the role of employee stock ownership plans in … · the role of employee stock ownership plans in...

TRANSCRIPT

The Role of Employee Stock OwnershipPlans in Compensation Philosophy andExecutive Compensation Arrangements

James F. Reda*

Employee stock ownershipplans, or ESOPs, have existedfor more than 60 years as a toolfor spreading all or part of theownership of corporationsamong its workers. ESOPs atpublicly traded companies pro-liferated in the mid-1980s as ananti-takeover defense and havereceived new interest for theannual Say on Pay votes.

What e�ect, if any, does anESOP have on a company'scompensation philosophy andexecutive compensation plansand programs? An ESOP plancan be viewed in one of threeways: (1) to concentrate share-holder vote with management,which is particularly importantfor an anti-takeover defense, (2)to provide �nancing the com-pany, which is helpful to transferownership and (3) provide a

pension for employees, whichcan also be integrated with ade�ned contribution plan suchas a 401(k) plan.

ESOP plans were introducedin the mid-1950s as an e�cientform of employee stockownership. They came underthe jurisdiction of ERISA in1974 and have existed in theirpresent form ever since. Al-though these plans do havesome very real limitations, theycan also provide employeeswith a substantial motivation tosave for their retirements.

Our �rm recently conductedresearch in order to determinewhether or not an ESOP mate-rially alters compensation phi-losophy and executive compen-sation levels at publ iccompanies at the executive

level. A well developed compen-sation philosophy is key for asuccessful company. It startswith a thesis as stated in acompensation program objec-tive and is underpinned withinternal characteristics, peergroup comparisons, pay posi-tioning strategy and alignmentwith the business plan. For pub-lic companies, the compensa-tion philosophy is described inthe Compensation Discussionand Analysis (“CD&A”) sectionin their proxy statements.

The answer is that, at the ex-ecutive level, ESOPs have virtu-ally no e�ect on either 1) com-pensation philosophy or 2)executive compensation ar-rangements at U.S. publiclytraded companies.

WHAT IS AN ESOP?

*JAMES F. REDA works with both public and private organizations in planning, creating, and implementing incentiveprograms. He also advises companies on incentive strategy, including long- and short-term senior executive employment ar-rangements, change-in-control metrics, business combinations, shareholder rights, and corporate governance issues. Mr. Reda isa recognized expert in the area of integrating incentive and corporate strategies. He has more than 27 years of experiencespeci�cally in the area of senior executive compensation. Prior to forming his own �rm in 2004 (which was acquired by Arthur J.Gallagher & Co. in 2011), Mr. Reda worked at three major executive compensation consulting �rms.

Journal of Compensation and Bene�ts E March/April 2015© 2015 Thomson Reuters

34

Figure 1. Overview of an ESOP

ESOP plans are the only typeof either retirement or employeestock purchase plans that holdseither company stock or cashin a separate trust, where em-ployees are the bene�ciariesand stock is placed in theirnames in separate accounts.They are de�ned contributionplans, but di�er from othertypes of de�ned contributionplans in that they can only beestablished by C or SubchapterS corporations (the latter are byfar the most common type ofESOP owner). No other type ofbusiness entity may use them,such as partnerships, profes-sional corporations, or soleproprietorships.

To create an ESOP plan, theemployer forms an ESOP com-mittee, usually consisting ofowners and key managementmembers, and perhaps somekey employees or a represen-tat ive for rank-and-�leemployees. The committeemakes decisions about how the

plan will be funded and oper-ated, and appoints a trustee torun the trust according to theirspeci�cations.

ESOP plans are also uniquein that they are typically fundedsolely by employer contribu-tions; although employee contri-butions are allowed, they areseldom required for this type ofplan. The employer makes tax-deductible contributions into theemployee accounts within thetrust each year according to apreset formula, which is typi-cally calculated according tosome combination of employeetenure and compensation on anindividual basis.

ESOPs are the only retire-ment plans allowed by law toborrow money; thus they canbe attractive to company own-ers and managers as instru-ments of corporate �nance andsuccession.

An ESOP formed using aloan, cal led a “leveraged

ESOP,” can provide a tax-advantaged means for the com-pany to raise capital. Accordingto a pro-ESOP organization, atleast 75 percent of ESOPs are,or were at some time,leveraged. In addition, ESOPscan be attractive instruments ofcorporate succession, allowinga retiring shareholder to diver-sify his or her company of stockwhile deferring capital gainstaxes inde�nitely.

Company insiders face ad-ditional con�icts of interest inconnection with an ESOP's pur-chase of company stock, whichmost often features companyinsiders as sellers, and in con-nection with decisions abouthow to vote the shares of stockheld by the ESOP but not yetal located to part ic ipants'accounts. In a leveraged ESOP,such unallocated shares oftenfar outnumber allocated shares,for many years after the lever-aged transaction. This can bevery helpful in providing votes

Role of Employee Stock Ownership Plans in Compensation Philosophy

Journal of Compensation and Bene�ts E March/April 2015© 2015 Thomson Reuters

35

for maintaining control in proxy�ghts as well as Say of Payvotes.

The total annual deductiblecontribution cannot exceed 25%of the total pay (salary andbonus) of all plan participantsfor a calendar year. For pur-poses of this allocation, totalpay is limited by the IRS, aswith 401(k) plans (the limit in2015 is $265,000). Thus, themaximum amount allocated tothe highest paid employee canonly be $66,250 in 2015 (25%times $265,000).

Employers typically fund theplan with shares of their ownstock that have been valued byan independent appraiser, butmay make cash contributionsas well, which is typically usedto fund the repurchase ofshares from employees whenthey retire. Long-term Incentiveawards (at grant date value) arenot considered pay for pur-poses of determining the ESOPallocation. Therefore, the e�ecton total pay, including LTI isless for senior executives.

WHO USES ESOPS?

There are approximately11,500 ESOPs in place in theU.S., covering approximately13million employees. According tothe National Center for Em-ployee Ownership, only 3% ofall ESOPs are in public compa-nies, and few are integral partsof corporate culture. In contrast,stock option, or other equitycompensation, plans are usedprimarily in public �rms as anemployee bene�t and in rapidlygrowing private companies.

A previous study on broad-based compensation at publiccompanies with ESOPs com-pared to comparable non-ESOPcompanies has concluded thatlarge ESOPs with employeeshare ownership greater than5% seem to have more or lessneutral e�ects on employeecompensation.1 However, sinceESOP contributions must be al-located at the same percentageacross the company, the e�ectwill be higher for lower-levelemployees.

In this article, we are measur-ing the e�ects of an ESOP on

executive compensation at pub-lic companies, speci�cally thatof the Chief Executive O�cer.However, both public compa-nies and private companieshave the same limitation on theamount allocated to each em-ployee, which is in general thelesser of (i) 25% times total payand (ii) $62,250 in 2015 (25%times IRS limit of $265,000).Thus, we expect the e�ect ofan ESOP to be similar at bothpublic and private companies.

ESOPS ANDCOMPENSATIONPHILOSOPHY

Simply put, a compensationphilosophy consists of the fol-lowing �ve components:

1. Compensation programobjectives.

2. Internal vs. external payequity.

3. Peer group comparisons.

4. Pay positioning strategy.

5. Performance alignmentwith business plan.

Journal of Compensation and Bene�ts

Journal of Compensation and Bene�ts E March/April 2015© 2015 Thomson Reuters

36

Figure 2. Components of a Compensation Philosophy

Most stated compensationphilosophies are really compen-sation program objectives, or astarting point in stating the realcompensation philosophy.

The compensation programobjectives are at the core of thecompensation philosophy, andset the stage for the other fourcomponents, as follows:

E Internal vs. External PayEquity. At some compa-nies, employees are moreconcerned with how theirpay stacks up against oth-ers within the organization,while at other companiesthere is more concern withhow pay stacks up againstother organizations. Ingeneral, a company shouldnot rely primarily on peergroup comparisons in set-ting pay.

At best, base salary levelsshould be compared

against a broad-basedpeer group, but shouldonly be used as a generalguide for short- and long-term incentive opportunityamounts.

E Peer Group Comparisons.Peer groups are used ba-sically for two purposes.First, they are used to setthe base salary, annualbonus, long-term incentiveand other compensationand bene�ts such ashealth and welfare plansand other compensationand bene�t plans (“Com-pensation Peer Group”).Second, they may be usedto measure the company's�nancial success com-pared against the peergroup (“Performance PeerGroup”).

E Developing a Pay Position-ing Strategy. The purpose

of a pay positioning strat-egy is to increase thecompany's pro�tability.You don't want to under-compensate employees asthey will leave the com-pany due to low pay, andyou do not want to overcompensate employeesresult ing in corporatewaste. There is a relation-ship between turnover rateand competitive marketpositioning.

E Alignment with the Busi-ness Plan. Because incen-tive compensation com-prises the bulk ofexecutive pay packages atpublicly-traded companies,boards of directors andsenior management arecontinually searching forthe right performancemeasures to balance re-wards with both �nancialand operational perfor-

Role of Employee Stock Ownership Plans in Compensation Philosophy

Journal of Compensation and Bene�ts E March/April 2015© 2015 Thomson Reuters

37

mance as well as non-�nancial and individualperformance. Once com-panies get beyond the dif-�culties of designing exec-ut ive programs thatadequately balance payversus performance, theynow have the added pres-sure of clearly explainingtheir pay-for-performanceformula to investors.

Public companies are re-quired to include a CD&A intheir annual proxy statement,which is where these compa-nies set forth a description oftheir compensation philosophyand articulate details about theirpolicies and procedures, suchas how the company hassought to al ign pay withperformance.

If ESOPs were an importantcomponent of the compensationphilosophy at the public compa-nies that have them, we wouldexpect to �nd them covered insu�cient detail within theCD&A. We reviewed the CD&Aof 32 public ESOP companies.Of these 32 companies, 20made no mention of the ESOPat all. Eleven mentioned theESOP only very brie�y. Onlyone of these 32 companiesdescribed their ESOP in detailand emphasized its signi�cance,stating that “Our principal re-tirement savings vehicle is ourEmployee Stock OwnershipPlan (the “ESOP”). Since our

initial public o�ering in 1993,the ESOP has been a signi�cantsource of retirement savings forall our employees, including ournamed executive o�cers.”

ESOPS AND EXECUTIVECOMPENSATIONARRANGEMENTS

In order to compare compen-sation arrangements of ESOPvs. Non-ESOP public compa-nies, we conducted an analysisusing the methodology de-scribed below:

E We reviewed a list ob-tained from the NCEO of217 public companies withEmployee Stock Owner-ship Plans and EmployeeStock Ownership through401-K plans, and sorted itaccording to their GICSclassi�cation. We then se-lected the �ve most prev-alent industries for a totalpopulation of 115 compa-nies (“ESOP Companies”).

E The �ve most prevalentindustries were: Banks (32— GICS: 4010), CapitalGoods (23 companies-GICS: 2010), Utilities (28companies-GICS: 5510),Materials (17 companies-GICS: 1510), and 15Health Care Equipment &Services (15 companies-GICS: 3510).

E We develop peer groupsfor these �ve industries

based primarily on their�scal year 2013 revenue(total assets in the case ofBanks), and ful l t imeemployees. Peer groupcompanies in the �ve in-dustries add up to 95companies (“Non-ESOPCompanies”).

E We pulled compensationinformation for the CEOfrom the most recentproxy �ling (correspondingto FY 2013 compensa-tion), for the ESOP Com-panies groups and theircorresponding Non-ESOPCompanies peer groupsand compared the di�er-ent elements of compen-sation (Base Salary, Tar-get Bonus and Long-termIncentive average of thelast three years).

We observed that compensa-tion arrangements are very sim-ilar across the �ve industries,and did not �nd any materialdi�erences between the ESOPand Non-ESOP groups. Somedi�erences in pay levels wereobserved in Banks and theHealth Care Equipment andServices industries.

Pay Levels

Average di�erential of the �veindustries is immaterial, withNon-ESOP Companies levelsonly 2.06% below ESOPCompanies. Pay levels forBanks is 27.41% higher for

Journal of Compensation and Bene�ts

Journal of Compensation and Bene�ts E March/April 2015© 2015 Thomson Reuters

38

ESOP Companies, and 27.35%lower in the case of Health CareEquipment and Services

companies. Pay di�erences forthe other three industries range

from -9.38% to 3.48%, asshown in Figure 3.

Figure 3. Pay Di�erentials: ESOP vs. Non-ESOP

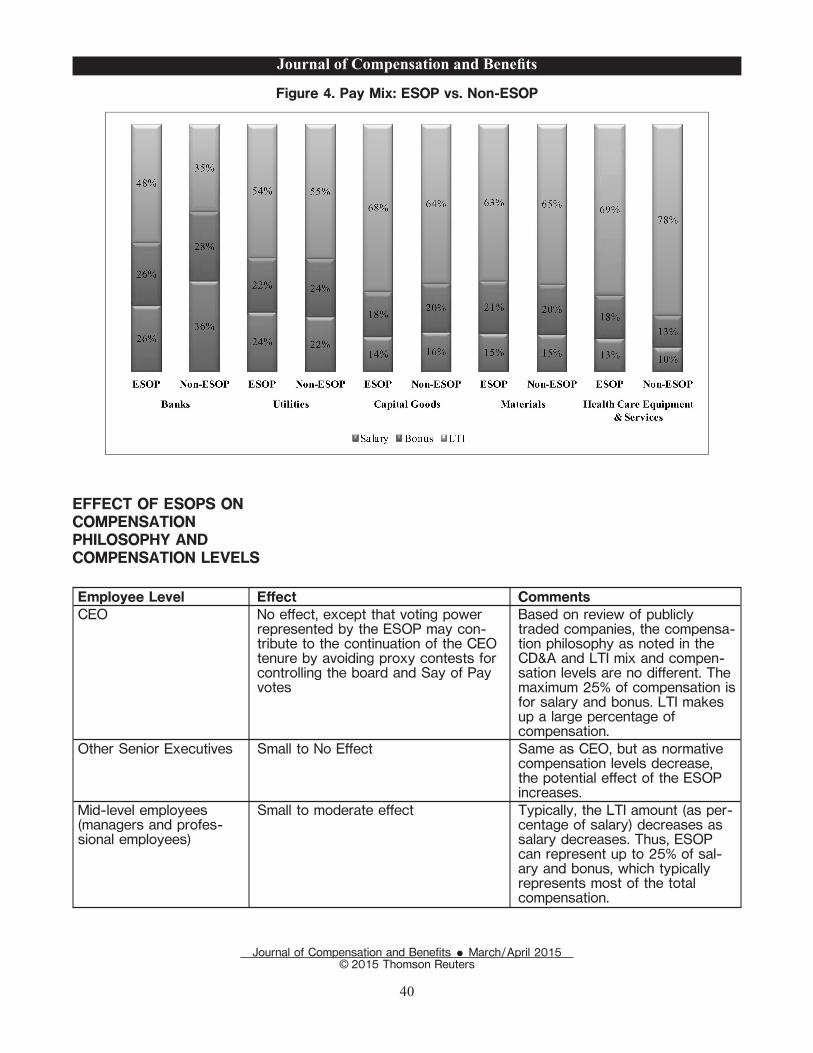

Pay Mix

Very similar pay mix schemeswere observed for the �ve in-

dustries as shown Figure 4,which illustrates the weights as-signed to the di�erent compo-

nents of compensation (i.e.Base Salary, Annual Bonus andLon-term Incentive).

Role of Employee Stock Ownership Plans in Compensation Philosophy

Journal of Compensation and Bene�ts E March/April 2015© 2015 Thomson Reuters

39

Figure 4. Pay Mix: ESOP vs. Non-ESOP

EFFECT OF ESOPS ONCOMPENSATIONPHILOSOPHY ANDCOMPENSATION LEVELS

Employee Level E�ect CommentsCEO No e�ect, except that voting power

represented by the ESOP may con-tribute to the continuation of the CEOtenure by avoiding proxy contests forcontrolling the board and Say of Payvotes

Based on review of publiclytraded companies, the compensa-tion philosophy as noted in theCD&A and LTI mix and compen-sation levels are no di�erent. Themaximum 25% of compensation isfor salary and bonus. LTI makesup a large percentage ofcompensation.

Other Senior Executives Small to No E�ect Same as CEO, but as normativecompensation levels decrease,the potential e�ect of the ESOPincreases.

Mid-level employees(managers and profes-sional employees)

Small to moderate e�ect Typically, the LTI amount (as per-centage of salary) decreases assalary decreases. Thus, ESOPcan represent up to 25% of sal-ary and bonus, which typicallyrepresents most of the totalcompensation.

Journal of Compensation and Bene�ts

Journal of Compensation and Bene�ts E March/April 2015© 2015 Thomson Reuters

40

Employee Level E�ect CommentsOther employees, typi-cally non-exempt em-ployees

Moderate to signi�cant e�ect ESOPs bene�t the lower levels ofemployees the most for reasonslisted above

CONCLUSION

The presence of an ESOPdoes not materially alter eithercompensation philosophy orcompensation arrangements atthe senior executive level. Forthose below the executive level,ESOPs can make up a substan-tial portion of compensation,particularly at the lower levelsof the Company. ESOPs canalso be a very large portion of

retirement income. ESOPs areencouraged by favorable U.S.tax treatment at both the com-pany and the employee level.Most publicly traded companieswho use ESOPs use them as away to concentrate manage-ment control. There are someexamples of ESOPs that controla majority of the company, butmost ESOPs provide a minorityownership interest.

NOTES:

1“Employee Capitalism or Corpo-rate Socialism? Broad-Based Em-ployee Stock Ownership,” E. Han Kimof the University of Michigan and PageOuimet of the University of North Car-olina, paper for American Finance As-sociation 2010 Annual Conference.Available at http://papers.ssrn.com/sol3/papers.cfm?abstract�id=1107974.

Role of Employee Stock Ownership Plans in Compensation Philosophy

Journal of Compensation and Bene�ts E March/April 2015© 2015 Thomson Reuters

41