bm&fbovespair.bmfbovespa.com.br/enu/568/itauconferencepresentation...and uncertainties that...

TRANSCRIPT

BM&FBOVESPAMay 2009May, 2009

1

Forward Looking Statements

This presentation may contain certain statements that express the management’s expectations, beliefs and assumptions about future events or results. Such statements are not historical fact, being based on currently available competitive, financial and economic data, and on current projections about the industries BM&F Bovespa works in.The verbs “anticipate,” “believe,” “estimate,” “expect,” “forecast,” “plan,” “predict,” “project,” “target” The verbs anticipate, believe, estimate, expect, forecast, plan, predict, project, target and other similar verbs are intended to identify these forward-looking statements, which involve risks and uncertainties that could cause actual results to differ materially from those projected in this presentation and do not guarantee any future BM&F Bovespa performance.The factors that might affect performance include, but are not limited to: (i) market acceptance of BM&F services; (ii) volatility related to (a) the Brazilian economy and securities markets and (b) the highly-services; (ii) volatility related to (a) the Brazilian economy and securities markets and (b) the highlycompetitive industries BM&F Bovespa operates in; (iii) changes in (a) domestic and foreign legislation and taxation and (b) government policies related to the financial and securities markets; (iv) increasing competition from new entrants to the Brazilian markets; (v) ability to keep up with rapid changes in technological environment, including the implementation of enhanced functionality demanded by BM&F customers; (vi) ability to maintain an ongoing process for introducing competitive new products and ; ( ) y g g p g p pservices, while maintaining the competitiveness of existing ones; (vii) ability to attract new customers in domestic and foreign jurisdictions; (viii) ability to expand the offer of BM&F Bovespa products in foreign jurisdictions.All forward-looking statements in this presentation are based on information and data available as of the date they were made, and BM&F Bovespa undertakes no obligation to update them in light of new information or future development.This presentation does not constitute an offer to sell or the solicitation of an offer to buy any securities, nor shall there be any sale of securities where such offer or sale would be unlawful prior to registration or qualification under the securities law. No offering shall be made except by means of a prospectus meeting the requirements of the Brazilian Securities Commission CVM Instruction 400 of 2003, as

2

amended.

BRAZILIAN AND INTERNATIONAL MARKET CONDITIONS

3

International ScenarioGroup of 30 (G30)

GROUP OF 30: Financial Report – A Framework for Financial StabilityChairman: Paul VockerVice-chairmans: Armínio Fraga Neto (BM&FBOVESPA Chairman) and Tomaso Padua Schiopa

• Main proposals

“…derivatives markets be held to regulatory, disclosure, and transparency standards at least comparable to those that have historically been applied to the public securities markets.”

“…Financial markets and products must be made more transparent, with better aligned risk and prudential incentives.”

“…problems include trade confirmation backlogs, lack of transparency on transaction reporting and pricing, contract closeout procedures, valuation practices and collateral disputes, and direct and indirect counterparty credit issues.”

“Prominent within that program are efforts to establish a central counterparty clearing (CCP) arrangement…”

“Given the global nature of the markets in which such managers and funds operate, it is imperative that a regulatory framework be applied on an internationally consistent basis.”

“Countries should reevaluate their regulatory structures with a view to eliminating unnecessary

4

Countries should reevaluate their regulatory structures with a view to eliminating unnecessary overlaps and gaps in coverage and complexity, removing the potential for regulatory arbitrage, and improving regulatory coordination.”

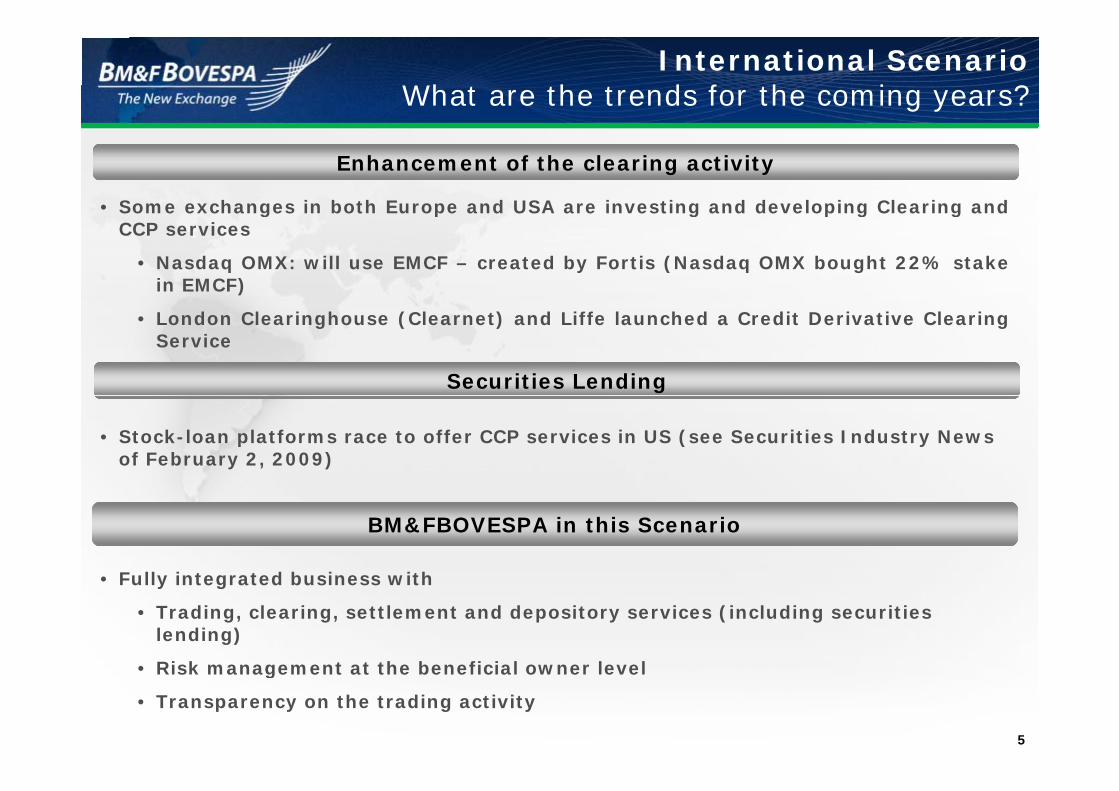

International ScenarioWhat are the trends for the coming years?

• Some exchanges in both Europe and USA are investing and developing Clearing and

Enhancement of the clearing activity

g p g p g gCCP services

• Nasdaq OMX: will use EMCF – created by Fortis (Nasdaq OMX bought 22% stakein EMCF)

• London Clearinghouse (Clearnet) and Liffe launched a Credit Derivative ClearingService

• CME launched its Clearing service (CDMX) for CDSsSecurities Lending

• Stock-loan platforms race to offer CCP services in US (see Securities Industry News of February 2, 2009)

Fully integrated business with

BM&FBOVESPA in this Scenario

• Fully integrated business with

• Trading, clearing, settlement and depository services (including securities lending)

Risk management at the beneficial owner level

5

• Risk management at the beneficial owner level

• Transparency on the trading activity

BUSINESS MODELBUSINESS MODEL

6

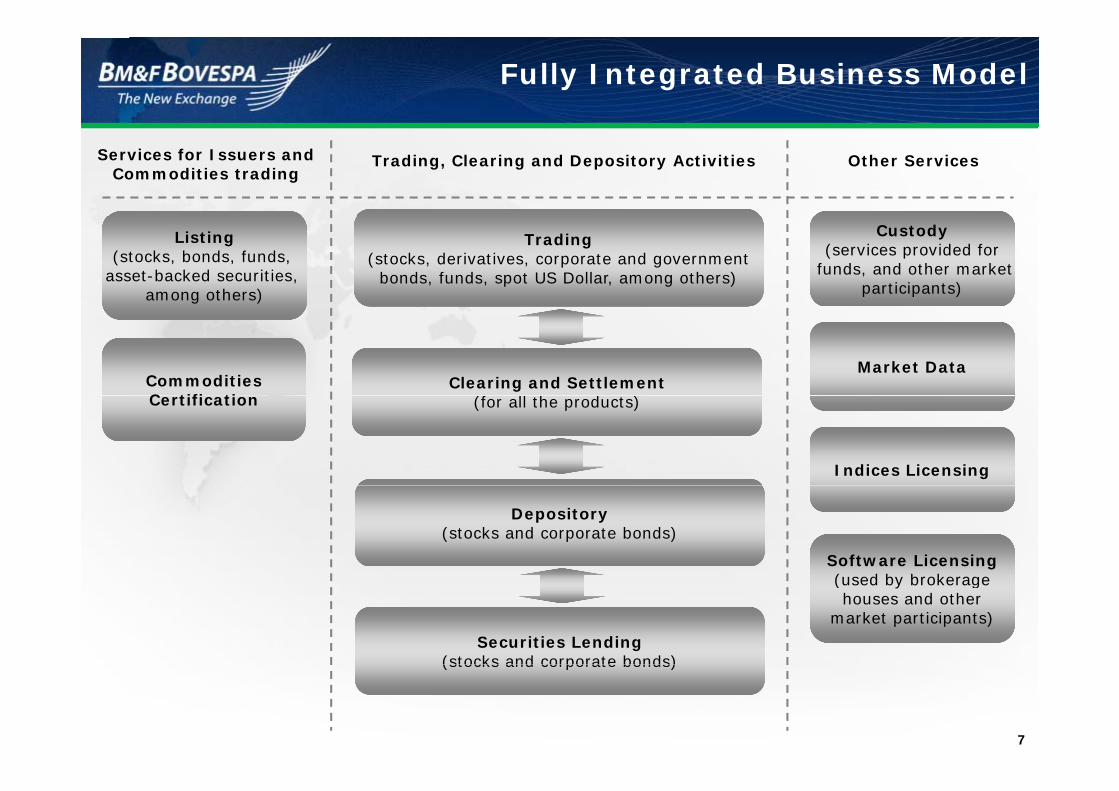

Fully Integrated Business Model

Services for Issuers andCommodities trading

Trading, Clearing and Depository Activities Other Services

Listing(stocks, bonds, funds,

asset-backed securities, among others)

Trading(stocks, derivatives, corporate and government

bonds, funds, spot US Dollar, among others)

Custody(services provided for

funds, and other marketparticipants)

CommoditiesC tifi ti

Clearing and Settlement(f ll h d )

Market Data

Certification (for all the products)

Indices Licensing

Depository(stocks and corporate bonds)

Software Licensing( d b b k

Securities Lending(stocks and corporate bonds)

(used by brokeragehouses and other

market participants)

7

(stocks and corporate bonds)

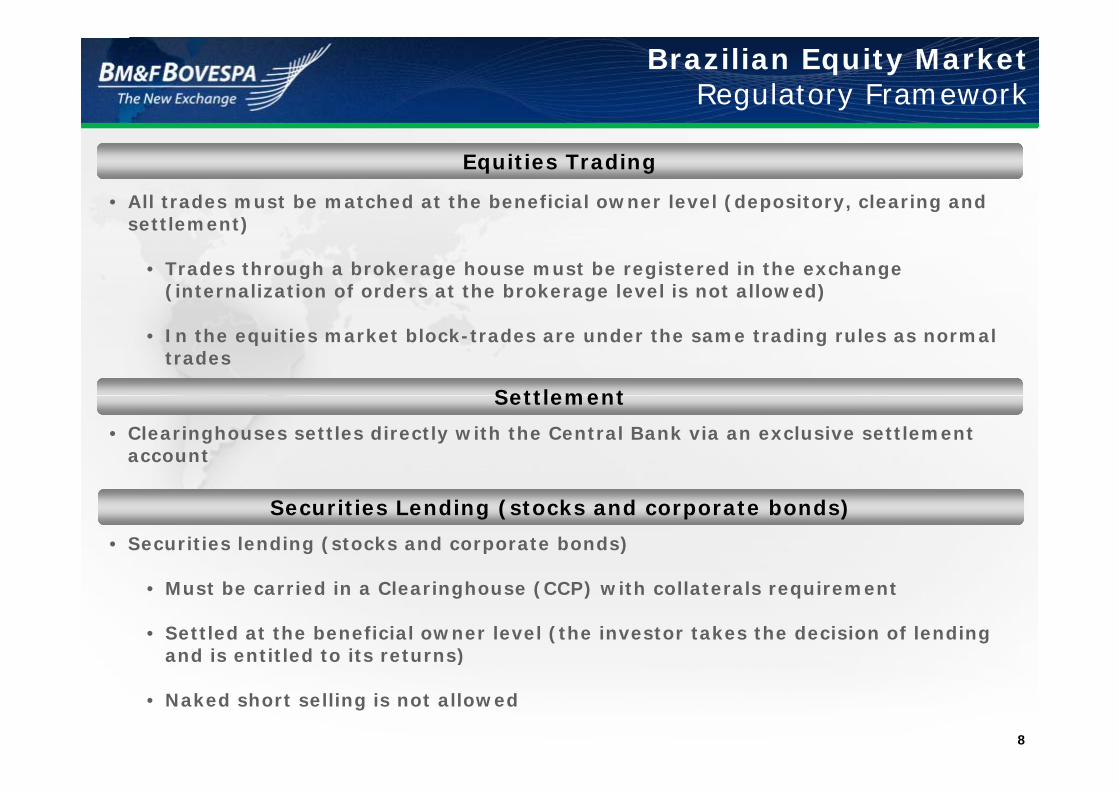

Brazilian Equity MarketRegulatory Framework

• All trades must be matched at the beneficial owner level (depository, clearing and

Equities Trading

settlement)

• Trades through a brokerage house must be registered in the exchange (internalization of orders at the brokerage level is not allowed)

• In the equities market block-trades are under the same trading rules as normal trades

Settlement

• Clearinghouses settles directly with the Central Bank via an exclusive settlement account

Settlement

• Securities lending (stocks and corporate bonds)

Securities Lending (stocks and corporate bonds)

• Must be carried in a Clearinghouse (CCP) with collaterals requirement

• Settled at the beneficial owner level (the investor takes the decision of lending and is entitled to its returns)

8

)

• Naked short selling is not allowed

Equity Market Settlement StructureBrazil compared with USA

BRAZIL US

OTC Dark Pools

Trading BVMF ATS ECN

OTC Dark Pools

Cl i (CCP)

NYSE NASDAQ

Clearing (CCP) BVMF

BVMF

DTCC

DTCC

C l

BVMF DTCC

Central DepositoryBroker Level

9

Beneficial Owner Level

Risk Management At the beneficial owner level

• Four Clearinghouses: derivatives, stocks and corporate bonds, FX spot and government bonds

• All of our Clearinghouses acts as CCP and manage the risk at beneficial owner level

• Mark to market (margin variation calls) done on intraday basis (each 15 minutes for derivatives market and ongoing for equity market)

Th b k h ( l i t) i ibl f it i th i li t ’ i k d • The brokerage house (clearing agent) is responsible for monitoring their clients’ risk and “know your customer policies”

• During the day any Clearinghouse can call additional collateral and the clearing agent is responsible for depositingresponsible for depositing

Clearinghouse Clearing Deposited(BRL billions)

Required(BRL billions)

Derivatives 71,4 34,1

ClearingAgent

ClearingAgent

, ,Cash Equities 26,7 16,6FX 3,7 0,8Fixed Income 1,0 0,0Total in BRL 102,7 51,5T t l i USD 49 1 24 6

Investor Investor Investor Investor

RiskManagement

Total in USD 49,1 24,6* On May 15, 2009

10

• There is no cross margining among the Clearinghouses

• Clearinghouses integration process: project kick off in 2009

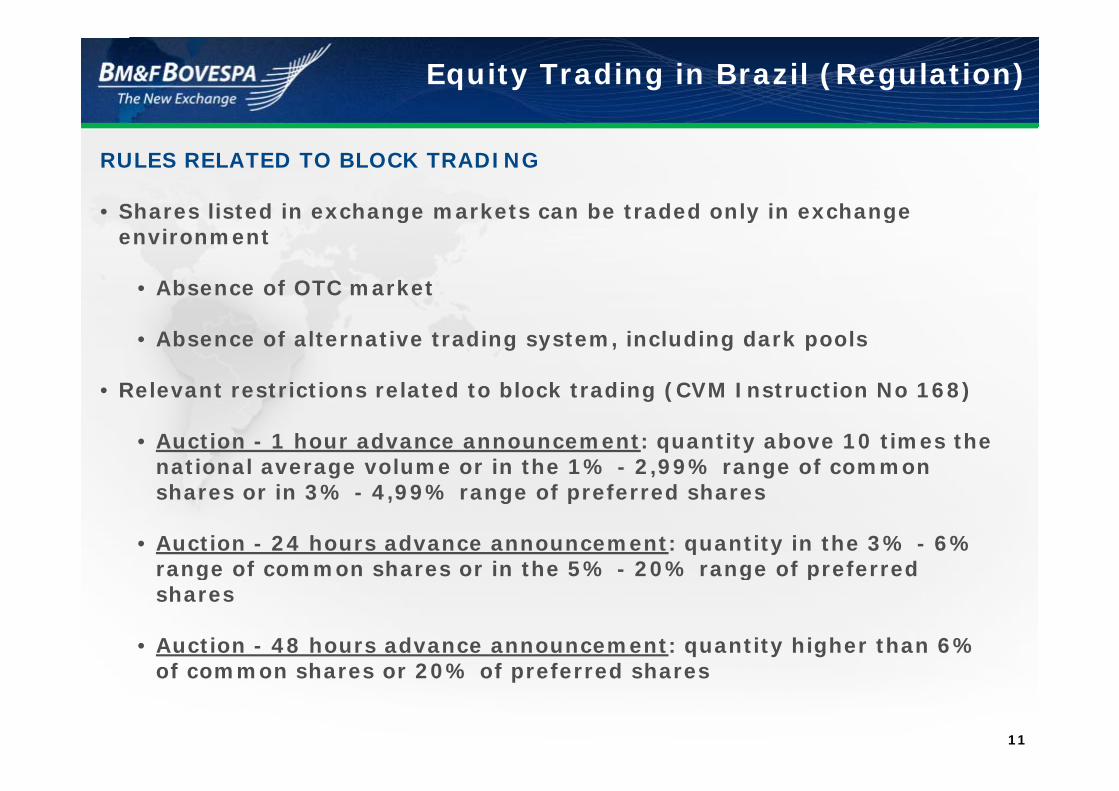

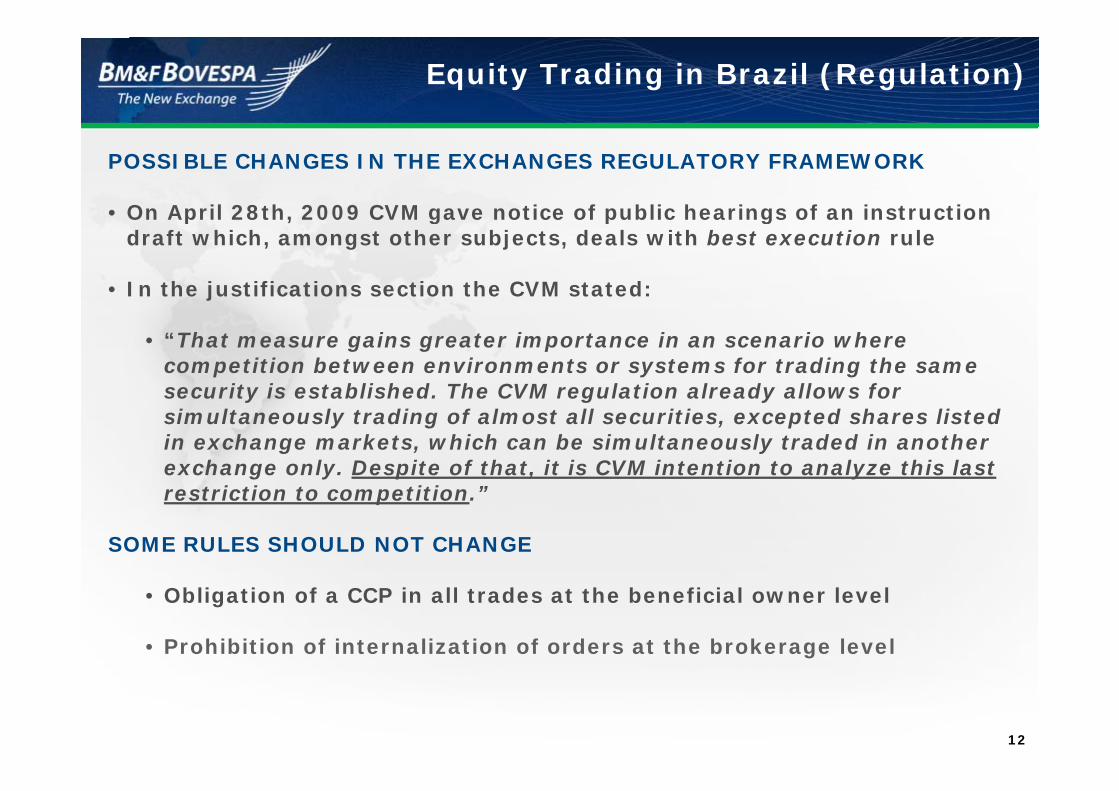

Equity Trading in Brazil (Regulation)

RULES RELATED TO BLOCK TRADING

• Shares listed in exchange markets can be traded only in exchange Shares listed in exchange markets can be traded only in exchange environment

• Absence of OTC market

• Absence of alternative trading system, including dark pools

• Relevant restrictions related to block trading (CVM Instruction No 168)Relevant restrictions related to block trading (CVM Instruction No 168)

• Auction - 1 hour advance announcement: quantity above 10 times the national average volume or in the 1% - 2,99% range of common h i 3% 4 99% f f d hshares or in 3% - 4,99% range of preferred shares

• Auction - 24 hours advance announcement: quantity in the 3% - 6% range of common shares or in the 5% - 20% range of preferred range of common shares or in the 5% 20% range of preferred shares

• Auction - 48 hours advance announcement: quantity higher than 6% f h 20% f f d h

11

of common shares or 20% of preferred shares

Equity Trading in Brazil (Regulation)

POSSIBLE CHANGES IN THE EXCHANGES REGULATORY FRAMEWORK

• On April 28th, 2009 CVM gave notice of public hearings of an instruction • On April 28th, 2009 CVM gave notice of public hearings of an instruction draft which, amongst other subjects, deals with best execution rule

• In the justifications section the CVM stated:

• “That measure gains greater importance in an scenario where competition between environments or systems for trading the same security is established. The CVM regulation already allows for security is established. The CVM regulation already allows for simultaneously trading of almost all securities, excepted shares listed in exchange markets, which can be simultaneously traded in another exchange only. Despite of that, it is CVM intention to analyze this last

i i i i ”restriction to competition.”

SOME RULES SHOULD NOT CHANGE

• Obligation of a CCP in all trades at the beneficial owner level

• Prohibition of internalization of orders at the brokerage level

12

Equity Trading in Brazil (Regulation)

BRAZILIAN SEC (CVM) RULE FOR EXCHANGE AND CLEARING COMPANIES

• CVM Instruction No 461 provides for the possibility of BVMF s u o o 6 p o d s o poss y oclearinghouse to settle trades matched outside BVMF trading systems

• Art.18 ... The managing entities of organized markets of securities h ld th l th f ll i h i d lshould agree upon themselves the following mechanisms and rules:

• I – ...

• II – that render the clearing and settlement of transactions effected outside their environments and trading systems

13

Equity Trading in Brazil (Regulation)

BVMF POSITIONING CONCERNING BLOCK TRADING REGULATION

• The Brazilian market has no efficient block trading mechanism, where The Brazilian market has no efficient block trading mechanism, where quantity discovery is more important than price discovery

• Brazilian ADRs are traded in alternative systems and dark pools in US

• BVMF could launch a platform designed for block trading with post trading services and CCP at the beneficial owner level

• BVMF can offer post trading services to other possible block trading providers

Bl k T di f• Block Trading frame:

• Minimization of the price impact due to large offers execution, making the large lot electronic trading viable and anonymousmaking the large lot electronic trading viable and anonymous

• Development of large lot liquidity in the BVMF system instead of in the brokers and banks trading desks

14

Exchanges and Block Trading SystemsBrazilian ADRs: Brazil vs. USA

THERE ARE 37 BRAZILIAN COMPANIES WITH ADRs PROGRAMS (LEVEL 2 AND LEVEL 3)

• Increase on Block Tradings’ share since 2007 while the NYSE share has been decreasing

Apr’09In Traded Value

32.4%

17.2%

27.9%

22.5%

15

OPERATIONAL FIGURESOPERATIONAL FIGURES

16

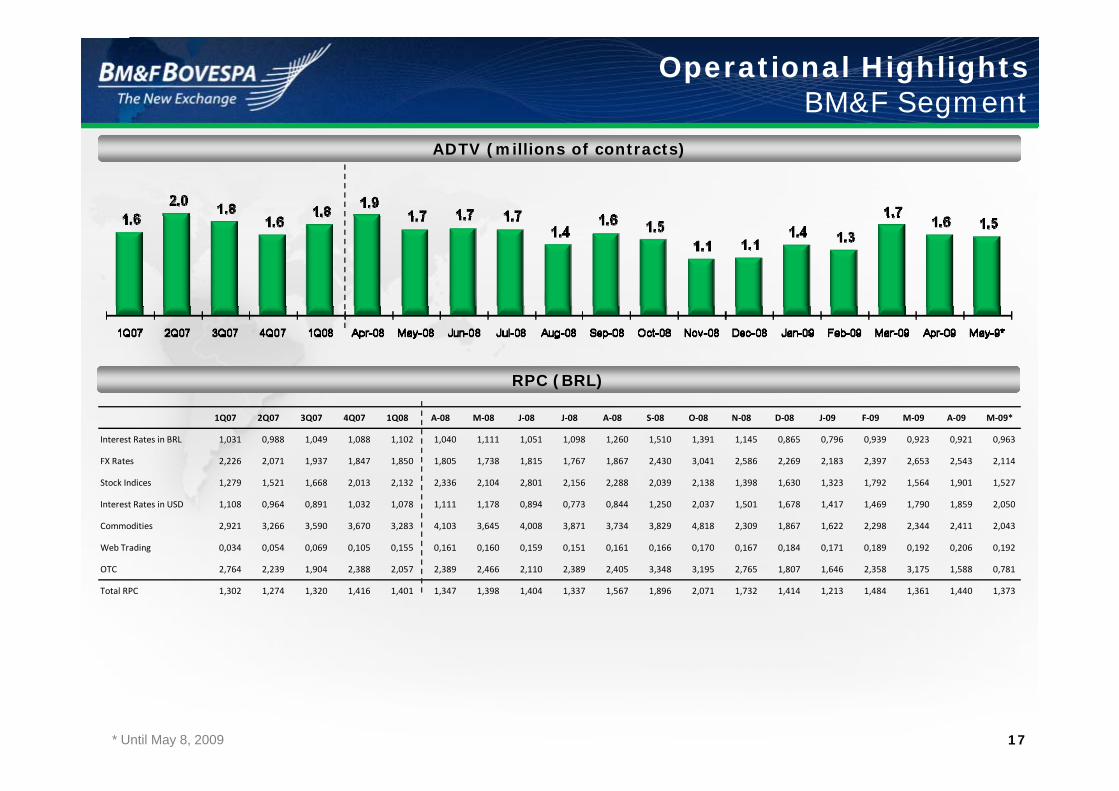

Operational HighlightsBM&F Segment

ADTV (millions of contracts)

RPC (BRL)

1Q07 2Q07 3Q07 4Q07 1Q08 A‐08 M‐08 J‐08 J‐08 A‐08 S‐08 O‐08 N‐08 D‐08 J‐09 F‐09 M‐09 A‐09 M‐09*

Interest Rates in BRL 1,031 0,988 1,049 1,088 1,102 1,040 1,111 1,051 1,098 1,260 1,510 1,391 1,145 0,865 0,796 0,939 0,923 0,921 0,963

FX Rates 2,226 2,071 1,937 1,847 1,850 1,805 1,738 1,815 1,767 1,867 2,430 3,041 2,586 2,269 2,183 2,397 2,653 2,543 2,114

Stock Indices 1,279 1,521 1,668 2,013 2,132 2,336 2,104 2,801 2,156 2,288 2,039 2,138 1,398 1,630 1,323 1,792 1,564 1,901 1,527Stock Indices 1,279 1,521 1,668 2,013 2,132 2,336 2,104 2,801 2,156 2,288 2,039 2,138 1,398 1,630 1,323 1,792 1,564 1,901 1,527

Interest Rates in USD 1,108 0,964 0,891 1,032 1,078 1,111 1,178 0,894 0,773 0,844 1,250 2,037 1,501 1,678 1,417 1,469 1,790 1,859 2,050

Commodities 2,921 3,266 3,590 3,670 3,283 4,103 3,645 4,008 3,871 3,734 3,829 4,818 2,309 1,867 1,622 2,298 2,344 2,411 2,043

Web Trading 0,034 0,054 0,069 0,105 0,155 0,161 0,160 0,159 0,151 0,161 0,166 0,170 0,167 0,184 0,171 0,189 0,192 0,206 0,192

OTC 2,764 2,239 1,904 2,388 2,057 2,389 2,466 2,110 2,389 2,405 3,348 3,195 2,765 1,807 1,646 2,358 3,175 1,588 0,781

Total RPC 1,302 1,274 1,320 1,416 1,401 1,347 1,398 1,404 1,337 1,567 1,896 2,071 1,732 1,414 1,213 1,484 1,361 1,440 1,373

17* Until May 8, 2009

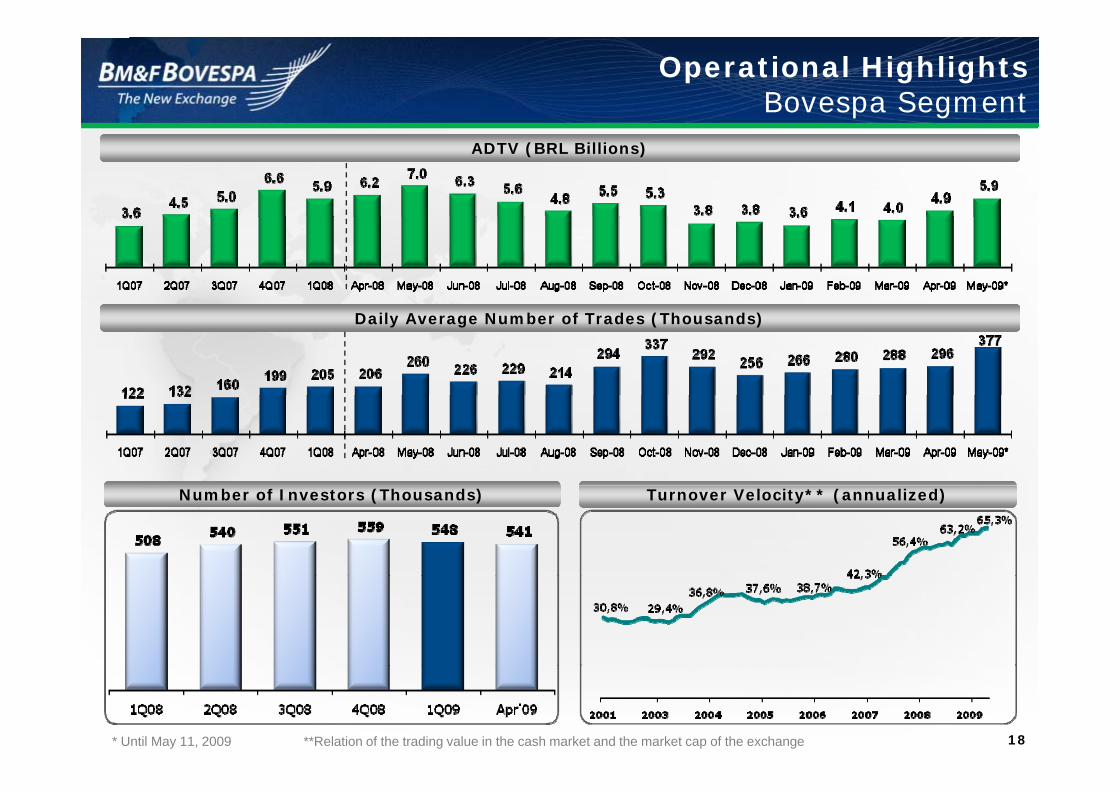

Operational HighlightsBovespa Segment

ADTV (BRL Billions)

Daily Average Number of Trades (Thousands)

Number of Investors (Thousands) Turnover Velocity** (annualized)

18* Until May 11, 2009 **Relation of the trading value in the cash market and the market cap of the exchange

Operational Highlights

BM&F Segment (Investor’s Participation in Total Volume)

Bovespa Segment (Investor’s Participation in Total Value)

19

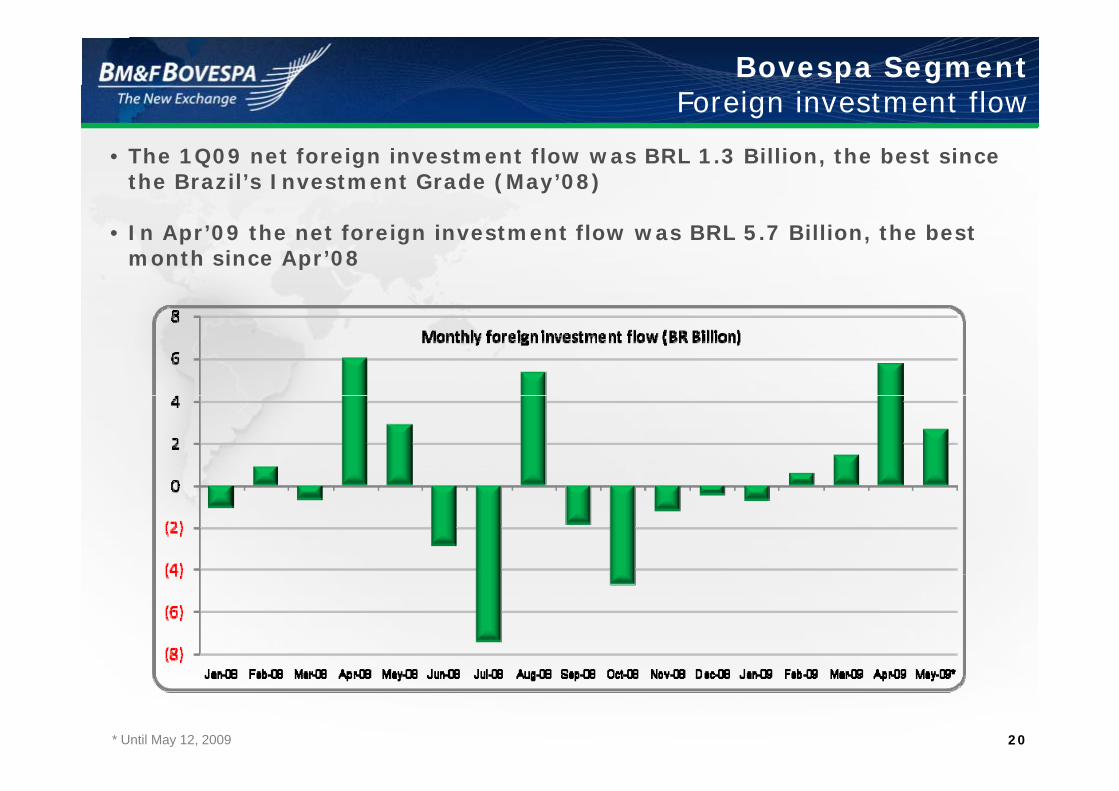

Bovespa SegmentForeign investment flow

• The 1Q09 net foreign investment flow was BRL 1.3 Billion, the best since the Brazil’s Investment Grade (May’08)

• In Apr’09 the net foreign investment flow was BRL 5.7 Billion, the best month since Apr’08

20* Until May 12, 2009

IT DEVELOPMENTSIT DEVELOPMENTS

21

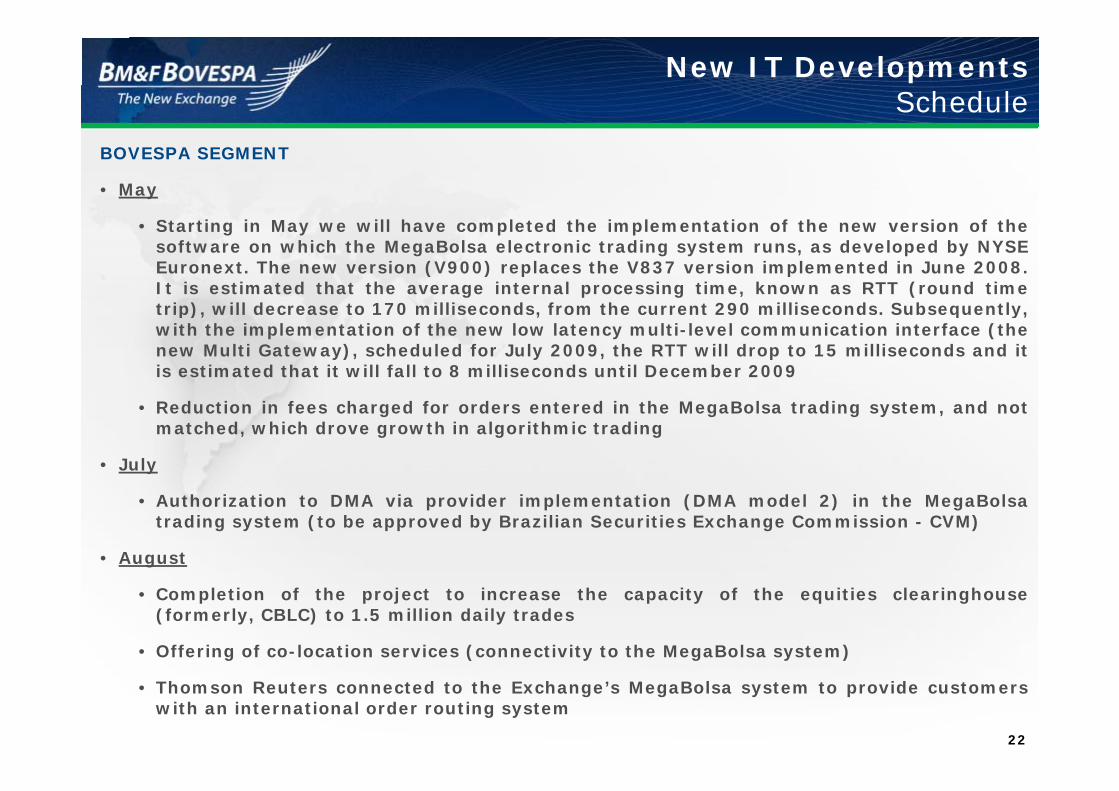

New IT DevelopmentsSchedule

BOVESPA SEGMENT

• May

• Starting in May we will have completed the implementation of the new version of thesoftware on which the MegaBolsa electronic trading system runs, as developed by NYSEEuronext. The new version (V900) replaces the V837 version implemented in June 2008.It is estimated that the average internal processing time, known as RTT (round timetrip) will decrease to 170 milliseconds from the current 290 milliseconds Subsequentlytrip), will decrease to 170 milliseconds, from the current 290 milliseconds. Subsequently,with the implementation of the new low latency multi-level communication interface (thenew Multi Gateway), scheduled for July 2009, the RTT will drop to 15 milliseconds and itis estimated that it will fall to 8 milliseconds until December 2009

• Reduction in fees charged for orders entered in the MegaBolsa trading system, and notmatched, which drove growth in algorithmic trading

• July

• Authorization to DMA via provider implementation (DMA model 2) in the MegaBolsatrading system (to be approved by Brazilian Securities Exchange Commission - CVM)

• August

• Completion of the project to increase the capacity of the equities clearinghouse(formerly, CBLC) to 1.5 million daily trades

• Offering of co-location services (connectivity to the MegaBolsa system)

22

• Thomson Reuters connected to the Exchange’s MegaBolsa system to provide customerswith an international order routing system

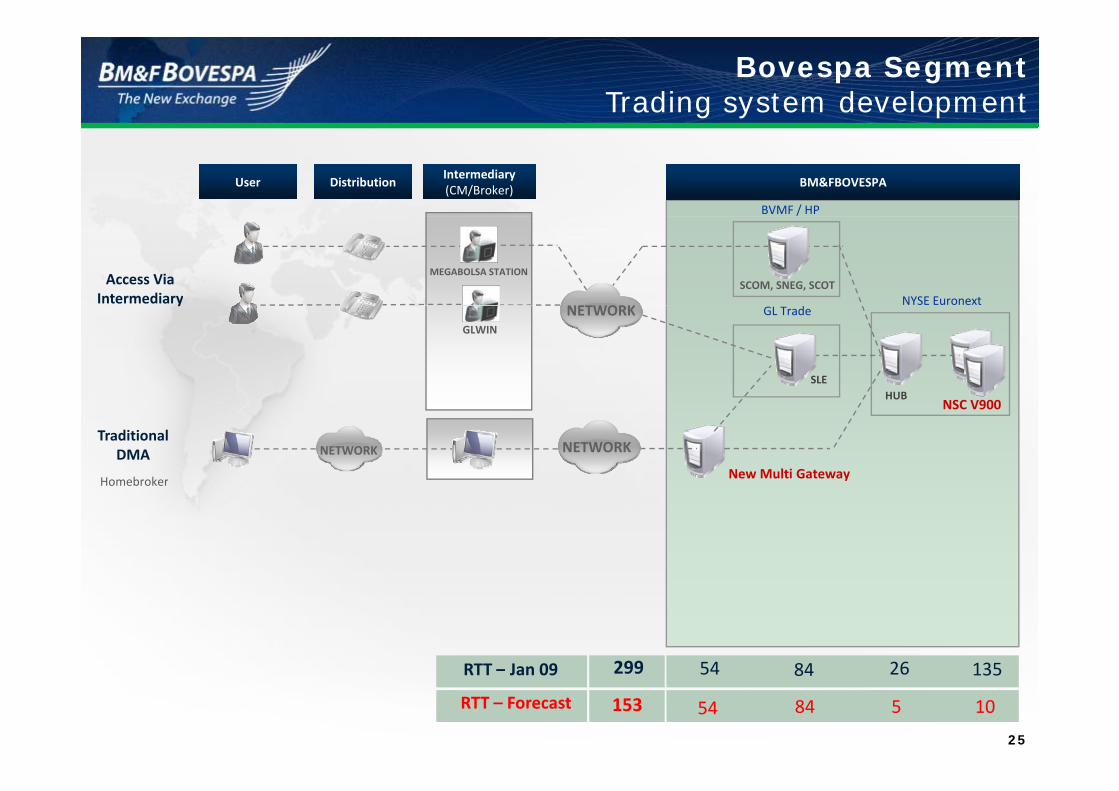

Bovespa SegmentTrading system development

User DistributionIntermediary(CM/Broker)

BM&FBOVESPA

BVMF / HP

MEGABOLSA STATIONSCOM, SNEG, SCOT

NYSE Euronext

Access Via Intermediary

NETWORK

SLE

GL Tradey

GLWIN

NETWORK

NSC V837HUB

Traditional DMA

Homebroker

NETWORK NETWORKMulti Gateway

NSC V837HUB

Homebroker

268454299RTT J 09 135

23

RTT – Forecast 54 135288 1584

268454299RTT – Jan 09 135

Bovespa SegmentTrading system development

User DistributionIntermediary(CM/Broker)

BM&FBOVESPA

BVMF / HP

MEGABOLSA STATIONSCOM, SNEG, SCOT

NYSE Euronext

Access Via Intermediary

NETWORK

SLE

GL Tradey

GLWIN

NETWORK

HUBNSC V900

Traditional DMA

Homebroker

NETWORK NETWORKMulti Gateway

HUB

Homebroker

268454299RTT J 09 135

24

RTT – Forecast 54 10153 584

268454299RTT – Jan 09 135

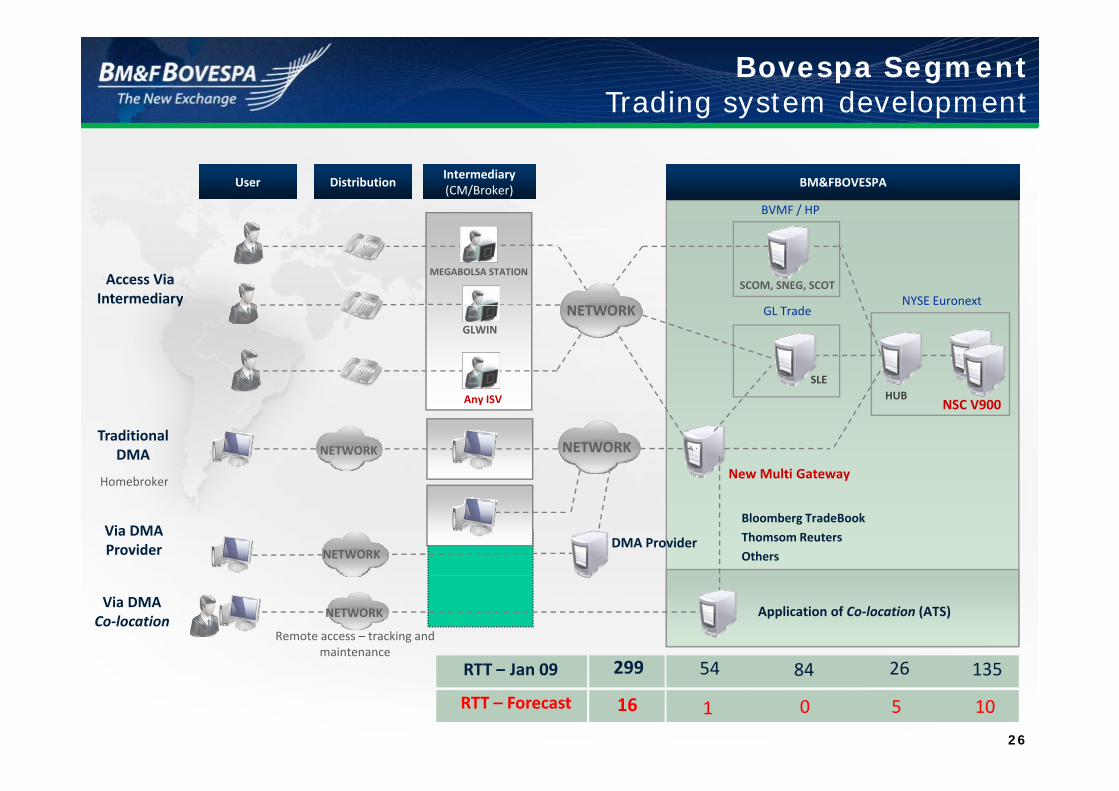

Bovespa SegmentTrading system development

User DistributionIntermediary(CM/Broker)

BM&FBOVESPA

BVMF / HP

MEGABOLSA STATIONSCOM, SNEG, SCOT

NYSE Euronext

Access Via Intermediary

NETWORK

SLE

GL Tradey

GLWIN

NETWORK

HUBNSC V900

New Multi Gateway

Traditional DMA

Homebroker

NETWORK NETWORK

HUB

Homebroker

268454299RTT J 09 135

25

RTT – Forecast 54 10153 584

268454299RTT – Jan 09 135

Bovespa SegmentTrading system development

User DistributionIntermediary(CM/Broker)

BM&FBOVESPA

BVMF / HP

MEGABOLSA STATIONSCOM, SNEG, SCOT

NYSE Euronext

Access Via Intermediary

NETWORK

SLE

GL Tradey

GLWIN

A ISV

NETWORK

HUBNSC V900

New Multi Gateway

Traditional DMA

Homebroker

Any ISV

NETWORK NETWORK

HUB

Via DMA Provider

Bloomberg TradeBook

Thomsom Reuters

Others

Homebroker

NETWORKDMA Provider

Via DMA Co‐location

Remote access – tracking and maintenance

Application of Co‐location (ATS)NETWORK

268454299RTT J 09 135

26

RTT – Forecast 1 1016 50

268454299RTT – Jan 09 135

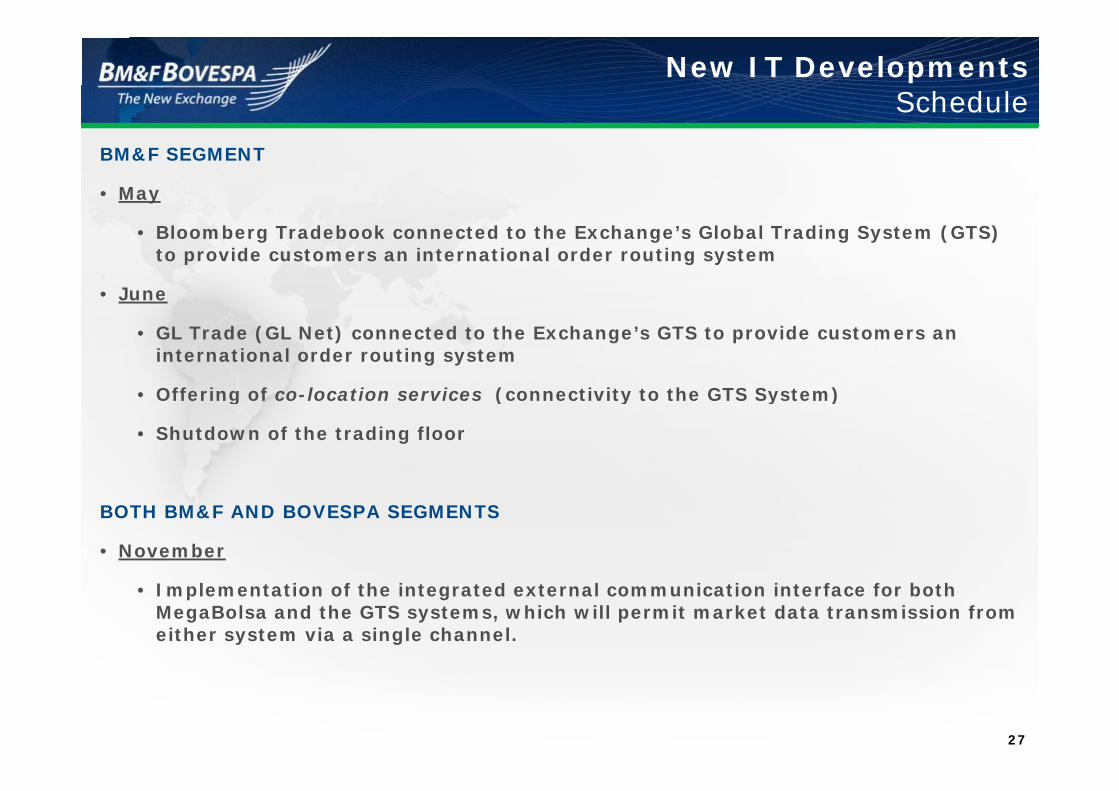

New IT DevelopmentsSchedule

BM&F SEGMENT

• May

• Bloomberg Tradebook connected to the Exchange’s Global Trading System (GTS) to provide customers an international order routing system

• June

• GL Trade (GL Net) connected to the Exchange’s GTS to provide customers an international order routing system

• Offering of co-location services (connectivity to the GTS System)• Offering of co-location services (connectivity to the GTS System)

• Shutdown of the trading floor

BOTH BM&F AND BOVESPA SEGMENTS

• November

• Implementation of the integrated external communication interface for both MegaBolsa and the GTS systems, which will permit market data transmission from either system via a single channel.

27

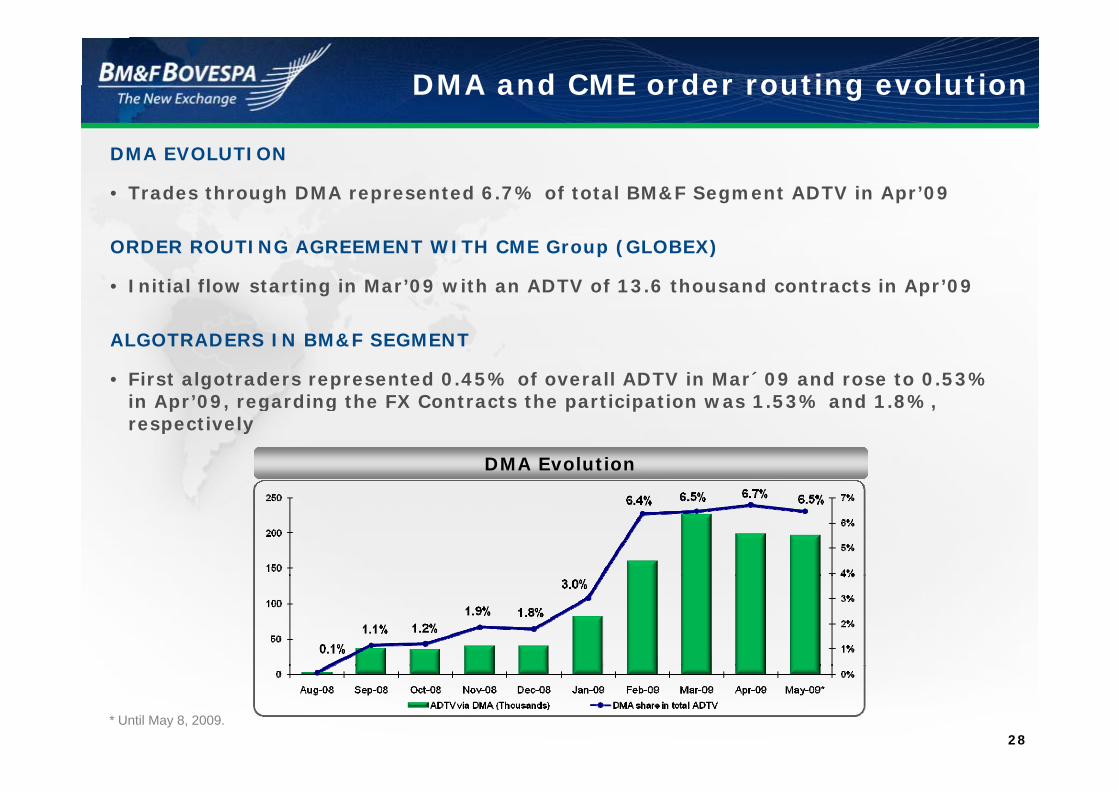

DMA and CME order routing evolution

DMA EVOLUTION

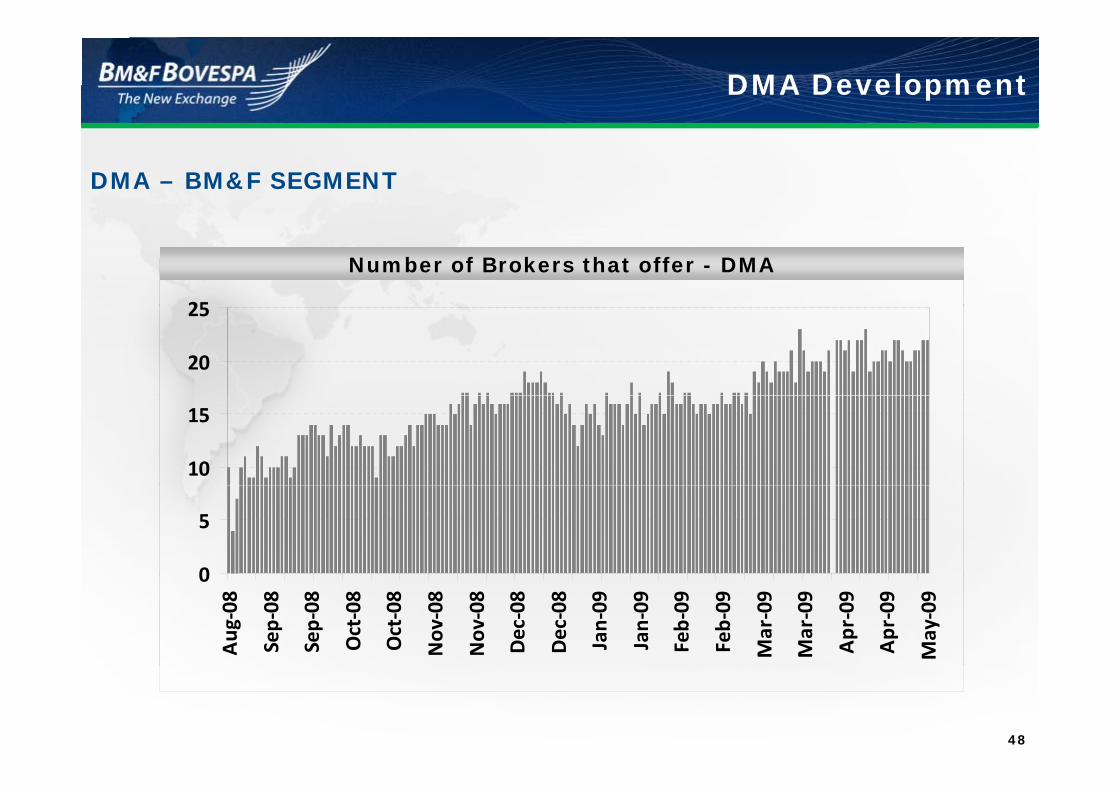

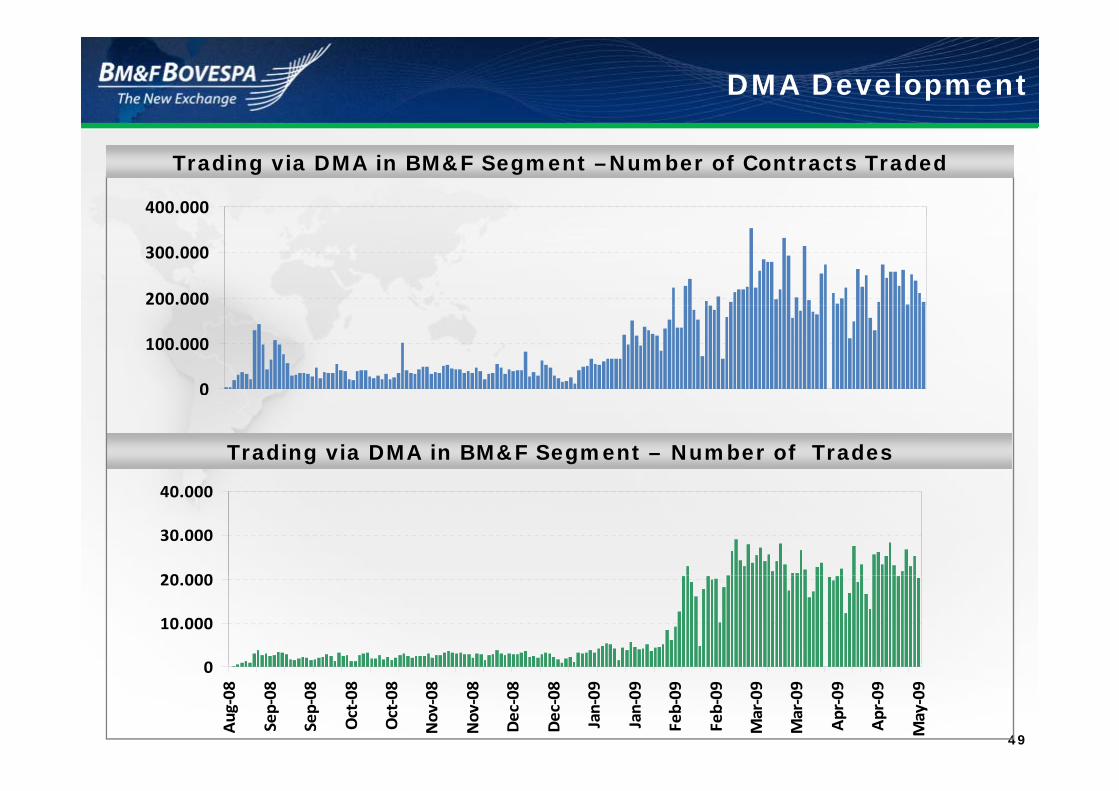

• Trades through DMA represented 6.7% of total BM&F Segment ADTV in Apr’09

ORDER ROUTING AGREEMENT WITH CME Group (GLOBEX)

• Initial flow starting in Mar’09 with an ADTV of 13.6 thousand contracts in Apr’09

ALGOTRADERS IN BM&F SEGMENT

• First algotraders represented 0.45% of overall ADTV in Mar´09 and rose to 0.53% i A ’09 di th FX C t t th ti i ti 1 53% d 1 8% in Apr’09, regarding the FX Contracts the participation was 1.53% and 1.8%, respectively

DMA Evolution

28* Until May 8, 2009.

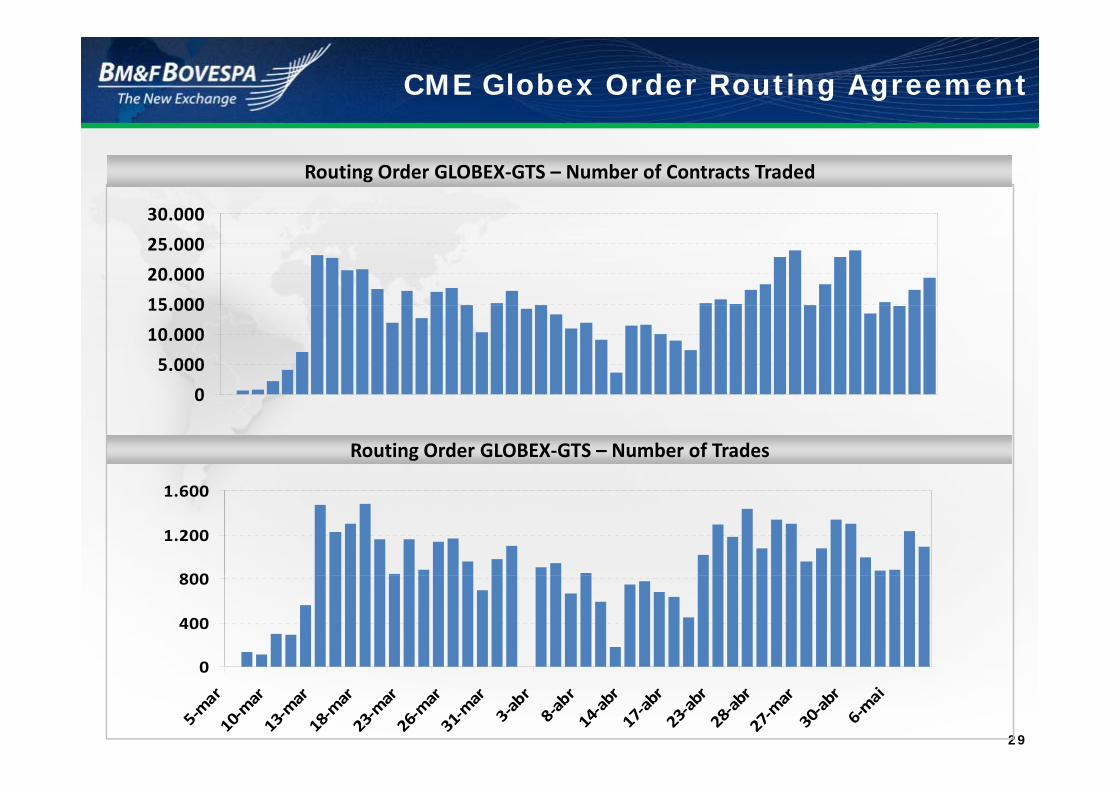

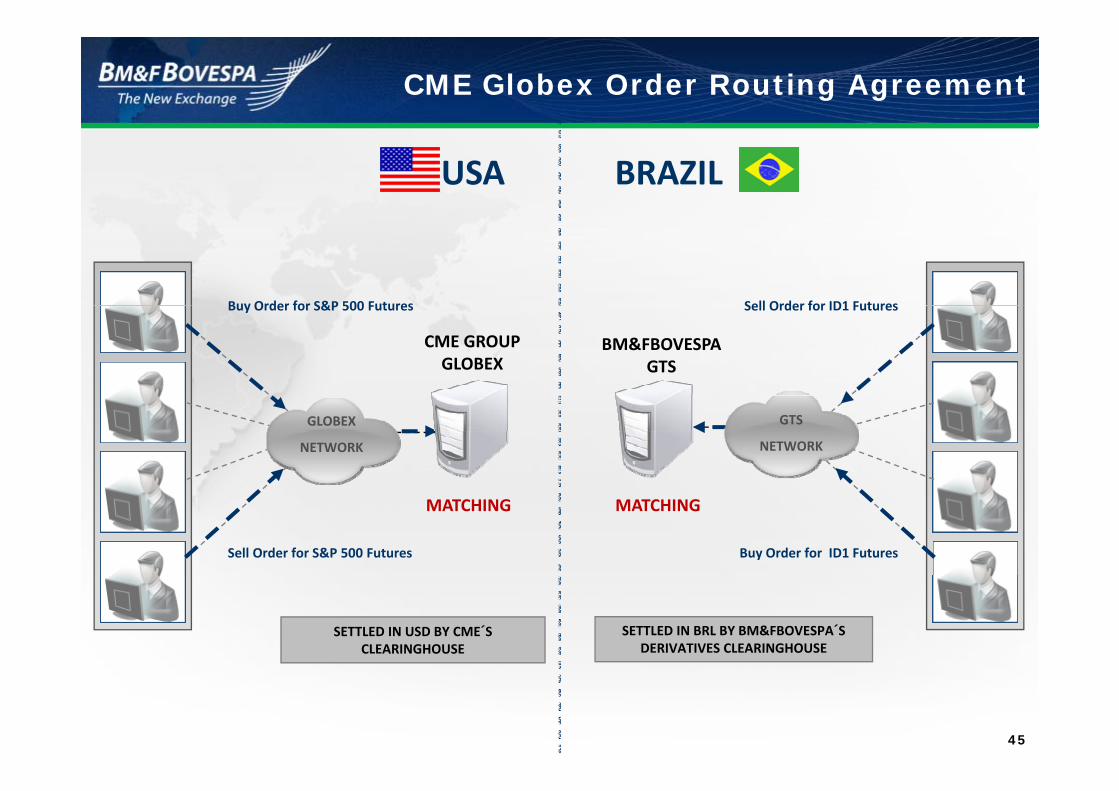

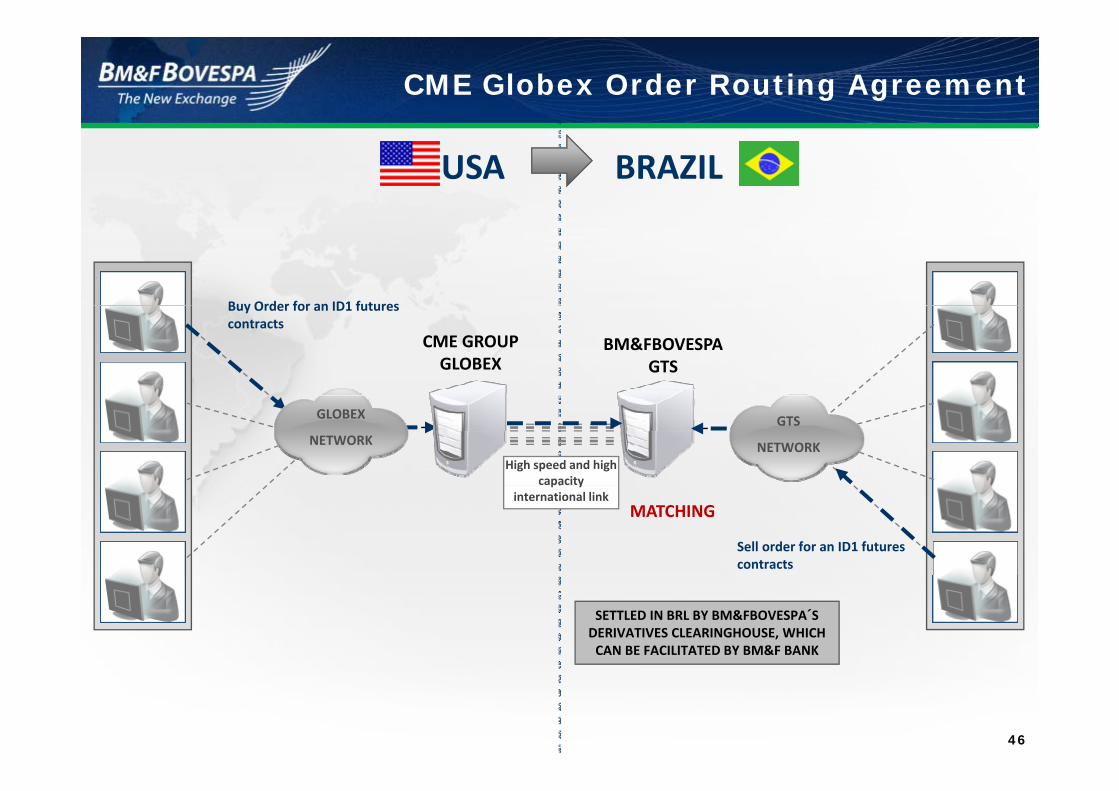

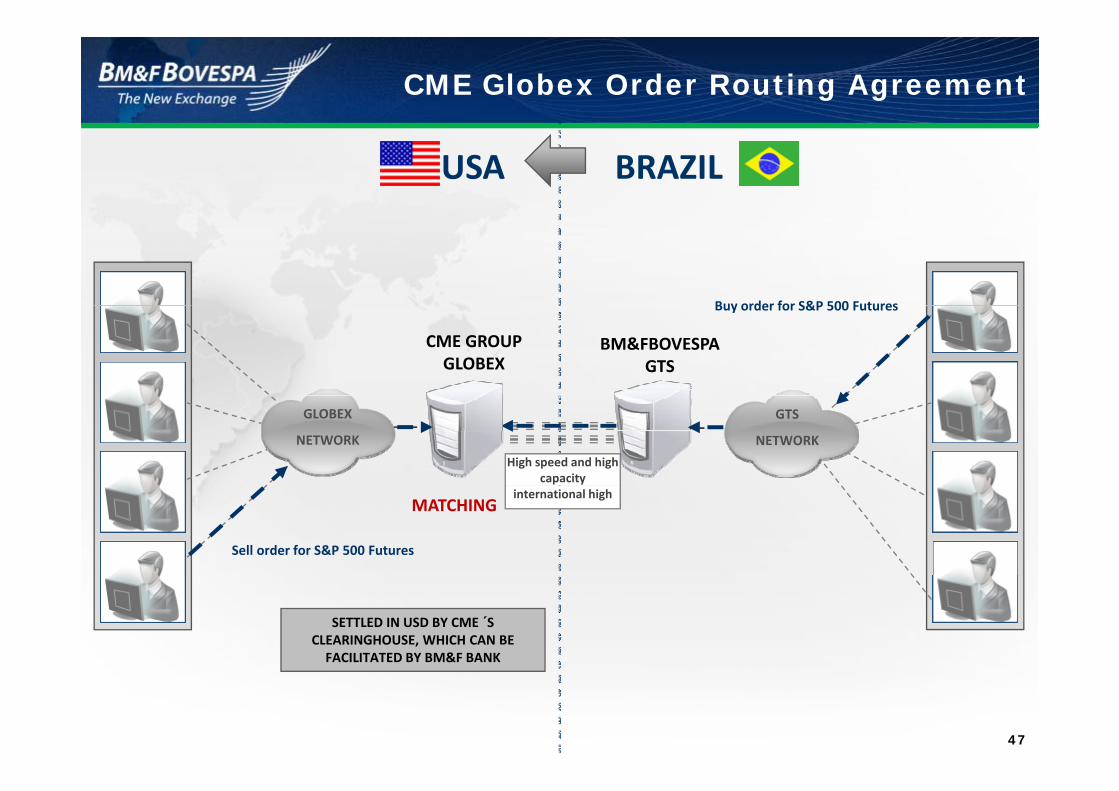

CME Globex Order Routing Agreement

Routing Order GLOBEX‐GTS – Number of Contracts Traded

30 000

15 000

20.000

25.000

30.000

0

5.000

10.000

15.000

Routing Order GLOBEX‐GTS – Number of Trades

0

800

1.200

1.600

0

400

800

29

0

5‐m

ar10

‐mar

13‐m

ar18

‐mar

23‐m

ar26

‐mar

31‐m

ar3‐

abr

8‐ab

r14

‐abr

17‐a

br23

‐abr

28‐a

br27

‐mar

30‐a

br6‐

mai

IT DevelopmentsCo location infrastructure

CO LOCATION AREA RACKS

BM&FBOVESPA WILL BE PREPARED FOR THE CO-LOCATION FOR BM&F SEGMENT IN JUN’09 AND FOR BOVESPA SEGMENT IN THE 3Q09

CO‐LOCATION AREA ‐ RACKS

Rack (40Us) H lf R k (20U ) Racks´lay out at theRack (40Us) Half Rack (20Us)

Unit Hosting

Structure where are installedh i h d )

Racks lay‐out at the co‐location´s area

30

the switches and servers)

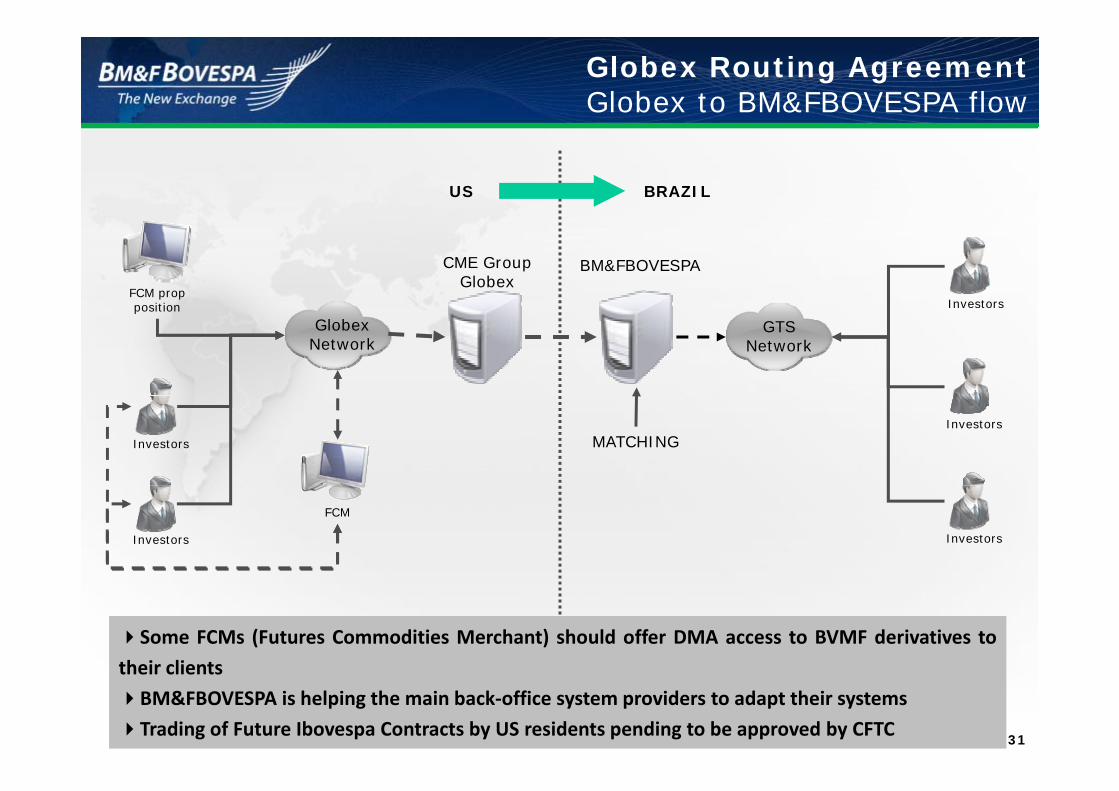

Globex Routing AgreementGlobex to BM&FBOVESPA flow

US BRAZIL

FCM prop position Investors

CME GroupGlobex

BM&FBOVESPA

GlobexNetwork

position

GTSNetwork

Investors

Investors

Investors

MATCHING

Investors

FCM

Investors

Some FCMs (Futures Commodities Merchant) should offer DMA access to BVMF derivatives to

their clients

31

their clients

BM&FBOVESPA is helping the main back‐office system providers to adapt their systems

Trading of Future Ibovespa Contracts by US residents pending to be approved by CFTC

IT DevelopmentsMore suitability for Algotraders

ALGORITHMIC TRADING PROFILE AND OPPORTUNITIES

• Arbitrage (determinist and statistic) - high frequency

• Cash Market versus ETF (Exchange Traded Fund)

• Cash Market versus Futures on Stock Index

D ti Sh ADR• Domestic Shares versus ADRs

• Futures versus Options

• Different s expirations of the same future contractp

• Trading of interest rate slope curve

• Trading with correlated instruments (soya bean BVMF x soya bean CME, coffee BVMF x coffee ICE etc)BVMF x coffee ICE etc)

• Mini contracts versus Standards contracts

• Order book’s depthp

DETERMINANT FACTORS

• Liquidity e volatility

32

• Electronic Access and low risk of execution

• Prices charged by the Exchange

FINANCIAL HIGHLIGHTSFINANCIAL HIGHLIGHTS

33

1Q09 Highlights versus 1Q08 Pro Forma

EPS: BRL 0.11 compared with BRL 0.11 in 1Q08

N t R d d b 20 1% th i

1Q09 EARNINGS Net Income / Adjusted Net Income* (BRL Millions)

-1.4% 12.2%

Net Revenues: decreased by 20.1% over the prior year

EBITDA margin: 55.8% in 1Q09 (67.5% Adjusted EBITDA) vs. 68.5% in 1Q08

Expense reduction: decreased by 17.4% between 1Q09 and 1Q08 (excluding depreciation, severance and Stock Option Plan costs)

HIGHLIGHTS

EBITDA / Adjusted EBITDA* (BRL Millions)

68.5% 68.5%

DMA development in BM&F Segment: in Apr’09, trades through DMA rose to 6.7% of the total traded volume

Globex and Algotraders: initial flow starting in Mar’09 with

-34.8% -21.3%55.8%

67.5%

an ADTV of 13.6 thousand contracts in Apr’09; in 1Q09, Algo represented 0.3% of Total ADTV and 0.6% of FX contracts

Foreign Investors: positive flow in 1Q09 of R$ 1.3 billion and grew to R$ 5.7 billion in Apr’09, its highest level in one year

Total Expenses / Adjusted Expenses** (BRL Millions)

12.2%grew to R$ 5.7 billion in Apr 09, its highest level in one year

MegaBolsa: new version (V900) launched on April 28 will reduce latency by 41%

Interest on Shareholders’ Equity: BRL 112 million to be paid

-17.4%

34

Interest on Shareholders’ Equity: BRL 112 million to be paid in May’09

* Adjusted Net Income and Adjusted EBITDA exclude severance and stock option plan costs.** Adjusted Expenses exclude depreciation, severance and stock option plan costs.

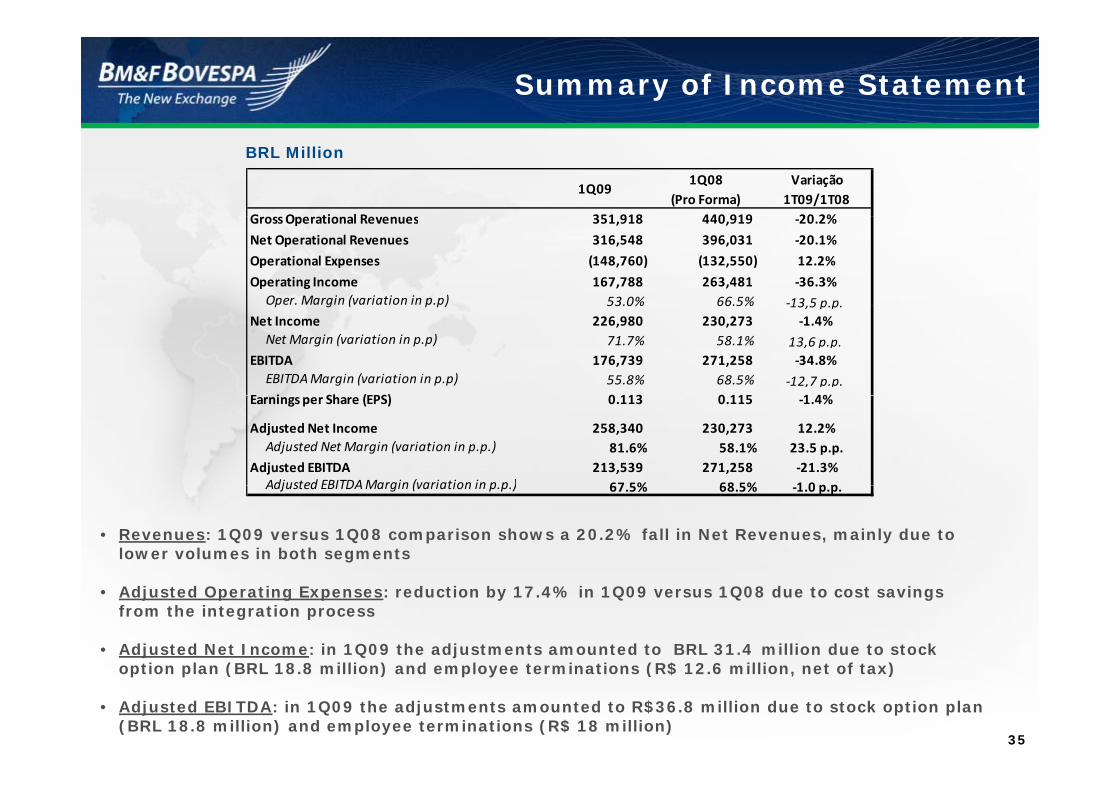

Summary of Income Statement

BRL Million

1Q091Q08

(Pro Forma)Variação

1T09/1T08G O ti l R 351 918 440 919 20 2%Gross Operational Revenues 351,918 440,919 ‐20.2%

Net Operational Revenues 316,548 396,031 ‐20.1%

Operational Expenses (148,760) (132,550) 12.2%

Operating Income 167,788 263,481 ‐36.3%Oper. Margin (variation in p.p) 53.0% 66.5% ‐13,5 p.p.p g ( p p) 53.0% 66.5% 13,5 p.p.

Net Income 226,980 230,273 ‐1.4%Net Margin (variation in p.p) 71.7% 58.1% 13,6 p.p.

EBITDA 176,739 271,258 ‐34.8%EBITDA Margin (variation in p.p) 55.8% 68.5% ‐12,7 p.p.

E i Sh (EPS) 0 113 0 115 1 4%Earnings per Share (EPS) 0.113 0.115 ‐1.4%

Adjusted Net Income 258,340 230,273 12.2%Adjusted Net Margin (variation in p.p.) 81.6% 58.1% 23.5 p.p.

Adjusted EBITDA 213,539 271,258 ‐21.3%Adjusted EBITDAMargin (variation in p p ) 67 5% 68 5% 1 0 p p

• Revenues: 1Q09 versus 1Q08 comparison shows a 20.2% fall in Net Revenues, mainly due to lower volumes in both segments

Adjusted EBITDA Margin (variation in p.p.) 67.5% 68.5% ‐1.0 p.p.

• Adjusted Operating Expenses: reduction by 17.4% in 1Q09 versus 1Q08 due to cost savings from the integration process

• Adjusted Net Income: in 1Q09 the adjustments amounted to BRL 31.4 million due to stock ti l (BRL 18 8 illi ) d l t i ti (R$ 12 6 illi t f t )

35

option plan (BRL 18.8 million) and employee terminations (R$ 12.6 million, net of tax)

• Adjusted EBITDA: in 1Q09 the adjustments amounted to R$36.8 million due to stock option plan (BRL 18.8 million) and employee terminations (R$ 18 million)

Revenues

Gross Revenues Composition – 1Q09 1Q091Q08

(Pro Forma)Variation

1Q09/1Q08Gross Operational Revenues 351,918 440,919 ‐20.2%

BM&F Segment 130,547 154,938 ‐15.7%Derivatives ‐ trad. / settlement 121,434 148,664 ‐18 3%/ , , 18.3%Foreign Exchange ‐ trad. / settlement 5,692 4,620 23.2%Securities ‐ trad. / settlement 44 107 ‐58.9%Brazilian Commodities Exchange 1,406 932 50.9%BM&F Bank 1,971 615 220.5%

Bovespa Segment 200,503 270,527 ‐25.9%Trading fees 113 732 164 342 30 8%Trading fees 113,732 164,342 ‐30.8%Clearing fees 44,464 66,044 ‐32.7%Securities Lending 6,127 15,380 ‐60.2%Listing 10,621 7,123 49.1%Depositary and custody 16,084 14,319 12.3%Trading access (Brokers) 9,475 3,319 185.5%

Other Operational Revenues 20,868 15,454 35.0%Vendors 11,521 9,688 18.9%Commodities classification fees 215 171 25.7%Dividends 5,371 ‐ ‐Others 3,761 5,595 ‐32.8%

Net Operational Revenues 316,548 396,031 ‐20.1%

• The revenues from other services (not tied to trading) increased by 16.5% over the prior year to BRL 66.5 million (BRL 57.1 million in 1Q08), mainly from:

• Depository: higher number of investors (mainly individuals): increased by 12 3%• Depository: higher number of investors (mainly individuals): increased by 12.3%

• Listing: new pricing policy: increased by 49.1%

• Trading Access Services: implementation of a policy for brokerage house access in both segments: increased by 185.5%

36

• Vendors: higher number of users: increased by 18.9%

• The share of non-trading sources increased to 18.9% of total revenues in 1Q09 versus 13% in 1Q08

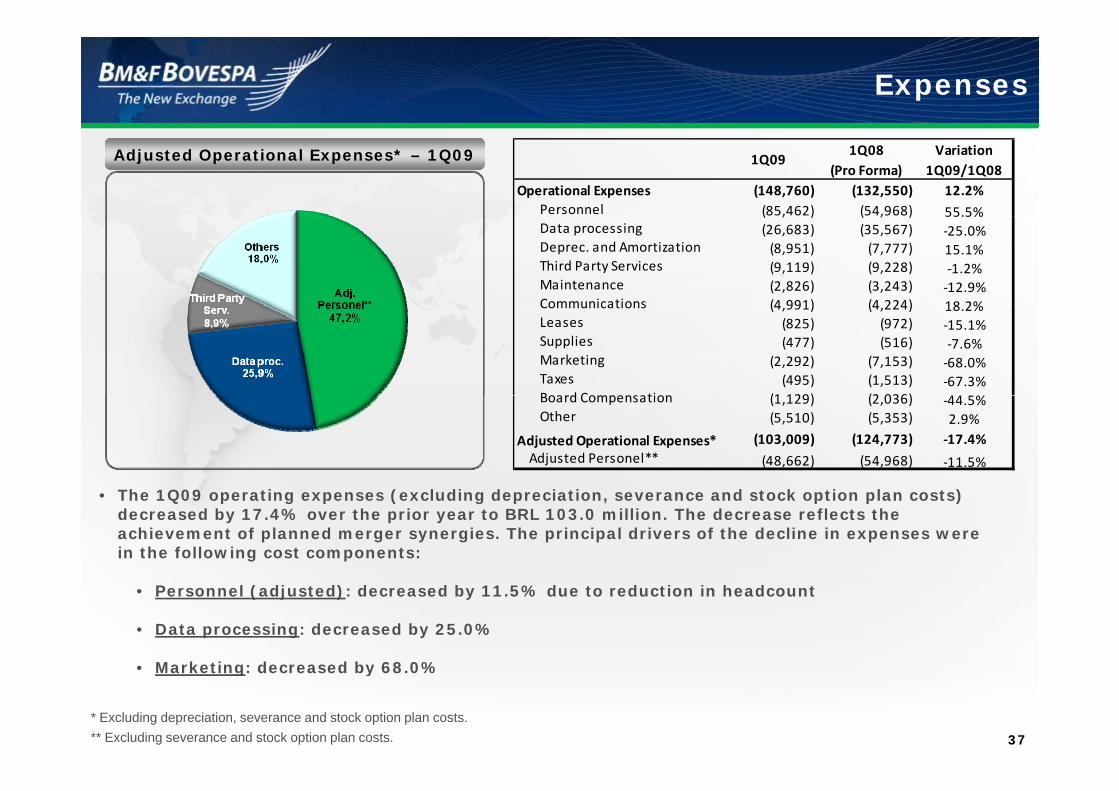

Expenses

Adjusted Operational Expenses* – 1Q09 1Q091Q08

(Pro Forma)Variation

1Q09/1Q08Operational Expenses (148,760) (132,550) 12.2%

Personnel (85,462) (54,968) 55.5%( , ) ( , ) 55.5% Data processing (26,683) (35,567) ‐25.0% Deprec. and Amortization (8,951) (7,777) 15.1% Third Party Services (9,119) (9,228) ‐1.2% Maintenance (2,826) (3,243) ‐12.9%Communications (4 991) (4 224) 18 2% Communications (4,991) (4,224) 18.2%

Leases (825) (972) ‐15.1% Supplies (477) (516) ‐7.6% Marketing (2,292) (7,153) ‐68.0% Taxes (495) (1,513) ‐67.3%Board Compensation (1 129) (2 036) 44 5% Board Compensation (1,129) (2,036) ‐44.5%

Other (5,510) (5,353) 2.9%

Adjusted Operational Expenses* (103,009) (124,773) ‐17.4%Adjusted Personel** (48,662) (54,968) ‐11.5%

• The 1Q09 operating expenses (excluding depreciation, severance and stock option plan costs) decreased by 17.4% over the prior year to BRL 103.0 million. The decrease reflects the achievement of planned merger synergies. The principal drivers of the decline in expenses were in the following cost components:

• Personnel (adjusted): decreased by 11.5% due to reduction in headcount

• Data processing: decreased by 25.0%

Marketing: decreased by 68 0%

37

• Marketing: decreased by 68.0%

* Excluding depreciation, severance and stock option plan costs.** Excluding severance and stock option plan costs.

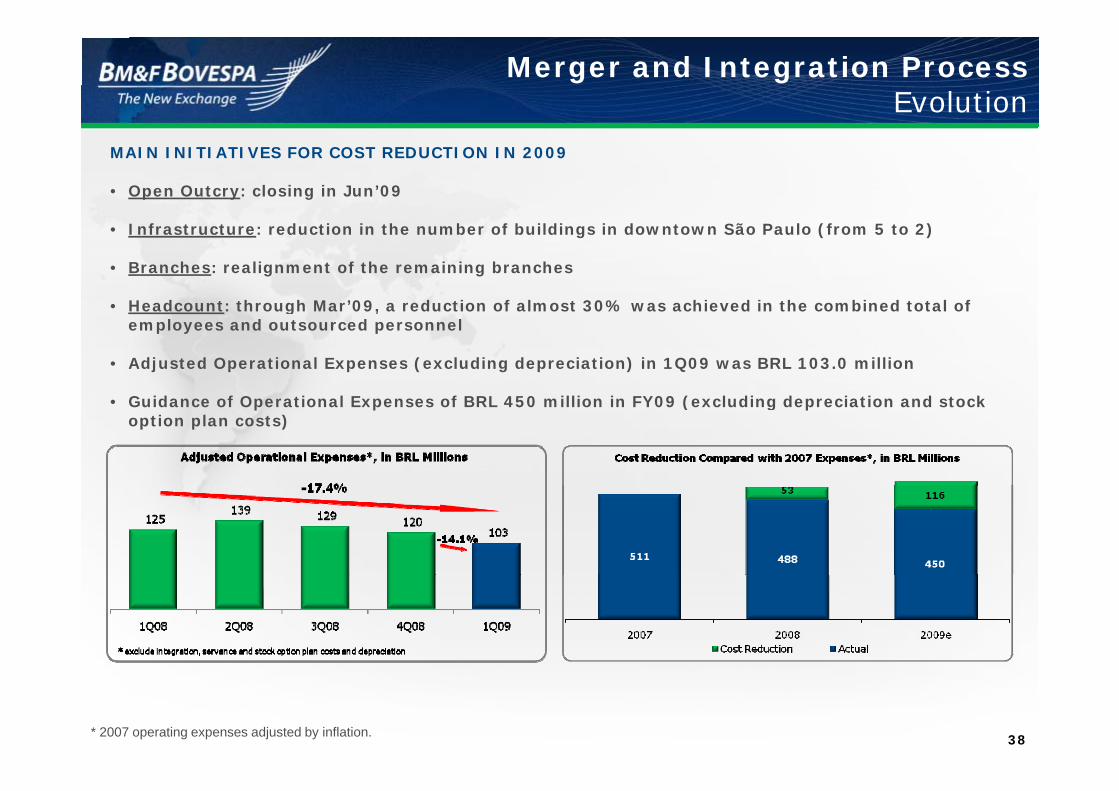

Merger and Integration ProcessEvolution

MAIN INITIATIVES FOR COST REDUCTION IN 2009

• Open Outcry: closing in Jun’09

• Infrastructure: reduction in the number of buildings in downtown São Paulo (from 5 to 2)

• Branches: realignment of the remaining branches

• Headcount: through Mar’09 a reduction of almost 30% was achieved in the combined total of • Headcount: through Mar 09, a reduction of almost 30% was achieved in the combined total of employees and outsourced personnel

• Adjusted Operational Expenses (excluding depreciation) in 1Q09 was BRL 103.0 million

G id f O i l E f BRL 450 illi i FY09 ( l di d i i d k • Guidance of Operational Expenses of BRL 450 million in FY09 (excluding depreciation and stock option plan costs)

38* 2007 operating expenses adjusted by inflation.

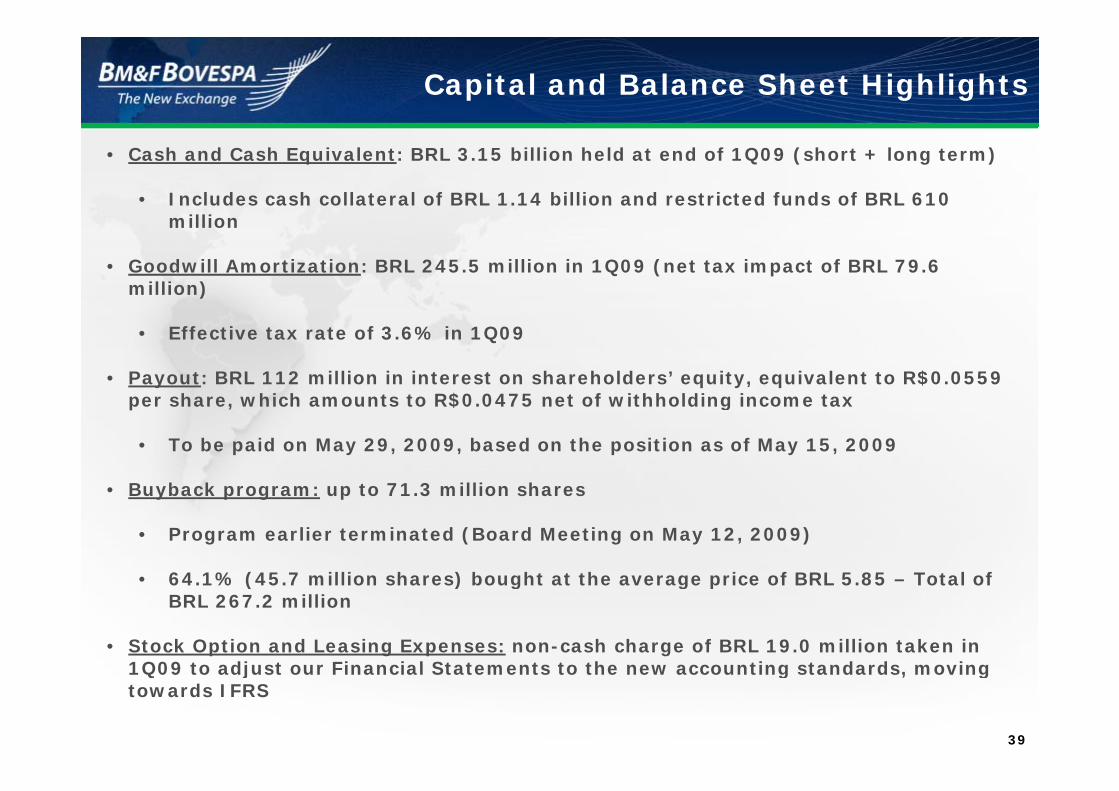

Capital and Balance Sheet Highlights

• Cash and Cash Equivalent: BRL 3.15 billion held at end of 1Q09 (short + long term)

• Includes cash collateral of BRL 1.14 billion and restricted funds of BRL 610 illimillion

• Goodwill Amortization: BRL 245.5 million in 1Q09 (net tax impact of BRL 79.6 million)

• Effective tax rate of 3.6% in 1Q09

• Payout: BRL 112 million in interest on shareholders’ equity, equivalent to R$0.0559 h hi h t t R$0 0475 t f ithh ldi i tper share, which amounts to R$0.0475 net of withholding income tax

• To be paid on May 29, 2009, based on the position as of May 15, 2009

B b k t 71 3 illi h• Buyback program: up to 71.3 million shares

• Program earlier terminated (Board Meeting on May 12, 2009)

64 1% (45 7 million shares) bought at the average price of BRL 5 85 Total of • 64.1% (45.7 million shares) bought at the average price of BRL 5.85 – Total of BRL 267.2 million

• Stock Option and Leasing Expenses: non-cash charge of BRL 19.0 million taken in 1Q09 to adjust our Financial Statements to the new accounting standards moving

39

1Q09 to adjust our Financial Statements to the new accounting standards, moving towards IFRS

APPENDIX

40

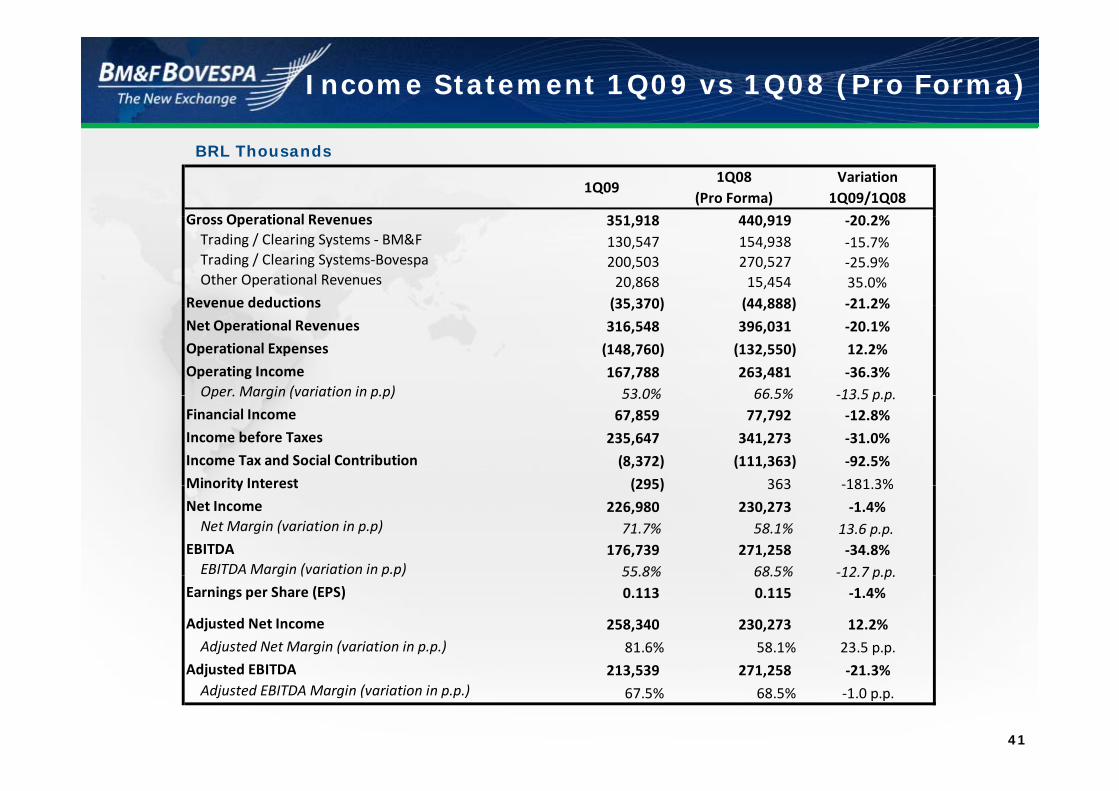

Income Statement 1Q09 vs 1Q08 (Pro Forma)

BRL Thousands

1Q091Q08

(Pro Forma)Variation

1Q09/1Q08G O ti l R 351 918 440 919 20 2%Gross Operational Revenues 351,918 440,919 ‐20.2%Trading / Clearing Systems ‐ BM&F 130,547 154,938 ‐15.7%Trading / Clearing Systems‐Bovespa 200,503 270,527 ‐25.9%Other Operational Revenues 20,868 15,454 35.0%

Revenue deductions (35 370) (44 888) ‐21 2%Revenue deductions (35,370) (44,888) 21.2%Net Operational Revenues 316,548 396,031 ‐20.1%Operational Expenses (148,760) (132,550) 12.2%Operating Income 167,788 263,481 ‐36.3%Oper. Margin (variation in p.p) 53 0% 66 5% ‐13 5 p pOper. Margin (variation in p.p) 53.0% 66.5% ‐13.5 p.p.

Financial Income 67,859 77,792 ‐12.8%Income before Taxes 235,647 341,273 ‐31.0%Income Tax and Social Contribution (8,372) (111,363) ‐92.5%Minority Interest (295) 363 ‐181 3%Minority Interest (295) 363 ‐181.3%Net Income 226,980 230,273 ‐1.4%Net Margin (variation in p.p) 71.7% 58.1% 13.6 p.p.

EBITDA 176,739 271,258 ‐34.8%EBITDA Margin (variation in p.p) 55.8% 68.5% ‐12.7 p.p.g ( p p) 55.8% 68.5% 12.7 p.p.

Earnings per Share (EPS) 0.113 0.115 ‐1.4%

Adjusted Net Income 258,340 230,273 12.2%Adjusted Net Margin (variation in p.p.) 81.6% 58.1% 23.5 p.p.

Adj d EBITDA

41

Adjusted EBITDA 213,539 271,258 ‐21.3%Adjusted EBITDA Margin (variation in p.p.) 67.5% 68.5% ‐1.0 p.p.

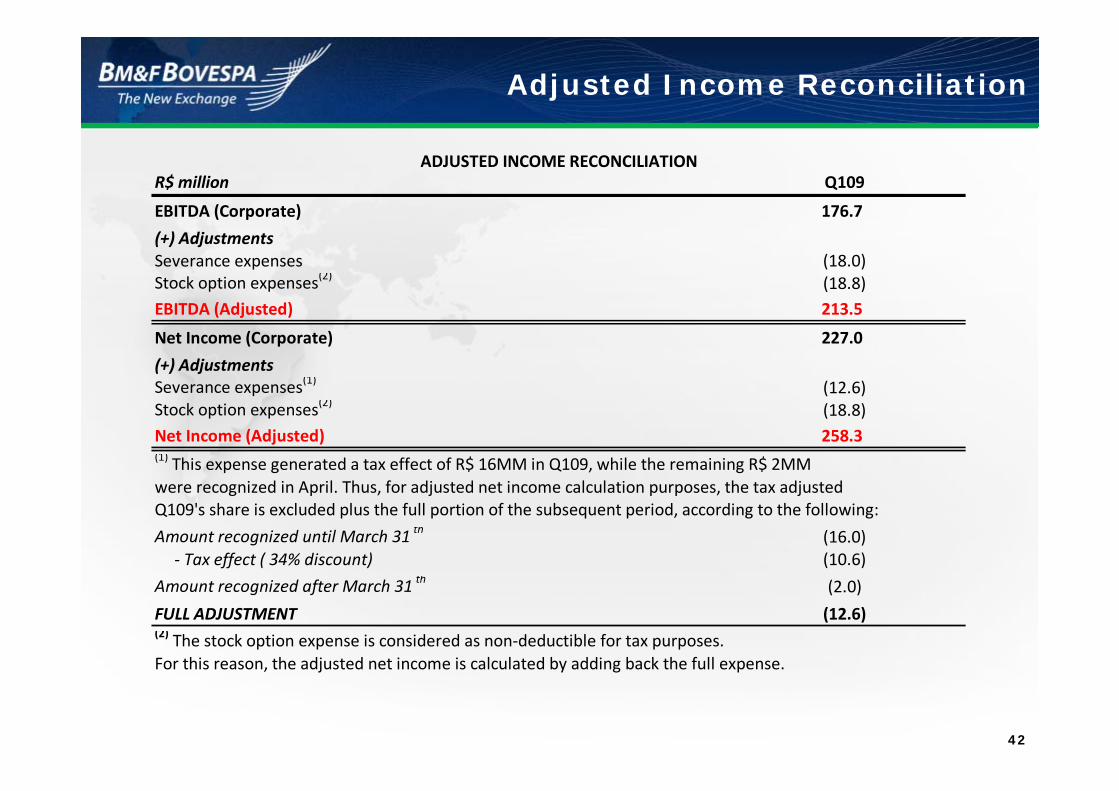

Adjusted Income Reconciliation

R$ million Q109

EBITDA (Corporate) 176.7

ADJUSTED INCOME RECONCILIATION

EBITDA (Corporate) 176.7

(+) AdjustmentsSeverance expenses (18.0)Stock option expenses(2) (18.8)EBITDA (Adj t d) 213 5EBITDA (Adjusted) 213.5

Net Income (Corporate) 227.0

(+) AdjustmentsSeverance expenses(1) (12.6)p ( )Stock option expenses(2) (18.8)Net Income (Adjusted) 258.3(1) This expense generated a tax effect of R$ 16MM in Q109, while the remaining R$ 2MMwere recognized in April Thus for adjusted net income calculation purposes the tax adjustedwere recognized in April. Thus, for adjusted net income calculation purposes, the tax adjusted Q109's share is excluded plus the full portion of the subsequent period, according to the following:

Amount recognized until March 31 th (16.0) ‐ Tax effect ( 34% discount) (10.6)

Amount recognized after March 31 th (2.0)

FULL ADJUSTMENT (12.6)(2) The stock option expense is considered as non‐deductible for tax purposes.For this reason the adjusted net income is calculated by adding back the full expense

42

For this reason, the adjusted net income is calculated by adding back the full expense.

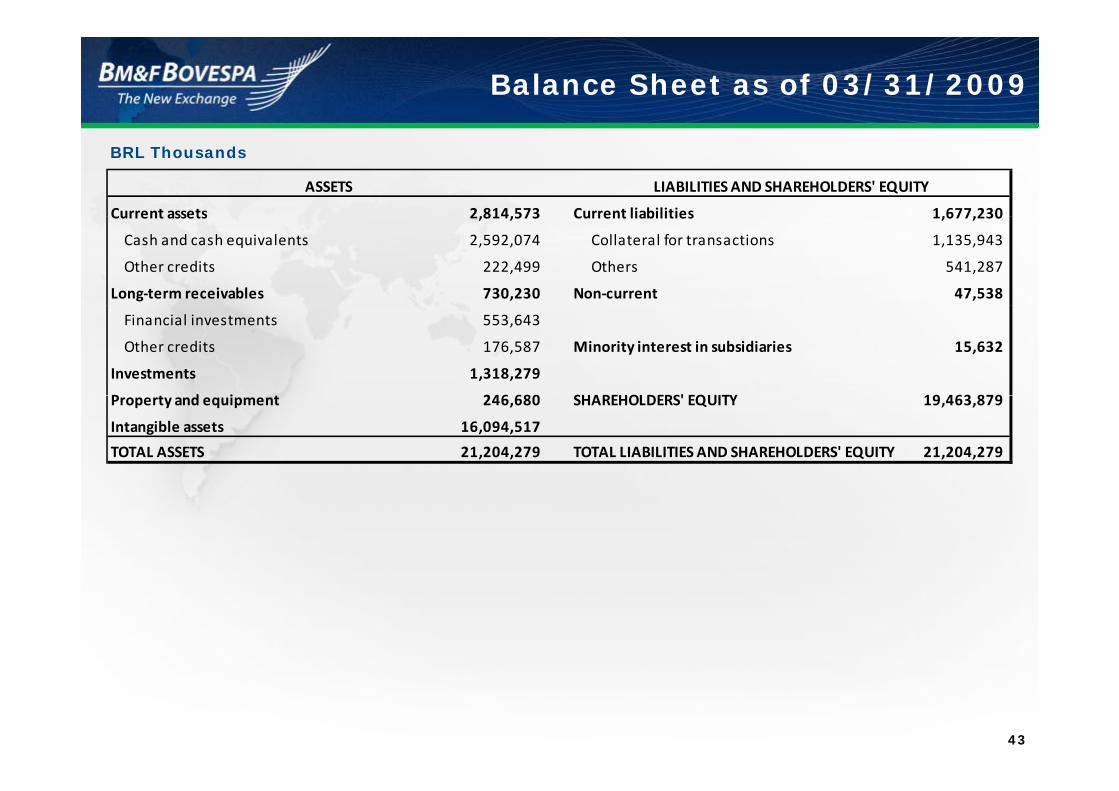

Balance Sheet as of 03/31/2009

BRL Thousands

Current assets 2 814 573 Current liabilities 1 677 230

ASSETS LIABILITIES AND SHAREHOLDERS' EQUITY

Current assets 2,814,573 Current liabilities 1,677,230

Cash and cash equivalents 2,592,074 Collateral for transactions 1,135,943

Other credits 222,499 Others 541,287

Long‐term receivables 730,230 Non‐current 47,538

Financial investments 553,643

Other credits 176,587 Minority interest in subsidiaries 15,632

Investments 1,318,279

P d i 246 680 SHAREHOLDERS' EQUITY 19 463 879Property and equipment 246,680 SHAREHOLDERS' EQUITY 19,463,879

Intangible assets 16,094,517

TOTAL ASSETS 21,204,279 TOTAL LIABILITIES AND SHAREHOLDERS' EQUITY 21,204,279

43

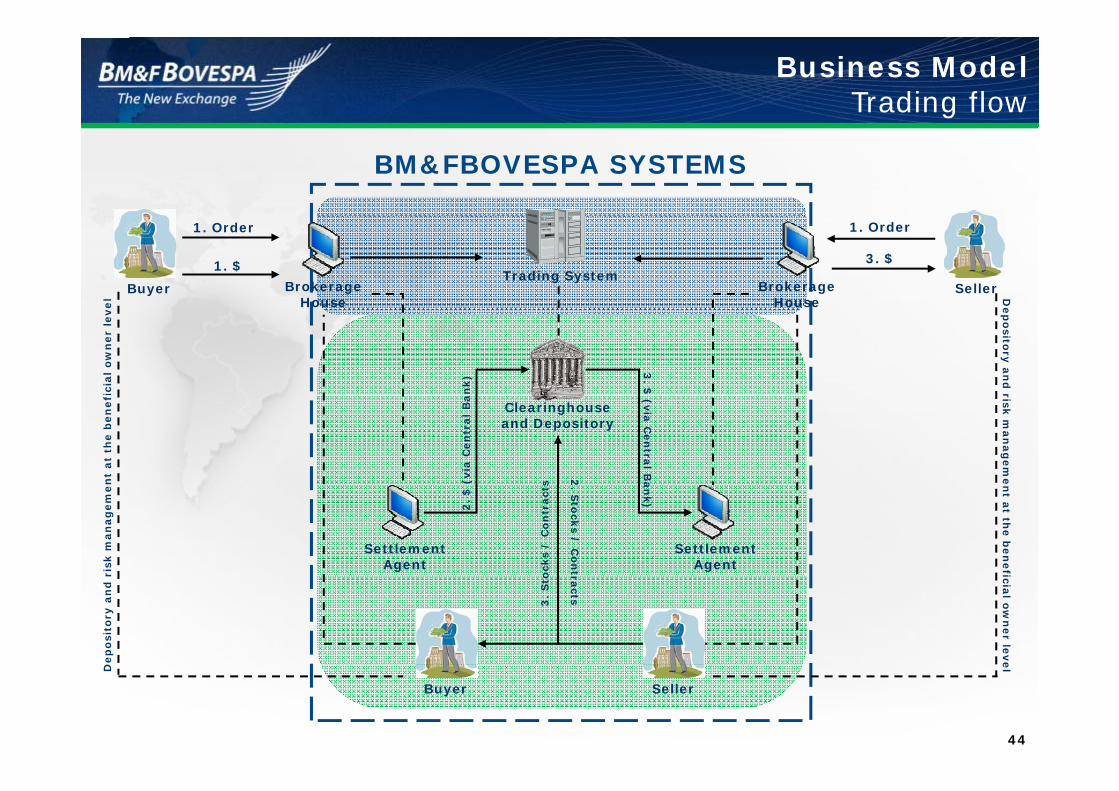

Business ModelTrading flow

BM&FBOVESPA SYSTEMS

el

1. Order

3. $1. $

1. Order

SellerBuyer BrokerageHouse

BrokerageHouse

Trading System

Dic

ial

ow

ner

leve HouseHouse

an

k)

3. $

Dep

osito

ry a

nd

rn

t at

the b

en

ef

Clearinghouseand Depository

(via

Cen

tral

Ba (v

ia C

en

tral B

a2s

risk m

an

ag

em

eri

sk m

an

ag

em

e

2.

$ a

nk)

SettlementAgent

SettlementAgent

2. S

tock

s / C

on

to

cks

/ C

on

tract

s nt a

t the b

en

ef

Dep

osi

tory

an

d r

tracts

3.

Sto

icial o

wn

er le

ve

44

D

Buyer Seller

el

CME Globex Order Routing Agreement

USA BRAZIL

Buy Order for S&P 500 Futures Sell Order for ID1 FuturesBuy Order for S&P 500 Futures Sell Order for ID1 Futures

CME GROUP GLOBEX

BM&FBOVESPA GTS

GLOBEX communication

network

GLOBEX

NETWORK

GTS

NETWORK

MATCHINGMATCHING

Sell Order for S&P 500 Futures Buy Order for ID1 Futures

SETTLED IN USD BY CME´SCLEARINGHOUSE

SETTLED IN BRL BY BM&FBOVESPA´S DERIVATIVES CLEARINGHOUSE

45

CME Globex Order Routing Agreement

USA BRAZIL

Buy Order for an ID1 futuresBuy Order for an ID1 futures contracts

CME GROUP GLOBEX

BM&FBOVESPA GTS

GLOBEX

NETWORK

High speed and high capacity

GTS

NETWORK

Sell order for an ID1 futures contracts

MATCHING

p yinternational link

SETTLED IN BRL BY BM&FBOVESPA´S DERIVATIVES CLEARINGHOUSE, WHICH CAN BE FACILITATED BY BM&F BANK

46

CME Globex Order Routing Agreement

USA BRAZIL

Buy order for S&P 500 Futures

CME GROUP GLOBEX

BM&FBOVESPA GTS

Buy order for S&P 500 Futures

GLOBEX

NETWORK

High speed and high capacity

GTS

NETWORK

Sell order for S&P 500 Futures

MATCHINGinternational high

SETTLED IN USD BY CME ´S CLEARINGHOUSE, WHICH CAN BE FACILITATED BY BM&F BANK

47

DMA Development

DMA – BM&F SEGMENT

25

Number of Brokers that offer - DMA

20

25

10

15

0

5

0

Aug

‐08

Sep‐08

Sep‐08

Oct‐08

Oct‐08

Nov

‐08

Nov

‐08

Dec‐08

Dec‐08

Jan‐09

Jan‐09

Feb‐09

Feb‐09

Mar‐09

Mar‐09

Apr‐09

Apr‐09

May‐09

48

DMA Development

Trading via DMA in BM&F Segment –Number of Contracts Traded

400.000

200.000

300.000

0

100.000

Trading via DMA in BM&F Segment – Number of Trades

20 000

30.000

40.000

0

10.000

20.000

49

0

Aug‐08

Sep‐08

Sep‐08

Oct‐08

Oct‐08

Nov‐08

Nov‐08

Dec‐08

Dec‐08

Jan‐09

Jan‐09

Feb‐09

Feb‐09

Mar‐09

Mar‐09

Apr‐09

Apr‐09

May‐09

New Pricing Policy

• BM&F Trading: implementation of a new price grid for BM&F segment based on volumes aiming at neutrality when compared with Aug’08 framework: February 16th 2009February 16th, 2009

• BOVESPA Trading and Depository Service

di i d i f l i f h d il i• Trading: progressive reduction of clearing fees charged to retail investors and private and public companies in the cash market: beginning on May 4th, 2009

• Progressive reduction: 0.0005% until Oct’09; 0.0010% until Jan’10; 0.0015% from Feb’10 onwards

• Depository: progressive adoption of a percentage charge system based on • Depository: progressive adoption of a percentage charge system based on value under custody with the depository: beginning on May 4th, 2009

• Progressive discounts: 67% until Oct’09; 33% until Jan’10; full new depository fee from Feb’10 onwards depository fee from Feb 10 onwards

• Securities Lending: rebate (5 bps) to the lenders, except for non residents: beginning on May 4th, 2009

50

• Market Data: since Apr’09 - closer to international prices

Securities Lending (BTC)

• Specific regulation for securities lending activity

• Must be carried in a Clearinghouse (CCP)

• Trading systems offers registration

• Lending is a investors’ decision and it’s done through a brokerage house

• Settlement agents are responsible by their clients settlement and collateral

• Full disclosure of the open interest positions by company on daily basis

• Corporate actions adjustments

• Risk management at the beneficial owner level with collateral requirement and daily k t k tmark to market

• Position Limit

Investor: the totality of positions cannot exceed 3% of the free floating of the • Investor: the totality of positions cannot exceed 3% of the free floating of the company

• Broker: the totality of positions cannot exceed 6.5% of the free floating of the company

51

company

• Market: the totality of positions cannot exceed 20% of the free floating of the company

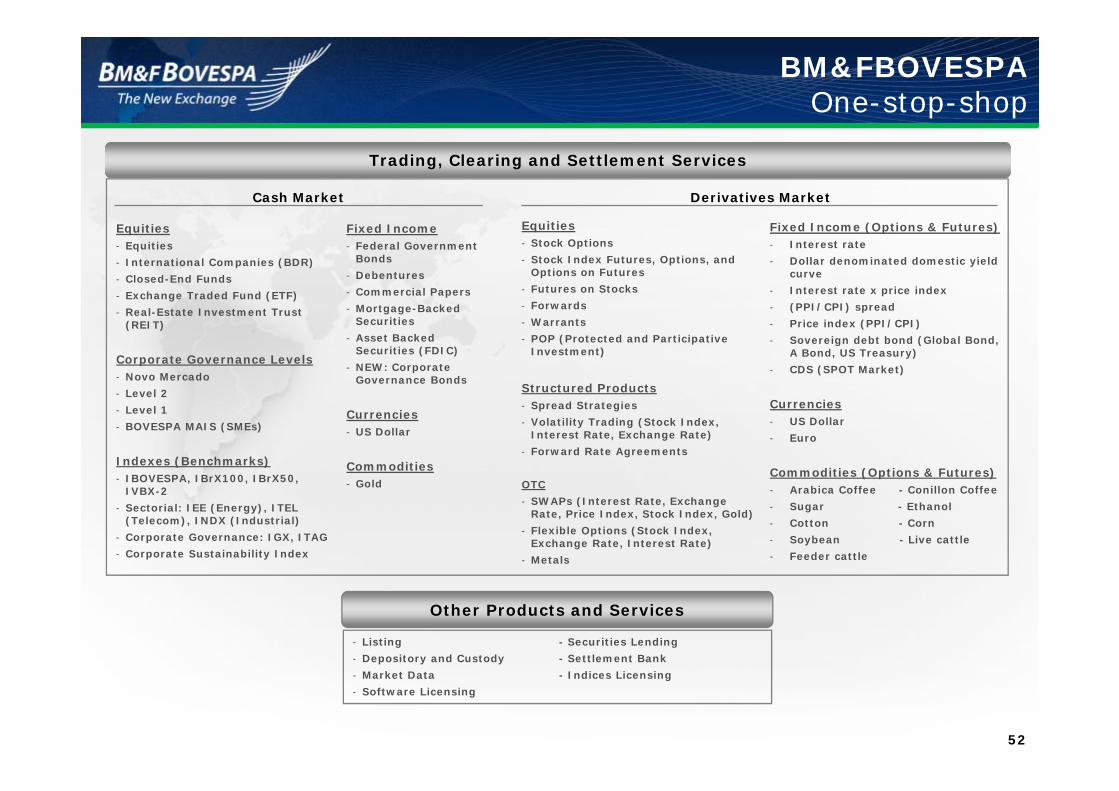

BM&FBOVESPAOne-stop-shop

Trading, Clearing and Settlement Services

Cash Market Derivatives Market

Equities- Equities

- International Companies (BDR)

- Closed-End Funds

- Exchange Traded Fund (ETF)

Fixed Income- Federal Government

Bonds

- Debentures

- Commercial Papers

M t B k d

Equities- Stock Options

- Stock Index Futures, Options, and Options on Futures

- Futures on Stocks

- Forwards

Fixed Income (Options & Futures)- Interest rate

- Dollar denominated domestic yield curve

- Interest rate x price index

(PPI/CPI) spread- Real-Estate Investment Trust (REIT)

Corporate Governance Levels- Novo Mercado

- Level 2

- Mortgage-Backed Securities

- Asset Backed Securities (FDIC)

- NEW: Corporate Governance Bonds

- Forwards

- Warrants

- POP (Protected and Participative Investment)

Structured Products

- (PPI/CPI) spread

- Price index (PPI/CPI)

- Sovereign debt bond (Global Bond, A Bond, US Treasury)

- CDS (SPOT Market)

Level 2

- Level 1

- BOVESPA MAIS (SMEs)

Indexes (Benchmarks)- IBOVESPA, IBrX100, IBrX50,

Currencies- US Dollar

Commodities- Gold

- Spread Strategies

- Volatility Trading (Stock Index, Interest Rate, Exchange Rate)

- Forward Rate Agreements

OTC

Currencies- US Dollar

- Euro

Commodities (Options & Futures)

IVBX-2

- Sectorial: IEE (Energy), ITEL (Telecom), INDX (Industrial)

- Corporate Governance: IGX, ITAG

- Corporate Sustainability Index

Gold OTC

- SWAPs (Interest Rate, Exchange Rate, Price Index, Stock Index, Gold)

- Flexible Options (Stock Index, Exchange Rate, Interest Rate)

- Metals

- Arabica Coffee - Conillon Coffee

- Sugar - Ethanol

- Cotton - Corn

- Soybean - Live cattle

- Feeder cattle

- Listing - Securities Lending

- Depository and Custody - Settlement Bank

Other Products and Services

52

- Market Data - Indices Licensing

- Software Licensing

Operational HighlightsBM&F Segment

Overall ADTV (Thousands) Interest Rates in BRL (Thousands)

FX Rates (Thousands) Indices (Thousands)

53* Until May 8, 2009.

Operational HighlightsBOVESPA Segment

ADTV (BRL Millions) Average Number of Trades (Thousands)

Number of Investors (Thousands) Turnover Velocity** (12 months)

54* Until May 11, 2009.

** Relation of the trading value in the cash market and the market cap of the exchange

Board Members (2009 – 2010)

BOARD MEMBERS

• Armínio Fraga (Chairman)* - Gavea Investimentos

• Claudio Haddad* - Ibmec

• Fabio de Oliveira Barbosa* - Vale (CFO)

• José Roberto Mendonça de Barros* - Economist and Consultant

• Marcelo Fernandes Trindade* - Lawyer

• Rene Marc Kern* - General Atlantic

• Renato Diniz Junqueira – Intercap

• Candido Botelho Bracher – Itau BBA

• Luis Stulhberger – Credit Suisse Hedging-Griffo

• Craig Donohue – CME Group

• Julio Siqueira de Araújo – Bradesco (Vice President)

55

* Independents

BM&F Bovespa Investor Relationsp

Web page: www.bmfbovespa.com.br/ri

Phone numbers: 55 11 3119 2007/ 3728 / 3729 / 3734

E-mail: [email protected]

56