was added which the “extended use requirement,” … · randall will discuss the approach of the...

TRANSCRIPT

LIHTC COMPLIANCE AFTER THE COMPLIANCE PERIOD: ONCE THE CREDITS ARE GONE

INTRODUCTION

Section 42 was enacted in 1986, and in 1989, Sec. 42(h)(6) (reprinted below) was added which the “extended use requirement,” obligating all LIHTC project to be subject to an affordability covenant lasting at least 30 years (i.e., for the 15-year Compliance Period, plus an additional 15 years). This panel will discuss various policy, legal and practical aspects of the extended use requirement.

* * * * * * * * A. Laura Abernathy. Not surprisingly, extended use restrictions can have a substantial effect on future affordability of housing developed under the Housing Credit program. Extended restrictions prevent an escalating loss of affordability and allow the assisted stock to grow, ensuring that units remain affordable to low-income families in the long term. Starting with the general policy considerations of long-term affordability, Laura will explore the various ways in which Housing Finance Agencies use their Qualified Allocation Plans to incentivize and in some cases require affordability beyond the federally mandated 30 years. The topic of qualified contracts and how this relates to long-term affordability will also introduced; the presentation will explore the trend among HFAs of requiring Housing Credit applicants to waive their rights to a qualified contract. B. Mark Shelburne. Mark will discuss the legal context of two ways to terminate the extended use period. Owners across the country continue to request qualified contacts, which is the start of a complex process. Mark will explain some of the specific statutory provisions, including both calculation of the statutory “price” and process for handling requests. He also will discuss whether QCs lead to significant numbers of sales. Fortunately foreclosures are a far less frequent way out of extended use. The rate for LIHTC properties is lower than for any other form of real estate. However, even with these small numbers, there is a concern with how they could occur. In a few isolated instances, foreclosures appear to have been planned as a way to end affordability. Mark will describe these and a proposal in the recently filed Affordable Housing Credit Improvement Act legislation (aka Cantwell-Hatch) to address this potential problem. C. Katie Day. It is not uncommon for developers of affordable housing projects to seek to modify the terms of the extended use agreement prior to its expiration, e.g., an amendment that relaxes or reduces affordability requirements. Some credit agencies have been willing to entertain these requests. However, it’s not clear that credit agencies have the authority to make these modifications, particularly in light of the statutory language of Section 42(h)(6)(B)(ii) of the Code, which allows former, current and prospective tenants who meet the income eligibility requirements to enforce the provisions of the extended use agreement and the decision of the Oregon Court of Appeals in Nordbye v. BRCP/GM Ellington (holding that a former tenant of a low-income

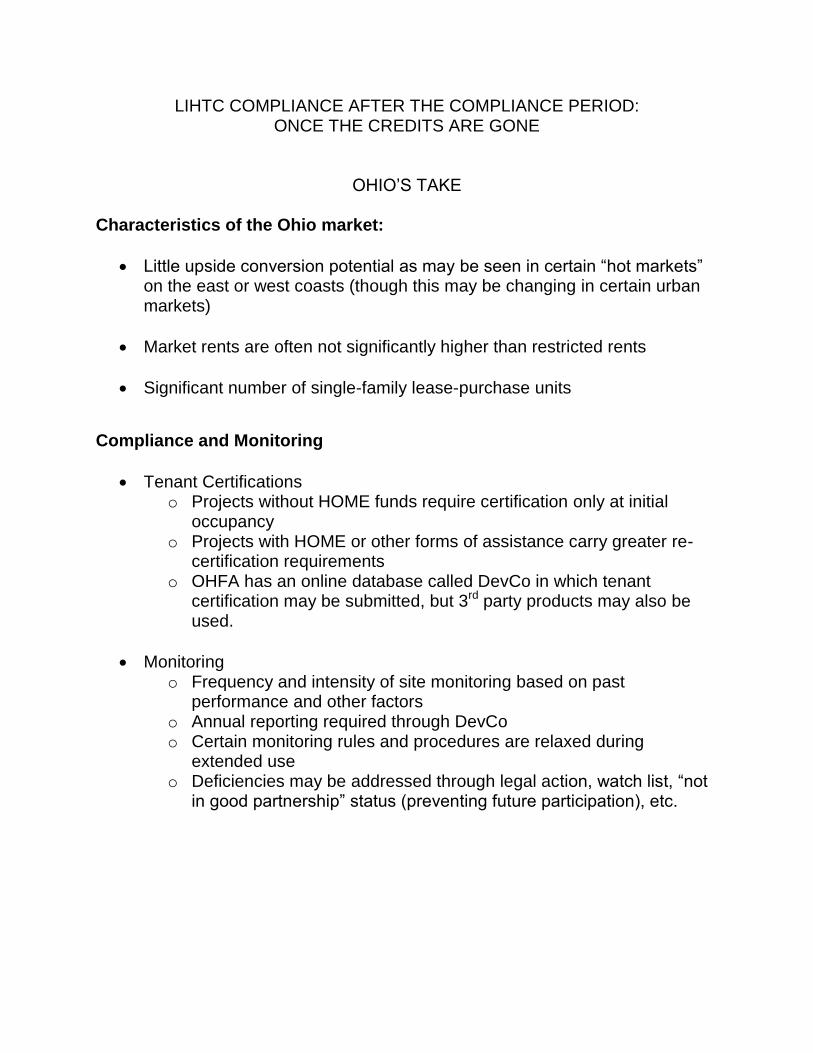

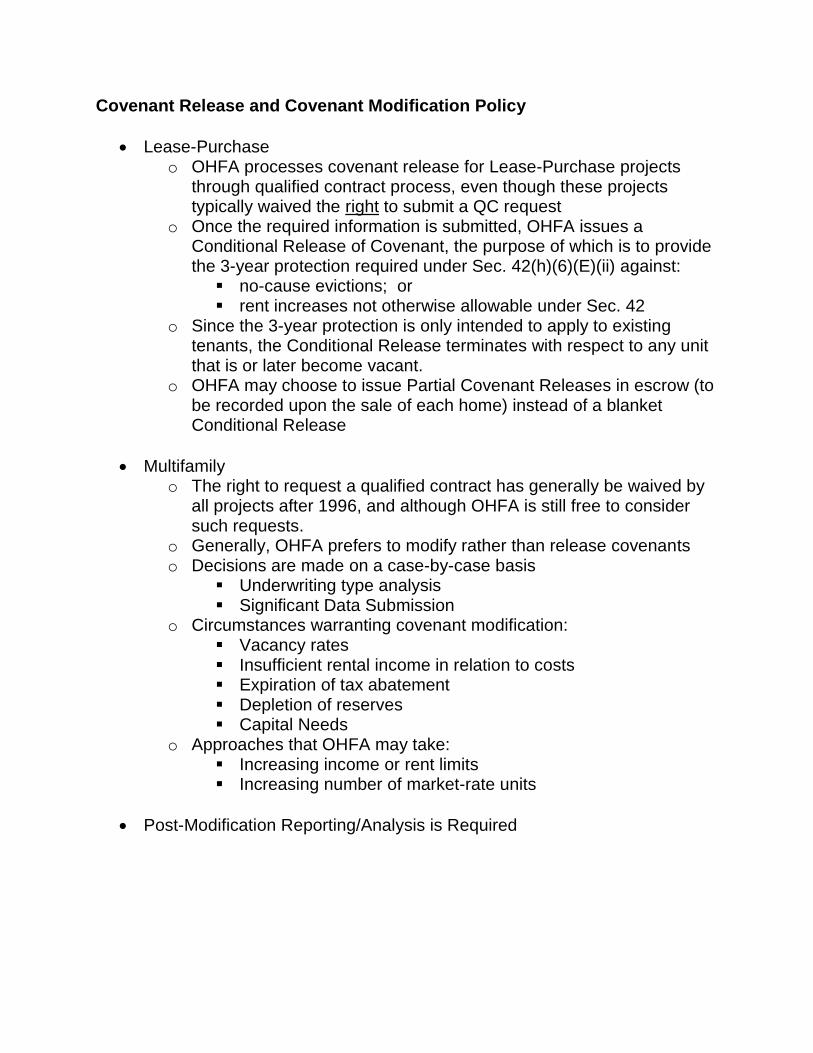

housing project has the right to enforce an extended use commitment despite a release agreement between the owner of the project and the state housing credit agency to terminate the agreement early). D. Randall Shorr. Randall will discuss the approach of the Ohio Housing Finance Agency (“OHFA”) to these issues, including its post-Year 15 monitoring requirements, its handling of qualified contract requests and its policies relating to requests for amending the LURA. Ohio has a significant portfolio of single-family lease purchase units, and of course the covenant must be released in order to deliver clear title to lease-purchase buyers, which still providing protections to renters who remain in these projects. Many multifamily projects reaching the end of the compliance period are facing severe financial challenges, and OHFA has developed a set of policies for considering requests for modifications to affordability covenants to allow these projects to remain financially viable.

* * * * * * * *

§42(h)(6) Buildings eligible for credit only if minimum long-term

commitment to low-income housing

(A) In general

No credit shall be allowed by reason of this section with respect to any

building for the taxable year unless an extended low-income housing

commitment is in effect as of the end of such taxable year.

(B) Extended low-income housing commitment

For purposes of this paragraph, the term "extended low-income housing

commitment" means any agreement between the taxpayer and the housing

credit agency -

(i) which requires that the applicable fraction (as defined in subsection

(c)(1)) for the building for each taxable year in the extended use period

will not be less than the applicable fraction specified in such agreement

and which prohibits the actions described in subclauses (I) and (II) of

subparagraph (E)(ii),

(ii) which allows individuals who meet the income limitation applicable to

the building under subsection (g) (whether prospective, present, or

former occupants of the building) the right to enforce in any State court

the requirement and prohibitions of clause (i),

(iii) which prohibits the disposition to any person of any portion of the

building to which such agreement applies unless all of the building to

which such agreement applies is disposed of to such person,

(iv) which prohibits the refusal to lease to a holder of a voucher or

certificate of eligibility under section 8 of the United States Housing Act

of 1937 because of the status of the prospective tenant as such a holder,

(v) which is binding on all successors of the taxpayer, and

(vi) which, with respect to the property, is recorded pursuant to State law as

a restrictive covenant.

(C) Allocation of credit may not exceed amount necessary to

support commitment

(i) In general

The housing credit dollar amount allocated to any building may not

exceed the amount necessary to support the applicable fraction specified

in the extended low-income housing commitment for such building,

including any increase in such fraction pursuant to the application of

subsection (f)(3) if such increase is reflected in an amended low-income

housing commitment.

(ii) Buildings financed by tax-exempt bonds

If paragraph (4) applies to any building the amount of credit allowed in

any taxable year may not exceed the amount necessary to support the

applicable fraction specified in the extended low-income housing

commitment for such building. Such commitment may be amended to

increase such fraction.

(D) Extended use period

For purposes of this paragraph, the term "extended use period" means the

period -

(i) beginning on the 1st day in the compliance period on which such

building is part of a qualified low-income housing project, and

(ii) ending on the later of -

(I) the date specified by such agency in such agreement, or

(II) the date which is 15 years after the close of the compliance period.

(E) Exceptions if foreclosure or if no buyer willing to

maintain low-income status

(i) In general

The extended use period for any building shall terminate -

(I) on the date the building is acquired by foreclosure (or instrument in

lieu of foreclosure) unless the Secretary determines that such

acquisition is part of an arrangement with the taxpayer a purpose of

which is to terminate such period, or

(II) on the last day of the period specified in subparagraph (I) if the

housing credit agency is unable to present during such period a

qualified contract for the acquisition of the low-income portion of

the building by any person who will continue to operate such

portion as a qualified low-income building. Subclause (II) shall not

apply to the extent more stringent requirements are provided in the

agreement or in State law.

(ii) Eviction, etc. of existing low-income tenants not

permitted

The termination of an extended use period under clause (i) shall not be

construed to permit before the close of the 3-year period following such

termination -

(I) the eviction or the termination of tenancy (other than for good

cause) of an existing tenant of any low-income unit, or

(II) any increase in the gross rent with respect to such unit not

otherwise permitted under this section.

(F) Qualified contract

For purposes of subparagraph (E), the term "qualified contract" means a bona

fide contract to acquire (within a reasonable period after the contract is entered

into) the nonlow-income portion of the building for fair market value and the

low-income portion of the building for an amount not less than the applicable

fraction (specified in the extended low-income housing commitment) of -

(i) the sum of -

(I) the outstanding indebtedness secured by, or with respect to, the

building,

(II) the adjusted investor equity in the building, plus

(III) other capital contributions not reflected in the amounts described

in subclause (I) or (II), reduced by

(ii) cash distributions from (or available for distribution from) the project.

The Secretary shall prescribe such regulations as may be necessary or

appropriate to carry out this paragraph, including regulations to prevent

the manipulation of the amount determined under the preceding

sentence.

(G) Adjusted investor equity

(i) In general

For purposes of subparagraph (E), the term "adjusted investor equity"

means, with respect to any calendar year, the aggregate amount of cash

taxpayers invested with respect to the project increased by the amount

equal to -

(I) such amount, multiplied by

(II) the cost-of-living adjustment for such calendar year, determined

under section 1(f)(3) by substituting the base calendar year for

"calendar year 1987". An amount shall be taken into account as an

investment in the project only to the extent there was an obligation

to invest such amount as of the beginning of the credit period and

to the extent such amount is reflected in the adjusted basis of the

project.

(ii) Cost-of-living increases in excess of 5 percent not

taken into account

Under regulations prescribed by the Secretary, if the CPI for any

calendar year (as defined in section 1(f)(4)) exceeds the CPI for the

preceding calendar year by more than 5 percent, the CPI for the base

calendar year shall be increased such that such excess shall never be

taken into account under clause (i).

(iii) Base calendar year

For purposes of this subparagraph, the term "base calendar year" means

the calendar year with or within which the 1st taxable year of the credit

period ends.

(H) Low-income portion

For purposes of this paragraph, the low-income portion of a building is the

portion of such building equal to the applicable fraction specified in the

extended low-income housing commitment for the building.

(I) Period for finding buyer

The period referred to in this subparagraph is the 1-year period beginning on

the date (after the 14th year of the compliance period) the taxpayer submits a

written request to the housing credit agency to find a person to acquire the

taxpayer's interest in the low-income portion of the building.

(J) Effect of noncompliance

If, during a taxable year, there is a determination that an extended low-income

housing agreement was not in effect as of the beginning of such year, such

determination shall not apply to any period before such year and subparagraph

(A) shall be applied without regard to such determination if the failure is

corrected within 1 year from the date of the determination.

(K) Projects which consist of more than 1 building

The application of this paragraph to projects which consist of more than 1

building shall be made under regulations prescribed by the Secretary.

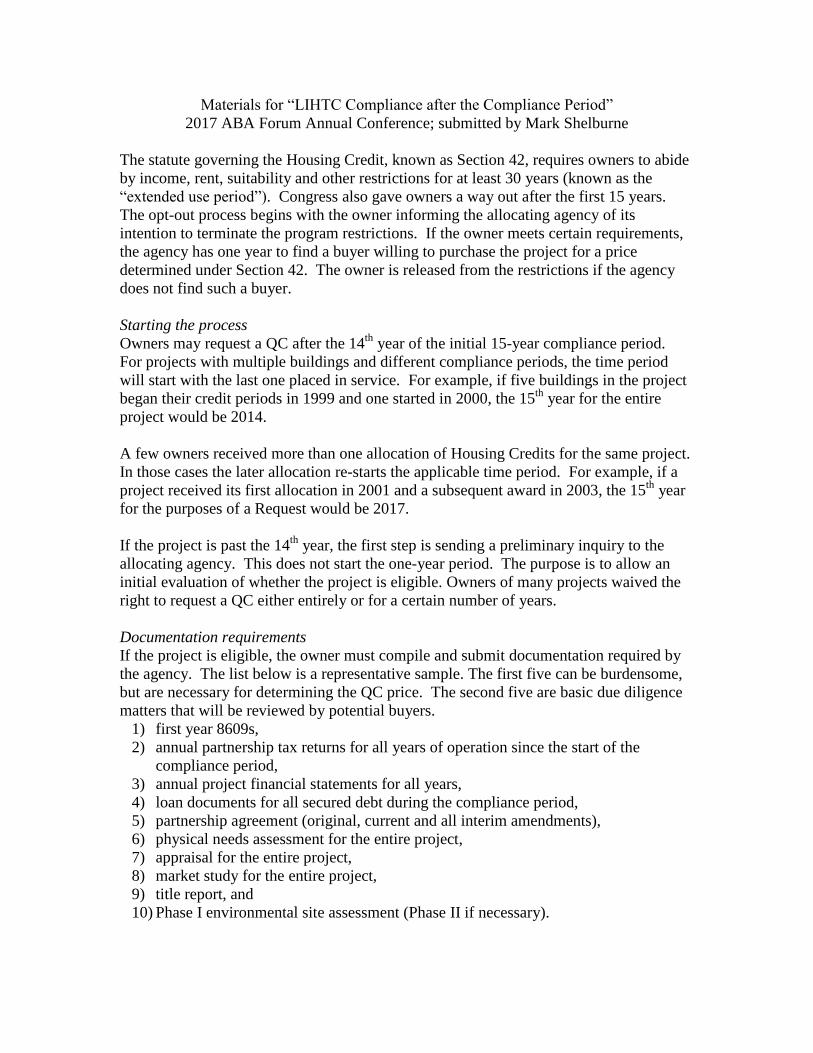

Materials for “LIHTC Compliance after the Compliance Period”

2017 ABA Forum Annual Conference; submitted by Mark Shelburne

The statute governing the Housing Credit, known as Section 42, requires owners to abide

by income, rent, suitability and other restrictions for at least 30 years (known as the

“extended use period”). Congress also gave owners a way out after the first 15 years.

The opt-out process begins with the owner informing the allocating agency of its

intention to terminate the program restrictions. If the owner meets certain requirements,

the agency has one year to find a buyer willing to purchase the project for a price

determined under Section 42. The owner is released from the restrictions if the agency

does not find such a buyer.

Starting the process

Owners may request a QC after the 14th

year of the initial 15-year compliance period.

For projects with multiple buildings and different compliance periods, the time period

will start with the last one placed in service. For example, if five buildings in the project

began their credit periods in 1999 and one started in 2000, the 15th

year for the entire

project would be 2014.

A few owners received more than one allocation of Housing Credits for the same project.

In those cases the later allocation re-starts the applicable time period. For example, if a

project received its first allocation in 2001 and a subsequent award in 2003, the 15th

year

for the purposes of a Request would be 2017.

If the project is past the 14th

year, the first step is sending a preliminary inquiry to the

allocating agency. This does not start the one-year period. The purpose is to allow an

initial evaluation of whether the project is eligible. Owners of many projects waived the

right to request a QC either entirely or for a certain number of years.

Documentation requirements

If the project is eligible, the owner must compile and submit documentation required by

the agency. The list below is a representative sample. The first five can be burdensome,

but are necessary for determining the QC price. The second five are basic due diligence

matters that will be reviewed by potential buyers.

1) first year 8609s,

2) annual partnership tax returns for all years of operation since the start of the

compliance period,

3) annual project financial statements for all years,

4) loan documents for all secured debt during the compliance period,

5) partnership agreement (original, current and all interim amendments),

6) physical needs assessment for the entire project,

7) appraisal for the entire project,

8) market study for the entire project,

9) title report, and

10) Phase I environmental site assessment (Phase II if necessary).

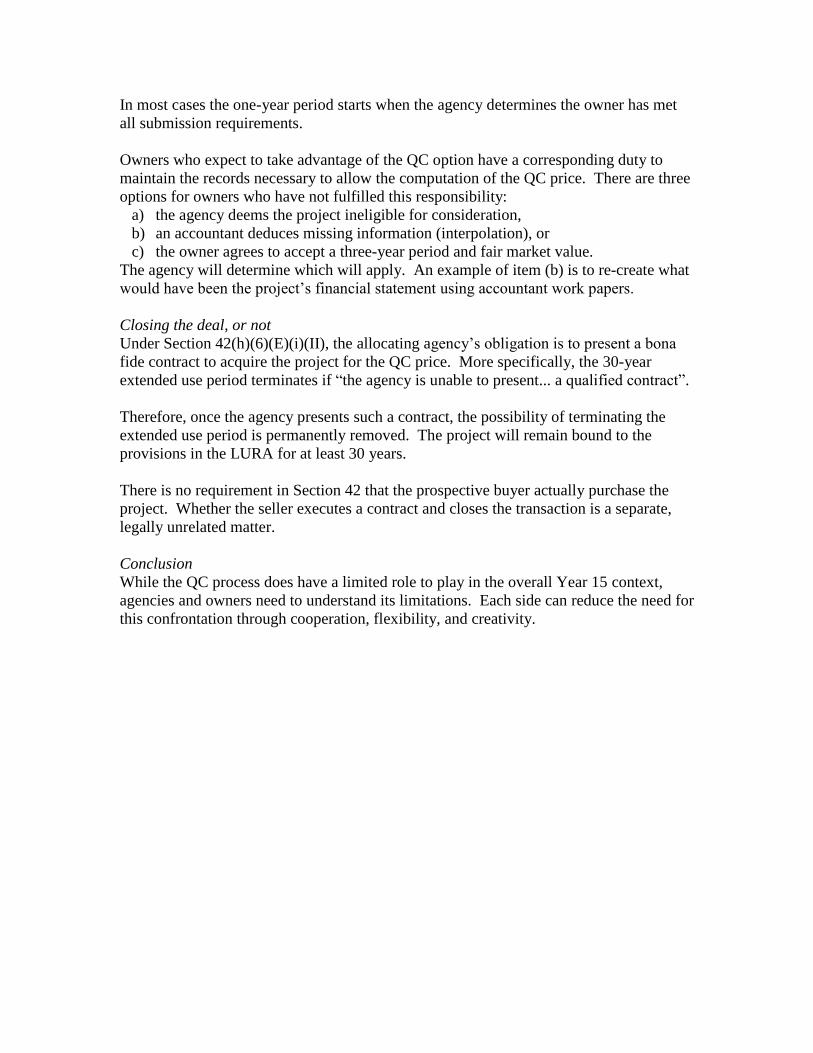

In most cases the one-year period starts when the agency determines the owner has met

all submission requirements.

Owners who expect to take advantage of the QC option have a corresponding duty to

maintain the records necessary to allow the computation of the QC price. There are three

options for owners who have not fulfilled this responsibility:

a) the agency deems the project ineligible for consideration,

b) an accountant deduces missing information (interpolation), or

c) the owner agrees to accept a three-year period and fair market value.

The agency will determine which will apply. An example of item (b) is to re-create what

would have been the project’s financial statement using accountant work papers.

Closing the deal, or not

Under Section 42(h)(6)(E)(i)(II), the allocating agency’s obligation is to present a bona

fide contract to acquire the project for the QC price. More specifically, the 30-year

extended use period terminates if “the agency is unable to present... a qualified contract”.

Therefore, once the agency presents such a contract, the possibility of terminating the

extended use period is permanently removed. The project will remain bound to the

provisions in the LURA for at least 30 years.

There is no requirement in Section 42 that the prospective buyer actually purchase the

project. Whether the seller executes a contract and closes the transaction is a separate,

legally unrelated matter.

Conclusion

While the QC process does have a limited role to play in the overall Year 15 context,

agencies and owners need to understand its limitations. Each side can reduce the need for

this confrontation through cooperation, flexibility, and creativity.

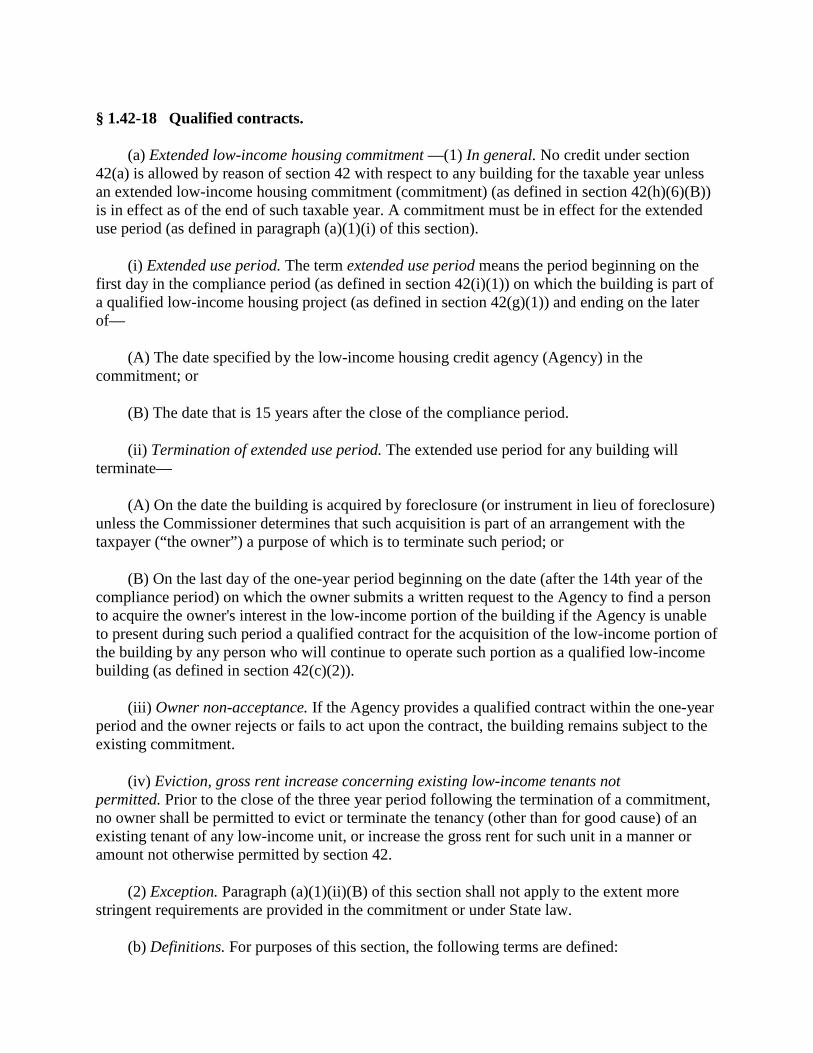

§ 1.42-18 Qualified contracts.

(a) Extended low-income housing commitment —(1) In general. No credit under section 42(a) is allowed by reason of section 42 with respect to any building for the taxable year unless an extended low-income housing commitment (commitment) (as defined in section 42(h)(6)(B)) is in effect as of the end of such taxable year. A commitment must be in effect for the extended use period (as defined in paragraph (a)(1)(i) of this section).

(i) Extended use period. The term extended use period means the period beginning on the first day in the compliance period (as defined in section 42(i)(1)) on which the building is part of a qualified low-income housing project (as defined in section 42(g)(1)) and ending on the later of—

(A) The date specified by the low-income housing credit agency (Agency) in the commitment; or

(B) The date that is 15 years after the close of the compliance period.

(ii) Termination of extended use period. The extended use period for any building will terminate—

(A) On the date the building is acquired by foreclosure (or instrument in lieu of foreclosure) unless the Commissioner determines that such acquisition is part of an arrangement with the taxpayer (“the owner”) a purpose of which is to terminate such period; or

(B) On the last day of the one-year period beginning on the date (after the 14th year of the compliance period) on which the owner submits a written request to the Agency to find a person to acquire the owner's interest in the low-income portion of the building if the Agency is unable to present during such period a qualified contract for the acquisition of the low-income portion of the building by any person who will continue to operate such portion as a qualified low-income building (as defined in section 42(c)(2)).

(iii) Owner non-acceptance. If the Agency provides a qualified contract within the one-year period and the owner rejects or fails to act upon the contract, the building remains subject to the existing commitment.

(iv) Eviction, gross rent increase concerning existing low-income tenants not permitted. Prior to the close of the three year period following the termination of a commitment, no owner shall be permitted to evict or terminate the tenancy (other than for good cause) of an existing tenant of any low-income unit, or increase the gross rent for such unit in a manner or amount not otherwise permitted by section 42.

(2) Exception. Paragraph (a)(1)(ii)(B) of this section shall not apply to the extent more stringent requirements are provided in the commitment or under State law.

(b) Definitions. For purposes of this section, the following terms are defined:

(1) As provided by section 42(h)(6)(G)(iii), base calendar year means the calendar year with or within which the first taxable year of the credit period ends.

(2) The low-income portion of a building is the portion of the building equal to the applicable fraction (as defined in section 42(c)(1)(B)) specified in the commitment for the building.

(3) The fair market value of the non-low-income portion of the building is determined at the time of the Agency's offer of sale of the building to the general public. The fair market value of the non-low-income portion also includes the fair market value of the land underlying the entire building (both the non-low-income portion and the low-income portion). This valuation must take into account the existing and continuing requirements contained in the commitment for the building. The fair market value of the non-low-income portion also includes the fair market value of items of personal property not included in eligible basis under section 42(d) that convey under the contract with the building.

(4) Qualifying building costs include —

(i) Costs that are included in eligible basis of a low-income housing building under section 42(d) and that are included in the adjusted basis of depreciable property that is subject to section 168 and that is residential rental property for purposes of section 142(d) and § 1.103-8(b);

(ii) Costs that are included in eligible basis of a low-income housing building under section 42(d) and that are included in the adjusted basis of depreciable property that is subject to section 168 and that is used in a common area or is provided as a comparable amenity to all residential rental units in the building; and

(iii) Costs of the type described in paragraph (b)(4)(i) and (ii) of this section incurred after the first year of the low-income housing building's credit period under section 42(f).

(5) The qualified contract amount is the sum of the fair market value of the non-low-income portion of the building (within the meaning of section 42(h)(6)(F) and paragraph (b)(3) of this section) and the price for the low-income portion of the building (within the meaning of section 42(h)(6)(F) and paragraph (b)(2) of this section) as calculated in paragraph (c)(2) of this section. If this sum is not a multiple of $1,000, then when the Agency offers the building for sale to the general public, the Agency may round up the offering price to the next highest multiple of $1,000.

(c) Qualified contract purchase price formula —(1) In general. For purposes of this section, qualified contract means a bona fide contract to acquire the building (within a reasonable period after the contract is entered into) for the qualified contract amount.

(i) Initial determination. The qualified contract amount is determined at the time of the Agency's offer of sale of the building to the general public.

(ii) Mandatory adjustment by the buyer and owner. The buyer and owner under a qualified contract must adjust the amount of the low-income portion of the qualified contract formula to reflect changes in the components of the qualified contract formula such as mortgage payments that reduce outstanding indebtedness between the time of the Agency's offer of sale to the general public and the building's actual sale closing date.

(iii) Optional adjustment by the Agency and owner. The Agency and owner may agree to adjust the fair market value of the non low-income portion of the building after the Agency's offer of sale of the building to the general public and before the close of the one-year period described in paragraph (a)(1)(ii)(B) of this section. If no agreement between the Agency and owner is reached, the fair market value of the non-low-income portion of the building determined at the time of the Agency's offer of sale of the building to the general public remains unchanged.

(2) Low-income portion amount. The low-income portion amount is an amount not less than the applicable fraction specified in the commitment, as defined in section 42(h)(6)(B)(i), multiplied by the total of—

(i) The outstanding indebtedness for the building (as defined in paragraph (c)(3) of this section); plus

(ii) The adjusted investor equity in the building for the calendar year (as defined in paragraph (c)(4) of this section); plus

(iii) Other capital contributions (as defined in paragraph (c)(5) of this section), not including any amounts described in paragraphs (c)(2)(i) and (ii) of this section; minus

(iv) Cash distributions from (or available for distribution from) the building (as defined in paragraph (c)(6) of this section).

(3) Outstanding indebtedness. For purposes of paragraph (c)(2)(i) of this section, outstanding indebtedness means the remaining stated principal balance (which is initially determined at the time of the Agency's offer of sale of the building to the general public) of any indebtedness secured by, or with respect to, the building that does not exceed the amount of qualifying building costs described in paragraph (b)(4) of this section. Thus, any refinancing indebtedness or additional mortgages in excess of such qualifying building costs are not outstanding indebtedness for purposes of section 42(h)(6)(F) and this section. Examples of outstanding indebtedness include certain mortgages and developer fee notes (excluding developer service costs not included in eligible basis). Outstanding indebtedness does not include debt used to finance nondepreciable land costs, syndication costs, legal and accounting costs, and operating deficit payments. Outstanding indebtedness includes only obligations that are indebtedness under general principles of Federal income tax law and that are actually paid to the lender upon the sale of the building or are assumed by the buyer as part of the sale of the building.

(4) Adjusted investor equity —(i) Application of cost-of-living factor. For purposes of paragraph (c)(2)(ii) of this section, the adjusted investor equity for any calendar year equals the unadjusted investor equity, as described in paragraph (c)(4)(ii) of this section, multiplied by the qualified-contract cost-of-living adjustment for that year, as defined in paragraph (c)(4)(iii) of this section.

(ii) Unadjusted investor equity. For purposes of this paragraph (c)(4), unadjusted investor equity means the aggregate amount of cash invested by owners for qualifying building costs described in paragraph (b)(4)(i) and (ii) of this section. Thus, equity paid for land, credit adjuster payments, Agency low-income housing credit application and allocation fees, operating deficit contributions, and legal, syndication, and accounting costs all are examples of cost payments that do not qualify as unadjusted investor equity. Unadjusted investor equity takes an amount into account only to the extent that, as of the beginning of the low-income building's credit period (as defined in section 42(f)(1)), there existed an obligation to invest the amount. Unadjusted investor equity does not include amounts included in the calculation of outstanding indebtedness as defined in paragraph (c)(3) of this section.

(iii) Qualified-contract cost-of-living adjustment. For purposes of this paragraph (c)(4), the qualified-contract cost-of-living adjustment for a calendar year is the number that is computed under the general rule in paragraph (c)(4)(iv) of this section or a number that may be provided by the Commissioner as described in paragraph (c)(4)(v) of this section.

(iv) General rule. Except as provided in paragraph (c)(4)(v) of this section, the qualified-contract cost-of-living adjustment is the quotient of—

(A) The sum of the 12 monthly Consumer Price Index (CPI) values whose average is the CPI for the calendar year that precedes the calendar year in which the Agency offers the building for sale to the general public (The term “CPI for a calendar year” has the meaning given to it by section 1(f)(4) for purposes of computing annual inflation adjustments to the rate brackets.); divided by

(B) The sum of the 12 monthly CPI values whose average is the CPI for the base calendar year (within the meaning of section 1(f)(4)), unless that sum has been increased under paragraph (c)(4)(iii)(D) of this section.

(v) Provision by the Commissioner of the qualified-contract cost-of-living adjustment. The Commissioner may publish in the Internal Revenue Bulletin (see § 601.601(d)(2) of this chapter) a process pursuant to which the Internal Revenue Service will compute the qualified-contract cost-of-living adjustment for a calendar year and make available the results of that computation.

(vi) Methodology. The calculations in paragraph (c)(4)(iv) of this section are to be made in the following manner:

(A) The CPI data to be used for purposes of this paragraph (c)(4) are the not seasonally adjusted values of the CPI for all urban consumers. (The U.S. Department of Labor's Bureau of Labor Statistics (BLS) sometimes refers to these values as “CPI-U.”) The BLS publishes the CPI

data on-line (including a History Table that contains monthly CPI-U values for all years back to 1913). See www.BLS.gov/data.

(B) The quotient is to be carried out to 10 decimal places.

(C) The Agency may round adjusted investor equity to the nearest dollar.

(D) If the CPI for any calendar year (within the meaning of section 1(f)(4)) during the extended use period after the base calendar year exceeds by more than 5 percent the CPI for the preceding calendar year (within the meaning of section 1(f)(4)), then the sum described in paragraph (c)(4)(i)(B) is to be increased so that the excess is never taken into account under this paragraph (c)(4).

(vii) Example. The following example illustrates the calculations described in this paragraph (c)(4):

Example. (i) Facts. Owner contributed $20,000,000 in equity to a building in 1997, which was the first year of the credit period for the building. In 2011, Owner requested Agency to find a buyer to purchase the building, and Agency offered the building for sale to the general public during 2011. The CPI for 1997 (within the meaning of section 1(f)(4)) is the average of the Consumer Price Index as of the close of the 12-month period ending on August 31, 1997. The sum of the CPI values for the twelve months from September 1996 through August 1997 is 1913.9. The CPI for 2010 (within the meaning of section 1(f)(4)) is the average of the Consumer Price Index as of the close of the 12-month period ending August 31, 2010. The sum of the CPI values for the twelve months from September 2009 through August 2010 is 2605.959. At no time during this period (after the base calendar year) did the CPI for any calendar year exceed the CPI for the preceding calendar year by more than 5 percent.

(ii) Determination of adjusted investor equity. The qualified-contract cost-of-living adjustment is 1.3615962171 (the quotient of 2605.959, divided by 1913.9). Owner's adjusted investor equity, therefore, is $27,231,924, which is $20,000,000, multiplied by 1.3615962171, rounded to the nearest dollar.

(5) Other capital contributions. For purposes of paragraph (c)(2)(iii) of this section, other capital contributions to a low-income building are qualifying building costs described in paragraph (b)(4)(ii) of this section paid or incurred by the owner of the low-income building other than amounts included in the calculation of outstanding indebtedness or adjusted investor equity as defined in this section. For example, other capital contributions may include amounts incurred to replace a furnace after the first year of a low-income housing credit building's credit period under section 42(f), provided any loan used to finance the replacement of the furnace is not secured by the furnace or the building. Other capital contributions do not include expenditures for land costs, operating deficit payments, credit adjuster payments, and payments for legal, syndication, and accounting costs.

(6) Cash distributions —(i) In general. For purposes of paragraph (c)(2)(iv) of this section, the term cash distributions from (or available for distribution from) the building include—

(A) All distributions from the building to the owners or to persons whose relationship to the owner is described in section 267(b) or section 707(b)(1)), including distributions under section 301 (relating to distributions by a corporation), section 731 (relating to distributions by a partnership), or section 1368 (relating to distributions by an S corporation); and

(B) All cash and cash equivalents available for distribution at, or before, the time of sale, including, for example, reserve funds whether operating or replacement reserves, unless the reserve funds are legally required by mortgage restrictions, regulatory agreements, or third party contractual agreements to remain with the building following the sale.

(ii) Excess proceeds. For purposes of paragraph (c)(6)(i) of this section, proceeds from the refinancing of indebtedness or additional mortgages that are in excess of qualifying building costs are not considered cash available for distribution.

(iii) Anti-abuse rule. The Commissioner will interpret and apply the rules in this paragraph (c)(6) as necessary and appropriate to prevent manipulation of the qualified contract amount. For example, cash distributions include payments to owners or persons whose relation to owners is described in section 267(b) or section 707(b) for any operating expenses in excess of amounts reasonable under the circumstances.

(d) Administrative discretion and responsibilities of the Agency —(1) In general. An Agency may exercise administrative discretion in evaluating and acting upon an owner's request to find a buyer to acquire the building. An Agency may establish reasonable requirements for written requests and may determine whether failure to follow one or more applicable requirements automatically prevents a purported written request from beginning the one-year period described in section 42(h)(6)(I). If the one-year-period has already begun, the Agency may determine whether failure to follow one or more requirements suspends the running of that period. Examples of Agency administrative discretion include, but are not limited to, the following:

(i) Concluding that the owner's request lacks essential information and denying the request until such information is provided.

(ii) Refusing to consider an owner's representations without substantiating documentation verified with the Agency's records.

(iii) Determining how many, if any, subsequent requests to find a buyer may be submitted if the owner has previously submitted a request for a qualified contract and then rejected or failed to act upon a qualified contract presented by the Agency.

(iv) Assessing and charging the owner certain administrative fees for the performance of services in obtaining a qualified contract (for example, real estate appraiser costs).

(v) Requiring all appraisers involved in the qualified contract process to be State certified general appraisers that are acceptable to the Agency.

(vi) Specifying other conditions applicable to the qualified contract consistent with section 42 and this section.

(2) Actual offer. Upon receipt of a written request from the owner to find a person to acquire the building, the Agency must offer the building for sale to the general public, based on reasonable efforts, at the determined qualified contract amount in order for the qualified contract to satisfy the requirements of this section unless the Agency has already identified a willing buyer who submitted a qualified contract to purchase the project.

(3) Debarment of certain appraisers. Agencies shall not utilize any individual or organization as an appraiser if that individual or organization is currently on any list for active suspension or revocation for performing appraisals in any State or is listed on the Excluded Parties Lists System (EPLS) maintained by the General Services Administration for the United States Government found at www.epls.gov.

(e) Effective date/applicability date. These regulations are applicable to owner requests to housing credit agencies on or after May 3, 2012 to obtain a qualified contract for the acquisition of a low-income housing credit building.

[T.D. 9587, 77 FR 26178, May 3, 2012]

LIHTC Compliance After the Compliance Period:

Once the Credits are Gone Materials submitted by Laura Abernathy, Director of State and Local Policy at the National

Housing Trust

Extended use restrictions can have a substantial effect on future affordability of housing

developed under the Low Income Housing Tax Credit (Housing Credit) program by

preventing an escalating loss of affordability and allowing the assisted stock to grow.

Section 42 of the Internal Revenue Code requires Housing Credit properties to be

affordable for 30 years – an initial 15-year compliance period, followed by a 15-year

extended use period. Many state Housing Finance Agencies use their Qualified

Allocation Plans to incentivize and in some cases require affordability beyond the

federally mandated 30 years.

Owners can “opt-out” of use restrictions during the 15-year extended use period through

a Qualified Contract. After the 14th year of the 15-year compliance period, an owner can

request that the Housing Finance Agency find a buyer for the property who is willing to

operate it as a Housing Credit property for the duration of the extended use period. If,

after one year’s time, the Agency is unable to find a qualified buyer, the land use

restrictions terminate. The existing owner can operate the building at market rate. Many

states require or incentivize applicants to waive their right to a Qualified Contract, either

indefinitely or for a specified number of years, ensuring that properties remain affordable.

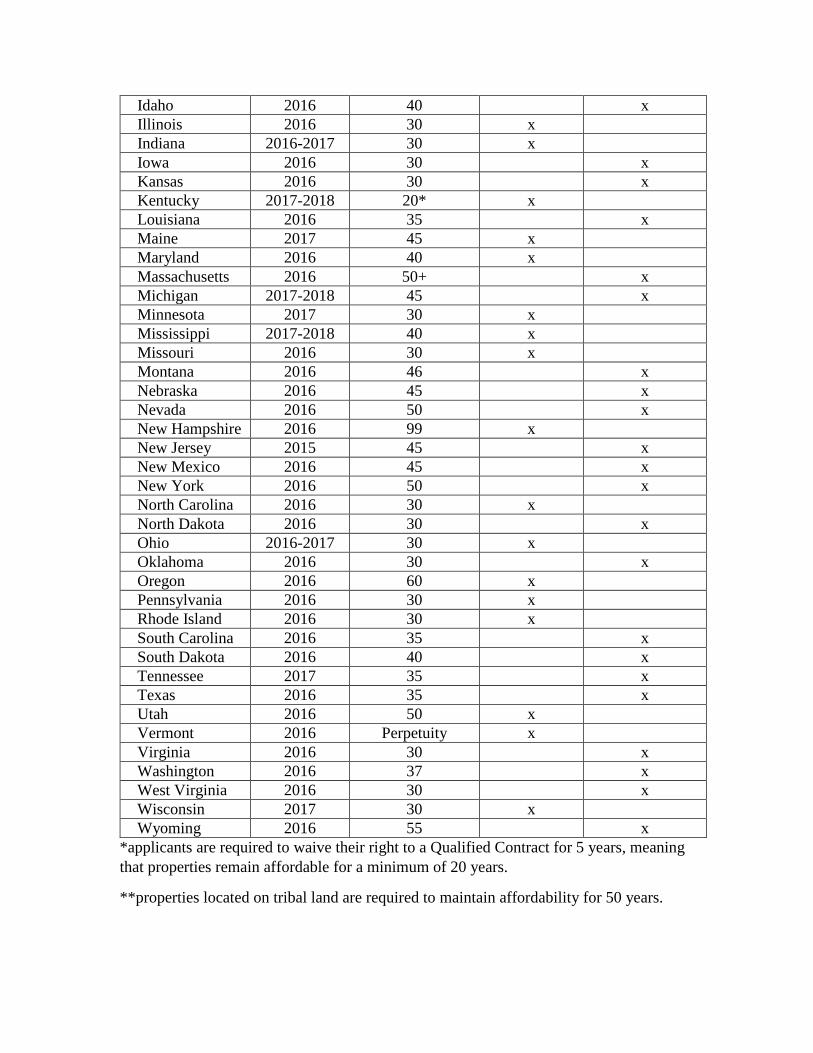

The table below illustrates the ways in which states require or incent long-term

affordability in the Housing Credit Program.

Table 1: Affordability by State

Housing Finance

Agency

QAP Year Years of

Affordability

Requirement Incentive

(points)

Alabama 2017 20* x

Alaska 2016 30 x

Arizona 2017 30 x

Arkansas 2016 35 x

California 2016 55** x

Colorado 2016 40 x

Connecticut 2016 40 x

DC 2012 50 x

Delaware 2016 60 x

Florida 2016 50 x

Georgia 2016 20 x

Hawaii 2017 61 x

Idaho 2016 40 x

Illinois 2016 30 x

Indiana 2016-2017 30 x

Iowa 2016 30 x

Kansas 2016 30 x

Kentucky 2017-2018 20* x

Louisiana 2016 35 x

Maine 2017 45 x

Maryland 2016 40 x

Massachusetts 2016 50+ x

Michigan 2017-2018 45 x

Minnesota 2017 30 x

Mississippi 2017-2018 40 x

Missouri 2016 30 x

Montana 2016 46 x

Nebraska 2016 45 x

Nevada 2016 50 x

New Hampshire 2016 99 x

New Jersey 2015 45 x

New Mexico 2016 45 x

New York 2016 50 x

North Carolina 2016 30 x

North Dakota 2016 30 x

Ohio 2016-2017 30 x

Oklahoma 2016 30 x

Oregon 2016 60 x

Pennsylvania 2016 30 x

Rhode Island 2016 30 x

South Carolina 2016 35 x

South Dakota 2016 40 x

Tennessee 2017 35 x

Texas 2016 35 x

Utah 2016 50 x

Vermont 2016 Perpetuity x

Virginia 2016 30 x

Washington 2016 37 x

West Virginia 2016 30 x

Wisconsin 2017 30 x

Wyoming 2016 55 x

*applicants are required to waive their right to a Qualified Contract for 5 years, meaning

that properties remain affordable for a minimum of 20 years.

**properties located on tribal land are required to maintain affordability for 50 years.

1

FILED: October 26, 2011

IN THE COURT OF APPEALS OF THE STATE OF OREGON

SARAH NORDBYE, individually and on behalf of all others similarly situated,

Plaintiff-Appellant,

v.

BRCP/GM ELLINGTON, an Oregon limited liability corporation;

and the OREGON HOUSING AND COMMUNITY SERVICES DEPARTMENT, Defendants-Respondents.

Multnomah County Circuit Court 071113782

A141698

Dale R. Koch, Judge. Argued and submitted on December 07, 2010. Alice Warner argued the cause for appellant. With her on the briefs was Edward Johnson. Thomas H. Tongue argued the cause for respondent BRCP/GM Ellington. With him on the brief were Brian R. Talcott and Dunn Carney Allen Higgins & Tongue LLP. Judy C. Lucas, Senior Assistant Attorney General, argued the cause for respondent Oregon Housing and Community Services Department. With her on the brief were John R. Kroger, Attorney General, and David B. Thompson, Interim Solicitor General. Jeffrey B. Litwak filed the brief amicus curiae for Columbia River Gorge Commission. Dennis Steinman and Kell Alterman & Runstein, LLP, filed the brief amicus curiae for National Housing Law Project. Mark Manulik, Sara Kobak, and Schwabe, Williamson & Wyatt, P.C., filed the brief amicus curiae for Oregon Land Title Association. Before Haselton, Presiding Judge, and Armstrong, Judge, and Duncan, Judge. HASELTON, P. J. Reversed and remanded.

2

HASELTON, P. J. 1

Plaintiff, a former tenant of a residential rental property that was financed, 2

at least in part, through the federal Low-Income Housing Tax Credit (LIHTC) program, 3

appeals.1 Plaintiff challenges (1) the trial court's allowance of summary judgment, on 4

grounds of "Chevron deference,"2 against her claims for injunctive and declaratory relief 5

pertaining to the enforceability of certain "use restrictions" related to the LIHTC 6

program; and (2) the court's denial of her cross-motion for summary judgment. As 7

described below, we conclude that Chevron deference is inapposite. We further conclude 8

that, as a matter of law, plaintiff is entitled to enforce the disputed use restrictions 9

pertaining to the operation of the property as low-income housing. Accordingly, we 10

reverse and remand. 11

Before turning to the particular circumstances of this dispute, it is not only 12

useful, but essential, to describe the LIHTC program. The purpose of the LIHTC 13

program is to encourage the development of low-income rental housing through the 14

allocation of tax credits pursuant to section 42 of the Internal Revenue Code (IRC). Oti 15

Kaga v. South Dakota Housing Dev. Authority, 188 F Supp 2d 1148, 1152 (D SD 2002), 16

1 Defendant BRCP/GM Ellington (BRCP) is the current owner of the property.

Defendant Oregon Housing and Community Services Department (the Department) is

responsible for monitoring property owners' compliance with LIHTC program

requirements, as was its predecessor entity, the Oregon Housing Authority. For ease of

reference, we refer to both entities as "the Department."

2 Chevron USA, Inc. v. Natural Res. Def. Council, 467 US 837, 104 S Ct 2778, 81 L

Ed 2d 694 (1984).

3

affd, 342 F3d 871 (8th Cir 2003). In general, the federal government allocates tax 1

credits, and state housing agencies are responsible for distributing the credits and 2

monitoring recipient projects for compliance with program requirements. Treas Reg § 3

1.42-1T; Treas Reg § 1.42-5. The LIHTC program is regulated by, and state housing 4

agencies report to, the Internal Revenue Service. IRC § 42(l), (n). Further, as a general 5

rule, the tax credits are claimed annually by the recipient taxpayer over the first 10 years 6

of a project. IRC § 42(f)(1); Treas Reg § 1.42-1T(a)(1). In return for receiving the tax 7

credits, the taxpayer must commit to maintain the project as low-income housing for 30 8

years. The 30-year term is comprised of an initial 15-year compliance period and an 9

additional 15-year "extended use period." IRC § 42(h)(6). 10

For our purposes, it is not necessary to describe the LIHTC program rental 11

and occupancy restrictions in detail. Suffice it to say there are three salient features. 12

First, the taxpayer agrees that a specified number of units in the project will be rented for 13

a restricted amount of rent to tenants whose income is a certain percentage less than the 14

median income of the geographical area in which the project is located. See IRC § 42(g). 15

Second, federal law requires that the taxpayer and state housing agency enter into an 16

"extended low-income housing commitment," which is to be "binding on all successors 17

of the taxpayer," and recorded as a restrictive covenant pursuant to state law. IRC § 18

42(h)(6)(A), (B). Third, "individuals who meet the income limitation applicable to the 19

building * * * (whether prospective, present, or former occupants of the building)" have 20

4

the right to enforce the extended low-income housing commitment "in any State court."3 1

IRC § 42(h)(6)(B)(ii). 2

Consistently with those requirements, in December 1990, Rose City Village 3

Limited Partnership, the original owner of the project, entered into a Low-Income 4

Housing Tax Credit Reservation and Extended Use Agreement (the extended use 5

agreement) with the Department. The original owner agreed, among other things, that it 6

would maintain 100 percent of the project as low-income housing for 30 years and that, 7

as a condition precedent to the issuance of tax credits, it would record a "declaration of 8

land use restrictive covenants." 9

In the Declaration of Land Use Restrictive Covenants for Low-Income 10

Housing Tax Credits (the declaration), which was recorded in Multnomah County, the 11

original owner acknowledged the obligations and restrictions imposed under the extended 12

use agreement. Section 2(b) of the declaration provides: 13

"The Owner intends, declares and covenants, on behalf of itself and all 14

future Owners and operators of the Project during the term of this 15

Declaration, that this Declaration and the covenants and restrictions set 16

forth in this Declaration regulating and restricting the use, occupancy and 17

transfer of the Project ([1]) shall be and are covenants running with the 18

Project land, encumbering the Project for the term of this Declaration, 19

binding upon the Owner's successors in title and all subsequent Owners and 20

Operators of the Project[,] ([2]) are not merely personal covenants of the 21

Owner, and ([3]) shall bind the Owner (and the benefits shall inure to the 22

Department and any past, present or prospective tenant of the Project) and 23

3 BRCP argued before the trial court that plaintiff did not meet the income

limitation applicable to the building and, thus, that she lacked standing to bring this

action. The trial court found that plaintiff satisfied the IRC section 42 income limitations,

and BRCP does not challenge that finding on appeal.

5

its respective successors and assigns during the term of this Declaration. 1

The Owner hereby agrees that any and all requirements of the laws of the 2

State of Oregon to be satisfied in order for the provisions of this 3

Declaration to constitute deed restrictions and covenants running with the 4

land shall be deemed to be satisfied in full, and that any requirements of 5

privileges [sic] of estate are intended to be satisfied, or in the alternate, that 6

an equitable servitude has been created to insure that these restrictions run 7

with the Project. For the longer of the period this Credit is claimed or the 8

term of this Declaration, each and every contract, deed or other instrument 9

hereafter executed conveying the Project or portion thereof shall expressly 10

provide that such conveyance is subject to this Declaration, provided, 11

however, the covenants contained herein shall survive and be effective 12

regardless of whether such contract, deed or other instrument hereafter 13

executed conveying the Project or portion thereof provides that such 14

conveyance is subject to this Declaration." 15

Further, and of critical significance, section 8 of the declaration, which is 16

captioned "Enforcement of Section 42 Occupancy Restrictions," provides, in part: 17

"(b) The Owner acknowledges that the primary purpose for requiring 18

compliance by the Owner with restrictions provided in this Declaration is to 19

assure compliance of the Project and the Owner with IRC Section 42 and 20

the applicable regulations, AND BY REASON THEREOF, THE OWNER 21

IN CONSIDERATION FOR RECEIVING LOW-INCOME HOUSING 22

TAX CREDITS FOR THIS PROJECT HEREBY AGREES AND 23

CONSENTS THAT THE DEPARTMENT AND ANY INDIVIDUAL 24

WHO MEETS THE INCOME LIMITATION APPLICABLE UNDER 25

SECTION 42 (WHETHER PROSPECTIVE, PRESENT OR FORMER 26

OCCUPANT) SHALL BE ENTITLED, FOR ANY BREACH OF THE 27

PROVISIONS HEREOF, AND IN ADDITION TO ALL OTHER 28

REMEDIES PROVIDED BY LAW OR IN EQUITY, TO ENFORCE 29

SPECIFIC PERFORMANCE BY THE OWNER OF ITS OBLIGATIONS 30

UNDER THIS DECLARATION IN A STATE COURT OF COMPETENT 31

JURISDICTION. The owner hereby further specifically acknowledges that 32

the beneficiaries of the Owner's obligations hereunder cannot be adequately 33

compensated by monetary damages in the event of any default hereunder." 34

(Uppercase in original.) 35

The Department allocated more than $2 million of LIHTC tax credits to the 36

project and monitored the project for conformity with LIHTC program requirements. 37

6

The project experienced compliance problems over the years. In the course of trying to 1

remediate those problems, the Department learned that, in 2002 or 2003, the original 2

owner had transferred ownership of the project to Rose City Village Affordable Housing 3

Limited Partnership (the middle owner). The manner in which the original owner 4

transferred the project violated the terms of the declaration. The declaration requires, 5

among other things, that the owner notify the Department prior to any transfer of 6

ownership and that the owner obtain the agreement of any buyer "that such acquisition is 7

subject to the requirements of" the declaration and IRC section 42. Those requirements 8

were not satisfied. 9

The Department ultimately concluded that, although the middle owner had 10

made substantial progress in some respects, the project could not be brought into full 11

compliance with all of the requirements of the LIHTC program.4 In 2004, a Department 12

compliance officer notified the Internal Revenue Service (IRS) of that conclusion in a 13

letter, which stated, in part: 14

"Due to the severity of the noncompliance issues relating to this project, it 15

has been determined that this project is not currently, is unlikely to be in the 16

future, and may not have ever been in compliance. It is apparent that the 17

Owner failed to make reasonable attempts to comply with the requirements 18

of the Program. Therefore, because of the egregious nature of the 19

noncompliance, it is the decision of [the Department] to remove this project 20

from the Low-Income Housing Tax Credit Program." 21

4 A Department employee subsequently identified the "largest problem" as the

original owner's failure to properly document the income eligibility of the initial project

tenants. Although the parties disagree about whether the Department was justified in

determining that full compliance was an impossibility, we need not resolve that dispute in

that it is immaterial to our analysis and disposition.

7

With that letter, the Department also submitted multiple IRS 8823 forms, entitled "Low-1

Income Housing Credit Agencies Report of Noncompliance or Building Disposition."5 2

The Department checked the same preprinted box on each form, indicating that the 3

"[p]roject is no longer in compliance nor participating in the low-income housing tax 4

credit program[.]" The federal government ultimately recaptured a portion of the tax 5

credits that had been allocated to the project.6 6

In 2005, the middle owner and the Department entered into a Settlement, 7

Satisfaction and Partial Release Agreement (the release agreement). The release 8

agreement recites that "the parties desire to resolve all outstanding issues between them 9

by means of this Agreement" and provides, in part: 10

"1. MUTUAL RELEASE. 11

"The parties hereby release one another from all claims, causes of action, 12

suits, and other liabilities, actual or potential, arising out of or related to the 13

allocation and subsequent rescission of the low-income housing tax credits 14

and the execution and recording of the related Declaration referenced 15

above, except as specifically indicated herein. 16

"2. SATISFACTION AND PARTIAL RELEASE OF DECLARATION. 17

"The Department hereby provides its satisfaction and partial release of that 18

Declaration except with respect to Section 6 (c)[7]

thereof which shall 19

5 The Department submitted a separate form for each building in the project.

6 From the record before us, the extent of that recoupment is unclear.

7 Section 6(c) of the declaration provides:

"Notwithstanding subsection (b) above, IRC Section 42 rent requirements

shall continue for a period of three years following the termination of the

extended use requirement pursuant to the procedures specified in

subsection (b) above for those tenants existing as of the date of termination.

8

remain in effect for three years from the date of this Agreement. For the 1

three years that Section 6 (c) remains in effect, the [middle owner], and any 2

successor in interest thereto, or other owner of the Property, shall not evict 3

or terminate the tenancy of an existing tenant of any low-income unit on the 4

Property other than for good cause and shall not increase the gross rent 5

above the maximum allowed under the IRC with respect to such low-6

income units." 7

Shortly after it was executed, the release agreement was recorded in Multnomah County. 8

In 2006, the middle owner sold the project to the present owner, BRCP, for 9

a very substantial profit. Later in that same year, and despite the three-year "safe harbor" 10

provision of the release agreement, BRCP issued a 30-day, no-cause eviction notice to 11

plaintiff, among other tenants. Plaintiff stated in her declaration that, by the time she 12

vacated her apartment in response to the eviction notice, almost all of her neighbors had 13

moved, and the project "was like a ghost town." BRCP does not operate the project in a 14

manner that complies with the restrictions of the LIHTC program and declaration. For 15

example, at the time of the summary judgment proceedings below, BRCP did not screen 16

tenants for income eligibility or rent exclusively to tenants who qualified as "low-17

income" under section 42 of the Internal Revenue Code. 18

Plaintiff subsequently filed this action, seeking declaratory and injunctive 19

During such three year period, the Owner shall not evict or terminate the

tenancy of an existing tenant of any low-income unit other than for good

cause and shall not increase the gross rent above the maximum allowed

under the IRC with respect to such low-income unit."

"Subsection (b)" of the declaration referenced in the excerpt set forth immediately above,

along with section 6(c) of the declaration, mirrors, in substance, IRC § 42(h)(6)(E), set

out below. See ___ Or App at ___ n 11 (slip op at 10 n 11).

9

relief to enforce the original owner's commitment to maintain the property as low-income 1

housing for the remainder of the declaration's 30-year term. BRCP and the Department 2

jointly moved for summary judgment, arguing that the release agreement is "valid and 3

enforceable against plaintiff and other current and future tenants[.]" In so contending, 4

defendants asserted, in part, that Chevron deference should be accorded to the 5

Department's decision to execute the 2005 release agreement. Plaintiff opposed 6

defendants' motion for summary judgment and filed a cross-motion, asserting that the 7

release agreement did not, and could not, abrogate her right to obtain specific 8

performance of the declaration. 9

The trial court granted defendants' motion for summary judgment and 10

denied plaintiff's cross-motion. The court determined that the Department's decisions to 11

"terminate" the project from participation in the LIHTC program and enter into the 12

release agreement effectively abrogated the ability of low-income tenants to obtain 13

specific performance of the declaration.8 That holding was predicated on the trial court's 14

conclusion that the Department's decisions to remove the project from the LIHTC 15

8 The release agreement does not explicitly address the rights conferred on low-

income tenants in the declaration. Instead, the middle owner and the Department state in

the release agreement that they "desire to resolve all outstanding issues between them"

and that they are releasing "one another." (Emphasis added.) Although an argument

could be made that the parties never intended that the release agreement would have any

effect on the right of a qualified tenant to enforce the use restrictions set forth in the

declaration, no such argument was made before the trial court or has been made on

appeal. It appears that the parties and the trial court assumed that the middle owner and

the Department intended that the release agreement would extinguish the enforcement

rights conferred on low-income tenants.

10

program and enter into the release agreement with the middle owner were entitled to 1

deference under the principles set forth in Chevron USA, Inc. v. Natural Res. Def. 2

Council, 467 US 837, 104 S Ct 2778, 81 L Ed 2d 694 (1984). The court thereafter 3

entered a general judgment of dismissal. 4

Plaintiff appeals, assigning error to the allowance of defendants' motion for 5

summary judgment and to the denial of her cross-motion for summary judgment.9 In an 6

appeal from a judgment that results from cross-motions for summary judgment, 7

"if both the granting of one motion and the denial of the other are assigned 8

as error, then both are subject to review. Each party that moves for 9

summary judgment has the burden of demonstrating that there are no 10

material issues of fact and that the movant is entitled to judgment as a 11

matter of law. We review the record for each motion in the light most 12

favorable to the party opposing it." 13

Eden Gate, Inc. v. D&L Excavating & Trucking, Inc., 178 Or App 610, 622, 37 P3d 233 14

(2002) (citations omitted). As amplified below, we conclude that deference under 15

Chevron is not warranted and that the 2005 release agreement did not abrogate plaintiff's 16

right to enforce the original use restrictions prescribed in the 1990 declaration. 17

Accordingly, the trial court erred in granting defendants' motion for summary judgment 18

and in denying plaintiff's cross-motion. 19

We begin with the trial court's basis for disposition--viz., deference in 20

9 Earlier in this appeal, BRCP filed a motion to dismiss for lack of jurisdiction,

arguing that this court lacks jurisdiction because plaintiff's exclusive remedy is under the

Administrative Procedures Act (ORS chapter 183). The Appellate Commissioner denied

the motion, and BRCP renews its jurisdictional argument in its answering brief. We deny

BRCP's renewed motion to dismiss for the reasons stated by the commissioner in the

court's order entered on April 29, 2010.

11

accordance with the principles set forth in Chevron.10

In Friends of Columbia Gorge v. 1

Columbia River (S055722), 346 Or 366, 378, 213 P3d 1164 (2009), the court generally 2

described the application of deference under Chevron: 3

"A long line of federal cases, beginning with Chevron, * * * holds that, 4

when a federal agency has been charged by Congress with implementing a 5

federal statute, courts should defer to that agency's interpretation of the 6

statute, treating that interpretation as controlling as long as it is reasonable." 7

However, deference is appropriate only where "Congress has not directly addressed the 8

precise question at issue[.]" Chevron, 467 US at 843. "If the intent of Congress is clear, 9

that is the end of the matter; for the court, as well as the agency, must give effect to the 10

unambiguously expressed intent of Congress." Id. at 842-43. 11

Here, invoking Chevron deference, the trial court noted that the Internal 12

Revenue Code explicitly identifies two situations in which the extended-use period will 13

terminate early (neither of which was applicable in the circumstances of this case).11

14

10

Although the Department argued before the trial court that Chevron-style

deference was appropriate, it has abandoned that argument on appeal and, in fact, now

argues that Chevron deference is inapposite. BRCP, however, defends the trial court's

rationale.

11 IRC section 42(h)(6)(E) provides:

"(i) In general.--The extended use period for any building shall terminate--

"(I) on the date the building is acquired by foreclosure (or instrument

in lieu of foreclosure) unless the Secretary determines that such

acquisition is part of an arrangement with the taxpayer a purpose of

which is to terminate such period, or

"(II) on the last day of the period specified in subparagraph (I) if the

housing credit agency is unable to present during such period a

qualified contract for the acquisition of the low-income portion of

12

Nevertheless, the court reasoned that that identification was not necessarily exclusive 1

and, thus, "Congress was silent" as to whether, in other circumstances, local housing 2

agencies can voluntarily terminate a project's participation in the LIHTC program before 3

the end of the extended-use period. Proceeding from that premise, the trial court 4

concluded that, 5

"[i]n light of the fact that some areas of noncompliance could never be 6

remedied[,] it was reasonable for the agency to determine that the property 7

owner would be unable to bring the property into compliance. Because [the 8

Department] acted reasonably, the court will defer to its interpretation of 9

the statute. This leaves the remaining question as to whether [the 10

Department and the middle owner] needed to give the tenants notice and 11

obtain their consent prior to modification of the Declaration." 12

As to that "remaining question," the court concluded that Congress had not directly 13

addressed the subject and that the "actions" of the parties to the release agreement "were 14

reasonable and will be entitled to deference." 15

The court's invocation of Chevron deference was erroneous because the 16

the building by any person who will continue to operate such portion

as a qualified low-income building.

"Subclause (II) shall not apply to the extent more stringent requirements are

provided in the agreement or in State law.

"(ii) Eviction, etc. of existing low-income tenants not permitted.--The

termination of an extended use period under clause (i) shall not be

construed to permit before the close of the 3-year period following such

termination--

"(I) the eviction or the termination of tenancy (other than for good

cause) of an existing tenant of any low-income unit, or

"(II) any increase in the gross rent with respect to such unit not

otherwise permitted under this section."

13

Department is not an entity to which deference is warranted under Chevron. The 1

Department is an agency established under state statute. See ORS 456.555(1). "A state 2

agency's interpretation of federal statutes is not entitled to the deference afforded a 3

federal agency's interpretation of its own statutes under Chevron * * *." Orthopaedic 4

Hosp. v. Belshe, 103 F3d 1491, 1495 (9th Cir 1997). 5

BRCP suggests, nevertheless, that deference to the Department is warranted 6

under Chevron because the circumstances here are analogous to those in Friends of 7

Columbia Gorge. We disagree. 8

In Friends of Columbia Gorge, the Oregon Supreme Court held that 9

interpretations by the Columbia River Gorge Commission (Gorge Commission) of certain 10

provisions of the Columbia River Gorge National Scenic Area Act, 16 USC §§ 544-544p, 11

were entitled to Chevron deference. In so holding, the court pointed to specific features 12

of the federal authorizing legislation--including those requiring the Gorge Commission to 13

develop, implement, and administer a management plan "in cooperation and consultation 14

with the United States Secretary of Agriculture"--and emphasized that, as a matter of 15

Congressional intent, "[t]he Act clearly contains gaps that the [Gorge] commission is 16

charged with filling." 346 Or at 369-70, 381-82. 17

Here, in contrast, nothing in the authorizing legislation for the LIHTC 18

program delegates to the Department or other state housing agencies the expansive type 19

of "rulemaking" authority conferred on the Gorge Commission. To the contrary, section 20

42(n) of the Internal Revenue Code provides that "[t]he Secretary shall prescribe such 21

14

regulations as may be necessary or appropriate to carry out the purposes of this 1

section[.]" 2

BRCP contends, alternatively, that Chevron deference applies because an 3

IRS employee's advice informed the Department's decision to remove the project from 4

the LIHTC program. In particular, BRCP points to evidence that an IRS employee 5

advised the Department in a phone conversation that the project could be "kicked out of" 6

the LIHTC program for noncompliance with program requirements.12

That argument is 7

unavailing. Only those administrative interpretations that Congress and the agency 8

intend to have the force of law are entitled to Chevron deference. United States v. Mead 9

Corp., 533 US 218, 226-27, 121 S Ct 2164, 150 L Ed 2d 292 (2001). The oral advice of 10

a federal employee, given on an ad hoc basis to a state agency, simply does not qualify. 11

In sum, the trial court erred in granting defendants' summary judgment 12

motion based on its application of Chevron deference. That, however, is merely the 13

beginning, not the end, of our inquiry. That is so because, as noted, plaintiff has also 14

challenged the denial of her cross-motion for summary judgment, and defendants, 15

individually and collectively, proffer alternative legal bases for affirming the trial court's 16

dismissal of plaintiff's claims. None of the parties suggests that those cross-cutting 17

contentions implicate disputed issues of material fact. For the reasons that follow, we 18

conclude that the 2005 release agreement did not abrogate plaintiff's entitlement to 19

12

The official position held by the IRS employee is not clear from the record. One

Department employee described the IRS employee as being a LIHTC compliance "guru,"

and another said the IRS employee was in charge of LIHTC compliance at the IRS.

15

enforce the use restrictions prescribed in the 1990 declaration and that defendants' 1

asserted defenses to the enforcement of those restrictions fail as a matter of law. 2

Accordingly, the trial court erred in denying plaintiff's cross-motion for summary 3

judgment. 4

We begin with the pertinent provisions of the declaration. In section 2(b) 5

of the declaration, the original owner of the project and the Department agreed that the 6

use restrictions set forth in the declaration would be "covenants running with the Project 7

land," encumbering the project for the term of the declaration and binding all successors 8

in title for the stated duration. See ___ Or App at ___ (slip op at 3-4). Section 2(b) 9

further provides that the "benefits" of the covenants and restrictions "shall inure to the 10

Department and any past, present or prospective tenant of the Project." (Emphasis 11

added.) Finally, under section 8(b) of the declaration, both the Department and "any 12

individual who meets the income limitation applicable under section 42 (whether 13

prospective, present or former occupant) shall be entitled * * * to enforce specific 14

performance" of obligations owed under that document. (Emphasis omitted.) Thus, 15

under the declaration, plaintiff is an intended third-party beneficiary of the use 16

restrictions and, pursuant to section 8(b), she is independently entitled to enforce those 17

use restrictions, even if the Department has waived its ability to do so. 18

BRCP contends, however, that the release agreement abrogated the use 19

restriction, precluding plaintiff or any other intended beneficiary from enforcing those 20

restrictions. That argument fails because, under Oregon law--which is expressly made 21

16

applicable by both section 8(e) of the declaration and section 4 of the release agreement--1

a grantor and grantee cannot terminate a restrictive covenant without the consent of the 2

intended beneficiary. Snashall et ux v. Jewell et ux, 228 Or 130, 137-38, 363 P2d 566 3

(1961). 4

In Snashall, the parties lived in the same subdivision and received their 5

deeds from common grantors. 228 Or at 132. The defendants' deed contained a 6

restrictive covenant prohibiting buildings over one story in height and also contained a 7

covenant that building plans be approved by the common grantors. The defendants, in 8

an attempt to defeat the restrictive covenant, transferred the property back to the original 9

grantors, who then reconveyed the land to the defendants, with the deed of reconveyance 10

effectively omitting the building restriction. Id. at 133. The plaintiffs subsequently, 11

successfully brought an action for breach of contract, asserting that the defendants' home 12

violated the restrictive covenants. 13

The defendants appealed, and the Supreme Court affirmed. In so holding, 14

the court determined that 15

"[t]his [reconveyance] maneuver did not, however, operate to change the 16

binding effect of the restrictions contained in the original deed because the 17

covenants which became operative upon the execution of the first deed to 18

defendants inured to the benefit of the other lot owners in the tract and 19

would continue to bind defendants as to those other owners unless the latter 20

were to release defendants from the obligations of the covenants. 21

Defendants treat the deed provision calling for the grantors' approval of 22

building plans as vesting in the grantors a dispensing power permitting the 23

lifting of the restriction on any lot at the will of the grantors. We do not so 24

construe the provision; it was intended to provide machinery in the aid of 25

the enforcement of the covenants rather than to provide a means by which 26

the common plan could be weakened by modification. It is manifest from 27

17

the content of the restrictive covenants that they were imposed for the 1

benefit of the owners of the several lots within the tract rather than for the 2

personal benefit of the grantors." 3

Id. at 137-38 (emphasis added). The Supreme Court concluded that, "by reason of either 4

the theory of third party beneficiary or the theory of implied reciprocal servitude, [the] 5

plaintiffs are entitled to enforce the restrictive covenant contained in [the] defendants' 6

deed." Id. at 138. See also Menstell et al. v. Johnson et al., 125 Or 150, 167, 262 P 853 7

(1927), reh'g den, 125 Or 169, 266 P 891 (1928) (restrictive covenant may not be 8

modified "without the consent or acquiescence of the [beneficiaries]"). 9

Plaintiff contends (we believe correctly) that Snashall is dispositive. 10

Notwithstanding plaintiff's invocation of Snashall, defendants do not directly address 11

Snashall, Menstell, and the other related cases cited by plaintiff13

--and offer no principled 12

basis for distinguishing those cases. Defendants appear to suggest, however, that 13

plaintiff's claim is foreclosed by the release agreement because the declaration does not 14

expressly require that qualified tenants consent to release of their interests. The problem 15

with that argument is that the declaration and the release agreement do expressly 16

incorporate Oregon law--including Snashall--and nothing in Snashall (or any related 17

case) conditions the right of an intended beneficiary to enforce a restrictive covenant on 18

the existence of an express contractual provision requiring the third-party beneficiary's 19

13

See, e.g., Stan Wiley v. Berg, 282 Or 9, 15-16, 578 P2d 384 (1978) (a promisor and

promisee generally cannot materially alter or abrogate the rights of an intended third-

party beneficiary once the beneficiary has "accepted, adopted, or acted upon" the promise

made for his or her benefit).

18

consent to the material modification or termination of the covenant. 1

BRCP further argues that, in all events, it is not bound by the use 2

restrictions set forth in the declaration because the declaration did not succeed in creating 3

covenants that run with the land at law.14

To create a covenant running with the land and 4

binding on successors, four requirements must be met: 5

"(1) there must be privity of the estate between the promisor and his 6

successors; (2) the promisor and promisee must intend that the covenant 7

run; (3) the covenant must touch and concern the land of the promisor; and 8

(4) the promisee must benefit in the use of some land possessed by him as a 9

result of the performance of the promise." 10

Johnson v. Highway Division, 27 Or App 581, 584, 556 P2d 724 (1976), rev den, 277 Or 11

99 (1977) (emphasis omitted). Specifically, BRCP argues that the first and fourth 12

requirements are not satisfied. 13

BRCP's argument fails because the declaration itself expressly provides that 14

all of the requirements under Oregon law for creation of a restrictive covenant running 15

with the land are deemed satisfied. In section 2(b), the parties to the declaration agreed 16

"that any and all requirements of the laws of the State of Oregon to be satisfied in order 17

for the provisions of this Declaration to constitute deed restrictions and covenants 18

running with the land shall be deemed to be satisfied in full[.]" BRCP does not cite, and 19

we are not aware of, any authority supporting the proposition that such an agreement is 20

legally ineffective. 21

14

The trial court determined that the declaration was recorded as a restrictive

covenant in the property's chain of title, and the Department does not dispute that the

declaration successfully created covenants running with the land.

19

In all events, even if the requisites of the covenant running with the land 1

were somehow not satisfied, BRCP would nevertheless be subject to enforcement of the 2

use restrictions as an equitable servitude. That is so because the original owner and the 3

Department agreed in section 2(b) of the declaration that, in the event that the declaration 4

somehow failed to create covenants running with the land at law, an equitable servitude 5

would be created "to insure that [the] restrictions run with the Project." In Ebbe v. Senior 6

Estates Golf, 61 Or App 398, 404-05, 657 P2d 696 (1983), we summarized the elements 7

of an equitable servitude: 8

"The general rule is that, even if all technical requirements for a 9

covenant to run with the land are not met, a promise is binding as an 10

equitable servitude if (1) the parties intend the promise to be binding; (2) 11

the promise 'concern[s] the land or its use in a direct and not a collateral 12

way'; and (3) 'the subsequent grantee [has] notice of the covenant * * *.' 20 13

Am Jur 2d Covenants, § 26 (1965)." 14

An equitable servitude creates a burden that will fall on subsequent holders of the 15

property "'with the single qualification that a subsequent owner who acquires the legal 16

estate for value and without notice takes it free from this burden.'" Hall v. Risley and 17

Heikkila, 188 Or 69, 99, 213 P2d 818 (1950) (quoting John Norton Pomeroy, 4 18

Pomeroy's Equity Jurisprudence § 1295, 850 (5th ed)). Either actual or constructive 19

notice of the covenant is sufficient to bind a subsequent owner. Ebbe, 61 Or App at 405. 20

BRCP remonstrates that an equitable servitude is inapposite because it did 21

not have actual or constructive notice of the use restrictions set forth in the declaration. 22

The uncontroverted evidence is to the contrary--and, indeed, BRCP had both actual and 23

constructive notice of the covenants. In particular, the individual in charge of due 24

20

diligence for BRCP's acquisitions acknowledged that she had learned of the existence of 1

the declaration and the covenants included therein before BRCP purchased the project. 2

Thus, BRCP acquired the project with actual notice of the use restrictions. In addition, 3

the recording of the declaration operated to give BRCP constructive notice of the use 4

restrictions imposed by that document. ORS 93.643 (addressing constructive notice from 5

recordation of interest in real property); see also Huff v. Duncan, 263 Or 408, 411, 502 6

P2d 584 (1972). 7