the swiss professional journal for payment traffic … · the swiss financial center needs a...

TRANSCRIPT

In the field of tension between sanctions and their applicationInterview with Roland E. Vock, Head of the section Sanctions, SECO

FATF – Stronger focus on payments and tax crimes

Switzerland on its way to a uniform payment slip

CLEARITThe Swiss professional journal for payment trafficEdition 53 | September 2012

Interview Page 4“Then there is the interim solution, to impose sanctions.”The Embargo Act has been in force for ten years in Switzer-land. Roland E. Vock, Head of the section Sanctions in the State Secretariat for Economic Affairs (SECO), discusses past experience, current developments and challenges for public authorities and financial institutions in the field of tension between sanctions and their application.

Compliance Page 8The effects of regulations on payment processingFollowing an EU Council decision, SWIFT announced in March of 2012 the decision to discontinue its communi-cations services to Iranian financial institutions that are subject to European sanctions. What this means for the financial institutions is that their payments will simply no longer be forwarded.

Compliance Page 9The FATF now has tax crimes in its sights The intergovernmental Financial Action Task Force (FATF) was founded over 20 years ago to combat money laun-dering. Its range of activities has since been enormously expanded and it is now also focused on the combating of serious tax offences.

Standardization Page 12Switzerland on its way to a uniform payment slip The Swiss financial center is future-oriented when it comes to payments. A clear majority of customers surveyed want a uniform payment slip and the exclusive use of the IBAN. The QR code doesn’t have as many advocates, but is already supported by a majority.

Products & Services Page 14Central banks pinpoint 122 innovations worldwide The number of innovations in retail payments is astound-ing, and yet only a handful of them attain notable success. For the first time, a central bank report looks at these in-novations from around the world, categorizes products, determines trends and dares a forecast. Contactless payment means and internet payments are perceived as having great growth potential.

2 Content / CLeArIT | September 2012

Share your opinion on CLEARIT and win an

iPod nano! Fill out the online questionnaire on

www.clearit.ch/Survey until 2 October 2012.

The Swiss financial center needs a regulatory strategyThe latest Swiss financial center numbers show that the Swiss banks’ added value has receded by 0.3% between the years of 2000 and 2011 – a slight decrease – while the national economy over all has grown an average 1.7% per year. Upon close examination, it becomes evident that a relatively steep decrease has occurred since 2008. In other words, the Swiss banking market has shrunk since the beginning of the financial crisis.

During that same timeframe, regulatory activity has significantly broadened. In the case of Basel III or the too-big-to-fail regulation, it happened because of the im mediate crisis impact experienced by system-relevant institutions. In the case of regulations governing production and distri-bution of financial products, the fallout of the Lehman Brothers and Madoff cases still influence the development of regulations. In addition, the revision of the collective in-vestment schemes act has become necessary with the introduction of the Alternative Investment Fund Managers Directive (AIFMD) in the EU. These three varying examples have one thing in common: The regulations go way beyond what would actually be necessary, with the two latter also being an expression of the newly increasing protectionism within the finance sector resulting from the financial crisis. After these most recent experiences, system and investor protection are legitimate concerns, of course. However, an appropriate balance should be maintained, and the fact that a successful financial center also depends on a framework of guidelines fostering competition may not be ignored.

Among other things, this is necessary in asset manage-ment, an area with long-term potential for being developed into the third mainstay of the financial center, in addition to private banking and investment banking. Better-quality regulation and supervision will be required, in particular, if the Swiss financial center would like to advance to benchmark level in asset management. Although it isn’t investor protection that is the main focus here, it’s important to set best practices standards in such a way that only truly qualified asset management experts can offer their services. The question of regulation and supervision related

to market access has to be raised in a slightly different way. The single market as regulated by the EU – through AIFMD, the Markets in Financial Instruments Directive (MiFID) and the European Market Infrastructure Regulation (EMIR) – provides the example that equivalent regulation and supervision are a market access prerequisite for the domestic financial services providers.

The simultaneous coexistence of equivalence, highest standards, customer and system protection, and compet-itiveness emphatically prove that regulation and supervision cannot be measured by the same yardstick. At this point, we need a coordinated effort between the authorities and the private sector, creating differentiated regulation and supervision geared towards the varying requirements of the Swiss financial services providers’ business activities. If we don’t want the shrinking process mentioned above to accelerate, it’s mandatory that we act now. That’s why I welcome the initiative of the State Secretariat for Inter-national Financial Matters in the Federal Department of Finance to develop a regulating strategy in cooperation with the private sector and the corresponding authorities.

Claude-Alain MargelischCEO, Swiss Bankers Association

3edItorIAL / CLeArIT | September 2012

Share your opinion on CLEARIT and win an

iPod nano! Fill out the online questionnaire on

www.clearit.ch/Survey until 2 October 2012.

“Then there is the interim solution, to impose sanctions.”

The Embargo Act has been in force for ten years in Switzerland. Roland E. Vock, Head of the section Sanctions in the State Secretariat for Economic Affairs (SECO), discusses past experience, current de-velopments and challenges for public authorities and financial institutions in the field of tension between sanctions and their application.

CLEARIT: “New trouble for Switzerland – due to lax Iran sanctions”, read a recent headline in the Swiss Tages-Anzei-ger newspaper. As a media consumer, one gets the feeling that the number and dimensions of sanction measures in Switzerland have continuously increased in recent years. Roland E. Vock: That feeling is not misleading. Switzerland did not participate in international sanctions until 7 August 1990, when the Federal Council decided to implement sanctions against Iraq. They were interpreted as economic warfare and unsuitable means to bring about political change. In addition, the UN Security Council only imposed binding sanctions twice in its history up to 1990 – including Southern Rhodesia in the sixties and against South Africa in the seventies. The Security Council usually failed to reach agreement during the Cold War. The situation changed after the fall of the Berlin Wall and the Iraqi invasion of Kuwait. The number of sanction resolutions has risen sharply since then. The 1990s have been called the “sanctions decade”. In August 1990, the Federal Council decided to join the UN embargo against Iraq, because it did not want to permit the circumvention of the measures taken by the global community through Switzerland. This represented a fun-damental shift in the political course.

Since then, the Swiss sanction measures have gone hand in hand with those of the UN and frequently also those of the EU. Based on the Swiss Embargo Act introduced 10 years ago, there are currently 20 sanctions in effect, whereas several have already been lifted. Six sanction regulations are based on EU decrees, while 14 are based on binding UN sanctions. In three cases – Iran, Libya and Guinea-Bis-sau – the Swiss sanction measures are a combination of UN and EU decrees.

“There is no legal or political obligation to join the sanctions decreed by the EU.”

Let’s stick with the example of Iran. A bank recently ex-perienced that the Iranian Central Bank was sanctioned by the EU, but the Swiss banks were not informed, or this information could not be called up at SECO. How do you

explain this?In regard to the Iranian sanctions program, Switzerland is in a special position. As you know, Switzerland has repre-sented the interests of the USA in Tehran for more than 30 years. As a so-called protector, we depend on having good access to Iranian representatives in order to effectively carry out our mandate for the USA. Sanctions are certainly not conducive in this regard. As a member of the UN, Switzer-land has implemented all UN sanctions against Iran that are binding under international law. Beyond that, however, there is no legal or political obligation to join the sanctions decreed by the EU. The Federal Council decides on a case by case basis whether it is in Switzerland’s interest to enact further measures in accordance with the EU. That we usually partially, or even entirely, adopt the EU sanctions has to do with the fact that Switzerland’s legal and political analyses frequently match those of the EU and that we do not wish to permit any circumventing transactions through Switzerland. For these reasons, Switzerland has adopted most, but not all, EU sanctions against Iran.

In regard to the Iranian Central Bank, it is correct that it is not on our sanctions list, because Switzerland, as opposed to the EU, has not sanctioned the central bank. Banks that wish to familiarize themselves with the legal situation in the EU must consult the corresponding EU regulations.

With the sanctioning of the Iranian Central Bank, the inter-national community has explicitly targeted payment traffic.That’s right. Since the central bank was sanctioned by the USA and the EU, financial transfers to and from Iran have become more difficult than before. Transactions with the Iranian Central Bank are not forbidden in Switzerland, but are subject to a reporting or authorization requirement to SECO. Especially due to the US sanctions, financial institu-tions in Switzerland consider very carefully whether they want to maintain business relations with this central bank.

Faute de mieux What successes can you name that can be demonstrably traced back to a sanction? You are referring to the effectiveness of sanction measures. That is certainly the most interesting question that can be asked in this area. Yet, it is also the one most difficult to answer. Theoretically, sanctions should apply economic pressure to bring about a change in politics. The more com-prehensive and globally binding an embargo, the better are its chances of success. Let’s take Syria for example. There are very many unilateral sanctions there, those decreed by the EU, the US, Japan, Australia, Norway and others. Switzerland has completely adopted the EU sanctions.

4 IntervIew / CLeArIT | September 2012

Short biography Roland E. Vock heads the section Sanctions in the State Secretariat for Economic Affairs SECO. He is in charge of the implementation of international sanctions and for controlling trade in raw diamonds and also represents Switzerland at international negotiations on this topic. He has been active in the field of commercial sanctions and export controls of strategic goods since 1999.

From 1986 to 1999, he worked in the field of international development cooperation. From 1987 to 1991, he lived in La Paz, Bolivia, where he participated in various rural and urban development projects. Between 1993 and 1999, he was in charge of Switzerland’s bilateral cooperation

with numerous Eastern European and Central Asian nations.

Roland E. Vock completed his studies at the Universi-ty of Zurich, where he graduated with a licentiate in economics. He afterwards completed the Postgraduate Course on Developing Countries (NADEL) at the Swiss Federal Institute of Technology (ETH) Zurich, followed by studies abroad at Harvard University in the field of environmental economics.

Roland E. Vock was born in 1960 in Zurich. He lives near Bern with his wife and their two children.

5IntervIew / CLeArIT | September 2012

But Russia is not participating and neither is China, which makes it difficult to build economic pressure. Even if there is an internationally binding embargo, there are sanctions violations from countries that control the embargo less dili-gently or even circumvent it.

Nevertheless, what are the alternatives? You can either do nothing, criticize through diplomatic channels or go to war. None of these are very attractive political approaches and – in the case of the use of force – involve enormous risks and costs. Then there is the interim solution, to impose sanctions. In my opinion, sanctions are resorted to so fre-quently because the other options are not very attractive, and not because they are considered to be a cure-all. The imposing of sanctions also buys time for diplomatic nego-tiations. While the economic consequences of sanctions can be roughly estimated, it is extremely difficult to say what political changes can be attributed to them. There are simply too many factors at work. However, this does not mean that sanctions cannot contribute – along with other measures – to preventing governments from further violating international law or from establishing a militaris-tic nuclear program.

“The banks are fundamentally bound to Swiss law.“

It is possible that sanctions can be imposed by the UN, but are not yet applicable for Switzerland?The fact is that we fundamentally implement a UN Security Council resolution with an ordinance as quickly as possible. Out of necessity, there is a time delay, because the directive must first be written and presented for decision by the Federal Council.

How long does it take until a UN decision becomes a Swiss ordinance?Anywhere from a few days to several weeks, depending on how complex and politically controversial the matter is. It goes without saying that we do our best to keep this phase as brief as possible.

Do the banks take on any legal risks during this transi-tional period?The banks are fundamentally bound to Swiss law. As far as I know, there have never yet been problems during the transitional period. However, it is true that in practice particularly internationally active banks act in their own interest and do not necessarily wait for publication of the Swiss ordinance to take a close look at their business relationships. They closely watch the development of inter-national sanction measures in order to be able to estimate the degree to which they might be affected by EU or US sanctions, for example, before the UN acts and Switzer-land follows suit.

Generally speaking, what is the interaction between inter-national organizations and the Swiss representatives like when it comes to establishing new or removing existing sanctions? Is there a leading institution in charge of the worldwide coordination?There is no worldwide coordination of sanctions measures. Only the UN Security Council is authorized to decree globally binding sanctions. As a member of the UN, Switzerland is obligated to implement the Security Council’s decisions. In a case such as Syria, where the vetoes by Russia and China mean that no sanctions are being imposed and the EU is nevertheless unilaterally taking action, we have generally followed the EU since 1998. In this area, we maintain good contacts with the EU representatives in charge.

How good is the cooperation between SECO and the Swiss financial institutions in general? We have daily contact with banks, for one thing, because in regard to Iran there are notification and approval requirements for financial transfers. Everything over CHF 10,000 must be reported to us and everything over CHF 50,000 must be approved. We have processed well over 3,000 cases since this sanction regime was introduced on 19 January 2011. And then there are, of course, also other enquiries pertaining to implementation of sanctions. Because of the great number of enquiries and our limited personnel resources, I appreciate your understanding if it is not always possible to handle all enquiries quickly.

“By the end of the year we will publish a consolidated, machine-readable list in XML format that covers all sanction regimes on our website.“

And is there anything like an institutionalized cooperation? If you mean in the sense of regular meetings, no, there is nothing like that. The exchange – if necessary – occurs spo-radically. In the recent past we had a structured dialogue with the Swiss Bankers Association and with several banks regarding the preparation of lists with sanctioned names. By the end of the year we will publish a consolidated, ma-chine-readable list in XML format that covers all sanction regimes on our website. It will also be equipped with an in-telligent search function. This list will be updated if things change in a manner that shows all historicized updates. We are certain that this handy, customized tool will make the banks’ work easier.

How many proceedings have been opened against Swiss banks due to violations of the Embargo Act?There are naturally a whole range of such proceedings. I cannot spontaneously name the exact figure, but there have been several dozen in recent years. There have also been convictions and the imposing of penalties.

6 IntervIew / CLeArIT | September 2012

7IntervIew / CLeArIT | September 2012

The new article from the revision of the Embargo Act, which was undisputed, read:

Criminal, civil and contract liability disclaimer Anyone who in good faith takes precautions pursuant to a sanction or unilaterally provides information to the authorities which could be related to a sanction, cannot be made liable for these actions due to violation of the official, profession or trade secrecy provisions or for contract infringement.

Doesn’t SECO have more comprehensive information than the banks? Basically no. If we did, we would publish it to simplify iden-tification. However, in specific cases we can attempt to obtain additional information through our foreign represen-tatives and intelligence agencies or directly from the UN and the EU. Recently we could quickly find out the date of birth of a minister on the list through the Swiss embassy in that particular country.

Interview: Gabriel Juri, SIX Interbank Clearing [email protected]

André Gsponer, Enterprise Services [email protected]

Speaking of the Embargo Act: The Federal Council elimi-nated its revision entirely at the end of 2011 in response to strong criticism by consultation participants. This also meant that the introduction of a criminal, civil and contract liability disclaimer also became obsolete, even though this had been universally welcomed. Such a disclaimer would have been significant, especially for the banks, because it would have created greater legal certainty. Will further efforts be made in this regard? Not at the current time, though the issue is clearly justified. That is also why we took it on. However, the core of this revision lay elsewhere in a modification in the area of in-ternational administrative assistance. Because a majority could not be found in consultation, the Federal Council decided to dispense with the entire revision.

When a general becomes a babyHow shall the banks handle this shortcoming? Well, they have been able to handle things as they are up to now. However, I must say that since I have been responsible for this dossier, I can only recall two or three conversations with bank representatives that were extremely delicate. In cases involving customer names, it is a bit tricky for the bank to call us in the first place – I am aware of that. The assessment of a business transaction is less problematic. The issue can be run by us for an initial reaction, without having to disclose the name of the business partner.

But sometimes the banks make it too easy for themselves. I remember back in the time of the Yugoslavia embargo. A Parachute Corps General was on the sanctions list – let’s call him Goran Dragovic. A bank actually reported a hit with this name to us. Then I took a closer look at the report and noticed that this particular Goran Dragovic had a youth savings account. He was a one to two-year baby. I don’t mean to make light of a serious subject; my point is that the plausibility of an identity can often be checked with little effort by the bank itself. On the other hand, there are also entirely justified enquiries for which not even we have reliable information. For example, if no date of birth can be allocated to a person and perhaps the bank has had no contact with them for over 10 years. That would be extremely difficult even for us.

Share your opinion on CLEARIT and win an

iPod nano! Fill out the online questionnaire on

www.clearit.ch/Survey until 2 October 2012.

The effects of regulations on payment processing

Following an EU Council decision, SWIFT announced in March of 2012 the decision to discontinue its commu-nications services to Iranian financial institutions that are subject to European sanctions. What this means for the financial institutions is that their payments will simply no longer be forwarded.

Even if this action is unique, it doesn’t change the fact that the Banque Cantonale Vaudoise (BCV) is increasingly affected by international regulations, particularly in con-nection with their daily payment activities.

PatchworkSwitzerland has passed binding regulations through various institutions. The State Secretariat for Economic Affairs (SECO) – the armed extension of the Swiss Financial Market Supervisory Authority (FINMA) – monitors the application of the embargo regulations determined by the Federal Council. Each country passes its own laws. Financial in-stitutions processing international payments are thus confronted with a “patchwork” of regulations that have to be implemented and applied.

Implementation of regulations – a challenge unto itself Headquartered in Lausanne, the BCV is subject to Swiss law. The processes based on the ”know your customer” concept are implemented and continually provide customer service consultants with information about unusual activi-ties. Necessary actions are taken in accordance with the regulations, as determined by the compliance department.

Costly resources For a few years now, IT resources have allowed the BCV to use their processes for customer identification (on black and PEP lists) and to filter transactions that are processed through SWIFT, SIC, euroSIC, SECOM and PostFinance channels. The BCV controls them according to the SECO, FATF and OFAC (Office of Foreign Assets Control) lists, but also using proprietary lists, whose management is continu-ally being monitored.

As far as the payment flow is concerned, blocked transac-tions are being analyzed and, depending on the result, are approved and executed or are returned to the customer, or the FINMA is notified.

All this requires use of powerful software that allows the generation of complex business rules, as well as fast pro-cessing. Last year, the BCV found itself faced with the need to replace the software purchased in 2003 with a new one and adding an additional staff member responsible for rule administration and monitoring of all activities in connec-tion with filtering.

All in all, the ramifications of Swiss and international regula-tions on IT investments and staff resources are substantial. The areas affected at BCV are IT, compliance, the legal department, organization and production. The return equals zero. The only “profit” is the satisfaction of being fully compliant with the Swiss authorities and being able to operate while meeting international standards. There certainly is a price to be paid for that.

Valéry-John Racine, Jean-Jacques Maillard, Banque Cantonale [email protected], [email protected]

8 CompLIAnCe / CLeArIT | September 2012

In June of 2012, the share of filtered incoming and outgoing payments that had to be stopped and analyzed was 0.6‰. Of these transactions, 99.4% were authorized; the rest were returned to the customer or reported to FINMA.

The BCV’s comprehensive product range as a universal bank results in a large number of payments being trans-ferred abroad. Those going to European countries and North America are unproblematic – as opposed to those going to countries deemed sensitive. As a result, the BCV needs to anticipate national conditions within the countries where the correspondence banks are located. Because, while some of them are headquartered in Switzerland or within the eurozone, some are also licensed within the banking market in the USA. In that case, payments of these correspondent banks not meeting regulations – regardless of their currencies – are not forwarded, not even when the US territory is not affected by that particular payment.

Example of a false-positive case

The FATF now has tax crimes in its sights

The intergovernmental Financial Action Task Force (FATF) was founded over 20 years ago to combat money laundering. Its range of activities has since been enormously expanded and it is now also focused on the combating of serious tax offences.

The FATF began its work by publishing 40 recommen-dations for the combating of money laundering, which became the standard in 1990. These recommendations, to which special recommendations for the combating of the financing of terrorism were later added, were revised last year and the revised recommendations were published in February 2012. But these recommendations are just one side of the coin. The comments that accompany each of the recommendations (interpretative notes) contain explanatory material that is not self-evident in the recom-mendations.

Tax crimes as predicate offences for money launderingThe FATF’s naming of tax crimes as predicate offences for money laundering was without a doubt the most sensa-tional for the media and the general public. Many got the impression that every case of tax evasion must now be reported to the Money Laundering Reporting Office Swit-zerland at the Federal Department of Justice and Police. Overlooked in the process is that, in terms of “tax crime”, the FATF is only referring to serious offences in the area of tax law and leaves it up to the individual member countries to define the statutory offence. Nevertheless, in this regard the question remains regarding which due diligence is to be applied by financial institutions in order to comply with the reporting obligation for tax offences. The structure set

up in the FINMA money laundering ordinance for the pre-vention of money laundering does not seem to be easily applicable here. It is to be assumed that based on indi-cations it can be determined whether the customer of a financial intermediary deposits money in the bank that originates from a crime. The clarification of the origin of the money provides essential knowledge to the financial intermediary. If it involves tax offences, the origin of the money will generally be legal, but the money simply has not been taxed. This means that in such cases another approach will have to be chosen.

The FATF’s criticism of the institution of bearer shares is nothing new. In its Recommendation no. 10, through customer due diligence the FATF requires that a financial intermediary must know a company’s ownership and control structures. Nevertheless, the FATF makes an exception for listed companies. Where transparency is ensured through legal disclosure obligations in terms of participations, it is not necessary to identify shareholders and any existing beneficial owners.

It makes sense that the FATF covers the risk-based approach in somewhat greater detail in regard to the due diligence of financial intermediaries in its comments to Recommendation 10. The risk-based approach is actually a key element for the gradation of the financial intermedi-ary’s due diligence according to the risks associated with a customer, a transaction, etc. The abstract term, risk-based approach, is thus given meaning. At the same time, it is the opposite of the standardized approach, which would require the same due diligence for a customer with a salary account as it would for a business relationship with a politically exposed person (PEP) from a country known for corruption. The risk-based approach when handling customers and transactions places the burden on the financial intermediary and gives them appropriate leeway to decide whether a business relationship is to be entered into with a customer or whether a transaction can be conducted.

The risk-based approach is then applied precisely for business relationships to PEPs, for example, the FATF now requires, on the one hand, that politically exposed people from inside the country must be indicated as such, however, that special due diligence is only indicated if specific risks also exist, while foreign PEPs must always be considered to be customers with enhanced risk.

Stronger focus on payment trafficWhat is especially interesting in this regard is the increasing involvement of the FATF in the field of financial infra-structure, particularly in payment traffic. This tendency

9CompLIAnCe / CLeArIT | September 2012

FATFThe Financial Action Task Force (FATF) is an in-tergovernmental organization founded in 1989 in Paris by the G-7 heads of state. The decision was made based on the recognition that money launde-ring represents a substantial threat to the banking system. Eight other countries, including Switzerland, shared this recognition and are among the founding members. The original duty of the FATF was to set standards for the combating of money laundering. After the terror attacks on September 11, 2011 in New York and elsewhere, the FATF added the combating of terrorism financing to its banner. Later came the combating of the financing of proliferation and now the FATF is also assisting tax authorities in the search for untaxed money.

appeared with the expansion of the 40 recommenda-tions for the combating of the terrorism financing in 2001 and also later with the addition of the combating of the financing of proliferation (supplying of weapons of mass destruction). However, according to the current wording of Recommendation no. 7, the latter case involves the as-certaining by member states that the sanction decisions of the United Nations Security Council against specific people or companies can be efficiently implemented. The due diligence of banks in the credit business was original-ly discussed, which would have seriously impacted this business.

This is in contrast to the current Recommendation no. 16, which involves payments and which contains more or less clear instructions regarding data transmission. In its original version, it was inserted in the FATF Rulebook as Special Recommendation no. 7 for the combating of terrorism financing. Back then it involved sending the payer’s data along with cross-border payment orders. This data included name, account number, address or national identity number or customer identification number or place and date of birth. This information could be dispensed with for domestic payments if the debtor bank was able to provide the corresponding information to the creditor bank within three days. This requirement entailed significant legal and technical changes. The re-quirement was quickly implemented by FINMA’s money laundering ordinance at the time, although the details were unclear. In practice, there seemed to be no alternative but

to clarify several issues in terms of best practice. What remained particularly unclear at the time was the degree to which the requirement to name the ordering party, even for cover payments, was to be adhered to.

Learning processThe FATF has since become aware that things are somewhat more complicated in practice than anticipat-ed at the time by the prosecutors and bank regulators represented in this organization. That is why they then integrated the new Recommendation no. 16 for cover payments and serial payments to expressly clarify that the intermediaries in a payment chain must also meet the same requirements. However, this proved unwork-able in terms of the participants’ diligence operations. If everyone involved in a payment had to verify that the information about the payer (name, account number, address or national identity number or customer identifi-cation number of place and date of birth) are complete and accurate, then straight through processing would hardly be possible. Ultimately, only the debtor bank can decide whether the payer’s data is not only complete in terms of the legal requirements, but also accurate. The FATF accordingly decided that intermediaries and beneficiary banks only had to verify that the legally required payer’s data was supplied.

This was augmented in the revision of the recommen-dation in 2012, which stipulated that beneficiary data was also to be supplied. Meanwhile, only the name and

10 CompLIAnCe / CLeArIT | September 2012

11produCt & ServICeS / CLeArIT | September 2012

account number are requested if the account is to be used to conduct the transaction. Here, only the payer’s bank and the intermediary must make sure that the legally required beneficiary data has been incorporated. Only the benefi-ciary bank can know whether this data is also accurate, which is why it is placed on them to verify the identity of the beneficiary of the payment order, if they have not yet previously done so; such would be the case if the benefi-ciary is their customer.

Even in its original form, which was only intended for the payer, the recommendation already anticipated that the member states could set a threshold for payment orders beneath which no payer data would be supplied. The Swiss banks have not made use of this option, which is why FINMA removed the corresponding reference in the money laundering ordinance. In the revised recommen-dation, the relaxation of the requirement for transactions below the threshold are so narrowly defined that it will make even less sense to implement them legally and technically. Beneath the threshold, the names of both payer and beneficiary must be given and, furthermore, an account number or transaction reference number for each. The accuracy of this data need not be verified, as long as no suspicion of money laundering or terrorism financing exists, which is the case every time data from participants in a transaction crops up in the scope of a sanctions screening.

Recommendations that are to be taken seriouslySome will ask themselves why the FATF recommenda-tions, which after all are not backed by law – for which the FATF has no authorization – are being implemented more or less as they are in the member states. The FATF has created a powerful tool to see that their ideas are implemented worldwide with their country evaluations and country ratings. The member states are periodically audited in regard to their implementation of the recom-mendations according to a specific assessment method and given corresponding ratings for each recommendation (fully compliant, largely compliant, partially compliant or non-compliant). Those who do not wish to be audited by a team of national experts comprised by the FATF can be audited by the International Monetary Fund and the World Bank. The FATF theoretically has the option of placing countries that do not or insufficiently implement the rec-ommendations on a blacklist. Currently, only Iran and North Korea are in the list of nations that do not implement the recommendations, and are thus considered to be so-called non-cooperative jurisdictions for which the members of the FATF must take countermeasures.

It is quite possible that the FATF will take on additional in-frastructure sectors in the future. A great deal more data is generated by the striving to attain greater transparency and increased and more comprehensive documentation of transactions, which is being driven by the financial and

credit crises. Such data is interesting to not only regula-tors, especially if it is collected, processed, stored and constantly updated, such as at trade repositories in the derivatives sector.

Renate Schwob, Schweizerische [email protected]

Due diligence at the SECB

The Swiss Euro Clearing Bank (SECB) is a bank, according to German law, and is subject to the moni-toring of the Federal Financial Supervisory Authority (BaFin) and the Deutsche Bundesbank. By direct par-ticipation in the major EU clearing systems, the SECB provides the euroSIC participants with payment paths for cross-border EU payments and manages their EU sight deposit accounts.

Being a financial institution, the SECB is bound to adhere to and execute national and international reg-ulations and measures relative to the prevention of money laundering and the financing of terrorism. In order to follow these legal due diligence requirements, which are practically congruent with the Swiss ones, the SECB has installed company safeguards relative to correspondent banking relations and transactions. For the purposes of identification and continuous monitoring of the correspondence bank relations, the SECB uses the know-your-customer process (KYC). In addition to identifying euroSIC participants and/or SECB euro sight deposit account holders by means of qualified documentation, KYC questionnaires are sent to all account holders at regular intervals, as well as questionnaires to fight money laundering (AML ques-tionnaire) developed by the internationally renowned Wolfsberg Group.

The SECB uses the information provided by official governing sector entities (sanctions/embargo lists) as the basis for ongoing monitoring for transaction pro-cessing. To this end, the transactions are compared to the sanctions/embargo lists. If irregularities surface, additional transaction processing is executed with the involvement of the money-laundering authority rep-resentative.

Susanne Eis, Swiss Euro Clearing Bank [email protected]

11CompLIAnCe / CLeArIT | September 2012

12 StAndArdIzAtIon / CLeArIT | September 2012

Switzerland on its way to a uniform payment slip

The Swiss financial center is future-oriented when it comes to payments. A clear majority of customers surveyed want a uniform payment slip and the exclusive use of the IBAN. The QR code doesn’t have as many advocates, but is already supported by a majority.

As described in the CLEARIT article in June 2012, ”Swiss payment traffic goes European,” the Swiss financial center adapts and improves its standards and processes for credit transfers direct debits to comply with ISO 20022, largely inspired by SEPA. In that same article, various courses of action with respect to paper-based payments were described, with reference to the Swiss financial center’s decision pertaining the uniform payment slip – which at that time was still pending. This decision was made in mid-2012.

After an 18-month study, the Swiss financial center has opted for a new uniform payment slip with QR code (Quick Response Code) as part and parcel of the payment traffic migration in Switzerland (PT CH). In the wake of the decision, there were three options:• Keeping on with the current payment slips• Enhancing the existing red inpayment slip (IS) with

message field and the orange one with reference number (ISR)

• Developing a new uniform payment slip

Necessary investment in paper slipsThe reader might rightfully wonder why the Swiss financial center is investing in a new slip, especially in view of the fact that due to the appeal of new electronic payment processes such as e-billing, a reduction in paper-based payments can be expected. The answer to this question lies in the current and future regulatory requirements. These would result in inevitable major adaptations of the existing payment slips. In particular, upgrading the orange inpayment slip (ISR) and its corresponding processes

would require significant investments. If one assumes that the continued use of paper slips beyond the year 2020 is undisputed, the question is easily answered: An investment in the paper slips is unavoidable. But the financial center has also stated its goal to generate ad-ditional value beyond the costs involved. That’s why the uniform payment slip became the option of choice among the three.

The determining factors for this decision included the many advantages for the financial institutions, such as the reduction of complexity within the slip and application landscape, the reduction of maintenance and development costs, and the increase in automation. It was agreed that the path to the uniform slip could only be taken with the agreement of a significant number of customers. That’s why conducting and evaluating a customer survey was a core element of this decision-making process.

Survey profileThe qualitative customer survey was conducted anony-mously during the first quarter of 2012. 557 replies were submitted, representing a participation rate of about 25%. Businesses and organizations of all sizes and industries were included. The survey was executed by representa-tives of the financial institutions.

Characteristics and use of the uniform slipListed below are the most important elements:• Replacing of all payment slips with one uniform slip,

applicable throughout the Swiss financial center, with an appropriate transition period.

• The uniform payment slip contains the present billing and payment processes (red/orange payment slips) for manual and/or automated administration of debtors.

• The account number is used in the IBAN format exclu-sively.

• The encoding line is replaced with the QR code, which contains all relevant payment information about the

This article, as well as additional information about the migration PT CH program, is available online under www.migration-pt.ch. (Please use your smartphone to read the QR code.)

13StAndArdIzAtIon / CLeArIT | September 2012

payer, beneficiary, credit account, amount and currency, making it possible for the payer to import the informa-tion using established devices such as a scanner or smartphone.

Based on the above description, billers benefit from the following advantages:• Simplified document printing due to uniform form

layout; the QR code tolerance for error, such as recog-nizing differing positioning or damaged forms, is higher than with the encoding line using the OCR-B font.

• Completely printed slips make subsequent data entry of paper-based payment unnecessary, leading to cost savings.

• By using the QR code and by straight through process-ing, customers receive additional information on their notifications, such as about the payer or the ultimate beneficiary, which reduces the number of inquiries.

• Higher interpretation rate for damaged slips will lead to lower costs for post-processing.

• Due to a specific QR code sector providing shipping information, for instance, the biller may simplify its logistics.

• With the use of the IBAN and structured reference, it’s also possible to adopt the concept of the orange payment slip (ISR) prevalent in Switzerland and use it for billing payers in other European countries.

Core messages from the customer surveyThe survey results prove that the customers confirm the added value of the uniform payment slip with QR code and IBAN. The following core messages can be extracted from the survey results:• 62% perceive the uniform payment slip as a simplifica-

tion while 18% think the opposite• 87% support the exclusive use of the IBAN; 2% are

against it• 54% welcome the QR code; 8% have a negative attitude

toward it• 53% would use the uniform payment slip for cross-bor-

der payments (eurozone).

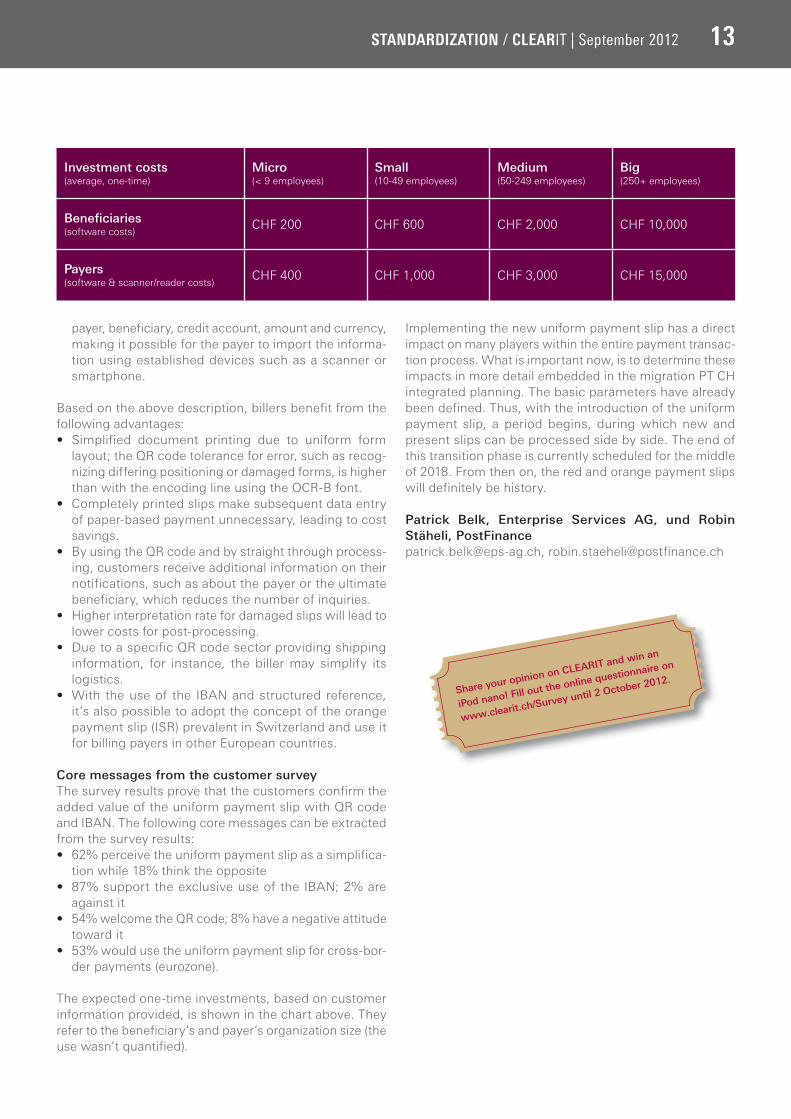

The expected one-time investments, based on customer information provided, is shown in the chart above. They refer to the beneficiary’s and payer’s organization size (the use wasn’t quantified).

Investment costs(average, one-time)

Micro(< 9 employees)

Small(10-49 employees)

Medium(50-249 employees)

Big(250+ employees)

Benefi ciaries(software costs)

CHF 200 CHF 600 CHF 2,000 CHF 10,000

Payers(software & scanner/reader costs)

CHF 400 CHF 1,000 CHF 3,000 CHF 15,000

Implementing the new uniform payment slip has a direct impact on many players within the entire payment transac-tion process. What is important now, is to determine these impacts in more detail embedded in the migration PT CH integrated planning. The basic parameters have already been defined. Thus, with the introduction of the uniform payment slip, a period begins, during which new and present slips can be processed side by side. The end of this transition phase is currently scheduled for the middle of 2018. From then on, the red and orange payment slips will definitely be history.

Patrick Belk, Enterprise Services AG, und Robin Stäheli, [email protected], [email protected]

Share your opinion on CLEARIT and win an

iPod nano! Fill out the online questionnaire on

www.clearit.ch/Survey until 2 October 2012.

14 produCtS & ServICeS / CLeArIT | September 2012

Central banks pinpoint 122 innovations worldwide

The number of innovations in retail payments is as-tounding, and yet only a handful of them attain notable success. For the first time, a central bank report looks at these innovations from around the world, categoriz-es products, determines trends and dares a forecast. Contactless payment means and internet payments are perceived as having great growth potential.

As a result of technological progress and regulatory in-terventions, there has been an upsurge in retail payment innovations over the past ten years. One CPSS working group analyzed 122 of these from 30 different countries (see box) in the areas of card, internet and mobile payments, Electronic Bill Presentment and Payment (EBPP), and in-frastructure and security.

Trends and outlookThe analysis resulted in five central insights:• The market is very dynamic worldwide, but only a

handful of innovations are truly successful. • Even though many similar innovative payment products

can be found in numerous countries, most of these can only be used nationally.

• Many innovations are intended to speed up payment processing.

• In various regions of the world, the integration of people without access to financial institutions is the primary motivation behind payments innovations.

• Pertaining to retail payments, the importance of non-banks has increased markedly over the past few years.

Paying contaclessly – one of the most promising innovations

15produCtS & ServICeS / CLeArIT | September 2012

CPSS

The Committee on Payments and Settlement Systems (CPSS) at the Bank for International Settlements in Basel has recently published a report about innova-tions in retail payments (www.bis.org/publ/cpss102.htm). The CPSS consists of representatives from 24 central banks and sets standards for payment and securities settlement systems, as well as central coun-terparties and trade repositories. In this context, it oversees and analyzes relevant developments, including those in retail payments.

Based on the resulting inventory, the report dares a prognosis on potential developments in retail payments over the coming years. First, the thus far clearly defined line between various payment instruments could be blurred increasingly. A contactless credit card payment, for example, can be made at a point of sale using a key ring or a mobile phone, without having to physically present the credit card. Second, contactless payment methods are expected to have great growth potential because of their speed and convenience. Third, with the growing internet trade, the demand for additional payment instruments will most likely increase, since today’s internet payment options are to some extent lagging behind user requirements in the areas of security and efficiency. Fourth, globally operating payment service providers can implement in-novations internationally and quickly realize economies of scale due to their global transaction processing infrastruc-ture. Fifth, certain innovations could revolutionize retail payments in countries with a less developed payment in-frastructure. One such example is M-Pesa, an innovative payment method using the mobile phone which became in a short time the dominant payment instrument for all kinds of retail payments in Kenya. The same innovations may however remain insignificant in countries with an advanced infrastructure. Sixth, it is assumed that in spite of similar innovations around the globe, regional differ-ences in retail payments will remain.

Innovations in SwitzerlandOver the past years, there have been numerous develop-ments in retail payments in Switzerland, too. An inventory of national innovations shows that PostFinance has played a role of some importance. Its national presence and customer base, as well as the processing capabilities of its own existing infrastructures, might support the launch of innovations. Typically, cooperation between various in-stitutions is required for the successful introduction of innovative developments within the banking sector, which may be a significant barrier. In addition, there were global innovations implemented in Switzerland, such as contact-less payment with payment cards by international card companies or prepaid cards for worldwide use. So far many innovations have had limited impact on customers’ payment behavior. Since Switzerland is a country with a well-developed and efficient payment infrastructure, with a large part of the population having access to a bank account and to electronic payment traffic, it seems unlikely that a development similar to that of the sweeping prolif-eration of the M-Pesa in Kenya might take place. But there is still room for innovative solutions, especially for those that can be processed via the established infrastructures.

Ramifications for central banksThe central banks are well advised to follow very closely the relevant developments in retail payments. They have to consider the following questions, for example: (I) Whether and to what extent they should contribute to finding new

solutions for standardization and interoperability issues in retail payments; (II) Which effects certain innova-tions would have on their own services in the areas of payment systems and cash, for example; Or (III) whether their arrangements for retail payment monitoring are still adequate.

David Maurer, Swiss National Bank [email protected]

Share your opinion on CLEARIT and win an

iPod nano! Fill out the online questionnaire on

www.clearit.ch/Survey until 2 October 2012.

PublisherSIX Interbank Clearing LtdHardturmstrasse 201CH-8021 Zurich

Ordering/[email protected]

EditionEdition 53 – September 2012Published regularly, also online at www.CLEARIT.ch. Circu-lation German (1300 copies), French (400 copies) and English (available in electronic format only on www.CLEARIT.ch).

CouncilPatrick Bürki, PostFinance, Boris Brunner, UBS AG, SusanneEis, SECB, Martin Frick, SIX Interbank Clearing Ltd, Andreas Galle, SIX Interbank Clearing Ltd, André Gsponer (Leiter), Enterprise Services AG, Gabriel Juri, SIX Interbank Clearing Ltd, Roger Mettier, Credit Suisse AG, Jean-Jacques Maillard, BCV, Silvio Schumacher, SNB

Editorial TeamAndré Gsponer, Enterprise Services AG, Andreas Galle,Gabriel Juri (Leiter) und Christian Schwinghammer, SIXInterbank Clearing Ltd

ImpressumTranslationFrench: Word + Image, English: HTS

LayoutFelber, Kristofori Group, Advertising agency

PrinterBinkert Druck AG, Laufenburg

ContactSIX Interbank Clearing LtdT +41 58 399 4747

Additional information about the Swiss payment traffic systems canbe found on the Internet at www.six-interbank-clearing.com

Share your opinion on CLEARIT and win an iPod nano!

Fill out the online questionnaire on www.clearit.ch/Survey until

2 October 2012.

You can also use this QR code with your smartphone or tablet

PC to access the survey form. Don’t forget to download a

freely available QR code app for scanning!