uaf cas and disclosure statement workshop - alaska.edu · uaf cas and disclosure statement workshop...

TRANSCRIPT

UAF CAS AND DISCLOSURE

STATEMENT WORKSHOP BUTROVICH BUILDING, BOR ROOM 109

Thursday, January 26, 2006

AGENDA

9:00 –9:10 Overview and History 9:10 – 9:20 Definitions 9:20 – 10:00 Cost Accounting Standards 10:00 – 10:15 Break 10:15 – 11:00 Identifying Compliance Issues Through the Accounting System

1

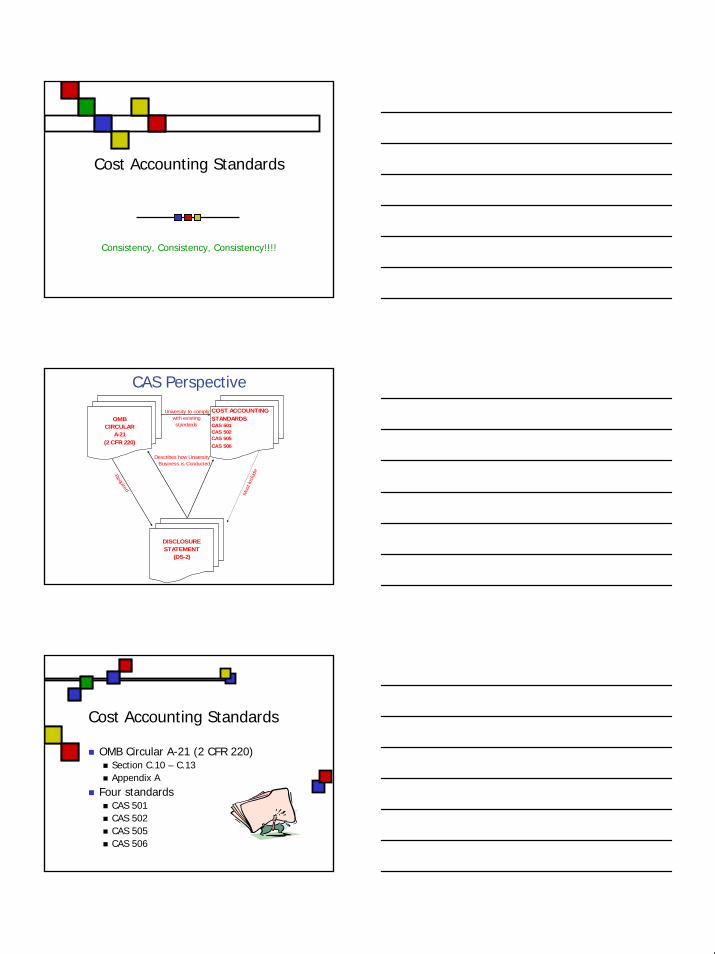

Cost Accounting Standards &Compliance Issues

Ginger BakerUA Statewide Systems Office

Office of Cost AnalysisJanuary 26, 2006

Agenda

History of CASDefinitionsCost Accounting StandardsCompliance Issues

Overview and History

Cost Accounting Standards (CAS)Result of government concern over

Contractor pricing Accounting practices of defense contractorsLack of consistency

2

Overview and History

1968 - 1989Feasibility StudyCreation of Cost Accounting Standards Board (CASB)CASB created CAS

19 commercial standardsImplemented standards in 1980

Overview and History

InitiallyApplied to negotiated defense contracts > $100,000

Threshold increased to $500,000 in 1988 and applied to all federal contracts

Educational institutions were exempted from CAS

Overview and History

CASB dissolvedCASB reestablished

Permanent, independent boardOffice of Federal Procurement Policy in OMB

3

Overview and History

1990-1995Significant F&A cost concerns and scandals at Universities CAS coverage extended to colleges and universities in 19944 StandardsDisclosure required if certain thresholds are exceeded

Overview and History

1996Amendment to A-21

Emphasis on consistency among and within institutionsIncorporates the four cost accounting standardsDisclosure statement requirements

Circular A-21, C.14Extends coverage of A-21 to all sponsored agreements at colleges and universities

Contracts and grants regardless of award amount

Overview and History

2003Government’s focus is on

Consistency and standardization

Institutions must be proactive in identifying compliance problems

4

Overview and History

2005OMB Circular A-21

Moved to Part 220 in 2 CFR (2 CRF 220)Chapter 2 of Subtitle A, Title 2

Definitions

A lot of words!

DefinitionsDefinitions

Cost objective A specific or major function of the institution, a particular service or project, sponsored agreement, or a facilities and administrative (F&A) cost activity

OMB Circular A-21, Section B.2.3.

Two categoriesDirectF&A (Indirect)

5

Definitions

Direct costThose costs that can be identified specifically with a particular sponsored project, an instructional activity, or any other institutional activity, or that can be directly assigned to these activities relatively easily with a high degree of accuracy.

OMB Circular A-21, Section D.1.

Definitions

F&A costs (Indirect Costs)Those costs incurred for common or joint objectives and therefore, cannot be identified readily and specifically with a particular sponsored project, an instructional activity, or any other institutional activity.

OMB Circular A-21, Section E.1.

Definitions

Allowable CostsCosts that are reasonable, allocable to sponsored agreements under principles and methods outlined A-21, given consistent treatment through application of those principles and methods, conform to any limitations or exclusions in A-21 or in the sponsored agreement as to types or amounts of cost items.

OMB Circular A-21, C.2.

6

Definitions

Unallowable costAny cost, which, under the provisions of any pertinent law, regulation, or sponsored agreement, cannot be included in prices, cost reimbursements, or settlements under Government sponsored agreement to which is is allocable.

CAS 9905.505-30 (4)

Definitions

ReasonableNature of goods or services acquired or applied, and the amount involved therefore, reflect the action that a prudent person would have taken under the circumstances prevailing at the time the decision to incur the cost was made.

OMB Circular A-21, C.2.

Definitions

AllocableA cost is allocable if

It is chargeable or assignable to a particular cost objective according to the relative benefit received or other equitable relationship.

OMB Circular A-21, Section C.4.a.

7

Definitions

Specifically, a cost is allocable to sponsored agreements if the cost

Is incurred to advance the work under the sponsored agreement;Benefits sponsored and other work

Proportions can be reasonably estimated; orIs necessary for the overall operation of the institution

OMB Circular A-21, Section C.4.a.

Definitions

AllocationProcess of assigning a cost, or a group of costs, to one or more cost objective, in reasonable and realistic proportion to the benefit provided or other equitable relationship.

OMB Circular A-21, Section B.2.3.

Definitions

Cost accounting practiceAny disclosed or established accounting method or technique which is used for allocation of cost to cost objectives, assignment of cost to cost accounting period, or measurement of cost

CAS 9903.302-1

8

Cost Accounting Standards

Consistency, Consistency, Consistency!!!!

CAS Perspective

Describes how UniversityBusiness is Conducted

University to complywith existingstandards

Required

Mus

t Inc

lude

OMB CIRCULAR

A-21(2 CFR 220)

COST ACCOUNTING STANDARDSCAS 501CAS 502CAS 505CAS 506

DISCLOSURESTATEMENT

(DS-2)

Cost Accounting Standards

OMB Circular A-21 (2 CFR 220)Section C.10 – C.13Appendix A

Four standardsCAS 501CAS 502CAS 505CAS 506

9

Cost Accounting Standards

Designed to achieve uniformity and consistency in the

Measurement, Assignment, and Allocation of costs to government contracts

Developed by the government in the interest of the government

Cost Accounting Standards

Cost Accounting Standards vs. Cost Principles (A-21)

CAS addresses measurement, assignment, and allocationA-21 addresses cost allowability

Costs that are not accounted for in accordance with CAS are unallowable

Cost Accounting Standards

Circular A-21 and CAS affect the accounting of funds from all funding sources due to

F&ACost sharing

10

Cost Accounting Standards

F&A University funds are included in the calculation of the F&A rate charged the federal government on sponsored agreements

Cost Accounting Standards

Distorted F&A cost rateIncorrect assignment and allocation of costs Results in an over or under recovery of F&A costs each time a project is billed for F&AAccumulated over recovery can result in repayment to the government

University funds sacrificed

Cost Accounting Standards

Cost sharingUniversity funds are included in total project costs funded by the federal government

Incorrect assignment of costs in rate calculationUnallowable costsMust be accounted for and reported

11

CAS 501CAS 501

Consistency in estimating, accumulating and reporting costs

CAS 501

Purpose Estimating practices for a proposal are consistent with cost accounting practices used in accumulating and reporting costsComparable transactions are treated alikeCost estimates are reliableImproved cost controlEnhanced accountability

CAS 501CAS 501

Fundamental requirementsEstimate costs same way that expenses are accumulated and reportedAccumulate and report costs consistent with cost estimating proceduresActual costs may be recorded in more detail than those provided in proposal estimates, but not vice versa

12

CAS 501

Techniques for applicationComparability

Must be able to compare costs estimated in proposal with actual costs

ConsistencyDirect or indirectAssignment to F&A cost pools Allocation methodologies

CAS 501

Examples of consistent practiceExample 1

Proposal estimateAverage direct labor rate by category

ActualActual labor recorded by the individual

Example 2Proposal estimate

Individual costs are estimated and identified to project in budget

ActualCosts are charged directly to the project as incurred

CAS 501

Examples of inconsistent practice Proposal estimate

PI effort proposed on a research project is the anticipated effort required to successfully perform the project

ActualEffort devoted to the project is charged to the restricted fund to the extent of available funding. Effort devoted to the project, but paid from general funds, is charged to an instruction account

13

CAS 502

Consistency in allocating costs incurred for the same purpose

CAS 502

PurposeEach type of cost is allocated only once and on only one basis to any contract or other cost objectiveCriteria for allocating costs to sponsored agreements is same for all similar cost objectivesPrevent overcharging, double counting, or double dipping

CAS 502

Fundamental requirementsAll costs incurred for the same purpose in like circumstances are either direct or indirect only If a sponsored agreement is charged directly for a cost, no other similar costs incurred for the same purpose, in like circumstances, can be in the F&A cost pools and subsequently the F&A rate (and vice versa)

14

CAS 502

Techniques for applicationApply to estimates used in proposals and to actual costsDescribe in DS-2 which cost items are direct which are indirectDescribe criteria of dissimilar circumstances and/or different purposes for hybrid costs

CAS 502

Examples of costs not incurred for same purpose

Test equipment costsSpecial - charged directlyGeneral purpose - normally indirectAccounting treatment disclosed

CAS 502

Example of costs incurred for same purpose

Purchasing supportIndirect costSponsored project requires disproportionate amount of subcontract administrationCosts cannot be charged both directly and indirectly

15

CAS 502

Costs incurred in preparing and submitting proposal

Renewal proposalExisting award’s specific requirement

Direct cost of existing contractExisting award has no specific requirement

Indirect cost of departmentNew Proposals

Indirect cost of department

CAS 502

Fire protection10 general firefighters

Indirect cost

New contract requires 3 firemen at fixed post 24 hours due to high risk materials

Direct cost

Circular A-21, Section F.6.b

Dept administration expenses“…special care should be exercised to ensure that costs incurred for the same purpose, in like circumstances, are treated consistently as either direct costs or F&A costs.”

16

Circular A-21, Section F.6.b

Normally directTechnical staff salaries, lab supplies, telephone toll charges, animals and care costs, computer costs travel costs, and specialized shop costsIdentifiable to particular project

Circular A-21, Section F.6.b

Normally F&AAdministrative & clerical salariesOffice suppliesPostageLocal telephone costsMemberships

Circular A-21, Section F.6.b

Potential different circumstancesNature of activity is not the sameDirect charging of administrative & clerical salaries may be appropriate where a major project or activity

Explicitly budgets for administrative or clerical services ANDIndividuals can be specifically identified with project or activity

17

Circular A-21, Section F.6.b

“Major project is defined as a project that requires an extensive amount of administrative or clerical support, which is significantly greater than the routine level of such services provided by academic departments.”

Circular A-21, Exhibit C

Criteria Inappropriate to charge these costs directly to a specific sponsored agreement if, in similar circumstances, the costs of performing the same type of activity for other sponsored agreements is included in department administration costs.

CAS 505

Accounting for Unallowable Costs

18

CAS 505

Purpose Facilitate the negotiation, audit, administration and settlement of sponsored agreements by establishing the guidelines covering

Identification of unallowable costsConsistent cost accounting treatment of all costs, including unallowable costs

Does not address which costs are allowable

CAS 505

Fundamental requirementsTwo types

Costs expressly unallowable by sponsor, laws, or rulesCosts directly associated with unallowable costs

Identify and exclude all costs from any billing, claim, application or proposal that are

Expressly unallowable ORMutually agreed to be unallowable

CAS 505

All unallowable costs are subject to the same cost accounting principles as allowable costs

Allocable

19

CAS 505

Fully allocate overrun costs to agreementsCost overruns must be identified

Amount over ceilingNot thru specific identification of particular cost items

CAS 505

Techniques for applicationDocumentation required as support for proposals, billings, or claims must be adequate to

Identify unallowable costs through specific account codes and program codesIdentify cost accounting treatment of the unallowable costs

CAS 505

A-21, Section JExamples of unallowables

AdvertisingAlumni activitiesBad debtDependent/spouse tuition waiversAlcoholic beveragesDonations

20

CAS 506

Cost Accounting Period

CAS 506

PurposeProvide criteria for the selection of cost accounting time periods for F&A rate developmentEnhance objectivity, consistency, and verifiability, and promote uniformity and comparability in sponsored agreement measurements

CAS 506

Fundamental requirementUse fiscal year, except

Costs of indirect function which exists for part of fiscal year may be allocated to cost objectives of same periodAnother annual period may be used if an established practice at institution

Recharge activities may have a different year

21

CAS 506

Same accounting period used for both F&A pool and direct base costsSame accounting period used for both F&A pool and direct base costs

CAS 506

Techniques for ApplicationGovernment can agree to allow institution to use a fixed annual period other than its fiscal year

10 minute break!10 minute break!

22

Case Study - CAS Compliance

From Cradle to Grave

January 26, 2006

The Principal Investigator

Associate Professor NewtouCollege of Useful InformationDepartment of Germane Data

The Sponsor

23

The Pre-Proposal

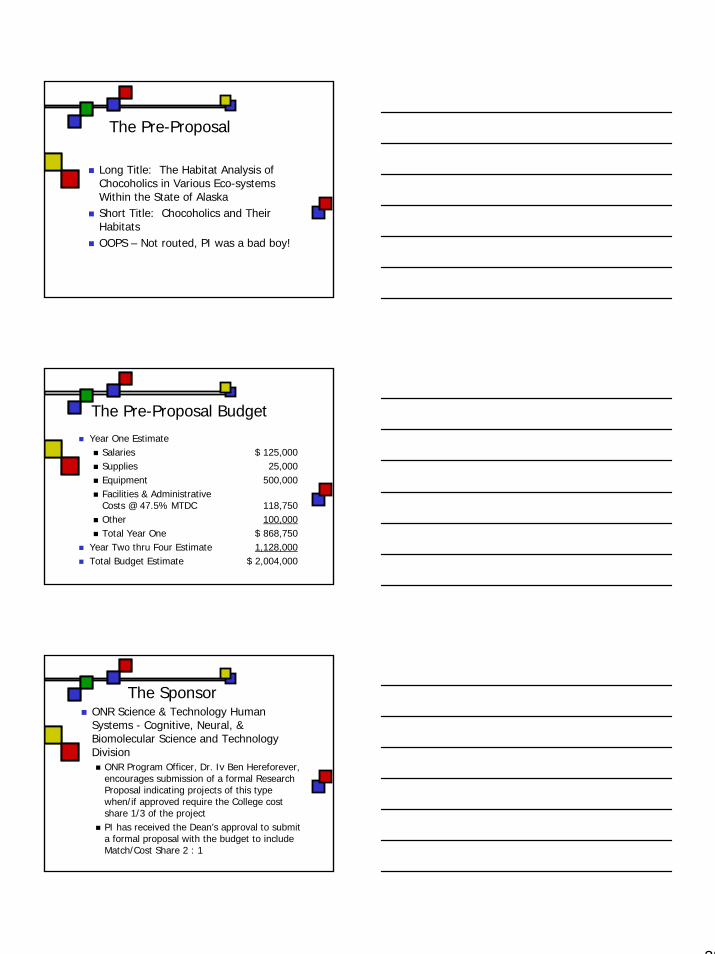

Long Title: The Habitat Analysis of Chocoholics in Various Eco-systems Within the State of AlaskaShort Title: Chocoholics and Their HabitatsOOPS – Not routed, PI was a bad boy!

The Pre-Proposal Budget

Year One EstimateSalaries $ 125,000Supplies 25,000Equipment 500,000Facilities & Administrative Costs @ 47.5% MTDC 118,750Other 100,000Total Year One $ 868,750

Year Two thru Four Estimate 1,128,000Total Budget Estimate $ 2,004,000

The Sponsor ONR Science & Technology Human Systems - Cognitive, Neural, & Biomolecular Science and Technology Division

ONR Program Officer, Dr. Iv Ben Hereforever, encourages submission of a formal Research Proposal indicating projects of this type when/if approved require the College cost share 1/3 of the projectPI has received the Dean’s approval to submit a formal proposal with the budget to include Match/Cost Share 2 : 1

24

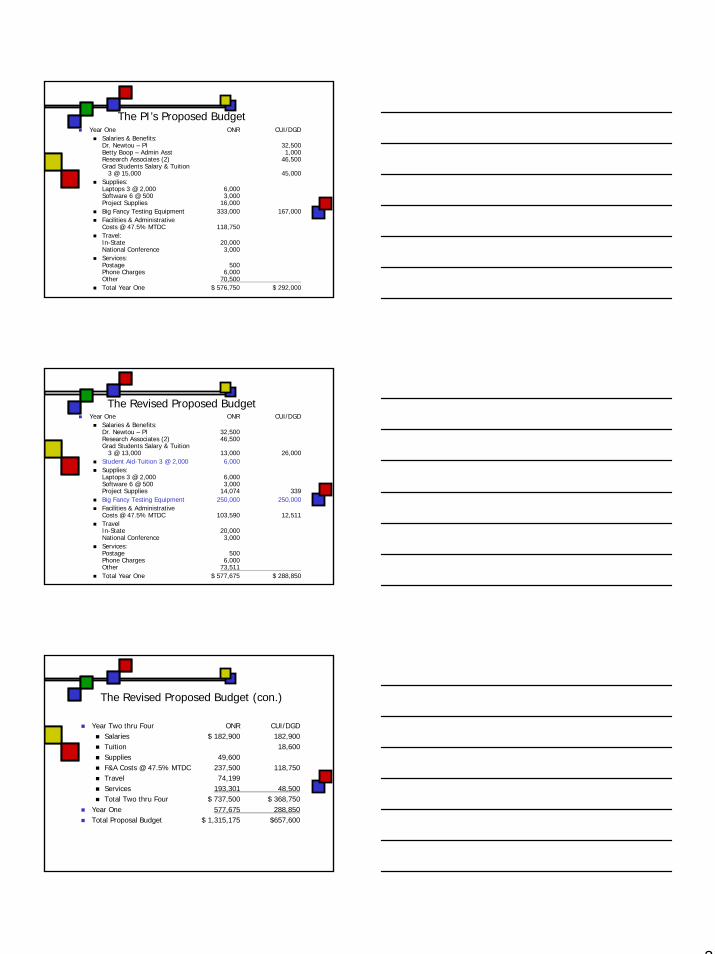

The PI’s Proposed BudgetYear One ONR CUI/DGD

Salaries & Benefits: Dr. Newtou – PI 32,500Betty Boop – Admin Asst 1,000Research Associates (2) 46,500Grad Students Salary & Tuition

3 @ 15,000 45,000Supplies:Laptops 3 @ 2,000 6,000Software 6 @ 500 3,000Project Supplies 16,000Big Fancy Testing Equipment 333,000 167,000Facilities & Administrative Costs @ 47.5% MTDC 118,750Travel:In-State 20,000National Conference 3,000Services:Postage 500Phone Charges 6,000Other 70,500Total Year One $ 576,750 $ 292,000

The Revised Proposed BudgetYear One ONR CUI/DGD

Salaries & Benefits: Dr. Newtou – PI 32,500Research Associates (2) 46,500Grad Students Salary & Tuition

3 @ 13,000 13,000 26,000Student Aid-Tuition 3 @ 2,000 6,000Supplies:Laptops 3 @ 2,000 6,000Software 6 @ 500 3,000Project Supplies 14,074 339Big Fancy Testing Equipment 250,000 250,000Facilities & Administrative Costs @ 47.5% MTDC 103,590 12,511TravelIn-State 20,000National Conference 3,000Services:Postage 500Phone Charges 6,000Other 73,511Total Year One $ 577,675 $ 288,850

The Revised Proposed Budget (con.)

Year Two thru Four ONR CUI/DGDSalaries $ 182,900 182,900Tuition 18,600Supplies 49,600F&A Costs @ 47.5% MTDC 237,500 118,750Travel 74,199Services 193,301 48,500Total Two thru Four $ 737,500 $ 368,750

Year One 577,675 288,850Total Proposal Budget $ 1,315,175 $657,600

25

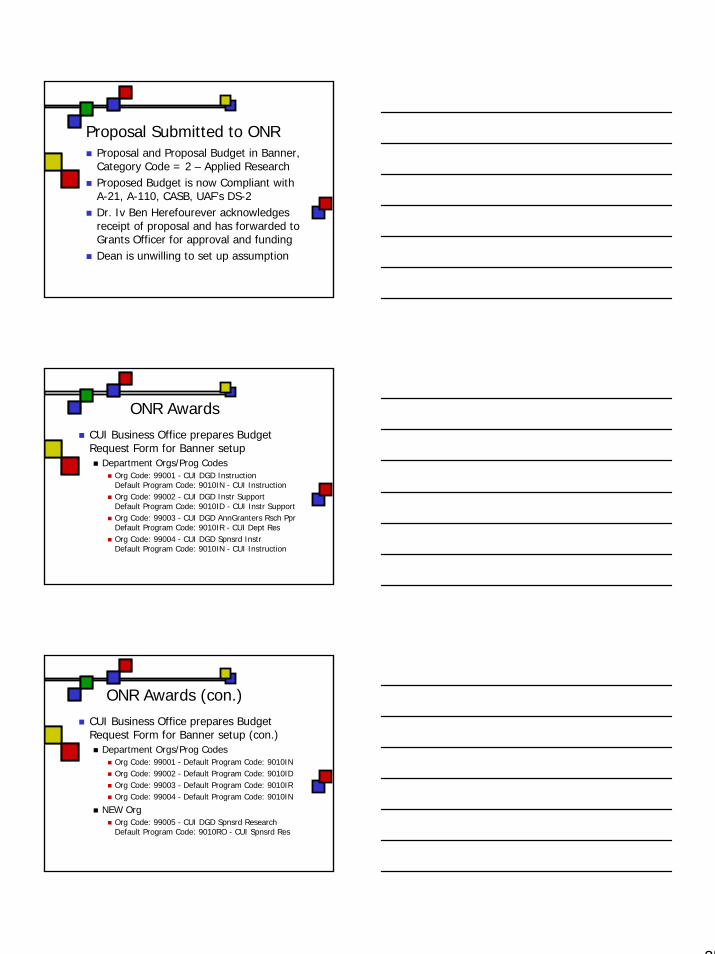

Proposal Submitted to ONRProposal and Proposal Budget in Banner, Category Code = 2 – Applied ResearchProposed Budget is now Compliant with A-21, A-110, CASB, UAF’s DS-2Dr. Iv Ben Herefourever acknowledges receipt of proposal and has forwarded to Grants Officer for approval and fundingDean is unwilling to set up assumption

ONR AwardsCUI Business Office prepares Budget Request Form for Banner setup

Department Orgs/Prog CodesOrg Code: 99001 - CUI DGD InstructionDefault Program Code: 9010IN - CUI InstructionOrg Code: 99002 - CUI DGD Instr SupportDefault Program Code: 9010ID - CUI Instr SupportOrg Code: 99003 - CUI DGD AnnGranters Rsch PprDefault Program Code: 9010IR - CUI Dept ResOrg Code: 99004 - CUI DGD Spnsrd InstrDefault Program Code: 9010IN - CUI Instruction

ONR Awards (con.)CUI Business Office prepares Budget Request Form for Banner setup (con.)

Department Orgs/Prog CodesOrg Code: 99001 - Default Program Code: 9010IN Org Code: 99002 - Default Program Code: 9010IDOrg Code: 99003 - Default Program Code: 9010IR Org Code: 99004 - Default Program Code: 9010IN

NEW OrgOrg Code: 99005 - CUI DGD Spnsrd ResearchDefault Program Code: 9010RO - CUI Spnsrd Res

26

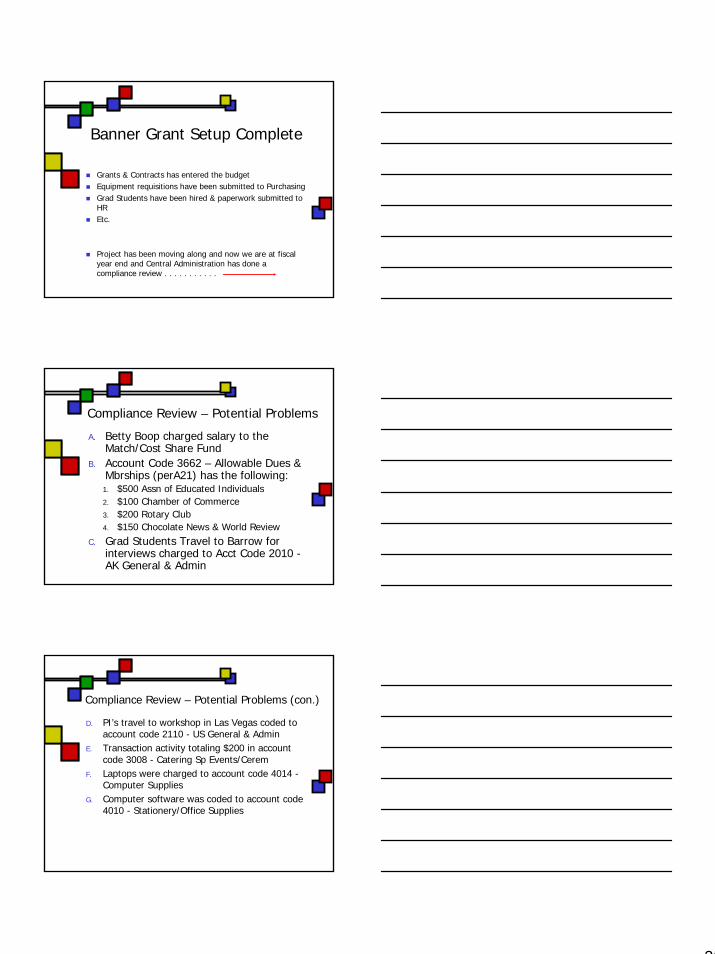

Banner Grant Setup Complete

Grants & Contracts has entered the budgetEquipment requisitions have been submitted to PurchasingGrad Students have been hired & paperwork submitted to HREtc.

Project has been moving along and now we are at fiscal year end and Central Administration has done a compliance review . . . . . . . . . . .

Compliance Review – Potential Problems

A. Betty Boop charged salary to the Match/Cost Share Fund

B. Account Code 3662 – Allowable Dues & Mbrships (perA21) has the following:

1. $500 Assn of Educated Individuals2. $100 Chamber of Commerce3. $200 Rotary Club4. $150 Chocolate News & World Review

C. Grad Students Travel to Barrow for interviews charged to Acct Code 2010 -AK General & Admin

Compliance Review – Potential Problems (con.)

D. PI’s travel to workshop in Las Vegas coded to account code 2110 - US General & Admin

E. Transaction activity totaling $200 in account code 3008 - Catering Sp Events/Cerem

F. Laptops were charged to account code 4014 -Computer Supplies

G. Computer software was coded to account code 4010 - Stationery/Office Supplies

27

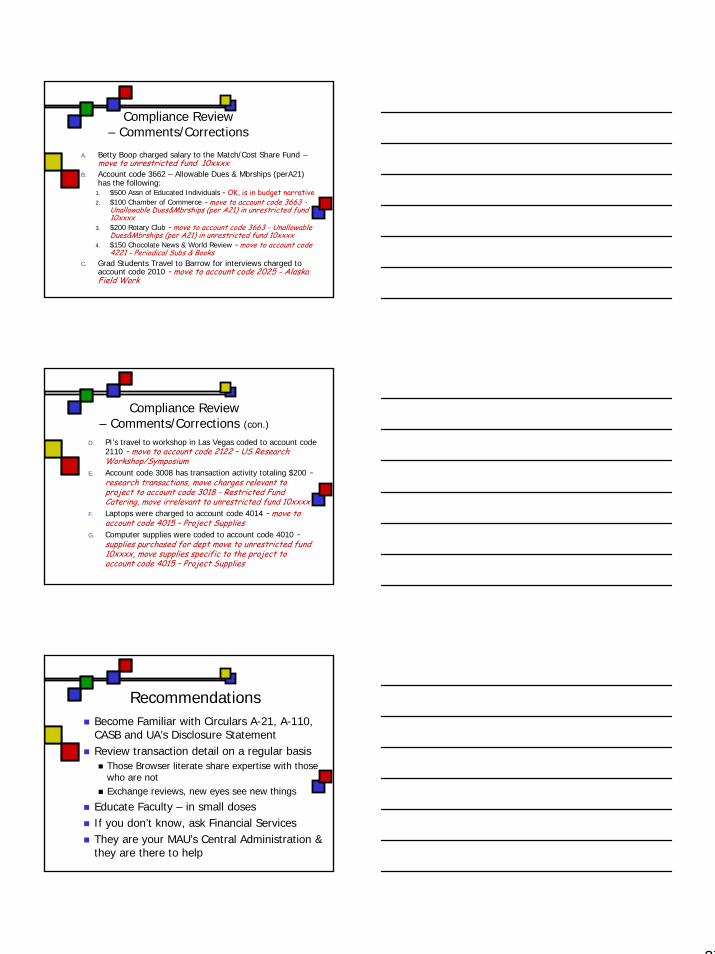

Compliance Review – Comments/Corrections

A. Betty Boop charged salary to the Match/Cost Share Fund –move to unrestricted fund 10xxxx

B. Account code 3662 – Allowable Dues & Mbrships (perA21) has the following:

1. $500 Assn of Educated Individuals – OK, is in budget narrative2. $100 Chamber of Commerce – move to account code 3663 -

Unallowable Dues&Mbrships (per A21) in unrestricted fund 10xxxx

3. $200 Rotary Club – move to account code 3663 - Unallowable Dues&Mbrships (per A21) in unrestricted fund 10xxxx

4. $150 Chocolate News & World Review – move to account code 4221 - Periodical Subs & Books

C. Grad Students Travel to Barrow for interviews charged to account code 2010 – move to account code 2025 - Alaska Field Work

Compliance Review – Comments/Corrections (con.)

D. PI’s travel to workshop in Las Vegas coded to account code 2110 – move to account code 2122 – US Research Workshop/Symposium

E. Account code 3008 has transaction activity totaling $200 –research transactions, move charges relevant to project to account code 3018 - Restricted Fund Catering, move irrelevant to unrestricted fund 10xxxx

F. Laptops were charged to account code 4014 – move to account code 4015 – Project Supplies

G. Computer supplies were coded to account code 4010 –supplies purchased for dept move to unrestricted fund 10xxxx, move supplies specific to the project to account code 4015 – Project Supplies

RecommendationsBecome Familiar with Circulars A-21, A-110, CASB and UA’s Disclosure StatementReview transaction detail on a regular basis

Those Browser literate share expertise with those who are notExchange reviews, new eyes see new things

Educate Faculty – in small dosesIf you don’t know, ask Financial ServicesThey are your MAU’s Central Administration & they are there to help

28

Please completePlease completefeedback sheets.feedback sheets.Thanks for coming!Thanks for coming!

History of the Cost Accounting Standards

Overview and History In general, the Cost Accounting Standards were the result of concerns about pricing and accounting practices of defense contractors and the lack of consistency. • 1968

o Amendments - Defense Production Act o Government Accounting Office (GAO)

Study to determine feasibility of • Establishing & applying cost accounting standards • Greater uniformity in cost accounting • Negotiating & administering procurement contracts

Recommendations • CAS

o Feasible - greater uniformity and consistency o Should not be limited to Defense contracts o Benefits vs. costs o Eliminate alternative practices

• Contractor should be required to maintain records • 1970

o Congress created CASB Tasked to increase uniformity and consistency CASB created CAS

• 19 commercial standards • Implemented standards in 1980

Applied to negotiated defense contracts in excess of $100,000 • 1978

o Educational Institutions were exempted from CAS • 1980

o CASB dissolved o Congress decided CASB had served it’s purpose so it dissolved the board

• 1988 o CASB reestablished

Permanent, independent board Five member board CASB has authority to make, promulgate, amend, and rescind cost

accounting standards and regulations Office of Federal Procurement Policy in OMB

o Increased contract threshold to $500,000 o Extended coverage to all Federal contracts

1 I:\Training\CAS\UAF CAS 01-26-06\History of the CAS.doc

• 1990-1993

o F&A cost concerns o Scandals

Some institutions were charging costs that were unallowable to federal awards

• 1994

o CAS coverage extended to colleges and universities Universities structured accounting systems to collect certain types of

costs directly and indirectly Variance of F&A rates among institutions was too high and

unexplainable Cost accounting practices were not comparable

• 1995

o Four standards o Negotiated Federal contracts and subcontracts greater than $500,000 o CAS Exemptions

Negotiated contracts and subcontracts less than $500,000 Sealed bid contracts Contracts and subcontracts with small businesses or foreign

governments or foreign concerns Contracts and subcontracts in which prices are set by law Firm fixed price contracts Contracts and subcontracts performed outside U.S.

o Disclosure Statement required if meet certain thresholds

• 1996 o Amendment to A-21

Emphasis on consistency among and within institutions Incorporates the four cost accounting standards Disclosure Statement Requirements Circular A-21, C.14 Extends coverage of A-21 to all sponsored agreements

• Contracts and grants regardless of award amount

• 2003 o Government focus is on

Consistency and standardization Institutions must be proactive in identifying compliance problems

o Consistency and standardization improves government’s ability to control through

Existing regulations Standardized F&A cost rate proposal format Simplifies federal audit procedures

2 I:\Training\CAS\UAF CAS 01-26-06\History of the CAS.doc

Direct and Indirect Costs January 26, 2006

Allowability Under OMB Circular A-21, all costs recovered on a sponsored project either directly or indirectly (F&A costs) must be allowable. A cost must meet specific criteria to be considered allowable. A cost must be:

• Reasonable (A-21, Section C.3) • Allocable (A-21, Section C.4) • Given consistent treatment (CAS) • Conform to any limitations or exclusions in A-21 or the terms and conditions of

the sponsored agreement, if applicable Note, costs may be considered “unallowable” under federal rules but allowable under state or UA regulation. Many of these federal “unallowable” expenses are a reasonable and necessary expense for UA. An expense that in “unallowable” under OMB Circular A-21 may still be incurred but UA must be able to clearly identify these federally “unallowable” costs in our accounting information so that UA can treat these costs appropriately for the F&A rate development process. UA uses the program codes associated with the organization code and specific account codes to identify most of these expenses and activities. Circular A-21, Section J. includes some items of cost that the federal government has specifically identified as unallowable. If there is a discrepancy between Circular A-21 and the specific sponsored agreement then the sponsored agreement governs. In addition, failure by the Circular to mention a particular item of cost does not imply that the cost is either allowable or unallowable. Review Section J for treatment of similar or related costs to determine the allowability of the particular cost. See handout on unallowable costs. Direct Costs Direct costs must meet the following criteria:

• Identified specifically with research, instruction, other sponsored activity, or any other institutional activities • With relative ease • With a high degree of accuracy

• Not be expressly disallowed in the sponsored agreement, if applicable When an institution has determined that a particular type of cost is a direct cost all costs incurred for the same purpose, in like circumstances, must be treated as a direct cost of all activities.

1 of 7

Indirect Costs Indirect costs are:

• General institutional costs • Incurred for common and joint objectives • Not identified readily and specifically to a particular direct activity

Indirect costs include:

• Operations and maintenance of buildings and grounds • Depreciation on buildings • Capital improvements and equipment • Central and department administrative expenses

• Department administrative expenses are incurred to support normal core operations of a unit

• Sponsored project administration • Library costs • Student administration and services

Indirect Costs Considered Direct Costs Certain type costs are often incurred for both direct and indirect purposes. Costs incurred for the same purpose, in like circumstances, must be consistently treated as direct or indirect. Cost normally charged as indirect may be charged as direct cost if purpose and circumstances for which the costs are incurred are different. Each activity must be evaluated on a case-by-case basis to determine if it represents cost will be incurred for a different purpose or in an unlike circumstance. Direct charging of department administration costs may be appropriate where:

• Services are required by scope of project and • Cost satisfies direct cost criteria • Approved budget clearly describes need for the services

While not final determining factors in making a determination of whether a cost that is normally an indirect cost should be treated as a direct cost, consider project:

• Size • Nature • Complexity

2 of 7

Other key factors include:

• Specific type and nature of services required are extensive and go beyond the normal departmental baseline support, or

• Nature of work performed is functionally different from the general business activities of clerical and administrative personnel

Examples of sponsored awards where it may be appropriate to charge indirect-type costs as direct costs:

• Large, complex programs, such as Program Projects or research centers, and other grants and contracts that require assembling and managing teams of investigators from a number of institutions.

• Extensive data accumulation, analysis and tabulation, • Preparation and production of manuals, large reports or books, • Extensive travel and meeting arrangements for large numbers of participants, • Management of a project in locations that are remote from campus, • Individual projects requiring project-specific database management;

individualized graphs or manuscript preparation; human or animal protocol, other project-specific regulatory protocols; and multiple project-related investigator coordination and communications.

Administrative costs associated with these types of major projects incurred to provide support in excess of the normal baseline support provided by the F & A rate are charged as direct costs. These costs are not incurred for the same purpose or circumstance as the common costs.

Non-federal Agreements Indirect-type costs may be charged as direct costs to non-federal agreements when not expressly prohibited by the sponsor. It is understood that this is technically noncompliant with OMB-A21, however, federally sponsored agreements are not adversely impacted financially due to a lower F & A rate as these costs are included in the appropriate base.

3 of 7

Distinguishing Between Direct and Indirect Costs

Direct Costs Indirect Costs Salaries, wages and related fringe benefits of faculty, technicians, scientists, research assistants, postdoctoral associates, other technical and programmatic personnel who are necessary to meet the objectives of the activity/project

Salaries, wages and related fringe benefits for administrative or clerical activities including secretarial assistance, procurement of materials & services, general accounting & bookkeeping, proposal preparation for new awards, payroll and human resource tasks. Also includes faculty and professionals performing administrative tasks.

Supplies and materials including non-capitalized equipment; project supplies; teaching supplies; professional, technical, and scientific supplies; computer software; field camp supplies; stockroom supplies; maintenance and repair commodities; periodical subscriptions and books; and other miscellaneous supplies or materials readily identifiable to project. Supplies purchased with sponsored project funds should be in quantities that are consumed during the normal course of the project and clearly identifiable to the project. Note, project supplies cannot be charged to a project via journal voucher from a supply cabinet usage log unless the supply cabinet meets the criteria for an authorized recharge center.

Office Supplies and computer Supplies including pens, paper, printer cartridges, envelopes, and software that support general operations.

Travel associated with research, public service, instruction, or other sponsored activity.

Administrative travel

Telephone including long distance nonrecurring charges, cellular telephone charges, remote and locations with telephones solely dedicated to a single identifiable project

Local telephone usage and base telephone rental costs are indirect costs for on-campus telephones.

Subcontract, Sub agreements, Sub awards

4 of 7

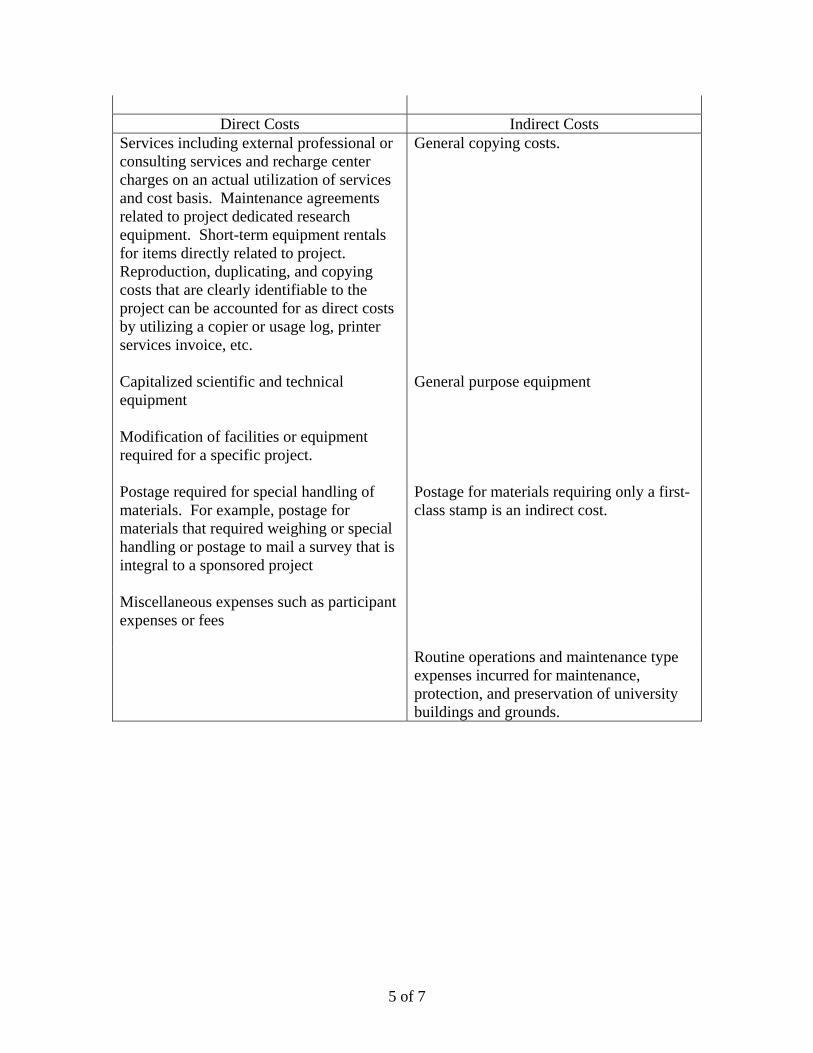

Direct Costs Indirect Costs

Services including external professional or consulting services and recharge center charges on an actual utilization of services and cost basis. Maintenance agreements related to project dedicated research equipment. Short-term equipment rentals for items directly related to project. Reproduction, duplicating, and copying costs that are clearly identifiable to the project can be accounted for as direct costs by utilizing a copier or usage log, printer services invoice, etc.

General copying costs.

Capitalized scientific and technical equipment

General purpose equipment

Modification of facilities or equipment required for a specific project.

Postage required for special handling of materials. For example, postage for materials that required weighing or special handling or postage to mail a survey that is integral to a sponsored project

Postage for materials requiring only a first-class stamp is an indirect cost.

Miscellaneous expenses such as participant expenses or fees

Routine operations and maintenance type expenses incurred for maintenance, protection, and preservation of university buildings and grounds.

5 of 7

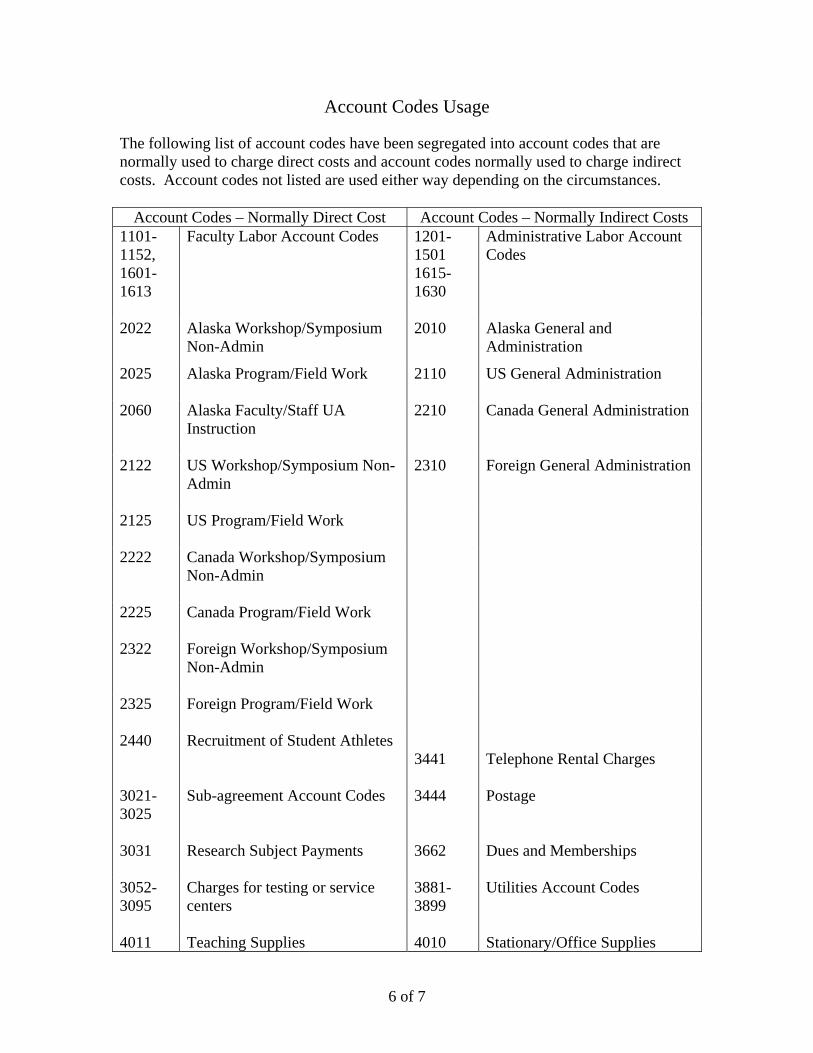

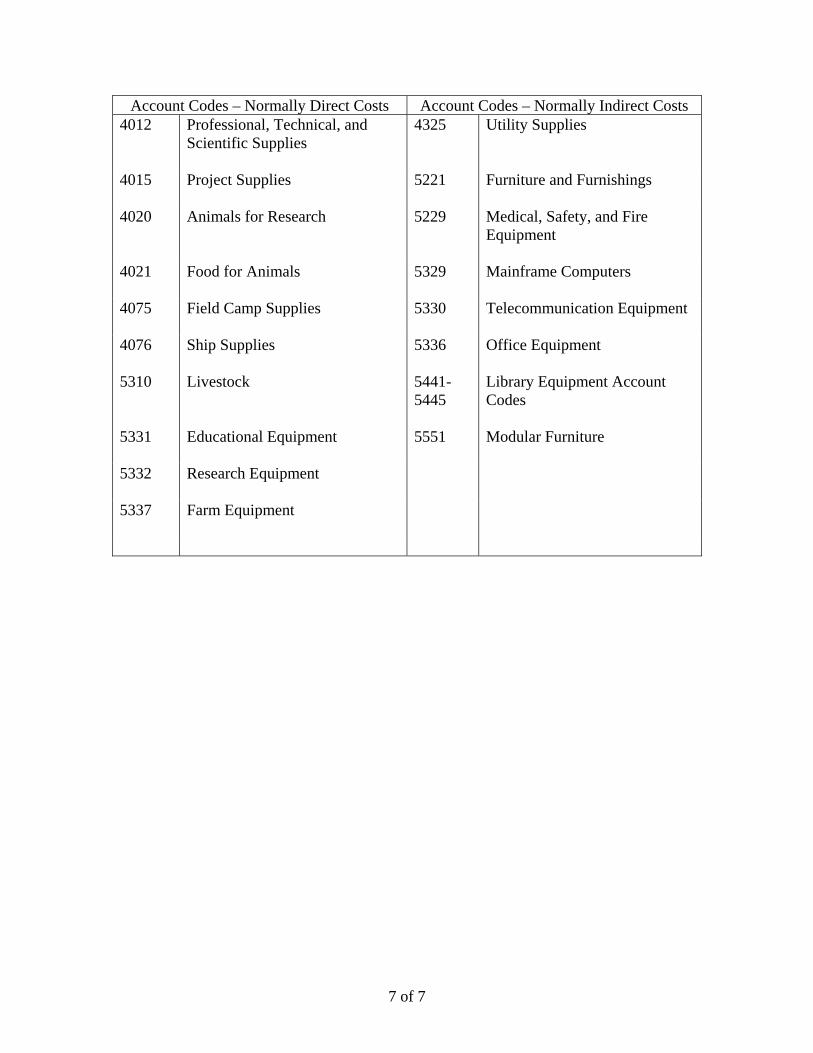

Account Codes Usage

The following list of account codes have been segregated into account codes that are normally used to charge direct costs and account codes normally used to charge indirect costs. Account codes not listed are used either way depending on the circumstances.

Account Codes – Normally Direct Cost Account Codes – Normally Indirect Costs 1101-1152, 1601-1613

Faculty Labor Account Codes 1201-1501 1615-1630

Administrative Labor Account Codes

2022 Alaska Workshop/Symposium Non-Admin

2010 Alaska General and Administration

2025 Alaska Program/Field Work 2110 US General Administration

2060 Alaska Faculty/Staff UA Instruction

2210 Canada General Administration

2122 US Workshop/Symposium Non-Admin

2310 Foreign General Administration

2125 US Program/Field Work

2222 Canada Workshop/Symposium Non-Admin

2225 Canada Program/Field Work

2322 Foreign Workshop/Symposium Non-Admin

2325 Foreign Program/Field Work

2440 Recruitment of Student Athletes 3441

Telephone Rental Charges

3021-3025

Sub-agreement Account Codes 3444 Postage

3031 Research Subject Payments

3662 Dues and Memberships

3052-3095

Charges for testing or service centers

3881-3899

Utilities Account Codes

4011 Teaching Supplies 4010 Stationary/Office Supplies

6 of 7

Account Codes – Normally Direct Costs Account Codes – Normally Indirect Costs 4012 Professional, Technical, and

Scientific Supplies

4325 Utility Supplies

4015 Project Supplies

5221 Furniture and Furnishings

4020 Animals for Research 5229 Medical, Safety, and Fire Equipment

4021 Food for Animals

5329 Mainframe Computers

4075 Field Camp Supplies

5330 Telecommunication Equipment

4076 Ship Supplies

5336 Office Equipment

5310 Livestock

5441-5445

Library Equipment Account Codes

5331 Educational Equipment

5551 Modular Furniture

5332 Research Equipment

5337 Farm Equipment

7 of 7

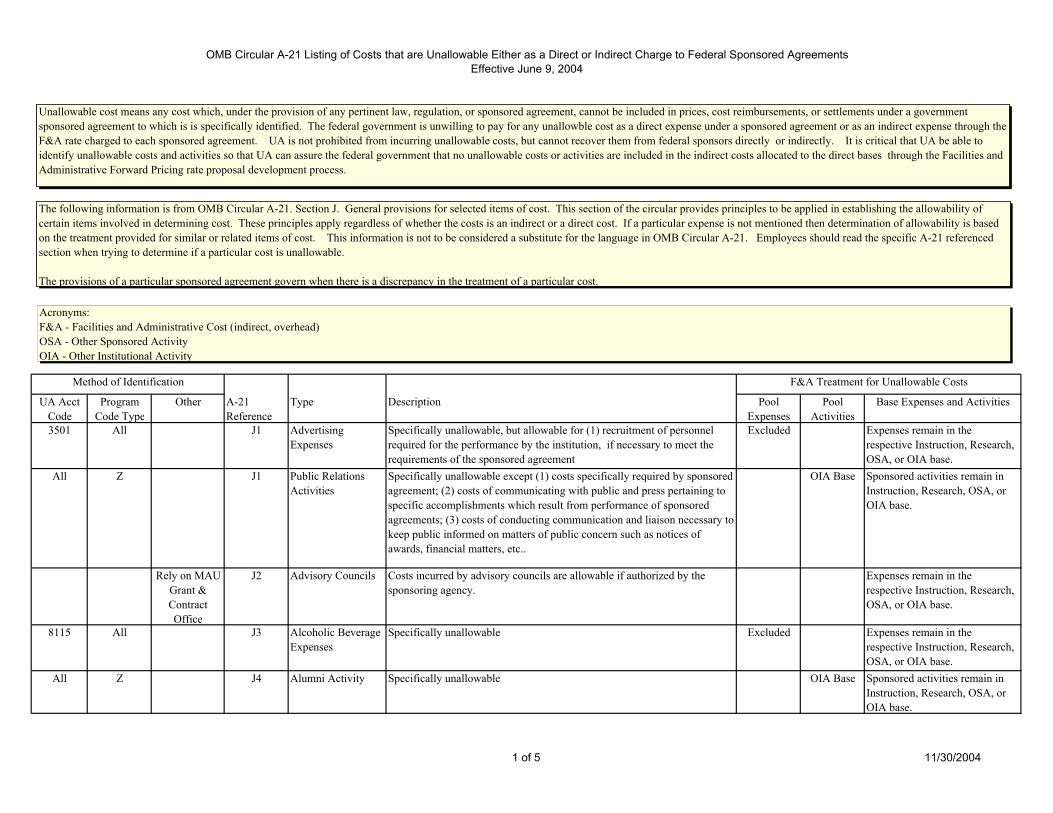

OMB Circular A-21 Listing of Costs that are Unallowable Either as a Direct or Indirect Charge to Federal Sponsored AgreementsEffective June 9, 2004

Method of Identification

UA Acct Code

Program Code Type

Other A-21 Reference

Type Description Pool Expenses

Pool Activities

Base Expenses and Activities

3501 All J1 Advertising Expenses

Specifically unallowable, but allowable for (1) recruitment of personnel required for the performance by the institution, if necessary to meet the requirements of the sponsored agreement

Excluded Expenses remain in the respective Instruction, Research, OSA, or OIA base.

All Z J1 Public Relations Activities

Specifically unallowable except (1) costs specifically required by sponsored agreement; (2) costs of communicating with public and press pertaining to specific accomplishments which result from performance of sponsored agreements; (3) costs of conducting communication and liaison necessary to keep public informed on matters of public concern such as notices of awards, financial matters, etc..

OIA Base Sponsored activities remain in Instruction, Research, OSA, or OIA base.

Rely on MAU Grant & Contract Office

J2 Advisory Councils Costs incurred by advisory councils are allowable if authorized by the sponsoring agency.

Expenses remain in the respective Instruction, Research, OSA, or OIA base.

8115 All J3 Alcoholic Beverage Expenses

Specifically unallowable Excluded Expenses remain in the respective Instruction, Research, OSA, or OIA base.

All Z J4 Alumni Activity Specifically unallowable OIA Base Sponsored activities remain in Instruction, Research, OSA, or OIA base.

F&A Treatment for Unallowable Costs

Unallowable cost means any cost which, under the provision of any pertinent law, regulation, or sponsored agreement, cannot be included in prices, cost reimbursements, or settlements under a government sponsored agreement to which is is specifically identified. The federal government is unwilling to pay for any unallowble cost as a direct expense under a sponsored agreement or as an indirect expense through the F&A rate charged to each sponsored agreement. UA is not prohibited from incurring unallowable costs, but cannot recover them from federal sponsors directly or indirectly. It is critical that UA be able to identify unallowable costs and activities so that UA can assure the federal government that no unallowable costs or activities are included in the indirect costs allocated to the direct bases through the Facilities and Administrative Forward Pricing rate proposal development process.

The following information is from OMB Circular A-21. Section J. General provisions for selected items of cost. This section of the circular provides principles to be applied in establishing the allowability of certain items involved in determining cost. These principles apply regardless of whether the costs is an indirect or a direct cost. If a particular expense is not mentioned then determination of allowability is based on the treatment provided for similar or related items of cost. This information is not to be considered a substitute for the language in OMB Circular A-21. Employees should read the specific A-21 referenced section when trying to determine if a particular cost is unallowable.

The provisions of a particular sponsored agreement govern when there is a discrepancy in the treatment of a particular cost.

Acronyms:F&A - Facilities and Administrative Cost (indirect, overhead)OSA - Other Sponsored ActivityOIA - Other Institutional Activity

1 of 5 11/30/2004

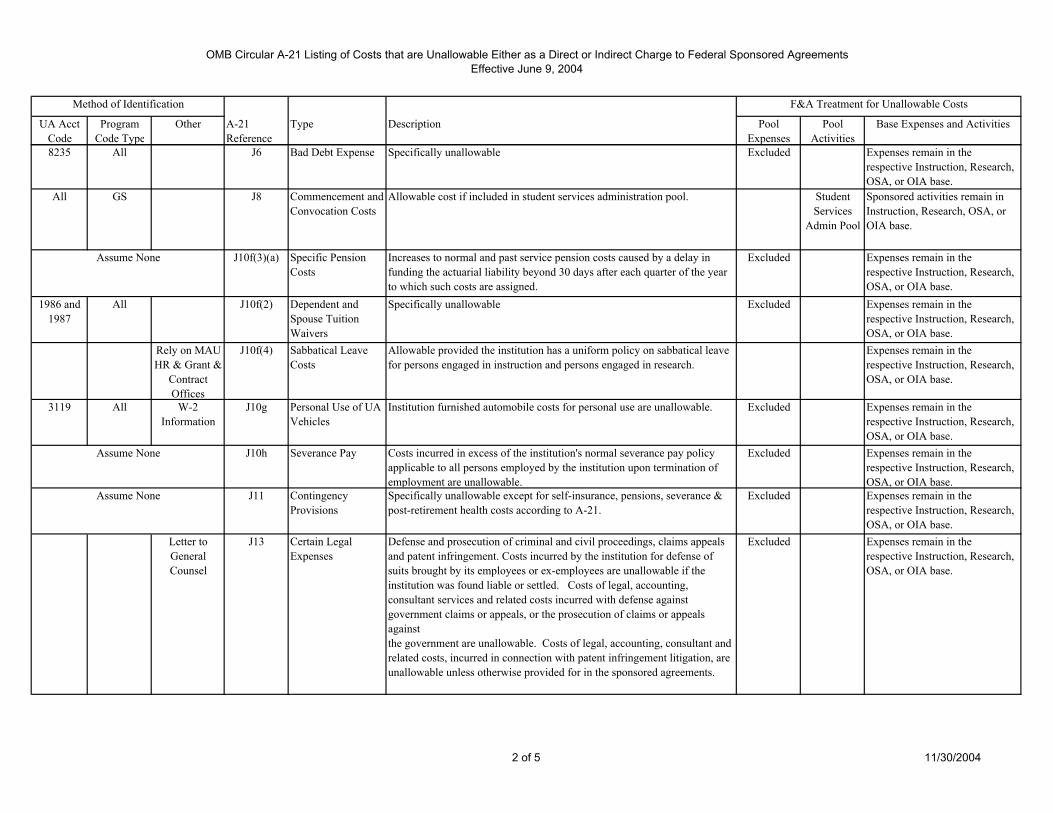

OMB Circular A-21 Listing of Costs that are Unallowable Either as a Direct or Indirect Charge to Federal Sponsored AgreementsEffective June 9, 2004

Method of Identification

UA Acct Code

Program Code Type

Other A-21 Reference

Type Description Pool Expenses

Pool Activities

Base Expenses and Activities

F&A Treatment for Unallowable Costs

8235 All J6 Bad Debt Expense Specifically unallowable Excluded Expenses remain in the respective Instruction, Research, OSA, or OIA base.

All GS J8 Commencement and Convocation Costs

Allowable cost if included in student services administration pool. Student Services

Admin Pool

Sponsored activities remain in Instruction, Research, OSA, or OIA base.

Assume None J10f(3)(a) Specific Pension Costs

Increases to normal and past service pension costs caused by a delay in funding the actuarial liability beyond 30 days after each quarter of the year to which such costs are assigned.

Excluded Expenses remain in the respective Instruction, Research, OSA, or OIA base.

1986 and 1987

All J10f(2) Dependent and Spouse Tuition Waivers

Specifically unallowable Excluded Expenses remain in the respective Instruction, Research, OSA, or OIA base.

Rely on MAU HR & Grant &

Contract Offices

J10f(4) Sabbatical Leave Costs

Allowable provided the institution has a uniform policy on sabbatical leave for persons engaged in instruction and persons engaged in research.

Expenses remain in the respective Instruction, Research, OSA, or OIA base.

3119 All W-2 Information

J10g Personal Use of UA Vehicles

Institution furnished automobile costs for personal use are unallowable. Excluded Expenses remain in the respective Instruction, Research, OSA, or OIA base.

J10h Severance Pay Costs incurred in excess of the institution's normal severance pay policy applicable to all persons employed by the institution upon termination of employment are unallowable.

Excluded Expenses remain in the respective Instruction, Research, OSA, or OIA base.

Assume None J11 Contingency Provisions

Specifically unallowable except for self-insurance, pensions, severance & post-retirement health costs according to A-21.

Excluded Expenses remain in the respective Instruction, Research, OSA, or OIA base.

Letter to General Counsel

J13 Certain Legal Expenses

Defense and prosecution of criminal and civil proceedings, claims appeals and patent infringement. Costs incurred by the institution for defense of suits brought by its employees or ex-employees are unallowable if the institution was found liable or settled. Costs of legal, accounting, consultant services and related costs incurred with defense against government claims or appeals, or the prosecution of claims or appeals against the government are unallowable. Costs of legal, accounting, consultant and related costs, incurred in connection with patent infringement litigation, are unallowable unless otherwise provided for in the sponsored agreements.

Excluded Expenses remain in the respective Instruction, Research, OSA, or OIA base.

Assume None

2 of 5 11/30/2004

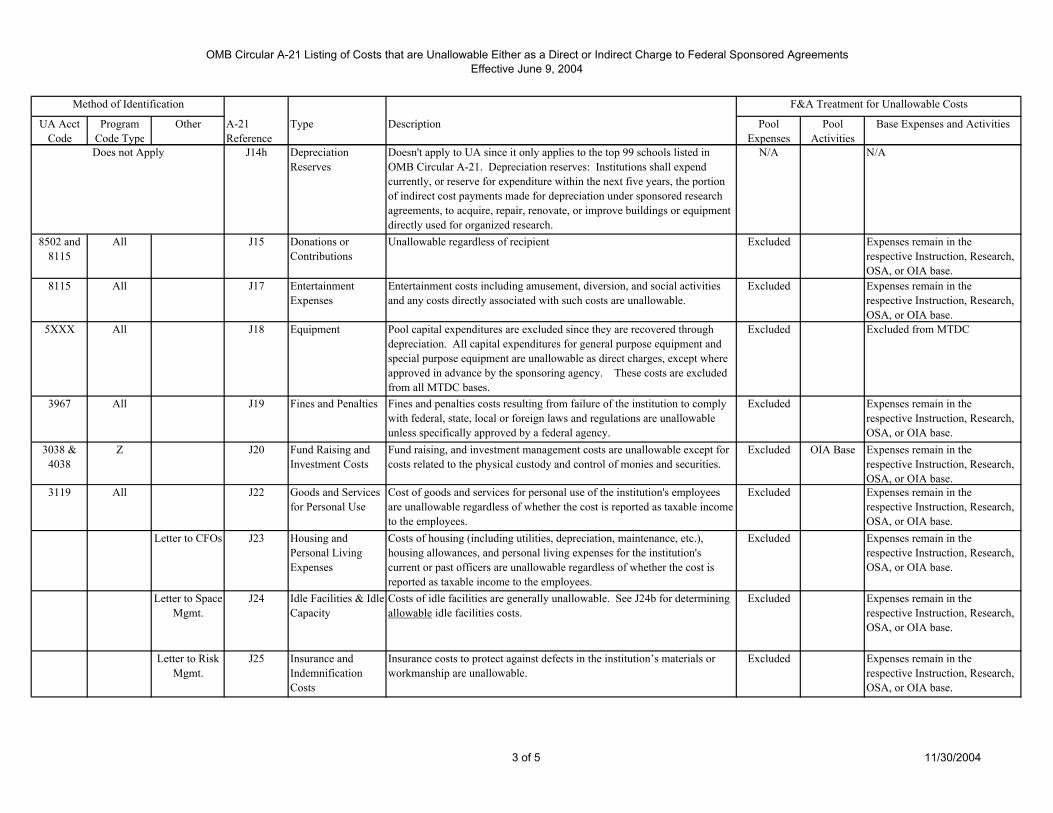

OMB Circular A-21 Listing of Costs that are Unallowable Either as a Direct or Indirect Charge to Federal Sponsored AgreementsEffective June 9, 2004

Method of Identification

UA Acct Code

Program Code Type

Other A-21 Reference

Type Description Pool Expenses

Pool Activities

Base Expenses and Activities

F&A Treatment for Unallowable Costs

Does not Apply J14h Depreciation Reserves

Doesn't apply to UA since it only applies to the top 99 schools listed in OMB Circular A-21. Depreciation reserves: Institutions shall expend currently, or reserve for expenditure within the next five years, the portion of indirect cost payments made for depreciation under sponsored research agreements, to acquire, repair, renovate, or improve buildings or equipment directly used for organized research.

N/A N/A

8502 and 8115

All J15 Donations or Contributions

Unallowable regardless of recipient Excluded Expenses remain in the respective Instruction, Research, OSA, or OIA base.

8115 All J17 Entertainment Expenses

Entertainment costs including amusement, diversion, and social activities and any costs directly associated with such costs are unallowable.

Excluded Expenses remain in the respective Instruction, Research, OSA, or OIA base.

5XXX All J18 Equipment Pool capital expenditures are excluded since they are recovered through depreciation. All capital expenditures for general purpose equipment and special purpose equipment are unallowable as direct charges, except where approved in advance by the sponsoring agency. These costs are excluded from all MTDC bases.

Excluded Excluded from MTDC

3967 All J19 Fines and Penalties Fines and penalties costs resulting from failure of the institution to comply with federal, state, local or foreign laws and regulations are unallowable unless specifically approved by a federal agency.

Excluded Expenses remain in the respective Instruction, Research, OSA, or OIA base.

3038 & 4038

Z J20 Fund Raising and Investment Costs

Fund raising, and investment management costs are unallowable except for costs related to the physical custody and control of monies and securities.

Excluded OIA Base Expenses remain in the respective Instruction, Research, OSA, or OIA base.

3119 All J22 Goods and Services for Personal Use

Cost of goods and services for personal use of the institution's employees are unallowable regardless of whether the cost is reported as taxable income to the employees.

Excluded Expenses remain in the respective Instruction, Research, OSA, or OIA base.

Letter to CFOs J23 Housing and Personal Living Expenses

Costs of housing (including utilities, depreciation, maintenance, etc.), housing allowances, and personal living expenses for the institution's current or past officers are unallowable regardless of whether the cost is reported as taxable income to the employees.

Excluded Expenses remain in the respective Instruction, Research, OSA, or OIA base.

Letter to Space Mgmt.

J24 Idle Facilities & Idle Capacity

Costs of idle facilities are generally unallowable. See J24b for determining allowable idle facilities costs.

Excluded Expenses remain in the respective Instruction, Research, OSA, or OIA base.

Letter to Risk Mgmt.

J25 Insurance and Indemnification Costs

Insurance costs to protect against defects in the institution’s materials or workmanship are unallowable.

Excluded Expenses remain in the respective Instruction, Research, OSA, or OIA base.

3 of 5 11/30/2004

OMB Circular A-21 Listing of Costs that are Unallowable Either as a Direct or Indirect Charge to Federal Sponsored AgreementsEffective June 9, 2004

Method of Identification

UA Acct Code

Program Code Type

Other A-21 Reference

Type Description Pool Expenses

Pool Activities

Base Expenses and Activities

F&A Treatment for Unallowable Costs

8340, 8341 & 8342

Z Lease Purchase

Analysis and Cash Flow Analysis

J26 Interest Interest costs are unallowable except for interest expenses paid to external parties for assets (buildings and equipment) used to support sponsored agreements. Additional specific criteria exist in OMB Circular A-21, J.26.b that must be satisfied in order for interest expenses to be allowable.

Excluded OIA Base Expenses remain in the respective Instruction, Research, OSA, or OIA base.

2090, 2190 & 3040

Z J28 Lobbying Unallowable lobbying costs and activities are defined broadly to include costs associated with any attempt to influence governmental (federal, state, local, etc.) elections and legislation. Legislative liaison activities are unallowable if the activity is carried on in support of or in preparation of unallowable lobbying activities. Executive lobbying costs incurred in attempting to apply any influence that induces or tends to induce either directly, indirectly, an employee or officer of the Executive Branch of the Federal Government to give consideration or to act regarding a sponsored agreement or a regulatory matter on any basis other than the merits of the matter. In general, lobbying expenses may not be paid for with funds from sponsored agreements unless specifically authorized by statute.

Excluded OIA Base Expenses remain in the respective Instruction, Research, OSA, or OIA base.

8661 Rely on MAU Grant and Contract Office

J29 Losses on Other Sponsored Agreements or Contracts

Costs in excess of income (overruns) under any sponsored agreement or contract are unallowable.

Excluded Expenses remain in the respective Instruction, Research, OSA, or OIA base.

3663 All J33 Memberships, Subscriptions, and Professional Activity Costs

Cost of membership in any civic, community, social, dining or country club or organization are unallowable.

Excluded Expenses remain in the respective Instruction, Research, OSA, or OIA base.

Rely on MAU Grant and Contract Office

J36 Preagreement Costs Cost incurred prior to the effective date of the sponsored agreement are unallowable unless approved by the sponsored agency.

Excluded Expenses remain in the respective Instruction, Research, OSA, or OIA base.

Letter to General

Counsel, Rely on MAU

Procurement & GCS Offices

J37 Professional Services Costs

Determine allowability for legal professional services costs in conjunction with J.13. Other professional services are allowable if the criteria listed in J37b are met.

Excluded Expenses remain in the respective Instruction, Research, OSA, or OIA base.

4 of 5 11/30/2004

OMB Circular A-21 Listing of Costs that are Unallowable Either as a Direct or Indirect Charge to Federal Sponsored AgreementsEffective June 9, 2004

Method of Identification

UA Acct Code

Program Code Type

Other A-21 Reference

Type Description Pool Expenses

Pool Activities

Base Expenses and Activities

F&A Treatment for Unallowable Costs

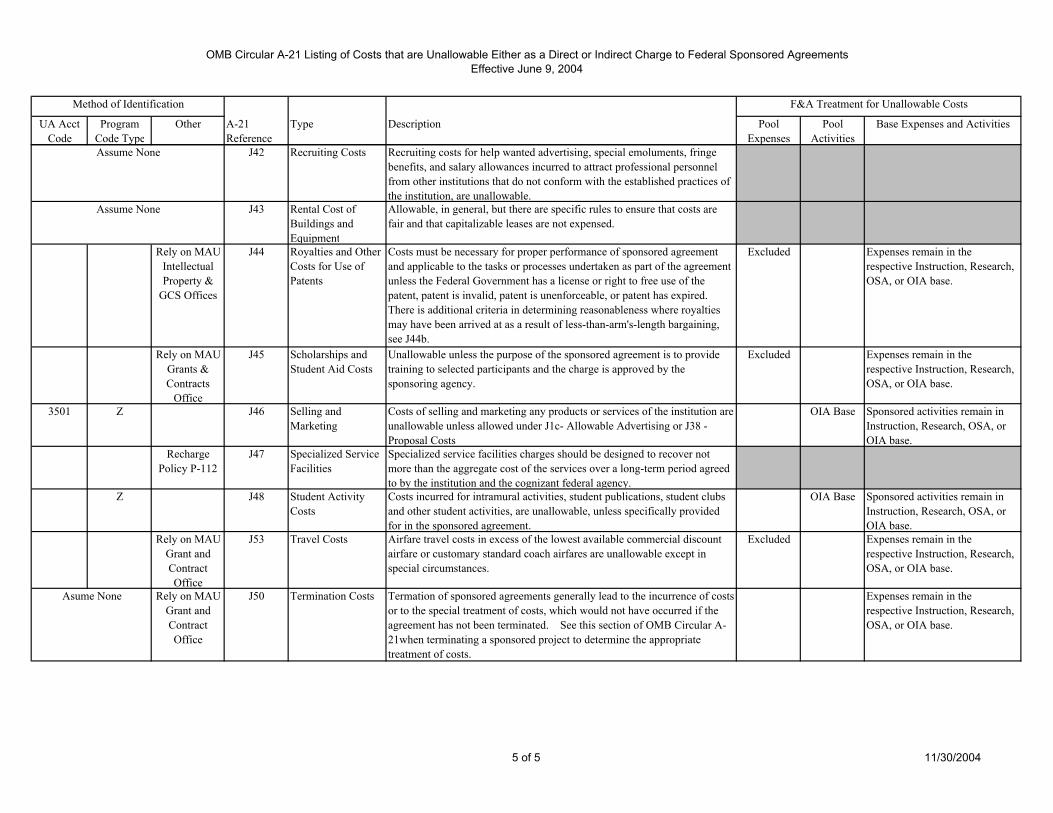

J42 Recruiting Costs Recruiting costs for help wanted advertising, special emoluments, fringe benefits, and salary allowances incurred to attract professional personnel from other institutions that do not conform with the established practices of the institution, are unallowable.

Assume None J43 Rental Cost of Buildings and Equipment

Allowable, in general, but there are specific rules to ensure that costs are fair and that capitalizable leases are not expensed.

Rely on MAU Intellectual Property &

GCS Offices

J44 Royalties and Other Costs for Use of Patents

Costs must be necessary for proper performance of sponsored agreement and applicable to the tasks or processes undertaken as part of the agreement unless the Federal Government has a license or right to free use of the patent, patent is invalid, patent is unenforceable, or patent has expired. There is additional criteria in determining reasonableness where royalties may have been arrived at as a result of less-than-arm's-length bargaining, see J44b.

Excluded Expenses remain in the respective Instruction, Research, OSA, or OIA base.

Rely on MAU Grants & Contracts

Office

J45 Scholarships and Student Aid Costs

Unallowable unless the purpose of the sponsored agreement is to provide training to selected participants and the charge is approved by the sponsoring agency.

Excluded Expenses remain in the respective Instruction, Research, OSA, or OIA base.

3501 Z J46 Selling and Marketing

Costs of selling and marketing any products or services of the institution are unallowable unless allowed under J1c- Allowable Advertising or J38 - Proposal Costs

OIA Base Sponsored activities remain in Instruction, Research, OSA, or OIA base.

Recharge Policy P-112

J47 Specialized Service Facilities

Specialized service facilities charges should be designed to recover not more than the aggregate cost of the services over a long-term period agreed to by the institution and the cognizant federal agency.

Z J48 Student Activity Costs

Costs incurred for intramural activities, student publications, student clubs and other student activities, are unallowable, unless specifically provided for in the sponsored agreement.

OIA Base Sponsored activities remain in Instruction, Research, OSA, or OIA base.

Rely on MAU Grant and Contract Office

J53 Travel Costs Airfare travel costs in excess of the lowest available commercial discount airfare or customary standard coach airfares are unallowable except in special circumstances.

Excluded Expenses remain in the respective Instruction, Research, OSA, or OIA base.

Asume None Rely on MAU Grant and Contract Office

J50 Termination Costs Termation of sponsored agreements generally lead to the incurrence of costs or to the special treatment of costs, which would not have occurred if the agreement has not been terminated. See this section of OMB Circular A-21when terminating a sponsored project to determine the appropriate treatment of costs.

Expenses remain in the respective Instruction, Research, OSA, or OIA base.

Assume None

5 of 5 11/30/2004