understanding the vodacom bee dealsept2008gminvestments.co.za/backup/events/understanding the...

TRANSCRIPT

UNDERSTANDING THE VODACOM BEE TRANSACTIONCraig Gradidge and Kagisho Mahura

AGENDA

¢ Welcome and Intro

¢ GMI Update

¢ Investment Context – key principles

¢ Vodacom BEE Transaction (YeboYethu)

¢ Admin Processes

Cyril RamaphosaForeword in Visions of Black Economic Empowerment2007

“Broad-base BEE comes not only with rewards

but also with responsibility. As BEE evolves, it

will have to be the responsibility of all those

that are empowered to contribute to the

broadening and deepening of economic

empowerment across society.”

GRADIDGE-MAHURA INVESTMENTS

A diversified investment advisory company

Investment Sub-advisory

Asset Management Consulting

Financial Education Services

Wealth Management

A diversified investment portfolio

•Unit Trusts•BEE Transactions

•Offshore Investments•Share Portfolios

Private Equity•ETFs (Satrix)

• Alternatives (Hedge Funds)

Investment Management

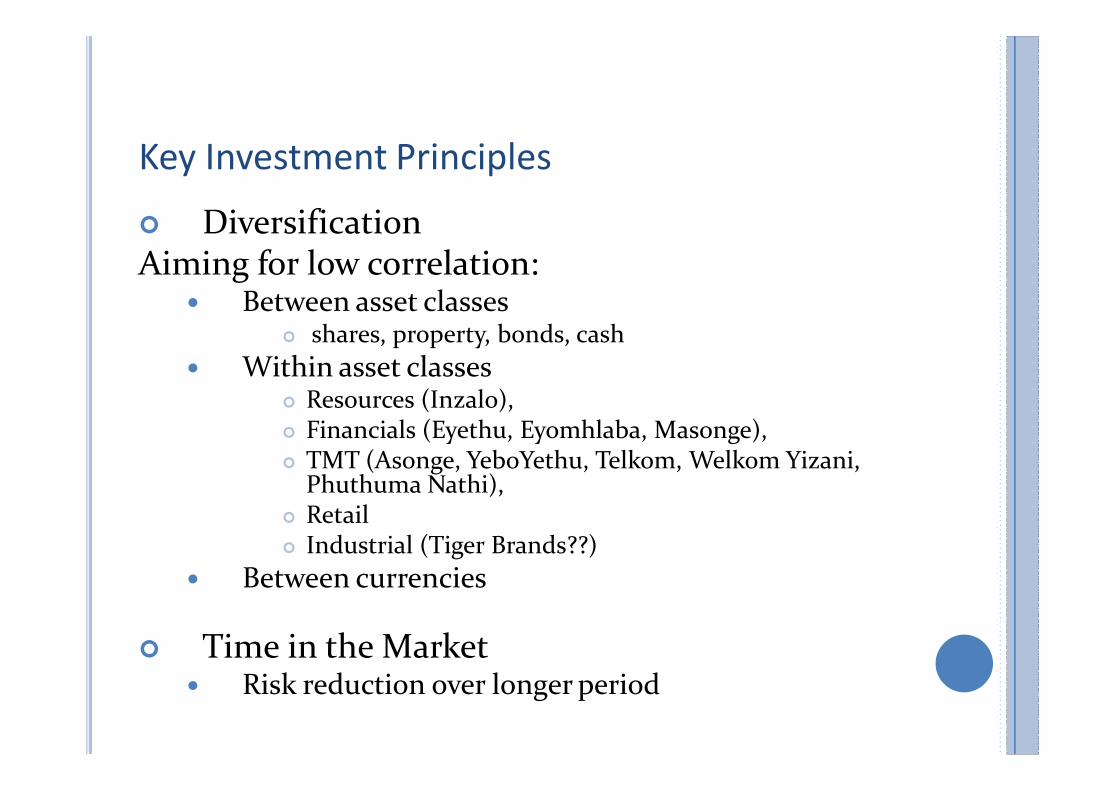

Key Investment Principles

¢ DiversificationAiming for low correlation:

� Between asset classes ¢ shares, property, bonds, cash

� Within asset classes¢ Resources (Inzalo), ¢ Financials (Eyethu, Eyomhlaba, Masonge), ¢ TMT (Asonge, YeboYethu, Telkom, Welkom Yizani,

Phuthuma Nathi), ¢ Retail¢ Industrial (Tiger Brands??)

� Between currencies

¢ Time in the Market� Risk reduction over longer period

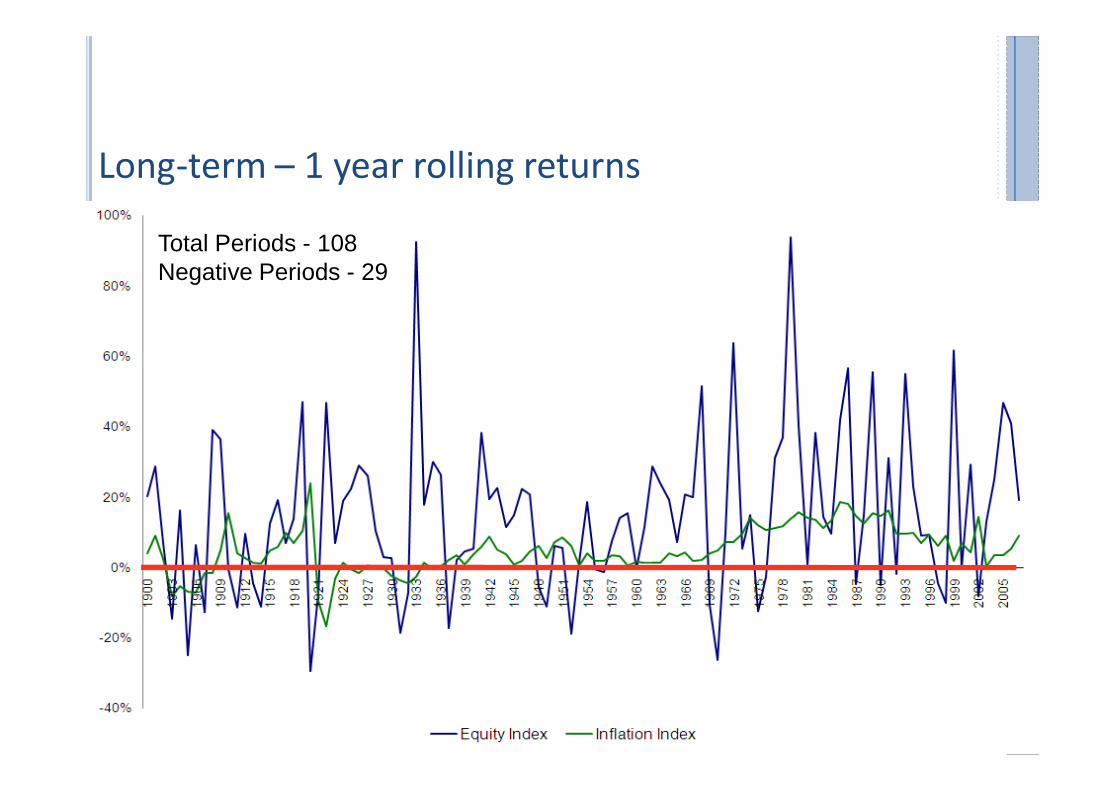

Long-term – 1 year rolling returns

Total Periods - 108Negative Periods - 29

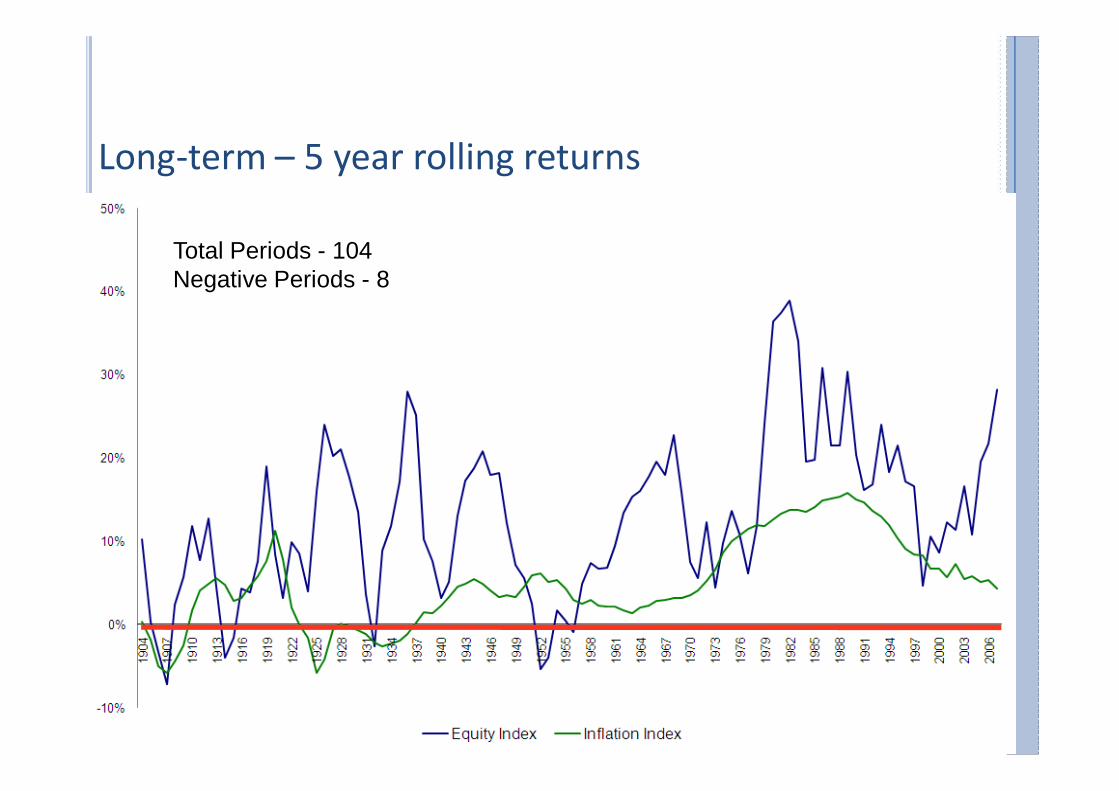

Long-term – 5 year rolling returns

Total Periods - 104Negative Periods - 8

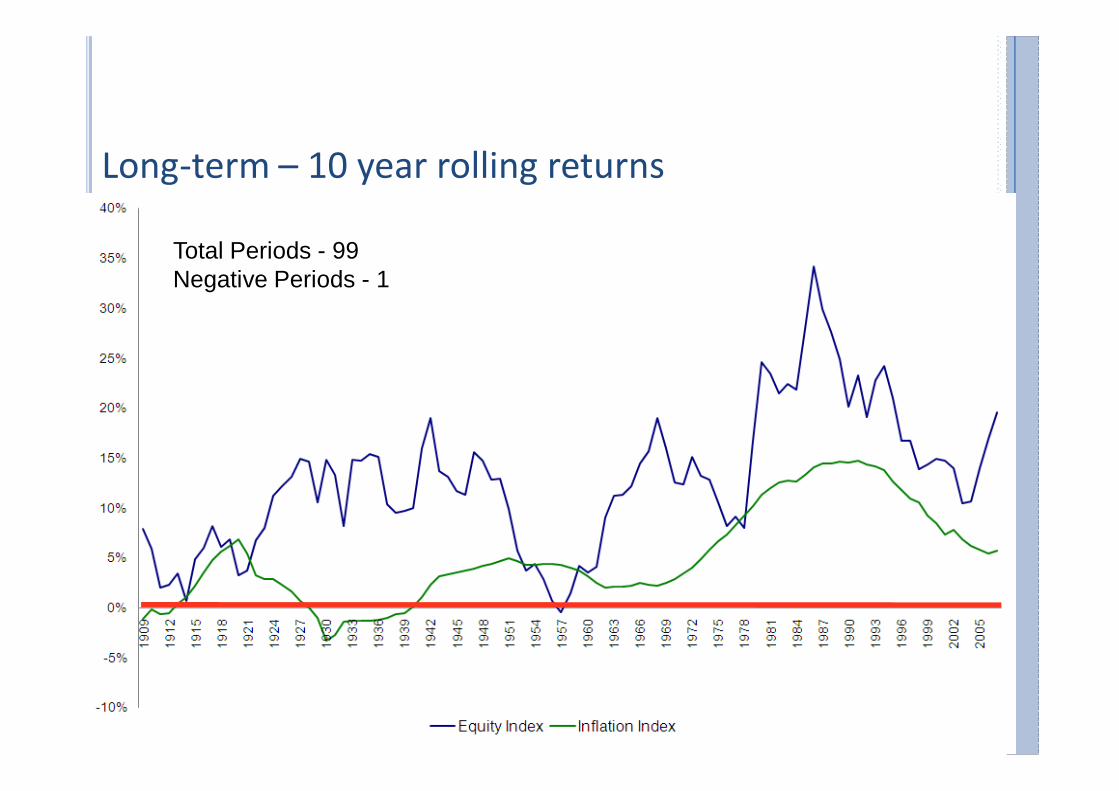

Long-term – 10 year rolling returns

Total Periods - 99Negative Periods - 1

UPDATE ON PREVIOUS SCHEMES

YeboYethu

Vodacom SA

Black Public ESOP

Vodacom Group YeboYethu Thebe Royal Bafokeng

45%55%

93.75% 3.44% 0.84% 1.97%

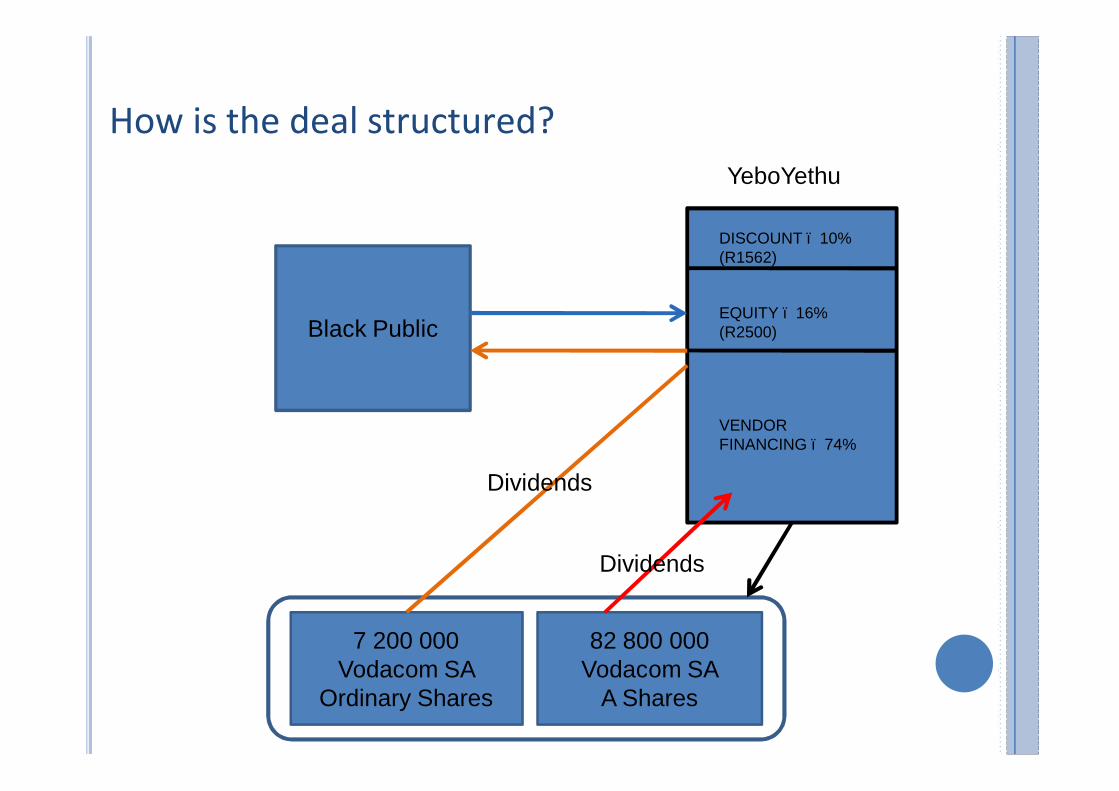

How is the deal structured?

DISCOUNT – 10% (R1562)

EQUITY – 16% (R2500)

VENDOR FINANCING – 74%

YeboYethu

Black Public

7 200 000Vodacom SA

Ordinary Shares

82 800 000 Vodacom SA

A Shares

Dividends

Dividends

YeboYethu

¢ Subscribe for shares in YeboYethu

¢ Shares sold at R25 each and in multiples of 100.

¢ Min 100 shares (R2500), max 1,440,000 (R36m)

¢ Total value of the deal – R2.2bn

¢ Can start trading after 5 years with other black investors

¢ Seven-year vendor financing facilitation period

¢ Unrestricted trading after 10 years

¢ Receive dividends from year 1!

WHERE SHOULD ONE PITCH EXPECTATIONS?

¢ Looking forward: need to make assumptions about

the future

¢ Vodacom: assumptions we made

� Growth Rate (of Vodacom profits)

� Dividend Policy (what % of profits paid as dividends)

� PE rating (value of Vodacom as a multiple of profits)

� Inflation (average rate over the period)

¢ As always – rather make conservative assumptions

¢ These are only illustrative figures

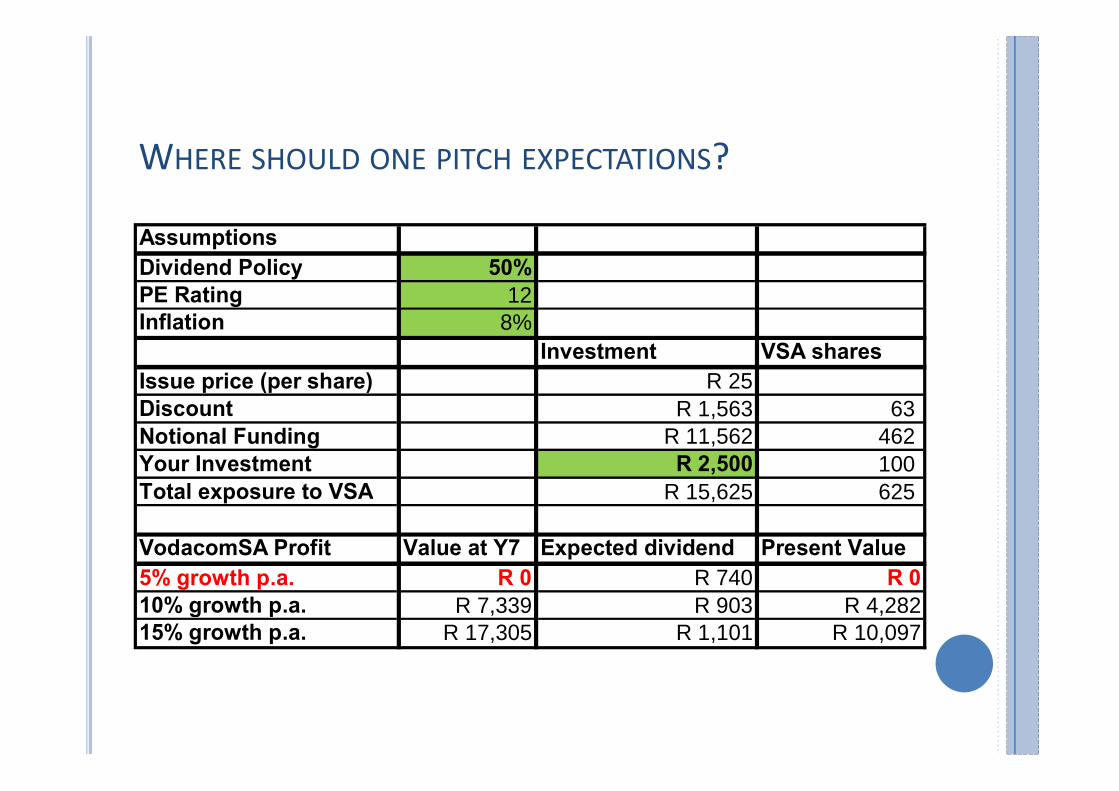

WHERE SHOULD ONE PITCH EXPECTATIONS?

AssumptionsDividend Policy 50%PE Rating 12Inflation 8%

Investment VSA sharesIssue price (per share) R 25Discount R 1,563 63 Notional Funding R 11,562 462 Your Investment R 2,500 100 Total exposure to VSA R 15,625 625

VodacomSA Profit Value at Y7 Expected dividend Present Value5% growth p.a. R 0 R 740 R 010% growth p.a. R 7,339 R 903 R 4,28215% growth p.a. R 17,305 R 1,101 R 10,097

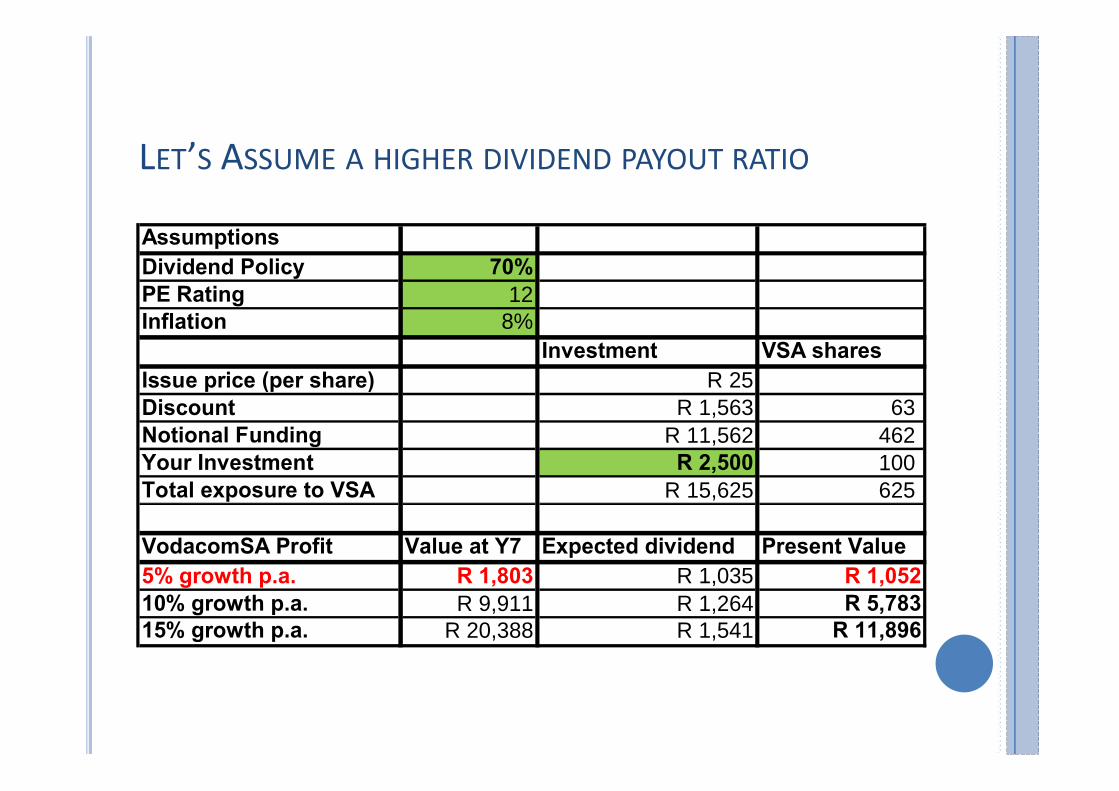

LET’S ASSUME A HIGHER DIVIDEND PAYOUT RATIO

AssumptionsDividend Policy 70%PE Rating 12Inflation 8%

Investment VSA sharesIssue price (per share) R 25Discount R 1,563 63 Notional Funding R 11,562 462 Your Investment R 2,500 100 Total exposure to VSA R 15,625 625

VodacomSA Profit Value at Y7 Expected dividend Present Value5% growth p.a. R 1,803 R 1,035 R 1,05210% growth p.a. R 9,911 R 1,264 R 5,78315% growth p.a. R 20,388 R 1,541 R 11,896

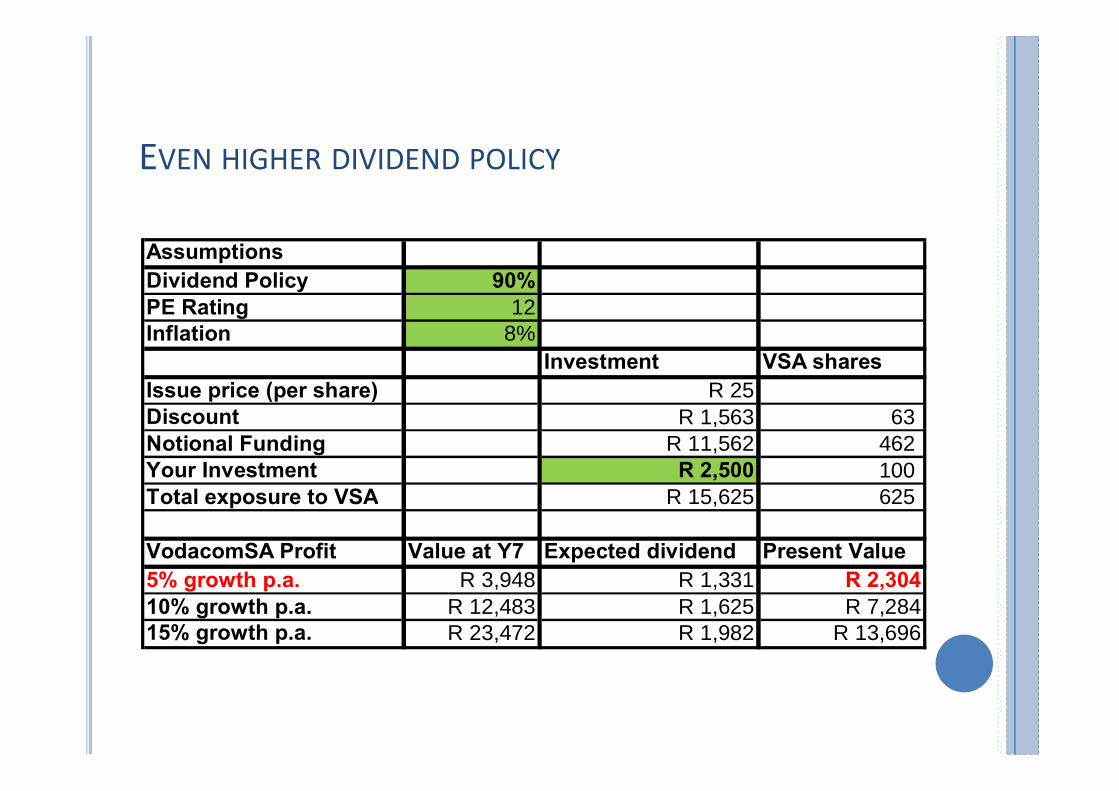

EVEN HIGHER DIVIDEND POLICY…

AssumptionsDividend Policy 90%PE Rating 12Inflation 8%

Investment VSA sharesIssue price (per share) R 25Discount R 1,563 63 Notional Funding R 11,562 462 Your Investment R 2,500 100 Total exposure to VSA R 15,625 625

VodacomSA Profit Value at Y7 Expected dividend Present Value5% growth p.a. R 3,948 R 1,331 R 2,30410% growth p.a. R 12,483 R 1,625 R 7,28415% growth p.a. R 23,472 R 1,982 R 13,696

Vodacom SA

Is the largest mobile communications network operator in South Africa, by both number of customers and

revenue. The company is dominant in its market and enjoys a market share of 55%. It offers a range of

mobile voice and data communication products. The company has an awesome track record of innovation with a number of firsts nationally and internationally

over the years.

Prospects – Vodacom SA

¢ Expanding Data and Content Service Offering

� MMS, internet, 3G, HSDPA, etc

¢ Vodacom Business

� Converged technology and communication services

¢ Mobile Advertising

¢ International Data Transmission

� Undersea cabling

Risks – Vodacom SA

¢ Mature market – fewer growth opportunities� Approx 60% of revenue from airtime sales

¢ Increased competition� MTN, Cell C, Virgin Mobile, Telkom?

¢ Disruptive technology¢ Pre-paid sales more sensitive to economic cycle

� 85% of Vodacom SA sales

¢ Regulatory environment changes¢ Currency risks

� Making imported equipment more expensive

¢ Health risks

Risks - YeboYethu

¢ No capital protection

¢ Limited liquidity when trading shares

¢ No regularly quoted share price – first 5 years

¢ Dividend does not fully cover outstanding debt

¢ Risks to Vodacom (as discussed above)

Unlisted shares

• Shares that are not listed or traded on a stock market • Trade “over-the-counter” on a trading platform• Participants on this platform usually have to register before

being able to trade• Advantages:

• Company does not incur cost of listing on stock market • Usually less volatile share prices

• Disadvantages:• Illiquid market• Price discovery – hampered by liquidity, and sometimes

subjected to third party valuation

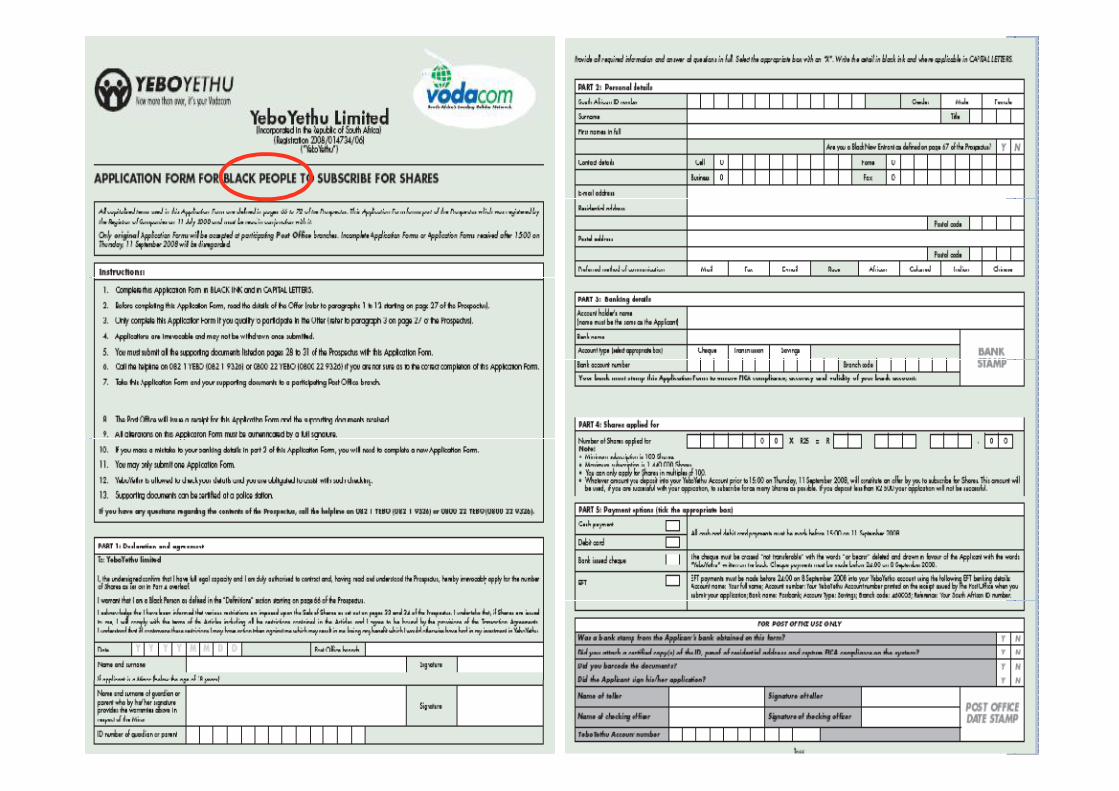

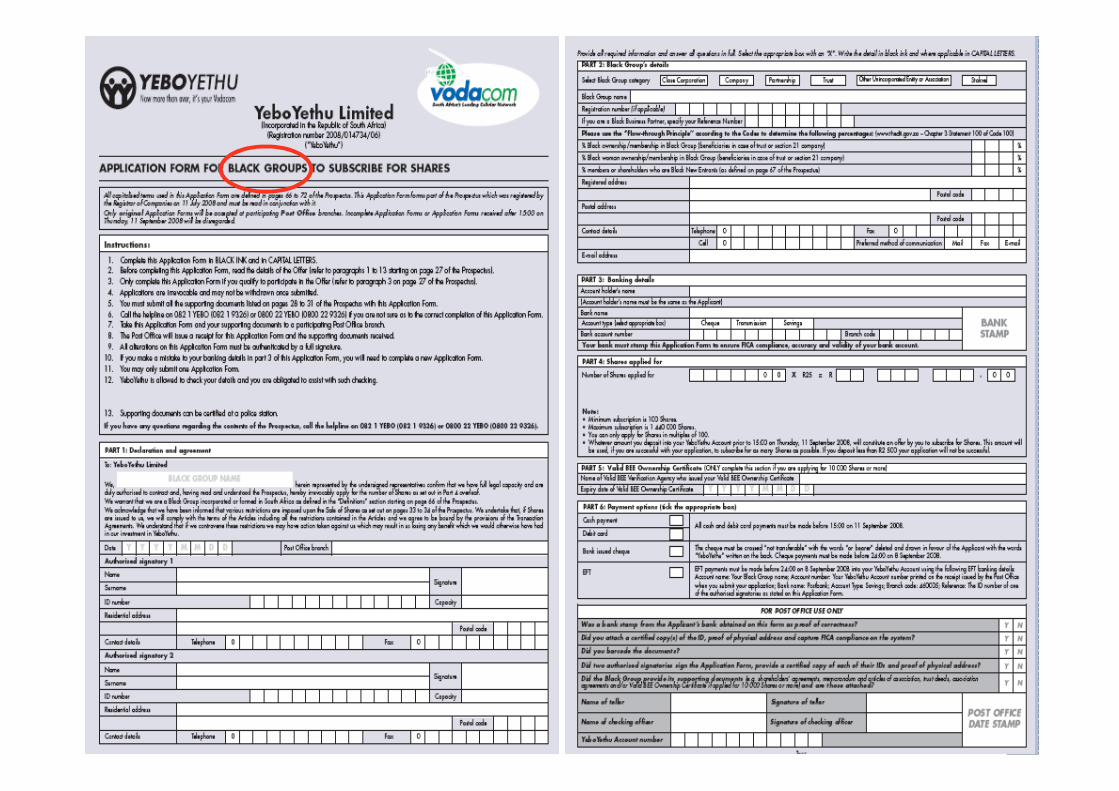

Requirements

¢ Offer opened 30 July 2008 and closes at 15:00 on 11 September 2008

¢ The prospectus containing application forms is available from Post Offices until 11 September 2008

¢ Only original Application Forms will be accepted.

� NOT those printed from YeboYethu’s website or photocopies!

¢ Black minors (under 18 yrs) can apply

� but must be assisted by a guardian and

� have a bank account in their own name

APPLICATION PROCESS

¢ Complete application form and sign

� Have application stamped at your bank (go with ID)

� Take application, certified copy of ID, proof of residence

to Post Office

� System generates temporary YeboYethu account.

� Please Note – EFT and Bank issued cheque payments

must be made before 8 September 2008!

¢ Keep record of all payments safe in case of disputes

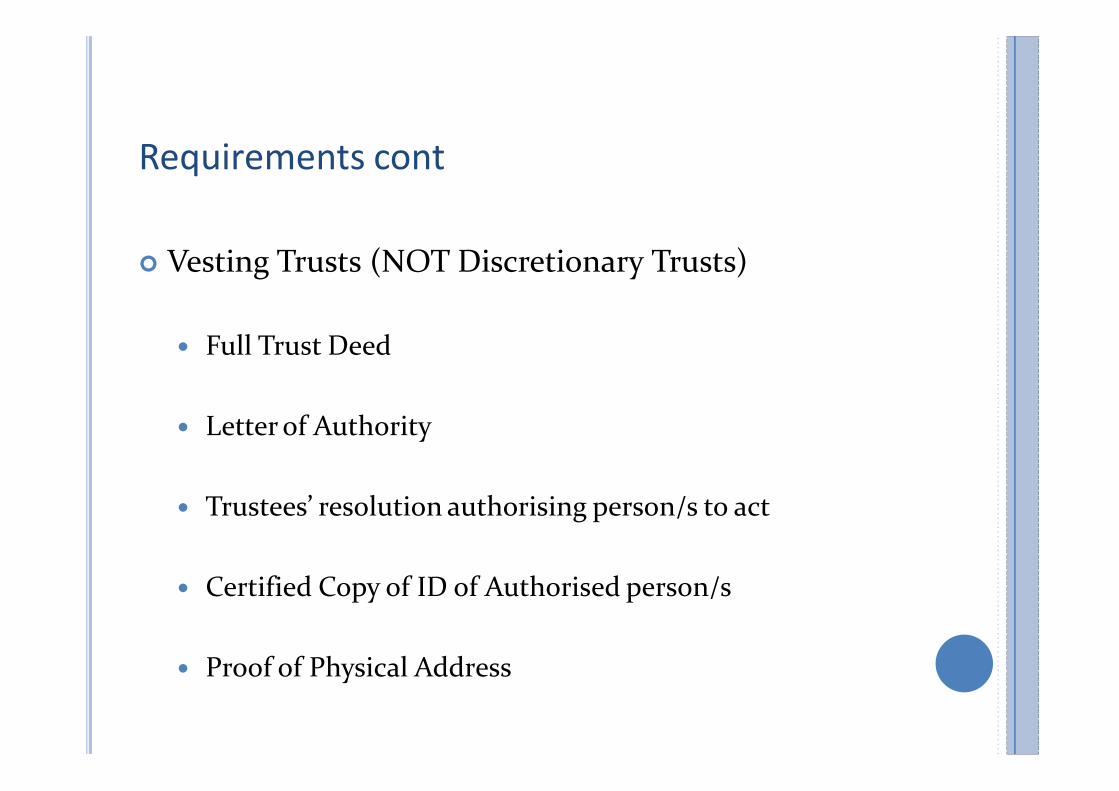

Requirements cont…

¢ Vesting Trusts (NOT Discretionary Trusts)

� Full Trust Deed

� Letter of Authority

� Trustees’ resolution authorising person/s to act

� Certified Copy of ID of Authorised person/s

� Proof of Physical Address

Requirements cont…

¢ Close Corporations

� CK1 – certificate of incorporation

� CK 2 – amended founding statement (if applicable)

� Members’ resolution authorising person/s to act

� Certified Copy of ID of Authorised person/s

� Proof of Physical Address

Requirements cont…

¢ Partnerships

� Partnership agreement

� Partners’ resolution authorising person/s to act

� Certified Copy of ID of Authorised person/s

� Proof of Physical Address

Requirements cont…

¢ Unincorporated Associations e.g. Stokkie

� Constitution

� Members’ resolution authorising person/s to act

� Certified Copy of ID of Authorised person/s

� Proof of Physical Address

Disclaimer

This presentation does not constitute advice.

While all due care has been taken to ensure accuracy of the content of

this presentation, neither Craig Gradidge, Kagisho Mahura nor

Gradidge–Mahura Investments (Pty) Ltd accept any liability for any

loss that may be suffered by anyone who relied directly or indirectly

on all or part of this presentation.

GMI is a representative of Renaissance Specialist Fund Managers

(FSP 25033)

THANK YOU

Kagisho Mahura: 082 494 7480, [email protected]

Craig Gradidge: 079 885 6215 [email protected]

A bit on vendor financing

Existing company(Vendor) New Company

Option: Borrow from the bank

• Two things: • Security• Affordability

• Main challenges:• Personal security• Interest rate risk• Banks usually demand marketable assets as security • Debt stands even if business falls over

A bit on vendor financing

Existing company(Vendor) New Company

Alternative option: Existing company provides funding

• Offer debt usually at favourable rate to New Company• Vendor sometimes guarantees dividend flow• Attractive option if vendor has record of paying high dividends• Positives:

• vendor does not need to convince itself that it is a good company• Deals can be structured on favourable terms• If deal falls flat, parties walk away – no outstanding debt!