think smaller for big growth · 2 think smaller for big growth • nearly half of global...

TRANSCRIPT

1Copyright © 2016 The Nielsen Company

Think Smaller for Big growThHow to tHrive in tHe new retail landscape

June 2016

2 Think Smaller for Big growTh

• Nearlyhalfofglobalrespondents(46%)saygroceryshoppingisachorethatthey

trytospendaslittletimeonaspossible.Thislowlevelofsatisfactionprimarily

stemsfromabeliefthatretailersdon’tunderstandanddeliverontheirneeds.

• Valueisaboutmorethanjustthelowestprice.Infact,consumersratehigh-quality

produce(57%),convenientlocation(56%)andproductavailability(54%)asmore

influentialinstore-selectiondecisionsthanthelowestprice.

• Manufacturersandretailersaredependentonpromotions.Tobreakthecycle,they

needtoknowwhichcategoriesaremoreorlesspricesensitive.Notsurprisingly,

discretionarycategoriesaremoresensitivetopriceincreasesthanstapleproducts.

SentimentinLatinAmericaandEuropesuggeststhatconsumerstherearemore

sensitivetopriceincreases,whileNorthAmericanrespondentsaretheleast

sensitive.

• Healthandwellnessisatoppriorityforconsumersaroundtheworld.Two-thirdsof

globalrespondents(67%)saytheyactivelyseekproductswithhealthfulingredients.

• Consumerscraveconvenienceandspeed;qualityprepared-mealoptionsandin-

storediningexperiencescanbeakeydifferentiatorforwhereconsumersdecide

toshop.Astheroleofthephysicalstoreevolves,in-storeadd-onservicesmay

drivesatisfactionandvisits.In-storebanking(42%),fastfood(40%),prepared

food(40%)andpharmacy(39%)arethemostwidelyavailableandusedin-store

services,butinterestinseveralothersishigh.

• Assortmentandproductavailabilityarebasicrequirementsinstore-selection

decisions,butwithlimitedshelfspaceinsmallformatsandanincreasing

expectationforcustomizedproductofferingsandrecommendations,gettingthe

assortmentpiecerightincreasinglymeansshiftingfromapushtoapullmind-set,

drivenbyconsumerdemand.

around The world

2

reTail evoluTion: why markeTing To The middle doeSn’T work anymore

3Copyright © 2016 The Nielsen Company 3

About the GlobAl Survey MethodoloGy

Thefindingsinthissurvey

arebasedonrespondents

withonlineaccessin61

countries(unlessotherwise

noted).Whileanonline

surveymethodologyallows

fortremendousscaleand

globalreach,itprovidesa

perspectiveonthehabitsof

onlyexistingInternetusers,

nottotalpopulations.In

developingmarketswhere

onlinepenetrationisstill

growing,respondentsmaybe

youngerandmoreaffluent

thanthegeneralpopulation

ofthatcountry.Inaddition,

surveyresponsesarebased

onclaimedbehavior,rather

thanactualmetereddata.

Culturaldifferencesin

reportingsentimentarelikely

factorsintheoutlookacross

countries.Thereportedresults

donotattempttocontrolor

correctforthesedifferences;

therefore,cautionshouldbe

exercisedwhencomparing

acrosscountriesandregions,

particularlyacrossregional

boundaries.

Modernretailhaslongbeenguidedbyapowerfulpremise:thebigger,the

better.Bigwasbetterforretailersbecausescaledrovedownunitcostand

soraisedreturnoninvestment(ROI).Itwasalsobetterforconsumers,who

gainedaccesstogreaterassortment,betterpricesandconvenientone-stop

shopping.Andbigwasbetterforsuppliers,whobenefitedfromgreatershelf

spacetodeploybrandandcategoryportfoliostrategies.

Overthepast10to15years,however,themodernretailstoremodelhas

evolved.Supplychainprocessimprovementshavemadeitpossibletoachieve

similarorevenhigherlevelsofprofitabilitywithsmallerstores,pavingtheway

forsmallerretailchainstoexpandandtakesharefromlargercompetitorsin

manymarkets.Shoppers,whoareabletomatchtheirpreferredstoreformat

morepreciselytotheirshoppingneedsandpreferencesondifferentpurchase

occasions,havebenefitedgreatlyfromthisincreaseinstoreformats.

Butformanybig-boxretailerstheshifthasn’tbeensuchaboon.Theresult

isthattoday’sretailenvironmentismorefragmentedthanever.Fierce

competitionforshoppershasledtoanincreasingdependencyonpromotions

amonglargeretailers.

Inaddition,fallingbirthrates,risingfoodprices,andstagnantwagesare

makingvolumegrowthindevelopedmarketsdifficulttoachieve.Meanwhile,

developingmarkets,whichwereexpectedtofollowthesameretailevolution

blueprintasdevelopedmarkets,haveforgedtheirownpath.Inseveral

markets,includingChina,Indonesia,PolandandTurkey,small-formatstores

havedriventhetransitiontomodernretail.Manyothermarketsarestill

undergoingtheshifttomodernretail—andit’slikelythatsomeofthese

developingmarketswillpartiallyskipthebrick-and-mortarphasebymoving

onlineearly.

“Perhapsthenewretailmantrashouldbe‘Gosmallorgohome,’asthe

‘Biggerisbetter’paradigmhasbeenchallengedvirtuallyeverywhere,”said

SteveMatthesen,globalpresidentofRetail,Nielsen“Hyper-localizationand

specializationarefuelingtoday’sretailgrowth.Aslifestyleandconsumption

habitschange,we’reseeingastructuralshiftinwhereconsumersshopand

whattheybuy,andsomesmallformatsaredrivingbiggrowth.Mass-market

strategiesarealsolosingrelevanceasconsumerslookforuniqueexperiences

thatmeettheirpersonaldemands.”

TheNielsenGlobalRetail-GrowthStrategiesSurveypolledmorethan30,000

onlinerespondentsin61countriestounderstandthepainandthepleasure

pointsabouttheshoppingexperience.Weexaminedhowwellretailers

arecurrentlymeetingconsumers’needsandwhyconsumerschooseone

storeoveranother.Wealsoreviewedaselectionof19productcategoriesto

determinetheproductattributesthataremostimportant.Lastly,wetooka

lookatconsumers’willingnesstouseadditionalin-storeservicesandtheir

preferredapproachtodealingwithpriceincreases,inordertoidentifyareasfor

developmentorimprovement.

4 Think Smaller for Big growTh

adapTing To ShifTing demographicSWanttoanticipateemergingtrendsinstoreformatpreferences?Startby

lookingatthedemographicandsocioeconomictrendsaffectingtheretail

landscape.Theshopofthefutureshouldbeareflectionoftheshopperofthe

future,anddemographicshiftsareshapingconsumers’preferences.Considera

fewofthem:

• Risingmiddleclass.TheOrganizationforEconomicCooperationand

Developmentpredictstheglobalmiddleclasswillincreaseto3.2billionby

2020andto4.9billionby2030.Economicprosperitywilllikelybeagrowth

engineforconsumption,especiallyinChinaandIndia,ashistoryhas

shownthatthoseinthemiddleclassenthusiasticallyacquirebothphysical

andhumancapital.Atthesametime,however,fallingrealincomesin

somedevelopedmarketsmaydrivethegrowthofvalueformatsthere.

• Urbanization.TheUnitedNationsprojectsthattwo-thirdsoftheworld’spopulationwillliveinurbanareasby2050,upfrom54%in2014.This

migrationhasalreadyledtotheriseofmegacities—citiesof10million

peopleormore—whichnearlytripledinnumberbetween1990and2014

(from10to28).Urbanizationtypicallydrivesconsumption—increasedjob

opportunities,acentralizedmarket,betterpayandtheprospectofhigher

individualwealthhavealldrawnpeopleintocities—anditwillhavemajor

implicationsforretailersinthefuturewithregardtostorelocation,store

footprintandomnichannelstrategies.Asmoreconsumersmovetourban

areas,retailerswillfollow.Smallstoresarewellsuitedtourbansettings

wherespaceisatapremium.

• Millennials.Globally,therearealmost2billionMillennials,andin

manyplaces,they’rericherandsmarterandhavemorefreedomsthan

anygenerationbeforethem.Theiruseoftechnologysetsthemapart:

Millennials(definedbytheU.S.Censusasthosebornbetween1982and

2000)grewupwiththeinternet,socialmediaandmobileasthenorm;in

fact,manydon’tknowaworldwithouttheseelements.Inaddition,many

cameofageduringperiodsofglobalizationandeconomicdisruption.Asa

result,theyhavedifferentexpectations,attitudesandbehaviorsthantheir

oldercounterparts.WithMillennials’comingintotheirprimeworkingand

spendingyearstoday,understandingthiscohort’sneedsanddemandsis

criticaltoretailers’healthandgrowth.

Asshiftingdemographictrendsmakeanindeliblemarkontheretaillandscape,

manyestablishedretailrealitiesneedcloserscrutiny,too.Fromthein-store

shoppingexperiencetopricing,productassortmentandagreaterneedfor

locationsnearby,consumers’expectationsarechanging—andso,too,must

consumerstrategies.

two-tHirds of the world’s

population will live in an urban

area by 2050

5Copyright © 2016 The Nielsen Company

ShoPPING IS A Chore For hAlF ArouNd the World

PerCeNtAGe Who StroNGly/SoMeWhAt AGree ShoPPING IS

A Chore

Source:NielsenGlobalRetail-GrowthStrategiesSurvey,Q32015

Latin america

46%

asia-Pacific

48%

euroPe

38%

africa/middLe

east

53%

GLoBaL

46%

iS iT poSSiBle To Turn choreS inTo cheerS?Howcanretailersstayaheadintherapidlychanginglandscape?Theycan

startbyassessinghowwellthey’redoingnow.Whatdoconsumersthink

abouttheshoppingexperience,andhowwelldotheythinktheirneedsare

currentlybeingmet?

Formany,groceryshoppingisachore.Infact,nearlyhalf(46%)of

respondentsaroundtheworldsaygroceryshoppingissomethingtheytry

tospendaslittletimeaspossibledoing.Sowhatisitabouttheshopping

experiencethatisparticularlyunpleasant?

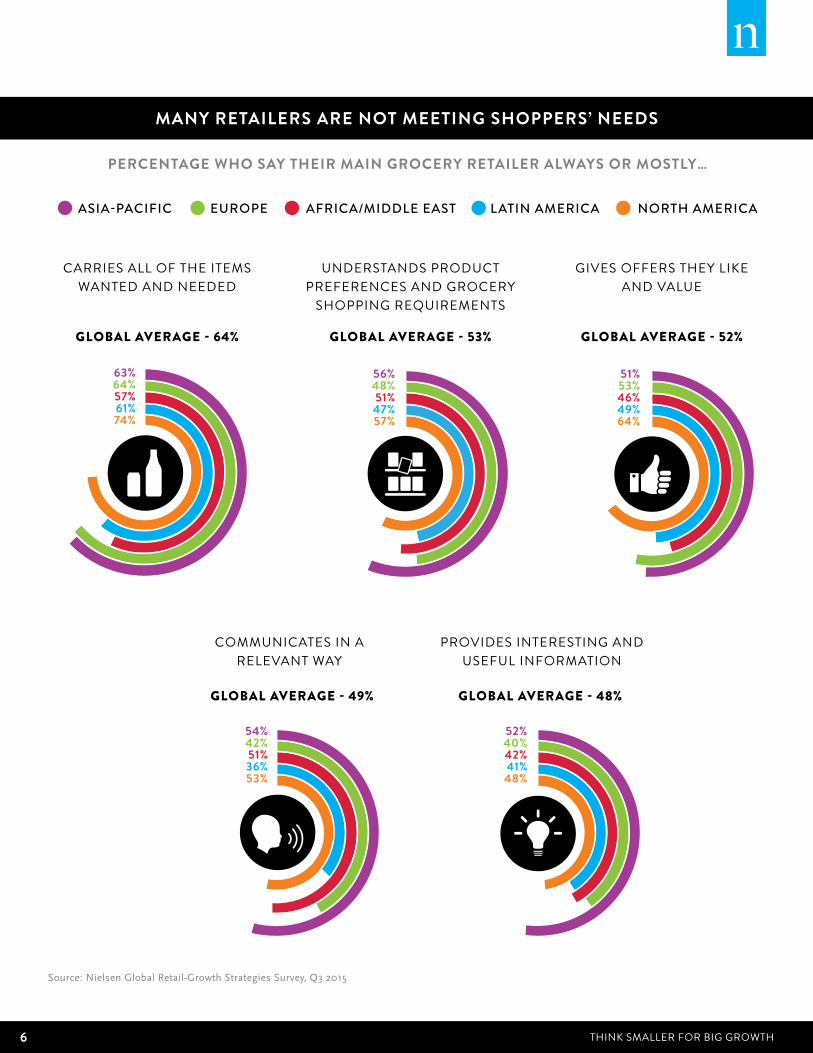

Perhapsthebiggestpainpointforconsumersisthatmanythinkretailers

don’tunderstandanddeliverontheirneeds.Lessthanhalfofglobal

respondents(49%)believetheirmaingroceryretaileralwaysormostly

communicateswiththeminarelevantway.Justoverhalfbelieveretailers

alwaysormostlyunderstandtheirgroceryrequirement(53%)andprovide

offerstheylikeandvalue(52%).Globally,retailersaredoingbetteronthe

productassortmentfront:64%saytheirmaingroceryretaileralwaysor

mostlycarriestheitemstheywant.

Butsentimentisn’tthesameeverywhere.RetailersinNorthAmerica—

and,toalesserdegree,Asia-Pacific—seemtobedoingabetterjobthan

theircounterpartsinEuropeandLatinAmerica.NorthAmericanretailers

particularlystandoutwhenitcomestoproductassortmentandproviding

valuedoffers.Roughlythree-quartersofNorthAmericanrespondents

(74%)saytheirmaingroceryretaileralwaysormostlycarriestheitemsthey

want,10percentagepointsabovetheglobalaverage(64%),andalmost

two-thirds(64%)saytheirmaingroceryretailerprovidesthemwithoffers

theylikeandvalue(comparedwith52%globally).Ofcourse,it’simportant

tonotethatNorthAmericanretailersmayberatedmorepositivelyinterms

ofassortmentbecausetheyhavemoreshelfspacetoworkwith.Inthe

U.S.,theaveragesellingspaceisabout25,000squarefeet.

north america

46%

6 Think Smaller for Big growTh

MANy retAIlerS Are Not MeetING ShoPPerS’ NeedS

PerCeNtAGe Who SAy theIr MAIN GroCery retAIler AlWAyS or MoStly…

asia-Pacific

Global averaGe - 64% Global averaGe - 53%

Global averaGe - 49%

Global averaGe - 52%

Global averaGe - 48%

euroPe africa/middLe east Latin america north america

understands product preferences and grocery

shopping requirements

gives offers they like and value

communicates in a relevant way

carries all of the items wanted and needed

56%48%51%47%57%

51%53%46%49%64%

63%64%57%61%74%

provides interesting and useful information

54%42%51%36%53%

52%40%42%41%48%

Source:NielsenGlobalRetail-GrowthStrategiesSurvey,Q32015

7Copyright © 2016 The Nielsen Company

price iS imporTanT, BuT iT’S noT everyThingAcoreelementinincreasingshareofwalletisunderstandingand

respondingtolocalconsumerneeds.Differentiationisthewaytobuild

acompetitiveadvantage.Sowhatareconsumerslookingfor?

It’snosurprisethatpriceisimportant;italwayshasbeenandalways

willbe.Infact,whenweexaminedthefactorsthatinfluencepurchasing

decisionsfor19productcategories,pricewasoneofthetoptwo

attributesinfluencingproductselectionamongglobalrespondents

(alongwithtasteforediblecategoriesandbrandnamefornon-

edibles).Andconsumersarelookingforgooddealsregardlessoftheir

economiccircumstances.Indeed,formanyconsumers,dealseeking

isthethrillofthechase.Globally,59%ofrespondentssaytheyenjoy

takingthetimetofindbargains,andagreementisevenhigherinNorth

America(68%)andLatinAmerica(64%).

But,assmartretailershavelongknown,priceandvaluearen’tthe

samething.Whenitcomestostoreselection,price-relatedattributes

fallbelowseveralothers.High-qualityproduce(57%),convenient

location(56%)andproductavailability(54%)areratedashighly

influentialindeterminingwheretoshop.Fewersaygoodvalue

formoney(52%),thelowestpricesoverall(48%),greatsalesor

promotions(47%),andgoodsalesorcouponsintheweeklycircular

(37%)arehighlyinfluential.Price-relatedattributesaremoreinfluential

inLatinAmericaandNorthAmericathantheglobalaverages.

“Whileintensepromotionalactivityamongretailersandmanufacturers

hascreatedanexpectationamongconsumersthatlowpricesshould

bethenorm,someconsumersarerecalibratingtheirspending—

andincreasingly,valueisaboutmorethanthelowestprice,”said

Matthesen.“Consumersareoftenwillingtopaymoreiftheythinkthe

benefitsoutweightheprice.Oneofthemosteffectivewaysretailers

canavoidpricingwarsandunsustainablepromotionstrategiesis

toincreasetheperceivedbenefitstheyprovide.Tokeepshoppers

comingback,however,brandsmustexceedshoppers’expectationsand

convincinglydemonstratethatthehigherpriceistrulyjustified.”

PrICe IS Not the MoSt IMPortANt Store-SeleCtIoN FACtor

global average: percentage who say attribute is highly

influential in their decision to shop at a particular retailer

1. high-quality fresh 57% produce

2. convenient location 56%

3. products wanted are 54% regularly in stock

4. good value for money 52%

5. carries the food and 50% non-food items that i need

6. lowest prices overall 48%

7. great sales and promotions 47%

8. organized layout 45%

9. easy to get in and get out 43% quickly

10. personnel are friendly & 42% knowledgeable

11. high-quality meat 42% department

12. short checkout lines/fast 41% checkout

13. variety of freshly prepared 40% foods

14. only store that carries 38% what i want

15. good sale/coupon items 37% in store ad/circular

16. customer loyalty card 32% program

Source:NielsenGlobalRetail-GrowthStrategiesSurvey,Q32015

assortment price/valueconvenience

8 Think Smaller for Big growTh

Indeed,inSoutheastAsia,aNielsenretailsalesanalysisof16categories

insixmarketsshowsdollarsalesinthepremiumsegmentgrewat

twicetherate(21%)ofthevalueandmainstreamtiers(10%and8%,

respectively)betweenOctober2012and2014.Chinashowsasimilar

trend,withevengreatergrowth(23%)inthepremiumtier.Andinmany

places,theretailersthatarewinningarepositionedatoppositeends

ofthepricespectrum.Whilemanyconsumersremainpriceconscious,

drivinggrowthinvaluechannels,someconsumersaretradingup

forwhattheyperceivetobeadditionalvalueandquality.IntheU.S.,

aNielsenanalysisofsupermarketvaluesalesrevealsthattwoniche

retailersappealingtoverydifferentcustomerbases—discountersand

natural/gourmetsupermarketchains—areexpandingstorecountsand

grabbingsharefrommainstreamsupermarkets.Between2015and

2020,growthintheseoutlets(projectedat2.6%and6.8%annually,

respectively)isexpectedtooutpacethatofmainstreamsupermarkets

(projectedat1.4%annually).Together,thesetrendshaveputpressure

onbig-boxretailers.

9Copyright © 2016 The Nielsen Company

49%

49%56

% 59%

56%

44% 48

%

45%

59%

54%

45% 48

%

47%

58%

55%

36%

36%

32%

45%

46%

33% 35%

28%

30% 34

%

PrICe-relAted AttrIbuteS Are MoSt IMPortANt IN lAtIN AMerICA ANd North AMerICA

PerCeNtAGe Who SAy AttrIbute IS hIGhly INFlueNtIAl IN theIr deCISIoN to ShoP At A PArtICulAr retAIler

asia-Pacific euroPe africa/middLe east Latin america north america

Source:NielsenGlobalRetail-GrowthStrategiesSurvey,Q32015

there were Good saLe/couPon items in Last week’s store ad/circuLar

the store has Great saLes and Promotions

the store has a customer LoyaLty card ProGram

i discover Good vaLue for my money when shoPPinG there

the store has the Lowest Prices overaLL

10 Think Smaller for Big growTh

AS PrICeS Go uP, MANy Cut doWN

global average: percentage who say they wouldn’t buy the

category if prices rose 10%

Break The promoTion addicTion Retailersandmanufacturershaveasharedrelianceonpromotions,butdecent

returnsontradepromotionspendareincreasinglyhardtogenerate.Infact,

thespiralingcostoftradepromotionshasyieldedadiminishingreturnon

investmentformanycategories.Knowingwhichcategoriesaremoreorless

sensitivetopricingchangesisessentialforbreakingthepromotionaddiction

anddrivinggrowth.

Whilepricesensitivityvariesbycategory,it’shelpfultounderstandwhat

consumerssaytheywoulddoifpricesweretoincreaseby10%.Not

surprisingly,nondiscretionaryitems,suchasdairy,freshfoodsandpersonal-

careproductsarelesspricesensitivethandiscretionaryitems,suchas

conveniencefoods,snacksandalcoholicbeverages*.Forexample,only13%

ofglobalrespondentssaytheywouldstoppurchasingdairyproducts,15%

saytheywouldnotbuypersonal-careproducts,and16%saytheywouldnot

purchasemeatorpoultry*ifpricesincreasedby10%.Morethanone-third,

however,saidtheywouldstoppurchasingconveniencefoods(37%)orprepared

meals(36%)ifpricesincreasedby10%.Forthemostpart,however,consumers

aren’tcuttingoutcategoriesaltogether.Rather,they’resimplybuyingless.

Howconsumerssaytheywouldrespondtopriceincreases,however,varies

acrossregions.RespondentsinLatinAmerica,whoaredealingwithtough

economicconditionsinmanycountries,exhibitsentimentthatismostlikelyto

changetheirbuyingbehaviorinresponsetopricehikes–primarilyvotingtocut

backfornondiscretionarycategories,andcutoutdiscretionaryones.Ingeneral,

Europeanrespondentsappeartobemorepricesensitivethantheaverage,

withfewerrespondentsthanaveragesayingtheirpurchasingwouldremain

unchangedifpricesroseforthemajorityofcategories.Incontrast,sentiment

amongNorthAmericanrespondentsshowstheleastsensitivitytoprice

increases.WhilethelargestpercentageofNorthAmericanrespondentssaythey

wouldbuylessatthehigherpriceforthemajorityofcategories,theregionalso

hasthehighestpercentageofrespondentswhosaytheywouldcontinuetheir

regularbuyinghabitsformostcategories,evenifpricesweretoincreaseby10%.

“It’stimetoabandonthepresumptionthatthesamepromotionstrategies

workforallcategories,”saidMatthesen.“Promotionspendneedstobe

tiedtoperformance,adjustingabove-the-linespendbasedonhowwellthe

productorportfoliohasdeliveredonthemoneyinvested.Fewer,smaller,better

promotions,ratherthanmore,biggerones,willdeliverbetterreturns.Focusing

promotionsonthemostprofitableoutletsiscritical.”Source:NielsenGlobalRetail-GrowthStrategiesSurvey,Q32015

*Note:AlcoholandMeat&PoultrydoesnotincludeEgypt,Morocco,SaudiArabiaandUAE.AlcoholalsodoesnotincludeIsrael.

discretionary cateGoriesstaPLe cateGories

alcoholic beverages*

loose, unpackaged, unbranded cereals

meat and poultry*

crisps and other snack foods

fish and seafood

prepared meals

cosmetics and skin care

dairy

bottled water

fresh or frozen fruits and vegetables

convenience foods

sweets, biscuits and other sweet items

personal care

canned fruits and vegetables

packaged foods

carbonated beverages

otc medications

breakfast cereals

bread and bakery

41%

36%

31%

28%

23%

37%

34%

29%

27%

20%

18%

16%

16%

15%

13%

36%

33%

28%

25%

11Copyright © 2016 The Nielsen Company

MoSt ANd leASt PrICe SeNSItIve CAteGorIeS IN eACh reGIoN

Least Price sensitivePercentage that say they would continue current buying habits

most Price sensitivePercentage that say they would cut back or cut out consumption

Source:NielsenGlobalRetail-GrowthStrategiesSurvey,Q32015

Note:AlcoholandMeat&PoultrydoesnotincludeEgypt,Morocco,SaudiArabiaandUAE.AlcoholalsodoesnotincludeIsrael.

asi

a-P

ac

ific

dairy 43%fresh or frozen fruits and veGetaBLes 41%PersonaL care 40%meat and PouLtry 38%otc medications 36%fish and seafood 36%

aLcohoLic BeveraGes 77%crisPs and other snack foods 77%carBonated BeveraGes 75%convenience foods 74%sweets and Biscuits 73%

1

3

5

2

4

6

Lati

n a

mer

ica crisPs and other snack foods 89%

PrePared foods 88%sweets and Biscuits 88%carBonated BeveraGes 88%aLcohoLic BeveraGes 87%convenience foods 87%

PersonaL care 32%dairy 30%meat and PouLtry 30%fresh or frozen fruits and veGetaBLes 27%Bread and Bakery 26%

1

3

5

2

4

6

afr

ica

/mid

dLe

ea

st

aLcohoLic BeveraGes 84%PrePared foods 80%carBonated BeveraGes 78%crisPs and other snack foods 78%sweets and Biscuits 78%

dairy 42%meat and PouLtry 41%Bread and Bakery 41%fresh or frozen fruits and veGetaBLes 36%PersonaL care 36%

1

3

5

2

4

eur

oPe

convenience foods 87%PrePared foods 86%crisPs and other snack foods 85%aLcohoLic BeveraGes 83%sweets and Biscuits 83%

dairy 45%Bread and Bakery 45%PersonaL care 39%meat and PouLtry 38% PackaGed foods 35%

1

3

5

2

4

no

rth

am

eric

a PrePared foods 73%aLcohoLic BeveraGes 73%sweets and Biscuits 72%Loose, unPackaGed, unBranded cereaLs 72%convenience foods 71%crisPs and other snack foods 71%

dairy 50%PersonaL care 47%fresh or frozen fruits and veGetaBLes 46%meat and PouLtry 43%otc medications 42%

1

3

5

2

4

6

12 Think Smaller for Big growTh

in Tough TimeS, more iS BeTTer Than leSS Priceincreasesareagrowingrealityforconsumers.Butthereare

waystodrivesalesandhelpconsumerscopewhenpricesarerising

butwagesarenot.Howcanmanufacturershelpkeepshoppers

comingbackwhentimesaretough?

Weaskedrespondentstorankdifferentpricingstrategies

manufacturerscoulduseifmaterialscostsforfoodorpersonalcare

rosesubstantially.

Themostpreferredstrategiesineveryregionwereformanufacturers

toofferlargereconomysizeswithlowerpriceperuseorserving

(citedby26%ofglobalrespondents),followedbyintroducingnew,

smallerpacksizesatlowerprices(19%).Reducingexistingpackage

sizes(alsocalleddownsizing)wasthepreferencefor15%ofglobal

respondents.Salesandpromotionalstrategieswerelessimportant.

Andit’sclearthatconsumersdonotwanttocompromiseonquality.

Only8%ofglobalrespondentssaytheywouldsacrificequalitytokeep

thesameprice.

MoNey-CruNChed CoNSuMerS PreFer to Go bIGglobal average: percentage who ranked action as their most preferred savings strategy if prices rose substantially

Source:NielsenGlobalRetail-GrowthStrategiesSurvey,Q32015

Note:Percentagedoesnotequal100%duetorounding

offer larger economy sizes with lower price per usage or serving

introduce new, smaller pack sizes at lower prices

modestly reduce packaging size of products, but keep price the same

raise prices of existing items proportionately

offer fewer sales

offer same number of sales, but at less of a savings

produce slightly lower quality products, but keep price the same

26%

19%

15%

11%

11%

11%

8%

13Copyright © 2016 The Nielsen Company

healThful opTionS are noT Simply “nice To have” Itcomesasnosurprisethathealthandwellnessisatoppriorityfor

consumersaroundtheworld,giventhatthishasregisteredasimportant

forsomeyearsnow.Two-thirdsofglobalrespondents(67%)saythey

activelyseekproductswithhealthfulingredients,62%saytheyread

nutritionallabelscarefully,and45%believetherearenotenoughhealthful

optionsavailabletobuy.Butareretailersandmanufacturersresponding

totheseneeds?

heAlthFul oPtIoNS Are GAMe ChANGerS

stronGLy/somewhat aGree neutraL stronGLy/somewhat disaGree

Source:NielsenGlobalRetail-GrowthStrategiesSurvey,Q32015Note:Percentagesmaynotequal100%duetorounding

asia-Pacific

euroPe

africa/middLe east

Latin america

north america

i read nutritionaL

LaBeLs carefuLLy

asia-Pacific

euroPe

africa/middLe east

Latin america

north america

i activeLy seek Products with

heaLthfuL inGredients

asia-Pacific

euroPe

africa/middLe east

Latin america

north america

65%54%

61%62%

61%

26%27%

23%23%

22%

9%20%16%16%

17%

71%55%

70%70%

65%

23%30%

22%22%

23%

6%15%

8%8%

11%

47%43%

50%47%

42%

37%35%

32%33%

32%

15%22%

18%20%

26%

there are not enouGh heaLthfuL oPtions avaiLaBLe

to Buy

14 Think Smaller for Big growTh

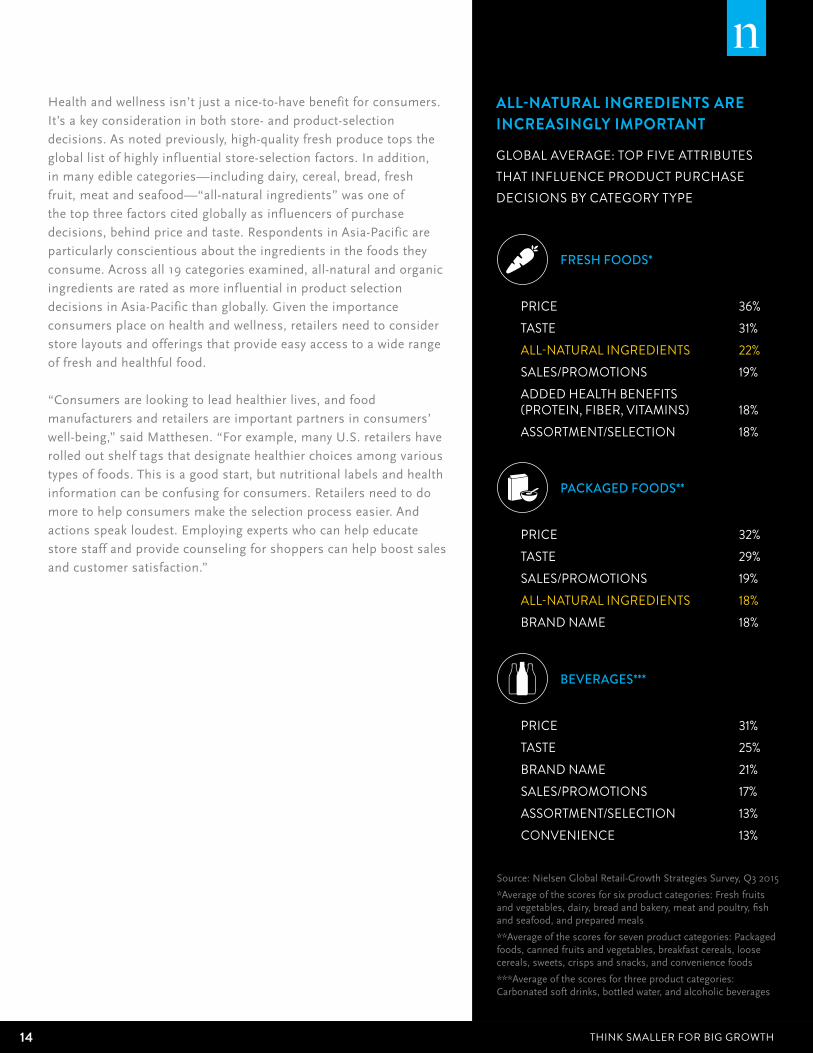

Healthandwellnessisn’tjustanice-to-havebenefitforconsumers.

It’sakeyconsiderationinbothstore-andproduct-selection

decisions.Asnotedpreviously,high-qualityfreshproducetopsthe

globallistofhighlyinfluentialstore-selectionfactors.Inaddition,

inmanyediblecategories—includingdairy,cereal,bread,fresh

fruit,meatandseafood—“all-naturalingredients”wasoneof

thetopthreefactorscitedgloballyasinfluencersofpurchase

decisions,behindpriceandtaste.RespondentsinAsia-Pacificare

particularlyconscientiousabouttheingredientsinthefoodsthey

consume.Acrossall19categoriesexamined,all-naturalandorganic

ingredientsareratedasmoreinfluentialinproductselection

decisionsinAsia-Pacificthanglobally.Giventheimportance

consumersplaceonhealthandwellness,retailersneedtoconsider

storelayoutsandofferingsthatprovideeasyaccesstoawiderange

offreshandhealthfulfood.

“Consumersarelookingtoleadhealthierlives,andfood

manufacturersandretailersareimportantpartnersinconsumers’

well-being,”saidMatthesen.“Forexample,manyU.S.retailershave

rolledoutshelftagsthatdesignatehealthierchoicesamongvarious

typesoffoods.Thisisagoodstart,butnutritionallabelsandhealth

informationcanbeconfusingforconsumers.Retailersneedtodo

moretohelpconsumersmaketheselectionprocesseasier.And

actionsspeakloudest.Employingexpertswhocanhelpeducate

storestaffandprovidecounselingforshopperscanhelpboostsales

andcustomersatisfaction.”

All-NAturAl INGredIeNtS Are INCreASINGly IMPortANt

global average: top five attributes that influence product purchase decisions by category type

fresh foods*

PackaGed foods**

BeveraGes***

price 36%taste 31%all-natural ingredients 22%sales/promotions 19%added health benefits (protein, fiber, vitamins) 18%assortment/selection 18%

price 32%taste 29%sales/promotions 19%all-natural ingredients 18%brand name 18%

price 31%taste 25%brand name 21%sales/promotions 17%assortment/selection 13%convenience 13%

Source:NielsenGlobalRetail-GrowthStrategiesSurvey,Q32015

*Averageofthescoresforsixproductcategories:Freshfruitsandvegetables,dairy,breadandbakery,meatandpoultry,fishandseafood,andpreparedmeals

**Averageofthescoresforsevenproductcategories:Packagedfoods,cannedfruitsandvegetables,breakfastcereals,loosecereals,sweets,crispsandsnacks,andconveniencefoods

***Averageofthescoresforthreeproductcategories:Carbonatedsoftdrinks,bottledwater,andalcoholicbeverages

15Copyright © 2016 The Nielsen Company

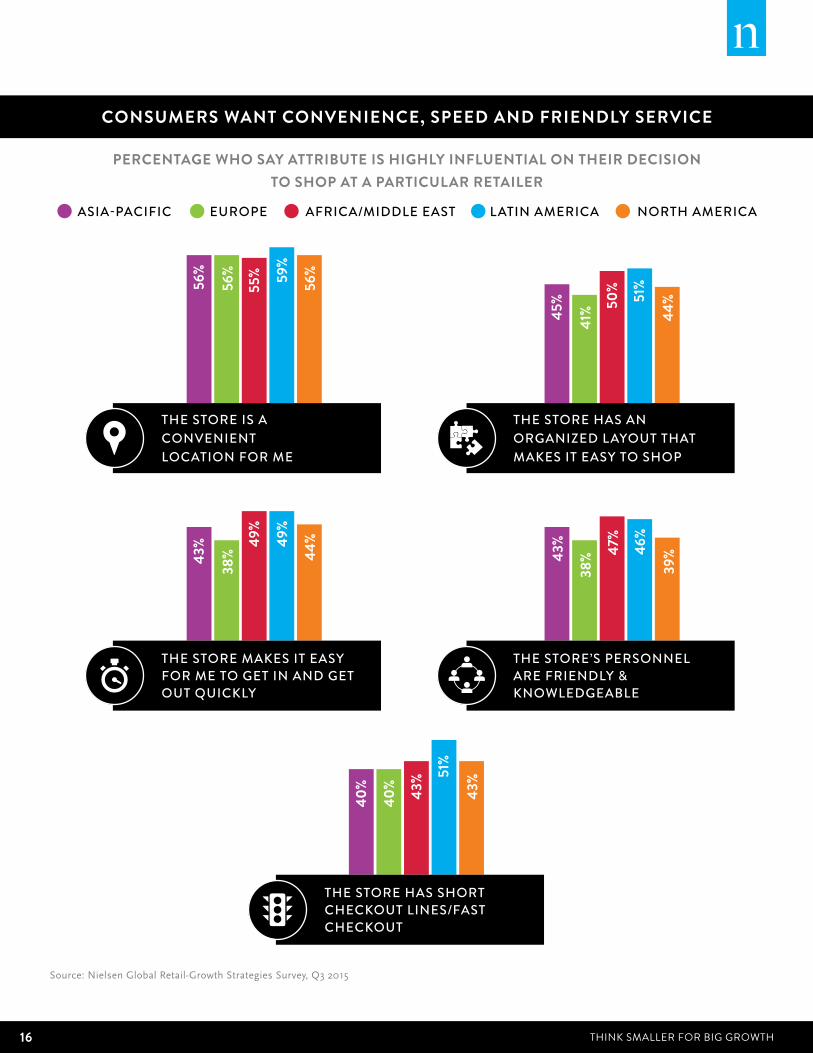

caTer To convenience Withlifemovingathyperspeed,consumerscraveconveniencefor

everythingfromchoosingthestorestheyshopintobuyingthefoods

theyeat.Fifty-sixpercentofglobalrespondentssayaconvenient

locationishighlyinfluentialintheirdecisiontoshopataparticular

retailer.Forty-fivepercentofglobalrespondentssaytheirstoreselection

decisionishighlyinfluencedbyanorganizedlayoutthatmakesiteasy

toshop;slightlyfeweridentifytheabilitytogetinandoutquickly(43%)

orfastcheckout(41%)ashighlyinfluential.Theseattributesaremore

influentialinLatinAmericaandAfrica/MiddleEastthanglobally.

Thisconveniencemind-sethasclearimplicationsforconsumers’eating

habits—andforgroceryretailers.On-the-goconsumersareeatingfewer

mealsathomeandinsteadlookingforconvenientmealsolutionsthatfit

intotheirdailyroutines.TheU.S.marketisaprimeexampleofhowthe

conveniencetrendistransformingwhatandwherefoodispurchased.

AccordingtodatafromtheU.S.CommerceDepartment,spendingat

restaurantsandbarseclipsedthatatgrocerystoresforthefirsttime

everinMarch2015.AnddatafromNielsenPerishablesGroupinthe

U.S.suggeststhat,eveningrocerystores,shoppersareincreasingly

choosingmealsandmealcomponentsoveringredients.Deli-prepared

foods,suchassoups,sushiandpizza,aredoingparticularlywell,with

valuesalesrising7%overthe52weeksendingFebruary2016.Having

avarietyoffreshlypreparedfoodsisahighlyinfluentialstore-selection

factorfor40%ofglobalrespondents,whileonly15%sayithasno

influenceonwheretheyshop.

“Affordable,qualitymealoptionsandin-storediningexperiencescan

beanimportantdifferentiatorforwhereconsumersdecidetoshop,”

saidMatthesen.“Competitioninthisspaceisextremelytough,however,

asretailersmustcontendwithnotonlytheirfellowgrocersand

restaurants,butnewentrantssuchasmealdeliveryservicesthatsend

mealingredients,inpremeasuredproportions,straighttoconsumers’

doorsteps.Tostandapart,retailersmustidentifyandfocusonunmet

needsorunderservedconsumersegments,suchasthepremium

segment,health-consciousshoppers,orseniorsandsmallhouseholds.

Andtheyshouldhighlightthesebenefitsintheirmarketingefforts—for

example,within-storetastingsandendcapdisplaysorbyhighlighting

themealoftheweekinweeklycirculars.”

16 Think Smaller for Big growTh

56%

55%

56% 59

%

56%

45% 50

%

41%

51%

44%

43% 49

%

38%

49%

44%

43% 47%

38% 46

%

39%

40% 43%

40%

51%

43%

CoNSuMerS WANt CoNveNIeNCe, SPeed ANd FrIeNdly ServICe

PerCeNtAGe Who SAy AttrIbute IS hIGhly INFlueNtIAl oN theIr deCISIoN to ShoP At A PArtICulAr retAIler

asia-Pacific euroPe africa/middLe east Latin america north america

Source:NielsenGlobalRetail-GrowthStrategiesSurvey,Q32015

the store is a convenient Location for me

the store has an orGanized Layout that makes it easy to shoP

the store makes it easy for me to Get in and Get out quickLy

the store’s PersonneL are friendLy & knowLedGeaBLe

the store has short checkout Lines/fast checkout

17Copyright © 2016 The Nielsen Company

Supply meeTS Specific demand Theconceptofsupplyanddemandissimpletounderstandyetcan

bedifficulttoachieve—especiallywhenconsumerchoiceisseemingly

limitlessanddemandforspecificproductsisgreaterthaneveratthe

sametime.Butassortmentisoneofthetopthreeinfluentialreasons

whyconsumerspickaparticularstoretoshop.Infact,morethanhalf

ofglobalrespondents(54%)saytheirstore-selectiondecisionishighly

influencedbywhetherthestorehastheproductstheywantregularly

instock,andslightlyfewer(50%)saytheyshopataparticularretailer

becausethestorecarriesthefoodandnonfooditemstheywant.Both

oftheseattributesareratedasmoreinfluentialinNorthAmericathan

globally.Inaddition,nearlyfourin10globalrespondents(38%)saythey

shopataparticularretailerbecauseitistheonlystorethatcarrieswhat

theywant.Onceagain,thisismoreinfluentialinNorthAmerica(44%)

thanglobally.

Carryingtherightselectionofproducts,however,isacarefulbalancing

act,asconsumersarelookingformorethanjusttheirfavoritego-to

products.Fifty-onepercentofglobalrespondentssaytheyoftentrynew

brandsbecausetheylikevarietyandgetboredwiththesameoldthings.

ThissentimentisparticularlystronginLatinAmerica(56%),while

Europetrailstheglobalaverage(42%).Butsometimesmoreissimply

toomuch.Forexample,respondentsinAfrica/MiddleEastandAsia-

Pacificaremorelikelytobelievetherearetoomanychoicesonstore

shelves(60%and58%,respectively)thanthoseinEurope(44%)and

NorthAmerica(41%).

“Doneright,assortmentcanhelpdrivegrowth,butasconsumers

demandhyper-localization,retailersneedtorethinkexistingstrategies,”

saidMatthesen.“Assortmentdecisionsneedtobeguidedmorebythe

shoppingmissionandconsumerdemand.Thatis,retailersmustshift

fromapushtoapullapproachbymakingiteasierforconsumerswith

differentmissionstofulfilltheirtrippurpose.It’shardtobeeverything

toeveryone,butyoucanenhance‘shopability’bymovingessentialsto

thefrontofthestoretobetterservequick-trip,grab-and-goshoppers.”

Retailerscanreduceseeminglyinfinitechoicesbycarefullycurating

selectionsbasedonconsumers’interestsandpreviouspurchasing

behaviors.Thispracticeisrelativelycommononline(thoughthereis

certainlyroomforimprovement),butretailersneedtodoabetterjob

ofleveragingdigitaltoolssuchasbeaconsorinteractivescreensto

guideconsumerstorelevantcategoriesorproductsandelicitdesired

shoppingbehaviorsinstore.

18 Think Smaller for Big growTh

54%

54%58% 66

%

58%

51%

51%56

% 59%

62%

47% 52

%54%

45%

57%

39% 43

%

41%

51%

49%

43%

42%

36% 41

%

38%

39%

39%

33%

34% 44

%

ProduCt AvAIlAbIlIty IS PArtICulArly IMPortANt IN North AMerICA

PerCeNtAGe Who SAy AttrIbute IS hIGhly INFlueNtIAl oN theIr deCISIoN to ShoP At A PArtICulAr retAIler

asia-Pacific euroPe africa/middLe east Latin america north america

Source:NielsenGlobalRetail-GrowthStrategiesSurvey,Q32015

the store has hiGh quaLity fresh Produce

the store has the Products i want and they are reGuLarLy in stock

the store carries the food and non-food items that i need

the store has a hiGh quaLity meat dePartment

the store has a variety of freshLy PrePared foods

it’s the onLy store that carries what i want

19Copyright © 2016 The Nielsen Company

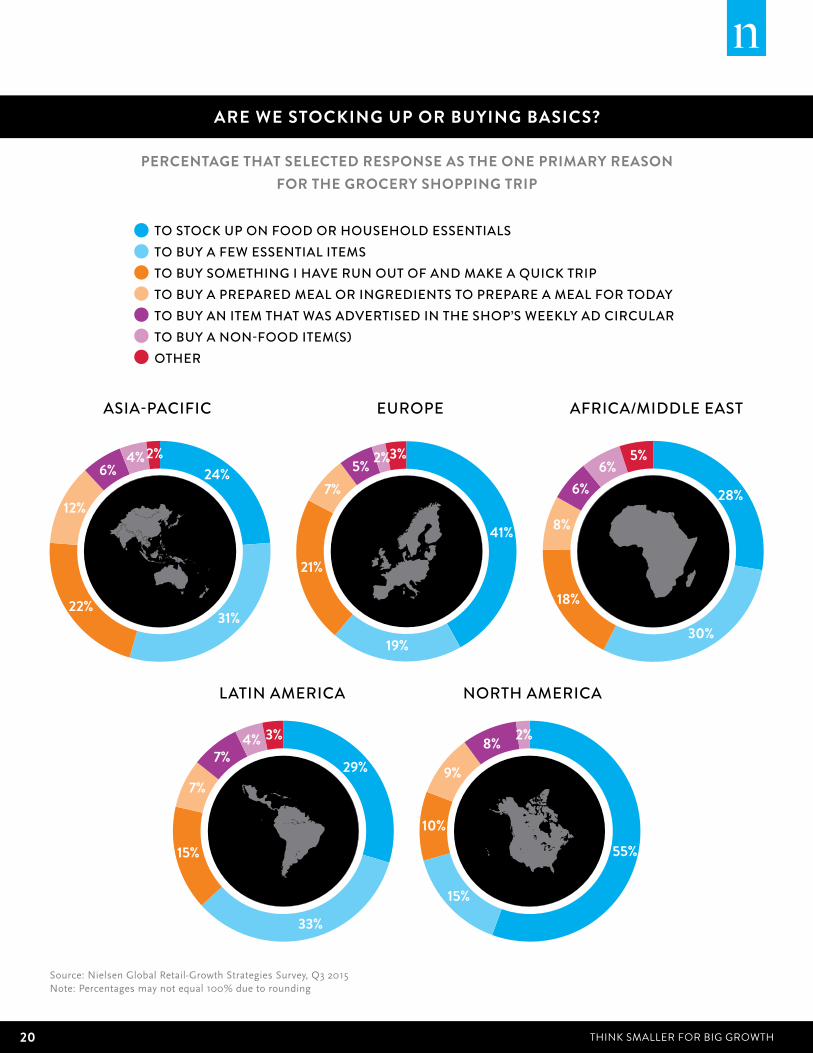

proximiTy reTailing: Buying Big or BaSicTrippurposelargelydependsonwhereyoulive.Ifyouliveina

developedmarketinNorthAmericaandEurope,stock-uptripsarethe

primaryreasonforshopping—byawidemargin.Fifty-fivepercentof

NorthAmericanrespondentssaythey’reshoppingprimarilytostock

uponfoodandhouseholdessentials,40percentagepointsabovethe

next-closestoption(buyingafewessentials).InEurope,thegapis20

percentagepoints(41%arestockingup,while21%aremakingaquick

triptofillanimmediateneed).

InthelargelydevelopingmarketsofLatinAmerica,Asia-Pacificand

Africa/MiddleEast,thereasonsforshoppingaremixed.Inallthree

regions,thelargestpercentagesaythey’reshoppingforafewessential

items(33%,31%and30%,respectively),butnearlyasmany(29%,24%

and28%,respectively)saythey’restockingup.

Thesedifferencesaredriveninpartbydifferencesinhouseholdstorage

space,transportationaccessandincome.EuropeandNorthAmerica

havesomeofthehighestaveragehouseholdincomesintheworld,and

manyconsumersintheseregionscanaffordtostockuponhousehold

essentials,cantransportthepurchaseswitheaseandhaveample

capacityforstorage,whileconsumersindevelopingmarketstypically

shopfortheday,buyingtheproductsthatareabsolutelyessential.

“Theidealformatdependsontheshoppers’missionandtheir

preferences,andretailerflexibilityiscritical,”saidMatthesen.“Store

formatsaren’tshoppedthesameway;thereissignificantvariationeven

withinsimilarlysizedformats.Therefore,retailersmustunderstand

whichattributesareconsideredessentialforeachformatandexcelin

deliveringonthosethatdriveequity.Oncethey’vemasteredthebasics,

theycanstrivefordifferentiation.Andasconsumers’needschange,

retailersmustreevaluateandreinventtostayrelevant.”

20 Think Smaller for Big growTh

Are We StoCkING uP or buyING bASICS?

PerCeNtAGe thAt SeleCted reSPoNSe AS the oNe PrIMAry reASoN For the GroCery ShoPPING trIP

to stock uP on food or househoLd essentiaLsto Buy a few essentiaL itemsto Buy somethinG i have run out of and make a quick triPto Buy a PrePared meaL or inGredients to PrePare a meaL for todayto Buy an item that was advertised in the shoP’s weekLy ad circuLarto Buy a non-food item(s)other

Source:NielsenGlobalRetail-GrowthStrategiesSurvey,Q32015Note:Percentagesmaynotequal100%duetorounding

24%

31%22%

12%

6%4%2%

29%

33%

15%

7%

7%4% 3%

55%

15%

10%

9%

8% 2%

41%

19%

21%

7%5% 2%3%

28%

30%

18%

8%

6%6%

5%

asia-Pacific

Latin america

euroPe

north america

africa/middLe east

21Copyright © 2016 The Nielsen Company

find pockeTS of unSaTiSfied demandConsumersareneversatisfiedwiththestatusquo,asthegrowth

ofnicheretailingoptionsandpremiumproductofferingsclearly

demonstrates.Thewaytostayrelevantandconnectedtoever-changing

consumerdemandistocontinuallylisten,learnandadapttoprovide

theproductsandservicesthatwillkeepconsumerssatisfiedandcoming

backtimeaftertime.Notallin-storeservicesareequallyvalued,so

understandingwheretherearepocketsofunsatisfieddemandcanhelp

buildtheservicesthatconsumerswant.

Whichonesaremostpopularwithconsumers?

Globally,thein-storeservicesmostwidelyavailableandusedare

convenientoptionsthatcatertoon-the-golifestyles.Roughlyfourin

10globalrespondentssaytheyusein-storebanking(42%),fastfood

(40%),preparedfood(40%)orpharmacy(39%)services.Inaddition,

36%saytheyusein-storecoffeeservices.Andaboutone-fifthof

consumerswouldusetheseservicesiftheywereavailable.

Otherservicesthatarelesswidelyavailableandused—suchascooking

classes(17%),healthclinics(27%),beautycare(27%)andpostal

services(29%)—havestrongpotential.Aboutoneinfourrespondents

saytheywouldusetheseservicesiftheywereavailable.

“Offeringmultiplefunctionsunderoneroofissmartastheadditionof

newin-storeservicesmayhelpdrawconsumersin,prolongtheirtime

spentinstoreandencouragerepeatvisits,”saidMatthesen.“Andthey

mayhelpretailersmaximizereturnsontheirreal-estateinvestmentsas

theywilllikelyhaveexcesssquarefeet.Insomecases,however,itmay

bebetterforretailerstopartnerwithanexperttoprovidetheseservices

ratherthantrytodoitthemselves.”

22 Think Smaller for Big growTh

Whiletheretaillandscapehasexperiencedenormouschangeinjusta

decade,we’relikelyjustgettingstarted.Inmostmarkets,connected

commercehashadasmallimpactonfast-movingconsumergoods(FMCG)

salestodate,buttheimplicationsarealreadyhuge.Whileconnected

commerceisnotthesubjectofthisreport,itistooimportanttoleaveout

entirely.

Theinternethasgivenshoppersaccesstothelargeststoreintheworld,and

technologyandbigdataarecreatingopportunitiestoprovidemorerelevant,

personalizedproductrecommendations—inrealtime—basedoninsights

aboutconsumerpreferences,behaviorsandlocation.Thedigitalrevolution

isevencreatingnewformsofcommerce.Theon-demandeconomyallows

consumerstoorderjustaboutanythingwiththeirmobiledevices.Some

manufacturersandretailershaverolledoutmass-customizationoptionsthat

allowconsumerstocreatetheirownuniqueproductsandexperiencesfor

shoesandsuits,bicyclesandcandy.Andsubscriptionservices—forproducts

asvariedasrazors,cosmeticsandmealkits—deliverproductsrightto

consumers’doorsatspecifiedtimes.

Connectedcommerce,however,shouldnotbeviewedasanextensionofthe

brick-and-mortarstore.Rather,it’sanewmodelwithdifferentcostdrivers

andadifferentvaluepropositionfortheshopper.Assuch,itrequiresa

reimaginingofright-time,right-placeandright-productstrategies.Shoppers

areincorporatingdigitaltouchpointsalongtheentirepathtopurchase,

fromreviewingproductsonlineathometousingsmartphonesaspersonal

shoppingassistantsinthestore.Thisisalreadyhavingimplicationsfor

physicalstores,asshoppers’expectationlevelshavefundamentallychanged,

andthisrateofchangewillonlyincrease.Thereisnodoubt:Thefutureof

retailisconnected,butmostimportantistheabilitytoleveragetheright

blendofonlineandofflinestrategiestofillunsatisfiedpocketsofdemand.

Nielsen’srecentConnected Commerce Reportdetailsstrategiesforsuccess.

The on-demand economy

uLtimateLy, success isn’t Just aBout technoLoGy or a ParticuLar store format; success is aBout knowinG what consumers want, need and exPect—even Before they know it,” said matthesen. “it’s not easy, But it’s achievaBLe. it requires a sharP focus on consumers’ exPectations as they evoLve, and a nimBLe and fLexiBLe aPProach that keePs Pace.

23Copyright © 2016 The Nielsen Company

navigaTing The new reTail landScapeTheonlyconstantintheretailenvironmentischange.Asretailers

considerwheretogofromhere,thereareafewtruthstokeepinmind.

• Differentiationandafocusontheconsumerwilldrivegrowth.Theretaillandscapeisincrediblycrowded,andtechnologyhasgiven

consumersaccesstomoreinformationandgreaterpoweroverthe

shoppingexperiencethaneverbefore.Retailersmustgiveshoppers

areasontochoosethemovertheircompetitors,anditcan’tjust

beaboutprice.Todifferentiate,retailersmustevolveandchange

withtheneedstatesoftheircustomers—whetherit’sadigitaltool

thatmakesshoppingeasierormoreconvenientorastaffwithdeep

expertisethatcanhelpconsumersselectthebestproductfortheir

lifestyleandpreferences.Andthisprocessmustbeongoing,with

retailerscontinuouslymonitoringandadjustingtoevolvingneeds.

• Thinkingsmallcanyieldbigrewards.Consumersaredictatinghow,

whenandwheretheyshop.Andthey’reincreasinglylookingfor

controlnotjustovertheshoppingexperience,butoverthefeatures

oftheproductsandservices,too.We’vealreadyseensomebrands

experimentwithmasspersonalizationforshoes,computersand

otherproducts.Inthefuture,wemayseeconsumersmoredirectly

involvedintheproductdevelopmentandinnovationprocessas

somebrandsrelyoncrowdsourcingandcocreationtoaddvalue,

differentiatethemselvesandengenderloyalty.Greaterlocalization

isalsolikelyintermsofhowretailerscommunicatewithandmarket

toconsumers.Retailerscannowleveragevastamountsofdata

totailorrecommendationsandprovidemorerelevantadvertising

andoffers—deliveredinrealtime—basedonconsumers’past

purchasingbehavior,theirpreferencesandtheshoppingoccasion.

24 Think Smaller for Big growTh

• Theroleofthephysicalstorewillchange.Storesaren’tgoingtodisappearanytimesoon,buttheywillundergoadramatic

transformationase-commercegrowsandshopperexpectations

change.Retailersneedtoconsiderwhatrolephysicalstoreswill

playintheiromnichannelstrategyandhowtheycanusethem

tostrengthentheirofferingsanddelivervalueeachtrip.Someof

thekeyquestionsbrick-and-mortarretailersneedtocontemplate

includethefollowing:

• Howwillweoperateinahyperlocalizedworld?

• Howdowecreateameaningfulconnectionwithourshoppers?

Whatservicesorexperiencescanweprovidetodifferentiate

ourselvesandmakeconsumerswantourbrandversusjust

fulfillinganeed?

• AmImaximizingreturnonmyreal-estateinvestment,ordoI

needtoreassess(andpossiblyreduce)myfootprint?

• Willourchildrenorgrandchildrenfinditcustomarytowaitin

linetopay?

• Howdoesthelevelofserviceprovidedinstorecomparewith

thelevelsprovidedonline?

• Howcanwematchtheabundanceofchoiceavailableonline

withouttheburdenofinventories?

• Shouldstoresbecomepickuppointsforalle-commerce

deliveries?

• Howwillweoperatewithcompletepricetransparency,given

consumers’increasedaccesstoinformation?

• Analyticscanenablegrowth.Bigdatahasenormousimplications

formarketers,butitspotentialgoesbeyondprovidingrelevantads

andoffers.Ithasthepowertohelpretailerssolvetheirbiggest

businessproblemsandidentifypromisingopportunities.Winning

retailersleverageadvancedanalyticsandinvestsignificanthuman

andfinancialcapitalinthesecapabilities,usingdatatooptimize

assortment,inventoryandsupplychainsandtomakepricing

decisionsthatreducecostsandmaximizeprofitsinrealtime.

25Copyright © 2016 The Nielsen Company

market internet penetration

Australia 93%

China 50%

HongKong 81%

India 30%

Indonesia 31%

Japan 91%

Malaysia 68%

NewZealand 94%

Philippines 43%

Singapore 82%

South Korea 92%

Taiwan 84%

Thailand 56%

Vietnam 50%

countries in the global survey

ASIA-PACIFIC

market internet penetration

Egypt 55%

Morocco 61%

Pakistan 15%

SaudiArabia 66%

SouthAfrica 49%

UnitedArabEmirates

93%

AFrICA/MIddle eASt

Source:MiniwattsMarketing,Internet World Stats,Nov.30,2015,www.internetworldstats.com

market internet penetration

Canada 95%

UnitedStates 87%

North AMerICA

euroPe

market internet penetration

Austria 83%

Belgium 85%

Bulgaria 57%

Croatia 75%

CzechRepublic 80%

Denmark 96%

Estonia 84%

Finland 94%

France 84%

Germany 88%

Greece 63%

Hungary 76%

Ireland 83%

Israel 75%

Italy 62%

Latvia 82%

Lithuania 82%

Netherlands 96%

Norway 96%

Poland 68%

Portugal 68%

Romania 56%

Russia 71%

Serbia 66%

Slovakia 83%

Slovenia 73%

Spain 77%

Sweden 95%

Switzerland 87%

Turkey 60%

UnitedKingdom 92%

Ukraine 43%

lAtIN AMerICA

market internet penetration

Argentina 80%

Brazil 58%

Chile 72%

Colombia 59%

Mexico 49%

Peru 53%

Venezuela 62%

26 Think Smaller for Big growTh

about the nielsen global survey TheNielsenGlobalRetail-GrowthStrategiesSurveywasconductedAug.

10–Sept.4,2015,andpolledmorethan30,000onlineconsumersin61

countriesthroughoutAsia-Pacific,Europe,LatinAmerica,theMiddle

East/AfricaandNorthAmerica.ThesampleincludesInternetuserswho

agreedtoparticipateinthissurveyandhasquotasbasedonageandsex

foreachcountry.ItisweightedtoberepresentativeofInternetconsumers

bycountry.Becausethesampleisbasedonthosewhoagreedto

participate,noestimatesoftheoreticalsamplingerrorcanbecalculated.

However,aprobabilitysampleofequivalentsizewouldhaveamargin

oferrorof±0.6%atthegloballevel.ThisNielsensurveyisbasedonly

onthebehaviorofrespondentswithonlineaccess.Internetpenetration

ratesvarybycountry.Nielsenusesaminimumreportingstandardof

60%Internetpenetrationoranonlinepopulationof10millionforsurvey

inclusion.

about nielsen NielsenHoldingsplc(NYSE:NLSN)isaglobalperformancemanagement

companythatprovidesacomprehensiveunderstandingofwhat

consumerswatchandbuy.Nielsen’sWatchsegmentprovidesmedia

andadvertisingclientswithTotalAudiencemeasurementservicesfor

alldevicesonwhichcontent—video,audioandtext—isconsumed.

TheBuysegmentoffersconsumerpackagedgoodsmanufacturers

andretailerstheindustry’sonlyglobalviewofretailperformance

measurement.ByintegratinginformationfromitsWatchandBuy

segmentsandotherdatasources,Nielsenalsoprovidesitsclientswith

analyticsthathelpimproveperformance.Nielsen,anS&P500company,

hasoperationsinover100countries,coveringmorethan90%ofthe

world’spopulation.

Formoreinformation,visitwww.nielsen.com.

Copyright©2016TheNielsenCompany.Allrightsreserved.Nielsenand

theNielsenlogoaretrademarksorregisteredtrademarksofCZT/ACN

Trademarks,L.L.C.Otherproductandservicenamesaretrademarksor

registeredtrademarksoftheirrespectivecompanies.16/10048

27Copyright © 2016 The Nielsen Company