ubl annual report 2010

TRANSCRIPT

• Honesty and integrity

• Commitment and dedication

• Fairness and meritocracy

• Teamwork and collaborative spirit

• Humility and mutual respect

• Caring and socially responsible

[ Core Values ]

[ Mission ]• Set the highest industry standard for quality, across all areas of our operation, on a sustained basis

• Optimize people, processes and technology to deliver the best possible financial solutions to our customers

• Become the most sought after investment and

• Be recognized as the employer of choice

[ Vision ]To be a world class bank dedicated to excellence and to surpass the highest expectations of

our customers and all other stakeholders.

[ Contents ]Company Information

Directors’ Profiles

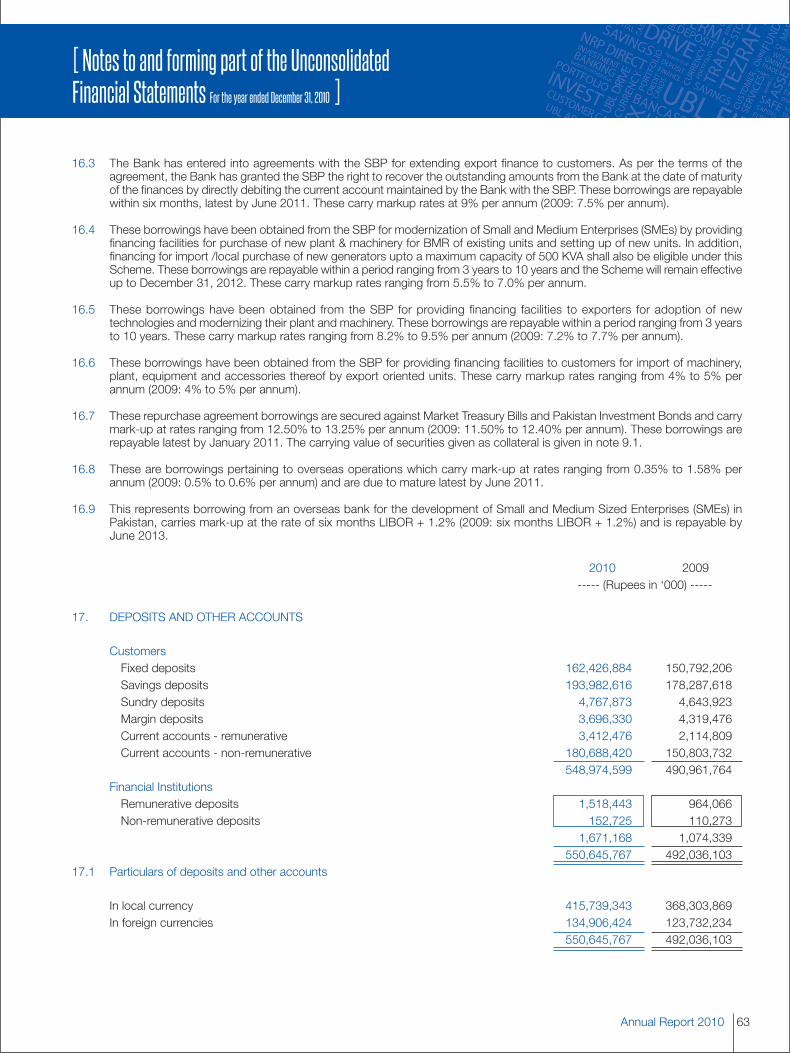

Directors’ Report to the Members

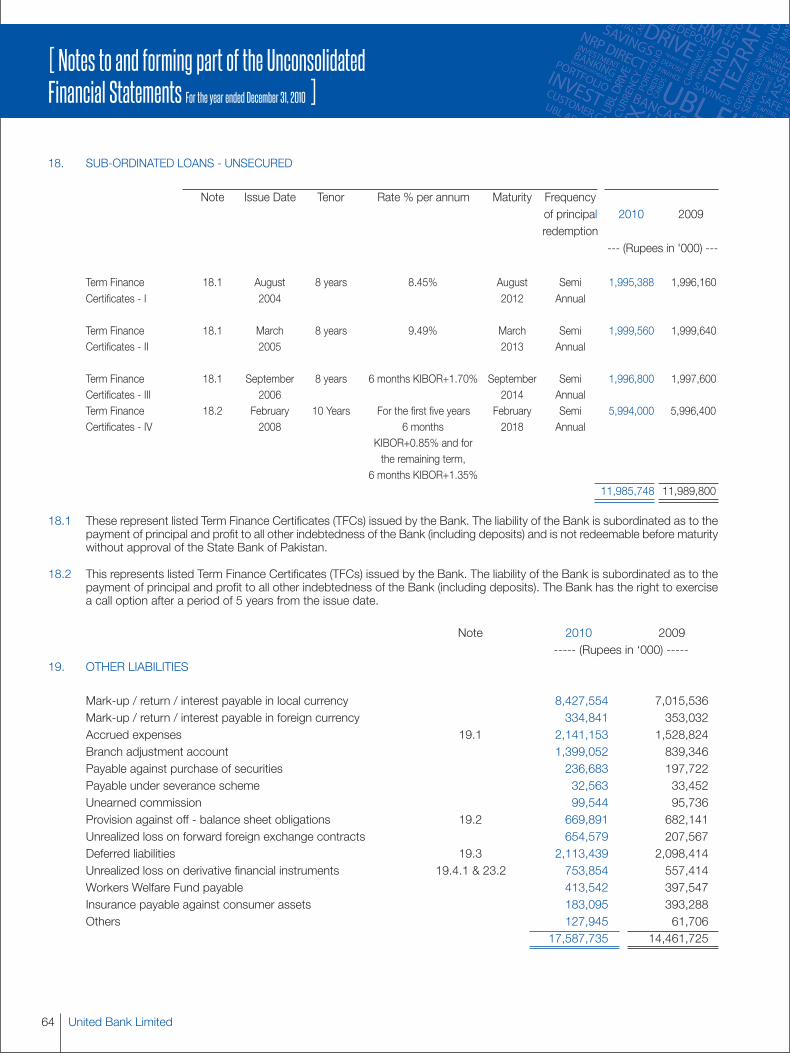

Statement of Corporate Social Responsibility

President & CEO Review

Growth at a Glance

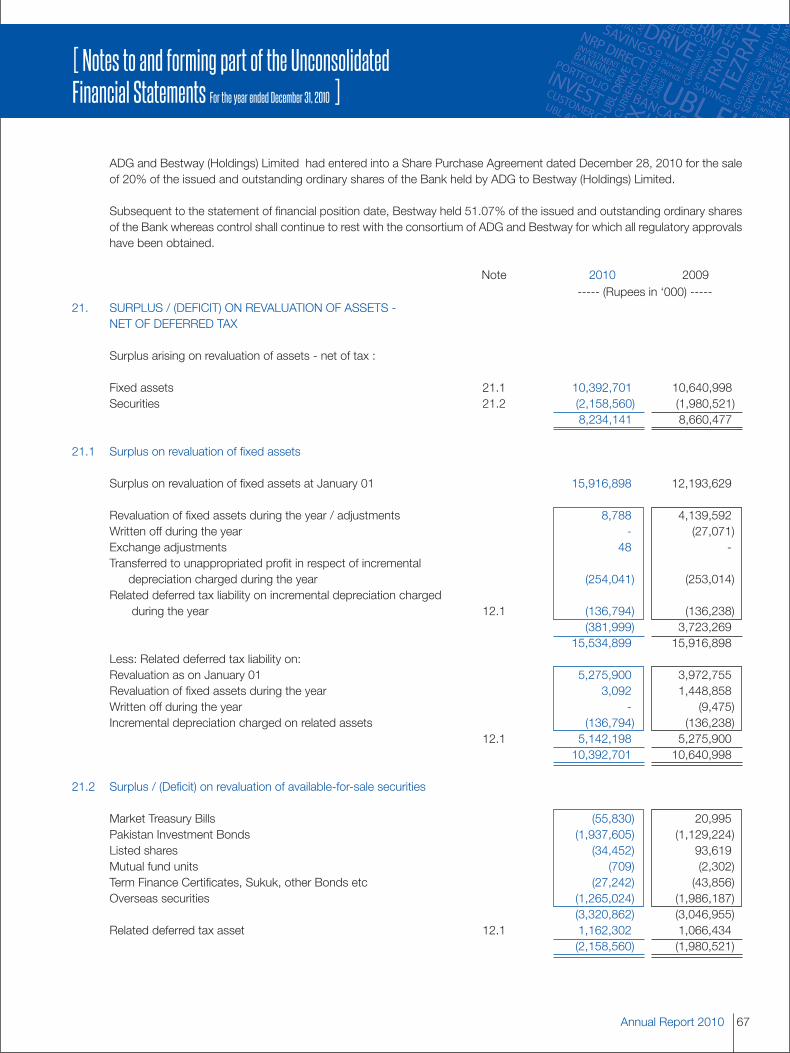

International Network

Shari'ah Advisor's Report

Statement of Compliance with the Code of Corporate Governance

Review Report to the Members on Statement of Compliance with Best Practices of Code of Corporate Governance

Statement of Internal Controls

Auditors’ Report to the Members

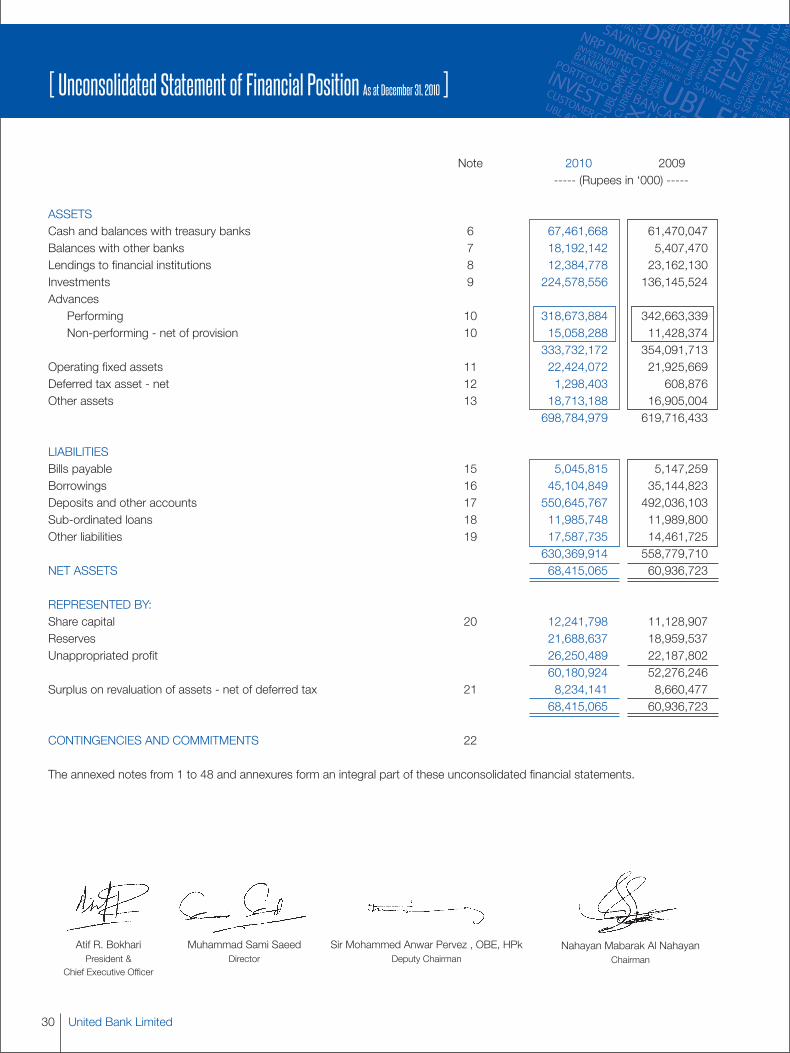

Unconsolidated Statement of Financial Position

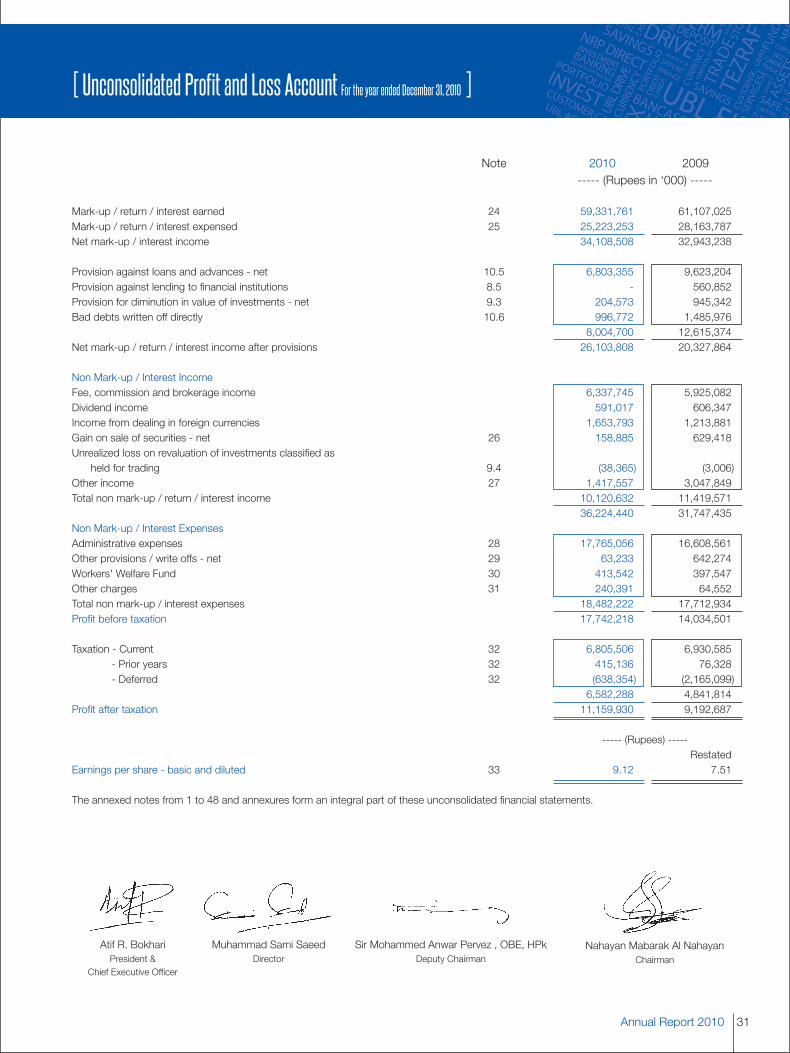

Unconsolidated Profit & Loss Account

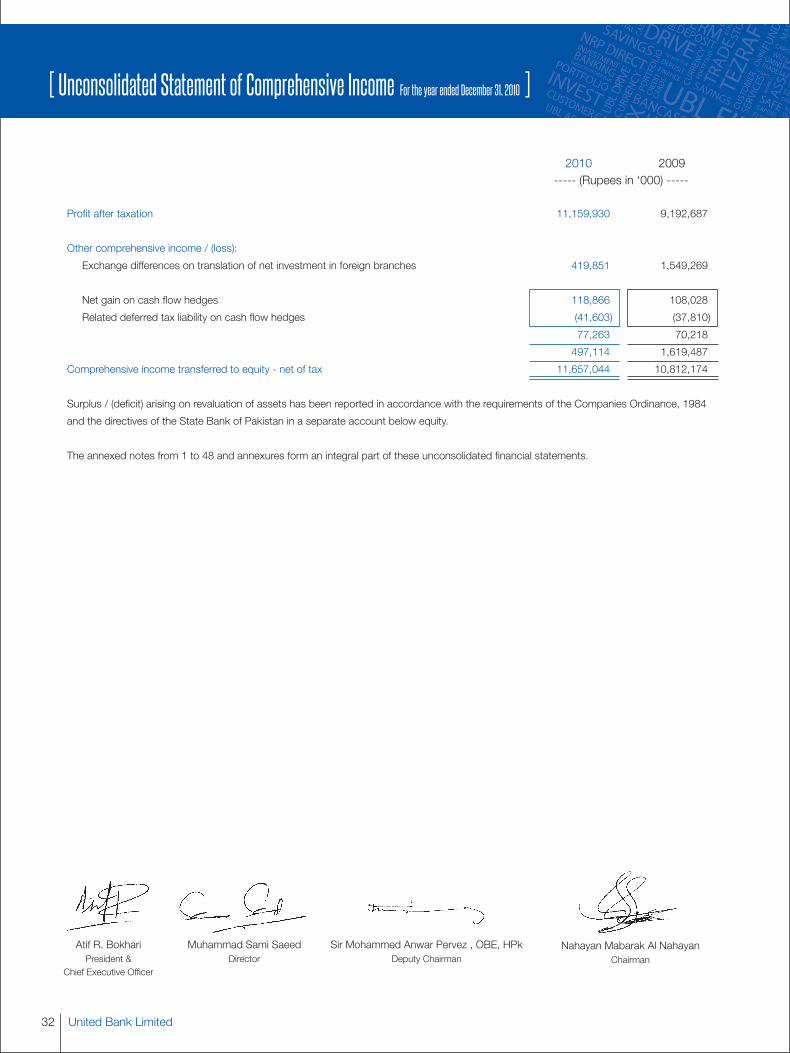

Unconsolidated Statement of Comprehensive Income

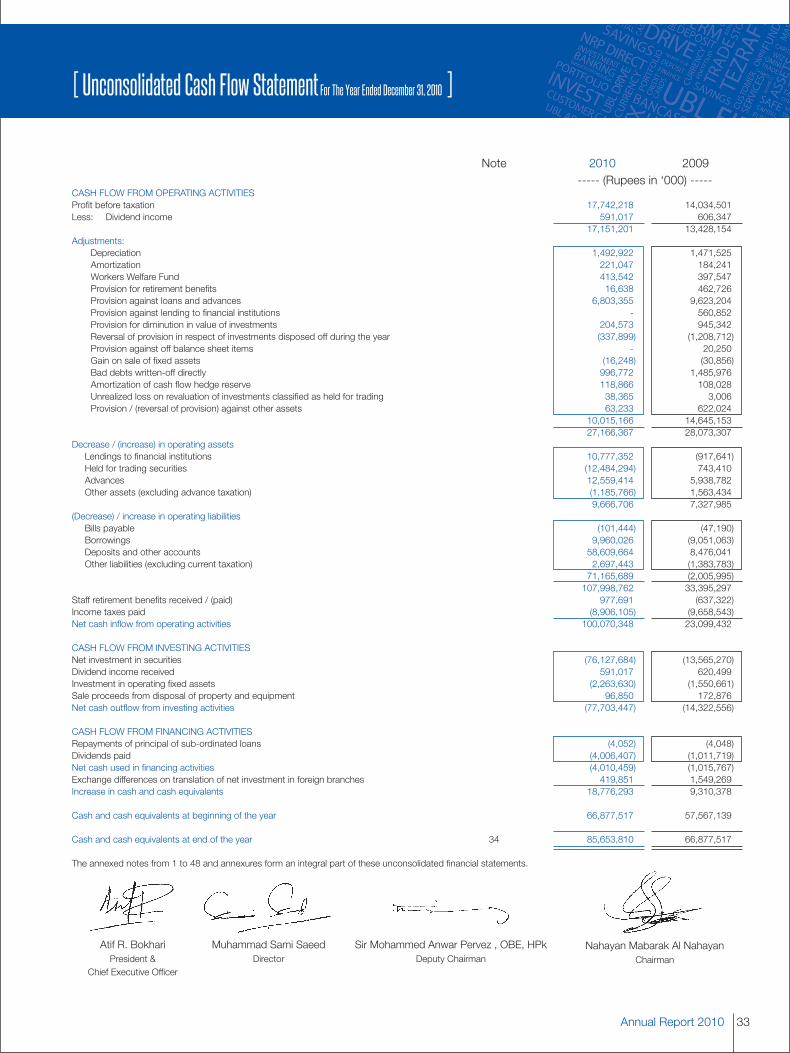

Unconsolidated Cash Flow Statement

Unconsolidated Statement of Changes in Equity

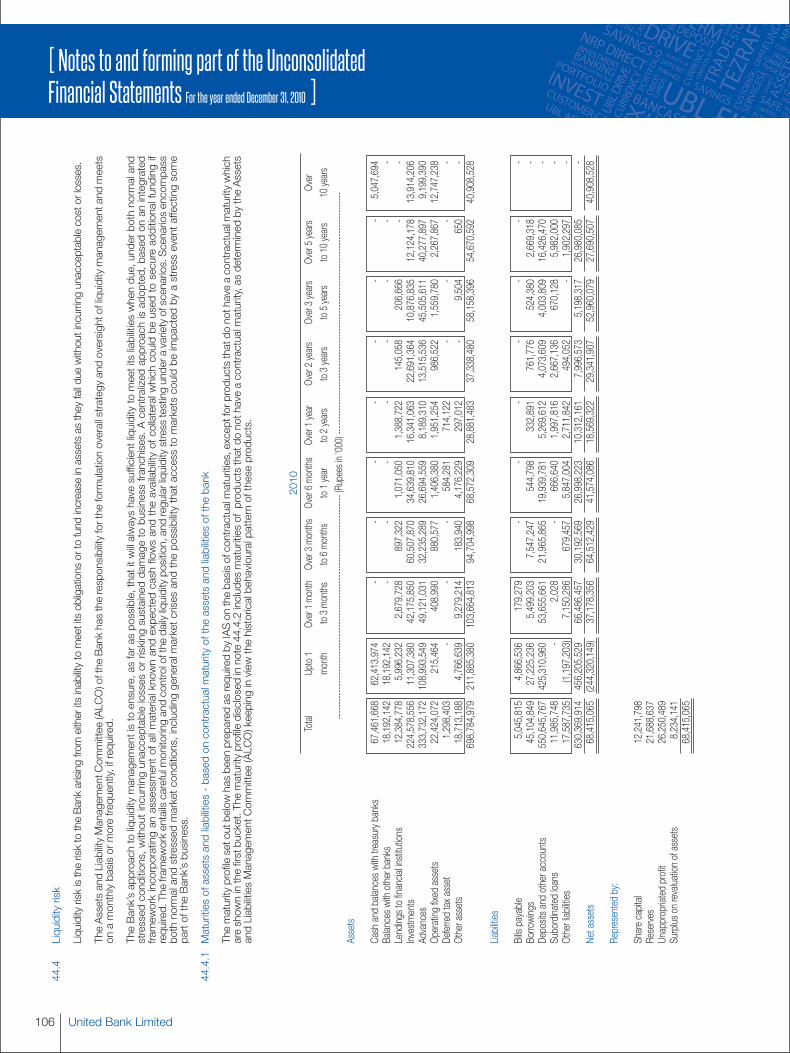

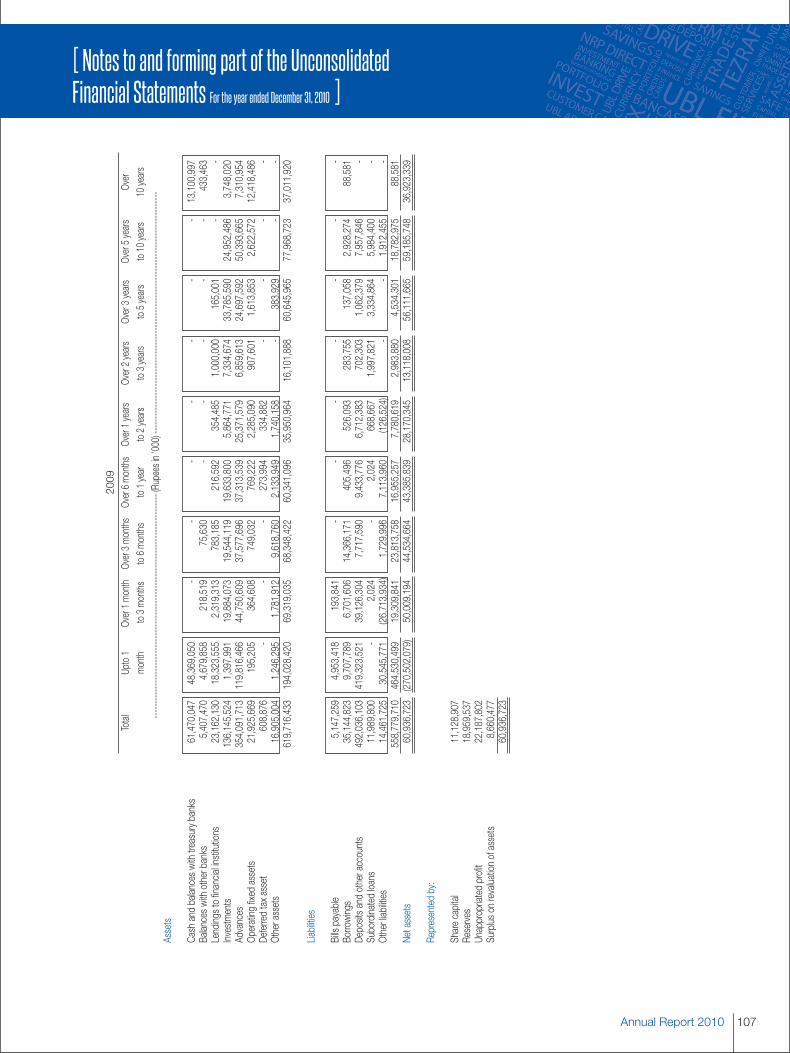

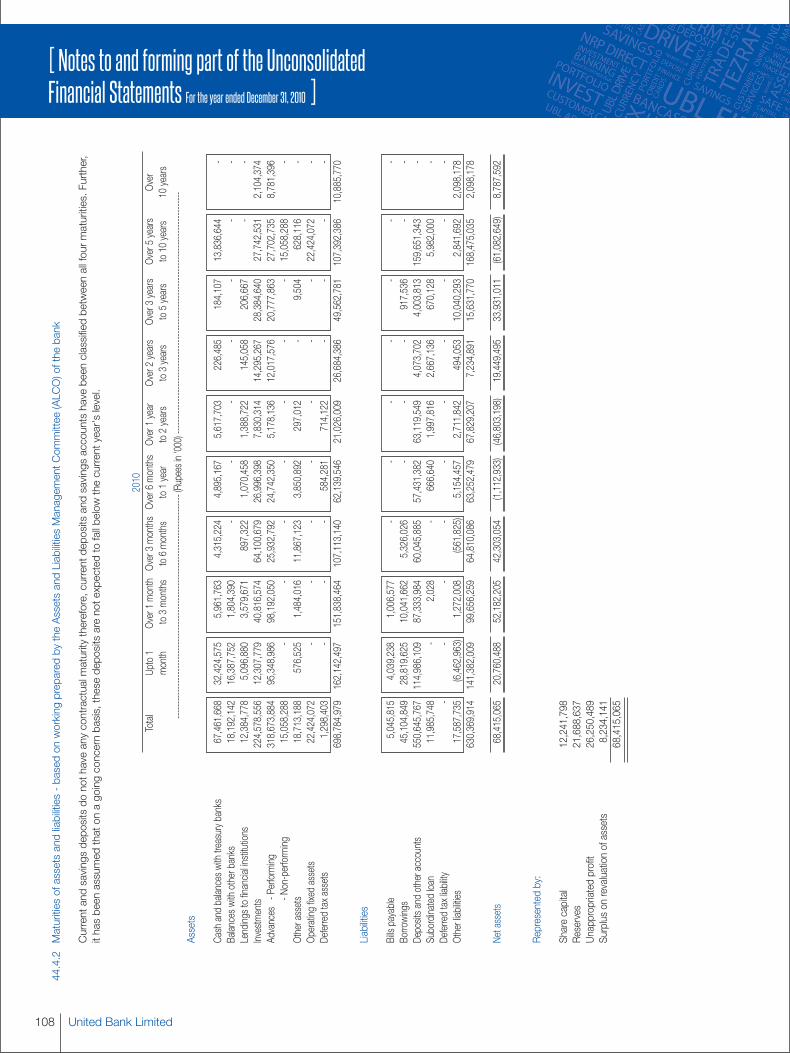

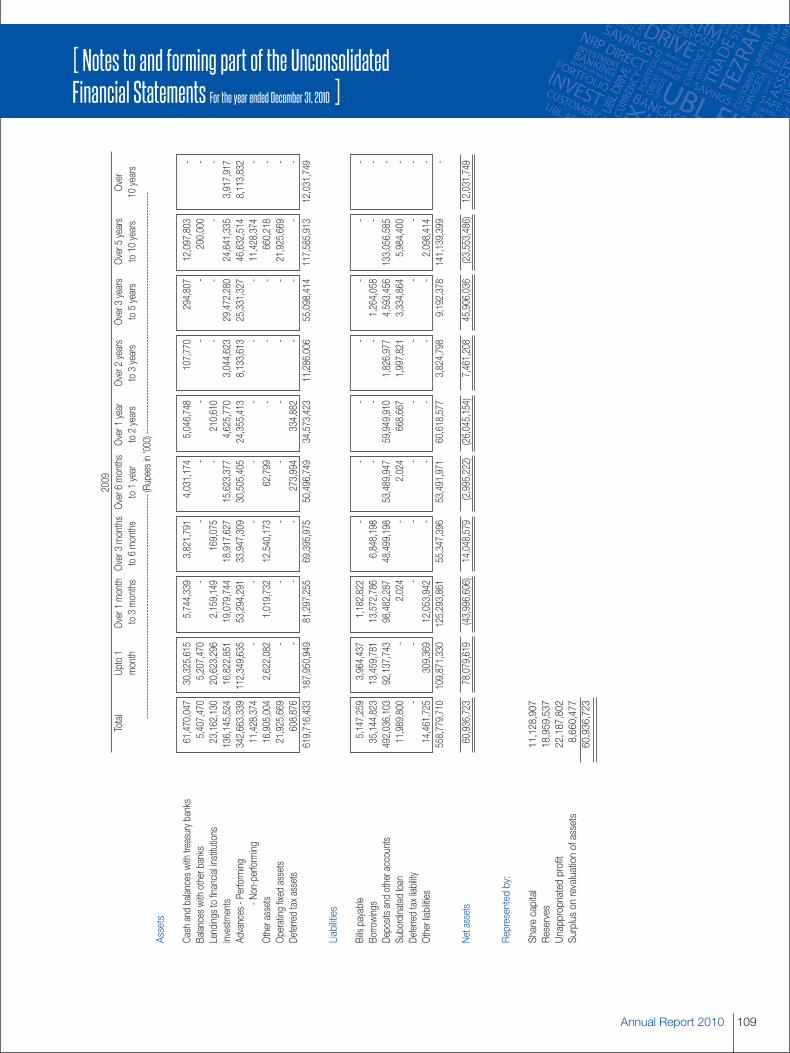

Notes to and forming part of the Unconsolidated Financial Statement

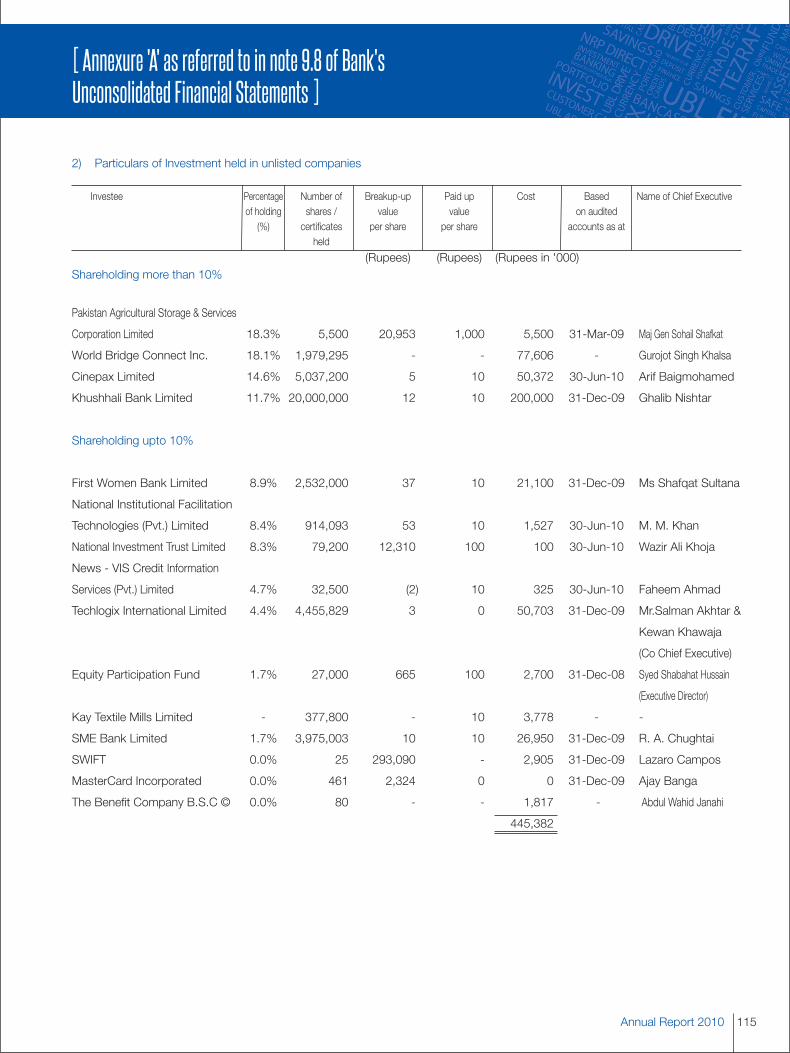

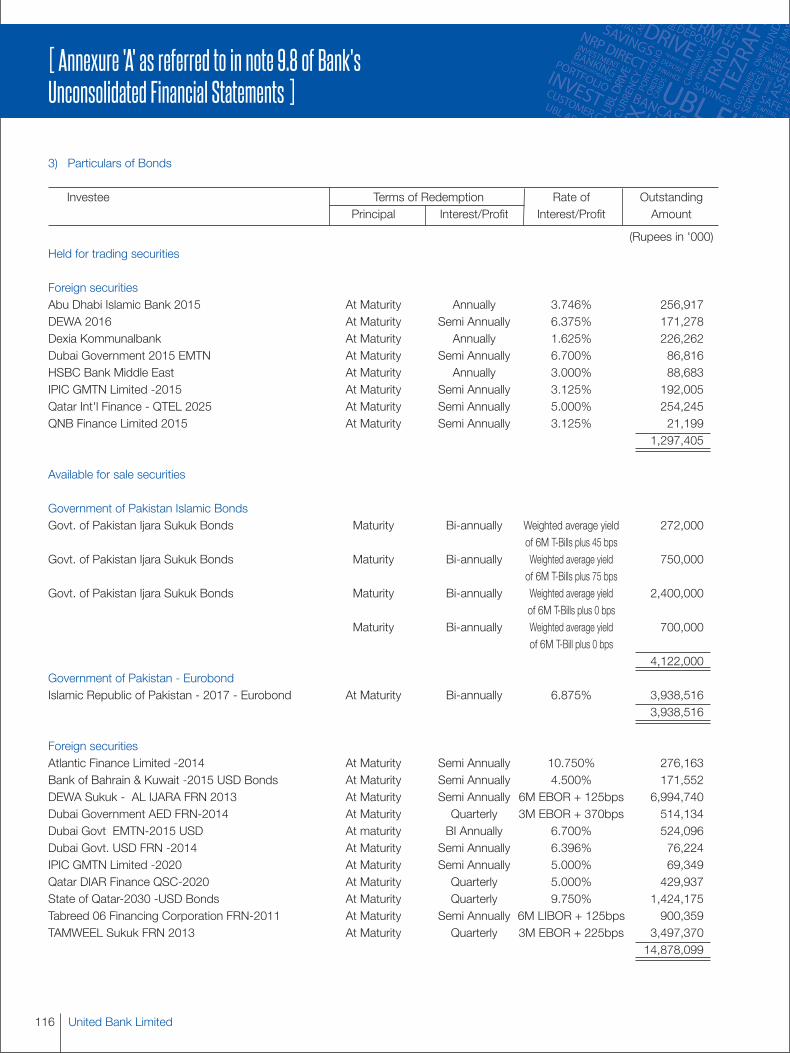

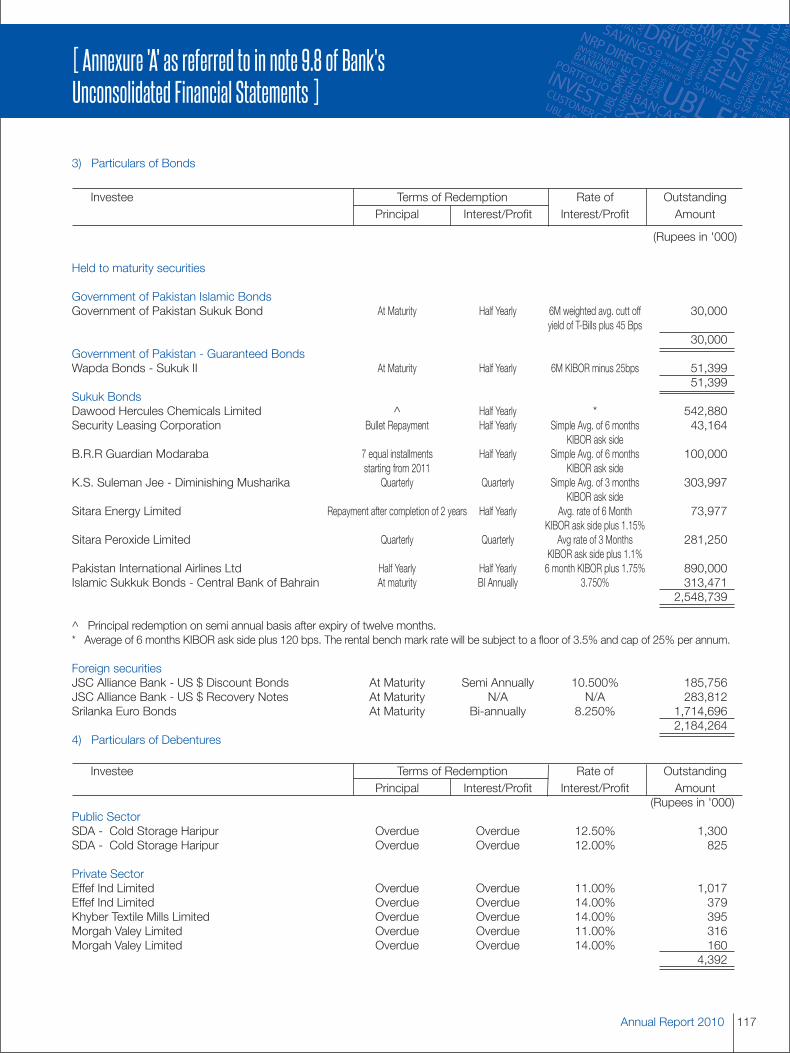

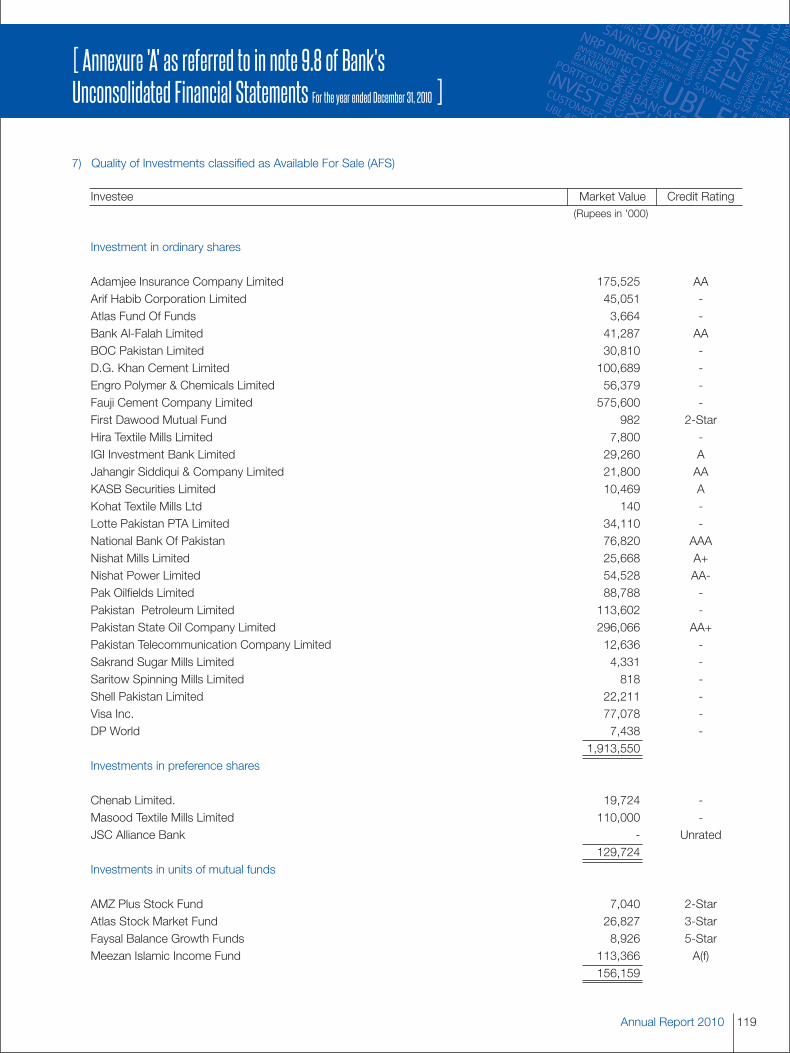

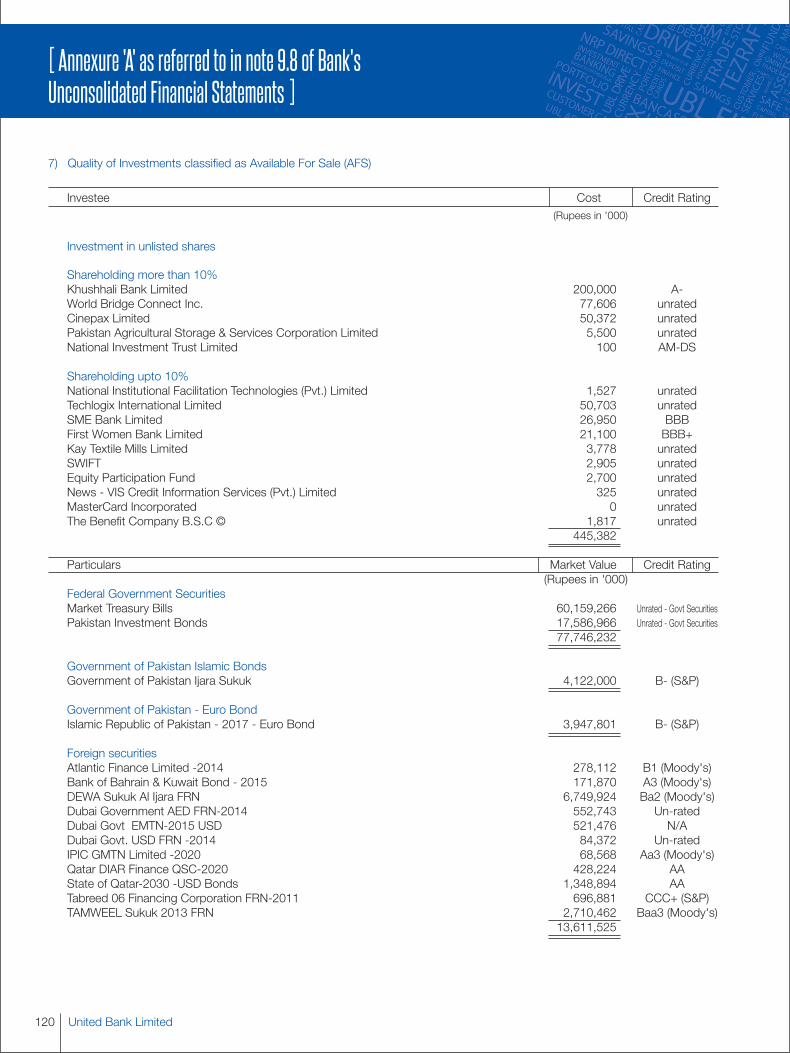

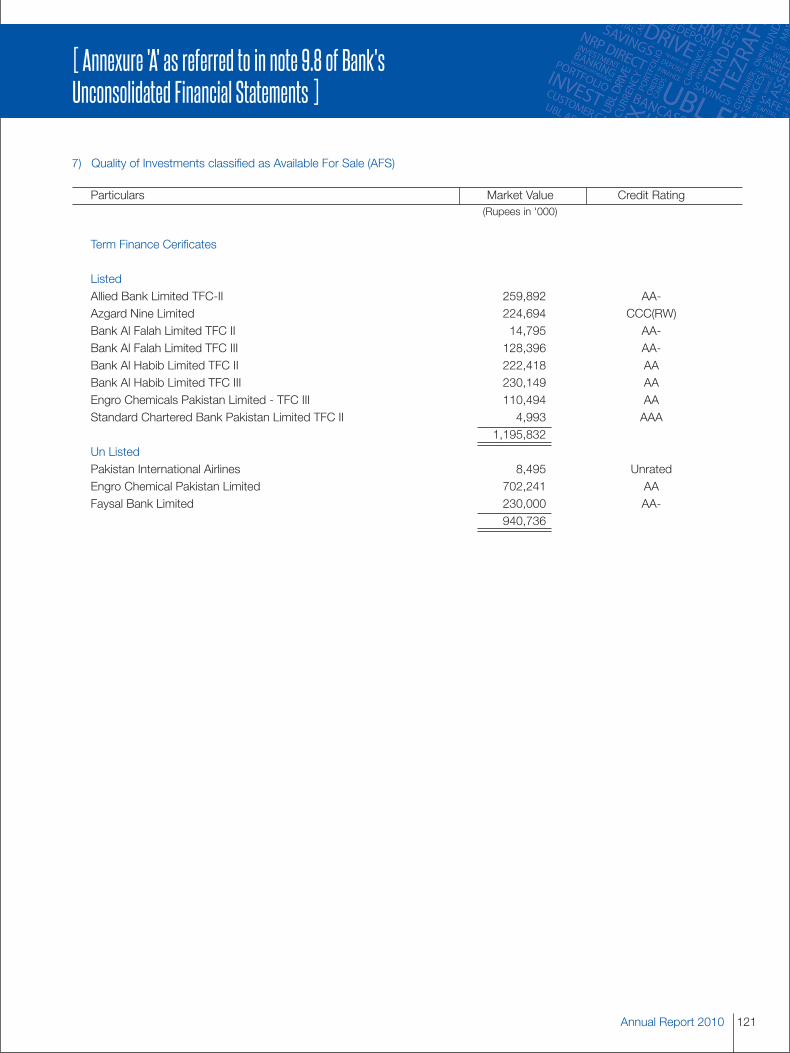

Annexure ‘A’ as referred to in note 9.8 of Bank’s Unconsolidated Financial Statements

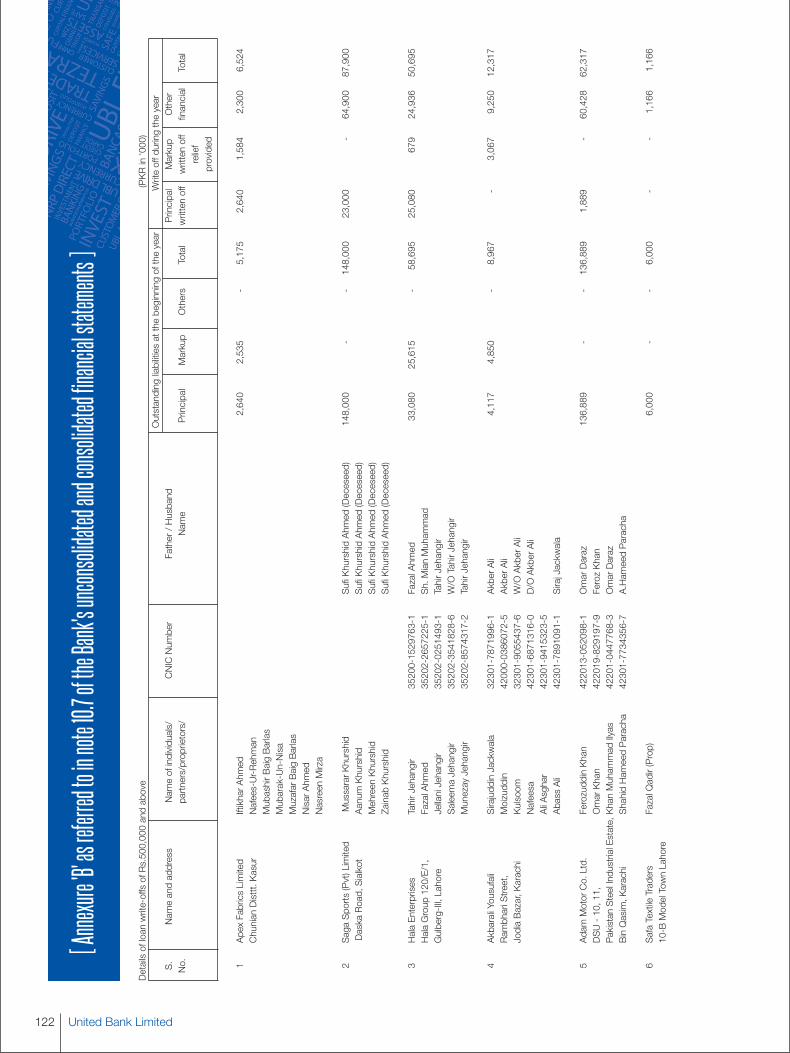

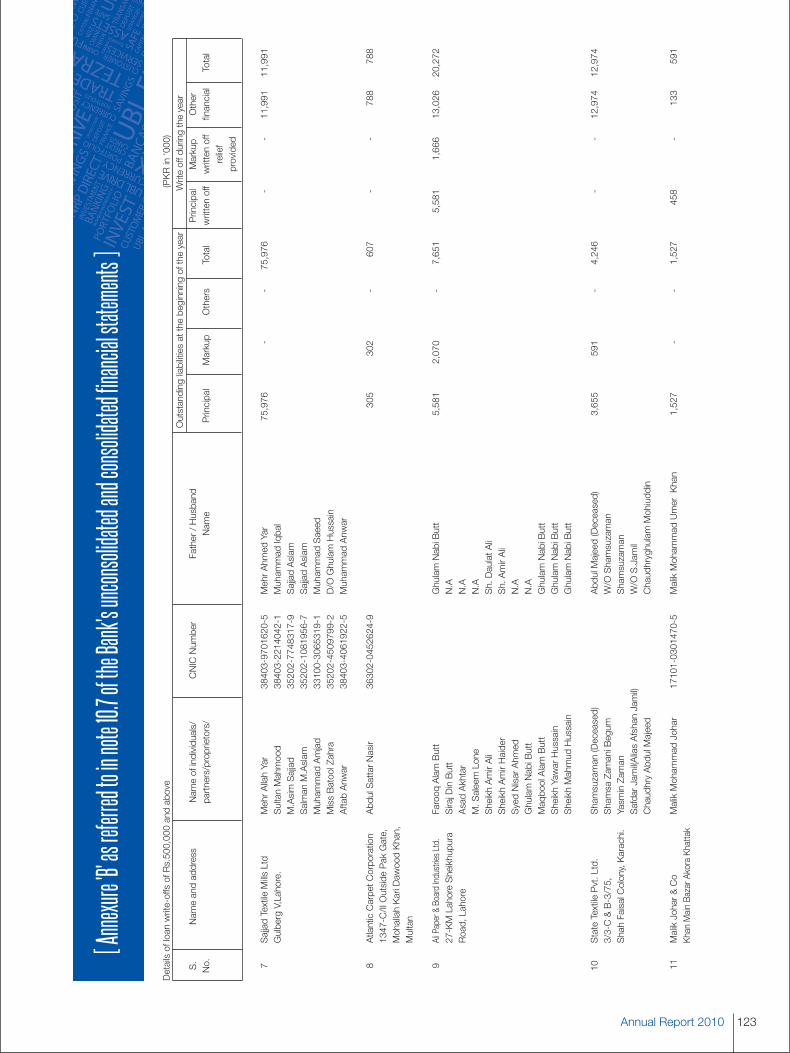

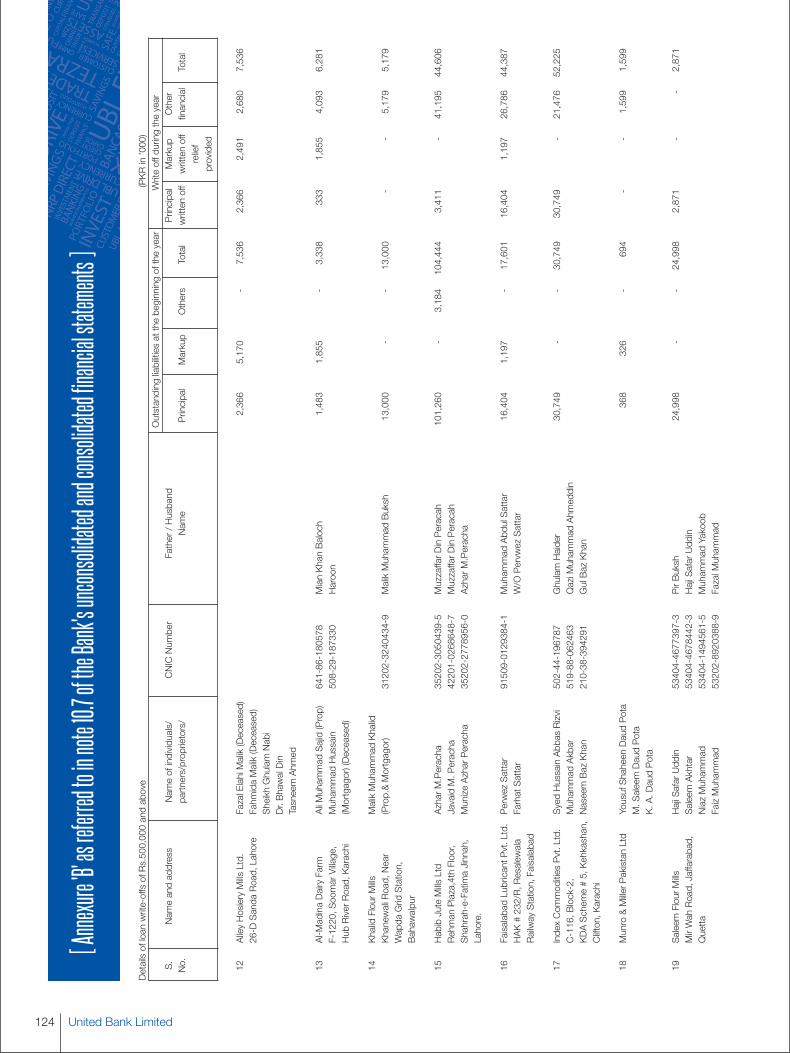

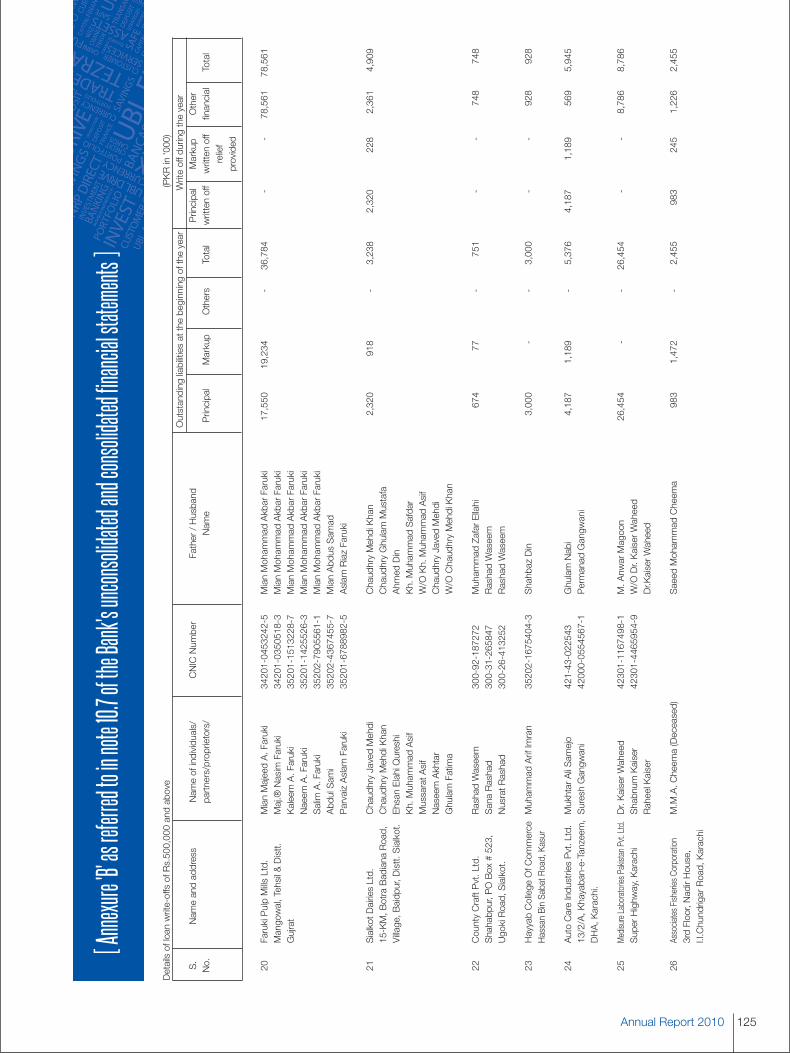

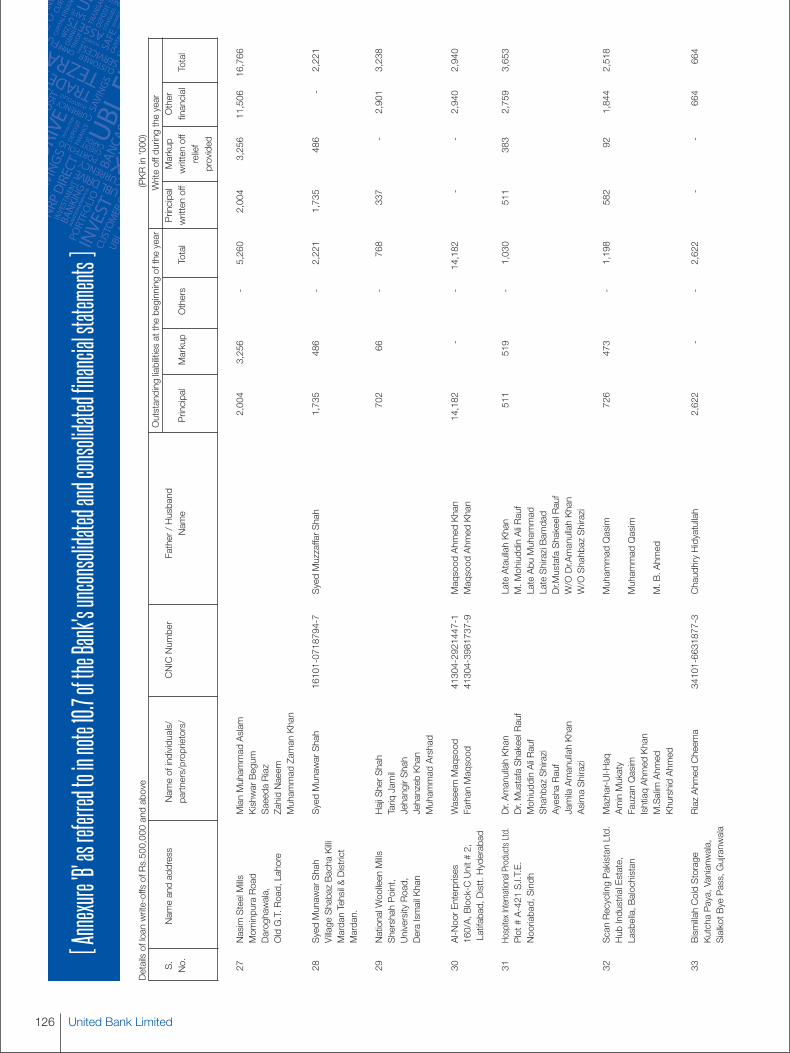

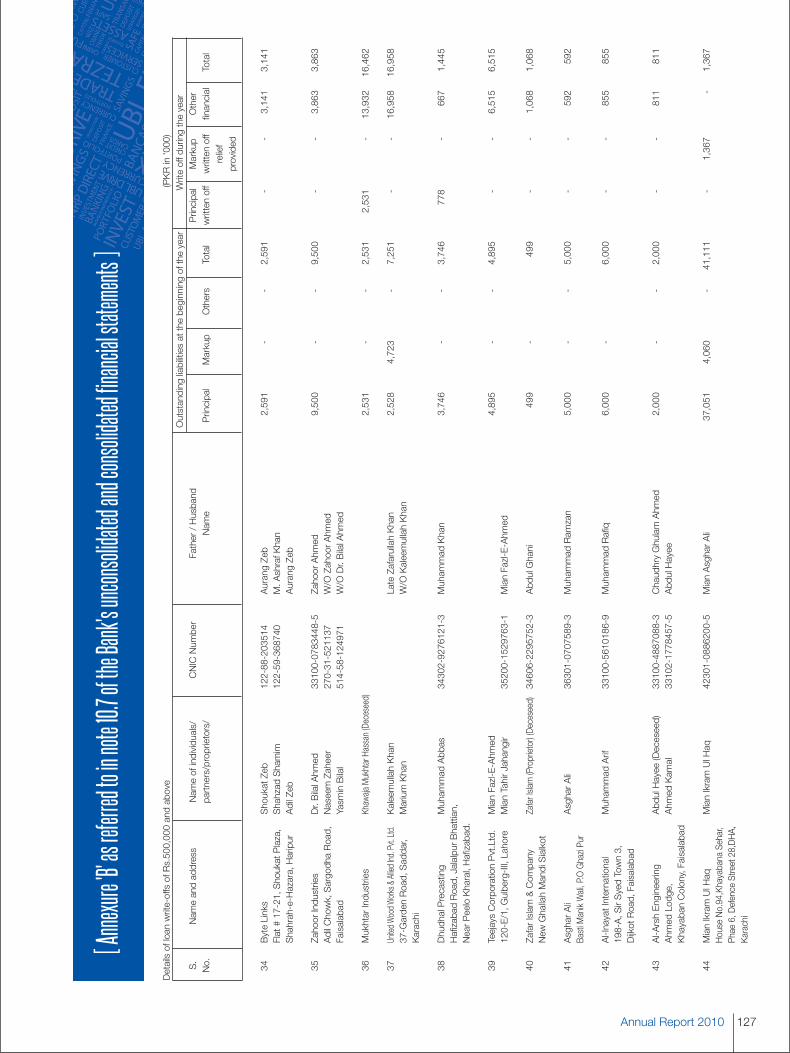

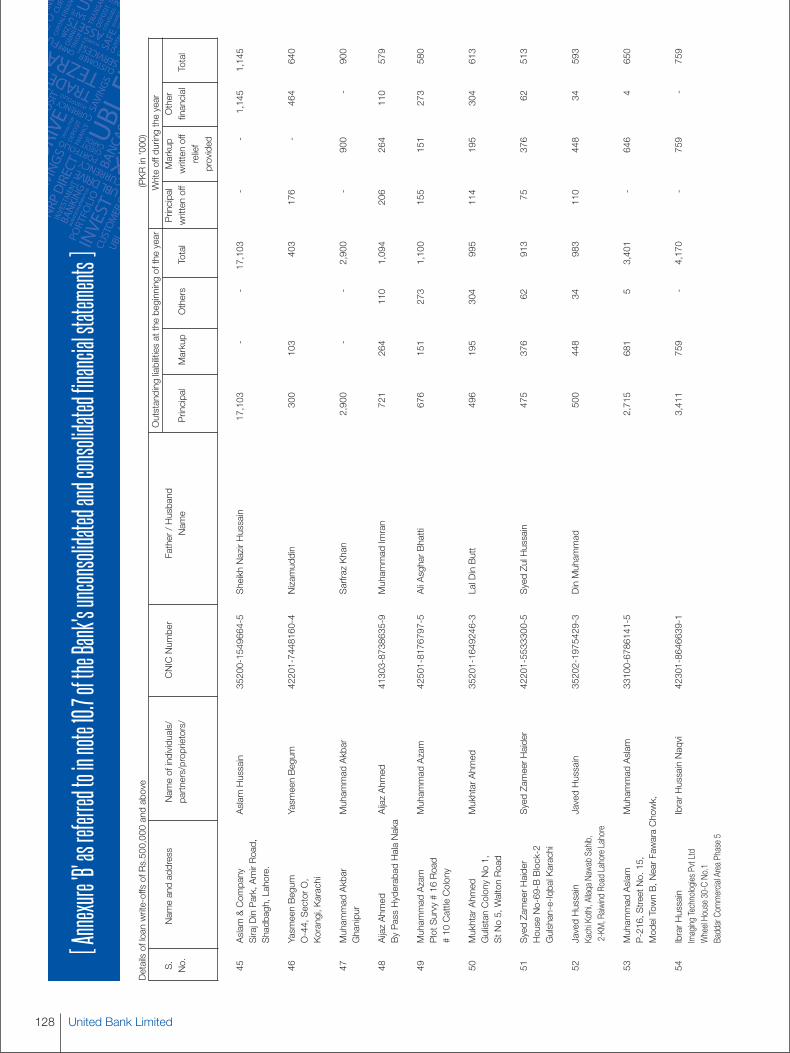

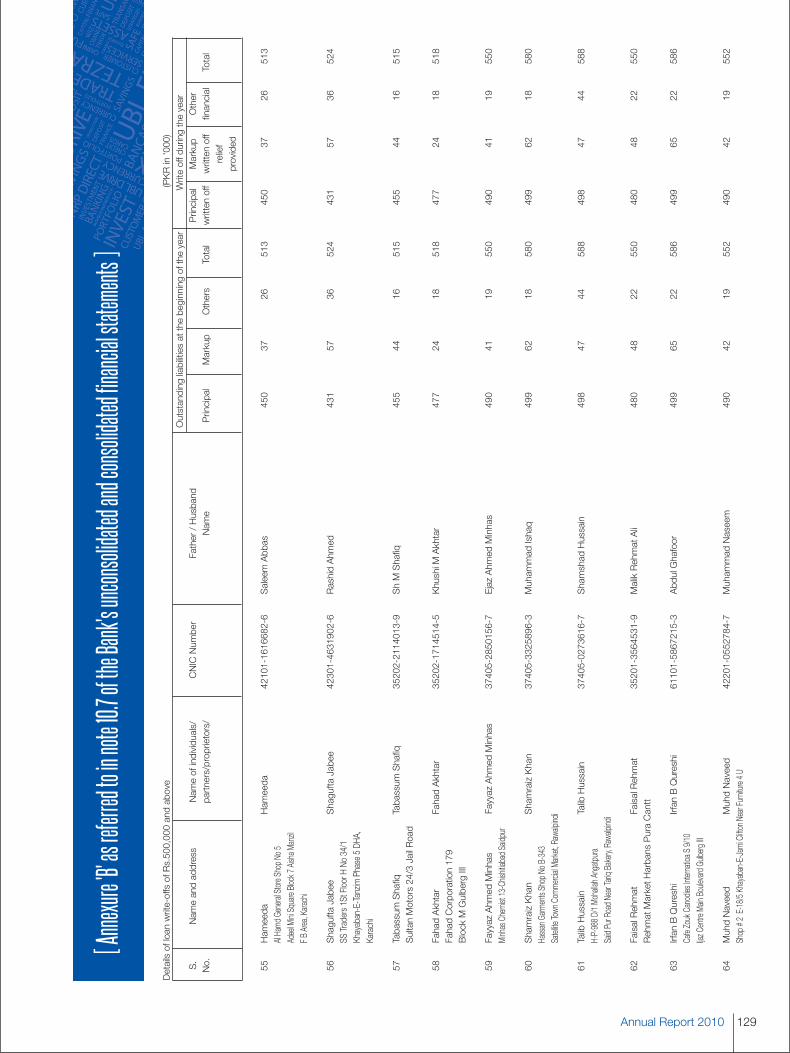

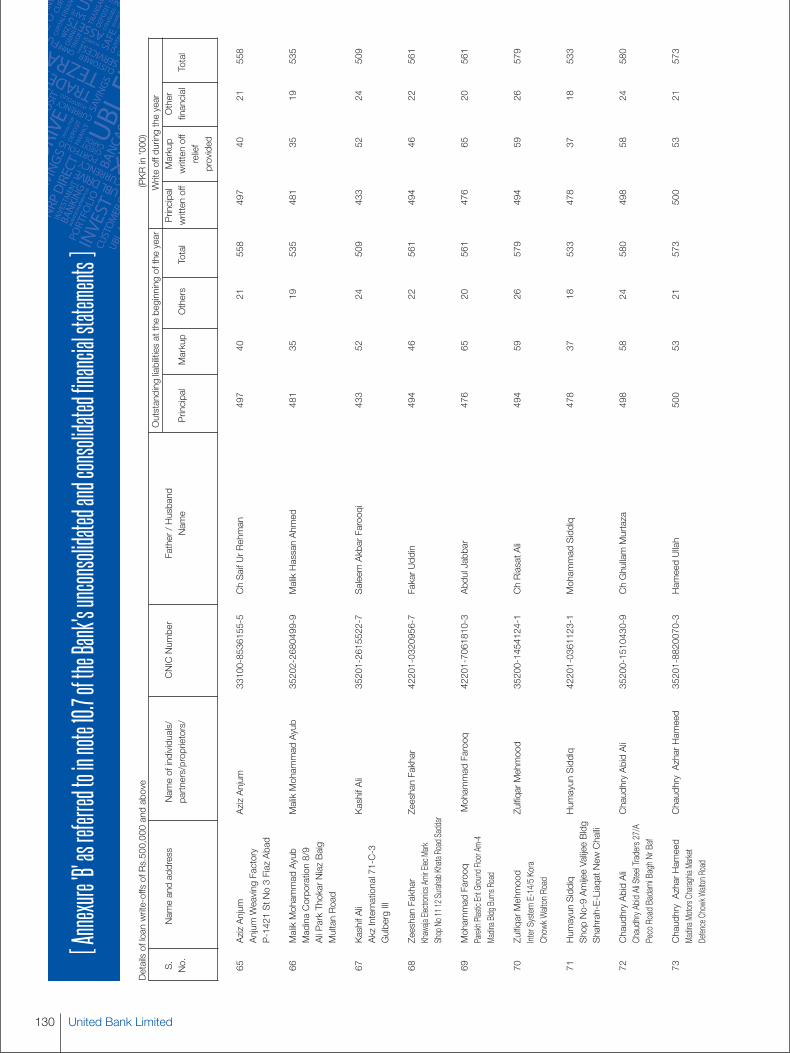

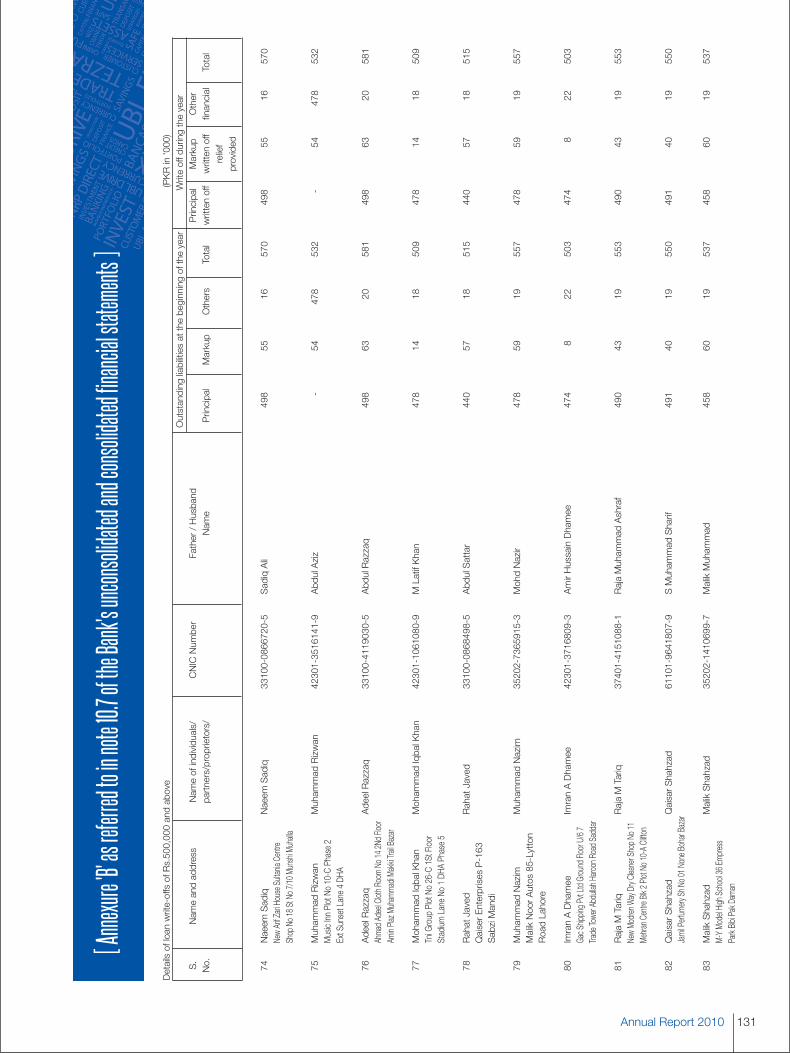

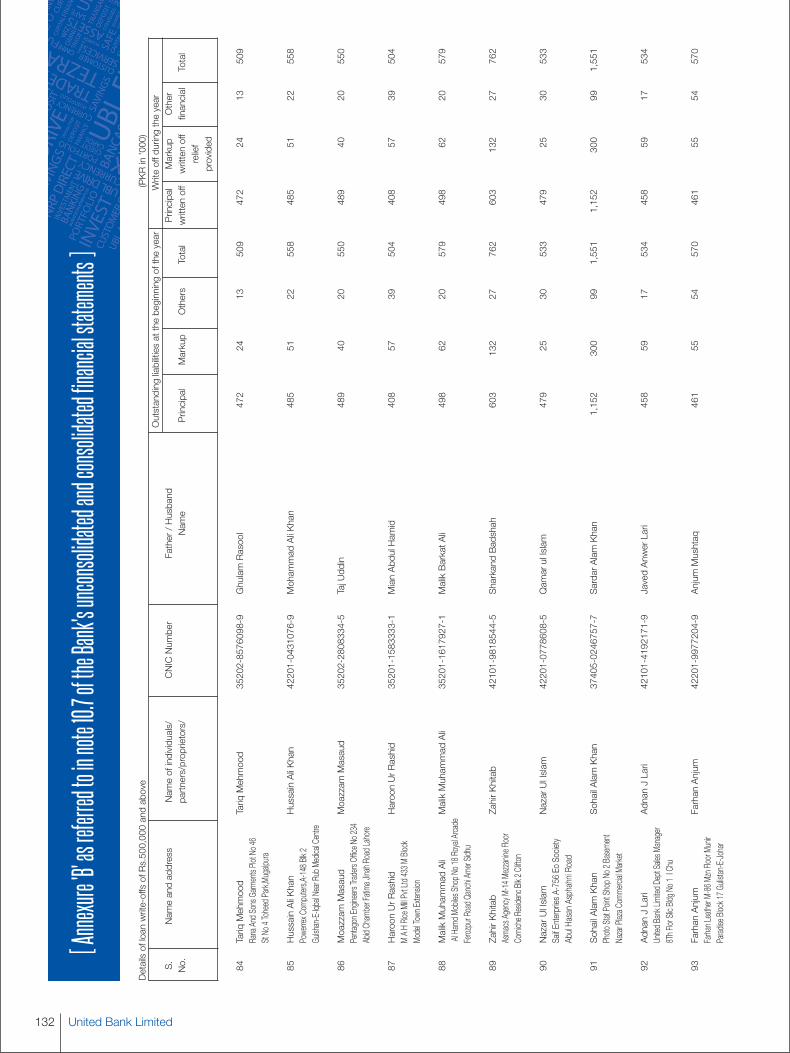

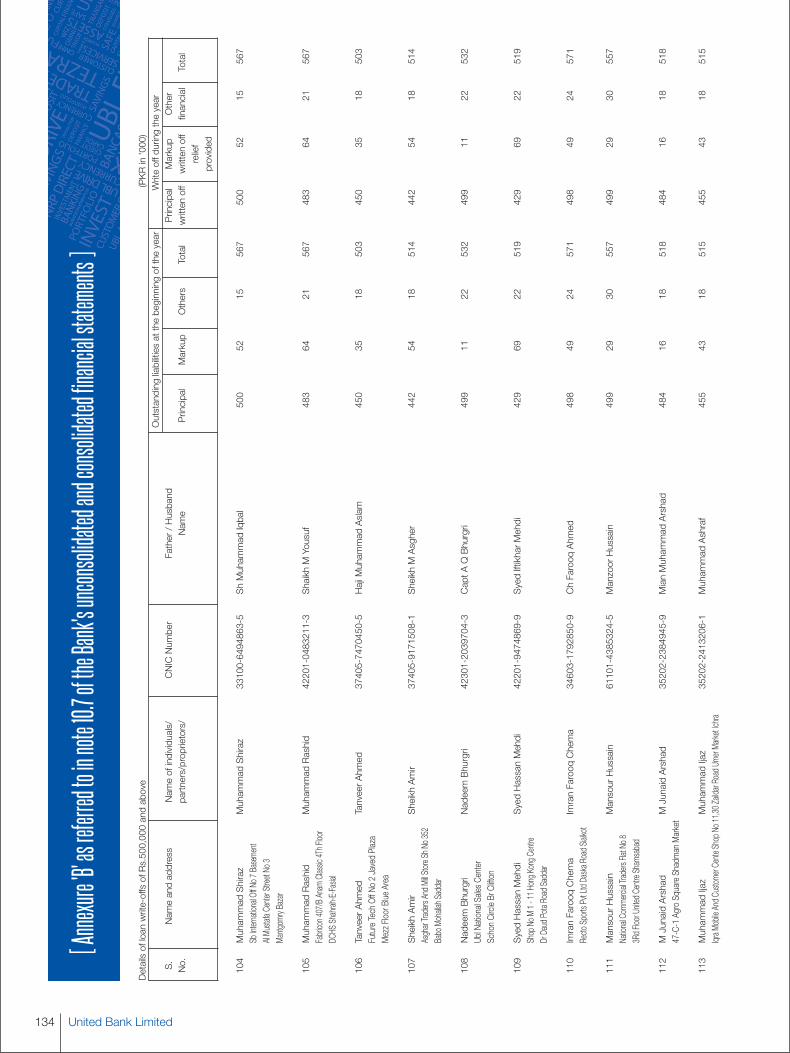

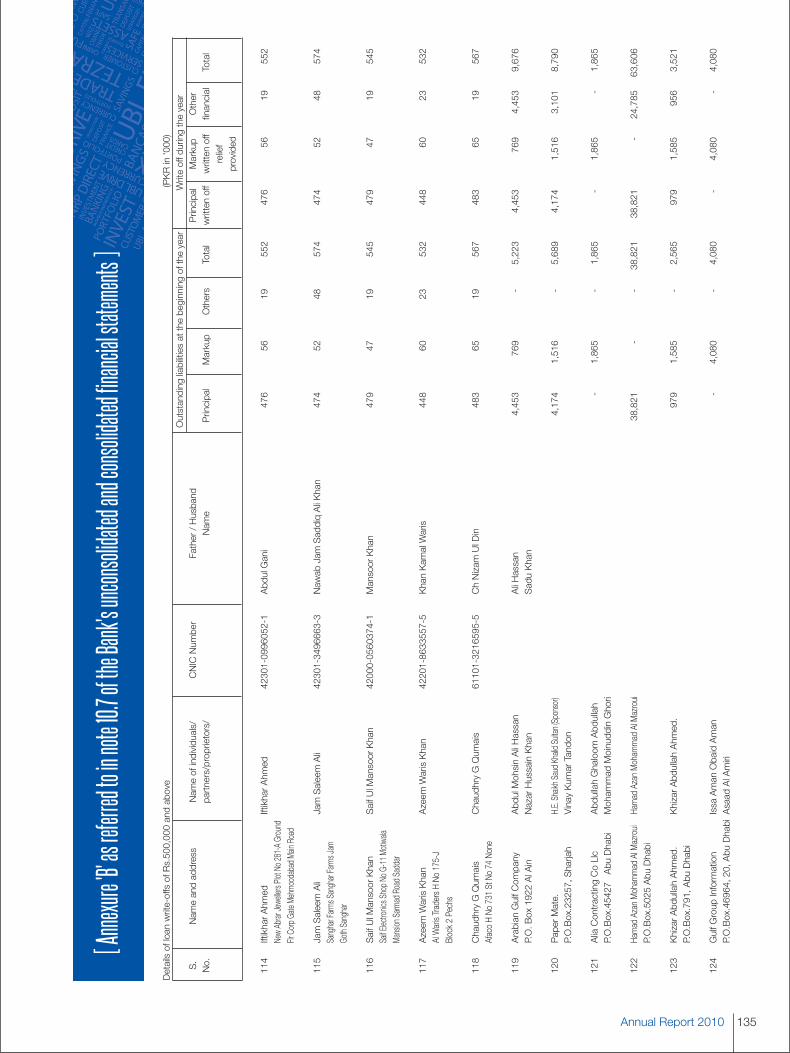

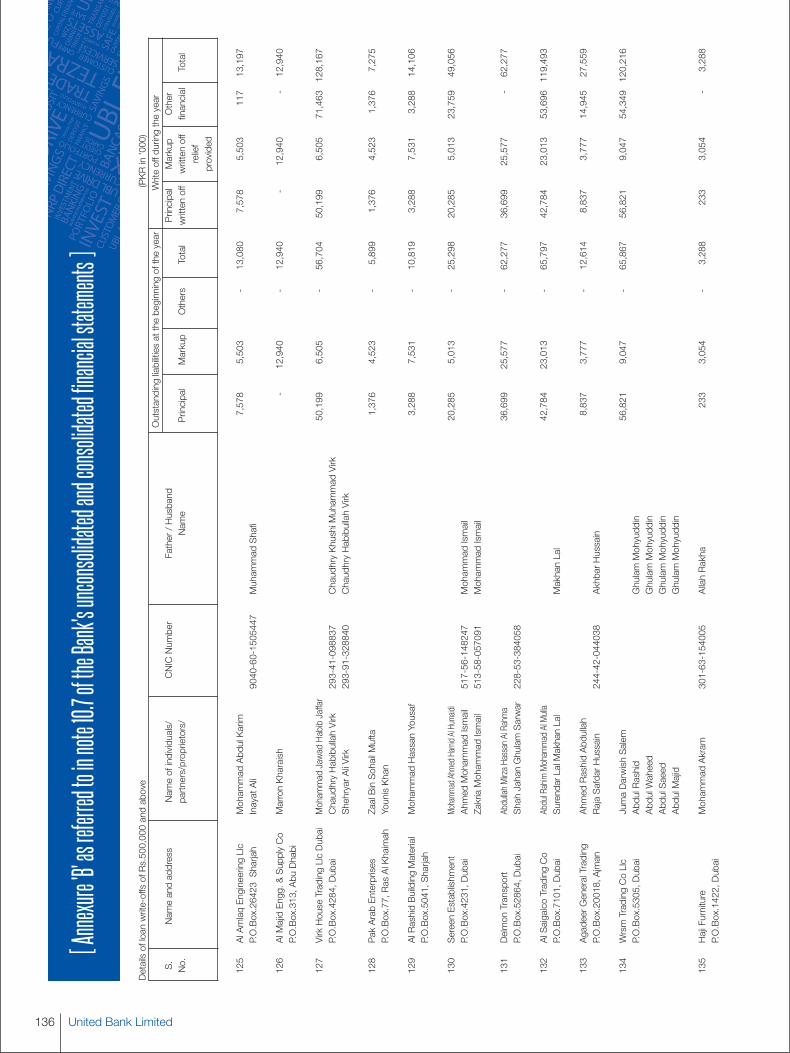

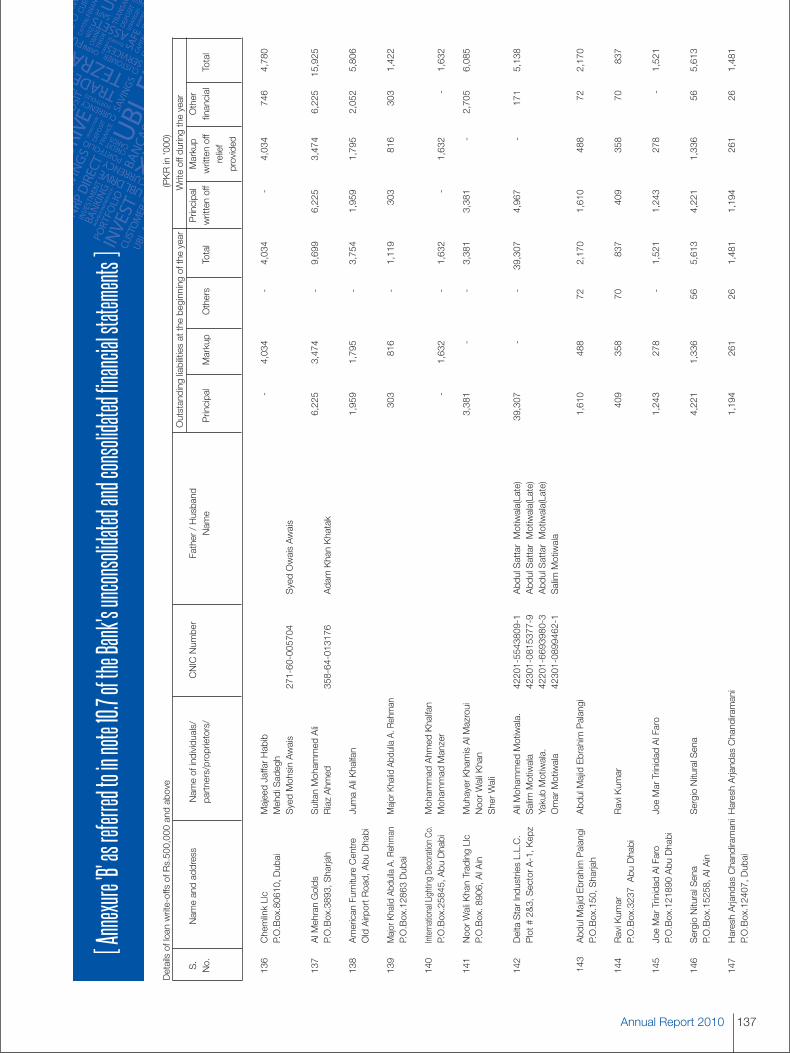

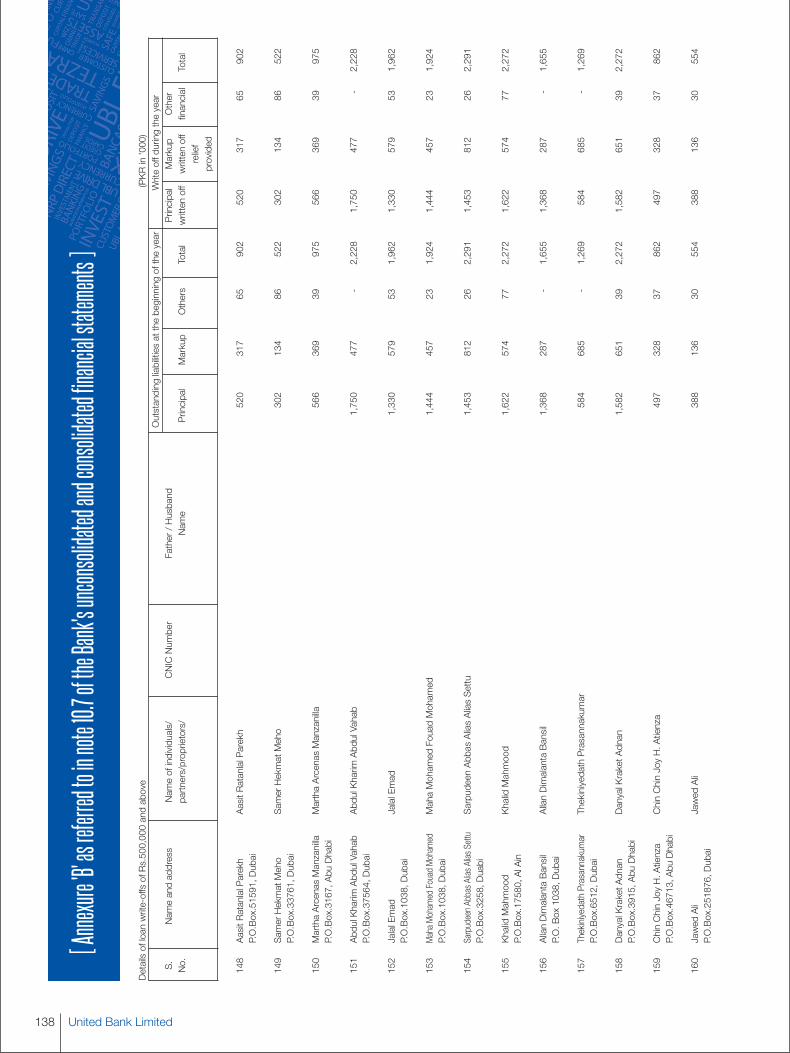

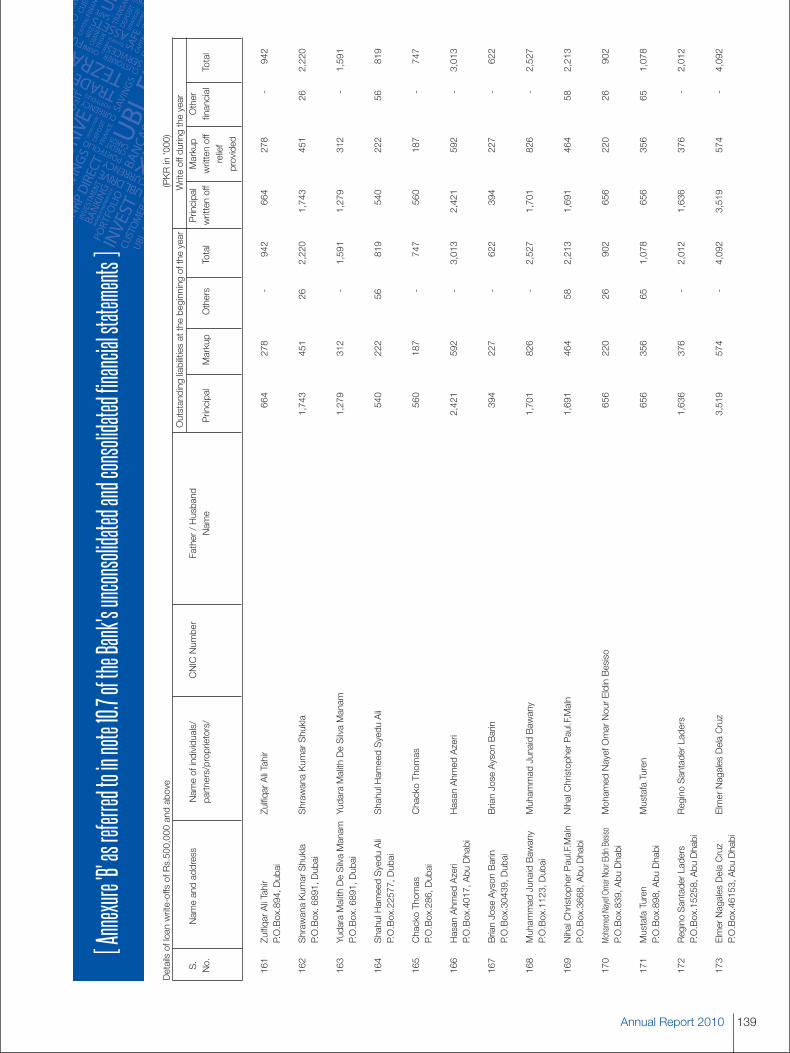

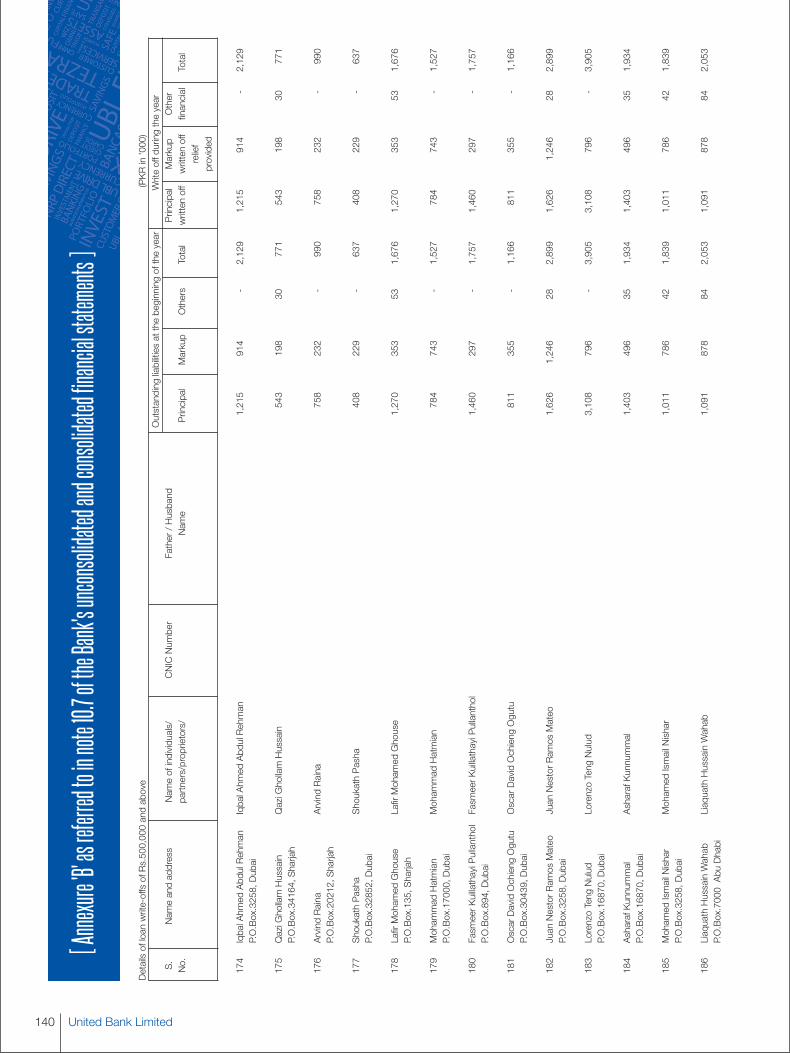

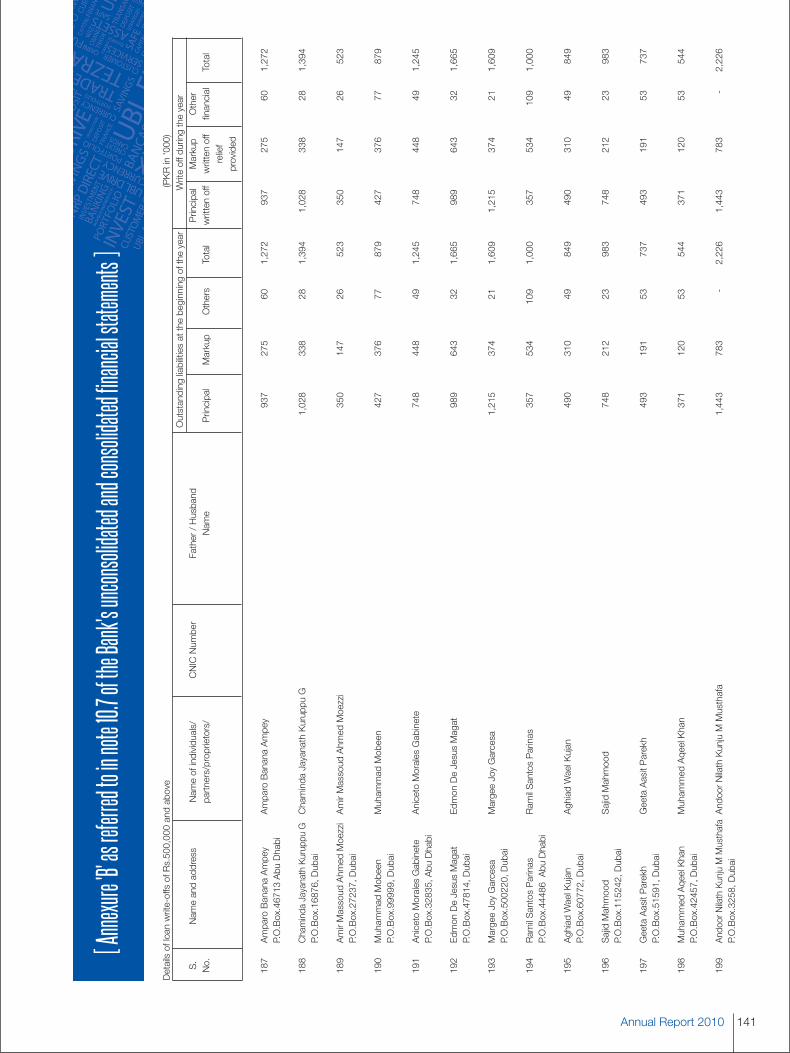

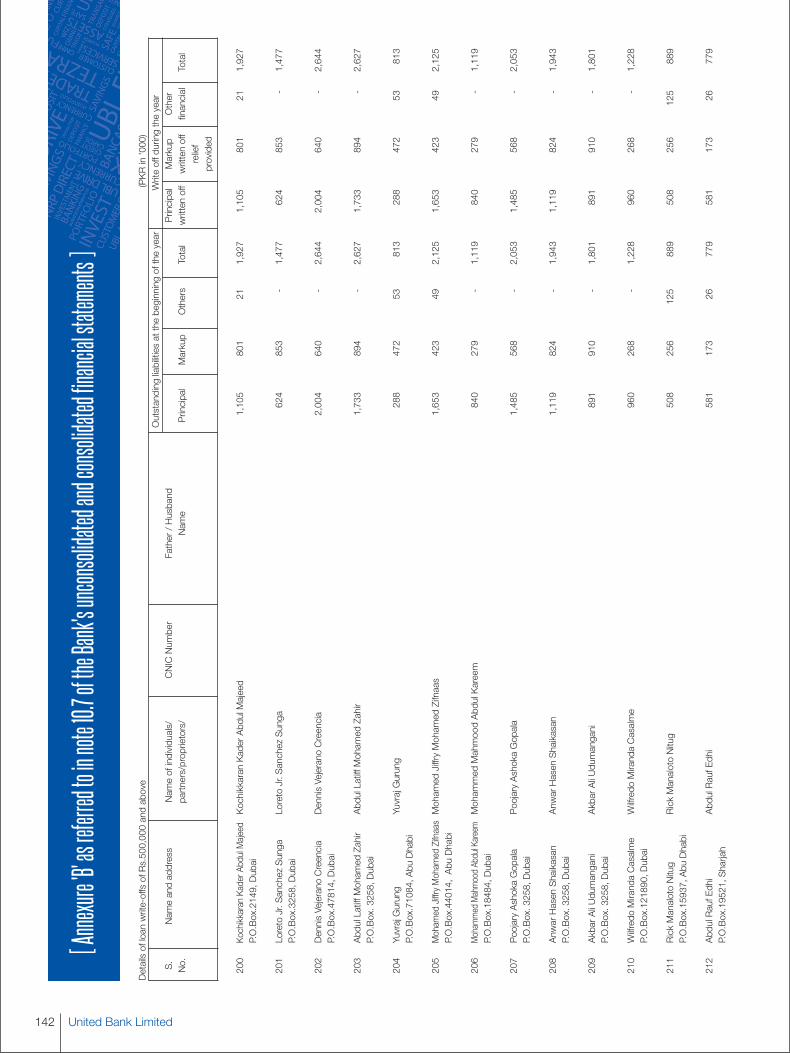

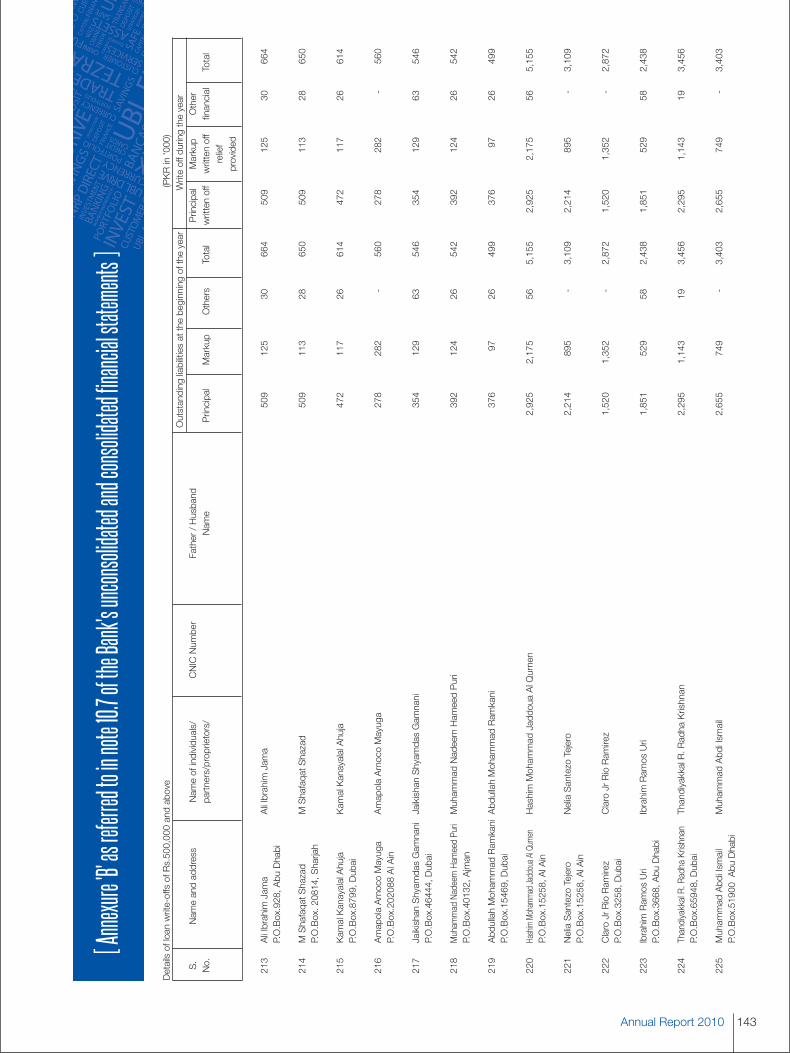

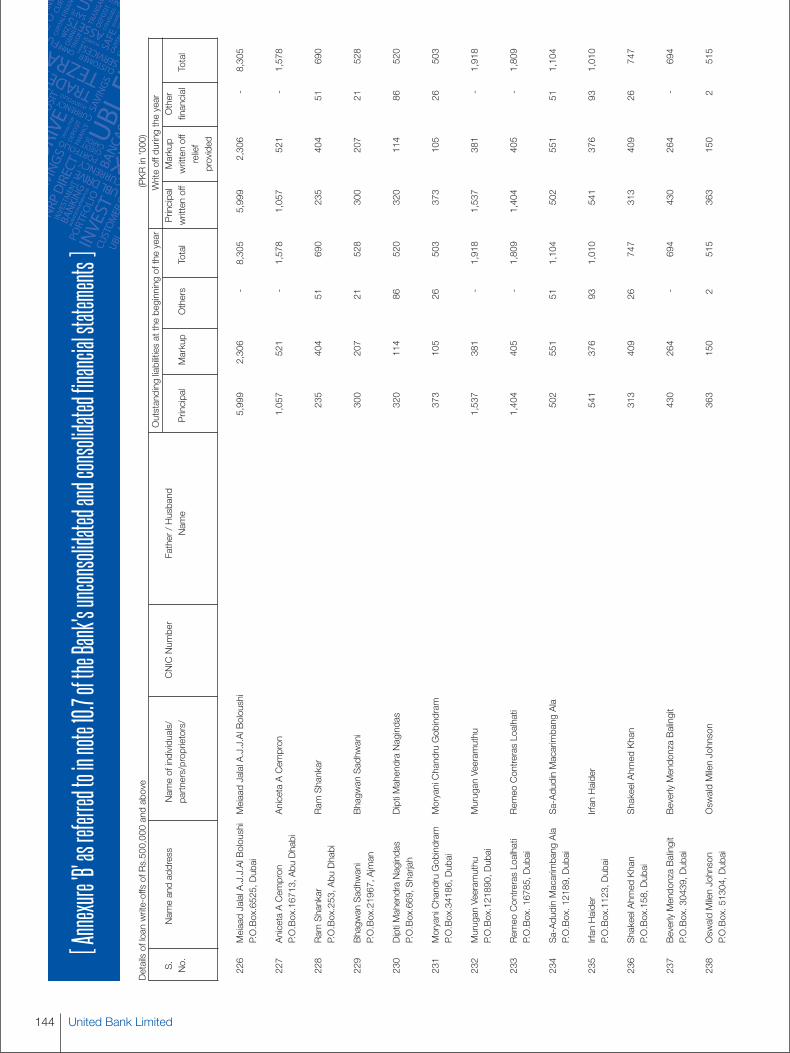

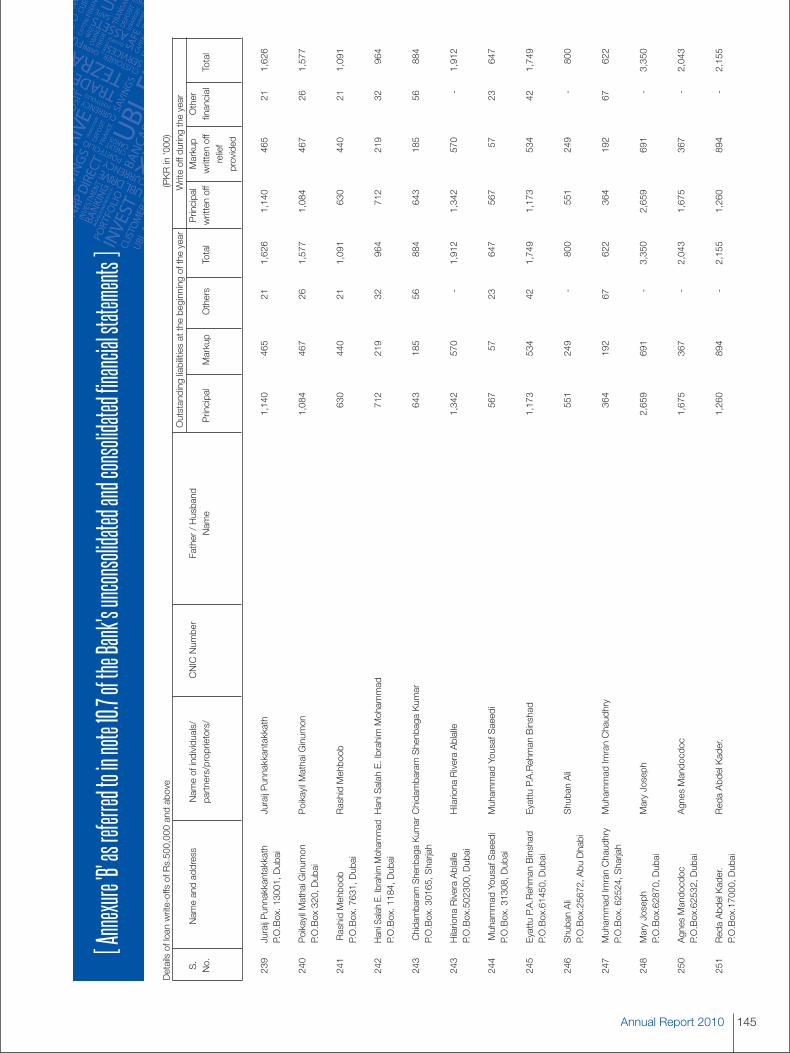

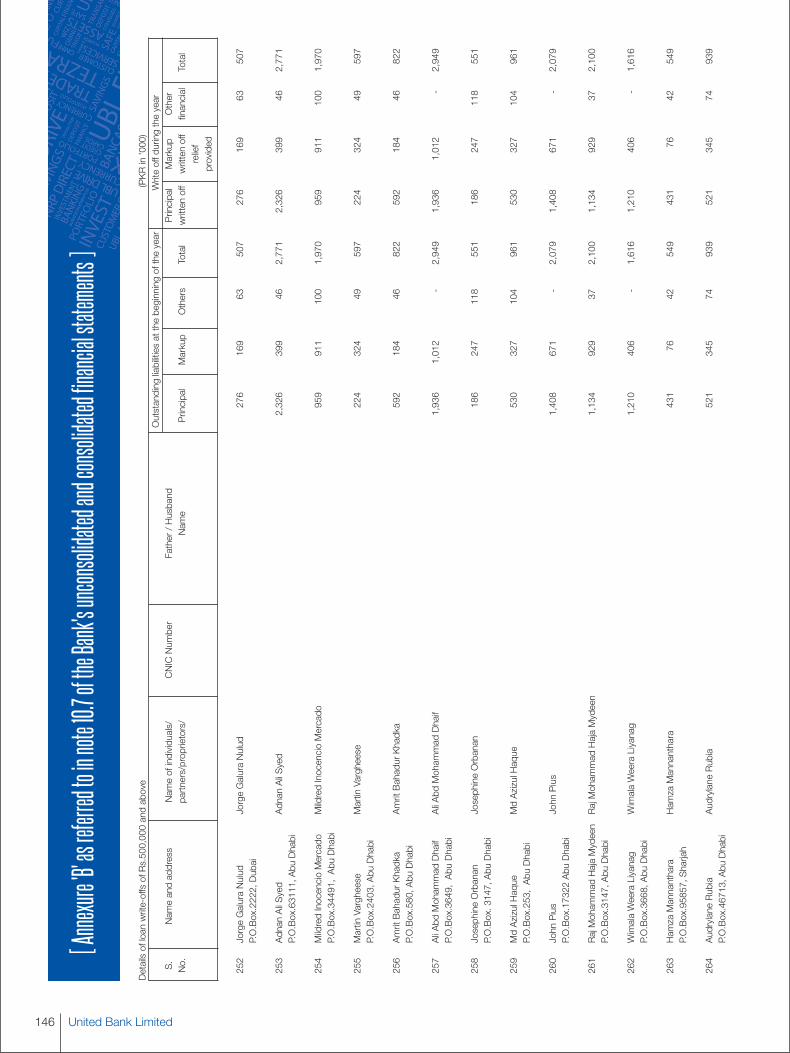

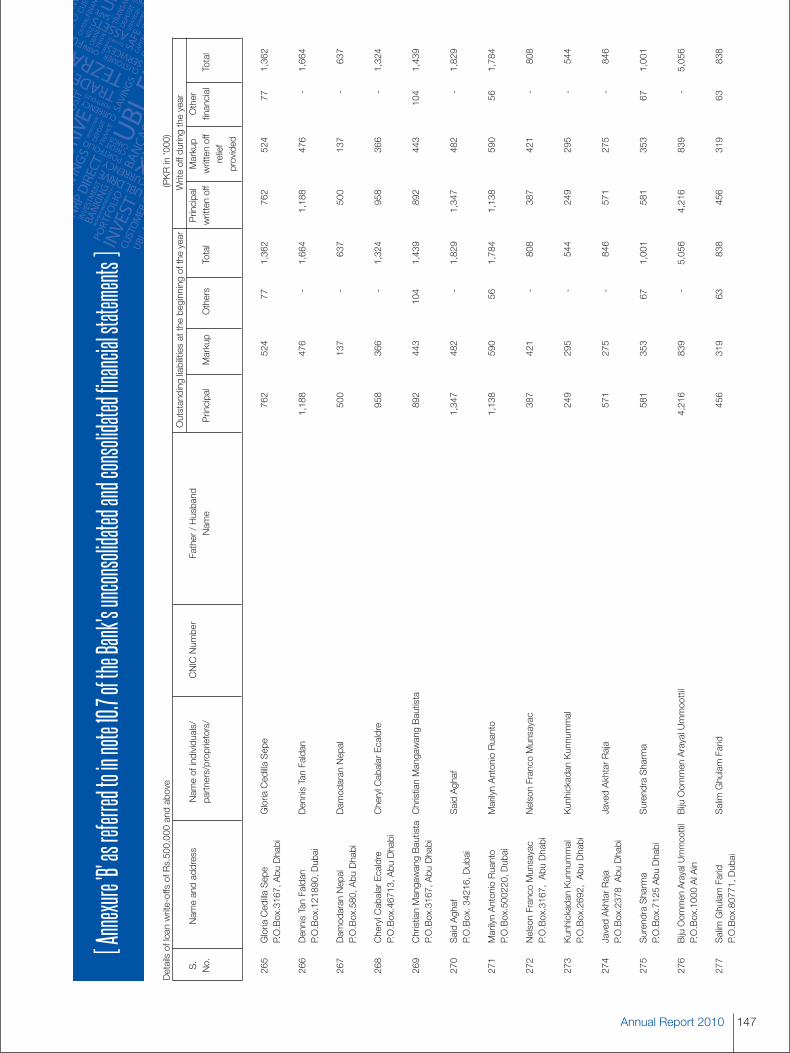

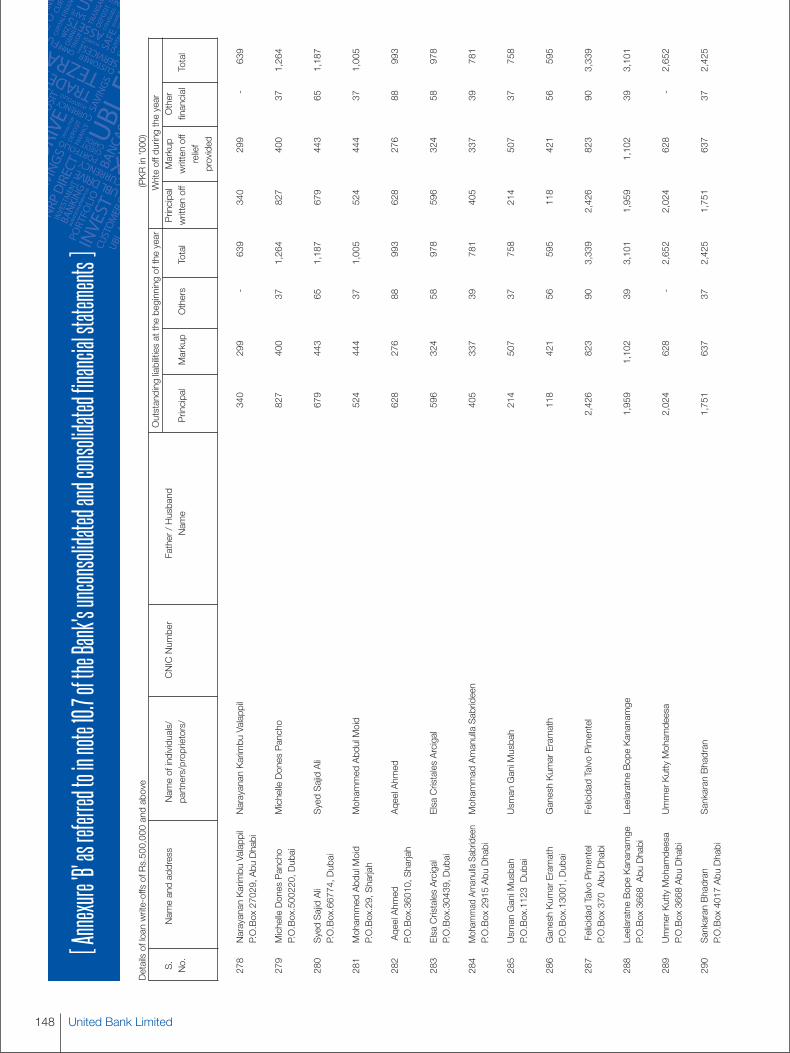

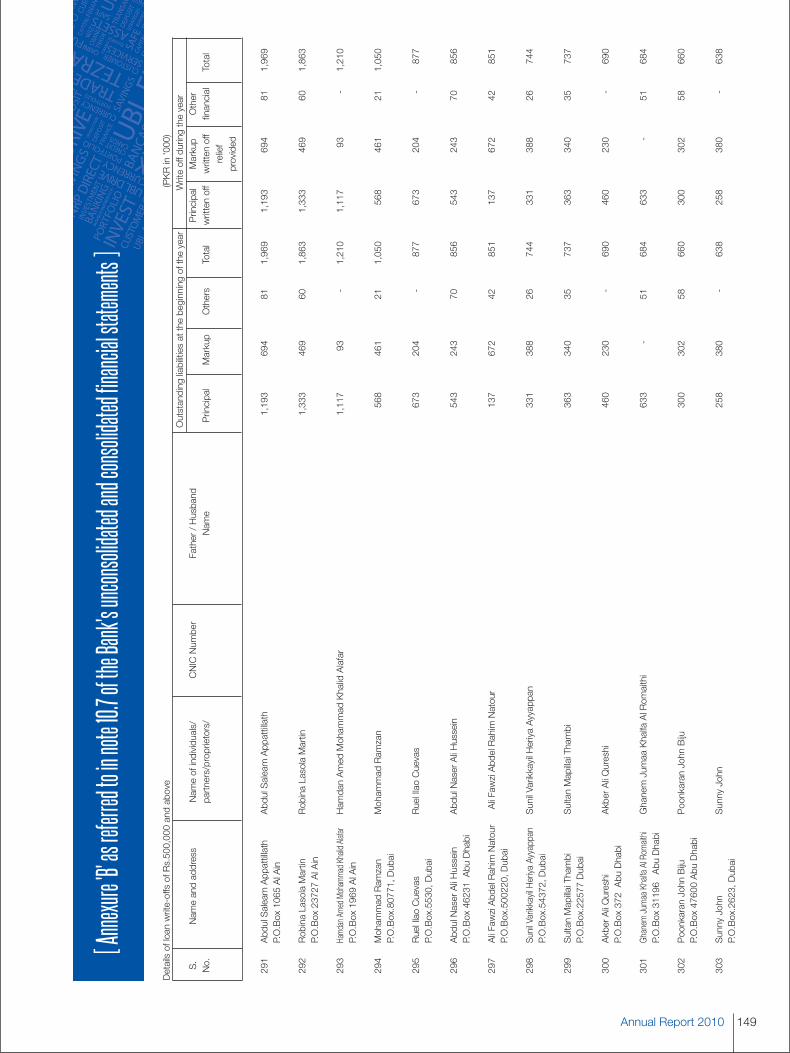

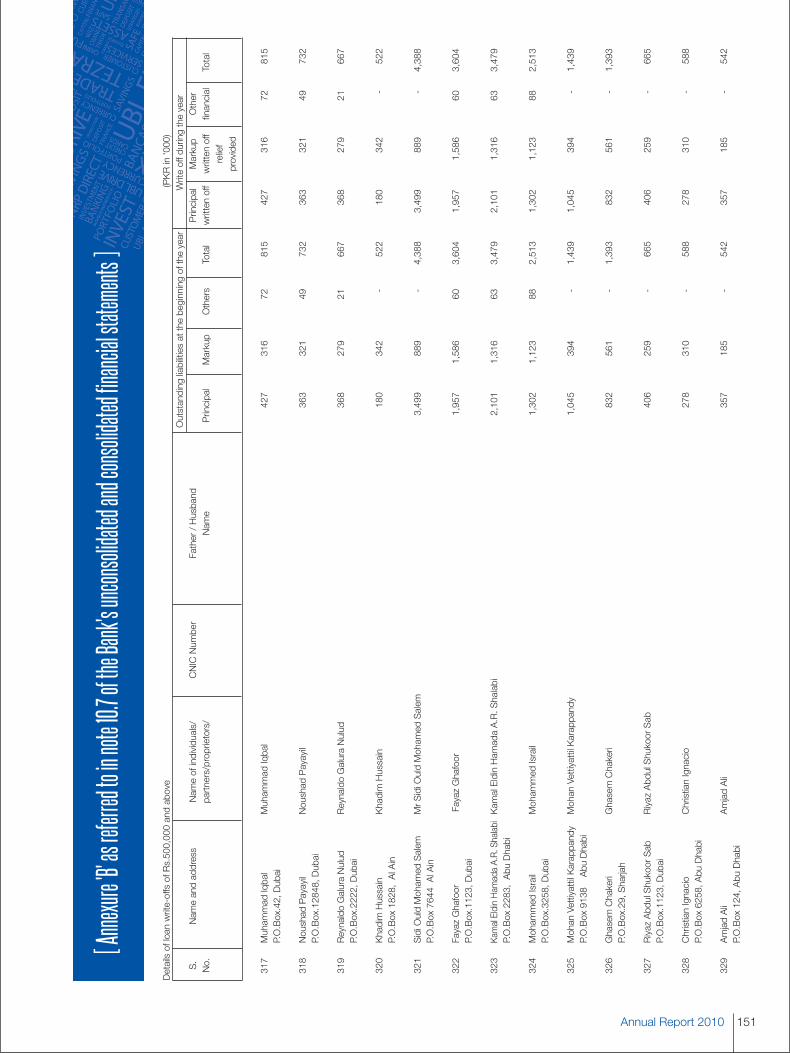

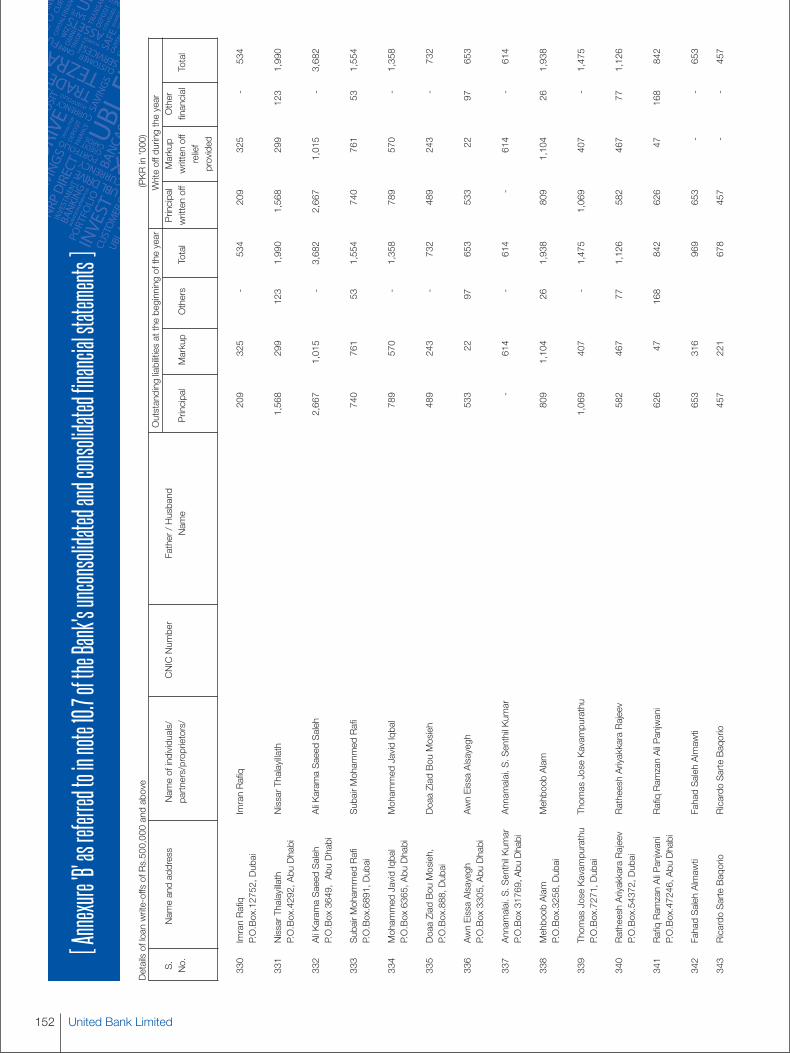

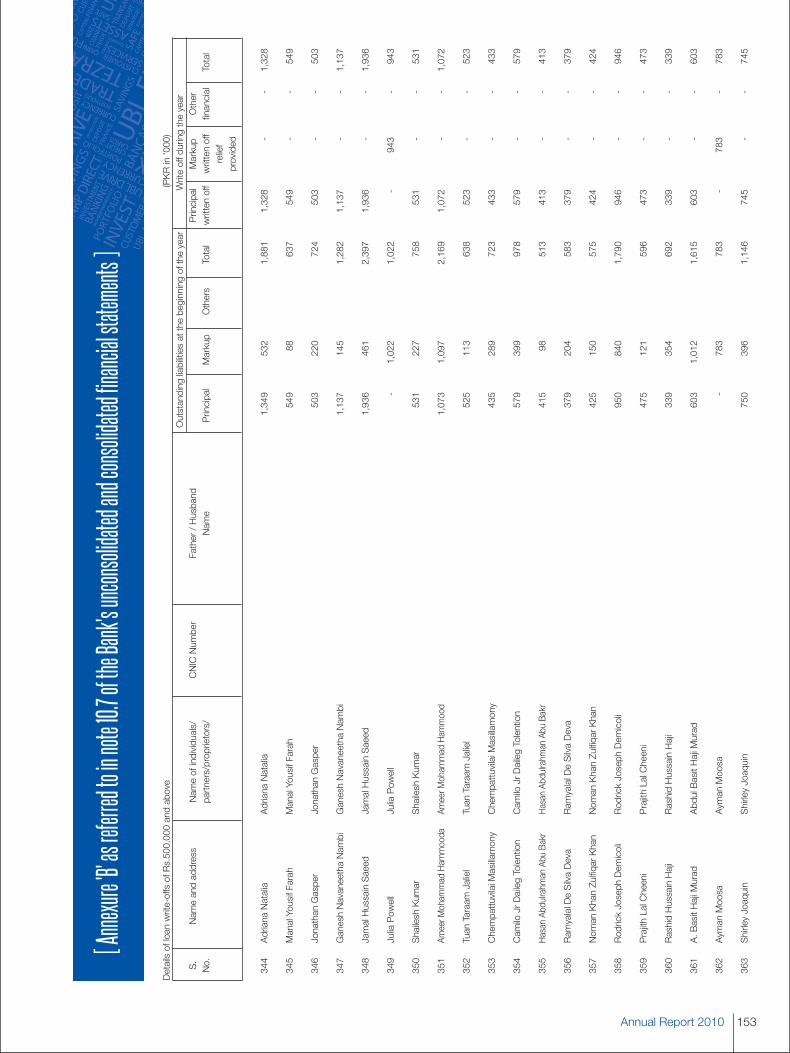

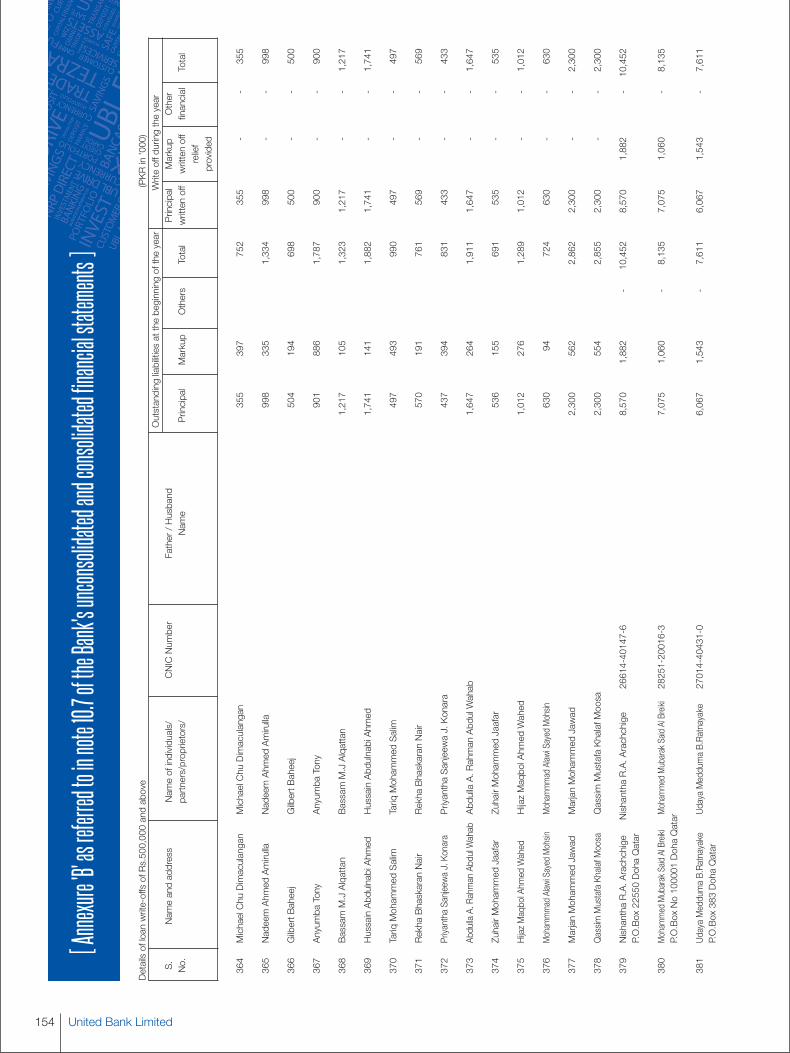

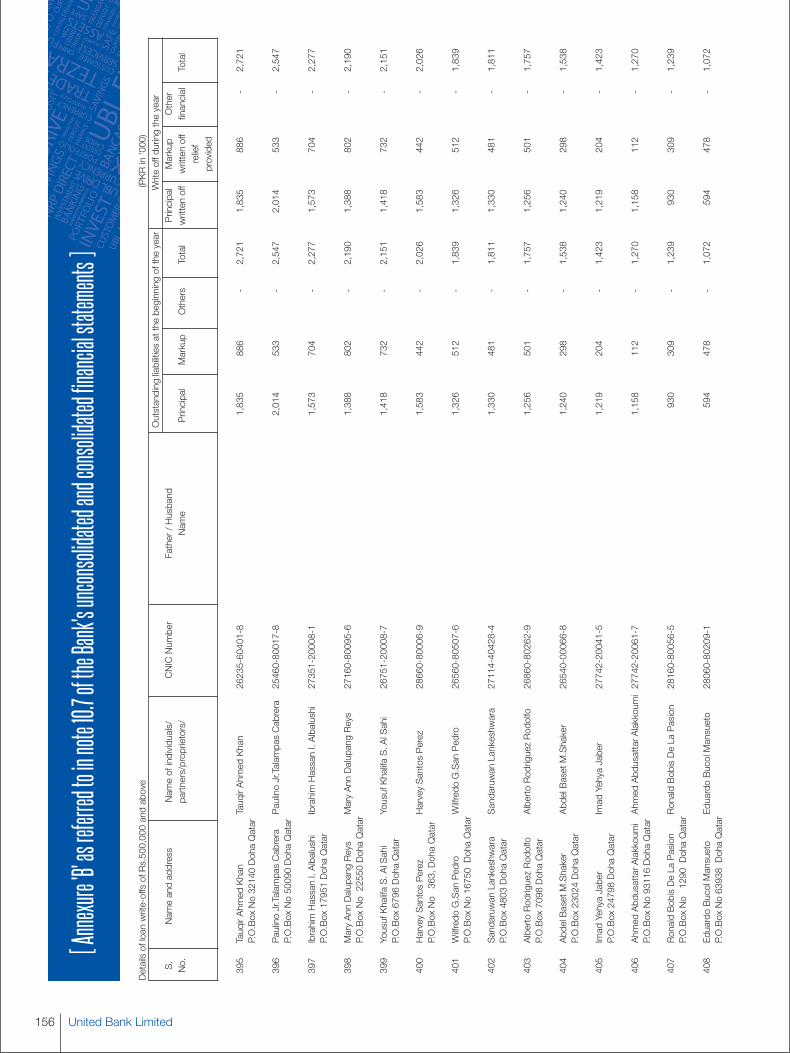

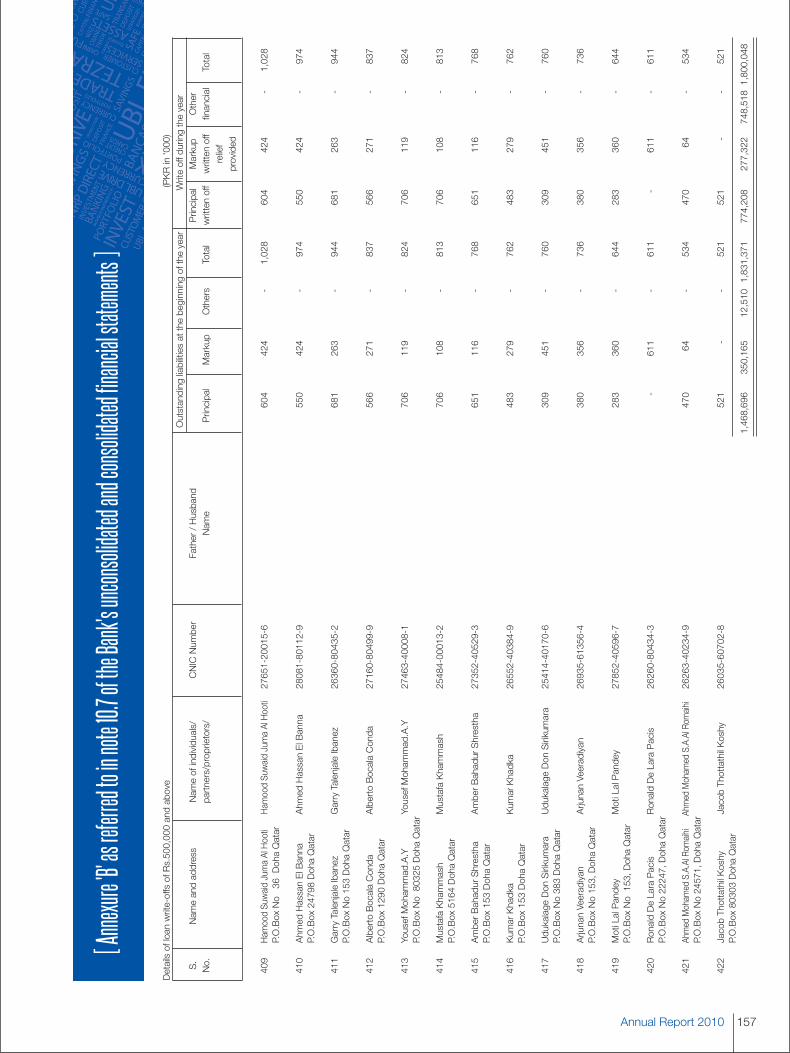

Annexure ‘B’ as referred to in note 10.7 of the Bank's unconsolidated and consolidated financial statements

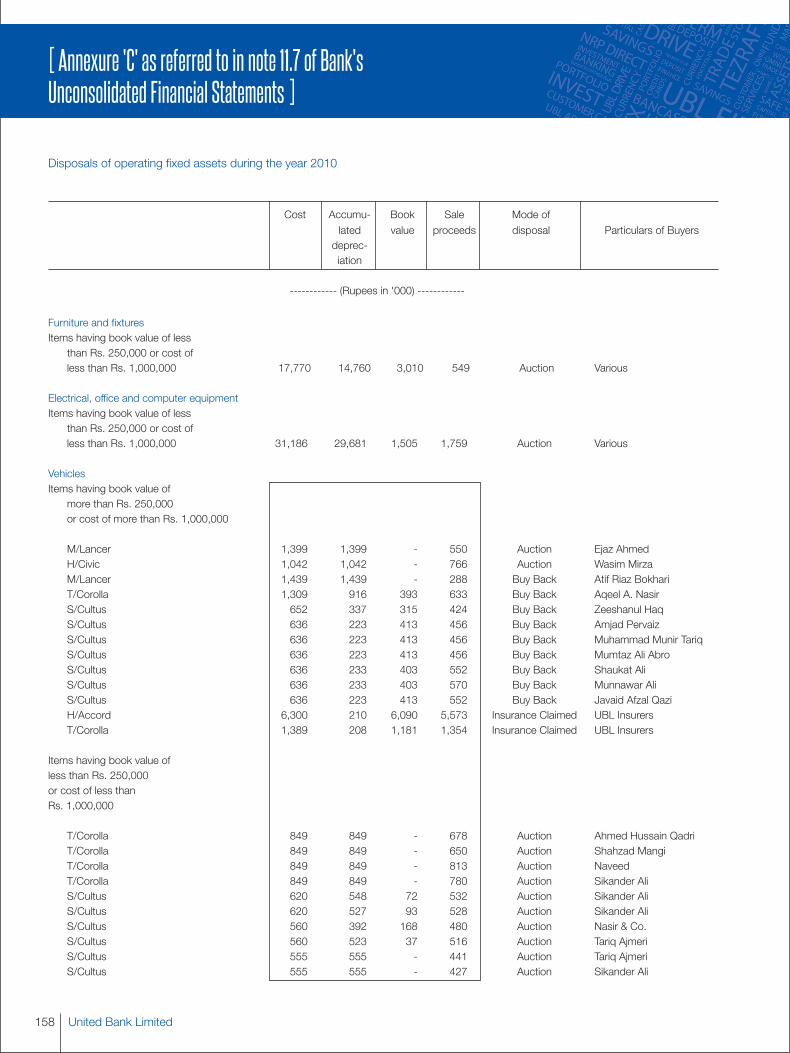

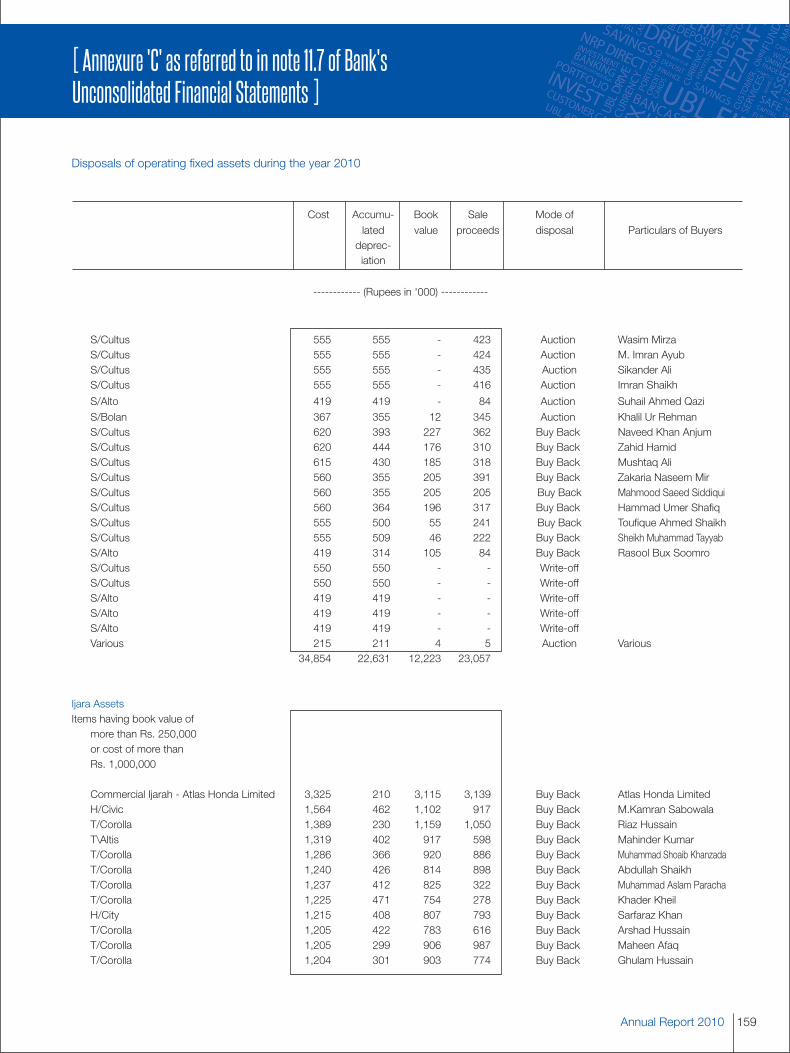

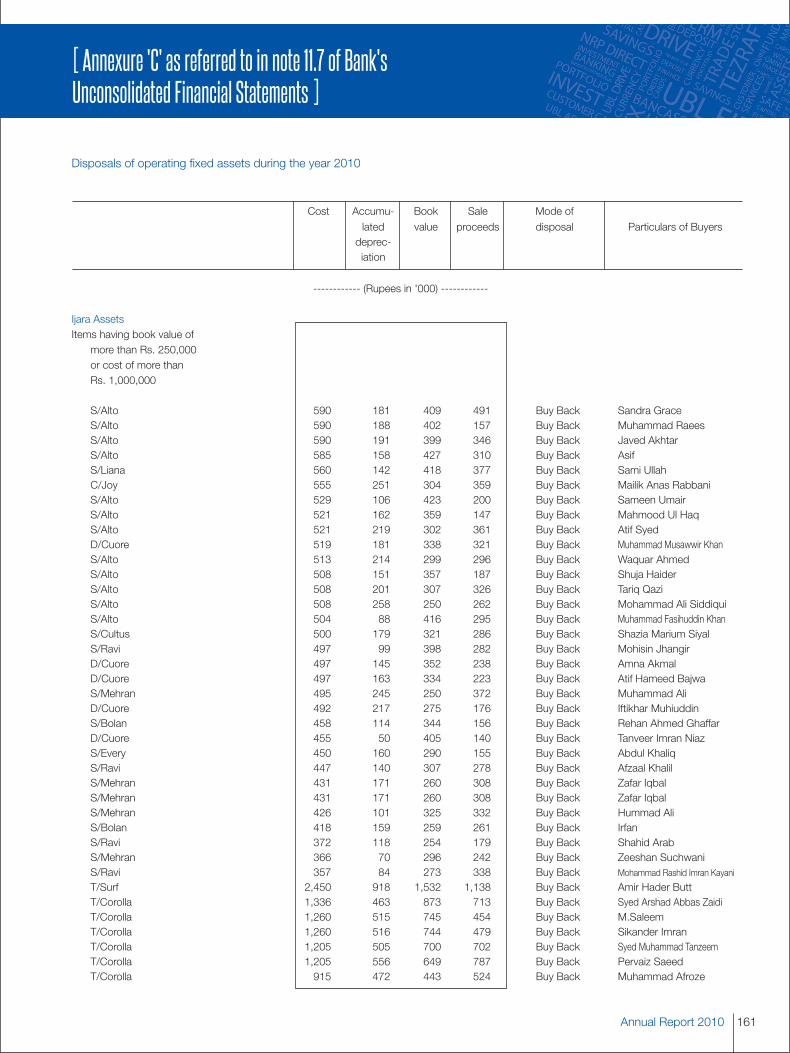

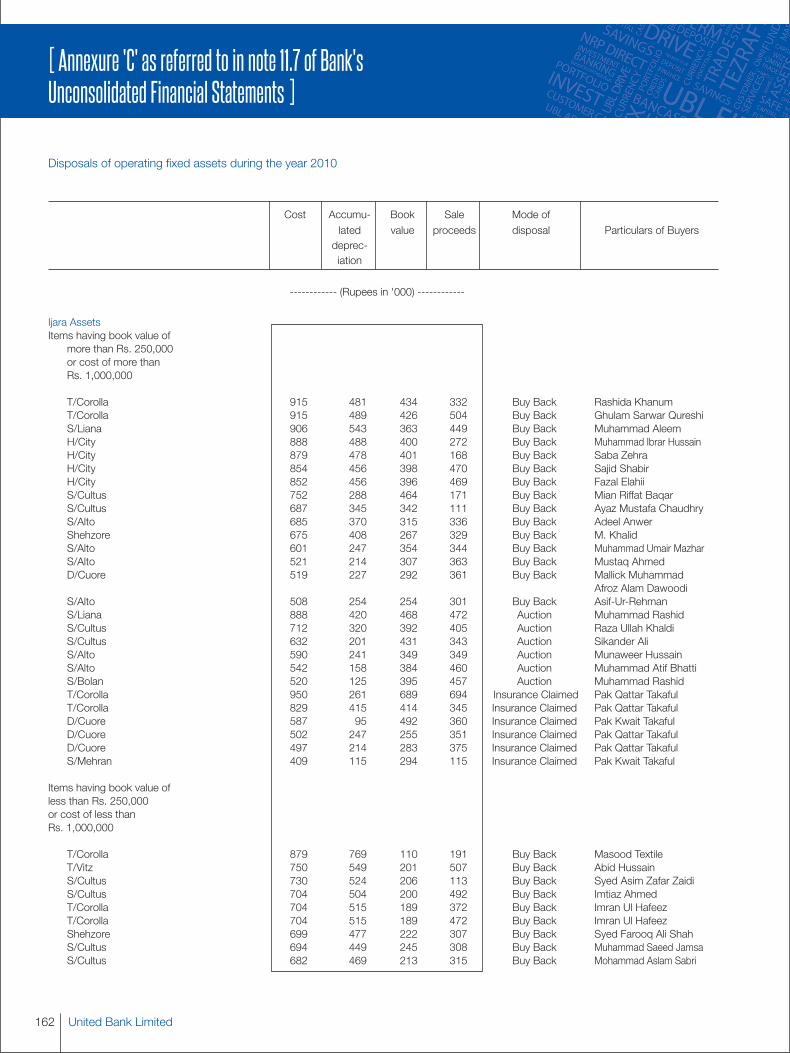

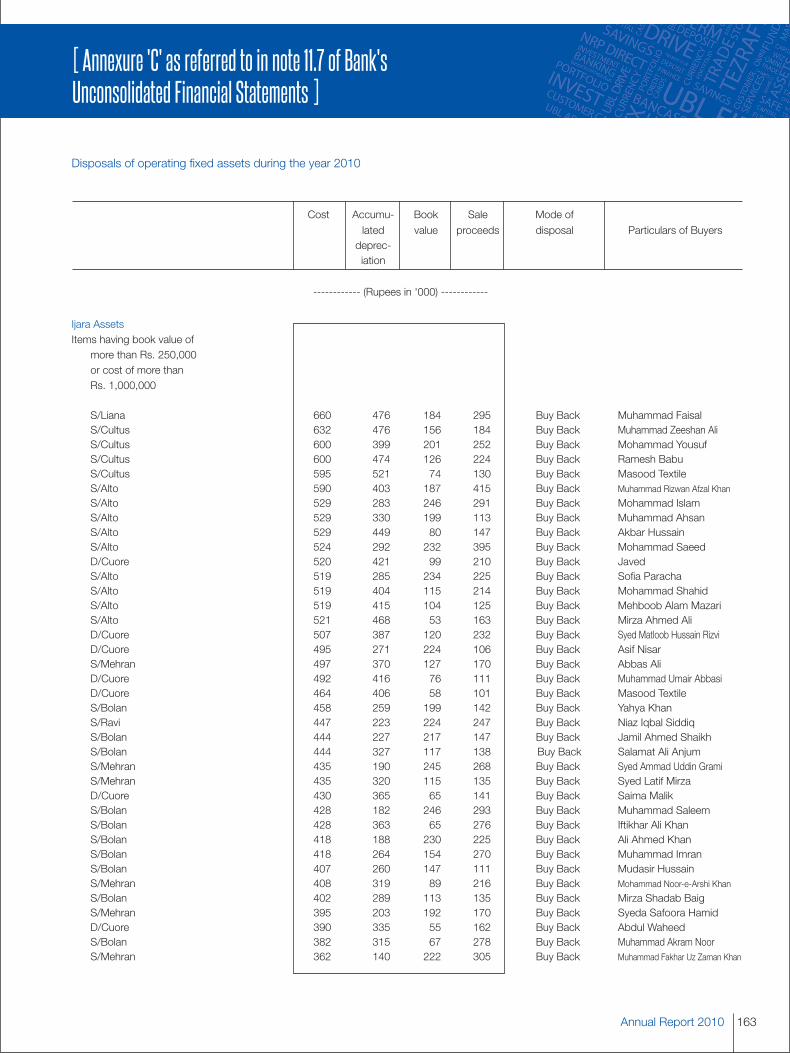

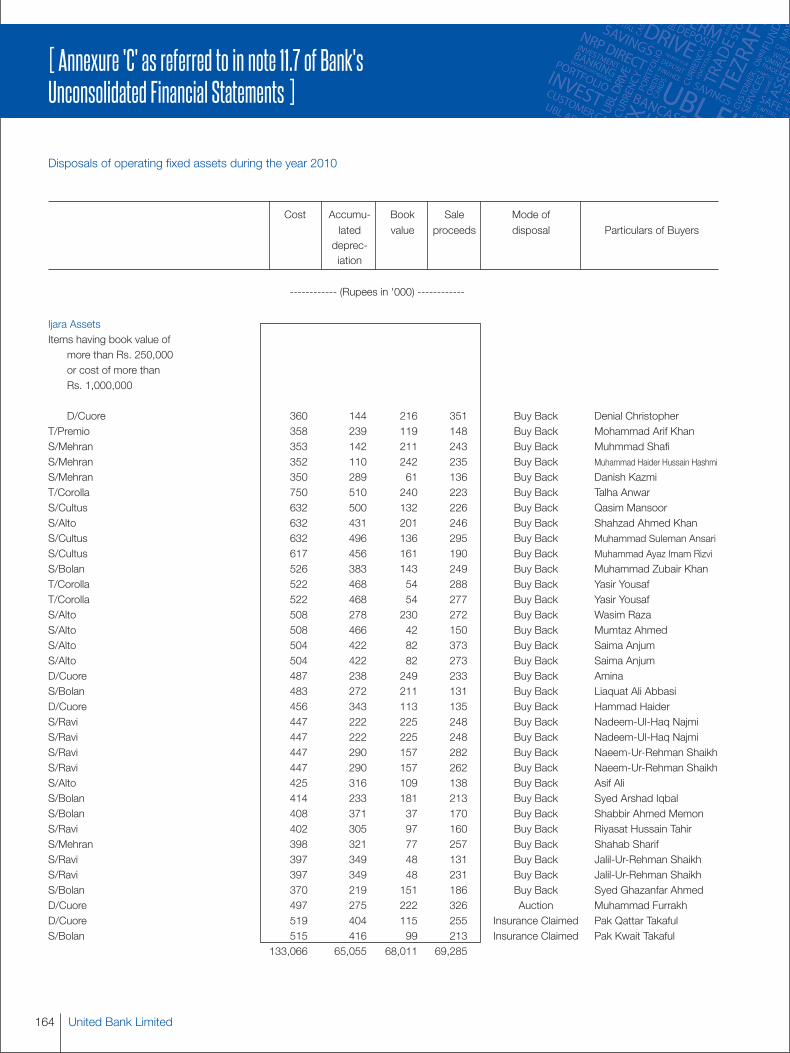

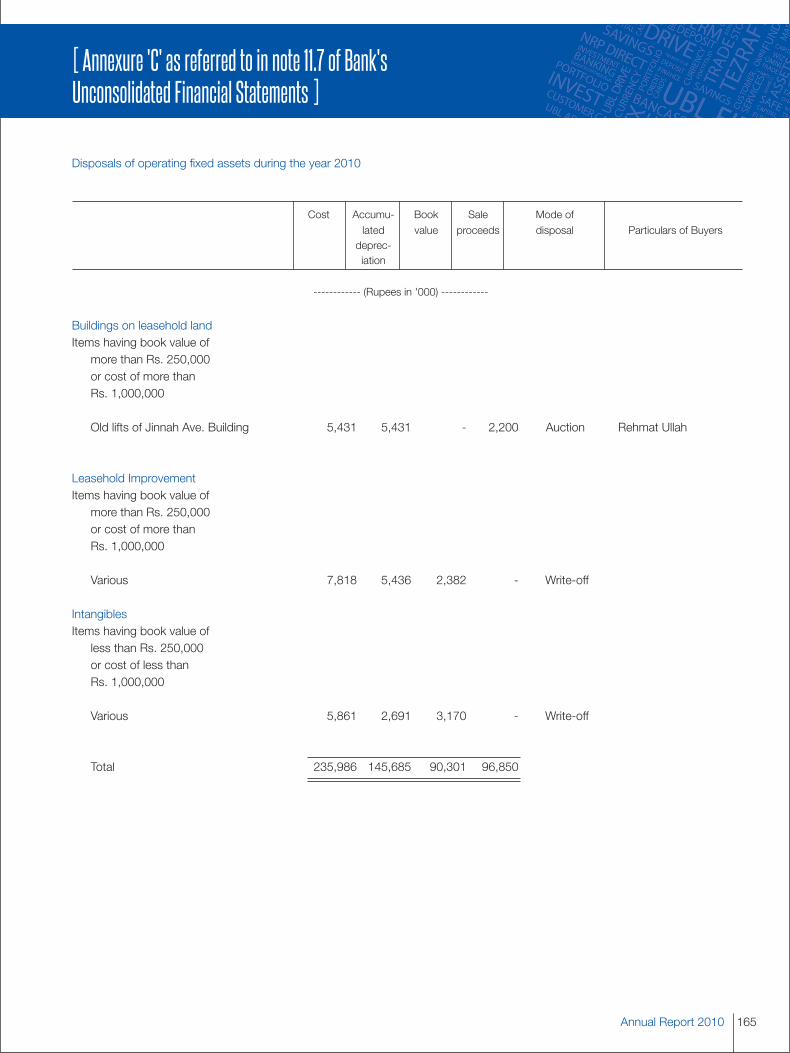

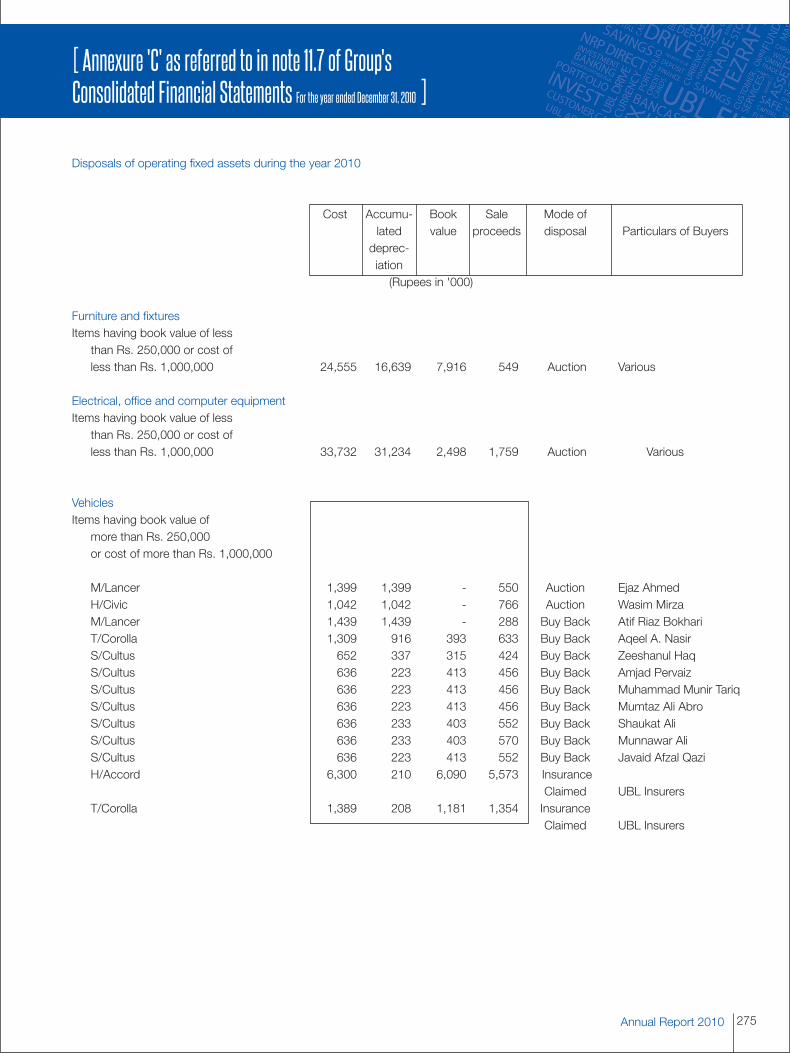

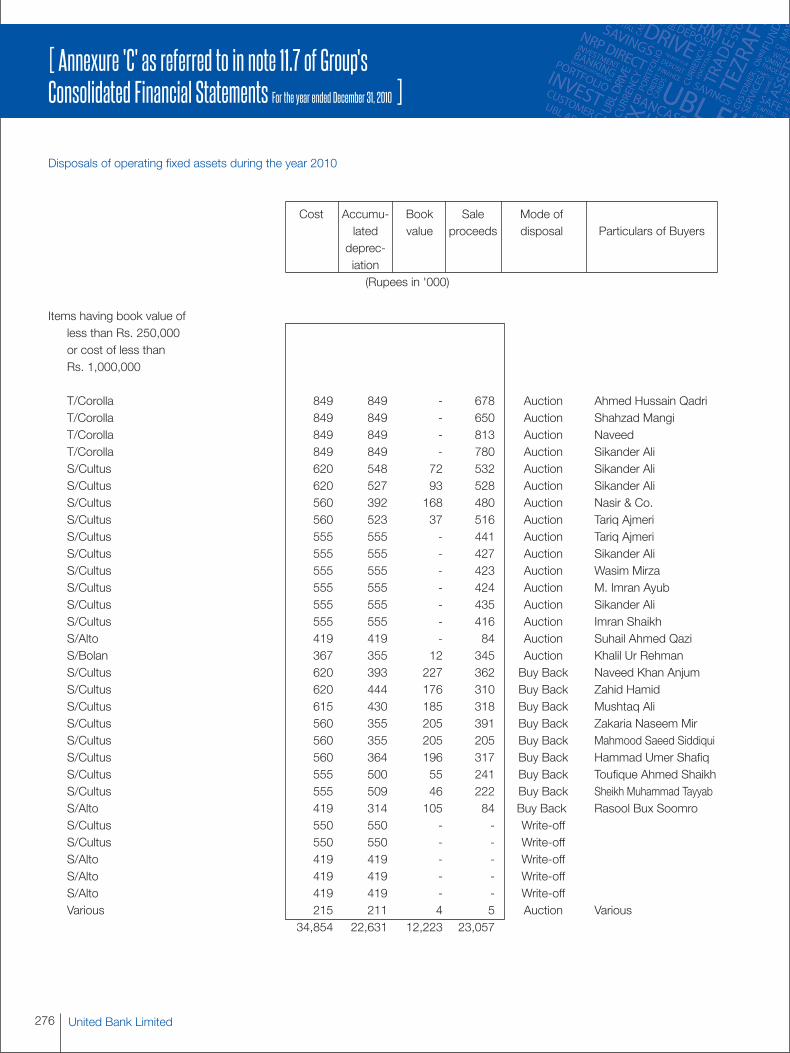

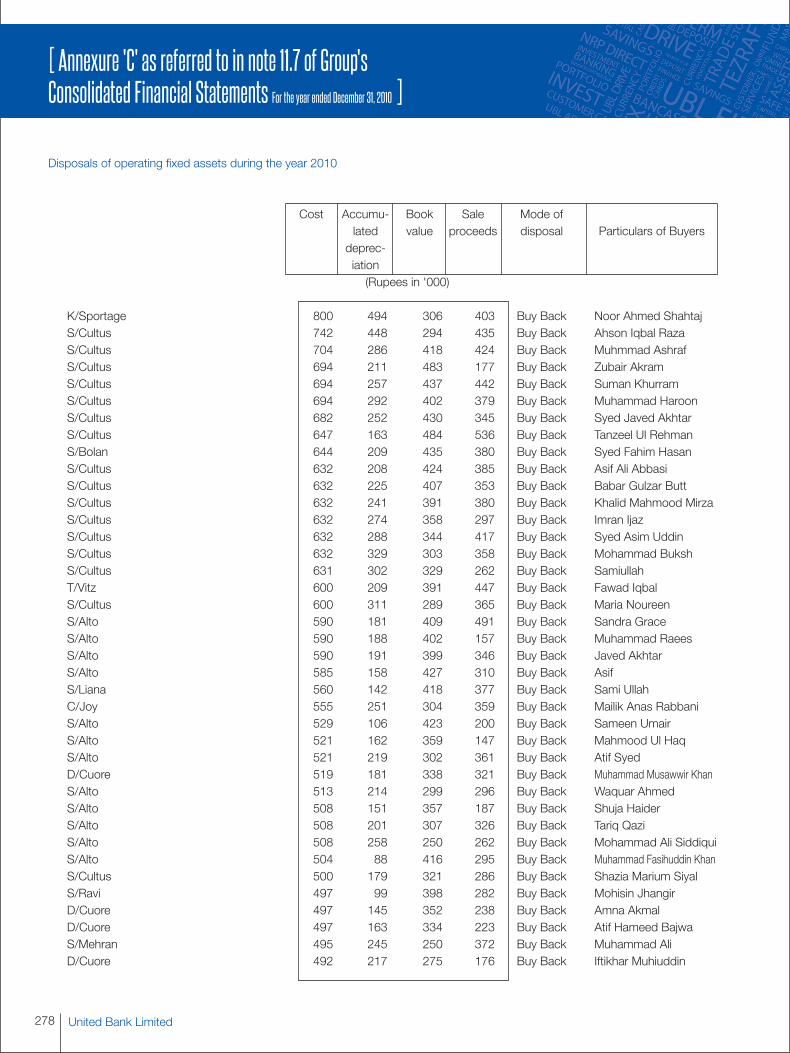

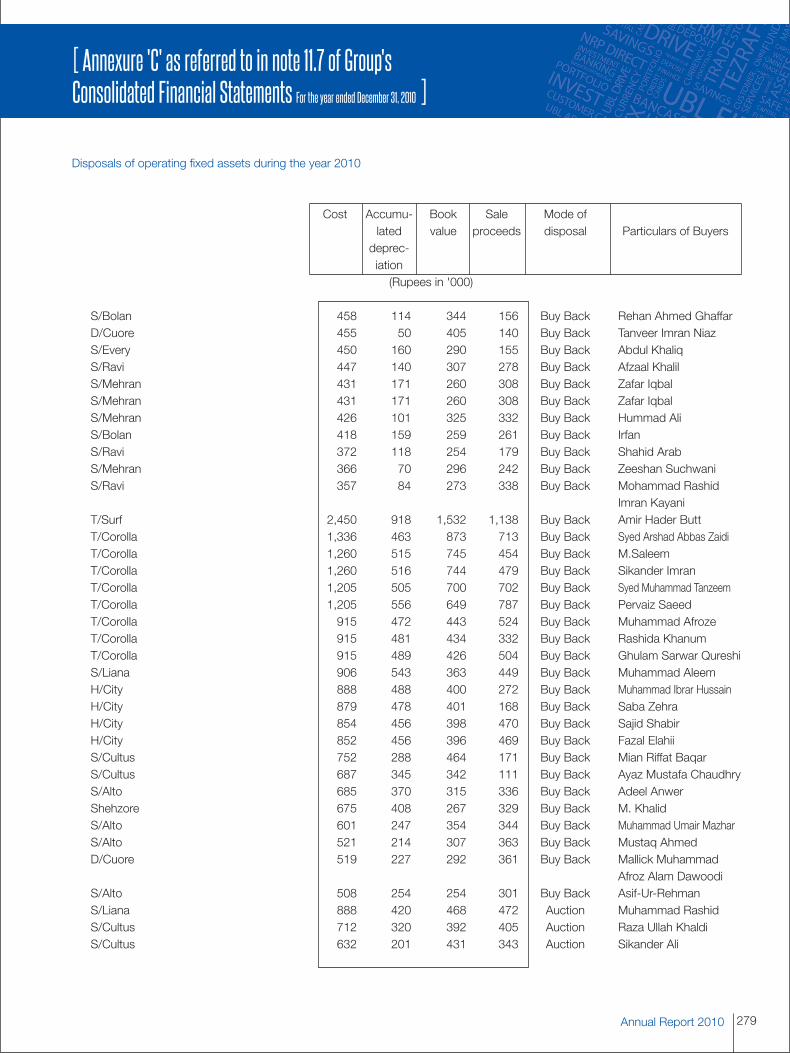

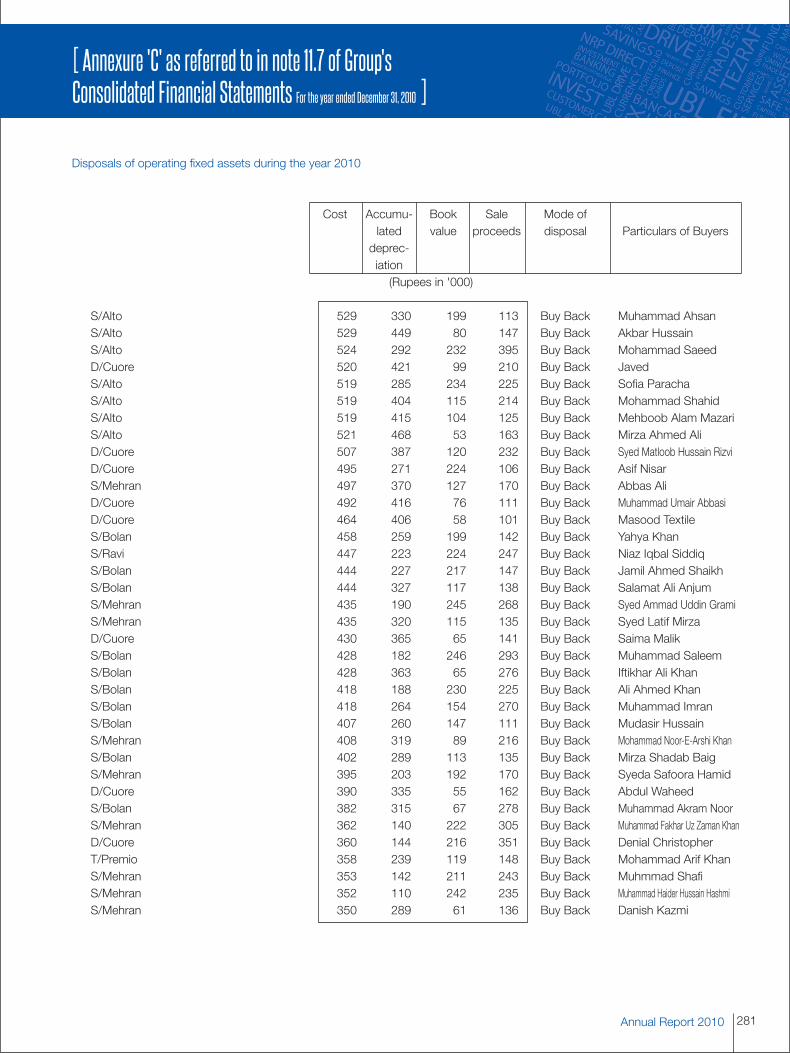

Annexure ‘C’ as referred to in note 11.7 of Bank’s Unconsolidated Financial Statements

Annexure ‘D’ of the Bank's Unconsolidated Financial Statements

Auditors’ Report to the Members

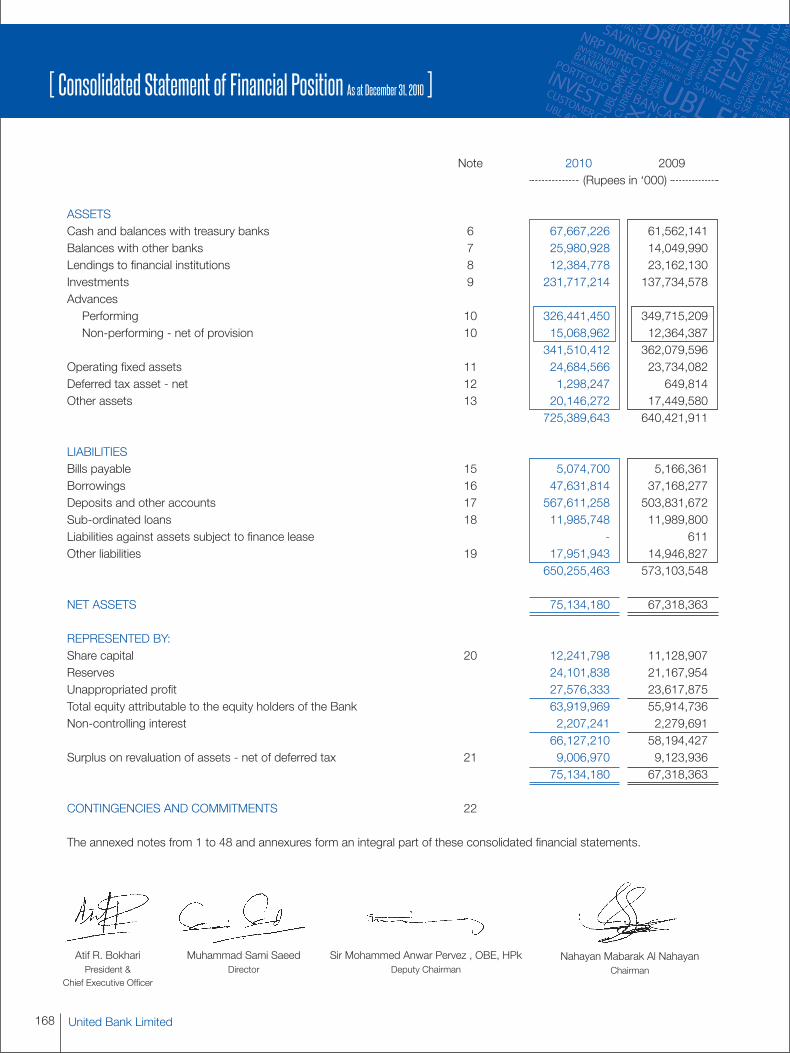

Consolidated Statement of Financial Position

Consolidated Profit & Loss Account

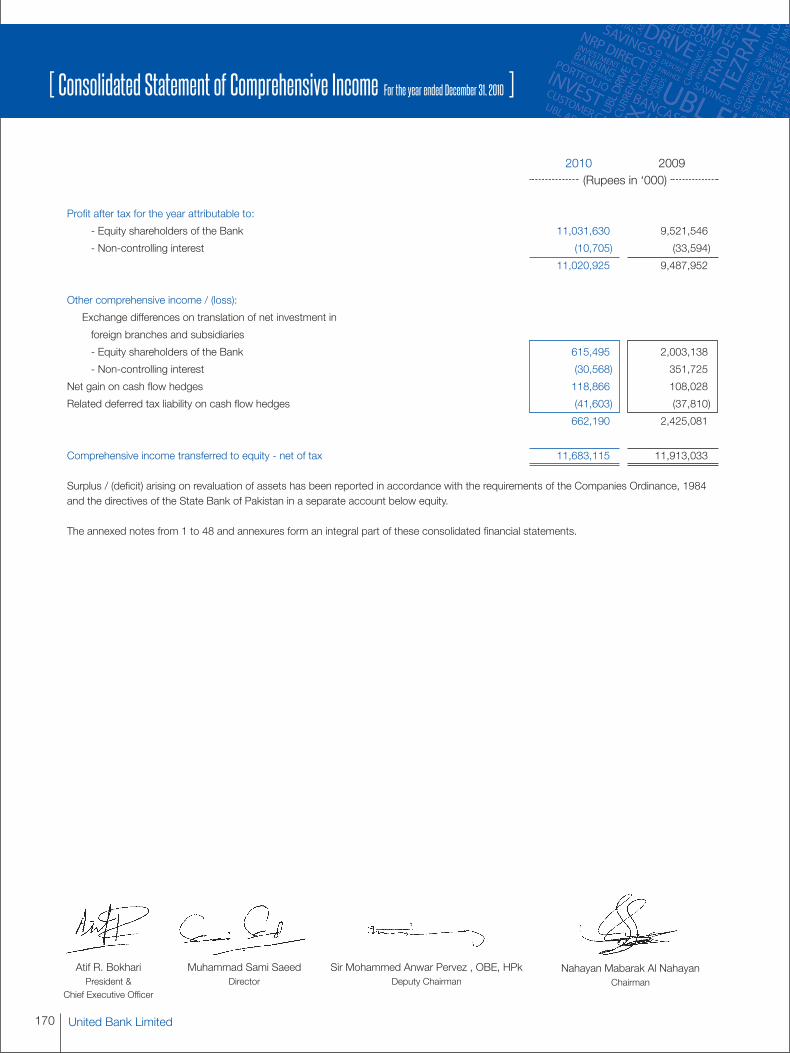

Consolidated Statement of Comprehensive Income

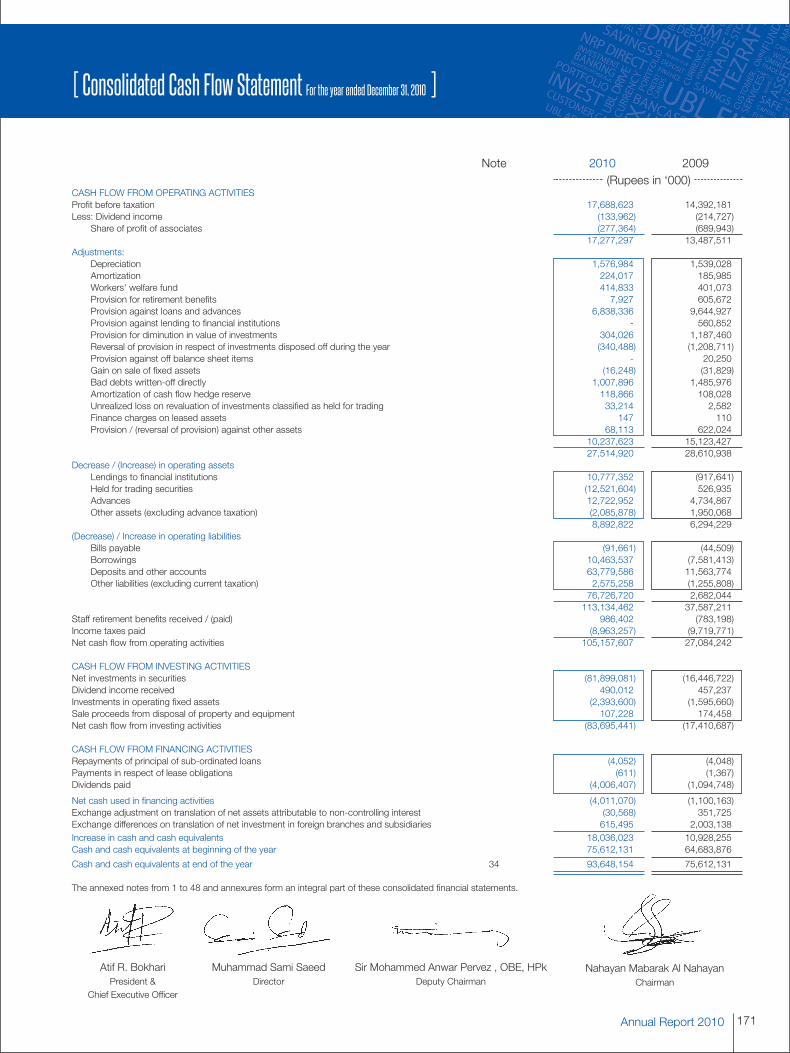

Consolidated Cash Flow Statement

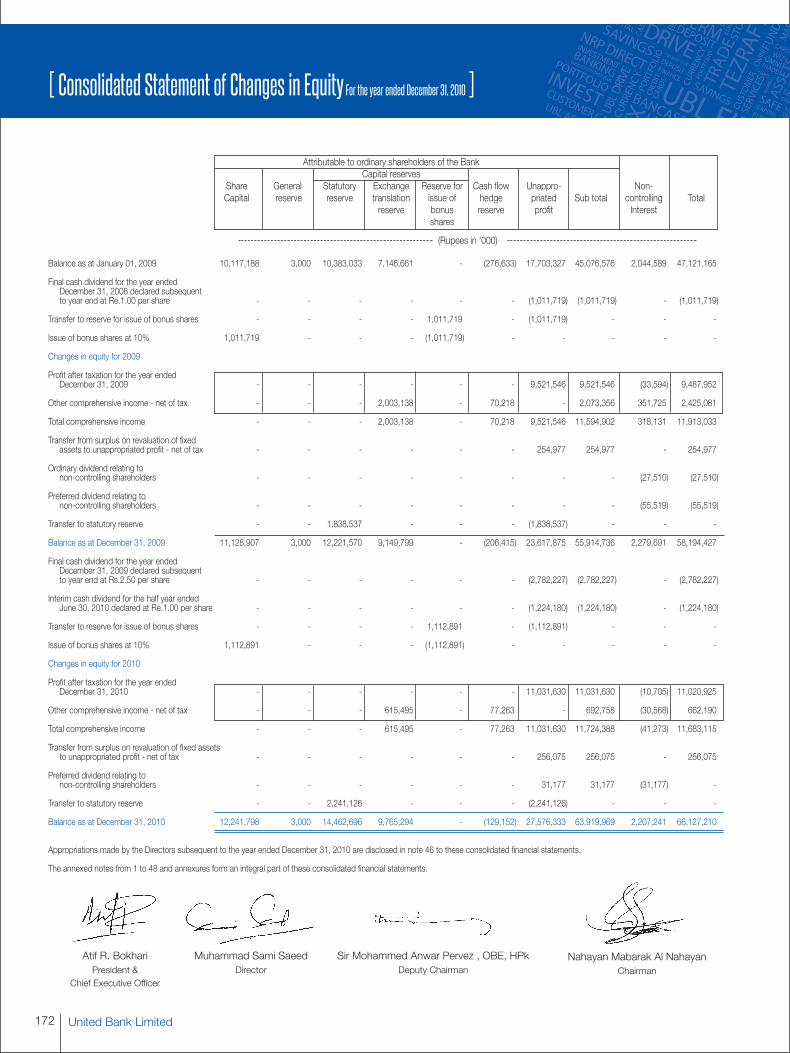

Consolidated Statement of Changes in Equity

Notes to and forming part of the Consolidated Financial Statements

Annexure 'A' as referred to in note 9.8 of Group's Consolidated Financial Statements

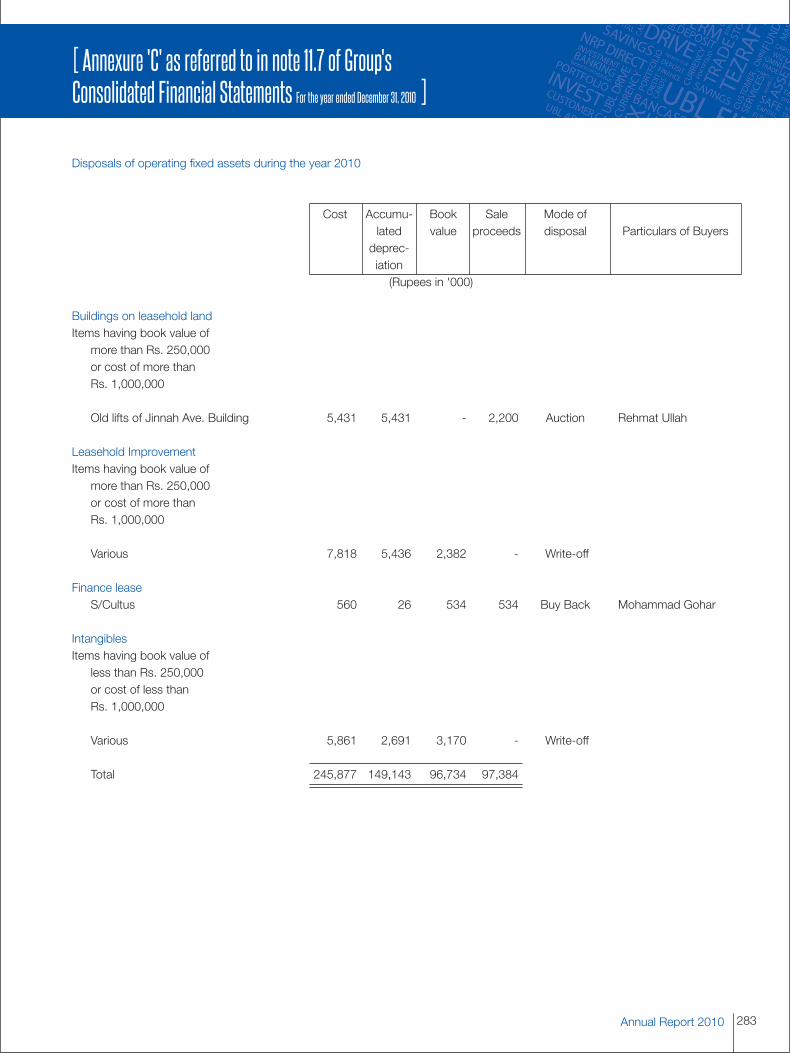

Annexure 'C' as referred to in note 11.7 of Group's Consolidated Financial Statements

Annexure 'D' of Group's Consolidated Financial Statements

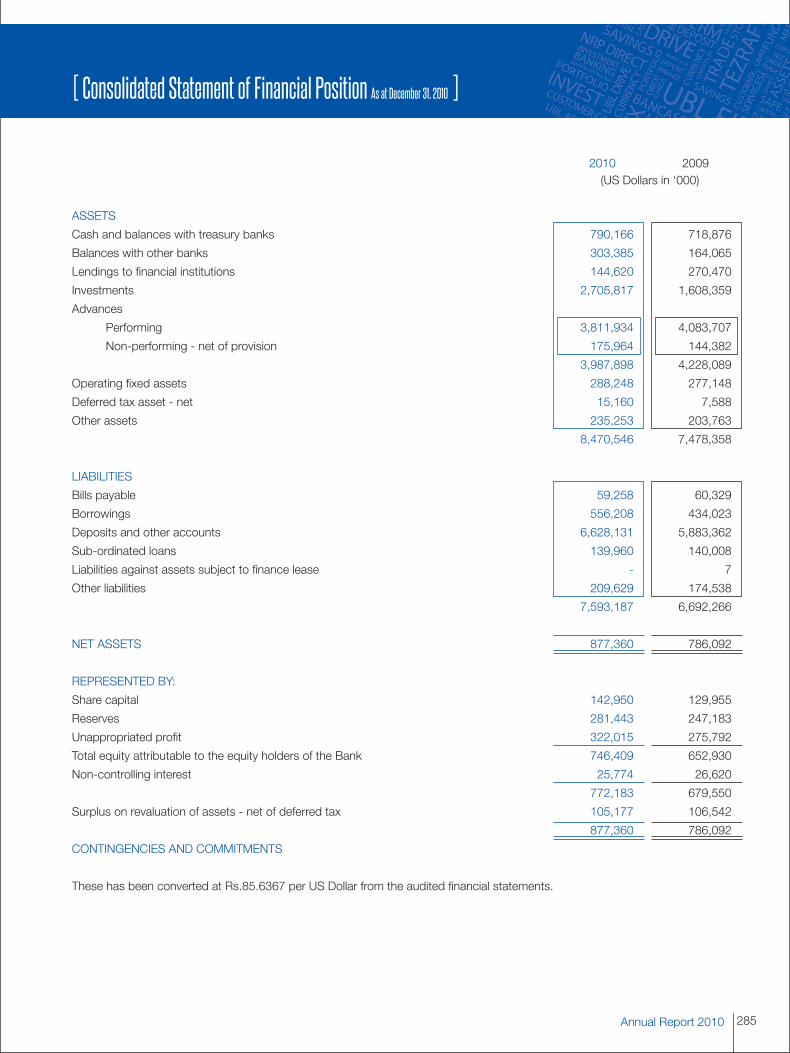

Consolidated Statement of Financial Position (in US Dollars)

Consolidated Profit and Loss Account (in US Dollars)

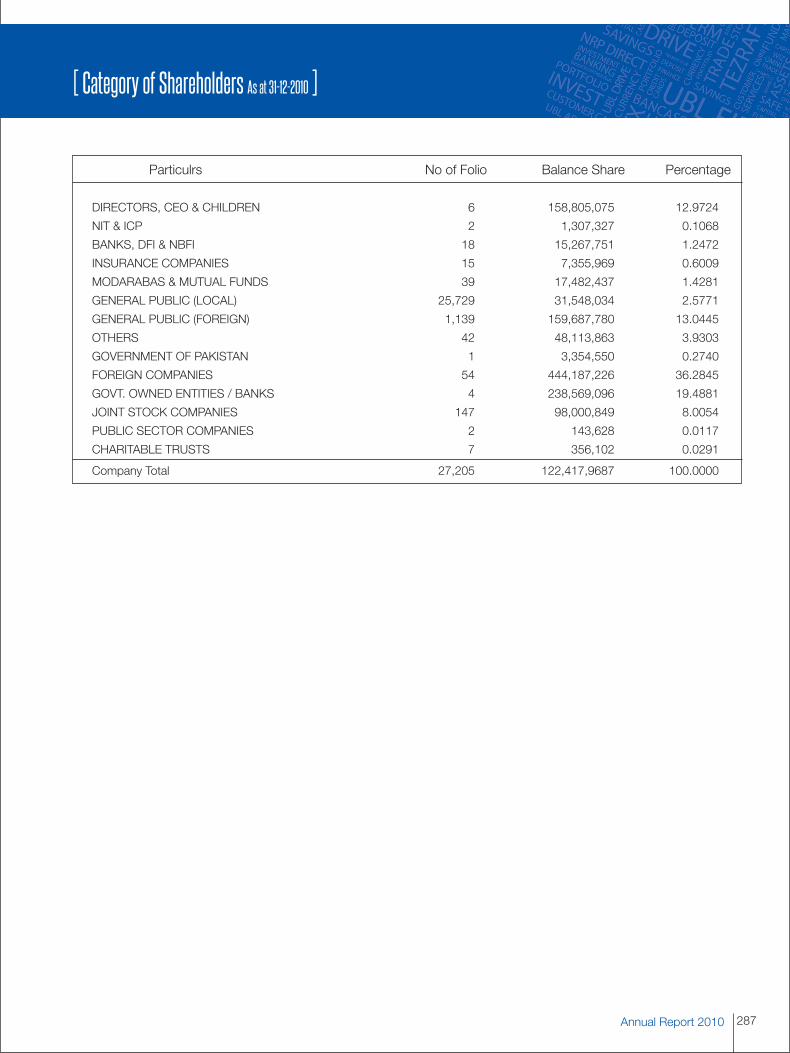

Categories of Shareholders

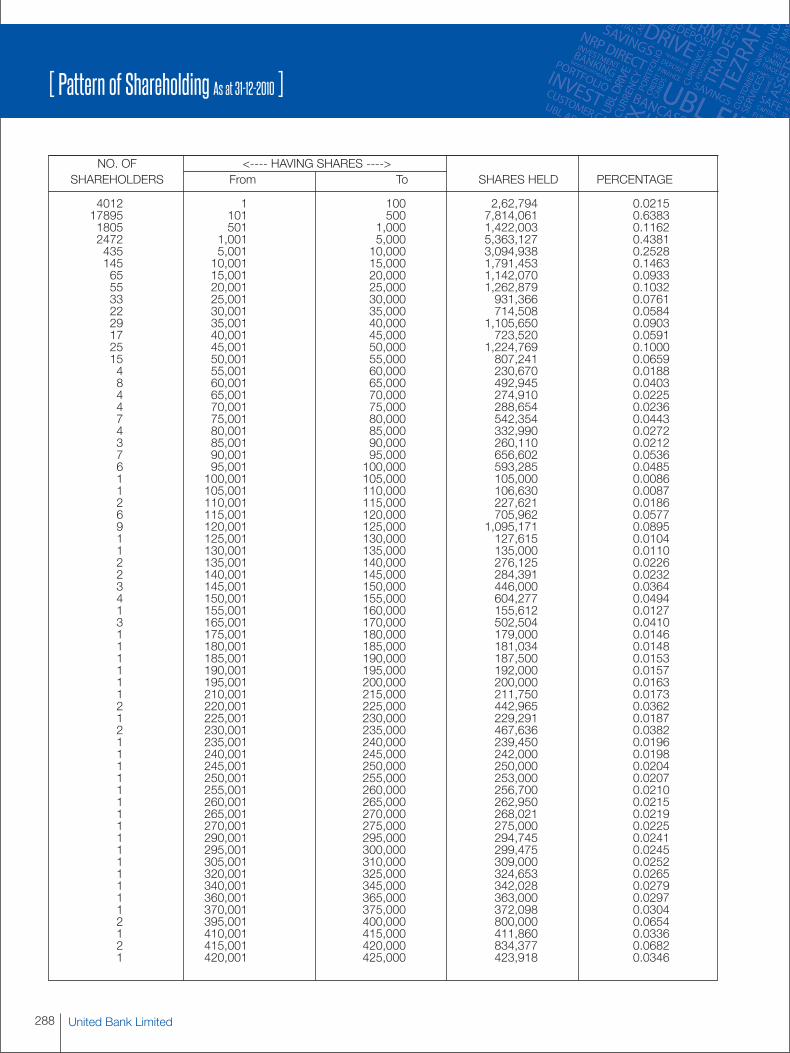

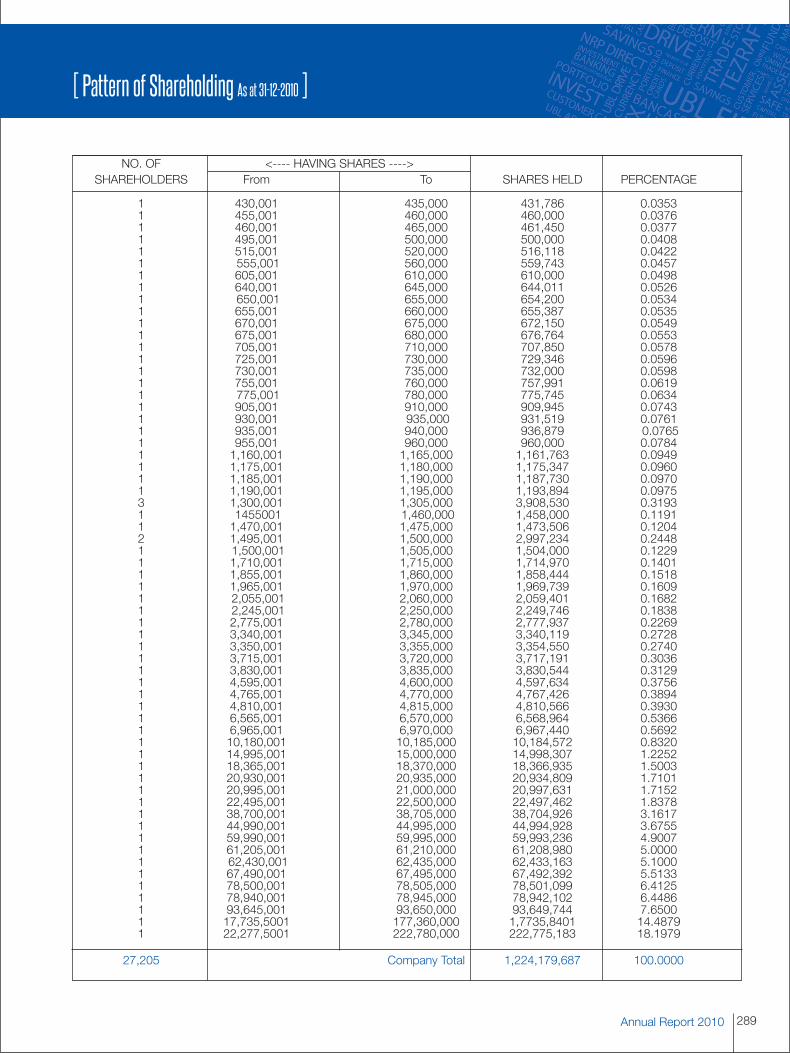

Pattern of Shareholding

Notice of 51st Annual General Meeting

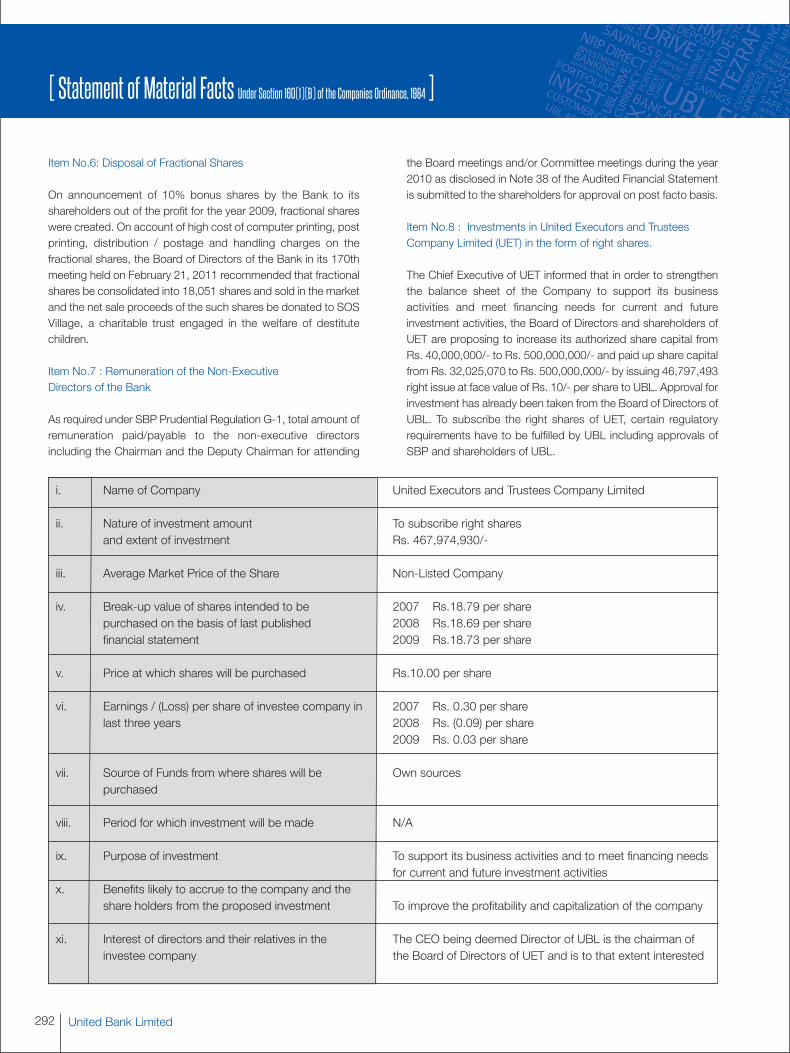

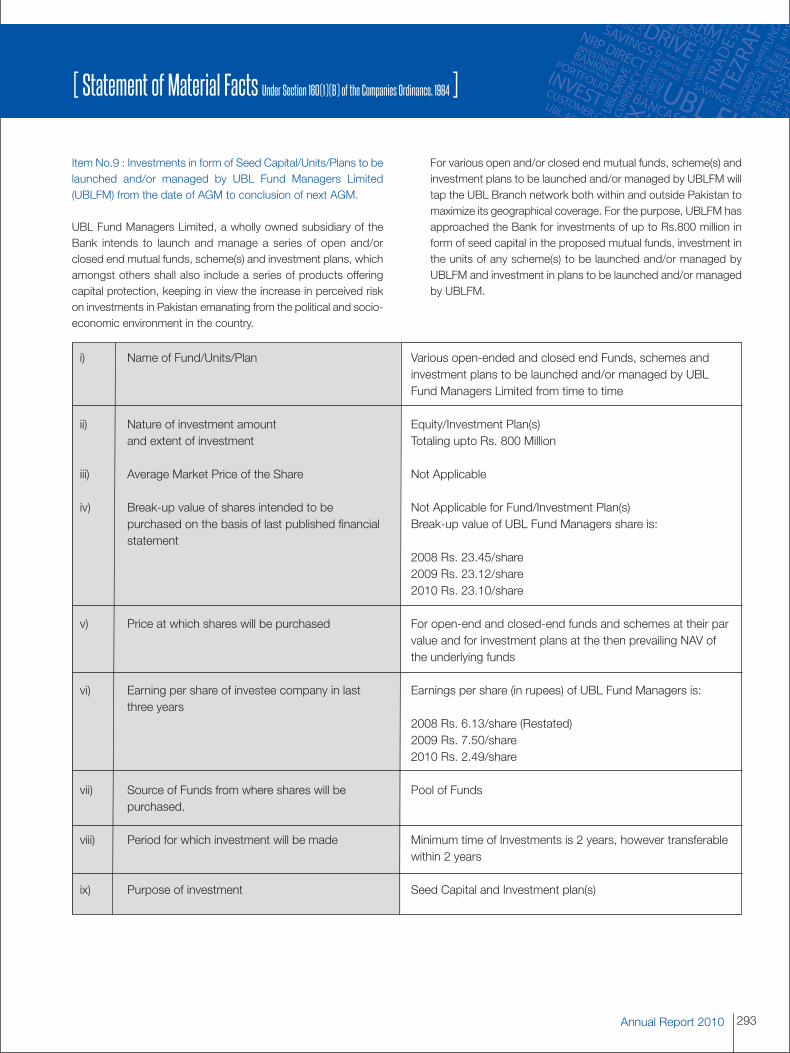

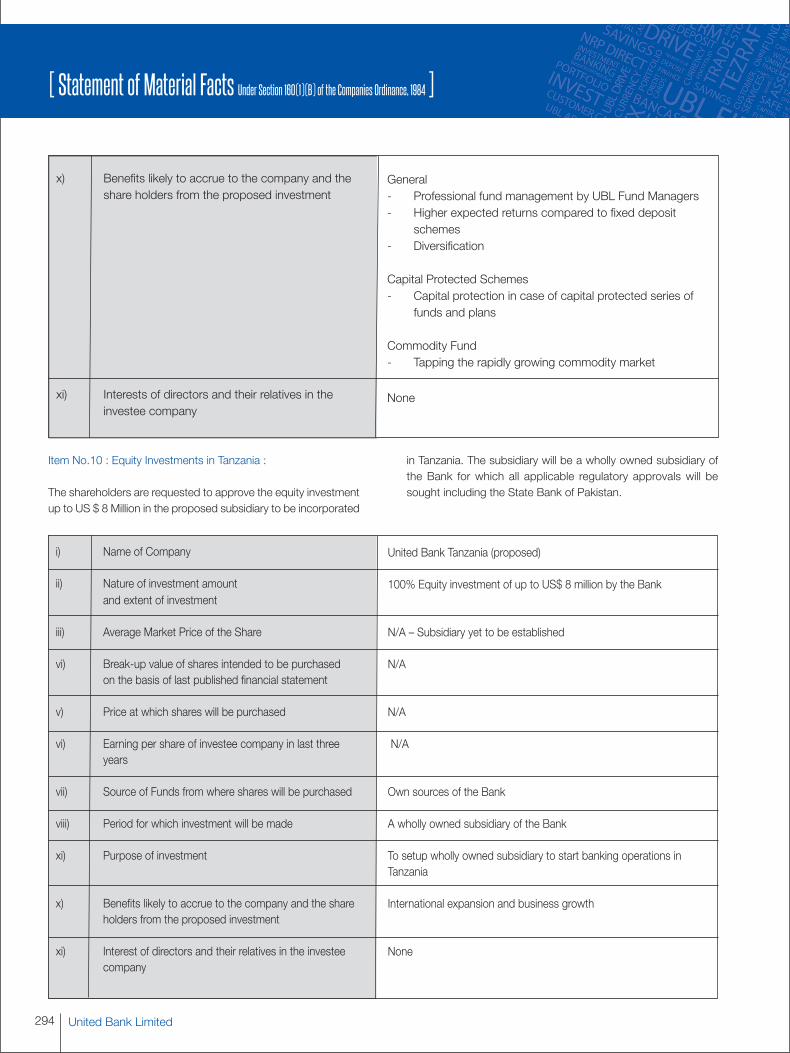

Statement of Material Facts

Form of Proxy

02

03

06

12

13

17

21

23

25

26

27

29

30

31

32

33

34

35

114

122

158

166

167

168

169

170

171

172

173

264

275

284

285

286

287

288

290

292

United Bank Limited02

Board of DirectorsHis Highness Sheikh Nahayan Mabarak Al NahayanChairman

Sir Mohammed Anwar Pervez, OBE, HPkDeputy Chairman

Mr. Omar Z. Al AskariDirector

Mr. Zameer Mohammed ChoudreyDirector

Mr. Muhammad Sami SaeedDirector

Mr. Seerat AsgharDirector

Mr. Amin UddinDirector

Mr. Arshad Ahmad MirDirector

Mr. Atif R. BokhariPresident & CEO

Committees of the Board

Board Audit CommitteeMr. Zameer Mohammed ChoudreyChairman

Mr. Muhammad Sami SaeedMember

Mr. Amin UddinMember

Mr. Aqeel Ahmed NasirSecretary

Board Human Resource &Compensation CommitteeMr. Omar Z. Al AskariChairman

Mr. Seerat AsgharMember

Mr. Atif R. BokhariMember

Mr. Jamal NasirSecretary

Board Risk Management CommitteeMr. Omar Z. Al AskariChairman

Mr. Arshad Ahmad MirMember

Mr. Atif R. BokhariMember

Mr. Ali SameerMember

[ Company Information ]

Chief Financial OfficerMr. Rayomond Kotwal

Company Secretary & Chief Legal CounselMr. Aqeel Ahmed Nasir

Registered Office13th Floor, UBL Building,Jinnah Avenue, Blue Area,Islamabad, Pakistan.

Head OfficeState Life Building No.1,I.I. Chundrigar Road,Karachi - 74000, Pakistan

Share RegistrarM/s. THK Associates (Pvt.) LimitedGround Floor, State Life Building No. 3,Dr. Ziauddin Ahmed Road,Karachi - Pakistan

AuditorsM/s. Ernst & Young Ford Rhodes Sidat Hyder,Chartered Accountants

M/s. BDO Ebrahim & Co.,Chartered Accountants

Legal AdvisorsM/s. Mehmood Abdul Ghani & Co.,Advocate

ContactsUAN: 111-825-111Contact Centre: 111-825-888Website: www.ubl.com.pk

Annual Report 2010 03

[ Directors Profile ]

Sheikh Nahayan Mabarak Al NahayanChairman, Board of Directors of United Bank Limited

The Chairman of the Board, Sheikh Nahayan Mabarak Al Nahayan'slife and career have been characterized by creativity, innovation, anddedicated public service. In his role as the Minister of Higher Educationand Scientific Research, he has guided and shaped higher educationin the United Arab Emirates and has established a successful modelfor higher education throughout the Gulf region.

In private business, Sheikh Nahayan is an active, successfulbusinessman, both within the United Arab Emirates and on theinternational stage. He heads the Abu Dhabi Group, one of the largestinternational investors in Pakistan, with interests in banking, tele-communications, pharmaceuticals, construction, petrochemicals,hotels, and real estate. He is chairman of the board of many importantcompanies, including Chairman of the Union National Bank in theUAE, Founder and Chairman of Warid Communications, Founder ofBank Al-Falah, in addition to being the chairman of United BankLimited.

In business, Sheikh Nahayan insists that all his projects must be “valuebased” as well as “goal driven.” Those who would work with him musthave integrity, a sound ethical touchstone, and a genuine concern forthose who are affected by the actions they take and the decisionsthey make. Sheikh Nahayan sees his role as one who sets standards,serves as a role model, and insists on accountability. He is also agreat believer in the social responsibility of private business, whereethics, morality, and transparency are important and where theoperations, practices, and attitudes of private companies must haverelevance to contemporary community values and needs.

A noted patron of the arts, Sheikh Nahayan strongly supports a widerange of activities, from natural history to music and culture, fromnational heritage to sports. He is a strong proponent of advancedtechnology and global best practices in education and business. Anactive philanthropist with a high sense of social responsibility, hechampions many humanitarian causes and provides strong supportfor individuals with disabilities. He also chairs and actively supportsmany groups and associations. These include: the Abu Dhabi Musicand Arts Foundation, the UAE Natural History Group, the MédecinsSans Frontières in the UAE, the Society of History and HistoricalHeritage of the UAE, The Millfield Association in the Arabian Peninsula,the Young Presidents Organization (YPO), the Abu Dhabi Cricket Club,the UAE Table Tennis Federation, the Arab Universities Sports Federation,and Friends of Al-Quds University in Abu Dhabi. A strong supporterof all cultural activities in Abu Dhabi and the UAE, including literature,theater, music, painting, sculpture, photography, and folk arts, SheikhNahayan is a regular patron of art exhibitions and heritage festivals.

Sheikh Nahayan is also a recognized leader in dealing with the majorsocial and economic issues that impact the United Arab Emirates andthe Arab region. He has played a major role in policy formulation relatedto the economic and social development of the United Arab Emirates. Sheikh Nahayan has chaired several cabinet committees on manpowerplanning and social development in the United Arab Emirates;committees charged with formulating policies for human and socialdevelopment in the country. He is an accomplished public speaker.He gives more than 150 public speeches and presentations everyyear. He is also an active sportsman. His sports hobbies includehorseback riding, flying helicopters and light aircraft, and falconry.

Sheikh Nahayan is the recipient of many national and internationalhonors and awards in addition to numerous honorary degrees fromuniversities around the world.

Sir Mohammed Anwar Pervez, OBE HPkDeputy Chairman

Sir Mohammed Anwar Pervez, OBE HPk is the Deputy Chairman ofthe Board of Directors of United Bank Limited since 19 October, 2002.He is also the Chairman of Bestway (Holdings) Limited, UK & itssubsidiaries, which include Batleys Limited in UK, Bestway Cementin Pakistan & Bestway Northern Limited in UK.

Sir Anwar began his career in food business in 1963 when he openeda mini supermarket in London. He ventured into the cash & carrybusiness in 1976 and has been responsible for growing Bestway intothe second largest cash & carry operator in the UK.

Sir Anwar was awarded the Order of the British Empire (OBE) in 1992and was conferred the title of Knight's Bachelor in 1999. In 2000 hewas awarded Hilal-e-Pakistan.

In 2005, Sir Anwar Pervez was voted winner of the prestigious GrocerCup for Outstanding Business Achievement by the Institute of GroceryDistribution, UK.

In 2006 he received Sitra-e-Essar and was chosen as the MasterEntrepreneur - UK at the Ernst & Young Entrepreneur of the Year 2006Awards.

He is also the Chairman of Bestway Foundation UK and Patron-in-Chief of Bestway Foundation Pakistan and a charter member of theDuke of Edinburgh Awards Scheme.

Omar Z. Al AskariDirector

Omar Ziad Al Askari is the Chairman and Chief Executive Officer ofUnited Technical Services. In 1972 he attained an MBA degree fromthe Kellogg Graduate School of Management at Northwestern University,having graduated in 1971 from the University of Oregon with a BBAdegree in business administration. He is a Certified Public Accountant.He began his career with Arthur Andersen & Co. in 1972 where hespecialized in audit and management consulting.

In 1976, he assumed control of Technical Services and SupplyCompany, a family concern based in Abu Dhabi, United Arab Emirates.In 1980, Mr. Al Askari established United Technical Services (UTS),now a leading force in sales and service of engineered products tothe oilfield and building services industries in the United Arab Emirates.He has served on numerous public and private company Boards.Currently he is a member of the Board of Directors of United BankLimited and is Chairman of AlFalah Exchange Co.

Mr. Al Askari served as International President of the Young Presidents'Organization in 1999-2000. He is a member of the World Presidents'Organization, the Chief Executives Organization, the American Instituteof Certified Public Accountants, Illinois CPA Society and the KelloggAlumni Advisory Board. He is a director of the Emirates Cricket Board.

United Bank Limited04

Zameer Mohammed ChoudreyDirector

Mr. Zameer Mohammed Choudrey has been a Member of the Boardof Directors of United Bank Limited since 19 October, 2002. He isChairman of the Board Audit Committee. He is also a Director of UBLInsurers Limited.

He is Chief Executive of Bestway Group, which is among the top tenfamily businesses in the UK with annual turnover of £2.1 billion. TheGroup's wholesale operations are the 2nd largest in the UK with an18% market share. Its cement operation is the second largest cementmanufacturer in Pakistan.

Zameer is a Chartered Accountant by profession. He joined BestwayGroup as a financial controller in 1984. In 1990, he was promotedas the Group Finance Director. In 1995, he was given additionalresponsibilities of business diversification both in UK and Pakistan andwas promoted as Chief Executive of Bestway Cement Limited. Hewas appointed as the Group CEO in 2004.

He is a fellow of the Institute of Chartered Accounts of England &Wales and a member of the Institute of Directors.

Zameer is a trustee of Bestway Foundation UK and Chairman ofBestway Foundation Pakistan. He is also a trustee of Caravan andCrimestoppers.

Muhammad Sami SaeedDirector

Mr. Muhammad Sami Saeed has been appointed as Director of UnitedBank Limited by the Government of Pakistan with effect from26 February 2008. He is also a Member of the Board Audit Committeeof the Bank. He did his M.A. from Punjab University in 1976 and post-graduation in Development Economics from University of Cambridge,UK, in 1986. He has done professional courses in economicmanagement and public finance from the IMF Institute, Washingtonand Kennedy School of Government, Harvard University, USA.At present, he is Additional Chief Secretary, Government of Punjab.

Prior to this, he was Chairman of Planning & Development Board,Government of Punjab, Additional Finance Secretary (Banking),Government of Pakistan. He also worked as Joint Secretary/AdditionalSecretary in Prime Minister's Secretariat (2006-2008), Secretary, Excise& Taxation Department (2002-2006), Secretary Agriculture (1998-99)in Government of Punjab and Deputy Commissioner Faisalabad (1990-93). He joined the Civil Service of Pakistan (District ManagementGroup) in 1980.

He also attended various international conferences and took part inbilateral negotiations in many countries as member of Government ofPakistan delegation. In January 2007, he attended World EconomicForum 2007 in Davos, Switzerland, as a member of the Pakistandelegation headed by the Prime Minister of Pakistan.

Amin UddinDirector

Mr. Amin Uddin has been appointed as member of Board of Directorsof United Bank Limited with effect from 5 March 2009. He is a memberof Board Audit Committee of UBL. He is also a Director of UBL InsurersLimited.

He did Banking Management course in 1986-87 from McGill University,Canada and B.A. (Economics and Statistics) from Punjab University,Lahore. He also attended various international professional trainingprograms.

He has a 40 years experience in Pakistan, Middle East, Europe, Africa& Canada. He worked in Ecobank Group, a leading Pan-Africancommercial banking group (1991-2002). He also worked in Bank ofCredit and Commerce INT (1977-1990) and Habib Bank Limited(1967-1977).

Annual Report 2010 05

Arshad Ahmad MirDirector

Mr. Arshad Ahmad Mir, appointed as member of Board of Directorswith effect from 26 October 2009, has over four decades of extensivecorporate experience in financial services, oil industry, managementconsultancy, manufacturing and wholesale distribution businesses.

He has served with major corporate entities in areas of generalmanagement, corporate planning, project management, complianceand consultancy. Geographical coverage of his corporate roles andresponsibilities encompass Pakistan, Middle East, Africa, UK & Europe.

Arshad Mir is a member of Institute of Chartered Accountants andInstitute of Bankers, UK. He has attended various management coursesand conferences including Advanced Management Programme ofLondon Business School.

He is also a member of the Board Risk Management Committee ofthe Bank.

Seerat AsgharDirector

Mr. Seerat Asghar has been appointed as Director of United BankLimited by the Government of Pakistan with effect from 30 March,2010. He is also a member of the Human Resources Committee ofthe Bank. Mr. Asghar has a vast experience gathered over a span ofmore than twenty nine years in public service at key GOP posts. Hebrings with him a rich professional and academic experience. He holdsan LLB and Master's degree in Political Science from Punjab University,Lahore. His last academic pursuit was at the prestigious CornellUniversity, USA, where he attended Executive Development Programin Food and Agriculture Business Management.

With a strong base in “Executive Leadership Development” fromHarvard University, he has developed a gradual niche in ProjectManagement, Procurement, as well as macro economic planning,resulting in representation of Pakistan at key international foras likeInternational Conference on E-Procurement In Seoul - Korea, TokyoUbiquitous Network Conference, Conference on Hazard RiskManagement at Delhi - India, 25th Session of the International GrainCouncil at London - UK, 133rd Session of the FAO Council and 34thSession of FAO Conference at Rome - Italy, US-Afghanistan-PakistanAgricultural Trilateral Conference In Istanbul, Turkey.

At present, he is Additional Secretary, Ministry of Finance, Governmentof Pakistan.

Atif R. BokhariPresident & CEO

Mr. Atif R. Bokhari, currently President & CEO, United Bank Limited(UBL) is a seasoned banker with extensive experience in domesticand international banking. He started his banking career in 1985 withBank of America, where he handled diverse assignments over a periodof 15 years. Subsequent to leaving Bank of America in July 2000,Mr. Bokhari joined Habib Bank Limited wherein he was Head ofCorporate and Investment Banking.

Mr. Bokhari was appointed as President & CEO of UBL in May 2004(18 months after privatization). Since then UBL has ventured into newdiversified business and revenue streams namely consumer financing,E-commerce, asset management and general insurance.

Mr. Bokhari holds the office of Chairman or Director in several UBLGroup companies. He is also a Director of First Women Bank Limitedand is very actively involved with a private sector program for thedevelopment of education in Karachi. Specifically he is a Director forthe envisaged Karachi Business School affiliated with the JudgeBusiness School, Cambridge, UK. He has been appointed as Chairmanof the Human Resource Committee of the Institute of Bankers inPakistan, which is headed by the Governor State Bank of Pakistan.He is also a member of the Executive Committee of Pakistan Banks'Association.

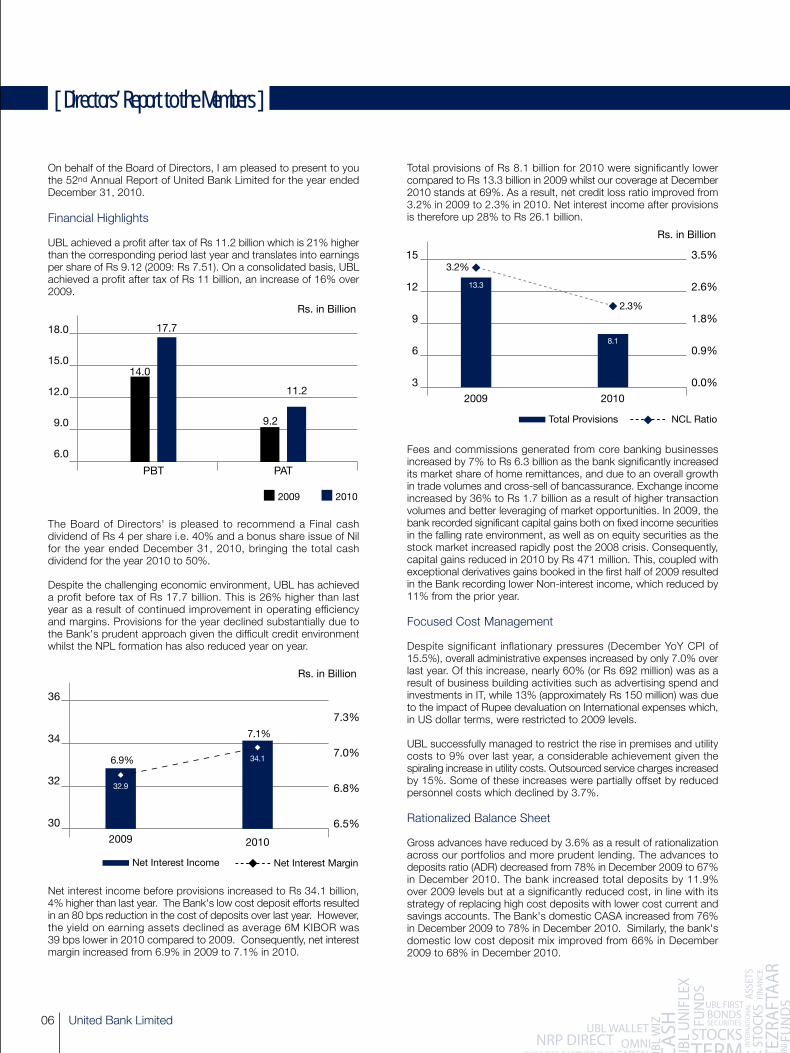

On behalf of the Board of Directors, I am pleased to present to youthe 52nd Annual Report of United Bank Limited for the year endedDecember 31, 2010.

Financial Highlights

UBL achieved a profit after tax of Rs 11.2 billion which is 21% higherthan the corresponding period last year and translates into earningsper share of Rs 9.12 (2009: Rs 7.51). On a consolidated basis, UBLachieved a profit after tax of Rs 11 billion, an increase of 16% over2009.

The Board of Directors' is pleased to recommend a Final cashdividend of Rs 4 per share i.e. 40% and a bonus share issue of Nilfor the year ended December 31, 2010, bringing the total cashdividend for the year 2010 to 50%.

Despite the challenging economic environment, UBL has achieveda profit before tax of Rs 17.7 billion. This is 26% higher than lastyear as a result of continued improvement in operating efficiencyand margins. Provisions for the year declined substantially due tothe Bank's prudent approach given the difficult credit environmentwhilst the NPL formation has also reduced year on year.

Net interest income before provisions increased to Rs 34.1 billion,4% higher than last year. The Bank's low cost deposit efforts resultedin an 80 bps reduction in the cost of deposits over last year. However,the yield on earning assets declined as average 6M KIBOR was39 bps lower in 2010 compared to 2009. Consequently, net interestmargin increased from 6.9% in 2009 to 7.1% in 2010.

Total provisions of Rs 8.1 billion for 2010 were significantly lowercompared to Rs 13.3 billion in 2009 whilst our coverage at December2010 stands at 69%. As a result, net credit loss ratio improved from3.2% in 2009 to 2.3% in 2010. Net interest income after provisionsis therefore up 28% to Rs 26.1 billion.

Fees and commissions generated from core banking businessesincreased by 7% to Rs 6.3 billion as the bank significantly increasedits market share of home remittances, and due to an overall growthin trade volumes and cross-sell of bancassurance. Exchange incomeincreased by 36% to Rs 1.7 billion as a result of higher transactionvolumes and better leveraging of market opportunities. In 2009, thebank recorded significant capital gains both on fixed income securitiesin the falling rate environment, as well as on equity securities as thestock market increased rapidly post the 2008 crisis. Consequently,capital gains reduced in 2010 by Rs 471 million. This, coupled withexceptional derivatives gains booked in the first half of 2009 resultedin the Bank recording lower Non-interest income, which reduced by11% from the prior year.

Focused Cost Management

Despite significant inflationary pressures (December YoY CPI of15.5%), overall administrative expenses increased by only 7.0% overlast year. Of this increase, nearly 60% (or Rs 692 million) was as aresult of business building activities such as advertising spend andinvestments in IT, while 13% (approximately Rs 150 million) was dueto the impact of Rupee devaluation on International expenses which,in US dollar terms, were restricted to 2009 levels.

UBL successfully managed to restrict the rise in premises and utilitycosts to 9% over last year, a considerable achievement given thespiraling increase in utility costs. Outsourced service charges increasedby 15%. Some of these increases were partially offset by reducedpersonnel costs which declined by 3.7%.

Rationalized Balance Sheet

Gross advances have reduced by 3.6% as a result of rationalizationacross our portfolios and more prudent lending. The advances todeposits ratio (ADR) decreased from 78% in December 2009 to 67%in December 2010. The bank increased total deposits by 11.9%over 2009 levels but at a significantly reduced cost, in line with itsstrategy of replacing high cost deposits with lower cost current andsavings accounts. The Bank's domestic CASA increased from 76%in December 2009 to 78% in December 2010. Similarly, the bank'sdomestic low cost deposit mix improved from 66% in December2009 to 68% in December 2010.

United Bank Limited06

[ Directors’ Report to the Members ]

18.0

15.0

12.0

9.0

6.0

PBT PAT

9.2

11.2

Rs. in Billion

17.7

14.0

2009 2010

36

34

32

30

Net Interest Income Net Interest Margin

2009

7.1%

6.9%

7.3%

7.0%

6.8%

6.5%

2010

32.9

34.1

Rs. in Billion

15

12

9

6

3

Total Provisions NCL Ratio

2009

2.3%

3.2%

13.3

8.1

3.5%

2.6%

1.8%

0.9%

0.0%2010

Rs. in Billion

We were successful in improving our return on average assets from1.5% in 2009 to 1.7% in 2010. Return on equity also improved from19.5% in 2009 to 19.8% in 2010.

Improved Capital Ratios

UBL's strong internal capital generation resulted in a Rs 6.1 billion(14%) increase in Tier 1 Capital, despite keeping Risk Assets flat.Consequently, the unconsolidated Capital Adequacy Ratio (CAR) ofthe Bank improved from 13.2% in December 2009 to 14.5% inDecember 2010. The Tier-1 CAR of the Bank has also improvedfrom 9.0% in December 2009 to 10.3% in December 2010. On aconsolidated basis, the CAR improved to 15.0% in December 2010(December 2009: 14.0%) while Tier-1 CAR improved from 9.5% inDecember 2009 to 10.4% in December 2010.

Economy Review

The year 2010 remained fraught with challenges, which impactedthe macroeconomic landscape of the country. In the second half ofthe year, record floods inundated nearly 20% of the country andinflicted significant damage to the fragile economy. Continuing severeshortages of power and gas have exacerbated the situation andLarge Scale Manufacturing (LSM), after exhibiting good growth of5% in FY10, remained subdued during the first half of the currentfiscal year. As a consequence, GDP growth estimates for 2010-11have been scaled down to 2.8% from pre-flood estimates of 4.3%.

Inflationary pressures remained active throughout the year, with CPIat 15.5% year-on-year in December 2010 and averaging 13.9% forthe year. Supply chain interruptions caused by crop damage resulted

in volatile food prices and remained a key driver behind surging pricepressures. Escalating power tariffs remained a regular featurethroughout 2010, further fueling inflation.

The fiscal position remained fragile as revenue generation remainedweak whilst expenditures escalated. FY 2010 fiscal deficit stood at6.3% of GDP, far exceeding the IMF target. Furthermore, taxationreforms including the Reformed General Sales Tax (RGST) have notyet been implemented due to severe opposition by political parties.The fiscal slippages and spiraling inflation have resulted in a steadyincrease in interest rates with the State Bank of Pakistan (SBP) raisingthe discount rate by 150 bps since July 2010 to 14.0%. Lack offiscal austerity continues to strain domestic liquidity as banks shifttowards government paper, which in turn has led to further crowdingout of the private sector.

The external account position remained a key positive as the currentaccount deficit for FY 2010 was better than expectations at 2% ofGDP due to higher remittances and aid inflows, services inflows andincreased exports. This trend has continued in FY 2011 as thecountry posted its first half-yearly current account surplus since2003. Pakistan's equity markets also performed well and continuedto attract foreign investment, with the KSE-100 Index gainingapproximately 26% during 2010.

The banking sector of Pakistan has been in a consolidation phasesince the beginning of 2009 due to the country's economicvulnerabilities. The sector has remained focused on deposits, whichgrew by nearly 15% in 2010, with aggressive solicitation of currentand savings accounts (CASA). Credit lending has remained subduedand Gross Advances increased by only around 5% during 2010.The effects of the depressed economic activity, power shortagesand high interest rates have significantly impacted borrowers. Non-Performing Loans (NPLs) have seen a sharp increase of 22%, standingat Rs 494 billion as of December 2010 while infection of the sector'sportfolio has also deteriorated from 12.2% in December 2009 to14.0% in December 2010.

International

UBL's International business continues to be a key segment for theBank. In line with the Bank's overall policy, lending remained cautious,resulting in a reduction of 10% in loans and advances. Revenue fromthe International Business thus declined by 3% from 2009. This wasmore than offset by cost being contained at prior year levels as wellas a 23% reduction in provisions. Consequently, pretax profit increasedby 14% over last year. As the global economy continues to recover,UBL is enthusiastic about the future prospects of the InternationalBusiness. The Bank will explore expansion into new territories whichhave the potential to enhance shareholder value and represent anatural progression from the existing footprint.

Core Banking Platform Implementation (Project Genesis)

Project Genesis continues to move forward as planned and sixbranches went live this year on the new core banking system (CBS).This was a significant milestone as it enabled the Bank to test thecapabilities of the system on a real time basis.

The Customer Service Platform (CSP), a customer relationshipmanagement tool, been rolled out in over 350 branches in 2010 andwill be rolled out across the country in 2011. The Loan OriginationSystem (LOS) has been implemented for Commercial loans andConsumer products. LOS implementation for the rest of the Bankwill be completed by 2012.

Annual Report 2010 07

Expensive Deposits Low Cost Deposits

197

295

211

340

551492

Dec-09 Dec-10

Rs. in Billion

10.3%

9.0%

Tier 1 CAR Total CAR

13.2%

14.5%

2009 2010

United Bank Limited08

[ Directors’ Report to the Members ]

UBL is already starting to see the technological benefits and theimproved service capability that these systems will bring to the Bankand its customers.

Key Developments During 2010

Watan Card

The Government of Pakistan (GOP) selected UBL to disburseRs 20,000 each to over one million families displaced by the flooding.For this effort UBL issued debit cards, called “Watan cards”, tobeneficiaries identified by NADRA and GOP. Additional plannedinstallments in 2011 will assure beneficiaries have multiple opportunitiesto use (and get used to) the cards. UBL's ultimate goal is to retainthe beneficiaries as Branchless Banking customers by introducingthem to the benefits of using additional services such as savings,remittances, and bill payments that are accessible via their Watancard Omni accounts.

The Bill & Melinda Gates Foundation will contribute US$1.5 millionthrough MEDA (Mennonite Economic Development Association) tosupport UBL's management and administrative costs of procuringand distributing the cards as well as the cost of ongoing disbursementsvia Omni Agents. The funding will also support MEDA in monitoringand documenting the UBL Watan experience, in order to sharelearnings with the wider microfinance and financial sector communitiesglobally.

UBL Omni

UBL Omni commenced commercial operations in April 2010 andwith it UBL achieved the honor of being the first commercial bankto launch branchless banking operations in Pakistan. With Omni,UBL aims to attract the unbanked population via its retail businessagents called Omni Dukaans which are located in over 350 townsand cities of Pakistan and currently number more than 2,300.

Pakistan has nearly 65 million unique mobile phone subscriberswhilst it has less than 20 million individuals with bank accounts.This provides the Bank with the unique platform of being able toinclude a large segment of the country's unbanked population andprovide them financial services which have previously remainedinaccessible to them.

In recognition of UBL's innovative product offering, strong managementcredentials and admirable goals of financial inclusion, the Bill andMelinda Gates Foundation has given UBL a grant of US$6.9 millionthrough ShoreBank International to promote UBL Omni and ensureits reach to the widest possible community.

Launch of UBL First Minor Account

The Bank launched 'UBL First Minor PLS Savings Account' in 2010,a savings account designed especially for children, with excitingbenefits that are unmatched in the industry. By providing an avenueto parents for financial planning for their children, it should alsoincrease the number of parents in the banking system, as well asdevelop a new generation of customers loyal to UBL. This producthas already generated a high degree of interest amongst childrenvia the Bank's youth outreach and social media campaigns.

Launch of UBL Business Partner Plus

UBL launched 'Business Partner Plus' in 2010, the best currentaccount offering in Pakistan. This is a specialized current checkingaccount, with a full menu of services, aimed at providing the necessarytools for individuals, traders, businessmen and commercial customersto transact their entire bank related business activities nationwidethrough a single platform. This product has been a major successstory in its first year of launch.

Signature: Priority Banking

2010 was the first full year of operations for the UBL Priority Bankinglounges launched in November 2009. These exclusive lounges caterto the Bank's existing and potential high-net-worth customers, withrelationship managers trained to offer a range of wealth managementproducts to service customer needs. UBL has had a successfulexperience with this offering and plans to expand this businessacross Pakistan in the future.

Launch of Pakistan's First Premium Debit Card

In 2010, UBL in collaboration with MasterCard, announced the launchof Pakistan's first Premium Debit MasterCard, exclusively designedto cater to the needs of affluent consumers in Pakistan. Customerswho fulfill the stipulated eligibility criteria are being offered this card,as part of UBL's continuing commitment to offering the best productsto its customers. In addition to the features and privileges inherentin the card program, UBL has also teamed up with various partnersto provide preferential benefits to its cardholders.

Wiz for ACCA

Wiz is a prepaid debit card which was launched in 2008, and UBLis the only bank in the country to have this offering. Customers candeposit up to a limit of Rs 200,000 in their debit card and use it allover the world. The card can be topped-up for usage (just like aprepaid mobile phone connection) from any UBL online branch.

UBL entered into a partnership with the Association of CharteredCertified Accountants, UK (ACCA), a global body of accountingprofessionals, which has thousands of registered students in Pakistan.In this connection, the Bank has launched a Wiz prepaid cardspecifically for ACCA students, which is especially convenient tothem in making fee payments online. This is a key initiative that isexpected to increase awareness and usage of the Wiz card.

Credit Ratings

The credit rating company JCR-VIS re-affirmed the bank's long-termentity rating at AA+ and the ratings of its four subordinated debtinstruments at AA. The short term ratings remain at A-1+ which isthe highest rating denoting the greatest certainty of timely paymentsby a financial institution. All ratings for UBL have been assigned aStable outlook.

Capital Intelligence (CI), the international credit rating agency, hasre-affirmed UBL's Foreign Currency long-term rating at B-, while it'sForeign Currency short-term rating has been upgraded from C to Bin line with CI's sovereign ratings action on Pakistan. In addition, theBank's Financial Strength rating has been re-affirmed at BB+, withthe Outlook upgraded from Negative to Stable based on the Bank'sstrong performance in 2009 and the first half of 2010.

Annual Report 2010 09

Future Outlook

Going forward, achieving macroeconomic stability remains a keychallenge for Pakistan. Continued power and gas shortages alongwith high borrowing costs are expected to place further pressure onthe LSM sector and consequently on GDP growth. Inflationarypressures are expected to remain high, averaging close to 15-16%for 2011.

Achieving fiscal austerity remains of utmost significance. The deficittarget for 2011 is likely to be breached due to lower revenue generationalong with weak expenditure control. However, the external accountposition should remain healthy as higher remittances, services inflowsand increased exports are likely to continue during 2011. Inflationarypressures combined with the weak fiscal position are expected toresult in a continued tight monetary policy during 2011.

Given the macroeconomic scenario, UBL's focus will remain onproactively managing its asset portfolio while exploring the acquisitionof quality assets. The Bank will continue to grow its low cost depositbase by more efficiently leveraging its branch network. UBL alsoplans to significantly expand its Branchless Banking product to makefinancial services available to a broader range of people. The Bankis confident that, with the investments it has made in people,technology and products, it is well positioned for further growth.

Statement Under Section XIX of the Code of CorporateGovernance

The Board is committed to ensure that requirements of corporategovernance set by Securities and Exchange Commission of Pakistanare fully met. The Bank has adopted good Corporate Governancepractices and the Directors are pleased to report that:

• The financial statements present fairly the state of affairs of theBank, the result of its operations, cash flows and changes in equity.

• Proper books of account of the Bank have been maintained.

• Appropriate accounting policies have been consistently appliedin preparation of these unconsolidated financial statements,except for the changes in the accounting policies as describedin note 5.1. Accounting estimates are based on reasonable andprudent judgment.

• International Accounting Standards, as applicable to Banks inPakistan have been followed in the preparation of the Accountsof financial statements without any departure there-from.

• The system of internal control in the Bank is sound in design,and effectively implemented and monitored.

• There are no significant doubts upon the Bank's ability tocontinue as a going concern.

• There has been no material departure from the best practicesof Corporate Governance.

• The Board has appointed the following three Committees withdefined terms of references

• Board Risk Management Committee

• Board Human Resources & Compensation Committee

• Board Audit Committee

• Performance highlights for the last six years are attached tothese unconsolidated financial statements.

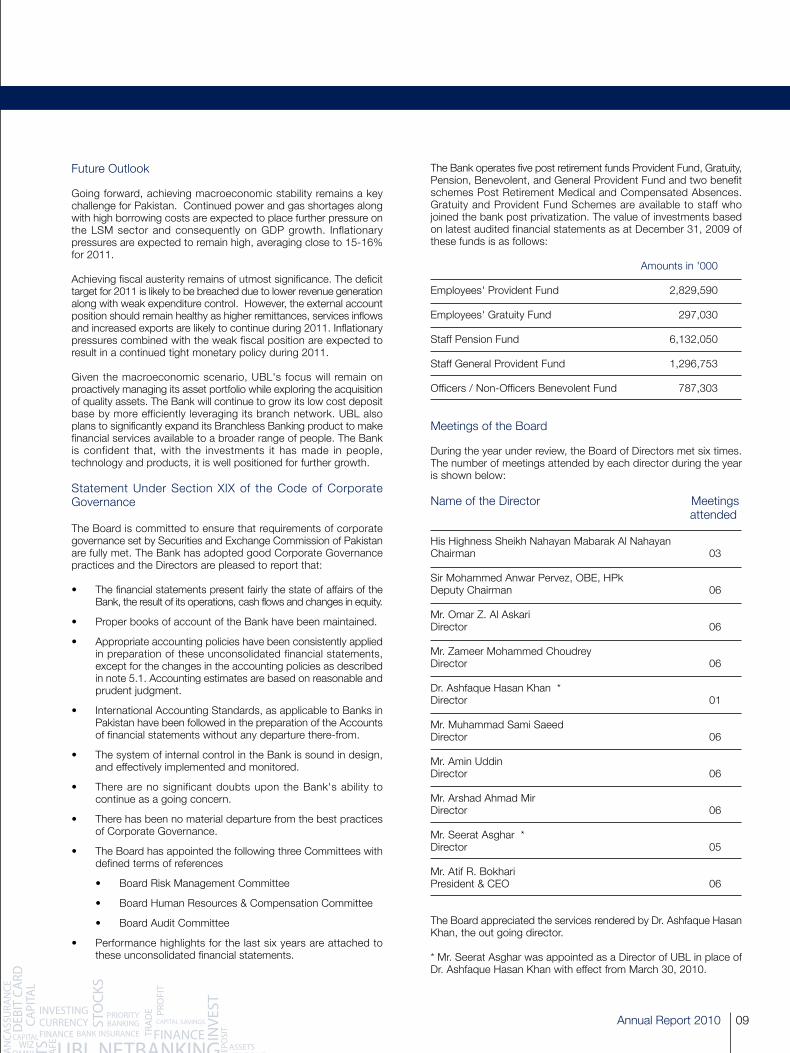

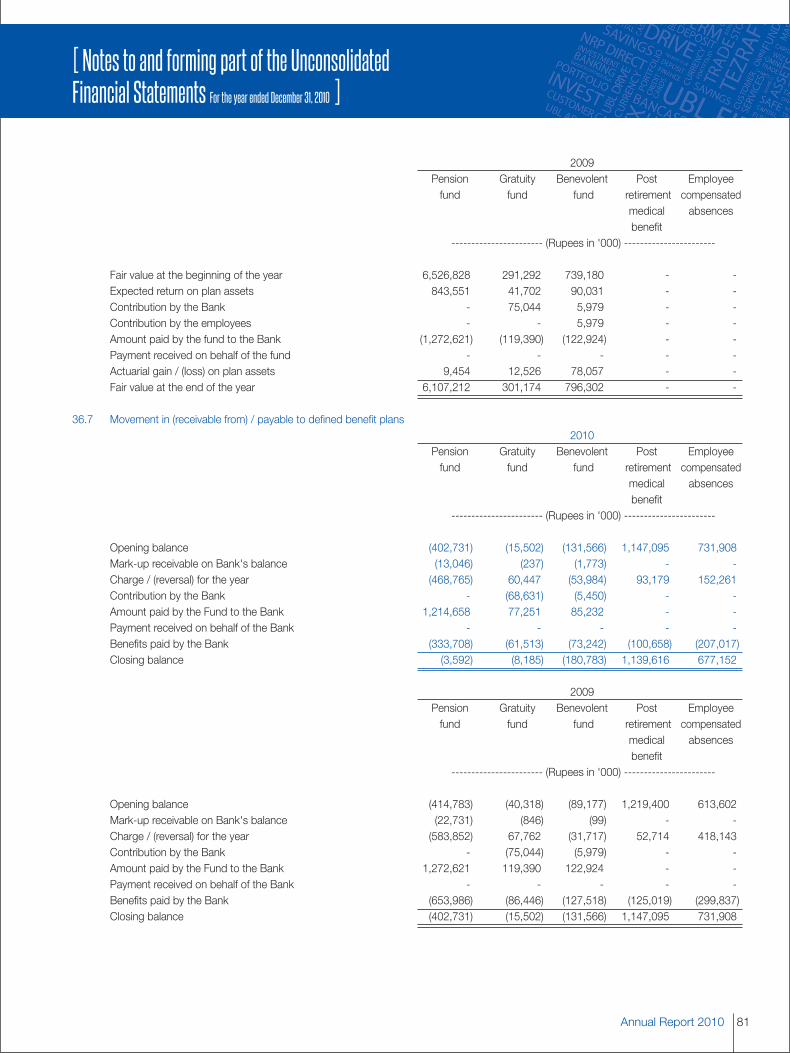

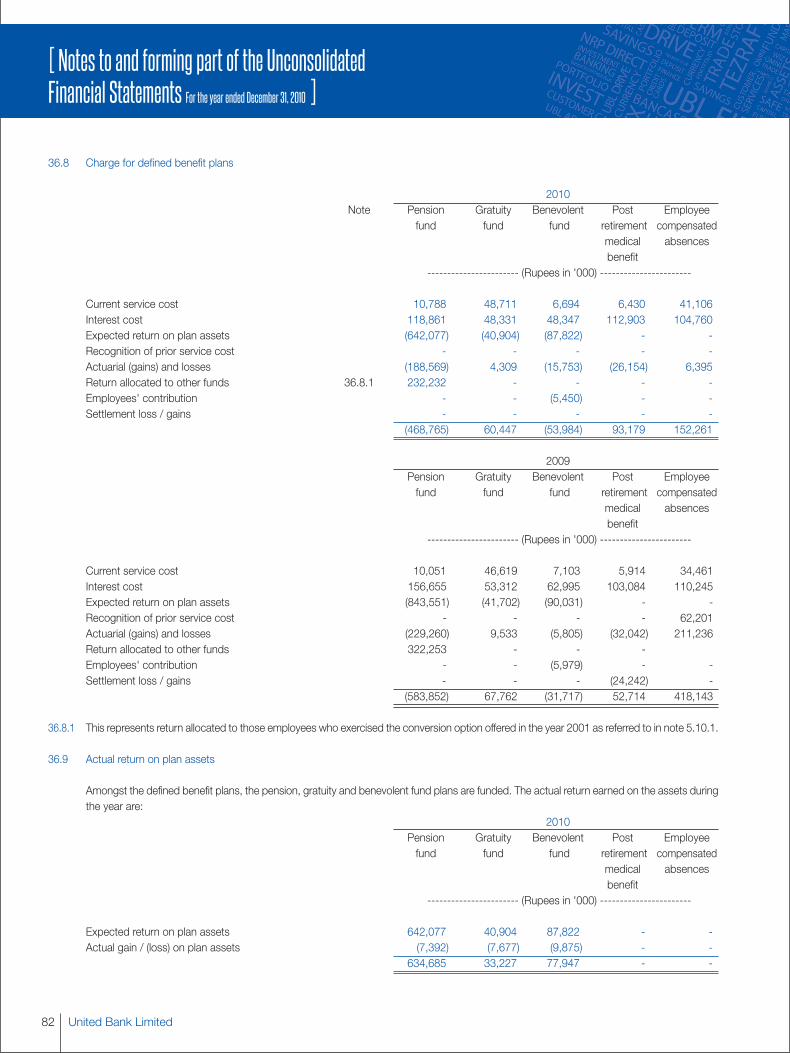

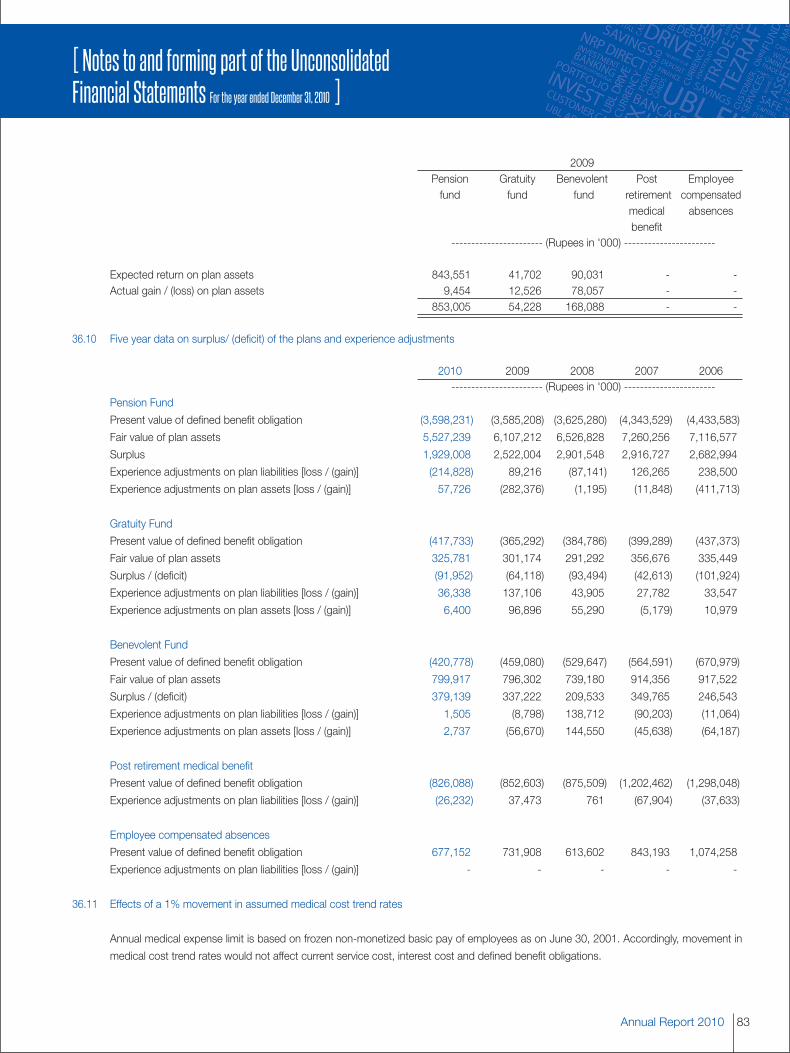

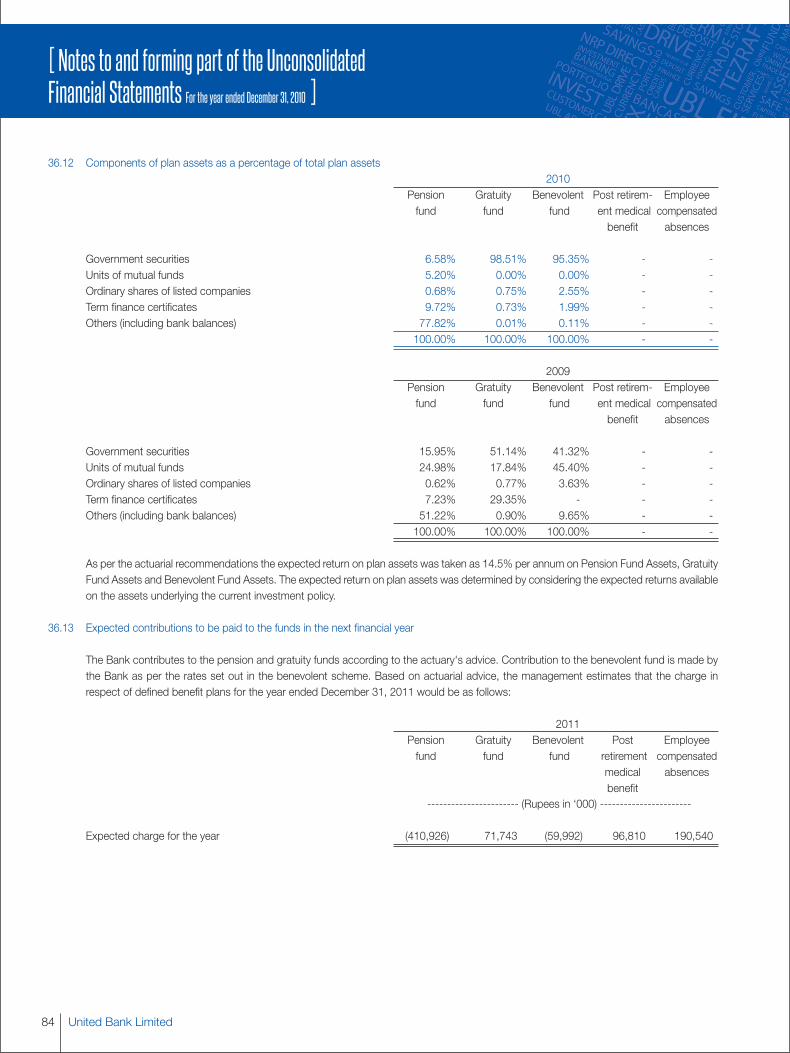

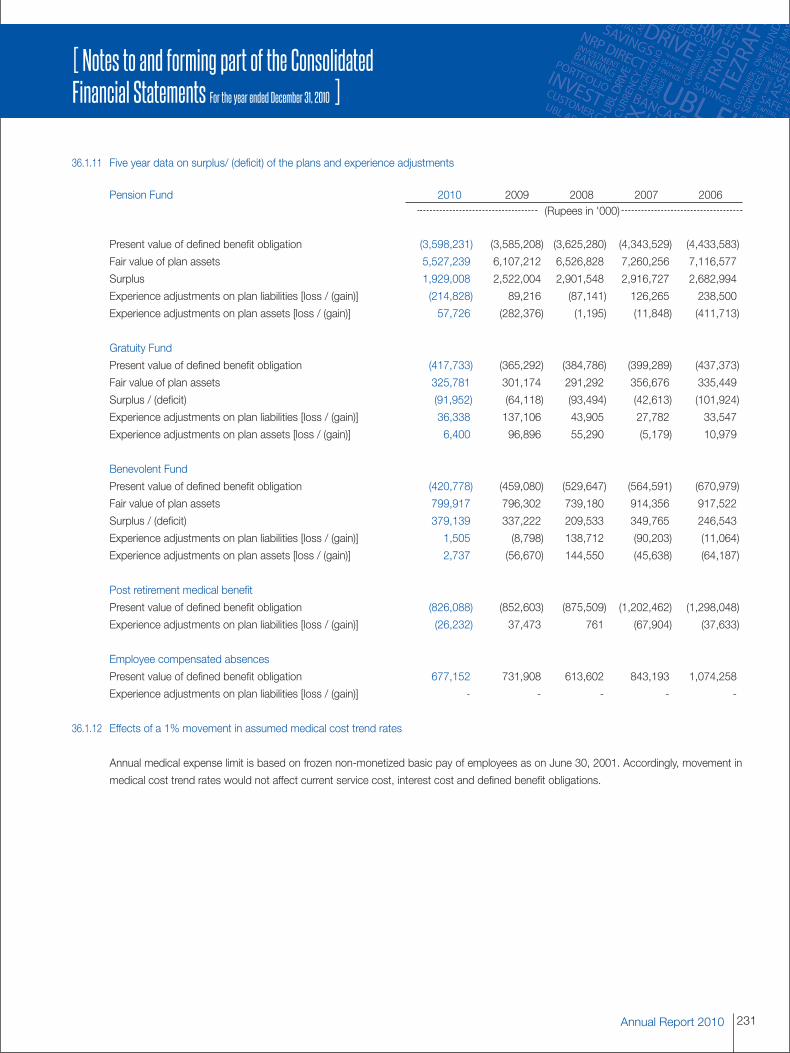

The Bank operates five post retirement funds Provident Fund, Gratuity,Pension, Benevolent, and General Provident Fund and two benefitschemes Post Retirement Medical and Compensated Absences.Gratuity and Provident Fund Schemes are available to staff whojoined the bank post privatization. The value of investments basedon latest audited financial statements as at December 31, 2009 ofthese funds is as follows:

Amounts in '000

Employees' Provident Fund 2,829,590

Employees' Gratuity Fund 297,030

Staff Pension Fund 6,132,050

Staff General Provident Fund 1,296,753

Officers / Non-Officers Benevolent Fund 787,303

Meetings of the Board

During the year under review, the Board of Directors met six times.The number of meetings attended by each director during the yearis shown below:

Name of the Director Meetingsattended

His Highness Sheikh Nahayan Mabarak Al NahayanChairman 03

Sir Mohammed Anwar Pervez, OBE, HPkDeputy Chairman 06

Mr. Omar Z. Al AskariDirector 06

Mr. Zameer Mohammed ChoudreyDirector 06

Dr. Ashfaque Hasan Khan *Director 01

Mr. Muhammad Sami SaeedDirector 06

Mr. Amin UddinDirector 06

Mr. Arshad Ahmad MirDirector 06

Mr. Seerat Asghar *Director 05

Mr. Atif R. BokhariPresident & CEO 06

The Board appreciated the services rendered by Dr. Ashfaque HasanKhan, the out going director.

* Mr. Seerat Asghar was appointed as a Director of UBL in place ofDr. Ashfaque Hasan Khan with effect from March 30, 2010.

United Bank Limited10

[ Directors’ Report to the Members ]

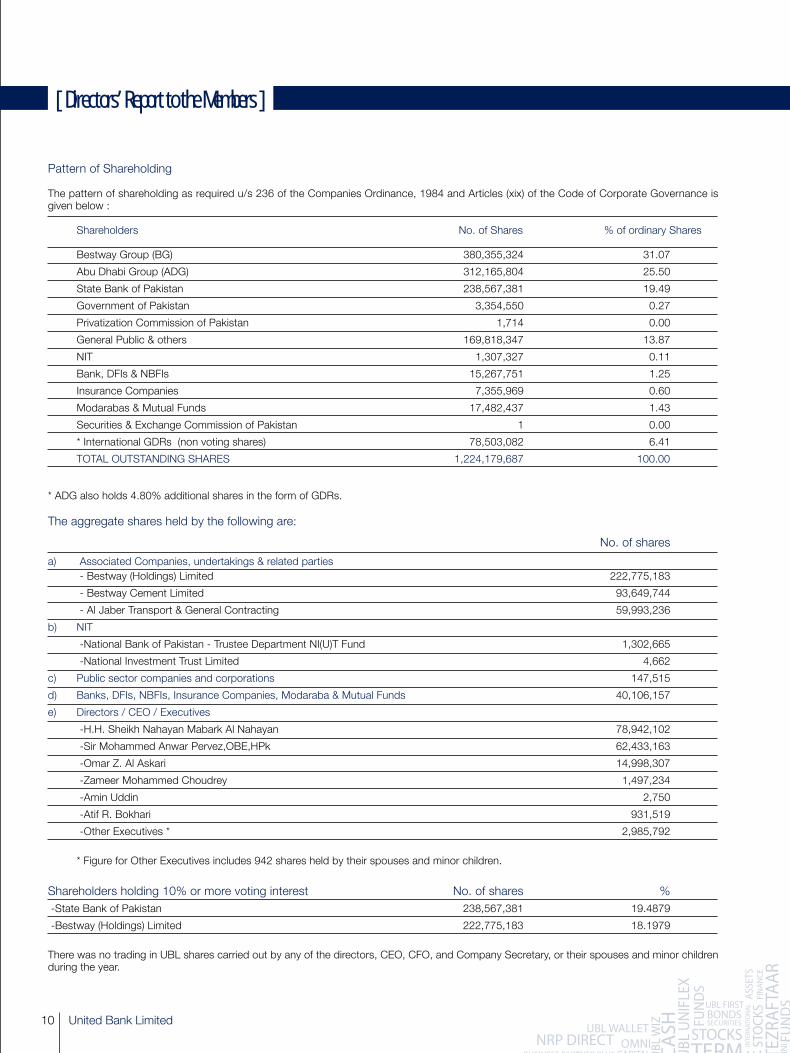

Pattern of Shareholding

The pattern of shareholding as required u/s 236 of the Companies Ordinance, 1984 and Articles (xix) of the Code of Corporate Governance isgiven below :

Shareholders No. of Shares % of ordinary Shares

Bestway Group (BG) 380,355,324 31.07

Abu Dhabi Group (ADG) 312,165,804 25.50

State Bank of Pakistan 238,567,381 19.49

Government of Pakistan 3,354,550 0.27

Privatization Commission of Pakistan 1,714 0.00

General Public & others 169,818,347 13.87

NIT 1,307,327 0.11

Bank, DFIs & NBFIs 15,267,751 1.25

Insurance Companies 7,355,969 0.60

Modarabas & Mutual Funds 17,482,437 1.43

Securities & Exchange Commission of Pakistan 1 0.00

* International GDRs (non voting shares) 78,503,082 6.41

TOTAL OUTSTANDING SHARES 1,224,179,687 100.00

* ADG also holds 4.80% additional shares in the form of GDRs.

The aggregate shares held by the following are:

No. of shares

a) Associated Companies, undertakings & related parties - Bestway (Holdings) Limited 222,775,183

- Bestway Cement Limited 93,649,744

- Al Jaber Transport & General Contracting 59,993,236

b) NIT

-National Bank of Pakistan - Trustee Department NI(U)T Fund 1,302,665

-National Investment Trust Limited 4,662

c) Public sector companies and corporations 147,515

d) Banks, DFIs, NBFIs, Insurance Companies, Modaraba & Mutual Funds 40,106,157

e) Directors / CEO / Executives

-H.H. Sheikh Nahayan Mabark Al Nahayan 78,942,102

-Sir Mohammed Anwar Pervez,OBE,HPk 62,433,163

-Omar Z. Al Askari 14,998,307

-Zameer Mohammed Choudrey 1,497,234

-Amin Uddin 2,750

-Atif R. Bokhari 931,519

-Other Executives * 2,985,792

* Figure for Other Executives includes 942 shares held by their spouses and minor children.

Shareholders holding 10% or more voting interest No. of shares % -State Bank of Pakistan 238,567,381 19.4879

-Bestway (Holdings) Limited 222,775,183 18.1979

There was no trading in UBL shares carried out by any of the directors, CEO, CFO, and Company Secretary, or their spouses and minor childrenduring the year.

Annual Report 2010 11

Risk Management Framework

The Bank has an integrated Risk Management structure in place.The Board Risk Management Committee (BRMC) oversees the wholerisk management process of the Bank. The Risk and Credit PolicyGroup assists the BRMC. The Group is organized into the functionsof Credit Administration, Market and Treasury Risk, Commercial andFI Credit Policy, Consumer and Retail Credit, Credit Risk Managementand Operational Risk & Basel II. Each risk category is headed by asenior manager who reports directly to the Group Executive, Riskand Credit Policy.

As Pakistan progresses through a period of eco-political turmoil,UBL strengthened its capacity for identifying and reducing risk. Theyear saw emphasis on close monitoring of the asset portfolio acrossall segments, including actively working with clients to help themwith repayments and restructuring. Steps were also taken to enhancethe efficiency of the credit approval process through appropriatedelegation of approval authority. A holistic Risk Management Policywas finalized in 2010. This is an umbrella policy, providing an integratedframework to encompass Credit, Liquidity, Agricultural, International,Market and Human Resource risk, aimed at portfolio qualityimprovement. A comprehensive Agriculture Credit Policy was alsodeveloped and finalized over the year. The formulation and approvalof these policies involved input from the Board and senior managementto ensure that risks were accurately assessed. In order to keepbusinesses aware of market and industry developments, the CreditPolicy & Research Division provided regular updates on majormacroeconomic issues and specific industry developments.

The Capital Adequacy Ratio (CAR) was maintained well above theprescribed regulatory threshold throughout the year. The CARcalculation process has been optimized through automation andsystem based reporting is expected to commence from 2011. TheBank continued its efforts towards implementing the OperationalRisk Management Framework across the bank and achieved thedeployment of operational risk monitor, a key milestone in this regard.The Bank plans to move to the Advanced Approach for Basel II,including all its components and has prepared a roadmap towardsimplementation.

In order to automate the loan origination process for Corporate,Commercial and SME borrowers, a Loan Origination System (LOS),one of the most critical components of UBL's new Core BankingSystem, has been implemented. LOS facilitates routing of creditapplications created on a predefined format to recommenders andapprovers electronically. During the year, the LOS has been successfullyimplemented for Consumer & SME loans. User Acceptance Testing(UAT) for Corporate and Commercial credit applications on LOS hasbeen done successfully and Bank wide roll out covering all segmentsand customers is expected in 2012.

Consumer financing portfolios remain stressed around the countrydue to the high inflationary environment with consequent escalationin borrowing costs. UBL continued to effectively manage its portfolioand developed a behavior scoring model as a risk management toolto facilitate automated credit limit management, collectionsmanagement and transaction authorization. The Bank is in theprocess of developing an Application Scoring model for identificationof quality acquisition prospects across the consumer portfolio.

The Market and Treasury Risk unit has continued to review riskpolicies and procedures to ensure that operating controls are robustand limits are in place to manage risk without unduly hamperingbusiness. Towards this end, several initiatives have been taken duringthe current year. For the equity trading portfolio, a Value-at-Risk

approach is being back tested and fine-tuned whereas for thederivatives portfolio a revised mechanism has been rolled out tomeasure and monitor pre-settlement risk. Market Risk Limit settingmechanisms have also been updated to place greater reliance onquantitative rather than subjective methods. For the banking book,several analytical tools are under review to supplement stress testingrequirements.

The Bank also continues to invest in systems and people as part ofits process of continuously strengthening the risk managementfunction.

Auditors

The present auditors M/S. Ernst & Young Ford Rhodes Sidat Hyder,Chartered Accountants and M/S. BDO Ebrahim & Co., CharteredAccountants retire and being eligible, offer themselves for re-appointment in the forthcoming Annual General Meeting.

Conclusion

In conclusion, I extend my thanks and appreciation to UBLshareholders and customers as well as to my fellow members of theBoard of Directors for their trust and support. We acknowledge theefforts and dedication demonstrated by our staff and would also liketo express our earnest appreciation to the Government, the StateBank of Pakistan, the Securities & Exchange Commission and otherregulatory bodies for their continued support.

For and on behalf of the Board,

Nahayan Mabarak Al NahayanChairman

Abu DhabiFebruary 21, 2011

United Bank Limited12

[ Statement of Corporate Social Responsibility ]

The commitment to continuously create value for its customers,employees and local communities is a major priority of UBL. In 2010,the Bank provided support of over Rs 80 million for CSR initiativesprincipally in the areas of education, health care and communitydevelopment. UBL's efforts in the field of CSR were also acknowledgedby the Pakistan Center for Philanthropy (PCP), an independentorganization, as one of the largest donors to charitable causes inPakistan.

UBL, as a “Contributing Sponsor” of the Karachi Education Initiative(KEI), contributed Rs 40 million to this cause. This initiative aims toset up a world class School of Business and Leadership in Karachi.Additionally, Rs 3.9 million were also donated to other organizationsoperating in the field of education, including The Citizens' Foundationand the Lahore University of Management Sciences.

In the areas of health and community development, UBL contributedover Rs 10 million to the Edhi Foundation, SOS Villages of Pakistan,Marie Adelaide Leprosy Centers, Special Olympics Pakistan, ThePolice Hospital Fund and Friends of Burns Center.

The massive floods across Pakistan in July 2010, resulted in almost20% of the country being inundated, and over 20 million peoplerendered homeless and stripped of basic needs such as food andclean drinking water. UBL initiated a donation program nationwide,accompanied by a significant media campaign, with a pledge tomatch each donation rupee for rupee. UBL's employees also answeredthe call; voluntarily donating one day's salary, which was also matchedby the Bank. These funds were then utilized towards rehabilitationof the flood affectees, with a focus on the provision of clean drinkingwater.

As a result of its previous success and credibility in distributingGovernment aid to the Internally Displaced Persons in Swat, theGovernment of Pakistan chose UBL to route payments of Rs 20,000each to 1 million households displaced in the floods. UBL made thispossible by collaborating with NADRA and using the Bank'sestablished Omni Branchless Banking platform to deliver paymentsto recipients via “Watan”-Visa debit cards. UBL successfully disbursedthe funds in 70 districts of Pakistan in record time, and with atransparency that has been appreciated by several internationaldonor organizations. Recognizing UBL Omni's efforts for financialinclusion of this previously unbanked population, the Bill and MelindaGates Foundation has supported UBL through a US$ 1.5 milliongrant for supporting the Watan project.

Annual Report 2010 13

[ President & CEO Review 2010 ]

Introduction

Pakistan's weak macroeconomic situation remained under pressureduring 2010, particularly in the wake of the floods that affected alarge part of the country. This was manifested through spiralinginflation driven by escalating food prices and frequent increases inutility rates, rising interest rates and slippages on fiscal targets. Inthis difficult environment, UBL has delivered a healthy growth of 26%on pretax profit.

During the year, the Bank's focus remained on prudent and proactivemanagement of its loan portfolio, low cost deposit growth and controlover costs. The Bank has been successful in these efforts as seenby lower provisions, reduced cost of funds and expense growthsubstantially below inflation levels. UBL also invested in technologyand new products and distribution channels which it believes willhelp the Bank in achieving its ambitious growth plans.

The performance of the Bank's International business also improvedover the last year as the Middle East economies stabilized. Costswere held at prior year levels while active portfolio managementresulted in significantly lower provisions. This business remains akey part of UBL's strategy and the Bank will be looking to consolidateand build on gains achieved this year.

Key financials

Despite the challenging economic environment, UBL has achievedan unconsolidated profit before tax of Rs 17.7 billion, 26% higherthan last year as a result of continued improvement in operatingefficiency and margins.

Deposits grew by nearly 12% as the Bank remained focused onmobilizing low cost deposits. UBL's domestic low cost deposit miximproved from 66% to 68% resulting in a reduction of 80 bps in thecost of deposits. Gross advances reduced by 4% as a result ofrationalization across our portfolios, and more prudent lending which,along with a lower average KIBOR, led to lower asset yields.Consequently, net interest margin increased from 6.9% in 2009 to7.1% in 2010 and Net interest income before provisions increasedto Rs 34.1 billion, 4% higher than last year.

Management of the loan portfolio remained a key priority for theBank which actively worked with borrowers to restructure those withgenuine difficulties while pursuing recoveries from defaulters. Lendingparameters were also tightened to ensure growth of quality assets.The Bank was thus able to reduce provisions to Rs 8.1 billion for2010 from Rs 13.3 billion in 2009, while also slowing the growth innon-performing loans. Net credit loss ratio improved to 2.3% in 2010.

Fees and commissions generated from core banking businessesincreased by 7% to Rs 6.3 billion through growth in home remittances,trade volumes and cross-sell of bancassurance. Exchange incomeincreased by 36% to Rs 1.7 billion as a result of higher transactionvolumes and better leveraging of market opportunities. However,the high capital gains recorded in 2009 were not repeated and thesereduced to Rs 159 million in 2010. Income from the derivativesbusiness also reduced as 2009 results included one-off gains whichwere not expected to recur.

Despite inflation of around 14%, overall administrative expensesincreased by only 7% over last year. Of this increase, the majoritywas for business building activities such as advertising spend andinvestments in IT. UBL remains committed to managing its costsprudently, in the best interests of its shareholders and customers.

UBL's key ratios showed improvement as the unconsolidated CARimproved from 13.2% to 14.5%, while Tier-1 CAR of the Bankimproved from 9.1% to 10.3%. The consolidated CAR also improvedby similar amounts. Shareholder returns also improved as the Returnon Assets improved from 1.5% to 1.7% and the Return on Equityimproved from 19.5% to 19.8%. The advances to deposits ratio(ADR) also reduced from 78% to 67% reflecting the improved liquiditysituation of the Bank.

Retail Bank

The Retail Bank consists of Commercial and Consumer Assets andAgri Lending. This business is also responsible for the majority ofthe branch network and deposit mobilization. In 2010, the RetailBank undertook some major new initiatives and product introductionsto supplement the menu of products and services.

The liabilities and branch banking business had a strong year, resultingin an improved deposit mix. Low cost deposit generation remainedthe key element of the deposit strategy and enabled the Bank toachieve a significantly lower cost of deposits. For the asset businesses,2010 was a year of consolidation, focusing on leveraging the rightmix of technology and people to manage the portfolio. There wasalso a focus on the newly introduced Relationship Model, to bestdeploy the strengths of the branch network in initiating and managingasset relationships.

Market conditions are still not conducive for large scale consumerlending. Consequently, the focus was on quality acquisitions, losscontainment from the legacy portfolio, and cost rationalization. Thisstrategy was complemented with key strategic alliances on both theacquisitions and the collections fronts, and initiatives to improve theoffering and service levels to our existing customers to maximizeloyalty.

During 2010, UBL also reached out to two significant segments; onewas the high net worth segment, through Signature, UBL's PriorityBanking offering. This has shown encouraging results in its first yearof operation, and is augmented by the introduction of the PremiumDebit MasterCard, a product which offers a range of benefits to theBank's large base of affluent customers.

The other segment targeted by the Retail Bank was the youth. Over70% of the population of Pakistan is under the age of 21, and varioustargeted offerings were developed for this market. UBL First MinorSavings Account, a product with exciting benefits targeted specificallyat children and their parents, offers a creative vehicle for parents tosave for their children as well as to teach them about sound financialplanning. UBL First will also serve to introduce a new generation toUBL and build customers for life.

Islamic Bank

UBL's Islamic Banking business, “Ameen”, also took steps towardsestablishing itself with an additional dedicated Islamic Banking branchand better leveraging of the availability of Islamic Banking servicesthroughout all UBL branches, including specialist Islamic Bankingwindows in key areas. The business doubled its deposit base in2010, and expects further strong growth in 2011.

Corporate Bank

The Corporate Banking Group at UBL continues to remain a preferredprovider of strategic and structured financial solutions to the top tiercorporate clientele in Pakistan. Backed by an experienced RelationshipManagement team stationed at Regional Corporate Centers across

United Bank Limited14

[ President & CEO Review 2010 ]

the country, the team is recognized for their knowledge and innovativesolutions which help maintain the highest quality of service standardsand further allows cross-sell of other UBL products within theInvestment Banking Group, Treasury, Trade Finance and CashManagement.

For the Corporate Bank, 2010 has been a year of proactivemanagement of its loan book, restructuring of stressed assets andrecovery. Despite the prevailing strained credit and economicenvironment, good progress was made as provisions declined by60% and NPL formation reduced substantially. However, with acontinued focused approach towards marketing, fees andcommissions revenue generated during the year increased by 50%over the previous year, primarily due to the innovative products andthe superior client servicing capabilities of the bank in the areas ofTrade Finance, Cash Management and Home Remittances.Complementing this healthy growth, operating cost increase wasrestricted to only 5%.

The Cash Management Business sustains its market leadershipposition and continued to provide around 31% growth over last year.Overall transaction volume handled reached nearly Rs 450 billionthrough provision of industry specific products and solutions forcollections and payments, despite increasing competitive pressures.The migration to the new core banking system (Symbols) is likely tofurther enhance maneuverability in terms of centralized data basemanagement and improved working capital cycle management.

The Home Remittances business during the year has furtherestablished UBL as a lead player, where market share has increasedto 18% recording an aggregate volume of US$1.7 billion. This YOYgrowth in volumes by around 43% is a result of continued supportof the Bank's correspondents all over the globe, persistent marketingefforts, development of new products and high quality servicestandards. UBL continued to launch innovative products for domesticand offshore clients, using its in-house state of the art cashmanagement and net banking solutions. Products like TezraftaarCheque and Account to Account Transfer have been in the marketfor some time while “Tezraftaar Cash” - Cash Over the Counterproduct was introduced during the year and was a significantcontributor towards attainment of these volumes. UBL plans tofurther expand its presence through actively pursuing foreigncounterparty tie-ups with the support from the Pakistan RemittanceInitiative and has already taken several steps in this direction.

Investment Banking

Despite a difficult environment, the Investment Banking Group (IBG)maintained its leadership in the domestic market during 2010. UBLcontinues to build on its Middle East initiative with a significant risein overseas earnings supplementing domestic revenues. A landmarktransaction during 2010 was the successful close of the first eversyndicated project finance transaction in Yemen amounting toUS$ 20 million.

Debt Capital Markets & Syndications remained a strong performerby successfully concluding a number of large and importanttransactions including leading one of the most high profile localmarket transactions of the year, i.e. the Rs 8 billion syndicatedfinancing facility for Qasim International Container Terminal.

Project & Structured Finance remained the largest contributor toIBG's fee earnings for the fifth consecutive year. Focus for the yearwas on soliciting and executing non-fund-based project advisoryassignments domestically, most notably that for a hydro powerproject sponsored by a Government of Korea owned entity. The

Middle East initiative remained a priority area during the year,especially in Yemen and the smaller UAE emirates with a focus onthe Energy and Power sectors.

The Equity & Advisory business emerged as a strong private equityshop within the domestic banking industry, aimed at developing andgrowing a middle-market M&A expertise both in Pakistan and theGCC. Carrying a sustainable deal pipeline into 2011, the businesshas gained significant momentum over the last eighteen months witha notable success being the successful arrangement of foreign directinvestment by a Korean multinational in one of the country's mostnotable food brands.

International

The impact of the global financial crisis that started in 2008 continuedto be felt in 2010, however, in general, macroeconomic stability wasseen in most GCC economies. Oil prices continued to rise andenhanced the revenue generation of two key markets of the franchise,Abu Dhabi and Qatar. The restructuring of the Dubai Worldconglomerate provided a much needed boost and helped reviveinvestor confidence in the region. This was evidenced by the launchof new bonds that were extremely well received and heavily over-subscribed.

The International Business continued to remain focused on liquiditymanagement, asset quality management and expense control.

The Asset portfolio was under constant scrutiny in every territorythrough proactive relationship management and prudent risk taking.Corporate Banking, the mainstay of the bank in most of the overseasoperations, performed well, and the bank continued to do businesswith top rated borrowers. Delinquencies in the unsecured retailportfolio have stabilized; however, the mortgage portfolio in UAEsuffered on account of the further downturn in the real estate market.

The overall lending was very closely monitored, with prudentprovisioning of loans as evidenced by the improvement in thecoverage ratio.

The Bank successfully completed the first syndicated investmentbanking transaction for a private power project in Yemen. This wasthe first ever transaction of its nature in Yemen and also the first everfor the Bank outside Pakistan. It has opened up new avenues forrevenue generation for the international operations and also enhancedthe brand image of the franchise.

Going forward, the international business of the bank is well positionedto build on the momentum started in 2010 with particular emphasison optimizing the existing customer base, focusing on non-fundincome streams and continuing proactive risk management strategies.The business remains alert to potential opportunities and will continueto enhance its presence both in existing and in new markets, whereappropriate returns are available.

Branchless & E-Banking

UBL rolled out the commercial launch of “Branchless Banking” inApril 2010. The array of services offered include basic bankingservices such as account opening, cash withdrawals and depositsas well as several value added services including remittances, billpayments and purchase of mobile airtime. Branchless Banking usershave access to multiple channels including ATMs and Phone Banking.In its first eight months, UBL Omni has managed to grow to a networkof more than 2,300 Dukaans (i.e. retail business agents) spreadacross more than 350 cities and towns of Pakistan. In 2010, more

Annual Report 2010 15

than 4 million transactions amounting to more than Rs 22 billionwere carried out through the Omni platform, including the paymentsto the flood affected population.

UBL Omni also managed to take the lead in transforming theGovernment to People (G2P) arena in Pakistan by working closelywith the GOP and multilateral agencies. The Bank provided transparentand efficient cash disbursement services for more than one millionflood affected people in KPK, Punjab, Sind and AJK, more than20,000 World Food Program beneficiaries and more than 400,000recipients of the Benazir Income Support Program in different remoteparts of Pakistan. These efforts have led UBL Omni to be recognizedas a benchmark and a role model for G2P payment services notonly locally but also internationally.

UBL Omni was also the recipient of a US$ 1.5 million grant by theBill & Melinda Gates Foundation through MEDA, for supporting theflood relief payments “Watan” project. In addition, the Bill & MelindaGates Foundation has also announced a US$ 6.9 million grantthrough ShoreBank to support enhanced financial inclusion of thecountry's underbanked population through UBL Omni. This grantwill be made available over a period of two years.

UBL Omni continues to create new and more efficient businessmodels and is already providing cash management services toFMCGs, fee collection services to schools and facilitating microfinanceinstitutions in increasing their reach by leveraging the 2,300 strongDukaan network for disbursements and collections services. UBLOmni plans to continue offering new products and services throughits platform. In addition to providing convenience to the Bank'scustomers, this channel also allows UBL to service its branchcustomers more efficiently by leveraging the agent network to divertroutine, repetitive transactions out of the branches.

Within the E-Banking area, products introduced by UBL over theyears such as Click-N-Remit, Click-N-Bank and NRP Direct havealready had wide acceptance. During 2010, UBL's Middle Eastbusiness was enabled to offer “netbanking” service to its customers- a feature that has been eagerly anticipated for a while by the Bank'sclients in those countries. At the same time, the internet bankingplatform is being enhanced locally to enable Corporate and SMEcustomers to also use this facility.

Treasury & Capital Markets

UBL promoted the introduction of SBP's electronic platform for GOPSecurities trading which was launched in January 2010. As a leadingPrimary Dealer, UBL provided support by actively trading on theBloomberg Electronic Bond platform, establishing itself as one ofthe top players for GOP Securities distribution. UBL has also beenranked amongst the top 3 Primary Dealers for the fiscal year 2009-2010.

UBL has been able to strengthen its liquidity management by investingin Securities portfolios which are generating regular inflows. TheInvestments portfolio has grown significantly and UBL has successfullytaken advantage of higher interest rates to optimize portfolio returns.

2010 saw a strong performance from the Treasury Sales desk witha focus towards greater client coverage in FX, Fixed Income andDerivatives products. The Treasury Sales team was strengthenedwith the addition of new dealers, along with formal training for theexisting staff. A separate Fixed Income desk was successfully setup and secondary market activity was doubled, making UBL a leadingplayer in the fixed income market.

A major milestone was the development and implementation of anew FX Sales system allowing streamlining of operational requirementsat all levels, and strengthening the MIS and transaction trackingsystem. Cross-functional training sessions were held for brancheshandling Foreign Exchange transactions, resulting in better clienthandling, transaction booking and efficient reporting. UBL hasimproved the turnover ratio for usage of its allocated limits andincreased its FX trading volumes resulting in substantial increase inprofitability

The Capital Markets team has consolidated and restructured itsEquity Trading portfolio and the Derivatives business continuesto provide innovative solutions and competitive pricing toCorporate clients.

Human Resources

In 2010 UBL maintained its focus on enhancing the quality of thestaff through development initiatives as well as induction of talent atvarious levels. As part of its annual plan, the Bank inducted over 180Retail Banking Officers and provided them comprehensive trainingin its Karachi, Lahore and Islamabad training centers, subsequentto which they have currently been assigned to various Retail branchesfor on-the-job training. The Bank also inducted 250 Cash officersinto the permanent cadre through a rigorous selection process afterhaving completed on-the-job training of over one year.

The emphasis on training and development of employees continued,with approximately 30,000 man days of training conducted duringthe year. The focus remained on enhancing technical and productknowledge with the goal of ultimately improving the service providedto the Bank's customers.

Investment was also initiated in the implementation of a state-of-theart employee and managerial self service system along with e-learningcapability. This is expected to be in place by early 2011 and willprovide the basis for enhanced skill and knowledge developmentcapability as well as management of staff related issues such as loanprocessing, leave applications, etc.

Nearly 200 UBL staff were also affected by the flooding in the country.The Bank provided all such staff logistical and financial support tohelp them in their hour of need.

Risk and Credit Policy

With the economy in a turbulent state, Risk & Credit Policy Groupincreased efforts to improve the Bank's risk management frameworkto bolster the asset quality of the corporate, commercial, consumerand international portfolios. Proactive portfolio management wasconducted through stringent monitoring of troubled accounts,specifically those of the Power and Textile sectors, coupled withfacilitating recovery through active restructuring. Steps were takento enhance the efficiency of the approval process through appropriatedelegation of credit approval authority, along with automation of theapproval process.

A comprehensive Risk Management Policy was finalized in 2010.This is an umbrella policy which develops an integrated frameworkto encompass Liquidity, Agricultural Credit, International/Local Credit,Market as well as Human Resource risk. An Agriculture Credit Policyhas also been developed and finalized over the year. Efforts toimplement the Operational Risk Management Framework across theBank have been ongoing and deployment of an Operational Risk

United Bank Limited16

[ President & CEO Review 2010 ]

Monitor system is one of the major milestones in this regard. In orderto automate the loan origination process for Corporate, Commercialand SME borrowers, a Loan Origination (LO) module has also beenindigenously designed. During the year the LO has been successfullyimplemented for SME and Consumer loans in Karachi and this isexpected to be rolled out Bank-wide in 2012.

For the equity trading portfolio, a value-at-risk methodology hasbeen implemented and is being back tested, while for the derivativesportfolio a revised mechanism has been rolled out for measurementand monitoring of pre-settlement risk. Market Risk limit settingmechanisms have also been revised to rely on quantitative ratherthan subjective methods. With regards to consumer credit, behavioralscoring and automated delinquent collection strategies have beenimplemented in order to perform customer segregation and thesubsequent curative action in a more efficient manner. UBL is alsoin the process of implementing an Application Scoring model, whichwill enable the risk decision makers to allocate limits/pricing facilitieson the basis of risk profile. Steps have also been taken towardsbetter information management during the year, with the Credit Policy& Research Division providing regular updates to business units onmajor macroeconomic and specific industry related happenings.

Core Banking Platform Implementation (Project Genesis)

During the year 2010, Project Genesis achieved a major milestone;six branches went live on the new Core Banking System (CBS).These included three Retail Branches and the Corporate branch ofKarachi besides Mortgage and Personal loan branches. This enabledthe bank to test the CBS with almost the entire spectrum oftransactions being conducted in UBL. With this migration, UBL alsoachieved a single Customer Information File for all the Bank'scustomers, providing a full view of all the customer's products withthe Bank.

The Enterprise Banking Suite (EBS) is the front end solution for CBScomprising the customer service platform (CSP) and the loanorigination system (LOS). CSP is a customer relationship managementtool and has been rolled out in over 350 branches. LOS has beenimplemented for Commercial loans and Consumer products and isunderway for Corporate loans and Credit Cards. During 2011, CSPwill be rolled out across the country while LOS implementation forall products will be completed in 2012. The implementation andintegration of CBS and EBS has provided seamless end to endprocessing for customer transactions.

Corporate Social Responsibility

UBL undertook several initiatives in its role as a good CorporateCitizen, which are described in detail on Page 12. The most importantof these was where UBL and its employees contributed nearly Rs38 million towards helping their fellow countrymen who were badlyaffected by the floods. UBL provided flood affectees with a unique“LifeStraw” filter, each of which purifies enough dirty water to caterto a family of five for 3 years. This not only ameliorated their immediateconcerns of access to clean drinking water, but had an equallyimportant secondary impact of staving off water-borne diseases, agreat threat in those conditions. UBL also ran a campaign encouragingthe general public to contribute towards this initiative and receivedgenerous contributions which were matched by UBL.

Conclusion

Through a difficult year, UBL has demonstrated a strong performance.This has been made possible through attention to several core issues,stringent monitoring of asset quality and credit performance andhiring and development of high quality talent. While the Bank remainsconscious of costs, it continues to make selective investments intechnology and new products and channels to maintain its reputationas an innovator. Although economic conditions remain challenging,the actions taken during the year position the Bank well to build onits solid base and take advantage of opportunities both locally andin overseas markets.

Atif R. BokhariPresident & CEO

Karachi.February 22, 2011

Annual Report 2010 17

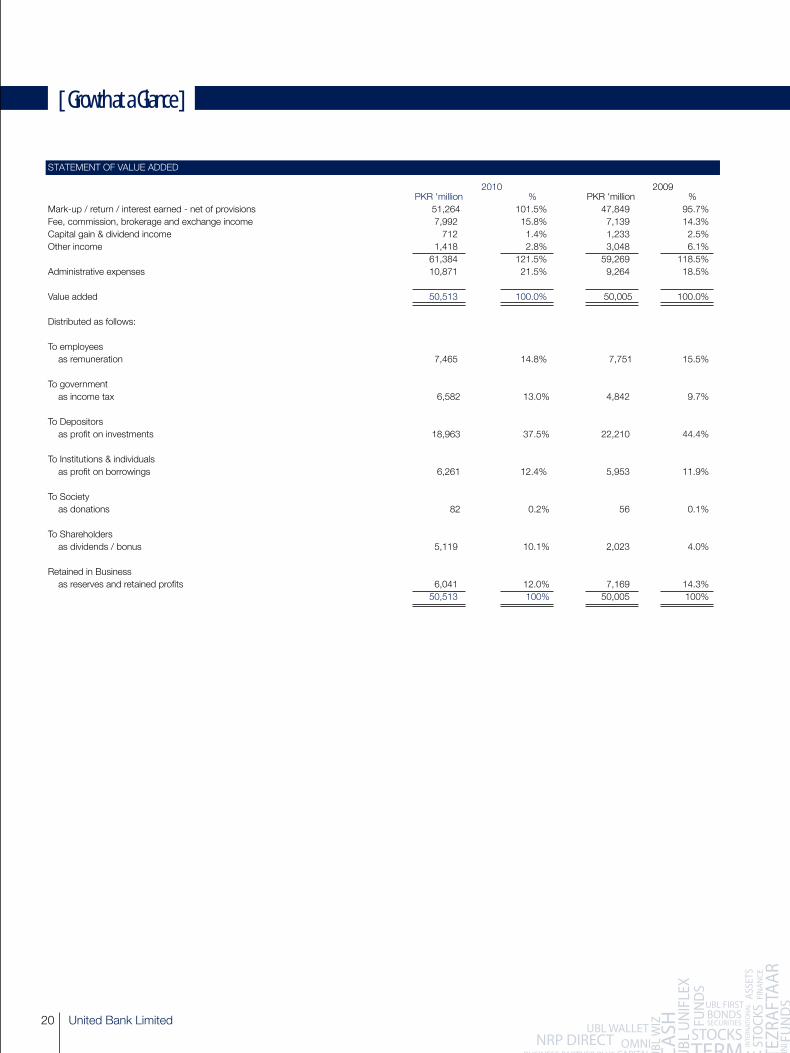

[ Growth at a Glance ]

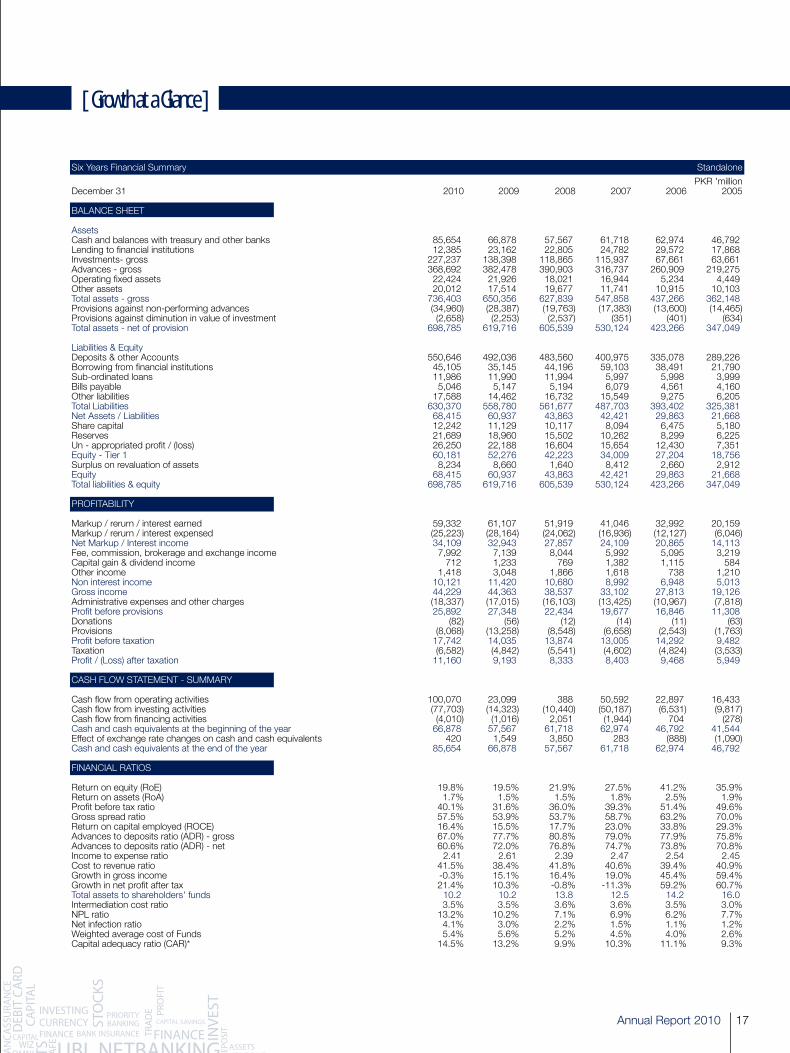

Six Years Financial Summary Standalone

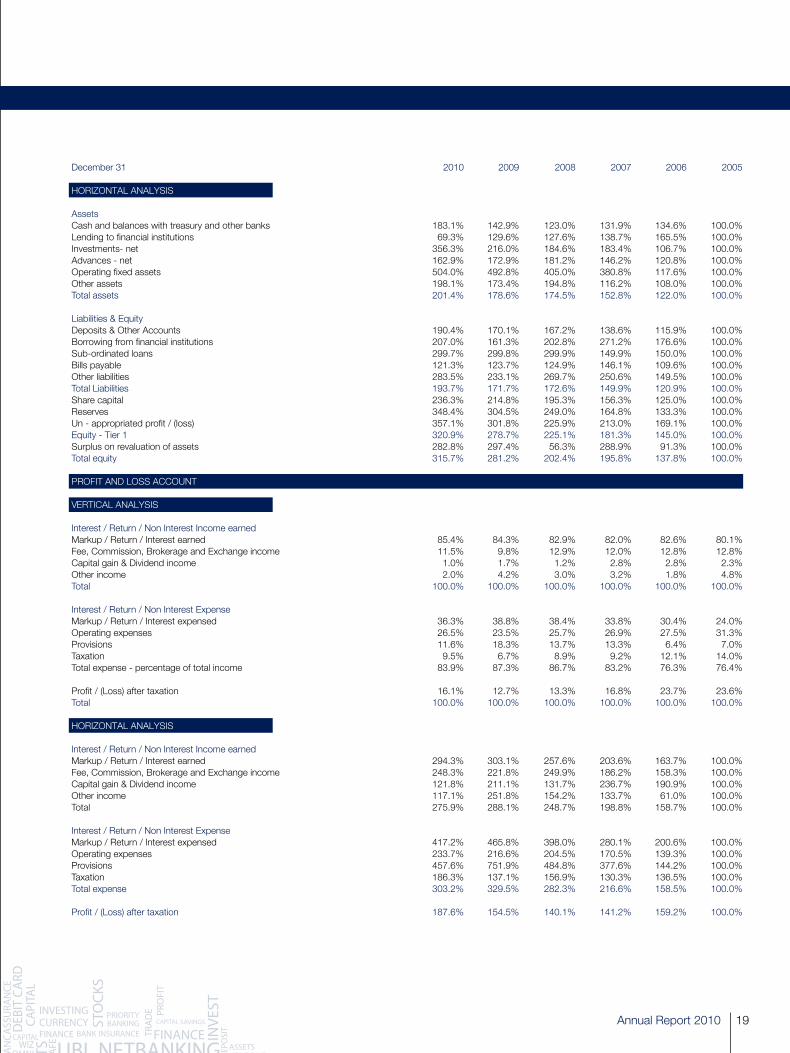

PKR 'millionDecember 31 2010 2009 2008 2007 2006 2005

BALANCE SHEET Assets Cash and balances with treasury and other banks 85,654 66,878 57,567 61,718 62,974 46,792Lending to financial institutions 12,385 23,162 22,805 24,782 29,572 17,868Investments- gross 227,237 138,398 118,865 115,937 67,661 63,661Advances - gross 368,692 382,478 390,903 316,737 260,909 219,275Operating fixed assets 22,424 21,926 18,021 16,944 5,234 4,449Other assets 20,012 17,514 19,677 11,741 10,915 10,103Total assets - gross 736,403 650,356 627,839 547,858 437,266 362,148Provisions against non-performing advances (34,960) (28,387) (19,763) (17,383) (13,600) (14,465)Provisions against diminution in value of investment (2,658) (2,253) (2,537) (351) (401) (634)Total assets - net of provision 698,785 619,716 605,539 530,124 423,266 347,049 Liabilities & Equity Deposits & other Accounts 550,646 492,036 483,560 400,975 335,078 289,226Borrowing from financial institutions 45,105 35,145 44,196 59,103 38,491 21,790Sub-ordinated loans 11,986 11,990 11,994 5,997 5,998 3,999Bills payable 5,046 5,147 5,194 6,079 4,561 4,160Other liabilities 17,588 14,462 16,732 15,549 9,275 6,205Total Liabilities 630,370 558,780 561,677 487,703 393,402 325,381Net Assets / Liabilities 68,415 60,937 43,863 42,421 29,863 21,668Share capital 12,242 11,129 10,117 8,094 6,475 5,180Reserves 21,689 18,960 15,502 10,262 8,299 6,225Un - appropriated profit / (loss) 26,250 22,188 16,604 15,654 12,430 7,351Equity - Tier 1 60,181 52,276 42,223 34,009 27,204 18,756Surplus on revaluation of assets 8,234 8,660 1,640 8,412 2,660 2,912Equity 68,415 60,937 43,863 42,421 29,863 21,668Total liabilities & equity 698,785 619,716 605,539 530,124 423,266 347,049 PROFITABILITY Markup / rerurn / interest earned 59,332 61,107 51,919 41,046 32,992 20,159Markup / rerurn / interest expensed (25,223) (28,164) (24,062) (16,936) (12,127) (6,046)Net Markup / Interest income 34,109 32,943 27,857 24,109 20,865 14,113Fee, commission, brokerage and exchange income 7,992 7,139 8,044 5,992 5,095 3,219Capital gain & dividend income 712 1,233 769 1,382 1,115 584Other income 1,418 3,048 1,866 1,618 738 1,210Non interest income 10,121 11,420 10,680 8,992 6,948 5,013Gross income 44,229 44,363 38,537 33,102 27,813 19,126Administrative expenses and other charges (18,337) (17,015) (16,103) (13,425) (10,967) (7,818)Profit before provisions 25,892 27,348 22,434 19,677 16,846 11,308Donations (82) (56) (12) (14) (11) (63)Provisions (8,068) (13,258) (8,548) (6,658) (2,543) (1,763)Profit before taxation 17,742 14,035 13,874 13,005 14,292 9,482Taxation (6,582) (4,842) (5,541) (4,602) (4,824) (3,533)Profit / (Loss) after taxation 11,160 9,193 8,333 8,403 9,468 5,949 CASH FLOW STATEMENT - SUMMARY Cash flow from operating activities 100,070 23,099 388 50,592 22,897 16,433Cash flow from investing activities (77,703) (14,323) (10,440) (50,187) (6,531) (9,817)Cash flow from financing activities (4,010) (1,016) 2,051 (1,944) 704 (278)Cash and cash equivalents at the beginning of the year 66,878 57,567 61,718 62,974 46,792 41,544Effect of exchange rate changes on cash and cash equivalents 420 1,549 3,850 283 (888) (1,090)Cash and cash equivalents at the end of the year 85,654 66,878 57,567 61,718 62,974 46,792 FINANCIAL RATIOS Return on equity (RoE) 19.8% 19.5% 21.9% 27.5% 41.2% 35.9%Return on assets (RoA) 1.7% 1.5% 1.5% 1.8% 2.5% 1.9%Profit before tax ratio 40.1% 31.6% 36.0% 39.3% 51.4% 49.6%Gross spread ratio 57.5% 53.9% 53.7% 58.7% 63.2% 70.0%Return on capital employed (ROCE) 16.4% 15.5% 17.7% 23.0% 33.8% 29.3%Advances to deposits ratio (ADR) - gross 67.0% 77.7% 80.8% 79.0% 77.9% 75.8%Advances to deposits ratio (ADR) - net 60.6% 72.0% 76.8% 74.7% 73.8% 70.8%Income to expense ratio 2.41 2.61 2.39 2.47 2.54 2.45Cost to revenue ratio 41.5% 38.4% 41.8% 40.6% 39.4% 40.9%Growth in gross income -0.3% 15.1% 16.4% 19.0% 45.4% 59.4%Growth in net profit after tax 21.4% 10.3% -0.8% -11.3% 59.2% 60.7%Total assets to shareholders' funds 10.2 10.2 13.8 12.5 14.2 16.0Intermediation cost ratio 3.5% 3.5% 3.6% 3.6% 3.5% 3.0%NPL ratio 13.2% 10.2% 7.1% 6.9% 6.2% 7.7%Net infection ratio 4.1% 3.0% 2.2% 1.5% 1.1% 1.2%Weighted average cost of Funds 5.4% 5.6% 5.2% 4.5% 4.0% 2.6%Capital adequacy ratio (CAR)* 14.5% 13.2% 9.9% 10.3% 11.1% 9.3%

United Bank Limited18

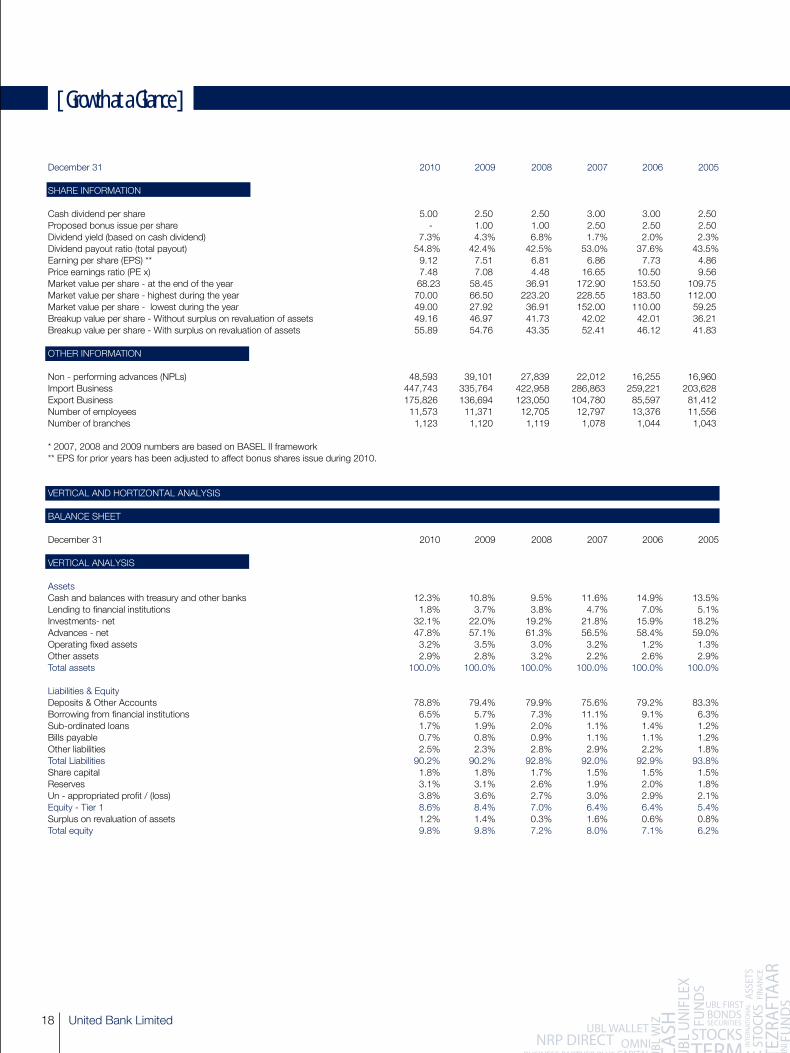

[ Growth at a Glance ]

December 31 2010 2009 2008 2007 2006 2005 SHARE INFORMATION Cash dividend per share 5.00 2.50 2.50 3.00 3.00 2.50Proposed bonus issue per share - 1.00 1.00 2.50 2.50 2.50Dividend yield (based on cash dividend) 7.3% 4.3% 6.8% 1.7% 2.0% 2.3%Dividend payout ratio (total payout) 54.8% 42.4% 42.5% 53.0% 37.6% 43.5%Earning per share (EPS) ** 9.12 7.51 6.81 6.86 7.73 4.86Price earnings ratio (PE x) 7.48 7.08 4.48 16.65 10.50 9.56Market value per share - at the end of the year 68.23 58.45 36.91 172.90 153.50 109.75Market value per share - highest during the year 70.00 66.50 223.20 228.55 183.50 112.00Market value per share - lowest during the year 49.00 27.92 36.91 152.00 110.00 59.25Breakup value per share - Without surplus on revaluation of assets 49.16 46.97 41.73 42.02 42.01 36.21Breakup value per share - With surplus on revaluation of assets 55.89 54.76 43.35 52.41 46.12 41.83 OTHER INFORMATION Non - performing advances (NPLs) 48,593 39,101 27,839 22,012 16,255 16,960Import Business 447,743 335,764 422,958 286,863 259,221 203,628Export Business 175,826 136,694 123,050 104,780 85,597 81,412Number of employees 11,573 11,371 12,705 12,797 13,376 11,556Number of branches 1,123 1,120 1,119 1,078 1,044 1,043 * 2007, 2008 and 2009 numbers are based on BASEL II framework ** EPS for prior years has been adjusted to affect bonus shares issue during 2010.