thefewleadingthemany ...econ.au.dk/.../research/seminars/2013/paper_jmartin.pdfthefewleadingthemany:...

TRANSCRIPT

The Few Leading The Many:Foreign Affiliates and Business Cycle Comovement∗

Jörn Kleinert1, Julien Martin2, and Farid Toubal3

1Department of Economics, University of Graz, Austria2IRES - Université catholique de Louvain, Belgium

3Ecole Nationale Supérieure de Cachan, Paris School of Economics and CEPII, France

December 2012

AbstractWe argue that the co-fluctuation of business cycles across countries is largely due

to linkages between multinational firms and their network of foreign affiliates. Wedocument that there are very few foreign affiliates in France, but that they contributeconsiderably to aggregate economic activities. Moreover, they share close ties withtheir country of origin. They could therefore drive the synchronization of internationalbusiness cycles. We exploit the heterogeneity in the intensity of activities and the ori-gin of foreign affiliates across French regions to identify their impact on comovement.We find that foreign affiliates increase business cycle comovement between their regionof location and their country of origin. We further show that the fragmentation of pro-duction within firm boundaries is an important mechanism explaining the internationaltransmission of shocks.

Keywords: Real Business Cycles, Multinational Firms, Intra-firm Trade.JEL classification: F23, F12, F4; F41

∗We wish to thank Paul Bergin, Matthew Cole, Jean Imbs, Lionel Fontagné, Philippe Martin, FlorianMayneris, Nicolas Schmitt and Linda Tesar. We also thank seminar participants at ETSG Leuven, Saint-Petersburg, Banque de France, Université catholique de Louvain, and Université Libre de Bruxelles. Thisresearch has received funding from the European Community Seventh Framework Programme (FP7/2007-2013) under grant agreement no 225551. Julien Martin is thankful for financial support to the FSR MarieCurie fellowship, and the ARC convention on "Geographical mobility of factors". Farid Toubal would like tothank the CEPR project "Globalization Investment and Services Trade" funded by the European Commissionunder FP7-PEOPLE-ITN-2008-21.

0

1 IntroductionAn extensive literature in international macroeconomics searches for the key forces drivingthe comovement of economic activities across countries. The empirical literature has listedmany potential candidates which include trade and financial integration, sector specializa-tion, or geography.1 Surprisingly, the role of multinational firms and their cross-bordernetwork of affiliates has received less attention.2 It is however a potential important factoras shocks are likely to propagate along the cross-country networks of multinational firms.Moreover, multinational firms and their foreign affiliates make up a large fraction of economicactivities such as employment, production and trade (Helpman, 2011). They might thereforehave meaningful economic effects and strengthen economic linkages between countries.

In this article, we analyze the effects of foreign affiliates on business cycle comovement,taking the other determinants pointed out by the literature into account. We use a uniquedatabase built from different sources of firm-level data. The firm-level data sets provideinformation on the balance sheet and the ownership of all firms located in France, andtheir bilateral (arm’s-length and intra-firm) trade with foreign partners. More specifically,it gives information on majority-owned affiliates that are controlled by foreign groups. Wedocument that foreign affiliates are deeply connected to their parent company. In the data,the median of the share of foreign ownership is 99% and more than 70% of the trade offoreign affiliates with their parent country is conducted intra-firm. Moreover, despite theirrelative low number, the foreign affiliates of multinational firms represent a substantial shareof economic activities in France and in French regions. In Alsace for instance, they accountfor 10% of the regional number of firms, half of total sales and value added, about a fifth ofemployment and about three quarters of international trade. These facts suggest that foreignaffiliates are large enough to affect aggregate economic outcomes and that there are strongeconomic linkages between foreign affiliates and their parents. Foreign affiliate networksmight therefore be partly responsible for the aggregate cofluctuation of economic activities.

Our data track the nationality of the ownership of firms located in France. We use thisinformation to document that the distribution of the activities of foreign affiliates based ontheir source country is uneven across regions.3 We exploit this heterogeneity to identify theeffect of foreign affiliates on business cycle synchronization. We aggregate the data at thelevel of the regions and for each nationality we construct the share of foreign affiliate employ-

1See di Giovanni and Levchenko (2010) for a discussion about the role of trade in the synchronization ofreal business cycles. A discussion about the role of financial integration is provided in Kalemli-Ozcan et al.(2009). See also Imbs (2004) for an investigation of the role of specialization and Clark and van Wincoop(2001) for an analysis of the role distance in business cycle comovements.

2One particularly interesting study is Burstein, Kurz and Tesar (2008), which provides evidence of the roleof trade in inputs within U.S. multinationals (used as a measure of production sharing) on the comovementof activities. In a theoretical paper, Zlate (2010) points to the transmission of economic shocks throughoffshoring. Bergin, Feenstra and Hanson (2009) show the impact of offshoring by US multinationals on thevolatility of employment in Mexico.

3Aggregating across regions by nationality, the share of value added generated by US foreign affiliatesin Haute Normandie is 5 times bigger than in Bretagne. The share of value added from Japanese foreignaffiliates in Nord Pas-de-Calais is 3,000 times bigger than in Midi-Pyrénées.

1

ment and their intensity in both arm’s-length and intra-firm trade. We match the data to alarge cross-section of bilateral pairs of correlations between the GDP growth rates of Frenchregions and 162 countries computed for the 1990 to 2006 period. We find a positive andsignificant impact of the presence of foreign affiliates on business cycle comovement betweenthe region of location of the affiliates and their parent country. This finding remains robustto the inclusion of the main driving forces of business comovement listed in the literature,as well as to the introduction of country- and region-level fixed effects. The fixed effectsaccount for the supply and demand shocks that may affect business cycle comovements. Themagnitude of the effect of the presence of foreign affiliates on business cycle comovements isalso economically meaningful. Based on our econometric results, a simulation exercise showsfor instance that the business cycle correlation between French regions and the US, one ofthe most important investors in France, is on average 10.1 percentage points lower withoutUS foreign affiliates.

We perform and report an extensive set of checks using different samples and usingalternative definitions of the foreign presence. Moreover, we control for other potential de-terminants such as distance and borders and also include the presence of foreign affiliatesfrom the same country in neighboring regions to account for spurious effects. These checkscorroborate our main findings which are that foreign affiliates substantially affect the corre-lation of real business cycles.

What type of international production network matters for the co-fluctuation of realbusiness cycles? From a theoretical viewpoint, the transmission of productivity or demandshocks is dependent on whether the affiliate is vertically integrated into its parent’s produc-tion network.4 In the case of vertical integration, any shocks will transmit to each stage ofthe international chain of production (Burstein et al., 2008; Tesar, 2008). Our second maincontribution is to investigate whether trade in inputs between firms which are part of ver-tically integrated production networks is an important determinant of synchronization. Werestrict our analysis to foreign affiliates involved in a vertical relationship with their parent.For this subsample of foreign affiliates, we still find an important effect of foreign affiliateson business cycle comovements. The findings suggest that shocks are partly propagatedby the fragmentation of operations by multinationals across countries. We investigate thisfurther by using precise information on trade by foreign affiliates with their home country.The data capture both the intra-firm and arm’s-length trade of foreign affiliates. We find astronger business cycle correlation when the trade of intermediate inputs takes place withinthe network of the multinational firm.

This article contributes to the literature on business cycle comovement in several respects.A few papers have focused on the role of foreign direct investment (FDI) on business cyclecorrelation (Jansen and Stokman, 2006; Hsu, Wu and Yau, 2011).5 Instead of measuring theactivities of foreign affiliates by using foreign direct investment, we use their real activities.In our data, the foreign affiliates are majority-owned while a firm will report a FDI flow

4See section 2 for a discussion of the theoretical mechanisms.5The evidence provided by Desai and Foley (2004) is also telling. They document the micro comovement

of the rates of returns and investments between U.S. multinational parents and their affiliates.

2

when it owns at least 10% of the equity capital of the foreign affiliate abroad. The investors’ability to control the affiliate with 10% is therefore unclear. A transmission of shocks is morelikely to occur if the parent exerts a strong control over its affiliate. Another limitation ofFDI data is that they are not only made up of equity, but also of debts from affiliated firmsthat inflate the value of the flows. This is particularly the case in France as shown by Terrien(2009). Measuring the real activities of foreign affiliates also circumvents this issue.

The cofluctuations of real business cycles and their determinants have been a topic ofintense research interest. Bilateral trade has been shown to be a key factor in the litera-ture. Beside the influent contribution of Frankel and Rose (1998), many papers have foundevidence that more bilateral trade between countries leads to more business cycle synchro-nization (Baxter and Kouparitsas, 2005; Kose and Yi, 2006; Calderon, Chong and Stein,2007; Inklaar, Jong-A-Pin and de Haan, 2008). In a refinement of the literature, a fewpapers have advocated the specificity of intra-industry trade (Imbs, 2004), trade in inter-mediate inputs or production sharing between countries (Burstein, Kurz and Tesar, 2008;di Giovanni and Levchenko, 2010; Ng, 2010). We include bilateral trade and intra-industrytrade in our regressions. We find that the effect of trade approximately has the same magni-tude as the effect of the share of foreign affiliate employment. Furthermore, the significanceof bilateral trade drops as we control for the activities of foreign affiliates, while the effect ofthe presence of foreign affiliates remains stable. This finding fits well with the evidence inthe trade literature that the lion’s share of international trade is done by a few large firmswhich are multinationals for the most part (Helpman, 2011).

Our empirical findings may be of importance for theory. In an important paper, Backuset al. (1992) show that bilateral trade is not sufficient to explain the cross-border comovementof activities in international real business cycle models. Subsequent works by Arkolakisand Ramanarayanan (2009) and Johnson (2012) reach the same conclusion from modelsintegrating input trade in the analysis. Our empirical findings suggest that the network ofmultinational firms is a simple explanation for the transmission of productivity shocks acrossborders. As long as foreign affiliates are also large enough, their contribution to aggregateco-fluctuations could be economically meaningful.

The paper is also related to a new strand of the literature pointing to the specific behaviorof large firms and their role in aggregate fluctuations. Gabaix (2011) has shown that U.S.aggregate fluctuations are greatly influenced by shocks to large firms. di Giovanni andLevchenko (2011) and di Giovanni, Levchenko and Méjean (2011) also provide systematicevidence of the key role of large firms in aggregate fluctuations. Parallel contributions pointto striking heterogeneity between large and small firms. They adjust labor differently alongthe cycle (Moscarini and Postel-Vinay, 2009), they have different pricing strategies (Goldbergand Hellerstein, 2009), and different innovation responses (Mansfield, 1962).6 We documentthat large firms differ also in terms of their ownership structure from smaller firms. Morespecifically, the share of foreign affiliates is substantially larger among large firms than among

6A few theoretical papers advocate that large firms actually behave differently from small firms (Shimo-mura and Thisse, 2009; Parenti, 2012). Neary (2009) suggests these superstar firms are (domestic or foreign)multinationals.

3

smaller ones. We then provide evidence that these few but large foreign affiliates give riseto (aggregate) business cycle co-fluctuations.

The remainder of this paper is structured as follows. Section 2 provides a discussionof the sources of influence of foreign affiliates on business cycle correlations. Section 3describes the construction of the bilateral database and presents the data. In section 4,we provide four sets of stylized facts that show (i) the importance of foreign affiliates inregional economic activities, (ii) the strength of vertical linkages between foreign affiliatesand their parent country, (iii) the spatial distribution of investors in French regions basedon their nationality, and (iv) the heterogeneity in the correlations between the GDP growthof French regions and the foreign countries. Section 5 describes the empirical methodologyand discusses the construction of the main empirical variables. In section 6, we present theeconometric results. Section 7 concludes.

2 Theoretical BackgroundWhat theoretical mechanisms link the presence of foreign affiliates in a country with businesscycle comovement between the country of location of the affiliate and its parent country?Let us start with an analogy with bilateral trade. From a theoretical point of view, moretrade does not necessarily lead to comovement. It depends on the nature of shocks and thepatterns of trade. For instance, productivity shocks should lead to a greater specializationof countries in a world of inter-industry trade, and thus less comovement. By contrast,in a world of intra-industry trade, the same shocks should have the opposite effects. Adeeper discussion can be found in di Giovanni and Levchenko (2010). Similarly to trade,the link between the presence of foreign affiliates and business cycle comovement dependson the pattern of linkages between the parent and its affiliates and the nature of the shocks.However, since we are now looking at firms, a third element of influence matters, namelythe size of the foreign affiliates. In order to understand the role of foreign affiliates in thesynchronization of business cycles, we need first to establish the conditions under whichthe shocks are transmitted from the parent to the affiliates. We will then explain howcomovement between parents and affiliates can lead to co-fluctuations of aggregate economicoutcomes.

Assume the two extreme cases of an international production network that is eithervertically or horizontally integrated. Trade in intermediate goods within the network of amultinational firm is characteristic of a vertically integrated network. This firm fragments itsproduction process across geographic space. In such cases, any demand shocks will transmitto each stage of the chain, inducing strong linkages between the activities of the parents andthe affiliates. A productivity shock or a technology shock may also be transmitted betweenthe parent and its affiliate.

Eventually, recent evidence provided by Ramondo, Rappoport and Ruhl (2011) showsvertical relationships between parents and affiliates without intra-firm flows. They suggestmultinational firms transfer intangible inputs through the production chain. Such transferscould also be the source of linkages between parents and affiliates. In the same vein, Atalay,

4

Hortacsu and Syverson (2012) provide evidence that, in the US economy, vertical linkagesbetween firms are not primarily concerned with goods trade. They show however that sucha structure allows firms to transfer intangible inputs.

If the network of firms is integrated horizontally, the foreign affiliates produce for thelocal market, and a local demand shock to the parent or to the affiliates should have noeffect on one or the other. The reason is that in this extreme case, the production of theaffiliates and the parent are independent. A positive correlation of activities would simplyreflect that demand shocks for the parents and the affiliates are correlated. In the case ofproductivity or technology shocks, the impact on the correlation of activities in unclear.One possibility is that the parents which receive a productivity shock (e.g. a new methodof management) transfer the technology to their affiliates. This would lead to a positivecorrelation of economic activities.

Trade within the international production network or technology transfers explain thepositive correlation of activities and the transmission of shocks between parents and affiliates.Assume now that this transmission takes place. We need to understand how the relationbetween the parent and the affiliates might influence aggregate business cycle comovement.We suppose first that the parent faces a macroeconomic shock. Examples of such macroshocks include a new technology available in the country or a natural disaster. In such cases,if the foreign affiliates are sufficiently large, then their own activities have a non-negligibleimpact on the activities of their regions of location. The macroeconomic shock in the parentcountry is thus transmitted to foreign affiliates and to the foreign country, which induces acorrelation of activities between the two economies.7

If the parent faces idiosyncratic shocks, then it must be large enough to drive outputfluctuations in its domestic country. Gabaix (2011) shows that part of the US GDP slowdownin 1970 was driven by a 10-week-long strike at General Motors. If this type of shock istransmitted to foreign affiliates, they might influence the fluctuation of GDP in their hostcountry, given that they are also large enough.

In the remainder of the paper, we document that foreign affiliates are large enoughto impact their host region’s GDP. We then show that the presence of foreign affiliatesaffects the correlation of the business cycles between their host regions and their country ofownership positively. Last, we present evidence that within firms, vertical linkages are keyto transmitting shocks from one country to another.

3 The DataAnalyzing the correlation between business cycle comovement and foreign affiliates requiresprecise information on the location and the economic activities of firms in France and onthe link between the foreign parents and their affiliates. Our data set is based on theaggregation of five confidential micro-level databases that are provided by different French

7For instance, the recent tsunami in Japan has strongly affected Japan’s GDP and all Japanese firms andmight also have affected the regions of location of their activities if their foreign affiliates were sufficientlylarge.

5

administrations. It describes value added, employment, and sales in French regions, as well asthese regions’ bilateral exports to and imports from 162 partner countries (with a distinctionbetween intra-firm trade and arm’s-length trade of foreign affiliates) in the manufacturing,extractive, and agricultural industries. Within regions, this information is disaggregatedbased on the ownership status of the firm. Namely, we distinguish the economic activities ofindependent firms, affiliates of French multinationals, and foreign affiliates , i.e. the affiliatesof foreign multinationals. The data are matched to a cross-section of bilateral correlationsof business cycles between 21 Metropolitan French regions and 162 countries. We brieflydescribe the main traits of our database in the next paragraphs. We give more details onthe data and data processing in Appendix A.

To appreciate the size of the activity of foreign affiliates in France, we need data onsales, value added and employment. This data is taken from the BRN database (BénéficeRéel Normal). The BRN is a compulsory report for all firms that have an annual turnoverof more than 763,000 euros. In order to identify the ownership status of the firms, we usethe LIFI data which is an administrative data set on the ownership and nationality of theparent company of firms located in France (LIaison FInancière).8 According to the Frenchstatistical institute (INSEE), a firm is an affiliate of a group if the latter has the (director indirect) majority of voting rights. In our data, the share of voting rights owned by theparent firms varies from 50% to 100%. While the average share of voting rights is 86%,the median is 99%. We can therefore expect the parent company to exert a control on thedecisions of the majority-owned affiliates. Moreover, having majority-owned affiliate ensuresthat the parent company is located in exactly one country. We classify firms based on theirnationality. A French affiliate, which we denote by MNE, is located in France and ownedby a French group. We denote the foreign affiliates by FME, which are located in Franceand owned by a foreign group. We also keep track of their nationality whenever they areforeign-owned. The residual group of firms is denoted by IND. It is composed of firms thatare located in France, but that are not majority owned by a group.

LIFI also has information on the main sector of activity of the parent and the affiliatesat the 4-digit level. This allows us to identify whether the affiliates in France are in thesame sector as their parent and gives us a crude method to distinguish between verticaland horizontal production networks (Buch, Kleinert, Liponner and Toubal, 2005; Ramondo,Rappoport and Ruhl, 2011). Moreover, we have precise information on foreign affiliate trade.We use the EIIG firm-level survey (Échanges Internationaux Intra-Groupe) from the INSEEwhich provides a detailed geographical breakdown of the trade value of French firms at theproduct level (HS4) and their sourcing modes – arm’s-length trade or intra-firm trade. Thedata are more precise than the data provided by the Bureau of Economic Analysis sincewe have information on arm’s-length trade of foreign affiliates in France. In addition, wecan identify through the product dimension whether the exports of a French affiliate to itscountry of origin are in intermediate inputs.

8All firms with more than 500 employees or a turnover above one million euros are asked about theirownership and financial structure. This includes their links with small businesses, which allows us to haveinformation on small foreign affiliates.

6

Data on bilateral exports and imports of firms located in France are provided by theFrench Customs. In 2004, 15% of the total number of registered firms were involved inforeign trade (exports, imports or both). Yet the participation of firms to foreign tradediffered to a great extent with their ownership structure and nationality. Among the threecategories of firms defined above, the group of independent firms was far less internationalizedthan the group of affiliates of French firms. While we only find 9.6% of the total numberof independent firms that were trading, there were respectively 36% of French affiliates and78% of foreign affiliates that participated to foreign trade.

A firm located in France might have branches in different regions. When it comes tofilling out the BRN or the Customs forms, the value added, sales or trade values are alwaysallocated to the region of location of the headquarters. We follow the INSEE methodologyand reallocate the value added, sales and trade of multi-plant firms across regions on thebasis of employment measured at the branch level.9 The statistics are then aggregated tothe level of the Metropolitan French regions for each year between 1999 and 2004.

Each cross-section is then combined with a vector of correlation of the business cyclesbetween a French region r and a partner country c. We construct the correlation betweeneach of the 21 regions and 162 partner countries over the 1990-2006 period.10 The data onregional GDP are taken from the INSEE while the data on national GDP are taken from theWorld Bank. The database is completed with the total exports and imports of the partnercountries that we take from the Direction Of Trade Statistics (DOTS).11

4 The Key Role of Foreign AffiliatesAs discussed in Section 3, there are two necessary conditions for business cycles to be trans-mitted across borders by multinational firms. First, the activities of the parent and foreignaffiliates must be positively correlated. Second, foreign affiliates must be large enough toaffect aggregate fluctuations in their host regions. The first condition was recently docu-mented by Desai and Foley (2004) who show a positive correlation between the financialactivity of parents and foreign affiliates. There is also a considerable literature on intra-firmtrade which shows that parent companies organize their production at a global scale usingtheir networks of foreign affiliates (Helpman, 2011). At first sight, the second condition isless obvious. The first set of facts provides evidence on the importance of domestic andforeign affiliates for the output of their region of location. The second set of facts highlightsthe strength of vertical linkages between foreign affiliates and their parent country.

In the empirical analysis, we use French regional data to measure the correlation betweenthe presence of multinationals and business cycle comovement. Thus, we need some hetero-

9In our sample, only 1.8% of firms are multi-plant and multi-region. Yet these firms account for 9.8%of total employment. Note that this is not a big issue since, in our main specification, we measure foreignaffiliates presence through employment, which is provided at the branch level.

10The correlation of the cycles between region r and country c is computed either as the correlation in theannual growth rates or as the correlation of HP-filtered GDPs.

11As detailed in Appendix A, values in dollars are converted into euros using the euro-dollar exchange ratefrom Eurostat.

7

geneity across regions to identify our econometric model. The third set of facts shows thatthere are disparities across regions in i) the intensity of the production of foreign multina-tional affiliates, ii) the origin of those foreign affiliates, and iii) in the pattern of aggregatecofluctuations. Last, we show the heterogeneity in the correlations between the GDP growthof French regions and their partner countries.

Facts I: the few leading the many. It is well documented that multinational firmsrepresent only a tiny fraction of the total number of firms. However, recent papers haveemphasized that even a few firms may contribute substantially to GDP and employmentfluctuations. We aim to show that the affiliates of foreign firms explain a non-negligiblepart of aggregate co-fluctuations despite their low number and because they are the largestfirms.12

In Table 1, we provide a regional breakdown of the yearly contribution of independentfirms, French affiliates, and foreign affiliates for six different outcomes: number of firms,employment, sales, value added and exports and imports. Perhaps the most informativefeature of Table 1 is the disproportionate role of affiliated firms - foreign affiliates in particular- in aggregate outcomes.

– Table 1 about here –

There are at least three interesting facts that emerge from this table.

1. Foreign affiliates and French affiliates account for the vast majority of employment,sales and trade while they represent very few firms (5.2% of firms are FMEs and 17.2%are MNEs). French affiliates account for more than 41% of employment, sales andvalue added. Foreign affiliates account for about 1/3 of value added and sales andmore than 22% of employment.

2. We find that trade is extremely concentrated within the group of foreign affiliates. Onaverage, FMEs which represent 5.2% of the total number of firms account for about47% of exports and more than 56% of imports. The contribution of French affiliatesto international trade is also sizeable. They account for one third of French importsand 40% of French exports.

3. The concentration is very pronounced in some regions as Alsace or Bretagne. In Alsace,10% of firms are foreign-owned while they represent about 50% of value added, 70% ofexports and 80% of imports. In Bretagne, foreign affiliates represent about 3 percentof firms in the region, but make up 15% of the region’s value added and about 2/3 ofits trade (import and export).

Within the group of foreign affiliates, the concentration of economic activities rests onvery few firms as shown in Table 2. In Auvergne, the five largest foreign affiliates account

12Note that we do not focus the analysis on idiosyncratic shocks driving comovement.

8

for two-thirds of the total value added of all foreign affiliates. Taking the 10 largest foreignaffiliates, this share reaches 73.8%. Given that foreign affiliates account for more than 30%of Auvergne’s value added, the ten largest foreign affiliates account for more than 22% ofthe regional value added. Auvergne is no exception since the concentration of economicactivities in the hands of a few foreign affiliates can be observed across regions.13 Withrespect to trade, the importance of the largest foreign affiliates is even more pronounced.

– Table 2 about here –

Stylized facts from Tables 1 and 2 point to the importance of foreign affiliates in Frenchregions. A change in their output or trade activities will affect regional GDPs directly.Adding indirect effects, through the link to local suppliers and customers, the impact offoreign affiliates would probably be even larger.

In Figure 1, we investigate the ownership breakdown of the share of value added by thelargest 1% firms. We also show figures on the composition of firms in the remaining sample,once we exclude the top 1% firms.

– Figures 1 about here –

The results are striking. About 30 to 70 percent of the largest (top1%) firms have aforeign ownership. Less than 10 percent are independent. By contrast, the remaining groupof small firms is mostly made up of independent firms and the share of foreign affiliates isnever greater than 10 percent.14. This fact suggests not only that firms are different withrespect to their size and that a few firms are sizably larger than other firms, but that theyare also different in terms of their ownership structure. In Appendix E, we show that theaffiliates of foreign parents tend to be the largest among the largest firms.

Facts II: intra-firm trade. Intra-firm trade has proved to be a particulary importantdeterminant of business cycle comovement (Burstein et al., 2008). Table 3 reports evidenceon intra-firm exports and imports by French and foreign affiliates across French regions. Thefirst set of results from Table 3 stems from the comparison of exports (columns 1 and 3) andimports (columns 2 and 4) by French and foreign affiliates. While the share of intra-firmtrade is already high for French affiliates, it appears that this share is even larger for foreignaffiliates. This is particularly relevant for imports. The share of intra-firm imports by foreign

13For instance, the ten largest foreign affiliates account for 19.1% of the total value added in Alsace, 18.3%in Lorraine, and 12.8% in Picardie.

14The information on the ownership of firms comes from LIFI. As discussed in Appendix A, this survey isexhaustive for firms with an annual turnover above 1 million euros and firms with more than 500 employees.If we focus on the sample of firms that are above one of these thresholds, we drop half of the firms, butthe remaining ones account for 94% of the total value added. Focusing on this reduced sample of firms,we find the same difference in the composition of the top 1% against the others. In particular, FMEs areover-represented in the largest 1% firms of this sample. Namely, FMEs account for 49% of the top 1% andMNEs account for 42%. By contrast, FMEs account for only 9.5% of the smallest firms, and MNEs 33%

9

affiliates is at least twice the share of intra-firm imports by French affiliates.15 The tableshows that there is an important degree of heterogeneity across regions. About 31% of thetrade of affiliates in Aquitaine is intra-firm, while it is 75% for Centre.

– Table 3 about here –

There are multiple potential financial and economic linkages between foreign affiliatesand their country of ownership. We have information on two important economic linkages,namely trade and intra-firm trade. Our data reveal that 13.6% of total exports and 25.6%of total imports of foreign affiliates are with their country of ownership. This is substantialgiven the large cross-section of countries that we have in our sample. Furthermore, the lasttwo columns of Table 3 show that almost three quarters of the total trade between foreignaffiliates and their parent country is intra-firm. More specifically, 15% of the exports offoreign affiliates are directed toward their parent country, and almost 80% of these exportsare intra-firm. This suggests that there are very strong vertical linkages between foreignaffiliates and their parent country.

Facts III: the heterogenous location of firms with different ownership nationali-ties. We have shown that foreign affiliates constitute a large share of regional employment,value added and trade. Another important dimension concerns their country of ownership.In order to have an impact on business cycle comovement, affiliates from a particular foreigncountry must contribute to a significant share of regional outcomes. In France, 55% of thenumber of foreign affiliates are owned by parents from the United States, Spain, Germany,the United Kingdom, and the Netherlands. They account for more than two-thirds of thetotal value added generated by foreign affiliates.

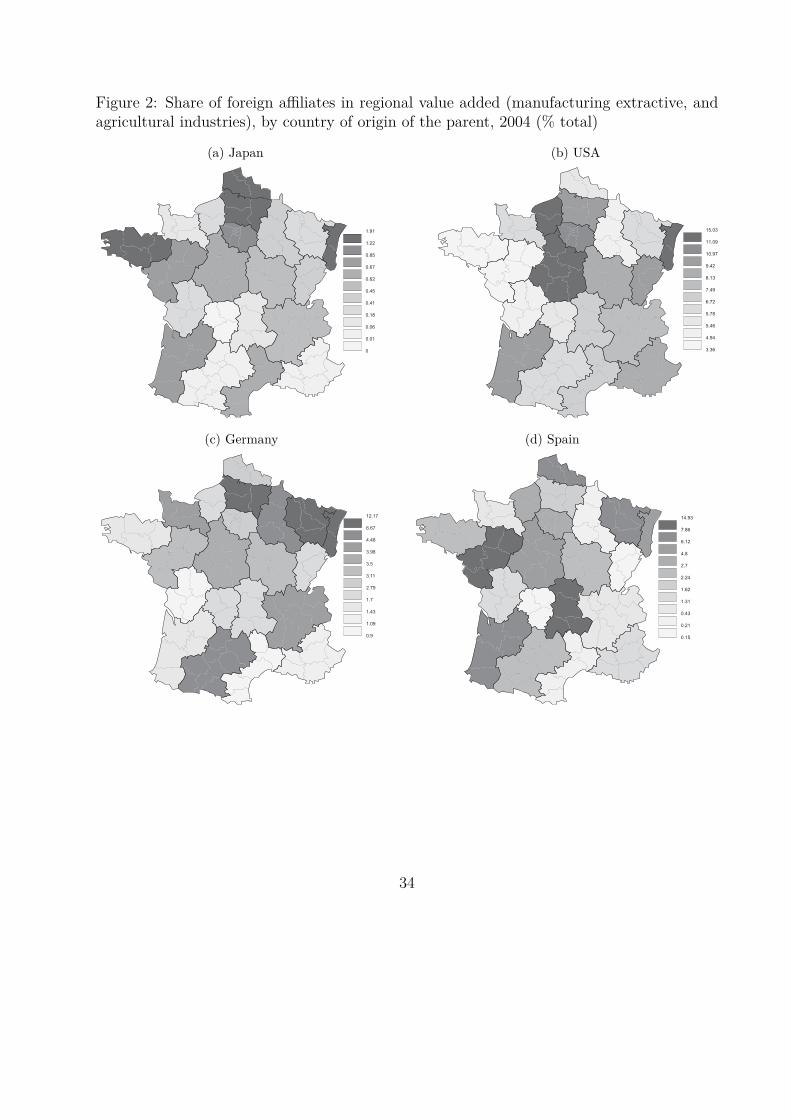

To be able to use the cross-region dimension of the data, we need some heterogeneitywith respect to the nationality of foreign affiliates across regions. The share of value addedis expected to be high for some investors in regions along the border, but the border alonecannot explain the location of activities and comovement. Fortunately, the shares of valueadded by country of ownership are not evenly distributed across all regions. It is interestingto look at the regional distribution of the shares of value added by important source countries;two sharing a border with France (Germany and Spain) and two outside Europe (the U.S.and Japan). This is represented in Figure 2.

– Figure 2 about here –

These maps show that the value added shares of German affiliates is large in Alsace-Lorraine, but also very large in Midi Pyrénées, which does not share a border with Germany.16

Spanish affiliates contribute largely to the value added created in Pays de la Loire and notin the neighboring regions of Midi-Pyrénées or Aquitaine.

15Given the share of intra-firm trade for MNEs and FMEs, and the share of FMEs and MNEs in totaltrade, about 40% of French exports and 45% of French imports are intra-firm. As a comparison, Bernard,Jensen, Redding and Schott (2010) report that 46% of US imports are intra-firm.

16With the presence of large affiliates such as Airbus Deutschland and Siemens VDO Automotive.

10

Facts IV: business cycle comovements. We now turn to the bilateral correlation be-tween French regional GDPs and the countries studied. If there was only one French businesscycle, the regional dimension would not add to the explanation of comovement. In Table4, we report the correlation of GDP growth between French regions. While the correlationis as high as 0.9 for a few regions, the correlation is very low and even negative for otherpairs. Hence, French regions do not share perfectly correlated business cycles. We will usethis characteristic later on when we analyze the impact of foreign affiliates on business cyclecorrelations between French regions.

– Tables 4 and 5 about here –

In Table 5, we report the maximum and minimum correlations of French regions withGermany, Spain, the U.S. and Japan. For Germany and Spain, the unconditional correlationof GDPs is among the highest with the regions where their foreign affiliates represent asubstantial share of regional value added. Unexpectedly, we find a negative unconditionalcorrelation for the U.S. and Japan in the regions where they account for a large share ofvalue added.

These stylized facts show that there is ** a ** heterogeneity in the GDP growth correla-tions along two dimensions. First, a single country might have a high level of synchronizationwith some French regions and not ** with ** others. This is the case of Germany with Alsaceand Auvergne. Second, a single region might have a high level of correlation with one coun-try but not with another. This is the case of the GDP growth of Alsace which is positivelycorrelated with the German GDP growth but not with the Spanish GDP growth.

5 Empirical StrategyOur analysis uses a cross-section of business cycle correlations between 21 Metropolitanregions and 162 countries. Not all countries in the sample invest in France, so that thevector of correlations has many zero values. There are thirty-four countries with majority-owned affiliates that report positive employment in the sample.17 However, most of thesecountries share a trade relationship with the French regions. We do not discard the zerovalues in our first test. Yet, we show in section 6 that our main findings hold when we doso. Our baseline equation is the following:

ρcr = αFMEcr + Ωcrβ + νr + νc + εcr (1)

where εrc is the disturbance term. ρcr is a vector of correlations of GDP growth ratesbetween a country c and a region r computed over the 1990-2006 period. It is defined as

17Australia, Austria, Belgium, Canada, China, the Czech Republic, Denmark, Germany, Greece, India,Ireland, Island, Israel, Italy, Finland, Japan, Korea, Lebanon, Malaysia, Morocco, the Netherlands, Norway,Portugal, Saudi Arabia, Singapore, Spain, Switzerland, Sweden, Thailand, Tunisia, Turkey, the UnitedKingdom, the United States, and Venezuela. Nine of them have positive employment in all regions: Belgium,Germany, Italy, Finland, the Netherlands, Switzerland, Sweden, the United Kingdom, and the United States.

11

ρcr = corr(GDPc,t−GDPc,t−1GDPc,t−1

, GDPr,t−GDPr,t−1GDPr,t−1

). To test the robustness of our results, we alsotransform the GDP series (in logs) using the filter proposed by Hodrick-Prescott (1997)and compute the correlation of the cyclical components of regional GDP and country GDPgrowth rate.18

In all regressions, we add a set of country and region fixed effects νr and νc that do notonly control for the demand and supply shocks, but also for omitted variables at the regionaland national level. Country fixed effects capture all the country characteristics that mayexplain the correlation between French regions and the country. In other words, the countryfixed effects capture the business cycle correlation of France and the country. The regionfixed effects capture the relative correlation of the region with respect to foreign countriesand the other French regions.

FMEcr is an indicator of the importance of foreign affiliates from country c in regionr. As argued by Lipsey (2008), the measurement of the location of the production of amultinational might be influenced by the tax strategies followed by the parent firm. Themeasurement of the FMEcr indicator therefore is not straightforward. In order to controlfor the importance of foreign affiliates in French regions, we take employment rather thanvalue added because employment is less subject to manipulation for tax reasons. We defineFMEcr as the share of employment by foreign affiliates of country c in region r.

FMEcr =∑

f Empfcr

Empr

(2)

where Empfcr is the employment of firm f with ownership from c in region r. Thedenominator Empr is the total employment in region r.19 Since we know both the sectorsof the foreign parent and the French affiliate, we also construct a measure of verticallyintegrated production networks. The construction is based on the 4-digit sector classificationof the foreign parent and its French affiliate. We assume that a vertical relationship occurswhenever the parent is classified in another sector than the one of its affiliate. At the 4-digit level of aggregation, the measurement of a vertically integrated production networkis underestimated.20 Moreover, we use a second indicator which is the share of intra-firmexports from region r to country c, IFcr. This variable is constructed as follows:

IFcr =∑

f∈C (IFEXfcr)(xcr +mcr)

(3)

where IFEXfcr is the value of intra-firm exports from the affiliates in region r to theparents in country c and xcr and mcr represents the value of bilateral export and import,respectively.21 As in Burstein, Kurz and Tesar (2008), we argue that the synchronization is

18Since we use yearly data, we apply a smoothing parameter of 6.25 as recommended by Ravn and Uhlig(2002).

19We also replicate the results using value added instead of employment.20While parents and affiliates classified in different sectors share a vertical relationship, we cannot distin-

guish between horizontally and vertically integrated networks for affiliates and parents that are in the samesector at the 4-digit level.

21As the intra-firm trade variable is constructed from a survey, it is not directly comparable to the regional

12

likely to be influenced by trade in inputs within the international production networks. Wetherefore need to identify these intermediates. To identify inputs, we use the data providedby Antras et al. (2012). They compute the distance from final consumption using U.S. input-output tables for 426 industries.22 Products with a distance to final use greater than twoare defined as intermediate inputs. This variable is computed as IFcr using the sample ofintra-firm exports of intermediate goods.

The literature has emphasized other important determinants of business cycle comove-ment. We include them in the Ωrc matrix. A first important factor relates to bilateral tradeintensity (Frankel and Rose, 1998). We construct the index of bilateral trade intensity asthe ratio of exports and imports between country c and region r over the sum of the regionand country GDP.

BTcr = xcr +mcr

GDPc +GDPr

(4)

It has also been shown that the productive structure as well as the structure of bilateraltrade are key determinants of business cycle comovement (Imbs, 2004). The similarity inthe production structure is usually computed from production data. In our case, such dataare very difficult to use because of the lack of similar classification between the countriesand the regions. Moreover, we do not have good sector-level production data for Frenchregions. The existing data are aggregated at the 1-digit sector level. Once merged withcountry data on production, this index would allow us to compare the relative specializationof countries in services, manufacturing and agriculture. Such an aggregate index hidesimportant heterogeneity within sectors, and specifically within the manufacturing sector.23

To circumvent this issue, we decided to compare the specialization of countries rather thantheir production. Both are tightly linked, and specialization presents the advantage to beeasily observable from trade level data (which are available for regions and a large set ofcountries at highly disaggregated levels). We thus compare the specialization/productionstructure of countries by looking at the composition of their exports. We compute thedissimilarity index as follows:

DISIMcr = 1−∑

k

|Xkc

Xc

− Xkr

Xr

| (5)

Where Xki /Xi is the share of sector k in the total exports of country i. Exports are

computed at the 3-digit ISIC revision sector level. Since more similar partners are likelyto face the same supply and demand shocks, a higher similarity should therefore lead to agreater synchronization of business cycles.

Having bilateral trade data at the sector level, we can also evaluate the importance of

share of foreign affiliate employment. In the following regression analysis, we will investigate their effectsseparately.

22The Bureau of Labor Statistics provides a correspondence table to transform the 426 commodity codesinto HS6 codes. We merge this information with our export data at the HS6 level.

23We report in the unpublished appendix specifications including this determinant. It does not affect ourresults.

13

intra-industry trade on business cycle comovements (Calderon et al., 2007; di Giovanni andLevchenko, 2010; Fidrmuc, 2004). We use the French Customs data to allocate exportersand importers across regions and compute a Grubel-Lloyd index for each pair of country andregion.

IITcr = 1−∑

k |Xkcr −Mk

cr|∑k Xk

cr +Mkcr

(6)

where Xkcr and Mk

cr are the exports to and imports from country c, by region r, for sectork. In our analysis, we consider 4-digit level sectors of the HS nomenclature. An index closeto one means that country c and region r trade similar types of products: they are engagedin intra-industry trade.

It is also likely that regions and countries that are geographically close to each other areaffected by similar demand and supply shocks (Clark and van Wincoop, 2001). To capturegeographical proximity, we use the distance and the presence of a common border betweenregions and countries. The border variable, Borderrc equals one if country c and region rshare a common border. To compute the distance between country c and region r, we firstidentify the latitude and longitude of each firm in our sample and of the capital city of eachcountry. We then compute the distance between each firm and each country. The distancebetween region r and country c is the arithmetic average of the individual distance thatseparates the firms of region r and the capital of country c.

Distrc =∑

f∈r distfc

N rf

(7)

where distfc is the distance between firm f (from region r ) and the capital of countryc, and N r

f is the number of firms in region r.There are other factors that might influence the synchronization of business cycles. Kose

and Yi (2006), Imbs (2004) and more recently Kalemli-Ozcan, Papaioannou and Peydro(2009) show that an increased financial integration affects business cycle comovement acrosscountries. We do not have information on this latter determinant. Our results are insensitiveto this variable as long as the financial integration between French regions and the foreigncountries is not correlated to the presence of foreign affiliates. This does not appear as astrong assumption since we do not have service and finance firms in our data.

6 Econometric ResultsBaseline Results. The results of the baseline estimation using the GDP growth ratecorrelation are reported in Table 7.24 The specifications include a full set of region- andcountry-specific effects.

24As an alternative proxy for the business cycle, we also compute the GDP growth rate from the HP-filtered GDPs. The results are presented in Table 16 of Appendix E. We show that our findings are robustto this alternative definition.

14

– Table 7 about here –

Columns (1) and (2) respectively investigate the effect of the share of foreign affiliateemployment and bilateral trade on business cycle correlations. Both variables have a pos-itive impact on the level of synchronization. Once we include both variables together, incolumn (3), the impact of the bilateral trade variable is less important and estimated witha much lesser degree of precision. It is an indication of the role of foreign affiliates in Frenchinternational trade.

The impact of the share of foreign affiliate employment is not only significant, but itis also quantitatively important. Based on the preferred estimates from column (4), thestandardized coefficient of the FMEcr variable is 0.06, while the standardized coefficients ofthe BTcr and IITcr variables are 0.03 and 0.02 respectively. The effect of foreign affiliatesis therefore great enough to be of substantial interest. Since we estimate a linear model, wecan evaluate the elasticity of the FMEcr variable at mean values. Taking information fromTable 6, we find that a 10% percent increase in the employment intensity of foreign affiliatesraises the business cycle correlation between their country of ownership and their region oflocation by about 0.6%.

In order to quantify the impact of foreign affiliates on business cycle correlations, basedon previous regressions, we evaluate the impact of the exit of all foreign affiliates from aregion on business cycle comovement. We conduct this experiment for each French regionfor the foreign affiliates from Germany, which is a major investor in France. In the firstcolumn of Table 8, we report the share of foreign affiliate employment from Germany foreach region. In the second and third columns, we report the deviation from the averageFrench comovement with and without the foreign affiliates from Germany.25

– Table 8 about here–

The results indicate that the French business cycle correlation with Germany is on average6.7 percentage points lower without foreign affiliates from Germany. The effect is greater inregions where the employment share of German affiliates is the largest. Concerning Alsace,the business correlation between Alsace and Germany is 17.1 percentage points above averagewith German affiliates, while it is 11.4 percentage points below average without accountingfor their presence. In a few regions with an important presence of German affiliates suchas Midi-Pyrénées, the correlation with Germany remains positive after the exit of Germanaffiliates. This is due to their sectoral specialization which is similar to that of Germany. InTable 17 of Appendix 16, we find a very similar pattern when conducting a similar analysisfor the United States. The French business cycle correlation with the United States is onaverage 10.1 percentage points lower without foreign affiliates from the U.S.

Turning to the other covariates, the results suggest that the effects of bilateral tradeand intra-industry trade are not significant, while the dissimilarity in the production struc-ture does matter. In line with Imbs (1999) and Imbs (2004), synchronization appears to be

25The bilateral and the average comovements are computed from the predictions of the equation reportedin the last column of Table 7.

15

smaller in regions that have dissimilar sectoral production patterns. The production struc-ture dissimilarity variable is negative and significant. It is robust across specifications.26

Further Analysis. The findings reported in Table 7 point to an impact of the presenceof foreign affiliates without distinguishing between the types of linkages that these affiliatesshare with their country of origin. An important aspect concerns the nature of the interna-tional production network, and whether it is vertically or horizontally integrated. The dataallows us to imperfectly identify vertically integrated networks. One crude methodology isto compare the 4-digit sector of the parent with the 4-digit sector of its affiliates. If thesesectors do not match, we have a measure of a vertically integrated network. As mentionedin Section 2, we should expect strong effects from this type of linkage. We report the resultsin Table 9:

– Table 9 about here –

Column (1) of Table 9 replicates the baseline analysis using the employment intensity ofaffiliates that are part of a vertically integrated network. We find a positive and significantimpact of this intensity on business cycle comovement. A 10% increase in the employmentintensity of vertically integrated affiliates raises the correlation of the GDP growth rate by0.4%. As mentioned earlier, we however underestimate the employment intensity as thesector classification of the parent and its affiliates is rather aggregated.

Another way to account for the vertical structure is to look at the exports of foreignaffiliates toward their country of origin. Our data captures both intra-firm and arm’s-lengthexports of foreign affiliates. In Column (2), we replicate the previous results using the shareof intra-firm exports in total exports as explanatory variable. We find that a 10% increasein the share of intra-firm exports increases the correlation of GDP growth rates by 0.2%.This impact is identical when we control for the share of exports that affiliates outsource totheir country of origin.27 These results confirm that the business cycle correlation is greaterwhen trade takes place within the network of the multinational firm.

In columns (3) and (4), we replicate the analysis using the sample of intermediate inputs.The results barely change. They confirm that vertically integrated networks are a channelof influence when analyzing the effects of foreign affiliates on business cycle correlation.

We now discuss the results of some further sensitivity tests. We investigate whether theresults are robust to the exclusion of countries that do not invest in France. Moreover, wereplicate the baseline analysis using the value added intensity. We investigate the role oftwo exogenous components, distance and border, and show that the results are robust totheir introduction. We finally consider a simple falsification exercise in which we allocatethe employment intensity FMEcr randomly across regions.

26We use an alternative definition of the dissimilarity index based on production data using a 1-digitclassification. The results are shown in Table 18 of Appendix E. The main findings remain robust to thealternative definition of the dissimilarity index.

27We refer to outsourcing since the foreign affiliate exports to an unaffiliated party.

16

Sensitivity Analysis. In the baseline estimations, we use the 1990-2006 period to computethe correlation of the GDP growth rates and of the year 2004 to construct the exogenousvariables. The explanatory variables are however available for different cross-sections from1999 to 2004. Each cross-section is composed of the same bilateral pairs of regions andcountries. We can therefore repeat the baseline analysis using different years of explanatoryvariables. In Table 10, we repeat the cross-sectional estimates of column 5 of Table 7.

– Table 10 about here –

As we can see, the results barely change and the robustness is high. In each cross-section,we evaluate the effect of the foreign affiliate employment intensity to be roughly the sameas in the baseline table. We find that a 10% percent increase in the employment intensityof foreign affiliates raises the business cycle correlation between their country of ownershipand their region of location by about 0.6%.

As a reminder, the baseline sample includes countries that may or may not invest in aregion, so that the share of foreign affiliate employment may be zero. One way to investigatewhether the results are driven by the zeros in employment intensity is to keep the countriesfor which we observe a positive value of employment in at least one region. We present theresults in Table 11. Notice that in this case, we drop about 80% of the observations of theinitial baseline sample.

– Table 11 about here –

Columns (1) to (4) show that the foreign affiliate employment share is still significantand positive. The estimated elasticity is slightly larger (because it is evaluated at differentmean values). In column (4), we find that a 10% percent increase in the employment shareof foreign affiliates raises the business cycle correlation between their country of ownershipand their region of location by about 0.7%.28 By contrast, the trade variable is insignificant(as in the baseline sample). In line with the previous findings, we find a negative impact ofthe dissimilarity index on the business cycle correlation.

As an additional test, we investigate whether our finding is not driven by the share offoreign affiliate employment from the same country in neighboring regions. To illustrate thesource of this concern, consider two regions a and b, and a country c. Assume that countryc has affiliates in region a only and that the real cycle of region b is perfectly correlatedto the real cycle of region a, because b produces inputs for a. We might find a correlationbetween country c and region b despite the absence of foreign affiliates from c. In this case thecoefficient of the FMEcr variable in the baseline regression should be biased downward.29 Toassess the robustness of the results, and to investigate the empirical relevance of our concern,we include a measure of the share of employment by foreign affiliates in other regions that

28The mean value of the GDP growth rate correlations and of the employment shares in this sample are0.12 and 0.001, respectively

29The coefficient should not be significant in our example: both regions are correlated with Germany whileone has German affiliates and the other does not.

17

come from the same country. Therefore, we compute an indicator which is the distance-weighted share of employment of foreign affiliates from country c in other regions. Thisindicator is computed as FMEother

cr = ∑r′

F MEr′clog(distrr′ )

.

– Table 12 about here –

Table 12 displays the results including this control variable. As expected, the presenceof foreign affiliates in neighboring regions increases the business cycle comovement of theregion with the parent country of these affiliates. However, the effect is not robust acrossspecifications. More importantly, in all the specifications, the FMEcr variable remainssignificant. Notice that compared to the baseline effects in Table 7, the coefficients areslightly larger.

It is also likely that regions and countries that are geographically close to each other areaffected by similar demand and supply shocks (Clark and van Wincoop, 2001). The resultsare reported in Table 13. Compared to the results of Table 7, the inclusion of the bilateraldistance and border variables does not involve any notable change to the explanatory powerof our regressions as measured by the R2.

– Table 13 about here –

In the first two columns, we analyze the impact of distance and border on business cyclecorrelations.30 The results point to a negative and significant effect of distance while theborder variable is insignificant. In columns (3) and (4), we introduce the foreign affiliateemployment intensity variable and the bilateral trade variable successively. Compared tothe estimates of the baseline estimation, we find that bilateral distance and borders do notinfluence the coefficient of the foreign affiliate employment intensity significantly. However,the introduction of both variables lowers the impact and significance of the bilateral tradevariable. In column (5), the impact of bilateral trade disappears while the foreign affiliateemployment intensity is still highly significant.

As a further test, we consider the ratio of foreign affiliate value added to regional GDP.This ratio is as an alternative measure of the foreign affiliate presence in the region. It is lessrelevant than the employment intensity since it is likely to be manipulated for tax reasons(Lipsey, 2008). Table 14 reports the results which are essentially identical to the baselinespecification.

– Table 14 about here –

The estimations consistently show a positive and significant impact of the foreign affiliatevalue added intensity on the correlation of GDP growth rates. This impact is howeverestimated with a lesser degree of precision than in the baseline estimations of Table 7. Themain difference is that we find a positive and slightly significant effect of the bilateral tradevariable once we control for all the other covariates as in column (4).

30We also control for region and country fixed effects.

18

As a final check, we propose a falsification exercise. We assign the true foreign affiliateemployment intensity of each region to another randomly.31 This exercise might be infor-mative since the business cycle comovement between a country and a region should not beinfluenced by the employment intensity of foreign affiliates coming from another country orlocated in another region. Table 15 reports the results.

– Table 15 about here –

The randomly assigned foreign affiliate employment intensity is always insignificant, asexpected.

Reverse causality. In a recent paper, Ramondo et al. (2010) revisit the proximity concen-tration trade-off adding uncertainty. In their model, firms are more likely to serve countrieswith a business cycle correlated with their own country through horizontal FDI rather thanthrough exports. In such a framework, business cycle comovement is a determinant of hori-zontal FDI. It is important to emphasize that the model applies for firms opening affiliatesabroad for horizontal purposes. Our baseline estimations may suffer from reverse causality.However, the effect of the presence of foreign affiliates on business cycle comovement remainssignificant once we focus on vertical foreign affiliates. Since the effects in this restricted spec-ification are of the same order of magnitude as in the baseline, we are quite confident thatreverse causality is not a major source of bias in our estimates.

7 ConclusionThis paper shows the importance of studying the ownership and nationality of firms whichcontribute to economic activities to better understand the sources of aggregate co-fluctuations.We find that the synchronization of international real business cycles is largely driven bycross-border networks of foreign affiliates.

Interestingly, the role of multinational firms and their foreign affiliates has been largelyunder-emphasized in the literature. The access to French micro data sets allows us todocument a variety of facts that help understand the contribution of foreign affiliates tobusiness cycle comovement between French regions and foreign countries. There is evidencein the data that foreign affiliates are large enough to affect aggregate economic outcomes. Weshow that the foreign affiliates of multinational firms account for a disproportionate share ofemployment, value added and trade of French regions. Moreover, there are strong linkagesbetween the foreign affiliates in France and their foreign parents. In the data, the medianof the share of foreign ownership is 99% and more than 70% of foreign-owned affiliate tradeis conducted intra-firm. This suggests that foreign affiliates can create economic linkagesbetween countries.

31For instance, we assign the German employment intensity in Alsace to a randomly chosen region and arandomly chosen employment intensity to Alsace.

19

Our empirical analysis shows the large contribution of foreign affiliates in the comovementof real business cycles between their region of location and their country of origin. Ourfindings are robust to the inclusion of the main driving factors in the literature and to theintroduction of fixed effects at the level of regions and countries. Interestingly, we find aweak impact of trade on the synchronization of real business cycles once we control for theimpact of foreign affiliates. This is partly due to the prominent role of foreign affiliates inconducting trade. However, the importance of foreign affiliates for business comovement goesbeyond their participation to international trade. This suggests multinational firms ease thetransmission of shocks across borders, within firm boundaries.

The richness of the French data allows us to investigate some types of linkages that areat work here. We show that vertical linkages between parents and affiliates and intra-firmtrade are important in explaining the comovements of real business cycles. One importanttopic for future research is to obtain a better understanding on the channel of transmissionbetween the parent and its affiliates. Other complementary economic linkages, such as thetransfers of financial assets and intangible inputs may strengthen the transmission of shockswithin multinational companies across countries.

20

ReferencesAntras, P., Chor, D., Fally, T. and Hillberry, R. (2012), ‘Measuring the upstreamness of pro-duction and trade flows’, American Economic Review Papers & Proceedings 102(3), 412–416.

Arkolakis, C. and Ramanarayanan, A. (2009), ‘Vertical specialization and international busi-ness cycle synchronization’, Scandinavian Journal of Economics 111(4), 655–680.

Atalay, E., Hortacsu, A. and Syverson, C. (2012), Why do firms own production chains?,Working Paper 18020, National Bureau of Economic Research.

Backus, D. K., Kehoe, P. J. and Kydland, F. E. (1992), ‘International real business cycles’,Journal of Political Economy 100(4), 745–75.

Baxter, M. and Kouparitsas, M. A. (2005), ‘Determinants of business cycle comovement: arobust analysis’, Journal of Monetary Economics 52(1), 113–157.

Bergin, P. R., Feenstra, R. C. and Hanson, G. H. (2009), ‘Offshoring and Volatility: Evidencefrom Mexico’s Maquiladora Industry’, American Economic Review 99(4), 1664–71.

Bernard, A. B., Jensen, J. B., Redding, S. J. and Schott, P. K. (2010), ‘Intrafirm trade andproduct contractibility’, American Economic Review 100(2), 444–48.

Buch, C., Kleinert, J., Liponner, A. and Toubal, F. (2005), ‘Determinants and effectsof foreign direct investment: Evidence from german firm-level data’, Economic Policy20(41), 53–110.

Burstein, A., Kurz, C. and Tesar, L. (2008), ‘Trade, production sharing, and the internationaltransmission of business cycles’, Journal of Monetary Economics 55(4), 775–795.

Calderon, C., Chong, A. and Stein, E. (2007), ‘Trade intensity and business cycle synchro-nization: Are developing countries any different?’, Journal of International Economics71(1), 2–21.

Clark, T. E. and van Wincoop, E. (2001), ‘Borders and business cycles’, Journal of Interna-tional Economics 55(1), 59–85.

Desai, M. A. and Foley, C. F. (2004), The comovement of returns and investment within themultinational firm, Nber working papers, National Bureau of Economic Research, Inc.

di Giovanni, J. and Levchenko, A. A. (2010), ‘Putting the Parts Together: Trade, Verti-cal Linkages, and Business Cycle Comovement’, American Economic Journal: Macroeco-nomics 2(2), 95–124.

di Giovanni, J. and Levchenko, A. A. (2011), Country size, international trade, and aggregatefluctuations in granular economies, NBER Working Papers 17335, National Bureau ofEconomic Research, Inc.

21

di Giovanni, J., Levchenko, A. A. and Méjean, I. (2011), Firms, Destinations, and AggregateFluctuations, mimeo.

Fidrmuc, J. (2004), ‘The endogeneity of the optimal currency area criteria, intra-industrytrade and emu enlargement’, Comptemporary Economic Policy 1, 1–12.

Frankel, J. A. and Rose, A. K. (1998), ‘The Endogeneity of the Optimum Currency AreaCriteria’, Economic Journal 108(449), 1009–25.

Gabaix, X. (2011), ‘The granular origins of aggregate fluctuations’, Econometrica 79(3), 733–772.

Goldberg, P. and Hellerstein, R. (2009), How rigid are producer prices?, Working Papers1184, Princeton University, Department of Economics, Center for Economic Policy Studies.

Helpman, E., ed. (2011), Understanding Global Trade, MA: Harvard University Press.

Hsu, C.-C., Wu, J.-Y. and Yau, R. (2011), ‘Foreign direct investment and business cycleco-movements: The panel data evidence’, Journal of Macroeconomics 33(4), 770 – 783.

Imbs, J. (2004), ‘Trade, Finance, Specialization, and Synchronization’, The Review of Eco-nomics and Statistics 86(3), 723–734.

Imbs, J. M. (1999), ‘Technology, growth and the business cycle’, Journal of Monetary Eco-nomics 44(1), 65–80.

Inklaar, R., Jong-A-Pin, R. and de Haan, J. (2008), ‘Trade and business cycle synchronizationin OECD countries–a re-examination’, European Economic Review 52(4), 646–666.

Jansen, W. J. and Stokman, A. C. J. (2006), ‘International rent sharing and domestic labourmarkets: A macroeconomic analysis’, Review of World Economics (WeltwirtschaftlichesArchiv) 142(4), 792–813.

Johnson, R. C. (2012), Trade in intermediate inputs and business cycle comovement, WorkingPaper 18240, National Bureau of Economic Research.

Kalemli-Ozcan, S., Papaioannou, E. and Peydro, J. L. (2009), Financial regulation, financialglobalization and the synchronization of economic activity, NBER Working Papers 14887,National Bureau of Economic Research, Inc.

Kose, M. A. and Yi, K.-M. (2006), ‘Can the standard international business cycle modelexplain the relation between trade and comovement?’, Journal of International Economics68(2), 267–295.

Lipsey, R. E. (2008), Measuring the location of production in a world of intangible produc-tive assets, fdi, and intrafirm trade, Working Paper 14121, National Bureau of EconomicResearch.

22

Mansfield, E. (1962), ‘Size of firm, market structure, and innovation’, Journal of PoliticalEconomy 71(6).

Moscarini, G. and Postel-Vinay, F. (2009), Large employers are more cyclically sensitive,NBER Working Papers 14740, National Bureau of Economic Research, Inc.

Neary, J. P. (2009), Two and a half theories of trade, CEPR Discussion Papers 7600, C.E.P.R.Discussion Papers.

Ng, E. C. (2010), ‘Production fragmentation and business-cycle comovement’, Journal ofInternational Economics 82(1), 1–14.

Parenti, M. (2012), International trade: David and goliath, mimeo, Paris School of Eco-nomics.

Ramondo, N., Rappoport, V. and Ruhl, K. J. (2010), The proximity-concentration trade-off under uncertainty, Working papers, New York University, Leonard N. Stern School ofBusiness, Department of Economics.

Ramondo, N., Rappoport, V. and Ruhl, K. J. (2011), Horizontal vs. vertical fdi : Revisitingevidence from u.s. multinationals, Working Papers 11-12, New York University, LeonardN. Stern School of Business, Department of Economics.

Ravn, M. O. and Uhlig, H. (2002), ‘On adjusting the Hodrick-Prescott filter for the frequencyof observations’, The Review of Economics and Statistics 84(2), 371–375.

Shimomura, K.-I. and Thisse, J.-F. (2009), Competition among the big and the small, CEPRDiscussion Papers 7404, C.E.P.R. Discussion Papers.

Terrien, B. (2009), A new standard for compiling and disseminating foreign direct investmentstatistics, Quarterly Selection of Articles 16, Banque de France.

Tesar, L. L. (2008), Production sharing and business cycle synchronization in the accessioncountries, in ‘NBER International Seminar on Macroeconomics 2006’, NBER Chapters,National Bureau of Economic Research, Inc, pp. 195–238.

Zlate, A. (2010), Offshore production and business cycle dynamics with heterogenous firms,International Finance Discussion Papers 995, Board of Governors of the Federal REserveSystem.

23

Appendix

A Data AppendixWe have built a database that describes value added, employment, and sales in the man-ufacturing, extractive, and agricultural sectors of French regions, as well as their bilateralexports to and imports from 162 partner countries and the value of intra-firm trade.32 Withinregions, we disentangle activities based on the ownership of firms. Namely, we distinguishactivities generated by independent firms, French affiliates, and foreign affiliates (dependingon their parent country). The data are matched to a vector of bilateral correlations of busi-ness cycles between 21 Metropolitan French regions and these 162 countries.33 This dataset is built from the aggregation of several sets of micro data that are provided by differentFrench administrations.

Firms in France need to report their tax statements (through one of three alternativeregimes) to the tax administration. The Bénéfice Réel Normal (BRN) needs to be filedby all firms that have an annual turnover of more than 763,000 euros in manufacturing andmore than 230,000 euros in services. Firms with a lower turnover might still opt for the BRNregime, but they are automatically registered under the Regime Simplifié d’Impositions (RSI)instead of the BRN. Firms file for an RSI account for an annual turnover of less than 4%and a total employment of less than 11% (see di Giovanni, Levchenko, and Méjean 2011).Entrepreneurs (owner-manager-single-employee firms) with an annual turnover of less than80,300 euros are subject to the MicroBIC regime, Micro Bénéfice Industriel et Commerciaux.These firms have a negligible weight in the distribution of annual turnover, value addedand employment. Of all those regimes, the BRN is the most comprehensive regarding theinformation available, including balance sheet information on total employment and totalvalue added.

The BRN is merged with the "LIFI élargi", a data set that has information on theownership and nationality of the parent company of firms located in France. The data setcombines two sources of information. First, a survey on "large" firms that gives detailedinformation on the ownership of groups, the link between affiliates (at home and abroad),and information on shareholders. Only firms with more than 500 employees, or having ayearly turnover greater than 20 million euros, or having more than 1.2 million euros of sharesin other firms are subject to this survey. The survey is completed with DIANE, a data setthat reports financial linkages between firms. Firms with an annual turnover above onemillion euros are surveyed. Notice that relatively large firms are surveyed, but they indicatetheir financial links with all their affiliates (if any) irrespective of their size. Furthermore,the sample of firms that are surveyed (the ones with more than 500 employees or more than1 million euros of turnover) represents half of the firms, but these firms account for 94% oftotal value added.

32We do not have information on services.33We exclude the comovement between French regions and France as a whole.

24

We classify firms according to their nationality and ownership. French domestic firms,which are located in France and not owned by a group, are denoted by IND (for independent).A French affiliate, MNE, is located in France and owned by a French group. Foreign affiliates,which are located in France and owned by a foreign group, are denoted by FME. Later on,we will distinguish the foreign affiliates based on their nationality. At this stage, our dataconsists of an exhaustive panel of 184,929 firms, for the 1999-2004 period.

We merge the data with a data set provided by French Customs that gives informationon bilateral exports and imports of firms located in France. For each firm, this databasereports the bilateral free-on-board value, the quantity of exports, the cost-insurance-freightvalue and the quantity of imports. Extra-European shipments of a value which is less than1,000 euros are subject to a simplified declaration procedure and do not appear in our data.Within the Single European Market, the reporting threshold is based on the cumulated yearlyexport value of each firm (all destinations within the EU). This threshold has increased overtime, up to 100,000 euros in 2002 and 150,000 euros in 2003.

Information on intra-firm trade is taken from the EIIG firm-level survey (Échanges In-ternationaux Intra-Groupe). The data are provided by INSEE (Institut National de laStatistique et de Etudes Economiques) and are only available for 1999. The survey wasaddressed to all French firms whose value of trade was over 1 million euros, owned by groupsthat controlled at least 50% of the equity capital of a foreign affiliate. It provides a detailedgeographical breakdown of the import and export value of French firms at product level(HS4) and their sourcing modes – outsourcing and/or intra-firm trade.

We aggregate the firm-level data at the regional level. A firm located in France might haveseveral plants in different regions. When it comes to filing the BRN or the Customs forms,the value added, sales or trade values are always allocated to the region of the headquartersof the multi-plant firm. In order to compute the regional GDP, INSEE reallocates the valueadded of multi-plant firms based on the share of employment generated by plants in eachregion. Each plant is recorded in a data set called STOJAN that has limited plant-levelinformation, mostly on its employment and its identifier. The identifier of the plant is suchthat it can be easily merged with the identifier of the firm. We use STOJAN to reallocatethe value added, sales and trade of multi-plant firms. In our sample, only 1.8% of firms aremulti-plant and multi-region. Yet these firms account for 9.8% of total employment.34 Weare now able to aggregate the statistics at the level of each of the 21 Metropolitan regions.

This database at the regional level is then combined with a data set that contains thecorrelation of the business cycles between a French region i and a partner country c. Weconsider 162 partner countries over the 1990-2006 period. The correlation of the cyclesbetween region i and country c is computed as the correlation in the annual growth rates orthe correlation of HP-filtered GDPs.

As a measure of regional GDP, we use the publicly available GDP computed by INSEEover the 1990-2006 period. We combine it with World Bank data for the GDP of countries, incurrent US dollars. While the GDP of the countries is in dollars, the French regional GDPsare in euros. We convert the GDP of the countries into euros using the EUR-USD exchange

34We have access to this data for the 1999-2004 period.

25

rate given by Eurostat. The database is completed with the total exports and imports ofthe partner countries that we take from the Direction Of Trade Statistics (DOTS).

26

B TablesTa

ble1:

French

region

s:contrib