webcast - 1q14 results

TRANSCRIPT

OPERATIONAL AND FINANCIAL RESULTS1st Quarter 2014__

Conference Call / WebcastMay 12th 2014

DISCLAIMER

FORWARD-LOOKING STATEMENTS:

DISCLAIMER

The presentation may contain forward-looking statements about futureevents within the meaning of Section 27A of the Securities Act of 1933, asamended, and Section 21E of the Securities Exchange Act of 1934, asamended, that are not based on historical facts and are not assurances offuture results. Such forward-looking statements merely reflect theCompany’s current views and estimates of future economic circumstances,industry conditions, company performance and financial results. Suchterms as "anticipate", "believe", "expect", "forecast", "intend", "plan","project", "seek", "should", along with similar or analogous expressions, areused to identify such forward-looking statements. Readers are cautionedthat these statements are only projections and may differ materially fromactual future results or events. Readers are referred to the documents filedby the Company with the SEC, specifically the Company’s most recentAnnual Report on Form 20-F, which identify important risk factors thatcould cause actual results to differ from those contained in the forward-looking statements, including, among other things, risks relating to generaleconomic and business conditions, including crude oil and othercommodity prices, refining margins and prevailing exchange rates,uncertainties inherent in making estimates of our oil and gas reservesincluding recently discovered oil and gas reserves, international andBrazilian political, economic and social developments, receipt ofgovernmental approvals and licenses and our ability to obtain financing.

We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information or futureevents or for any other reason. Figures for 2014 on are estimates ortargets.

All forward-looking statements are expressly qualified in their entiretyby this cautionary statement, and you should not place reliance on anyforward-looking statement contained in this presentation.

NON-SEC COMPLIANT OIL AND GAS RESERVES:

CAUTIONARY STATEMENT FOR US INVESTORS

We present certain data in this presentation, such as oil and gasresources, that we are not permitted to present in documents filed withthe United States Securities and Exchange Commission (SEC) undernew Subpart 1200 to Regulation S-K because such terms do notqualify as proved, probable or possible reserves under Rule 4-10(a) ofRegulation S-X.

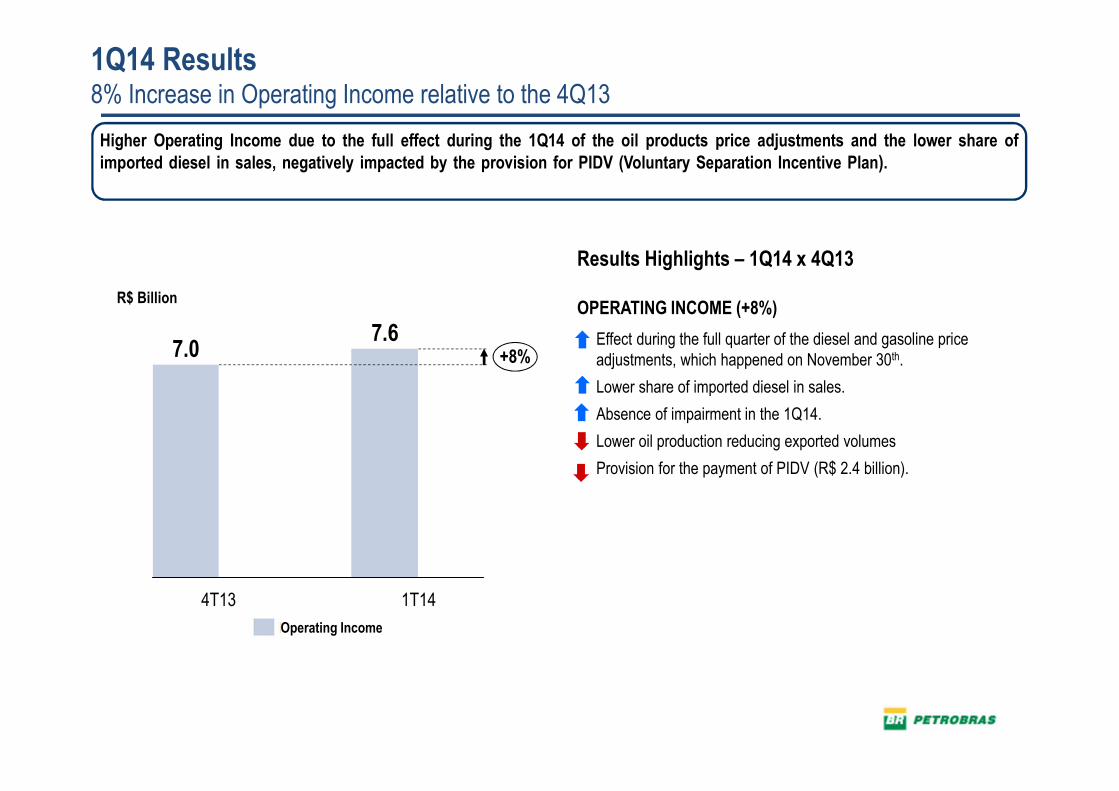

1Q14 Results8% Increase in Operating Income relative to the 4Q13

+8%7.6

7.0

R$ Billion

4T13 1T14

Results Highlights – 1Q14 x 4Q13

OPERATING INCOME (+8%)

� Effect during the full quarter of the diesel and gasoline price adjustments, which happened on November 30th.

� Lower share of imported diesel in sales.

� Absence of impairment in the 1Q14.

� Lower oil production reducing exported volumes

� Provision for the payment of PIDV (R$ 2.4 billion).

Higher Operating Income due to the full effect during the 1Q14 of the oil products price adjustments and the lower share of

imported diesel in sales, negatively impacted by the provision for PIDV (Voluntary Separation Incentive Plan). A queda do lucrolíquido foi função do efeito positivo, no 4T13, do benefício fiscal dos juros sobre capital próprio no valor de R$ 3,2 bilhões.

Operating Income

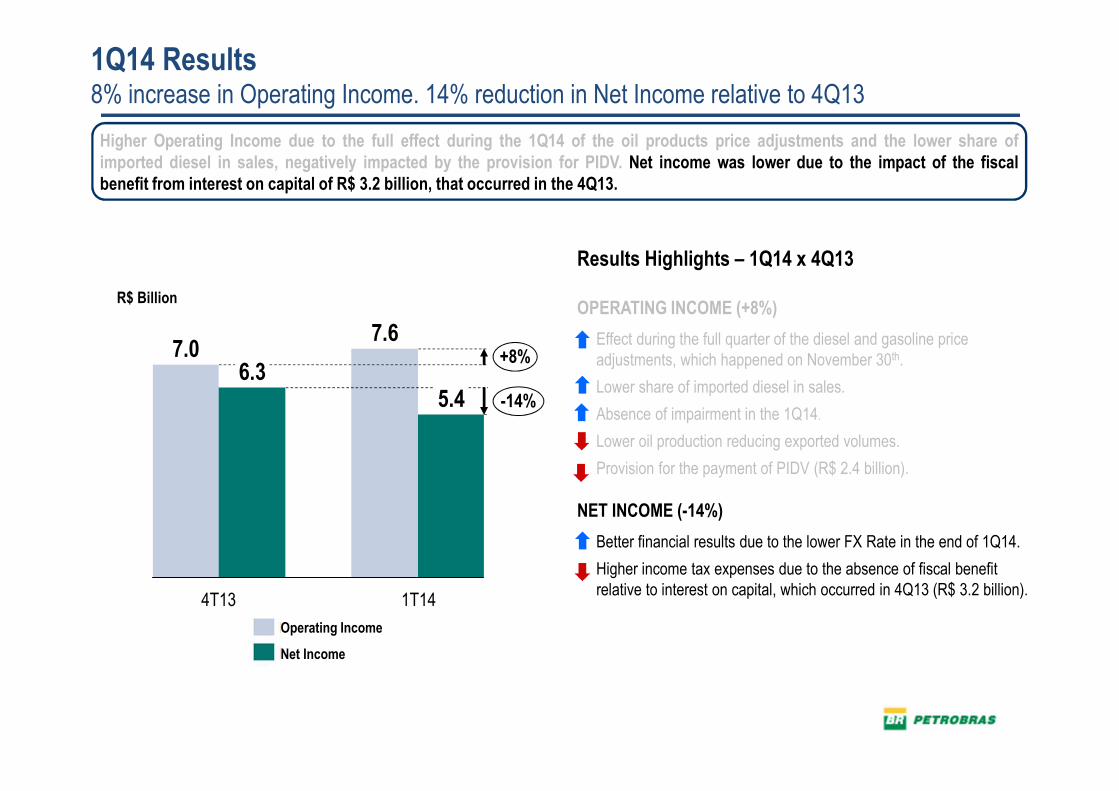

1Q14 Results8% increase in Operating Income. 14% reduction in Net Income relative to 4Q13

-14%5.4

+8%7.6

6.37.0

R$ Billion

4T13 1T14

Results Highlights – 1Q14 x 4Q13

OPERATING INCOME (+8%)

� Effect during the full quarter of the diesel and gasoline price adjustments, which happened on November 30th.

� Lower share of imported diesel in sales.

� Absence of impairment in the 1Q14.

� Lower oil production reducing exported volumes.

� Provision for the payment of PIDV (R$ 2.4 billion).

NET INCOME (-14%)

� Better financial results due to the lower FX Rate in the end of 1Q14.

� Higher income tax expenses due to the absence of fiscal benefit relative to interest on capital, which occurred in 4Q13 (R$ 3.2 billion).

Higher Operating Income due to the full effect during the 1Q14 of the oil products price adjustments and the lower share ofimported diesel in sales, negatively impacted by the provision for PIDV. Net income was lower due to the impact of the fiscalbenefit from interest on capital of R$ 3.2 billion, that occurred in the 4Q13.

Operating Income

Net Income

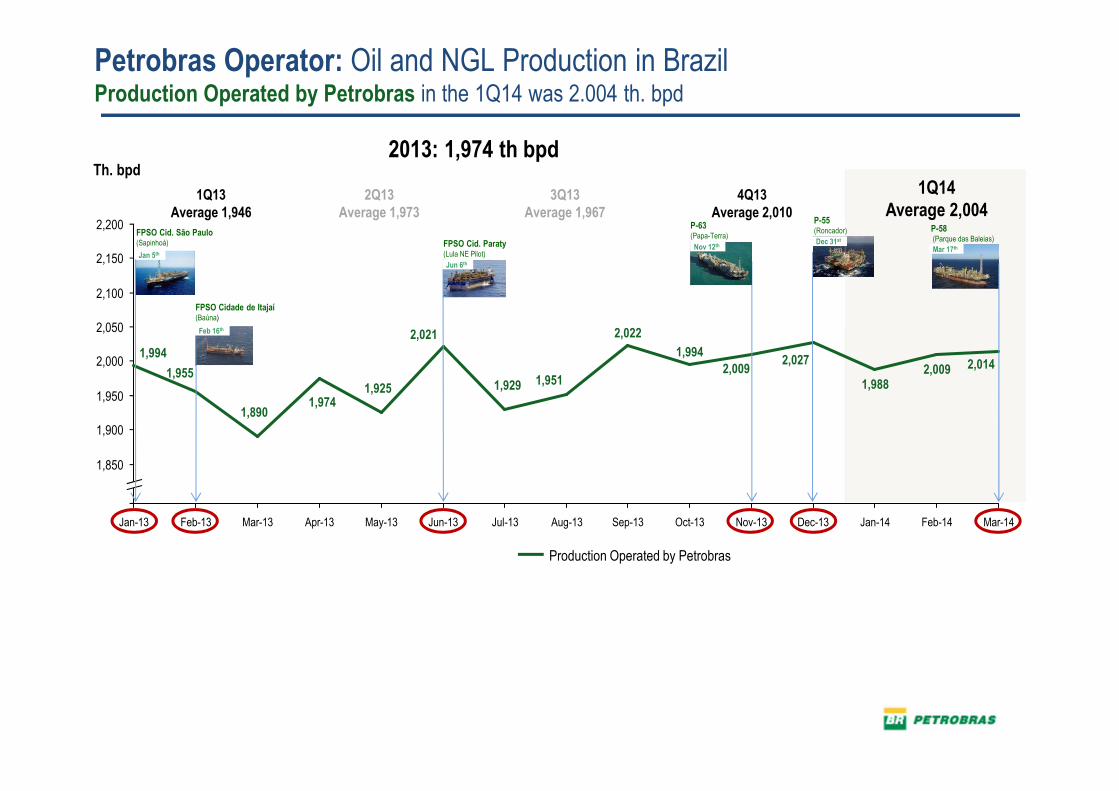

FPSO Cid. São Paulo(Sapinhoá)

2,150

2,100

2,050

2,000

1,950

1,900

1,850

2,200

2,022

Aug-13

1,951

Jul-13 Mar-14Jun-13

2,021

May-13

1,925

Apr-13

1,929

1,974

Mar-13

1,890

1,955

Jan-13

1,994

Feb-13 Sep-13

2,014

Feb-14

2,009

Jan-14

1,988

Dec-13

2,027

Nov-13

2,009

Oct-13

1,994

Th. bpd2013: 1,974 th bpd

1Q13Average 1,946

2Q13Average 1,973

4Q13Average 2,010

1Q14Average 2,004

3Q13Average 1,967

P-58(Parque das Baleias)

P-55(Roncador)

P-63(Papa-Terra)

Nov 12thFPSO Cid. Paraty(Lula NE Pilot)

FPSO Cidade de Itajaí(Baúna)

Feb 16th

Jan 5thMar 17th

Dec 31st

Production Operated by PetrobrasPetrobras Production

Jun 6th

Petrobras Operator: Oil and NGL Production in BrazilProduction Operated by Petrobras in the 1Q14 was 2.004 th. bpd

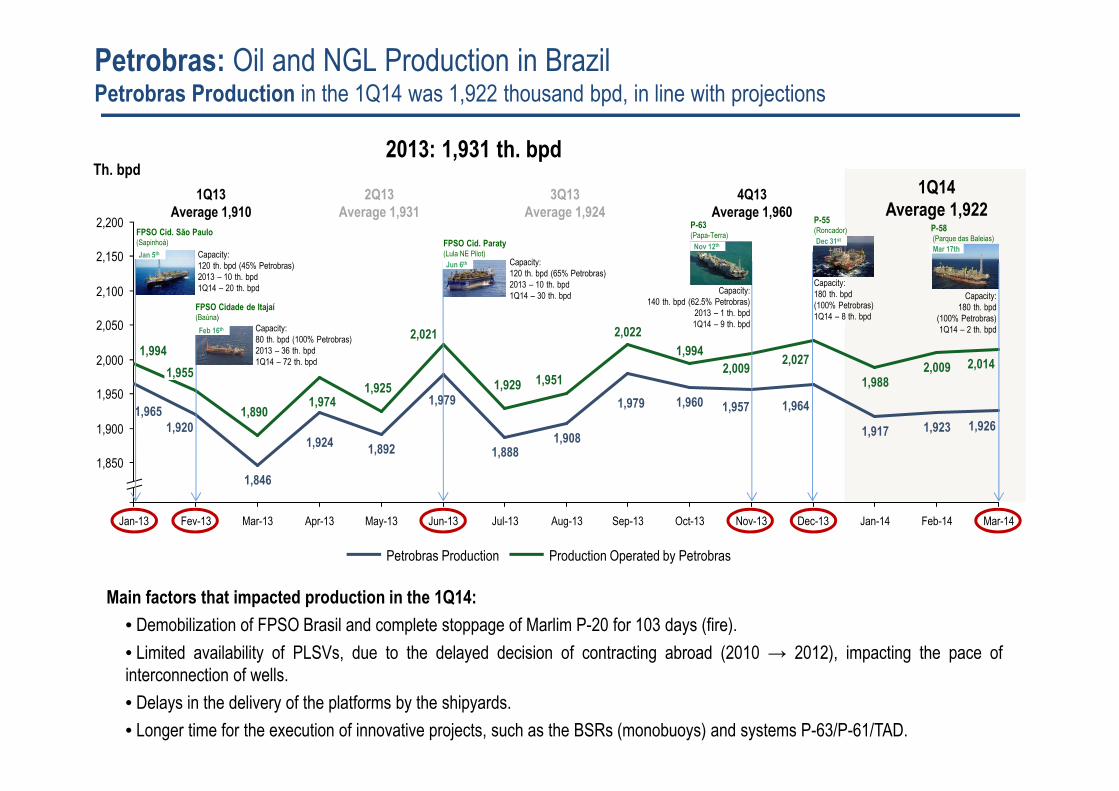

FPSO Cid. São Paulo(Sapinhoá)

2,200

2,000

2,100

2,050

2,150

1,850

1,950

1,900

1,974

1,924

Mar-13

1,890

1,846

Fev-13

1,955

Jan-13

1,994

1,965

Jan-14

2,009

1,920 1,923

Dec-13

1,926

Mar-14

1,964

Feb-14

1,917

2,014

Apr-13

1,892

Nov-13

1,957

2,027

1,988

Oct-13

1,925

1,994

1,960

Sep-13

2,022

1,979

Aug-13

1,9512,009

Jul-13

1,929

1,888

Jun-13

2,021

1,979

May-13

1,908

Th. bpd

Petrobras: Oil and NGL Production in BrazilPetrobras Production in the 1Q14 was 1,922 thousand bpd, in line with projections

1Q13Average 1,910

2Q13Average 1,931

4Q13Average 1,960

1Q14Average 1,922

3Q13Average 1,924

P-58(Parque das Baleias)

P-55(Roncador)

P-63(Papa-Terra)

Nov 12thFPSO Cid. Paraty(Lula NE Pilot)

FPSO Cidade de Itajaí(Baúna)

Feb 16th

Jan 5thMar 17th

Dec 31st

Capacity:120 th. bpd (45% Petrobras)2013 – 10 th. bpd1Q14 – 20 th. bpd

Capacity:80 th. bpd (100% Petrobras)2013 – 36 th. bpd1Q14 – 72 th. bpd

Capacity:120 th. bpd (65% Petrobras)2013 – 10 th. bpd1Q14 – 30 th. bpd

Capacity:140 th. bpd (62.5% Petrobras)

2013 – 1 th. bpd1Q14 – 9 th. bpd

Capacity:180 th. bpd (100% Petrobras)1Q14 – 8 th. bpd

Capacity:180 th. bpd

(100% Petrobras)1Q14 – 2 th. bpd

Petrobras Production Production Operated by Petrobras

Jun 6th

Main factors that impacted production in the 1Q14:

• Demobilization of FPSO Brasil and complete stoppage of Marlim P-20 for 103 days (fire).

• Limited availability of PLSVs, due to the delayed decision of contracting abroad (2010 → 2012), impacting the pace ofinterconnection of wells.

• Delays in the delivery of the platforms by the shipyards.

• Longer time for the execution of innovative projects, such as the BSRs (monobuoys) and systems P-63/P-61/TAD.

2013: 1,931 th. bpd

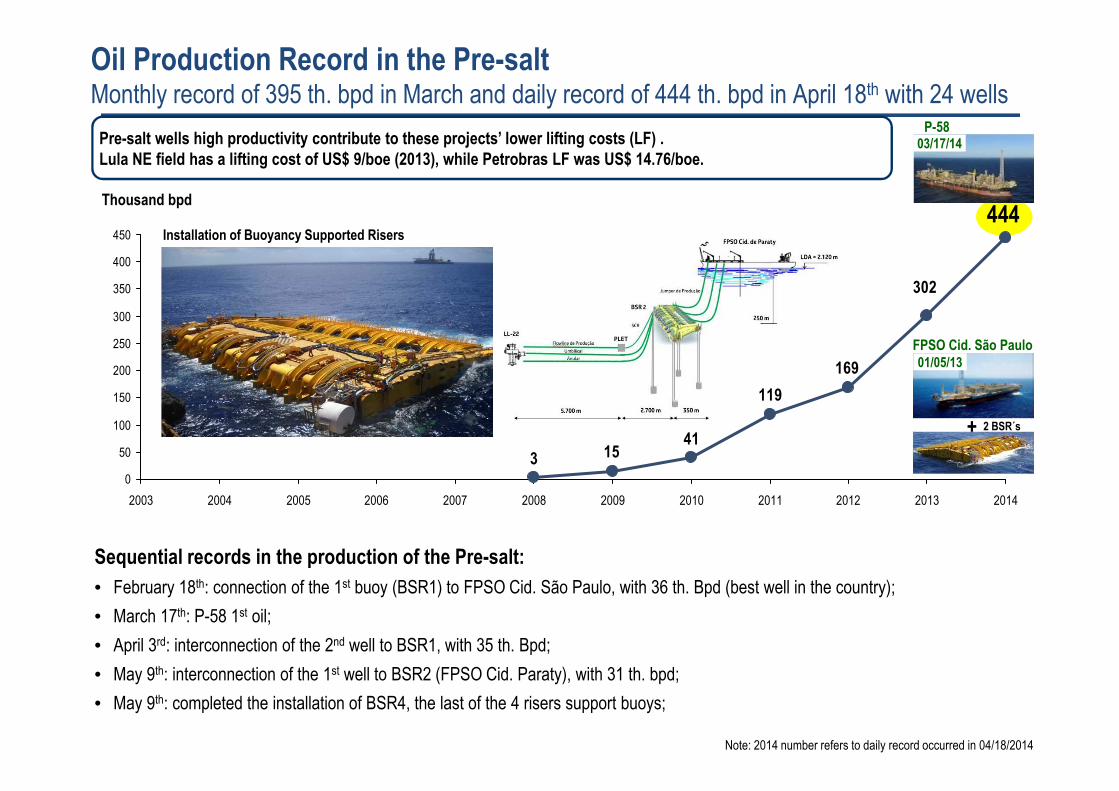

302

169

119

41153

444

0

50

100

150

200

250

300

350

400

450

20122011 2014201320102009200820072006200520042003

Oil Production Record in the Pre-saltMonthly record of 395 th. bpd in March and daily record of 444 th. bpd in April 18th with 24 wells

Thousand bpd

Note: 2014 number refers to daily record occurred in 04/18/2014

P-5803/17/14

FPSO Cid. São Paulo01/05/13

+

Installation of Buoyancy Supported Risers

Pre-salt wells high productivity contribute to these projects’ lower lifting costs (LF) .Lula NE field has a lifting cost of US$ 9/boe (2013), while Petrobras LF was US$ 14.76/boe.

2 BSR´s

Sequential records in the production of the Pre-salt:

• February 18th: connection of the 1st buoy (BSR1) to FPSO Cid. São Paulo, with 36 th. Bpd (best well in the country);

• March 17th: P-58 1st oil;

• April 3rd: interconnection of the 2nd well to BSR1, with 35 th. Bpd;

• May 9th: interconnection of the 1st well to BSR2 (FPSO Cid. Paraty), with 31 th. bpd;

• May 9th: completed the installation of BSR4, the last of the 4 risers support buoys;

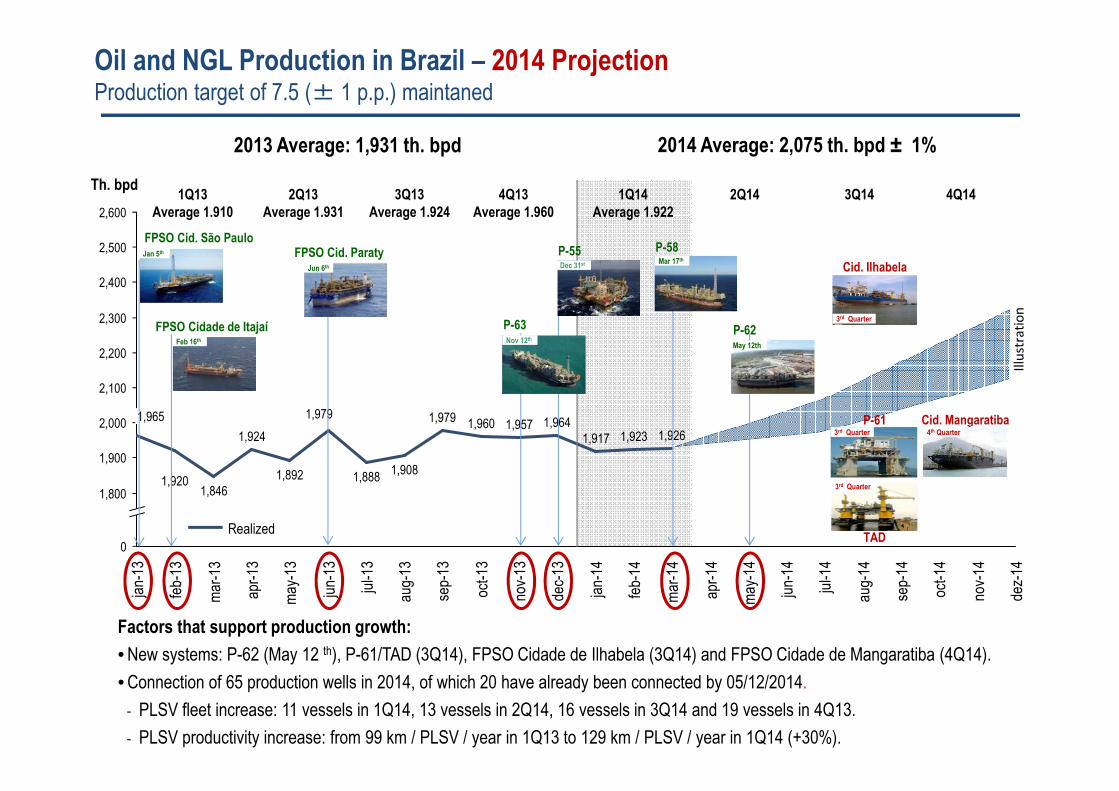

Oil and NGL Production in Brazil – 2014 ProjectionProduction target of 7.5 (± 1 p.p.) maintaned

2Q14 3Q14 4Q14

2014 Average: 2,075 th. bpd ± 1%

Factors that support production growth:

• New systems: P-62 (May 12 th), P-61/TAD (3Q14), FPSO Cidade de Ilhabela (3Q14) and FPSO Cidade de Mangaratiba (4Q14).

• Connection of 65 production wells in 2014, of which 20 have already been connected by 05/12/2014.

- PLSV fleet increase: 11 vessels in 1Q14, 13 vessels in 2Q14, 16 vessels in 3Q14 and 19 vessels in 4Q13.

- PLSV productivity increase: from 99 km / PLSV / year in 1Q13 to 129 km / PLSV / year in 1Q14 (+30%).

Th. bpd

2,400

2,600

2,500

2,300

2,200

2,100

2,000

1,900

1,800

0

jul-1

4

may

-14

aug-

14

jun-

14

apr-

14

oct-

14

dez-

14

nov-

14

sep-

14

mar

-14

1,926

feb-

14

1,923

jan-

14

1,917

dec-

13

1,964

nov-

13

1,957

oct-

13

1,960

sep-

13

1,979au

g-13

1,908

jul-1

3

1,888

jun-

13

1,979

may

-13

1,892

apr-

13

1,924

mar

-13

1,846

feb-

13

1,920

jan-

13

1,965

2Q13Average 1.931

3Q13Average 1.924

4Q13Average 1.960

2013 Average: 1,931 th. bpd

1Q13Average 1.910

1Q14Average 1.922

P-62

Realized

FPSO Cid. São PauloFPSO Cid. Paraty

FPSO Cidade de Itajaí

Jan 5th P-55

P-63

Cid. Ilhabela

Cid. Mangaratiba4th Quarter

3rd Quarter

3rd Quarter

3rd Quarter

P-61

TAD

P-58

May 12th

Jun 6th

Feb 16th Nov 12th

Dec 31st Mar 17th

3rd Quarter

Illustration

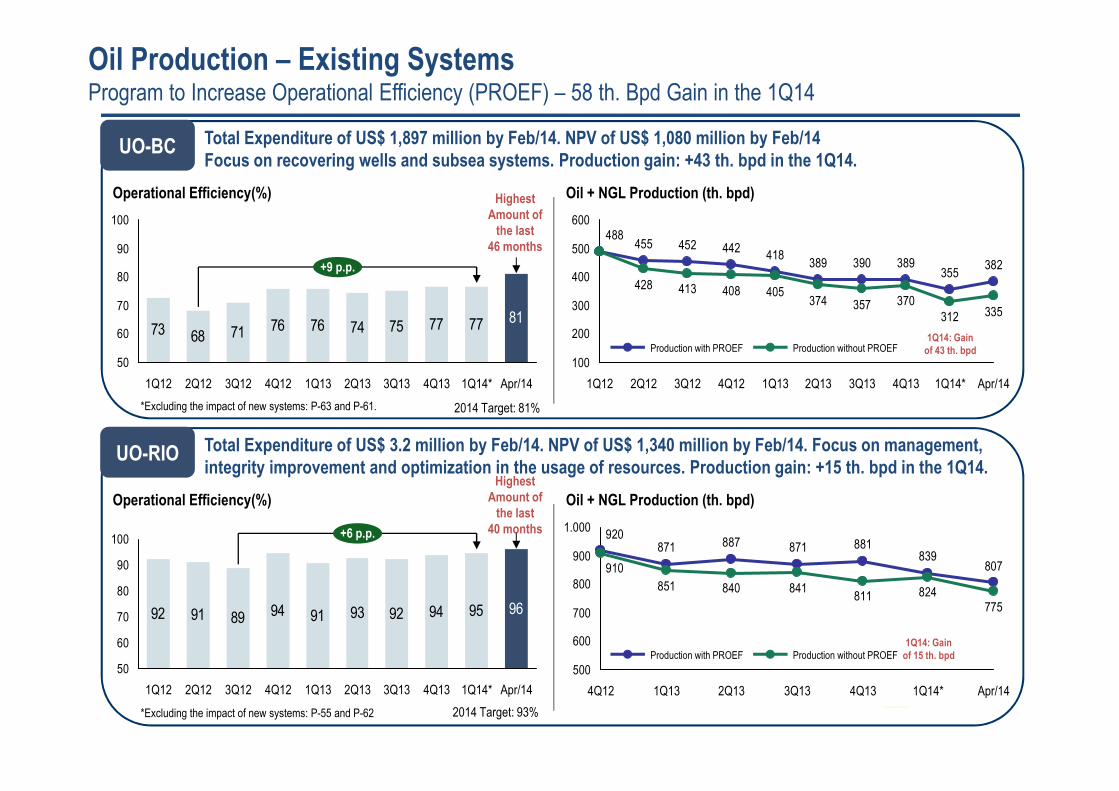

Oil Production – Existing SystemsProgram to Increase Operational Efficiency (PROEF) – 58 th. Bpd Gain in the 1Q14

UO-BC

Oil + NGL Production (th. bpd) Operational Efficiency(%)

73 68 71 76 76 74 75 77 77 81

50

60

70

80

90

100

+9 p.p.

Apr/141Q14*4Q133Q132Q131Q134Q123Q122Q121Q12

382355

389390389418

442452455488

335312370357374

405408413428

100

200

300

400

500

600

Apr/141Q14*4Q133Q132Q131Q134Q123Q122Q121Q12

Production without PROEFProduction with PROEF

Total Expenditure of US$ 1,897 million by Feb/14. NPV of US$ 1,080 million by Feb/14Focus on recovering wells and subsea systems. Production gain: +43 th. bpd in the 1Q14.

*Excluding the impact of new systems: P-63 and P-61.

1Q14: Gainof 43 th. bpd

UO-RIO

Oil + NGL Production (th. bpd) Operational Efficiency(%)

92 91 89 94 91 93 92 94 95 96

50

60

70

80

90

100 +6 p.p.

Apr/141Q14*4Q133Q132Q131Q134Q123Q122Q121Q12

807839

881871887871920

775824811

841840851

910

500

600

700

800

900

1.000

Apr/141Q14*4Q133Q132Q131Q134Q12

Production without PROEFProduction with PROEF

Total Expenditure of US$ 3.2 million by Feb/14. NPV of US$ 1,340 million by Feb/14. Focus on management, integrity improvement and optimization in the usage of resources. Production gain: +15 th. bpd in the 1Q14.

*Excluding the impact of new systems: P-55 and P-62

1Q14: Gainof 15 th. bpd

2014 Target: 93%

2014 Target: 81%

HighestAmount of

the last46 months

HighestAmount of

the last40 months

10

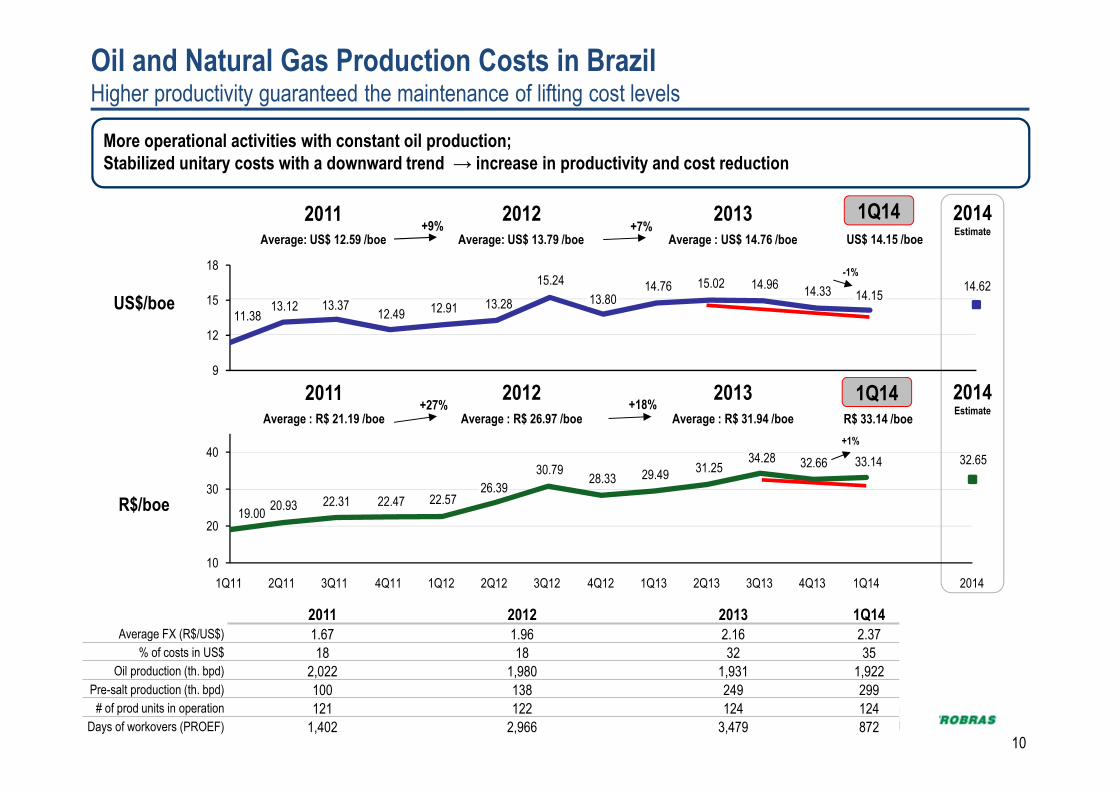

Oil and Natural Gas Production Costs in BrazilHigher productivity guaranteed the maintenance of lifting cost levels

1Q14

More operational activities with constant oil production;Stabilized unitary costs with a downward trend → increase in productivity and cost reduction

11.3813.12

12.49 12.91 13.28

15.24 14.76 15.02 14.9614.33 14.62

9

12

15

18

13.37 13.80 14.15

2012 20132011

19.0020.93 22.31 22.47 22.57

30.7928.33 29.49

31.2534.28 32.66 33.14 32.65

10

20

30

40

2Q124Q113Q11 1Q122Q111Q11 3Q12

26.39

20141Q144Q133Q132Q131Q134Q12

US$/boe

2014Estimate

R$/boe

Average: US$ 12.59 /boe Average: US$ 13.79 /boe Average : US$ 14.76 /boe+9% +7%

US$ 14.15 /boe

2012 20132011 2014Estimate

Average : R$ 21.19 /boe Average : R$ 26.97 /boe Average : R$ 31.94 /boe+27% +18%

R$ 33.14 /boe

2011 2012 2013 1Q14Average FX (R$/US$) 1.67 1.96 2.16 2.37

% of costs in US$ 18 18 32 35Oil production (th. bpd) 2,022 1,980 1,931 1,922

Pre-salt production (th. bpd) 100 138 249 299# of prod units in operation 121 122 124 124

Days of workovers (PROEF) 1,402 2,966 3,479 872

1Q14

-1%

+1%

11

Oil products output in Brazil1Q14 production 1% above 4Q13. Sales dropped 2.2% in the period (seasonality)

1Q14 x 4Q13

• Lower diesel and gasoline production, mainly due toREPLAN’s scheduled stoppage.

• Higher utilization factor (from 95% to 96%) and highershare of Brazilian oil in throughput (+21 th.bpd).

Oil products output

0%

839 841 822

453 499 483

288 248 290

197 211 208

1251281409286113

1059198

2,127

1Q13

+1%

1Q14

2,124

4Q13

2,105

-2,2%

-3,2%

Oil products sales – Brazil

LPG Diesel

Gasoline

Jet Fuel

NaphthaFuel Oil

Others*

(th. bpd)(th. bpd)

921 947

580610 601

213235 222

196204 202

178164180

111108105

11011899

1Q14

2,371

-2.2%

4Q13

2,425

1,005

1Q13

2,313

+2.5%

-5,8%

-1,5%

1Q14 x 4Q13

• Diesel (-58 th. bpd): Seasonality effect, offset by higherdiesel consumption in thermal power plants. 4Q has higherindustrial production and planting of crops, whereas in the 1Qthere is a reduction in retail and industry sales.

• LPG (-13 th. bpd): Higher temperatures in 1Q14 and holidayseason reduce LPG consumption.(*) Others – Lubricants, Asphalt, Coke, Propene, Solvent, Benzene, Kerosene and Intermediates.

12

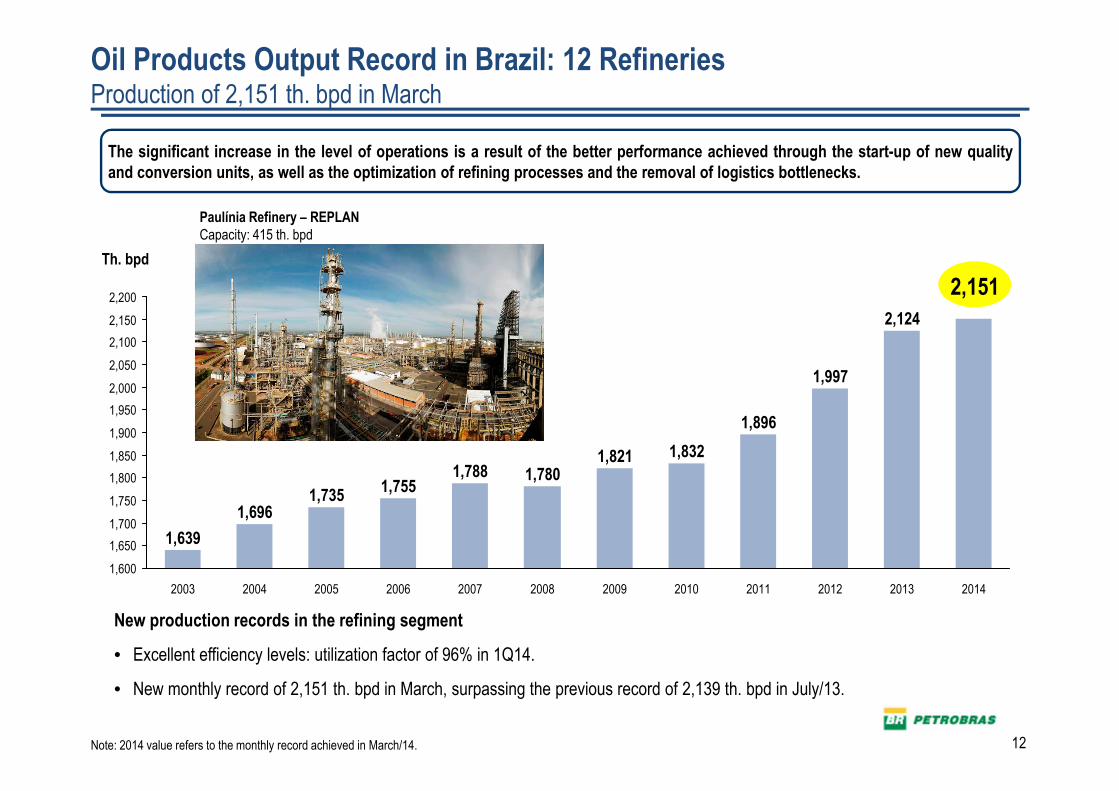

Oil Products Output Record in Brazil: 12 RefineriesProduction of 2,151 th. bpd in March

2,200

2,150

2,100

2,050

2,000

1,950

1,900

1,850

1,800

1,750

1,700

1,650

1,600

20142013

2,124

2012

1,997

2011

1,896

2010

1,832

2009

1,821

2008

1,780

2007

1,788

2006

1,755

2005

1,735

2004

1,696

2003

1,639

Note: 2014 value refers to the monthly record achieved in March/14.

Th. bpd

2,151

New production records in the refining segment

• Excellent efficiency levels: utilization factor of 96% in 1Q14.

• New monthly record of 2,151 th. bpd in March, surpassing the previous record of 2,139 th. bpd in July/13.

Paulínia Refinery – REPLANCapacity: 415 th. bpd

The significant increase in the level of operations is a result of the better performance achieved through the start-up of new qualityand conversion units, as well as the optimization of refining processes and the removal of logistics bottlenecks.

13

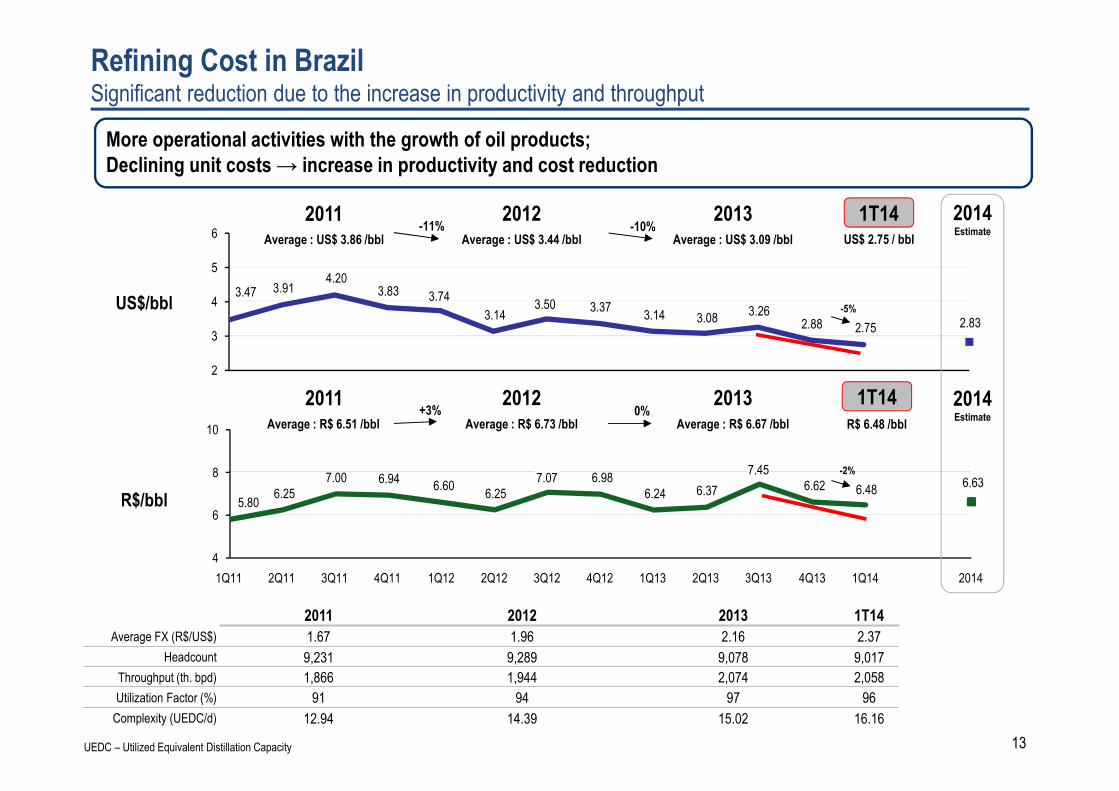

3.47 3.914.20

3.83

3.143.37

3.14 3.083.26

2.88 2.75 2.83

2

3

4

5

6

3.503.74

2012 20132011

5.806.25

7.00 6.946.60

6.256.98

6.24 6.37 6.62 6.486.63

4

6

8

10

4Q13 1Q14 20141Q134Q123Q12

7.07

2Q121Q124Q113Q112Q111Q11

7.45

3Q132Q13

US$/bbl

R$/bbl

Average : US$ 3.86 /bbl Average : US$ 3.44 /bbl Average : US$ 3.09 /bbl-11% -10%

US$ 2.75 / bbl

2012 20132011Average : R$ 6.51 /bbl Average : R$ 6.73 /bbl Average : R$ 6.67 /bbl

+3% 0%R$ 6.48 /bbl

Refining Cost in BrazilSignificant reduction due to the increase in productivity and throughput

More operational activities with the growth of oil products;Declining unit costs → increase in productivity and cost reduction

2011 2012 2013 1T14

Average FX (R$/US$) 1.67 1.96 2.16 2.37

Headcount 9,231 9,289 9,078 9,017

Throughput (th. bpd) 1,866 1,944 2,074 2,058

Utilization Factor (%) 91 94 97 96

Complexity (UEDC/d) 12.94 14.39 15.02 16.16

1T14

1T14

-5%

-2%

2014Estimate

2014Estimate

UEDC – Utilized Equivalent Distillation Capacity

14

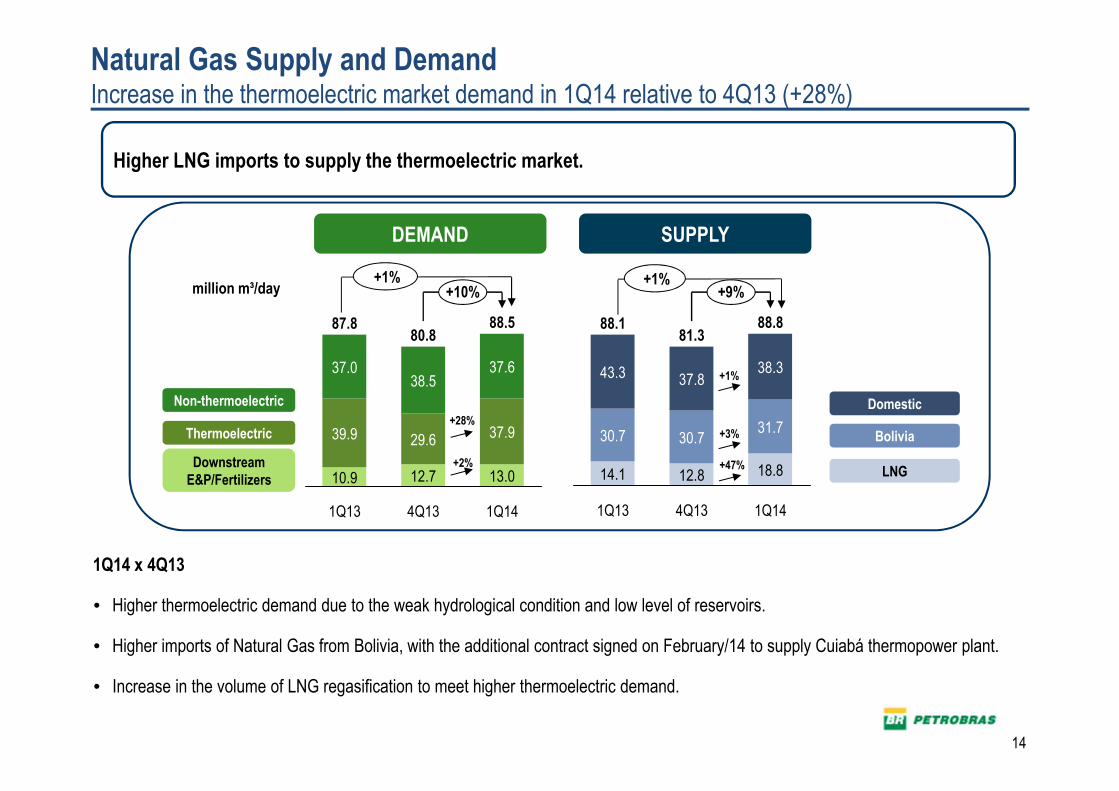

Natural Gas Supply and DemandIncrease in the thermoelectric market demand in 1Q14 relative to 4Q13 (+28%)

Higher LNG imports to supply the thermoelectric market.

1Q14 x 4Q13

• Higher thermoelectric demand due to the weak hydrological condition and low level of reservoirs.

• Higher imports of Natural Gas from Bolivia, with the additional contract signed on February/14 to supply Cuiabá thermopower plant.

• Increase in the volume of LNG regasification to meet higher thermoelectric demand.

million m³/day

SUPPLYDEMAND

40,2

37,0

11,7

39,3

+1% +1% +10%

1Q14

88.5

13.0

37.9

37.6

4Q13

80.8

12.7

29.6

38.5

1Q13

87.8

10.9

39.9

37.0 38.3

4Q13

88.8

18.8

31.7

+9%

1Q14

81.3

12.8

30.7

37.8

1Q13

88.1

14.1

30.7

43.3

+28%

+2%

+3%

+47%

+1%

39,9

Non-thermoelectric

Thermoelectric

Downstream E&P/Fertilizers

Domestic

Bolivia

LNG

15

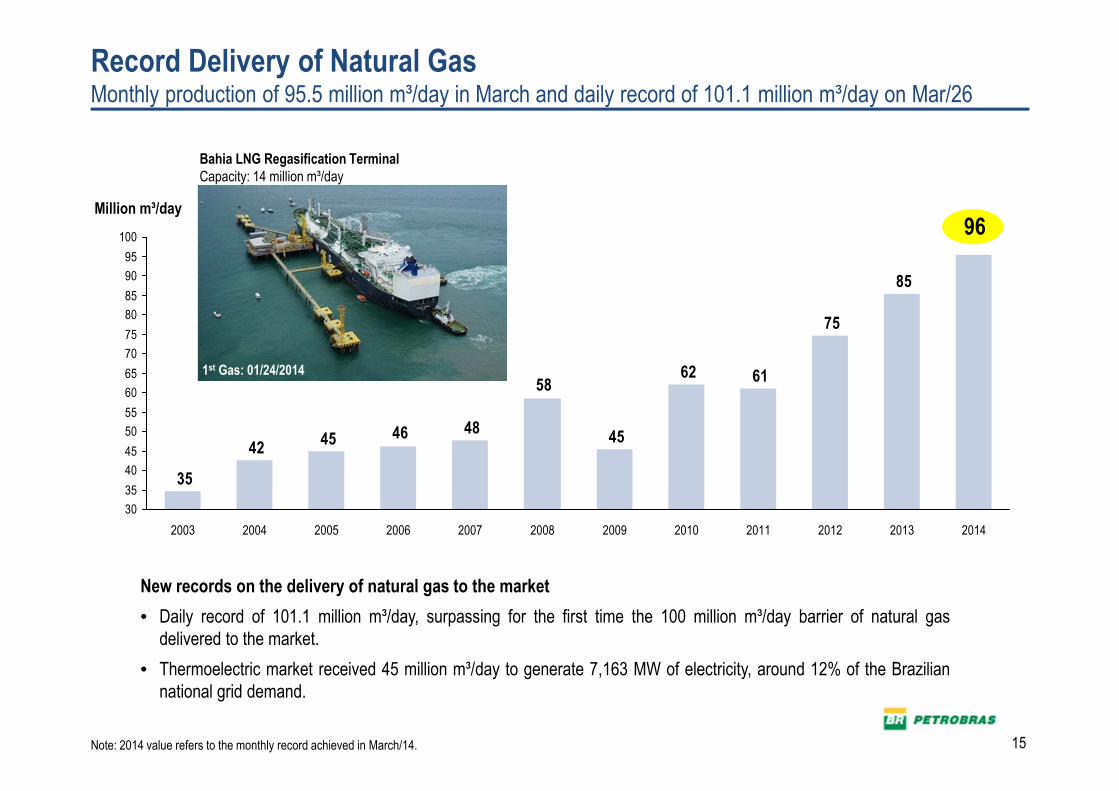

Record Delivery of Natural GasMonthly production of 95.5 million m³/day in March and daily record of 101.1 million m³/day on Mar/26

85

75

6162

45

58

48464542

35

30

35

40

45

50

55

60

65

70

75

80

85

90

95

100

201420132012201120102009200820072006200520042003

Note: 2014 value refers to the monthly record achieved in March/14.

Million m³/day

96

New records on the delivery of natural gas to the market

• Daily record of 101.1 million m³/day, surpassing for the first time the 100 million m³/day barrier of natural gasdelivered to the market.

• Thermoelectric market received 45 million m³/day to generate 7,163 MW of electricity, around 12% of the Braziliannational grid demand.

Bahia LNG Regasification TerminalCapacity: 14 million m³/day

1st Gas: 01/24/2014

16

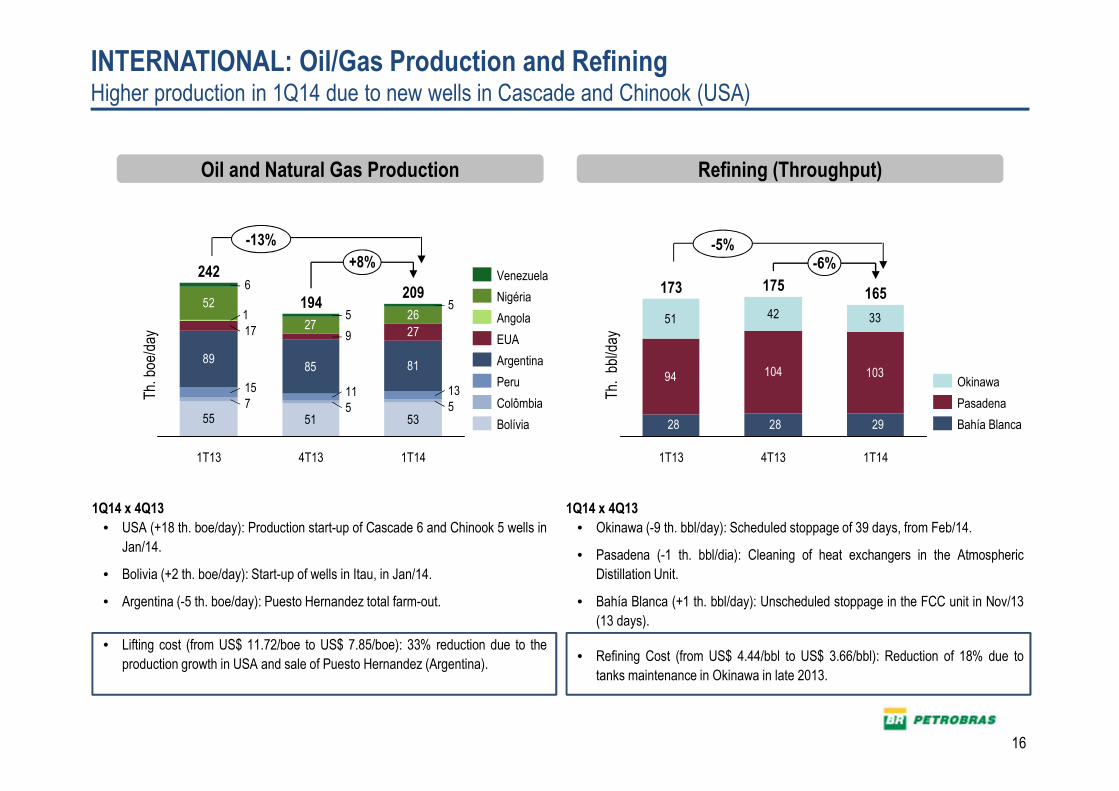

INTERNATIONAL: Oil/Gas Production and RefiningHigher production in 1Q14 due to new wells in Cascade and Chinook (USA)

Oil and Natural Gas Production Refining (Throughput)

Th.

bbl

/day

94 104 103

51 42 33

292828

-6%

1T14

165

4T13

175

1T13

173

Bahía Blanca

Pasadena

Okinawa

-5%

1Q14 x 4Q13

• USA (+18 th. boe/day): Production start-up of Cascade 6 and Chinook 5 wells in

Jan/14.

• Bolivia (+2 th. boe/day): Start-up of wells in Itau, in Jan/14.

• Argentina (-5 th. boe/day): Puesto Hernandez total farm-out.

• Lifting cost (from US$ 11.72/boe to US$ 7.85/boe): 33% reduction due to the

production growth in USA and sale of Puesto Hernandez (Argentina).

1Q14 x 4Q13

• Okinawa (-9 th. bbl/day): Scheduled stoppage of 39 days, from Feb/14.

• Pasadena (-1 th. bbl/dia): Cleaning of heat exchangers in the Atmospheric

Distillation Unit.

• Bahía Blanca (+1 th. bbl/day): Unscheduled stoppage in the FCC unit in Nov/13

(13 days).

• Refining Cost (from US$ 4.44/bbl to US$ 3.66/bbl): Reduction of 18% due to

tanks maintenance in Okinawa in late 2013.

55 51 53

8985 81

52

2726

557131115

917 27

15

5

6

+8%

1T14

209

4T13

194

1T13

242

Bolívia

Colômbia

Peru

Argentina

EUA

Angola

Nigéria

Venezuela

Th.

boe

/day

-13%

17

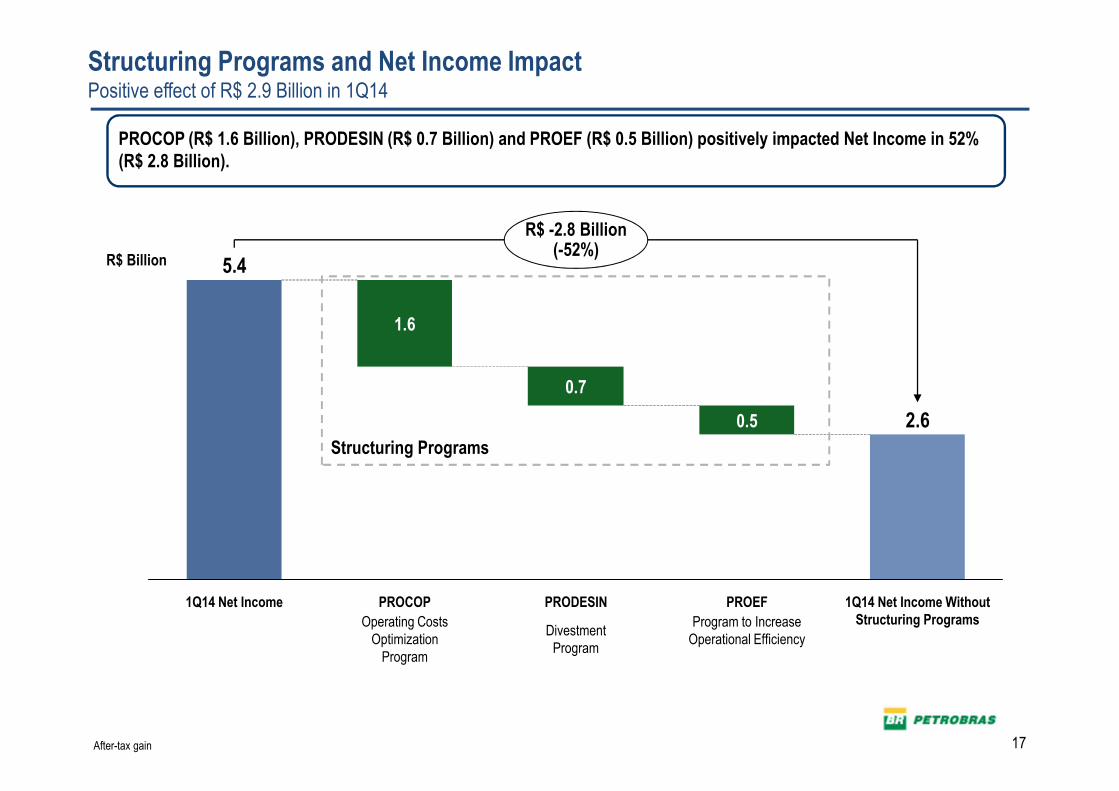

Structuring Programs and Net Income ImpactPositive effect of R$ 2.9 Billion in 1Q14

0.5

PRODESIN

0.7

PROCOP

1.6

1Q14 Net Income

5.4

R$ -2.8 Billion(-52%)

1Q14 Net Income Without Structuring Programs

2.6

PROEF

R$ Billion

PROCOP (R$ 1.6 Billion), PRODESIN (R$ 0.7 Billion) and PROEF (R$ 0.5 Billion) positively impacted Net Income in 52% (R$ 2.8 Billion).

Structuring Programs

Divestment Program

Operating Costs Optimization

Program

Program to IncreaseOperational Efficiency

After-tax gain

18

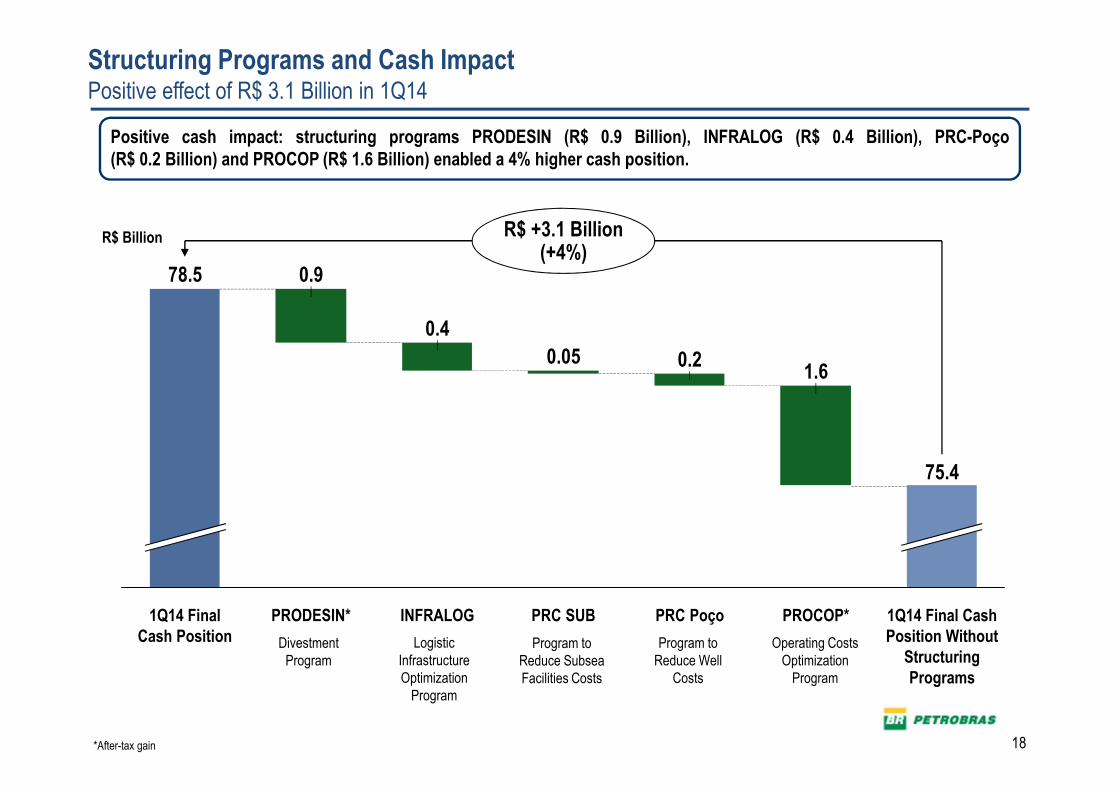

Positive cash impact: structuring programs PRODESIN (R$ 0.9 Billion), INFRALOG (R$ 0.4 Billion), PRC-Poço(R$ 0.2 Billion) and PROCOP (R$ 1.6 Billion) enabled a 4% higher cash position.

INFRALOG

0.4

PRODESIN*

0.9

PROCOP* 1Q14 Final Cash Position Without

Structuring Programs

0.2

PRC SUB PRC Poço

R$ +3.1 Billion (+4%)

1.6

75.4

78.5

1Q14 Final Cash Position

0.05

*After-tax gain

R$ Billion

Structuring Programs and Cash ImpactPositive effect of R$ 3.1 Billion in 1Q14

Divestment Program

Program to Reduce Subsea Facilities Costs

Program to Reduce Well

Costs

Operating Costs Optimization

Program

Logistic Infrastructure Optimization

Program

19

3,52

4,00

39% 39%

-10%

0%

10%

20%

30%

40%

50%

1,5

2,5

3,5

4,5

4Q13 1Q14

Net Debt / EBITDA ¹Net Debt / Net Capitalization ²

LEV

ER

AG

E

ND

/ EB

ITD

A

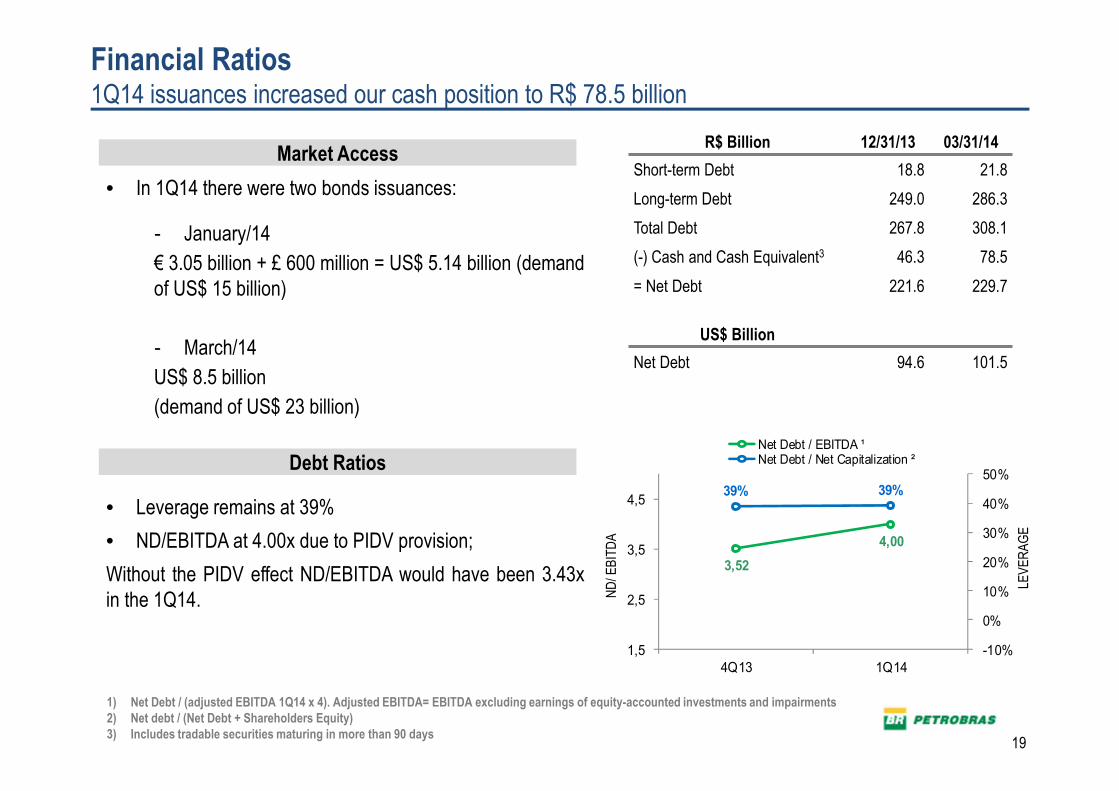

Financial Ratios1Q14 issuances increased our cash position to R$ 78.5 billion

• In 1Q14 there were two bonds issuances:

- January/14

€ 3.05 billion + £ 600 million = US$ 5.14 billion (demandof US$ 15 billion)

- March/14

US$ 8.5 billion

(demand of US$ 23 billion)

• Leverage remains at 39%

• ND/EBITDA at 4.00x due to PIDV provision;

Without the PIDV effect ND/EBITDA would have been 3.43xin the 1Q14.

Market Access

Debt Ratios

R$ Billion 12/31/13 03/31/14

Short-term Debt 18.8 21.8

Long-term Debt 249.0 286.3

Total Debt 267.8 308.1

(-) Cash and Cash Equivalent3 46.3 78.5

= Net Debt 221.6 229.7

US$ Billion

Net Debt 94.6 101.5

1) Net Debt / (adjusted EBITDA 1Q14 x 4). Adjusted EBITDA= EBITDA excluding earnings of equity-accounted investments and impairments 2) Net debt / (Net Debt + Shareholders Equity)3) Includes tradable securities maturing in more than 90 days

20

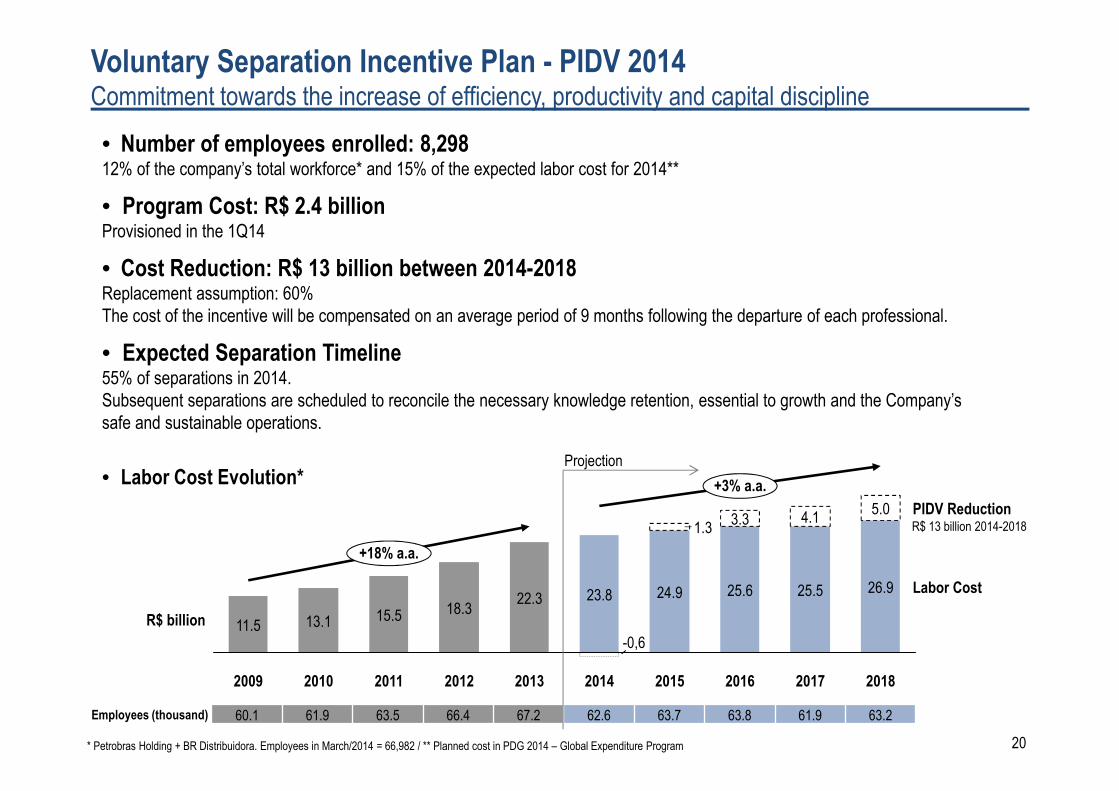

• Number of employees enrolled: 8,29812% of the company’s total workforce* and 15% of the expected labor cost for 2014**

• Program Cost: R$ 2.4 billionProvisioned in the 1Q14

• Cost Reduction: R$ 13 billion between 2014-2018Replacement assumption: 60% The cost of the incentive will be compensated on an average period of 9 months following the departure of each professional.

• Expected Separation Timeline55% of separations in 2014. Subsequent separations are scheduled to reconcile the necessary knowledge retention, essential to growth and the Company’s safe and sustainable operations.

• Labor Cost Evolution*

* Petrobras Holding + BR Distribuidora. Employees in March/2014 = 66,982 / ** Planned cost in PDG 2014 – Global Expenditure Program

Voluntary Separation Incentive Plan - PIDV 2014Commitment towards the increase of efficiency, productivity and capital discipline

2009

11.5

2010

13.118.3

2011

15.5

PIDV Reduction

26.9

2012

+3% a.a.

5.0

2015

25.6

2016

25.524.9

4.13.3

Labor Cost

2017

+18% a.a.

2018

1.3

2014

23.8

2013

22.3

R$ billion

Employees (thousand) 60.1 61.9 63.5 66.4 67.2 62.6 63.7 63.8 61.9 63.2

R$ 13 billion 2014-2018

-0,6

Projection

21

Information:

Investor Relations

+55 21 3224-1510

OPERATIONAL AND FINANCIAL RESULTS1st Quarter 2014__