topic 9 – position sizing (weighting) · topic 9 – position sizing (weighting) on portfolio123,...

TRANSCRIPT

1

Portfolio123 Virtual Strategy Design Class By Marc Gerstein

Topic9–PositionSizing(Weighting)

OnPortfolio123,thedefaultposition-weighting(%PortfolioWeighting)forsimulationsandliveportfoliosisequal.Fromthere,unlessyouhaveaBuyorSellrulethatsaysotherwise,theweightsofcontinuously-heldpositionswillriseorfallbasedonmarketconditionsuntilyoueventuallysell,andnewpositionswillbeequallyweightedfromavailablecash.ThosewhowouldliketosetweightsmorestrategicallycandosousingFormulaWeighting.ThisTopicdiscussesstrategicconsiderationsaroundsuchchoices,andconcludewithanillustrativecasestudy.Whyuseafancyweightingprotocol?Theshortansweristhatyoudon’thavetouseFormulaWeighting:Portfolio123usershavedonewellwithourtraditional%ofPortfolioprotocolforalongtimeandcancontinuetodolikewiseindefinitelyintothefuture.Buttherearetwoveryimportantbenefitsthatcanbeachievedbygoingbeyondthat.LiquidityThisconsiderationdoesnotnecessarilyrelatetoanindividualinvestorortraderworkingwithpersonalportfolios.Butliquiditycanbeacriticaldeal-breakerforprofessionalsandotherswhoinvestlargeamounts.Assumehypothetically,atwostockprofessionalportfolio:AppleandthefictionalMicroEnterpriseswithamarketcapitalizationof$7million.(Iknowit’saweirdexample;pretenditsaniconoclastichedgefund.)

• Ifthiswouldhavebeena$10,000personalportfolio,itcouldhavebeenequallyweightedwithoutblinkinganeye.

• Butifthetotalportfoliosizeif$10million,thatwouldposeaproblem.AfullstakeinApplecouldeasilybebought.Butgettingafull$5millionpositioninMicrowouldlikelyrequiresomeSECfilings,theservicesofaninvestmentbanker,andprobablyatenderofferandallthatsortofthing.

o Soa$10millionportfolioholdingjustthosetwosecuritieswouldreallyneedtousemarketcaporsomeotherkindofsize-basedweighting(withjudiciouslysetboundarieslestthestakeinMicroroundtozero).

Ifyouaredealingwithpersonalportfolios,suchliquidity-orientedconsiderationsarenotlikelytoberelevant(unlessyou’reamongthosewholiketopushagainstthelimitsonwhatyoucantradeatthelowerendofthemarket).Thisdoesnot,necessarilyexcludeyoufromusingweightingbasedonmarketcaporsomeothersize-relatedconceptlikeEV,Assets,Revenues,etc.Itdoes,however,meanyou’dbedoingsoforadifferentsortofreason,namelystrategic,orconfidence-basedweighting.

2

Ifliquidityisparamount,youwillmostlikelybeforcedtodosomesortofsize-basedweighting.Themostpopularsuchapproachismarketcapitalizationweighting.Oryoucan,ofyouwish,pickanothermetric(suchasCompanySales)thatisalsolikelytofunnelthelargestportionsofcapitaltothelargestmostliquidissues.ConfidenceLet’sstartwiththemostbasicfactofweighting(asidefromliquidity):Ithastodowithconfidence.Ifyouhaveperfectconfidenceinyourabilitytopickstocks,youneednotthinkaboutweightingorevendiversification.Theonlyrationaldecisionwouldbetoinvest100%ofyourcapitalinyourfavoriteasset.Nobodydoesthatbecausenobodyhasperfectconfidenceinanything.Ifyouhaveequaldegreesofconfidence(orfear)inallyourpositions,thenequalweightingisthemostlogicallyproperwaytoallocateaportfolio.Andthatisveryoftenaperfectlyfinewaytogo.ModernPortfolioTheory(MPT),aboutwhichmuchhasbeenwrittenlately,introducedascientificapproachtoevaluatingvaryingdegreesofconfidence.Itboilseverythingdowntoexpectedreturnoffsetbyexpectedrisk(variation)ofeachsecurity,andintheportfolioasawhole(1+1doesnotnecessarilyequal2;weintroducingcovariance-correlation,thedegreesofriskeachsecurityhasrelativetoothersintheportfolio)andtries,withformulationsthatlookliketheycamedirectlyfromHomer’squill(mathequationswithlotsofGreekterms),tocomeupwiththebestofallpossible(“optimal”)weightings.Wedon’tdoMPTonPortfolio123.Butithelpssetacontextforwhatwe(andothers)aretryingtodowithourweightingalgorithms.Ittakesmodelbuildingtostep2.

• Step1isanattempttogetanedgeoverapassivesolutionthroughthedecisionswemaketoincludesomestocksandexcludealltherest.Thisalonecanaccomplishquitealot,asmanyPortfolio123usershaveexperienced.Soagain,useoftraditional%PortfolioWeightingisaperfectlyfinechoice.

• Step2takesituptothenextlevelbylookingforwaystoamplifyourstrategybygivingmoreweighttostocksinwhichwe’remoreconfident.

Sowhatsortsofthingsmightjustifyhigherlevelsofconfidence?Manyassumebiggerisbetter–andthisisnotassimplisticasitmayseematfirstglance.The“better”islikelytomanifestmoreontherisksideoftheequationthaningrowth(thebiggerthecompany,theharderitcanbetopostincrementalgrowth;that’slife,notjustinbusinessbutineverything).Biggercompaniesarebetterabletoabsorbfixedcosts,thusmakingtheirbottomlineslessvolatileforagivendegreeofrevenuefluctuation.Also,biggerfirmsaremorelikelytobebetterdiversifiedintermsofintermsofbusinessline

3

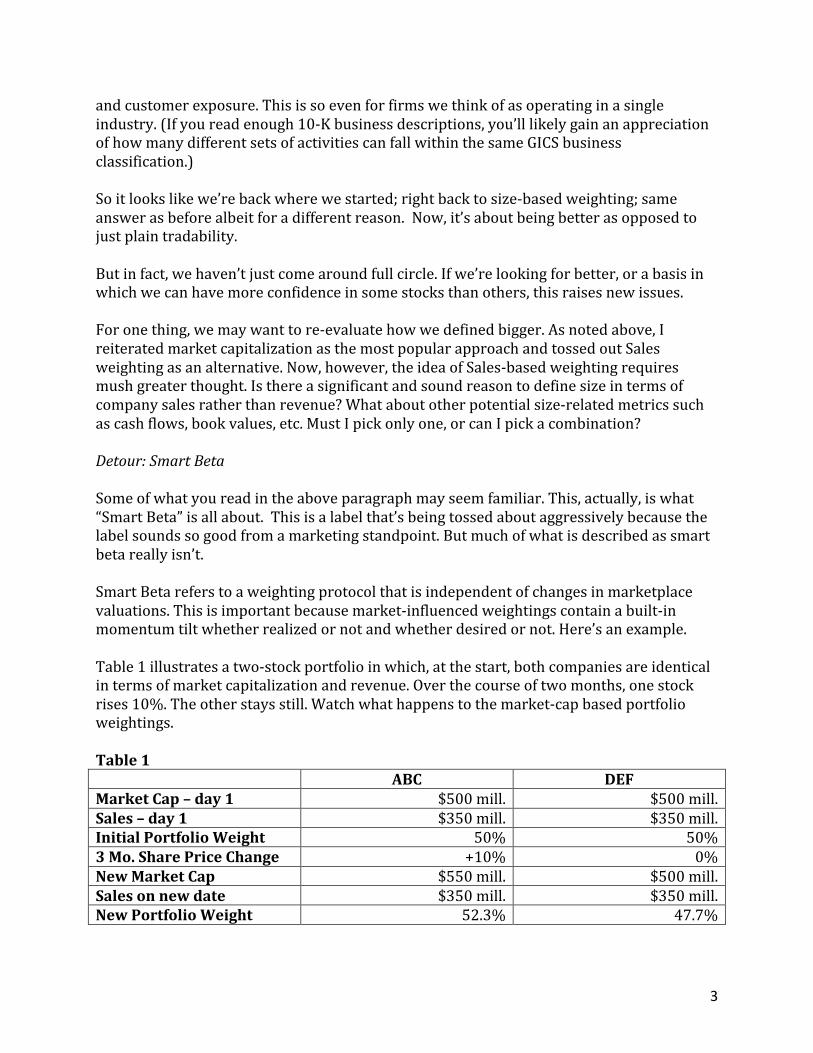

andcustomerexposure.Thisissoevenforfirmswethinkofasoperatinginasingleindustry.(Ifyoureadenough10-Kbusinessdescriptions,you’lllikelygainanappreciationofhowmanydifferentsetsofactivitiescanfallwithinthesameGICSbusinessclassification.)Soitlookslikewe’rebackwherewestarted;rightbacktosize-basedweighting;sameanswerasbeforealbeitforadifferentreason.Now,it’saboutbeingbetterasopposedtojustplaintradability.Butinfact,wehaven’tjustcomearoundfullcircle.Ifwe’relookingforbetter,orabasisinwhichwecanhavemoreconfidenceinsomestocksthanothers,thisraisesnewissues.Foronething,wemaywanttore-evaluatehowwedefinedbigger.Asnotedabove,IreiteratedmarketcapitalizationasthemostpopularapproachandtossedoutSalesweightingasanalternative.Now,however,theideaofSales-basedweightingrequiresmushgreaterthought.Isthereasignificantandsoundreasontodefinesizeintermsofcompanysalesratherthanrevenue?Whataboutotherpotentialsize-relatedmetricssuchascashflows,bookvalues,etc.MustIpickonlyone,orcanIpickacombination?Detour:SmartBetaSomeofwhatyoureadintheaboveparagraphmayseemfamiliar.This,actually,iswhat“SmartBeta”isallabout.Thisisalabelthat’sbeingtossedaboutaggressivelybecausethelabelsoundssogoodfromamarketingstandpoint.Butmuchofwhatisdescribedassmartbetareallyisn’t.SmartBetareferstoaweightingprotocolthatisindependentofchangesinmarketplacevaluations.Thisisimportantbecausemarket-influencedweightingscontainabuilt-inmomentumtiltwhetherrealizedornotandwhetherdesiredornot.Here’sanexample.Table1illustratesatwo-stockportfolioinwhich,atthestart,bothcompaniesareidenticalintermsofmarketcapitalizationandrevenue.Overthecourseoftwomonths,onestockrises10%.Theotherstaysstill.Watchwhathappenstothemarket-capbasedportfolioweightings.Table1 ABC DEFMarketCap–day1 $500mill. $500mill.Sales–day1 $350mill. $350mill.InitialPortfolioWeight 50% 50%3Mo.SharePriceChange +10% 0%NewMarketCap $550mill. $500mill.Salesonnewdate $350mill. $350mill.NewPortfolioWeight 52.3% 47.7%

4

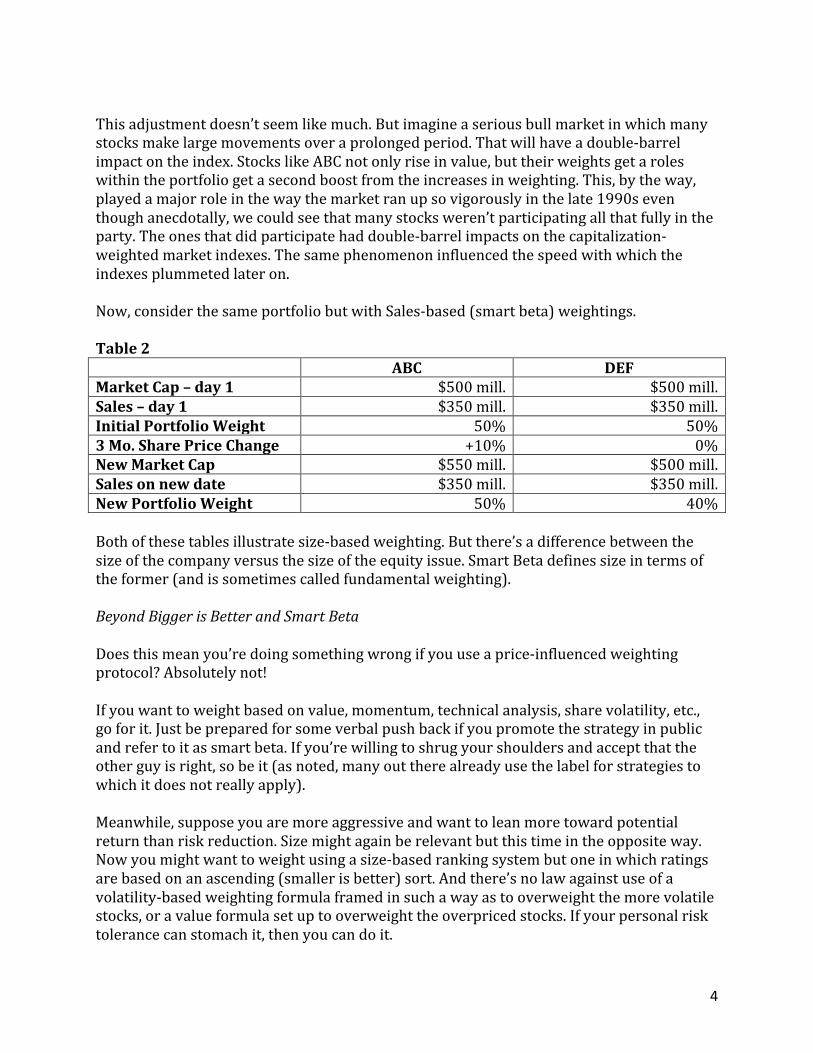

Thisadjustmentdoesn’tseemlikemuch.Butimagineaseriousbullmarketinwhichmanystocksmakelargemovementsoveraprolongedperiod.Thatwillhaveadouble-barrelimpactontheindex.StockslikeABCnotonlyriseinvalue,buttheirweightsgetaroleswithintheportfoliogetasecondboostfromtheincreasesinweighting.This,bytheway,playedamajorroleinthewaythemarketranupsovigorouslyinthelate1990seventhoughanecdotally,wecouldseethatmanystocksweren’tparticipatingallthatfullyintheparty.Theonesthatdidparticipatehaddouble-barrelimpactsonthecapitalization-weightedmarketindexes.Thesamephenomenoninfluencedthespeedwithwhichtheindexesplummetedlateron.Now,considerthesameportfoliobutwithSales-based(smartbeta)weightings.Table2 ABC DEFMarketCap–day1 $500mill. $500mill.Sales–day1 $350mill. $350mill.InitialPortfolioWeight 50% 50%3Mo.SharePriceChange +10% 0%NewMarketCap $550mill. $500mill.Salesonnewdate $350mill. $350mill.NewPortfolioWeight 50% 40%Bothofthesetablesillustratesize-basedweighting.Butthere’sadifferencebetweenthesizeofthecompanyversusthesizeoftheequityissue.SmartBetadefinessizeintermsoftheformer(andissometimescalledfundamentalweighting).BeyondBiggerisBetterandSmartBetaDoesthismeanyou’redoingsomethingwrongifyouuseaprice-influencedweightingprotocol?Absolutelynot!Ifyouwanttoweightbasedonvalue,momentum,technicalanalysis,sharevolatility,etc.,goforit.Justbepreparedforsomeverbalpushbackifyoupromotethestrategyinpublicandrefertoitassmartbeta.Ifyou’rewillingtoshrugyourshouldersandacceptthattheotherguyisright,sobeit(asnoted,manyouttherealreadyusethelabelforstrategiestowhichitdoesnotreallyapply).Meanwhile,supposeyouaremoreaggressiveandwanttoleanmoretowardpotentialreturnthanriskreduction.Sizemightagainberelevantbutthistimeintheoppositeway.Nowyoumightwanttoweightusingasize-basedrankingsystembutoneinwhichratingsarebasedonanascending(smallerisbetter)sort.Andthere’snolawagainstuseofavolatility-basedweightingformulaframedinsuchawayastooverweightthemorevolatilestocks,oravalueformulasetuptooverweighttheoverpricedstocks.Ifyourpersonalrisktolerancecanstomachit,thenyoucandoit.

5

AndaslongasPandora’sboxhasbeenpriedopen,youdoalotmore.Youcanrankbasedongrowthprospects,financialstrength,analystsentiment,valuation,...andinanycombinationsyouwish.Andrememberthe#Sector,#SubSector,#Industryand#SubIndustryparametersthatarepartoftheFrankfunction;youcanweightbasedonwhereacompanystands,notrelativetotheuniverseasawhole,butrelativetoapeergroupasyoudefineit.Sodialupthecreativityandhaveatit.Attheendoftheday,yourother-than-liquidity-drivenweightingformulacanbebasedonwhateveritisthatcausesyoutohavemoreconfidenceinsomeportfolioholdingversusothers.ImplicationsforModelDesignWithsimple%PortfolioWeighting,youapproachmodeldesignwithafour-prongedintellectualarsenal:(1)BuyRules,(2)Ranking,(4)Refreshprotocols,and(4)SellRules.Acronym:BRRS.WithFormulaWeighting,youexpandyourarsenaltofive:(1)BuyRules,(2)Ranking,(3)Weighting,(4)Refreshprotocols,and(5)SellRules.Expandedacronym:BRWRSBRRSiseasy(asstrategydesigngoes)becauseyouknowgoinginyou’llhavetouseallfourweapons,Buy,Rank,RefreshandSell.Youdon’thavethatluxurywhenconsideringuseofweights.Youcangooneofthreeways:

1. BRWRS(useallintellectualweaponsinyourarsenal)2. BRRS(youcangotraditionalwithoutthefancyweights,butnow,it’saconscious

choice,nottheonlyavailableoption)3. RWRS(eliminateBuyrulesorlimityourselfonlytothemostcursoryBuyrules,and

relymoreheavilyonweightingtocontributetoalpha).RWRSstrategiesarewidelyusedintheprofessionalarena.Traditionally,manyinstitutionalportfoliosusedS&P500mimickingasastartingpointandthenimplementedactivebullishorbearishjudgmentstooverweightorunderweightparticularpositons.SoifamanagerwasespeciallybearishaboutXYZ,whichwasweighted2.25%intheS&P500,thatsentimentwouldbeimplementednotbyeliminatingXYZbutbyunderweightingit,sayto1.00%.Andthis,bytheway,iswhyBuy-sidefolkshateitwhenSell-sideanalystssaySell.Theyknowtheycan’treallyselltoeliminatetheposition;liquidityconcernsoftencompelinstitutionstousetheS&P500orsomeotherindexasastartingpointandfinditdifficultifnotimpossibletoexplaintoclientswhyXYZisstillintheportfolio(albeitunderweighted)eventhoughit’sadog.Modernquant,factorandsmartbetaETFsdoessentiallysamething,thedifferencebeingthattheyunderweightoroverweightbasedonobjectiverulesratherthansubjectivejudgement,anditswhytoday’sactive-versus-passivedebateissostale.Activeinvestors

6

saythissortofthingispassive.Passiveinvestorssaythissortofthingisactive.Isaywhocares,itjustis.Sonow,youcandolikethebigtimepros.YoucanpickalargegrouptoowninitsentiretyandbuildanRWRSmodel,inwhichyouimplementyourstock-pickingskillsthroughweights.And,bytheway,ifyoueverdreamedofcreatingandlicensingyourownETFandgettingintothebigtime,goforit.YouhaveasmuchRWRScapabilityasanybodyoutthere.Allyouneednowistheidea.Note,though,thatyoudon’thavetogobigorgoproinordertobenefitfromRWRS.Youcandoitwithpersonal-sizedportfoliosaswell,althoughyouwillneedatleastsomecursorysetofbuyrulestodefineamini-marketwithinwhichyou’llstrategicallyweight.Let’scallthisbRWRS(withalower-caseb).Whateverchoiceyoumake,BRRS,BRWRS,RWRS,orbRWRS,it’sveryimportantthatyourchoicebeaconsciousdecision.It’sOKtochangeyourmindasyougoalongifyoufindyourinitialsetofideasisn’tquiteworking.Butyoureallymust,atalltimes,understandwhatkindofmodelyou’reworkingon.Thisisn’taPortfolio123rule.It’sruleyoushouldimposeonyourselfinordertoguardagainstinformationoverloadandhavingyourbrainspinitswayintoamigraine.EstablishingaWeightingFormulaAweightingformulacanbebasedonanythingthatisalegitimatestrategicconsiderationasdiscussedinalltheotherTopicsofthiscourse.Everythingyounowknowandeverythingyouwilllearninthefutureisonthetable.Ifyou’rebigbelieverinmomentumortechnicalanalysis,thenusethatasthebasisforyourformula.Ifexcesscashgenerationisofinteresttoyou,buildaformulaonthebasisofthat.Again,everythingyouknowandeverythingyou’lllearninthefutureisavailabletoyou.Youcanexpresssomethingasasinglefactor,asinglefunction,orasingleformula.Butifasinglefunction,factororformuladoesn’tcutit,youcanusearankingsystem.Infact,ifyoulookattheprospectusesoftoday’snouvelleETFs,you’llfindthat’swhattheyaredoing.Theyusescoresasdeterminedbymulti-factorrankingsystemsasthebasisforweighting.Soindecidingwhattodostrategically,I’llborrowawell-usedphraseyoumayhaveseenfromtherealmoflegalese:EverythingdiscussedinTopics1-8is“incorporatedhereinbyreference.”Beyondthat,however,aresomepracticalitiesthatareofspecialimportancewhenthoseformulasareusedforweighting.Youwon’twanttowindupwightanyoldsetofnumbers.You’llwanttheformula’soutputtoconsistofasensiblewell-distributedsetofnumbers.Therefor,youshouldbeespeciallysensitivetotwosetsofconsiderations.

7

1. GuardAgainstImpracticalNumbers(OutliersandNegativevalues)Let’sassumeyouwanttoweighta5-stockportfolioonthebasisoftheTTMEPSgrowth.Herearethebasics:Table3Ticker %GrowthRateABC 8.5DEF 3,745GHI 16.2JKL -5.1MNO 9.7TheDEF3,745%growthratecaneasilybecorrect.ImagineacompanywhoseEPSrisesfromapennyortwopershareinoneperiod,toarespectableprofitintheequivalentperiodayearlater.Andweseenegativegrowthratesallthetime.Wecouldeasilyaddressthesebysettingminimumandmaximumallowableweights.Indeed,theplatform’sdefaulttoazerominimumautomaticallyknocksoutnegativenumbers.Soyoucanveryeasilygetarationalandusablesetofweightsforthisportfolio.Butwoulditbeagoodsetofweights?Don’tassumesomethingisworthyofusingsimplybecauseitdoesn’tleadtoanErrormessage.It’spossibleDEFmay,indeed,bethebeststockandthatitshouldgetthehighestweight.Buthowhighshoulditgo?Bearinmindtheexactmagnitudeofthegrowthrateweseeislikelytheresultofsomethingodd,probablyawrite-offintheyear-earlierperiod,andnotsomethingthatissustainable.Dowereallywanttheweightingtoreflectthat?AnddoesitreallymakesensetozerooutJKL?Ifyou’reonthefence,let’schangetheexampletothis:Table4Ticker %GrowthRateABC -43.6DEF 3.2GHI 16.2JKL -5.1MNO -9.7Again,youcanweightthesewithoutbeingflaggedforanerrormessage,butdoyoureallywanttodothat.WhynothaveagrowthorientedportfolioinwhichJKLisweightedmoreheavilythanMNO,andmuchmoreheavilythanABC.

8

Isuggestyoubeverycarefulaboutusinganyrawnumbersorratiosasweightingfactors.IfIwereworkingwitheitherofthesestrategies,myweightfactorwouldabsolutelynotbeEPS%ChgTTM.Instead,I’dattheveryleastuseFrank(“EPS%ChgTTM”).Thatwouldgiveeachstockapositiveweightandadistributionofweightsthatisprobablymoreinlinewiththesubstanceofmystrategy.Andifthatstillleaverssomethingtobedesired(whichispossible;someitemsproducereallyextremedistributions),youcanworkwiththeZScorefunction,whichexpressesitemsintermsofhowmanystandarddeviationstheyarefromthemeanandallowsyoutotrimoutliers.UseofrawnumbersisbestreservedforthetamestdatasetssuchasMktCap,SalesTTM,andEV.Andeventhesemaynotbehaveaswellaswe’dlikeifyouapplythemtoapersonal-sizedportfolio,ratherthanasubstantialRWRSmodel.Ifyouhaven’tyetbecomeproficientinuseofFrankandZScore,thiswouldbeareallygoodtimetocatchuponthosefunctions.

2. TheSubtletiesofusingRankingSystemsYoucanusetheoutputofarankingsystem(withrankscorescalculatedbasedontheuniversebeingusedinyourmodel)asabasisforweighting.Andasnoted,thiswilloftenbeaverygoodthingtodo.Infact,ifitbecomestheonlywayyoudoit,that’sfine;you’llbeinreallygoodcompany(i.e.thenewbreedofquantportfolioandETFbuilders).Asyoumayalreadyknow,ifyouaccessarankingsystemviatheRANKfunction,you’llbeusingthesamerankingsystemthatwasusedtopicktheto10,15,20,...,Nstocksthatultimatelyareputintotheportfolio.Youcandothis.Butunderstandthiswillgiveyousomethingveryclosetoequalweightingattheoutset,sinceyourdayoneranksarelikelytobesomethingalongthelinesof99.42,99.19,.98.53,97.12,97.01,etc.Foralowturnoverportfolio,thatmayworkquitewellsinceitcanbeexpectedthattherankswillchangeovertimesoayearlater,thosesamestocksmayberanked,say,91.14,74.36,68.14,62.12,57.14and50.85.Thatmeansoverthecourseoftheyear,youwillhaveshiftedmoneyoutofdeterioratingpositionsintomoresolidones.IfyouhaveaRANK<50Sellrule,twoofthosestocksareclearlyonprobationandmaygetwhackedinthenearfuture.Isthisagoodthingtodo?Idon’tknow.Testitandsee.Themoremainstreamapproachwouldbetolookforabetter-disburseddistributionfromdayone.Todothis,avoidrepeatingyourselfbyusingRANKasaweightingformula.UseRating()instead.Thisallowsyoutomakeuseofarankingsystemthatdiffersfromtheoneyou’reusingtosortstocks.IfthesystemyouspecifyviaRating()issimilartotheonespecifiedviaRANK(e.g.,twoValue-orientedranklingsystems),youmayfindyourselfbackinthesameboat.Thebest

9

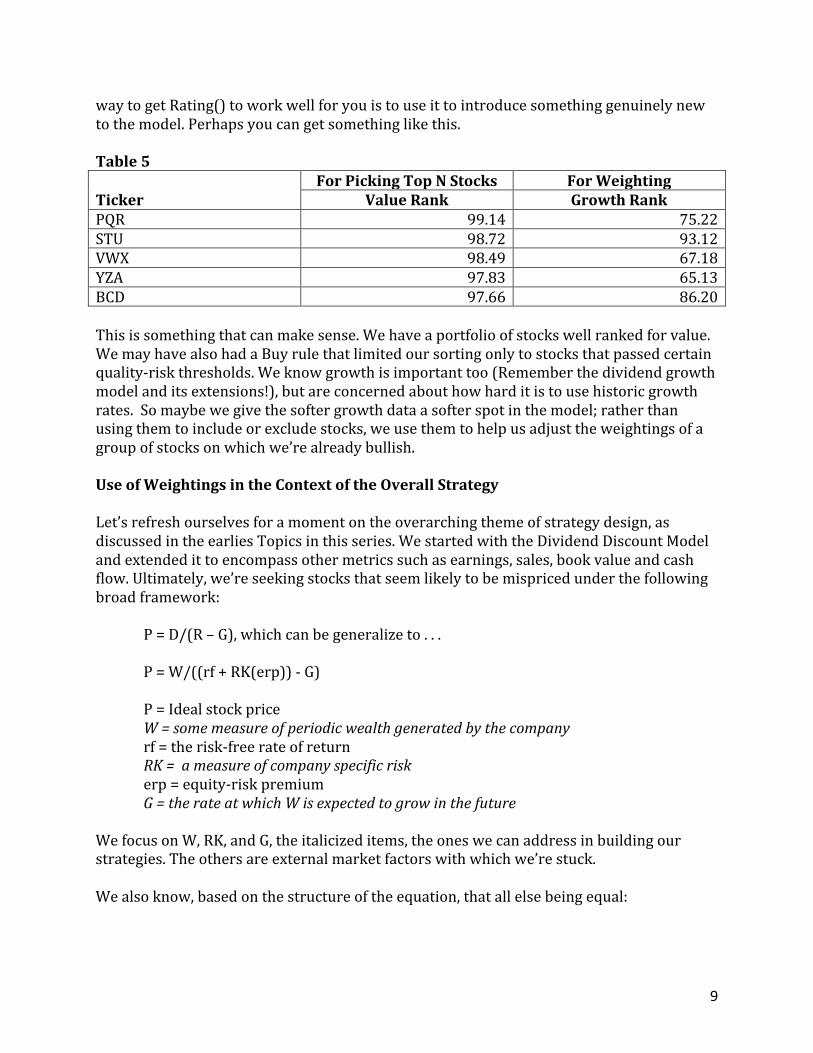

waytogetRating()toworkwellforyouistouseittointroducesomethinggenuinelynewtothemodel.Perhapsyoucangetsomethinglikethis.Table5

TickerForPickingTopNStocks ForWeighting

ValueRank GrowthRankPQR 99.14 75.22STU 98.72 93.12VWX 98.49 67.18YZA 97.83 65.13BCD 97.66 86.20Thisissomethingthatcanmakesense.Wehaveaportfolioofstockswellrankedforvalue.WemayhavealsohadaBuyrulethatlimitedoursortingonlytostocksthatpassedcertainquality-riskthresholds.Weknowgrowthisimportanttoo(Rememberthedividendgrowthmodelanditsextensions!),butareconcernedabouthowharditistousehistoricgrowthrates.Somaybewegivethesoftergrowthdataasofterspotinthemodel;ratherthanusingthemtoincludeorexcludestocks,weusethemtohelpusadjusttheweightingsofagroupofstocksonwhichwe’realreadybullish.UseofWeightingsintheContextoftheOverallStrategyLet’srefreshourselvesforamomentontheoverarchingthemeofstrategydesign,asdiscussedintheearliesTopicsinthisseries.WestartedwiththeDividendDiscountModelandextendedittoencompassothermetricssuchasearnings,sales,bookvalueandcashflow.Ultimately,we’reseekingstocksthatseemlikelytobemispricedunderthefollowingbroadframework:

P=D/(R–G),whichcanbegeneralizeto...P=W/((rf+RK(erp))-G)P=IdealstockpriceW=somemeasureofperiodicwealthgeneratedbythecompanyrf=therisk-freerateofreturnRK=ameasureofcompanyspecificriskerp=equity-riskpremiumG=therateatwhichWisexpectedtogrowinthefuture

WefocusonW,RK,andG,theitalicizeditems,theoneswecanaddressinbuildingourstrategies.Theothersareexternalmarketfactorswithwhichwe’restuck.Wealsoknow,basedonthestructureoftheequation,thatallelsebeingequal:

10

AsWrises,so,too,doesPAsRKfall,PrisesAsGrises,so,too,doesP

Let’snowfocusonthethreeprimarytoolsweusetoimplementstrategiesthatseektoexploitmarketinefficienciesinthesearea,

Ranking:Wesetupacriterionforclassifyingstocksfrombesttoworst.Ifwedoourworkperfectly,the#1stockwillbebetterthanthe#2stock;the#2stockwillbebetterthanthe#3stock,etc.,etc.,etc.Rankingisnotblack-or-white;itinvolvesshadesofgrey.Screening/BuyRules:Weliveinahighlyimperfectworldand,henceshouldexpectourRanking-systemtobeimperfect.Sowetrytogiveitsomehelp,totiltprobabilitiesinadesirabledirection,bylimitingtherank-basedsorttoasubsetofstocksthathasbeenpre-qualifiedhopefullytobemorelikelytobesuccessfullyrank-able.Screeningisblack-or-white;pass-or-fail.Therearenoshadesofgrey.

SoweseethatRankingandBuyruleseachplayadistinctrolewithinthemodel.Inthatcontext,let’snowconsidertheroleofweightings(again,assumingweusethemforstrategicpurposesandnotjusttofacilitateliquidity).

Weightings:Functionallyspeaking,thisisahybridbetweenScreeningandRanking.ItresemblesScreeninginthatitplaysarolethatsupportsourimperfectrankingsystemsandtriestonudgethemtowardahigherprobabilityofsuccessfulsorting.Itresemblesrankinginthatitdealswithshadesofgrey,notblack-or-white.Weapproachweightingknowingthatweneednotdoanythinghereifwehaveequaldegreesofconfidenceorcomfortwiththeoutputofwhatwe’vedonewithRankingandScreening.WeuseWeightingiforwhenwedecidethattheworld’simperfectionsareenoughtowarrantanextralayerofhelp.TheextrahelpwegetfromtheWeightingprotocolneednotbefanaticallyprecisesincewe’vealreadydonealot,viaScreeningandRanking,togettothefinalNnumberofstocks.TheweightingprotocolshouldnotbeusedtotrytofightwithorevencanceltheimpactofwhatweaccomplishedwithScreeningandRanking.Thatwouldbeamoveintheoppositedirectionfromwherewewanttogo(toincreasethelikelihoodtherankingsystemswillhavedeliveredgoodstockstous).

Giventheroleoftheweightingformula,asanextralayerofsupport,therearetwoapproacheswecantake:

1. UseaformulathatisconsistentwiththestrategicideasembodiedintheRankingsystemsand/orBuyrules.Youmight,forexample,useRANKorRating(“Value2”)or,perhaps(Frank(“PEGLT,#Sector,#Asc)”toweightaportfoliothatuses“Value1”as

11

itsprimaryrankingsystemand,perhaps,aQuality-orientedscreentoaddresstheRK(risk)elementofthestrategy.

2. Useaformulathataddssomethinggenuinelynewtothemodel,somethingtrulyworthusingbutwhichyouwereunabletosqueezeintoScreenandRank.GoingbacktotheaboveValue1-QualityScreenmodel,youmightusetheweightingprotocoltoaddresstheheretoforeomittedG(growth)factor.Youmightweightbasedonarankingsystemthatusesacollectionofhistoricalgrowthrates,oryoumightusearankingsystembuiltonthebasisofsentimentortechnicalanalysis(proxiesforexpectationsoffuturegrowth),orevenamorecomprehensiveGS(growth-sentiment)typeofrankingsystem.

Beingconsciouslyawareofwhatyouwantyourweightingprotocolisimportant.It’sOKtochangeyourmindafteryougetstartedanddosometesting.Butkeepingtheroleyouwantweightingtoplaytopofmindwillhelpyouavoidtheinformation-overloadspinning-in-placephenomenon.Thisframeworkisnotintendedtotellyouwhatformulatouse.It’sintendedtoillustratehowyoucanmakeacontrolledthoughtfulchoiceofformula.ImplicationsfortheRefreshCycleWeeklyrebalancing-reconstitutionisapopularapproachonPortfolio123.It’sfinetogothatrouteifyou’recheckingoftenforadjustmentsthatneedtobemadeinamodelbuiltforfewsellsandlowturnover.Butit’snotnecessarilyOKtodothatsimplytotakeadvantageofthefreshestdatayoucanget.Businessesdon’tdevelopandinvestorsdon’tevaluatethematanywherenearthespeedwithwhichcontemporarysystemscanrefreshinformation.It’sOKtotradeweeklyifyourmodelisgenuinelybuiltuponastoryyouexpecttoplayoutorfizzlerapidly.Moreoftenthannot,though,you’llneedmoretimetogiveyourideastimetotakeroot.Ireiteratethisherebecausewhenyourstrategyincludestheadditionallayerofweightings,youmayfindyoucangiveyourmodelsevenmoretimetopanout.Thiswon’talwaysbeso.ButifyoudotakeadvantageofFormulaWeighting,makesuretorunsometestsusinglongerreconstitutionperiodsthanyouhavebeenaccustomedtousing,andexperimentwithreconstitutionperiodsthatarelongerthantherebalanceintervals.Whenitcomestotimehorizon,don’ttakeanythingforgrantedfromyourpreviousexperience.Testandlearnanew.ImplicationsforTargetNumberofPositionsThenumberofpositionsyouwanttoholdinyourportfolioisanotherareainwhichyoushouldrefrainfromtakinganythingforgrantedandregardingwhichyoushouldtestandlearnanew.

12

Theboundarybetweenhavingenoughpositionstoovercomeindividualaberrationsandgiveyourideasanopportunitytoplayout,versushavingsomanypositionsthatyoumightjustaswellindex,hasalwaysbeenachallengetoidentify.Asyousearchforthisfuzzylineofdemarcation,bearinmindthatifuseofformulaweightingallowsyoutostretchtherefreshcyclesyouhadbeenusinginthepast,thatcouldmakeittolerable,fromatradingcostperspective,toholdmorepositionsthanyoupreviouslyhad.Totheextentyoucanaffordtotakesomeextrawiggleroominthisregard,considerdoingit.Foronething,weightingislikelytobemoreeffectiveifthereareenoughsecuritiesfortheprotocoltooperaterationally(e.g.,somethingthatisnotan85%-15%thing)andmakeadifference.Also,ithasbeenmyobservationthatmanyonPortfolio123whohaveexposedmodelstopublicviewhavetendedtoerronthesideoftoofewstocks.Useofformulaweightingwouldmakeforagoodoccasiontorethinkthisissue.CaseStudyForpurposesofillustration,let’sworklookatacasestudythatusesthefollowingmodelasastartingpoint.Don’tlookforustoultimatelygettosomethinggreat,somethinginwhichyou’llwanttoinvestrealmoney.Thegoal,here,istoillustratehowFormulaWeightingcanimpactwhatyoudo.Universe:S&P500Benchmark:iSharesSPDRS&P500ETF(SPY)TargetedNumberofStocks:20Refresh(ReconstitutionandRebalancing)Interval:3MonthsRankingSystem:“Comprehensive:QVGM”(Quality-Value-Growth-Momentum”)BuyRules:Rating(Basic:Value”)>=75Rating(Basic:Sentiment”)>=75SellRules:Rating(Basic:Value”)<50Rating(Basic:Sentiment”)<50 Rank<80Resultsof10-yearsimulationstestingvariousweightingprotocolsareshownonthefollowingpages.

13

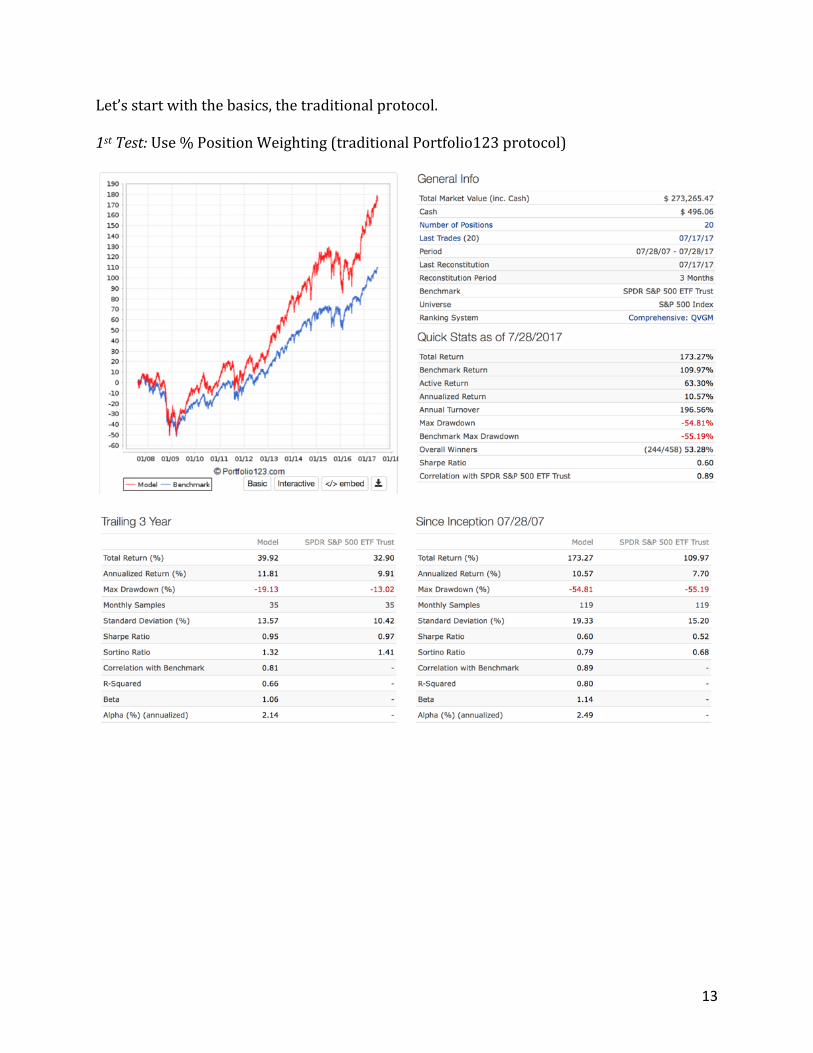

Let’sstartwiththebasics,thetraditionalprotocol.1stTest:Use%PositionWeighting(traditionalPortfolio123protocol)

14

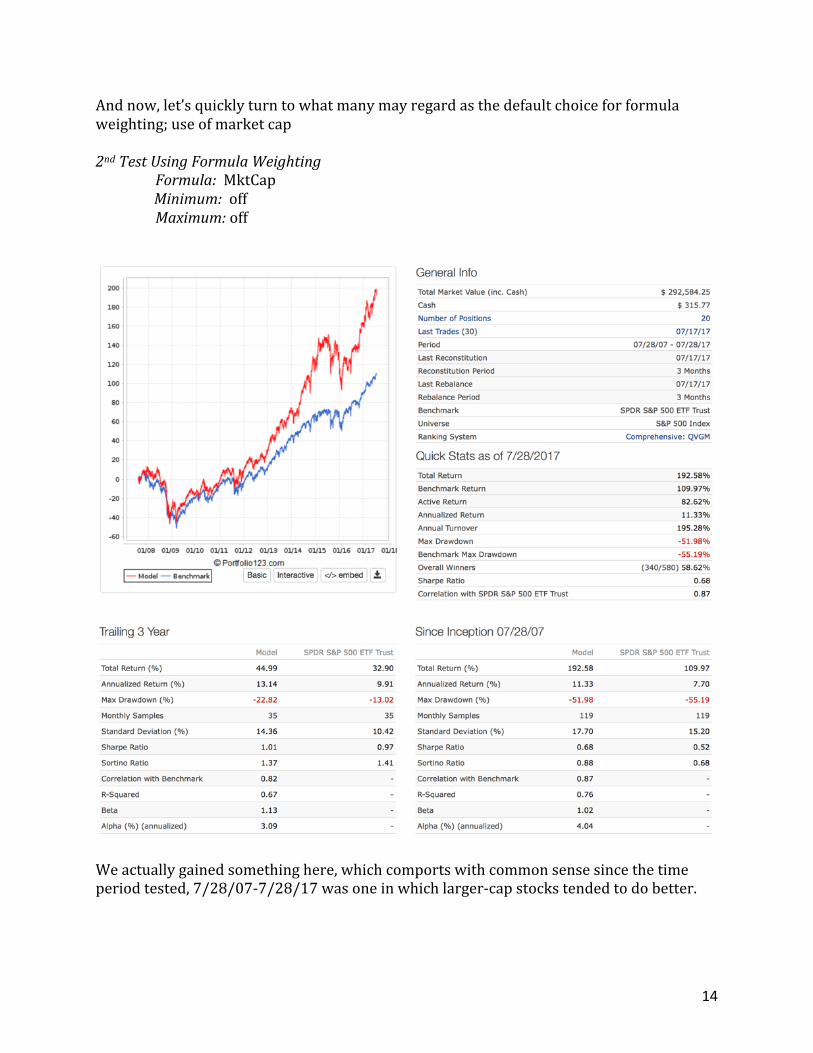

Andnow,let’squicklyturntowhatmanymayregardasthedefaultchoiceforformulaweighting;useofmarketcap2ndTestUsingFormulaWeightingFormula:MktCap Minimum:offMaximum:off

Weactuallygainedsomethinghere,whichcomportswithcommonsensesincethetimeperiodtested,7/28/07-7/28/17wasoneinwhichlarger-capstockstendedtodobetter.

15

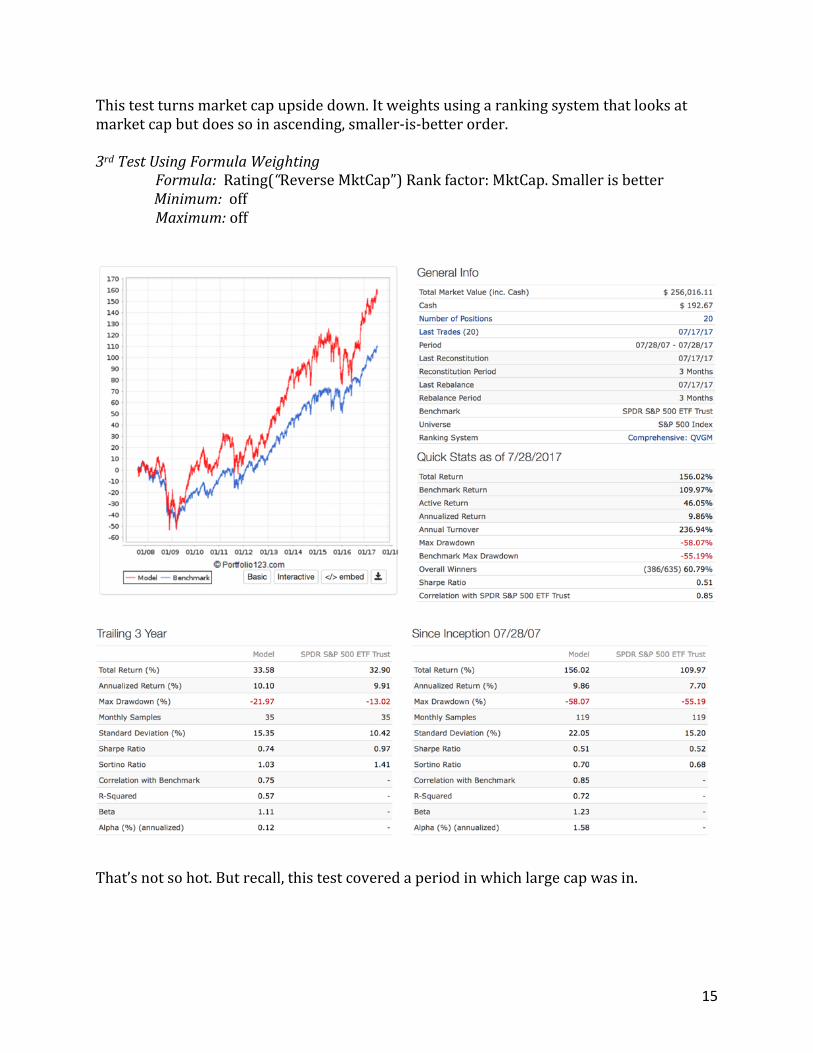

Thistestturnsmarketcapupsidedown.Itweightsusingarankingsystemthatlooksatmarketcapbutdoessoinascending,smaller-is-betterorder.3rdTestUsingFormulaWeightingFormula:Rating(“ReverseMktCap”)Rankfactor:MktCap.Smallerisbetter Minimum:offMaximum:off

That’snotsohot.Butrecall,thistestcoveredaperiodinwhichlargecapwasin.

16

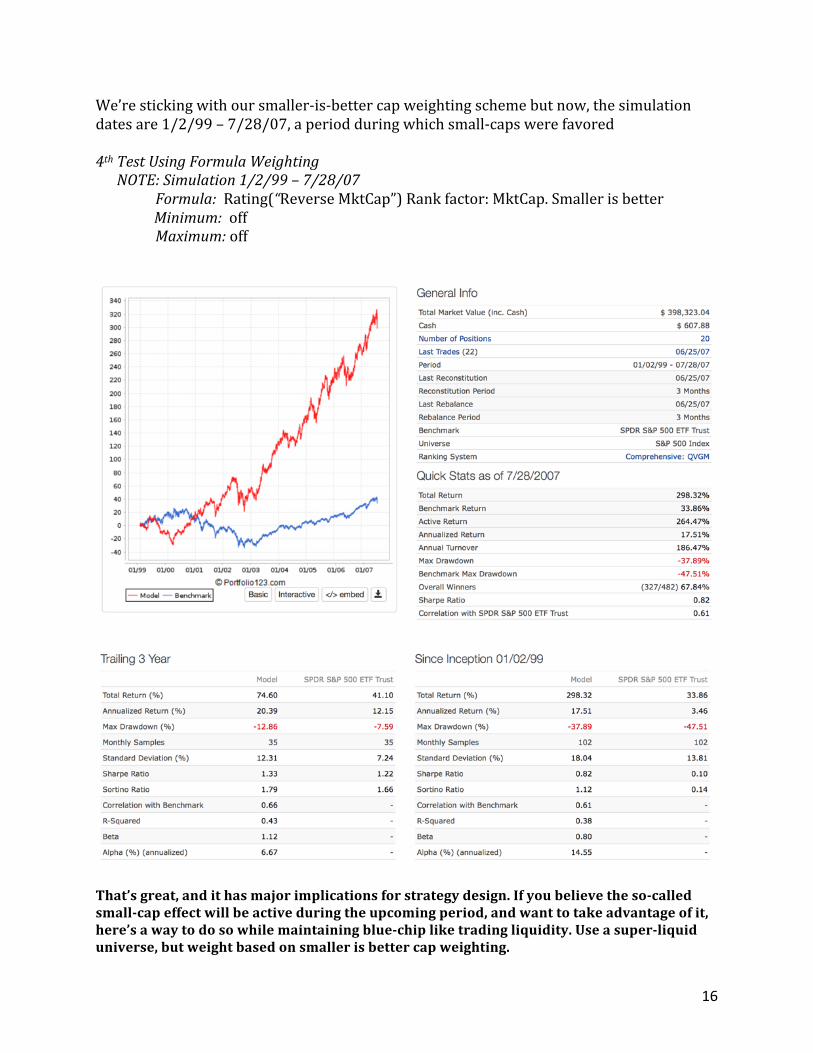

We’restickingwithoursmaller-is-bettercapweightingschemebutnow,thesimulationdatesare1/2/99–7/28/07,aperiodduringwhichsmall-capswerefavored4thTestUsingFormulaWeightingNOTE:Simulation1/2/99–7/28/07Formula:Rating(“ReverseMktCap”)Rankfactor:MktCap.Smallerisbetter Minimum:offMaximum:off

That’sgreat,andithasmajorimplicationsforstrategydesign.Ifyoubelievetheso-calledsmall-capeffectwillbeactiveduringtheupcomingperiod,andwanttotakeadvantageofit,here’sawaytodosowhilemaintainingblue-chipliketradingliquidity.Useasuper-liquiduniverse,butweightbasedonsmallerisbettercapweighting.

17

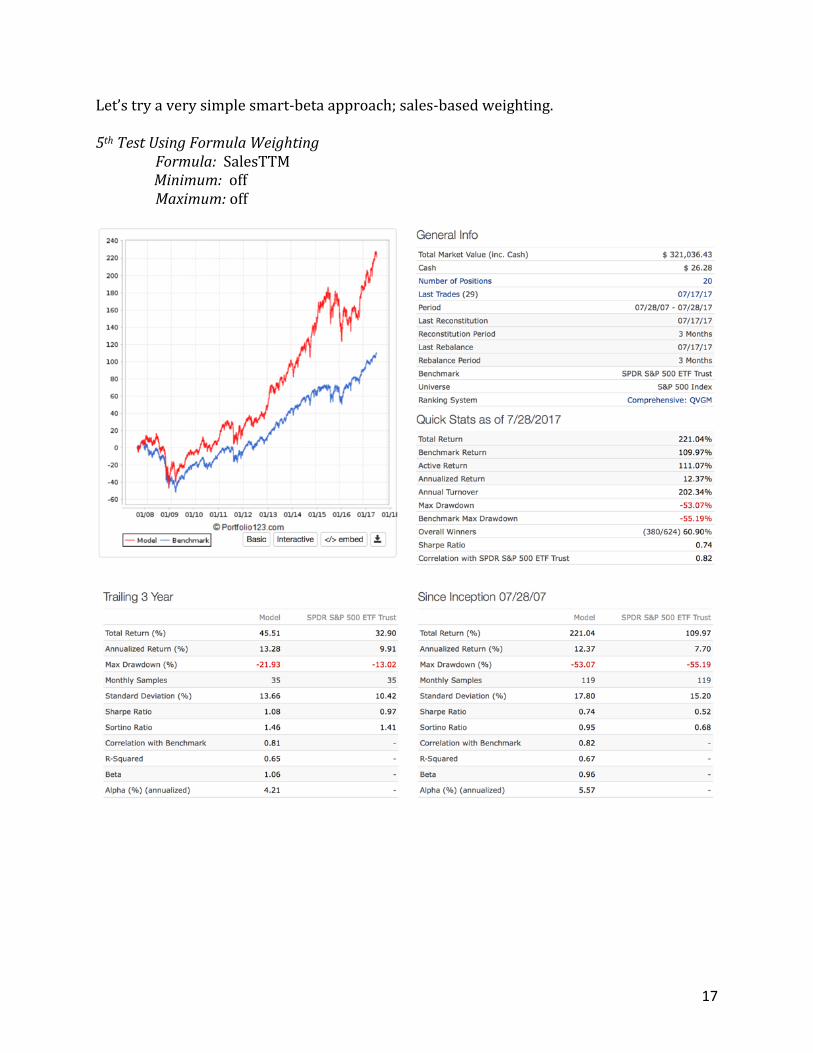

Let’stryaverysimplesmart-betaapproach;sales-basedweighting.5thTestUsingFormulaWeightingFormula:SalesTTM Minimum:offMaximum:off

18

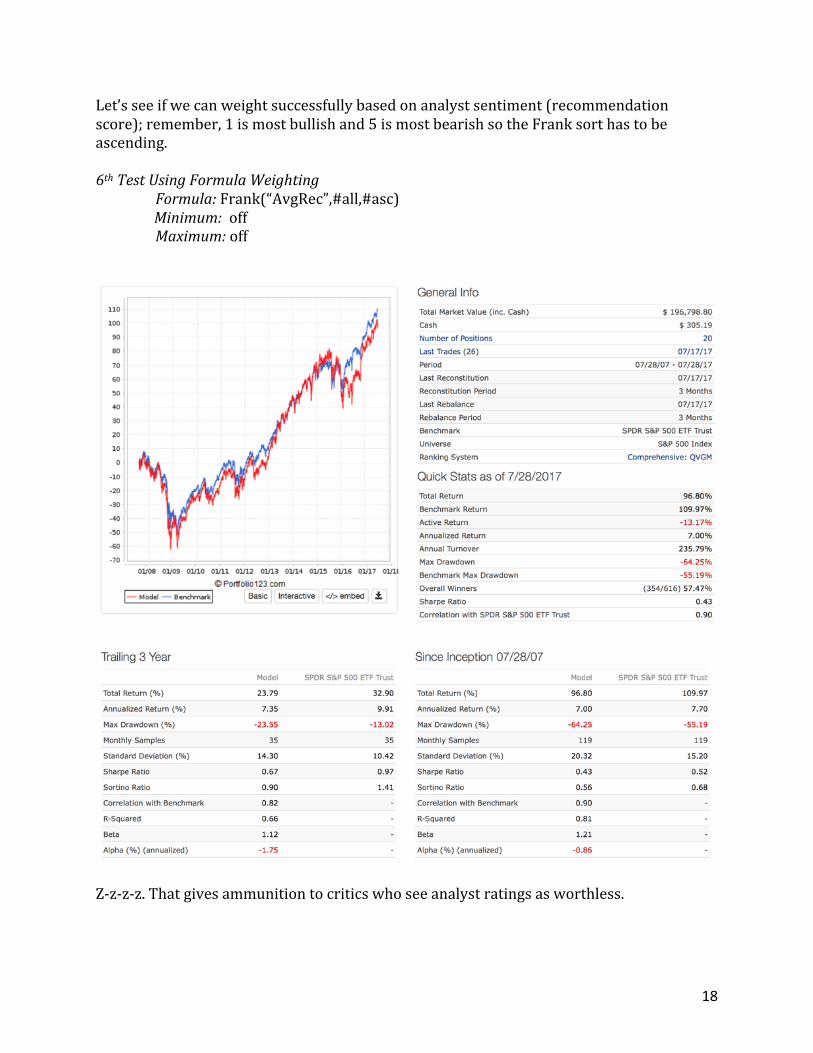

Let’sseeifwecanweightsuccessfullybasedonanalystsentiment(recommendationscore);remember,1ismostbullishand5ismostbearishsotheFranksorthastobeascending.6thTestUsingFormulaWeightingFormula:Frank(“AvgRec”,#all,#asc) Minimum:offMaximum:off

Z-z-z-z.Thatgivesammunitiontocriticswhoseeanalystratingsasworthless.

19

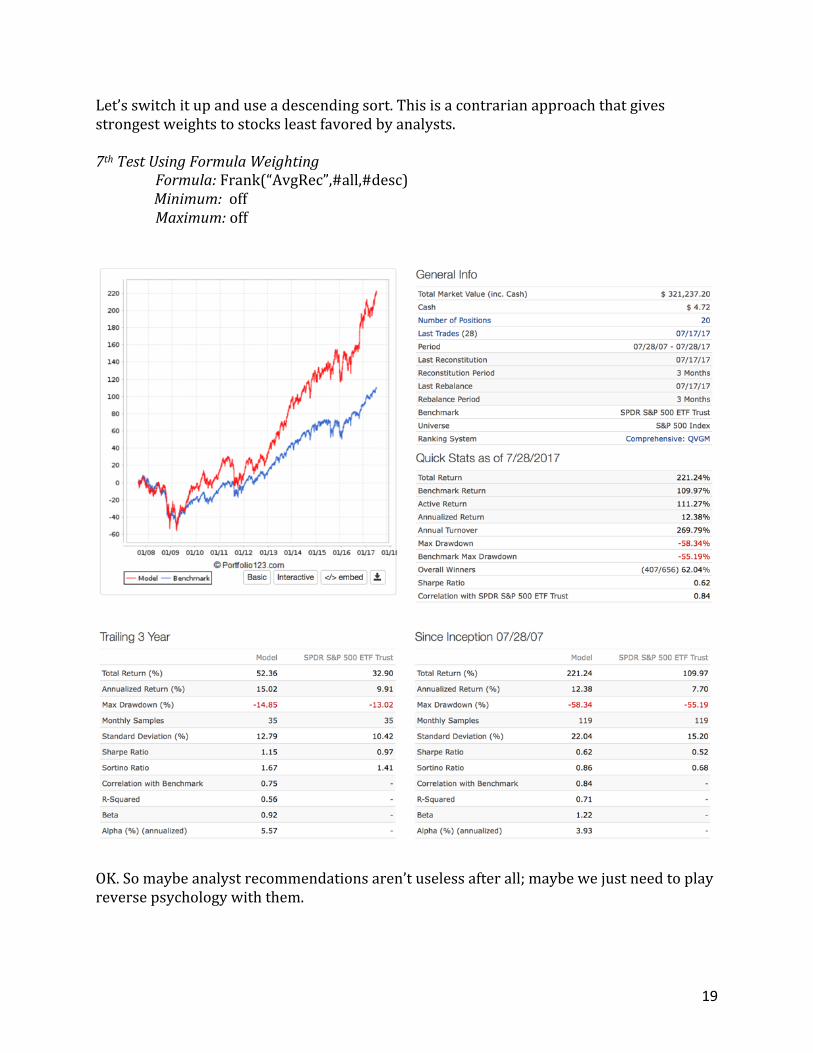

Let’sswitchitupanduseadescendingsort.Thisisacontrarianapproachthatgivesstrongestweightstostocksleastfavoredbyanalysts.7thTestUsingFormulaWeightingFormula:Frank(“AvgRec”,#all,#desc) Minimum:offMaximum:off

OK.Somaybeanalystrecommendationsaren’tuselessafterall;maybewejustneedtoplayreversepsychologywiththem.

20

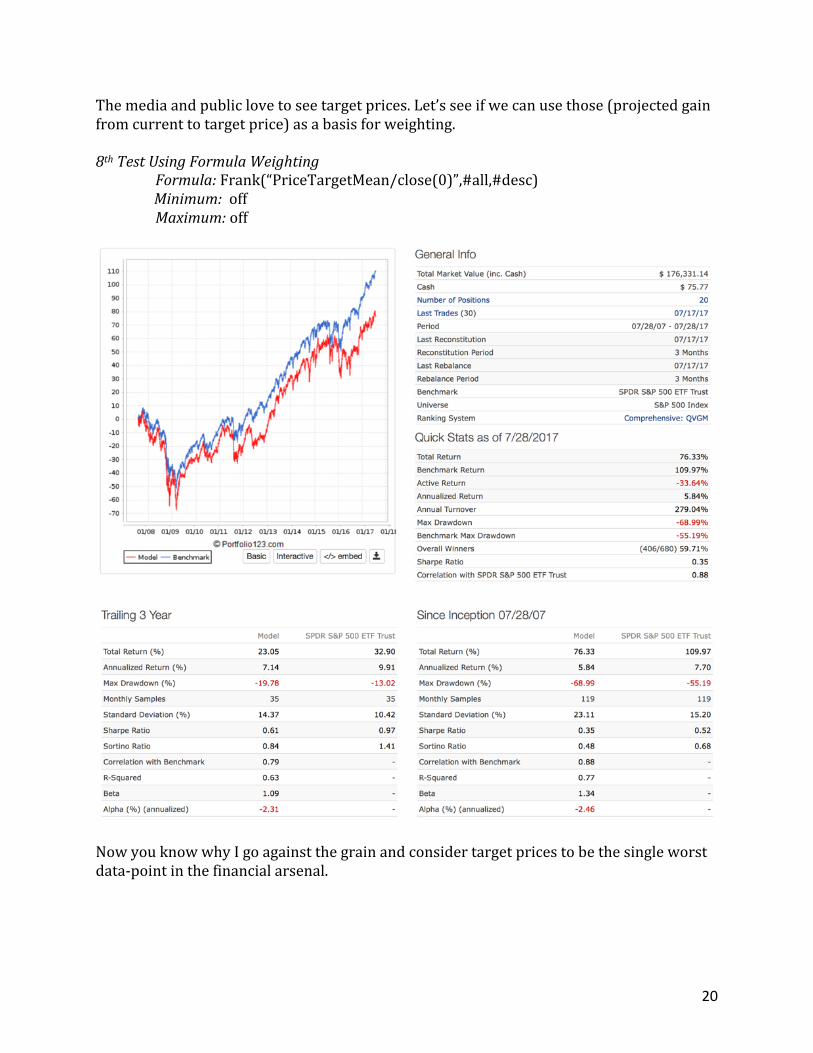

Themediaandpubliclovetoseetargetprices.Let’sseeifwecanusethose(projectedgainfromcurrenttotargetprice)asabasisforweighting.8thTestUsingFormulaWeightingFormula:Frank(“PriceTargetMean/close(0)”,#all,#desc) Minimum:offMaximum:off

NowyouknowwhyIgoagainstthegrainandconsidertargetpricestobethesingleworstdata-pointinthefinancialarsenal.

21

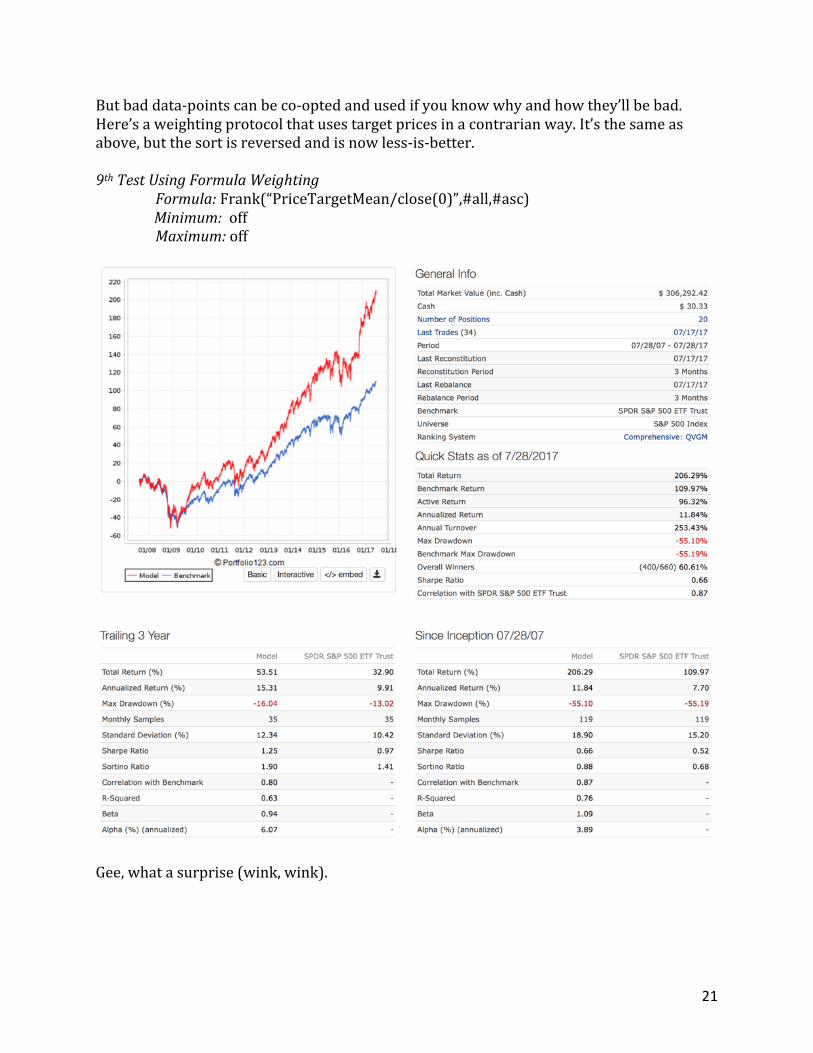

Butbaddata-pointscanbeco-optedandusedifyouknowwhyandhowthey’llbebad.Here’saweightingprotocolthatusestargetpricesinacontrarianway.It’sthesameasabove,butthesortisreversedandisnowless-is-better.9thTestUsingFormulaWeightingFormula:Frank(“PriceTargetMean/close(0)”,#all,#asc) Minimum:offMaximum:off

Gee,whatasurprise(wink,wink).

22

ConclusionPositionsizingisaverypowerfulandimportantpartofthestockstrategist’sintellectualarsenal.Notonlydoesitallowyoutomakefurtheruseofallthecreativityyou’vecalleduponuptillnowasyoudecidedwhatstockstoincludeandexcludefromyourportfolios,italsoallowsyoutocalluponthosesamecreativeprocesseswithoutchangingtherosterofstocks.Thatcanbeofmake-or-breakimportanceif,forsomereason,yourportfoliomustcontainspecificnames.Italsomakesformuchmorerelevantportfolio-benchmarkcomparisons,sinceweonlyhaveasmallnumberofequally-weightedbenchmarks.Finally,aswithrankingsystems,buyrulesandsellrules,makesureyouhaveasoundcommonsensereasonforweightingasyoudo.