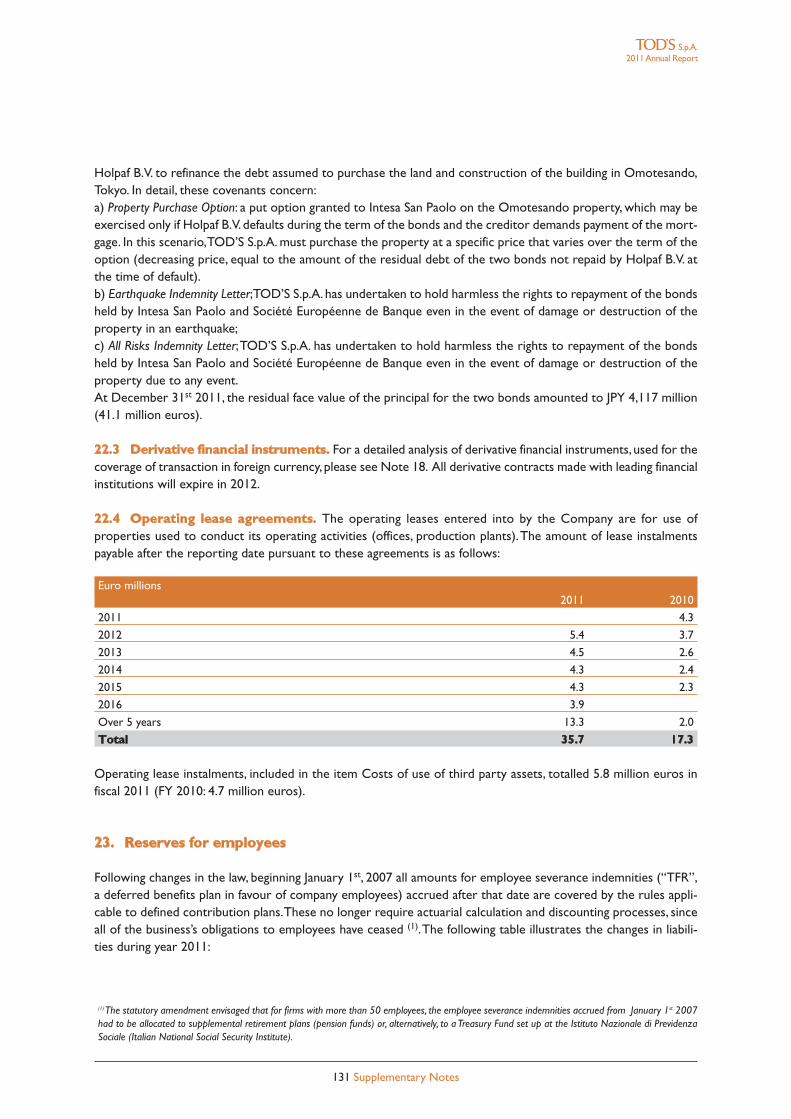

(translation of the 2011annual report approved in italian, …€¦ · · 2017-02-03letter to our...

TRANSCRIPT

2011 ANNUAL REPORT

(Translation of the 2011 Annual report approved in Italian,solely for the convenience of international readers)

2011Annual Report

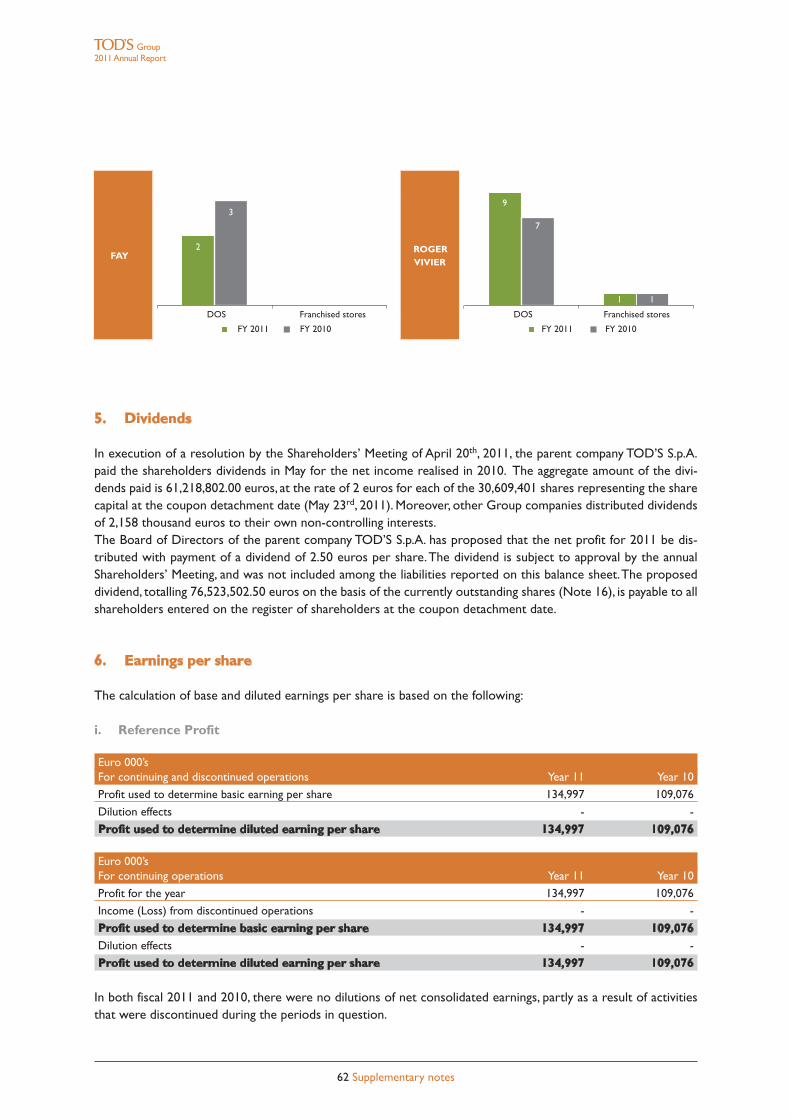

4 Table of contents

TABLE OF CONTENTS

Letter to our Shareholders . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9Company’s data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10Corporate Governance bodies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11TOD’S Group . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12Group’s organizational chart . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13Distribution network as of December 31st 2011 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14Key consolidated financial figures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15Highlights of results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

TOD’S Group - Consolidated Financial Statements as at December 31st 2011

Report on operationsIntroduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29Alternative indicators of performances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29Group’s activity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29Group’s brands . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30Organizational structure of the Group. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31Foreign currency markets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31Main events and operations during the period . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31The Group’s results in 2011 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32Research and development . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38Reconciliation of the result for the period and net equity of the Group withthe analogous values of the Parent Company. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39Corporate Governance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39Significant events occurring after the end of the period . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41Business outlook . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41Approval of Financial Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41

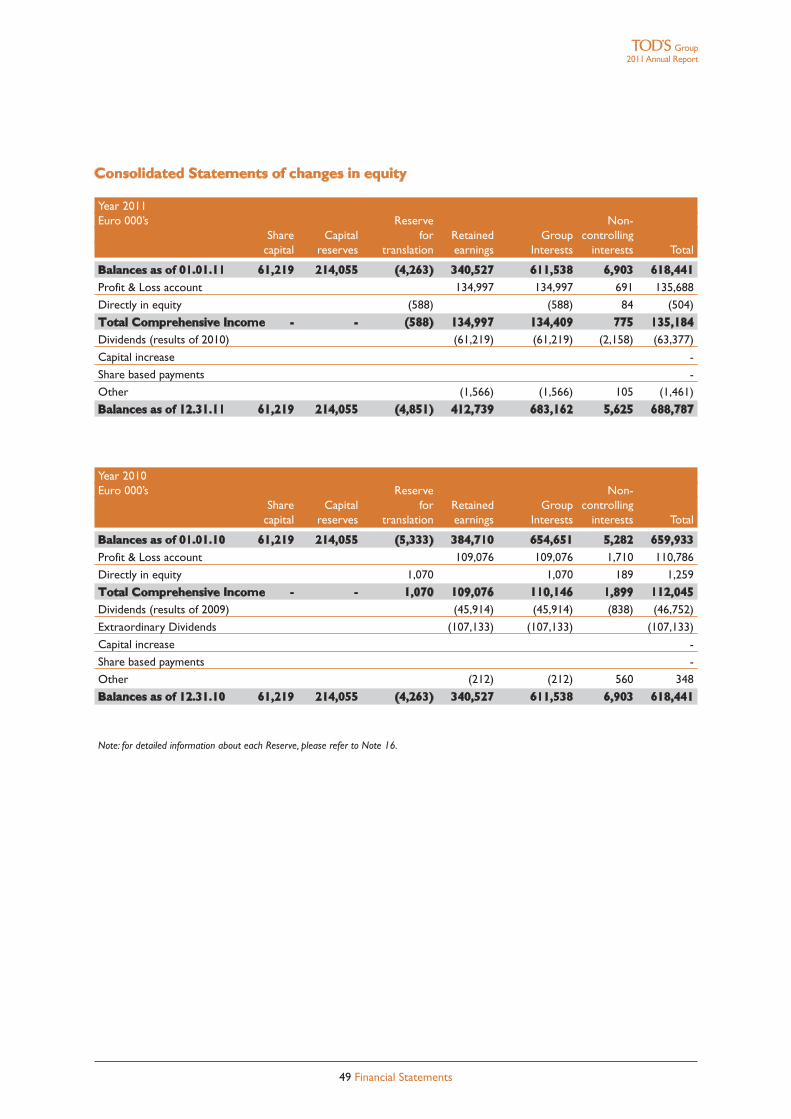

Financial StatementsConsolidated Profit & Loss . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44Consolidated Comprehensive Income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45Consolidated Statement of Financial position. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46Consolidated Statement of Cash Flows . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48Consolidated Statement of changes in equity. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

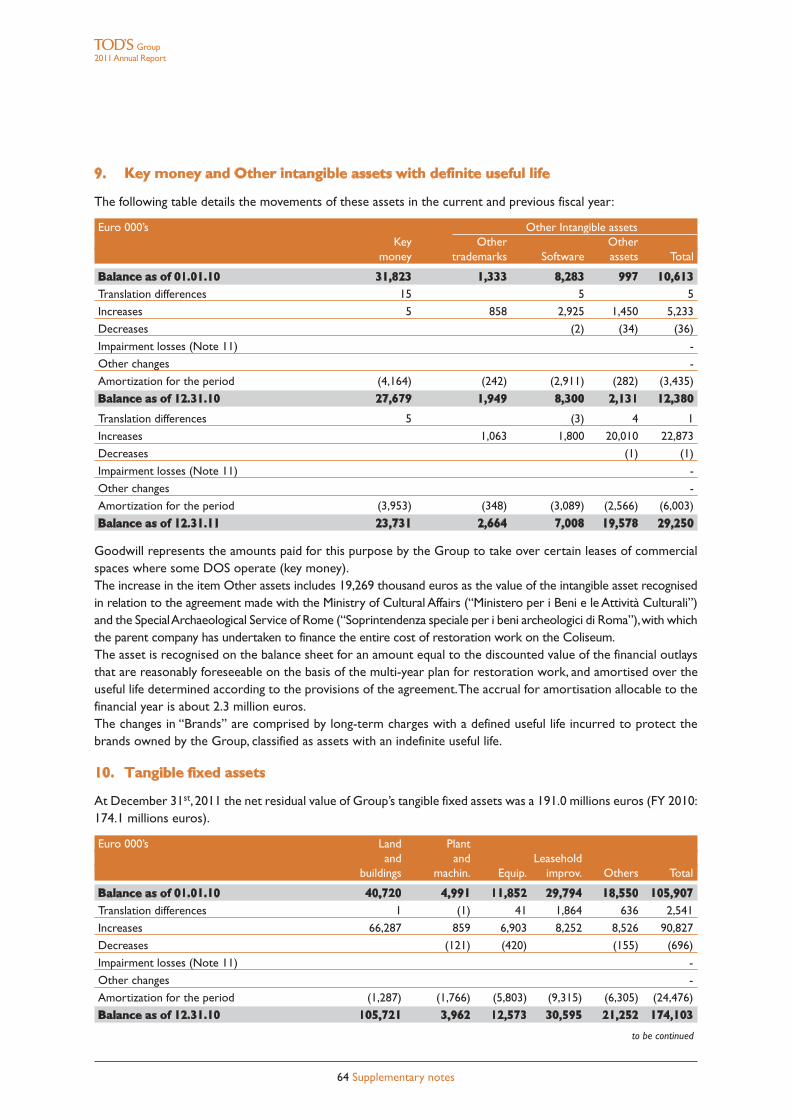

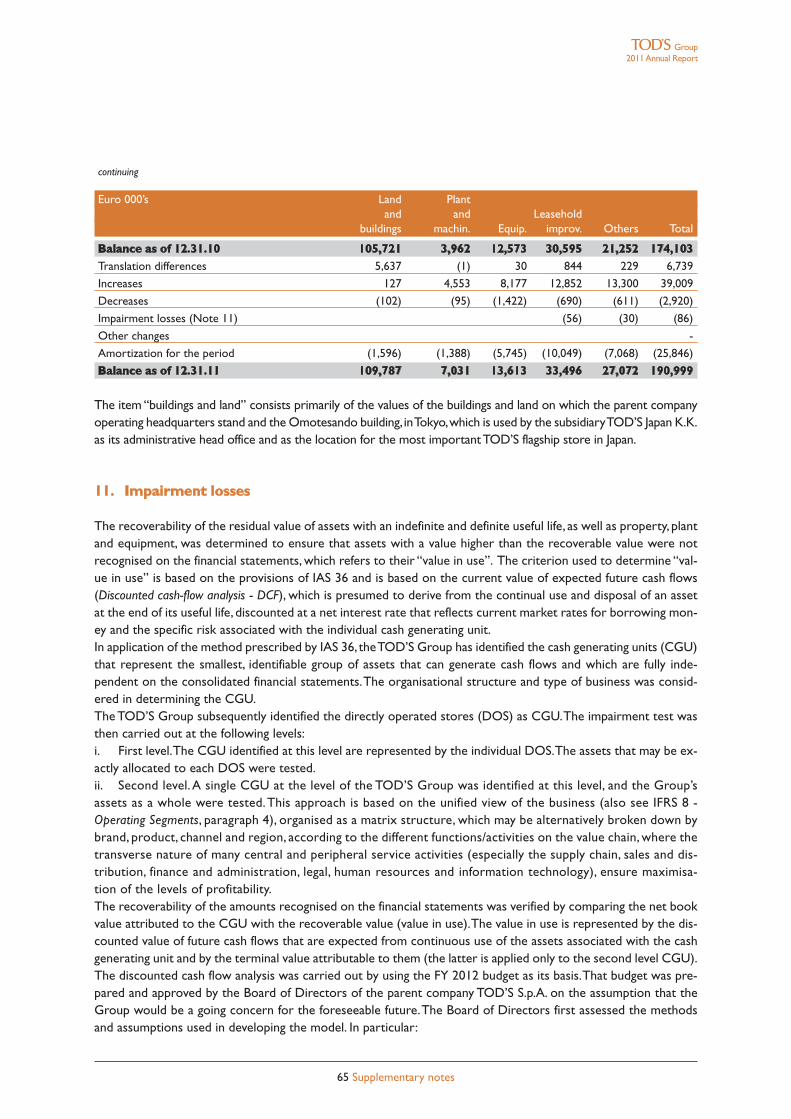

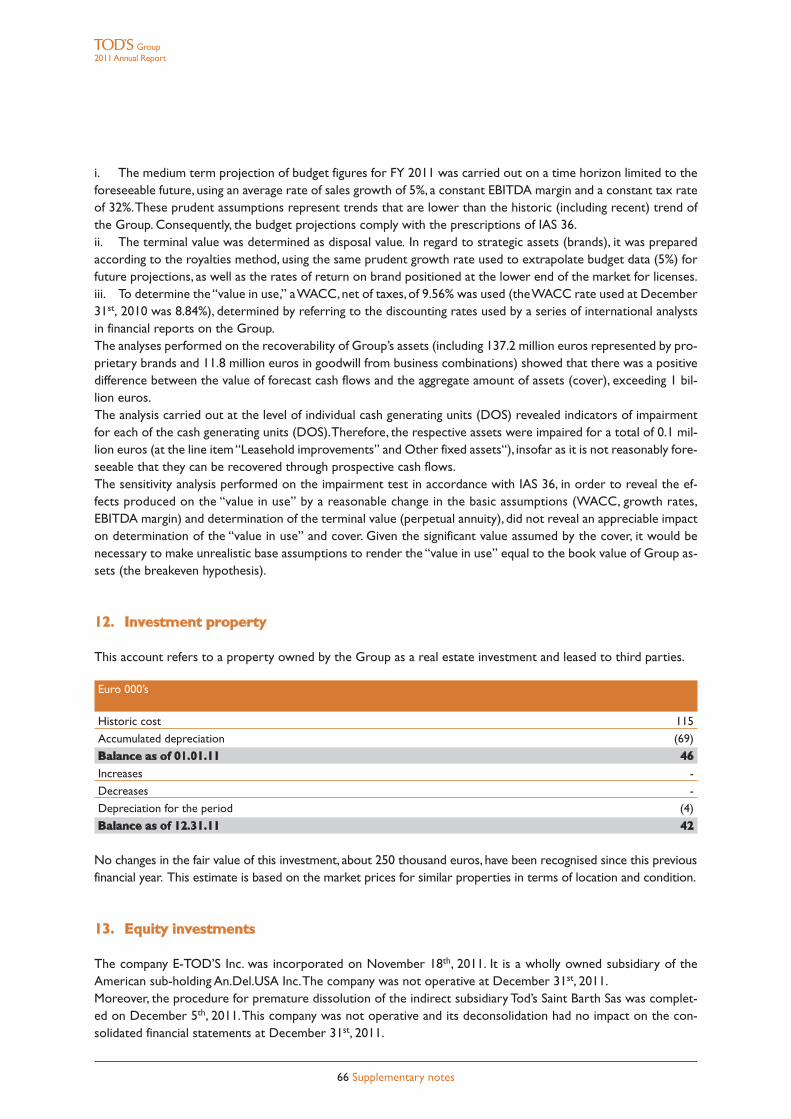

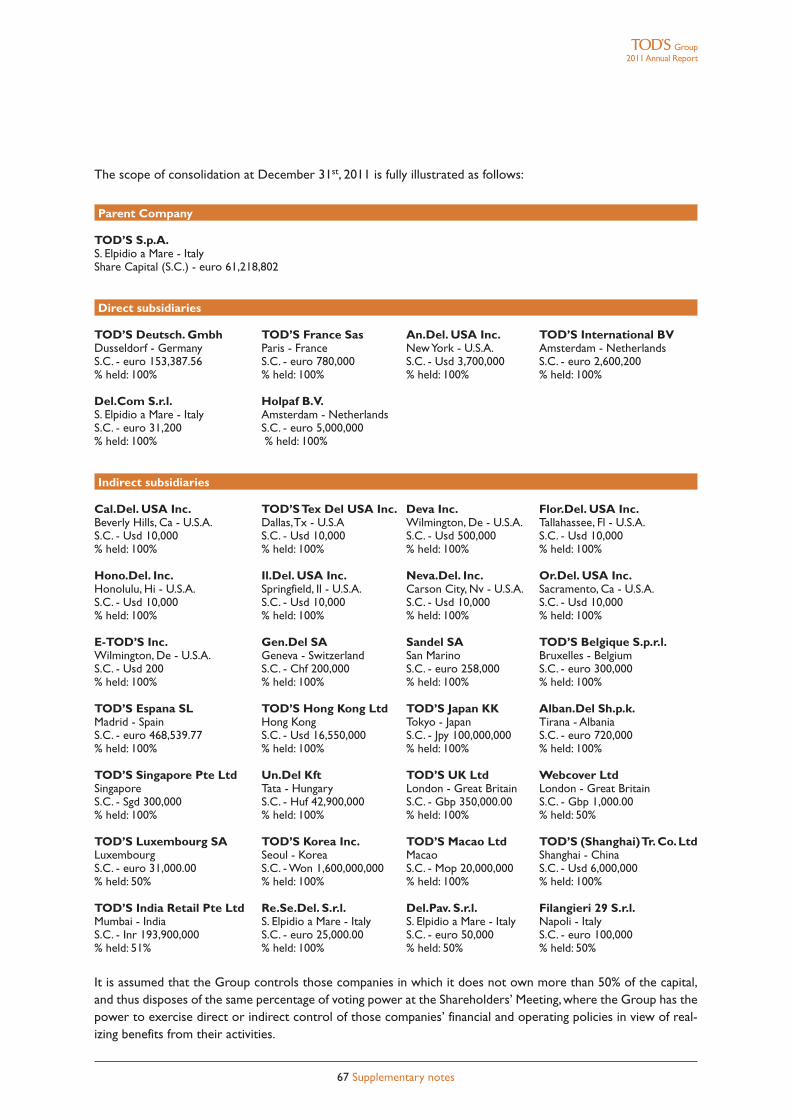

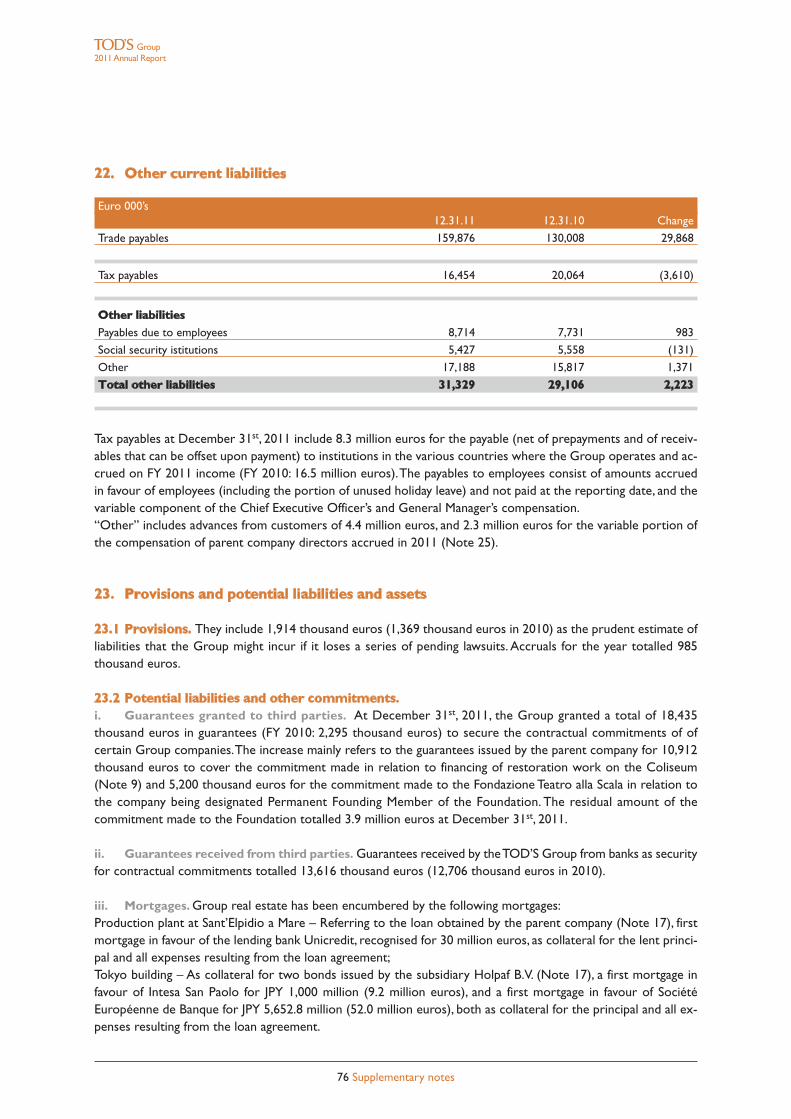

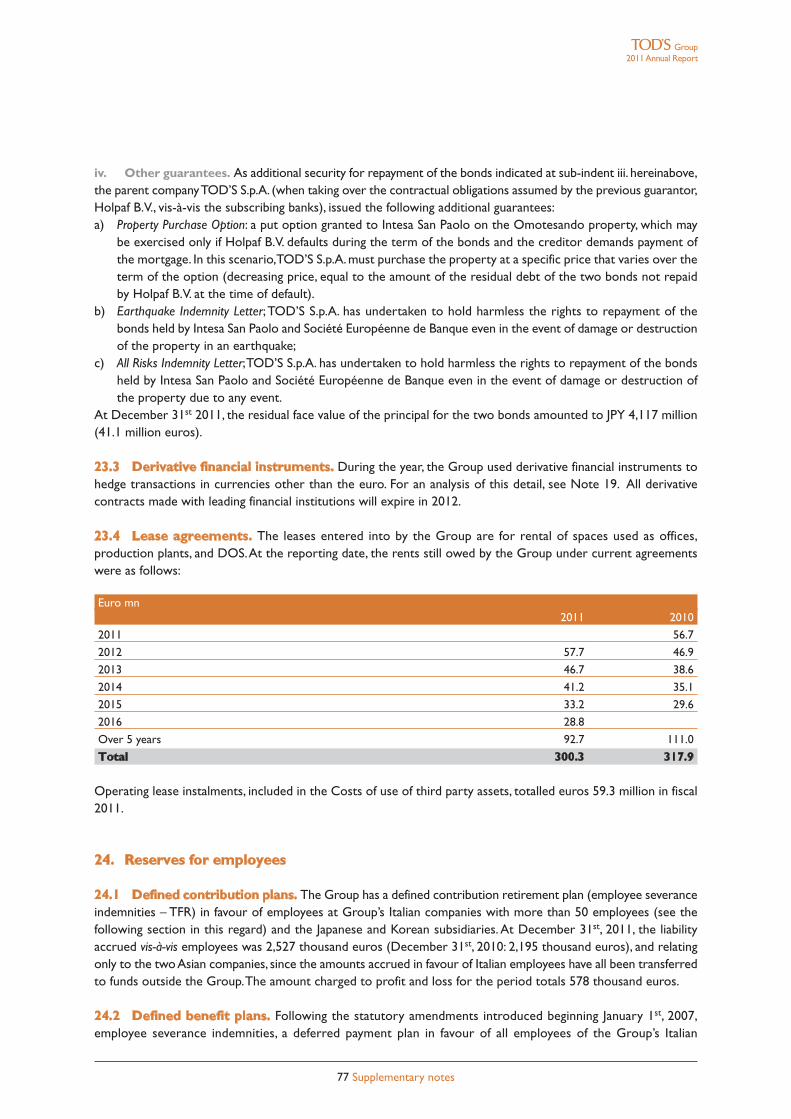

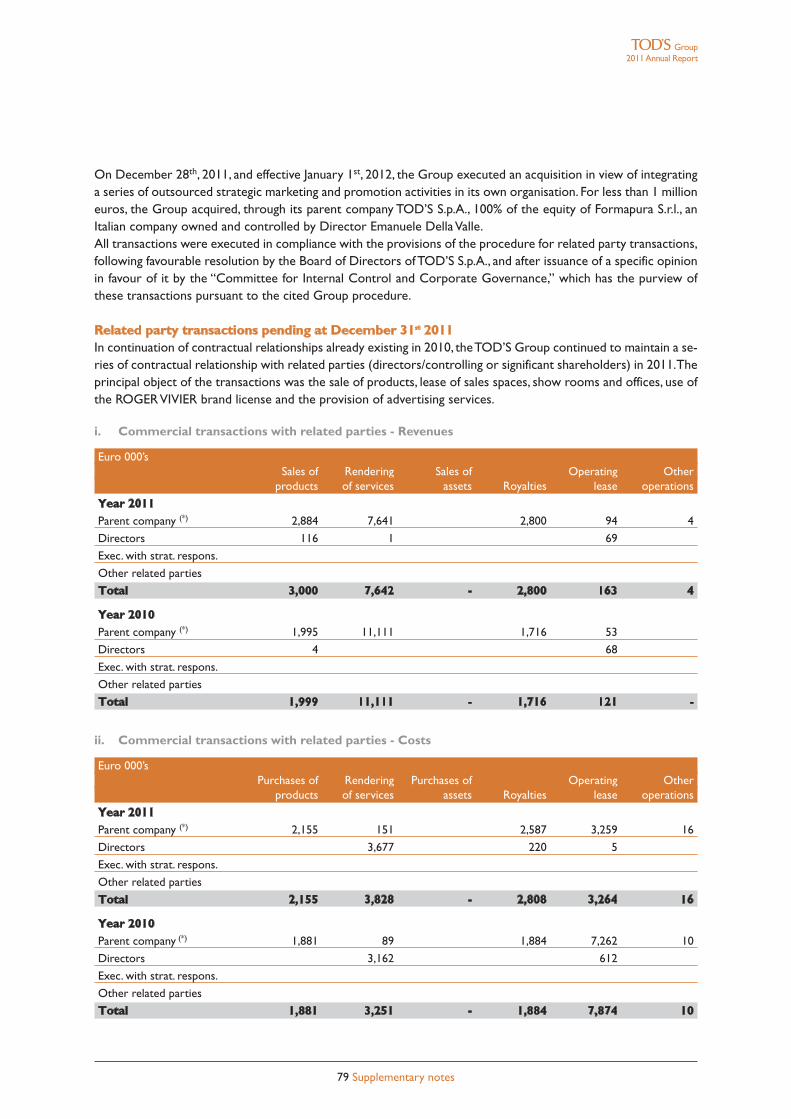

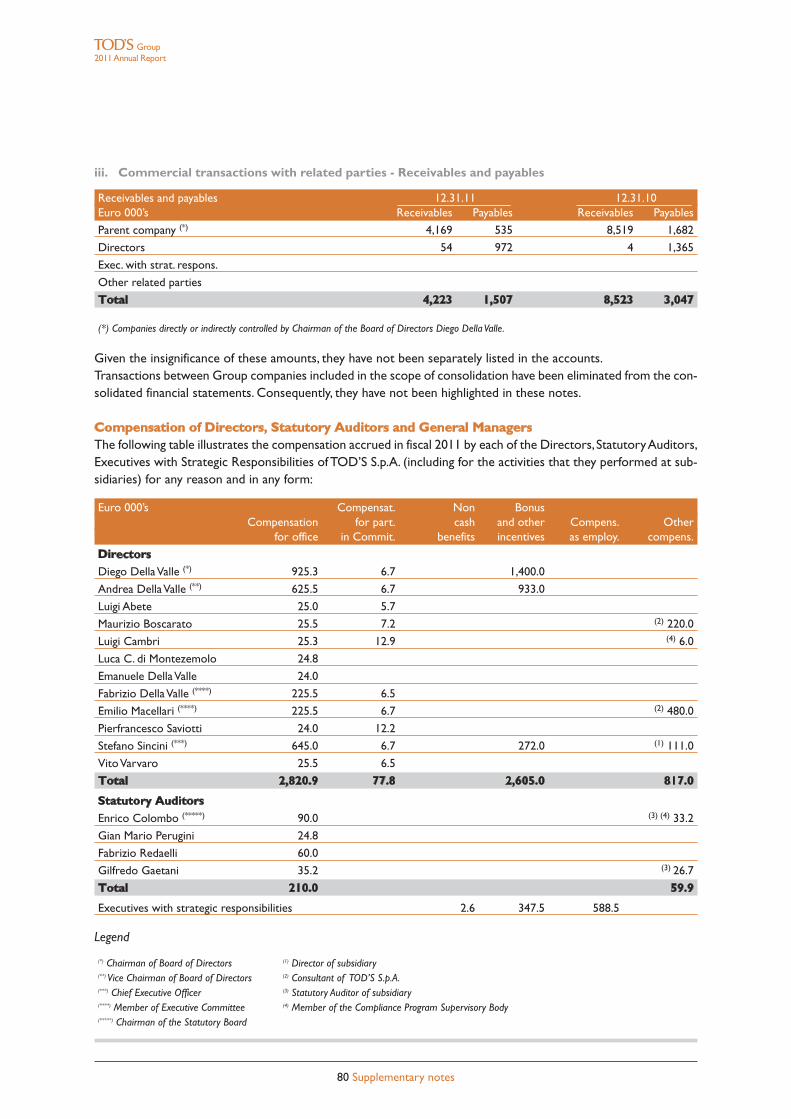

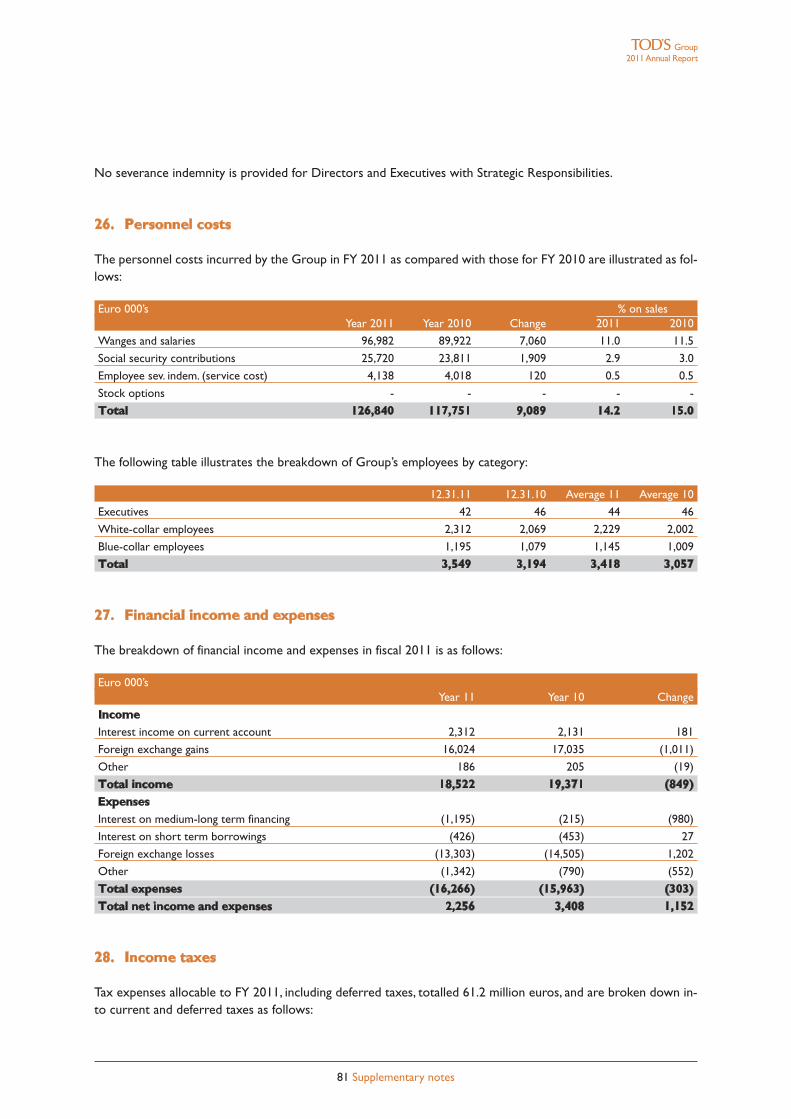

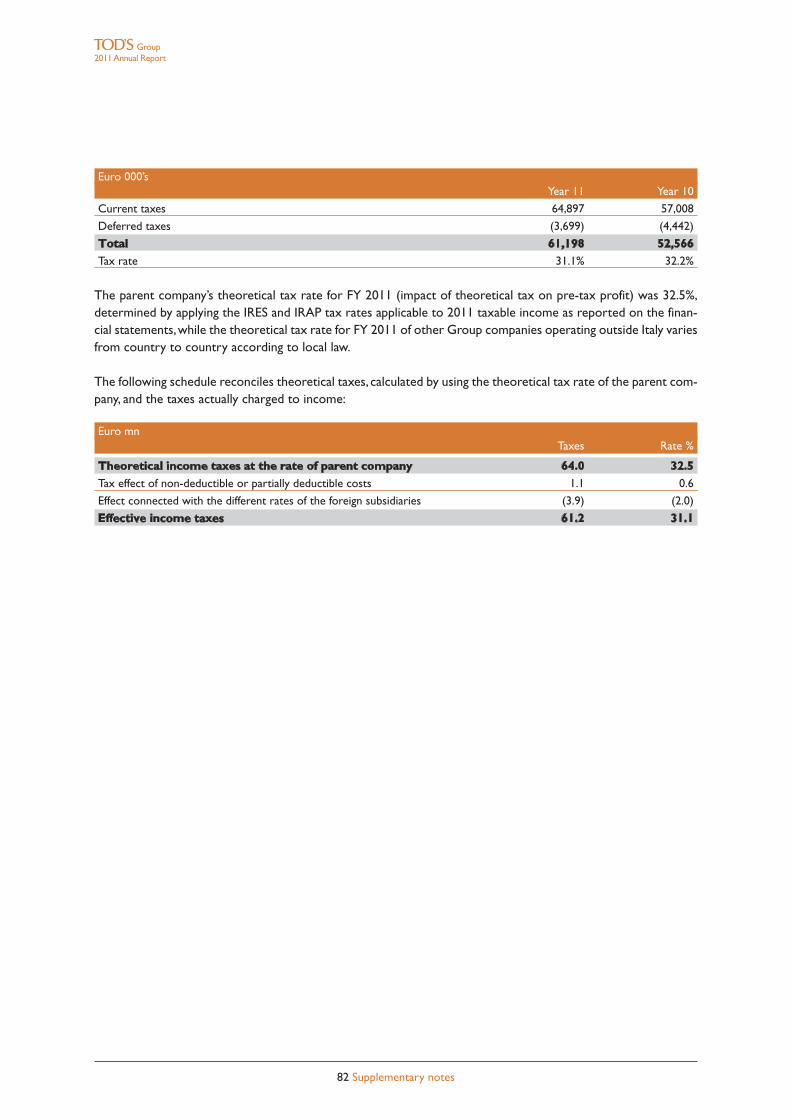

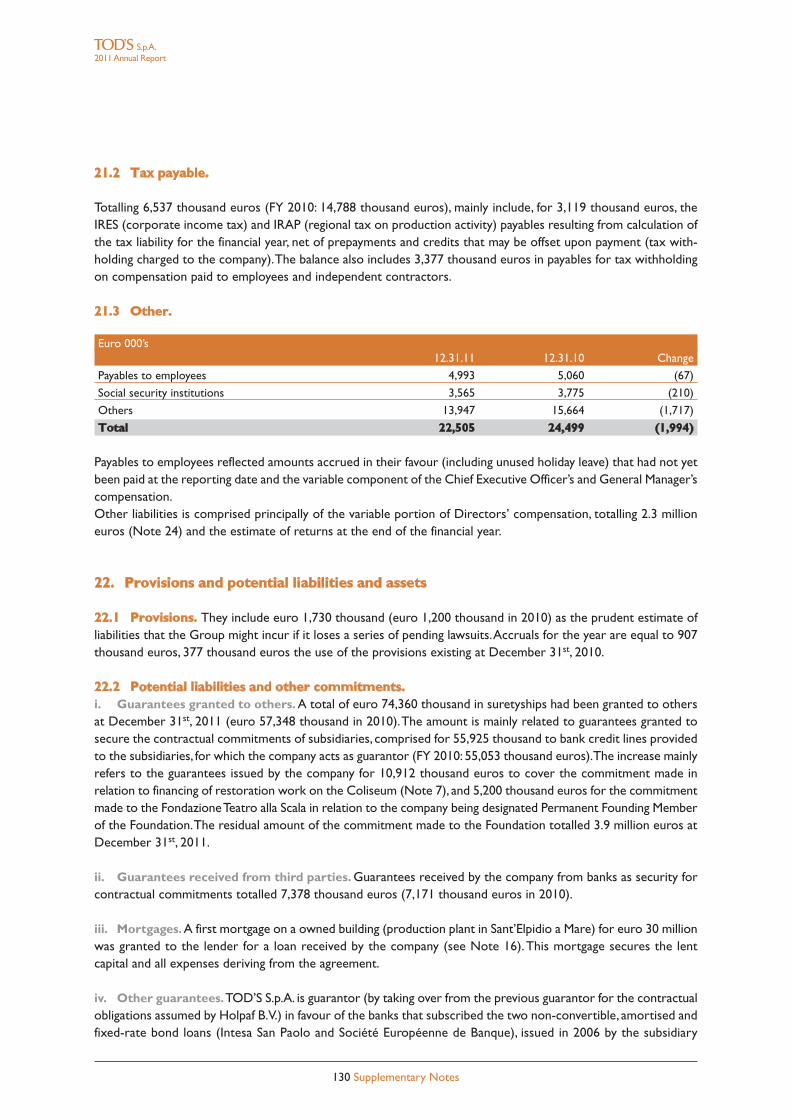

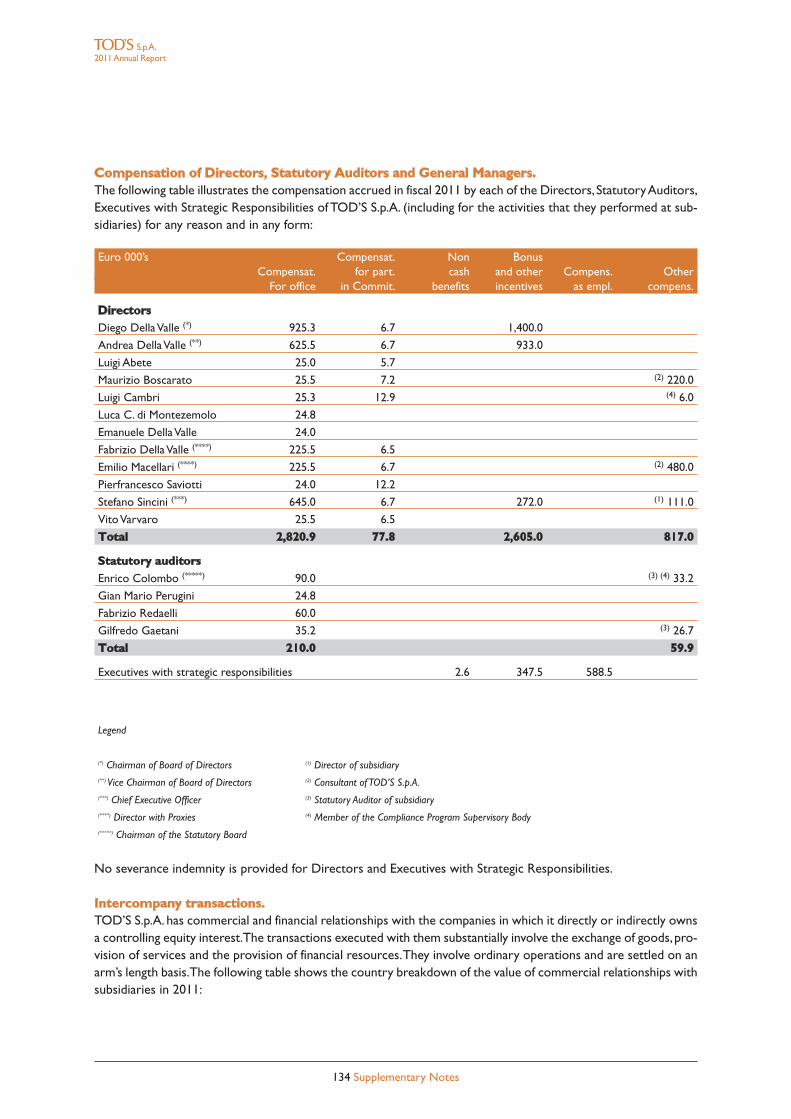

Supplementary notes1. General notes. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 522. Financial statements formats: choice of form and classification principles . . . . . . . . . . . . . . . . . . . . . . . . . . 523. Highlights of the accounting standards . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 524. Segment reporting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 605. Dividends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 626. Earnings per share . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 627. Assets held for sale . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 638. Assets with indefinite useful life. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 639. Key money and Other intangible assets with definite useful life. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6410. Tangible fixed assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6411. Impairment losses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6512. Investment property . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6613. Equity investments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6614. Inventories . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6815. Other current assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6816. Equity attributable to the Group. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6917. Financial liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7018. Other non current liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7119. Derivative financial instruments. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7120 Hedging of financial risks (IFRS 7) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7221. Deferred tax assets and liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7522. Other current liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7623. Provisions and potential liabilities and assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7624. Reserves for employees. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7725. Transactions with related parties. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7826. Personnel costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81

27. Financial income and expenses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8128. Income taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81

Report of Independent Auditors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 86

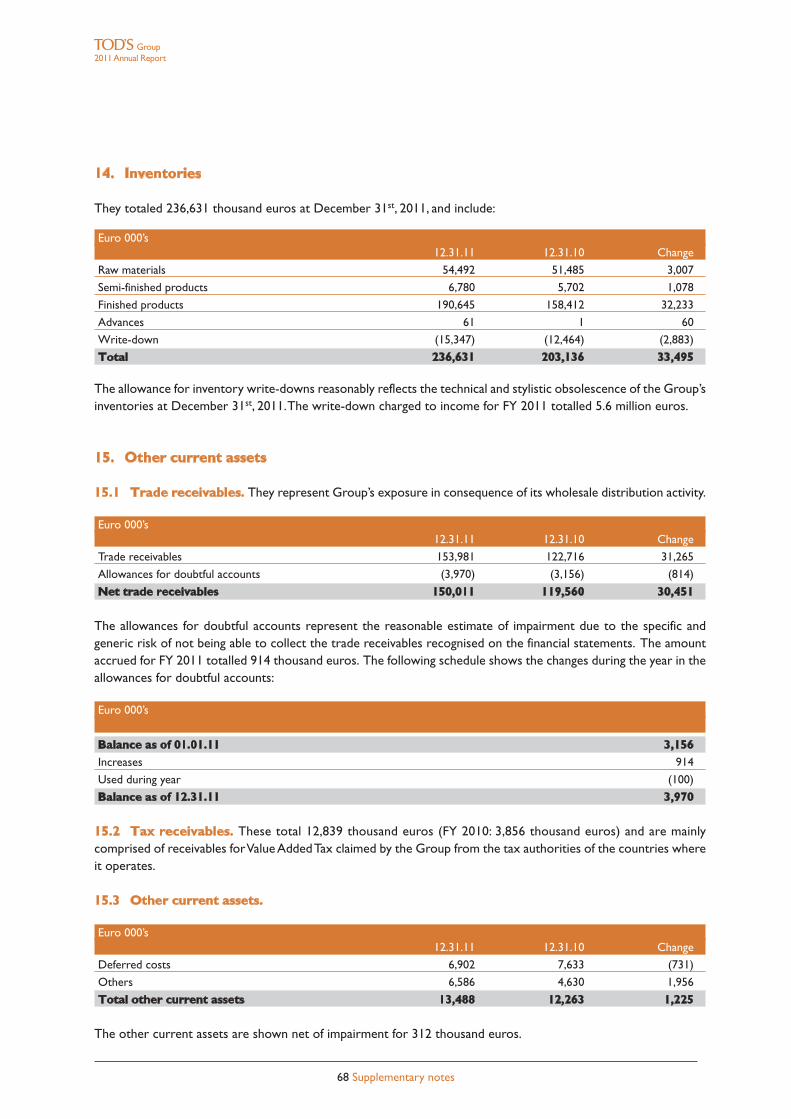

TOD'S S.p.A. - IAS/IFRS Annual Report as of December 31st 2011

Report on operationsIntroduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91Alternative indicators of performances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91Operating performances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91Research and development . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 95Information on Share Capital . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 95Corporate Governance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 95Management and coordination activities. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 97Significant events occurring after the end of the fiscal year . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 98Business outlook . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 98Motion for allocation of the profit for the year . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 98

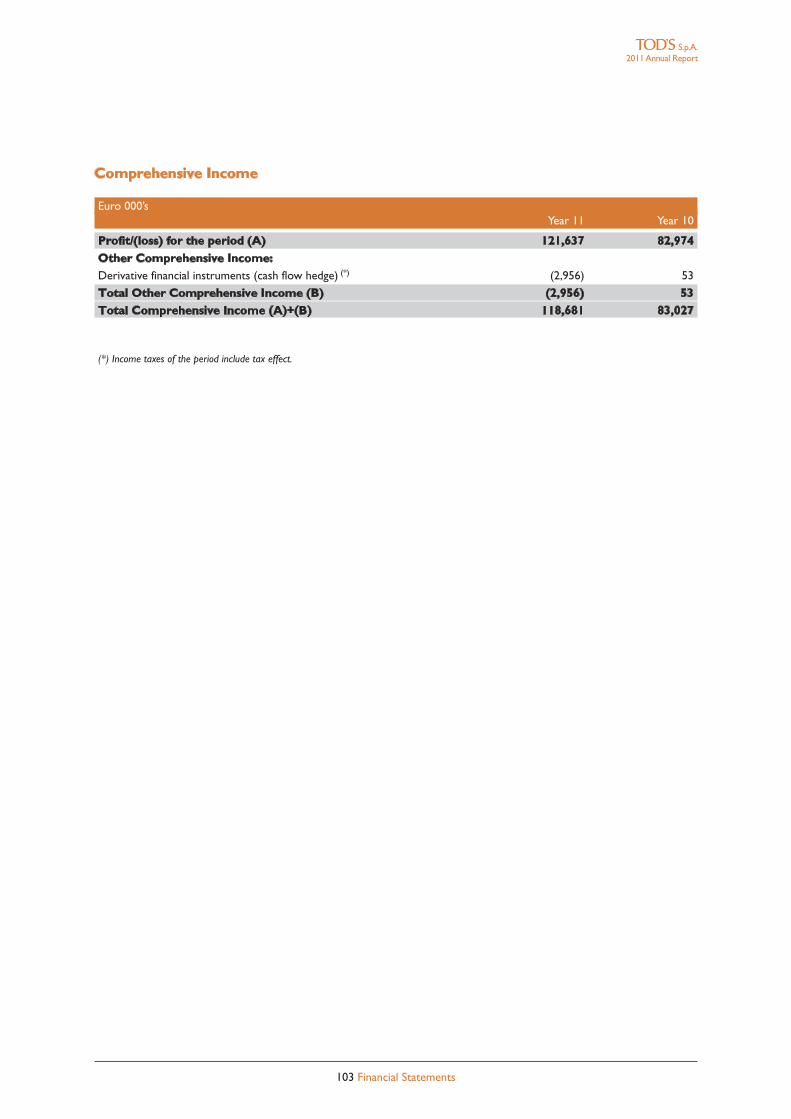

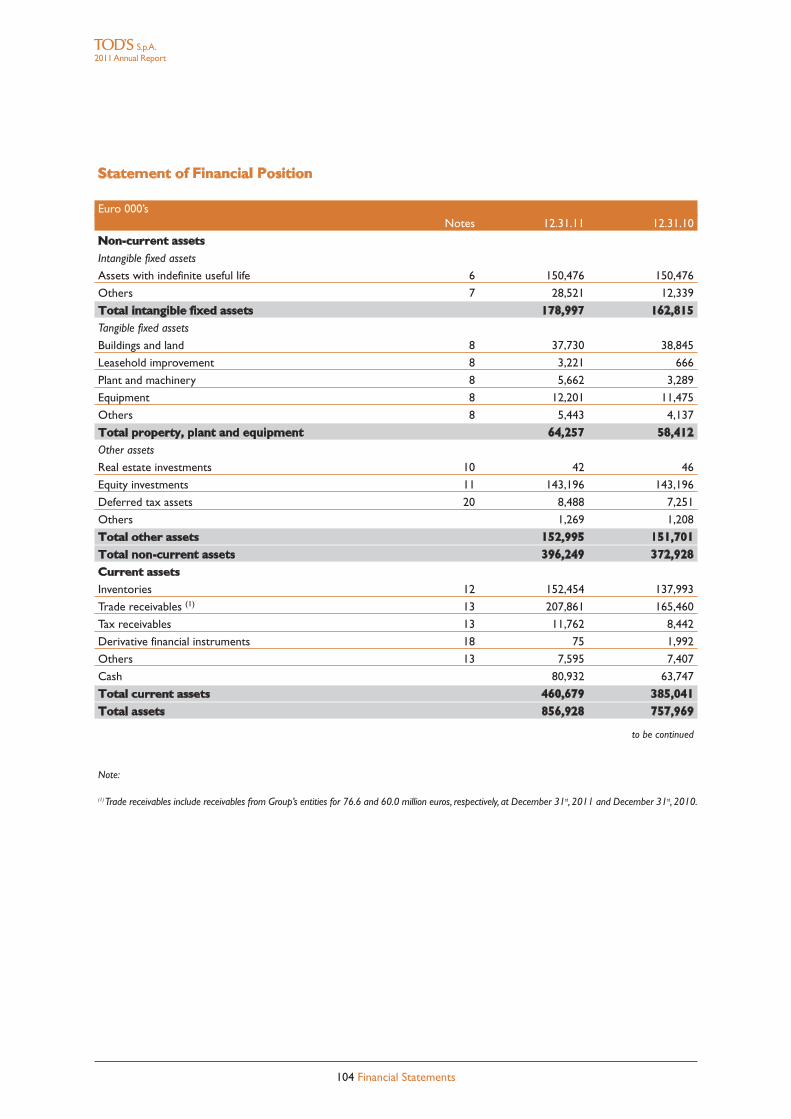

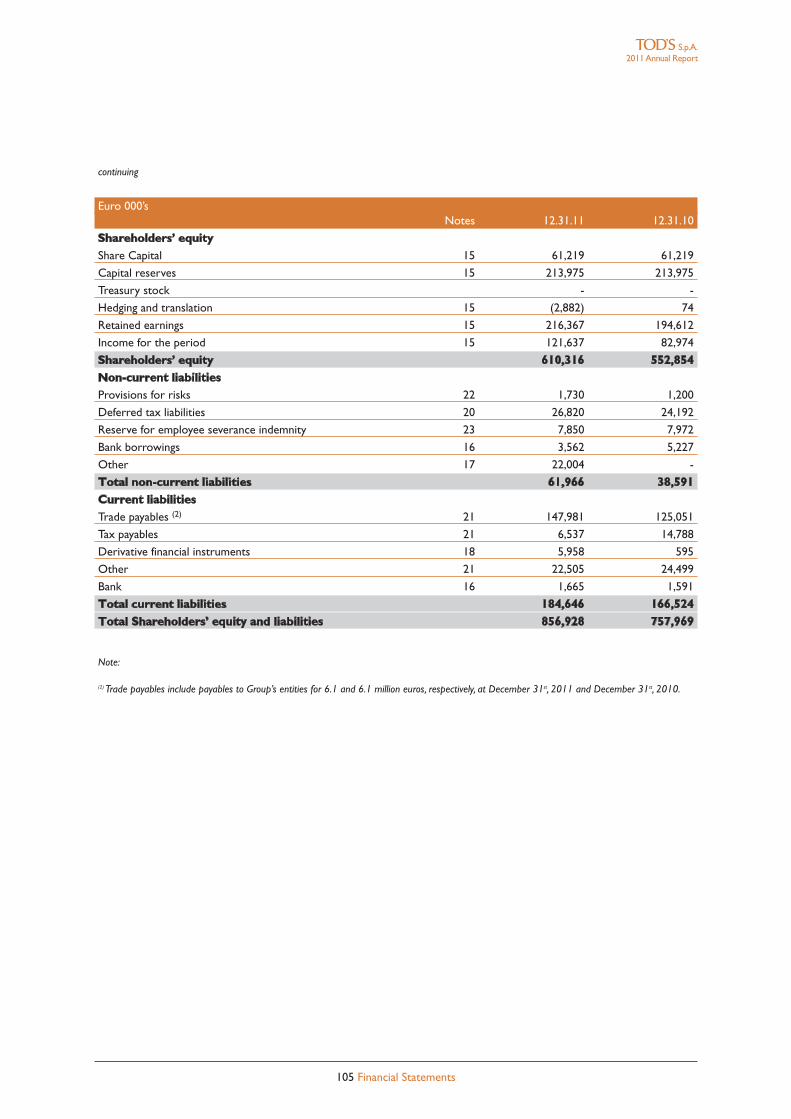

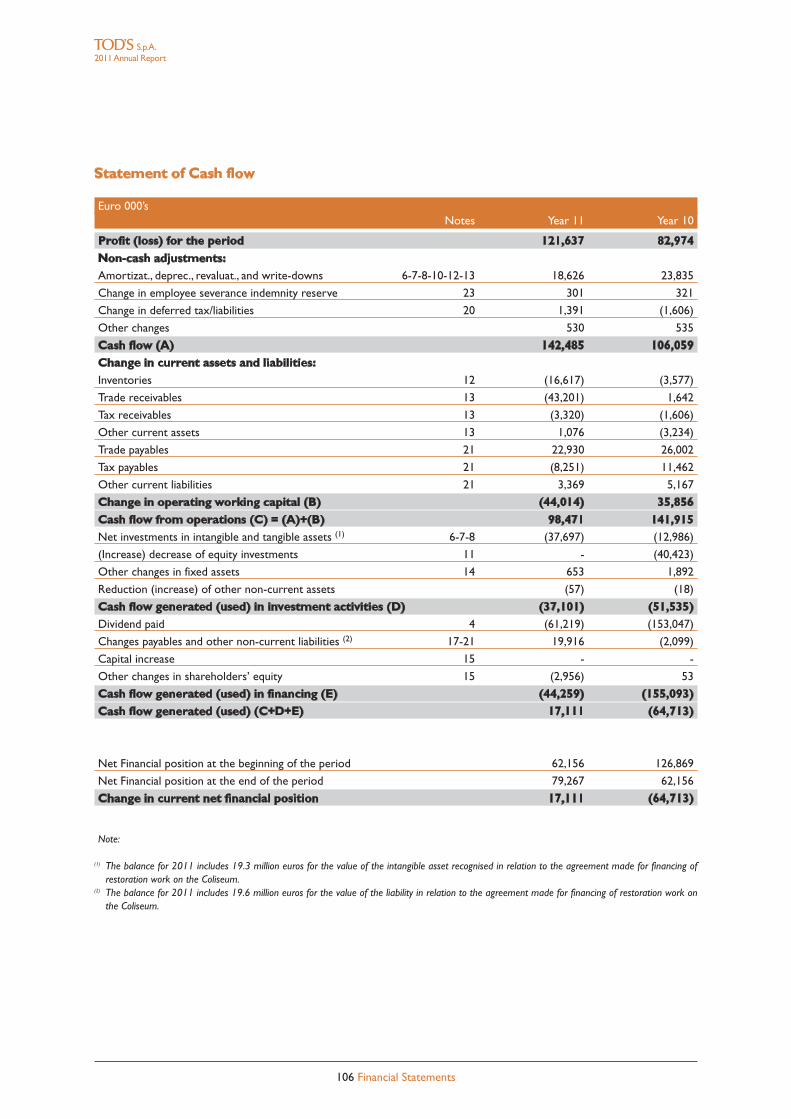

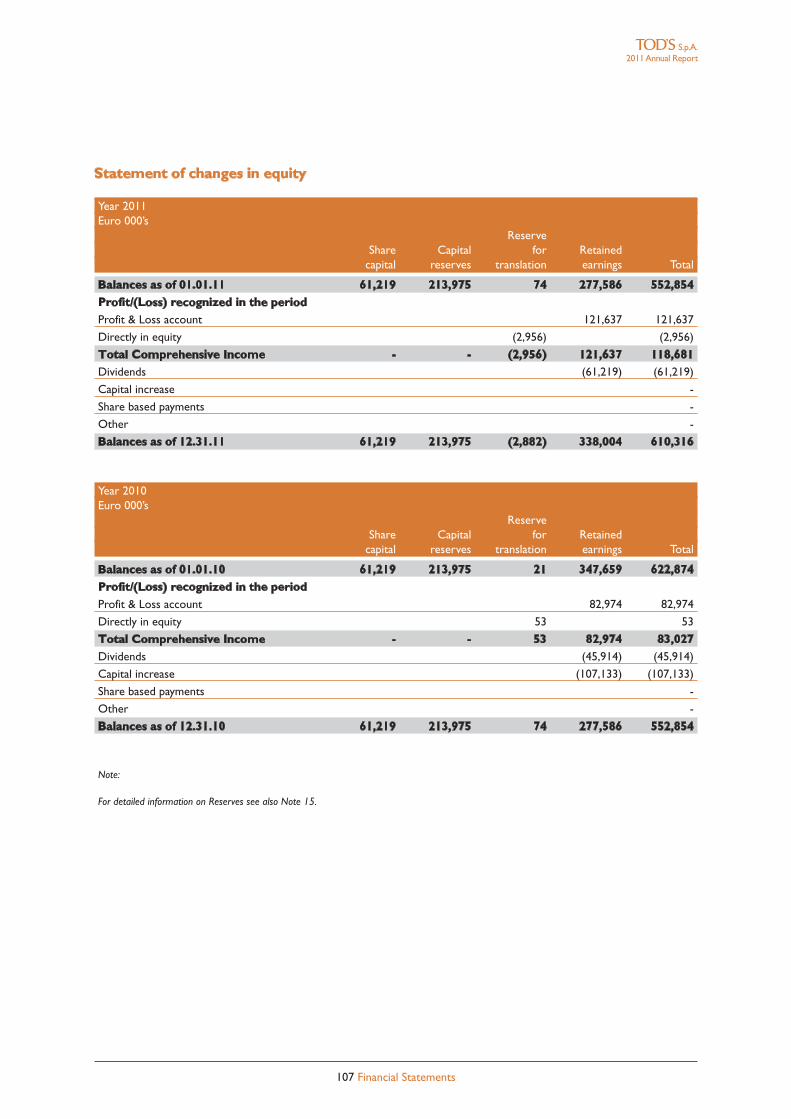

Financial StatementsProfit & Loss . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 102Comprehensive Income. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 103Statement of Financial Position . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 104Statement of Cash flow . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 106Statement of changes in equity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 107

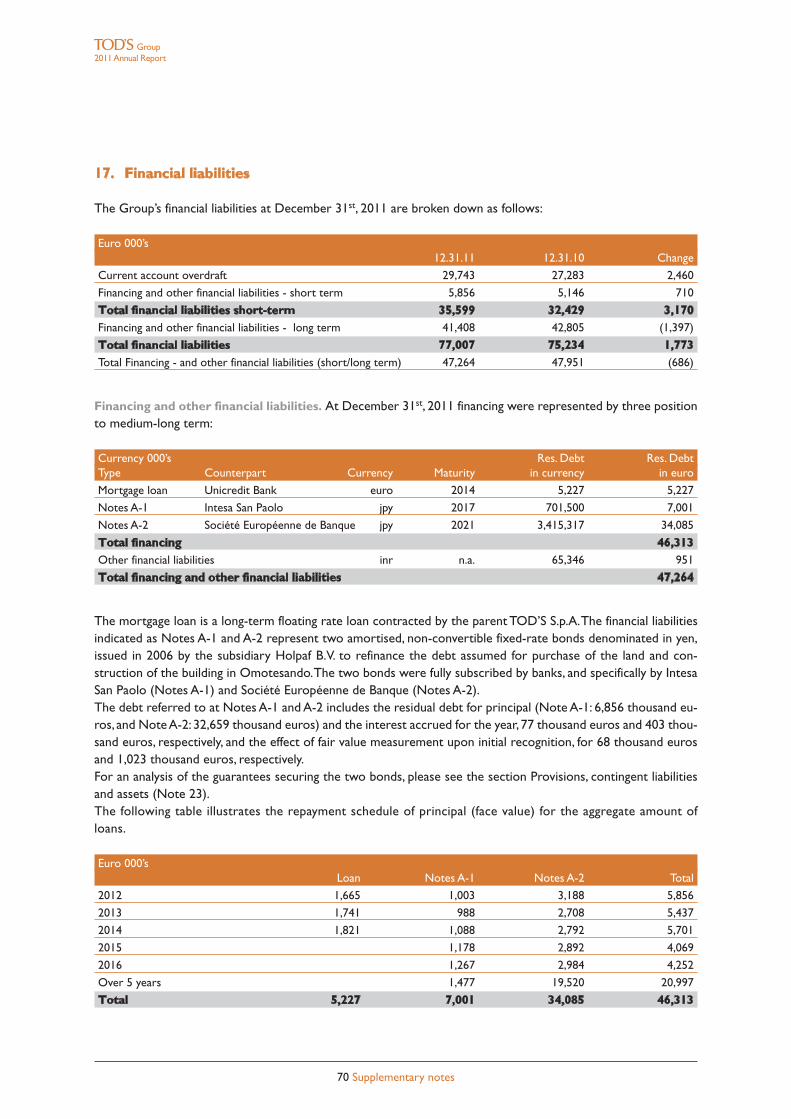

Supplementary notes1. General notes. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1102. Financial statements format: choice of form and classification principles. . . . . . . . . . . . . . . . . . . . . . . . . . . 1103. Highlights of the accounting standards . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1104. Dividends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1175. Earnings per share . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1176. Assets with indefinite useful life. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1187. Other assets. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1188. Tangible assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1199. Impairment losses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11910. Investment property . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12011. Investments in subsidiaries, joint ventures and associated companies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12012. Inventories . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12113. Other current assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12214. Financial assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12315. Shareholders’ equity. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12316. Bank overdraft and financing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12417. Other non current liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12518 Derivative financial instruments. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12519. Hedging of financial risks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12620. Deferred tax assets and liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12821. Other current liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12922. Provisions and potential liabilities and assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13023. Reserves for employees. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13124. Transactions with related parties. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13225. Personnel costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13526. Financial income and expenses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13627. Income from subsidiaries . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13628. Income taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13629. Independent Auditors compensation. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13730. Certification of the Separate Financial Statements of TOD’S S.p.A. and the Consolidated

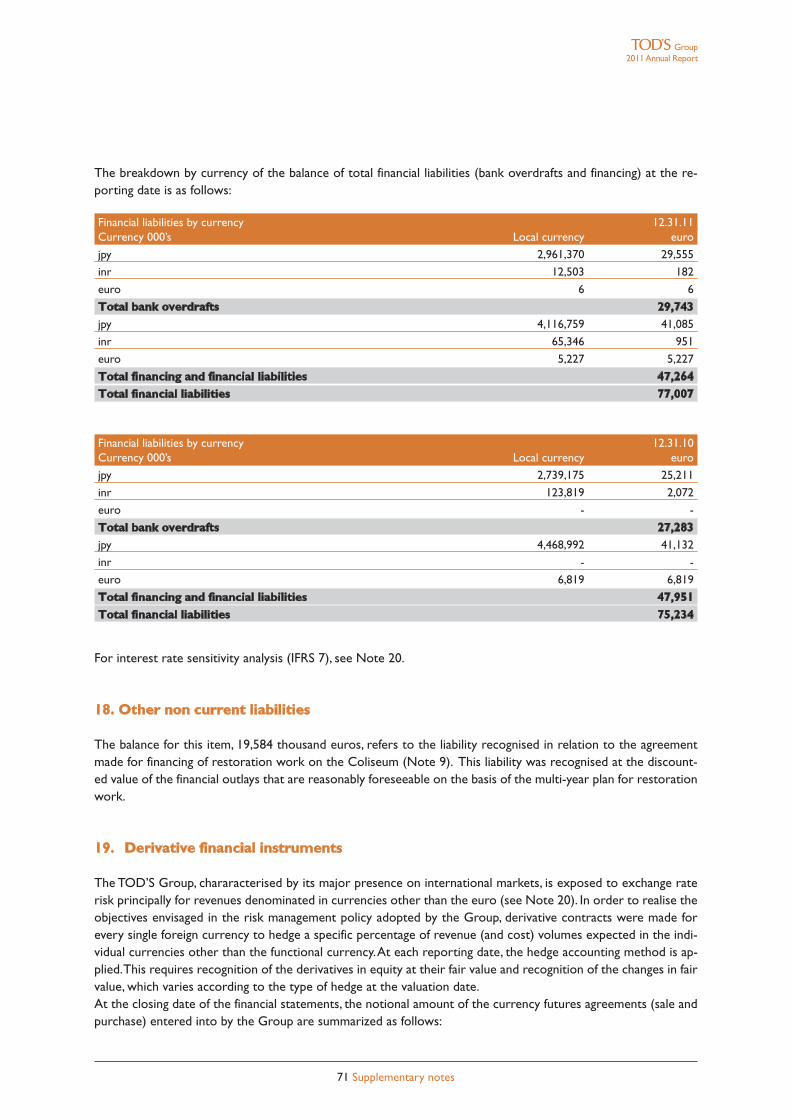

Financial Statements of the TOD’S Group pursuant to Article 81-ter of Consob Regulationno. 11971 of May 14th, 1999, as amended . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 138

Report of the Board of Statutory Auditors. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 142

Report of Independent Auditors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 145

2011Annual Report

5 Table of contents

2011Annual report

Diego DellaValleChairman and Chief Executive Officer

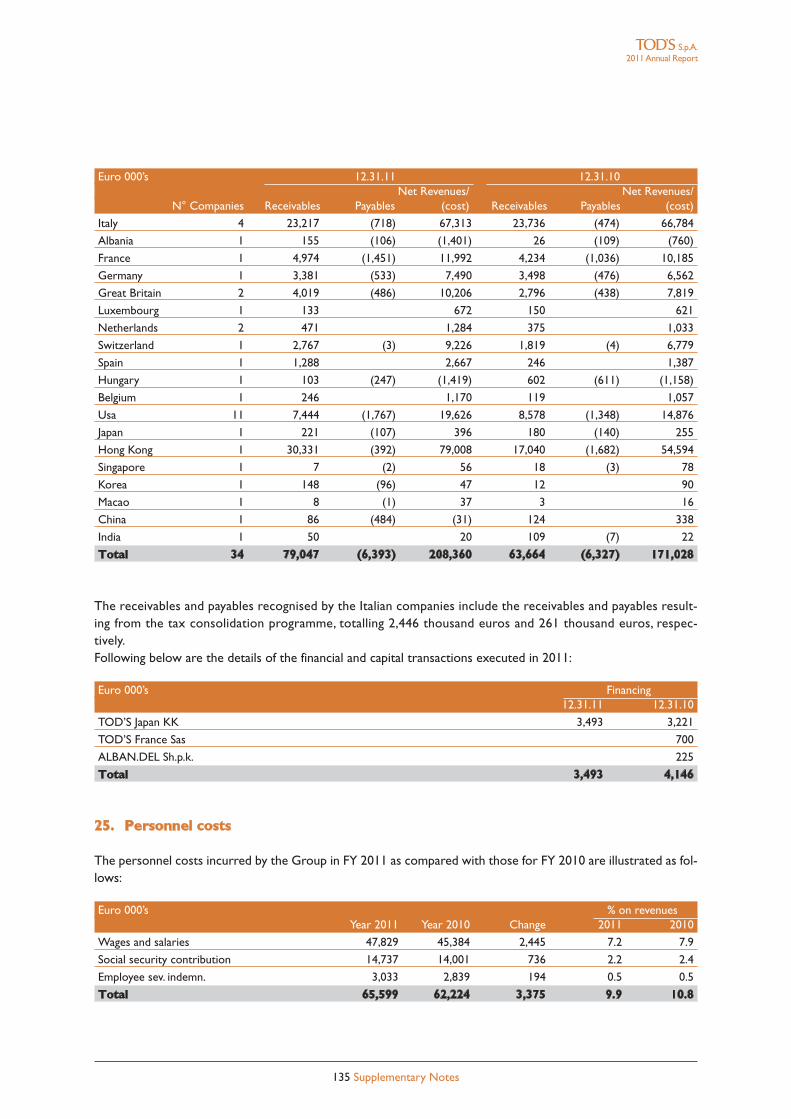

2011Annual Report

9 Letter to our Shareholders

Letter to our Shareholders

Dear Shareholders,

I’m pleased to comment excellent results for our Group also this year, which are even more significant if we consid-er that they were achieved in particularly difficult times for the market. The double-digit growth in sales has been ac-companied by a considerable improvement in operating profitability and, even more importantly, in the net profits.

These results confirm that our business model is successful and that our growth strategy, which combines thedevelopment of revenues and profits, is valid and effective.

In the course of the year, each trademark continued to develop on the basis of its guidelines for growth, both ge-ographically and in terms of product categories, maintaining a selective distribution policy, aiming to preservingits exclusive positioning.Excellent results were achieved in the USA and Asia, the markets with the greatest growth potential at the pres-ent time, in which Tod’s has a particularly high brand awareness.

Our Group has a well developed international distribution network, with flagship stores in the most prestigiousshopping streets of the world. This year, as in the past, we continued to invest in the extension and modernisa-tion of the network. Our new store opening policy this year focused on the Chinese market, which offers thegreatest potential for growth and in which the Group had 41 directly operated stores at the end of December.

In our firm, which is leader in one of the major districts for luxury shoes and leather goods of the world, the crafts-manship of the made in Italy lives together with a highly efficient logistic structure; therefore we are confident tohave all the production capacity necessary to face the future growth of turnover, while keeping the same top qual-ity levels. Our skilled personnel has also the task to train new young employees and to teach team our values ofcraftsmanship, quality and passion for details.

Our client are loyal to our products, which are more and more appreciated for their highest quality and recog-nisability, and their nature to be timeless icons, not linked to fashion trends. To purchase our products is the re-alization of a dream, but also an investment.

In 2011, we set up an agreement with the Ministry for the Cultural Affairs and the Supervisor for central Rome’sarchaeological area, to became the sole sponsor for the restructuring works on the Coliseum, with a total com-mittment of 25 million Euros, spread during the duration of the works. Tod’s also became a Permanent FoundingMember of the La Scala Theatre Foundation of Milan, for which it will pay out a sum of 5.2 million Euros to sup-port the activities of the theatre.Tod’s, which is one of the most prestigious names in Italian made products, believes that it is its duty, as well asan honour, to contribute to the image of two of the most famous symbols of Italy in the eyes of the world.

The Group has also confirmed its sound financial situation, high quality receivables, a solidly positive cash balanceand a strong cashflow. Once again this year, we increased the dividend, confirming a significant and stable payout,which guarantees a very interesting return for the shareholders, while, at the same time, ensuring that the Groupretains all the resources it needs to drive its growth.

As always, I wish to express my sincere thanks to all the Group employees for their commitment and dedication,to you, the shareholders, for the confidence you have shown in the company, and to all our customers for theirappreciation of the very high quality of our products.

Kindest regards,Diego DellaValleChairman of the Board of Directors

2011Annual Report

10 Company’s data

Company’s data

Registered office

TOD’S S.p.A.Via Filippo DellaValle, 163811 Sant’Elpidio a Mare (Fermo) - ItalyTel. +39 0734 8661

Legal dataParent company

Share capital resolved euro 61,218,802Share capital subscribed and paid euro 61,218,802Fiscal Code and registration number on Company Register of Court of Fermo: 01113570442Registered with the Chamber of Commerce of Fermo under n. 114030 R.E.A.

Offices and Showrooms Dusseldorf - Kaistrasse, 2Hong Kong - Three Pacific Place, 1 Queen’s Road EastLondon - Old Bond Street, 16Milan - CorsoVenezia, 30Milan -Via Savona, 56Milan -Via Serbelloni 1-4Milan -Via della Spiga, 22NewYork - 450,West 15th StreetParis - Rue Royale, 20Seoul - 89-10, Cheongdam-dong, Kangnam-kuShanghai - 1717 Nanjing West Road,Wheelock Square 45/FTokyo - Omotesando Building, 5-1-5 Jingumae

Production facilities Comunanza (AP) -Via Merloni, 7Comunanza (AP) -Via S. Maria, 2-4-6Sant’Elpidio a Mare (FM) -Via Filippo DellaValle, 1Bagno a Ripoli, Loc.Vallina (FI) -Via del Roseto, 60Bagno a Ripoli, Loc.Vallina (FI) -Via del Roseto, 50Tolentino (MC) -Via Sacharov 41/43

2011Annual Report

11 Corporate Governance bodies

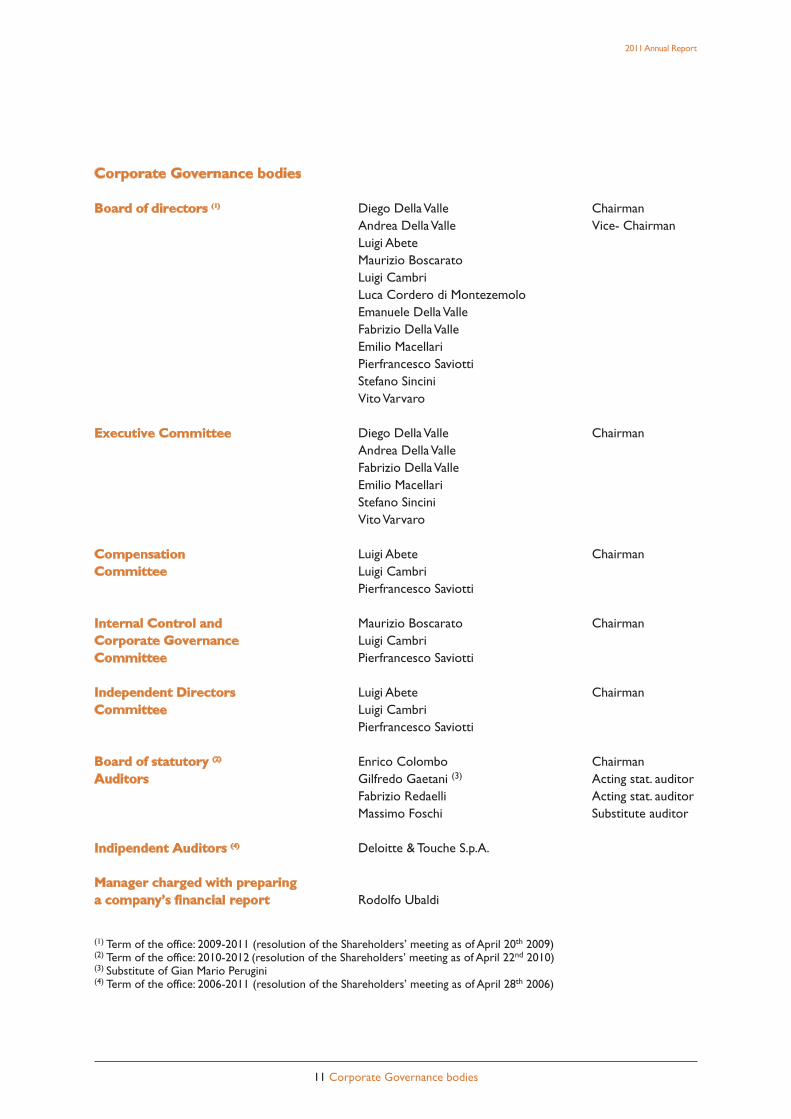

Corporate Governance bodies

Board of directors (1) Diego DellaValle ChairmanAndrea DellaValle Vice- ChairmanLuigi AbeteMaurizio BoscaratoLuigi CambriLuca Cordero di MontezemoloEmanuele DellaValleFabrizio DellaValleEmilio MacellariPierfrancesco SaviottiStefano SinciniVitoVarvaro

Executive Committee Diego DellaValle ChairmanAndrea DellaValleFabrizio DellaValleEmilio MacellariStefano SinciniVitoVarvaro

Compensation Luigi Abete ChairmanCommittee Luigi Cambri

Pierfrancesco Saviotti

Internal Control and Maurizio Boscarato ChairmanCorporate Governance Luigi CambriCommittee Pierfrancesco Saviotti

Independent Directors Luigi Abete ChairmanCommittee Luigi Cambri

Pierfrancesco Saviotti

Board of statutory (2) Enrico Colombo ChairmanAuditors Gilfredo Gaetani (3) Acting stat. auditor

Fabrizio Redaelli Acting stat. auditorMassimo Foschi Substitute auditor

Indipendent Auditors (4) Deloitte & Touche S.p.A.

Manager charged with preparinga company’s financial report Rodolfo Ubaldi

(1) Term of the office: 2009-2011 (resolution of the Shareholders’ meeting as of April 20th 2009)(2) Term of the office: 2010-2012 (resolution of the Shareholders’ meeting as of April 22nd 2010)(3) Substitute of Gian Mario Perugini(4) Term of the office: 2006-2011 (resolution of the Shareholders’ meeting as of April 28th 2006)

2011Annual Report

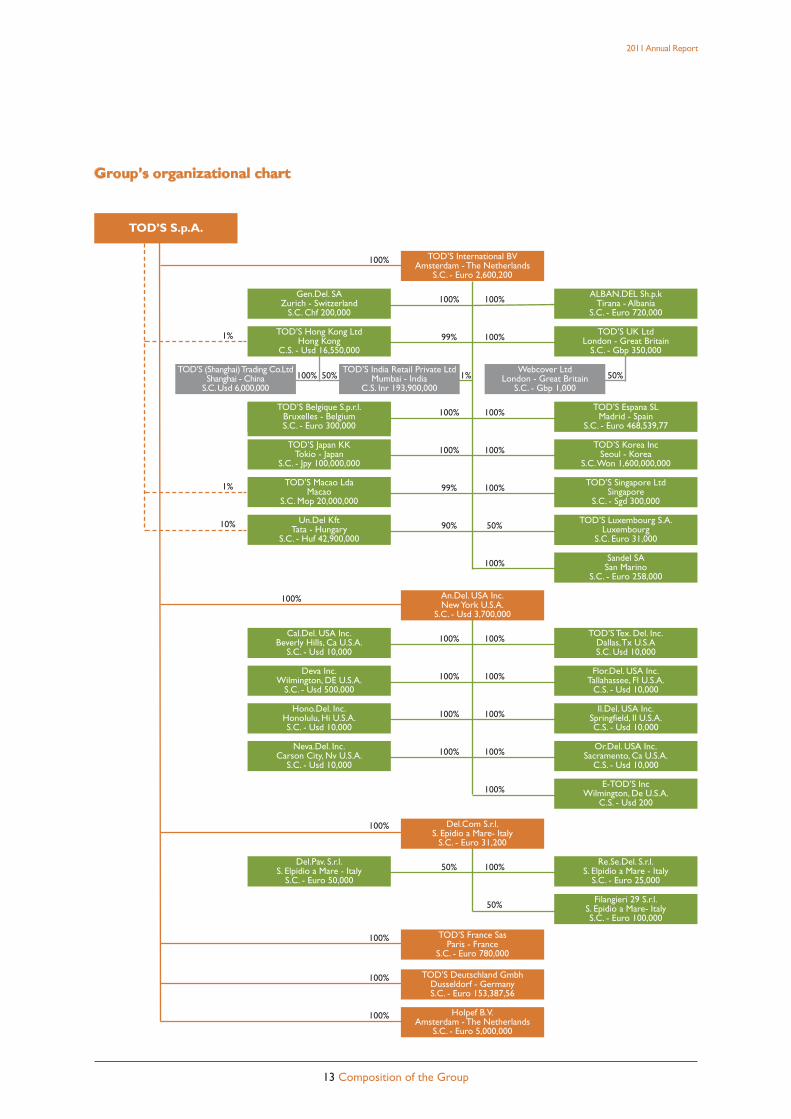

12 Composition of the Group

TOD’S S.p.A.Parent Company, owner of TOD’S, HOGAN andFAY brands and licensee of ROGERVIVIER brand.

Del.Com. S.r.l.Subholding for operation of national sub-sidiaries and DOS in Italy.

TOD’S International B.V.Subholding for operation of internationalsubsidiaries and DOS in The Netherlands.

An.Del. Usa Inc.Subholding for operation of subsidiaries inthe United States.

Del.Pav S.r.l.Company that operates DOS in Italy.

Filangieri 29 S.r.l.Company that operates DOS in Italy.

Gen.del. SACompany that operates DOS in Switzerland.

TOD’S Belgique S.p.r.l.Company that operates DOS in Belgium.

TOD’S Deutschland GmbhCompany that distributes and promotesproducts in Germany and manages DOS inGermany.

TOD’S Espana SLCompany that operates DOS in Spain.

TOD’S France SasCompany that distributes and promotesproducts in France and manages DOS inFrance.

TOD’S Luxembourg S.A.Company that operates DOS in Luxembourg.

TOD’S Hong Kong LtdCompany that distributes and promotesproducts in Far East and South Pacific andmanages DOS in Hong Kong.

TOD’S Japan KKCompany that operates DOS in Japan.

TOD’S Korea Inc.Company that operates DOS in Korea.

TOD’S Macao LtdCompany that operates DOS in Macao.

TOD’S Retail India Private LtdCompany that operates DOS in India.

TOD’S (Shanghai)Trading Co. LtdCompany that operates DOS in China.

TOD’S Singapore Pte LtdCompany that operates DOS in Singapore.

TOD’S UK LtdCompany that distributes and promotesproducts in Great Britain and manages DOSin Great Britain.

Webcover LtdCompany that operates DOS in Great Britain.

Cal.Del. Usa Inc.Company that operates DOS in California(USA).

Deva Inc.Company that distributes and promotesproducts in North America, and managesDOS in the State of NY (USA).

Flor. Del. Usa Inc.Company that operates DOS in Florida (USA).

Hono. Del. Inc.Company that operates DOS in Hawaii(USA).

Il. Del. Usa Inc.Company that operates DOS in Illinois(USA).

Neva. Del. Inc.Company that operates DOS in Nevada(USA).

Or. Del. Usa Inc.Company that operates DOS in California(USA).

TOD’STex. Del. Usa Inc.Company that operates DOS inTexas (USA).

E-TOD’S Inc.E-commerce company for US market.

Sandel SANot operating company.

Un.Del. KftProduction company.

Alban.Del Sh.p.k.Production company.

Holpaf B.V.Real estate company.

Re.Se.Del. S.r.l.Company for services.

TOD’S Group

2011Annual Report

13 Composition of the Group

Group’s organizational chart

TOD’S S.p.A.

Gen.Del. SAZurich - Switzerland

S.C. Chf 200,000

TOD’S Belgique S.p.r.l.Bruxelles - BelgiumS.C. - Euro 300,000

TOD’S Japan KKTokio - Japan

S.C. - Jpy 100,000,000

TOD’S Macao LdaMacao

S.C. Mop 20,000,000

Un.Del KftTata - Hungary

S.C. - Huf 42,900,000

Cal.Del. USA Inc.Beverly Hills, Ca U.S.A.

S.C. - Usd 10,000

Deva Inc.Wilmington, DE U.S.A.

S.C. - Usd 500,000

Hono.Del. Inc.Honolulu, Hi U.S.A.S.C. - Usd 10,000

Neva.Del. Inc.Carson City, Nv U.S.A.

S.C. - Usd 10,000

Del.Pav. S.r.l.S. Elpidio a Mare - Italy

S.C. - Euro 50,000

TOD’S Espana SLMadrid - Spain

S.C. - Euro 468,539,77

TOD’S Korea IncSeoul - Korea

S.C.Won 1,600,000,000

TOD’S Singapore LtdSingapore

S.C. - Sgd 300,000

TOD’S Luxembourg S.A.Luxembourg

S.C. Euro 31,000

Sandel SASan Marino

S.C. - Euro 258,000

TOD’S Tex. Del. Inc.Dallas,Tx U.S.AS.C. Usd 10,000

Flor.Del. USA Inc.Tallahassee, Fl U.S.A.

C.S. - Usd 10,000

Il.Del. USA Inc.Springfield, Il U.S.A.C.S. - Usd 10,000

Or.Del. USA Inc.Sacramento, Ca U.S.A.

C.S. - Usd 10,000

Re.Se.Del. S.r.l.S. Elpidio a Mare - Italy

S.C. - Euro 25,000

Filangieri 29 S.r.l.S. Epidio a Mare- ItalyS.C. - Euro 100,000

TOD’S International BVAmsterdam - The Netherlands

S.C. - Euro 2,600,200

TOD’S Deutschland GmbhDusseldorf - GermanyS.C. - Euro 153,387,56

Holpef B.V.Amsterdam - The Netherlands

S.C. - Euro 5,000,000

ALBAN.DEL Sh.p.kTirana - Albania

S.C. - Euro 720,000

TOD’S India Retail Private LtdMumbai - India

C.S. Inr 193,900,000

An.Del. USA Inc.NewYork U.S.A.

S.C. - Usd 3,700,000

Del.Com S.r.l.S. Epidio a Mare- Italy

S.C. - Euro 31,200

100%

99%

100%

100%

99%

90%

1%

1%

10%

100%

100%

100%

100%

E-TOD’S IncWilmington, De U.S.A.

C.S. - Usd 200100%

50%

100%

100%

100%

100%

100%

50%

100%

100%

100%

100%

100%

100%

50%

100%

TOD’S France SasParis - France

S.C. - Euro 780,000

100%

100%

100%

100%

TOD’S (Shanghai)Trading Co.LtdShanghai - China

S.C.Usd 6,000,000

TOD’S UK LtdLondon - Great Britain

S.C. - Gbp 350,000

TOD’S Hong Kong LtdHong Kong

C.S. - Usd 16,550,000

100% 50% 1%Webcover Ltd

London - Great BritainS.C. - Gbp 1,000

50%

100%

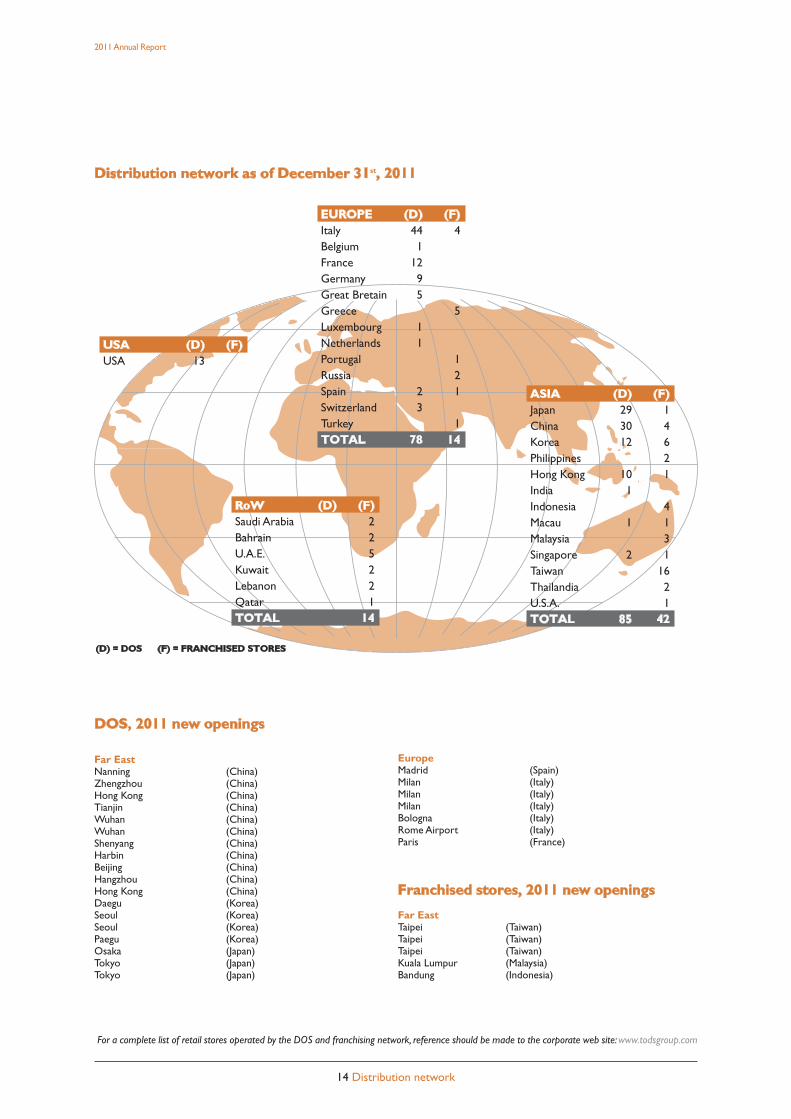

Distribution network as of December 31st, 2011

2011Annual Report

14 Distribution network

DOS, 2011 new openings

Far EastNanning (China)Zhengzhou (China)Hong Kong (China)Tianjin (China)Wuhan (China)Wuhan (China)Shenyang (China)Harbin (China)Beijing (China)Hangzhou (China)Hong Kong (China)Daegu (Korea)Seoul (Korea)Seoul (Korea)Paegu (Korea)Osaka (Japan)Tokyo (Japan)Tokyo (Japan)

EuropeMadrid (Spain)Milan (Italy)Milan (Italy)Milan (Italy)Bologna (Italy)Rome Airport (Italy)Paris (France)

Franchised stores, 2011 new openings

Far EastTaipei (Taiwan)Taipei (Taiwan)Taipei (Taiwan)Kuala Lumpur (Malaysia)Bandung (Indonesia)

For a complete list of retail stores operated by the DOS and franchising network, reference should be made to the corporate web site:www.todsgroup.com

EUROPE (D) (F)Italy 44 4Belgium 1France 12Germany 9Great Bretain 5Greece 5Luxembourg 1Netherlands 1Portugal 1Russia 2Spain 2 1Switzerland 3Turkey 1TOTAL 78 14

RoW (D) (F)Saudi Arabia 2Bahrain 2U.A.E. 5Kuwait 2Lebanon 2Qatar 1TOTAL 14

ASIA (D) (F)Japan 29 1China 30 4Korea 12 6Philippines 2Hong Kong 10 1India 1Indonesia 4Macau 1 1Malaysia 3Singapore 2 1Taiwan 16Thailandia 2U.S.A. 1TOTAL 85 42

USA (D) (F)USA 13

(D) = DOS (F) = FRANCHISED STORES

2011Annual Report

15 Key consolidated financial figures

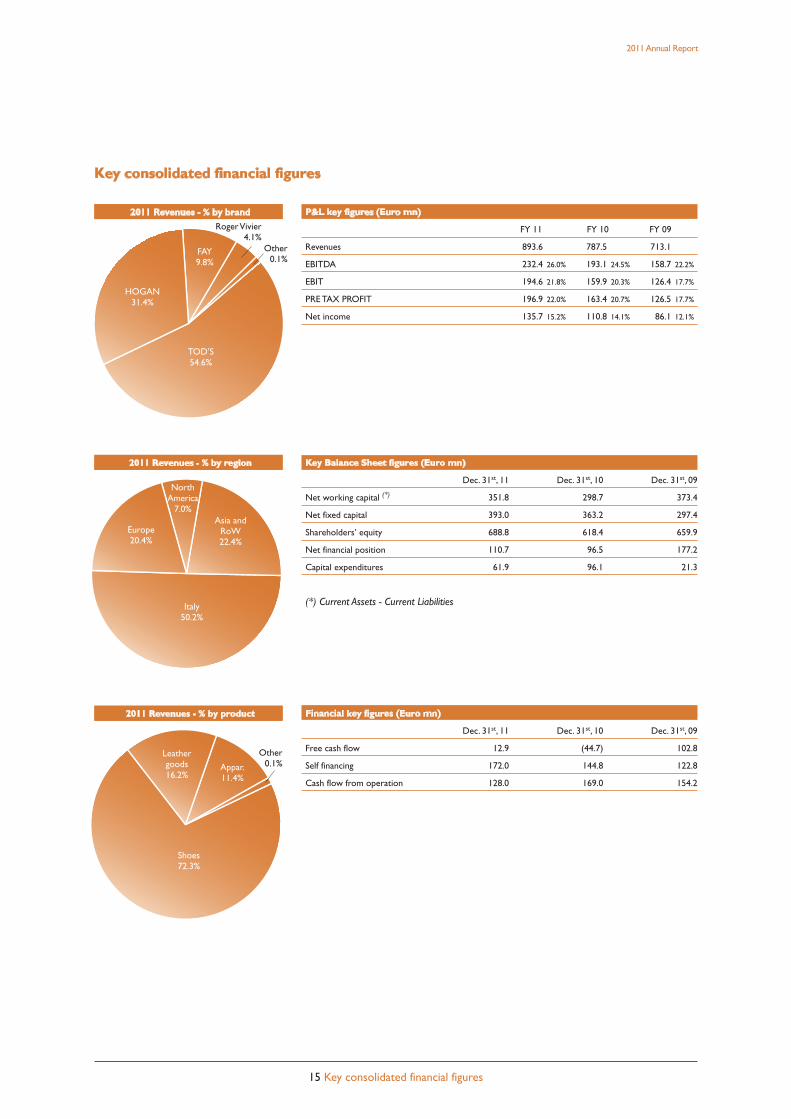

Key consolidated financial figures

P&L key figures (Euro mn)

FY 11 FY 10 FY 09

Revenues 893.6 787.5 713.1

EBITDA 232.4 26.0% 193.1 24.5% 158.7 22.2%

EBIT 194.6 21.8% 159.9 20.3% 126.4 17.7%

PRE TAX PROFIT 196.9 22.0% 163.4 20.7% 126.5 17.7%

Net income 135.7 15.2% 110.8 14.1% 86.1 12.1%

Key Balance Sheet figures (Euro mn)

Dec. 31st, 11 Dec. 31st, 10 Dec. 31st, 09

Net working capital (*) 351.8 298.7 373.4

Net fixed capital 393.0 363.2 297.4

Shareholders’ equity 688.8 618.4 659.9

Net financial position 110.7 96.5 177.2

Capital expenditures 61.9 96.1 21.3

(*) Current Assets - Current Liabilities

Financial key figures (Euro mn)

Dec. 31st, 11 Dec. 31st, 10 Dec. 31st, 09

Free cash flow 12.9 (44.7) 102.8

Self financing 172.0 144.8 122.8

Cash flow from operation 128.0 169.0 154.2

2011 Revenues - % by brand

2011 Revenues - % by region

2011 Revenues - % by product

TOD’S54.6%

HOGAN31.4%

FAY9.8%

RogerVivier4.1%

Europe20.4%

NorthAmerica

7.0%Asia and

RoW22.4%

Italy50.2%

Leathergoods16.2%

Appar.11.4%

Shoes72.3%

Other0.1%

Other0.1%

2011Annual Report

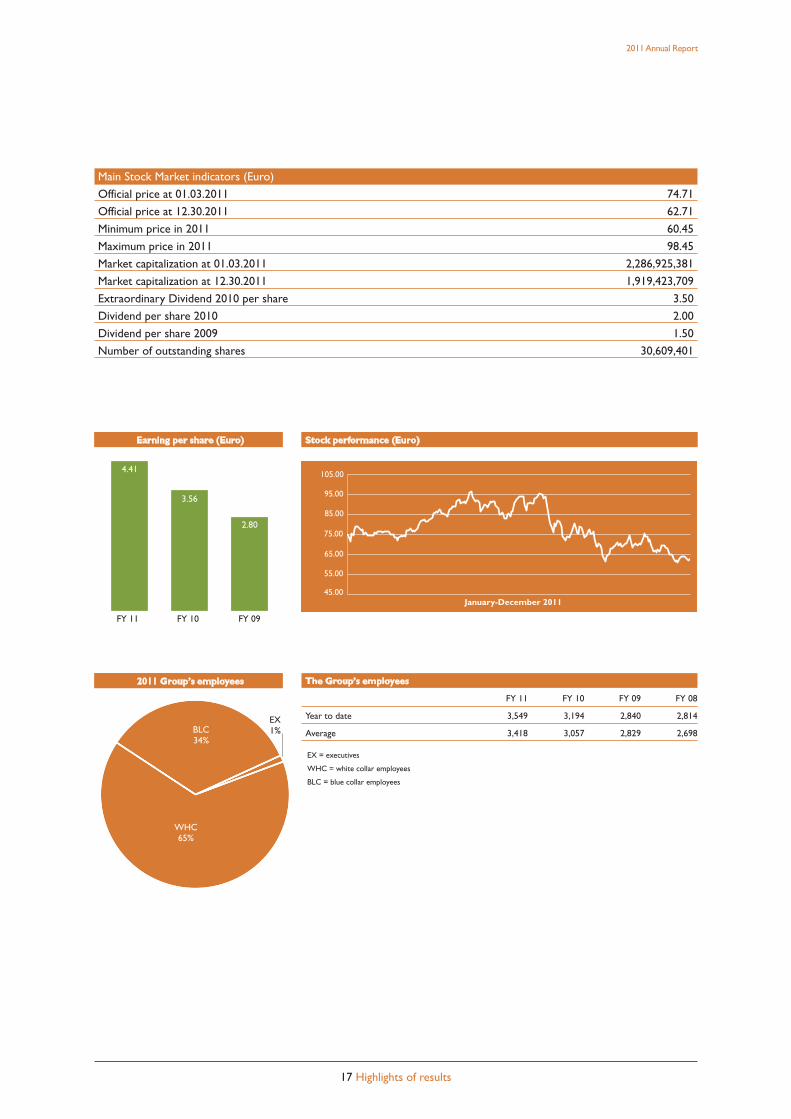

16 Highlights of results

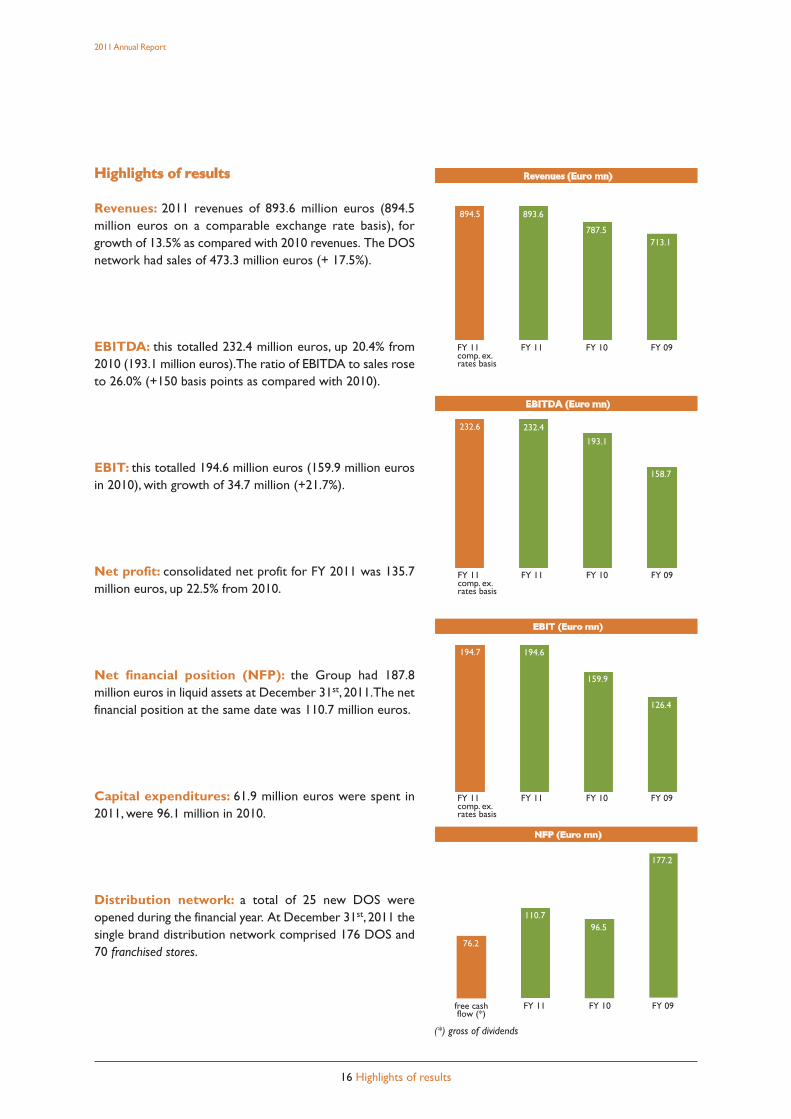

Highlights of results

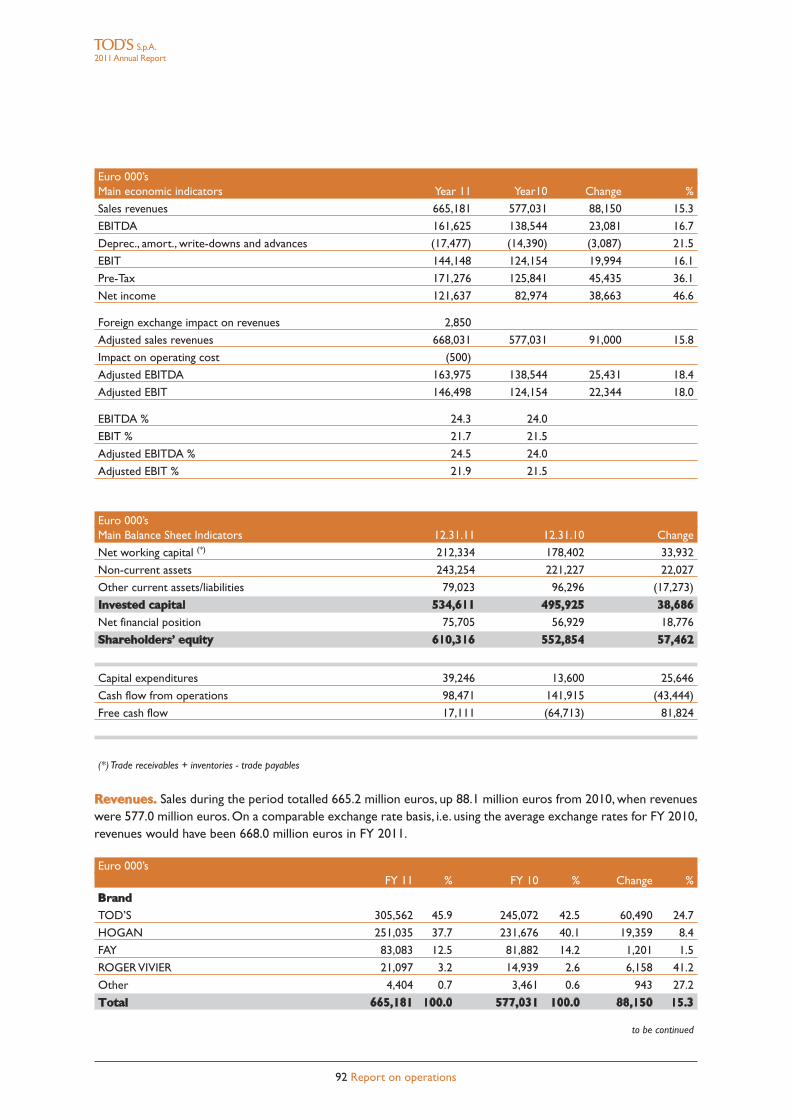

Revenues: 2011 revenues of 893.6 million euros (894.5million euros on a comparable exchange rate basis), forgrowth of 13.5% as compared with 2010 revenues. The DOSnetwork had sales of 473.3 million euros (+ 17.5%).

EBITDA: this totalled 232.4 million euros, up 20.4% from2010 (193.1 million euros).The ratio of EBITDA to sales roseto 26.0% (+150 basis points as compared with 2010).

EBIT: this totalled 194.6 million euros (159.9 million eurosin 2010), with growth of 34.7 million (+21.7%).

Net profit: consolidated net profit for FY 2011 was 135.7million euros, up 22.5% from 2010.

Net financial position (NFP): the Group had 187.8million euros in liquid assets at December 31st, 2011.The netfinancial position at the same date was 110.7 million euros.

Capital expenditures: 61.9 million euros were spent in2011, were 96.1 million in 2010.

Distribution network: a total of 25 new DOS wereopened during the financial year. At December 31st, 2011 thesingle brand distribution network comprised 176 DOS and70 franchised stores.

Revenues (Euro mn)

FY 11 FY 11 FY 10 FY 09comp. ex.rates basis

893.6894.5

787.5713.1

EBITDA (Euro mn)

FY 11 FY 11 FY 10 FY 09comp. ex.rates basis

232.4232.6

193.1

158.7

EBIT (Euro mn)

FY 11 FY 11 FY 10 FY 09comp. ex.rates basis

194.6194.7

159.9

126.4

NFP (Euro mn)

free cash FY 11 FY 10 FY 09flow (*)

110.7

76.2

96.5

177.2

(*) gross of dividends

2011Annual Report

17 Highlights of results

The Group’s employees

FY 11 FY 10 FY 09 FY 08

Year to date 3,549 3,194 2,840 2,814

Average 3,418 3,057 2,829 2,698

EX = executives

WHC = white collar employees

BLC = blue collar employees

Earning per share (Euro) Stock performance (Euro)

FY 11 FY 10 FY 09

3.56

4.41

2.80

2011 Group’s employees

BLC34%

WHC65%

EX1%

Main Stock Market indicators (Euro)

Official price at 01.03.2011 74.71

Official price at 12.30.2011 62.71

Minimum price in 2011 60.45

Maximum price in 2011 98.45

Market capitalization at 01.03.2011 2,286,925,381

Market capitalization at 12.30.2011 1,919,423,709

Extraordinary Dividend 2010 per share 3.50

Dividend per share 2010 2.00

Dividend per share 2009 1.50

Number of outstanding shares 30,609,401

45.00

55.00

65.00

75.00

85.00

95.00

105.00

January-December 2011

[THIS PAGE HAS BEEN INTENTIONALLY LEFT BLANK]

18 2011 Annual Report

HOGAN.COM

TOD’S GROUP – CONSOLIDATED FINANCIAL STATEMENTSAS AT DECEMBER 31ST 2011

REPORT ON OPERATIONS

Group2011Annual Report

29 Report on operations

Introduction

The Report of the Board of Directors on Operations is based on the TOD’S Group Consolidated FinancialStatements at December 31st, 2011, prepared in accordance with IAS/IFRS (International Accounting Standards –IAS, and International Financial Reporting Standards – IFRS) issued by the IASB and approved by the EuropeanUnion at the same date. IAS/IFRS refers also to all revised International Accounting Standards (IAS) and all interpre-tative documents issued by the IFRIC (International Financial Reporting Interpretations Committee), previously nomi-nated Standing Interpretations Committee (SIC).The Consolidated Financial Statements have been prepared on the assumption that the Group can operate as agoing concern.The Group believes that there are no asset, liability, financial or organizational indicators of mate-rial uncertainties, as defined in paragraph 25 of IAS 1 on business continuity.The Report on Operations must be read together with the Financial Statements and Notes to the FinancialStatements,which are an integral part of the 2011 ConsolidatedAnnual Report.The Report on Operations also in-cludes the additional information required by CONSOB,pursuant to the orders issued in implementation ofArticle9 of Legislative Decree 38/2005 (Resolutions 15519 and 15520 of July 27th, 2006 and memorandum DEM/6064293of July 28th, 2006, as well as all subsequent notices containing provisions regarding financial disclosures.

Alternative indicators of performances

In order to strip the effects of changes in exchange rates with respect to the average values for the previous yearfrom the results for the 2011 financial year, the typical economic reference indicators (Revenues,EBITDA and EBIT)have been recalculated by applying the average exchange rates for 2010, rendering them fully comparable withthose for the previous reference period. Note that on the one hand, these principles for measurement of busi-ness performance represent a key to interpretation of results not envisaged in IFRSs, and on the other hand, mustnot be considered as substitutes for what is set out in those standards.

Group’s activity

The TOD’S Group operates in the luxury sector under its proprietary brands (TOD’S, HOGAN and FAY) and li-censed brands (ROGERVIVIER). It actively creates, produces and distributes shoes, leather goods and accessories,and apparel.The firm’s mission is to offer global customers top-quality products that satisfy their functional re-quirements and aspirations.

Development of production. The Group’s production structure is based on complete control of the productionprocess, from creation of the collections to production and then distribution of the products.This approach isconsidered key to assuring the prestige of its brands.Shoes and leather goods are produced in Group-owned plants,with partial outsourcing to specialized workshops.All of these outsourcers are located in areas with a strong tradition of shoe and leather good production.Thispreference reflects the fact that an extremely high standard of professional quality is required to make these items,with a significantly high level of added value contributed to the final product by manual work.The Group relies exclusively on selected specialized outsourcers, which enables it to exploit their respective spe-cializations in crafting the individual products sold as part of the apparel line.

Distribution structure. The prestige of the Group’s brands and the high degree of specialization necessary tooffer the respective products to customers entails distribution through a network of similarly specialized stores.Accordingly, the Group relies principally on three channels:DOS (directly operated stores), franchised retail stores,and a series of selected, independent multibrand stores.The Group’s strategy is focused on development of the DOS and franchising networks, given that these channelsoffer greater control and more faithful transmission of the individual brands. It is also clear that, in particular mar-

Group2011Annual Report

30 Report on operations

ket situations, distribution through independent multibrand stores is more efficient.This channel is of key impor-tance to the Group.

Group’s brands

The Tod’s brand is known for shoes and luxury leather goods, with styles that have become icons of modern liv-ing;Tod’s is known in the luxury goods sector as a symbol of the perfect combination of tradition, quality andmodernity. Each product is hand-crafted with highly-skilled techniques, intended, after laborious reworking, to be-come an exclusive, recognisable, modern and practical object. Some styles, like the Driving Shoe and the D bag,are cherished by celebrities and ordinary people worldwide, and have become icons and forerunners of a new con-cept of elegance, for both women and men.

Begun in the 80s with shoe collections for women, men and children, the Hogan brand now also crafts variousleather goods items.The Hogan brand is distinctive for high quality, functionality and design. Every product stemsfrom a highly skilled design technique and is created using quality materials with a particular passion for detailsand a search for perfection.Hogan products are the highest expression of a “new luxury” lifestyle.Hogan is meantfor someone who cherishes the type of luxury associated with product excellence, innovative original design andconsummate practicality.The Traditional and the Interactive shoe styles endure as continuing “best sellers”.

FAY is a brand created in the mid 80s with a product range of high quality casual wear.The brand is known for itsquality craftsmanship, for the excellence of its materials, a meticulous attention to craft details and its high function-ality without sacrificing style and quality. FAY products are wearable everywhere: from the stadium to the office, inurban areas and in the countryside.The line, which has seasonal men’s, women’s and junior’s collections, focuses onclassic evergreen styles, continuously modified and refreshed with innovative and recognisably eye-catching design.

The Fabergé of shoes, and creator of the first stiletto heel in the 1950’s, Roger Vivier designed extravagant andluxuriously decorated shoes that he described as being “sculptures.” The artistic heritage and excellent tradition-al roots of theVivier fashion house have been revived through acquisition of the brand by Diego DellaValle.Underthe management of Creative Director Bruno Frisoni,Vivier’s work and vision endure. New chapters are added tothis unique life story every year, which goes beyond expertise in the craft of shoe making to include handbags,small leather goods, jewellery and sunglasses.

Group2011Annual Report

31 Report on operations

Organizational structure of the Group

The Group’s organisational configuration rotates around TOD’S S.p.A. that is at the heart of the Group’s organi-sation, its parent company that owns the TOD’S, HOGAN and FAY brands, holds the licenses of the ROGERVIVIER, and manages the Group’s production and distribution.Through a series of sub-holdings, the organisationis rounded out by a series of commercial companies that are delegated complete responsibility for retail distri-bution through the DOS network.Certain of them, strategically located on international markets, are assigned ma-jor roles in product distribution, marketing and promotion, and public relations processes along the “value chain”,while simultaneously guaranteeing the uniform image that Group brands must have worldwide.

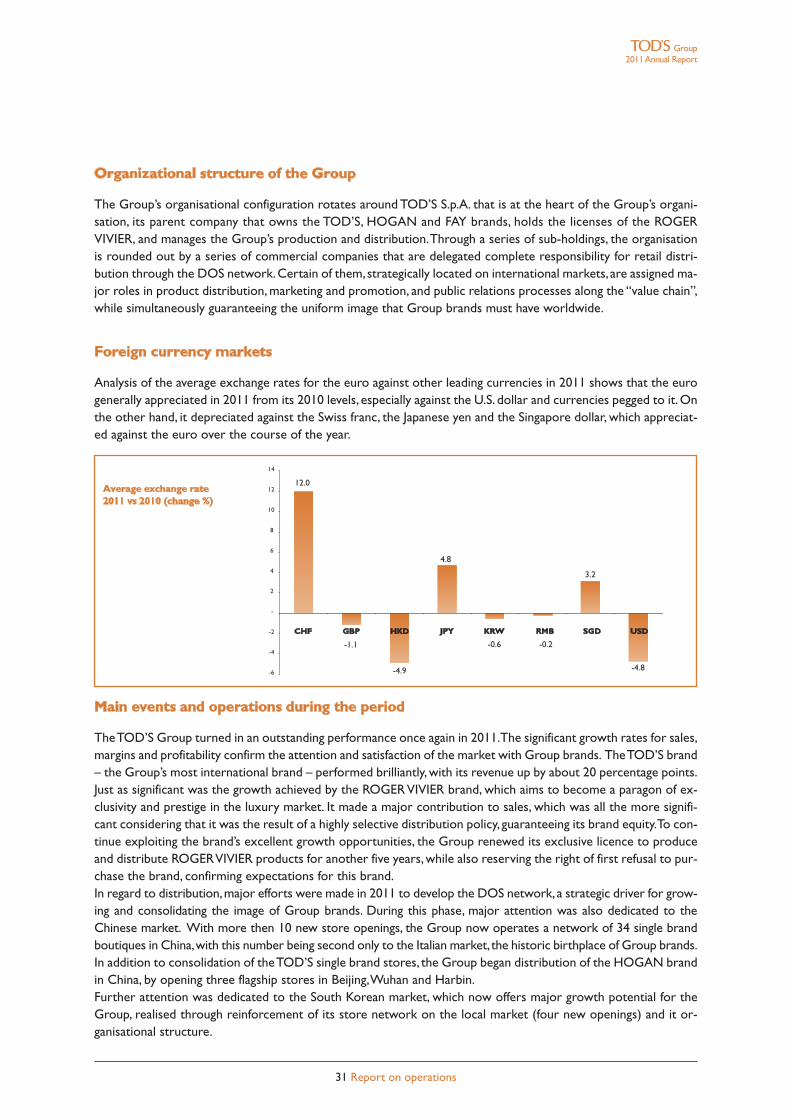

Foreign currency markets

Analysis of the average exchange rates for the euro against other leading currencies in 2011 shows that the eurogenerally appreciated in 2011 from its 2010 levels, especially against the U.S. dollar and currencies pegged to it.Onthe other hand, it depreciated against the Swiss franc, the Japanese yen and the Singapore dollar, which appreciat-ed against the euro over the course of the year.

Main events and operations during the period

TheTOD’S Group turned in an outstanding performance once again in 2011.The significant growth rates for sales,margins and profitability confirm the attention and satisfaction of the market with Group brands. TheTOD’S brand– the Group’s most international brand – performed brilliantly,with its revenue up by about 20 percentage points.Just as significant was the growth achieved by the ROGERVIVIER brand, which aims to become a paragon of ex-clusivity and prestige in the luxury market. It made a major contribution to sales, which was all the more signifi-cant considering that it was the result of a highly selective distribution policy, guaranteeing its brand equity.To con-tinue exploiting the brand’s excellent growth opportunities, the Group renewed its exclusive licence to produceand distribute ROGERVIVIER products for another five years, while also reserving the right of first refusal to pur-chase the brand, confirming expectations for this brand.In regard to distribution,major efforts were made in 2011 to develop the DOS network, a strategic driver for grow-ing and consolidating the image of Group brands. During this phase, major attention was also dedicated to theChinese market. With more then 10 new store openings, the Group now operates a network of 34 single brandboutiques in China,with this number being second only to the Italian market, the historic birthplace of Group brands.In addition to consolidation of theTOD’S single brand stores, the Group began distribution of the HOGAN brandin China, by opening three flagship stores in Beijing,Wuhan and Harbin.Further attention was dedicated to the South Korean market, which now offers major growth potential for theGroup, realised through reinforcement of its store network on the local market (four new openings) and it or-ganisational structure.

-6

-4

-2

-

2

4

6

8

10

12

14

Average exchange rate2011 vs 2010 (change %)

GBP HKD JPY KRW RMB SGD USDCHF

12.0

-1.1

-4.9

4.8

-0.6 -0.2

3.2

-4.8

Group2011Annual Report

32 Report on operations

The second part of the year was marked by the launch of a project to set up an e-commerce platform.The “golive,” whose timing will vary from market to market, is scheduled to coincide with the Spring-Summer 2012 col-lection. In the first phase, it will involve the TOD’S brand on the United States market.The 2011 financial year was also characterised by the Group’s major commitment to social responsibility. Its twomost important initiatives were dedicated to the protection and promotion of Italian heritage.The first of these projects involved full financing, as sole sponsor, of urgent restoration work on the Coliseum.Following the agreement reached on January 21st, 2011 with the Ministry of Cultural Affairs and the SpecialArchaeological Service in Rome, the Group committed itself to pay 25 million euros for restoration of this mon-ument, which symbolises the history and culture of Italy.This commitment will be spread out over the entire du-ration of the restoration work.The Special Archaeological Service of Rome will remain responsible for planning(currently underway) and executing that work.Following a resolution by the General Meeting of the Fondazione Teatro alla Scala,TOD’S S.p.A. acquired the sta-tus of Permanent Founding Member of the Foundation on May 16th, 2011. By donating 5.2 million euros to theFoundation, to be paid over four years, the company manifested its intention to support the activity of this the-atre.The aim of this contribution is that La Scala continue affirming its enormous prestige and organisational ex-cellence around the world, and preserve its status as a global paragon of products “made in Italy”.

The Group’s results in 2011

The Group turned in an excellent performance in 2011 as measured by all leading economic indicators.The re-sults that it has achieved are even more important given the general volatility prevailing on the market and, aboveall, the extremely challenging basis of comparison for the Group,which unlike most of its peers in the luxury goodssector as a whole, has continued to grow, even after the crisis that exploded at the end of 2008.Revenues during the year grew by 106.1 million euros, from 787.5 million euros in 2010 (+13.5%) to 893.6 millioneuros in 2011.The foreign exchange effect did not have a particular significant impact on Group sales (894.5 mil-lion euros on a comparable exchange rate basis). Growth as measured by operating margins was even stronger.EBITDA and EBIT totalled 232.4 million euros and 194.6 million euros, respectively (FY 2010: EBITDA and EBITwere 193.1 million euros and 159.9 million euros, respectively), growing by more than 20 percentage points.Net profit rose sharply: consolidated net income was 135.7 million euros, up 22.5% from the 110.8 million eurosreported in FY 2010.

Euro 000’sMain economic indicators Year 11 Year 10 Change %Sales revenues 893,638 787,539 106,099 13.5EBITDA 232,417 193,059 39,358 20.4Deprec., amort., write-downs and advances (37,787) (33,115) (4,672) 14.1EBIT 194,630 159,944 34,686 21.7Pre-Tax 196,886 163,352 33,534 20.5Consolidated net profit 135,688 110,786 24,902 22.5

Foreign exchange impact on revenues 821Adjusted Sales revenues 894,459 787,539 106,920 13.6Foreign exchange impact on operating costs (590)Adjusted EBITDA 232,648 193,059 39,589 20.5Foreign exchange impact on deprec. & amort. (130)Adjusted EBIT 194,731 159,944 34,787 21.7

EBITDA % 26.0 24.5EBIT % 21.8 20.3Adjusted EBITDA % 26.0 24.5Adjusted EBIT % 21.8 20.3Tax rate % 31.1 32.2

Group2011Annual Report

33 Report on operations

Euro 000’sMain Balance Sheet Indicators 12.31.11 12.31.10 Change

Net working capital (*) 226,766 192,688 34,078

Non current assets 393,004 363,186 29,818

Other current assets/liabilities (41,732) (33,928) (7,804)

Net assets held for sale - - -

Invested capital 578,038 521,946 56,092Net financial position 110,749 96,495 14,254

Shareholders’ equity 688,787 618,441 70,346

Capital expenditures 61,882 96,067 (34,185)

Cash flow from operations 128,040 168,950 (40,910)

Free cash flow 12,857 (44,708) 57,565

(*)Trade receivables + inventories - trade payables

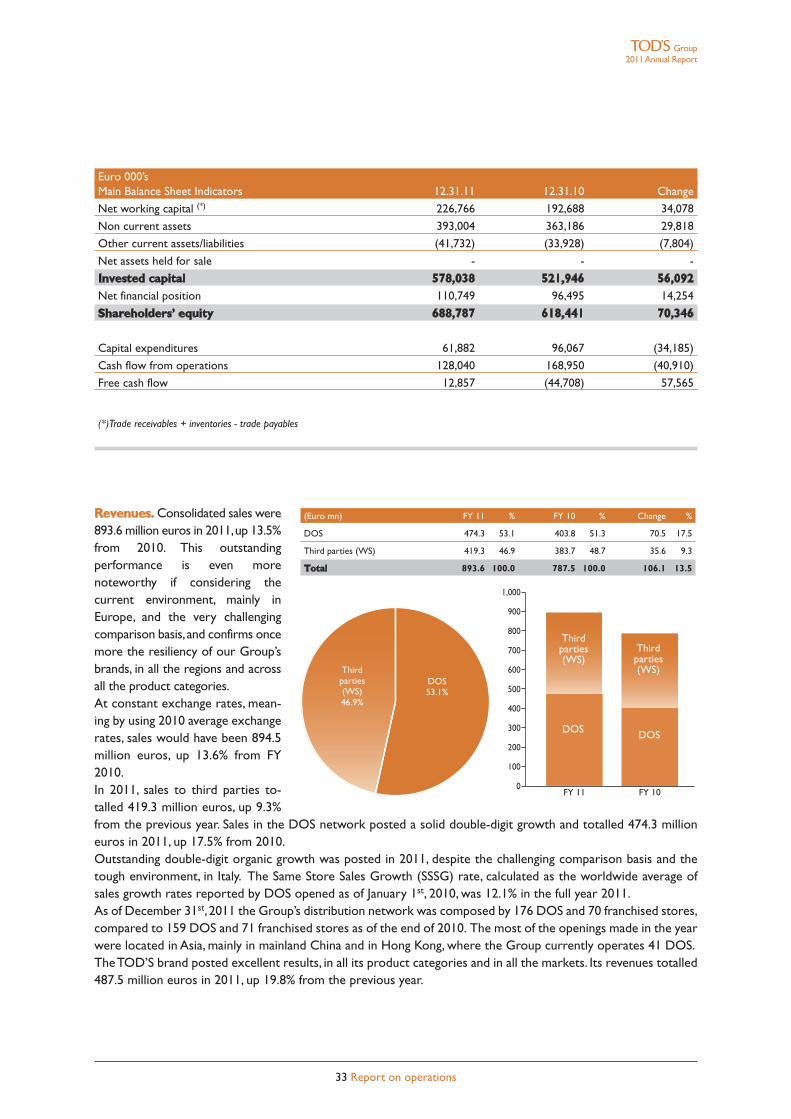

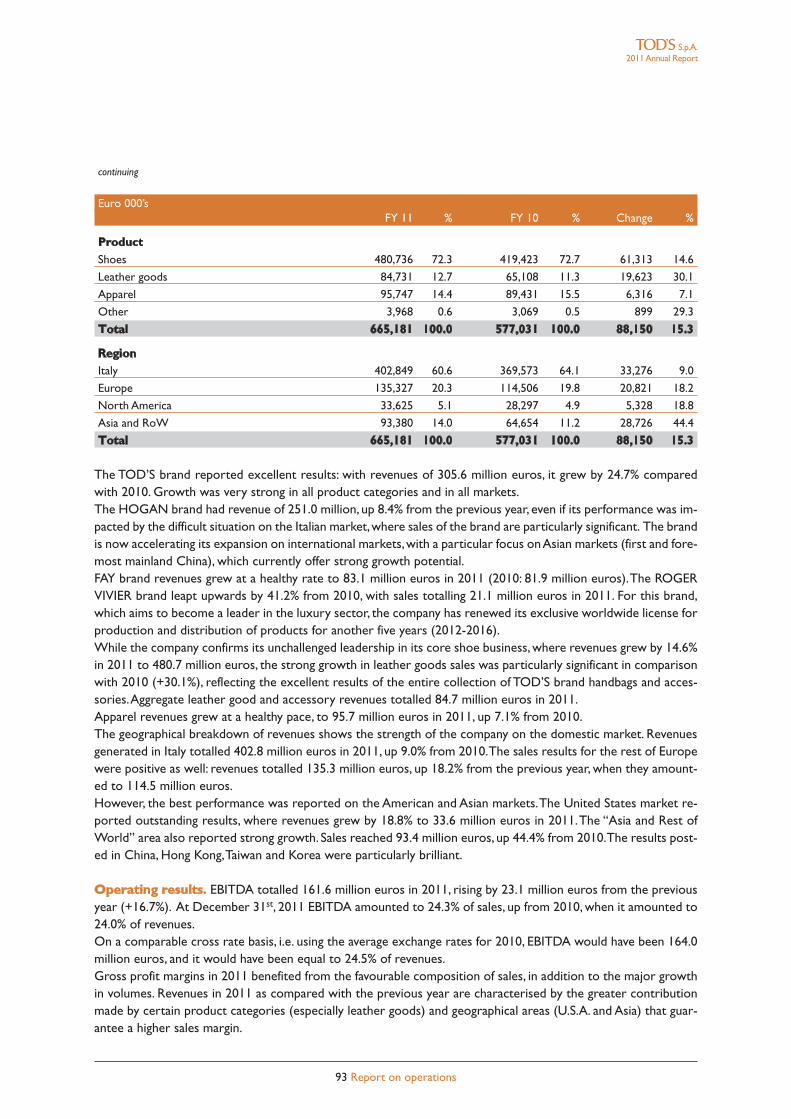

Revenues. Consolidated sales were893.6 million euros in 2011,up 13.5%from 2010. This outstandingperformance is even morenoteworthy if considering thecurrent environment, mainly inEurope, and the very challengingcomparison basis,and confirms oncemore the resiliency of our Group’sbrands, in all the regions and acrossall the product categories.At constant exchange rates, mean-ing by using 2010 average exchangerates, sales would have been 894.5million euros, up 13.6% from FY2010.In 2011, sales to third parties to-talled 419.3 million euros, up 9.3%from the previous year. Sales in the DOS network posted a solid double-digit growth and totalled 474.3 millioneuros in 2011, up 17.5% from 2010.Outstanding double-digit organic growth was posted in 2011, despite the challenging comparison basis and thetough environment, in Italy. The Same Store Sales Growth (SSSG) rate, calculated as the worldwide average ofsales growth rates reported by DOS opened as of January 1st, 2010, was 12.1% in the full year 2011.As of December 31st, 2011 the Group’s distribution network was composed by 176 DOS and 70 franchised stores,compared to 159 DOS and 71 franchised stores as of the end of 2010. The most of the openings made in the yearwere located in Asia, mainly in mainland China and in Hong Kong, where the Group currently operates 41 DOS.TheTOD’S brand posted excellent results, in all its product categories and in all the markets. Its revenues totalled487.5 million euros in 2011, up 19.8% from the previous year.

100

200

300

400

500

600

700

900

FY 11 FY 10

800

1,000

0

(Euro mn) FY 11 % FY 10 % Change %

DOS 474.3 53.1 403.8 51.3 70.5 17.5

Third parties (WS) 419.3 46.9 383.7 48.7 35.6 9.3

Total 893.6 100.0 787.5 100.0 106.1 13.5

Thirdparties(WS)46.9%

Thirdparties(WS)

DOS DOS

Thirdparties(WS)

DOS53.1%

Group2011Annual Report

34 Report on operations

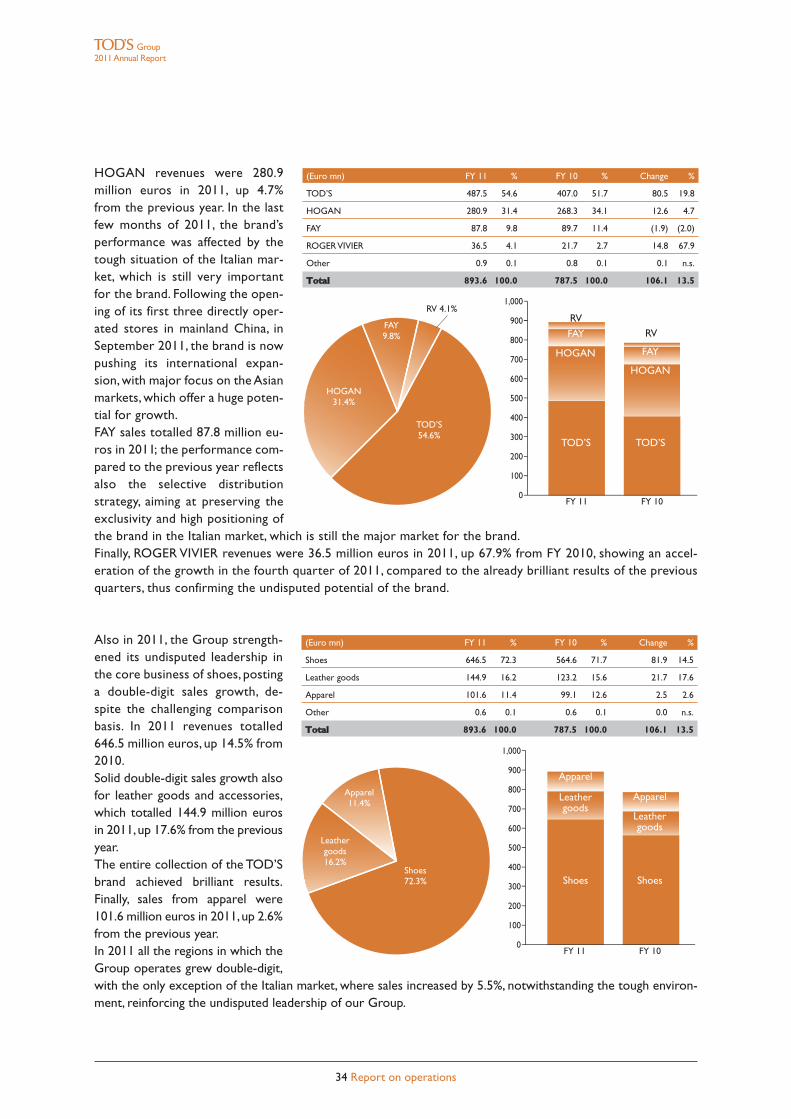

HOGAN revenues were 280.9million euros in 2011, up 4.7%from the previous year. In the lastfew months of 2011, the brand’sperformance was affected by thetough situation of the Italian mar-ket, which is still very importantfor the brand. Following the open-ing of its first three directly oper-ated stores in mainland China, inSeptember 2011, the brand is nowpushing its international expan-sion, with major focus on the Asianmarkets, which offer a huge poten-tial for growth.FAY sales totalled 87.8 million eu-ros in 2011; the performance com-pared to the previous year reflectsalso the selective distributionstrategy, aiming at preserving theexclusivity and high positioning ofthe brand in the Italian market, which is still the major market for the brand.Finally, ROGER VIVIER revenues were 36.5 million euros in 2011, up 67.9% from FY 2010, showing an accel-eration of the growth in the fourth quarter of 2011, compared to the already brilliant results of the previousquarters, thus confirming the undisputed potential of the brand.

Also in 2011, the Group strength-ened its undisputed leadership inthe core business of shoes, postinga double-digit sales growth, de-spite the challenging comparisonbasis. In 2011 revenues totalled646.5 million euros, up 14.5% from2010.Solid double-digit sales growth alsofor leather goods and accessories,which totalled 144.9 million eurosin 2011,up 17.6% from the previousyear.The entire collection of the TOD’Sbrand achieved brilliant results.Finally, sales from apparel were101.6 million euros in 2011,up 2.6%from the previous year.In 2011 all the regions in which theGroup operates grew double-digit,with the only exception of the Italian market, where sales increased by 5.5%, notwithstanding the tough environ-ment, reinforcing the undisputed leadership of our Group.

100

200

300

400

500

600

700

900

FY 11 FY 10

800

1,000

0

(Euro mn) FY 11 % FY 10 % Change %

TOD’S 487.5 54.6 407.0 51.7 80.5 19.8

HOGAN 280.9 31.4 268.3 34.1 12.6 4.7

FAY 87.8 9.8 89.7 11.4 (1.9) (2.0)

ROGERVIVIER 36.5 4.1 21.7 2.7 14.8 67.9

Other 0.9 0.1 0.8 0.1 0.1 n.s.

Total 893.6 100.0 787.5 100.0 106.1 13.5

TOD’S54.6%

HOGAN31.4%

FAY9.8%

RV 4.1%RV

HOGAN

TOD’S

FAY

FAY

HOGAN

TOD’S

RV

100

200

300

400

500

600

700

900

FY 11 FY 10

800

1,000

0

(Euro mn) FY 11 % FY 10 % Change %

Shoes 646.5 72.3 564.6 71.7 81.9 14.5

Leather goods 144.9 16.2 123.2 15.6 21.7 17.6

Apparel 101.6 11.4 99.1 12.6 2.5 2.6

Other 0.6 0.1 0.6 0.1 0.0 n.s.

Total 893.6 100.0 787.5 100.0 106.1 13.5

Apparel

Leathergoods

Shoes

Apparel

Leathergoods

Shoes

Apparel11.4%

Shoes72.3%

Leathergoods16.2%

Group2011Annual Report

35 Report on operations

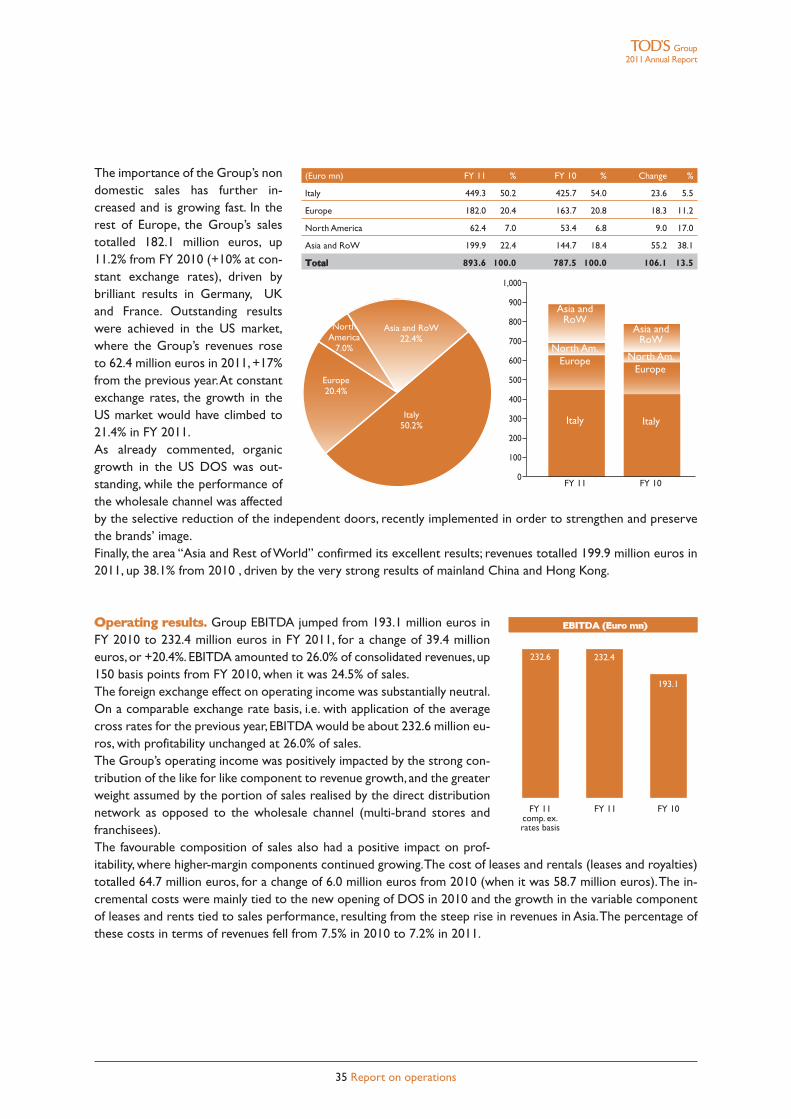

The importance of the Group’s nondomestic sales has further in-creased and is growing fast. In therest of Europe, the Group’s salestotalled 182.1 million euros, up11.2% from FY 2010 (+10% at con-stant exchange rates), driven bybrilliant results in Germany, UKand France. Outstanding resultswere achieved in the US market,where the Group’s revenues roseto 62.4 million euros in 2011, +17%from the previous year.At constantexchange rates, the growth in theUS market would have climbed to21.4% in FY 2011.As already commented, organicgrowth in the US DOS was out-standing, while the performance ofthe wholesale channel was affectedby the selective reduction of the independent doors, recently implemented in order to strengthen and preservethe brands’ image.Finally, the area “Asia and Rest of World” confirmed its excellent results; revenues totalled 199.9 million euros in2011, up 38.1% from 2010 , driven by the very strong results of mainland China and Hong Kong.

Operating results. Group EBITDA jumped from 193.1 million euros inFY 2010 to 232.4 million euros in FY 2011, for a change of 39.4 millioneuros,or +20.4%. EBITDA amounted to 26.0% of consolidated revenues, up150 basis points from FY 2010, when it was 24.5% of sales.The foreign exchange effect on operating income was substantially neutral.On a comparable exchange rate basis, i.e. with application of the averagecross rates for the previous year, EBITDA would be about 232.6 million eu-ros, with profitability unchanged at 26.0% of sales.The Group’s operating income was positively impacted by the strong con-tribution of the like for like component to revenue growth, and the greaterweight assumed by the portion of sales realised by the direct distributionnetwork as opposed to the wholesale channel (multi-brand stores andfranchisees).The favourable composition of sales also had a positive impact on prof-itability, where higher-margin components continued growing.The cost of leases and rentals (leases and royalties)totalled 64.7 million euros, for a change of 6.0 million euros from 2010 (when it was 58.7 million euros).The in-cremental costs were mainly tied to the new opening of DOS in 2010 and the growth in the variable componentof leases and rents tied to sales performance, resulting from the steep rise in revenues in Asia.The percentage ofthese costs in terms of revenues fell from 7.5% in 2010 to 7.2% in 2011.

100

200

300

400

500

600

700

900

FY 11 FY 10

800

1,000

0

(Euro mn) FY 11 % FY 10 % Change %

Italy 449.3 50.2 425.7 54.0 23.6 5.5

Europe 182.0 20.4 163.7 20.8 18.3 11.2

North America 62.4 7.0 53.4 6.8 9.0 17.0

Asia and RoW 199.9 22.4 144.7 18.4 55.2 38.1

Total 893.6 100.0 787.5 100.0 106.1 13.5

NorthAmerica

7.0%

Asia and RoW22.4%

Italy50.2%

Asia andRoW

North Am.Europe

Italy

Asia andRoW

North Am.Europe

Italy

Europe20.4%

EBITDA (Euro mn)

FY 11 FY 11 FY 10comp. ex.rates basis

232.6 232.4

193.1

Group2011Annual Report

36 Report on operations

The change in personnel costs is related principally to the increase inheadcount. Wages and salaries totalled 126.8 million euros, comparedwith 117.8 million euros in the previous year, for an increase of 9.1 millioneuros in absolute terms.This cost is equal to 14.2% of Group revenues, sig-nificantly better than the 15.0% figure reported for 2010. At December31st, 2011, the Group had 3,549 employees, 355 more than at December31st, 2010 (3,194 employees at that date).Most of the employees who werenewly hired during 2011 were used to build up the Group’s production or-ganisation and operate new retail stores.Amortisation, depreciation and impairment expenses increased during theyear. Amortisation, depreciation and impairment for FY 2011 totalled 35.9million euros, as compared with 32.1 million euros in 2010. At December31st, 2011, amortisation and depreciation equalled 4.0% of Group rev-enues, down slightly from 4.1% in the previous year.

EBIT thus totalled 194.6 million euros (159.9 million euros in 2010), forgrowth of 34.7 million euros.This represented a 21.7% increase. EBIT in2011 was equal to 21.8% of consolidated sales (FY 2010: 20.3%).The foreign exchange effect on EBIT was negligible. On a comparable ex-change rate basis, EBIT during the period would have been 194.7 million eu-ros, representing 21.8% of consolidated sales.

Net financial income in FY 2011 was also positive, totalling 2.3 million eu-ros. In addition to the typical contribution made by interest, resulting fromthe investment of enormous amounts of cash generated by operating ac-tivities (a total of 2.3 million euros in interest income accrued on financialassets), net foreign exchange gains were also positive at 2.7 million euros(representing the difference between exchange gains and losses).Net of theeffect generated by foreign exchange risk hedging activities (2.0 million eu-ros), the total balance of foreign exchange gains and losses would have beena positive 0.3 million euros.

GROUP’S EMPLOYEES

FY 11 FY 10 FY 09 FY 08

3,549

3,194

2,840 2,814

EBIT (Euro mn)

FY 11 FY 11 FY 10comp. ex.rates basis

194.7

159.9

194.6

FINANCIAL INC/EXP. (Euro mn)

2.7

0.7

Foreignexch.

gains &losses

Net interests

Other

-1.1

Group2011Annual Report

37 Report on operations

Income taxes owed for the period totalled 61.2 million euros, including theeffects of deferred taxes.The tax rate was significant, amounting to 31.1%,which represented a major improvement from the 32.2% reported for2010.Consequently, net profit was outstanding, with consolidated net incomeamounting to 135.7 million euros in 2011, up 22.5% from 2010, when it to-talled 110.8 million euros (+24.9 million euros). Net income was equal to15.2% of consolidated revenues, as compared with 14.1% in the previousyear.

Capital expenditures. Capital expenditures totalled 61.9 million euros in 2011.This figure includes about 19.3million euros to reflect the intangible asset in relation to the agreement signed for financing of restoration workon the Coliseum. Net of this asset, the outlay for operating capital expenditure totalled 42.6 million euros,compared with 29.8 million euros in the same period of 2010 (96.1 million euros including the acquisition of theoperating site of the Group in Tokyo).

The capital expenditure dedicated to the DOS network during the yeartotalled about 20.1 million euros, compared with 16.1 million euros in2010, and was used mainly for setting up the newly opened stores duringthe financial year.The most important projects were expansion of the TOD’S store spacein Madrid and renovation of the TOD’S boutique in Düsseldorf.The remaining portion of capital expenditure during the year was spentnot only on normal updating of industrial structures and equipment, butalso and above all on expansion of the showrooms in Milan and develop-ment of corporate management software.A particularly important proj-ect involves the installation of a photovoltaic plant at Group headquarters.This investment will assure a high degree of energy autonomy for the en-tire corporate complex, as well as produce major savings on energy costsfor at least the next 20 years.

Net financial position and cash flow. The Group’s net financial position at December 31st, 2011 was 110.7million euros, reflecting a change of 14.3 million euros from December 31st, 2010 (96.5 million euros). Cash andcash equivalents of 187.8 million euros (which totalled 171.7 million euros at December 31st, 2010) are set offagainst liabilities of 77.0 million euros (75.2 million euros at December 31st, 2010), of which 47.3 million eurosrepresented by loans and other financial liabilities (both short and long-term).

Tax Rate

FY 11 FY 10 FY 09 FY 08

31.1% 32.2% 31.9%33.1%

INVESTMENTS BY ALLOCATION

DOS34%

Produc.17%

Other49%

FY 11 FY 10 FY 09 FY 08 FY 07

61.9

96.1

21.3

40.8 45.2

Tangible & IntangibleassetsCapital expenditures(Euro mn)

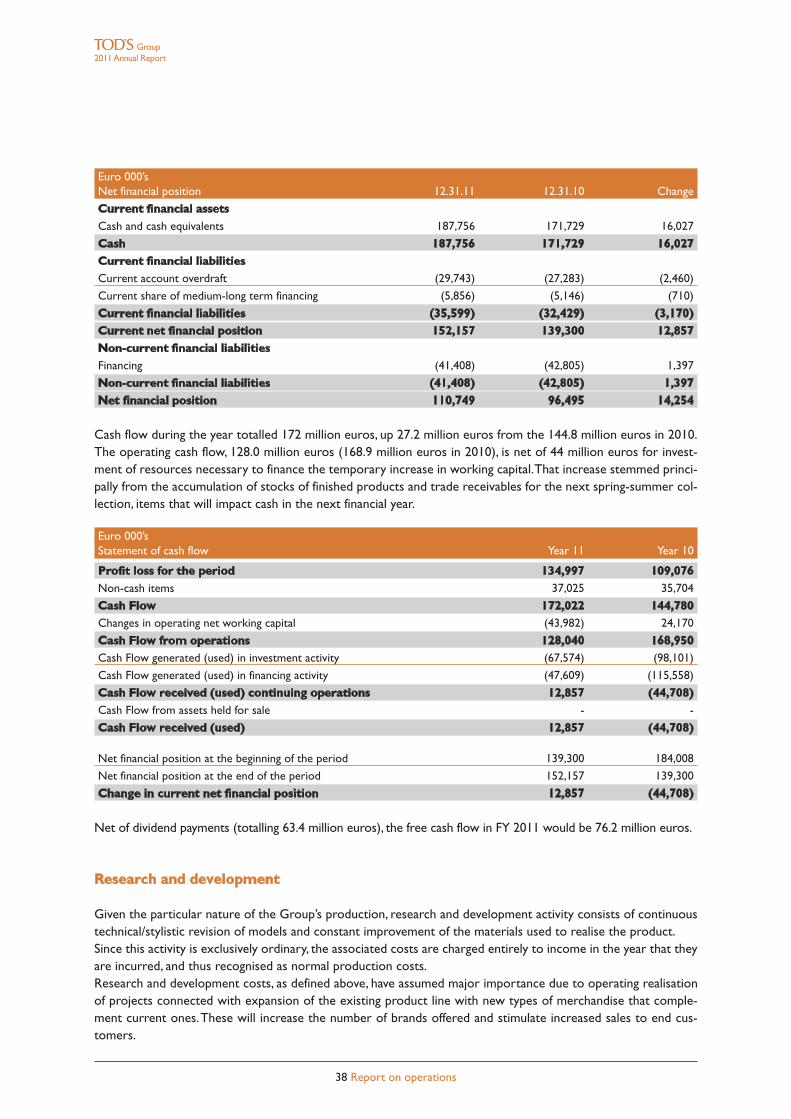

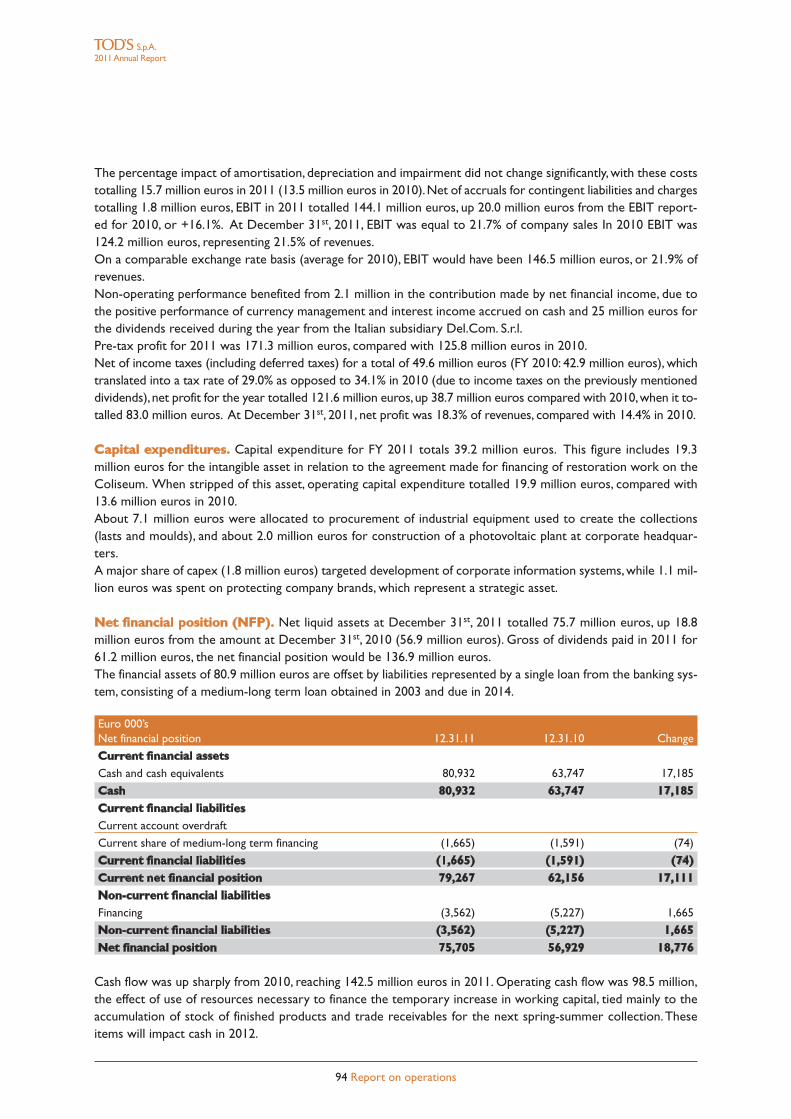

Euro 000’sNet financial position 12.31.11 12.31.10 Change

Current financial assetsCash and cash equivalents 187,756 171,729 16,027

Cash 187,756 171,729 16,027Current financial liabilitiesCurrent account overdraft (29,743) (27,283) (2,460)

Current share of medium-long term financing (5,856) (5,146) (710)

Current financial liabilities (35,599) (32,429) (3,170)Current net financial position 152,157 139,300 12,857Non-current financial liabilitiesFinancing (41,408) (42,805) 1,397

Non-current financial liabilities (41,408) (42,805) 1,397Net financial position 110,749 96,495 14,254

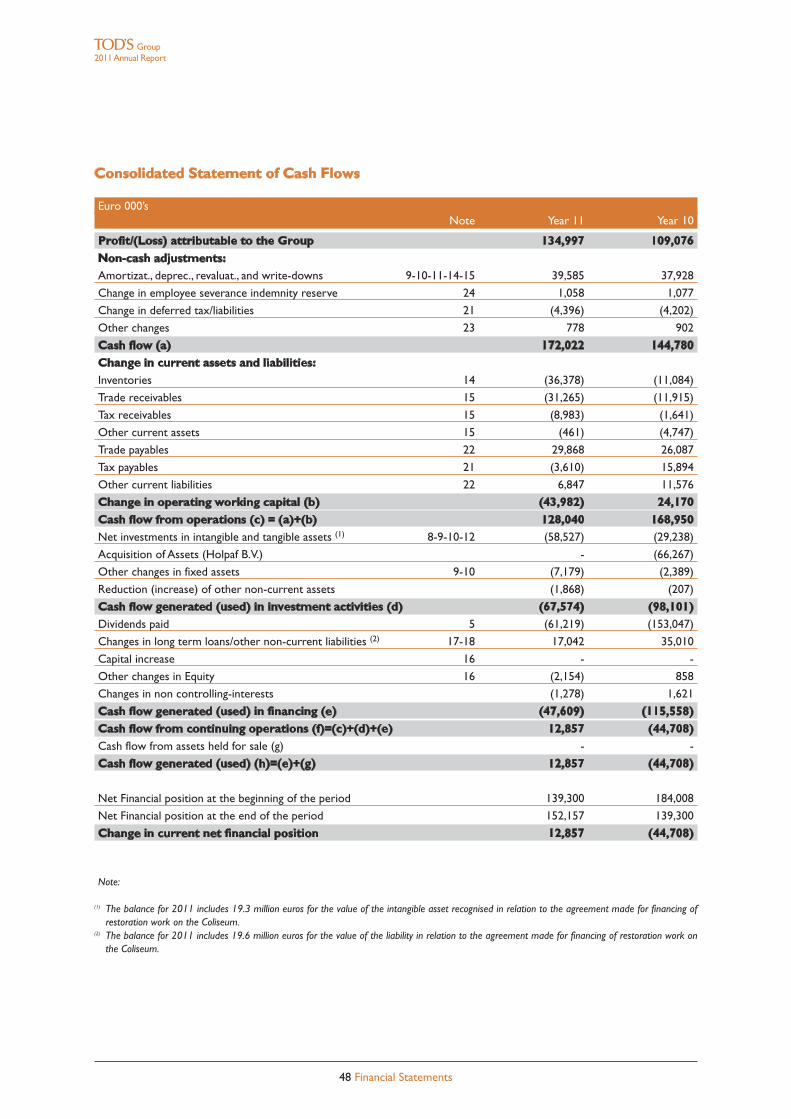

Cash flow during the year totalled 172 million euros, up 27.2 million euros from the 144.8 million euros in 2010.The operating cash flow, 128.0 million euros (168.9 million euros in 2010), is net of 44 million euros for invest-ment of resources necessary to finance the temporary increase in working capital.That increase stemmed princi-pally from the accumulation of stocks of finished products and trade receivables for the next spring-summer col-lection, items that will impact cash in the next financial year.

Euro 000’sStatement of cash flow Year 11 Year 10

Profit loss for the period 134,997 109,076Non-cash items 37,025 35,704

Cash Flow 172,022 144,780Changes in operating net working capital (43,982) 24,170

Cash Flow from operations 128,040 168,950Cash Flow generated (used) in investment activity (67,574) (98,101)

Cash Flow generated (used) in financing activity (47,609) (115,558)

Cash Flow received (used) continuing operations 12,857 (44,708)Cash Flow from assets held for sale - -

Cash Flow received (used) 12,857 (44,708)

Net financial position at the beginning of the period 139,300 184,008

Net financial position at the end of the period 152,157 139,300

Change in current net financial position 12,857 (44,708)

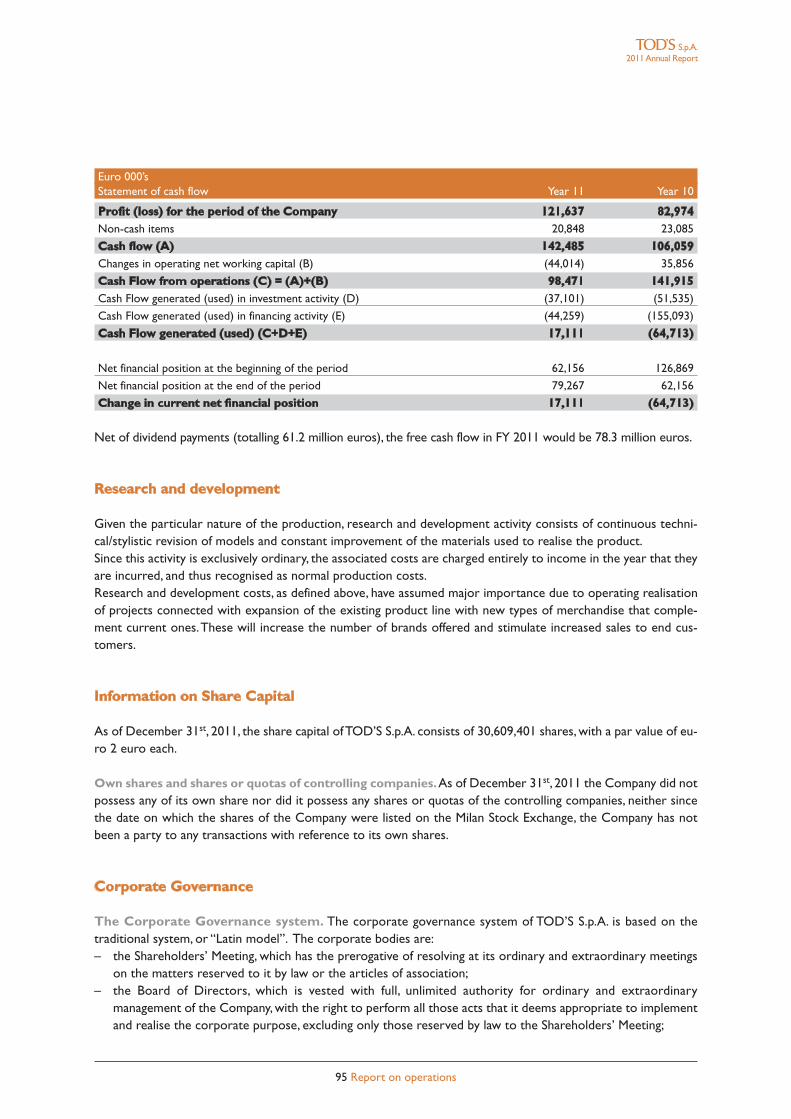

Net of dividend payments (totalling 63.4 million euros), the free cash flow in FY 2011 would be 76.2 million euros.

Research and development

Given the particular nature of the Group’s production, research and development activity consists of continuoustechnical/stylistic revision of models and constant improvement of the materials used to realise the product.Since this activity is exclusively ordinary, the associated costs are charged entirely to income in the year that theyare incurred, and thus recognised as normal production costs.Research and development costs, as defined above, have assumed major importance due to operating realisationof projects connected with expansion of the existing product line with new types of merchandise that comple-ment current ones.These will increase the number of brands offered and stimulate increased sales to end cus-tomers.

38 Report on operations

Group2011Annual Report

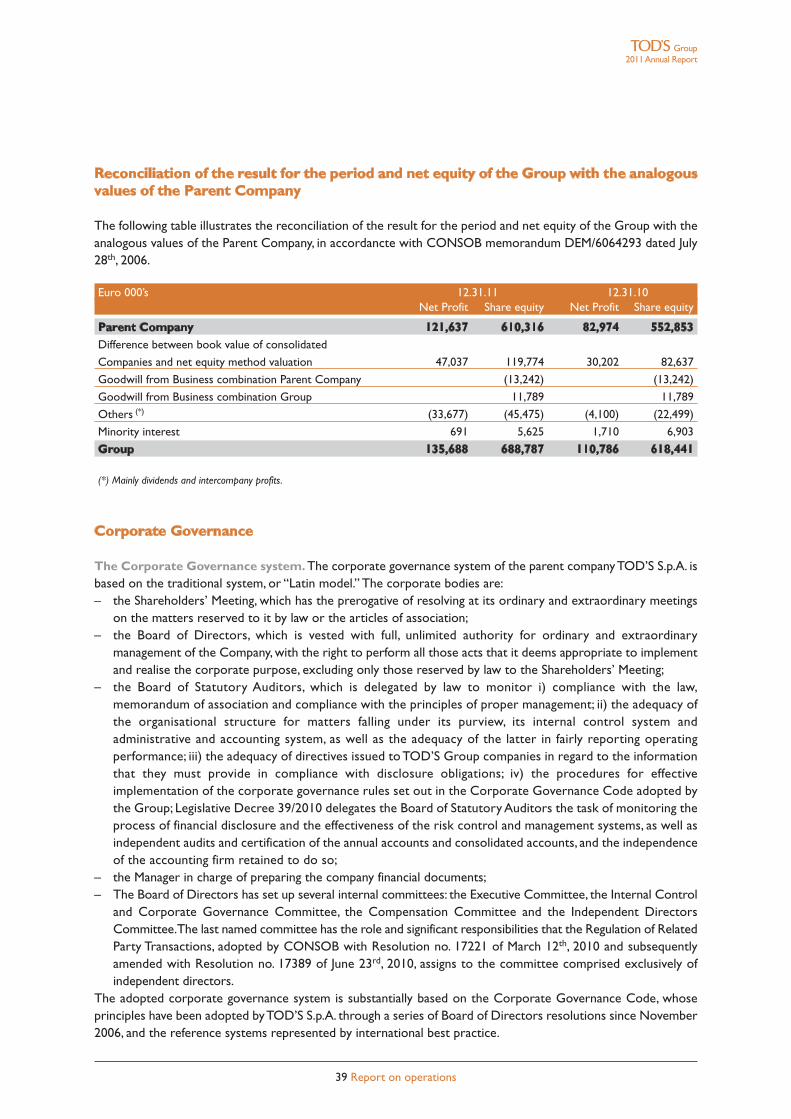

Reconciliation of the result for the period and net equity of the Group with the analogousvalues of the Parent Company

The following table illustrates the reconciliation of the result for the period and net equity of the Group with theanalogous values of the Parent Company, in accordancte with CONSOB memorandum DEM/6064293 dated July28th, 2006.

Euro 000’s 12.31.11 12.31.10Net Profit Share equity Net Profit Share equity

Parent Company 121,637 610,316 82,974 552,853Difference between book value of consolidated

Companies and net equity method valuation 47,037 119,774 30,202 82,637

Goodwill from Business combination Parent Company (13,242) (13,242)

Goodwill from Business combination Group 11,789 11,789

Others (*) (33,677) (45,475) (4,100) (22,499)

Minority interest 691 5,625 1,710 6,903

Group 135,688 688,787 110,786 618,441

(*) Mainly dividends and intercompany profits.

Corporate Governance

The Corporate Governance system. The corporate governance system of the parent companyTOD’S S.p.A. isbased on the traditional system, or “Latin model.” The corporate bodies are:– the Shareholders’ Meeting, which has the prerogative of resolving at its ordinary and extraordinary meetings

on the matters reserved to it by law or the articles of association;– the Board of Directors, which is vested with full, unlimited authority for ordinary and extraordinary

management of the Company, with the right to perform all those acts that it deems appropriate to implementand realise the corporate purpose, excluding only those reserved by law to the Shareholders’ Meeting;

– the Board of Statutory Auditors, which is delegated by law to monitor i) compliance with the law,memorandum of association and compliance with the principles of proper management; ii) the adequacy ofthe organisational structure for matters falling under its purview, its internal control system andadministrative and accounting system, as well as the adequacy of the latter in fairly reporting operatingperformance; iii) the adequacy of directives issued to TOD’S Group companies in regard to the informationthat they must provide in compliance with disclosure obligations; iv) the procedures for effectiveimplementation of the corporate governance rules set out in the Corporate Governance Code adopted bythe Group; Legislative Decree 39/2010 delegates the Board of Statutory Auditors the task of monitoring theprocess of financial disclosure and the effectiveness of the risk control and management systems, as well asindependent audits and certification of the annual accounts and consolidated accounts, and the independenceof the accounting firm retained to do so;

– the Manager in charge of preparing the company financial documents;– The Board of Directors has set up several internal committees: the Executive Committee, the Internal Control

and Corporate Governance Committee, the Compensation Committee and the Independent DirectorsCommittee.The last named committee has the role and significant responsibilities that the Regulation of RelatedParty Transactions, adopted by CONSOB with Resolution no. 17221 of March 12th, 2010 and subsequentlyamended with Resolution no. 17389 of June 23rd, 2010, assigns to the committee comprised exclusively ofindependent directors.

The adopted corporate governance system is substantially based on the Corporate Governance Code, whoseprinciples have been adopted byTOD’S S.p.A. through a series of Board of Directors resolutions since November2006, and the reference systems represented by international best practice.

39 Report on operations

Group2011Annual Report

Insofar as the term of the current Board of Directors will expire upon approval of the 2011 Annual Report, it wasdecided to delegate the new Board of Directors with the task of adopting the principles set out in the newCorporate Governance Code of Listed Italian Companies approved by Borsa Italiana S.p.A. in December 2011,which the issuers are asked to implement by the end of FY 2012. However, all those principles for which theCorporate Governance Code recommends adoption prior to the suggested deadline will still have to be appliedbeforehand.

Disclosure pursuant toArticle 123-bis of Legislative Decree 58/1998 (“TUF”).At its meeting on March 13th

2012, the Board of Directors of the parent company TOD’S S.p.A. approved the annual Report on CorporateGovernance and Shareholdings, which provides the disclosures mandated pursuant to Article 123-bis (1) of theConsolidated Law on Finance (T.U.F.).That report also analytically illustrates the corporate governance system ofTOD’S S.p.A., and it includes not only the information required under Article 123-bis (2) T.U.F., but also acomprehensive examination of the status of implementation of the corporate governance principles recommendedby the Corporate Governance Code in accordance with the “comply or explain” rule.The reader is referred to the Annual Corporate Governance and Shareholdings Report, which is available to thepublic together with this Report on Operations and accounting documentation. It may be consulted in the cor-porate section of the www.todsgroup.com website.

Disclosure pursuant to Article 123-ter of Legislative Decree 58/1998 (Consolidated Law on Finance -“TUF”). On March 13th, 2012, the Board of Directors ofTod’s S.p.A. approved, in compliance with Article 123-terof Legislative Decree 58 of February 24th, 1998 (the “Consolidated Finance Law” or “T.U.F.”), as amended, andArticle 84-ter of Consob Resolution no. 11971/99 (the “Issuers Regulation”), as amended, the RemunerationReport.The Report is composed of two sections:(i) the first is the policy ofTOD’S S.p.A. in regard to remuneration of the members of the Board of Directors, theGeneral Manager, and the executives with strategic responsibilities in regard to the 2012 financial year, as well asthe procedures used for adoption and implementation of this policy;(ii) the other is aimed at representing each of the items that compose remuneration, and describing the compen-sation paid in 2011 to members of the Board of Directors and Board of Statutory Auditors, the General Managerand the executives with strategic responsibilities;it will be submitted to the Shareholders’ Meeting called forApril 19th, 2012,which will be asked to resolve in favourof or against the first section with a non-binding resolution.The Remuneration Report is available at the registered office of the Company, at Borsa Italiana S.p.A. and on thecorporate website www.todsgroup.com.

Disclosure of Significant Companies outside the EU. TOD’S S.p.A., the parent company, directly or indirectlycontrols six companies that are incorporated and regulated pursuant to the laws of countries that do not belongto the European Union (“Significant Companies outside the EU,” as defined by Consob Resolution no.16191/2007,as amended).In reference to these companies, note that:– all of them prepare accounts used to prepare the consolidated financial statements.The balance sheet and

income statement of these entities are provided to shareholders of TOD’S S.p.A. at the times and in the waysenvisaged by applicable regulations;

– TOD’S S.p.A. has acquired the bylaws and composition and powers of the corporate bodies;– the Significant Companies outside the EU: i) provide the parent company’s independent auditor with information

that the latter needs to audit the annual and interim accounts of the parent; ii) have an administrative andaccounting system that is adequate for providing the management,Board of StatutoryAuditors and independentauditor of the parent company with the operating, financial position and earnings figures necessary for preparingthe consolidated financial statements.

In order to satisfy its own statutory obligations, the Board of Statutory Auditors of TOD’S S.p.A. has audited theadequacy of the administrative and accounting system regularly to provide the management and independent au-

40 Report on operations

Group2011Annual Report

ditor of TOD’S S.p.A. with the operating, financial position and earnings figures necessary for preparation of theconsolidated financial statements and the effective flow of information through meetings with the independent au-ditor and with the Financial Reporting Manager.

Disclosure pursuant to Consob Resolution no. 17221 of March 12th, 2010 (Related Parties Regulation). In2011 the Group did not conclude highly significant transactions with related parties or related party transactionsthat had a material impact on the assets, liabilities or net income of the Group, and there were no modificationsor developments in the transactions described in the 2010 Annual Report that had the same effects.All information regarding existing relations with related parties in 2011 are set out in the explanatory notes.

Significant events occurring after the end of the period

Effective January 1st, 2012, in view of integrating in its organisation a whole series of outsourced strategic mar-keting and promotion activities, the Group acquired, through the parent TOD’S S.p.A., 100% of the units ofFormapura S.r.l., an Italian company with which it had a collaboration relationship involving the aforementionedactivities for several years. In view of completing the integration process, and realising a more streamlined and func-tional structure in terms of assets, liabilities and earnings by simplifying the Group corporate structures, the boardsof directors of the respective entities resolved in favour of merger through takeover of Formapura S.r.l. byTOD’SS.p.A.

Business outlook

The FY 2011 results have confirmed the solidity of TOD’S Group fundamentals, and especially the strength ofbrands whose high quality and other aspects characterise Group products, guarantee constant appreciation by con-sumers of Group brands.On the basis of the foregoing, the strong start for the year under way,when the strong organic growth of the DOSnetwork continued (the SSSG figure is +6.8% for the first 10 weeks of the year), and the expansion plans for thesingle brand store network, it is reasonable to forecast that the Group may realise additional revenue and profitgrowth in 2012 .

Approval of Financial Statements

The consolidated financial statements of the TOD’S Group were approved by the Board of Directors on March13th, 2012.

Milan, March 13th, 2012The Chairman of the Board of Directors

Diego DellaValle

41 Report on operations

Group2011Annual Report

[THIS PAGE HAS BEEN INTENTIONALLY LEFT BLANK]

42 2011 Annual Report

FINANCIAL STATEMENTS

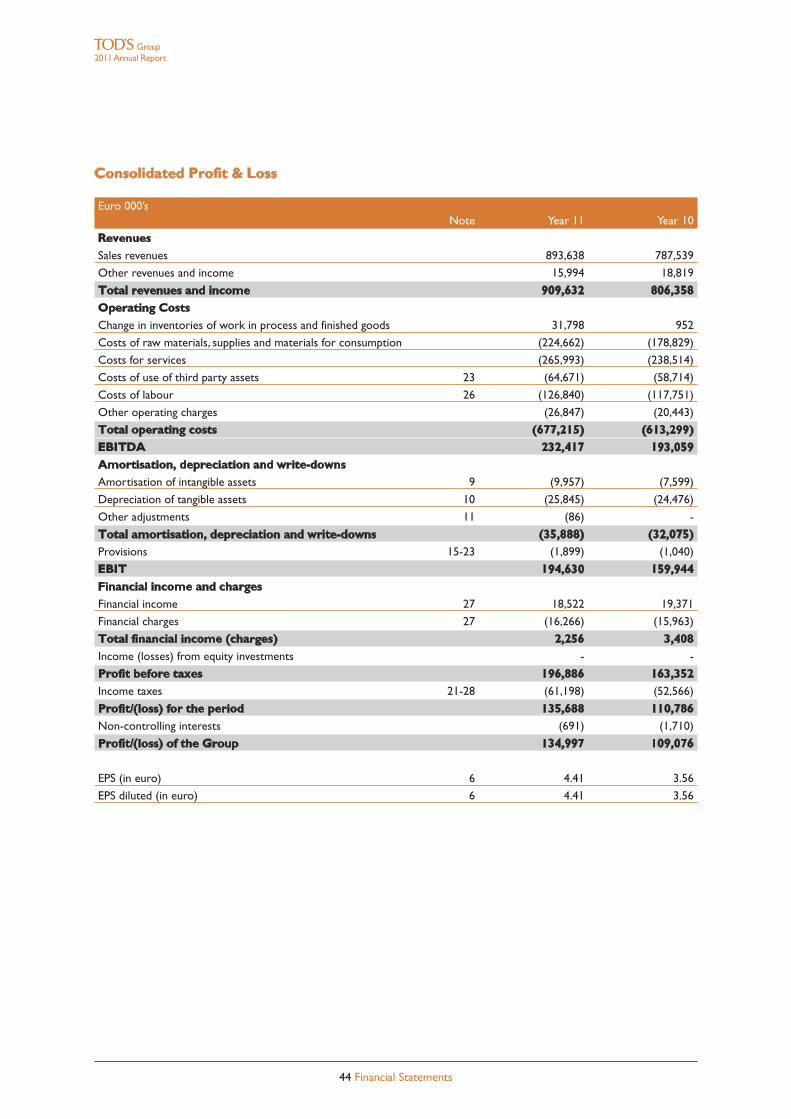

Consolidated Profit & Loss

Euro 000’sNote Year 11 Year 10

RevenuesSales revenues 893,638 787,539

Other revenues and income 15,994 18,819

Total revenues and income 909,632 806,358Operating CostsChange in inventories of work in process and finished goods 31,798 952

Costs of raw materials, supplies and materials for consumption (224,662) (178,829)

Costs for services (265,993) (238,514)

Costs of use of third party assets 23 (64,671) (58,714)

Costs of labour 26 (126,840) (117,751)

Other operating charges (26,847) (20,443)

Total operating costs (677,215) (613,299)EBITDA 232,417 193,059Amortisation, depreciation and write-downsAmortisation of intangible assets 9 (9,957) (7,599)

Depreciation of tangible assets 10 (25,845) (24,476)

Other adjustments 11 (86) -

Total amortisation, depreciation and write-downs (35,888) (32,075)Provisions 15-23 (1,899) (1,040)

EBIT 194,630 159,944Financial income and chargesFinancial income 27 18,522 19,371

Financial charges 27 (16,266) (15,963)

Total financial income (charges) 2,256 3,408Income (losses) from equity investments - -

Profit before taxes 196,886 163,352Income taxes 21-28 (61,198) (52,566)

Profit/(loss) for the period 135,688 110,786Non-controlling interests (691) (1,710)

Profit/(loss) of the Group 134,997 109,076

EPS (in euro) 6 4.41 3.56

EPS diluted (in euro) 6 4.41 3.56

44 Financial Statements

Group2011Annual Report

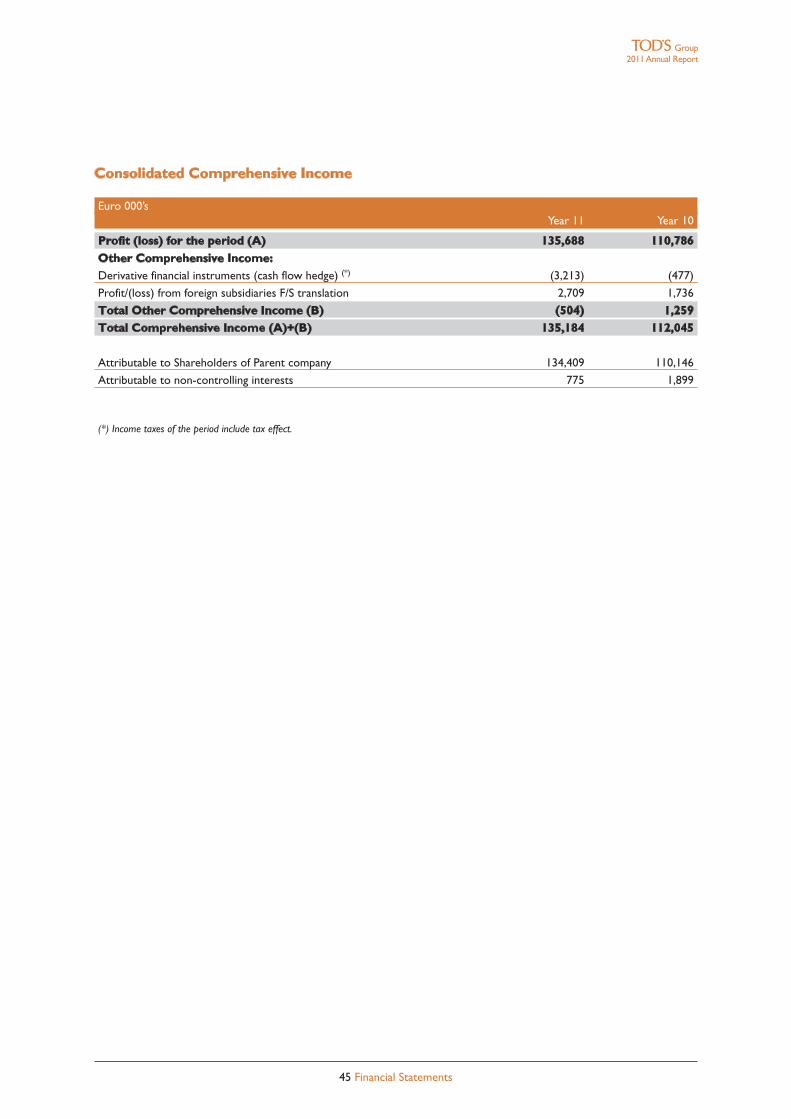

Consolidated Comprehensive Income

Euro 000’sYear 11 Year 10

Profit (loss) for the period (A) 135,688 110,786Other Comprehensive Income:Derivative financial instruments (cash flow hedge) (*) (3,213) (477)

Profit/(loss) from foreign subsidiaries F/S translation 2,709 1,736

Total Other Comprehensive Income (B) (504) 1,259Total Comprehensive Income (A)+(B) 135,184 112,045

Attributable to Shareholders of Parent company 134,409 110,146

Attributable to non-controlling interests 775 1,899

(*) Income taxes of the period include tax effect.

45 Financial Statements

Group2011Annual Report

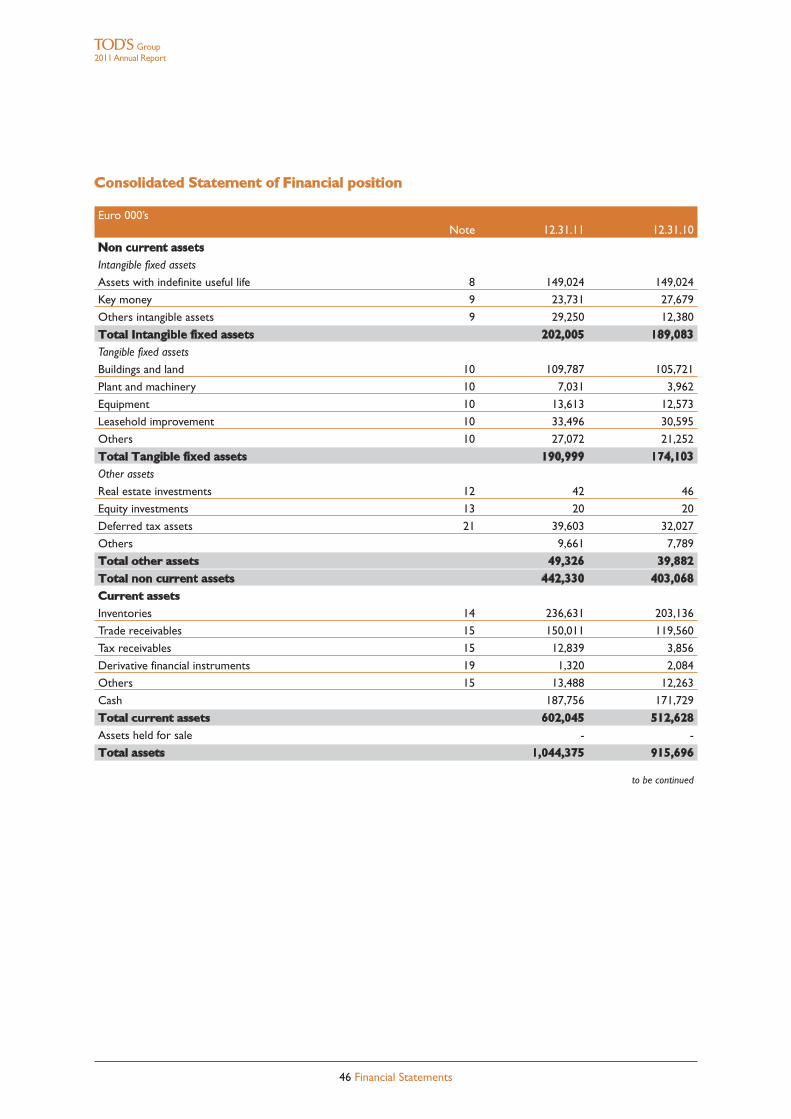

Consolidated Statement of Financial position

Euro 000’sNote 12.31.11 12.31.10

Non current assetsIntangible fixed assets

Assets with indefinite useful life 8 149,024 149,024

Key money 9 23,731 27,679

Others intangible assets 9 29,250 12,380

Total Intangible fixed assets 202,005 189,083Tangible fixed assets

Buildings and land 10 109,787 105,721

Plant and machinery 10 7,031 3,962

Equipment 10 13,613 12,573

Leasehold improvement 10 33,496 30,595

Others 10 27,072 21,252

Total Tangible fixed assets 190,999 174,103Other assets

Real estate investments 12 42 46

Equity investments 13 20 20

Deferred tax assets 21 39,603 32,027

Others 9,661 7,789

Total other assets 49,326 39,882Total non current assets 442,330 403,068Current assetsInventories 14 236,631 203,136

Trade receivables 15 150,011 119,560

Tax receivables 15 12,839 3,856

Derivative financial instruments 19 1,320 2,084

Others 15 13,488 12,263

Cash 187,756 171,729

Total current assets 602,045 512,628Assets held for sale - -

Total assets 1,044,375 915,696

to be continued

Group2011Annual Report

46 Financial Statements

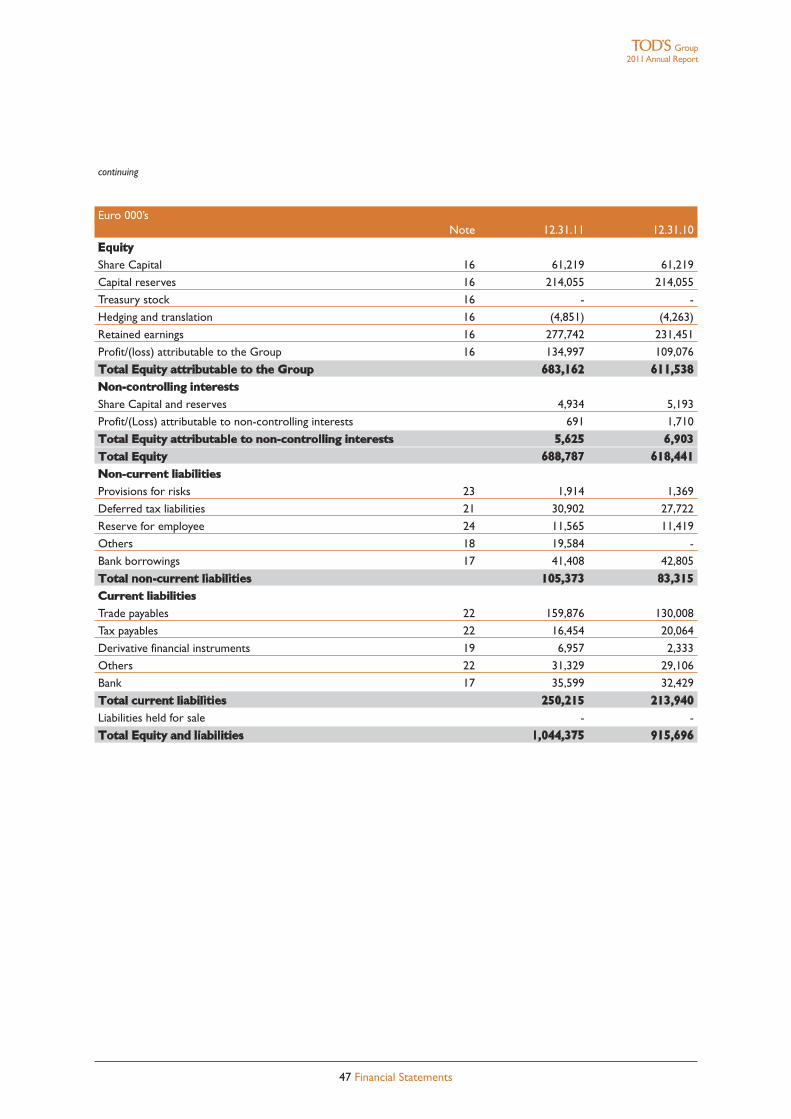

continuing

Euro 000’sNote 12.31.11 12.31.10

EquityShare Capital 16 61,219 61,219

Capital reserves 16 214,055 214,055

Treasury stock 16 - -

Hedging and translation 16 (4,851) (4,263)

Retained earnings 16 277,742 231,451

Profit/(loss) attributable to the Group 16 134,997 109,076

Total Equity attributable to the Group 683,162 611,538Non-controlling interestsShare Capital and reserves 4,934 5,193