to

get money to accomplish these things.

How does Inflation Affect Me?

Let’s say you are earning 1% interest on your savings account. So over the course of a year, with $100 in the bank, you would make $1 in interest.

Now, let’s say the inflation rate is 2%. That means that everything costs 2% more.

Your bank balance is now $101, but it that amount won’t buy what it did a year ago. What you could buy for $101 will now cost you $103.02 ($101 plus 2%).

You saved $101.00 but lost 2.02 in purchasing power with that money.

Inflation and Standard of Living

Let’s take a look at how inflation affects our standard of living.

Click link

Calculating Simple InterestPrincipal: The amount you borrow (on a loan) or deposited (in some form of savings instrument)Interest: The percentage rate of interest

The formula for this is very simple: I=PRT

• I is interest

•P is Principal

•R is the percentage rate expressed as decimal

•T is time, generally expressed in years, assuming your rate is an annual rate.

So, if you borrow $5000 at 6% for 5 years, I = 5000.00 x 6% x 5 = $1500.00 You will have to repay a total of $6500.00.Source: WikiHow

Let’s try an

online calculator

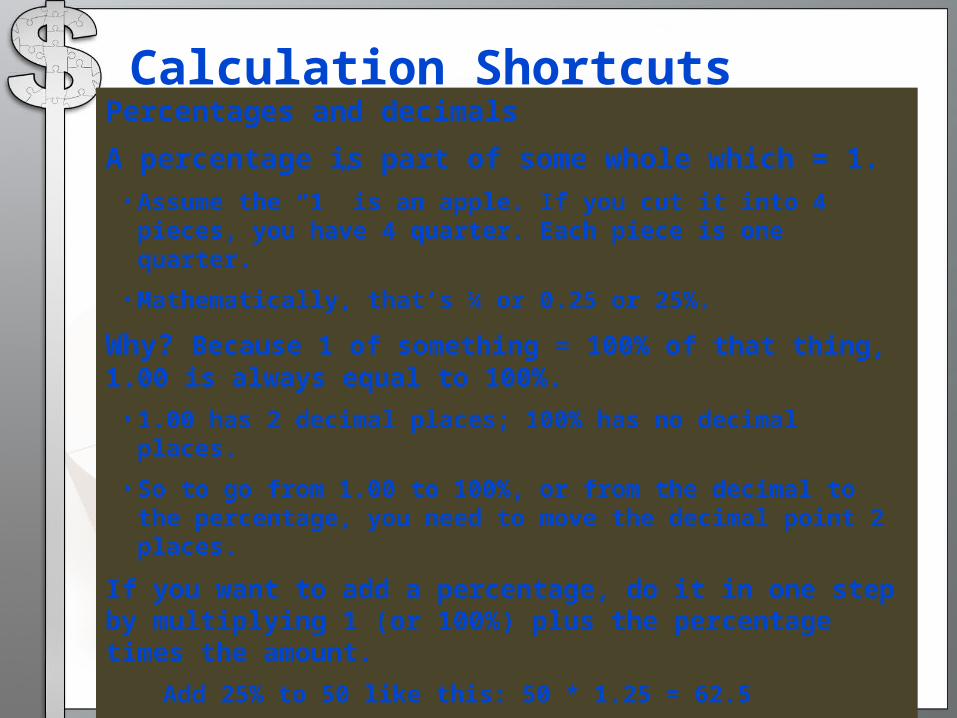

Calculation ShortcutsPercentages and decimals

A percentage is part of some whole which = 1.• Assume the “1” is an apple. If you cut it into 4 pieces, you have 4 quarter. Each piece is one quarter.

• Mathematically, that’s ¼ or 0.25 or 25%.

Why? Because 1 of something = 100% of that thing,1.00 is always equal to 100%.

• 1.00 has 2 decimal places; 100% has no decimal places.

• So to go from 1.00 to 100%, or from the decimal to the percentage, you need to move the decimal point 2 places.

If you want to add a percentage, do it in one step by multiplying 1 (or 100%) plus the percentage times the amount.

Add 25% to 50 like this: 50 * 1.25 = 62.5

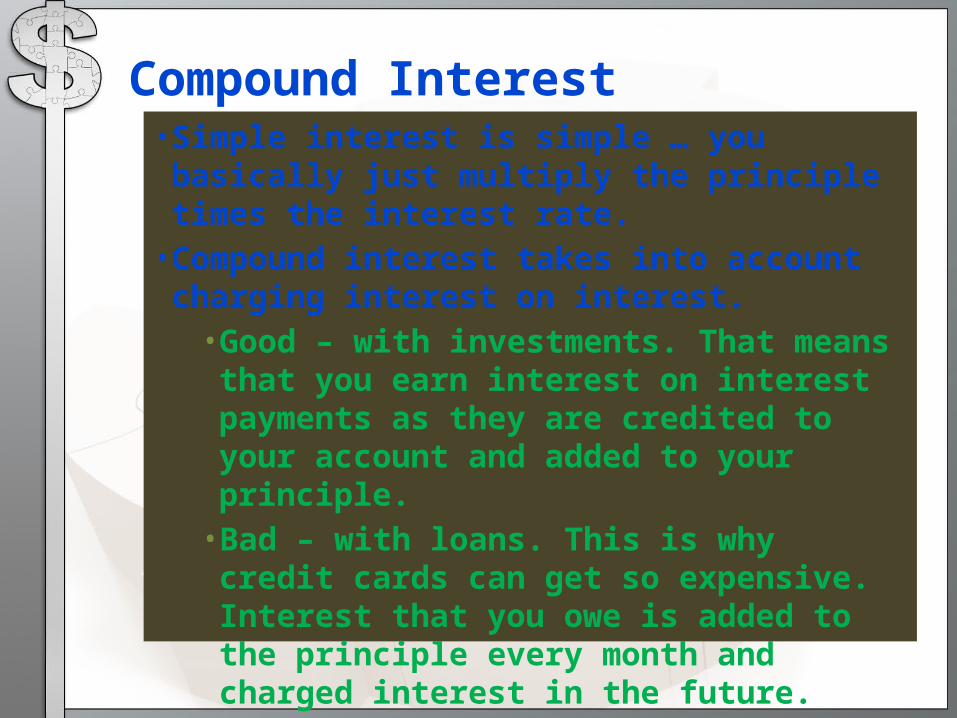

Compound Interest• Simple interest is simple … you basically just multiply the principle times the interest rate.• Compound interest takes into account charging interest on interest. •Good – with investments. That means that you earn interest on interest payments as they are credited to your account and added to your principle.•Bad – with loans. This is why credit cards can get so expensive. Interest that you owe is added to the principle every month and charged interest in the future.

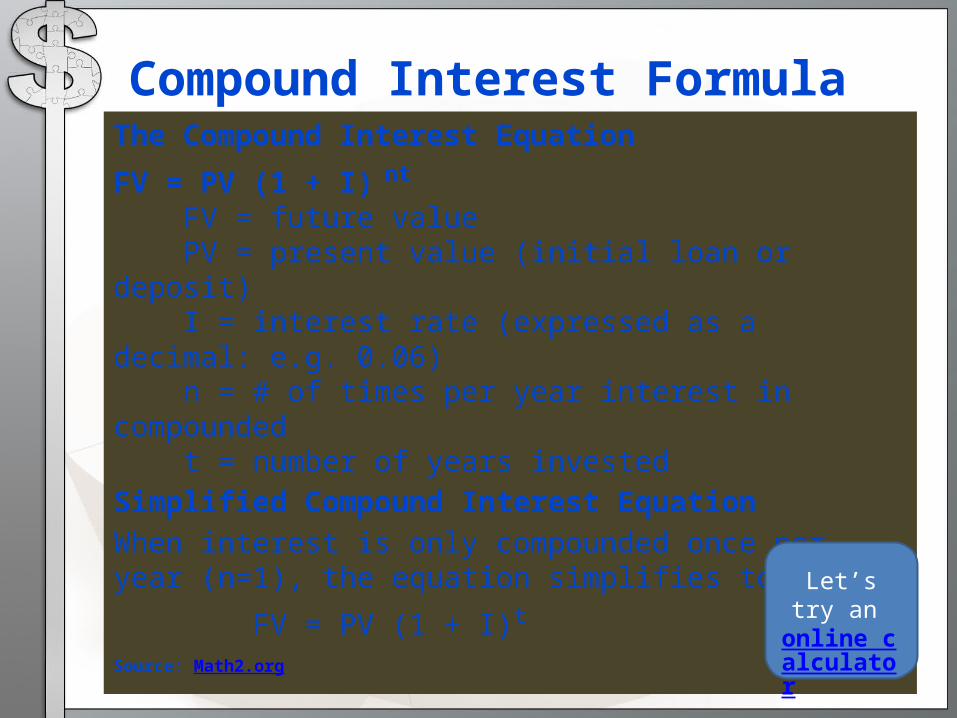

Compound Interest FormulaThe Compound Interest Equation

FV = PV (1 + I) nt

FV = future value PV = present value (initial loan or deposit) I = interest rate (expressed as a decimal: e.g. 0.06) n = # of times per year interest in compounded t = number of years investedSimplified Compound Interest EquationWhen interest is only compounded once per year (n=1), the equation simplifies to:

FV = PV (1 + I)t

Source: Math2.org

Let’s try an

online calculator