tracfin - economie.gouv.fr

TRANSCRIPT

ML/TF risk trends and analysis in 2019-2020

TRACFIN

TRACFINUnit for intelligence processing

and action against illicit financial networks

FOREWORD

Tracfin is publishing its sixth annual report on money laundering and terrorist financing (ML/TF) risk trends and analysis. The assessment process’s starting point is the implementation, at Tracfin level, of the requirement set out in recommendation 1 of the Financial Action Task Force (FATF) standards, which specifies that “countries should identify, assess and understand the money laundering and terrorist financing risks for the country”. 1

Tracfin’s risk assessment relies on three sources of information: suspicious transaction reports (STRs) submitted by the reporting entities concerned by anti-money laundering and combating the financing of terrorism (AML/CFT) which are specifically mentioned in the French Monetary and Financial Code (CMF); financial intelligence sent by the administrative departments and foreign Financial Intelligence Units (FIUs); the content of investigation files referred by Tracfin to the courts or partner departments.

Since 2014, Tracfin’s ML/TF risk trends and analysis reports have described the main recurrent and nascent typologies with an eye to providing the reporting entities with the most relevant information to inform their risk classification. This 2019-2020 edition follows on from the previous reports and supplements the 2019 Annual Report and the communication media disseminated by the Unit (joint guidelines, newsletters).

The ML/TF risk trends and analysis in 2019-2020 report contains three components:– The first is centred on a summary of the main ML/TF trends that have been

pinpointed by examining the reporting flows handled by Tracfin which have been constantly increasing in terms of both volume and standard. The summary is enhanced by citing examples of the main underlying violations that have been noted, analysed and submitted by the Unit.

– The second focuses on substantiating the analysis of the risks being run by the economic sectors which are the most vulnerable to money laundering and terrorist financing. This section highlights shortcomings and details, where applicable, ways to bolster the AML/CFT system.

– The report’s third and final component homes in on the new financial vectors which, as part of the digitalisation of economic and financial activities, may be used for ML/TF purposes.

1. FATF: International standards on combating money laundering and the financing of terrorism & proliferation, The FATF Recommendations, February 2012.

TR

AC

FIN

- M

L/T

F R

ISK

TR

END

S A

ND

AN

ALY

SIS

IN 2

019-

2020

3

TABLE OF CONTENTS

DETAILING THE TRENDS OVERVIEW OF THE MAIN ML/TF RISKS IDENTIFIED BY TRACFIN 9

THE ANALYSIS OF REPORTING FLOWS IN 2019-2020 HIGHLIGHTS RISK INDICATORS WHICH SUPPLEMENT THE NATIONAL ANALYSIS OF ML/TF RISKS 10

THE NATIONAL RISK ANALYSIS STRIVES TO RATE THE RISKS ATTACHED TO THE MAIN ML/TF VECTORS 10

THE ANALYSIS OF REPORTING FLOWS HANDLED BY TRACFIN IN 2019-2020 COMPLEMENTS

THE NATIONAL RISK ANALYSIS 11

TRENDS OBSERVED 13

EXAMPLES OF TRENDS: THREE RECURRENT ACTIVITIES AS REGARDS FIGHTING FINANCIAL CRIME, COMBATING FRAUD AND INTERNATIONAL COOPERATION 15

EXAMPLE 1: THE PERPETUATION OF FRAUD AGAINST THE PUBLIC PURSE 15

EXAMPLE 2: DETECTING THE LAUNDERING OF THE PROCEEDS OF ILLEGAL TRAFFICKING IS PARTLY

RELIANT ON MONITORING FLOWS OF CASH 22

EXAMPLE 3: THE MAIN MONEY LAUNDERING TRENDS MAKE ACTIVE COOPERATION BETWEEN TRACFIN

AND ITS FOREIGN COUNTERPARTS ESSENTIAL 26

MITIGATING VULNERABILITIES A REVIEW OF THREE SECTORS THAT CARRY HIGH ML/TF RISKS 33

PROPERTY, A SECTOR IMPLICATED IN ALL THE STAGES OF MONEY LAUNDERING 35

A SECTOR USED TO FOSTER CONSPIRACY TO COMMIT FRAUD 35

A SECTOR USED AS A VECTOR IN THE INTEGRATION STAGE OF MONEY LAUNDERING 36

A SECTOR EXPOSED TO LAUNDERING THE PROCEEDS OF BRIBERY AND THE MISAPPROPRIATION

OF PUBLIC FUNDS 36

THE ART SECTOR IS VULNERABLE TO THE RISKS OF BOTH MONEY LAUNDERING AND TERRORIST FINANCING 43

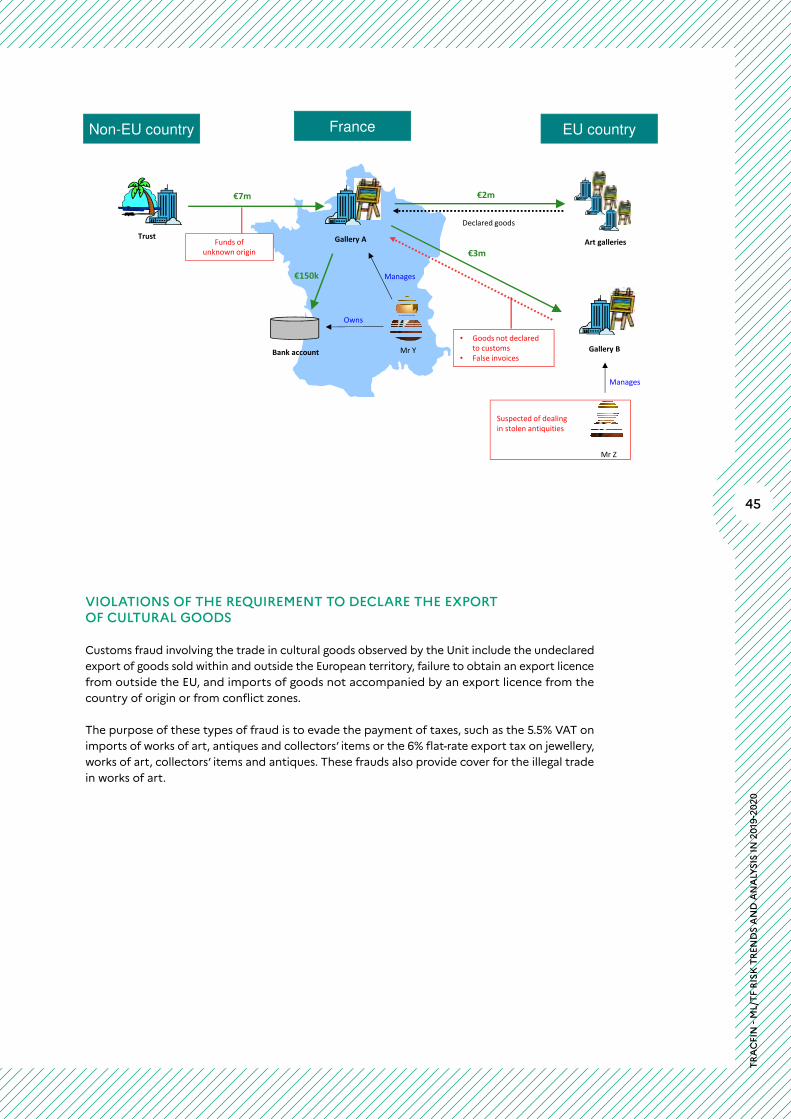

A SECTOR USED TO CIRCUMVENT TAX OBLIGATIONS 44

VIOLATIONS OF THE REQUIREMENT TO DECLARE THE EXPORT OF CULTURAL GOODS 44

THE ART MARKET IS CONDUCIVE TO TERRORIST FINANCING 47

PROFESSIONAL SPORT, A SECTOR REQUIRING FORCEFUL APPLICATION OF THE AML/CFT SYSTEM 49

THE STILL-RECENT REGULATION OF THE PROFESSION OF SPORTS AGENT NEEDS TO BE TIGHTENED

TO BOLSTER VERIFICATION OF THE RELATED FINANCIAL FLOWS 49

A SECTOR SUSCEPTIBLE TO BRIBERY, IN PARTICULAR FOR THE AWARDING OF SPORTS COMPETITIONS 51

A SECTOR IN WHICH COMPETITIONS MAY BE FIXED BY THE PLACING OF SPORTS BETS 52

TR

AC

FIN

- M

L/T

F R

ISK

TR

END

S A

ND

AN

ALY

SIS

IN 2

019-

2020

5

ANTICIPATING RISKS NEW ML/TF CIRCUITS DUE TO THE DIGITALISATION OF PAYMENT SERVICES 55

E-MONEY AND CRYPTO-ASSESTS ARE STILL LEADING MEANS OF MONEY LAUNDERING AND TERRORIST FINANCING 58

DESPITE MAJOR LEGISLATIVE REFORM, PREPAID CARDS AND VOUCHERS STILL PROVIDE ANONYMITY 59

MORE HARMONISED OVERSIGHT AT EUROPEAN LEVEL WOULD HELP CLOSE THE LOOPHOLES

INTRODUCED BY THE EUROPEAN PASSPORT 62

ACCOUNTS OPENED ONLINE MAY PROVIDE NEW ANGLES FOR INVESTIGATIONS 66

NEW RISKS IN THE CRYPTO-ASSETS SECTOR 68

POTENTIAL FRAUD RISK IN INITIAL COIN OFFERINGS USED TO RAISE FUNDS 68

THE FRENCH AML/CFT SYSTEM FACED WITH THE EXPANSION OF STABLECOINS 70

BIG TECH’S ENTRY INTO FINANCIAL SERVICES: A EUROPE-WIDE EXPANSION THAT CALLS FOR REGULATORY ATTENTION 73

NEW COMPETITION FOR EUROPEAN MONEY TRANSFER AND ONLINE PAYMENT SERVICE PROVIDERS 73

ACQUIRING STAKES AND FORMING PARTNERSHIPS: BUSINESS STRATEGIES WITH LONG-TERM RISKS 74

SUMMARY OF MAIN RECOMMENDATIONS 75

APPENDICES 77

APPENDIX I: LIST OF CASE STUDIES 78

APPENDIX II: STATISTICAL METHODOLOGY FOR ANALYSING REPORTING FLOWS 80

APPENDIX III: LIST OF ABBREVIATIONS AND ACRONYMS 81

TR

AC

FIN

- M

L/T

F R

ISK

TR

END

S A

ND

AN

ALY

SIS

IN 2

019-

2020

6

TR

AC

FIN

- M

L/T

F R

ISK

TR

END

S A

ND

AN

ALY

SIS

IN 2

019-

2020

7

1T

RA

CFI

N -

ML/

TF

RIS

K T

REN

DS

AN

D A

NA

LYSI

S IN

201

9-20

20

8

DETAILING THE TRENDSOVERVIEW OF THE MAIN ML/TF RISKS IDENTIFIED BY TRACFIN

TR

AC

FIN

- M

L/T

F R

ISK

TR

END

S A

ND

AN

ALY

SIS

IN 2

019-

2020

9

The main areas of risks faced by the French AML/CFT system, which have been set out in the reports on the risk trends and analysis regarding money laundering and terrorist financing published by Tracfin since 2014, are established by cross-referencing a number of areas of analysis: the main underlying violations noted by Tracfin, the principal vectors or arrangements used by money laundering networks and the most-exposed economic sectors.

THE ANALYSIS OF REPORTING FLOWS IN 2019-2020 HIGHLIGHTS RISK INDICATORS WHICH SUPPLEMENT THE NATIONAL ANALYSIS OF ML/TF RISKS

THE NATIONAL RISK ANALYSIS STRIVES TO RATE THE RISKS ATTACHED TO THE MAIN ML/TF VECTORS

The national analysis of ML/TF risks in France2 (ANR) was adopted on 17 September 2019. It is an interministerial approach, coordinated by the AML/CFT Advisory Board (COLB), which strives to flag up the threats, vulnerabilities and level of resulting risks as regards ML/TF at national level. National risk analysis, which is vital for summarising the regular analysis work carried out by the relevant authorities, helped with the groundwork for the FATF’s 2020 mutual evaluation of the French AML/CFT system.

Methodology based on cross-referencing threats and vulnerabilities The methodology for the national risk analysis abides by the principles laid down by the FATF, especially the cross-referencing of threats and vulnerabilities to assess the extent of the resulting associated risk for each major ML/TF vector.

A three-level ranking (low, moderate or high exposure) has been applied for the ML/TF threat for each product or sector. The vulnerability of each product, service or transaction has also be subject to the same type of ranking. Cross-referencing threats and vulnerabilities has enabled the level of risk for each product or sector to be determined.

Targeted findings on the main ML/TF vectorsNational risk analysis reports on the main criminal threats faced by France and provides substantiated information on the primary vectors used for ML/TF purposes. With respect to terrorist financing, the analysis focuses on the main vectors for financial flows for the benefit of Jihadi groups: networks of collectors, the non-profit sector, innovative financing methods.

Similarly, for money laundering, it establishes the vulnerabilities of the financial and non-financial sectors, and highlights the use of complex legal structures, cash, instruments that foster anonymity (e-money, digital assets), property acquisitions or non-profits of a sensitive nature, as being exposed vectors.

2. COLB, Analyse nationale des risques de blanchiment de capitaux et de financement du terrorisme en France, September 2019, available on the website of the Directorate General of the Treasury: https://www.tresor.economie.gouv.fr/Articles/2019/09/20/le-conseil-d-orientation-de-la-lutte-contre-le-blanchiment-de-capitaux-et-le-financement-du-terrorisme-approuve-l-analyse-nationale-des-risques-anr-en-france (in French).

TR

AC

FIN

- M

L/T

F R

ISK

TR

END

S A

ND

AN

ALY

SIS

IN 2

019-

2020

10

THE ANALYSIS OF REPORTING FLOWS HANDLED BY TRACFIN IN 2019-2020 COMPLEMENTS THE NATIONAL RISK ANALYSIS

The analysis of reporting flows handled by Tracfin in 2019-2020 draws on metho-dology involving cross-referencing the main reported offences and the related sectors of activity.3 Money laundering, excluding terrorist financing, underlies all the violations presented in this report. The purpose of the analysis is to shed light on the extent to which an economic sector can be used as an ML/TF vector. It does not call into question either the involvement or detection capabilities of the relevant reporting entities working in some of these sectors but just aims to underscore their level of exposure to ML/TF risks due to the amount of information relating to them.

A sector of activity is examined with regard to its exposure to risk criteria which are materialised as underlying violations: to what extent does it enable cash to be laun-dered, for income of undetermined origin or undeclared work to be concealed? How far does it suit the requirements and operating methods of criminal networks involved in fraud, bribery or terrorist financing? What is the likelihood of it being used to cloud the traceability of financial flows?

The division of reporting flows by economic sector, as set out in the table below, was carried out using suspicious transaction reports (STRs) received by the Unit and information from investigations. It sets out three levels of exposure to ML risks: – “ * ”: economic sector exposed to ML/TF risk – “ ** ”: economic sector highly exposed to ML/TF risk – “ *** ”: economic sector very highly exposed to ML/TF risk

These findings draw on an analysis of the volume of reporting flows and the bias already contained in the STRs received by Tracfin. The resulting conclusions highlight the recurrent trends handled by the Unit on a daily basis. In this respect, Tracfin’s analysis does not represent, in itself, a ranking of the sectoral ML/TF risk but is part of a collective approach to enhance the national risk analysis in consultation with its partners.

This means that the original nature of some areas of risk analysed on the fringes of these trends is not explicitly flagged up. Although the breakdown of reporting flows has less impact on certain economic sectors, this is not a sign that they are not exposed to the ML/TF risk.

Conversely, it demonstrates that a number of “pockets” of risk, which are more rarely noted, fly under the radars of the reporting entities and require heightened diligence. Phenomena having unique ML/TF features such as white certificate (CEE) fraud in the environment sector, bribery in the armaments sector or investment fraud in the commodities sector have been detailed by Tracfin in its various ML/TF risk trends and analysis reports since 2014.

3. Detailed methodology is set out in Appendix II.

TR

AC

FIN

- M

L/T

F R

ISK

TR

END

S A

ND

AN

ALY

SIS

IN 2

019-

2020

11

Economic sectors

Offences

Terrorist financing

Tax evasion, social security and customs

fraud

Undeclared work

Misuse of company

assets

Fraud and theft

Trafficking

Bankruptcy and

organisation of insolvency

Bribery and breaches

of the duty of probity

Cash4

Aeronautics and space *Farming – Agrifood * * *Armaments ** *Crafts, art professions and trade in cultural goods

* *** * * ** **

Non-profit organisations *** * * *Audiovisual *Audit, accounting, management * *Automotive * *** ** ** ** * * **Banks, insurance * **Construction * *** *** *** *** *** ** * ***Biology, chemicals, pharmaceuticals

Trading – distribution ** *** ** ** *** *** ** * ***Communication *Education *Environment *Civil service * ***Hotel – restaurant *** * ** ** * **Property *** ** ** * ** *** **Manufacturing *IT, telecoms ** * * ** ** *Gambling ** * * ** ***Medical * * *Fashion and textiles * *

Legal professions * *

Human resources *

Sports ** * *Tourism * *Transport – logistics ** ** ** ** * *

4. Unlike the table’s other columns, use of cash does not represent an offence. Nevertheless, its intensive use in certain sectors justifies it having its own category.

Reporting activity of reporting entities

TR

AC

FIN

- M

L/T

F R

ISK

TR

END

S A

ND

AN

ALY

SIS

IN 2

019-

2020

12

TRENDS OBSERVED

The economic sectors in which there are the largest number of suspected offences are construction, and trading and distribution. These two sectors alone account for a very substantial proportion of the STRs submitted to Tracfin. The STRs which are processed also very often concern the property, art, hotel-restaurant, transport, logistics, IT and telecoms sectors.

The main potential offences logged by Tracfin relate to tax evasion and social security fraud, undeclared work and, to a lesser extent, misuse of company assets and theft/fraud. The Unit pays particular attention to all STRs concerning the financing of terrorism, illegal trafficking and breaches of the duty of probity.

Fraud against the public purse,5 primarily tax evasion and social security fraud, is examined separately below.6 It takes place mainly in sectors in which large amounts of cash are handled (construction, restaurants, hotels) and in the retail trade (automotive, trading and distribution). Tax evasion tied in with property transactions should be subject to special attention. With a broader interpretation, this category can also include the organisation of insolvency which is noted less frequently in the same economic sectors. The many different types of tax evasion, social security or customs fraud are set out every year in Tracfin’s Annual Reports and the ML/TF risk trends and analysis reports.

Undeclared work involves either basic defrauding of social security organisations and violations of labour law, or more sophisticated money laundering circuits that use the payment of undeclared workers to launder cash of criminal origin. This takes place essentially in the construction industry.

A significant amount of fraud, particularly when committed as a conspiracy, has been reported to Tracfin. Since 2015, the Unit has provided details of many different types of fraud in its ML/TF risk trends and analysis reports on, inter alia, false transfer orders, fraudulent Forex investments, physical diamonds or crypto-assets or fraud against public schemes such as white certificates (CEE) misused at the expense of the mandatory participants7. Clients of credit institutions and insurance companies are the primary victims of these offences. The perpetrators set up companies in the IT, trading or distribution sectors to get rid of and launder the proceeds of the fraud. In most cases, these companies have no actual business activity.

Combating the financing of terrorism is one of the Unit’s imperative assignments. Besides recurrent trends such as microfinancing and the use of cash collection networks, Tracfin has noted increased exposure of the community-based non-profit sector to the financing of radicalisation and terrorist organisations, especially Islamic ones.

5. The National Anti-Fraud Office (DNLF) defines fraud against the public purse as including both tax evasion (individuals and businesses) and all forms of social security fraud (undeclared work and benefit fraud).See https://www.economie.gouv.fr/dnlf/quest-que-fraude-aux-finances-publiques (in French).

6. See page 15.

7. The mandatory participants are energy generating companies (suppliers of electricity, gas, fuel, oil, etc.) that are tasked by the scheme with achieving energy savings based on their volume of sales. The workings of the scheme are described on page 27 of Tracfin’s ML/TF risk trends and analysis in 2017/2018 report.

TR

AC

FIN

- M

L/T

F R

ISK

TR

END

S A

ND

AN

ALY

SIS

IN 2

019-

2020

13

Suspected trafficking, such as that of drugs and weapons, smuggling, counterfeiting or of humans concerns persons operating in the field of organised crime,8 and the laundering of the cash generated through various economic sectors (e.g. construction, trading, restaurants). Fighting this trafficking is one of Tracfin’s main strategic objectives (see Example 2 below).

Breaches of the duty of probity9 often involve complex legal structures which frequently have an international dimension. As a result of how international banking flows are organised, the intermediation of correspondent banks is noted when the proceeds of an offence of bribery or the misappropriation of public funds, which is committed abroad, are transferred to France. The French property and art sectors are especially susceptible to the laundering of the proceeds of these offences. In addition, the public sector, through semi-public companies, could be exposed to the risk of breaches of the duty of probity.

Lastly, besides the violations mentioned, the plethora of STRs concerning the handling of cash of unknown origin bears witness to this vector’s presence in many stages of money laundering. Laundering cash is most often carried out by:10

– networks for transnational fundraising, physical transport and informal remittance – injecting cash into companies with a legitimate business activity, particularly those

operating in construction, vehicle trading (especially second-hand),11 import-export, or other sectors in which cash is extensively used such as local shops, bars, tobac-conists, cafés and restaurants

– paying undeclared workers – gambling (purchases of winning lottery, horse racing and sports tickets, cash bets

in casinos)

Although it is not expressly mentioned in the analysis of reporting flows, intelligence of economic interest covers sectors which are sensitive as regards France’s fundamental interests. Tracfin focuses on information concerning the pharmaceutical industry, the armaments sector, the circumvention of economic embargos, and on the taking of interests or takeover of leading French companies by foreign investors.

8. Organised crime is defined on page 10 of Tracfin’s ML/TF risk trends and analysis in 2018/2019 report by referring, inter alia, to the United Nations Convention against Transnational Organized Crime, which was adopted in Palermo in December 2000, as “a structured group of three or more persons, existing for a period of time and acting in concert with the aim of committing one or more serious crimes or offences […] in order to obtain, directly or indirectly, a financial or other material benefit”.

9. Tracfin, ML/TF risk trends and analysis in 2016 report, pp. 38 to 42, ML/TF risk trends and analysis in 2017/2018 report, pp. 78 to 83 and ML/TF risk trends and analysis in 2018/2019 report, pp. 21 to 29.

10. Tracfin, ML/TF risk trends and analysis in 2015 report, pp. 22 to 25 and pp. 35 to 41.

11. Tracfin, ML/TF risk trends and analysis in 2017/2018 report, pp. 35 to 37.

TR

AC

FIN

- M

L/T

F R

ISK

TR

END

S A

ND

AN

ALY

SIS

IN 2

019-

2020

14

EXAMPLES OF TRENDS: THREE RECURRENT ACTIVITIES AS REGARDS FIGHTING FINANCIAL CRIME, COMBATING FRAUD AND INTERNATIONAL COOPERATION

The main ML/TF trends described above highlight Tracfin’s core assignments as part of the government’s AML/CFT policy: fighting economic and financial crime, tax evasion and social security fraud and combating the financing of terrorism. The purpose of this section is to provide examples of this observation to substantiate Tracfin’s work to tackle fraud against the public purse and illegal trafficking, and to describe how the Unit cooperates with its foreign counterparts to successfully accomplish these assignments.

EXAMPLE 1: THE PERPETUATION OF FRAUD AGAINST THE PUBLIC PURSE

Fighting tax evasion and social security fraud is set out clearly in the new national intelligence strategy of July 2019.12 For this purpose, verification and penalty provisions have been bolstered, in particular by the Anti-Fraud Act of 23 October 2018. According to the tax authorities, the amount of fraud detected in these two areas stood at €5.73bn in 201813.

Social security fraud damages the government’s financial interests Social security fraud is one of the main money laundering threats.14 It covers all fraudulent behaviour and acts against social security, and encompasses two concepts: social security contribution fraud, essentially through undeclared work (as defined by Article L.8211-1 of the French Labour Code) and benefit fraud (receipt of undue welfare benefits).

Combating social security fraud is essential to ensure economic effectiveness and social justice. According to the report on benefit fraud published by the Government Audit Office in 2020, the main social security funds detected €1bn in losses suffered and avoided as part of anti-fraud measures.15 Fighting fraud mainly involves looking for irregularities after the fact. But, these discrepancies could, theoretically, be more easily stemmed by verification work during the day-to-day management of benefits.

Tracfin is continuing to improve its detection of fraud affecting social protection organisations. The types of illegal activities are broken down between contribution fraud (undeclared work, under declarations by self-employed workers to the social security scheme or the MSA social agricultural mutual fund) and benefit fraud (receipt of unemployment benefit at the same time as carrying on undeclared work, residence fraud, “collection account” schemes for undue benefits).

In 2020, the extraordinary circumstances caused by the COVID-19 pandemic and the worsening of the economic situation of certain sectors fostered a new type of fraud against the short-time working benefits scheme.

12. Government, Bilan 2019 de lutte contre la fraude et renforcement du civisme fiscal, February 2020 (in French).

13. National Anti-Fraud Office (DNLF), Les grandes tendances du bilan 2018 de la lutte contre la fraude aux finances publiques, 30 December 2019 (in French).

14. AML/CFT Advisory Board (COLB), Analyse nationale des risques de blanchiment de capitaux et de financement du terrorisme en France, September 2019, p.26 (in French).

15. Government Audit Office, La lutte contre les fraudes aux prestations sociales, September 2020 (in French).

TR

AC

FIN

- M

L/T

F R

ISK

TR

END

S A

ND

AN

ALY

SIS

IN 2

019-

2020

15

A new phenomenon in 2020: fraud against the short-time working benefits scheme which was introduced in response to the health crisis Against the backdrop of the health crisis caused by the COVID-19 pandemic and the economic support measures rolled out by the government, Tracfin acted to help the reporting entities by informing them of the main risks of fraud and money laun-dering observed in this context.16

One of these measures, introduced by Decree no. 2020-325 of 25 March 2020, fol-lowed by Order no. 2020-346 of 27 March 2020, allowed for the recasting of the short-time working scheme (called “partial unemployment or temporary layoffs”), to facilitate entitlement, retrospectively to 1 March 2020. A streamlined procedure was opted for to provide businesses and employees with rapid support. The Ministry for Labour, Employment and Integration estimates that 7.2 million French workers were subject to short-time working for one or several days per week in March, 8.8 million in April and 7.9 million in June 2020.

16. Tracfin, Les risques de BC/FT liés à la crise sanitaire et économique de la pandémie COVID-19. Analyse typologique des principaux risques identifiés, May 2020. https://www.economie.gouv.fr/tracfin/les-risques-de- blanchiment-de-capitaux- et-de-financement-du- terrorisme-lies-la-crise (in French).

APPLICATIONS FOR SHORT-TIME WORKING BENEFIT

Employers file applications for benefits for hours not worked by employees on the activitépartielle.emploi.gouv.fr website, following a simplified online registration process. Unlike the current scheme, they no longer require prior authorisation to use short-time working arrangements.

Eight pieces of easily-obtainable information are needed to set up an account: the SIRET number, the company’s name and address, an email address, a landline number and details of the contact person (name and email address), and a bank account identification document (RIB).

Once the account has been set up, the employer can file its benefit application using the

codes received at the email address provided. It then enters the names of the employees, the number of working hours and the gross hourly rate. As part of COVID-19 measures, the benefit paid is in proportion to the wages of workers placed under short-time working arrangements within a limit of 4.5 times the gross French statutory minimum wage (SMIC). Applications were initially approved after 48 hours but the timeline is now 15 days.

No supporting documents are required but subsequent checks may be carried out by officials from the Regional Directorates for Enterprises, Competition Policy, Consumer Affairs, Labour and Employment (DIRECCTE), who may ask to be provided with pay slips.

Tracfin uncovered widespread short-time working fraud. The total amount of the fraud is thought to be €225m,17 more than half of which has been able to be blocked and recovered. To contain the phenomenon, checks have been set up throughout the benefit process chain. This was materialised by the extension of the timeline for approving applications from 48 hours to 15 days, data visualisation to pinpoint suspicious applications, the introduction of upstream verification with a blocking mechanism via an embedded system detecting inactive SIRET codes or multiple applications, a downstream on-site documentary audit by teams from the Ministry for Labour, and checks by the payer organisation, the French Services and Payment Agency (ASP).

17. Estimates from the Ministry for Labour, Employment and Integration (see Le Monde, “Chômage partiel : le montant des fraudes estimé à 225 millions d’euros, dont plus de la moitié a été récupérée”, 17 September 2020).

TR

AC

FIN

- M

L/T

F R

ISK

TR

END

S A

ND

AN

ALY

SIS

IN 2

019-

2020

16

Short-time working fraud is deemed to be social security contribution fraud within the meaning of the French Labour Code.18 Fraudsters risk the following penalties: – Full repayment of the amounts received for short-time working – Ban on receiving government aid for employment and training for a maximum of

five years – Two years’ imprisonment and a €30,000 fine under Article 441-6 of the French

Penal Code

Following its verification work, the Ministry for Labour flagged up two types of short-time working fraud: – Fraud: identity theft or use of fictitious businesses. With identity theft, the

application for payment of benefit by online declaration is filed using the corporate name and SIRET identification number of existing companies that have not applied for short-time working benefits

– False declarations: declared hours that do not correspond to actual hours not worked, etc.

Since the health crisis started, Tracfin has received a large number of STRs concerning this type of fraud from credit institutions. At 30 September 2020, Tracfin had referred over 90 cases representing a total of over €22m to the courts, with average financial stakes of €238,000 per case. In this respect, the Unit exercised its right of opposition more than 30 times between June and September 2020 for an aggregate amount of €2.2m. By way of comparison, it exercised that right 18 times in 2018 and 11 times in 2019; the figure between June and September 2020 is therefore three times higher than for 2019 as a whole.

In most cases, the arrangements noted have common features and enable the following warning signs to be highlighted: – Dormant companies filing an application for short-time working benefit – No employees in the company (the business has not declared any employees and

does not pay any wages, etc.) – Inconsistency between the amount of benefit received and the number of

employees declared by the company – The benefit received is not used to pay wages – The benefit received is followed by international transfers to individuals or other

companies domiciled abroad – Identity theft or use of fake documents to receive benefit on behalf and in the

place of another company

The Unit also receives reports concerning individuals or legal entities who/which, on the basis of investigations conducted, are acting in a conspiracy.

18. Articles L.5124-1 and L.5429-1 of the French Labour Code set out the conditions which constitute undeclared work. These articles refer to benefits paid as part of a short-time working scenario. This means that short-time working fraud falls within the category of social security contribution fraud.

TR

AC

FIN

- M

L/T

F R

ISK

TR

END

S A

ND

AN

ALY

SIS

IN 2

019-

2020

17

CASE STUDY 1

Short-time working fraud, criminal seizures with the perpetrator being placed on remandBetween May and August 2020, the catering company X and its manager, Ms A, received almost €450,000 in short-time working benefit due to the COVID-19 pandemic from a Regional Public Finances Directorate (DRFiP). €300,000 of this amount were received in the name of other companies. The unduly received funds were then transferred to bank accounts held abroad.

Ms A had been known to the police for fraud offences since 2006. Company X had filed 16 advance hiring notices since 2017 showing that it had between four and eight employees. Strangely, the €150,000 in benefit requested for its employees were not credited to company X’s bank accounts but to the personal account of its manager, Ms A. Concurrently, company X’s bank account was credited with 15 payments totalling €300,000 whose descriptions show the names of three other companies.

Part of the funds received by company X and Ms A was used to settle personal debts. Another part was transferred to accounts held by Ms A in EU Member States. One of these accounts was used as a transit account towards North African countries to pay for IT and consulting services. At Tracfin’s request, funds were seized in France and in two non-EU countries from transit accounts held within the EU and in the country where the funds were ultimately destined.

Referral of this case to the Court of Justice led to the accused being placed on remand for money laundering and conspiracy to defraud. Several tens of thousands of euros were subject to criminal seizures. Ms A risks up to ten years in prison and a fine of one million euros.

Warning signs:

– Receipt of part of the funds on the manager’s personal account – Description of the transfer for the benefit of a company other than the one receiving the funds

– Transfer of part of the benefit received to an account held abroad CASE STUDY 1: Short-time working fraud, criminal seizures with the perpetrator being placed on remand

Personal bank account

Mrs AManager

€150kShort-time working

benefit

Company X

Company X’s bank account

Benefit in the name of three other companies received on company X’s bank account

€300kShort-time working

benefit

Settlement of personal debts

Mrs A’s personal bank accounts

Benefit received on behalf of company X on the manager’s personal account

Transit account North Africa

Known to the police for fraud since 2006

Country (EU)

Seizure of part of the funds following a proposal from Tracfin

TR

AC

FIN

- M

L/T

F R

ISK

TR

END

S A

ND

AN

ALY

SIS

IN 2

019-

2020

18

Tracfin has cutting-edge expertise to tackle all forms of tax evasion In 2019, the proportion of STRs with a direct or indirect bearing on tax evasion accounted for around 30% of reporting flows. The number of information notes sent by Tracfin and concerning tax evasion offences was up 15% in 2019.19 In the reporting flows, the most frequent forms of evasion were undeclared business activity, under-declaring company turnover, possession of undeclared foreign bank accounts or assets, concealed gifts and reducing wealth tax, and then property wealth tax, liability.

Whilst tax evasion may be an exclusive offence, it often underlies the main violation. In the first case, Tracfin reports the matter to the tax authorities; in the second, the report is sent to the courts.

To heighten coordination between the departments involved in fighting tax evasion, a task force focusing on tax intelligence was set up in October 2019 at the Ministry for the Economy, Finance and the Recovery.20 The task force has members from the National Tax Investigation Directorate (DNEF), the National Directorate for Customs Intelligence and Investigations (DNRED) and Tracfin. It is tasked with fostering the circulation of information that may be of use in identifying complex tax evasion arrangements.21 Its operational structure, comprised of representatives designated within the three departments, centralises all exchanges and disseminates information concerning targeted cases to the field operatives.

Value added tax (VAT) fraud and scams cause major losses for the public purse Tracfin’s work to combat VAT fraud is essentially focused on recently set up businesses which receive VAT credit refunds for fairly small amounts and which, subsequently, file further applications. The suspicion of fraud is raised by the immediate transfer of these funds to a bank account held abroad. Tracfin aims to allow for upstream intervention to rapidly interrupt the VAT refund chain.22

Carousel fraud is one of the procedures that is the most-used by fraudsters. The circuit for this fraud involves setting up a chain of companies in a number of EU Member States which make intra-Community acquisitions and supplies, or imports and exports, between themselves. These companies artificially generate entitlement to deduct VAT through so-called “letterbox” shell companies which create fictitious VAT by means of a circuit of false invoices. The arrangements used by the fraudsters have become increasingly complex and use a host of shell companies with an ever-shorter lifespan.

The anti-VAT fraud system becomes stronger every year. An operational interministerial coordination structure, called the “VAT task force” was set up in 2014 and is primarily responsible for steering the fight against VAT fraud with an eye to coordinating and improving performance levels. Tracfin takes part in the task force’s work, alongside tax and customs officials, and representatives from the Ministries of the Interior and Justice.

19. Tracfin, 2019 Annual Report, July 2020, pp. 75 to 76.

20. Ministry for Government Action and Public Accounts when the task force was set up.

21. Government, Bilan 2019 de lutte contre la fraude et renforcement du civisme fiscal, February 2020 (in French).

22. TRACFIN, Rapport annuel d’activité 2019, juillet 2020, p. 78.

TR

AC

FIN

- M

L/T

F R

ISK

TR

END

S A

ND

AN

ALY

SIS

IN 2

019-

2020

19

CASE STUDY 2

Conspiracy to commit VAT fraud through a network of companies set up using fake documents and an e-money institution Tracfin uncovered a series of fraudulent VAT refunds based on a network of 500 fictitious companies set up using fake documents and identity theft. The fraud was scaled up in several layers:

– First, an initial group of companies was registered with commercial court registries. To do so, they used fake ID documents and produced fund deposit certificates that usurped the capacity and names of members of the same notary’s practice

– Once set up, these companies filed VAT credit refund applications using false invoices. This process continued until the first rejection decisions by the tax departments.

– The funds received financed the registration of new companies which repeated the same procedure

– The funds were then transferred to the accounts of an e-money institution operating in France under the freedom to provide services regime. This institution was managed by Mr A, who had been targeted by a Europol request in 2015 for fraud and who was known to the police for a number of suspicious financial transactions. Mr A and certain members of this institution could have been at the origin or could have facilitated the laundering of the funds received by this network of shell companies.

Warning signs:

– Use of fake documents and identity theft to set up companies – VAT credit refund applications using false invoices – Part of the funds received for VAT credit refunds is used to set up new companies

TR

AC

FIN

- M

L/T

F R

ISK

TR

END

S A

ND

AN

ALY

SIS

IN 2

019-

2020

20

CASE STUDY 2: Conspiracy to commit VAT fraud through a network of companies set up using fake documents and an e-money institution

First group of network companies EME

E-money institution Operating in France under the freedom

to provide services regime

Identity theft Fake ID documents

Commercial CourtsRegistration

Using false invoices

Refund applications

VAT credits

New group of network companies

Identity theft Fake ID documents

Registration

Funds received

Funds received

Bank accounts

Domiciled

Mr A

Targeted by a Europol request in 2015 for fraud and known to the police Could facilitate, via his e-money institution, the laundering of the funds fraudulently received by the network of companies

Manager

Commercial Courts

Risks in the life and non-life insurance segmentsThe entire life and non-life insurance sector is covered by the AML/CFT system pursuant to Article L.310-1 of the French Monetary and Financial Code. The Unit exercises particular due diligence in respect of transactions concerning life insurance policies, including redemption of such policies.

Life insurance policies can be used as leverage to commit different types of fraud such as tax evasion, abuse of weakness or scams. These may take the following forms: – Laundering the proceeds of tax evasion by investing in life insurance policies.

The laundered funds are usually held abroad and have not been declared to the French tax authorities.

– Fraud related to searching for the beneficiaries of life insurance policies: one or more individuals pretend to be lawyers or insurance companies from which they steal the logo. They contact individuals and wrongfully inform them that they are the beneficiaries of the life insurance policy of a person who has died. They then ask the alleged beneficiaries to send their bank details, a copy of an ID document and to pay administrative charges.

– Redemption of life insurance policies by elderly persons who are victims of abuse of weakness

– Redemption of a life insurance policy under cover of a disguised redundancy to benefit from the provisions of Article 125-0 A of the French General Tax Code (CGI)

CASE STUDY 3

Suspected tax evasion as part of the redemption of a life insurance policyAs part of the redemption of one of their life insurance policies, Mr A and his wife, Mrs B, received several transfers for a total of €600,000. The capital gains on redemption of this policy amounted to €65,000 which was subject to €2,500 in social levies. As Mr A had been made redundant several months earlier, Mrs B and himself asked to benefit from the provisions of Article 125-0 A of the French General Tax Code which provides that revenue from capitalisation warrants or contracts or life insurance policies are tax exempt when their redemption is due to their beneficiary being made redundant.

Several months prior to the redemption of the life insurance policy, Mr A was hired by his wife for a very short period even though the latter had discontinued her business activity. The hiring followed very soon after by Mr A being made redundant just before the redemption of the policy appears to have been carried out with the sole aim of avoiding paying income tax.

Warning signs:

– Mr A hired by his wife who had discontinued her business activity – Hiring followed by redundancy within a short period of time – Redundancy occurring shortly prior to the redemption of the life insurance policy

TR

AC

FIN

- M

L/T

F R

ISK

TR

END

S A

ND

AN

ALY

SIS

IN 2

019-

2020

21

EXAMPLE 2: DETECTING THE LAUNDERING OF THE PROCEEDS OF ILLEGAL TRAFFICKING IS PARTLY RELIANT ON MONITORING FLOWS OF CASH

The use of cash transfers is a laundering method for all types of illegal trafficking (drugs, counterfeits, humans). Money remittance transactions enable cash to be sent to the countries of origin or transit of the goods and persons subject to the trafficking. The ringleaders use intermediaries to pay suppliers and collect the revenue generated.

Tracfin receives information on some of the transfers made to and from France by means of systematic information disclosures (COSIs) concerning money remittance transactions.23 The Unit is able to use this information to work on transactions for small amounts which would not have been subject to STRs, but which could allow for identification of cash transfer channels connected to trafficking, for the network of targeted stakeholders to be broadened and for potential international connections to be pinpointed.

The enactment of the EU’s Fifth AML/CFT Directive in French law24 bolsters Tracfin’s detection and investigation capabilities. The Unit can now send information requests concerning the persons referred to in the systematic information disclosures provided for by Article L.561-15-1 of the French Monetary and Financial Code in the same manner as those mentioned in the STRs or the information received from national government departments or foreign FIUs.

Drug trafficking, a closely monitored national threat The national risk analysis has flagged up drug trafficking as one of the largest threats in France. The French drugs market, which is one of the most active in Europe, has witnessed the arrival of organised drug crime (narco-banditisme), materialised by heightened cooperation between different types of criminals (traffickers, traditional organised crime and foreign criminal groups). Due to its geographic location and its port and airport infrastructure, France is both a drug consumption area and a transit point towards other countries.

Many vectors are involved in laundering the proceeds of drug trafficking in France as well as in the producer or transit countries. Usual methods for fund remittance, the physical transportation of cash and international transfers exist alongside more elaborate methods such as the organisation of cash collection and settlement networks or the conversion of cash into gold. The proceeds of trafficking can also feed into the underground economy, in particular undeclared work, or be laundered through property investments, takeovers of commercial companies or gambling.

23. Credit, payment and e-money institutions are bound to systematically provide Tracfin with information on money remittance transactions carried out from a cash payment or by using e-money of an amount of €1,000 per transaction or a total of €2,000 per customer for a calendar month (Articles L.561-15-1 and D.561-31-1 of the French Monetary and Financial Code).

24. Order no. 2020-155 of 12 February 2020 bolstering the French AML/CFT system and Decrees no. 2020-118 and no. 2020-119 of 12 February 2020.

TR

AC

FIN

- M

L/T

F R

ISK

TR

END

S A

ND

AN

ALY

SIS

IN 2

019-

2020

22

CASE STUDY 4

Repatriation of funds originating from suspected drug traffickingA dozen or so South American nationals living in mainland France made a large number of cash transfers that were not commensurate with their insecure financial and employment situations. Four of them were known to the authorities for multiple offences connected with the acquisition, possession, use, transportation and import of drugs (cocaine and cannabis).

Over a period of several years, the group received over €95,000 from around sixty senders based in different towns and cities in mainland France. Concurrently, the group transferred €250,000 in cash from a dozen French towns and cities to a hundred or so individuals in French Guiana. A number of these French senders and Guianese beneficiaries were known for offences against drugs legislation. Associative links were established between several individuals which revealed a network structure: money remittance transactions carried out from the same institution, use of shared telephone numbers, collectors’ homes within a close geographic radius, senders connected by common beneficiaries.

The main sender of cash to French Guiana was Ms X. She managed a number of catering businesses (bars, cafés) and travelled on a regular basis between mainland France and French Guiana. Her companies had no business activity except for atypical financial transactions: receipt of funds from companies not operating in her sector of activity, receipt of welfare benefits. Ms X’s companies appeared to have been set up solely to launder the proceeds of drug trafficking.

Warning signs:

– Cash transfers between individuals without economic reasons between areas at risk as regards drug production

– Associative links between the individuals – Physical travel between the cash transfer sending and receipt areas – Use of a company with low, or even fictitious, volumes of business activity

TR

AC

FIN

- M

L/T

F R

ISK

TR

END

S A

ND

AN

ALY

SIS

IN 2

019-

2020

23

Mrs X

French Guiana

South American nationals

€95k

Potential injection of funds of criminal origin

Manager

Catering company

€250k

Criminal records for drug-related offences

Physical travel

CASE STUDY 4: Repatriation of funds originating from suspected drug trafficking

Criminal records for drug-related

offencesCriminal records for drug-related offences

The fight against counterfeiting, a challenge for the protection of consumers and intellectual property rights Counterfeiting involves reproducing, imitating or using an intellectual property right, such as a trademark, patent, drawing, model or work, without its owner’s authorisation. It affects all types of products, including clothing, fashion accessories, mobile phones, medicinal products or car parts. At European level, it is estimated that, between 2012 and 2016, the trade in counterfeit products accounted for 6.8% of imports and caused tax losses of €16.3bn every year.25 France is thought to be one of the countries most affected by sales of counterfeits from Asia or from Italian mafia networks, in particular the ‘Ndrangheta.

It is hard to detect underlying networks due to the large number of cash transactions in the illegal trade in counterfeit products. But, the huge increase in online sales of counterfeits raises the core question of the accountability of digital platforms in the prevention, detection and dissemination of counterfeit content. As there are no binding obligations, the majority of platforms do not currently take action in this respect. The emergence of counterfeit trafficking on e-commerce platforms and the subsequent use of electronic payments via payment service providers (PSPs) nevertheless open up broader detection channels for financial institutions if due diligence requirements are complied with across the entire payment chain.

Financial institutions are alerted when all or some of the following signs appear: – Unusually large financial flows on online sales platforms – Use of several foreign PSPs to make it more difficult to track flows – Company’s corporate purpose related to the types of goods susceptible to

counterfeiting (e.g. “retail clothing sales”) – Financial links with individuals or legal entities based in a country “at risk”

as regards counterfeiting – For an individual, financial movements incommensurate with the declared lifestyle – For a legal entity, financial flows inconsistent with the declared business activity

25. Government Audit Office, La lutte contre les contrefaçons, March 2020 (in French).

TR

AC

FIN

- M

L/T

F R

ISK

TR

END

S A

ND

AN

ALY

SIS

IN 2

019-

2020

24

CASE STUDY 5

Network laundering the proceeds of suspected counterfeit product trafficking A group of a dozen individuals, with insecure employment and financial situations, were involved in the transfer and receipt of cash totalling almost €300,000 over a 20-month period. The transactions were carried out between various French départements and were destined for country A which was notorious for manufacturing counterfeit goods. The individuals in question had already carried on a retail activity or kept stands on markets; one of them was also known to the customs authorities for repeat counterfeit selling offences.

The group received cash from a hundred of so different individuals who were all based in France. A number of them were known for violation of anti-counterfeit legislation, such as the possession and transportation of counterfeit goods, tobacco smuggling or possession of counterfeit or forged money. One of the senders was identified on social media accounts set up especially for the sale of counterfeits. The collected funds were then transferred to around fifty individuals in France, several of whom were known for counterfeit selling offences. Within the network, Mr J appeared to have a key role both in terms of the proportion of amounts in cash handled by him and his presence in country A. His bank account was also credited with cash payments for a total of €150,000 without any justification of the origin of the funds.

The group was suspected of trafficking counterfeit products as part of a structured network in France which could have been acting as a purchasing platform in relation with country A, enabling supplies to be made to a number of French cities.

Warning signs:

– Inconsistency between the amounts of transferred funds and the individuals’ declared income

– Connection between the individuals (common senders and beneficiaries, transfers made from the same counters)

TR

AC

FIN

- M

L/T

F R

ISK

TR

END

S A

ND

AN

ALY

SIS

IN 2

019-

2020

25

Markets, social media, e-commerce platforms

Network of collectors

CASE STUDY 5: Network laundering the proceeds of suspected counterfeit product trafficking

Mr J

Country A

Country “at risk” as regards counterfeiting

1

Counterfeits?

3

4

Handling counterfeits?

2

Individuals

€300k

EXAMPLE 3: THE MAIN MONEY LAUNDERING TRENDS MAKE ACTIVE COOPERATION BETWEEN TRACFIN AND ITS FOREIGN COUNTERPARTS ESSENTIAL

Reporting entities are bound to send STRs to the FIU of the country in which they are based. This territorial notion is supplemented by the related requirement of sharing and comparing information between FIUs. As part of these exchanges, the FIUs must use safe communication channels and are encouraged to use FIU.net, a secure and decentralised network for exchanging operational data between FIUs of EU Member States. To allow for reliable, operational and effective exchanges, Tracfin has worked in the area of bilateral relations to execute cooperation agreements with its foreign counterparts, including European ones.

Heightening cooperation between national FIUs is a strategic imperative of the European Council. The fifth Anti-Money Laundering Directive 2018/843, which was enacted in French law in February 2020, aims to improve operational cooperation between national FIUs. There is no doubt that close international cooperation is now vital.

Specifically, international cooperation can be effectively leveraged against terrorism and financial crime. Cross-border cooperation between Tracfin and other FIUs covers very broad issues such as tax evasion and laundering its proceeds, fraud and laundering its proceeds and terrorist financing.

TR

AC

FIN

- M

L/T

F R

ISK

TR

END

S A

ND

AN

ALY

SIS

IN 2

019-

2020

26

Unsolicited reports sent by the FIUs to Tracfin provide crucial information as the internationalisation of financial circuits is on the rise. Reporting entities experience more problems in detecting international financial circuits, especially when the latter are restricted to an approach by departure or arrival channel in France. As a result, international cooperation enables the information reported by the entities to be substantiated and leads to investigations being sent to the courts or to other departments.

INSTITUTIONAL COOPERATION BETWEEN TRACFIN AND THE FINANCIAL INTELLIGENCE UNIT (FIU) OF THE NETHERLANDS CONTRIBUTES TO COORDINATION OF EUROPEAN FIUS

Hennie Verbeek-Kusters, Head of the FIU of the Netherlands

In July 2019, Hennie Verbeek-Kusters, Head of the Dutch FIU and the Head of Tracfin’s International Department, were elected to represent the FIUs of the EU and the European Economic Area (EEA) on the Egmont Committee (equivalent of the Egmont Group’s board).

In this respect, they organise, at each Egmont Group meeting (twice yearly) and on the fringes of each meeting of the EU FIUs Platform in Brussels (four times per year), a regional meeting of the FIUs of the Egmont Europe I region. The meeting deals with Egmont Group news related to the Committee’s work such as the review of the IT tool which enables the member FIUs to exchange information. The projects handled by European FIUs within the Egmont Group’s various Working Groups, for which contributions are sometimes expected, are also discussed. Hennie Verbeek- Kusters considers that “these regional meetings are crucial moments in the functioning of the Egmont Group; they enable the FIUs of each region – which have similar features and face similar challenges – to discuss operational issues of joint interest, such as bolstering the capabilities of FIUs to combat the use of virtual assets in money laundering or terrorist financing scenarios”. In this respect, the Dutch and French FIUs organised a workshop, which took place in Brussels in

December 2019, to present their respective working methods and the resources used by their specialists to examine transactions carried out using blockchain, not only with the aim of promoting best practices but also to flag up the scope for progress in cooperation between FIUs in the field of crypto-currencies.

More broadly, Ms Verbeek-Kusters and Tracfin’s International Department are looking to heighten coordination and harmonisation of the stances of European FIUs on all European subjects of common interest and, in particular, as part of the many discussions undertaken in wake of the European Commission’s publication of its anti-money laundering “package” in July 2019 and its action plan in May 2020. They took the initiative of drafting a number of “non-papers” which set out constructive and bold proposals from European FIUs to outline a future “support and coordination mechanism” for FIUs which has been called for by the Commission and the European Parliament. “It is vital for European FIUs to take an active part in these discussions to help, especially by making the European institutions aware of the operational reality of their day-to-day operations, strengthen their ability to collectively combat money laundering and terrorist financing”, said the Head of the International Department. Against this backdrop, European FIUs are advocating setting up a network of FIUs which would allow for greater consistency in European financial intelligence strategy and would ensure operational cooperation between FIUs by, for instance, promoting the standardisation of certain practices and resources used by the latter.

TR

AC

FIN

- M

L/T

F R

ISK

TR

END

S A

ND

AN

ALY

SIS

IN 2

019-

2020

27

CASE STUDY 6

Identification of potential fraud due to reports from a FIUFInformation received from one of Tracfin’s partners showed that a company trading in IT components (company A), which was based in a neighbouring country (country A) and managed by Ms X, a French national who lived in France, received a large number of transfers from French individuals on a number of bank accounts held in country A. Concurrently, another report revealed that French individuals were also transferring funds to another company (company B) which sold software, was registered in another EU Member State (country B) and was also managed by Ms X.

The funds sent by the individuals to these two companies, which sometimes represented very large amounts, appeared to be for investments in crypto-assets which are allegedly highly profitable. On a mirror website, which was cloned from the company’s official site, unknown operators offered potential clients based in France the opportunity of making financial investments by leading them to believe that they were visiting a website specialising in crypto-asset investments.

As it turned out, the returns were low, despite aggregate investments of €3m. Companies A and B then transferred all the funds received to foreign companies based outside the EU or in Asia and whose corporate purpose was not connected with the crypto-asset sector.

The large overall amount of these transfers abroad over a short period of time, and the number of contributors and beneficiaries abroad led to suspicions that there was a huge fraudulent network at transnational level based on promises of very high returns on an intangible product.

TR

AC

FIN

- M

L/T

F R

ISK

TR

END

S A

ND

AN

ALY

SIS

IN 2

019-

2020

28

French individuals investing in crypto-assets

Company A

Company B

Country A

Country B

Manager

Mrs X

Bank accounts held in country A

Banks accounts held in country B

Companies based outside the EU or in Asia and not

specialised in the sale of crypto-assets

Transfer of all the fraudulent funds

Transfer of all the fraudulent funds

€3m

Unknown operators in contact with potential investors via a mirror website for

companies A and B

CASE STUDY 6: Identification of potential fraud due to reports from a FIU

An effective anti-tax evasion mechanism International cooperation is a particularly effective means of fighting tax evasion. Within the EU, organising financial arrangements for the sole purposes of tax evasion has been made easier by the setting up of the SEPA which has standardised payments and facilitated the opening of bank accounts in all the area’s countries.

A number of FIUs, which were previously reluctant to disseminate tax-related information, have made a U-turn. This has been materialised by the stepping up of international cooperation in this field.

Unsolicited reports from FIUs enable Tracfin to identify assets held by French residents that have not been declared to the French tax authorities. This information can substantially clarify facts already set out in the STRs sent by the reporting entities. This means that the reports can lead to information being sent to the French tax authorities and to tax audits.

CASE STUDY 7

Unsolicited information from a FIU leading to a report being sent to the French tax authorities Mr Z, a resident of France for tax purposes, had autoentrepreneur status for his business activity as a repairman. He was known to the police for acts of violence, fraud and damage to the property of third parties. As part of his activity, he was involved in numerous scams on the Internet. A number of testimonies from individuals attested to improper practices: prohibitive prices, damage to property when carrying out repairs. He was also known to the tax authorities which carried out two audits after having discovered foreign bank accounts that had not been declared by Mr Z.

In an unsolicited report, the FIU of country A advised Tracfin that Mr Z had three bank accounts in that country through which almost €2m had transited since 2010. According to Mr Z, the majority of this amount came from his business activity which was, however, carried on in France. The accounts were mainly credited by paying in cheques made out to Mr Z in payment of invoices related to his activity. Almost €300,000 had been collected since 2019 whereas Mr Z only declared income of €20,000 for that year to the tax authorities. Mr Z’s bank accounts in country A were therefore used to conceal a large proportion of income from his activity in France.

Tax audits may be followed by searches. Cooperation between Spain’s Financial Intelligence Unit (SEPBLAC) and Tracfin led to tax searches as part of tax evasion cases.26 26. For more information

on this case, see Tracfin, ML/TF risk trends and analysis in 2018/2019 report, December 2019, p. 37.

TR

AC

FIN

- M

L/T

F R

ISK

TR

END

S A

ND

AN

ALY

SIS

IN 2

019-

2020

29

CROSS-BORDER COOPERATION FOR AML/CFT ISSUES BETWEEN FRANCE AND SPAIN

Cross-border cooperation between FIUs which face AML/CFT issues with similar features is vital to enable rollout of prevention measures or penalties (judicial investigations, tax searches, seizures). Collaboration between Tracfin and SEPBLAC, Spain’s FIU, which was formalised by a bilateral cooperation agreement executed in 1996, plays an active role, through exchanges of information, in identifying suspected cross-border ML/TF.

These exchanges of information cover various tax evasion issues: avoidance, concealing income, doubts as to the residence for tax purposes of the individual in question. They also enable circuits for laundering the proceeds of various fraudulent activities such as false transfer orders to be brought to light and for suspicions of terrorist financing to be confirmed or disproven when suspect financial transactions involving nationals of both countries are identified.

INTERVIEW WITH SEPBLAC

“In 2019 SEPBLAC received 57 requests for information from Tracfin (which represents a 60% increase compared to the 34 received in 2017) and 3 spontaneous disclosures (4 in 2017 and 5 in 2018). Meanwhile, SEPBLAC made 11 requests for information to Tracfin and shared 28 reports in the form of spontaneous disclosure.

Year after year the level and quality of the cross-border collaboration between SEPBLAC and Tracfin has drastically improved. The exchange of information between our FIUS is smooth, effective and does not present any specific problem. Currently Tracfin constitutes a great example of how international exchange of information should work.

– How is SEPBLAC organised to deal with cooperation requests from foreign counterparts and how do you share with them spontaneous reports? How many people are conducting investigations and more particularly from an operational perspective, how many people are dedicated to international cooperation?SEPBLAC is organized in three main coordination areas: Financial Intelligence, Supervision and Inspection, and Planning. Likewise, the Central Financial Intelligence Brigade of the National Police, the Investigation Unit of the Civil Guard and a Unit of the State Tax Administration Agency (AEAT by its initials in Spanish) are also assigned to SEPBLAC. SEPBLAC is an inter-agency body in which, under a single direction, professionals from five different State institutions (Ministry of Economic Affairs and Digital Transformation, Bank of Spain, Tax Administration (which includes Customs Surveillance), National Police and Civil Guard), perform their AML/CFT functions taking stock of these synergies.Around 60 employees are currently conducting financial analysis from an operational perspective. This figure includes officers from National Police, Guardia Civil and the Tax Administration. The team devoted to the exchange of information at international level is composed of 6 analysts.

– What are the main ML/TF typologies observed by SEPBLAC which involve French nationals or the French territory? What are the most common typologies on which SEPBLAC questions Tracfin?« Main typologies involving French nationals or the French Territory include intra-community VAT, fraud taxes schemes, frauds and scams and

TR

AC

FIN

- M

L/T

F R

ISK

TR

END

S A

ND

AN

ALY

SIS

IN 2

019-

2020

30

in a lesser extent, foreign PEPs/corruption and terrorism financing. Half of the requests for information remitted by SEPBLAC to Tracfin in 2019 had origin in ongoing investigations being conducted by the Spanish LEAs whilst the other half came from SARs. No common typologies patterns could be observed since the requests were related to a wide range of activities and underlying offences, including drug trafficking, organized crime, robbery, scams, terrorism financing or the intensive use of cash.

– What are the main criteria to launch an investigation by SEPBLAC, based on a report shared by Tracfin? What are the strengths on which SEPBLAC can rely to initiate in-depth investigations? Did SEPBLAC ever refer to the prosecuting authorities based on a report shared by Tracfin? If yes, on what typologies?According to our files, in 2019 SEPBLAC received 3 spontaneous reports from Tracfin. From these one was filed as the information provided had already been analyzed as a consequence of a previous SAR, another involving a BEC (business email compromise)27 fraud was disseminated to Guardia Civil and the last one, referring a tax matter, was shared with the Tax Agency. The information received from Tracfin disclosures (as any other operational information received by SEPBLAC) is treated, according to a risk approach, and categorized with a level of risk that will determine the urgency of the dissemination. The information may have an urgent treatment, depending on aggregate risk elements (associated predicate offences, main ML/TF risks, links to ongoing LEA investigations, etc.).

In 2019 SEPBLAC received 57 requests for information from Tracfin relating a great variety of suspicious activities, in many cases involving bank accounts located in Spain. According to the nature and relevance of the criminality involved, the possible links with other analysis being conducted at SEPBLAC or with ongoing LEAs investigations and the utility of the information provided, an assessment is made to establish an eventual interest of the whole intelligence gathered by the international team (not only the information coming from Tracfin but also that may be obtained from the variety of sources available to us). In that sense, a great deal of the information contained in your requests was shared with the Spanish competent authorities, mostly National Police and Civil Guard but also the Tax Agency and in a lesser extent, the Special units within National Police and Civil Guard dealing with terrorism financing matters. At least in 2019 none of the intelligence reports including information from TRACFIN was disseminated to the prosecuting authorities.

– What are your priorities on a short term and mid-term perspective and what are the ML/TF issues on which Tracfin could provide support?Our priorities comprise a variety of typologies (organized crime, drug trafficking, all types of fraud/scams, corruption, human trafficking...), having present that the fight against terrorism financing is a key priority to SEPBLAC and that enhancing the level of understanding of the risks associated with new financial technologies is also a priority for us in the short term”.

27. Attempted spamming or phishing against a business.

A key measure in the fight against terrorist financing International cooperation for fighting terrorist financing is crucial: information exchanged between FIUs enables individuals with ties to extremist or terrorist organisations to be identified, for the links between these individuals to be pinpointed and for the connections of the networks to which they are affiliated to be highlighted.

When unsolicited reports from FIUs concern French nationals or individuals residing in France, who may be participating in a terrorist organisation, they enable the Unit to cross-reference these reports with other information. The Unit may, where applicable, share this intelligence with other national departments involved in combating terrorist financing.

TR

AC

FIN

- M

L/T

F R

ISK

TR

END

S A

ND

AN

ALY

SIS

IN 2

019-

2020

31

2T

RA

CFI

N -

ML/

TF

RIS

K T

REN

DS

AN

D A

NA

LYSI

S IN

201

9-20

20

32

MITIGATING VULNERABILITIES

A REVIEW OF THREE SECTORS THAT CARRY HIGH ML/TF RISKS

TR

AC

FIN

- M

L/T

F R

ISK

TR

END

S A

ND

AN

ALY

SIS

IN 2

019-

2020

33

TR

AC

FIN

- M

L/T

F R

ISK

TR

END

S A

ND

AN

ALY

SIS

IN 2

019-

2020

34

PROPERTY, A SECTOR IMPLICATED IN ALL THE STAGES OF MONEY LAUNDERING

Property investments are an important money laundering vector in France because of the specificity of certain market segments such as the Parisian housing market, which is driven by upward price pressure, and prestigious real estate in regions with high tourist potential such as the Côte d’Azur and certain mountain resorts.

However, ML risks in the property sector are not limited to these two segments. Tracfin has identified money being laundered through the purchase of mass-market suburban residential properties, financed by profits from drug trafficking, bribery of foreign public officials or unusual financial practices such as tontines.28 Commercial properties also offer opportunities for money-laundering networks.

The real estate sector involves a variety of professionals, some of whom are particularly exposed to ML risks. This is particularly true of property developers, property dealers and certain specialised investment funds registered abroad. The latter use complex arrangements to conceal the beneficial owner of the property and the origin of the funds used for its acquisition. The variety of professions present in the real estate market exposes this sector to all three money laundering phases: placement, layering and integration.

Risks exist at all stages of the lifecycle of a property project: during the award of property contracts (bribery of public officials), during the construction phase (use of undeclared labour by construction companies), during property transactions or leases (concealment of profits from various crimes, manipulation of property prices, fraudulent use of tax exemption schemes, Ponzi schemes), or when taking out a property loan (use of false documents).

Notaries and estate agents, who are subject to AML/CFT obligations, play a key role in detecting money laundering schemes in the property sector. TRACFIN has noted that their involvement increased in 2019. Notaries submitted 1,816 STRs (a 23% increase year-on-year), while property professionals submitted 376 (a 37% increase). However, the volume of information reported remains modest in view of the number of property transactions carried out each year in France (1,059,000 sales of existing housing between 1 October 2018 and 30 September 2019).29

A SECTOR USED TO FOSTER CONSPIRACY TO COMMIT FRAUD

Financing property transactions exposes financial institutions to lending money obtained illegally by fraudsters. The use of falsified documents concerning income and assets, or using false identity papers is frequently cited in STRs received by Tracfin.

These scams carried out by organised groups of criminals are based on an in-depth knowledge of the sector, sometimes with the backing of notaries or specialised professionals such as property dealers. The property dealer profession is not regulated by any specific legislation, and is not subject to AML/CFT reporting requirements. Nevertheless, it is a source of particularly high money laundering risk. It appears in the following typologies: – In association with large offshore fortunes or members of criminal gangs seeking

to reinvest some of their gains in property in France

28. The tontine is a scheme in the form of a collective annuity association. It allows a group of people to pool financial assets that are managed by a service provider. At the end of its term, the capital and income generated by its management are divided among the surviving members of the tontine. Although the scheme is legal, its operation has the particularity of resulting in the disappearance of the assets invested by the investor, thus suggesting an attempt to conceal them. See also Tracfin, ML/TF risk trends and analysis in 2015 report, December 2016, pp. 51-54.

29. National Association of Notaries (CSN).

TR

AC

FIN

- M

L/T

F R

ISK

TR

END

S A

ND

AN

ALY

SIS

IN 2

019-

2020

35

– International corruption scenarios, compensation of dubious intermediaries or funneling money to concealed investors through the payment of economically unjustified commissions

– Mortgage fraud, misuse of company assets, carousel fraud or the use of undeclared labour for renovation works

CASE STUDY 8

Property loan fraud with the collusion of a notary’s officesMs X was an account manager at a credit institution. At the same time, she worked as a property dealer through Company M, of which she was the manager and sole partner. Ms X had personal financial connections with Mr Y, who appeared to be the de facto manager of Company M.

In the space of one year, Company M acquired nine properties for a total of €3 million without having the necessary financial resources to carry out these transactions. The properties were financed by third parties who took out mortgages with several banks using false documents such as false pay slips, false sales agreements and false deeds of purchase. The fraudulent loans were obtained with the collusion of a notary’s office, which issued certificates of authenticity for the loans. The notary’s office issued certificates of deposit of personal funds to its account, although the financial considerations could not be ascertained. It also recorded calls for funds from several banking institutions for the financing of a single property.

Unbeknownst to the lending banks, the funds were redirected from the notary’s office account to Company M. The final deeds of purchase drawn up by the notary’s office did not mention the borrowers as purchasers of the property, but rather Company M. In return, the individuals who had taken out mortgages appear to have been paid for their role in the fraud and the laundering of the proceeds by means of a low-value credit flow from the notary’s office account.