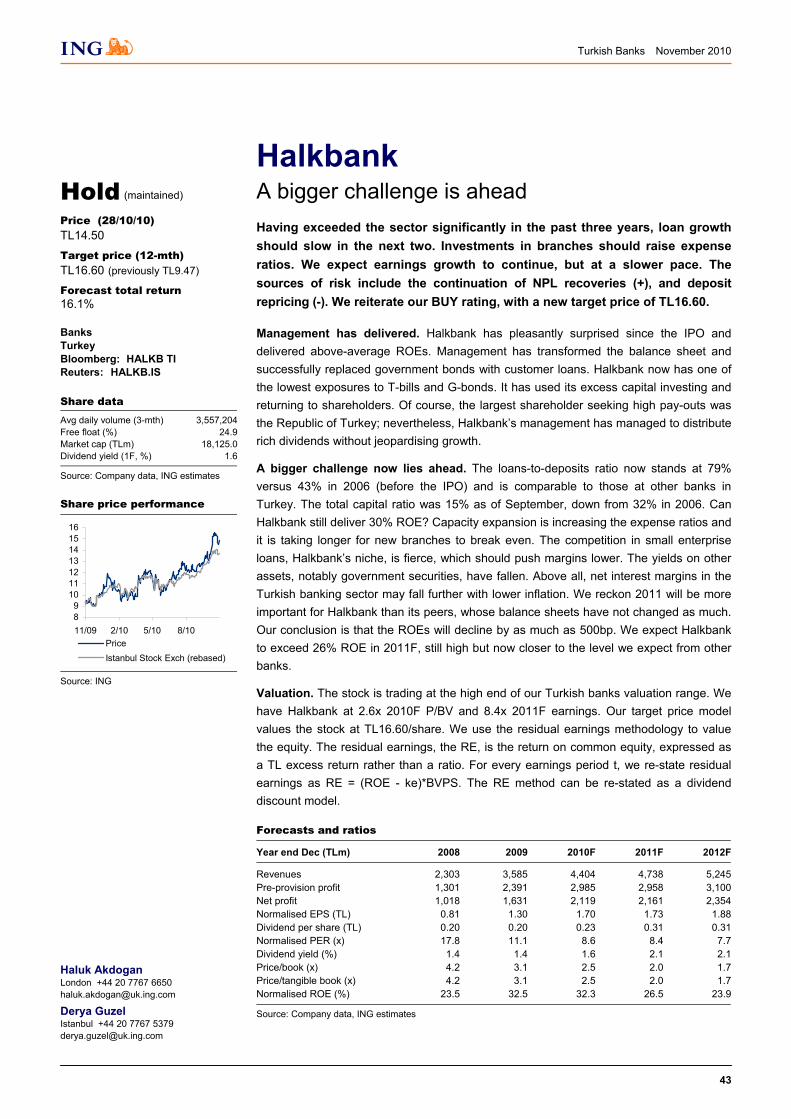

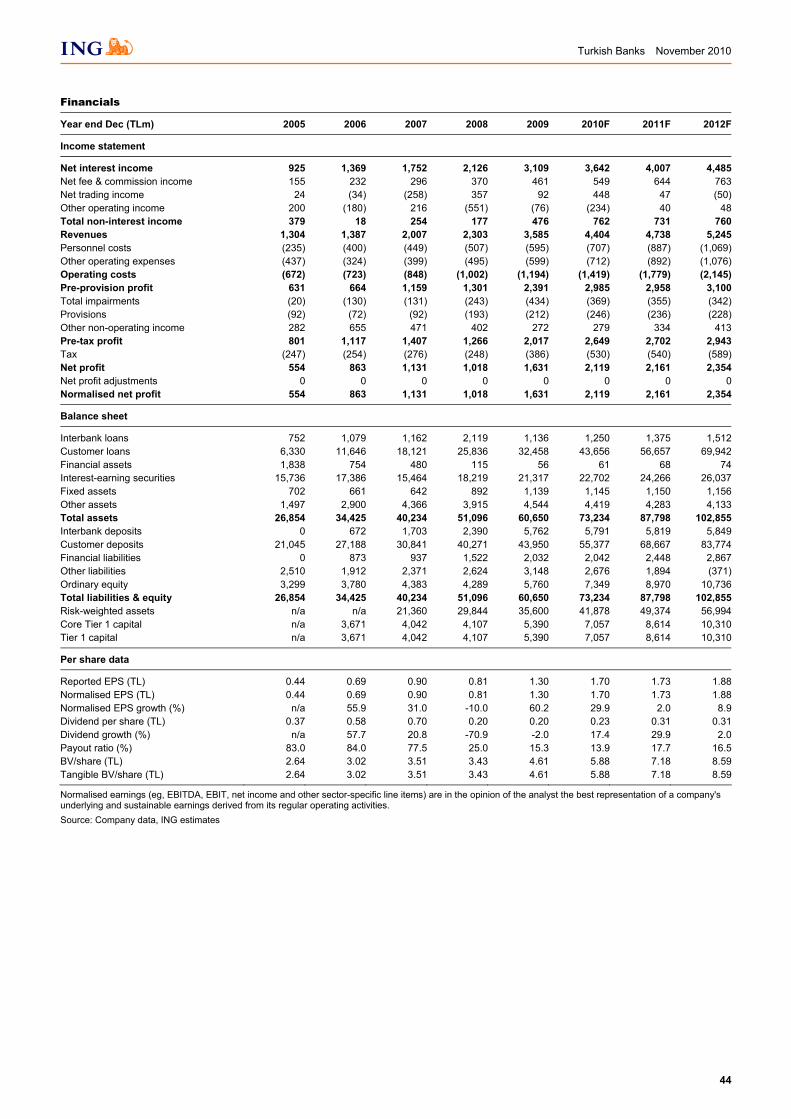

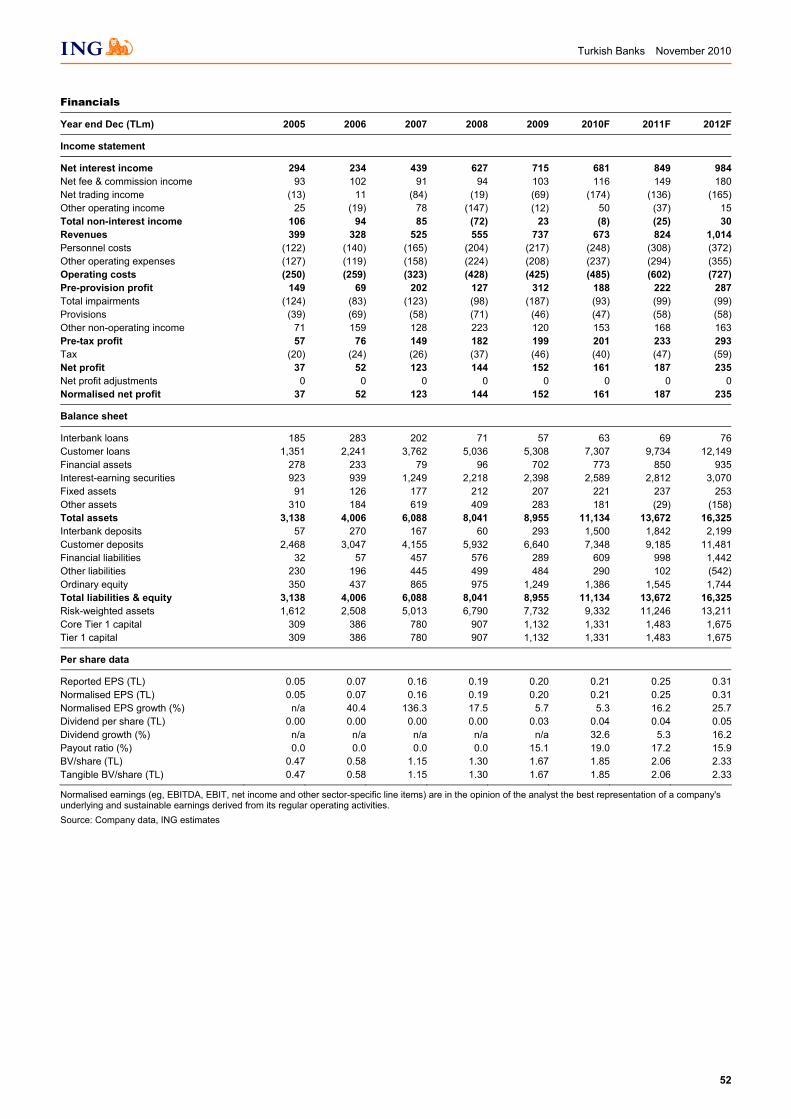

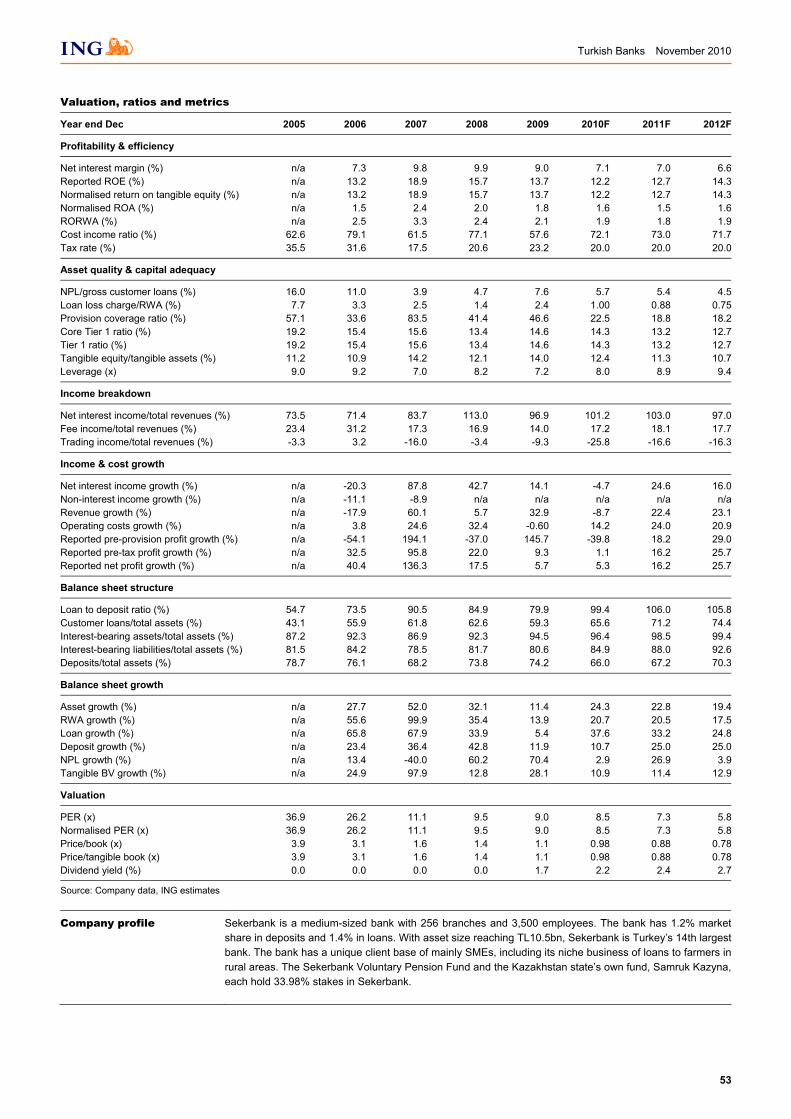

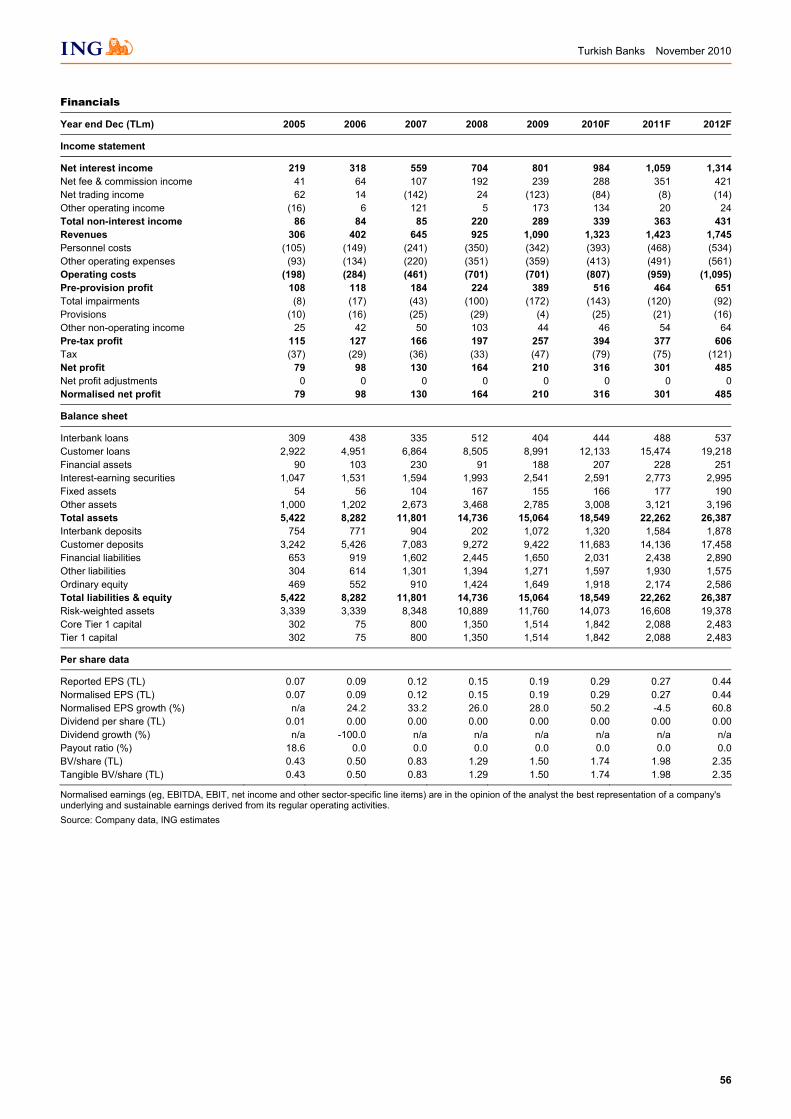

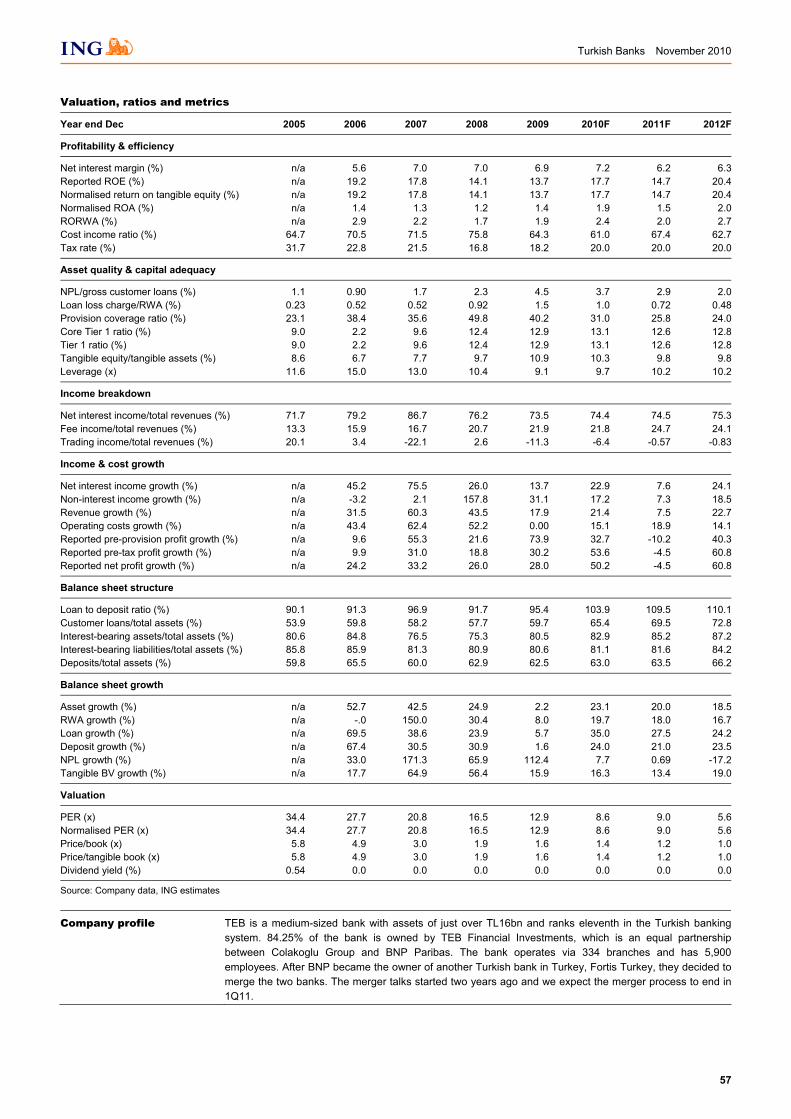

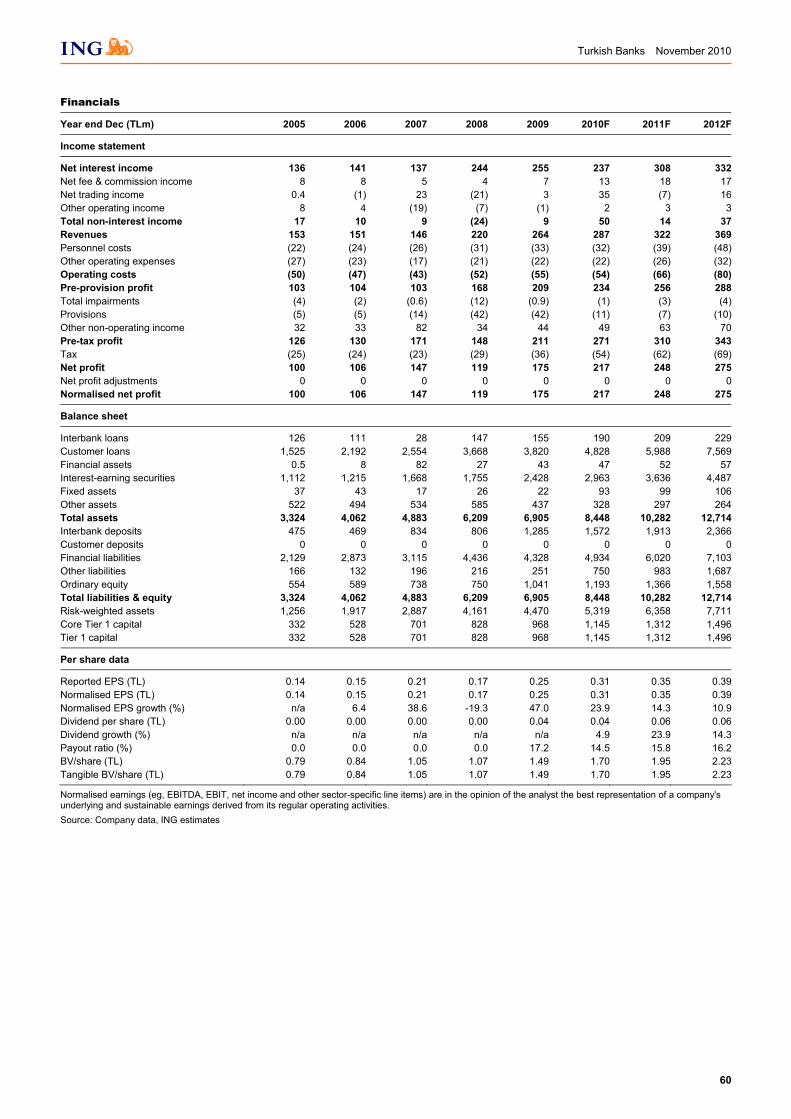

turkish banks - türk ekonomi bankası turkish... · turkish banks november 2010 1 sector review...

TRANSCRIPT

Turkish Banks November 2010

1

Turkish Banks Positioning for 2011 and beyond

EQUITY RESEARCH

research.ing.com SEE THE DISCLOSURES APPENDIX FOR IMPORTANT DISCLOSURES & ANALYST CERTIFICATION

Sector review 3 November 2010

ING ratings and targets (TL)

Target price Rating Price Old New

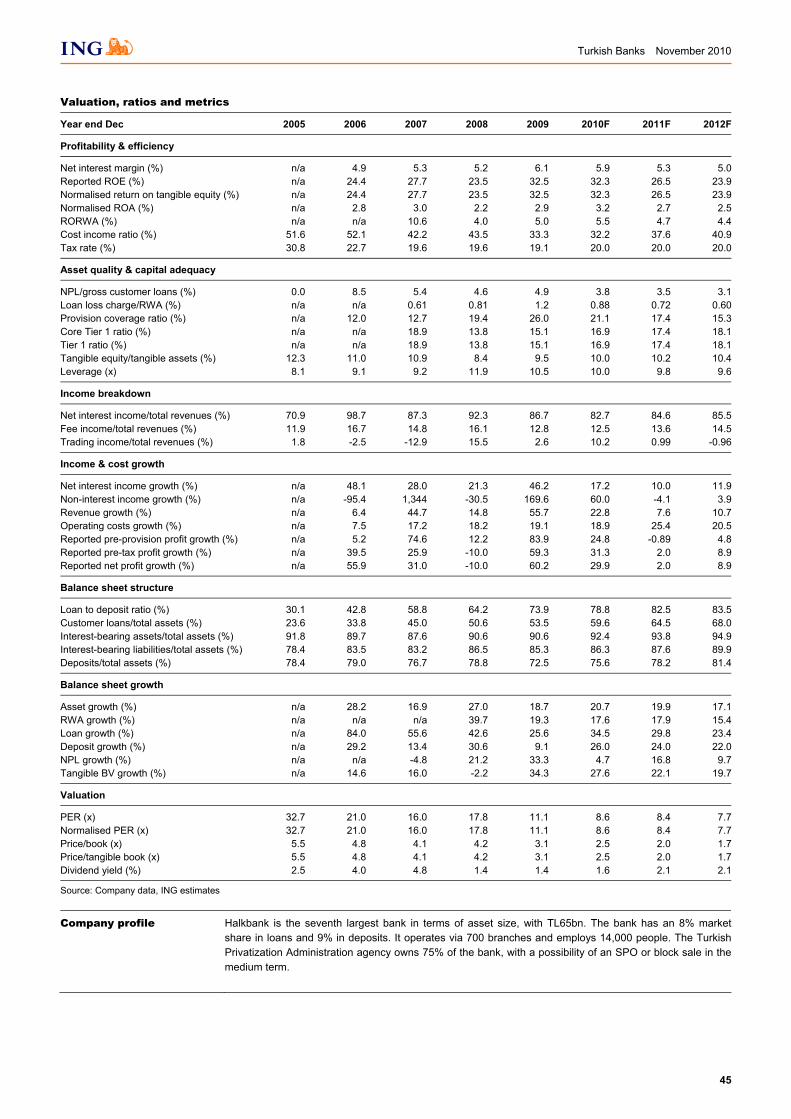

Akbank SELL 9.00 6.00 8.13Fortis HOLD 2.32 1.65 2.28Garanti BUY 8.80 7.50 10.47Halkbank HOLD 14.50 9.47 16.60Isbank BUY 6.45 4.77 7.48Sekerbank BUY 1.82 1.73 2.65TEB BUY 2.46 2.24 3.34TSKB BUY 2.64 2.37 3.11Vakifbank HOLD 4.64 3.15 4.78Yapi Kredi BUY 5.50 4.50 6.78

Priced on 28 October 2010

Source: Bloomberg

Key changes

Stock Comment

Garanti BUY reiterated, TP raised Isbank BUY reiterated, TP raised Sekerbank Hold to BUY, TP raised TSKB BUY reiterated, TP raised Yapi Kredi BUY reiterated, TP raised

Source: ING

Turkish banks multiples (x)

Ticker 2011F PER

2011F P/BV

Akbank AKBNK TI 11.0 2.00Fortis FORTS TI 11.8 1.11Garanti GARAN TI 9.6 2.09Halkbank HALKB TI 8.4 2.23Isbank ISCTR TI 9.5 1.59Sekerbank SKBNK TI 7.3 0.88TEB TEBNK TI 9.0 1.24TSKB TSKB TI 7.5 1.35Vakifbank VAKBN TI 10.7 1.29Yapi Kredi YKBNK TI 9.7 1.95

Priced on 28 October 2010 Source: ING estimates

We see a secular shift in Turkish banking. The ROEs are likely to fall next year but so is the cost of equity. Turkish banks should generate an average 19% ROE over our forecast period 2011-13, now rolled over one year. We reduce CoE by 100bp and raise our target prices. The strong rally may prompt profit taking; we would take the opportunity and buy. We reiterate BUY on Yapi Kredi, Garanti, Isbank, TEB and TSKB and upgrade Sekerbank to BUY.

Model revisions and new targets. We have revisited our revenue model and balance sheet assumptions. Our target values are higher because we have: (1) reduced cost of equity by 100bp; (2) raised our 2011F loan growth expectation to 25% (coverage average), from 17% previously; and (3) rolled over the forecast period one year, as we usually do in the December quarter. The revisions raise our target prices by an average of 48%.

Operating outlook. The Central Bank of Turkey has taken action to tighten liquidity, but has not completely reversed monetary policy. We do not expect rate hikes before September 2011, and we see inflation remaining low until 2012. Low rates should prompt further growth in lending. We expect volume growth in 2010/11 to be large enough to offset any further decline in NIM. We expect low deposit interest rates throughout 2011. Provisions could still surprise on the upside: we expect cost of risk to fall below the 1% mark at major Turkish banks by the end of 2011, from an estimated 1.3% average in 2010. Capital levels are adequate at the banks we follow, in our view. The sector’s average CAR stands at 19% and LDR at 80% as at June 2010, giving ample room for balance sheet growth. The duration of liabilities is increasing as banks seek alternative funding vehicles, including issuing corporate bonds and new syndications. We believe the balance sheets will transform considerably in the next three years to accommodate the growth in longer dated assets, notably retail loans.

Re-rating. The ROEs are likely to fall next year, but what Turkish banks are experiencing is nothing short of a re-rating. It is because of this paradigm shift that the shares have continued to rally despite several analyst and strategist downgrades. There is no question it has been a very strong rally, but the rally alone is no reason to sell. If the shares were to fall on profit taking, we would see it as an opportunity to buy.

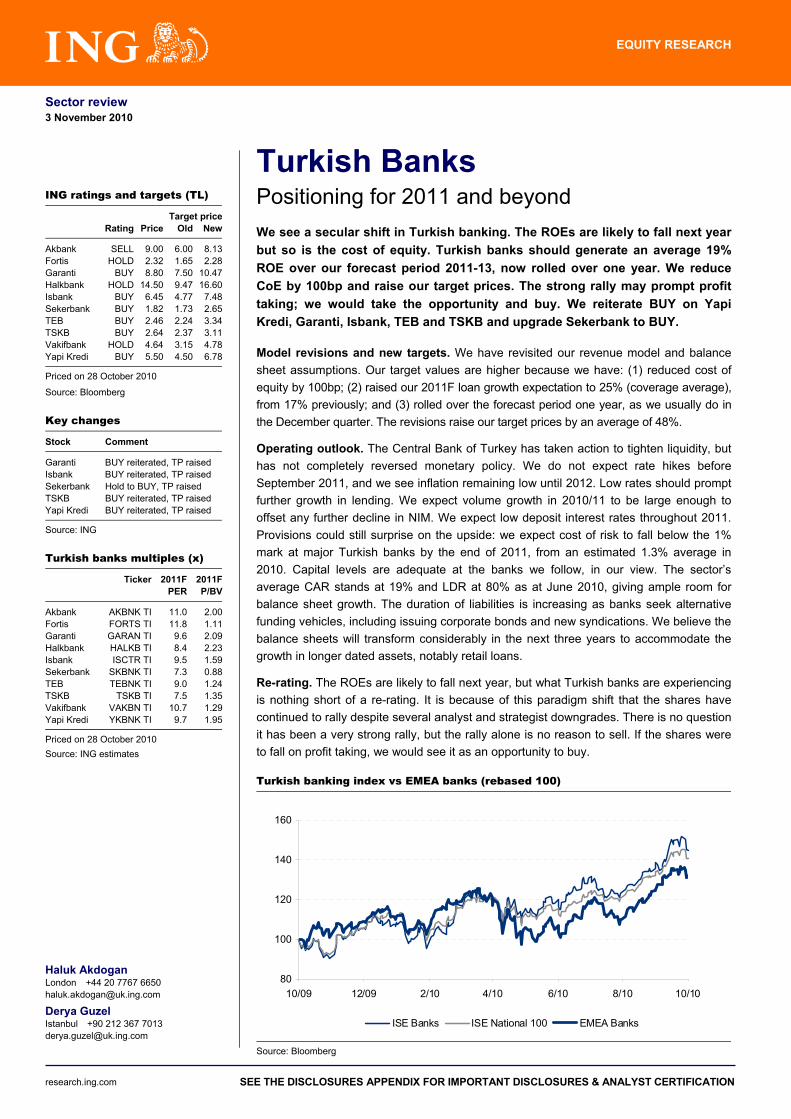

Turkish banking index vs EMEA banks (rebased 100)

80

100

120

140

160

10/09 12/09 2/10 4/10 6/10 8/10 10/10

ISE Banks ISE National 100 EMEA Banks

Source: Bloomberg

Haluk Akdogan London +44 20 7767 6650 [email protected]

Derya Guzel Istanbul +90 212 367 7013 [email protected]

Turkish Banks November 2010

2

Contents

Investment case 3

Recommendation 7

Valuation 10

Consensus 12

Sources of risk 14

Asset quality trends 18

Net NPLs 19

Cost of risk trends 20

Expense ratios 21

Return on assets 22

Monetary policy 23

Economic fundamentals 25

Companies 28 Akbank .............................................................................................................................31 Fortis Bank (Turkey).........................................................................................................35 Garanti Bank ....................................................................................................................39 Halkbank ..........................................................................................................................43 Isbank ..............................................................................................................................47 Sekerbank ........................................................................................................................51 Turk Ekonomi Bankasi .....................................................................................................55 TSKB................................................................................................................................59 Vakifbank .........................................................................................................................63 Yapi Kredi Bankasi...........................................................................................................67

Disclosures Appendix 70

Turkish Banks November 2010

3

Investment case

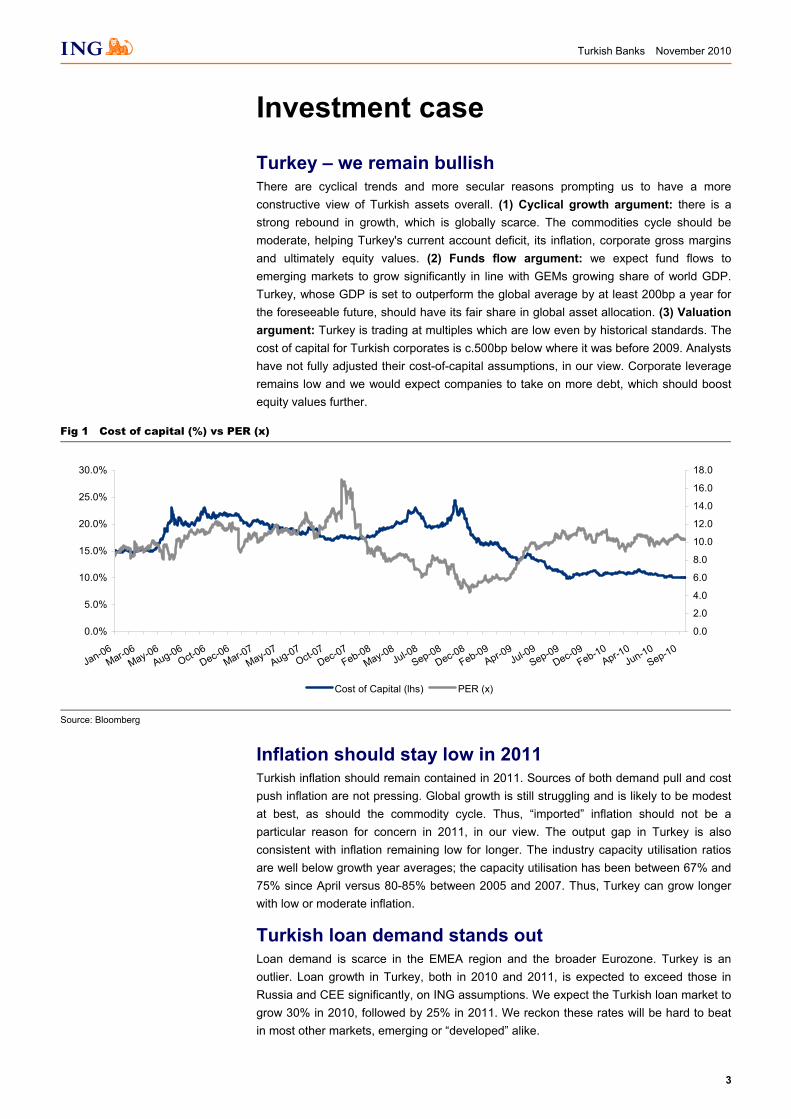

Turkey – we remain bullish There are cyclical trends and more secular reasons prompting us to have a more constructive view of Turkish assets overall. (1) Cyclical growth argument: there is a strong rebound in growth, which is globally scarce. The commodities cycle should be moderate, helping Turkey's current account deficit, its inflation, corporate gross margins and ultimately equity values. (2) Funds flow argument: we expect fund flows to emerging markets to grow significantly in line with GEMs growing share of world GDP. Turkey, whose GDP is set to outperform the global average by at least 200bp a year for the foreseeable future, should have its fair share in global asset allocation. (3) Valuation argument: Turkey is trading at multiples which are low even by historical standards. The cost of capital for Turkish corporates is c.500bp below where it was before 2009. Analysts have not fully adjusted their cost-of-capital assumptions, in our view. Corporate leverage remains low and we would expect companies to take on more debt, which should boost equity values further.

Fig 1 Cost of capital (%) vs PER (x)

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

Jan-06Mar-06

May-06Aug-06

Oct-06Dec-06

Mar-07May-07

Aug-07Oct-07

Dec-07Feb-08

May-08Jul-08

Sep-08Dec-08

Feb-09Apr-09

Jul-09Sep-09

Dec-09Feb-10

Apr-10Jun-10

Sep-10

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

Cost of Capital (lhs) PER (x)

Source: Bloomberg

Inflation should stay low in 2011 Turkish inflation should remain contained in 2011. Sources of both demand pull and cost push inflation are not pressing. Global growth is still struggling and is likely to be modest at best, as should the commodity cycle. Thus, “imported” inflation should not be a particular reason for concern in 2011, in our view. The output gap in Turkey is also consistent with inflation remaining low for longer. The industry capacity utilisation ratios are well below growth year averages; the capacity utilisation has been between 67% and 75% since April versus 80-85% between 2005 and 2007. Thus, Turkey can grow longer with low or moderate inflation.

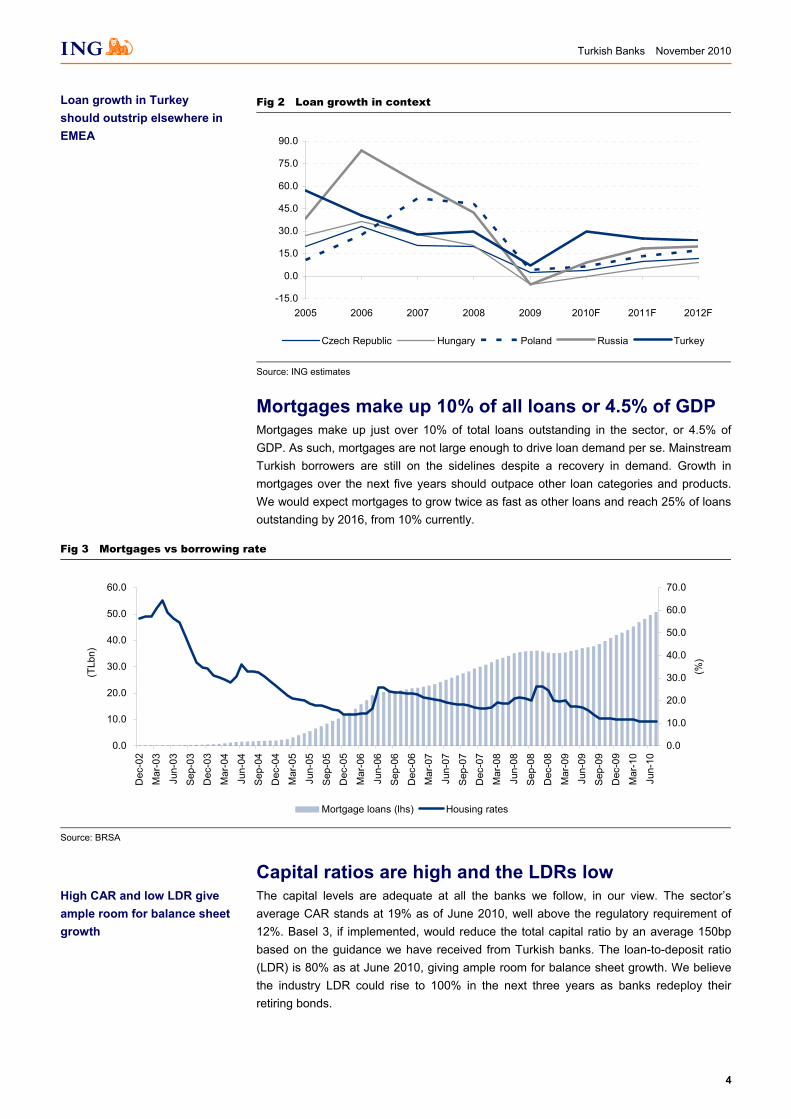

Turkish loan demand stands out Loan demand is scarce in the EMEA region and the broader Eurozone. Turkey is an outlier. Loan growth in Turkey, both in 2010 and 2011, is expected to exceed those in Russia and CEE significantly, on ING assumptions. We expect the Turkish loan market to grow 30% in 2010, followed by 25% in 2011. We reckon these rates will be hard to beat in most other markets, emerging or “developed” alike.

Turkish Banks November 2010

4

Fig 2 Loan growth in context

-15.0

0.0

15.0

30.0

45.0

60.0

75.0

90.0

2005 2006 2007 2008 2009 2010F 2011F 2012F

Czech Republic Hungary Poland Russia Turkey

Source: ING estimates

Mortgages make up 10% of all loans or 4.5% of GDP Mortgages make up just over 10% of total loans outstanding in the sector, or 4.5% of GDP. As such, mortgages are not large enough to drive loan demand per se. Mainstream Turkish borrowers are still on the sidelines despite a recovery in demand. Growth in mortgages over the next five years should outpace other loan categories and products. We would expect mortgages to grow twice as fast as other loans and reach 25% of loans outstanding by 2016, from 10% currently.

Fig 3 Mortgages vs borrowing rate

0.0

10.0

20.0

30.0

40.0

50.0

60.0

Dec

-02

Mar

-03

Jun-

03

Sep

-03

Dec

-03

Mar

-04

Jun-

04

Sep

-04

Dec

-04

Mar

-05

Jun-

05

Sep

-05

Dec

-05

Mar

-06

Jun-

06

Sep

-06

Dec

-06

Mar

-07

Jun-

07

Sep

-07

Dec

-07

Mar

-08

Jun-

08

Sep

-08

Dec

-08

Mar

-09

Jun-

09

Sep

-09

Dec

-09

Mar

-10

Jun-

10

(TLb

n)

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

(%)

Mortgage loans (lhs) Housing rates

Source: BRSA

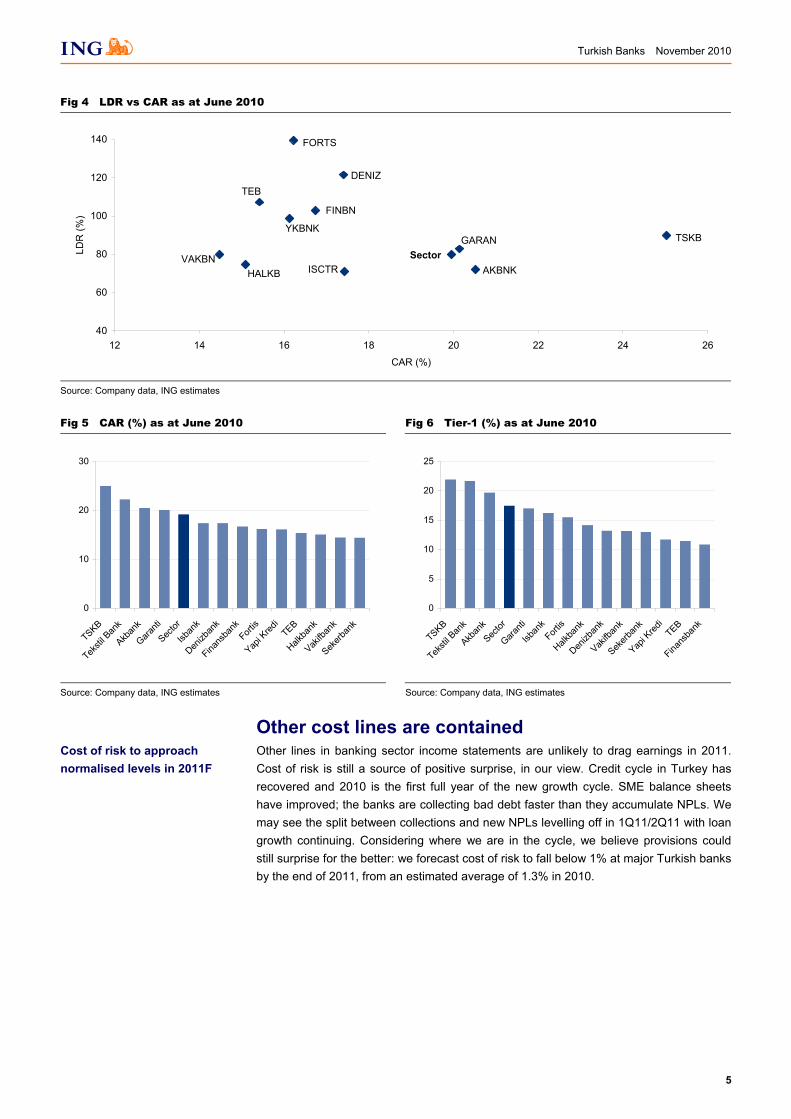

Capital ratios are high and the LDRs low The capital levels are adequate at all the banks we follow, in our view. The sector’s average CAR stands at 19% as of June 2010, well above the regulatory requirement of 12%. Basel 3, if implemented, would reduce the total capital ratio by an average 150bp based on the guidance we have received from Turkish banks. The loan-to-deposit ratio (LDR) is 80% as at June 2010, giving ample room for balance sheet growth. We believe the industry LDR could rise to 100% in the next three years as banks redeploy their retiring bonds.

Loan growth in Turkey should outstrip elsewhere in EMEA

High CAR and low LDR give ample room for balance sheet growth

Turkish Banks November 2010

5

Fig 4 LDR vs CAR as at June 2010

AKBNK

GARANSectorVAKBN

YKBNK

FINBN

DENIZ

FORTS

TEB

HALKB

TSKB

ISCTR

40

60

80

100

120

140

12 14 16 18 20 22 24 26

CAR (%)

LDR

(%)

Source: Company data, ING estimates

Fig 5 CAR (%) as at June 2010

Fig 6 Tier-1 (%) as at June 2010

0

10

20

30

TSKB

Teksti

l Ban

k

Akban

k

Garanti

Sector

Isban

k

Denizb

ank

Finans

bank

Fortis

Yapi K

redi

TEB

Halkba

nk

Vakifb

ank

Sekerb

ank

0

5

10

15

20

25

TSKB

Teksti

l Ban

k

Akban

kSec

tor

Garanti

Isban

kFort

is

Halkba

nk

Denizb

ank

Vakifb

ank

Sekerb

ank

Yapi K

redi

TEB

Finans

bank

Source: Company data, ING estimates Source: Company data, ING estimates

Other cost lines are contained Other lines in banking sector income statements are unlikely to drag earnings in 2011. Cost of risk is still a source of positive surprise, in our view. Credit cycle in Turkey has recovered and 2010 is the first full year of the new growth cycle. SME balance sheets have improved; the banks are collecting bad debt faster than they accumulate NPLs. We may see the split between collections and new NPLs levelling off in 1Q11/2Q11 with loan growth continuing. Considering where we are in the cycle, we believe provisions could still surprise for the better: we forecast cost of risk to fall below 1% at major Turkish banks by the end of 2011, from an estimated average of 1.3% in 2010.

Cost of risk to approach normalised levels in 2011F

Turkish Banks November 2010

6

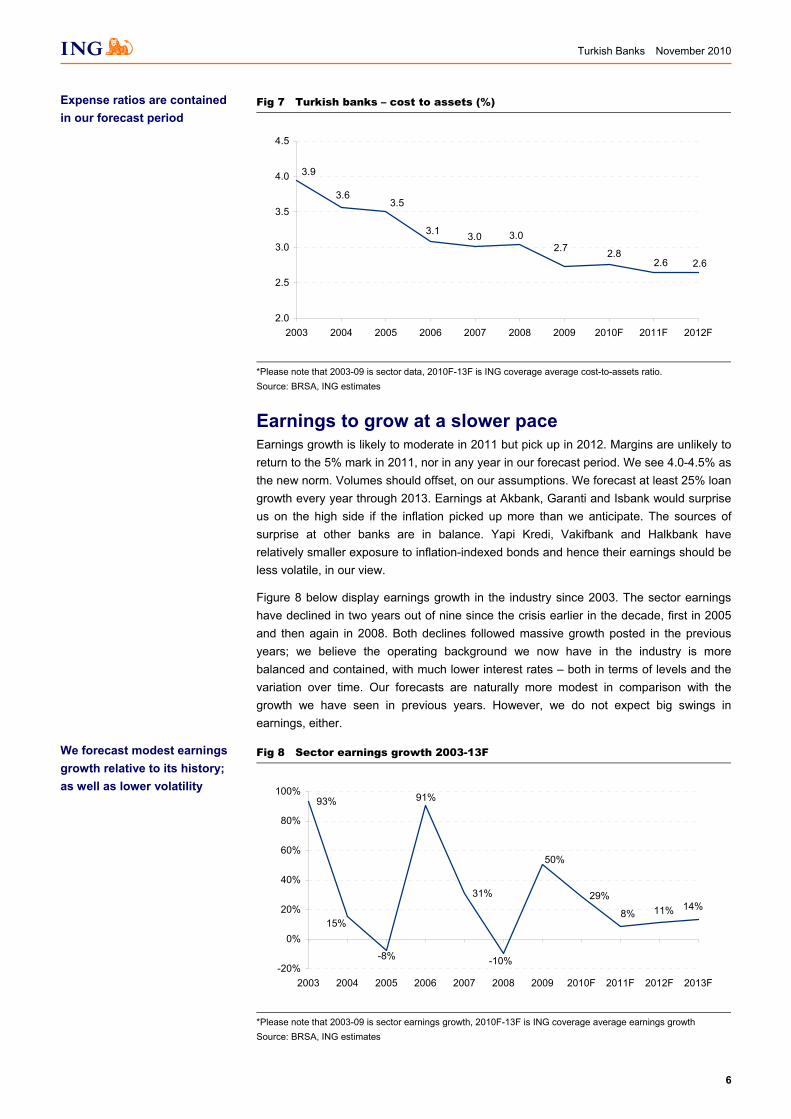

Fig 7 Turkish banks – cost to assets (%)

3.6

3.9

2.73.03.03.1

3.5

2.82.6 2.6

2.0

2.5

3.0

3.5

4.0

4.5

2003 2004 2005 2006 2007 2008 2009 2010F 2011F 2012F

*Please note that 2003-09 is sector data, 2010F-13F is ING coverage average cost-to-assets ratio. Source: BRSA, ING estimates

Earnings to grow at a slower pace Earnings growth is likely to moderate in 2011 but pick up in 2012. Margins are unlikely to return to the 5% mark in 2011, nor in any year in our forecast period. We see 4.0-4.5% as the new norm. Volumes should offset, on our assumptions. We forecast at least 25% loan growth every year through 2013. Earnings at Akbank, Garanti and Isbank would surprise us on the high side if the inflation picked up more than we anticipate. The sources of surprise at other banks are in balance. Yapi Kredi, Vakifbank and Halkbank have relatively smaller exposure to inflation-indexed bonds and hence their earnings should be less volatile, in our view.

Figure 8 below display earnings growth in the industry since 2003. The sector earnings have declined in two years out of nine since the crisis earlier in the decade, first in 2005 and then again in 2008. Both declines followed massive growth posted in the previous years; we believe the operating background we now have in the industry is more balanced and contained, with much lower interest rates – both in terms of levels and the variation over time. Our forecasts are naturally more modest in comparison with the growth we have seen in previous years. However, we do not expect big swings in earnings, either.

Fig 8 Sector earnings growth 2003-13F

93%

31% 29%14%11%8%

91%

50%

-10%-8%

15%

-20%

0%

20%

40%

60%

80%

100%

2003 2004 2005 2006 2007 2008 2009 2010F 2011F 2012F 2013F

*Please note that 2003-09 is sector earnings growth, 2010F-13F is ING coverage average earnings growth Source: BRSA, ING estimates

We forecast modest earnings growth relative to its history; as well as lower volatility

Expense ratios are contained in our forecast period

Turkish Banks November 2010

7

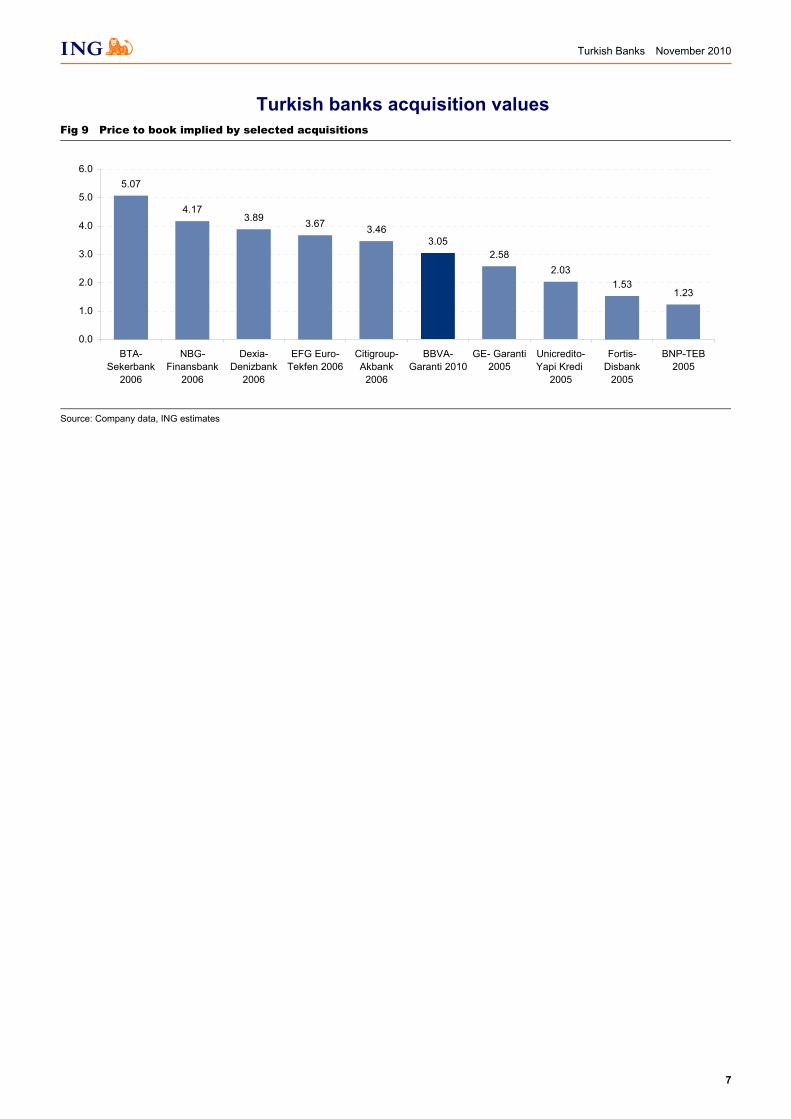

Turkish banks acquisition values Fig 9 Price to book implied by selected acquisitions

5.07

4.173.89 3.67 3.46

3.052.58

2.031.53

1.23

0.0

1.0

2.0

3.0

4.0

5.0

6.0

BTA-Sekerbank

2006

NBG-Finansbank

2006

Dexia-Denizbank

2006

EFG Euro-Tekfen 2006

Citigroup-Akbank

2006

BBVA-Garanti 2010

GE- Garanti2005

Unicredito-Yapi Kredi

2005

Fortis-Disbank

2005

BNP-TEB2005

Source: Company data, ING estimates

Turkish Banks November 2010

8

Recommendation Forecast revisions We have fine-tuned our forecasts and rolled over the forecast period. Our target values are now higher because we have: (1) reduced cost of equity by 100bp; (2) raised our 2011 loan growth expectation to 25% (coverage average) from 17% previously; and (3) rolled over the forecast period one year. A summary of revisions, old and new target prices, and our ratings are displayed in Figure 9.

Fig 10 Forecast revisions (TL)

Share price Old target New target Upside (%) Old EPS 11F New EPS 11F Old rating New rating

Akbank 9.00 6.00 8.13 -9.6 0.70 0.82 Sell SELLFortis Bank 2.32 1.65 2.28 -1.8 0.17 0.20 Hold HOLDGaranti 8.80 7.50 10.47 19.0 0.89 0.78 Buy BUYHalkbank 14.50 9.47 16.60 14.5 1.18 1.73 Hold HOLDIsbank 6.45 4.77 7.48 15.9 0.53 0.68 Buy BUYSekerbank 1.82 1.73 2.65 45.4 0.33 0.25 Hold BUYTEB 2.46 2.24 3.34 35.9 0.29 0.27 Buy BUYTSKB 2.64 2.37 3.11 17.7 0.38 0.35 Buy BUYVakifbank 4.64 3.15 4.78 3.0 0.42 0.43 Hold HOLDYapi Kredi 5.50 4.50 6.78 23.3 0.54 0.56 Buy BUY

Priced on 28 October 2010 Source: ING estimates

We remain BUYers of Isbank, Yapi Kredi and Garanti The stocks have had a good run since 2009 and the share price trajectory should be less steep while the share price gains are likely to moderate. The sources of surprise at other banks are in balance. Among the major banks, we remain BUYers of Isbank, Yapi Kredi and Garanti. Isbank should earn an average 20% ROE in our forecast period (2011-13) and we see Yapi Kredi and Garanti earning an average ROE of c.21% over the same period.

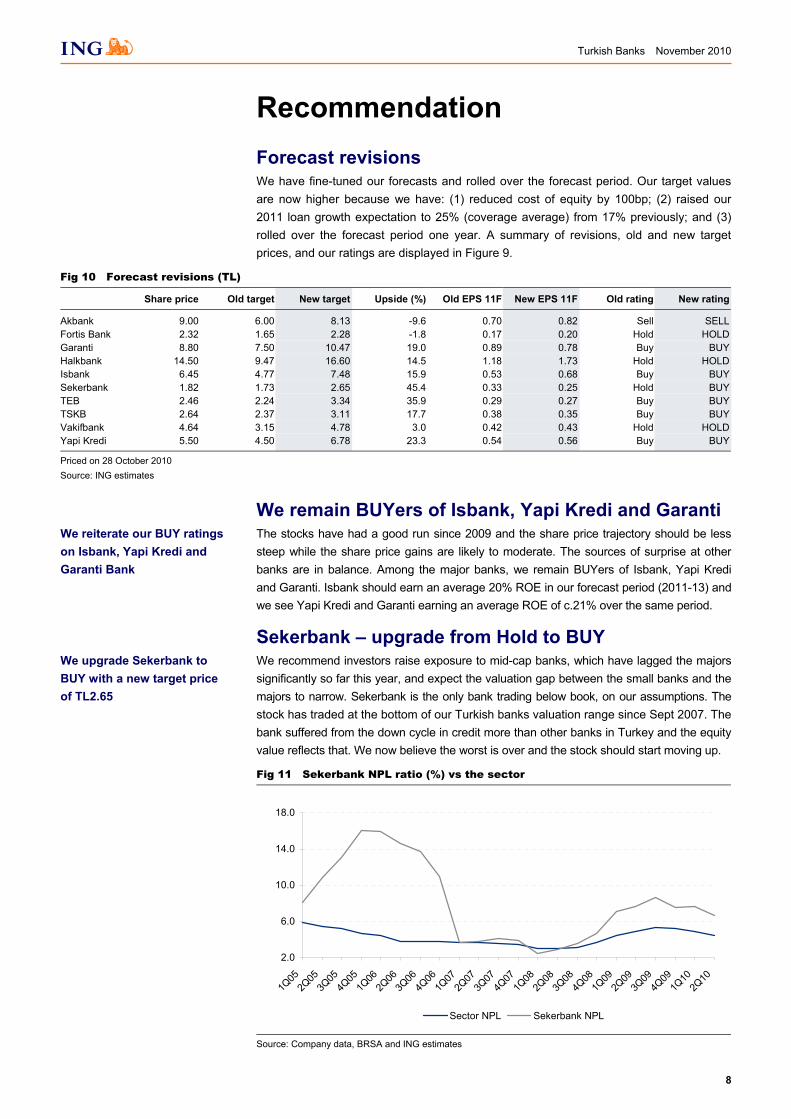

Sekerbank – upgrade from Hold to BUY We recommend investors raise exposure to mid-cap banks, which have lagged the majors significantly so far this year, and expect the valuation gap between the small banks and the majors to narrow. Sekerbank is the only bank trading below book, on our assumptions. The stock has traded at the bottom of our Turkish banks valuation range since Sept 2007. The bank suffered from the down cycle in credit more than other banks in Turkey and the equity value reflects that. We now believe the worst is over and the stock should start moving up.

Fig 11 Sekerbank NPL ratio (%) vs the sector

2.0

6.0

10.0

14.0

18.0

1Q05

2Q05

3Q05

4Q05

1Q06

2Q06

3Q06

4Q06

1Q07

2Q07

3Q07

4Q07

1Q08

2Q08

3Q08

4Q08

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

Sector NPL Sekerbank NPL

Source: Company data, BRSA and ING estimates

We upgrade Sekerbank to BUY with a new target price of TL2.65

We reiterate our BUY ratings on Isbank, Yapi Kredi and Garanti Bank

Turkish Banks November 2010

9

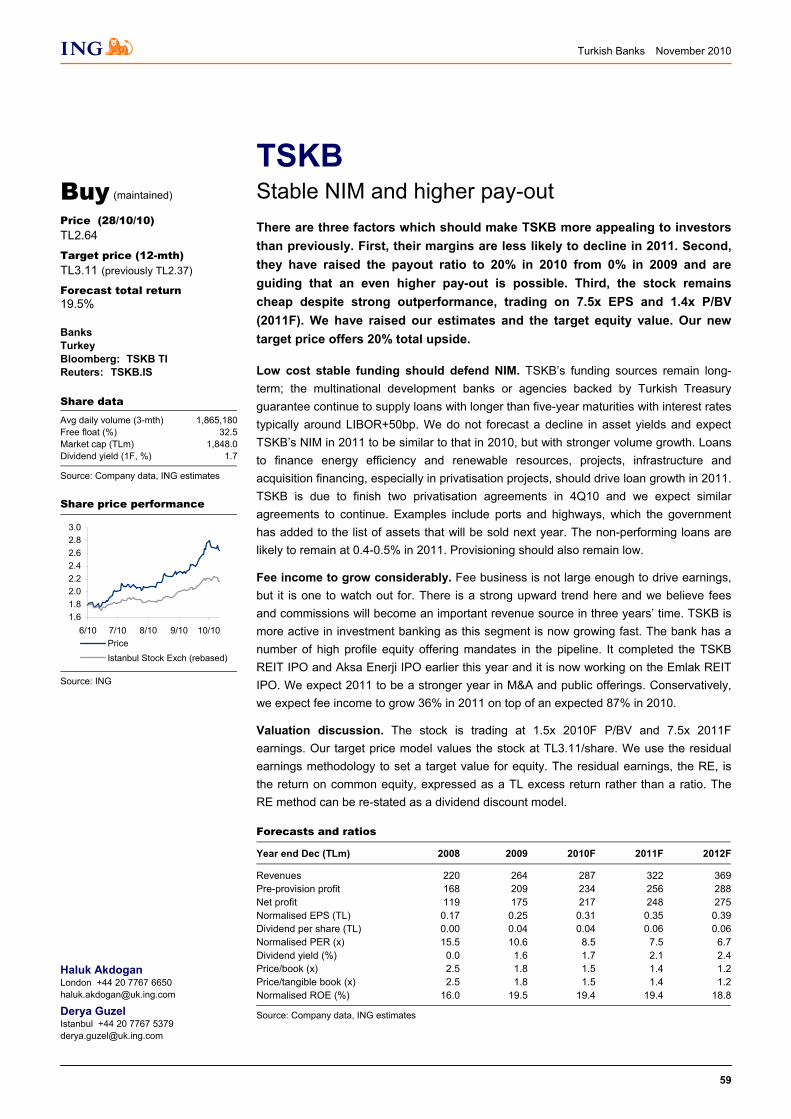

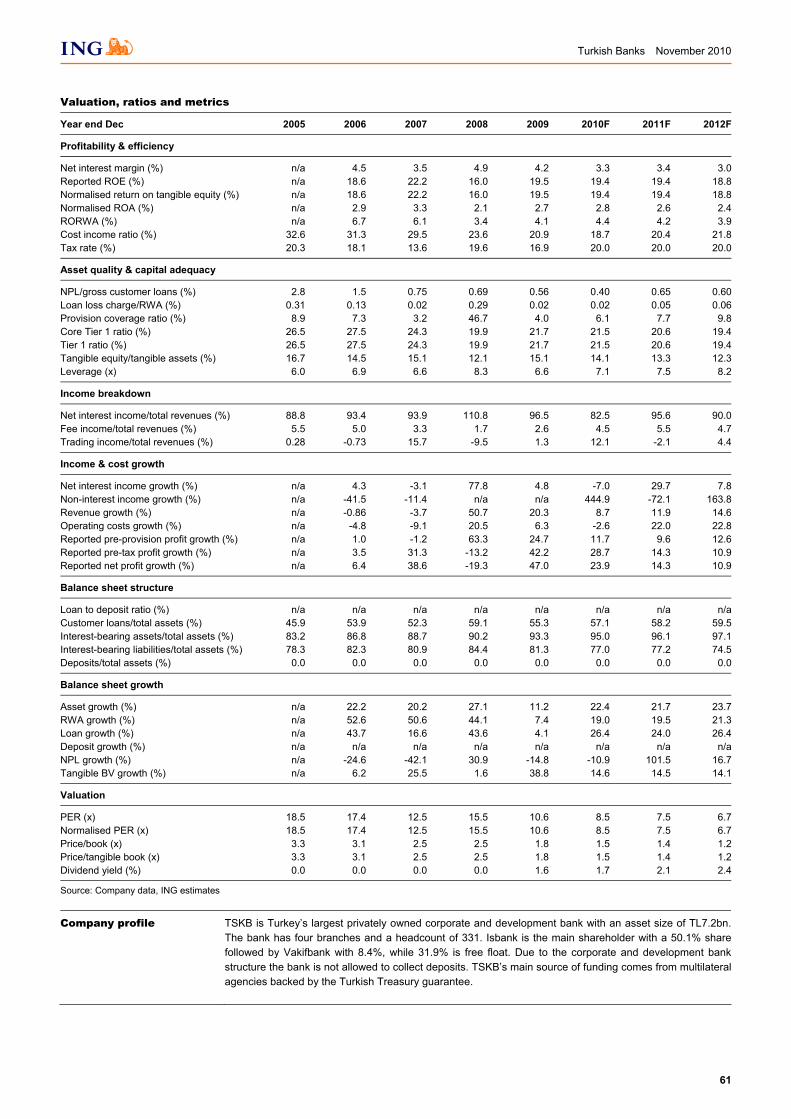

TEB and TSKB – BUY reiterated We reiterate our BUY ratings in TSKB and TEB with target values revised upwards. There are three factors which should make TSKB more appealing to investors this time. First, their margins are less likely to decline in 2011. Second, they have raised the payout ratio in 2010 to 20%, from 0% in 2009. We believe the pay-out may be further upgraded in 2011. Third, the stock remains cheap despite strong outperformance trading on 7.5x EPS and 1.4x book (2011F). We have revisited our model and raised estimates and the target equity value. Our new target price offers 17% upside.

Turkish Banks November 2010

10

Valuation

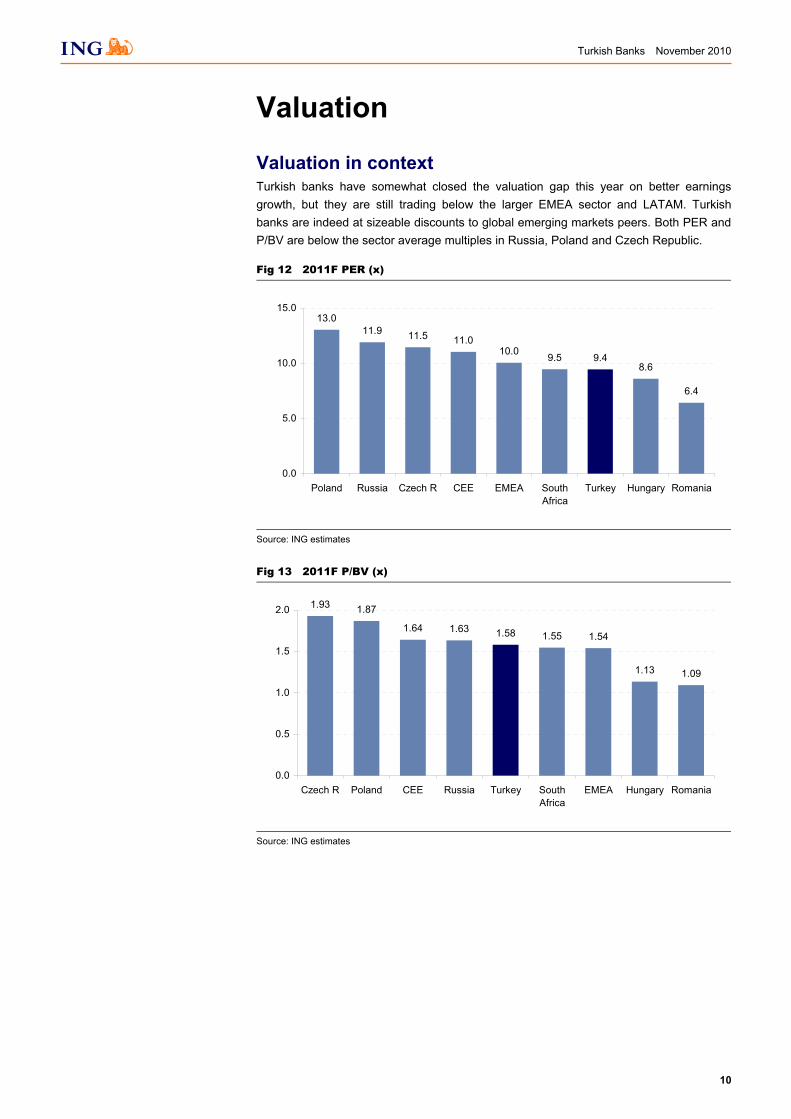

Valuation in context Turkish banks have somewhat closed the valuation gap this year on better earnings growth, but they are still trading below the larger EMEA sector and LATAM. Turkish banks are indeed at sizeable discounts to global emerging markets peers. Both PER and P/BV are below the sector average multiples in Russia, Poland and Czech Republic.

Fig 12 2011F PER (x)

13.011.9

11.010.0 9.5 9.4

6.4

8.6

11.5

0.0

5.0

10.0

15.0

Poland Russia Czech R CEE EMEA SouthAfrica

Turkey Hungary Romania

Source: ING estimates

Fig 13 2011F P/BV (x)

1.93 1.87

1.63 1.58 1.55 1.54

1.09

1.64

1.13

0.0

0.5

1.0

1.5

2.0

Czech R Poland CEE Russia Turkey SouthAfrica

EMEA Hungary Romania

Source: ING estimates

Turkish Banks November 2010

11

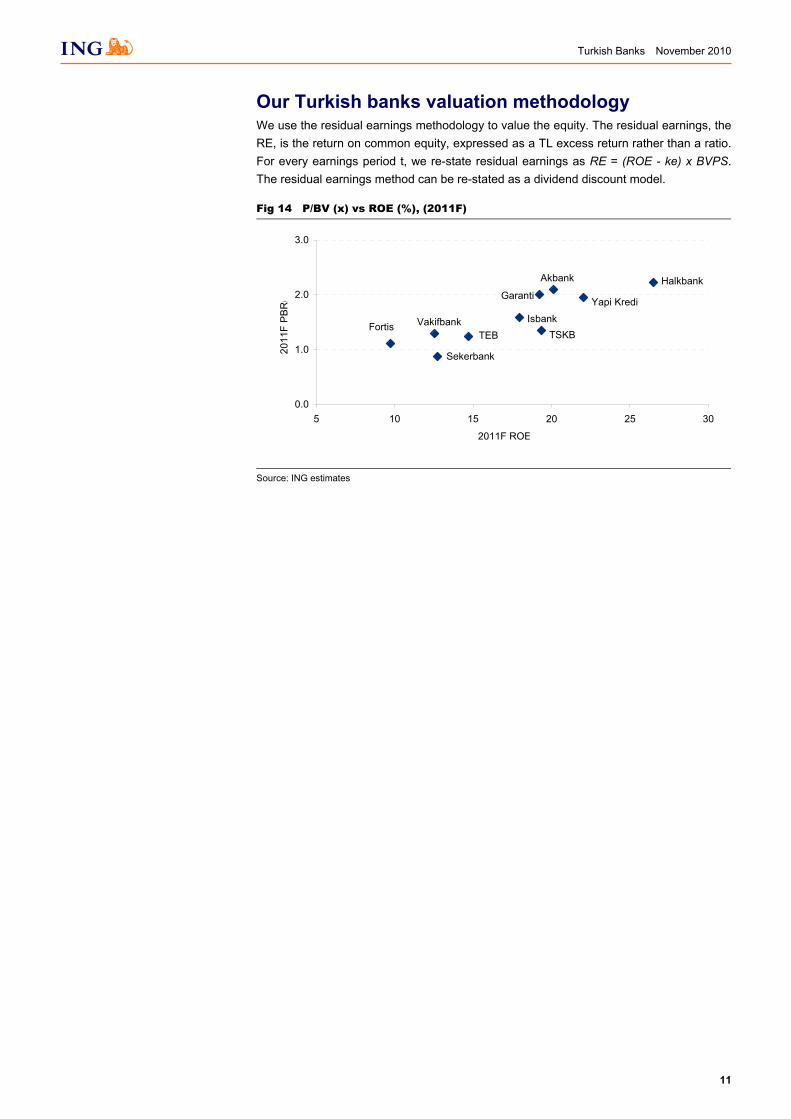

Our Turkish banks valuation methodology We use the residual earnings methodology to value the equity. The residual earnings, the RE, is the return on common equity, expressed as a TL excess return rather than a ratio. For every earnings period t, we re-state residual earnings as RE = (ROE - ke) x BVPS. The residual earnings method can be re-stated as a dividend discount model.

Fig 14 P/BV (x) vs ROE (%), (2011F)

Akbank

Garanti

IsbankVakifbank

Yapi Kredi

Sekerbank

FortisTEB

Halkbank

TSKB

0.0

1.0

2.0

3.0

5 10 15 20 25 30

2011F ROE(%)

2011

F P

BR

(x)

Source: ING estimates

Turkish Banks November 2010

12

Consensus

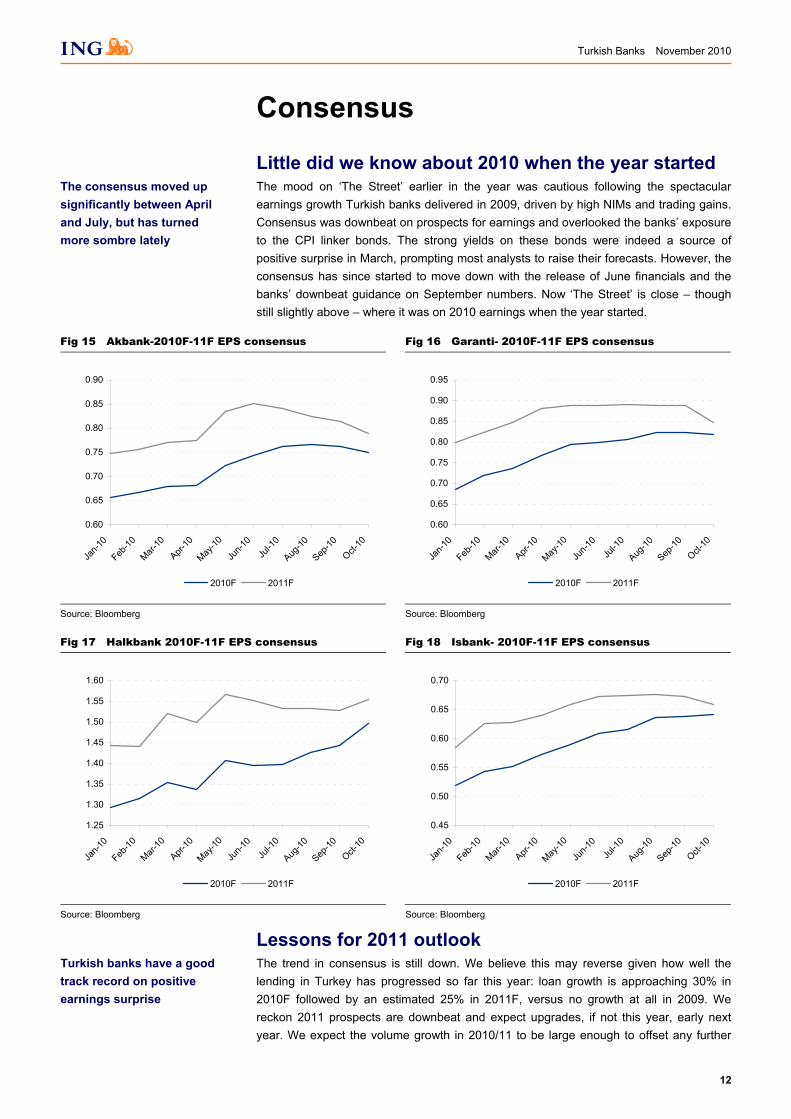

Little did we know about 2010 when the year started The mood on ‘The Street’ earlier in the year was cautious following the spectacular earnings growth Turkish banks delivered in 2009, driven by high NIMs and trading gains. Consensus was downbeat on prospects for earnings and overlooked the banks’ exposure to the CPI linker bonds. The strong yields on these bonds were indeed a source of positive surprise in March, prompting most analysts to raise their forecasts. However, the consensus has since started to move down with the release of June financials and the banks’ downbeat guidance on September numbers. Now ‘The Street’ is close – though still slightly above – where it was on 2010 earnings when the year started.

Fig 15 Akbank-2010F-11F EPS consensus

Fig 16 Garanti- 2010F-11F EPS consensus

0.60

0.65

0.70

0.75

0.80

0.85

0.90

Jan-1

0

Feb-10

Mar-10

Apr-10

May-10

Jun-1

0Ju

l-10

Aug-10

Sep-10

Oct-10

2010F 2011F

0.60

0.65

0.70

0.75

0.80

0.85

0.90

0.95

Jan-1

0

Feb-10

Mar-10

Apr-10

May-10

Jun-1

0Ju

l-10

Aug-10

Sep-10

Oct-10

2010F 2011F

Source: Bloomberg Source: Bloomberg

Fig 17 Halkbank 2010F-11F EPS consensus

Fig 18 Isbank- 2010F-11F EPS consensus

1.25

1.30

1.35

1.40

1.45

1.50

1.55

1.60

Jan-1

0

Feb-10

Mar-10

Apr-10

May-10

Jun-1

0Ju

l-10

Aug-10

Sep-10

Oct-10

2010F 2011F

0.45

0.50

0.55

0.60

0.65

0.70

Jan-1

0

Feb-10

Mar-10

Apr-10

May-10

Jun-1

0Ju

l-10

Aug-10

Sep-10

Oct-10

2010F 2011F

Source: Bloomberg Source: Bloomberg

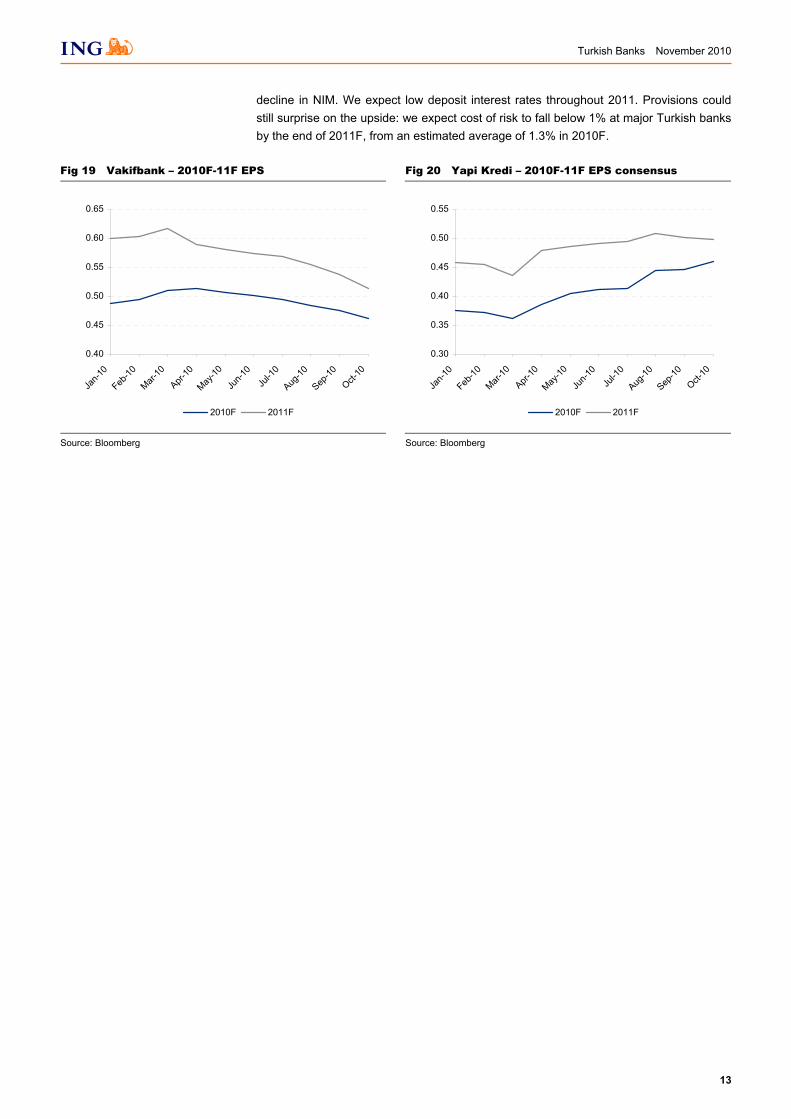

Lessons for 2011 outlook The trend in consensus is still down. We believe this may reverse given how well the lending in Turkey has progressed so far this year: loan growth is approaching 30% in 2010F followed by an estimated 25% in 2011F, versus no growth at all in 2009. We reckon 2011 prospects are downbeat and expect upgrades, if not this year, early next year. We expect the volume growth in 2010/11 to be large enough to offset any further

The consensus moved up significantly between April and July, but has turned more sombre lately

Turkish banks have a good track record on positive earnings surprise

Turkish Banks November 2010

13

decline in NIM. We expect low deposit interest rates throughout 2011. Provisions could still surprise on the upside: we expect cost of risk to fall below 1% at major Turkish banks by the end of 2011F, from an estimated average of 1.3% in 2010F.

Fig 19 Vakifbank – 2010F-11F EPS

Fig 20 Yapi Kredi – 2010F-11F EPS consensus

0.40

0.45

0.50

0.55

0.60

0.65

Jan-1

0

Feb-10

Mar-10

Apr-10

May-10

Jun-1

0Ju

l-10

Aug-10

Sep-10

Oct-10

2010F 2011F

0.30

0.35

0.40

0.45

0.50

0.55

Jan-1

0

Feb-10

Mar-10

Apr-10

May-10

Jun-1

0Ju

l-10

Aug-10

Sep-10

Oct-10

2010F 2011F

Source: Bloomberg Source: Bloomberg

Turkish Banks November 2010

14

Sources of risk We recognise: (1) yields on CPI-linked Turkish Treasury bonds; (2) asset disposals at selected banks; (3) industry loan growth; and (4) further decline in and normalisation of cost of risk, as sources of both upside and downside risks to our estimates. We list and discuss some of these factors below.

Inflation as a source of risk – upside and downside Inflation is a risk source for banks with exposure to indexed bonds. The indexed bonds are probably the most important source of surprise given how much the banks added in 3Q10. Earnings at Akbank, Garanti and Isbank would surprise us on the high side if the inflation increased more than we anticipate. Yapi Kredi, Vakifbank and Halkbank have relatively smaller exposure to inflation indexed bonds and hence their earnings should be less volatile, in our view. A 100bp surprise in inflation would alter earnings 2-3% in either direction at selected banks, notably Akbank, Garanti and Isbank. Our view on inflation is that it will be flat or down between now and the end of 2011. We are thus less enthusiastic about banks that have accumulated inflation indexed bonds.

Asset disposals as a source of upside risk We also see divestitures as sources of upside risk. There are four banks which could benefit from assets sales in the next two years. These are, in decreasing order of importance, Garanti Bank, Isbank, Yapi Kredi, and Vakifbank.

1) Garanti Bank is likely to sell down its remaining stake in insurance. Both the put option held by Garanti and the call option on Garanti Emeklilik, the life and pensions business, held by Eureka, are now exercisable. Management expects to exercise the put option and sell its 20% share in Garanti Sigorta, the non-life business, to Eureka, possibly later this year. The call option, if exercised, would add an estimated 17-18% to Garanti Bank’s 2011 earnings and the put option would contribute 3-4%.

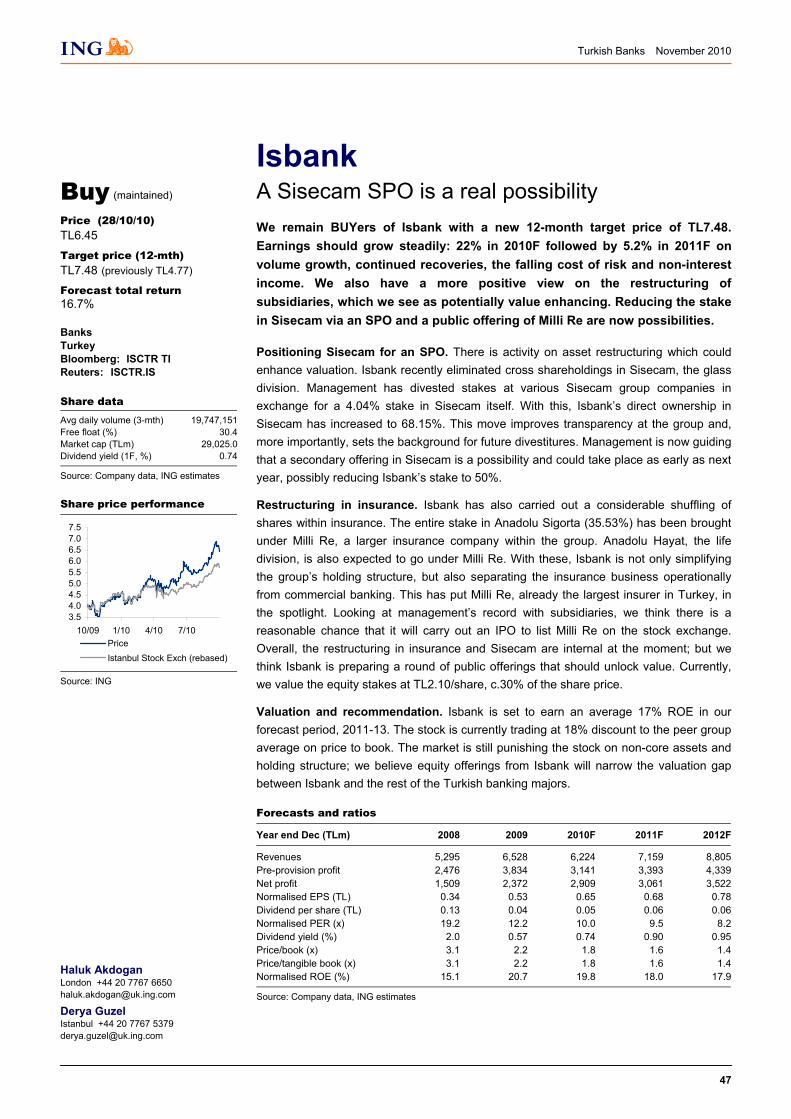

2) Isbank may reduce its stake in Sisecam (currently 68%), in a secondary public offering. The restructuring in the insurance division is well underway and we are now expecting the bank’s stake in Anadolu Hayat, the life insurance subsidiary, to come under Milli Re. Isbank may consider selling shares in Milli Re in an IPO. Both the Sisecam SPO and a potential Milli Re IPO should unlock value at the Isbank level. Our estimates and valuation do not factor in any asset sales or equity offerings.

3) Yapi Kredi may sell its controlling stake in Yapi Kredi Sigorta (74%). The prospects are less clear on this but if the bank did sell its insurance subsidiary in 2011, this would conservatively add an estimated 15% to earnings, on our preliminary assumptions on valuation.

4) Vakifbank also has a stake in Güneş Sigorta, part-owned by Groupama SA. Looking at the M&A activity of late in the Turkish insurance sector, we believe Vakifbank may want to sell its 34% stake in Güneş. Groupama has already declared its interest. Earlier this year NKSJ Holdings Inc. agreed to acquire Fiba Sigorta AS, an insurance business.

Inflation is a risk source for banks with exposure to indexed bonds. The indexed bonds are probably the most important source of surprise given how much the banks added in 3Q10. A 100bp surprise in inflation would alter earnings 2-3% in either direction at selected banks, notably Akbank, Garanti and Isbank.

Garanti Bank: further stake sale in insurance

Isbank and potential asset disposals: Sisecam and Milli Re

Yapi Kredi and Yapi Kredi Sigorta

Vakifbank and Güneş Sigorta

Turkish Banks November 2010

15

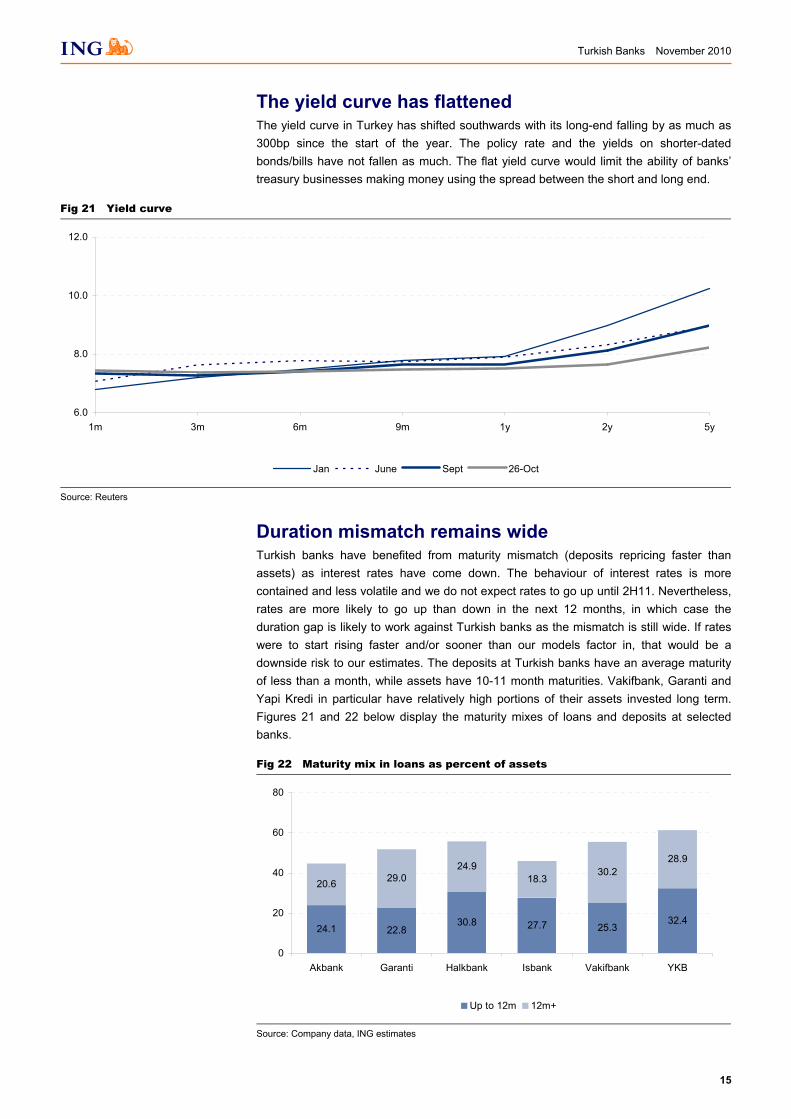

The yield curve has flattened The yield curve in Turkey has shifted southwards with its long-end falling by as much as 300bp since the start of the year. The policy rate and the yields on shorter-dated bonds/bills have not fallen as much. The flat yield curve would limit the ability of banks’ treasury businesses making money using the spread between the short and long end.

Fig 21 Yield curve

6.0

8.0

10.0

12.0

1m 3m 6m 9m 1y 2y 5y

Jan June Sept 26-Oct

Source: Reuters

Duration mismatch remains wide Turkish banks have benefited from maturity mismatch (deposits repricing faster than assets) as interest rates have come down. The behaviour of interest rates is more contained and less volatile and we do not expect rates to go up until 2H11. Nevertheless, rates are more likely to go up than down in the next 12 months, in which case the duration gap is likely to work against Turkish banks as the mismatch is still wide. If rates were to start rising faster and/or sooner than our models factor in, that would be a downside risk to our estimates. The deposits at Turkish banks have an average maturity of less than a month, while assets have 10-11 month maturities. Vakifbank, Garanti and Yapi Kredi in particular have relatively high portions of their assets invested long term. Figures 21 and 22 below display the maturity mixes of loans and deposits at selected banks.

Fig 22 Maturity mix in loans as percent of assets

24.1 22.830.8 27.7 25.3

32.4

20.6 29.024.9

18.330.2

28.9

0

20

40

60

80

Akbank Garanti Halkbank Isbank Vakifbank YKB

Up to 12m 12m+

Source: Company data, ING estimates

Turkish Banks November 2010

16

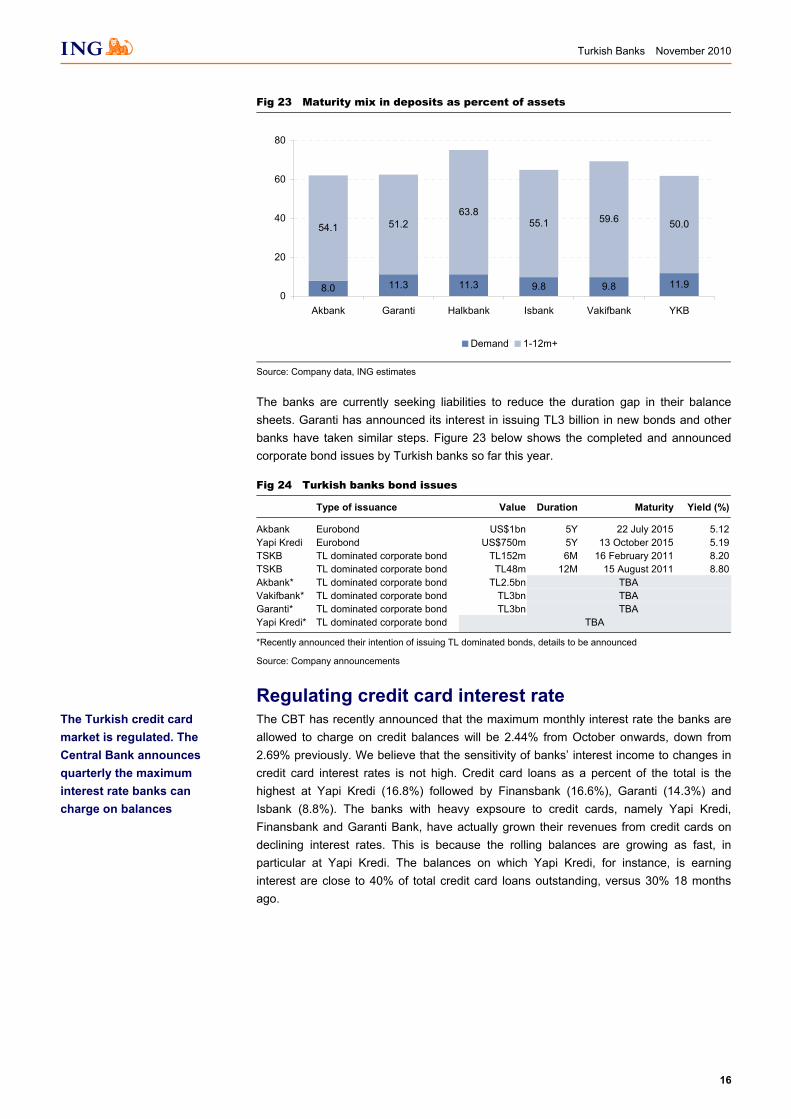

Fig 23 Maturity mix in deposits as percent of assets

8.0 11.3 11.3 9.8 9.8 11.9

54.1 51.263.8

55.1 59.6 50.0

0

20

40

60

80

Akbank Garanti Halkbank Isbank Vakifbank YKB

Demand 1-12m+

Source: Company data, ING estimates

The banks are currently seeking liabilities to reduce the duration gap in their balance sheets. Garanti has announced its interest in issuing TL3 billion in new bonds and other banks have taken similar steps. Figure 23 below shows the completed and announced corporate bond issues by Turkish banks so far this year.

Fig 24 Turkish banks bond issues

Type of issuance Value Duration Maturity Yield (%)

Akbank Eurobond US$1bn 5Y 22 July 2015 5.12Yapi Kredi Eurobond US$750m 5Y 13 October 2015 5.19TSKB TL dominated corporate bond TL152m 6M 16 February 2011 8.20TSKB TL dominated corporate bond TL48m 12M 15 August 2011 8.80Akbank* TL dominated corporate bond TL2.5bn TBA Vakifbank* TL dominated corporate bond TL3bn TBA Garanti* TL dominated corporate bond TL3bn TBA Yapi Kredi* TL dominated corporate bond TBA

*Recently announced their intention of issuing TL dominated bonds, details to be announced

Source: Company announcements

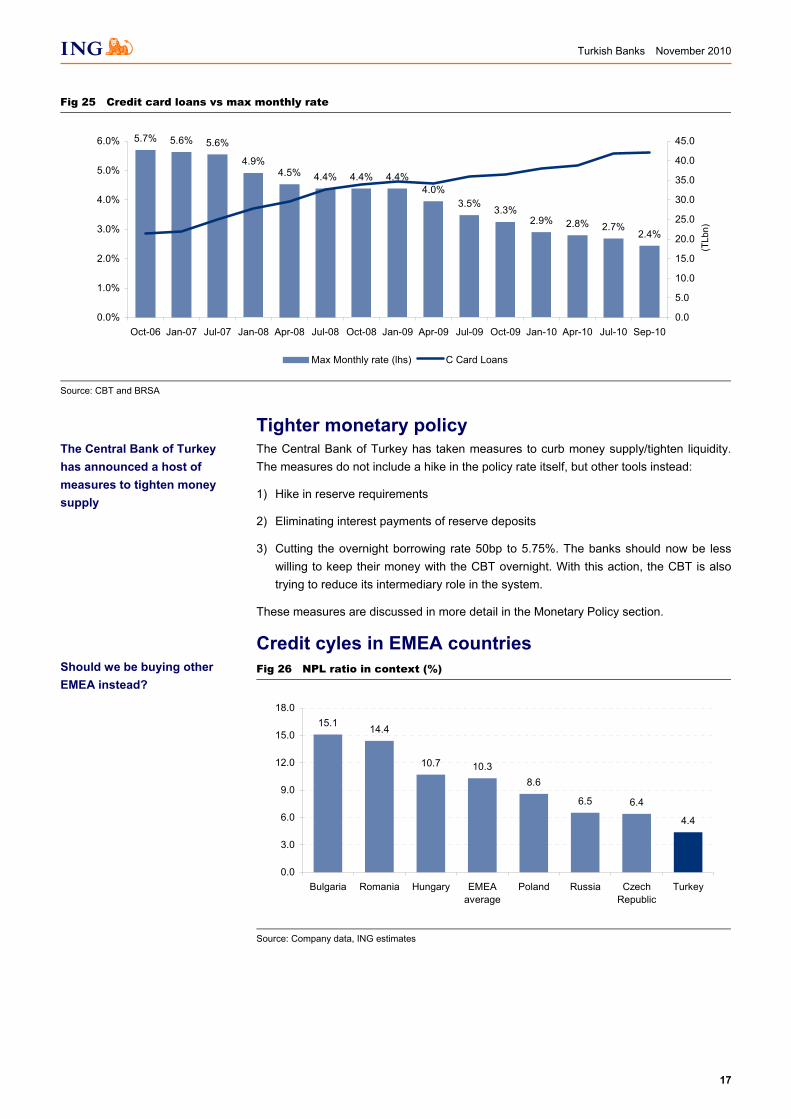

Regulating credit card interest rate The CBT has recently announced that the maximum monthly interest rate the banks are allowed to charge on credit balances will be 2.44% from October onwards, down from 2.69% previously. We believe that the sensitivity of banks’ interest income to changes in credit card interest rates is not high. Credit card loans as a percent of the total is the highest at Yapi Kredi (16.8%) followed by Finansbank (16.6%), Garanti (14.3%) and Isbank (8.8%). The banks with heavy expsoure to credit cards, namely Yapi Kredi, Finansbank and Garanti Bank, have actually grown their revenues from credit cards on declining interest rates. This is because the rolling balances are growing as fast, in particular at Yapi Kredi. The balances on which Yapi Kredi, for instance, is earning interest are close to 40% of total credit card loans outstanding, versus 30% 18 months ago.

The Turkish credit card market is regulated. The Central Bank announces quarterly the maximum interest rate banks can charge on balances

Turkish Banks November 2010

17

Fig 25 Credit card loans vs max monthly rate

5.7% 5.6% 5.6%

4.9%4.5% 4.4% 4.4% 4.4%

4.0%3.5%

3.3%2.9% 2.8% 2.7%

2.4%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Oct-06 Jan-07 Jul-07 Jan-08 Apr-08 Jul-08 Oct-08 Jan-09 Apr-09 Jul-09 Oct-09 Jan-10 Apr-10 Jul-10 Sep-10

%

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

TLbn

Max Monthly rate (lhs) C Card Loans

Source: CBT and BRSA

Tighter monetary policy The Central Bank of Turkey has taken measures to curb money supply/tighten liquidity. The measures do not include a hike in the policy rate itself, but other tools instead:

1) Hike in reserve requirements

2) Eliminating interest payments of reserve deposits

3) Cutting the overnight borrowing rate 50bp to 5.75%. The banks should now be less willing to keep their money with the CBT overnight. With this action, the CBT is also trying to reduce its intermediary role in the system.

These measures are discussed in more detail in the Monetary Policy section.

Credit cyles in EMEA countries Fig 26 NPL ratio in context (%)

15.1 14.4

10.7 10.38.6

6.5 6.4

4.4

0.0

3.0

6.0

9.0

12.0

15.0

18.0

Bulgaria Romania Hungary EMEAaverage

Poland Russia CzechRepublic

Turkey

Source: Company data, ING estimates

The Central Bank of Turkey has announced a host of measures to tighten money supply

Should we be buying other EMEA instead?

(TLb

n)

Turkish Banks November 2010

18

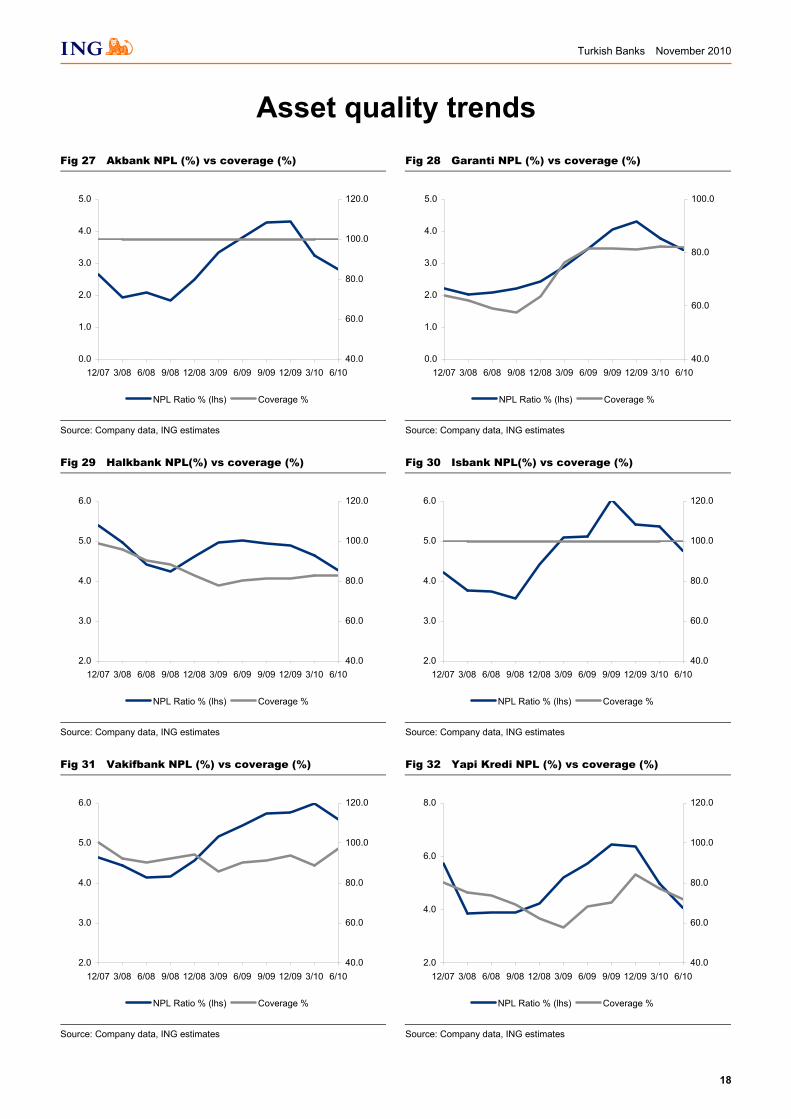

Asset quality trends Fig 27 Akbank NPL (%) vs coverage (%)

Fig 28 Garanti NPL (%) vs coverage (%)

0.0

1.0

2.0

3.0

4.0

5.0

12/07 3/08 6/08 9/08 12/08 3/09 6/09 9/09 12/09 3/10 6/1040.0

60.0

80.0

100.0

120.0

NPL Ratio % (lhs) Coverage %

0.0

1.0

2.0

3.0

4.0

5.0

12/07 3/08 6/08 9/08 12/08 3/09 6/09 9/09 12/09 3/10 6/1040.0

60.0

80.0

100.0

NPL Ratio % (lhs) Coverage %

Source: Company data, ING estimates Source: Company data, ING estimates

Fig 29 Halkbank NPL(%) vs coverage (%)

Fig 30 Isbank NPL(%) vs coverage (%)

2.0

3.0

4.0

5.0

6.0

12/07 3/08 6/08 9/08 12/08 3/09 6/09 9/09 12/09 3/10 6/1040.0

60.0

80.0

100.0

120.0

NPL Ratio % (lhs) Coverage %

2.0

3.0

4.0

5.0

6.0

12/07 3/08 6/08 9/08 12/08 3/09 6/09 9/09 12/09 3/10 6/1040.0

60.0

80.0

100.0

120.0

NPL Ratio % (lhs) Coverage %

Source: Company data, ING estimates Source: Company data, ING estimates

Fig 31 Vakifbank NPL (%) vs coverage (%)

Fig 32 Yapi Kredi NPL (%) vs coverage (%)

2.0

3.0

4.0

5.0

6.0

12/07 3/08 6/08 9/08 12/08 3/09 6/09 9/09 12/09 3/10 6/1040.0

60.0

80.0

100.0

120.0

NPL Ratio % (lhs) Coverage %

2.0

4.0

6.0

8.0

12/07 3/08 6/08 9/08 12/08 3/09 6/09 9/09 12/09 3/10 6/1040.0

60.0

80.0

100.0

120.0

NPL Ratio % (lhs) Coverage %

Source: Company data, ING estimates Source: Company data, ING estimates

Turkish Banks November 2010

19

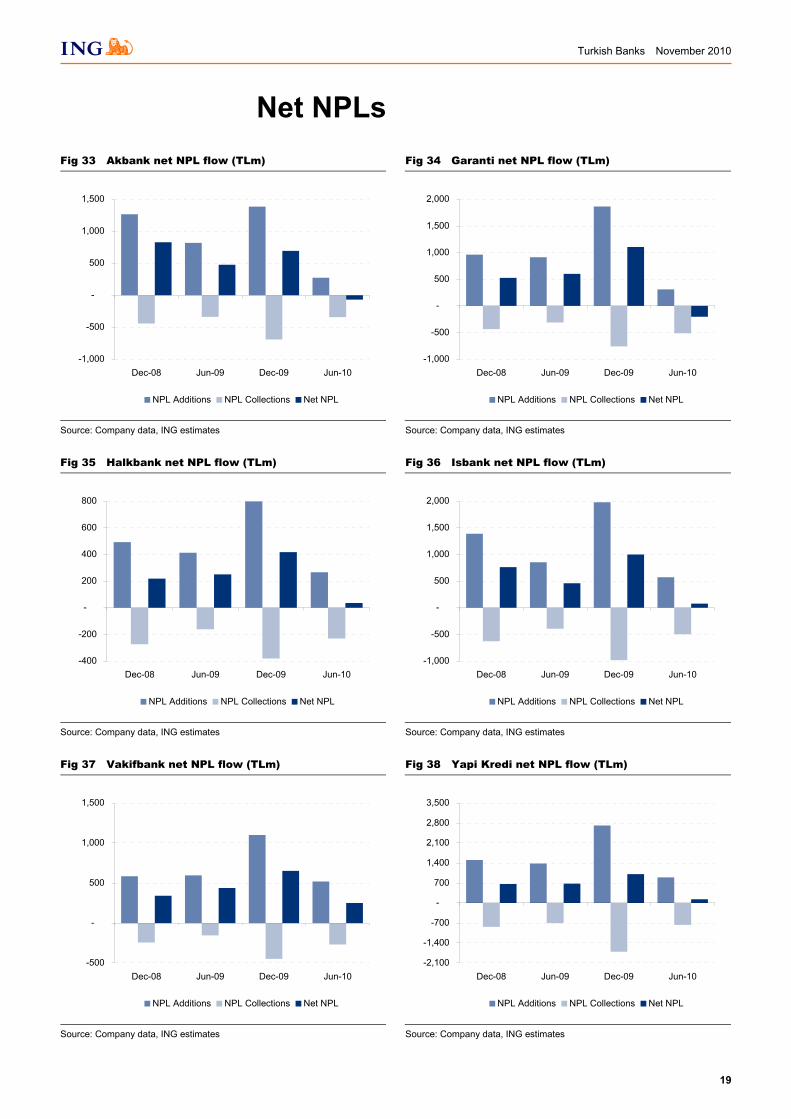

Net NPLs Fig 33 Akbank net NPL flow (TLm)

Fig 34 Garanti net NPL flow (TLm)

-1,000

-500

-

500

1,000

1,500

Dec-08 Jun-09 Dec-09 Jun-10

NPL Additions NPL Collections Net NPL

-1,000

-500

-

500

1,000

1,500

2,000

Dec-08 Jun-09 Dec-09 Jun-10

NPL Additions NPL Collections Net NPL

Source: Company data, ING estimates Source: Company data, ING estimates

Fig 35 Halkbank net NPL flow (TLm)

Fig 36 Isbank net NPL flow (TLm)

-400

-200

-

200

400

600

800

Dec-08 Jun-09 Dec-09 Jun-10

NPL Additions NPL Collections Net NPL

-1,000

-500

-

500

1,000

1,500

2,000

Dec-08 Jun-09 Dec-09 Jun-10

NPL Additions NPL Collections Net NPL

Source: Company data, ING estimates Source: Company data, ING estimates

Fig 37 Vakifbank net NPL flow (TLm)

Fig 38 Yapi Kredi net NPL flow (TLm)

-500

-

500

1,000

1,500

Dec-08 Jun-09 Dec-09 Jun-10

NPL Additions NPL Collections Net NPL

-2,100

-1,400

-700

-

700

1,400

2,100

2,800

3,500

Dec-08 Jun-09 Dec-09 Jun-10

NPL Additions NPL Collections Net NPL

Source: Company data, ING estimates Source: Company data, ING estimates

Turkish Banks November 2010

20

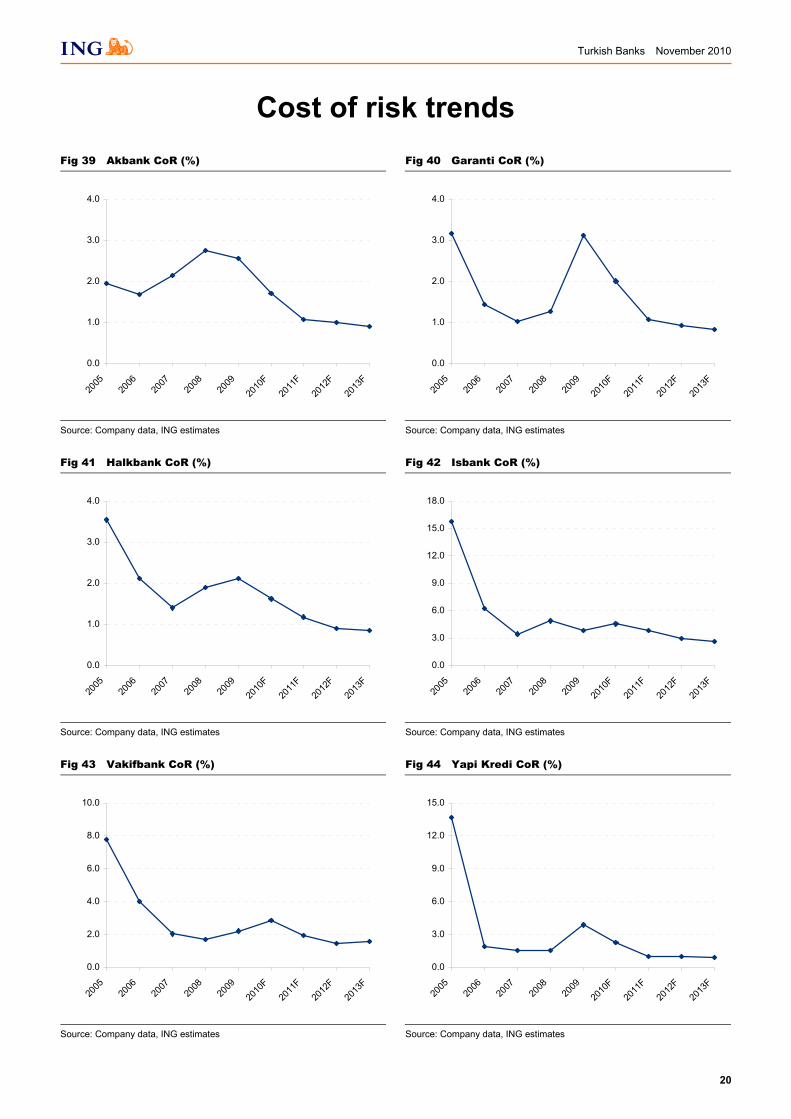

Cost of risk trends Fig 39 Akbank CoR (%)

Fig 40 Garanti CoR (%)

0.0

1.0

2.0

3.0

4.0

2005

2006

2007

2008

2009

2010

F20

11F

2012

F20

13F

0.0

1.0

2.0

3.0

4.0

2005

2006

2007

2008

2009

2010

F20

11F

2012

F20

13F

Source: Company data, ING estimates Source: Company data, ING estimates

Fig 41 Halkbank CoR (%)

Fig 42 Isbank CoR (%)

0.0

1.0

2.0

3.0

4.0

2005

2006

2007

2008

2009

2010

F20

11F

2012

F20

13F

0.0

3.0

6.0

9.0

12.0

15.0

18.0

2005

2006

2007

2008

2009

2010

F20

11F

2012

F20

13F

Source: Company data, ING estimates Source: Company data, ING estimates

Fig 43 Vakifbank CoR (%)

Fig 44 Yapi Kredi CoR (%)

0.0

2.0

4.0

6.0

8.0

10.0

2005

2006

2007

2008

2009

2010

F20

11F

2012

F20

13F

0.0

3.0

6.0

9.0

12.0

15.0

2005

2006

2007

2008

2009

2010

F20

11F

2012

F20

13F

Source: Company data, ING estimates Source: Company data, ING estimates

Turkish Banks November 2010

21

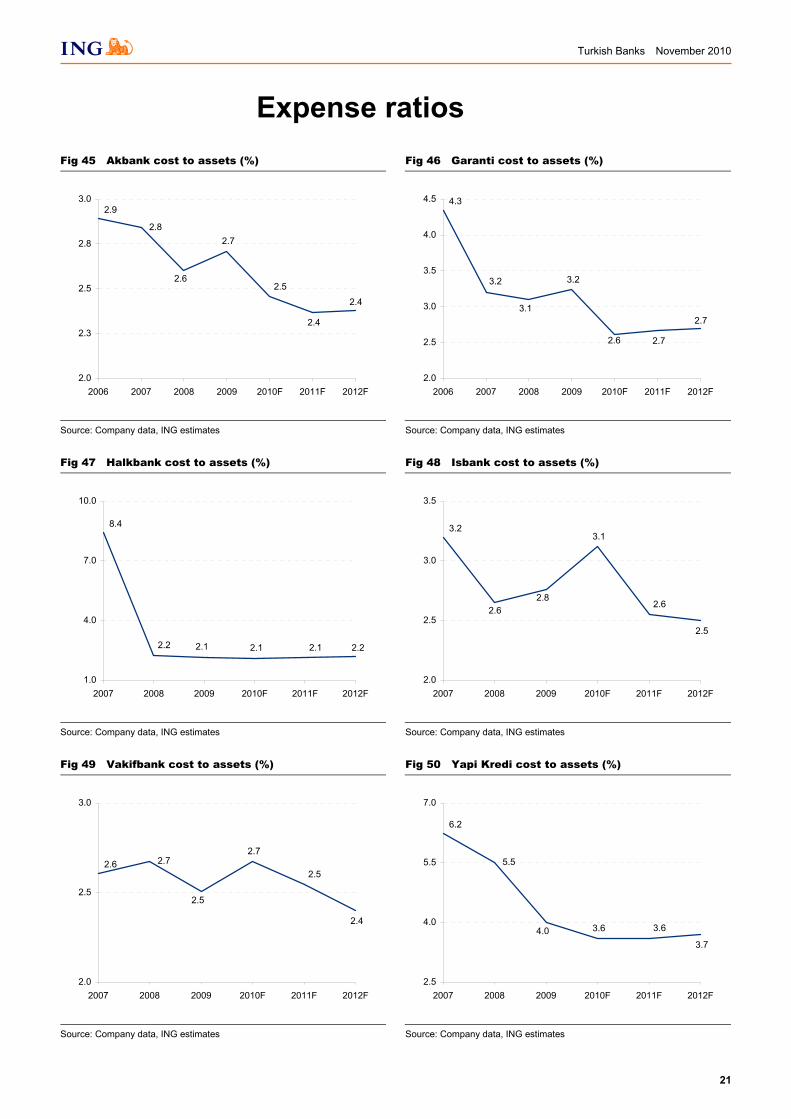

Expense ratios Fig 45 Akbank cost to assets (%)

Fig 46 Garanti cost to assets (%)

2.8

2.9

2.4

2.4

2.5

2.7

2.6

2.0

2.3

2.5

2.8

3.0

2006 2007 2008 2009 2010F 2011F 2012F

3.2

3.1

3.2

2.6 2.7

2.7

4.3

2.0

2.5

3.0

3.5

4.0

4.5

2006 2007 2008 2009 2010F 2011F 2012F

Source: Company data, ING estimates Source: Company data, ING estimates

Fig 47 Halkbank cost to assets (%)

Fig 48 Isbank cost to assets (%)

2.2

8.4

2.22.12.12.1

1.0

4.0

7.0

10.0

2007 2008 2009 2010F 2011F 2012F

2.62.8

3.1

2.6

2.5

3.2

2.0

2.5

3.0

3.5

2007 2008 2009 2010F 2011F 2012F

Source: Company data, ING estimates Source: Company data, ING estimates

Fig 49 Vakifbank cost to assets (%)

Fig 50 Yapi Kredi cost to assets (%)

2.72.6

2.4

2.5

2.7

2.5

2.0

2.5

3.0

2007 2008 2009 2010F 2011F 2012F

5.5

4.0 3.6 3.6

3.7

6.2

2.5

4.0

5.5

7.0

2007 2008 2009 2010F 2011F 2012F

Source: Company data, ING estimates Source: Company data, ING estimates

Turkish Banks November 2010

22

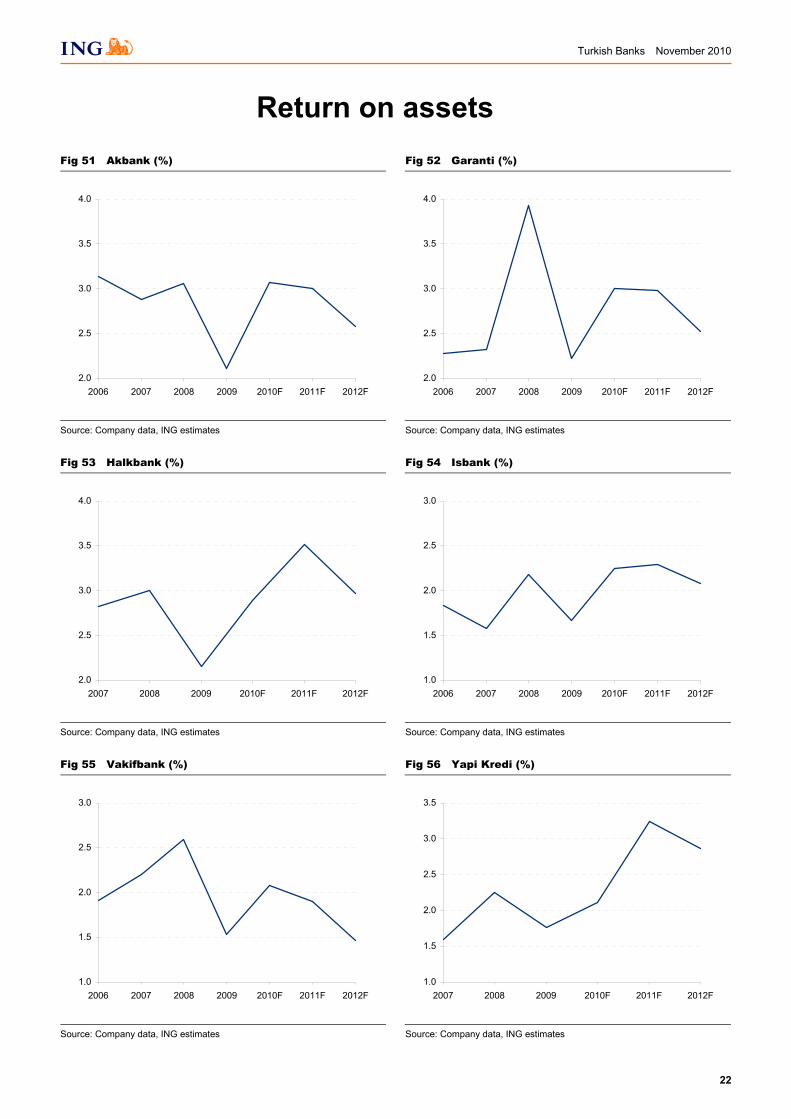

Return on assets Fig 51 Akbank (%)

Fig 52 Garanti (%)

2.0

2.5

3.0

3.5

4.0

2006 2007 2008 2009 2010F 2011F 2012F

2.0

2.5

3.0

3.5

4.0

2006 2007 2008 2009 2010F 2011F 2012F

Source: Company data, ING estimates Source: Company data, ING estimates

Fig 53 Halkbank (%)

Fig 54 Isbank (%)

2.0

2.5

3.0

3.5

4.0

2007 2008 2009 2010F 2011F 2012F

1.0

1.5

2.0

2.5

3.0

2006 2007 2008 2009 2010F 2011F 2012F

Source: Company data, ING estimates Source: Company data, ING estimates

Fig 55 Vakifbank (%)

Fig 56 Yapi Kredi (%)

1.0

1.5

2.0

2.5

3.0

2006 2007 2008 2009 2010F 2011F 2012F

1.0

1.5

2.0

2.5

3.0

3.5

2007 2008 2009 2010F 2011F 2012F

Source: Company data, ING estimates Source: Company data, ING estimates

Turkish Banks November 2010

23

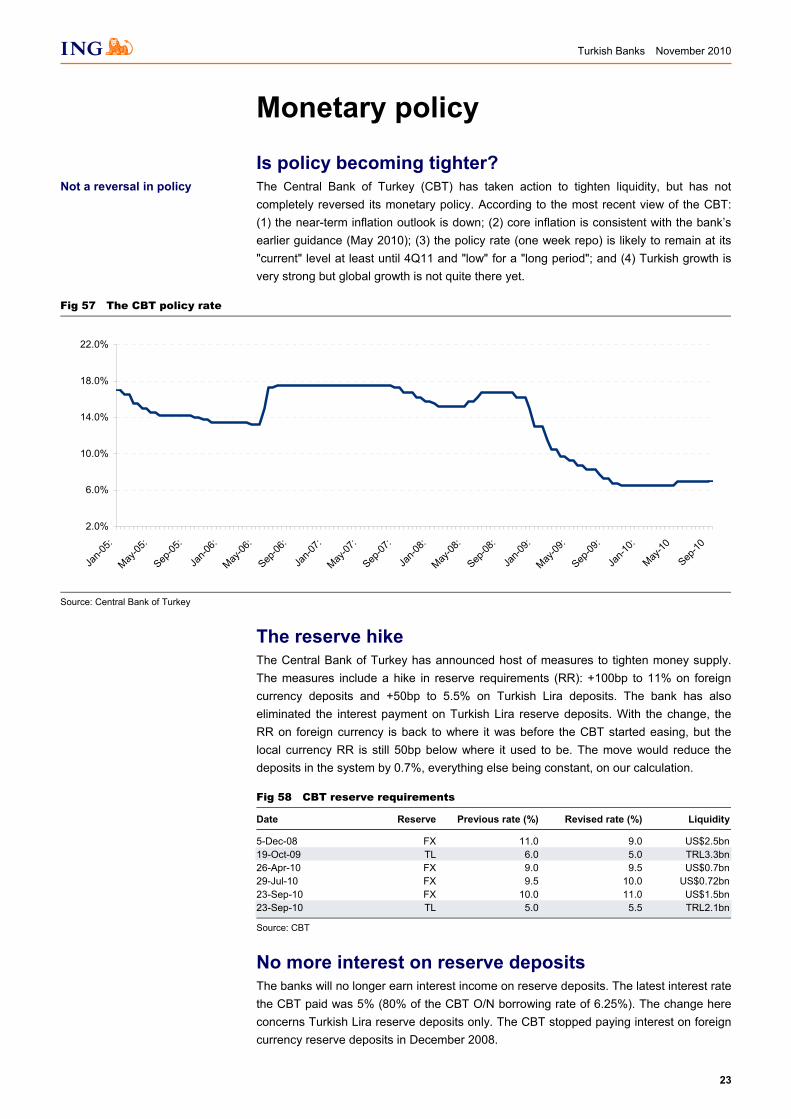

Monetary policy

Is policy becoming tighter? The Central Bank of Turkey (CBT) has taken action to tighten liquidity, but has not completely reversed its monetary policy. According to the most recent view of the CBT: (1) the near-term inflation outlook is down; (2) core inflation is consistent with the bank’s earlier guidance (May 2010); (3) the policy rate (one week repo) is likely to remain at its "current" level at least until 4Q11 and "low" for a "long period"; and (4) Turkish growth is very strong but global growth is not quite there yet.

Fig 57 The CBT policy rate

2.0%

6.0%

10.0%

14.0%

18.0%

22.0%

Jan-0

5:

May-05

:

Sep-05

:

Jan-0

6:

May-06

:

Sep-06

:

Jan-0

7:

May-07

:

Sep-07

:

Jan-0

8:

May-08

:

Sep-08

:

Jan-0

9:

May-09

:

Sep-09

:

Jan-1

0:

May-10

Sep-10

Source: Central Bank of Turkey

The reserve hike The Central Bank of Turkey has announced host of measures to tighten money supply. The measures include a hike in reserve requirements (RR): +100bp to 11% on foreign currency deposits and +50bp to 5.5% on Turkish Lira deposits. The bank has also eliminated the interest payment on Turkish Lira reserve deposits. With the change, the RR on foreign currency is back to where it was before the CBT started easing, but the local currency RR is still 50bp below where it used to be. The move would reduce the deposits in the system by 0.7%, everything else being constant, on our calculation.

Fig 58 CBT reserve requirements

Date Reserve Previous rate (%) Revised rate (%) Liquidity

5-Dec-08 FX 11.0 9.0 US$2.5bn19-Oct-09 TL 6.0 5.0 TRL3.3bn26-Apr-10 FX 9.0 9.5 US$0.7bn29-Jul-10 FX 9.5 10.0 US$0.72bn23-Sep-10 FX 10.0 11.0 US$1.5bn23-Sep-10 TL 5.0 5.5 TRL2.1bn

Source: CBT

No more interest on reserve deposits The banks will no longer earn interest income on reserve deposits. The latest interest rate the CBT paid was 5% (80% of the CBT O/N borrowing rate of 6.25%). The change here concerns Turkish Lira reserve deposits only. The CBT stopped paying interest on foreign currency reserve deposits in December 2008.

Not a reversal in policy

Turkish Banks November 2010

24

The Turkish Lira borrowing window is nearly shut In its most recent MPC meeting, the CBT kept the one-week repo rate at 7% as expected, but reduced the overnight borrowing rate 50bp to 5.75%. This is the rate banks get if they park their money with the CBT overnight. The CBT is trying to reduce its intermediary role in TL and asking banks to use interbank (lend/borrow among themselves) instead. The bank’s objective here is to decrease the end-of-day excess liquidity in the system, and they have been doing this since September.

Liquidity is tighter near term Both the reserve hike and the elimination of payments on reserve deposits are in line with the Central Bank’s “exit” strategy. The CBT has already guided the markets that it has looked to raise the RR and stop paying interest on TL reserves. Thus, there is no surprise here and the banks most likely knew when the actual announcement would come. We expect the policy rate to remain at 7% until after the elections. The CBT will find it hard to start hiking rates when the global stimuli is likely to continue in 2011 at a pace no slower than that in 2010, or before the Federal Reserve and ECB reverse their policies. We are also of the view that any negative impacts of the reserve hike and the elimination of interest payment on reserve deposits should be offset by the weekly repo rate remaining at its current level longer than the market expects.

Liquidity is tighter near-term but the policy rate should remain low for longer

Turkish Banks November 2010

25

Economic fundamentals

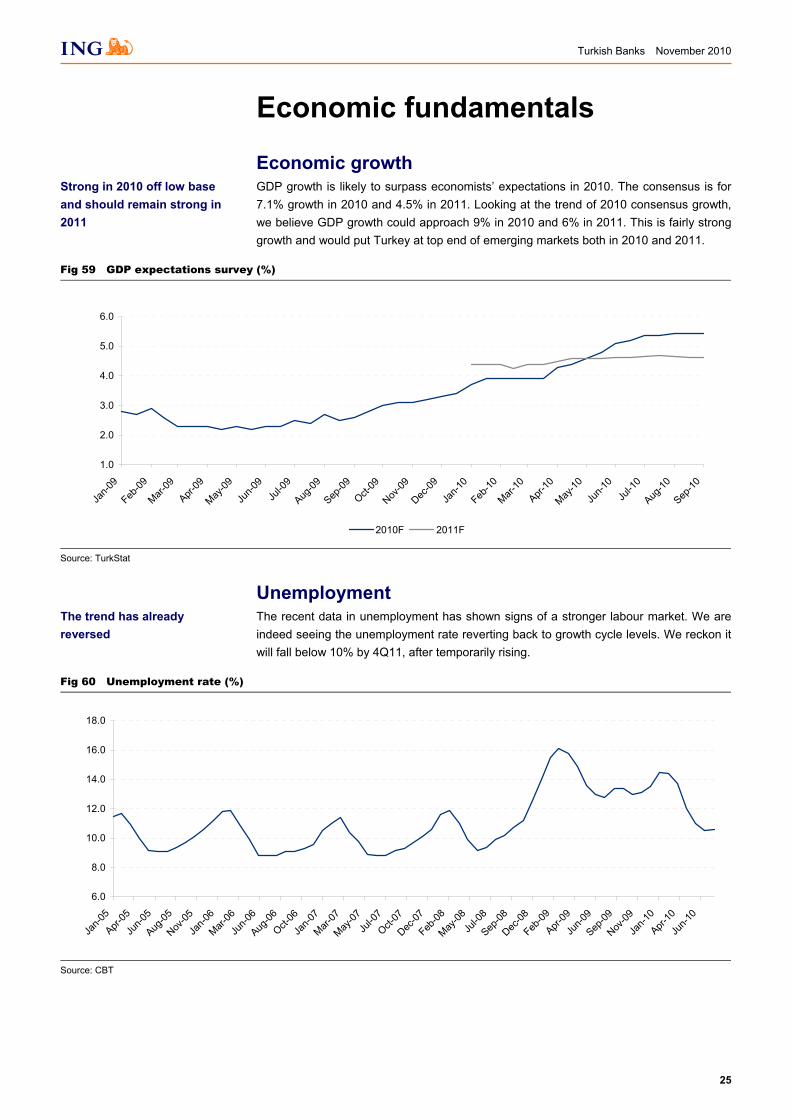

Economic growth GDP growth is likely to surpass economists’ expectations in 2010. The consensus is for 7.1% growth in 2010 and 4.5% in 2011. Looking at the trend of 2010 consensus growth, we believe GDP growth could approach 9% in 2010 and 6% in 2011. This is fairly strong growth and would put Turkey at top end of emerging markets both in 2010 and 2011.

Fig 59 GDP expectations survey (%)

1.0

2.0

3.0

4.0

5.0

6.0

Jan-0

9

Feb-09

Mar-09

Apr-09

May-09

Jun-0

9Ju

l-09

Aug-09

Sep-09

Oct-09

Nov-09

Dec-09

Jan-1

0

Feb-10

Mar-10

Apr-10

May-10

Jun-1

0Ju

l-10

Aug-10

Sep-10

2010F 2011F

Source: TurkStat

Unemployment The recent data in unemployment has shown signs of a stronger labour market. We are indeed seeing the unemployment rate reverting back to growth cycle levels. We reckon it will fall below 10% by 4Q11, after temporarily rising.

Fig 60 Unemployment rate (%)

6.0

8.0

10.0

12.0

14.0

16.0

18.0

Jan-0

5

Apr-05

Jun-0

5

Aug-05

Nov-05

Jan-0

6

Mar-06

Jun-0

6

Aug-06

Oct-06

Jan-0

7

Mar-07

May-07

Jul-0

7

Oct-07

Dec-07

Feb-08

May-08

Jul-0

8

Sep-08

Dec-08

Feb-09

Apr-09

Jun-0

9

Sep-09

Nov-09

Jan-1

0

Apr-10

Jun-1

0

Source: CBT

Strong in 2010 off low base and should remain strong in 2011

The trend has already reversed

Turkish Banks November 2010

26

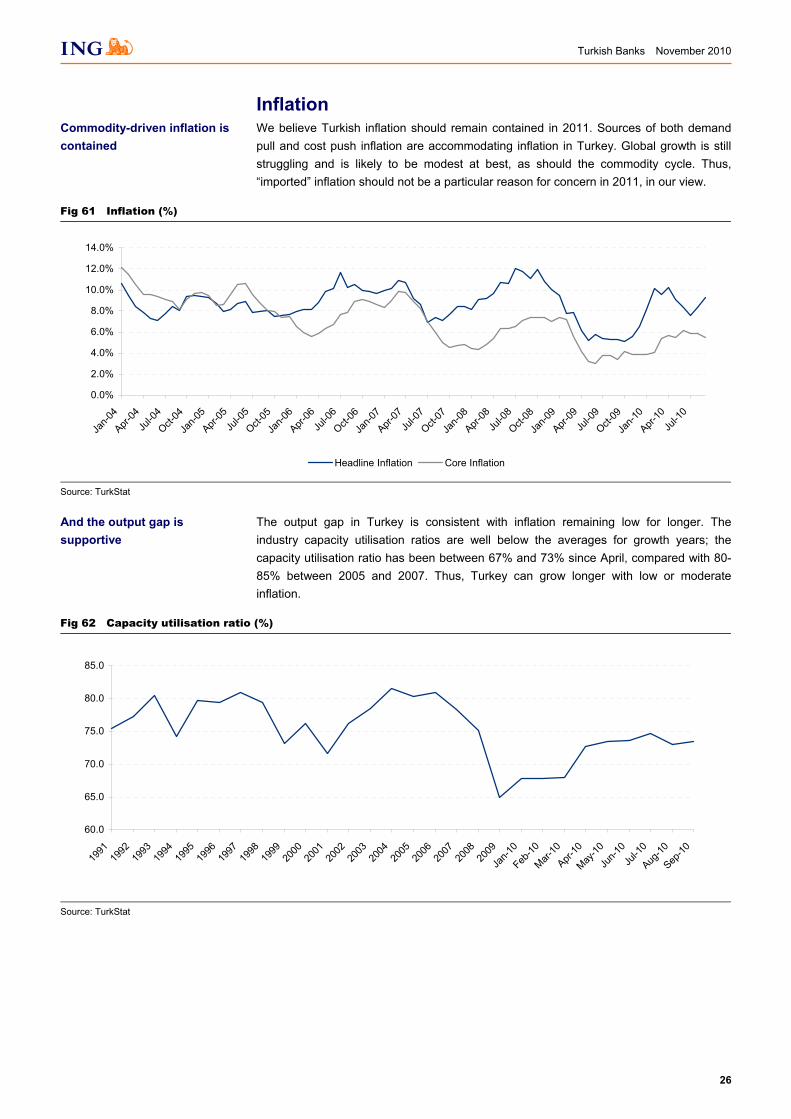

Inflation We believe Turkish inflation should remain contained in 2011. Sources of both demand pull and cost push inflation are accommodating inflation in Turkey. Global growth is still struggling and is likely to be modest at best, as should the commodity cycle. Thus, “imported” inflation should not be a particular reason for concern in 2011, in our view.

Fig 61 Inflation (%)

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

Jan-0

4

Apr-04

Jul-0

4

Oct-04

Jan-0

5

Apr-05

Jul-0

5

Oct-05

Jan-0

6

Apr-06

Jul-0

6

Oct-06

Jan-0

7

Apr-07

Jul-0

7

Oct-07

Jan-0

8

Apr-08

Jul-0

8

Oct-08

Jan-0

9

Apr-09

Jul-0

9

Oct-09

Jan-1

0

Apr-10

Jul-1

0

Headline Inflation Core Inflation

Source: TurkStat

The output gap in Turkey is consistent with inflation remaining low for longer. The industry capacity utilisation ratios are well below the averages for growth years; the capacity utilisation ratio has been between 67% and 73% since April, compared with 80-85% between 2005 and 2007. Thus, Turkey can grow longer with low or moderate inflation.

Fig 62 Capacity utilisation ratio (%)

60.0

65.0

70.0

75.0

80.0

85.0

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Jan-1

0

Feb-10

Mar-10

Apr-10

May-10

Jun-1

0Ju

l-10

Aug-10

Sep-10

Source: TurkStat

Commodity-driven inflation is contained

And the output gap is supportive

Turkish Banks November 2010

27

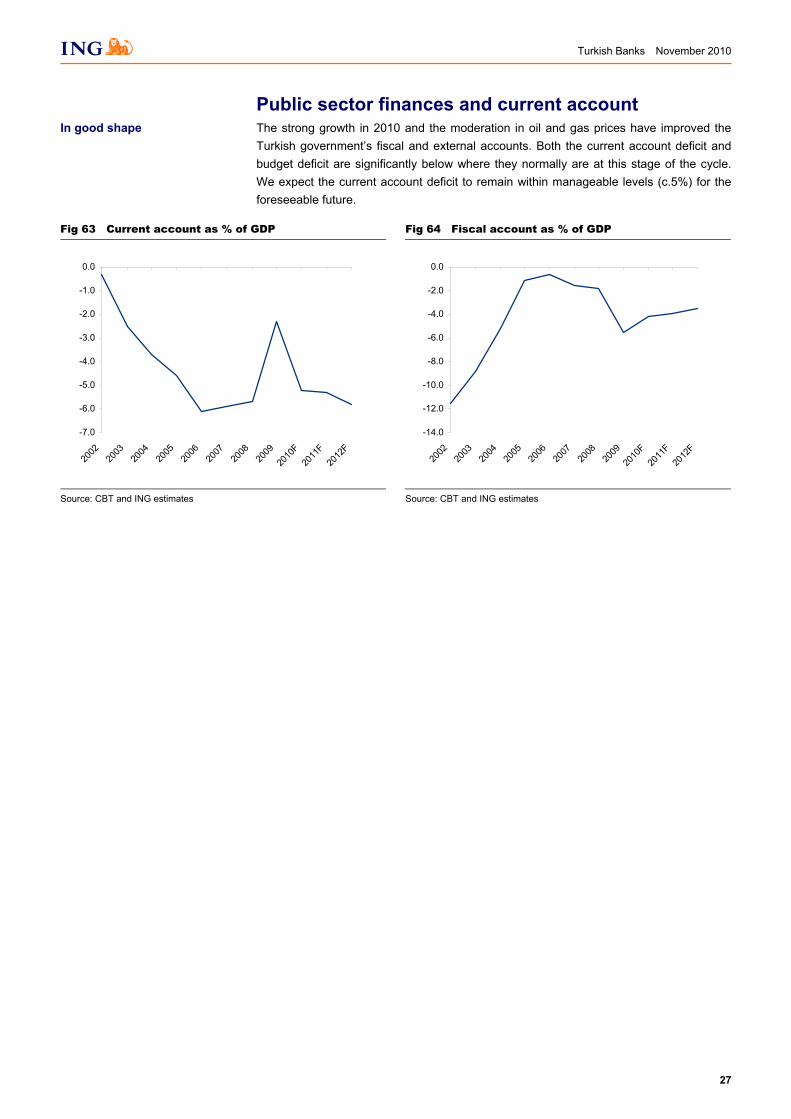

Public sector finances and current account The strong growth in 2010 and the moderation in oil and gas prices have improved the Turkish government’s fiscal and external accounts. Both the current account deficit and budget deficit are significantly below where they normally are at this stage of the cycle. We expect the current account deficit to remain within manageable levels (c.5%) for the foreseeable future.

Fig 63 Current account as % of GDP

Fig 64 Fiscal account as % of GDP

-7.0

-6.0

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

2002

2003

2004

2005

2006

2007

2008

2009

2010

F20

11F

2012

F

-14.0

-12.0

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2002

2003

2004

2005

2006

2007

2008

2009

2010

F20

11F

2012

F

Source: CBT and ING estimates Source: CBT and ING estimates

In good shape

Turkish Banks November 2010

28

This page is left blank intentionally

Turkish Banks November 2010

29

Companies

Turkish Banks November 2010

30

This page is left blank intentionally

Turkish Banks November 2010

31

Akbank A play on inflation

We have modified our revenue model and balance sheet forecasts and rolled over the forecast period. We foresee 5% EPS growth in 2011 followed by 14% in 2010. The biggest source of upside risk to our forecasts is inflation, as Akbank has heavily invested in CPI-linked government bonds. Other sources of risk include a continuation of bad loan recoveries (+) and irrational deposit repricing (-).

NIM to disappoint unless inflation picks up. Akbank has 15% of its balance sheet (c.33% of bonds) invested in CPI linkers. Indeed, it is because of its exposure to inflation-indexed bonds that the bank’s earnings have surprised the market significantly sinceMarch. Growing revenues will be a bigger challenge next year, with margins unlikely to improve before 2H11. If inflation picks up sooner than expected, then Akbank’s earnings would surprise on the upside, probably significantly. If, on the other hand, inflation stays at current levels – our base case – Akbank would struggle to grow its NIM with yields on other assets declining. The bank’s exposure to CPI linkers remains the most likely source of a potential surprise: a 100bp surprise in inflation would alter 2011 earnings by as much as 3% in either direction.

Loan growth is strong, replacing bonds. The balance sheet growth has gained momentum and management also sounds more upbeat. We would expect Akbank’s exposure to marketable securities to decline gradually and its loan growth to outperform the industry in 2011. On our assumptions, the loan growth should approach 30% this year and exceed 25% in 2011. These growth rates are sufficient to grow earnings at mid-single digits next year, assuming inflation remains flat.

Valuation. The stock is trading towards the high end of our Turkish banks valuation range despite Akbank’s below average ROE. We have the stock at 2.20x on 2010F P/BV and 11x on 2011F earnings. Our target price model values the stock at TL8.13/share. We use the residual earnings methodology to value the equity. The residual earnings (the RE), is the return on common equity, expressed as a TL excess return rather than a ratio. For every earnings period t, we restate residual earnings as RE = (ROE - ke)*BVPS. The RE method can be re-stated as a dividend discount model.

Forecasts and ratios

Year end Dec (TLm) 2008 2009 2010F 2011F 2012F

Revenues 4,624 6,028 6,680 7,208 7,934Pre-provision profit 2,437 3,844 4,149 4,127 4,378Net profit 1,705 2,726 3,116 3,278 3,471Normalised EPS (TL) 0.43 0.68 0.78 0.82 0.87Dividend per share (TL) 0.10 0.09 0.09 0.11 0.11Normalised PER (x) 21.1 13.2 11.6 11.0 10.4Dividend yield (%) 1.1 0.95 1.0 1.2 1.2Price/book (x) 3.2 2.5 2.2 2.0 1.8Price/tangible book (x) 3.2 2.5 2.2 2.0 1.8Normalised ROE (%) 15.6 21.5 20.6 19.2 18.2

Source: Company data, ING estimates

Haluk Akdogan London +44 20 7767 6650 [email protected]

Derya Guzel Istanbul +44 20 7767 5379 [email protected]

Sell (maintained)

Price (28/10/10)

TL9.00

Target price (12-mth)

TL8.13 (previously TL6.00)

Forecast total return -8.6%

Banks Turkey Bloomberg: AKBNK TI Reuters: AKBNK.IS

Share data Avg daily volume (3-mth) 6,416,551Free float (%) 39.0Market cap (TLm) 36,000.0Dividend yield (1F, %) 1.0

Source: Company data, ING estimates

Share price performance

5.5

6.5

7.5

8.5

9.5

10.5

10/09 1/10 4/10 7/10PriceIstanbul Stock Exch (rebased)

Source: ING

Turkish Banks November 2010

32

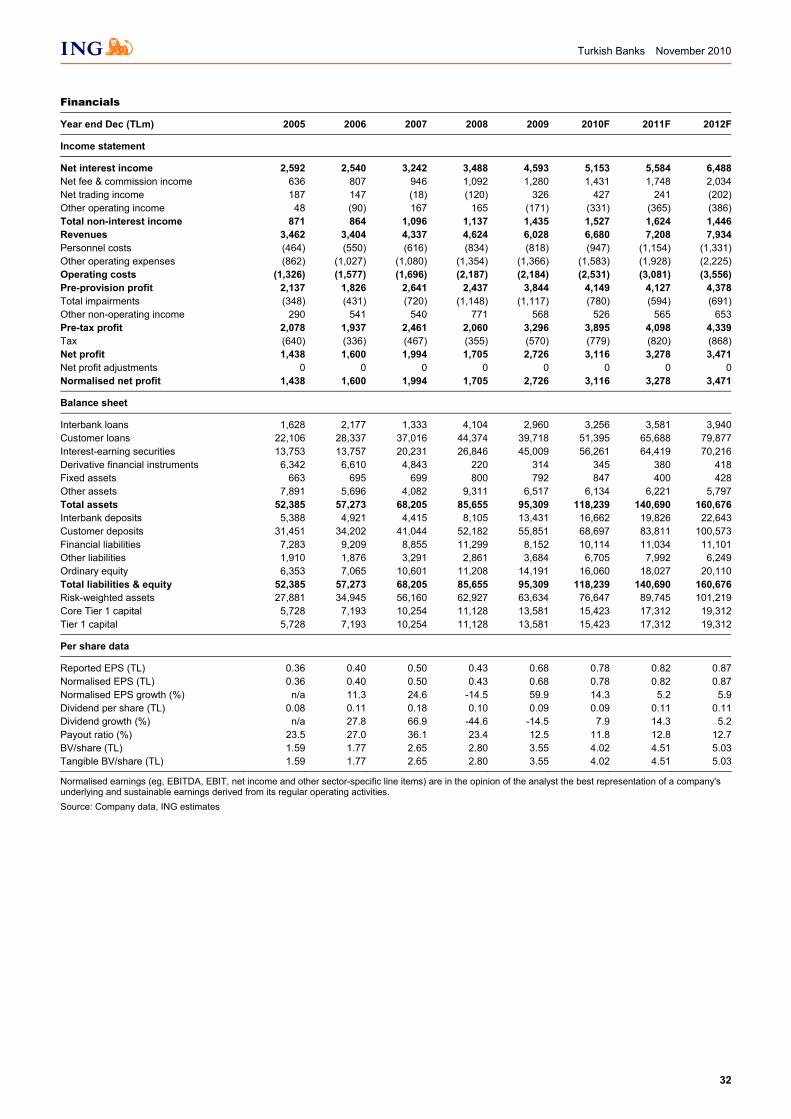

Financials

Year end Dec (TLm) 2005 2006 2007 2008 2009 2010F 2011F 2012F

Income statement

Net interest income 2,592 2,540 3,242 3,488 4,593 5,153 5,584 6,488Net fee & commission income 636 807 946 1,092 1,280 1,431 1,748 2,034Net trading income 187 147 (18) (120) 326 427 241 (202)Other operating income 48 (90) 167 165 (171) (331) (365) (386)Total non-interest income 871 864 1,096 1,137 1,435 1,527 1,624 1,446Revenues 3,462 3,404 4,337 4,624 6,028 6,680 7,208 7,934Personnel costs (464) (550) (616) (834) (818) (947) (1,154) (1,331)Other operating expenses (862) (1,027) (1,080) (1,354) (1,366) (1,583) (1,928) (2,225)Operating costs (1,326) (1,577) (1,696) (2,187) (2,184) (2,531) (3,081) (3,556)Pre-provision profit 2,137 1,826 2,641 2,437 3,844 4,149 4,127 4,378Total impairments (348) (431) (720) (1,148) (1,117) (780) (594) (691)Other non-operating income 290 541 540 771 568 526 565 653Pre-tax profit 2,078 1,937 2,461 2,060 3,296 3,895 4,098 4,339Tax (640) (336) (467) (355) (570) (779) (820) (868)Net profit 1,438 1,600 1,994 1,705 2,726 3,116 3,278 3,471Net profit adjustments 0 0 0 0 0 0 0 0Normalised net profit 1,438 1,600 1,994 1,705 2,726 3,116 3,278 3,471

Balance sheet

Interbank loans 1,628 2,177 1,333 4,104 2,960 3,256 3,581 3,940Customer loans 22,106 28,337 37,016 44,374 39,718 51,395 65,688 79,877Interest-earning securities 13,753 13,757 20,231 26,846 45,009 56,261 64,419 70,216Derivative financial instruments 6,342 6,610 4,843 220 314 345 380 418Fixed assets 663 695 699 800 792 847 400 428Other assets 7,891 5,696 4,082 9,311 6,517 6,134 6,221 5,797Total assets 52,385 57,273 68,205 85,655 95,309 118,239 140,690 160,676Interbank deposits 5,388 4,921 4,415 8,105 13,431 16,662 19,826 22,643Customer deposits 31,451 34,202 41,044 52,182 55,851 68,697 83,811 100,573Financial liabilities 7,283 9,209 8,855 11,299 8,152 10,114 11,034 11,101Other liabilities 1,910 1,876 3,291 2,861 3,684 6,705 7,992 6,249Ordinary equity 6,353 7,065 10,601 11,208 14,191 16,060 18,027 20,110Total liabilities & equity 52,385 57,273 68,205 85,655 95,309 118,239 140,690 160,676Risk-weighted assets 27,881 34,945 56,160 62,927 63,634 76,647 89,745 101,219Core Tier 1 capital 5,728 7,193 10,254 11,128 13,581 15,423 17,312 19,312Tier 1 capital 5,728 7,193 10,254 11,128 13,581 15,423 17,312 19,312

Per share data

Reported EPS (TL) 0.36 0.40 0.50 0.43 0.68 0.78 0.82 0.87Normalised EPS (TL) 0.36 0.40 0.50 0.43 0.68 0.78 0.82 0.87Normalised EPS growth (%) n/a 11.3 24.6 -14.5 59.9 14.3 5.2 5.9Dividend per share (TL) 0.08 0.11 0.18 0.10 0.09 0.09 0.11 0.11Dividend growth (%) n/a 27.8 66.9 -44.6 -14.5 7.9 14.3 5.2Payout ratio (%) 23.5 27.0 36.1 23.4 12.5 11.8 12.8 12.7BV/share (TL) 1.59 1.77 2.65 2.80 3.55 4.02 4.51 5.03Tangible BV/share (TL) 1.59 1.77 2.65 2.80 3.55 4.02 4.51 5.03

Normalised earnings (eg, EBITDA, EBIT, net income and other sector-specific line items) are in the opinion of the analyst the best representation of a company's underlying and sustainable earnings derived from its regular operating activities. Source: Company data, ING estimates

Turkish Banks November 2010

33

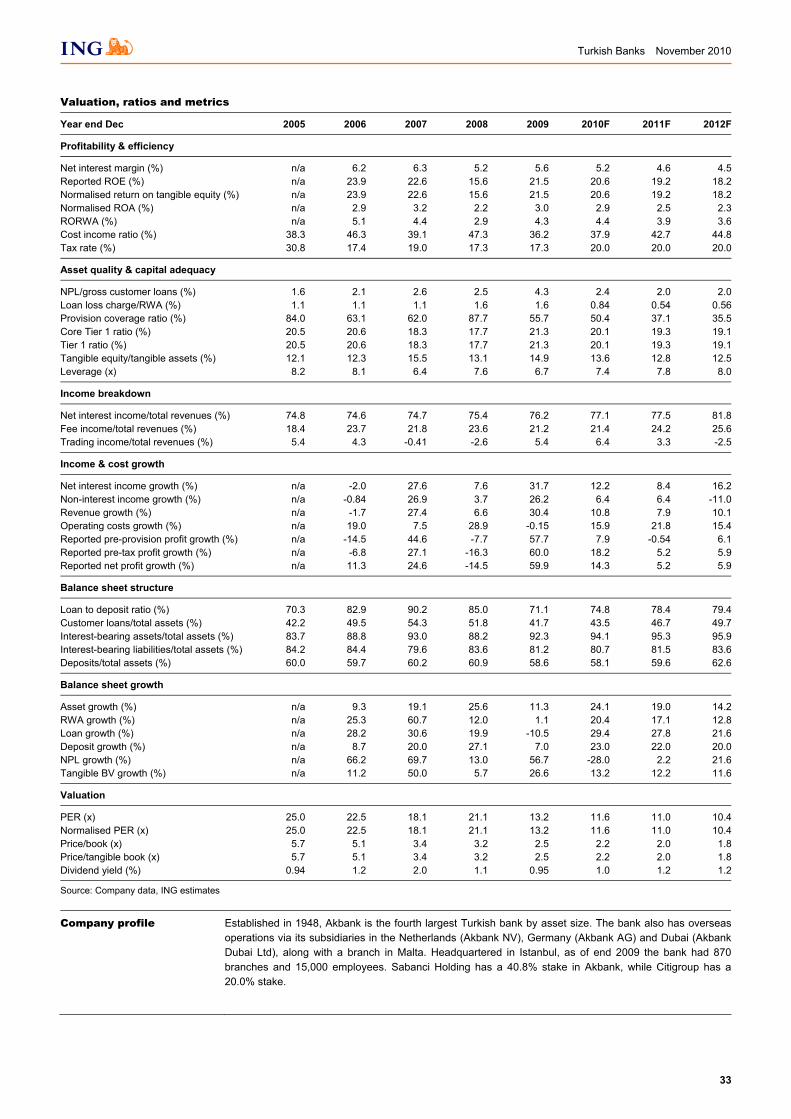

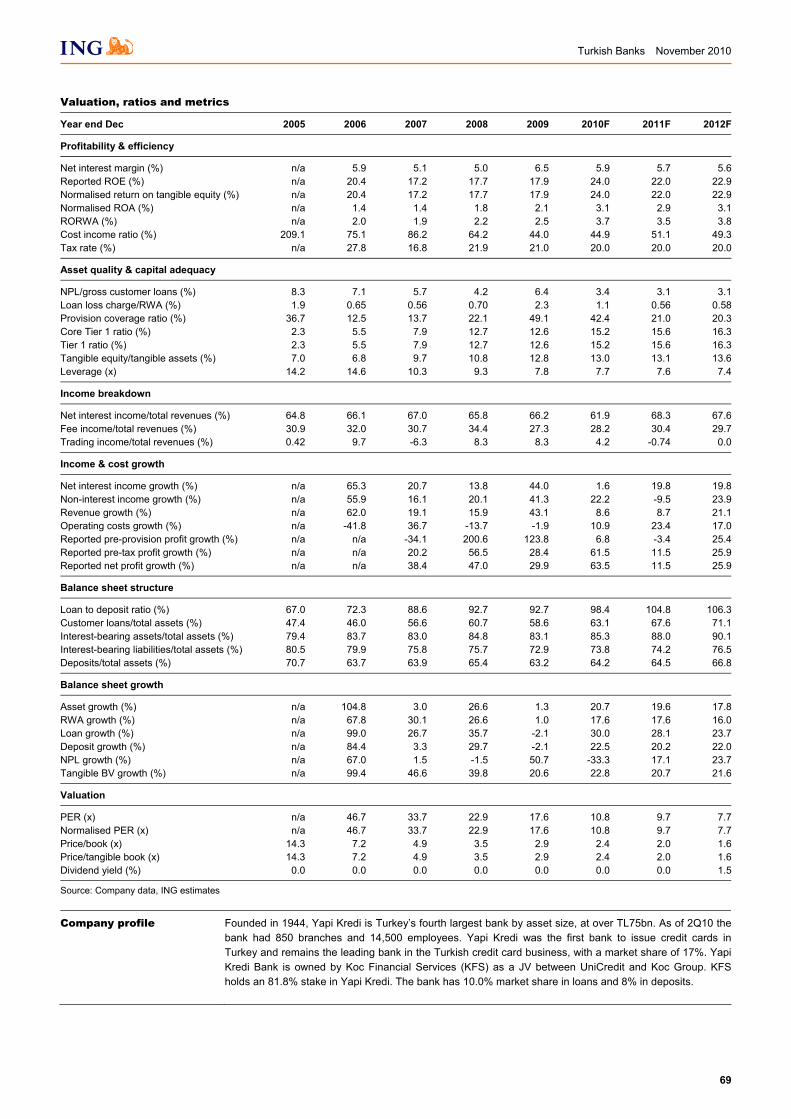

Valuation, ratios and metrics

Year end Dec 2005 2006 2007 2008 2009 2010F 2011F 2012F

Profitability & efficiency

Net interest margin (%) n/a 6.2 6.3 5.2 5.6 5.2 4.6 4.5Reported ROE (%) n/a 23.9 22.6 15.6 21.5 20.6 19.2 18.2Normalised return on tangible equity (%) n/a 23.9 22.6 15.6 21.5 20.6 19.2 18.2Normalised ROA (%) n/a 2.9 3.2 2.2 3.0 2.9 2.5 2.3RORWA (%) n/a 5.1 4.4 2.9 4.3 4.4 3.9 3.6Cost income ratio (%) 38.3 46.3 39.1 47.3 36.2 37.9 42.7 44.8Tax rate (%) 30.8 17.4 19.0 17.3 17.3 20.0 20.0 20.0

Asset quality & capital adequacy

NPL/gross customer loans (%) 1.6 2.1 2.6 2.5 4.3 2.4 2.0 2.0Loan loss charge/RWA (%) 1.1 1.1 1.1 1.6 1.6 0.84 0.54 0.56Provision coverage ratio (%) 84.0 63.1 62.0 87.7 55.7 50.4 37.1 35.5Core Tier 1 ratio (%) 20.5 20.6 18.3 17.7 21.3 20.1 19.3 19.1Tier 1 ratio (%) 20.5 20.6 18.3 17.7 21.3 20.1 19.3 19.1Tangible equity/tangible assets (%) 12.1 12.3 15.5 13.1 14.9 13.6 12.8 12.5Leverage (x) 8.2 8.1 6.4 7.6 6.7 7.4 7.8 8.0

Income breakdown

Net interest income/total revenues (%) 74.8 74.6 74.7 75.4 76.2 77.1 77.5 81.8Fee income/total revenues (%) 18.4 23.7 21.8 23.6 21.2 21.4 24.2 25.6Trading income/total revenues (%) 5.4 4.3 -0.41 -2.6 5.4 6.4 3.3 -2.5

Income & cost growth

Net interest income growth (%) n/a -2.0 27.6 7.6 31.7 12.2 8.4 16.2Non-interest income growth (%) n/a -0.84 26.9 3.7 26.2 6.4 6.4 -11.0Revenue growth (%) n/a -1.7 27.4 6.6 30.4 10.8 7.9 10.1Operating costs growth (%) n/a 19.0 7.5 28.9 -0.15 15.9 21.8 15.4Reported pre-provision profit growth (%) n/a -14.5 44.6 -7.7 57.7 7.9 -0.54 6.1Reported pre-tax profit growth (%) n/a -6.8 27.1 -16.3 60.0 18.2 5.2 5.9Reported net profit growth (%) n/a 11.3 24.6 -14.5 59.9 14.3 5.2 5.9

Balance sheet structure

Loan to deposit ratio (%) 70.3 82.9 90.2 85.0 71.1 74.8 78.4 79.4Customer loans/total assets (%) 42.2 49.5 54.3 51.8 41.7 43.5 46.7 49.7Interest-bearing assets/total assets (%) 83.7 88.8 93.0 88.2 92.3 94.1 95.3 95.9Interest-bearing liabilities/total assets (%) 84.2 84.4 79.6 83.6 81.2 80.7 81.5 83.6Deposits/total assets (%) 60.0 59.7 60.2 60.9 58.6 58.1 59.6 62.6

Balance sheet growth

Asset growth (%) n/a 9.3 19.1 25.6 11.3 24.1 19.0 14.2RWA growth (%) n/a 25.3 60.7 12.0 1.1 20.4 17.1 12.8Loan growth (%) n/a 28.2 30.6 19.9 -10.5 29.4 27.8 21.6Deposit growth (%) n/a 8.7 20.0 27.1 7.0 23.0 22.0 20.0NPL growth (%) n/a 66.2 69.7 13.0 56.7 -28.0 2.2 21.6Tangible BV growth (%) n/a 11.2 50.0 5.7 26.6 13.2 12.2 11.6

Valuation

PER (x) 25.0 22.5 18.1 21.1 13.2 11.6 11.0 10.4Normalised PER (x) 25.0 22.5 18.1 21.1 13.2 11.6 11.0 10.4Price/book (x) 5.7 5.1 3.4 3.2 2.5 2.2 2.0 1.8Price/tangible book (x) 5.7 5.1 3.4 3.2 2.5 2.2 2.0 1.8Dividend yield (%) 0.94 1.2 2.0 1.1 0.95 1.0 1.2 1.2

Source: Company data, ING estimates

Company profile Established in 1948, Akbank is the fourth largest Turkish bank by asset size. The bank also has overseasoperations via its subsidiaries in the Netherlands (Akbank NV), Germany (Akbank AG) and Dubai (AkbankDubai Ltd), along with a branch in Malta. Headquartered in Istanbul, as of end 2009 the bank had 870 branches and 15,000 employees. Sabanci Holding has a 40.8% stake in Akbank, while Citigroup has a20.0% stake.

Turkish Banks November 2010

34

This page is left blank intentionally

Turkish Banks November 2010

35

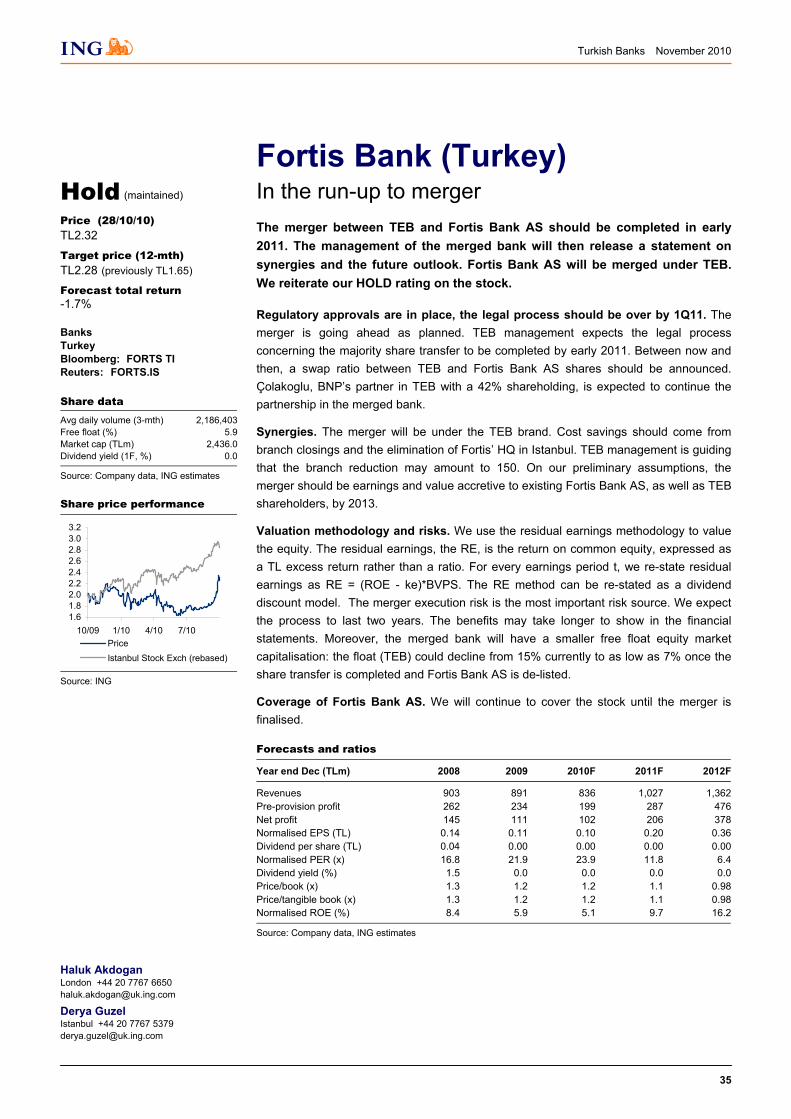

Fortis Bank (Turkey) In the run-up to merger

The merger between TEB and Fortis Bank AS should be completed in early 2011. The management of the merged bank will then release a statement on synergies and the future outlook. Fortis Bank AS will be merged under TEB. We reiterate our HOLD rating on the stock.

Regulatory approvals are in place, the legal process should be over by 1Q11. The merger is going ahead as planned. TEB management expects the legal process concerning the majority share transfer to be completed by early 2011. Between now and then, a swap ratio between TEB and Fortis Bank AS shares should be announced. Çolakoglu, BNP’s partner in TEB with a 42% shareholding, is expected to continue the partnership in the merged bank.

Synergies. The merger will be under the TEB brand. Cost savings should come from branch closings and the elimination of Fortis’ HQ in Istanbul. TEB management is guiding that the branch reduction may amount to 150. On our preliminary assumptions, the merger should be earnings and value accretive to existing Fortis Bank AS, as well as TEB shareholders, by 2013.

Valuation methodology and risks. We use the residual earnings methodology to value the equity. The residual earnings, the RE, is the return on common equity, expressed as a TL excess return rather than a ratio. For every earnings period t, we re-state residual earnings as RE = (ROE - ke)*BVPS. The RE method can be re-stated as a dividend discount model. The merger execution risk is the most important risk source. We expect the process to last two years. The benefits may take longer to show in the financial statements. Moreover, the merged bank will have a smaller free float equity market capitalisation: the float (TEB) could decline from 15% currently to as low as 7% once the share transfer is completed and Fortis Bank AS is de-listed.

Coverage of Fortis Bank AS. We will continue to cover the stock until the merger is finalised.

Forecasts and ratios

Year end Dec (TLm) 2008 2009 2010F 2011F 2012F

Revenues 903 891 836 1,027 1,362Pre-provision profit 262 234 199 287 476Net profit 145 111 102 206 378Normalised EPS (TL) 0.14 0.11 0.10 0.20 0.36Dividend per share (TL) 0.04 0.00 0.00 0.00 0.00Normalised PER (x) 16.8 21.9 23.9 11.8 6.4Dividend yield (%) 1.5 0.0 0.0 0.0 0.0Price/book (x) 1.3 1.2 1.2 1.1 0.98Price/tangible book (x) 1.3 1.2 1.2 1.1 0.98Normalised ROE (%) 8.4 5.9 5.1 9.7 16.2

Source: Company data, ING estimates

Haluk Akdogan London +44 20 7767 6650 [email protected]

Derya Guzel Istanbul +44 20 7767 5379 [email protected]

Hold (maintained)

Price (28/10/10)

TL2.32

Target price (12-mth)

TL2.28 (previously TL1.65)

Forecast total return -1.7%

Banks Turkey Bloomberg: FORTS TI Reuters: FORTS.IS

Share data Avg daily volume (3-mth) 2,186,403Free float (%) 5.9Market cap (TLm) 2,436.0Dividend yield (1F, %) 0.0

Source: Company data, ING estimates

Share price performance

1.61.82.02.22.42.62.83.03.2

10/09 1/10 4/10 7/10PriceIstanbul Stock Exch (rebased)

Source: ING

Turkish Banks November 2010

36

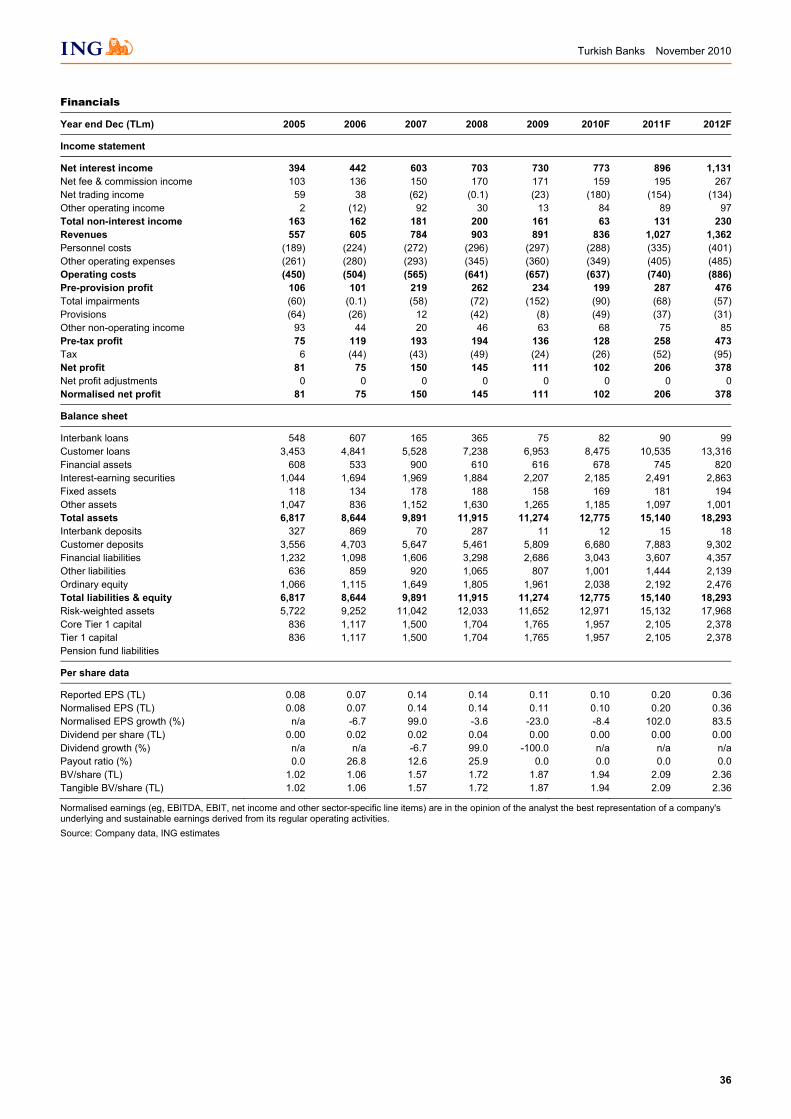

Financials

Year end Dec (TLm) 2005 2006 2007 2008 2009 2010F 2011F 2012F

Income statement

Net interest income 394 442 603 703 730 773 896 1,131Net fee & commission income 103 136 150 170 171 159 195 267Net trading income 59 38 (62) (0.1) (23) (180) (154) (134)Other operating income 2 (12) 92 30 13 84 89 97Total non-interest income 163 162 181 200 161 63 131 230Revenues 557 605 784 903 891 836 1,027 1,362Personnel costs (189) (224) (272) (296) (297) (288) (335) (401)Other operating expenses (261) (280) (293) (345) (360) (349) (405) (485)Operating costs (450) (504) (565) (641) (657) (637) (740) (886)Pre-provision profit 106 101 219 262 234 199 287 476Total impairments (60) (0.1) (58) (72) (152) (90) (68) (57)Provisions (64) (26) 12 (42) (8) (49) (37) (31)Other non-operating income 93 44 20 46 63 68 75 85Pre-tax profit 75 119 193 194 136 128 258 473Tax 6 (44) (43) (49) (24) (26) (52) (95)Net profit 81 75 150 145 111 102 206 378Net profit adjustments 0 0 0 0 0 0 0 0Normalised net profit 81 75 150 145 111 102 206 378

Balance sheet

Interbank loans 548 607 165 365 75 82 90 99Customer loans 3,453 4,841 5,528 7,238 6,953 8,475 10,535 13,316Financial assets 608 533 900 610 616 678 745 820Interest-earning securities 1,044 1,694 1,969 1,884 2,207 2,185 2,491 2,863Fixed assets 118 134 178 188 158 169 181 194Other assets 1,047 836 1,152 1,630 1,265 1,185 1,097 1,001Total assets 6,817 8,644 9,891 11,915 11,274 12,775 15,140 18,293Interbank deposits 327 869 70 287 11 12 15 18Customer deposits 3,556 4,703 5,647 5,461 5,809 6,680 7,883 9,302Financial liabilities 1,232 1,098 1,606 3,298 2,686 3,043 3,607 4,357Other liabilities 636 859 920 1,065 807 1,001 1,444 2,139Ordinary equity 1,066 1,115 1,649 1,805 1,961 2,038 2,192 2,476Total liabilities & equity 6,817 8,644 9,891 11,915 11,274 12,775 15,140 18,293Risk-weighted assets 5,722 9,252 11,042 12,033 11,652 12,971 15,132 17,968Core Tier 1 capital 836 1,117 1,500 1,704 1,765 1,957 2,105 2,378Tier 1 capital 836 1,117 1,500 1,704 1,765 1,957 2,105 2,378Pension fund liabilities

Per share data

Reported EPS (TL) 0.08 0.07 0.14 0.14 0.11 0.10 0.20 0.36Normalised EPS (TL) 0.08 0.07 0.14 0.14 0.11 0.10 0.20 0.36Normalised EPS growth (%) n/a -6.7 99.0 -3.6 -23.0 -8.4 102.0 83.5Dividend per share (TL) 0.00 0.02 0.02 0.04 0.00 0.00 0.00 0.00Dividend growth (%) n/a n/a -6.7 99.0 -100.0 n/a n/a n/aPayout ratio (%) 0.0 26.8 12.6 25.9 0.0 0.0 0.0 0.0BV/share (TL) 1.02 1.06 1.57 1.72 1.87 1.94 2.09 2.36Tangible BV/share (TL) 1.02 1.06 1.57 1.72 1.87 1.94 2.09 2.36

Normalised earnings (eg, EBITDA, EBIT, net income and other sector-specific line items) are in the opinion of the analyst the best representation of a company's underlying and sustainable earnings derived from its regular operating activities. Source: Company data, ING estimates

Turkish Banks November 2010

37

Valuation, ratios and metrics

Year end Dec 2005 2006 2007 2008 2009 2010F 2011F 2012F

Profitability & efficiency

Net interest margin (%) n/a 6.6 7.4 7.5 7.3 7.3 7.1 7.3Reported ROE (%) n/a 6.9 10.9 8.4 5.9 5.1 9.7 16.2Normalised return on tangible equity (%) n/a 6.9 10.9 8.4 5.9 5.1 9.7 16.2Normalised ROA (%) n/a 0.98 1.6 1.3 0.96 0.85 1.5 2.3RORWA (%) n/a 1.0 1.5 1.3 0.94 0.83 1.5 2.3Cost income ratio (%) 80.9 83.3 72.0 71.0 73.8 76.2 72.0 65.1Tax rate (%) n/a 36.8 22.4 25.4 17.8 20.0 20.0 20.0

Asset quality & capital adequacy

NPL/gross customer loans (%) 4.9 3.5 4.2 5.1 7.5 3.3 2.7 2.1Loan loss charge/RWA (%) 1.0 0.00 0.52 0.60 1.3 0.70 0.45 0.32Provision coverage ratio (%) 33.7 0.07 23.9 18.5 27.2 31.4 23.1 20.5Core Tier 1 ratio (%) 14.6 12.1 13.6 14.2 15.1 15.1 13.9 13.2Tier 1 ratio (%) 14.6 12.1 13.6 14.2 15.1 15.1 13.9 13.2Tangible equity/tangible assets (%) 15.6 12.9 16.7 15.1 17.4 16.0 14.5 13.5Leverage (x) 6.4 7.8 6.0 6.6 5.7 6.3 6.9 7.4

Income breakdown

Net interest income/total revenues (%) 70.7 73.2 76.9 77.9 81.9 92.5 87.3 83.1Fee income/total revenues (%) 18.4 22.5 19.2 18.8 19.1 19.0 19.0 19.6Trading income/total revenues (%) 10.5 6.3 -7.9 -0.01 -2.6 -21.6 -15.0 -9.8

Income & cost growth

Net interest income growth (%) n/a 12.3 36.3 16.6 3.8 5.9 15.9 26.2Non-interest income growth (%) n/a -0.52 11.7 10.3 -19.4 -61.1 109.0 76.3Revenue growth (%) n/a 8.5 29.7 15.1 -1.3 -6.2 22.8 32.6Operating costs growth (%) n/a 11.8 12.2 13.4 2.6 -3.1 16.1 19.8Reported pre-provision profit growth (%) n/a -5.2 117.1 19.6 -10.9 -15.0 44.5 65.7Reported pre-tax profit growth (%) n/a 58.3 62.1 0.29 -30.1 -5.9 102.0 83.5Reported net profit growth (%) n/a -6.7 99.0 -3.6 -23.0 -8.4 102.0 83.5

Balance sheet structure

Loan to deposit ratio (%) 97.1 102.9 97.9 132.5 119.7 126.9 133.6 143.2Customer loans/total assets (%) 50.7 56.0 55.9 60.7 61.7 66.3 69.6 72.8Interest-bearing assets/total assets (%) 82.9 88.8 86.6 84.7 87.4 89.4 91.6 93.5Interest-bearing liabilities/total assets (%) 75.0 77.2 74.0 75.9 75.4 76.2 76.0 74.8Deposits/total assets (%) 52.2 54.4 57.1 45.8 51.5 52.3 52.1 50.9

Balance sheet growth

Asset growth (%) n/a 26.8 14.4 20.5 -5.4 13.3 18.5 20.8RWA growth (%) n/a 61.7 19.3 9.0 -3.2 11.3 16.7 18.7Loan growth (%) n/a 40.2 14.2 30.9 -3.9 21.9 24.3 26.4Deposit growth (%) n/a 32.3 20.1 -3.3 6.4 15.0 18.0 18.0NPL growth (%) n/a -0.75 37.8 60.9 43.8 -48.5 2.4 -5.2Tangible BV growth (%) n/a 4.5 48.0 9.4 8.6 3.9 7.6 12.9

Valuation

PER (x) 30.1 32.3 16.2 16.8 21.9 23.9 11.8 6.4Normalised PER (x) 30.1 32.3 16.2 16.8 21.9 23.9 11.8 6.4Price/book (x) 2.3 2.2 1.5 1.3 1.2 1.2 1.1 0.98Price/tangible book (x) 2.3 2.2 1.5 1.3 1.2 1.2 1.1 0.98Dividend yield (%) 0.0 0.83 0.77 1.5 0.0 0.0 0.0 0.0

Source: Company data, ING estimates

Company profile Turkey’s 13th largest bank with assets of TL13bn. After BNP became owner of two banks in Turkey (TEB42% and Fortis 94% owned by BNP) it decided to merge the two. The merger is going ahead as planned.TEB management expects the legal process concerning the majority share transfer to be completed early in2011. Between now and then, a swap ratio between TEB and Fortis Bank AS shares should be announced.Çolakoglu, BNP’s partner in TEB with 42% shareholding, is expected to continue the partnership in themerged bank.

Turkish Banks November 2010

38

This page is left blank intentionally

Turkish Banks November 2010

39

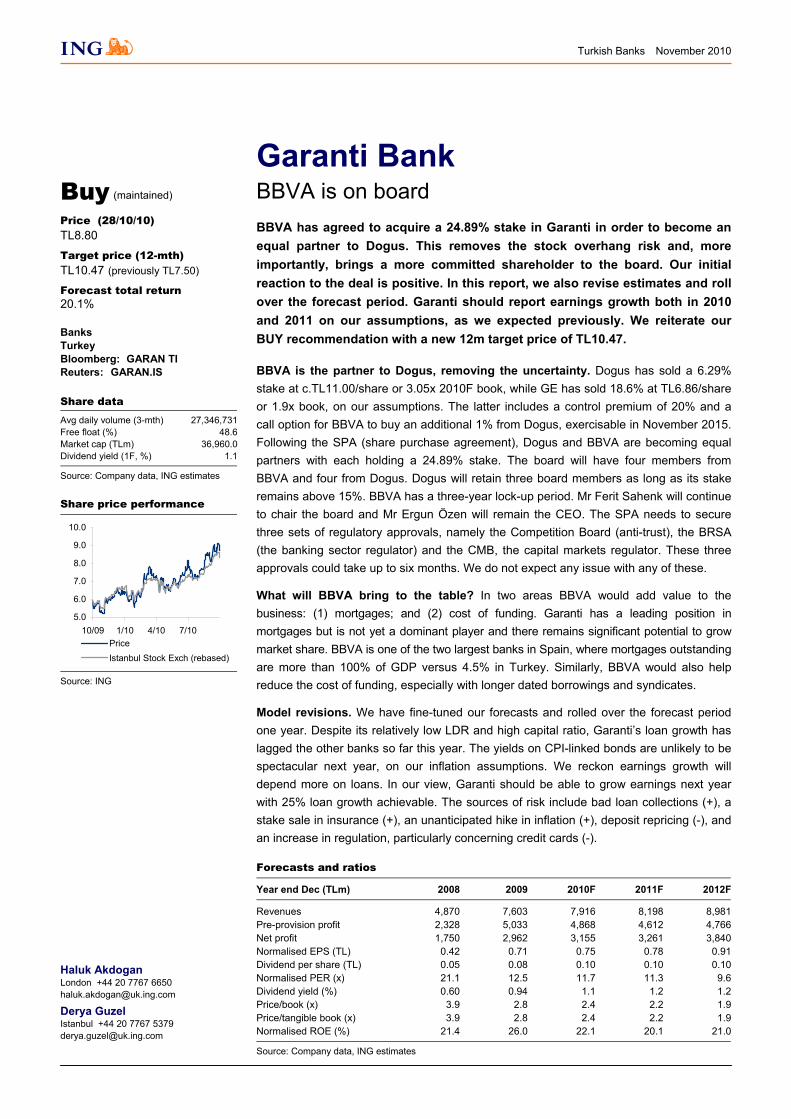

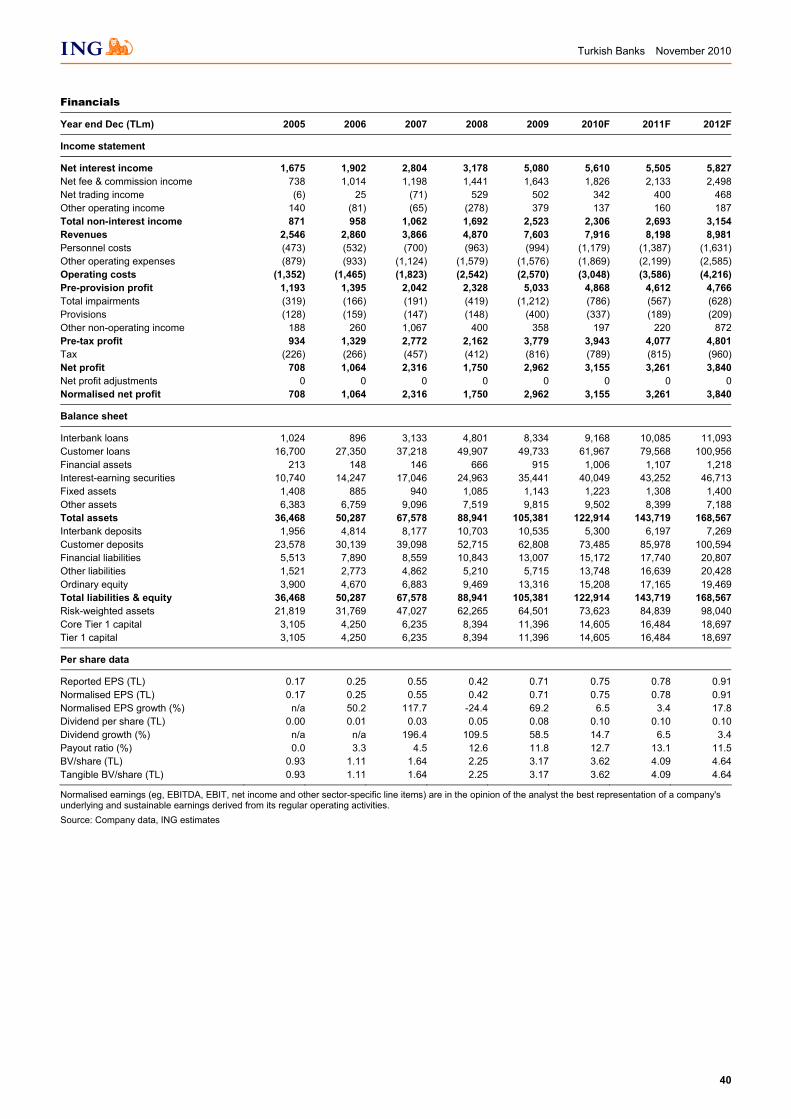

Garanti Bank BBVA is on board

BBVA has agreed to acquire a 24.89% stake in Garanti in order to become an equal partner to Dogus. This removes the stock overhang risk and, more importantly, brings a more committed shareholder to the board. Our initial reaction to the deal is positive. In this report, we also revise estimates and roll over the forecast period. Garanti should report earnings growth both in 2010 and 2011 on our assumptions, as we expected previously. We reiterate our BUY recommendation with a new 12m target price of TL10.47.

BBVA is the partner to Dogus, removing the uncertainty. Dogus has sold a 6.29% stake at c.TL11.00/share or 3.05x 2010F book, while GE has sold 18.6% at TL6.86/share or 1.9x book, on our assumptions. The latter includes a control premium of 20% and a call option for BBVA to buy an additional 1% from Dogus, exercisable in November 2015. Following the SPA (share purchase agreement), Dogus and BBVA are becoming equal partners with each holding a 24.89% stake. The board will have four members from BBVA and four from Dogus. Dogus will retain three board members as long as its stake remains above 15%. BBVA has a three-year lock-up period. Mr Ferit Sahenk will continue to chair the board and Mr Ergun Özen will remain the CEO. The SPA needs to secure three sets of regulatory approvals, namely the Competition Board (anti-trust), the BRSA (the banking sector regulator) and the CMB, the capital markets regulator. These three approvals could take up to six months. We do not expect any issue with any of these.

What will BBVA bring to the table? In two areas BBVA would add value to the business: (1) mortgages; and (2) cost of funding. Garanti has a leading position in mortgages but is not yet a dominant player and there remains significant potential to grow market share. BBVA is one of the two largest banks in Spain, where mortgages outstanding are more than 100% of GDP versus 4.5% in Turkey. Similarly, BBVA would also help reduce the cost of funding, especially with longer dated borrowings and syndicates.

Model revisions. We have fine-tuned our forecasts and rolled over the forecast period one year. Despite its relatively low LDR and high capital ratio, Garanti’s loan growth has lagged the other banks so far this year. The yields on CPI-linked bonds are unlikely to be spectacular next year, on our inflation assumptions. We reckon earnings growth will depend more on loans. In our view, Garanti should be able to grow earnings next year with 25% loan growth achievable. The sources of risk include bad loan collections (+), a stake sale in insurance (+), an unanticipated hike in inflation (+), deposit repricing (-), and an increase in regulation, particularly concerning credit cards (-).

Forecasts and ratios

Year end Dec (TLm) 2008 2009 2010F 2011F 2012F

Revenues 4,870 7,603 7,916 8,198 8,981Pre-provision profit 2,328 5,033 4,868 4,612 4,766Net profit 1,750 2,962 3,155 3,261 3,840Normalised EPS (TL) 0.42 0.71 0.75 0.78 0.91Dividend per share (TL) 0.05 0.08 0.10 0.10 0.10Normalised PER (x) 21.1 12.5 11.7 11.3 9.6Dividend yield (%) 0.60 0.94 1.1 1.2 1.2Price/book (x) 3.9 2.8 2.4 2.2 1.9Price/tangible book (x) 3.9 2.8 2.4 2.2 1.9Normalised ROE (%) 21.4 26.0 22.1 20.1 21.0

Source: Company data, ING estimates

Haluk Akdogan London +44 20 7767 6650 [email protected]

Derya Guzel Istanbul +44 20 7767 5379 [email protected]

Buy (maintained)

Price (28/10/10)

TL8.80

Target price (12-mth)

TL10.47 (previously TL7.50)

Forecast total return 20.1%

Banks Turkey Bloomberg: GARAN TI Reuters: GARAN.IS

Share data Avg daily volume (3-mth) 27,346,731Free float (%) 48.6Market cap (TLm) 36,960.0Dividend yield (1F, %) 1.1

Source: Company data, ING estimates

Share price performance

5.0

6.0

7.0

8.0

9.0

10.0

10/09 1/10 4/10 7/10PriceIstanbul Stock Exch (rebased)

Source: ING

Turkish Banks November 2010

40

Financials

Year end Dec (TLm) 2005 2006 2007 2008 2009 2010F 2011F 2012F

Income statement

Net interest income 1,675 1,902 2,804 3,178 5,080 5,610 5,505 5,827Net fee & commission income 738 1,014 1,198 1,441 1,643 1,826 2,133 2,498Net trading income (6) 25 (71) 529 502 342 400 468Other operating income 140 (81) (65) (278) 379 137 160 187Total non-interest income 871 958 1,062 1,692 2,523 2,306 2,693 3,154Revenues 2,546 2,860 3,866 4,870 7,603 7,916 8,198 8,981Personnel costs (473) (532) (700) (963) (994) (1,179) (1,387) (1,631)Other operating expenses (879) (933) (1,124) (1,579) (1,576) (1,869) (2,199) (2,585)Operating costs (1,352) (1,465) (1,823) (2,542) (2,570) (3,048) (3,586) (4,216)Pre-provision profit 1,193 1,395 2,042 2,328 5,033 4,868 4,612 4,766Total impairments (319) (166) (191) (419) (1,212) (786) (567) (628)Provisions (128) (159) (147) (148) (400) (337) (189) (209)Other non-operating income 188 260 1,067 400 358 197 220 872Pre-tax profit 934 1,329 2,772 2,162 3,779 3,943 4,077 4,801Tax (226) (266) (457) (412) (816) (789) (815) (960)Net profit 708 1,064 2,316 1,750 2,962 3,155 3,261 3,840Net profit adjustments 0 0 0 0 0 0 0 0Normalised net profit 708 1,064 2,316 1,750 2,962 3,155 3,261 3,840

Balance sheet

Interbank loans 1,024 896 3,133 4,801 8,334 9,168 10,085 11,093Customer loans 16,700 27,350 37,218 49,907 49,733 61,967 79,568 100,956Financial assets 213 148 146 666 915 1,006 1,107 1,218Interest-earning securities 10,740 14,247 17,046 24,963 35,441 40,049 43,252 46,713Fixed assets 1,408 885 940 1,085 1,143 1,223 1,308 1,400Other assets 6,383 6,759 9,096 7,519 9,815 9,502 8,399 7,188Total assets 36,468 50,287 67,578 88,941 105,381 122,914 143,719 168,567Interbank deposits 1,956 4,814 8,177 10,703 10,535 5,300 6,197 7,269Customer deposits 23,578 30,139 39,098 52,715 62,808 73,485 85,978 100,594Financial liabilities 5,513 7,890 8,559 10,843 13,007 15,172 17,740 20,807Other liabilities 1,521 2,773 4,862 5,210 5,715 13,748 16,639 20,428Ordinary equity 3,900 4,670 6,883 9,469 13,316 15,208 17,165 19,469Total liabilities & equity 36,468 50,287 67,578 88,941 105,381 122,914 143,719 168,567Risk-weighted assets 21,819 31,769 47,027 62,265 64,501 73,623 84,839 98,040Core Tier 1 capital 3,105 4,250 6,235 8,394 11,396 14,605 16,484 18,697Tier 1 capital 3,105 4,250 6,235 8,394 11,396 14,605 16,484 18,697

Per share data

Reported EPS (TL) 0.17 0.25 0.55 0.42 0.71 0.75 0.78 0.91Normalised EPS (TL) 0.17 0.25 0.55 0.42 0.71 0.75 0.78 0.91Normalised EPS growth (%) n/a 50.2 117.7 -24.4 69.2 6.5 3.4 17.8Dividend per share (TL) 0.00 0.01 0.03 0.05 0.08 0.10 0.10 0.10Dividend growth (%) n/a n/a 196.4 109.5 58.5 14.7 6.5 3.4Payout ratio (%) 0.0 3.3 4.5 12.6 11.8 12.7 13.1 11.5BV/share (TL) 0.93 1.11 1.64 2.25 3.17 3.62 4.09 4.64Tangible BV/share (TL) 0.93 1.11 1.64 2.25 3.17 3.62 4.09 4.64

Normalised earnings (eg, EBITDA, EBIT, net income and other sector-specific line items) are in the opinion of the analyst the best representation of a company's underlying and sustainable earnings derived from its regular operating activities. Source: Company data, ING estimates

Turkish Banks November 2010

41

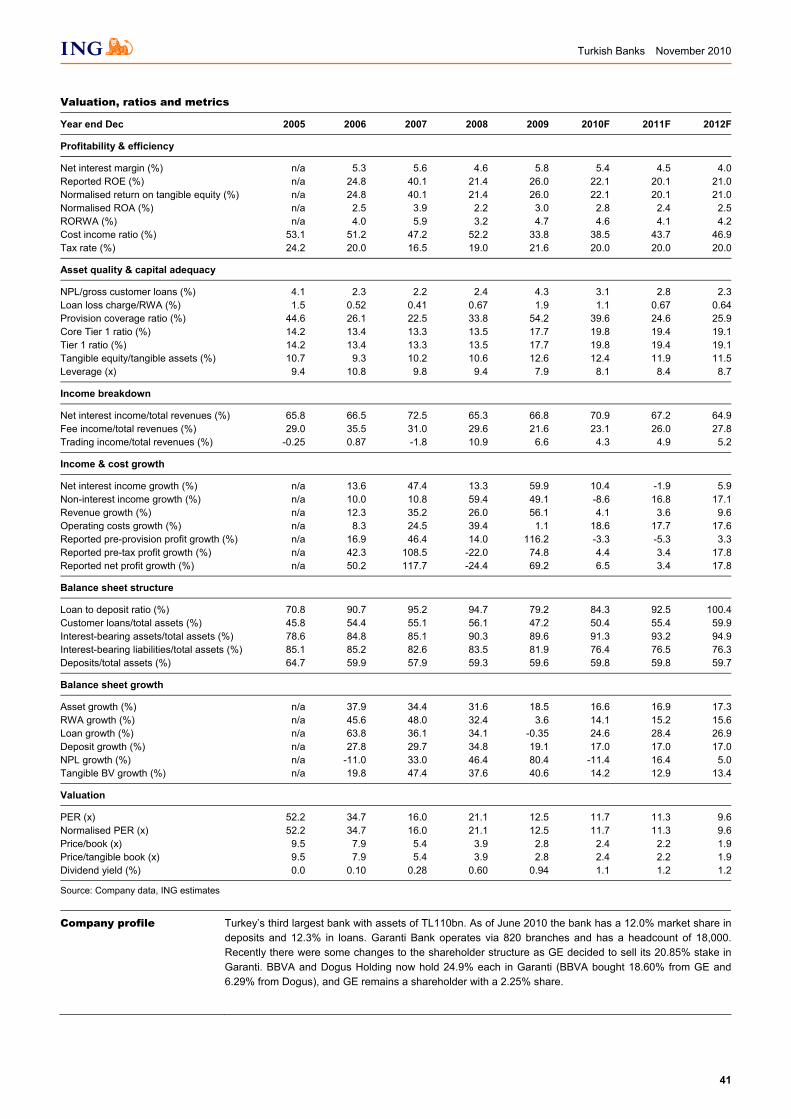

Valuation, ratios and metrics

Year end Dec 2005 2006 2007 2008 2009 2010F 2011F 2012F

Profitability & efficiency

Net interest margin (%) n/a 5.3 5.6 4.6 5.8 5.4 4.5 4.0Reported ROE (%) n/a 24.8 40.1 21.4 26.0 22.1 20.1 21.0Normalised return on tangible equity (%) n/a 24.8 40.1 21.4 26.0 22.1 20.1 21.0Normalised ROA (%) n/a 2.5 3.9 2.2 3.0 2.8 2.4 2.5RORWA (%) n/a 4.0 5.9 3.2 4.7 4.6 4.1 4.2Cost income ratio (%) 53.1 51.2 47.2 52.2 33.8 38.5 43.7 46.9Tax rate (%) 24.2 20.0 16.5 19.0 21.6 20.0 20.0 20.0

Asset quality & capital adequacy

NPL/gross customer loans (%) 4.1 2.3 2.2 2.4 4.3 3.1 2.8 2.3Loan loss charge/RWA (%) 1.5 0.52 0.41 0.67 1.9 1.1 0.67 0.64Provision coverage ratio (%) 44.6 26.1 22.5 33.8 54.2 39.6 24.6 25.9Core Tier 1 ratio (%) 14.2 13.4 13.3 13.5 17.7 19.8 19.4 19.1Tier 1 ratio (%) 14.2 13.4 13.3 13.5 17.7 19.8 19.4 19.1Tangible equity/tangible assets (%) 10.7 9.3 10.2 10.6 12.6 12.4 11.9 11.5Leverage (x) 9.4 10.8 9.8 9.4 7.9 8.1 8.4 8.7

Income breakdown

Net interest income/total revenues (%) 65.8 66.5 72.5 65.3 66.8 70.9 67.2 64.9Fee income/total revenues (%) 29.0 35.5 31.0 29.6 21.6 23.1 26.0 27.8Trading income/total revenues (%) -0.25 0.87 -1.8 10.9 6.6 4.3 4.9 5.2

Income & cost growth

Net interest income growth (%) n/a 13.6 47.4 13.3 59.9 10.4 -1.9 5.9Non-interest income growth (%) n/a 10.0 10.8 59.4 49.1 -8.6 16.8 17.1Revenue growth (%) n/a 12.3 35.2 26.0 56.1 4.1 3.6 9.6Operating costs growth (%) n/a 8.3 24.5 39.4 1.1 18.6 17.7 17.6Reported pre-provision profit growth (%) n/a 16.9 46.4 14.0 116.2 -3.3 -5.3 3.3Reported pre-tax profit growth (%) n/a 42.3 108.5 -22.0 74.8 4.4 3.4 17.8Reported net profit growth (%) n/a 50.2 117.7 -24.4 69.2 6.5 3.4 17.8

Balance sheet structure

Loan to deposit ratio (%) 70.8 90.7 95.2 94.7 79.2 84.3 92.5 100.4Customer loans/total assets (%) 45.8 54.4 55.1 56.1 47.2 50.4 55.4 59.9Interest-bearing assets/total assets (%) 78.6 84.8 85.1 90.3 89.6 91.3 93.2 94.9Interest-bearing liabilities/total assets (%) 85.1 85.2 82.6 83.5 81.9 76.4 76.5 76.3Deposits/total assets (%) 64.7 59.9 57.9 59.3 59.6 59.8 59.8 59.7

Balance sheet growth