ticker symbol: aeommoore.ba.ttu.edu/valuationreports/spring2007/american...key statistics industry...

TRANSCRIPT

- 1 -

Ticker Symbol: AEO

Jennifer Pfieffer ([email protected])

Lisa Hase ([email protected]) Michael Gerrish ([email protected])

Carl Ebbern ([email protected])

Kevin Cooper ([email protected])

- 2 -

Table of Contents

Executive Summary 3

Company Overview 7

Five Forces Model 9

Formal Accounting Analysis 27

Financial Ratio Analysis 49

Forecasting 79

Regression Analysis 89

Valuation 91

Appendix 1 106

Appendix 2 121

Works Cited 126

- 3 -

Executive Summary

www.finance.yahoo.com

Investment Recommendation: Overvalued, Sell

Key Statistics Industry Members PPS (as of 4/1/07)Index NYSE Abercrombie and FitchPPS AEO (as of 4/1/07) $29.99 Aeropostale52-week range $20.07 - $34.80 GapRevenue (2006) $2.8 B LimitedMarket Capitalization $6.6 BShares Outstanding $221 M Comparables ValuationsEnterprise Value $7 B P/E (trailing) $33.74 UndervaluedDividend Payout Ratio 15.9% P/E (forecast) $32.25 Undervalued3 month Avg. Daily Trading Volume 3.2 mil. P/B $24.12 OvervaluedPrice/Earnings 17.13 Dividends/Price $18.09 OvervaluedPrice/Earnings forecast 15.30 P.E.G. $27.24 OvervaluedBook value per share $8.98 P/EBITDA $31.85 UndervaluedReturn on Equity 33.5% P/(FCF per share) $16.27 OvervaluedReturn on Assets 24.10% Enterprise Value/EBITDA $34.92 Undervalued

Cost of Capital Est. Beta R2 Ke Intrinsic Valuation72 months -0.80 3.0% 1.9% Discounted Dividends $6.64 Overvalued60 months -0.36 -0.7% 3.6% Free Cash Flows $90.97 Undervalued48 months -1.49 8.3% -0.8% Free Cash Flows (Cap. Leases) $283.02 Undervalued36 months -0.75 -0.4% 2.1% Residual Income $11.90 Overvalued24 months -0.52 -3.3% 3.0% Abnormal Earnings Growth $19.78 OvervaluedPublished Beta 1.2

Ke 13% Altman Z-Score 3.75 Low RiskWACC 11% Altman Z-Score(Capitalized) 2.66 Moderate Risk

$40.23$17.21$26.06

4/1/2007

$75.68

- 4 -

Analysts’ Recommendation – Overvalued, Sell

Company and Industry Overview and Analysis

American Eagle Inc. was established in 1977 to offer affordable, quality

clothing to the younger generation. American Eagle is in a sub-industry of the

apparel industry, which consists of other competitors Gap Inc., Limited Brands,

Abercrombie and Fitch Co., and Aeropostale. These companies sell denim, shirts,

footwear, swimwear, accessories, and outerwear. Rivalry amongst existing firms

is intensified by focusing on a smaller market, and competition is propelled by

the industry’s constant need to have the latest fashions when demanded.

American Eagle and its direct competitors expand their economies of scope into

sub-brands and a wider variety of merchandise in order to capture more market

share. The current competition deters new entrants because it is hard for new

entrants to secure channels of distribution in order to deliver to customers.

Department stores pose a threat of substitution for cheaper clothes and a wider

variety. Although department stores are more convenient, consumers of

American Eagle are loyal to it and its competitors because these consumers are

driven by brand names and logos. This helps eliminate the threat of substitutes

of cheaper clothes. Consumers have low switching costs between the direct

competitors because consumers alternate between the stores seamlessly.

American Eagle sets itself apart in the specialty retail sub-industry by offering its

products at a lower price and emphasizing a healthy brand image.

Accounting Analysis

American Eagle altered its accounting policies in 2003 in order to improve

efficiency. The company did this by changing inventory policies and how they

manage discounted merchandise. GAAP allows companies in the specialty retail

sub-industry a wide range of flexibility when determining goodwill amortization,

- 5 -

asset depreciation, classifying leases, and accounting for inventory. This

flexibility enables the management to convey the workings of the company to

shareholders with additional explanations to provide understanding for investors.

When analyzing American Eagle, we considered many sales and expense

manipulation diagnostics to investigate management’s treatment of revenues and

expenses. The only “red flag” raised was the operating leases which expenses

only the current portion of the lease obligation instead of capitalizing the future

lease holds on the balance sheet. This underestimates assets and liabilities and

modifies a potential investor’s view of the company. When the leases are

capitalized we gain a better knowledge of American Eagle’s true financial

situation.

Financial Ratio Analysis and Forecasting

A firm’s financial ratios are broken down into three categories: liquidity

ratios, profitability ratios, and capital structure ratios. American Eagle presents

average liquidity ratios in comparison to the industry. The current ratio is

currently 2.6, which means $2.60 of current assets are available for every $1 of

current liabilities. Therefore, American Eagle has plenty of liquidity that would

appeal to lenders. According to our analysis, American Eagle has high profitability

ratios and it leads the industry in gross profit margin and operating profit margin.

This is because American Eagle is able to purchase its merchandise at a cheap

rate from a variety of vendors. They are then able to turn the product around

and sell in a high end market to gain a high gross profit. The capital structure

ratios show that American Eagle is financed mostly by equity, which frees them

from payments to bond holders who could hold leverage over the company.

In order to forecast American Eagle’s financial statements out for the next

ten years, we created a common-size statement of the balance sheet and income

statement. This helped us determine structural trends for the company to better

forecast future growth. Since American Eagle changed accounting policies in

- 6 -

2003, the past five years has seen a dramatic alteration across the financials.

Therefore, we used the past three years in order to determine trends to grow

net sales and total assets. In the forecasted balance sheet, we compensated for

the operating leases and capitalized the leases on a second balance sheet.

American Eagle already grows in sales at about 14%, which is consistent with

the industry.

Intrinsic Valuation

When calculating the intrinsic valuations, we first calculated the cost of

debt and cost of equity to determine the weighted average cost of capital. We

adjusted cost of debt when we capitalized leases. We then valued the company

through the discounted dividends model, free cash flows model, residual income

model, and abnormal earnings growth model. The discounted dividends, residual

income, and abnormal earnings growth models all stated American Eagle is

overvalued in the market. We based our recommendation on the residual income

and abnormal earnings growth models because they presented the most

accurate valuations. The two averaged a $15.84 value for American Eagle Stock

compared to the observed April 1, 2007 price of $29.99. We finally considered

Altman’s z-score to examine American Eagle’s credit risk. The z-score revealed

American Eagle to have minimal chance of going bankrupt with a 3.75 score

considering operating leases. After converting the leases to capital leases, the z-

score fell to 2.66, making the company an indeterminable risk. Ultimately, we

believe American Eagle to be at moderate to low risk of going bankrupt. Our

overall conclusion is the firm is overvalued by approximately $14.

- 7 -

Company Overview American Eagle Outfitters, Inc., also known as American Eagle or AE, was

established in 1977. The corporate headquarters are currently located in

Warrendale, Pennsylvania, but will soon be moving to Pittsburgh, PA. It is a

specialty apparel retailer of fashionable clothing targeting people between the

ages 15 and 25. American Eagle sells jeans, t-shirts, accessories, footwear,

swimwear, and outerwear. It has expanded its operations from the United

States, into Canada, and Puerto Rico. Currently there are a total of 911 stores,

839 in the U.S., and 72 in Canada. (www.ae.com)

American Eagle considers itself to be a part of the competitive, “brand

name”, specialty apparel industry. Its successes derive from its ability to adapt

and offer the newest trends at a reasonable price. Other firms in this unique

industry include the following: Abercrombie and Fitch Co., Gap Inc., Aeropostale

Inc., and Limited Brands Inc. The following graph illustrates the market

capitalization for each firm not only as a number but also as a percentage of this

sub-industry. It is calculated by multiplying the price per share times the number

of shares outstanding.

www.abercrombie.com, www.ae.com, www.aeropostale.com, www.gap.com, www.limitedbrands.com

Industry Market Cap (in billions of dollars)

$6.64

$6.68

$2.39

$18.81

$10.37American EagleAbercrombie and FitchAeropostaleGapLimited

- 8 -

All members of this industry design, market, and sell their own lines of

specialty apparel. American Eagle intends to increase its market share by

continuing to promote brand loyalty through the customer loyalty programs. In

addition, the company will provide the newest fashion the customers want, at

the prices they can afford. They have also recently expanded its customer base

by introducing the MARTIN + OSA, and aerie sub-brands. MARTIN + OSA

consists of sportswear targeting 25 to 40 year olds, and aerie is a new collection

of dorm wear and intimates for young women (AEO 10-K).

Revenues for the 2006 fiscal year increased over 20 percent to the

amount of $2,794,3409,000. The majority of the firms in this industry

experienced similar increases in revenue. In addition to increasing revenue, total

asset value has also increased. The chart below describes the percent change in

total asset value for American Eagle over last five years. There has been a

definite increase in asset value for each of the years with the largest increase

from 2004 to 2005. Analyzing a firm’s total asset value is another way to

measure the size of a company.

AEOS Asset Values

Year Asset Value (in

thousands) % Change from Previous

Year 2006 $1,987,484 19.21% 2005 $1,605,649 17.23% 2004 $1,328,926 29.84% 2003 $932,414 20.49% 2002 $741,339 N/A

www.abercrombie.com, www.ae.com, www.aeropostale.com, www.gap.com, www.limitedbrands.com

The following graph, found on the yahoo website, illustrates American

Eagle’s stock price performance for the past five years. It experienced a 5-year

low of $3.35 on October 9, 2002, and the 5-year high of %34.34 occurred on

January 16, 2007. After adjusting for splits and dividends, the data shows that

the stock price has tripled in the past five years. This graph also shows all of

American Eagle’s industry competitors and their stock price performances over

- 9 -

the past five years. The firms in this industry seem to be following the same

general stock price trends (www.finance.yahoo.com).

Splits:06-Jan-98 [3:2], 11-May-98 [3:2], 04-May-99 [2:1], 26-Feb-01 [3:2], 08-Mar-05 [2:1], 19-Dec-06 [3:2]

Five Forces Model The five forces model details the extent of competition within an industry

by analyzing factors such as rivalry among existing firms, threat of new entrants,

threat of substitutes, buying power of buyers, and bargaining power of suppliers.

When the competition level is properly assessed, a company can better

determine its core competencies so it can best succeed in the industry.

Rivalry Among Existing

Firms

Threat of New

Entrants

Threat of Substitutes

Buying Power of Buyers

Bargaining Power of Suppliers

High Low Medium High Low

- 10 -

The apparel industry consists of a wide variety of clothing, footwear, and

accessories stores. Within this large industry is a smaller sub-industry of

specialty retail. The specialty retail industry is made up of companies such as

Abercrombie and Fitch Co., American Eagle Outfitters Inc., Gap Inc., Aeropostale

Inc., and Limited Brands Inc. These stores are competitive in higher end retail

and market to a narrower customer base. This customer base focuses on

consumers from ages 15-25 (www.ae.com). The key is to balance a different,

yet trendy product and proved a price that suggests value to the customer while

being affordable.

Rivalry Among Existing Firms

Rivalry among existing firms breaks down the competition level between the

leading competitors in an industry. The competition is best depicted by

analyzing the growth of the industry, concentration and balance of competitors,

degree of differentiation and switching costs, ratio to fixed and variable costs,

and exit barriers and excess capacity. The different degrees of competition

determined by these factors affect how companies relate to one another in order

to prove successful.

INDUSTRY GROWTH

Industry growth determines if companies must fight for their share of the

market. If the industry is growing, there are plenty of consumers for each

company to be profitable. In the specialty retail sector, the industry has been

growing steadily which should lower competition. The sub-industry, specialty

retail is encompassed by the apparel industry; competitors include American

Eagle Outfitters Inc. Gap Inc., Aeropostale Inc., Abercrombie and Fitch Co.,

Limited Brands Inc. These companies make up a cluster of specialty retail stores

that market quality clothing to a younger generation. The industry has shown a

- 11 -

steady increase in stock value over the past five years. The cyclical nature of

this industry is created by quarterly fashion trends; this creates a constant

demand for the latest product.

These companies offer a differentiated product but they also compete

heavily with each other. The industry strives by marketing higher end clothing to

15-25 year olds. Although the industry is growing, limiting marketing to such a

small portion of the population intensifies competition. The companies

differentiate themselves with highly recognized brand names. The brand name

and quality of clothes separate each company from the other, giving them a

unique advantage over other general clothing shops such as department stores.

In this portion of the industry, brand is everything and the customers pay a

premium for it. The demand for these styles of clothing is limited to certain age

groups, causing more stores to fight for the same market share and therefore

increasing competition. Nevertheless, firms in this industry seem to be

experiencing growth.

Total Assets

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

2002 2003 2004 2005 2006

Year

Tota

l Ass

ets

(in

thou

sand

s of

dol

lars

)

American Eagle

Abercrombie and Fitch

Aeropostale

Gap

Limited

Industry Average

www.abercrombie.com, www.ae.com, www.aeropostale.com, www.gap.com, www.limitedbrands.com

- 12 -

As illustrated in the previous graph, the firms in this industry are steadily

increasing their assets with the exception of Gap Inc. and the Limited Brands.

By measuring changes in total assets, we can analyze the amount of growth

within a firm or an industry. The growth trends of this industry are further

evident in the following pie chart. The chart illustrates industry market share.

Industry Market Share (based on net sales)

32%31%

7%

31%

9%30%

10%

4%

31%

6%

5%

55%

2%

6%5%

55%

3%

6%

53%

3%

7%

50%

4%

8%

47%

American Eagle

Abercrombie and Fitch

Aeropostale

Gap

Limited2002

2006

2005

2004

2003

www.abercrombie.com, www.ae.com, www.aeropostale.com, www.gap.com, www.limitedbrands.com

Market share is the portion of the market a particular firm controls as a

percentage of the entire industry. This chart uses net sales as the determinate

for market share of a firm. Net sales must increase at an equal or greater rate

than the competition in order to maintain market share. According to the chart

ANF, AEO, and ARO appear to be gaining market share, while GPS and LTD seem

- 13 -

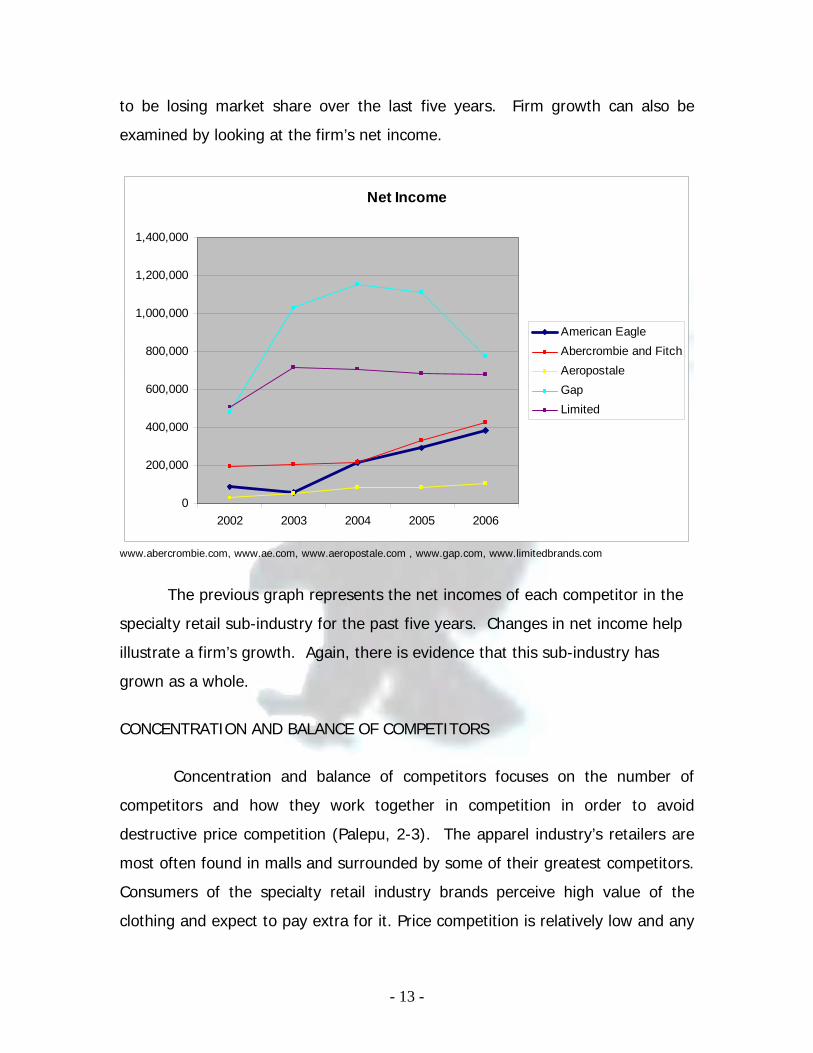

to be losing market share over the last five years. Firm growth can also be

examined by looking at the firm’s net income.

Net Income

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

2002 2003 2004 2005 2006

American EagleAbercrombie and FitchAeropostaleGapLimited

www.abercrombie.com, www.ae.com, www.aeropostale.com , www.gap.com, www.limitedbrands.com

The previous graph represents the net incomes of each competitor in the

specialty retail sub-industry for the past five years. Changes in net income help

illustrate a firm’s growth. Again, there is evidence that this sub-industry has

grown as a whole.

CONCENTRATION AND BALANCE OF COMPETITORS

Concentration and balance of competitors focuses on the number of

competitors and how they work together in competition in order to avoid

destructive price competition (Palepu, 2-3). The apparel industry’s retailers are

most often found in malls and surrounded by some of their greatest competitors.

Consumers of the specialty retail industry brands perceive high value of the

clothing and expect to pay extra for it. Price competition is relatively low and any

- 14 -

discounts to the customer are considered bonuses. But, with so many direct

competitors centrally located, the companies must fight to lure customers into

their stores as opposed to the others. Additionally, companies are continuing to

search for new mall to add locations, create sub-brands within their own stores,

and remodel and update current stores to increase the concentration and

consequently the competition. Therefore, this intense concentration of

competitors stimulates a high degree of competition.

DEGREE OF DIFFERENTIATION AND SWITCHING COST

The degree of differentiation refers to the ability of a company to distinguish

its products from other stores’ merchandise. By increasing differentiation,

competition is decreased because people are willing to pay more for a unique

product. Switching costs determine the customers’ likelihood to change their

product preference. American Eagle’s portion of the apparel industry is

completely different than other clothing stores in the industry such as Kohl’s or

Dillard’s. The clothes in the specialty retail industry are styled to have a more

casual, laidback look that appeals to 15-25 year olds. This different, specialized

style is what separates the companies from other clothing stores in the apparel

industry.

Consumers of these products tend to switch quite frequently between the

different direct competitors. The companies offer very similar clothing styles to

the same targeted market. Therefore, the low switching cost 15-25 year old

buyers stimulates higher competition between the companies. Within this unique

sector of the apparel industry, some firms offer more affordable clothing. It is

within the specialized section that American Eagle, for example, uses price

competition as a business strategy (www.ae.com).

In addition to using price to attract consumers to American Eagle, the

company launched the AE All-Access Pass in Fiscal 2005 to encourage brand

loyalty. This pass rewards frequent customers by granting “credits” after buying

- 15 -

a certain amount of merchandise. The credits can be accumulated to purchase

free merchandise from the American Eagle website (www.ae.com). Similarly,

American Eagle, Gap, and Abercrombie and Fitch all have brand credit cards for

purchases made in their stores and on their respective websites. Although

gimmicks such as credit cards are used to sway the customer from switching

between brands, it is not entirely effective. Since switching costs are low and

the degree of differentiation between these specialty retail shops is low,

competition for the targeted market remains high.

RATIO OF FIXED TO VARIABLE COSTS

If the ratio of fixed to variable costs is high, there is higher competition

because fewer variable costs can be minimized to enhance profits. Firms can

decrease prices to attract more consumers. The ratio of fixed to variable costs is

low in the apparel industry. Fixed costs for American Eagle primarily consist of

building leases for stores, offices, and two distribution centers. Abercrombie and

Fitch, Aeropostale, and Limited Brands all lease their properties as well

(www.abercrombie.com, www.aeropostale.com, www.gap.com,

www.limitedbrands.com). This is common in stores primarily located in malls or

shopping centers. Variable costs consist of purchasing inventory and paying

wages along with other selling and administrative expenses, which make up a

large percentage of total costs. The costs are based on the quantity of inventory

each store chooses to buy and its ability to sell it. This decreases competition

because it allows the store to adjust to the economy or buying trends and can

avoid burdening itself with excessive inventories.

EXIT BARRIERS AND EXCESS CAPACITY

Exit barriers occur when a specific product would be hard to liquidate or

sell if the firm left the industry. In the apparel industry, inventory is easy to sell

with a single sale or clearance. A firm in the apparel industry must turnover

- 16 -

most of its merchandise four times a year as the seasons change. Therefore,

there are four times a year a firm in this industry could easily exit the apparel

industry if it chooses not to replenish its inventory. The barriers to exit this

industry are relatively low because of the frequent total inventory turnover.

Companies in this industry will only buy enough merchandise it can sell in a

single season to prevent discounts and receive optimal profits.

Excess capacity is when supply surpasses consumer demand and there is

unsold merchandise. Retail stores can easily prevent this by holding sales to

move of the leftover seasonal inventory. Firms place clothes on sale at the end of

each quarter before new shipments of clothes arrive. Low exit barriers and low

excessive capacity leads to low competition because a firm can exit the industry

whenever necessary without suffering heavy consequences.

In conclusion, the degree of competition among existing firms is very high

within the select specialty retail industry. Competitors market a similar clothing

style to a very limited amount of people. This makes supply surpass demand and

companies must work to stress the importance of brand loyalty to the customer.

Threat of New Entrants

If a company in the industry is earning abnormal profits, competitors are

likely to enter because the potential profit is high and attainable. This threat can

force firms already in the industry to keep prices low to discourage new entrants.

In this industry, a competing firm must be differentiated from the industry, but in

its sub-industry firms need to be a price leader. If the competing companies fail

to become price leaders, there will be new entrants who will drive down profit

margins and gain market share.

ECONOMIES OF SCALE

Economies of scale differ in every industry. An industry with large

economies of scale is unlikely to see a substantial amount of new entrants.

- 17 -

Economies of scale include brand advertising, research and development, and

investment in physical assets. In this industry, there are large economies of

scale in brand advertising. Although it is very easy to compete on price in the

apparel industry, consumers are willing to pay for the label. The businesses

already competing with each other are very well known among the target

consumer. In order to enter this business a new company would have to put

enormous capital into advertising to increase brand awareness and become the

“cool” brand. A competitor could enter the industry by undercutting the

competition in price, but face an obstacle if they wanted to compete with stores

such as Gap and Abercrombie and Fitch. This industry is easy to enter because

the cost of capital can be quite cheap relative to the price of goods sold, but

hitting the target market can be quite difficult because of brand recognition.

Because of the necessity brand recognition, the threat of new entrants is greatly

reduced.

LEARNING ECONOMIES

Learning economies refer to industries that require an extra amount of skill

or knowledge that makes it difficult for new companies to enter the field. Firms

in the apparel industry focus on knowing the up and coming trends to produce

clothing, footwear, and accessories in a timely fashion to meet customer

expectations. If the company was unaware of popular fashions for youth, they

would be left behind the style curve. The industry is able to advertise to the

target market “what is in style” in several ways such as, ads seen industry-wide

feature popular stars, and attractive people modeling the clothes found in the

stores. The stores in this industry also have a visual appeal that is lacking from

other retail chains. Young, good-looking employees are hired to work the retail

side of the business. These employees are able to tell customers what looks

best on them while focusing on what will make their store the most money. The

learning economies in this industry reduce the threat of new entrants.

- 18 -

ECONOMIES OF SCOPE

Economies of scope refer to the variety of business within a company.

Some companies provide various goods and services to expand their customer

base while other companies emphasize certain products. For example, in Fiscal

2005r American Eagle expanded by introducing two sub-brands, aerie and

MARTIN + OSA. Aerie is a line of intimates and dormwear for young women,

while MARTIN + OSA is a line of casual sports wear for men and women ages

25-40. If successful, these sub-brands will expand the market share of the

company to customers not in its original business model (www.ae.com). For the

industry to stay competitive, the consumer is likely to see sub-brands being

offered at all the major competitors in this industry. The expanded scope utilized

by companies in this industry lead to an intense challenge for new entrants to

overcome in order to be successful.

FIRST MOVER ADVANTAGE

In an industry that is dominated by brand recognition, there is a very

apparent first mover advantage. The competitors in the high end retail industry

all started competing around the late 1990s. These competitors wanted to offer

a substitute to higher end department stores for the consumer in the mid teens

to mid twenties. The target consumer takes pride in owning name brand

products. To have a name brand the company must establish itself by being in

the industry for a significant amount of time. There are exceptions to this rule, if

a movie star finds a designer that they like, a first mover advantage can be

attained by getting the designer to design for the company. If a start up

company can grab the designer before one of the companies already in place,

the new company will have a competitive advantage. This industry is filled with

- 19 -

brands that have been around for quite awhile, and with very few exceptions

there are no new entrants.

ACCESS TO CHANNELS OF DISTRIBUTION AND RELATIONSHIPS

Access to channels of distribution and the relationships with suppliers

plays a substantial role in an industry such as this. Fashion constantly changes

with the seasons, so inventory turnover is continually happening. Without good

reliable relationships with suppliers, the stores in this industry would not be able

to provide the current season’s line of clothing in stores when demanded. Poor

channels of distribution lead to poor quarterly sales and force stores to discount

merchandise to move it off the shelves. This industry thrives on having the

latest fashion. Even the most prestigious firm will fail if it can not keep up with

the ever changing pace. This means that one late shipment from the companies’

suppliers can be devastating for bottom line profits. This pressure will

discourage new entrants.

LEGAL BARRIERS

Because of the nature of retail, there are not many legal barriers to entry

in the industry. The largest legal barrier that new entrants face is trademarks.

The new entrant must differentiate its brand logo and their clothing enough so

that it is not exactly like the competition, but keep the same basic ideas to

appeal to the targeted market. Legal barriers do exist in the form of credit/debit

sales, but this is a risk that should be calculated for on the financial statements

of the company. Legal barriers also exist for high end retail stores that offer

there own credit cards. A final legal issue that every retail store faces is the

possibility of lawsuits from consumers who injure themselves at the stores. The

small number of legal barriers leads to an increase in the likelihood of new

entrants.

- 20 -

CONCLUSION

In conclusion, the threat of new entrants is relatively low in this industry

because this industry has large economies of scale, large learning economies,

large economies of scope, a large first mover advantage, and access to

distribution channels is well set. Legal barriers pose less of a threat as the other

categories, but they still will discourage new entrants on a smaller scale than the

other categories.

Threat of Substitutes

The threat of substitutes refers to products that potentially replace other

products due to changes in the economy or consumer preferences. The apparel

industry does not need to worry about the threat of a physical product

substituting the need for clothing. Companies worry about preserving their brand

name and work to make their name the must-have. If the brand name looses its

significance, consumers are likely to substitute the specialty retail shops with

something more convenient like a department store.

Department stores expand past casual comfortable wear and sell casual,

formal, and professional clothes for all ages. They also sell jewelry, makeup,

furniture, and other products making the department store a big time saver for

consumers. If a customer does not value a brand name but does value their

time, they are more likely to shop at the department store to get everything they

need at once.

Firms in the specialty retail industry tend to locate their stores close to

department stores. This helps to eliminate the threat of department stores being

too far from specialty retail stores. Therefore, it is not too much of a burden to

go to one of these specialty retail stores to find the desired brand name. This

way most of the family can shop at department stores and youth from ages 15

to 25 can shop at a specialty retail store. As long as these companies can

- 21 -

preserve the significance of brand names, the threat of substitute products is

low.

Power of Buyers

Buyers hold the ultimate power in deciding which companies within the

specialty retail industry succeed because they determine demand. Price

sensitivity and bargaining power are forums on which buyers base their

purchasing decisions. Many of these specialty stores are located in shopping

malls. Abercrombie and Fitch, Gap, Aeropostale, and American Eagle are usually

located close to each other in malls and shopping centers. The majority of the

industry’s buyers shop at more than one of the specialty stores which make

switching costs for customers within the specialty retail apparel industry almost

non-existent and could lead to direct competition between all industry

competitors. However, buyers are usually willing to pay the industry’s premium

prices as long as a firm maintains relatively high levels of design and quality.

Power of Suppliers

In an industry with few suppliers, buyers are forced to pay the demanded

price for supply. They also increase their demand by supplying at a lower cost

than their competitors. However, the suppliers in this specialized retail industry

have very little bargaining power over the companies they supply. Cheap

manufacturing labor is abundant throughout the world. Though each company

uses different purchasing methods, no one in the industry relies heavily on a

specific supplier. For example, Abercrombie & Fitch has no more than 5% of its

apparel coming from a single supplier. (www.abercrombie.com) Though the

majority of the firms’ merchandise is purchased from lone venders, the firms are

under no contractual obligation to continue to purchase merchandise from the

said vendor. Because these companies are not held to a contract with their

- 22 -

suppliers, the cost of switching vendors would be low. The vast majority of

materials and product manufacturing in the industry are purchased from

overseas (mainly in Southeast Asia and Central America). The merchandise is

shipped to the distribution centers (located in Warrendale, Pennsylvania and

Ottawa, Kansas in American Eagle’s case) where it is inspected for quality and

consistency. Due to the nature of foreign shipping, imports can be affected by

trade laws, increased taxes or changes in foreign economies or political systems.

This volatility increases the risk of receiving merchandise late or at an increased

price. This is another reason why the retailers are hesitant to put responsibility

and power into the hands of the suppliers (www.ae.com).

Industry Classification

The five forces model indicates that this is a competitive sub-industry that

differentiates itself from the larger retail clothing industry. As shown, this is a

mixed industry with competition ranging from high to medium and even to low.

More work exists for a firm in order to remain a major competitor in such a

mixed industry. It is this mixed industry that gives companies within the industry

the opportunity to increase their market shares fairly easily because the threat of

new entrants remains low.

Value Chain Analysis

The value chain is how a firm derives value from its every day operating

policies and procedures. Because we have classified this industry as a mixed

competition industry, there are many things a business can do to gain the most

value out of its activities. This industry requires competitors to differentiate and

keep manufacturing costs low. To be successful in this sub-industry, competitors

must be able to keep costs low and provide merchandise that consumers are

willing to pay a premium for. To do this, firms spend money on their brand

- 23 -

image and find additional places to cut costs. Each firm in the industry chooses

how to achieve its optimum balance of differentiation and cost efficiency.

Because this is a higher end retail industry, if a company does not differentiate;

the consumer will see it as a substitute to low-end clothing brands. Having a

product that is different is not enough though because consumers can easily

switch between companies. In order to stay profitable, a company must engage

in cost leadership practices. Corporate strategies in this sub-industry can be

costly. Each firm uses its corporate strategies to attempt to add value to the

firm. Examples of corporate strategies that derive value in this industry are

consumer benefits though discount cards and credit cards, maintaining low

manufacturing costs, expanding world-wide through the use of the internet, and

being innovative when introducing new lines (www.abercrombie.com,

www.ae.com, www.aeropostale.com, www.gap.com, www.limitedbrands.com).

Industry-wide, a competitive company must both be a cost leader and be

differentiated. All the firms in this industry sell very similar products; they are

produced with superior quality. This industry produces quality products

efficiently. It also exercises tight const control over production and shipping.

Within each of the firms in the sub-industry, there is a very high degree of

customer service. The customer service draws a consumer to buy more

products. Every store in this industry has spent considerable money on their

brand image. Consumers shopping in this industry know their preferred brands.

Money must also be invested in research and development, to determine the up

and coming fashions for each season. The nature of the fashion industry

requires that each company anticipate what is going to be in style the next

season so that they can start production and meet the demand of consumers.

American Eagle: Differentiation or Cost Leadership or Both?

American Eagle has had to both differentiate itself and be a cost leader in

the industry. To start with differentiation, American Eagle has selected a specific

- 24 -

target consumer. According to their 10-K, also provide “high quality

merchandise.” During the 2005 fiscal year, American Eagle spent $53.3 million

on advertising (AEO 10-K). This shows just a small portion of its investment into

brand image. American Eagle states in its 10-K that it relies heavily on personnel

in upper management positions as well in retail sales positions to move the

products it sells off the shelves and into the hands of consumers.

Although American Eagle has a strategy of differentiation, this only

propels it to the high end retail sub-industry. Within this sub-industry, American

Eagle is a cost leader. The 10-K states that it will not only provide high quality

goods, but they will be at “affordable prices.” The economies of scale and scope

mentioned earlier also help American Eagle be a cost leader. Specifically,

manufacturing of the goods that American Eagle sells in its stores has been

outsourced all over the world. In order to enforce quality standards, American

Eagle has a strict program that requires factories to comply with “global

workplace standards and their code of conduct” (AEO 10-K).

American Eagle offers a private label credit card. The credit card is issued

through a third party bank, so American Eagle recognizes no bad debt on its

income statement. Although there are undisclosed expenses associated with this

service, the benefit of not having bad debt far outweighs those expenses. This

helps American Eagle be a cost leader because it does not have to set money

aside for an allowance for bad debt. In conclusion, American Eagle succeeds in

the specialty retail sub-industry because it is able to differentiate itself from

department stores, while remaining a cost leader among its direct competitors.

American Eagle’s Corporate Strategies

Corporate strategy is how a firm sets itself apart based on its

infrastructure as a business. This includes differentiation and cost leadership

techniques. American Eagle uses the following techniques to improve customer

loyalty and relationships, minimize costs, and maximize market share.

- 25 -

AE ALL ACCESS PASS

The AE All Access Pass rewards customers for purchasing American Eagle

products by granting credits that are redeemable at www.ae.com . The purpose

of this program, according to www.ae.com, is to increase switching costs and

provide incentive for customer loyalty towards American Eagle. The All Access

Pass gives the holder access to exclusive American Eagle music. Customers are

entitled to sales and contests that only All Access Pass members are privileged to

attend. There are also other incentives, such as computer wallpapers, based

online for All Access Pass members.

AE CREDIT CARD

The American Eagle Credit Card also encourages customer loyalty through

small purchases. In addition, the credit card provides special promotional

information and advance notice of sales and other events. This increases

customer relations because customers are better informed of events and are

more likely to participate in said events.

The credit card also benefits American Eagle because they outsource the

bad debt through a private third party bank. This relieves American Eagle of

potentially unrecoverable accounts receivable (www.ae.com).

COST OF MANUFACTURING

American Eagle minimizes costs by outsourcing the majority of production.

In order to maintain low costs, the company uses a variety of suppliers so no

single supplier can control American Eagle’s production. In addition to

outsourcing, American Eagle participates in the Customs-Trade Partnership

Against Terrorism program, where they work with the United States Customs

Agency to ensure the security of the safety chains. By securing the safety

- 26 -

chains, American Eagle minimizes their potential liabilities and reduces excessive

insurance rates that protect their merchandise (AEO 10-K).

EXPANSIONARY SUB-BRANDS

In the 2005 fiscal year, American Eagle started to expand past their

previous targeted market group by establishing a sub-brand MARTIN + OSA.

This sub-brand is a line that combines the traditional sport, classic, and denim

clothing but is geared towards 25-40 year old men and women. In addition to

expanding their market share, American Eagle is broadening their scope for

younger women by introducing the sub-brand aerie. Aerie is a line that

specializes in dormwear and intimates. By expanding through sub-brands,

American Eagle is making itself more competitive with the leaders in the industry

(www.ae.com).

EXPANSION TO CANADA

In 2000, American Eagle purchased three Canadian businesses:

Bluenotes, which was recently discontinued, Braemar, and National Logistics

Services (NLS). Bluenotes is a previously established Canadian retail store. By

acquiring a well known clothing chain, Canadian consumers were able to

maintain confidence in the firm’s products. Braemar is similar to American Eagle

with premier mall locations. NLS is a 400,000 square foot distribution center

located near Toronto, and it enables American Eagle to ship products to the

growing Canadian market (AEO 10-K) (www.ae.com). By expanding into

Canada, American Eagle has created a competitive advantage by being on the

forefront of Canadian expansion within the industry. This creates barriers for

entry for American Eagle’s competitors because consumers are more likely to

trust the brand that they have been around the longest.

- 27 -

THE FUTURE OF AMERICAN EAGLE

American Eagle is expected to continue expansion in Canada and the

United States. Currently, there are no disclosed plans for expansion into Europe;

however, e-commerce allows people worldwide to purchase American Eagle

products. By expanding through e-commerce, American Eagle has unlimited

potential for future growth (www.ae.com).

Formal Accounting Analysis

Companies often distort financial statements to produce numbers more

appeasing to shareholders and reflect a better picture of the company. This bias

clouds the true value of the company and therefore the firm must be

reevaluated. The purpose of analyzing companies’ accounting policies is to undo

the accounting distortions to better assess the financial infrastructure of the

company (Palepu, 3-4). Bias can come from three different sources: noise from

accounting rules, forecast errors, and managers' accounting choices. Accounting

rules sometimes create noise because "it is often difficult to restrict management

discretion without reducing the information content of accounting data" (Palepu,

3-4). Forecast errors occur because it is difficult to predict what is going to

happen and how much inventory to have on hand for the future. It is also

difficult to accurately predict bad debt expense and write-offs. GAAP allows

managers to choose to be more aggressive or conservative when implementing

certain accounting policies. Ideally, the manager will aim for an accounting policy

somewhere between the two extremes. Managers also hold freedom to a level of

disclosure in regards to the firm’s financial statements. When a firm improves its

disclosure level, an analyst has a better chance of valuing the company

accurately.

- 28 -

Key Accounting Policies

In identifying key accounting policies, we consider the key success factors

of the industry and how American Eagle deals with and accounts for those

success factors. It is also important to analyze the level of disclosure with

regards to these success factors. In the retail industry, we analyze how American

Eagle manages its inventory and then compare it to the rest of the industry. We

should also review the way American Eagle deals with their leases and gift

cards. We need to look at the firm’s benefit and retirement plans and how they

account for goodwill impairments. The final two things we should examine are

how they handle expenses related to marketing and branding.

American Eagle leases both its retail spaces and the warehouses used to

store their merchandise. This makes them a cost leader because it allows for

tight cost control. GAAP flexibility allows many firms in this niche industry to use

the operating leases. American Eagle tends to establish contractual five to ten

year leases with set annual rental payments. The firm accounts for these rental

expenses though the use of operating leases. These operating leases could in

fact be revalued at a more applicable level though the use of capital leasing. This

is possible because American Eagle holds the future rights to these rental

properties with lease holding rights. Since American Eagle has acquired the

future use of the properties through contracts, they could list it as an asset on

the consolidated balance sheet to show a more accurate representation of the

company.

The subsequent chart compares the estimated present value of capital

leases to the present value of operating leases based on an industry mortgage

rate of 8%. Most retail firms prefer operating leases to capital leases simply

because operating leases will minimize liabilities and keep these contractual

obligations off of the balance sheet. American Eagle and its competitors have

true capital leases however, because stores are found in malls. The corporation

that owns the mall leases space to retail stores. By capitalizing American Eagle’s

- 29 -

leases we will gain an insight to their balance sheet that can show issues within

their liabilities and assets.

Operating & Capital Lease Present Values

$0$100,000$200,000$300,000$400,000$500,000$600,000$700,000$800,000$900,000

$1,000,000

2002 2,003 2004 2004 2006

Year

Pres

ent V

alue

s (th

ousa

nds)

Operating Lease PVCapital Lease PV

American Eagle evaluates their goodwill every year; however, the number

has not changed in the past two years. Goodwill for the past fiscal year was

nearly one million while assets were 1.6 billion. Therefore only .6% of American

Eagle’s assets are based on goodwill. This is a .1% drop from the previous

year's goodwill. Previously, the goodwill decreased at an accelerated rate due to

impairment. In 2003 American Eagle approximated its goodwill decreased value

by an approximated $14.1 million due to the "continued weak performance of

the Bluenotes segment" (AE 2003 10-K). Although American Eagle properly

recognized goodwill impairment, it failed to amortize the goodwill over a given

amount of time. If the goodwill held a greater portion of the company’s assets, it

would be considered an aggressive accounting strategy if the firm failed to

amortize it on an annual basis. By disclosing the amortization of the goodwill, an

analyst can better value the company’s true total asset value.

American Eagle increased inventory and the number of store locations over

the past five years. Sales have increased along with inventory. Inventory as a

- 30 -

percentage of sales is approximately 9.07% for the 2004 fiscal year. This

percentage stayed at about 9.13% for the 2005 fiscal year, and in fiscal 2006

this ratio increased to 9.4%. This shows the company is attempting to maintain

a steady ratio between sales and inventory. American Eagle efficiently

outsources production, and is able to better maintain a low cost of production

which leads to a greater profit margin. Although American Eagle outsources

production, it holds rigorous standards for the quality of its clothing. These

higher standards help American Eagle differentiate from the competition. These

disclosures in the 10-K allows analysts to place additional value on the high

standard for quality clothing and therefore determine a more relevant value.

American Eagle participates in a 401(K) plan and a stock purchase plan.

Both of these plans include company matches up to a certain percent. This falls

under customer service because both of plans require employees to stay

employed in order to optimize their potential benefits. The benefit plans attract

higher quality employees, which in turn improves customer service in the long

run. It also reduces training costs for new employees by encouraging current

employees to work diligently and increase employee loyalty to American Eagle.

The disclosure in the annual report reveals American Eagle puts a high emphasis

on taking care of their employees through the use of these benefit plans.

Gift cards are a means to increase the switching costs for customers,

which guarantees American Eagle a liability that they will later expense within

the next two years when the cards are redeemed or expired. American Eagle

had a more than 10 million dollar increase in unredeemed store value cards and

gift cards from fiscal years 2005 to 2006. This number reflects the value of gift

cards that are over two years old and can legally be counted as revenue.

American Eagle defines and utilizes gift cards as a key success factor (AE 10-K).

American Eagle established itself by initially creating the brand name and

then advertising the logo. This was accomplished through purchasing a

trademark and also implementing extensive advertisements. By creating a

demanded brand, the company then allows the customers to continue the

- 31 -

advertisements with a simple eagle logo found on the bottom of an American

Eagle shirt to set it apart from other clothing brands. These things come at a

cost, with trademark expenses and advertising expense. Advertising expenses

made up $53.3 million of Fiscal 2005's budget. Trademark costs are included in

intangible assets and are amortized over five to fifteen years. Although these

costs must be expensed, they also create true value for future cash flows with

potential customers.

Accounting Flexibility

Financial Statements for publicly traded companies must follow Generally

Accepted Accounting Principles (GAAP). GAAP attempts to set accounting

standards which will allow consistent evaluations of each firm within an industry

on a level field. GAAP allows for quite a bit of flexibility in certain areas. The

flexibilities are there to ensure truer valuations on the different financial

statements. However, some aspects of GAAP severely limit firms’ abilities to

properly value their company. Assessing the degree of accounting flexibility of a

particular firm’s key accounting policies will allow us to properly identify where a

firm might biasly report its worth instead of presenting a true value. These

discrepancies might come from limitations or flexibilities in GAAP.

American Eagle utilizes the flexibilities in GAAP to report different aspects of

its key accounting policies. Leases can be classified operating leases or capital

leases, but most of the firms in the specialty retail industry, including American

Eagle, choose to record leases as operating leases. GAAP allows for this

flexibility because not all leases are the same, and the different types require

different accounting measures. American Eagle chose operating leases because

it can reduce liabilities. This flexibility allows for these firms to manipulate their

values to shareholders.

American Eagle also utilizes the flexibilities of GAAP with respects to

estimating depreciation and amortization rates and schedules. GAAP will let the

- 32 -

firms decide how they want to value their assets because every asset is different.

Assets provide different values to different firms across industries. It would be

almost impossible to establish standards for every type of asset. Therefore,

assets such as goodwill can be amortized at the rate at the company’s discretion.

American Eagle has great flexibility in these areas, and the true value of the firm

is distorted because of the flexibility.

American Eagle also exercises flexibility by recognizing inventory at a

lower of average cost or market as opposed to LIFO or FIFO like other retailers.

In this method, American Eagle expenses cost of goods sold by using the lesser

of the weighted average cost as compared to the estimated market value. Some

may consider this to be a fairly accurate method which expresses the true value

of the inventory sold. However, American Eagle has autonomy in these

“estimations”, which may not be entirely unbiased.

GAAP allows for great flexibility with respects to merchandising

markdowns. American Eagle expenses merchandise markdowns at the current

term instead of counting the markdown as a contra-asset. GAAP also mandates

accrual based accounting for publicly trade firms. The American Eagle 10-K cites

in Fiscal 2004, the company had a net increase in cost of sales by $359,000. The

firm discloses that a non-related third party purchased the marked down

merchandise in a “strategic plan to eliminate transactions” with related parties

(AE 10-K). With the lower of average cost or market inventory system, the

company must expense the marked down merchandise. By selling it to a third

party, merely the proceeds affect the cost of goods sold and therefore the

company minimizes costs. If American Eagle did not find a third party to

purchase the merchandise, it would have to expense the entire loss to cost of

goods sold and would not recover any compensation. Selling to a third party

enables the firm to forgo the greater loss. However, this flexibility may have

been used to inaccurately report the firm’s value in the financial statements.

Gift cards provided limited room for flexibility. In the retail industry, the

companies recognize unearned revenues and increase liabilities until the gift card

- 33 -

is redeemed or expired. At that point, the revenue from the gift card is

recognized. American Eagle exercises flexibility by choosing to expiring gift cards

after two years. The card then requires a one dollar per month reactivation fee

after that time. American Eagle has been given much flexibility with deciding how

fast and how long to expire the gift cards.

Although GAAP allows for much flexibility in the industry, it also enforces

strict regulations in certain accounting areas. "Marketing and brand building are

key to the success of consumer goods firms, they are required to expense all

their marketing outlays" (Palepu 3-7). This portion of the retail industry must

expense advertisements and marketing. Firms in the specialized retail industry

rely on marketing to establish a strong customer base. This strong customer

base or future economic benefit could be considered an asset. Due to the

inflexibility of GAAP in this accounting aspect, assets might be greatly

undervalued.

Accounting Strategy

Based on the degree of accounting flexibility allowed by GAAP in the

specialty retail industry, firms such as American Eagle choose how aggressive or

conservative they would like to report different aspects of the financial

statements. This is important because flexibility enables managers of a company

to over additional explanations or to hide facts in the financial statements. A

good balance between the two extremes is essential to a firm's success, so they

may provide enough information to offer shareholders a representative value

while not unfolding all of their key business strategies to the competition. In the

United States firms can choose where they would like to be in the spectrum. We

can evaluate the accounting strategy by comparing American Eagle's accounting

policies to industry wide accounting policies.

American Eagle uses operating leases as opposed to capital leases as

discussed in the previous sections. By using operating leases, the firm only

- 34 -

recognizes the current year’s rent as a liability. When capitalizing a lease,

liabilities are increased by the present value of all future rent payments.

Liabilities increase by this future value and so assets also increase by this future

value. American Eagle has a contract to the future rights of the leased property;

therefore, the leases could be capitalized as assets. By not capitalizing the

leases, the firm understates its liabilities, making it more appealing to lenders.

This practice leads to overstating the company’s value and could be considered a

very aggressive accounting policy.

American Eagle is one of two firms in the industry that records goodwill as

an asset that has enough significance to disclose on the balance sheet. The

amortization rate of goodwill is based on the opinion of the upper level

managers. American Eagle annually reevaluates the market value of its goodwill

and checks for impairments. A very conservative firm would choose to quickly

amortize goodwill. Conversely a very aggressive firm might inflate its assets by

slowly amortizing goodwill. This reduces annual expenses and artificially inflates

net income. The annual reevaluations of goodwill are neither aggressive nor

conservative conveying a relatively true value of goodwill.

American Eagle reports inventory at lower of average cost or market

utilizing the retail method. This means "markdowns are fully accounted for in

the month in which they have been taken. It assumes most of the markdowns

apply to goods sold and therefore that few of those goods are part of the ending

inventory" (www.cfpsa.com). Looking at other firms in the industry,

Abercrombie & Fitch and The Limited Brands use this same method with their

inventory, while Aeropostale and The Gap use the first-in first-out method.

Assuming inflation, the first-in first-out method will provide an artificially low cost

of goods sold which will inflate net income. This inventory accounting is

considered aggressive. Conversely a last-in first-out method would be

conservative accounting. Because of the method American Eagle has chosen to

use, they are again neither aggressive nor conservative. The market rate that is

- 35 -

involved in their inventory calculations reveals a more relevant estimate of

inventory value.

By reporting gift cards as a current liability, American Eagle practices

conservative accounting. American Eagle only recognizes revenue when the gift

card is redeemed for merchandise. American Eagle can also credit their selling,

general, and administrative expenses when a card has been inactive for more

than twenty-four months. A more aggressive firm would deduct more value from

a gift card at a faster rate for inactivity on the account. This will allow them to

recognize more revenue sooner. Conversely a more conservative firm might not

recognize revenue from unredeemed gift cards for an unidentified time period.

American Eagle, once again, appears to have taken a moderate stance in

another area of their financial statements.

Overall American Eagle is relatively moderate in accounting for their key

success factors. Because of this, their financial statements more closely reflect

true values than other firms that take more aggressive or conservative stances.

Quality of Disclosure

The quality of disclosure is important because it helps identify a

company’s accounting strategy. Poor disclosure potentially raises red flags; a

company may be concealing information to smooth out financial statements.

Disclosure elaborates on the business based on the consolidated financial

statements through the use of footnotes and explanations. Quality of disclosure

has more importance than the quantity of disclosure. This is a very important

distinction because a firm that discloses more than enough information could be

trying to overwhelm analysts and stockholders, so they miss underlying problems

the company is facing.

In previous fiscal years, AE presented a higher quality of disclosure. As

we continued to search for necessary line items to compute ratios to gain a

better understanding, we ran into problems. The company offers a poor list of

- 36 -

what liabilities entail and fails to offer essential information such as the interest

rates that accompany debt. By failing to disclose this information we must make

assumptions to determine the value for the company. However, American Eagle

disclosed how each new FASB Pronouncement directly affected their financial

statements with respect to Fiscal 2004, and how it will affect the company in

years to come. Many entries on the financial statements have supplementary

notes to help better explain specific entries. The table of contents is very

informative and specific. This makes it easier to find specialized information.

American Eagle also experienced disclosure problems in a few other

areas. For example, the "Merchandise Inventory" disclosure was confusing

because American Eagle uses lower of average cost or market, but they did not

define what the implications of utilizing that method entailed. American Eagle

did not disclose the legal proceedings that arise out of the conduct of business.

The vagueness of the "legal proceedings and claims" section leaves the investor

to draw their own conclusions about such an important aspect of business.

SALES MANIPULATION DIAGNOSTICS

Sales manipulation diagnostics allows analysts to compare net sales

dollars to other revenue related accounts: cash from sales, net accounts

receivables, unearned revenues and inventory. The following tables compare

American Eagle with its major competitors in the retail industry over a five year

span. The tables also provide a five year average among the industry. By

comparing the five most recent years, we can compare American Eagle to within

the industry to identify red flags, and determine how past accounting policies

influenced where the company is now.

- 37 -

Net Sales/Cash From Sales

0.99

1.00

1.01

1.02

1.03

2002 2003 2004 2005 2006

Year

Net

Sal

es/C

ash

from

Sal

es

American Eagle

Abercrombie and Fitch

Aeropostale

Gap

Limited

Industry Average

In this section of the retail industry, the net sales/cash from sales ratio

suggests that almost all revenue in net sales comes from cash over the past five

years. The accounts receivable (non-cash sales) makes up a minimal portion of

sales and therefore hardly impacts the ratio. This stays consistent over the five

year period throughout the industry. A third party assumes all of the consumer

accounts receivable and compensates American Eagle with cash. Therefore,

Accounts Receivable from customers is never actually recorded on the company’s

balance sheet. This is how companies in the apparel industry maintain a net

sales/cash from sales ratio so close to one. This means that the industry, based

solely on this ratio has some liquidity.

- 38 -

The net sales/net accounts receivables ratio for the past five years in the

retail industry was inconsistent and unpredictable. After looking into American

Eagle’s previous 10-Ks, we found accounts receivables detailed, and then we

analyzed the dramatic increase in 2003. The increase is a result of collected

smaller increases over different categories including fabrics, related parties, sell-

offs to non-related parties, etc. which caused a substantial overall effect in

accounts receivable. Aeropostale and Gap cannot be included in this ratio

because they do not disclose their accounts receivables balance in their 10-Ks.

These numbers tell us that, although most of the companies in the industry do

have accounts receivable, this balance makes up a very small portion of their

business.

Net Sales/Net Accounts Receivables

0.00

50.00

100.00

150.00

200.00

250.00

2002 2003 2004 2005 2006

Year

Net

Sal

es/N

et A

ccou

nts

Rec

eiva

bles

American Eagle

Abercrombie and Fitch

Aeropostale

Gap

Limited

Industry Average

- 39 -

Unlike its competitors, American Eagle discloses unearned revenues due

to gift cards. This disclosure allows us to assess net sales/unearned revenues

ratio. By listing the unearned revenue, American Eagle recognizes it is liable to

the customer, and it allows analysts to acknowledge potential liabilities that may

be recorded as assets in future periods.

Net Sales/Unearned Revenues

56.0058.0060.0062.0064.0066.0068.0070.0072.00

2002 2003 2004 2005 2006

Year

Net

Sal

es/U

near

ned

Rev

enue

s

AEOS

Net Sales/Inventory

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

2002 2003 2004 2005 2006

Year

Net

Sal

es/In

vent

ory American Eagle

Abercrombie and Fitch

Aeropostale

Gap

Limited

Industry Average

- 40 -

The net sales/inventory ratio for the past five years has steadily

decreased. This is consistent with the industry, although American Eagle is

higher than the industry average. American Eagle has been attempting to better

match inventory with projected sales to become more efficient and drive the

ratio down. American Eagle is decreasing the ratio in order to become more like

the industry leaders. As it shifts its trend to a more stable and cost efficient level

of inventory, they further secure their place in the market. This ratio informs

analysts that this industry is very efficient and appears to be getting more

efficient with time.

CORE EXPENSES MANIPULATING DIAGNOSTICS

On the other side of the spectrum, core expense manipulating diagnostics

analyze how expenses affect operations and production. If expenses decrease

too much, then there is a chance the expenses are understated and therefore

signaling a red flag.

Declining Asset Turnover

0.00

0.50

1.00

1.50

2.00

2.50

3.00

2002 2003 2004 2005 2006

Year

Dec

linin

g A

sset

Tur

nove

r

American Eagle

Abercrombie and Fitch

Aeropostale

Gap

Limited

Industry Average

- 41 -

The total asset turnover ratio measures net sales divided by total assets. A

company wants its assets to produce more sales, and therefore should strive for

a higher ratio. In the retail industry, all of the companies seem to have a

wavering ratio and therefore American Eagle’s declining ratio does not merit a

red flag. Looking into American Eagle’s sales compared to assets, the figures are

both inclining at a steady rate. Because American Eagle has been restructuring

their company, this could explain the declining ratio. A red flag is not merited

because in the most recent years the ratio has been increasing, and American

Eagle remains close to the industry average.

American Eagle’s four year average for changes in cash from operating

cash flow over operating income is higher than the other averages in their

portion of the retail industry. This implies investments made in operating income

effectively increased the cash flows from operations. This average is heavily

biased by the Fiscal year 2003 where the ratio is .83. Although a .83 ratio looks

Changes in CFFO/OI

-0.80

-0.60

-0.40

-0.20

0.00

0.20

0.40

0.60

0.80

1.00

2002 2003 2004 2005 2006

Year

Cha

nges

in C

FFO

/OI

American Eagle

Abercrombie and Fitch

Aeropostale

Gap

Limited

Industry Average

- 42 -

appealing on face value, the ratio is so high because of a significant decrease in

operating income. The operating income stabilized over the remaining years in

the average. Because of the stabilization process, American Eagle’s ratio does

not raise a red flag.

The cash flows from operations to net of assets ratio compares CFFO

against plant, property, equipment (net of depreciation) and inventory. American

Eagle produces higher than industry average ratios because they increase their

CFFO at a much greater rate than the competitors. American Eagle increases by

more than $100,000,000 while their competitors increase their CFFO by closer to

$50,000,000. This indicates the firm is growing at a much faster rate than the

other companies in the industry. Reading American Eagle’s 10-K leads us to

conclude that American Eagle’s growth strategy causes this ratio to be so high.

American Eagle plans how many stores to implement each year, and this number

is higher than other firms in the industry.

Changes in CFFO/NOA

-0.30

-0.20

-0.10

0.00

0.10

0.20

0.30

0.40

2002 2003 2004 2005 2006

Year

Cha

nges

in C

FFO

/NO

A

American Eagle

Abercrombie and Fitch

Aeropostale

Gap

Limited

Industry Average

- 43 -

The total accruals/change ratio in sales analyzes the inventory less the

cash flows from operations over the change in sales. This ratio is negative

because the CFFO is higher than the inventory. Changes in sales are increasing

which drives the ratio even smaller in Fiscal 2004 and 2005. The AE 10-K fails to

disclose additional reasons for the smaller ratio. This ratio would raise a red flag

when looking at just American Eagle, but the entire industry also has a negative

ratio. Because this negative ratio is seen industry wide we must assume that it

is standard for the industry. American Eagle’s ratio falls in the middle of the

industry which also provides some confidence that this ratio should not be

alarming.

The figures for these ratios were easy to find in the American Eagle 10-K

as opposed to their competitors. Gap and Aeropostale both failed to report their

accounts receivables but instead lump them into oversimplified categories such

as current assets. American Eagle’s disclosure elaborated on many of their

policies including retirement plans, the details of expenses, and plenty of

footnotes to elaborate on management’s reasons and methods. This helps not

Total Accruals/Change in Sales

-2.00

-1.50

-1.00

-0.50

0.00

0.50

1.00

2002 2003 2004 2005 2006

Year

Tota

l Acc

rual

s/C

hang

e in

Sal

es

American Eagle

Abercrombie and Fitch

AeropostaleGap

Limited

Industry Average

- 44 -

only investors, but analysts so we can better appraise the true value of the

company.

CONCLUSION

These diagnostics deal with sales and expense manipulation in many

ways. Most of the ratios include sales as one part of them. It is easy to spot

areas that a company in the industry attempts to compensate their numbers by

comparing each ratio to the industry and the industry average and also analyzing

the relevant revenues or expenses. American Eagle has very few examples

where the ratio is not around the industry average. This can be explained by

American Eagle’s recent growth strategy and restructuring.

Potential Red Flags

Analyzing "red flags" can show potential pitfalls of the firm. "Red flags"

are the easiest way to find quality errors in accounting. Although "red flags" can

be hazardous to a company, some red flags deal with good business practices.

In looking for "red flags", the fourth quarter statements are crucial. This is

because adjustments are more likely to be made in this time period trying to

smooth out end of year numbers to appeal more to stock holders. We should

watch for changes in auditors, financial ratios changing, and changes in

accounting in the face of poor performance. We should examine accounts

receivable and inventory in relation to sales, and if there is a big change we

should be concerned.

American Eagle’s disclosure level allowed us to analyze ratios and

management strategies clearly and have yet to find substantial red flags. Even

so, there are a few factors we need to double check before approving of all

accounting. Two of these factors include their leases and how they amortize

goodwill. The operating leases produce the only noteworthy “red flag” because

the company expenses leases instead of capitalizing the lease as an asset and

- 45 -

adding the liability. American Eagles amortization of goodwill is not significant

and does not greatly affect the accounting of the firm.

Undo Accounting Distortions

After going through this long process, it is possible to "fix" the accounting

of a company so that we can see what is really going on in a business. American

Eagle’s operating leases could be considered a distortion because the lease

contract implies future economic gain. Therefore, the leases should be

capitalized as assets in order to properly value the firm’s assets. By not doing

this, it overvalues the firm because the liabilities are understated. The following

is a table showing the present value of operating leases as opposed to

capitalized leases.

Capitalization of American Eagle's Operating Leases

Operating Leases Capital Leases Year FV PV Factor (8%) PV Year FV PV Factor (8%) PV 2006 $149,645 0.926 $138,560 2006 $157,582 0.926 $145,909 2007 $149,545 0.857 $128,211 2007 $150,530 0.857 $129,055 2008 $145,321 0.794 $115,360 2008 $142,922 0.794 $113,456 2009 $137,838 0.735 $101,315 2009 $135,044 0.735 $99,261 2010 $124,257 0.681 $84,567 2010 $127,133 0.681 $86,525 2011 $165,352 0.630 $104,200 2011 $119,676 0.630 $75,416 2012 $165,352 0.583 $96,481 2012 $108,335 0.583 $63,212