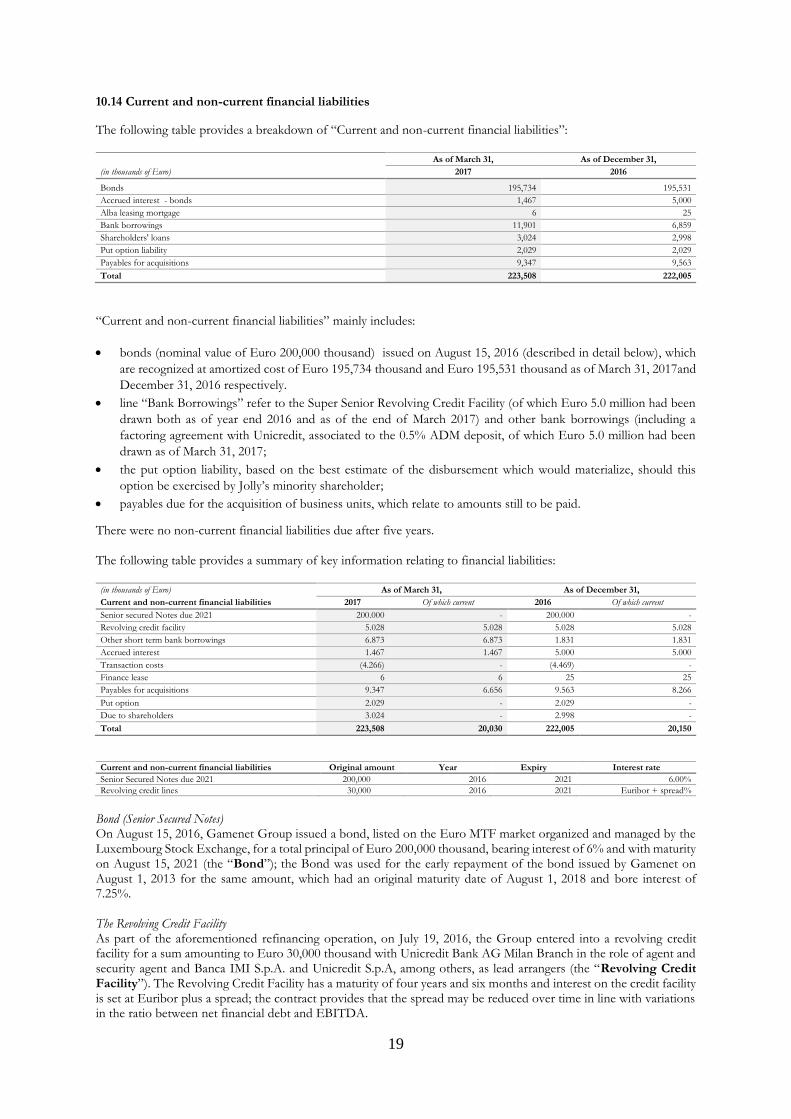

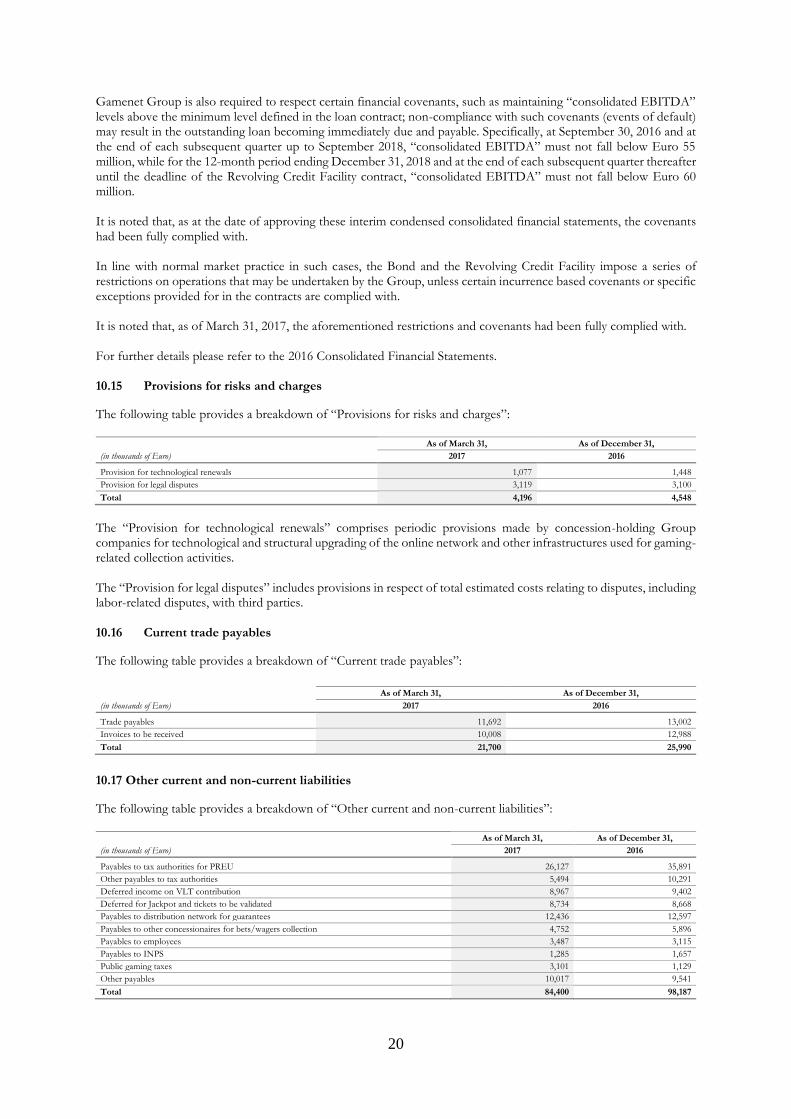

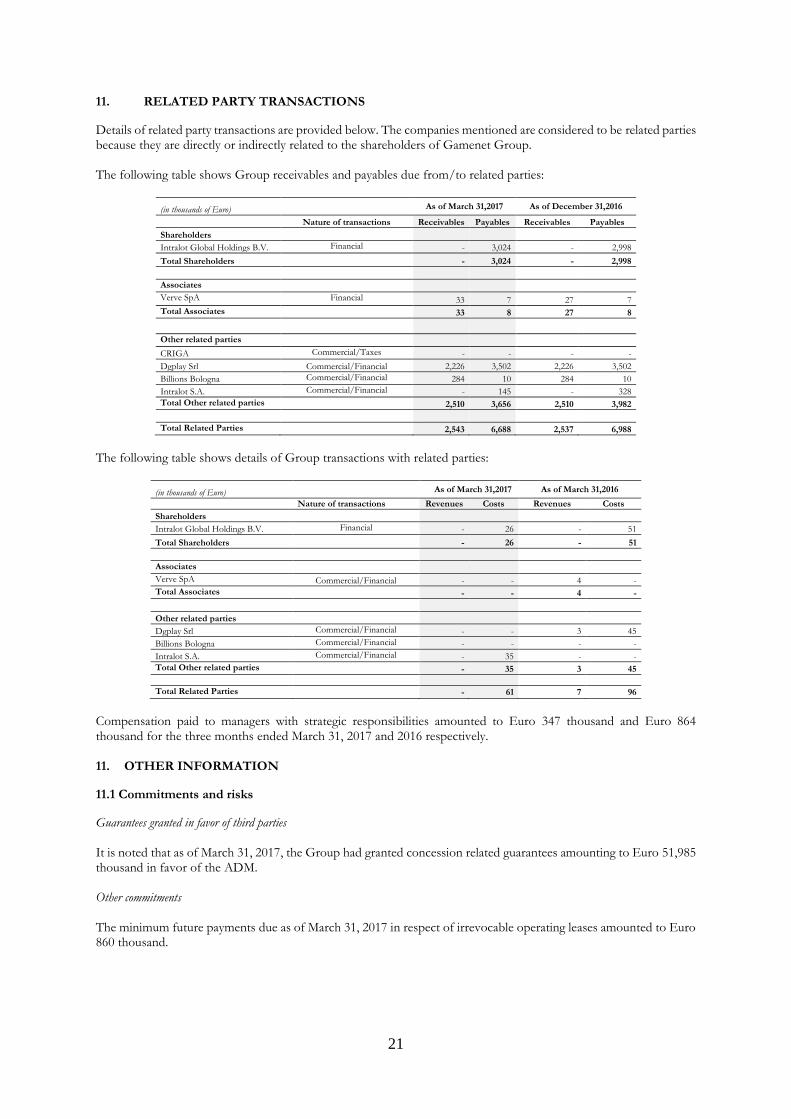

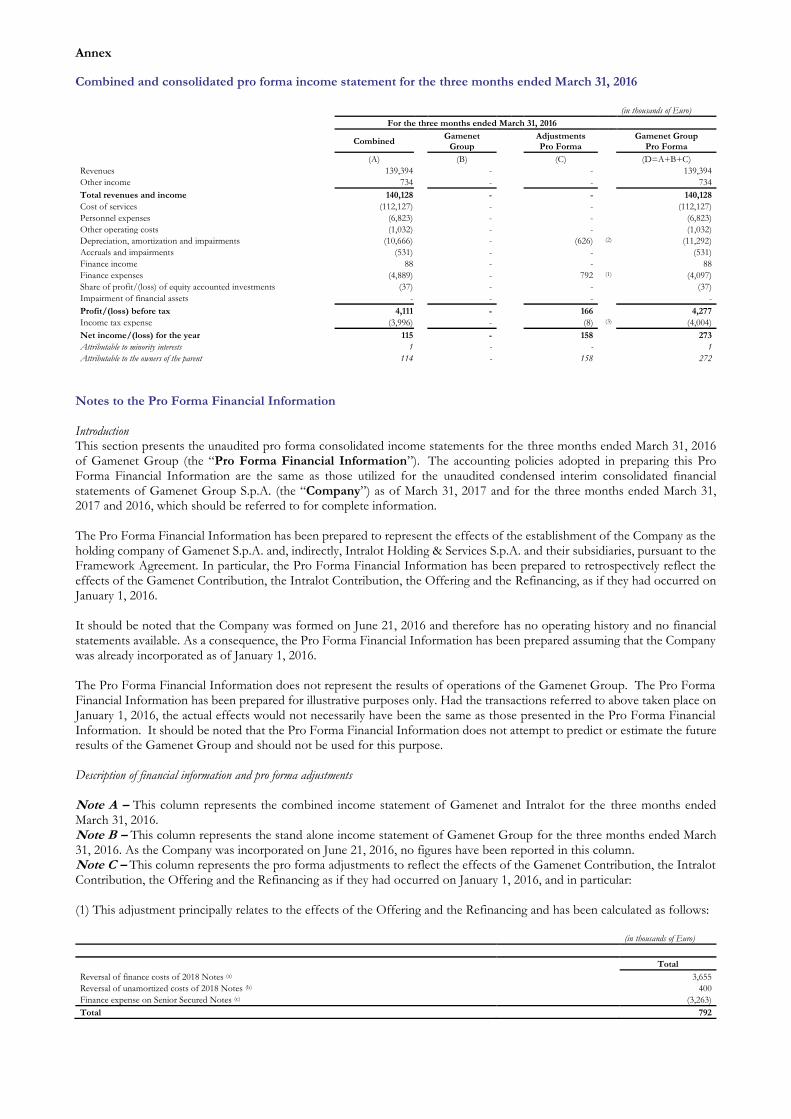

unaudited interim condensed consolidated financial ... · gamenet group unaudited interim condensed...

TRANSCRIPT

GAMENET GROUP

UNAUDITED INTERIM CONDENSED CONSOLIDATED

FINANCIAL STATEMENTS

AS OF MARCH 31, 2017 AND FOR THE THREE MONTHS ENDED

MARCH 31, 2017 AND 2016

The following information is confidential and does not constitute an offer to sell or a solicitation of an offer to buy any securities of Gamenet Group S.p.A. or any of its subsidiaries or affiliates. Any such securities may not be offered or sold in the United States absent registration unless pursuant to an applicable exemption from the registration requirements of the U.S. Securities Act and other applicable securities laws. The information provided on the following pages is not intended for distribution into or within the United States of America or to U.S. persons other than to “qualified institutional buyers” as defined under Rule 144A of the U.S. Securities Act. Statements on the following pages which are not historical facts are forward-looking statements. All forward-looking statements involve risks and uncertainties which could affect Gamenet Group S.p.A.’s actual results and could cause its actual results to differ materially from those expressed in any forward-looking statements made by, or on behalf of, Gamenet Group S.p.A..

Management’s report on the Group’s result at March 31, 2017

BASIS OF PRESENTATION Gamenet Group S.p.A. (hereafter ‘‘Gamenet Group’’, the ‘‘Company’’ or the ‘‘Parent’’ and together with its subsidiaries and associates the ‘‘Group’’ or “Gamenet Group”) is a company incorporated and domiciled in Italy, with registered offices in Rome, Corso d’Italia 6, organized under the laws of the Republic of Italy. The Company was incorporated on June 21, 2016 to effect the acquisition (hereafter the ‘‘Acquisition”) on June 27, 2016 of Intralot Holding & Services S.p.A. (hereafter ‘‘Intralot”) by Gamenet S.p.A. (hereafter ‘‘Gamenet”).

The Company is controlled by TCP Lux Euroinvest S.à.r.l. (hereafter ‘‘TCP”), which holds 79.1% of the share capital; the remaining share capital is held 20% by the Dutch company Intralot Italian Investments B.V. (hereafter “Intralot B.V.”) and 0.9% by Stefano Francolini. Gamenet Group is one of the largest operators in the Italian public gaming sector, which is regulated by the Customs and

Monopolies Agency (Agenzia delle Dogane e dei Monopoli hereafter “ADM”). The Group is an active gaming concessionaire and

has a product offering ranging from AWP (Amusement With Prizes) and VLT (Video Lottery Terminals), to management of

its nationwide network of variously branded company owned points of sales, betting and online as well as service provision

to business partners.

This report on operations has been prepared to provide additional information and offer a more complete representation of the Group’s financial position and economic results.

OVERVIEW

We are one of the largest players in the gaming industry in Italy based on total bet and distribution network with Euro 1.8 billion in bets collected in the three months ended March 31, 2017 across a network of approximately 14,000 points of sale.

As of March 31, 2017, our distribution network included 781 gaming halls. Of the 781 gaming halls in our distribution network, we owned (or held a majority interest) in 64. In these gaming halls, we hold the required authorizations and the lease contracts.

The Group operates in four main business areas: (i) video lottery terminal (“VLT”), (ii) amusement with prize (“AWP”), (iii) betting and online (“Betting and online”), (iv) company owned gaming halls and direct AWP operations (“Retail and Street Operations”).

VLT

VLTs were first introduced to Italy in August 2010 and to date they represent the most innovative and attractive gaming solution for players, due to the wide variety of games offered and a high average payout ratio. They also offer the chance to win jackpots of up to Euro 500,000.

At present, Gamenet offers three VLT platforms, Spielo, Novomatic and Inspired, which differ in terms of the games on offer and whether or not jackpots are foreseen.

Group VLTs accept Euro 0.50, Euro 1 and Euro 2 coins as well as Euro 5, Euro 10, Euro 20, Euro 50 and Euro 100 notes. In each game, bets may range from a minimum of Euro 0.50 to a maximum of Euro 10.

The percentage of bets paid out as winnings may not be lower than 85%, with reference both to the gaming system as a whole and to each individual game.

The maximum payout for a single game is Euro 5,000. However, in the case of the Spielo VLTs, higher winnings are possible as a result of the Jackpot mechanism referred to above.

As of March 31, 2017 we operated 8,225 VLTs.

MANAGEMENT’S REPORT ON THE GROUP’S RESULT AT

MARCH 31, 2017

AWP

AWPs are traditional slot machines that offer players a good level of interaction, using a graphical reel containing pictures; they also offer controlled-win games that pay cash to winners.

The maximum cost of each single game is Euro 1.00 and the maximum win is set at Euro 100.00. Each game must last at least 4 seconds and any winnings must be distributed immediately after the game (only) in coins.

Winnings, which are calculated by the machines on a random basis over a cycle comprising a maximum of 140,000 games, must not fall below 70% of the amounts bet. New slot machines may not reproduce the game of poker nor, even partially, its basic rules.

AWPs may be installed in all authorized betting shops pursuant to Articles 86 or 88 of the TULPS, including bars, coffee shops and similar outlets, public gaming halls, horse racing and sports betting shops and corners, etc.

As of March 31, 2017 we provided network connection services to 40,384 AWPs.

Betting and online

Gamenet Group is active in the betting and online segment through a network of around 750 sport betting rights e 58 horse betting rights. The Company operates through its subsidiaries Gamenet Scommesse S.p.A. Intralot Italia S.p.A. and Veneta Servizi which offer their customers a wide range of games mainly including sports betting, virtual games and horse racing through 683 active points of sale. In addition, a wide variety of online products including poker casino games, bingo and prediction games are offered through the websites Gamenet.it and Intralot.it.

Retail and Street Operations

In 2012, Gamenet Group began to pursue a strategy of vertical integration in the retail segment by establishing a company, Gamenet Entertainment S.r.l., to conduct gaming hall business. Significant efforts have resulted in the Group now directly managing 64 company-owned gaming halls (7 of which are large-size gaming halls).

More recently, the Group continued pursuing its vertical integration strategy through:

• Retail: the acquisition, in March 2015, of 51% of Billions Italia S.r.l. (which opened two additional gaming halls during 2016); the acquisition through Gamenet Entertainment S.r.l. of 100% of Gamecity S.r.l. in August 2016; Verve S.p.A.’s company owned gaming hall started operations in 2016 (as also disclosed later in this document, the Group in April 2016 increased its equity interest in Verve from 51% to 100%); the acquisition, in March 2017, through Gamenet Entertainment, of 60% of La Chance S.r.l., which owns the entire share capital of Slot Planet S.r.l.

• Street Operations: the acquisition of 100% of Gnetwork S.r.l. in August 2015; the acquisition of 70% of Jolly Videogiochi S.r.l. and 51% of NewMatic S.r.l. in June 2016, all aimed at developing the Group’s position in the AWP Street Operations business.

• Service providing: the acquisition in July 2016 of 60% of Agesoft S.r.l., a company specialized in the development of software for the AWP business.

Significant events

Relating to Gamenet Group S.p.A.

On March 23, 2017 Intralot Global Holdings B.V., which held 20% of the issued and paid up share capital of Gamenet Group S.p.A., contributed and transferred the full legal and beneficial right, title and interest in and to Intralot Italian Investments B.V., in which Intralot Global Holdings B.V. holds the entire issued share capital. Relating to Gamenet S.p.A. / Intralot Gaming Machines S.p.A. / Intralot Holdigs & Services S.p.A

• On January 31, 2017, 2% of the share capital of Intralot Gaming Machines S.p.A., owned by Gamenet S.p.A., was transferred to Intralot Holding & Services S.p.A.. As a result of this operation, the company's share capital is now 100% owned by Intralot Holding & Services S.p.A..

MANAGEMENT’S REPORT ON THE GROUP’S RESULT AT

MARCH 31, 2017

• During the first quarter of 2017, the board of directors of Gamenet S.p.A. / Intralot Holdings & Services S.pA. / Intralot Gaming Machines S.p.A. approved the merger project (“Progetto di Fusione”) of both Intralot Gaming Machines S.p.A. and Intralot Holdings & Services S.p.A. into Gamenet S.p.A. The merger, which is expected to be completed during the second quarter of 2017, is meant to streamline the existing corporate structure.

Relating to Gamenet Entertainment S.r.l.

On March 2, 2017 Gamenet Entertainment S.r.l. acquired 60% of the share capital of La Chance S.r.l., which owns the entire share capital of Slot Planet S.r.l.. These companies are active in the public gaming sector through the management of VLT gaming halls.

MANAGEMENT’S REPORT ON THE GROUP’S RESULT AT

MARCH 31, 2017

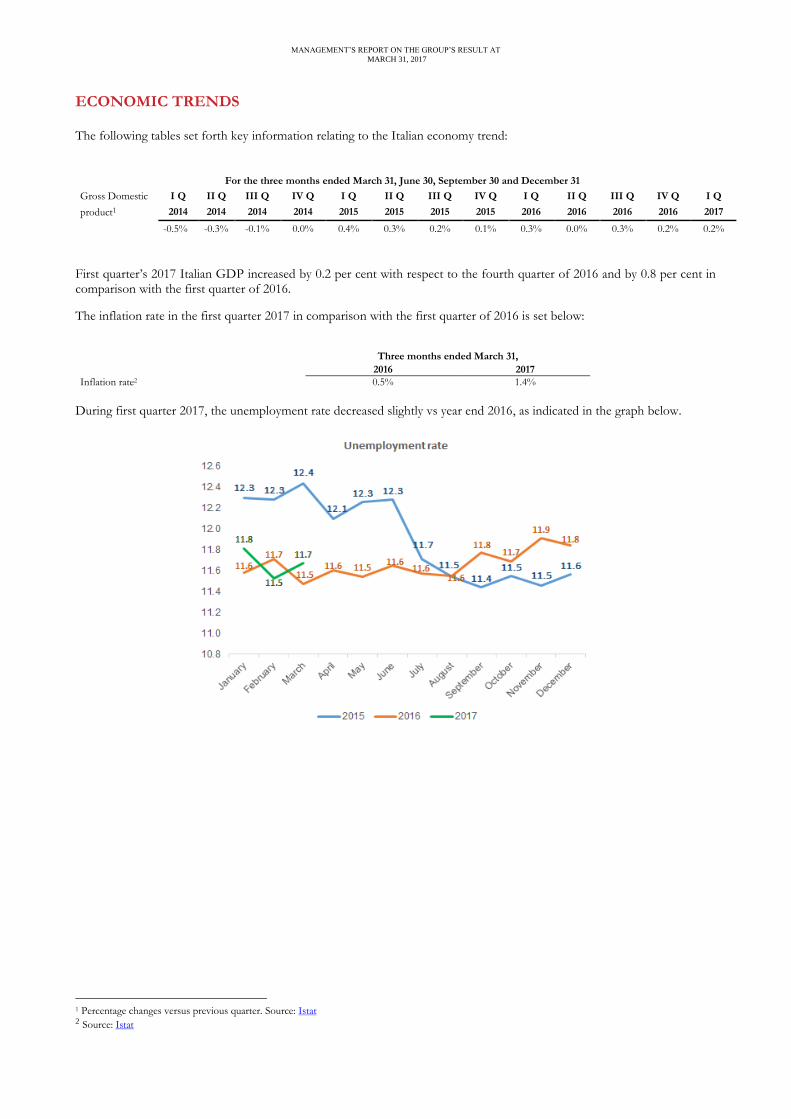

ECONOMIC TRENDS

The following tables set forth key information relating to the Italian economy trend:

For the three months ended March 31, June 30, September 30 and December 31 Gross Domestic I Q II Q III Q IV Q I Q II Q III Q IV Q I Q II Q III Q IV Q I Q

product1 2014 2014 2014 2014 2015 2015 2015 2015 2016 2016 2016 2016 2017

-0.5% -0.3% -0.1% 0.0% 0.4% 0.3% 0.2% 0.1% 0.3% 0.0% 0.3% 0.2% 0.2%

First quarter’s 2017 Italian GDP increased by 0.2 per cent with respect to the fourth quarter of 2016 and by 0.8 per cent in comparison with the first quarter of 2016.

The inflation rate in the first quarter 2017 in comparison with the first quarter of 2016 is set below:

Three months ended March 31,

2016 2017

Inflation rate23 0.5% 1.4%

During first quarter 2017, the unemployment rate decreased slightly vs year end 2016, as indicated in the graph below.

1 Percentage changes versus previous quarter. Source: Istat 2 Source: Istat

MANAGEMENT’S REPORT ON THE GROUP’S RESULT AT

MARCH 31, 2017

OPERATING INFORMATION

The following table sets forth key information for the VLT activities for the three months ended March 31, 2017 and the three months ended March 31, 2016:

For the three months ended March 31, 2017 2016

(€ in millions, except non-financial information and percentages)

Number of VLT licenses awarded 8,570

7,805

Average number of VLTs in operation for the period 8,205

7,437

Number of VLTs in operation as of the period end 8,225

7,489

As a percentage of VLT rights 96.0%

96.0%

VLT Bet (*) 811

773

VLT PREU (as percentage of bet) 5.5% 5.5%

(*)This figure does not include bet generated by the Retail segment in the Isola del Tesoro, Gamecity and Billions (Rome and Bologna) gaming halls connected to other concessionaires, amounting to Euro 75.1 million.

As of March 31, 2017, Gamenet Group held 8,570 licenses, of which 8,225 VLT machines were in operation, equal to 96.0% of available licenses, which represents full deployment when considering the machines under maintenance or subject to asset management activities. Total VLT bet increased by 4.9% from 773 million for the three months ended March 31, 2016 to Euro 811 million for the three months ended March 31, 2017. This is mainly due to a 10.3% increase in the average number of VLTs in operation during the period, partly compensated by a 4.9% decrease in unit bet. Considering Intralot as part of the consolidation area also in the three months ended March 31, 2016, bet would have increased by 2.8% from Euro 789 million to Euro 811 million for the three months ended March 31, 2017. The following table sets forth key information for the AWP business for the three months ended March 31, 2017 and 2016:

For the three months ended March 31,

2017 2016

(€ in millions, except non-financial information and percentages)

Number of AWPs in operation as of the period end 40,384 28,754

Average number of AWPs in operation for the period 39,621 28,760

AWP Bet (*) 655 574

AWP PREU (as percentage of bet) 17.5% 17.5%

(*)This figure does not include bet generated by the Retail segment in the Isola del Tesoro, Gamecity and Billions (Rome and Bologna) gaming halls connected to other concessionaires, amounting to Euro 42.0 million.

For the three months ended March 31, 2017, we had an average of 39,621 machines in operation, an increase of 37.8% compared to the three months ended March 31, 2016. Total AWP bet increased by 14.1% amounting to Euro 655 million for the three months ended March 31, 2017 and Euro 574 million for the three months ended March 31, 2016. This is mainly due to the increase in the average number of AWPs in operation mentioned above, partly offset by a 17.2% reduction in unit bet. This decline is a market wide event, primarily driven by the fact that the so called “gestori” (i.e. the members of the supply chain who actually own the AWPs) temporarily reduced their investments in new games, waiting to have more clarity around the expected 30% reduction in the number of AWPs. In other words: players start to get used to existing games / there is limited “novelty” effect generated by new products being introduced into the market (and having new products available help offset the impact of AWP payout reduction, which increased by about 15% the unit cost of entertainment for players). Considering Intralot as part of the consolidation area for the three months ended March 31, 2016, the average number of operational machines would have increased by 3.4% while bet would have decreased by 13.0%. The following table sets forth key information for the Betting and Online business for the three months ended March 31, 2017 and 2016:

MANAGEMENT’S REPORT ON THE GROUP’S RESULT AT

MARCH 31, 2017

For the three months ended March 31,

2017 2016

(€ in millions, except non-financial information and percentages) Number of licenses/concessions (1) 750 185 Number of active points of sale as of March 31 (shops and corner) 683 165 Average number of active points of sale (shops and corner) 678 167 Total retail bet 134.8 17.8 Average bet per point of sale for the period 0.20 0.11 Total online bet 60.4 2.8

(1) Does not include the 58 licenses related to horse racing bet Total bets for the first quarter ended March 31, 2017, increased by more than 100% compared to the same period of last year (moving from Euro 20.6 million in 2016 to Euro 195.2 million in 2017), mainly due to the Intralot acquisition. Specifically, Retail bet increased from Euro 17.8 million in 2016 to Euro 133.9 million in 2017 and Online bet increased from Euro 2.9 million to Euro 60.4 million. The average bet per point of sale increased very significantly, from Euro 0.11 million for the three months ended March 2016 to Euro 0.20 million for the three months ended March 2017. This is because of Intralot’s best in class product offering, now extended also to the heritage Gamenet network. Considering Intralot as part of the consolidation area also in the three months ended March 31, 2016 total bet would have increased by 15.4%. As far as the Retail & Street Operations segment is concerned, bet increased from Euro 98.3 million for the three months ended March 31, 2016 to Euro 117.2 million for the three months ended March 31, 2017, representing a 19.4% year on year increase. After reclassifying bet generated in company owned gaming halls (through machines connected to the Group’s Concessionaires) the Retail and Street Operations segment generated about Euro 219 million worth of bet for the three months ended 31 March, 2017 (i.e. 29.3% up vs Euro 169.3 million in the same period of last year).

MANAGEMENT’S REPORT ON THE GROUP’S RESULT AT

MARCH 31, 2017

KEY FINANCIAL INDICATORS

The following table provides details of the main financial and economic indicators.

For the three months ended March 31, 2017 2016

(€ in thousands) Revenues 155,489 103,202 EBITDA(1) 17,441 16,657 Profit (loss) for the period 274 572 Shareholders’ Equity 66,174 65,885 Net financial debt (177,843) (158,849)

(1) EBITDA is defined as net profit (or loss) for the year adjusted for: (i) Income tax expense; (ii) Finance expenses; (iii) Finance income; (iv) Share of profit/(loss) of equity accounted investments (v) Impairment of financial assets; (vi) Depreciation, amortization and impairments; (vii) Reclassification to profit or loss of multiannual prepayments; (viii) Non-recurring income and expenses

For the three months ended March 31, 2017 2016

(€ in thousands)

Net profit (loss) for the period 274

571

Income tax expense 2,379 3,995 Finance income (193) (87) Finance expenses 4,005 4,620 Share of (profit)/loss of equity accounted investments 15 37 Impairment of financial assets - - Depreciation, amortization and impairment 9,110 6,432 Non-monetary costs (reclassification to profit or loss of multiannual prepayments) 1,162 1,089 Non recurring income and expense (1) 688 - EBITDA 17,441 16,657

(1) Non recurring income and expense refer to severance costs and ancillary costs on acquisitions

MANAGEMENT’S REPORT ON THE GROUP’S RESULT AT

MARCH 31, 2017

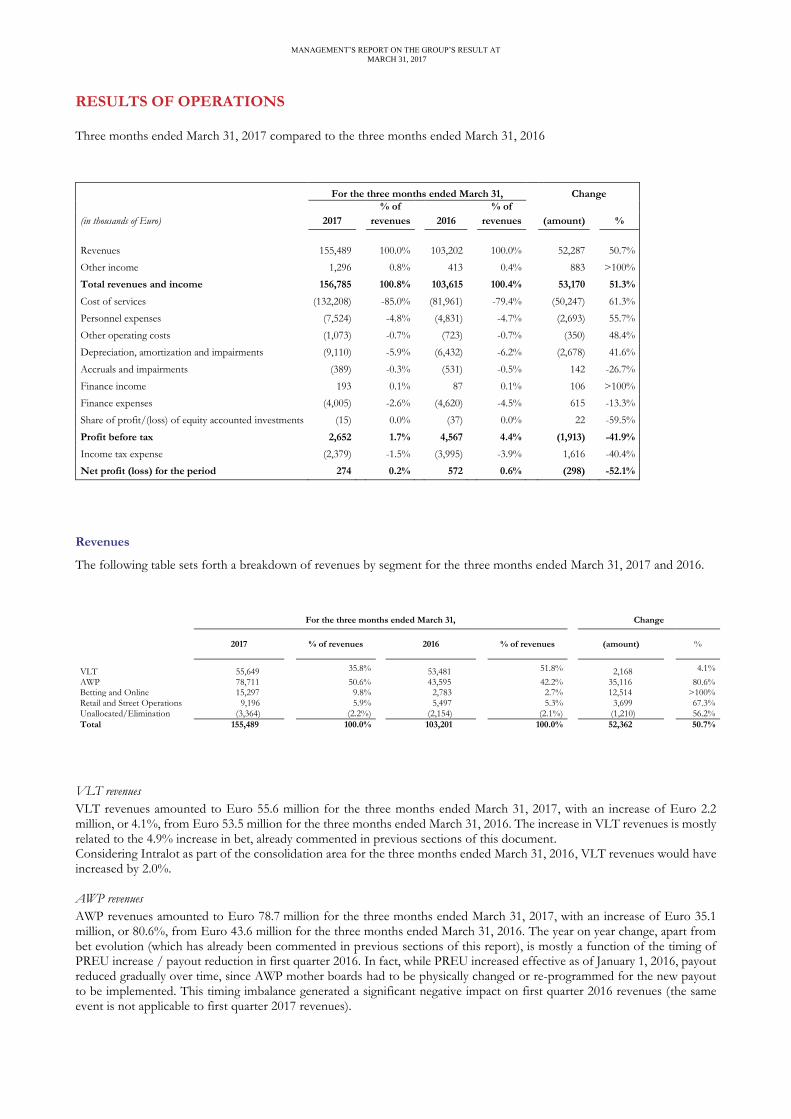

RESULTS OF OPERATIONS

Three months ended March 31, 2017 compared to the three months ended March 31, 2016

For the three months ended March 31, Change

% of % of (in thousands of Euro) 2017 revenues 2016 revenues (amount) %

Revenues 155,489 100.0% 103,202 100.0% 52,287 50.7%

Other income 1,296 0.8% 413 0.4% 883 >100%

Total revenues and income 156,785 100.8% 103,615 100.4% 53,170 51.3%

Cost of services (132,208) -85.0% (81,961) -79.4% (50,247) 61.3%

Personnel expenses (7,524) -4.8% (4,831) -4.7% (2,693) 55.7%

Other operating costs (1,073) -0.7% (723) -0.7% (350) 48.4%

Depreciation, amortization and impairments (9,110) -5.9% (6,432) -6.2% (2,678) 41.6%

Accruals and impairments (389) -0.3% (531) -0.5% 142 -26.7%

Finance income 193 0.1% 87 0.1% 106 >100%

Finance expenses (4,005) -2.6% (4,620) -4.5% 615 -13.3%

Share of profit/(loss) of equity accounted investments (15) 0.0% (37) 0.0% 22 -59.5%

Profit before tax 2,652 1.7% 4,567 4.4% (1,913) -41.9%

Income tax expense (2,379) -1.5% (3,995) -3.9% 1,616 -40.4%

Net profit (loss) for the period 274 0.2% 572 0.6% (298) -52.1%

Revenues

The following table sets forth a breakdown of revenues by segment for the three months ended March 31, 2017 and 2016.

For the three months ended March 31, Change

2017

% of revenues

2016

% of revenues

(amount)

%

VLT 55,649 35.8% 53,481 51.8%

2,168 4.1%

AWP 78,711 50.6% 43,595 42.2% 35,116 80.6% Betting and Online 15,297 9.8% 2,783 2.7% 12,514 >100% Retail and Street Operations 9,196 5.9% 5,497 5.3% 3,699 67.3% Unallocated/Elimination (3,364) (2.2%) (2,154) (2.1%) (1,210) 56.2%

Total 155,489 100.0% 103,201 100.0% 52,362 50.7%

VLT revenues

VLT revenues amounted to Euro 55.6 million for the three months ended March 31, 2017, with an increase of Euro 2.2 million, or 4.1%, from Euro 53.5 million for the three months ended March 31, 2016. The increase in VLT revenues is mostly related to the 4.9% increase in bet, already commented in previous sections of this document. Considering Intralot as part of the consolidation area for the three months ended March 31, 2016, VLT revenues would have increased by 2.0%. AWP revenues

AWP revenues amounted to Euro 78.7 million for the three months ended March 31, 2017, with an increase of Euro 35.1 million, or 80.6%, from Euro 43.6 million for the three months ended March 31, 2016. The year on year change, apart from bet evolution (which has already been commented in previous sections of this report), is mostly a function of the timing of PREU increase / payout reduction in first quarter 2016. In fact, while PREU increased effective as of January 1, 2016, payout reduced gradually over time, since AWP mother boards had to be physically changed or re-programmed for the new payout to be implemented. This timing imbalance generated a significant negative impact on first quarter 2016 revenues (the same event is not applicable to first quarter 2017 revenues).

MANAGEMENT’S REPORT ON THE GROUP’S RESULT AT

MARCH 31, 2017

Considering Intralot as part of the consolidation area for the three months ended March 31, 2016 AWPs revenues would have increased by 33.2%.

Betting & Online Revenues

Betting & Online revenues amounted to Euro 15.3 million for the three months ended March 31, 2017, with an increase of Euro 12.5 million, or more than 100%, compared to Euro 2.8 million for the three months ended March 31, 2016. As already commented, the key driver of this year on year increase is the Intralot acquisition. Considering Intralot as part of the consolidation area for the three months ended March 31, 2016 betting and online revenues would have decreased by 29.2%. This is primarily a function of the market wide evolution in payout (with Retail Sport Betting payout moving from 79.9% in first quarter 2016 to 88.6% in first quarter 2017). Retail & Street Operations Revenues

Retail & Street Operations revenues amounted to Euro 9.2 million for the three months ended March 31, 2017, with an increase of Euro 3.7 million, or 67.3%, compared to Euro 5.5 million for the three months ended March 31, 2016. The increase essentially reflects the impact of acquisitions finalized in the period, as well as organic growth / improved performance of existing operations.

Other income

Other income amounted to Euro 1.3 million for the three months ended March 31, 2017, with an increase of Euro 0.9 million, from Euro 0.4 million for the three months ended March 31, 2016. The year on year increase in mainly attributable to the impact of new acquisitions and other miscellaneous items (including penalties).

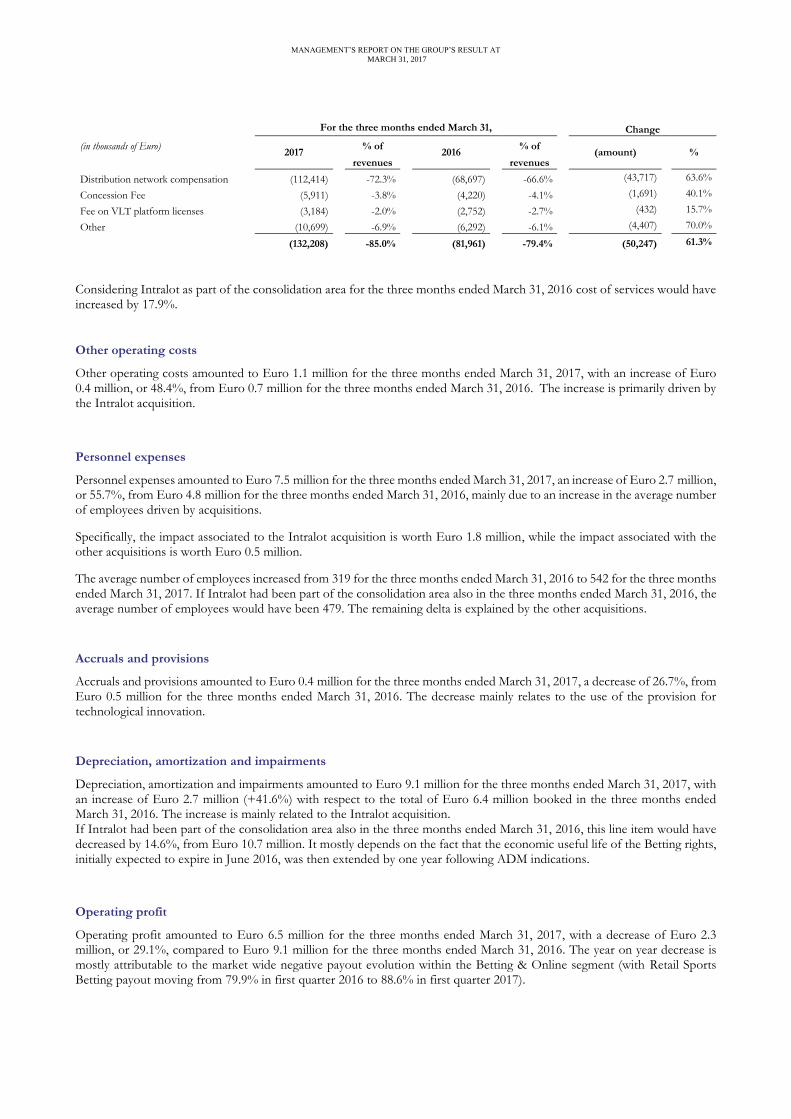

Cost of services

Cost of services amounted to Euro 132.2 million for the three months ended March 31, 2017, with an increase of Euro 50.2 million, or 61.3%, from Euro 82.0 million for the three months ended March 31, 2016. As a percentage of revenues, cost of services accounted to 85.0% for the three months ended March 31, 2017 compared to 79.4% for the three months ended March 31, 2016. Cost of services mainly relate to the compensation paid to the distribution network, which amounted to Euro 112.4 million for the three months ended March 31, 2017, with an increase of Euro 43.7 million, or 63.6%, from Euro 68.7 million for the three months ended March 31, 2016. This increase is mainly a function of the evolution in first quarter’s 2016 revenues which has been commented earlier (as a reminder, revenues were negatively impacted by the timing of PREU increase vis-à-vis payout reduction). Since the AWP contractual structure is largely pass through vis-à-vis revenue changes, lower revenues translate into lower distribution costs. First quarter 2017 is not impacted by these dynamics. The year on year increase in Distribution Network Compensation is also explained by higher Betting & Online wagers, following the Intralot acquisition. This factor is worth Euro 10.6 million.

Cost of services also includes the ADM concession fee which amounted to Euro 5.9 million for the three months ended March 31, 2017, with an increase of Euro 1.7 million, or 40.1% compared to Euro 4.2 million for the three months ended March 31, 2016. The ADM concession fee, calculated as a percentage of AWP, VLT and Betting and online wagers, accounted to 0.36% for the three months ended March 31, 2017 compared to 0.31% for the three months ended March 31, 2016. The year on year increase refers primarily to the increase in betting wagers which carry a higher concession fee.

Fee on VLT platform licenses amounted to Euro 3.2 million for the three months ended March 31, 2017, an increase of Euro 0.4 million, or 15.7%, from Euro 2.8 million for the three months ended March 31, 2016. Percentage wise, the year on year increase in VLT platform license costs exceeds bet increase. This is due to a mix effect with a higher proportion of bet from platforms with higher unit costs.

Other cost of services increased from Euro 6.3 million for the three months ended March 31, 2016 to Euro 10.7 million for the three months ended March 31, 2017. Among the drivers, increased lease, marketing and utility costs, linked to the Intralot acquisition as well as to the full year impact of recently finalized acquisitions within the Retail and Street Operations segment.

The following table sets forth an analysis of cost of services for the periods indicated.

MANAGEMENT’S REPORT ON THE GROUP’S RESULT AT

MARCH 31, 2017

For the three months ended March 31,

Change

(in thousands of Euro) 2017

% of 2016

% of (amount) %

revenues

revenues

Distribution network compensation (112,414) -72.3% (68,697) -66.6% (43,717) 63.6%

Concession Fee (5,911) -3.8% (4,220) -4.1% (1,691) 40.1%

Fee on VLT platform licenses (3,184) -2.0% (2,752) -2.7% (432) 15.7%

Other (10,699) -6.9% (6,292) -6.1% (4,407) 70.0%

(132,208) -85.0% (81,961) -79.4% (50,247) 61.3%

Considering Intralot as part of the consolidation area for the three months ended March 31, 2016 cost of services would have increased by 17.9%.

Other operating costs

Other operating costs amounted to Euro 1.1 million for the three months ended March 31, 2017, with an increase of Euro 0.4 million, or 48.4%, from Euro 0.7 million for the three months ended March 31, 2016. The increase is primarily driven by the Intralot acquisition.

Personnel expenses

Personnel expenses amounted to Euro 7.5 million for the three months ended March 31, 2017, an increase of Euro 2.7 million, or 55.7%, from Euro 4.8 million for the three months ended March 31, 2016, mainly due to an increase in the average number of employees driven by acquisitions.

Specifically, the impact associated to the Intralot acquisition is worth Euro 1.8 million, while the impact associated with the other acquisitions is worth Euro 0.5 million.

The average number of employees increased from 319 for the three months ended March 31, 2016 to 542 for the three months ended March 31, 2017. If Intralot had been part of the consolidation area also in the three months ended March 31, 2016, the average number of employees would have been 479. The remaining delta is explained by the other acquisitions.

Accruals and provisions

Accruals and provisions amounted to Euro 0.4 million for the three months ended March 31, 2017, a decrease of 26.7%, from Euro 0.5 million for the three months ended March 31, 2016. The decrease mainly relates to the use of the provision for technological innovation.

Depreciation, amortization and impairments

Depreciation, amortization and impairments amounted to Euro 9.1 million for the three months ended March 31, 2017, with an increase of Euro 2.7 million (+41.6%) with respect to the total of Euro 6.4 million booked in the three months ended March 31, 2016. The increase is mainly related to the Intralot acquisition. If Intralot had been part of the consolidation area also in the three months ended March 31, 2016, this line item would have decreased by 14.6%, from Euro 10.7 million. It mostly depends on the fact that the economic useful life of the Betting rights, initially expected to expire in June 2016, was then extended by one year following ADM indications.

Operating profit

Operating profit amounted to Euro 6.5 million for the three months ended March 31, 2017, with a decrease of Euro 2.3 million, or 29.1%, compared to Euro 9.1 million for the three months ended March 31, 2016. The year on year decrease is mostly attributable to the market wide negative payout evolution within the Betting & Online segment (with Retail Sports Betting payout moving from 79.9% in first quarter 2016 to 88.6% in first quarter 2017).

MANAGEMENT’S REPORT ON THE GROUP’S RESULT AT

MARCH 31, 2017

Finance expenses

Finance expenses amounted to Euro 4.0 million for the three months ended March 31, 2017, a decrease of Euro 0.6 million, or 13.3%, from Euro 4.6 million for the three months ended March 31, 2016. The decrease mainly relates to the lower interest rate applicable to the Euro 200 million senior secured notes due 2021 issued by Gamenet Group S.p.A. on August 15, 2016.

Profit before tax

Profit before tax amounted to Euro 2.7 million for the three months ended March 31, 2017, with a decrease of Euro 1.9 million from the profit of Euro 4.6 million for the three months ended March 31, 2016. The drivers of this year on year decrease have been commented earlier.

Income tax

Income tax amounted to Euro 2.4 million for the three months ended March 31, 2017, with a decrease of Euro 1.6 million, or -40.4%, from Euro 4.0 million for the three months ended March 31, 2016.

Profit for the period

As a result of the factors explained above, the profit for the period amounted to Euro 0.3 million for the three months ended March 31, 2017, with a decrease of Euro 0.3 million from Euro 0.6 million for the three months ended March 31, 2016.

MANAGEMENT’S REPORT ON THE GROUP’S RESULT AT

MARCH 31, 2017

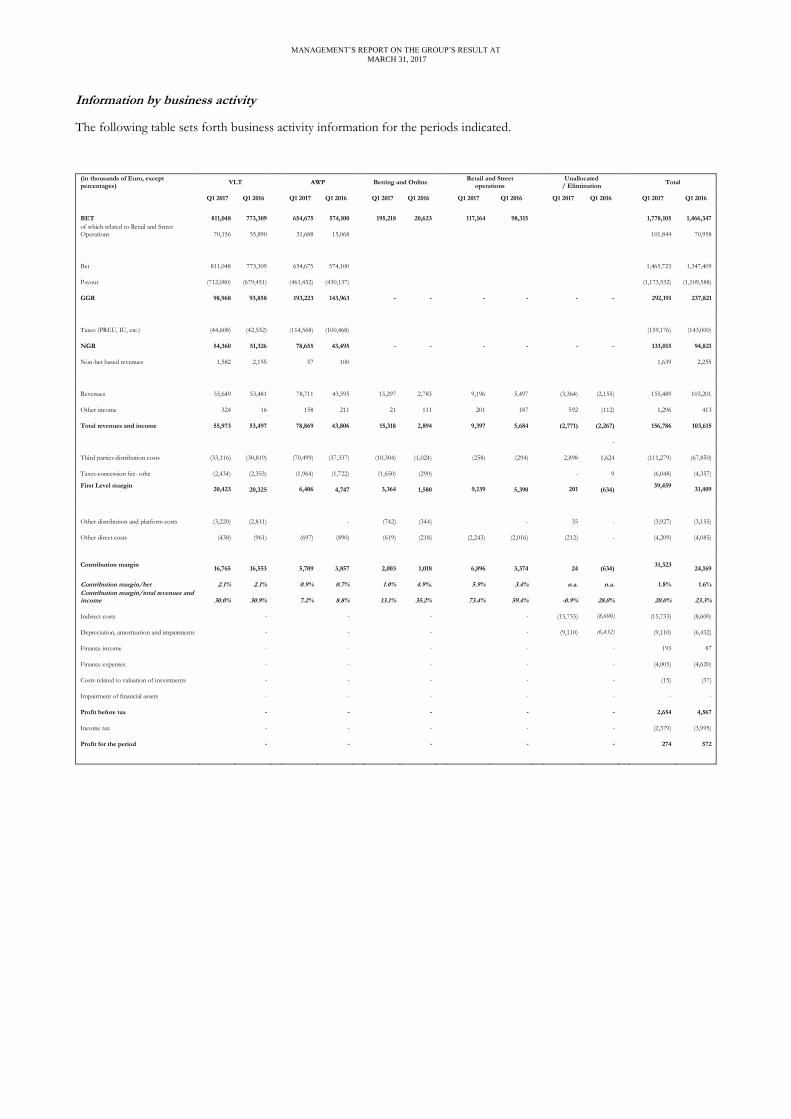

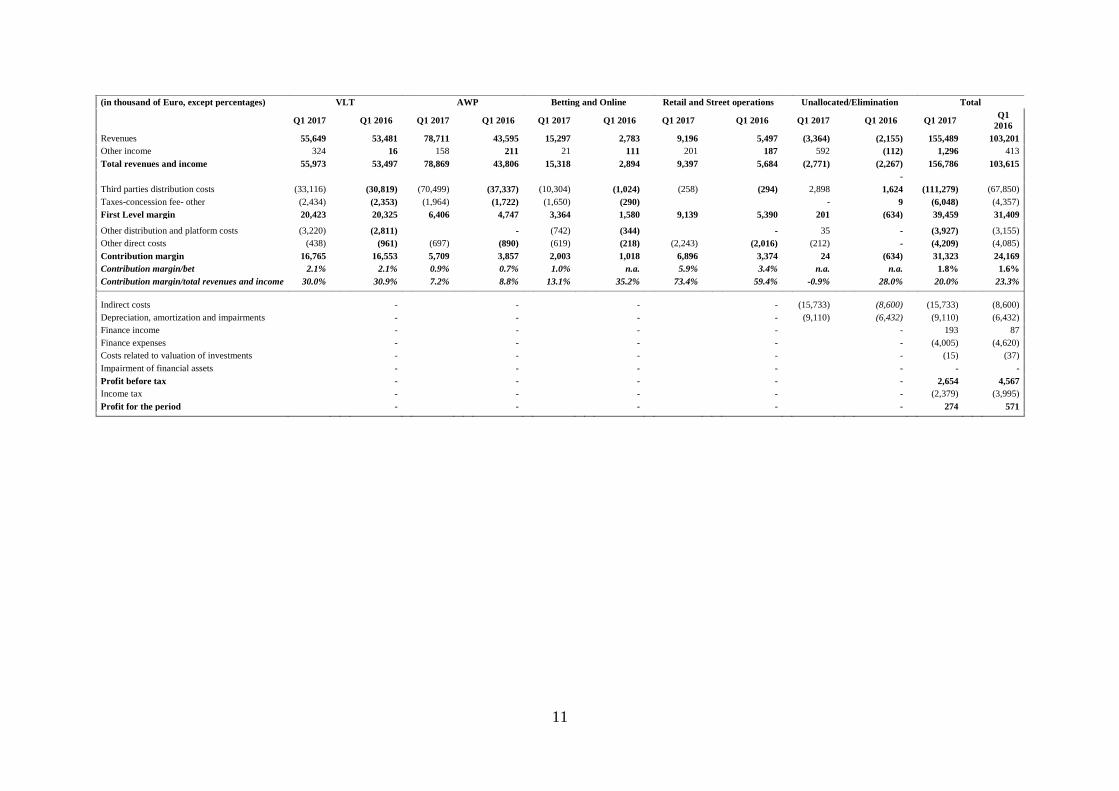

Information by business activity

The following table sets forth business activity information for the periods indicated.

(in thousands of Euro, except percentages)

VLT AWP

Betting and Online

Retail and Street operations

Unallocated / Elimination

Total

Q1 2017 Q1 2016 Q1 2017 Q1 2016 Q1 2017 Q1 2016 Q1 2017 Q1 2016 Q1 2017 Q1 2016 Q1 2017 Q1 2016

BET

811,048

773,309

654,675

574,100

195,218

20,623

117,164

98,315 1,778,105

1,466,347

of which related to Retail and Street Operations

70,156

55,890

31,688

15,068 101,844

70,958

Bet

811,048

773,309

654,675

574,100 1,465,723

1,347,409

Payout

(712,080)

(679,451)

(461,452)

(430,137) (1,173,532)

(1,109,588)

GGR

98,968

93,858

193,223

143,963

-

-

-

-

-

- 292,191

237,821

Taxes (PREU, IU, etc.)

(44,608)

(42,532)

(114,568)

(100,468) (159,176)

(143,000)

NGR

54,360

51,326

78,655

43,495

-

-

-

-

-

- 133,015

94,821

Non-bet based revenues

1,582

2,155

57

100 1,639

2,255

Revenues

55,649

53,481

78,711

43,595

15,297

2,783

9,196

5,497

(3,364)

(2,155) 155,489

103,201

Other income

324

16

158

211

21

111

201

187

592

(112) 1,296

413

Total revenues and income

55,973

53,497

78,869

43,806

15,318

2,894

9,397

5,684

(2,771)

(2,267) 156,786

103,615

-

Third parties distribution costs

(33,116)

(30,819)

(70,499)

(37,337)

(10,304)

(1,024)

(258)

(294)

2,898

1,624 (111,279)

(67,850)

Taxes-concession fee- othe

(2,434)

(2,353)

(1,964)

(1,722)

(1,650)

(290)

-

9 (6,048)

(4,357)

First Level margin

20,423

20,325

6,406

4,747

3,364

1,580

9,139

5,390

201

(634)

39,459

31,409

Other distribution and platform costs

(3,220)

(2,811)

-

(742)

(344)

-

35

- (3,927)

(3,155)

Other direct costs

(438)

(961)

(697)

(890)

(619)

(218)

(2,243)

(2,016)

(212)

- (4,209)

(4,085)

Contribution margin

16,765

16,553

5,709

3,857

2,003

1,018

6,896

3,374

24

(634) 31,323

24,169

Contribution margin/bet 2.1% 2.1% 0.9% 0.7% 1.0% 4.9%. 5.9% 3.4% n.a. n.a. 1.8% 1.6%

Contribution margin/total revenues and income 30.0% 30.9% 7.2% 8.8% 13.1% 35.2% 73.4% 59.4% -0.9% 28.0% 20.0% 23.3%

Indirect costs

-

-

-

-

(15,733)

(8,600) (15,733)

(8,600)

Depreciation, amortization and impairments

-

-

-

-

(9,110)

(6,432) (9,110)

(6,432)

Finance income

-

-

-

-

- 193

87

Finance expenses

-

-

-

-

- (4,005)

(4,620)

Costs related to valuation of investments

-

-

-

-

-

(15)

(37)

Impairment of financial assets

-

-

-

-

- -

-

Profit before tax

-

-

-

-

- 2,654

4,567

Income tax

-

-

-

-

-

(2,379)

(3,995)

Profit for the period

-

-

-

-

- 274

572

MANAGEMENT’S REPORT ON THE GROUP’S RESULT AT

MARCH 31, 2017

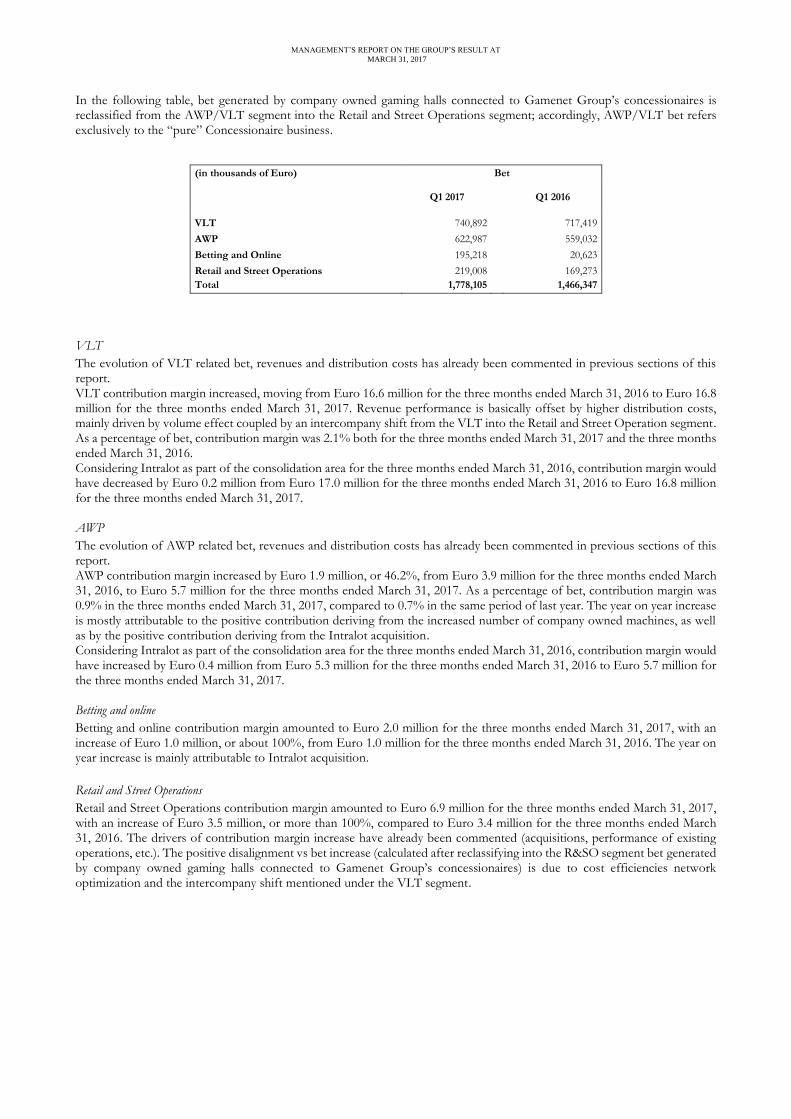

In the following table, bet generated by company owned gaming halls connected to Gamenet Group’s concessionaires is reclassified from the AWP/VLT segment into the Retail and Street Operations segment; accordingly, AWP/VLT bet refers exclusively to the “pure” Concessionaire business.

(in thousands of Euro) Bet

Q1 2017

Q1 2016

VLT 740,892 717,419

AWP 622,987 559,032

Betting and Online 195,218 20,623

Retail and Street Operations 219,008 169,273

Total 1,778,105 1,466,347

VLT

The evolution of VLT related bet, revenues and distribution costs has already been commented in previous sections of this report. VLT contribution margin increased, moving from Euro 16.6 million for the three months ended March 31, 2016 to Euro 16.8 million for the three months ended March 31, 2017. Revenue performance is basically offset by higher distribution costs, mainly driven by volume effect coupled by an intercompany shift from the VLT into the Retail and Street Operation segment. As a percentage of bet, contribution margin was 2.1% both for the three months ended March 31, 2017 and the three months ended March 31, 2016. Considering Intralot as part of the consolidation area for the three months ended March 31, 2016, contribution margin would have decreased by Euro 0.2 million from Euro 17.0 million for the three months ended March 31, 2016 to Euro 16.8 million for the three months ended March 31, 2017. AWP

The evolution of AWP related bet, revenues and distribution costs has already been commented in previous sections of this report. AWP contribution margin increased by Euro 1.9 million, or 46.2%, from Euro 3.9 million for the three months ended March 31, 2016, to Euro 5.7 million for the three months ended March 31, 2017. As a percentage of bet, contribution margin was 0.9% in the three months ended March 31, 2017, compared to 0.7% in the same period of last year. The year on year increase is mostly attributable to the positive contribution deriving from the increased number of company owned machines, as well as by the positive contribution deriving from the Intralot acquisition. Considering Intralot as part of the consolidation area for the three months ended March 31, 2016, contribution margin would have increased by Euro 0.4 million from Euro 5.3 million for the three months ended March 31, 2016 to Euro 5.7 million for the three months ended March 31, 2017. Betting and online

Betting and online contribution margin amounted to Euro 2.0 million for the three months ended March 31, 2017, with an increase of Euro 1.0 million, or about 100%, from Euro 1.0 million for the three months ended March 31, 2016. The year on year increase is mainly attributable to Intralot acquisition.

Retail and Street Operations

Retail and Street Operations contribution margin amounted to Euro 6.9 million for the three months ended March 31, 2017, with an increase of Euro 3.5 million, or more than 100%, compared to Euro 3.4 million for the three months ended March 31, 2016. The drivers of contribution margin increase have already been commented (acquisitions, performance of existing operations, etc.). The positive disalignment vs bet increase (calculated after reclassifying into the R&SO segment bet generated by company owned gaming halls connected to Gamenet Group’s concessionaires) is due to cost efficiencies network optimization and the intercompany shift mentioned under the VLT segment.

MANAGEMENT’S REPORT ON THE GROUP’S RESULT AT

MARCH 31, 2017

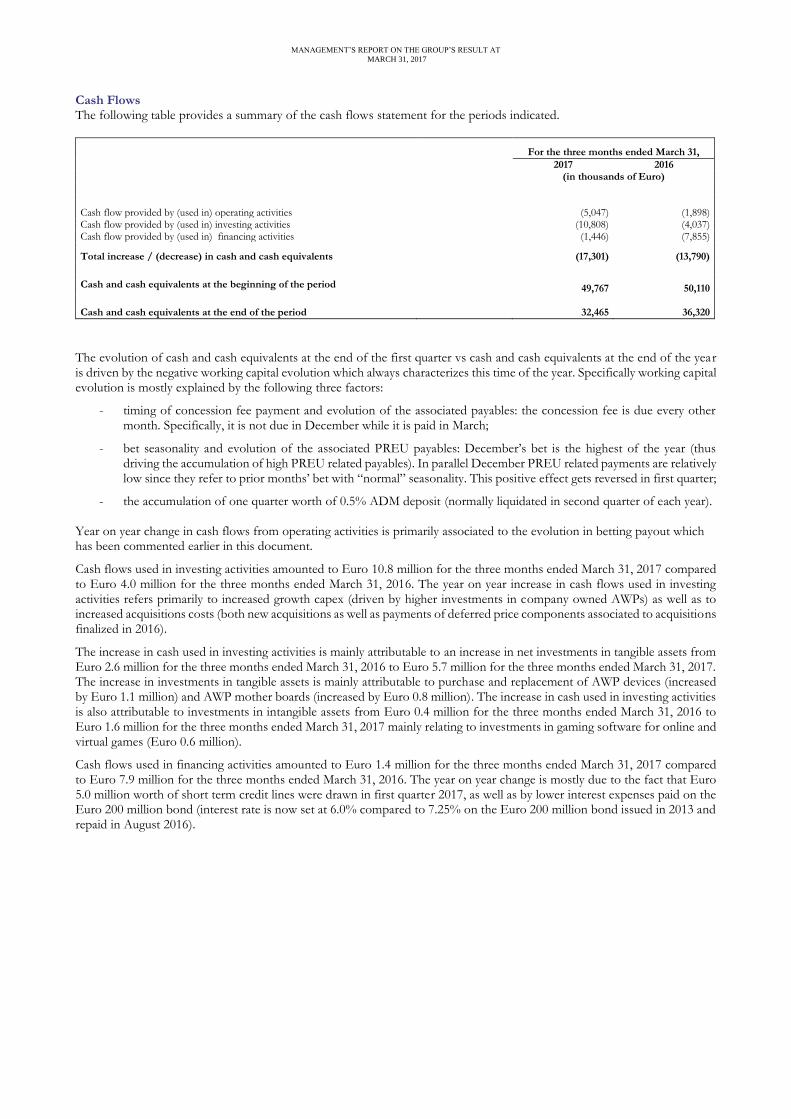

Cash Flows The following table provides a summary of the cash flows statement for the periods indicated.

For the three months ended March 31,

2017 2016 (in thousands of Euro)

Cash flow provided by (used in) operating activities (5,047)

(1,898) Cash flow provided by (used in) investing activities (10,808) (4,037) Cash flow provided by (used in) financing activities (1,446) (7,855)

Total increase / (decrease) in cash and cash equivalents (17,301) (13,790)

Cash and cash equivalents at the beginning of the period 49,767 50,110

Cash and cash equivalents at the end of the period 32,465 36,320

The evolution of cash and cash equivalents at the end of the first quarter vs cash and cash equivalents at the end of the year is driven by the negative working capital evolution which always characterizes this time of the year. Specifically working capital evolution is mostly explained by the following three factors:

- timing of concession fee payment and evolution of the associated payables: the concession fee is due every other month. Specifically, it is not due in December while it is paid in March;

- bet seasonality and evolution of the associated PREU payables: December’s bet is the highest of the year (thus driving the accumulation of high PREU related payables). In parallel December PREU related payments are relatively low since they refer to prior months’ bet with “normal” seasonality. This positive effect gets reversed in first quarter;

- the accumulation of one quarter worth of 0.5% ADM deposit (normally liquidated in second quarter of each year).

Year on year change in cash flows from operating activities is primarily associated to the evolution in betting payout which has been commented earlier in this document.

Cash flows used in investing activities amounted to Euro 10.8 million for the three months ended March 31, 2017 compared to Euro 4.0 million for the three months ended March 31, 2016. The year on year increase in cash flows used in investing activities refers primarily to increased growth capex (driven by higher investments in company owned AWPs) as well as to increased acquisitions costs (both new acquisitions as well as payments of deferred price components associated to acquisitions finalized in 2016).

The increase in cash used in investing activities is mainly attributable to an increase in net investments in tangible assets from Euro 2.6 million for the three months ended March 31, 2016 to Euro 5.7 million for the three months ended March 31, 2017. The increase in investments in tangible assets is mainly attributable to purchase and replacement of AWP devices (increased by Euro 1.1 million) and AWP mother boards (increased by Euro 0.8 million). The increase in cash used in investing activities is also attributable to investments in intangible assets from Euro 0.4 million for the three months ended March 31, 2016 to Euro 1.6 million for the three months ended March 31, 2017 mainly relating to investments in gaming software for online and virtual games (Euro 0.6 million).

Cash flows used in financing activities amounted to Euro 1.4 million for the three months ended March 31, 2017 compared to Euro 7.9 million for the three months ended March 31, 2016. The year on year change is mostly due to the fact that Euro 5.0 million worth of short term credit lines were drawn in first quarter 2017, as well as by lower interest expenses paid on the Euro 200 million bond (interest rate is now set at 6.0% compared to 7.25% on the Euro 200 million bond issued in 2013 and repaid in August 2016).

MANAGEMENT’S REPORT ON THE GROUP’S RESULT AT

MARCH 31, 2017

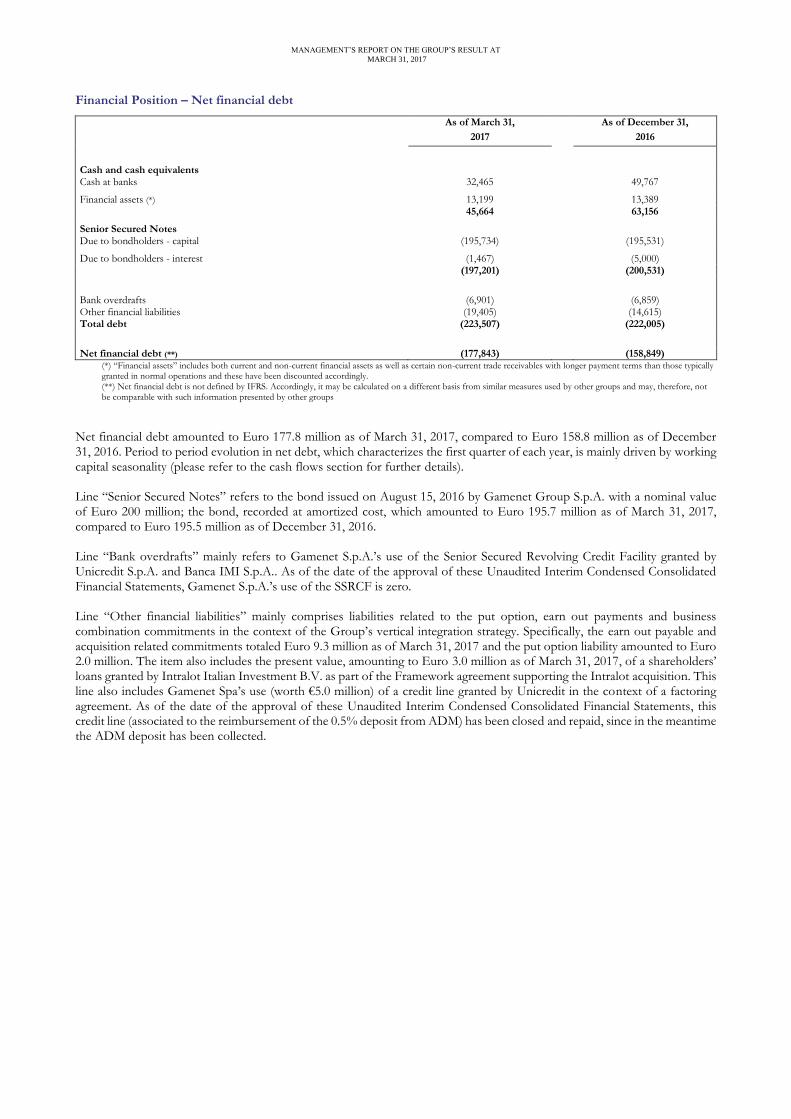

Financial Position – Net financial debt

As of March 31, As of December 31,

2017 2016

Cash and cash equivalents Cash at banks 32,465 49,767

Financial assets (*) 13,199 13,389 45,664 63,156

Senior Secured Notes Due to bondholders - capital (195,734) (195,531)

Due to bondholders - interest (1,467) (5,000) (197,201) (200,531)

Bank overdrafts (6,901) (6,859) Other financial liabilities (19,405) (14,615) Total debt (223,507) (222,005)

Net financial debt (**) (177,843) (158,849)

(*) “Financial assets” includes both current and non-current financial assets as well as certain non-current trade receivables with longer payment terms than those typically granted in normal operations and these have been discounted accordingly. (**) Net financial debt is not defined by IFRS. Accordingly, it may be calculated on a different basis from similar measures used by other groups and may, therefore, not be comparable with such information presented by other groups

Net financial debt amounted to Euro 177.8 million as of March 31, 2017, compared to Euro 158.8 million as of December 31, 2016. Period to period evolution in net debt, which characterizes the first quarter of each year, is mainly driven by working capital seasonality (please refer to the cash flows section for further details). Line “Senior Secured Notes” refers to the bond issued on August 15, 2016 by Gamenet Group S.p.A. with a nominal value of Euro 200 million; the bond, recorded at amortized cost, which amounted to Euro 195.7 million as of March 31, 2017, compared to Euro 195.5 million as of December 31, 2016. Line “Bank overdrafts” mainly refers to Gamenet S.p.A.’s use of the Senior Secured Revolving Credit Facility granted by Unicredit S.p.A. and Banca IMI S.p.A.. As of the date of the approval of these Unaudited Interim Condensed Consolidated Financial Statements, Gamenet S.p.A.’s use of the SSRCF is zero. Line “Other financial liabilities” mainly comprises liabilities related to the put option, earn out payments and business combination commitments in the context of the Group’s vertical integration strategy. Specifically, the earn out payable and acquisition related commitments totaled Euro 9.3 million as of March 31, 2017 and the put option liability amounted to Euro 2.0 million. The item also includes the present value, amounting to Euro 3.0 million as of March 31, 2017, of a shareholders’ loans granted by Intralot Italian Investment B.V. as part of the Framework agreement supporting the Intralot acquisition. This line also includes Gamenet Spa’s use (worth €5.0 million) of a credit line granted by Unicredit in the context of a factoring agreement. As of the date of the approval of these Unaudited Interim Condensed Consolidated Financial Statements, this credit line (associated to the reimbursement of the 0.5% deposit from ADM) has been closed and repaid, since in the meantime the ADM deposit has been collected.

1

Unaudited Interim Condensed Consolidated Financial Statements

as of March 31, 2017 and for the three months ended March 31,

2017 and 2016

2

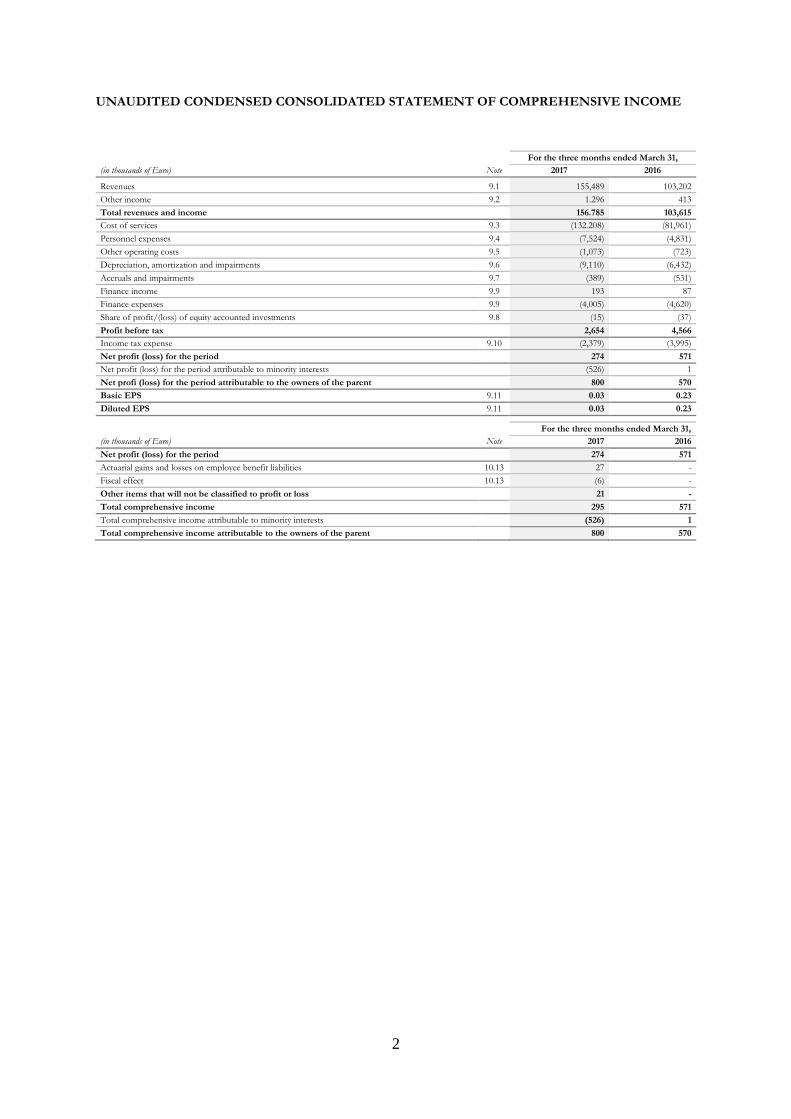

UNAUDITED CONDENSED CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME

For the three months ended March 31,

(in thousands of Euro) Note 2017 2016

Revenues 9.1 155,489 103,202

Other income 9.2 1.296 413

Total revenues and income 156.785 103,615

Cost of services 9.3 (132.208) (81,961)

Personnel expenses 9.4 (7,524) (4,831)

Other operating costs 9.5 (1,073) (723)

Depreciation, amortization and impairments 9.6 (9,110) (6,432)

Accruals and impairments 9.7 (389) (531)

Finance income 9.9 193 87

Finance expenses 9.9 (4,005) (4,620)

Share of profit/(loss) of equity accounted investments 9.8 (15) (37)

Profit before tax 2,654 4,566

Income tax expense 9.10 (2,379) (3,995)

Net profit (loss) for the period 274 571

Net profit (loss) for the period attributable to minority interests (526) 1

Net profi (loss) for the period attributable to the owners of the parent 800 570

Basic EPS 9.11 0.03 0.23

Diluted EPS 9.11 0.03 0.23

For the three months ended March 31,

(in thousands of Euro) Note 2017 2016

Net profit (loss) for the period 274 571

Actuarial gains and losses on employee benefit liabilities 10.13 27 -

Fiscal effect 10.13 (6) -

Other items that will not be classified to profit or loss 21 -

Total comprehensive income 295 571

Total comprehensive income attributable to minority interests (526) 1

Total comprehensive income attributable to the owners of the parent 800 570

3

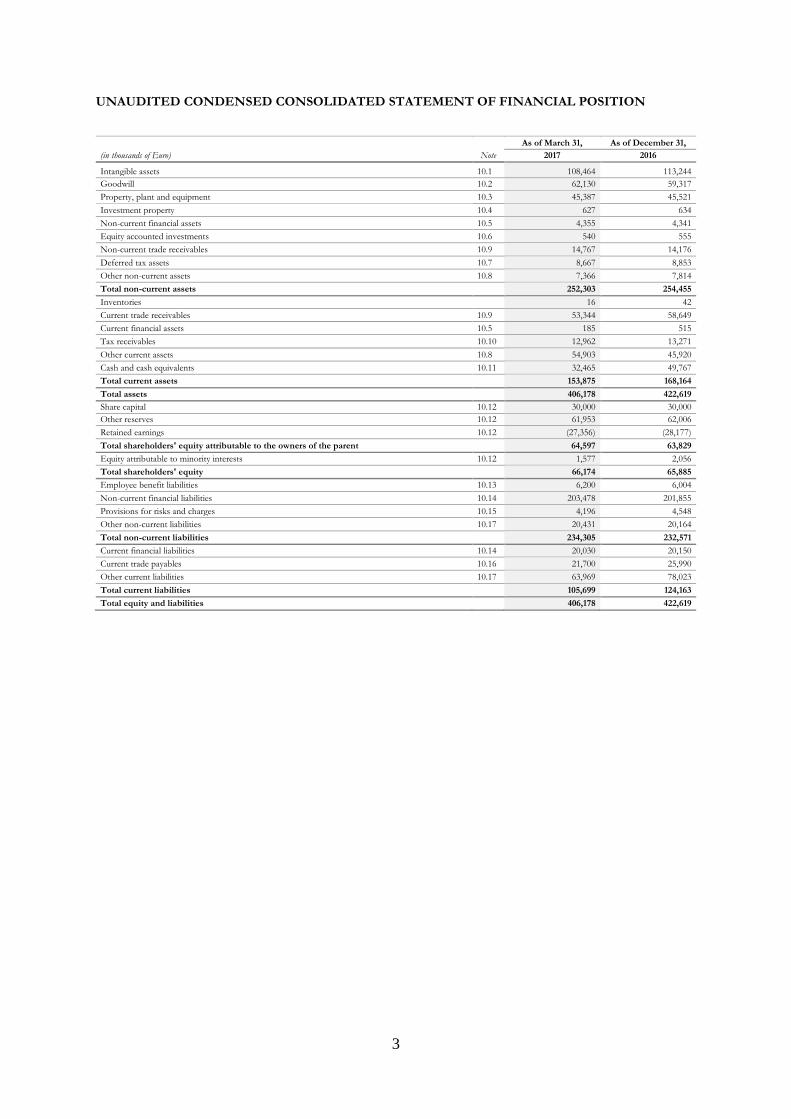

UNAUDITED CONDENSED CONSOLIDATED STATEMENT OF FINANCIAL POSITION

As of March 31, As of December 31,

(in thousands of Euro) Note 2017 2016

Intangible assets 10.1 108,464 113,244

Goodwill 10.2 62,130 59,317

Property, plant and equipment 10.3 45,387 45,521

Investment property 10.4 627 634

Non-current financial assets 10.5 4,355 4,341

Equity accounted investments 10.6 540 555

Non-current trade receivables 10.9 14,767 14,176

Deferred tax assets 10.7 8,667 8,853

Other non-current assets 10.8 7,366 7,814

Total non-current assets 252,303 254,455

Inventories 16 42

Current trade receivables 10.9 53,344 58,649

Current financial assets 10.5 185 515

Tax receivables 10.10 12,962 13,271

Other current assets 10.8 54,903 45,920

Cash and cash equivalents 10.11 32,465 49,767

Total current assets 153,875 168,164

Total assets 406,178 422,619

Share capital 10.12 30,000 30,000

Other reserves 10.12 61,953 62,006

Retained earnings 10.12 (27,356) (28,177)

Total shareholders' equity attributable to the owners of the parent 64,597 63,829

Equity attributable to minority interests 10.12 1,577 2,056

Total shareholders' equity 66,174 65,885

Employee benefit liabilities 10.13 6,200 6,004

Non-current financial liabilities 10.14 203,478 201,855

Provisions for risks and charges 10.15 4,196 4,548

Other non-current liabilities 10.17 20,431 20,164

Total non-current liabilities 234,305 232,571

Current financial liabilities 10.14 20,030 20,150

Current trade payables 10.16 21,700 25,990

Other current liabilities 10.17 63,969 78,023

Total current liabilities 105,699 124,163

Total equity and liabilities 406,178 422,619

4

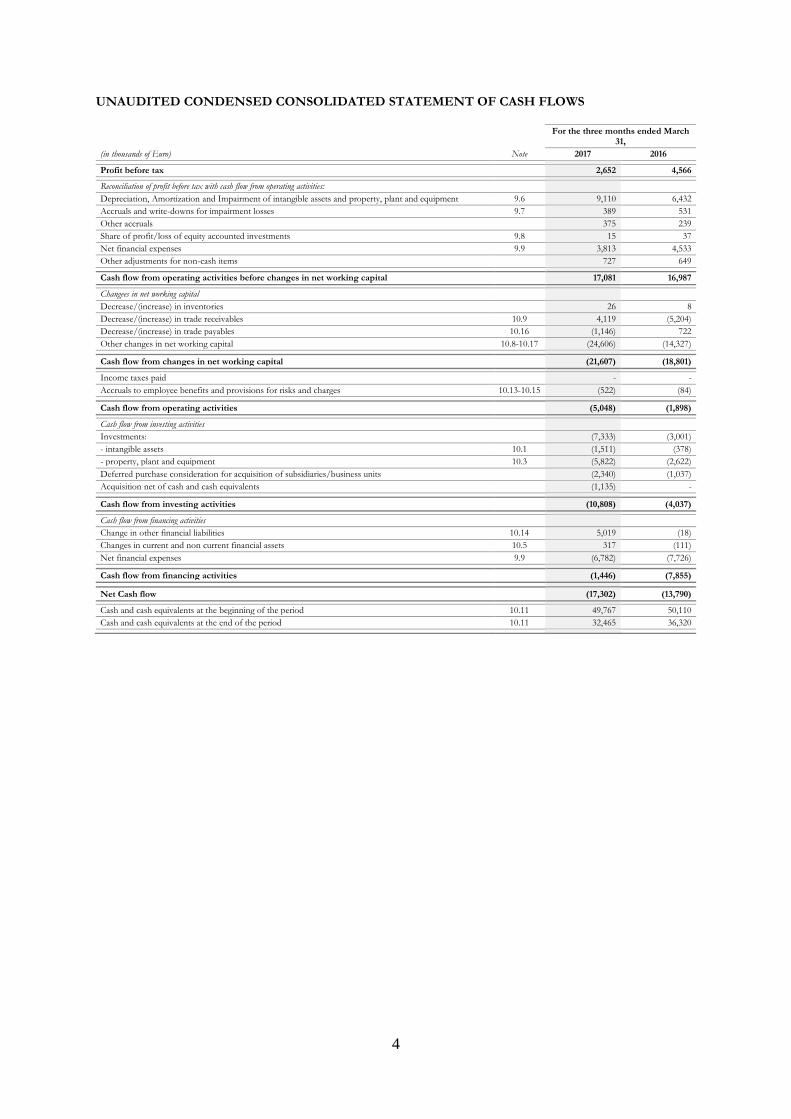

UNAUDITED CONDENSED CONSOLIDATED STATEMENT OF CASH FLOWS

For the three months ended March 31,

(in thousands of Euro) Note 2017 2016

Profit before tax 2,652 4,566

Reconciliation of profit before tax with cash flow from operating activities: Depreciation, Amortization and Impairment of intangible assets and property, plant and equipment 9.6 9,110 6,432

Accruals and write-downs for impairment losses 9.7 389 531

Other accruals 375 239

Share of profit/loss of equity accounted investments 9.8 15 37

Net financial expenses 9.9 3,813 4,533

Other adjustments for non-cash items 727 649

Cash flow from operating activities before changes in net working capital 17,081 16,987

Changees in net working capital Decrease/(increase) in inventories 26 8

Decrease/(increase) in trade receivables 10.9 4,119 (5,204)

Decrease/(increase) in trade payables 10.16 (1,146) 722

Other changes in net working capital 10.8-10.17 (24,606) (14,327)

Cash flow from changes in net working capital (21,607) (18,801)

Income taxes paid - -

Accruals to employee benefits and provisions for risks and charges 10.13-10.15 (522) (84)

Cash flow from operating activities (5,048) (1,898)

Cash flow from investing activities Investments: (7,333) (3,001)

- intangible assets 10.1 (1,511) (378)

- property, plant and equipment 10.3 (5,822) (2,622)

Deferred purchase consideration for acquisition of subsidiaries/business units (2,340) (1,037)

Acquisition net of cash and cash equivalents (1,135) -

Cash flow from investing activities (10,808) (4,037)

Cash flow from financing activities Change in other financial liabilities 10.14 5,019 (18)

Changes in current and non current financial assets 10.5 317 (111)

Net financial expenses 9.9 (6,782) (7,726)

Cash flow from financing activities (1,446) (7,855)

Net Cash flow (17,302) (13,790)

Cash and cash equivalents at the beginning of the period 10.11 49,767 50,110

Cash and cash equivalents at the end of the period 10.11 32,465 36,320

5

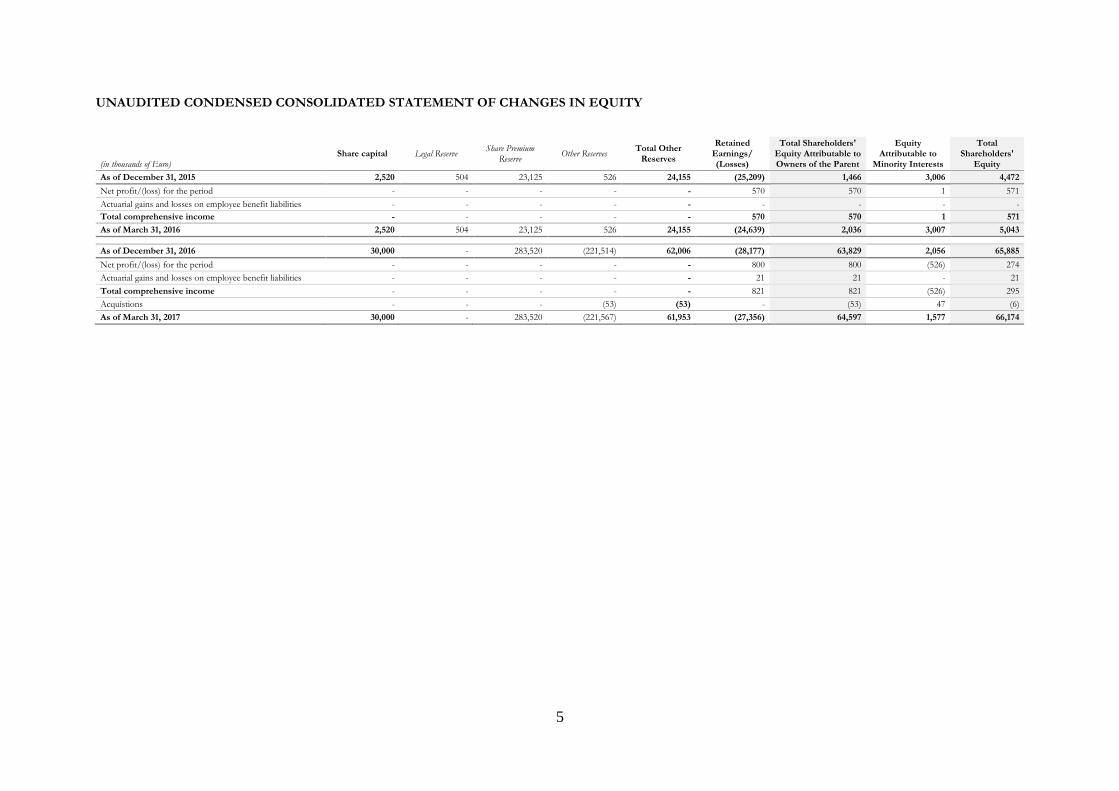

UNAUDITED CONDENSED CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

(in thousands of Euro) Share capital Legal Reserve

Share Premium Reserve

Other Reserves Total Other

Reserves

Retained Earnings/ (Losses)

Total Shareholders' Equity Attributable to Owners of the Parent

Equity Attributable to

Minority Interests

Total Shareholders'

Equity

As of December 31, 2015 2,520 504 23,125 526 24,155 (25,209) 1,466 3,006 4,472

Net profit/(loss) for the period - - - - - 570 570 1 571

Actuarial gains and losses on employee benefit liabilities - - - - - - - - -

Total comprehensive income - - - - - 570 570 1 571

As of March 31, 2016 2,520 504 23,125 526 24,155 (24,639) 2,036 3,007 5,043

As of December 31, 2016 30,000 - 283,520 (221,514) 62,006 (28,177) 63,829 2,056 65,885

Net profit/(loss) for the period - - - - - 800 800 (526) 274

Actuarial gains and losses on employee benefit liabilities - - - - - 21 21 - 21

Total comprehensive income - - - - - 821 821 (526) 295

Acquistions - - - (53) (53) - (53) 47 (6)

As of March 31, 2017 30,000 - 283,520 (221,567) 61,953 (27,356) 64,597 1,577 66,174

6

NOTES TO THE INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 1. GENERAL INFORMATION

Gamenet Group S.p.A. (hereafter ‘‘Gamenet Group’’, the ‘‘Company’’ or the ‘‘Parent’’ and together with its subsidiaries and associates the ‘‘Group’’ or “Gamenet Group”) is a company incorporated and domiciled in Italy, with registered offices in Rome, Corso d’Italia 6, organized under the laws of the Republic of Italy. The Company was incorporated on June 21, 2016 to effect the acquisition (hereafter the ‘‘Acquisition”) on June 27, 2016 of Intralot Holding & Services S.p.A. (hereafter ‘‘Intralot”) by Gamenet S.p.A. (hereafter ‘‘Gamenet”). The Company is controlled by TCP Lux Euroinvest S.à.r.l. (hereafter ‘‘TCP”), which holds 79.1% of the share capital; the remaining share capital is held 20% by the Dutch company Intralot Italian Investments B.V. (hereafter “Intralot B.V.”) and 0.9% by Stefano Francolini. Gamenet Group is one of the largest operators in the Italian public gaming sector, which is regulated by the Customs and Monopolies Agency (Agenzia delle Dogane e dei Monopoli hereafter “ADM”). The Group is an active gaming concessionaire and has a product offering ranging from AWP (Amusement With Prizes) and VLT (Video Lottery Terminals), to management of its nationwide network of variously branded company owned points of sales, betting and online as well as service providing to business partners. 2. BASIS OF PREPARATION AND PRINCIPLES OF CONSOLIDATION

2.1 Basis of preparation

These unaudited interim condensed consolidated financial statements as of March 31, 2017 and for the three months ended March 31, 2017 and 2016 (hereafter the “Unaudited Interim Condensed Consolidated Financial Statements”) have been prepared following IAS 34, “Interim financial reporting” which governs interim financial reporting. IAS 34 permits a significantly lower amount of information to be included in interim financial statements from what is required for annual financial statements by International Financial Reporting Standards issued by the International Accounting Standards Board and approved by the European Union (hereafter “EU-IFRS”), given that the entity has prepared its financial statements compliant with EU-IFRS for the previous financial year. The Unaudited Interim Condensed Consolidated Financial Statements should be read in conjunction with the annual consolidated financial statements of the Group for the year ended December 31, 2016.

* * * The Unaudited Interim Condensed Consolidated Financial Statements were approved by the Company’s board of directors on May 29, 2017. This Unaudited Interim Condensed Consolidated Financial Statements was not audited by the statutory independent auditors. 2.2 Format and content of the financial statements

The Unaudited Interim Condensed Consolidated Financial Statements are presented in Euro, currency in which Group companies operate. Unless otherwise specified, all amounts in this document are expressed in thousands of Euro (Euro ‘000). The formats of the consolidated financial statements and related classification criteria adopted by the Group (among the options available under IAS 1—Presentation of financial statements) are as follows:

• the consolidated statement of financial position, which classifies assets and liabilities based on whether they are current/non-current;

• the consolidated statement of comprehensive income, which classifies costs and revenues according to their nature and sets out the profit or loss for the year, together with other amounts that, in accordance with EU-IFRS, are recognized directly in equity separately from those relating to operations with the Company’s shareholders;

• the consolidated statement of cash flows, which is prepared using the indirect method. The formats used are those considered to provide the best representation of the Group’s results and financial position. 2.3 Scope of consolidation

The Unaudited Interim Condensed Consolidated Financial Statements include the financial statements of the Company and its subsidiaries and are prepared based on the accounting records of the individual companies, adjusted as necessary to align them with the accounting principles applied by the Group.

7

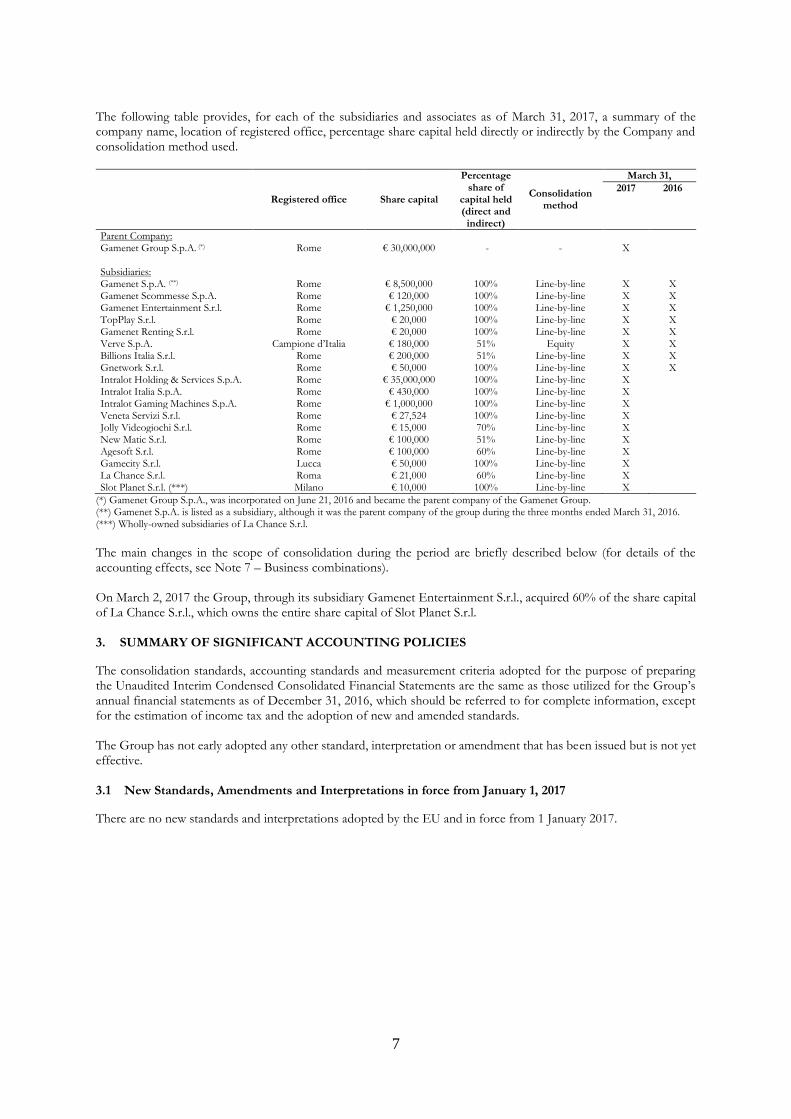

The following table provides, for each of the subsidiaries and associates as of March 31, 2017, a summary of the company name, location of registered office, percentage share capital held directly or indirectly by the Company and consolidation method used.

Registered office Share capital

Percentage share of

capital held (direct and indirect)

Consolidation method

March 31,

2017 2016

Parent Company: Gamenet Group S.p.A. (*) Rome € 30,000,000 - - X

Subsidiaries: Gamenet S.p.A. (**) Rome € 8,500,000 100% Line-by-line X X Gamenet Scommesse S.p.A. Rome € 120,000 100% Line-by-line X X Gamenet Entertainment S.r.l. Rome € 1,250,000 100% Line-by-line X X TopPlay S.r.l. Rome € 20,000 100% Line-by-line X X Gamenet Renting S.r.l. Rome € 20,000 100% Line-by-line X X Verve S.p.A. Campione d’Italia € 180,000 51% Equity X X Billions Italia S.r.l. Rome € 200,000 51% Line-by-line X X Gnetwork S.r.l. Rome € 50,000 100% Line-by-line X X Intralot Holding & Services S.p.A. Rome € 35,000,000 100% Line-by-line X Intralot Italia S.p.A. Rome € 430,000 100% Line-by-line X Intralot Gaming Machines S.p.A. Rome € 1,000,000 100% Line-by-line X Veneta Servizi S.r.l. Rome € 27,524 100% Line-by-line X Jolly Videogiochi S.r.l. Rome € 15,000 70% Line-by-line X New Matic S.r.l. Rome € 100,000 51% Line-by-line X Agesoft S.r.l. Rome € 100,000 60% Line-by-line X Gamecity S.r.l. Lucca € 50,000 100% Line-by-line X La Chance S.r.l. Roma € 21,000 60% Line-by-line X Slot Planet S.r.l. (***) Milano € 10,000 100% Line-by-line X

(*) Gamenet Group S.p.A., was incorporated on June 21, 2016 and became the parent company of the Gamenet Group. (**) Gamenet S.p.A. is listed as a subsidiary, although it was the parent company of the group during the three months ended March 31, 2016. (***) Wholly-owned subsidiaries of La Chance S.r.l.

The main changes in the scope of consolidation during the period are briefly described below (for details of the accounting effects, see Note 7 – Business combinations). On March 2, 2017 the Group, through its subsidiary Gamenet Entertainment S.r.l., acquired 60% of the share capital of La Chance S.r.l., which owns the entire share capital of Slot Planet S.r.l.

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The consolidation standards, accounting standards and measurement criteria adopted for the purpose of preparing the Unaudited Interim Condensed Consolidated Financial Statements are the same as those utilized for the Group’s annual financial statements as of December 31, 2016, which should be referred to for complete information, except for the estimation of income tax and the adoption of new and amended standards. The Group has not early adopted any other standard, interpretation or amendment that has been issued but is not yet effective. 3.1 New Standards, Amendments and Interpretations in force from January 1, 2017

There are no new standards and interpretations adopted by the EU and in force from 1 January 2017.

8

3.2 New Standards and Interpretations not yet applicable for which the Group did not choose early adoption

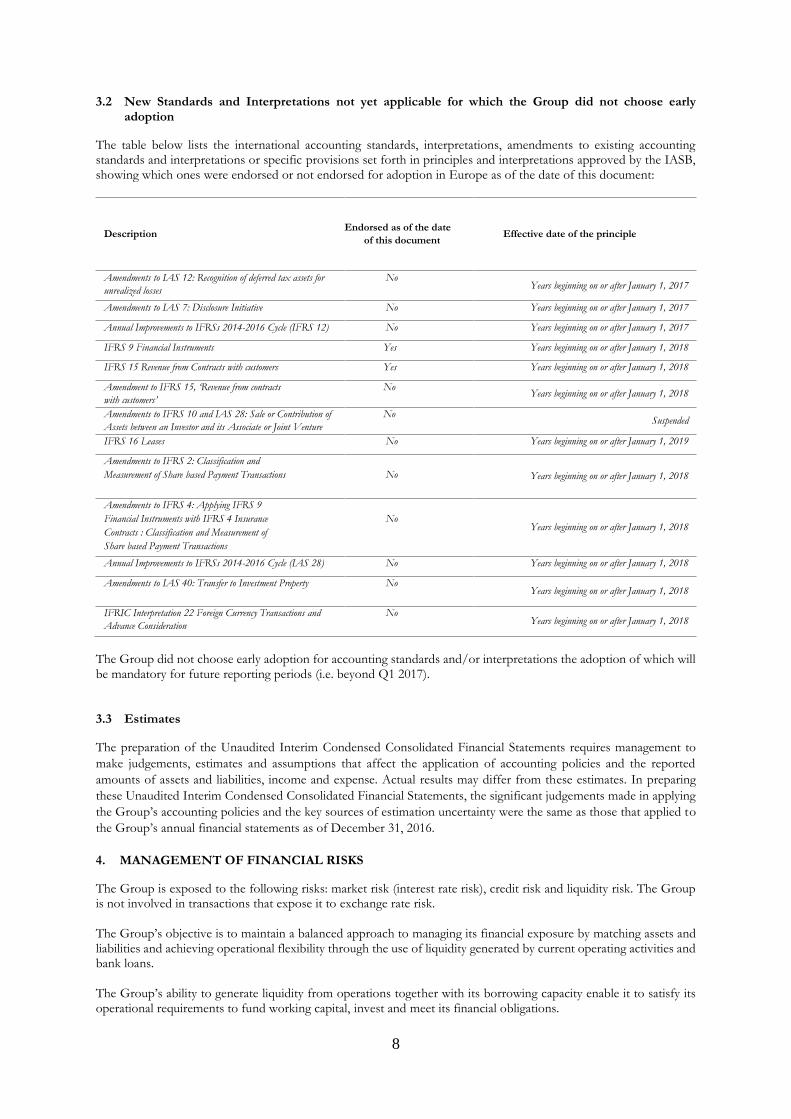

The table below lists the international accounting standards, interpretations, amendments to existing accounting standards and interpretations or specific provisions set forth in principles and interpretations approved by the IASB, showing which ones were endorsed or not endorsed for adoption in Europe as of the date of this document:

Description Endorsed as of the date

of this document Effective date of the principle

Amendments to IAS 12: Recognition of deferred tax assets for

unrealized losses

No Years beginning on or after January 1, 2017

Amendments to IAS 7: Disclosure Initiative No Years beginning on or after January 1, 2017

Annual Improvements to IFRSs 2014-2016 Cycle (IFRS 12) No Years beginning on or after January 1, 2017

IFRS 9 Financial Instruments Yes Years beginning on or after January 1, 2018

IFRS 15 Revenue from Contracts with customers Yes Years beginning on or after January 1, 2018

Amendment to IFRS 15, ‘Revenue from contracts

with customers’

No Years beginning on or after January 1, 2018

Amendments to IFRS 10 and IAS 28: Sale or Contribution of

Assets between an Investor and its Associate or Joint Venture

No Suspended

IFRS 16 Leases No Years beginning on or after January 1, 2019

Amendments to IFRS 2: Classification and

Measurement of Share based Payment Transactions

No Years beginning on or after January 1, 2018

Amendments to IFRS 4: Applying IFRS 9

Financial Instruments with IFRS 4 Insurance

Contracts : Classification and Measurement of

Share based Payment Transactions

No Years beginning on or after January 1, 2018

Annual Improvements to IFRSs 2014-2016 Cycle (IAS 28) No Years beginning on or after January 1, 2018

Amendments to IAS 40: Transfer to Investment Property No Years beginning on or after January 1, 2018

IFRIC Interpretation 22 Foreign Currency Transactions and

Advance Consideration

No Years beginning on or after January 1, 2018

The Group did not choose early adoption for accounting standards and/or interpretations the adoption of which will be mandatory for future reporting periods (i.e. beyond Q1 2017). 3.3 Estimates

The preparation of the Unaudited Interim Condensed Consolidated Financial Statements requires management to

make judgements, estimates and assumptions that affect the application of accounting policies and the reported

amounts of assets and liabilities, income and expense. Actual results may differ from these estimates. In preparing

these Unaudited Interim Condensed Consolidated Financial Statements, the significant judgements made in applying

the Group’s accounting policies and the key sources of estimation uncertainty were the same as those that applied to

the Group’s annual financial statements as of December 31, 2016.

4. MANAGEMENT OF FINANCIAL RISKS

The Group is exposed to the following risks: market risk (interest rate risk), credit risk and liquidity risk. The Group is not involved in transactions that expose it to exchange rate risk. The Group’s objective is to maintain a balanced approach to managing its financial exposure by matching assets and liabilities and achieving operational flexibility through the use of liquidity generated by current operating activities and bank loans. The Group’s ability to generate liquidity from operations together with its borrowing capacity enable it to satisfy its operational requirements to fund working capital, invest and meet its financial obligations.

9

Treasury and financial risk management are centralized within the Group. Specifically, the central finance function is responsible for evaluating and approving forecasted financial requirements, monitoring trends and taking corrective action as necessary. 4.1 Market risk

Interest rate risk While the effect of interest rate changes on the variable component of financial payables and liquidity may result in higher/lower finance income/charges, it is noted that the Group has limited exposure to interest rate risk as the main part of its financial debt, represented by the bond, is at fixed rate. 4.2 Credit risk

Credit risk represents the Group’s exposure to the risk of potential losses resulting from the non-fulfillment of obligations by counterparts. Collecting receivables deriving from betting and or AWP/VLT operations may generate credit risk for the Group, whose revenues are generated by the concessions granted by the Customs and Monopolies Agency (ADM), as the failure of, or losses incurred by, one or more members of the distribution network or the interruption of relations with any of them for whatever reason can have a negative impact on the Group’s results, business activities, financial conditions and future prospects. Trade receivables are recognized net of provisions, calculated on the basis of the risk of non-fulfillment of obligations by counterparts, in turn based on information available regarding the counterparty’s solvency and historical data. Provisions are made against individually significant receivables for which an objective risk of partial or total non-collection is identified.

4.3 Liquidity risk

Liquidity risk is the risk that, owing to an inability to access new funds or sell assets, the Group is unable to meet its payment obligations, leading to a negative impact on results if it is then obliged to incur additional costs to meet its obligations or deal with insolvency. The Group manages this risk by seeking to establish a financial structure that, consistent with its business objectives and defined limits, ensures sufficient liquidity, while minimizing the related opportunity cost, and maintains an appropriate balance in terms of duration and composition of debt. The Group’s exposure to liquidity risk relates mainly to obligations arising in relation to the refinancing operation undertaken in August 2016 through the issuance of a bond and use of a revolving loan facility. 4.4 Determination of fair value

Financial instruments carried at fair value are reported by valuation method. The different valuation levels are defined as follows:

- Quoted prices (unadjusted) in active markets for identical assets or liabilities (Level 1). - Inputs other than quoted prices included within level 1 that are observable for the asset or liability, either

directly (that is, as prices) or indirectly (that is, derived from prices) (Level 2). - Inputs for the asset or liability that are not based on observable market data (that is, unobservable inputs)

(Level 3). Both at March 31, 2017 and December 31 2016 the Group reported no outstanding assets and liabilities measured at fair value. 5. CAPITAL MANAGEMENT

The Group’s capital management is aimed at guaranteeing solid credit ratings and adequate capital indicators to support its investment plans, while meeting contractual obligations with lenders.

10

The Group ensures it has sufficient capital to finance its business development needs and meet operating requirements; to guarantee a balanced financial structure and minimize the total cost of capital, finances are sourced through a mix of risk capital and debt to the benefit of all stakeholders. Regarding certain financial liabilities, the Group is subject to certain restrictions (for further details see “Note 10.14 Current and non-current financial liabilities”). Returns on capital are monitored by reviewing market trends and business performance, net of other commitments, including borrowing costs. In order to ensure the Group’s going concern status, to develop the business and to provide an adequate return on capital, Management monitors the Group’s debt to equity ratio, on an ongoing basis, also in comparison with business trend and expected future cash flows in the medium/long term. 6. OPERATING SEGMENTS

The following disclosure regarding operating segments is provided in accordance with IFRS 8 "Operating segments” (hereafter “IFRS 8”), which requires that such disclosure reflects the manner in which management manages the business and makes operational decisions. Accordingly, the operating segments and related disclosures are based on internal reporting used by management to make decisions about resources to be allocated to the various operating segments and assess performance. IFRS 8 defines an operating segment as a component of an entity that: i) engages in business activities from which it may earn revenues and incur expenses (including revenues and expenses relating to transactions with other components of the same entity); ii) whose operating results are regularly reviewed by the entity’s chief operating decision maker to make decisions about resources to be allocated to the segment and assess its performance; and iii) for which discrete financial information is available. The Group organizes and manages its business activities in terms of the following operating segments: (i) video lottery terminal (“VLT”); (ii) amusement with prize (“AWP”); (iii) “Betting and online”; and (iv) direct ownership of VLT gaming halls and direct AWP operations (Retail & Street Operations). Operating segments are monitored based on: i) revenues and other income; ii) first level margin; and iii) contribution margin. First level margin is defined as revenues and other income net of distribution and platform costs, concession fees and other costs. Contribution margin is defined as first level margin, net of other distribution and platform costs and other direct costs. Management believes that the aforementioned indicators provide a good indication of the performance of the four

operating segments.

The following table provides details of Group operating segments for the periods indicated:

11

(in thousand of Euro, except percentages) VLT AWP Betting and Online Retail and Street operations Unallocated/Elimination Total

Q1 2017

Q1 2016 Q1 2017

Q1 2016 Q1 2017

Q1 2016 Q1 2017

Q1 2016 Q1 2017

Q1 2016 Q1 2017

Q1

2016

Revenues 55,649 53,481 78,711 43,595 15,297 2,783 9,196 5,497 (3,364) (2,155) 155,489 103,201

Other income 324 16 158 211 21 111 201 187 592 (112) 1,296 413

Total revenues and income 55,973 53,497 78,869 43,806 15,318 2,894 9,397 5,684 (2,771) (2,267) 156,786 103,615

-

Third parties distribution costs (33,116) (30,819) (70,499) (37,337) (10,304) (1,024) (258) (294) 2,898 1,624 (111,279) (67,850)

Taxes-concession fee- other (2,434) (2,353) (1,964) (1,722) (1,650) (290) - 9 (6,048) (4,357)

First Level margin 20,423 20,325 6,406

4,747 3,364 1,580 9,139

5,390 201 (634) 39,459

31,409

Other distribution and platform costs (3,220) (2,811) - (742) (344) - 35 - (3,927) (3,155)

Other direct costs (438) (961) (697) (890) (619) (218) (2,243) (2,016) (212) - (4,209) (4,085)

Contribution margin 16,765 16,553 5,709

3,857 2,003 1,018 6,896

3,374 24 (634) 31,323

24,169

Contribution margin/bet 2.1% 2.1% 0.9% 0.7% 1.0% n.a. 5.9% 3.4% n.a. n.a. 1.8% 1.6%

Contribution margin/total revenues and income 30.0% 30.9% 7.2% 8.8% 13.1% 35.2% 73.4% 59.4% -0.9% 28.0% 20.0% 23.3%

Indirect costs - - - - (15,733) (8,600) (15,733) (8,600)

Depreciation, amortization and impairments - - - - (9,110) (6,432) (9,110) (6,432)

Finance income - - - - - 193 87

Finance expenses - - - - - (4,005) (4,620)

Costs related to valuation of investments - - - - - (15) (37)

Impairment of financial assets - - - - - - -

Profit before tax - - - - - 2,654 4,567

Income tax - - - - - (2,379) (3,995)

Profit for the period - - - - - 274 571

12

Given the range of services and products sold by the Group, there are no significant concentrations of revenues with individual customers. The Group currently operates solely in Italy. Finally, in terms of the balance sheet, management does not monitor assets by segment. 7. BUSINESS COMBINATIONS

The business combinations that took place during the three months ended March 31, 2017 had the effect of extending the scope of the Group consolidation. All of the acquisitions (described below) were made in the context of the Group’s vertical integration strategy. 7.1 Acquisition of La Chance S.r.l. and Slot Planet S.r.l.

On March 2, 2017, Gamenet Entertainment S.r.l. signed a framework agreement for the purchase of 60% of the share capital of La Chanche S.r.l., which is active in the public gaming sector both directly, through its management of a gaming hall (with 15 AWPs and 33 VLTs) , and indirectly through its ownership of the entire share capital of Slot Planet, which manages a gaming hall (with 34 AWPs and 22 VLTs) . Costs relating to the transaction were fully recognized in the income statement in the year to which they related. Cash flows relating to the consideration paid for the three months ended March 31, 2017 amounted to Euro 885 thousand. 7.2 Acquisition of businesses concerns

In the first quarter of 2017, Gamenet S.p.A. acquired an AWP related business concern. The fair values of assets acquired and liabilities assumed were determined in accordance with the provisions of IFRS 3 and the excess of the consideration paid with respect to the fair value of the net assets acquired, amounting to Euro 913 thousand, was recognized as goodwill. Costs relating to the transaction were fully recognized in the income statement in the year to which they related. Cash flows relating to the consideration paid for the three months ended March 31, 2017 amounted to Euro 250 thousand. Please note that the purchase agreement did not provide for an earn-out payment or other conditions or limitations which may have future adverse effects. 8. SEASONALITY

With respect to seasonality, the Group’s business is not subject to significant fluctuations, although it should be considered that the number of sports events, in particular football matches, for which bets are accepted, is higher in the first and fourth quarters than in other quarters of the year. As far as AWP / VLT bet is concerned, fourth quarter’s bet is higher than in any other quarters.

9. NOTES TO THE UNAUDITED INTERIM CONDENSED CONSOLIDATED STATEMENT OF

COMPREHENSIVE INCOME

9.1 Revenues

The following table provides a breakdown of “Revenues”:

For the three months ended March 31,

(in thousands of Euro) 2017 2016

VLT 55.649 53,481

AWP 78.711 43,595

Betting and Online 15.297 2,783

Retails and Street Operations 9.196 5,497

Not allocated/eliminations (3.364) (2,155)

Total 155,489 103,201

13

9.2 Other income

“Other income” amounted to Euro 1,296 thousand and Euro 413 thousand for the three months ended March 31, 2017 and 2016 respectively and related for the main part to compensation and reimbursement for damages, gains on the disposal of property plant and equipment and other transactions income. 9.3 Cost of services

The following table provides a breakdown of “Cost of services”:

For the three months ended March 31,

(in thousands of Euro) 2017 2016

Distribution network compensation (112,414) (68,697)

Concession Fee (5,911) (4,220)

Fee on VLT platform licenses (3,184) (2,752)

Leases and rentals (2,282) (1,619)

Technical assistance and network management (2,084) (1,169)

Marketing and advertising (1,504) (549)

Utility costs, postal and logistics costs, security services (1,713) (996)

Board of Directors remunerations and costs (141) (111)

Tax, administrative and legal consultancy costs (721) (316)

Bank and insurance expenses (400) (142)

Data transmission (382) (569)

Costs of providers and live bettings (63) (213)

Other (1,409) (608)

Total (132,208) (81,961)

9.4 Personnel expenses

The following table provides a breakdown of “Personnel expenses”:

For the three months ended March 31,

(in thousands of Euro) 2017 2016

Remuneration (4,945) (3,475)

Social security contributions (1,479) (1,108)

Employees' termination pay (375) (239)

Other personnel costs (725) (9)

Total (7,524) (4,831)

9.5 Other operating costs

The following table provides a breakdown of “Other operating costs”:

For the three months ended March 31,

(in thousands of Euro) 2017 2016

Purchase of goods and other purchases (448) (452)

Fines, penalties and losses on receivables (259) (53)

Taxes and sundry duties (116) (170)

Entertainment expenses (53) (33)

Other expenses (197) (15)

Total (1,073) (723)

9.6 Depreciation, amortization and impairments

The following table provides a breakdown of “Depreciation, amortization and impairments”:

For the three months ended March 31,

(in thousands of Euro) 2017 2016

Amortization of intangible assets (5,334) (4,278)

Depreciation of property, plant and equipment (3,721) (1,855)

Depreciation of investment property (7) (7)

Impairments of property, plant and equipment and intangible assets (48) (292)

Total (9,110) (6,432)

14

9.7 Accruals and impairments

The following table provides a breakdown of “Accruals and impairments”:

For the three months ended March 31,

(in thousands of Euro) 2017 2016

Allowance for doubtful receivables (723) (514)

Provision for write-downs of AAMS' guarantee deposits (10) (17)

Provision for technological innovation 344 -

Total (389) (531)

Provisions are stated net of releases. 9.8 Share of profit of equity accounted investments

The following table provides a breakdown of “Share of profit of equity accounted investments”:

For the three months ended March 31,

(in thousands of Euro) 2017 2016

Loss related to equity method valuation (Verve) (15) (37)

Total (15) (37)

9.9 Finance income and expenses (net)

The following table provides a breakdown of Finance income and expenses (net):

For the three months ended March 31,

(in thousands of Euro) 2017 2016

Interest income related to distribution network 33 69

Interest income on bank current accounts 2 1

Other interest income 158 17

Total 193 87

Interest expense on bonds (3,000) (3,655)

Amortized cost on bond (206) (400)

Commission on sureties (561) (353)

Other interest expense (238) (212)

Total (4,005) (4,620)

Financial income and expenses, net (3,812) (4,533)

9.10 Income tax expense

The following table provides a breakdown of “Income tax expense”:

For the three months ended March 31,

(in thousands of Euro) 2017 2016

Current taxes (2,199) (1,120)

Deferred taxes (180) (2,875)

Total (2,379) (3,995)

The Group calculates the period income tax expense using the tax rate that would be applicable to the expected total annual earnings. 9.11 Earnings per share

The following table shows the calculation of the basic and diluted earnings per share.

For the three months ended March 31,

2017 2016

Net profit (loss) for the period attributable to the owners of the parent (in thousands of Euro) 800 570

Weighted average number of shares (in thousands) 30.000 2,520

Earnings per share (in Euro) 0.03 0.23

Diluted earnings per share is equal to basic earnings per share as no financial instruments having potential dilutive effects had been issued.

15

10. NOTES TO THE UNAUDITED INTERIM CONDENSED CONSOLIDATED STATEMENT OF

FINANCIAL POSITION

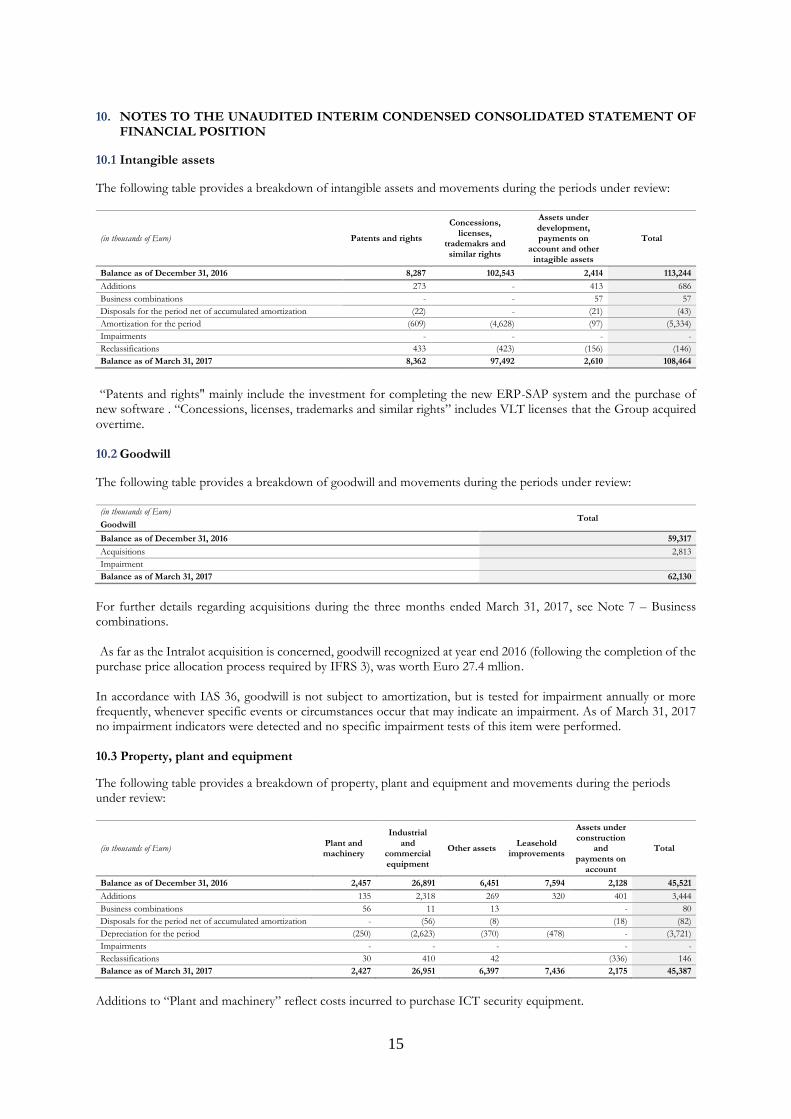

10.1 Intangible assets

The following table provides a breakdown of intangible assets and movements during the periods under review:

(in thousands of Euro) Patents and rights

Concessions, licenses,

trademakrs and similar rights

Assets under development, payments on

account and other intagible assets

Total

Balance as of December 31, 2016 8,287 102,543 2,414 113,244

Additions 273 - 413 686

Business combinations - - 57 57

Disposals for the period net of accumulated amortization (22) - (21) (43)

Amortization for the period (609) (4,628) (97) (5,334)

Impairments - - - -

Reclassifications 433 (423) (156) (146)

Balance as of March 31, 2017 8,362 97,492 2,610 108,464

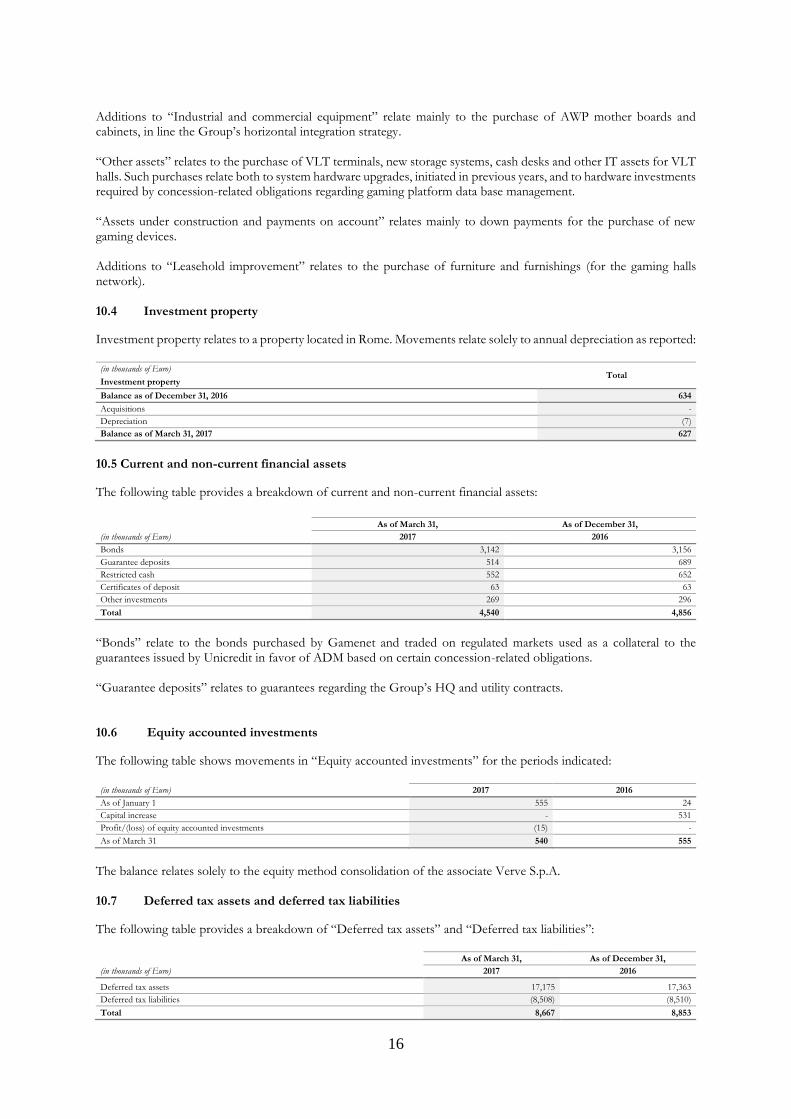

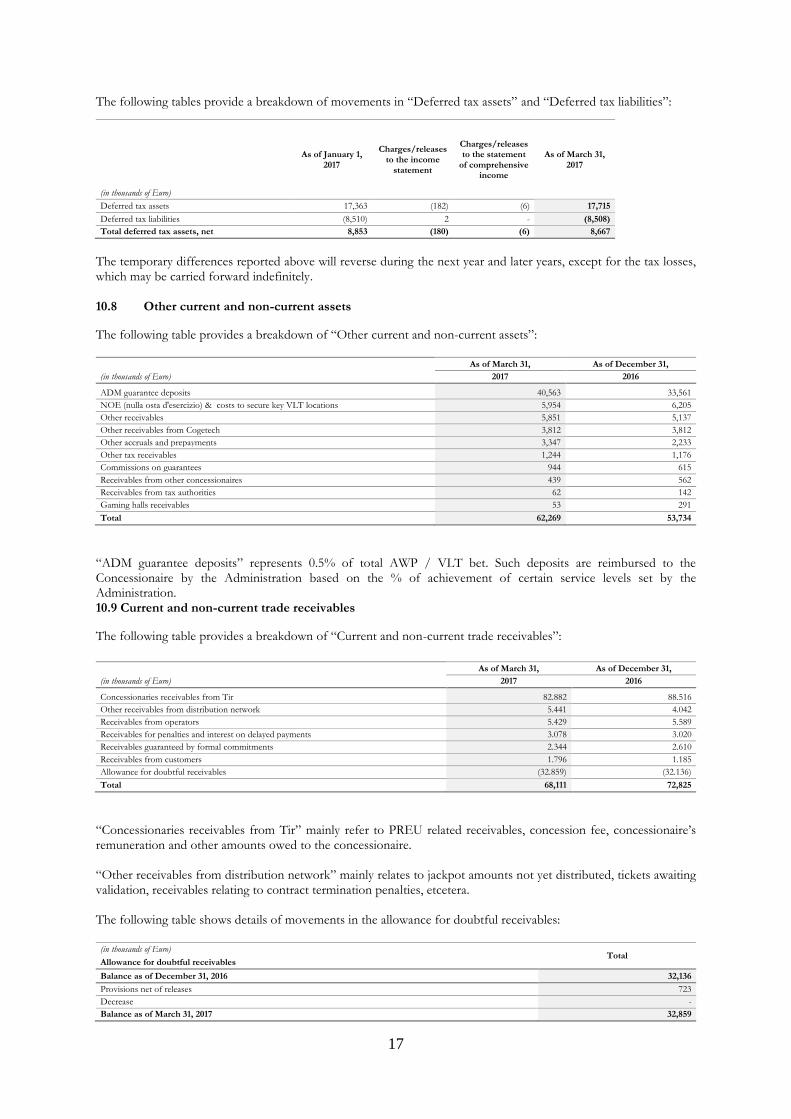

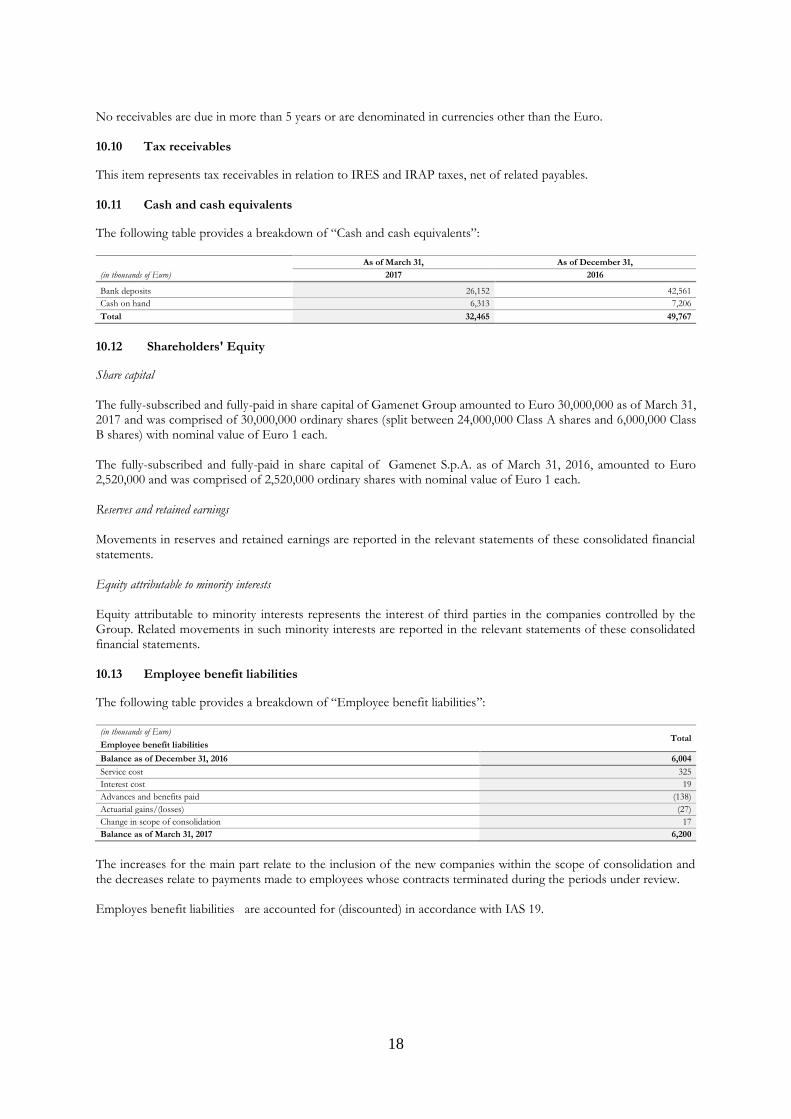

“Patents and rights" mainly include the investment for completing the new ERP-SAP system and the purchase of new software . “Concessions, licenses, trademarks and similar rights” includes VLT licenses that the Group acquired overtime. 10.2 Goodwill

The following table provides a breakdown of goodwill and movements during the periods under review: (in thousands of Euro)

Total Goodwill

Balance as of December 31, 2016 59,317

Acquisitions 2,813