webcast 2q14

TRANSCRIPT

OPERATIONAL AND

FINANCIAL RESULTS

2nd Quarter 2014

__

Conference Call / Webcast

August, 11th 2014

DISCLAIMER

FORWARD-LOOKING STATEMENTS:

DISCLAIMER

The presentation may contain forward-looking statements about future

events within the meaning of Section 27A of the Securities Act of 1933, as

amended, and Section 21E of the Securities Exchange Act of 1934, as

amended, that are not based on historical facts and are not assurances of

future results. Such forward-looking statements merely reflect the

Company’s current views and estimates of future economic circumstances,

industry conditions, company performance and financial results. Such

terms as "anticipate", "believe", "expect", "forecast", "intend", "plan",

"project", "seek", "should", along with similar or analogous expressions, are

used to identify such forward-looking statements. Readers are cautioned

that these statements are only projections and may differ materially from

actual future results or events. Readers are referred to the documents filed

by the Company with the SEC, specifically the Company’s most recent

Annual Report on Form 20-F, which identify important risk factors that

could cause actual results to differ from those contained in the forward-

looking statements, including, among other things, risks relating to general

economic and business conditions, including crude oil and other

commodity prices, refining margins and prevailing exchange rates,

uncertainties inherent in making estimates of our oil and gas reserves

including recently discovered oil and gas reserves, international and

Brazilian political, economic and social developments, receipt of

governmental approvals and licenses and our ability to obtain financing.

We undertake no obligation to publicly update or revise any forward-

looking statements, whether as a result of new information or future

events or for any other reason. Figures for 2014 on are estimates or

targets.

All forward-looking statements are expressly qualified in their entirety

by this cautionary statement, and you should not place reliance on any

forward-looking statement contained in this presentation.

NON-SEC COMPLIANT OIL AND GAS RESERVES:

CAUTIONARY STATEMENT FOR US INVESTORS

We present certain data in this presentation, such as oil and gas

resources, that we are not permitted to present in documents filed with

the United States Securities and Exchange Commission (SEC) under

new Subpart 1200 to Regulation S-K because such terms do not

qualify as proved, probable or possible reserves under Rule 4-10(a) of

Regulation S-X.

3

Petrobras: Oil and NGL production in Brazil Production operated by Petrobras in 2Q14 was 2,072 th. bpd

FPSO Cid. São Paulo (Sapinhoá)

2,300

1,950

1,900

2,350

1,850

2,050

2,400

2,250

2,200

2,000

2,150

2,100

2,019

Mar-14

2,017

Feb-14

2,152

Jun-14

2,120

May-14

2,078

Jul-14 Apr-14

2,025

Aug-13

1,954

Jul-13

1,932

2,012

Jan-14

1,990

Dec-13

2,029

Nov-13

2,012

Oct-13

1,997

Sep-13

1,977

Mar-13

1,893

Feb-13

1,957

Jun-13

2,024

May-13

1,925

Apr-13 Jan-13

1,996

Th. bpd 2013: 1.977 th. bpd 1Q13

Average 1.948

2Q13

Average 1.975

4Q13

Average 2.013

2Q14

Average 2.072 3Q13

Average 1.969

P-58 (Parque das Baleias)

P-55 (Roncador)

P-63 (Papa-Terra)

11/Nov FPSO Cid. Paraty (Piloto de Lula NE)

FPSO Cidade de Itajaí (Baúna)

16/Fev

5/Jan 17/Mar

31/Dez Capacity:

120 th. bpd (45% Petrobras)

2013 – 11 th. bpd

2Q14 – 40 th. bpd

Capacity :

80 th. bpd (100% Petrobras)

2013 – 36 th. bpd

2Q14 – 69 th. bpd

Capacity :

120 th. bpd (65% Petrobras)

2013 – 10 th. bpd

2Q14 – 28 th. bpd Capacity :

140 th. bpd (62,5% Petrobras)

2013 – 1 th. bpd

2Q14 – 17 th. bpd

Capacity :

180 th. bpd

(100% Petrobras)

2Q14 – 18 th. bpd

Capacity :

180 th. bpd

(100% Petrobras)

2Q14 – 38 th. bpd

Production Operated by Petrobras

6/Jun

1Q14

Average 2.006 P-62 (Roncador)

12/Mai

Capacity :

180 th. bpd

(100% Petrobras)

2Q14 – 8 th. bpd

4

Petrobras: Oil and NGL production in Brazil Petrobras Production in 2Q14 was 1,972 th. bpd, an increase of 50 th. bpd over 1Q14

Main factors influencing 2Q14 oil production, as compared to 1Q14

Start-up of production for P-62 (Roncador)

Contribution from new wells for P-55 (Roncador), P-58 (Parque das Baleias) and FPSO Cidade de São Paulo (Sapinhoá).

Sustainable production growth (from 1,926 th. bpd in March to 2008 th. bpd in July), i.e., +82 th. bpd production throughout 2Q14.

FPSO Cid. São Paulo (Sapinhoá)

2,050

2,150

2,100

1,900

2,400

2,200

2,250

1,850

2,300

1,950

2,350

2,000

2,024

May-13

1,892

1,925

Apr-13

1,977

Mar-13

1,846

1,893

Feb-13

2,120

1,920

1,957

Jan-13

1,924

1,996 1,997

Jun-14

2,008

Sep-13

1,979

2,025

Aug-13

2,152

1,965

2,049

1,908

Jul-14

1,954

Jul-13

1,888

1,932

Jun-13

1,979

May-14

1,975

2,078

Apr-14

1,933

2,019

Mar-14

1,926

2,017

Feb-14

1,923

2,012

Jan-14

1,917

1,990

Dec-13

1,964

2,029

Nov-13

1,957

2,012

Oct-13

1,960

Th. bpd 2013: 1,931 th. bpd 1Q13

Average 1,910

2Q13

Average 1,931

4Q13

Average 1,960

2Q14

Average 1,972 3Q13

Average 1,924

P-58 (Parque das Baleias)

P-55 (Roncador)

P-63 (Papa-Terra)

11/Nov FPSO Cid. Paraty (Piloto de Lula NE)

FPSO Cidade de Itajaí (Baúna)

16/Fev

5/Jan 17/Mar

31/Dez Capacity:

120 th. bpd (45% Petrobras)

2013 – 11 th. bpd

2Q14 – 40 th. bpd

Capacity:

80 th. bpd (100% Petrobras)

2013 – 36 th. bpd

2Q14 – 69 th. bpd

Capacity:

120 th. bpd (65% Petrobras)

2013 – 10 th. bpd

2Q14 – 28 th. bpd Capacity:

140 th. bpd (62,5% Petrobras)

2013 – 1 th. bpd

2Q14 – 17 th. bpd

Capacity:

180 th. bpd

(100% Petrobras)

2Q14 – 18 th. bpd

Capacity:

180 th. bpd

(100% Petrobras)

2Q14 – 38 th. bpd

6/Jun

1Q14

Average 1,922 P-62 (Roncador)

12/Mai

Capacity:

180 th. bpd

(100% Petrobras)

2Q14 – 8 th. bpd

Petrobras Production Production Operated by Petrobras

5

302

169

119

41153

546

0

50

100

150

200

250

300

350

400

450

500

550

2014 2013 2012 2011 2010 2009 2008 2007 2006 2005 2004 2003

Oil Production in the Pre-Salt Daily Record of 546 th. bpd on July/13 with 25 wells

Th. bpd

High productivity of Pre-salt wells contributed to lower lifting costs (LF) for these projects.

Lula field has a lifting cost of US$ 9/boe (2013), whereas Petrobras LF was US$ 14.76/boe.

Sequential records in Pre-Salt production:

February 18th: connection of the 1st buoy (BSR1) to FPSO Cid. São Paulo, with 36 th. Bpd (best well in the country);

March 17th: P-58 1st oil;

April 3rd: interconnection of the 2nd well to BSR1, with 35 th. Bpd;

April 15th: Start-up of gas exports from FPSO Cid. São Paulo;

May 9th: interconnection of the 1st well to BSR2 (FPSO Cid. Paraty), with 31 th. bpd;

May 9th: Installation of BSR4 finalized, the last of the 4 Buoyancy Supported Risers;

June 25th: Start-up of gas exports from FPSO-Cid. Paraty;

June 28th: Start-up of gas exports from P-58.

Note: 2014 value refers to daily record reached on 07/13/2014

P-58 FPSO Cidade de São Paulo

Capacity: 180 th. bpd

(100% Petrobras)

1Q14: 2 th. bpd

2Q14: 38 th. bpd

Capacity: 120 th. bpd (45% Petrobras)

Total Production:

2013: 24 th. bpd / 1Q14: 44 th. bpd / 2Q14: 89 th. bpd (01/05/13) (03/17/14) )

6

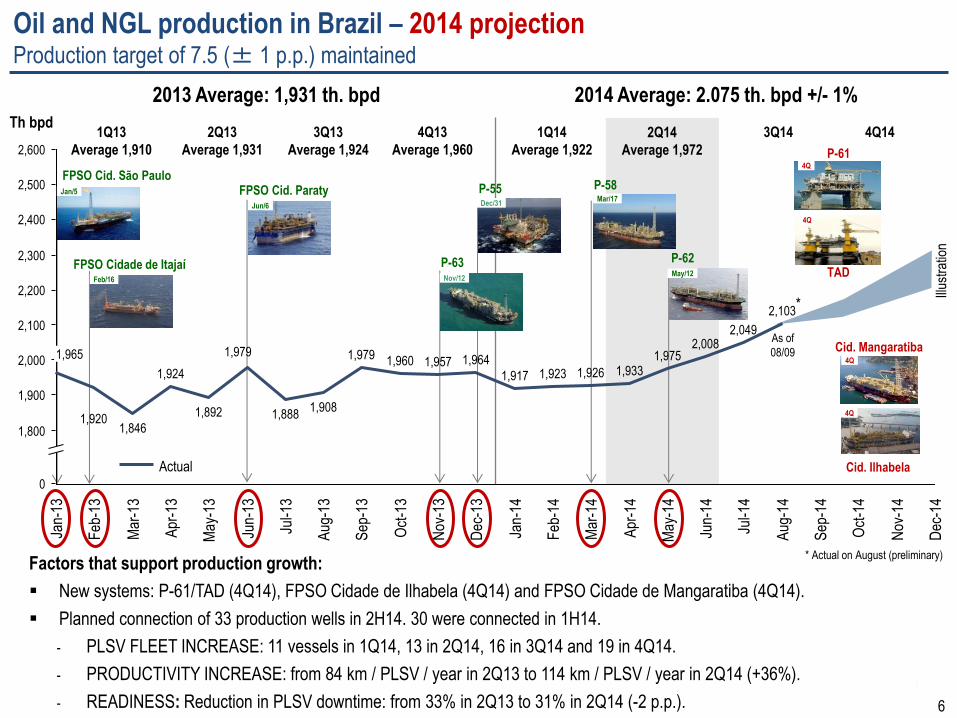

3Q14 4Q14

2014 Average: 2.075 th. bpd +/- 1%

Factors that support production growth:

New systems: P-61/TAD (4Q14), FPSO Cidade de Ilhabela (4Q14) and FPSO Cidade de Mangaratiba (4Q14).

Planned connection of 33 production wells in 2H14. 30 were connected in 1H14.

- PLSV FLEET INCREASE: 11 vessels in 1Q14, 13 in 2Q14, 16 in 3Q14 and 19 in 4Q14.

- PRODUCTIVITY INCREASE: from 84 km / PLSV / year in 2Q13 to 114 km / PLSV / year in 2Q14 (+36%).

- READINESS: Reduction in PLSV downtime: from 33% in 2Q13 to 31% in 2Q14 (-2 p.p.).

Th bpd

2,400

2,600

2,500

2,300

2,200

2,100

2,000

1,900

1,800

0

Dec

-14

Nov

-14

Oct

-14

Sep

-14

Aug

-14

2,103

Jul-1

4

2,049

Jun-

14

2,008

May

-14

1,975

Apr

-14

1,933

Mar

-14

1,926

Feb

-14

1,923

Jan-

14

1,917

Dec

-13

1,964

Nov

-13

1,957

Oct

-13

1,960 S

ep-1

3 1,979

Aug

-13

1,908

Jul-1

3

1,888

Jun-

13

1,979

May

-13

1,892

Apr

-13

1,924

Mar

-13

1,846

Feb

-13

1,920

Jan-

13

1,965

2Q13

Average 1,931

3Q13

Average 1,924

4Q13

Average 1,960

2013 Average: 1,931 th. bpd

1Q13

Average 1,910

1Q14

Average 1,922

P-62

Actual

FPSO Cid. São Paulo FPSO Cid. Paraty

Jun/6

FPSO Cidade de Itajaí Feb/16

Jan/5 P-55

P-63 Nov/12

Dec/31

4Q

4Q

P-61

TAD

P-58 Mar/17

Illus

trat

ion

2Q14

Average 1,972

Cid. Ilhabela

Cid. Mangaratiba 4Q

4Q

Oil and NGL production in Brazil – 2014 projection Production target of 7.5 (± 1 p.p.) maintained

May/12

* Actual on August (preliminary)

*

As of

08/09

7

Oil and Natural Gas Production Costs in Brazil Higher productivity leads to stable lifting cost

2Q14

Cost reduction in Reais when compared to 1Q14, due to the increase in total production (+2.6%), resulting from ramp-up of

new systems (P-58, P-55, P-62 and FPSO São Paulo). Small increase in cost when expressed in US$, due to FX appreciation

11.38 13.12

12.49 12.91 13.28

15.24 14.76 15.02 14.96 14.33 14.57

14.16

9

12

15

18

13.37 13.80 14.15

2012 2013 2011

19.00 20.93 22.31 22.47 22.57

30.79 28.33 29.49

31.25 34.28 32.66 33.14 32.30

32.57

10

20

30

40

26.39

2014

US$/boe

2014 Projection

R$/boe

Average: US$ 12.59 /boe Average: US$ 13.79 /boe Average: US$ 14.76 /boe +9% +7%

US$ 14.57 /boe

2012 2013 2011 2014 Projection

Average: R$ 21.19 /boe Average: R$ 26.97 /boe Average: R$ 31.94 /boe +27% +18%

R$ 32.30 /boe

2011 2012 2013 1Q14 2Q14 Average FX (R$/US$) 1.67 1.96 2.16 2.37 2.23

% of Costs in US$ 18 18 32 35 33

Oil Production (th. bpd) 2,022 1,980 1,931 1,922 1,972

Pre-salt production (th. bpd) 100 138 249 299 347

# of production units in operation 121 122 124 124 125

Days of workovers (PROEF) 1,402 2,966 3,479 872 647

2Q14

+3%

-3% +2%

-4%

4Q13 1Q14 1Q13 4Q12 3Q12 2Q12 1Q12 4Q11 3Q11 2Q11 1Q11 3Q13 2Q13 2Q14

8

Oil Products Sales - Brazil

Considers only Downstream sales

(*) Others – Lubricants, Asphalt, Coke, Propene, Solvent, Benzene, Kerosene and Intermediates.

*

Oil Products Output and Sales in Brazil 2Q14 production up 3% when compared to 1Q14, due to higher diesel and gasoline output

Oil Products Output

Th. bpd +2%

855 822 857

501 483 496

146 135

245 290 284

203 208 219

125

879288102105100

+3%

2Q14

2,180

1Q14

2,124

2Q13

2,138

2Q14 x 1Q14

Oil products output grew 3% due to the production of REPLAN’s

destillation unit, following scheduled turnaround in 1Q14.

Higher utilization factor (from 96% to 98%).

2Q14 x 1Q14

Diesel (5% growth) – seasonality effect, following reduction of

industrial and agricultural activity at the beginning of the year.

Gasoline (3% growth) – increase in light vehicles fleet and increasing

competitiveness to ethanol.

LPG (7% growth) – lower average temperatures and increase in

economic activity.

Diesel

Gasoline

LPG

Naphtha

Jet Fuel

Fuel Oil

Others

978 947 999

583 601 619

233 222237

170 178 162

201 202 204

108111104

114110103

+3%

2.443

2Q14 1Q14

2.371

2Q13

2.372

+3%

5%

3%

+4,3%

+2,6%

July/14:

Output: 2,236 th. bpd

(500 Gasoline and 896 Diesel)

9

Oil Products Output Record in Brazil: 12 Refineries Throughput of 2,172 th. bpd of oil in June

2,100

2,150

2,200

1,850

2,050

2,000

1,950

1,900

1,800

1,750

1,700

1,650

1,600

1,550

2013

2,074

2012

1,944

2011

1,862

2010

1,798

2009

1,799

2008

1,765

2007

1,779

2014

1,746

2005

1,727

2004 2006 2003

1,588

2,172

+228 th. Bpd +12%

1,704

Note: 2014 value refers to the monthly record achieved in June/14.

Th. bpd

New production records in the refining segment

• Excellent efficiency levels: utilization factor of 98% in 2Q14.

• New monthly record of 2,172 th. bpd in June, 21 th. bpd above the previous record achieved in March 2014

Paulínia Refinery – REPLAN

Capacity: 415 th. bpd

The significant increase in the level of output resulted from better performance achieved by the start-up of new quality

and conversion units, as well as the optimization of refining processes and the removal of logistics bottlenecks.

10

Trade Balance: Oil and Oil Products 2Q14 vs. 1Q14: Higher oil imports lowers gasoline imports

2Q14 vs. 1Q14

Reduction in oil exports due to export cargos in transit (and therefore not yet recognized) and higher refining throughput.

Lower product imports as a result of higher gasoline production.

Higher oil imports during 2Q14, particularly in June, based on market conditions that should favor refining higher

volumes of imported oil. Additionally, REPLAN’s stoppage in 1Q14 distorts basis for comparison.

-396-164

-285

-237

-253-64

2002001802858

13

17916668

534359

447

343638 136135159138195162

941

-417

2Q13 2Q14

366

1Q14

359

783

2Q13

708

308

1Q14

-16%

2Q14

-633

-349

1Q14

+52%

+20%

2Q13 2Q14

th. b

pd

-14%

+33%

+82%

Oil Oil Products Gasoline Diesel Others Oil Products Fuel Oil

Exports Imports Balance

July/14: Oil exports 321 th. bpd

Oil imports 193 th. bpd

11

3.47 3.91 4.20

3.83

3.14 3.37

3.14 3.08 3.26

2.88 2.75 2.94 .3,03

2

3

4

5

6

3.50 3.74

2012 2013 2011

5.80 6.25

7.00 6.94 6.60

6.25

6.98

6.24 6.37 6.62 6.48 6.56 6.95

4

6

8

10

4Q13 1Q14 2014 1Q13 4Q12 3Q12

7.07

2Q12 1Q12 4Q11 3Q11 2Q11 1Q11

7.45

3Q13 2Q13

US$/bbl

R$/bbl

Average: US$ 3.86 /bbl Average: US$ 3.44 /bbl Average: US$ 3.09 /bbl -11% -10%

US$ 2.94 / bbl

2012 2013 2011 Average: R$ 6.51 /bbl Average: R$ 6.73 /bbl Average: R$ 6.67 /bbl

+3% 0% R$ 6.56 /bbl

Refining Cost in Brazil Reduction in costs due to the increases in productivity and throughput

2011 2012 2013 1T14 2T14

Average FX (R$/US$) 1,67 1.96 2.16 2.37 2.23

Headcount 9,231 9,289 9,078 9,017 8,938

Throughput (th. bpd) 1,866 1,944 2,074 2,058 2,101

Utilization Factor (%) 91 94 97 96 98

Complexity (UEDC/d) 12.94 14.39 15.02 16.16 16.58

2Q14

2Q14

+7%

+1,2%

2014 Projection

2014 Projection

In Reais, unit cost stable. Increase of 7% in US$ due to FX appreciation. Cost stability a result of optimizing operational costs

(PROCOP) and from increasing sustainable levels of throughput (PROMEGA).

2Q14

+4%

-2%

12

2Q14 x 1Q14

Gas supply to the market totaled 96 million m3/day, a 6% growth over 1Q14. Increase in supply led primarily by LNG

imports to meet higher thermoelectric demand.

Petrobras power generation reached 4.7 GW (4.1 GW in 1Q14), with margin gains, since spot price for energy was

stable (approximately R$ 650/MWh) while unit cost of imported LNG was 8% lower than 2Q14.

Natural Gas Supply and Demand Increase in thermoelectric demand in 2Q14 when compared to 1Q14 and 2Q13

39,9

Million m³/dia

National

Bolivia

LNG

Non-thermoelectric

Thermoelectric

Downstream/Fertilizers

SUPPLY DEMAND

40,2

37,0

11,7

39,3

+6% +6% +6%

2Q14

96.3

2.0 13.4

41.9

38.9

1Q14

91.1

1.9 13.0

37.8

38.4

2Q13

91.2

1.8 12.1

38.1

39.2

18.8

32.8

39.5

2Q13

91.2

18.3

31.6

41.2

22.1

33.0

41.2

1Q14

91.1

+6%

2Q14

96.3

+11%

+18%

+4% +1%

Gas to the System*

July/14:

Demand: 94.3 MM m³/d

Thermoelectric: 41,3 MM m³/d

Supply: 94.3 MM m³/d

National: 45,8 MM m³/d

13

Growth in 2Q14 Operating Income mainly due to the absence of the provision in 1Q14 for Voluntary Separation Incentive

Plan (PIDV)

7.6 +17%

8.8

1Q14 2Q14

R$ Billion

2Q14 Results Operating Income up 17% from 1Q14

2Q14 x 1Q14 Operating Income

Lower unit import costs due to the appreciation of the Real

Absence of the PIDV provision in 1Q14

Lower oil exports volumes

Lower asset sales gains

Write-downs of E&P projects

Operating Income

14

5.4

7.6

-8%

+17%

5.0

8.8

1Q14 2Q14

R$ Billion

Growth in 2Q14 Operating Income due mainly to the absence of the provision for Voluntary Separation Incentive Plan

(PIDV) in 1Q14. Reduction in Net Income due to change in net financial results and a higher effective income tax rate.

2Q14 Results Operating Income up 17% on 1Q14. Net Income down 8%.

2Q14 x 1Q14 Net Income

Lower unit import costs due to the appreciation of the Real

Absence of the PIDV provision in 1Q14

Lower oil exports volumes

Lower gains from asset sales

Write-offs of E&P projects

Lower net financial results, due to the increase in interest

expense and the reduction in financial revenue

Higher effective income tax rate due to 1Q14 fiscal credits

Operating Income

Net Income

15

Structuring Programs and Net Income Impact Positive effect of R$ 3.1 Billion in 2Q14

PROCOP

1.6

2Q14 Net Income

5.0

0.3

R$ -3.1 Billion (-63%)

2Q14 Net Income Without

Structuring Programs

1.9

PROEF

1.2

PRODESIN

Outcome 2.4 0.3 1.8

Income Tax -0.8 - -0.6

Net Income 1.6 0.3 1.2

R$ Billion

PROCOP (R$ 1.6 Billion), PRODESIN (R$ 0.3 Billion) and PROEF (R$ 1.2 Billion) positively impacted Net Income by 63%

(R$ 3.1 Billion).

Structuring Programs

PROCOP: Operating Costs Optimization Program. PRODESIN: Divestment Program. PROEF: Program to Increase Operational Efficiency

16

3.5 3.6 3.5 3.5 3.5 3.6 3.1

R$

Mill

ion

+1.6% +7.8%

+15.8%

1H14

5,140

2H13

5,691

1H13

5,060

2H12

5,146

1H12

4,696

2H11

4,589

1H11

4,057

2012 2013 1H14

General and Administrative Expenses Strong slowdown of the growth rate due to Procop and PIDV

2011

+1.6%

Petrobras

Holding

Others

1H14

5,140

3,552 (69%)

1,587

1H13

5,060

3,507 (69%)

1,554

% of

Revenue

+1%

Personnel

1H14

3,552

1,891

(53%)

1,661

(47%)

1H13

3,507

1,856

(53%)

1,651

(47%)

Typ

e o

f

Exp

end

itu

re

Data Processing, Services, Rentals, Training, Consulting and Depreciation

Flight Tickets

Ground Transportation

Building Management

ICT

Evolution from 2011 to 2014

Petrobras System

Holding

Initiatives PROCOP

PIDV*: 581 employees departured

from Apr/14 to Jun/14

Jan-14

-7%

7.6

May-14

7.9

Apr-14

8.2

Mar-14

8.2

Feb-14

8.3

Jan-14

8.2

Dec-13

8.2 thous emp.

* PIDV: Voluntary Separation Incentive Plan

17

4,00 3,94

39% 40%

0%

10%

20%

30%

40%

50%

1,5

2,5

3,5

4,5

1Q14 2Q14

Net Debt / EBITDA ¹Net Debt / Net Capitalization ²

LEV

ER

AG

E

ND

/ EB

ITD

A

Financial Ratios

Total debt stable

Decrease of cash and cash equivalents due to

yearly dividend payment and investments during

the period.

Leverage steady, at 40%.

ND/EBITDA decreases from 4.00x to 3.94x due to

the dilution of 1Q14 PIDV provision

Indebtedness

Debt Ratios

R$ Billion 03/31/14 06/30/14

Short-term Debt 21.8 23.5

Long-term Debt 286.3 284.2

Total Debt 308.1 307.7

(-) Cash and Cash Equivalent3 78.5 66.4

= Net Debt 229.7 241.3

US$ Billion

Net Debt 101.5 109.6

1) Net Debt / (adjusted EBITDA 1H14 x 2). Adjusted EBITDA= EBITDA excluding earnings of equity-accounted investments and impairments

2) Net debt / (Net Debt + Shareholders Equity)

3) Includes tradable securities maturing in more than 90 days

18

2014 Projections

Oil Products Output (th. bpd) Yield improvement: more Diesel and Gasoline in 2H14

850 840 917

491 489 520

783 823 803

+4%

Diesel

Gasoline

Others

2H14

Forecast

2,240

1H14

2,152

2013

2,124

Oil Production (th. bpd) Production target maintained

2014

Forecast

2013

1,931

7,5% +/- 1p.p.

Oil Exports (th. bpd) Sustainable growth of oil exports

250

166207

+51%

2S14

Forecast

1S14 2013

9%

6%

th. bpd

th. bpd

th. bpd

Domestic Natural Gas Supply (MM m³/day) Higher domestic supply to reduce LNG imports

4049

41

+21%

2H14

Forecast

1H14 2013

MM m³/day

OPERATIONAL AND

FINANCIAL RESULTS

2nd Quarter 2014

__

Information:

Investor Relations

+55 21 3224-1510