w to refinance your mortgage

TRANSCRIPT

When To Refinance Your Mortgage

US Mortgage Corporation (NMLS ID#3901). Corporate Office is located at 201 Old Country Road, Suite 140, Melville, NY 11747; 631-580-2600 or (800) 562-6715 (LOANS15). Licensed Mortgage Banker-NYS Department of Financial Services- AK, AL, AR, CA, CO, CT, DC, DE, FL, GA, IA,ID, IL, IN, KS, KY, LA, MA, MD, ME, MI, MN, MS, MT, NC, ND, NE, NH, NJ, NM, OH, OK, OR, PA, RI, SC, SD, TN, TX, VA, VT, WA, WI, WV, WY State Banking Departments/Regulators. Rates, fees and program guidelines are subject to change without notice. Certain restrictions may apply. Some loans arranged through third parties. First mortgages only. Not all products and/or programs are available in all states.

Table of conTenTs

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Page 01

Mortgage Length Adjustment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Page 03

Changing To A Fixed Rate Mortgage From An Adjustable Rate Mortgage . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Page 05

Calculate Your Break Even Point . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Page 07

Refinancing To Get The Equity From Your Home . . . . . . . . . . . . . . . . . . . . . Page 09

Check For Hidden Costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Page 10

When Not To Refinance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Page 11

inTRoducTion

www.usmortgage.com01

Has there been a fall in interest rates lately? Or, are you expecting the rates to climb? Has there been an improvement in your credit score, making you eligible for lower mortgage rates? Or, do you want

to move to a different kind of mortgage?

Your answer to these questions will help you decide if you should go for a refinance or not. But before you take this decision, you should understand what is at stake. Note that a person’s home is his most important financial asset. You should be careful when you choose a broker or a lender to refinance your home. Also, be careful about mortgages on specific terms. There are certainly benefits to refinancing, but there are costs involved also.

When you refinance, you are essentially paying off your old mortgage and creating a new one. You may also want to combine the primary mortgage and the new one into a single new mortgage.

Why and When Should You refinance?To lower the interest rate: The amount you pay on the mortgage every month is directly tied with the rate of interest on the mortgage. Note that by refinancing, the debt will not be paid off, it will only get restructured (with a lower rate of interest and different term). The most common reason why people opt for refinancing is to lower the monthly interest payments.

Low rates will usually mean lower monthly payments. If there has been an improvement in your credit score or if conditions in the market are conducive, you might get lower rates on a refinance loan.

www.usmortgage.com 02

MoRTgage lengThadjuStMent

03 www.usmortgage.com

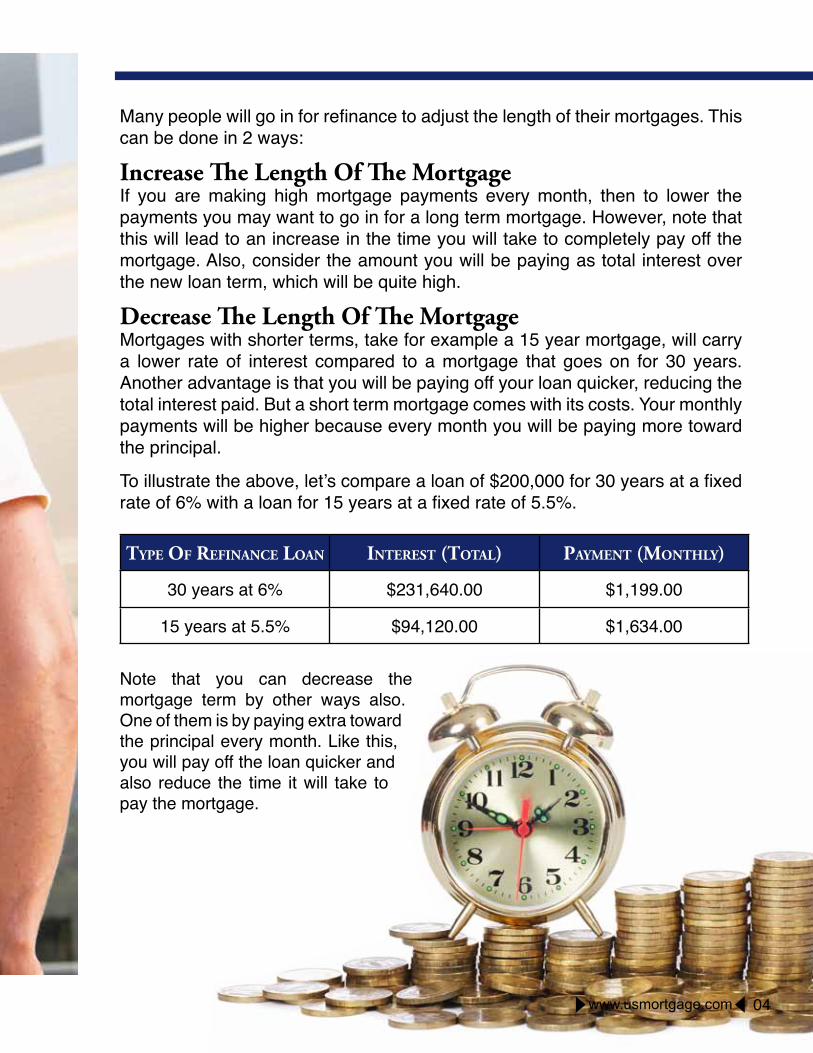

Many people will go in for refinance to adjust the length of their mortgages. This can be done in 2 ways:

Increase The Length of The MortgageIf you are making high mortgage payments every month, then to lower the payments you may want to go in for a long term mortgage. However, note that this will lead to an increase in the time you will take to completely pay off the mortgage. Also, consider the amount you will be paying as total interest over the new loan term, which will be quite high.

decrease The Length of The MortgageMortgages with shorter terms, take for example a 15 year mortgage, will carry a lower rate of interest compared to a mortgage that goes on for 30 years.Another advantage is that you will be paying off your loan quicker, reducing the total interest paid. But a short term mortgage comes with its costs. Your monthly payments will be higher because every month you will be paying more toward the principal.

To illustrate the above, let’s compare a loan of $200,000 for 30 years at a fixed rate of 6% with a loan for 15 years at a fixed rate of 5.5%.

Note that you can decrease the mortgage term by other ways also. One of them is by paying extra toward the principal every month. Like this, you will pay off the loan quicker and also reduce the time it will take to pay the mortgage.

Type of Refinance loan inTeResT (ToTal) payMenT (MonThly)

30 years at 6% $231,640.00 $1,199.00

15 years at 5.5% $94,120.00 $1,634.00

04www.usmortgage.com

changing To a fixed RaTe MoRTgage fRoM an adjusTable RaTe MoRTgage

In the case of an adjustable rate mortgage (ARM), as the rate of interest changes at regular intervals, the monthly payments also change. If you have this type of mortgage, your monthly payments can either decrease or increase depending on the market.

Many people are not comfortable with the idea of an increased monthly payment. If you have this worry, you can think about shifting to a fixed rate mortgage to take advantage of the steady monthly payments and fixed rate of interest. If you have reason to believe that interest rates could go up very soon, then you have to consider a fixed rate mortgage.

If your fixed rate monthly payments include payments into escrow accounts for insurance or taxes, note that your monthly payments could change when insurance or property taxes change.

going In For an arM on Better termsIf fixed mortgage rates are higher than adjustable mortgage rates in the market at a certain time, then an ARM can be a better option than a 30 year fixed rate mortgage. If you are paying for an ARM loan, see if the next adjustment in the interest rate will lead to a substantial increase in monthly payments. Then you could consider a new ARM with improved terms. The new loan may begin with a lower interest rate. This loan could carry lower adjustments on interest rates and even lower caps on payment. This helps if you don’t want the interest rate to exceed a given limit .

Note that if you are refinancing from one ARM into another, you must be aware of initial rates and fully indexed rates. Also, ask about adjustments to the rate that you might have to face, during the loan term .

05 www.usmortgage.com

If you have reason to believe that interest rates could go up very soon, then you have to consider a fixed rate mortgage.

www.usmortgage.com 06

calculaTe youR bReak even poinT

www.usmortgage.com07

If you are planning to stay in your mortgaged property even after retirement, you should seriously consider refinancing. But, if you are

planning to sell the house within some years, it may not be wise to refinance.

A good estimate of when to go for refinancing is to consider the break even point. The break even point for refinancing is the number of months you will have to keep the house to recoup your investments in the closing costs. For example, you calculate that you will be saving $100 every month after refinancing. You paid $3000 as closing costs. Now divide the closing costs by the monthly savings. This comes to 30 months. So you will have to keep your house for 30 months, after you refinance it, to cover the closing costs. If you plan to live in your home longer than this period, then refinancing can be a worthwhile decision.

So how do you calculate the monthly savings? Ask for an estimate on the rate that you will be qualifying for. The loan officer or the mortgage broker can tell you this. Try to find out the interest and the principal that you will have to pay on the loan .

Don’t compare this with the mortgage payment that you are currently paying. The current payment may include insurance and property tax payments. You can even get this from the payment statement. This way you can get an idea of how much you can save monthly.

08www.usmortgage.com

Refinancing To geT The equiTy

FroM Your HoMe

Home equity is the difference between the property value and the outstanding mortgage

principal. When you refinance for an amount more than the mortgage balance left on the home, you can get the difference in the form of a cash payment. This is known as cash-out refinance. You can go in for this when you want to make some improvements in your home or if you want to pay for your child’s education.

But you should not forget that after you cash in on the equity in your home and sell your home in the future, you may not get as much money as you could have. If you are refinancing to get equity out, there are some other alternatives that you can think about. You can go in for a home equity loan or a line of credit. Compare the equity loan with the cash out refinance and see which option is better.

Note that refinancing to cash out equity is frowned upon by many in the industry, especially if you want to use the cash to pay unsecured debt (such as credit cards) or even secured loans such as a car loan. Before you choose this plan, you should seek an expert’s advice .

09 www.usmortgage.com

check foR hidden cosTs

See if your current mortgage contract has a prepayment clause. If it does, you will have to make allowances for it too when you refinance. Prepayments can go up to six months of interest payments.

Some of the costs that will usually be included in a refinance are application fee (you may have to pay this fee even if the loan is eventually denied - could be up to $300), loan origination fee, attorney fee, appraisal fee, inspection fee, extra insurance fee, recording fee, survey fee, mortgage insurance, underwriting fee, title insurance fee, and other fees.

Another important fee is points. One point is one percent of the mortgage amount. Points can go up to 3% of the loan amount. Points are of two kinds. The first one is loan discount point - a one-time fee to reduce the rate of interest on the loan. The second kind is charged by brokers and lenders to earn cash. You can possibly sit with your lender and negotiate the points.

If you are not careful, you can end up paying up to 6% of your outstanding principal in refinance fees.

So, when you are looking for a refinance, start with your current mortgage company. Many companies have marketing programs specially designed for existing customers (to retain them by offering low rates or no-cost refinance options).

Even when your lender offers you a deal that you like, you should use that deal as a benchmark and look around for better deals. For help and information, you can ask your family members, real estate agents, co-workers, and other people who you trust, especially those who’ve recently gone in for a refinance.

10www.usmortgage.com

When noT To Refinance

11 www.usmortgage.com

during Later Years of a Mortgage Every year, more and more of your monthly payments will go toward paying the principal, while interest payments will decrease. Therefore, in later years of a mortgage, more of the payments will apply to the principal, thereby helping you build equity. If you refinance late in your mortgage, the amortization process restarts. Again, more of the payments every month will get credited to interest and not to the principal to build equity.

When The Mortgage Carriesa Prepayment PenaltyIf you are refinancing with your lender, ask if they can waive off the prepayment penalty. If not, carefully consider the savings you will gain by refinancing. Prepayment penalties may increase the break even period.

When You are Planning to Move away From The Home In a Few YearsYour monthly savings from low payments may not offset the refinancing costs quickly. Do a break even analysis to understand if it will be worth your while to refinance the house in case you are planning to move out in the nearby future.

12www.usmortgage.com

201 Old Country Road, Suite 140Melville, NY 11747

On US: [email protected] • www.USMortgage.com

coRpoRaTe office

19942014