the philippine it-bpm industry outlook & prospects · growth projections by 3% ... bpo...

TRANSCRIPT

The PhilippineIT-BPM IndustryOutlook & Prospects

Voice – Based Services Suppliers Homegrown Suppliers

Banking, Financial Services and Insurance IT and Software Services

NASSCOM’S Top BPOs Shared Service Centers / Captives

Who Are With Us

Maintenance, Repair, Overhaul Services

Clinical Research Outsourcing

HR Outsourcing Legal Process Outsourcing

Engineering Services OutsourcingCreative Services Outsourcing

Medical Services Outsourcing

Who Are With Us

O n e M i l li o n

3

Philippine IT-BPM industry size

2006–2014; US$ billionx% YoY Growth

1Philippines IT-BPM market as percentage of global offshore services market, in revenue termsSources: BPAP, ACPI, CCAP, GDAP, HIMOAP, PSIA

# FTEs

(~‘000) 236 371 424 527

3.44.5

6.17.1

8.9

11.0

13.2

16.1

18.9

2006 2007 2008 2009 2010 2011 2012 2013 2014

34%17%

25%

24%

Copyright ©2014: BPAP. All rights reserved.

19%

298 640 777

The Philippine IT-BPM 2014 Performance

31%45%

22%

917

4

1071

19%

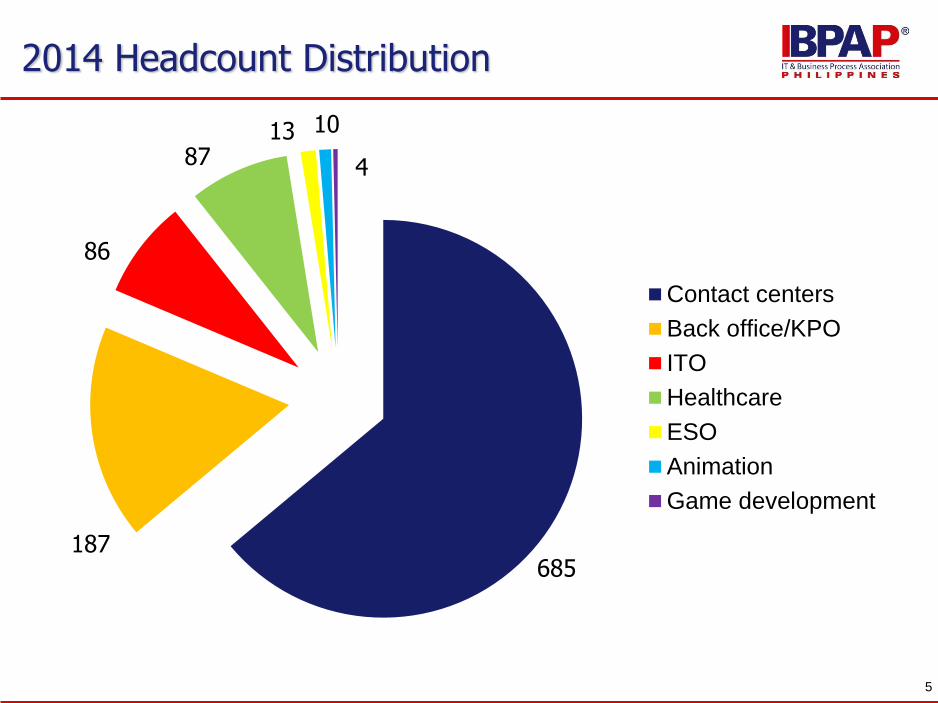

2014 Headcount Distribution

Contact centers

Back office/KPO

ITO

Healthcare

ESO

Animation

Game development

5

685187

86

8713 10

4

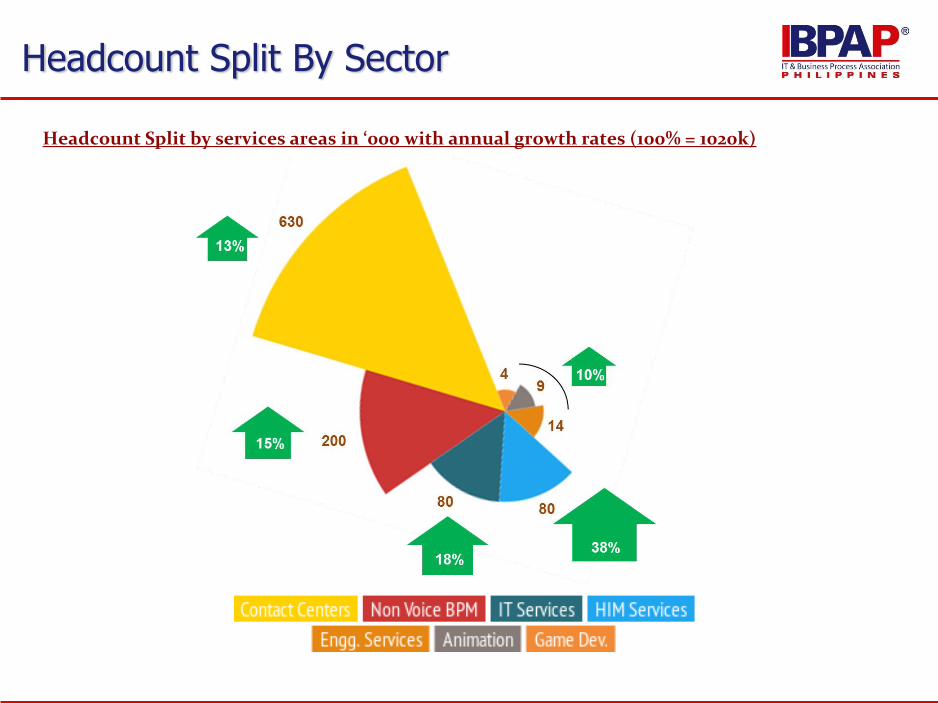

Headcount Split by services areas in ‘000 with annual growth rates (100% = 1020k)

Headcount Split By Sector

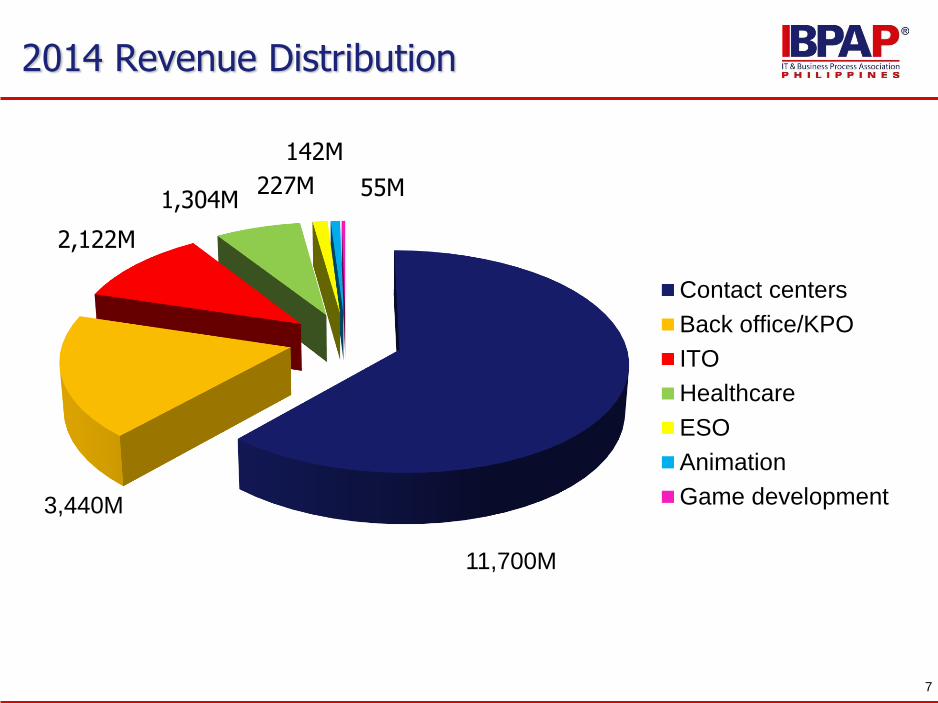

2014 Revenue Distribution

Contact centers

Back office/KPO

ITO

Healthcare

ESO

Animation

Game development

7

11,700M

3,440M

2,122M

1,304M227M

142M

55M

77% 9%

9%

5%

IBPAP, Tholons Analysis

Revenue Contribution by Regions (%, 100% = USD 18.4 BN)

Key Global Markets

9

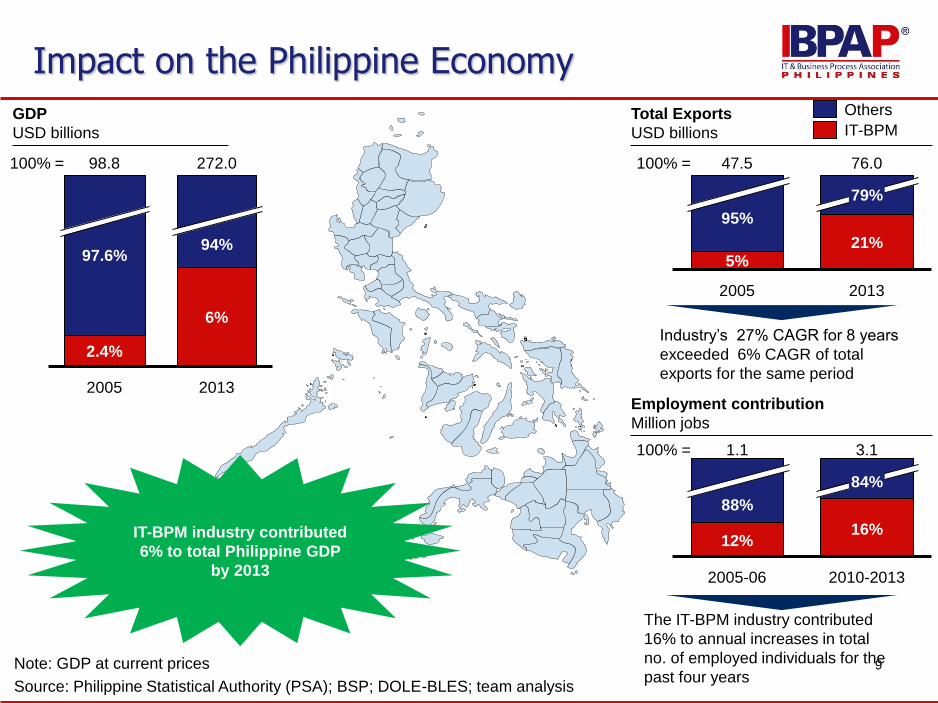

Impact on the Philippine Economy

Note: GDP at current prices

Source: Philippine Statistical Authority (PSA); BSP; DOLE-BLES; team analysis

Total Exports

USD billions

Employment contribution

Million jobs

97.6%

2.4%

98.8

2005

94%

6%

272.0

2013

100% =

95%

5%

47.5

2005

79%

21%

76.0

2013

100% =

GDP

USD billions

IT-BPM industry contributed

6% to total Philippine GDP

by 2013

Industry’s 27% CAGR for 8 years

exceeded 6% CAGR of total

exports for the same period

The IT-BPM industry contributed

16% to annual increases in total

no. of employed individuals for the

past four years

88%

12%

1.1

2005-06

84%

16%

3.1

2010-2013

100% =

Others

IT-BPM

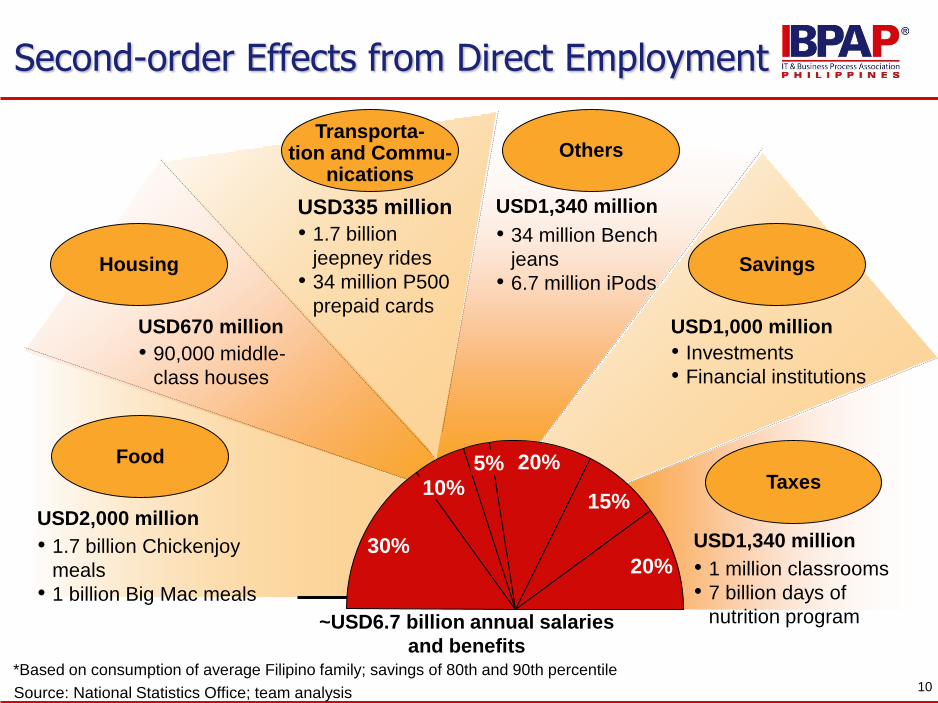

*Based on consumption of average Filipino family; savings of 80th and 90th percentile

Source: National Statistics Office; team analysis

~USD6.7 billion annual salaries

and benefits

Housing Savings

Others

• 34 million Bench

jeans

• 6.7 million iPods

USD1,340 million

• Investments

• Financial institutions

USD1,000 million

• 90,000 middle-

class houses

USD670 million

Food

• 1.7 billion Chickenjoy

meals

• 1 billion Big Mac meals

USD2,000 million

Taxes

USD1,340 million

• 1 million classrooms

• 7 billion days of

nutrition program

• 1.7 billion

jeepney rides

• 34 million P500

prepaid cards

USD335 million

Second-order Effects from Direct Employment

Transporta-tion and Commu-

nications

30%

10%5% 20%

15%

20%

10

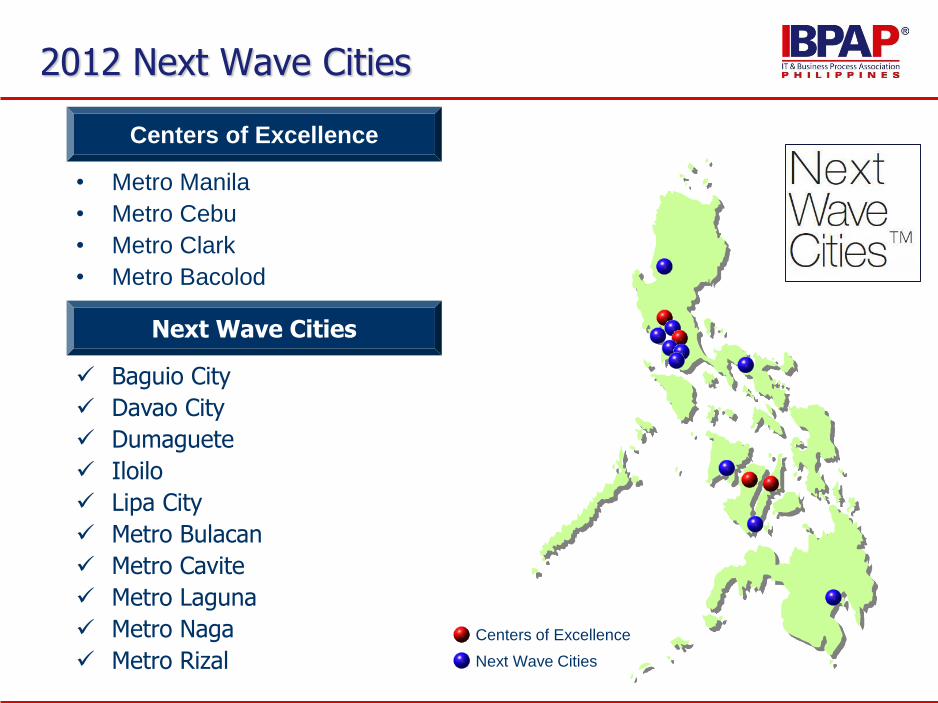

Centers of Excellence

• Metro Manila

• Metro Cebu

• Metro Clark

• Metro Bacolod

Next Wave Cities

Baguio City

Davao City

Dumaguete

Iloilo

Lipa City

Metro Bulacan

Metro Cavite

Metro Laguna

Metro Naga

Metro Rizal Next Wave Cities

Centers of Excellence

2012 Next Wave Cities

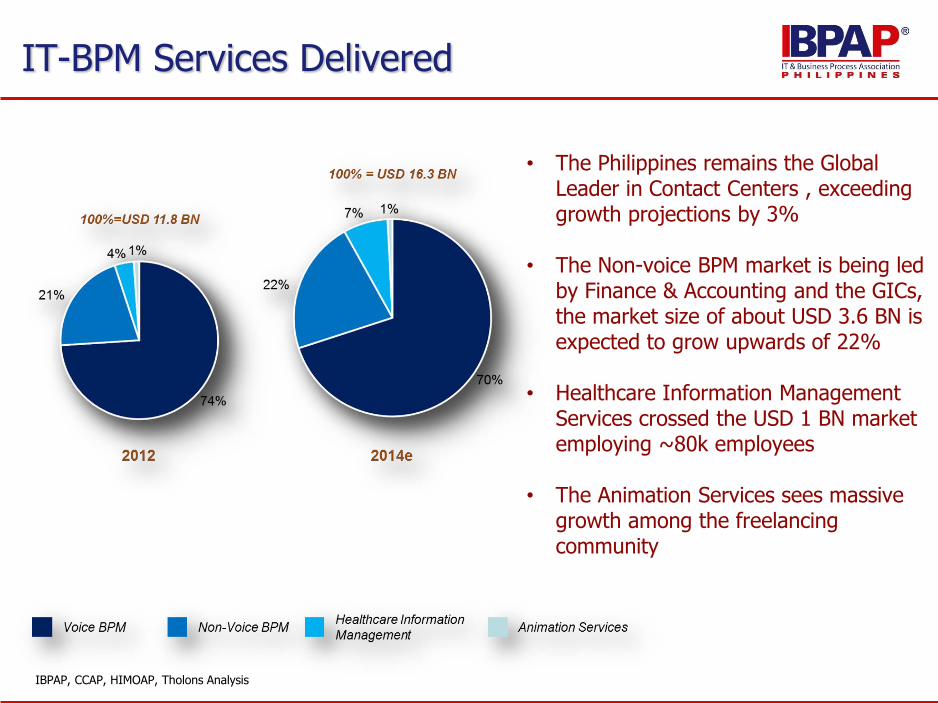

• The Philippines remains the Global Leader in Contact Centers , exceeding growth projections by 3%

• The Non-voice BPM market is being led by Finance & Accounting and the GICs, the market size of about USD 3.6 BN is expected to grow upwards of 22%

• Healthcare Information Management Services crossed the USD 1 BN market employing ~80k employees

• The Animation Services sees massive growth among the freelancing community

IBPAP, CCAP, HIMOAP, Tholons Analysis

IT-BPM Services Delivered

Contact Centers

Philippines

in the

Headcount Growth

14

Contact Center Service Offerings

15

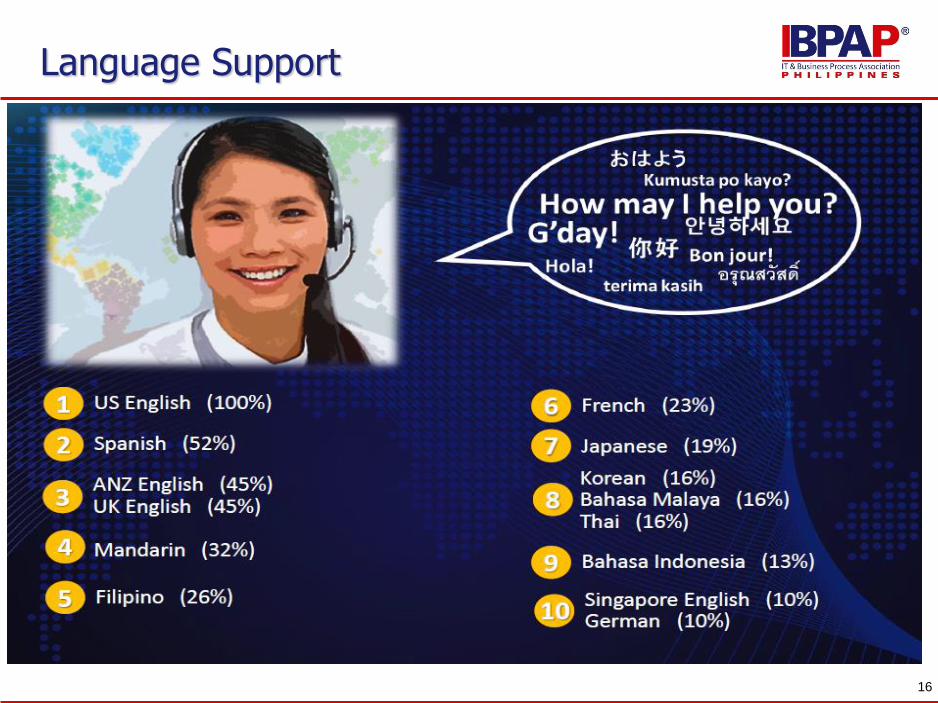

Language Support

16

GIC landscape

Philippines

in the

More than 40 of the 2014 Fortune 1000 and other

large global companies have a Global In-House Center (GIC or

“Captive”) in the Philippines

GICs in the Philippines

- Increasing leverage on Manila to meet shared services and back-office needs of the APAC region

- GICs have built sizeable scale in the Philippines and have been driving the growth of non-voice and complex services in the country

- Pressure to grow rapidly by taking on new activities or entirely new lines of business not originally planned

- Lack of multilingual skills (Korean, Japanese)

- Scalability challenges as companies aspire to deliver more non-voice services

GICs 2014: Highs and Lows

Largest GICs in the Philippines

Company Services

J.P. Morgan Chase Voice (inbound and outbound), banking and financial services

HSBC Global Services Center Customer service, banking and financial services

HP ADM/IT support

Shell SSC Financial services, HR, customer service

Manulife BPS F&A, HR, IT, Healthcare, Marketing and sales, Analytics, Underwriting, Actuarial, Legal

Maersk Non-voice, KPO, logistics

DKS Financial analysis and reporting

SC Reservation (Intercontinental Group) Inbound hotel reservation

Chevron Finance, HR, IT, Procurement

Citigroup Customer services, HR, IT, banking and financial services

ANZ Global ServicesAccounts payable, Back-office, HR, IT, Property services, Sourcing

AIG Shared ServicesCustomer contact, Legal, F&A, HR, Logistics, IT Support and software dev. 21

industry

challenges

22

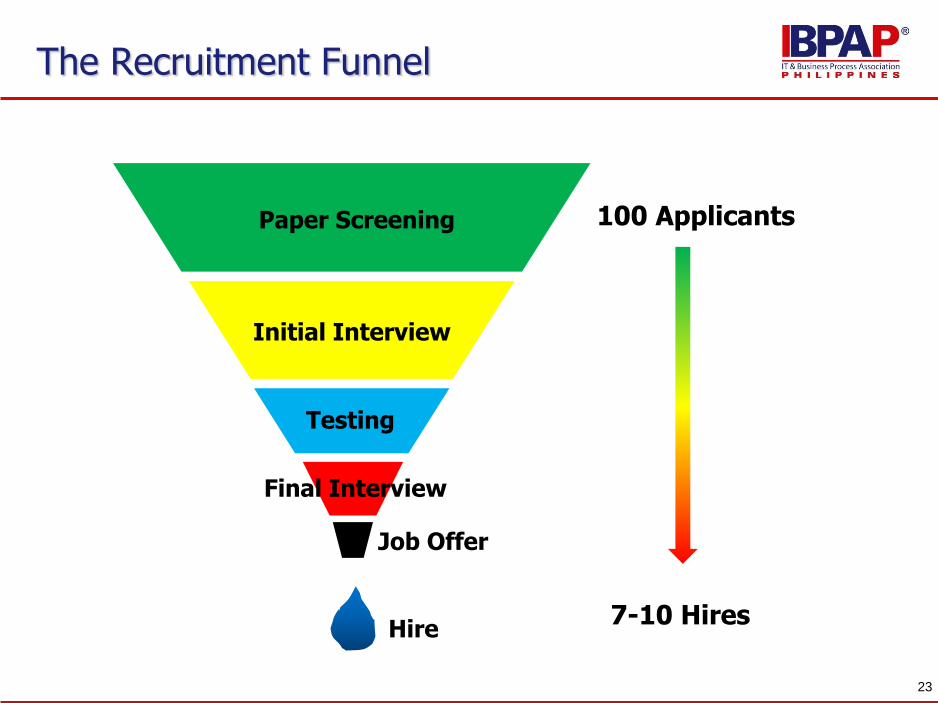

Paper Screening

Initial Interview

Testing

Final Interview

Job Offer

Hire

100 Applicants

7-10 Hires

The Recruitment Funnel

23

• Basic Skills• Learning Ability (Verbal and Numerical)• English Proficiency• Perceptual Speed and Accuracy• Computer Literacy

• Behavioral (Service Orientation)• Communication• Learning Orientation• Courtesy• Empathy• Reliability• Responsiveness

• Conducted across 3,000 agents and 20,000 students

Global Competitiveness Assessment Test (GCAT)

24

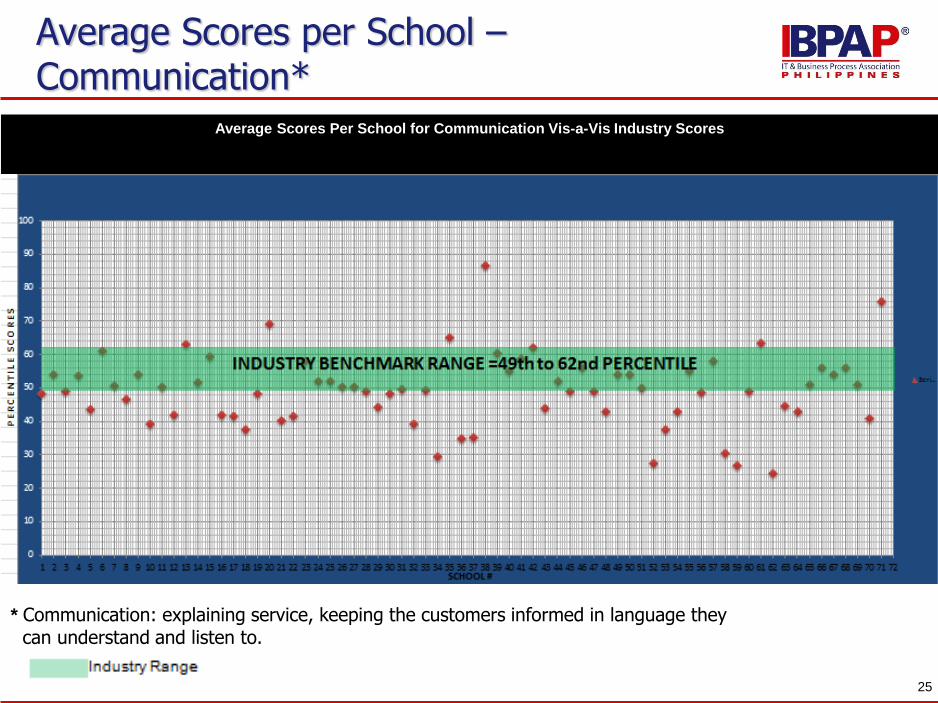

Average Scores Per School for Communication Vis-a-Vis Industry Scores

* Communication: explaining service, keeping the customers informed in language they can understand and listen to.

Average Scores per School –Communication*

25

Targets by end of Project:685 Teachers trained in SMP

2,800 Teachers trained in Language Tracks

20,000 Students enrolled in SMP

Service Management Program

26

SMP Rollout

27

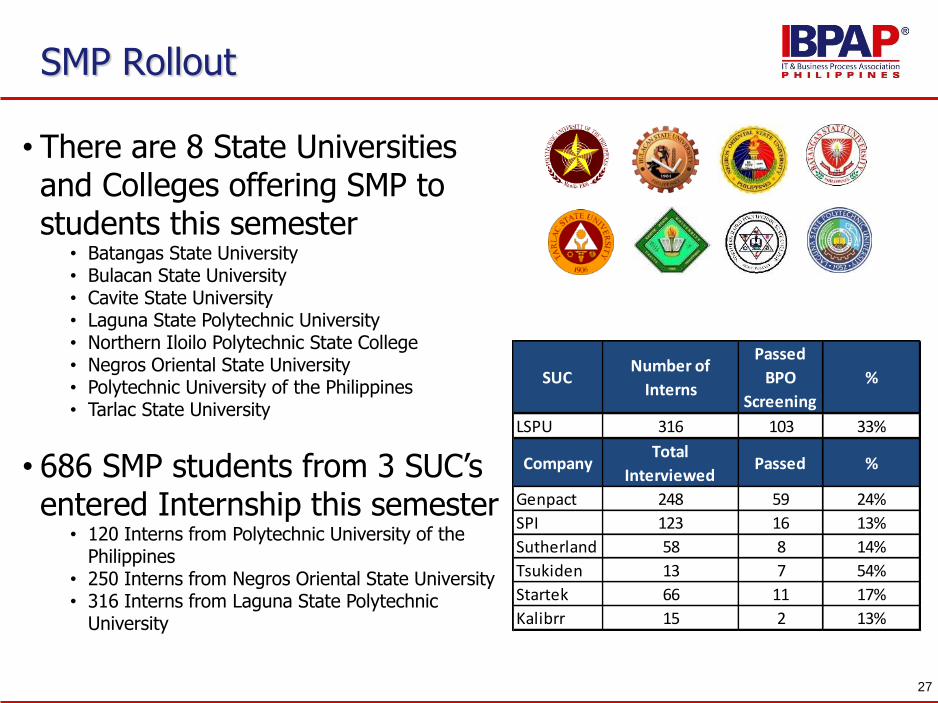

• There are 8 State Universities and Colleges offering SMP to students this semester

• Batangas State University• Bulacan State University• Cavite State University• Laguna State Polytechnic University• Northern Iloilo Polytechnic State College• Negros Oriental State University• Polytechnic University of the Philippines • Tarlac State University

• 686 SMP students from 3 SUC’s entered Internship this semester

• 120 Interns from Polytechnic University of the Philippines

• 250 Interns from Negros Oriental State University• 316 Interns from Laguna State Polytechnic

University

SUCNumber of

Interns

Passed

BPO

Screening

%

LSPU 316 103 33%

CompanyTotal

InterviewedPassed %

Genpact 248 59 24%

SPI 123 16 13%

Sutherland 58 8 14%

Tsukiden 13 7 54%

Startek 66 11 17%

Kalibrr 15 2 13%

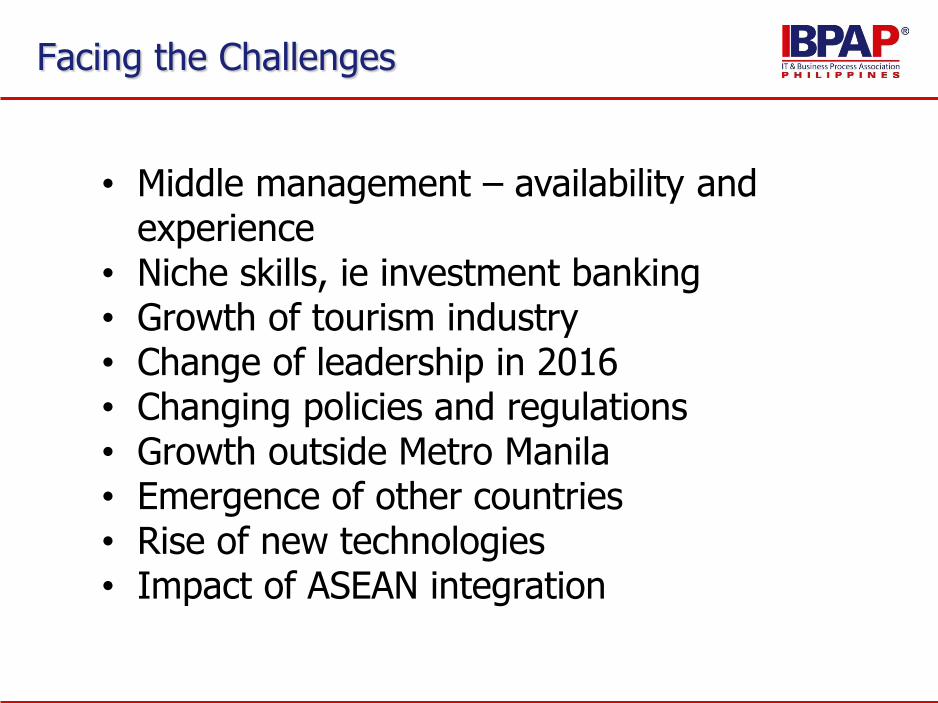

Facing the Challenges

• Middle management – availability and experience

• Niche skills, ie investment banking• Growth of tourism industry• Change of leadership in 2016• Changing policies and regulations• Growth outside Metro Manila • Emergence of other countries• Rise of new technologies• Impact of ASEAN integration

The

Road ahead

29

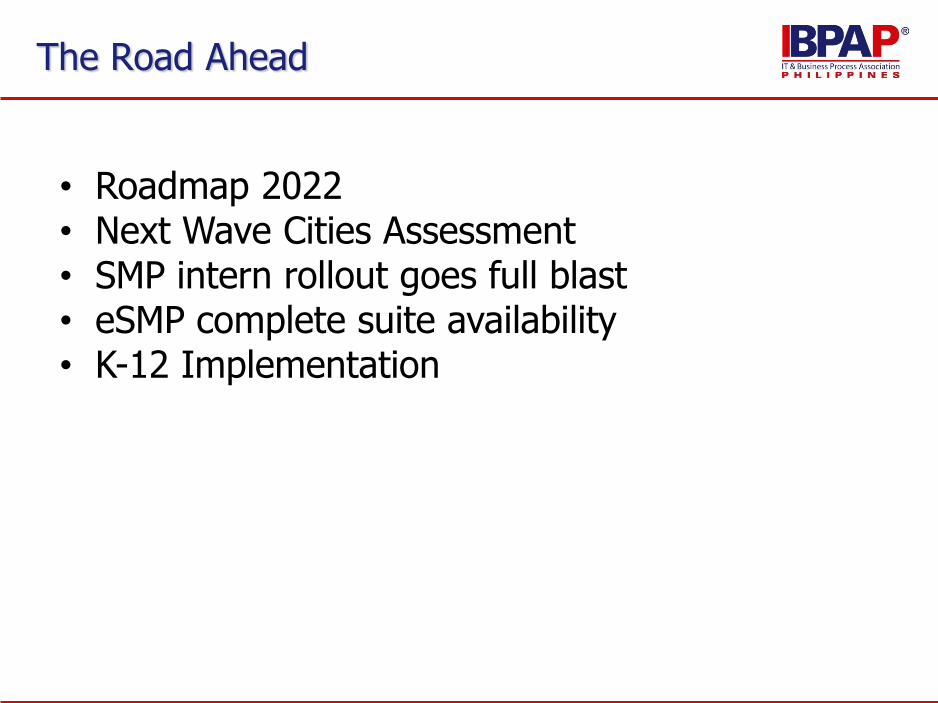

The Road Ahead

• Roadmap 2022• Next Wave Cities Assessment• SMP intern rollout goes full blast• eSMP complete suite availability• K-12 Implementation

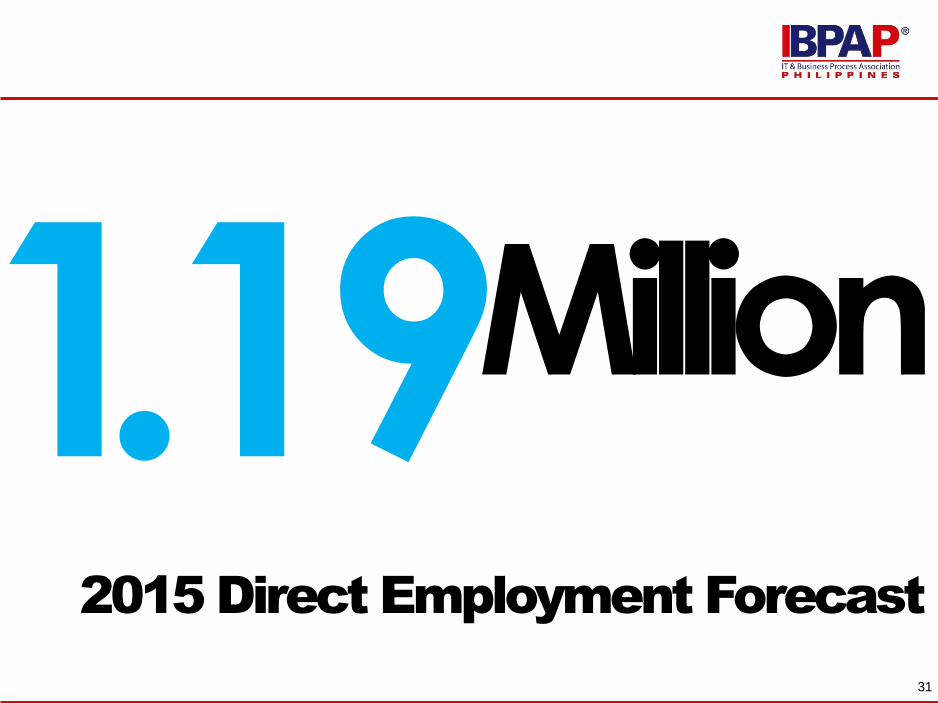

Million

2015 Direct Employment Forecast

31

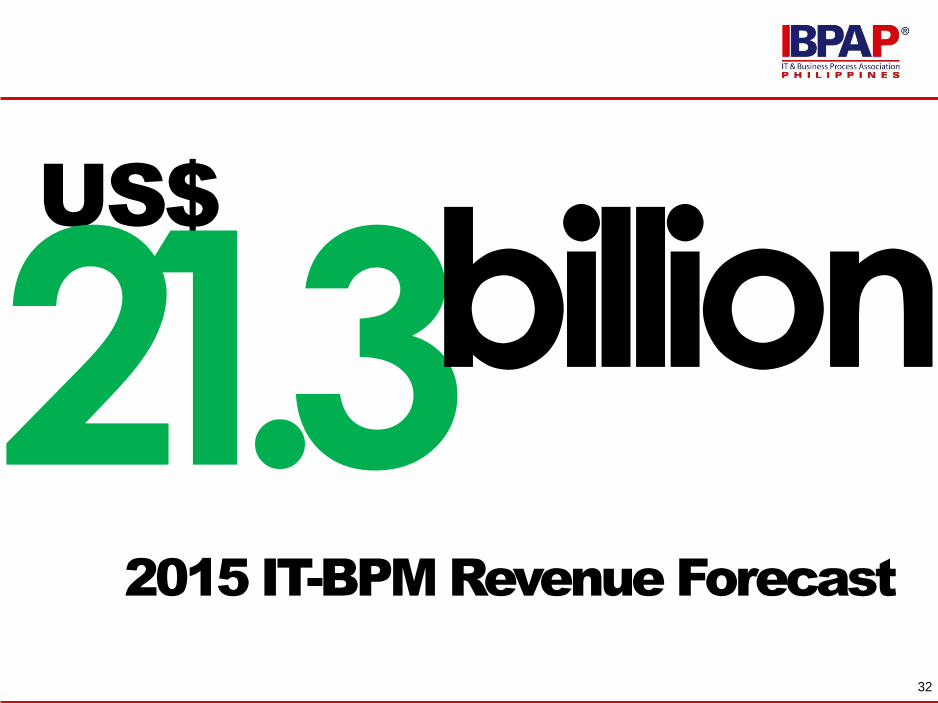

US$

billion2015 IT-BPM Revenue Forecast

32

Thank

you!!

33