the next stage in the health care economy: aligning the interests of patients, providers, and...

TRANSCRIPT

Physician leadership

The next stage in the health care economy: aligning the interests ofpatients, providers, and third-party payers through consumer-driven

health care plans

Thomas W. Samuel, J.D., M.B.A.a,b, Stephen G. Raleighb, Judith M. Hower, M.S.b,Richard W. Schwartz, M.D., M.B.Ab,c,d,*

aSchool of Public Health and College of Health Sciences, University of Kentucky, Lexington, KY, USAbCenter for Health Services Management Research, University of Kentucky, Lexington, KY, USA

cDepartment of Surgery, College of Medicine, and Chandler Medical Center, University of Kentucky, and Clinical Operations, Veterans Affairs MedicalCenter, Lexington, KY, USA

Manuscript received September 12, 2002; revised manuscript February 1, 2003

Abstract

This article reviews employers’ attempts over the past 25 years to address the cost and accessibility of health care services for theiremployees and the effect these efforts have had on U.S. health care delivery. The difficulties in aligning the interests of all parties in athird-party health beneficiary contract are examined. Many employers are considering consumer-driven health care plans as an alternativeto managed care plans to both control health care costs and improve employee satisfaction. Such plans differ from fee-for-service andmanaged care models in terms of the economic alignment of the parties. Consumer-driven plans align the employer’s economic interest withthe employee/patient, and reduce health benefit costs by providing information, tools, and direct economic incentives to employees forself-management of health care dollars. Because these incentives are designed to reduce the consumption of services, providers are the partyleft out of economic alignment under the consumer-driven model. © 2003 Excerpta Medica, Inc. All rights reserved.

Keywords: Health care; Finance; Insurance; Universal coverage; Consumer-driven health care

As the promotion for the 2002 Benefits Management Forumand Expo stated, “The talk of the benefits industry is ‘de-fined contribution’ health care, often referred to as ‘con-sumer-driven’ health care plans.” Defined-contributionhealth care refers to health care plans in which fixed healthcare contributions by employers are established in employeepretax accounts. Depending on the plan, annual unuseddollars can sometimes be rolled over by employees to payfor future health care costs or to be invested in individualretirement accounts (IRAs). Thus, in such plans, dollarspreviously held by insurers, health benefit plans, and healthmaintenance organizations (HMOs) are placed into “thehands of consumers.” Consumer-driven plans usually offerinformational tools to assist employees in managing theirpersonal health care and their benefit dollars.

In contrast, during the previous half century, health care

plans were almost exclusively dominated by “defined-ben-efit” plans, in which third-party payers, rather than committo set expenditures, committed instead to virtually unlimitedcoverage based on percentages of health care costs. Whythis shift away from managed care and defined benefits?The answer lies mainly in the combined dissatisfaction ofpatients, providers, and third-party payers (employers andinsurance companies) regarding cost and access of servicesand lack of economic alignment among the three parties.The dissatisfaction of patients with HMOs led to the PatientBill of Rights legislation, designed to protect patients frommanaged care restrictions [1]. The dissatisfaction of provid-ers with HMOs has centered on reimbursement levels con-sidered as grossly inadequate and on restrictions on treat-ment options. Lastly, the dissatisfaction of employers withHMOs has been twofold: (1) fear of offering dissatisfactory“benefits” to employees in terms of the quality and acces-sibility of health care services, and (2) the financial burdenof excessive costs associated with defined benefits. Further-

* Corresponding author. Tel.: �1-859-323-6346.E-mail address: [email protected]

The American Journal of Surgery 186 (2003) 117–124

0002-9610/03/$ – see front matter © 2003 Excerpta Medica, Inc. All rights reserved.doi:10.1016/S0002-9610(03)00189-2

more, some state legislatures have imposed restrictions onmanaged care plans and mandated benefits that have re-sulted in increased costs of health benefits to employers/insurers and to employees/patients. Concomitantly, the costof managed care to employers and patients escalated in2002 [2], and additional increases are forecast for futureplan years.

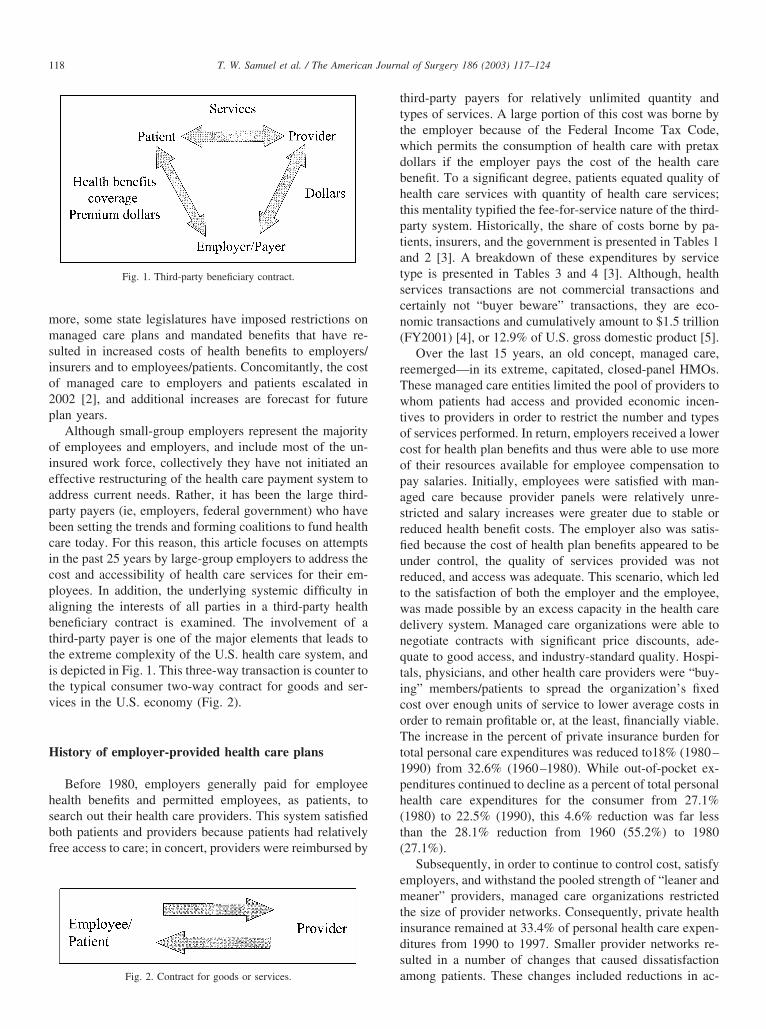

Although small-group employers represent the majorityof employees and employers, and include most of the un-insured work force, collectively they have not initiated aneffective restructuring of the health care payment system toaddress current needs. Rather, it has been the large third-party payers (ie, employers, federal government) who havebeen setting the trends and forming coalitions to fund healthcare today. For this reason, this article focuses on attemptsin the past 25 years by large-group employers to address thecost and accessibility of health care services for their em-ployees. In addition, the underlying systemic difficulty inaligning the interests of all parties in a third-party healthbeneficiary contract is examined. The involvement of athird-party payer is one of the major elements that leads tothe extreme complexity of the U.S. health care system, andis depicted in Fig. 1. This three-way transaction is counter tothe typical consumer two-way contract for goods and ser-vices in the U.S. economy (Fig. 2).

History of employer-provided health care plans

Before 1980, employers generally paid for employeehealth benefits and permitted employees, as patients, tosearch out their health care providers. This system satisfiedboth patients and providers because patients had relativelyfree access to care; in concert, providers were reimbursed by

third-party payers for relatively unlimited quantity andtypes of services. A large portion of this cost was borne bythe employer because of the Federal Income Tax Code,which permits the consumption of health care with pretaxdollars if the employer pays the cost of the health carebenefit. To a significant degree, patients equated quality ofhealth care services with quantity of health care services;this mentality typified the fee-for-service nature of the third-party system. Historically, the share of costs borne by pa-tients, insurers, and the government is presented in Tables 1and 2 [3]. A breakdown of these expenditures by servicetype is presented in Tables 3 and 4 [3]. Although, healthservices transactions are not commercial transactions andcertainly not “buyer beware” transactions, they are eco-nomic transactions and cumulatively amount to $1.5 trillion(FY2001) [4], or 12.9% of U.S. gross domestic product [5].

Over the last 15 years, an old concept, managed care,reemerged—in its extreme, capitated, closed-panel HMOs.These managed care entities limited the pool of providers towhom patients had access and provided economic incen-tives to providers in order to restrict the number and typesof services performed. In return, employers received a lowercost for health plan benefits and thus were able to use moreof their resources available for employee compensation topay salaries. Initially, employees were satisfied with man-aged care because provider panels were relatively unre-stricted and salary increases were greater due to stable orreduced health benefit costs. The employer also was satis-fied because the cost of health plan benefits appeared to beunder control, the quality of services provided was notreduced, and access was adequate. This scenario, which ledto the satisfaction of both the employer and the employee,was made possible by an excess capacity in the health caredelivery system. Managed care organizations were able tonegotiate contracts with significant price discounts, ade-quate to good access, and industry-standard quality. Hospi-tals, physicians, and other health care providers were “buy-ing” members/patients to spread the organization’s fixedcost over enough units of service to lower average costs inorder to remain profitable or, at the least, financially viable.The increase in the percent of private insurance burden fortotal personal care expenditures was reduced to18% (1980–1990) from 32.6% (1960–1980). While out-of-pocket ex-penditures continued to decline as a percent of total personalhealth care expenditures for the consumer from 27.1%(1980) to 22.5% (1990), this 4.6% reduction was far lessthan the 28.1% reduction from 1960 (55.2%) to 1980(27.1%).

Subsequently, in order to continue to control cost, satisfyemployers, and withstand the pooled strength of “leaner andmeaner” providers, managed care organizations restrictedthe size of provider networks. Consequently, private healthinsurance remained at 33.4% of personal health care expen-ditures from 1990 to 1997. Smaller provider networks re-sulted in a number of changes that caused dissatisfactionamong patients. These changes included reductions in ac-

Fig. 1. Third-party beneficiary contract.

Fig. 2. Contract for goods or services.

118 T. W. Samuel et al. / The American Journal of Surgery 186 (2003) 117–124

cess to providers, elimination of selected benefits such aseye care, enlargement of co-payments, and the reintroduc-tion of deductibles. Finally, employees said “enough” andvoiced their dissatisfaction by switching to more open ac-cess health benefit plans. In response, managed care plansbecame less restrictive in order to retain their membershipbase. The negotiating power of providers increased, and theprice of managed care plans increased. Insurers competed tocontrol the cost of their products or services, while employ-ers competed to provide salaries and health benefit plans toattract and retain employees. Employers and third-partypayers started to look for alternatives to managed care.Movements away from managed care were in evidence in1998 as private health insurance began to increase as apercent of total personal health care expenditures. Likewise,out-of-pocket payments also increased as a percent of totalpersonal health care expenditures beginning that year.

During this period, the preferred provider organization(PPO) model of managed care emerged. This model nowrepresents the largest managed care model in most healthcare markets. Preferred provider organizations are moreloosely managed than traditional HMOs and are the harbin-gers of consumer-driven health care. Although they lack thepersonal account feature of consumer-driven plans, they aresimilar to consumer-driven plans in that the insured hasgreater access to services by being able to opt out of theprovider network by paying a larger percent of costs out ofpocket.

Note that we are neither stating nor implying that theexclusive motivation for providing health care services iseconomic gain. In fact, employers have recently moved toaggressively address issues related to the quality of healthcare, as evidenced by the establishment of organizationssuch as the Midwest Business Group on Health and theLeapfrog Group for Patient Safety [4]. Nevertheless, theprimary factors that shape health benefit plans remain thealignment of the employer and employee interests and cost.

Employers are interested in retaining employees and con-taining costs as payers of employee compensation (eg, sal-aries, FICA taxes, retirement benefits, health care premi-ums). Employees are interested in access to high quality andreasonably priced health care services [2]. The key issue forboth payers and patients is the perception of value; as in anyeconomic transaction, value equals quality divided by cost.Also implicit to this discussion, although the details ofwhich are beyond the scope of this article, is the fact that theeconomic impact of health care payment systems unavoid-ably influences the behavior of providers.

In addition, to discuss health care expenditures in 2003,one must also examine prescription drug expenditures as amajor cost driver that must be targeted by employers andhealth benefit plans (Tables 5 and 6). Prescription drugexpenditures declined from 96.0% out-of-pocket paymentsin 1960 to 32.0% in 2000. This decline is not as dramatic asthe decline in payments for hospital care and physicianservices, but is still a significant shift away from the con-sumer paying at the point of consumption. To further em-phasize the shift away from expenditures at the point ofservice for prescription drugs, Table 6 shows that the in-crease in out-of-pocket expenditures for the consumer ofdrugs increased in 2000 dollars from 37.4 billion in 1990 to$39.0 billion in 2000, or 4.2%. Over a 10-year period this isa very limited increase, particularly considering the totalprescription drug expenditures increased in 2000-adjusteddollars from $63.3 billion to $121.8 billion, or 48.0% [3].To grasp further the significance of prescription drug coststo private health insurance and the government, one canexamine them as a percentage of the total personal healthcare expenditures. Prescription drug expenditures declinedfrom 10% of total personal health care expenditures in 1960to 4.9% in 1980. These expenditures then increased as a

Table 1Personal health care expenditures by source of funds*

Source of funds 1960 1980 1990 2000

Out-of pocket payments 55.2% $12.9 27.1% $58.2 22.5% $137.1 17.2% $194.4Private health insurance 21.4% $5.0 28.3% $60.7 33.4% $203.5 34.6% $391.1Government 21.4% $5.0 40.3% $86.5 39.0% $237.7 43.3% $489.5Other 2.0% $0.5 4.3% $9.2 5.0% $30.5 5.0% $56.5

* Amount dollars in billions and percent distribution (includes some rounding errors) [3].

Table 2Inflation adjusted personal health care expenditures by source of funds*

Source of funds 1960 1980 1990 2000

Out-of-pocket payments $176.0 $207.0 $224.1 $194.1Private health insurance $68.0 $216.1 $333.7 $391.1Government $68.0 $308.0 $389.8 $489.5

* Year 2000 dollars, in billions of dollars [3].

Table 3Break down of expenditures by service*

Type of national health expenditure 1960 1980 1990 2000

Hospital care 34.4% 41.3% 36.5% 31.7%Physician and clinical services 20.1% 19.2% 22.6% 22.0%Other professional (including dental) 8.9% 6.9% 7.1% 7.6%Nursing home and home health 3.4% 8.2% 9.4% 9.6%Prescription drugs 10.0% 4.9% 5.8% 9.4%Other medical products—retail outlets 8.5% 5.6% 4.7% 3.8%

* National health expenditures percent distribution by type expenditures[3].

119T. W. Samuel et al. / The American Journal of Surgery 186 (2003) 117–124

percent of total personal health care expenditures to 5.8% in1990 and 9.4% in 2000 (see Table 3) [3]. Another means ofreporting the impact of prescription drug expenditures is asa percent of physician service expenditures. Prescriptiondrug expenditures as a percent of physician service expen-ditures decreased from 50% in 1960 to 25.5% in 1980 andthen increased to 42.5% in 2000 [3].

Employer health care benefit models

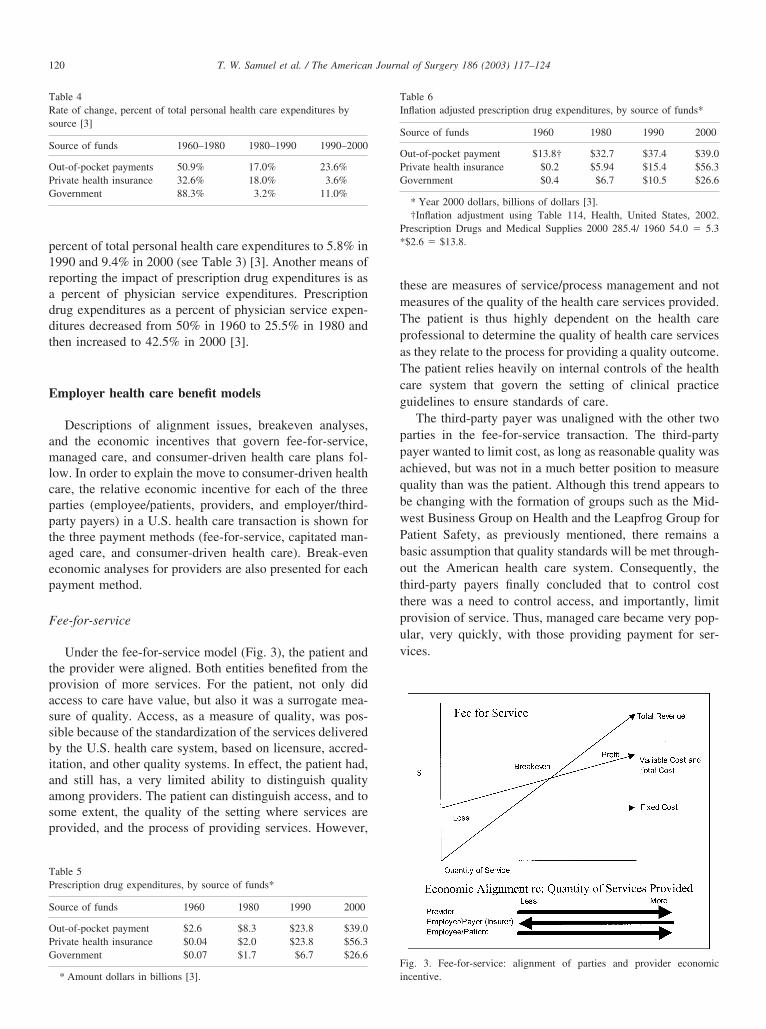

Descriptions of alignment issues, breakeven analyses,and the economic incentives that govern fee-for-service,managed care, and consumer-driven health care plans fol-low. In order to explain the move to consumer-driven healthcare, the relative economic incentive for each of the threeparties (employee/patients, providers, and employer/third-party payers) in a U.S. health care transaction is shown forthe three payment methods (fee-for-service, capitated man-aged care, and consumer-driven health care). Break-eveneconomic analyses for providers are also presented for eachpayment method.

Fee-for-service

Under the fee-for-service model (Fig. 3), the patient andthe provider were aligned. Both entities benefited from theprovision of more services. For the patient, not only didaccess to care have value, but also it was a surrogate mea-sure of quality. Access, as a measure of quality, was pos-sible because of the standardization of the services deliveredby the U.S. health care system, based on licensure, accred-itation, and other quality systems. In effect, the patient had,and still has, a very limited ability to distinguish qualityamong providers. The patient can distinguish access, and tosome extent, the quality of the setting where services areprovided, and the process of providing services. However,

these are measures of service/process management and notmeasures of the quality of the health care services provided.The patient is thus highly dependent on the health careprofessional to determine the quality of health care servicesas they relate to the process for providing a quality outcome.The patient relies heavily on internal controls of the healthcare system that govern the setting of clinical practiceguidelines to ensure standards of care.

The third-party payer was unaligned with the other twoparties in the fee-for-service transaction. The third-partypayer wanted to limit cost, as long as reasonable quality wasachieved, but was not in a much better position to measurequality than was the patient. Although this trend appears tobe changing with the formation of groups such as the Mid-west Business Group on Health and the Leapfrog Group forPatient Safety, as previously mentioned, there remains abasic assumption that quality standards will be met through-out the American health care system. Consequently, thethird-party payers finally concluded that to control costthere was a need to control access, and importantly, limitprovision of service. Thus, managed care became very pop-ular, very quickly, with those providing payment for ser-vices.

Table 4Rate of change, percent of total personal health care expenditures bysource [3]

Source of funds 1960–1980 1980–1990 1990–2000

Out-of-pocket payments 50.9% 17.0% 23.6%Private health insurance 32.6% 18.0% 3.6%Government 88.3% 3.2% 11.0%

Table 5Prescription drug expenditures, by source of funds*

Source of funds 1960 1980 1990 2000

Out-of-pocket payment $2.6 $8.3 $23.8 $39.0Private health insurance $0.04 $2.0 $23.8 $56.3Government $0.07 $1.7 $6.7 $26.6

* Amount dollars in billions [3].

Table 6Inflation adjusted prescription drug expenditures, by source of funds*

Source of funds 1960 1980 1990 2000

Out-of-pocket payment $13.8† $32.7 $37.4 $39.0Private health insurance $0.2 $5.94 $15.4 $56.3Government $0.4 $6.7 $10.5 $26.6

* Year 2000 dollars, billions of dollars [3].†Inflation adjustment using Table 114, Health, United States, 2002.

Prescription Drugs and Medical Supplies 2000 285.4/ 1960 54.0 � 5.3*$2.6 � $13.8.

Fig. 3. Fee-for-service: alignment of parties and provider economicincentive.

120 T. W. Samuel et al. / The American Journal of Surgery 186 (2003) 117–124

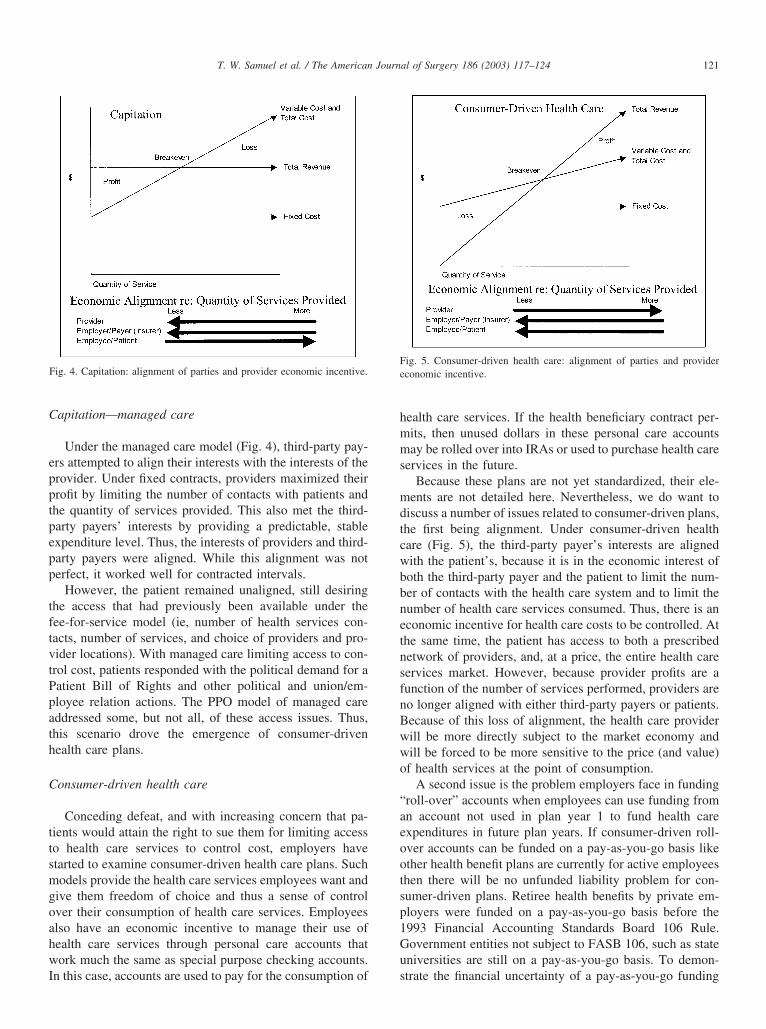

Capitation—managed care

Under the managed care model (Fig. 4), third-party pay-ers attempted to align their interests with the interests of theprovider. Under fixed contracts, providers maximized theirprofit by limiting the number of contacts with patients andthe quantity of services provided. This also met the third-party payers’ interests by providing a predictable, stableexpenditure level. Thus, the interests of providers and third-party payers were aligned. While this alignment was notperfect, it worked well for contracted intervals.

However, the patient remained unaligned, still desiringthe access that had previously been available under thefee-for-service model (ie, number of health services con-tacts, number of services, and choice of providers and pro-vider locations). With managed care limiting access to con-trol cost, patients responded with the political demand for aPatient Bill of Rights and other political and union/em-ployee relation actions. The PPO model of managed careaddressed some, but not all, of these access issues. Thus,this scenario drove the emergence of consumer-drivenhealth care plans.

Consumer-driven health care

Conceding defeat, and with increasing concern that pa-tients would attain the right to sue them for limiting accessto health care services to control cost, employers havestarted to examine consumer-driven health care plans. Suchmodels provide the health care services employees want andgive them freedom of choice and thus a sense of controlover their consumption of health care services. Employeesalso have an economic incentive to manage their use ofhealth care services through personal care accounts thatwork much the same as special purpose checking accounts.In this case, accounts are used to pay for the consumption of

health care services. If the health beneficiary contract per-mits, then unused dollars in these personal care accountsmay be rolled over into IRAs or used to purchase health careservices in the future.

Because these plans are not yet standardized, their ele-ments are not detailed here. Nevertheless, we do want todiscuss a number of issues related to consumer-driven plans,the first being alignment. Under consumer-driven healthcare (Fig. 5), the third-party payer’s interests are alignedwith the patient’s, because it is in the economic interest ofboth the third-party payer and the patient to limit the num-ber of contacts with the health care system and to limit thenumber of health care services consumed. Thus, there is aneconomic incentive for health care costs to be controlled. Atthe same time, the patient has access to both a prescribednetwork of providers, and, at a price, the entire health careservices market. However, because provider profits are afunction of the number of services performed, providers areno longer aligned with either third-party payers or patients.Because of this loss of alignment, the health care providerwill be more directly subject to the market economy andwill be forced to be more sensitive to the price (and value)of health services at the point of consumption.

A second issue is the problem employers face in funding“roll-over” accounts when employees can use funding froman account not used in plan year 1 to fund health careexpenditures in future plan years. If consumer-driven roll-over accounts can be funded on a pay-as-you-go basis likeother health benefit plans are currently for active employeesthen there will be no unfunded liability problem for con-sumer-driven plans. Retiree health benefits by private em-ployers were funded on a pay-as-you-go basis before the1993 Financial Accounting Standards Board 106 Rule.Government entities not subject to FASB 106, such as stateuniversities are still on a pay-as-you-go basis. To demon-strate the financial uncertainty of a pay-as-you-go funding

Fig. 4. Capitation: alignment of parties and provider economic incentive.Fig. 5. Consumer-driven health care: alignment of parties and providereconomic incentive.

121T. W. Samuel et al. / The American Journal of Surgery 186 (2003) 117–124

plan, the unfunded liability of Medicare is estimated to be$8.9 trillion, which in 1999 was twice the total federal debtheld by the public [6].

The third issue regarding consumer-driven plans is ad-verse selection. If an employer offers fully insured plans andhealthy, young persons with relatively low and predictablehealth care costs choose consumer-driven plans and chron-ically ill persons choose traditional, defined-benefit plans(ie, PPOs, HMOs), then the traditional plans will dispropor-tionately increase in cost and will likely become excessivelyexpensive for the employer and the employee. This can beprevented by offering only consumer-driven plans or by theemployer sharing the risk among the various plans offeredthrough pricing and design of the products or by self-insuring the entire risk of the entity or both [7].

Finally, in order to retain freedom of access to healthcare services employees will be required to directly assume,as consumers at the point of consumption, more of the costsof health care services. The only question is how employeeswill assume these costs. Will the employer share costs at thepoint of consumption through increased co-payments, coin-surance, deductibles and nonpayment for certain proce-dures, or through consumer-driven plans forcing the em-ployee/patient/consumer to assume greater risk and out-of-pocket expense? This is emphasized by Table 2, whichshows that, in inflation-adjusted 2000 dollars, out-of-pocketpersonal health care expenditures declined 13.4% from1990 ($224.1 billion) to 2000 ($194.1 billion). The assump-tion of greater financial risk at the point of consumptionmeans the employee/patient/consumer must assume moreresponsibility for managing their health status. Thus tomake consumer-driven plans effective, it is essential that theconsumer have tools and nonfinancial incentives in placethat discourage the use of higher priced alternative servicesand yet keep the employee healthy. This essential long-termstrategy must focus on bringing about change in employee/patient/consumer behavior and have a positive effect on thecost of health care services consumption [8].

Consumer satisfaction: Herzberg’s theory

Consumer satisfaction is yet one more reason why em-ployers/payers are seriously considering the adoption of theconsumer-driven health care model. Health care benefits canbe viewed as “compensation,” with which the employeecould potentially be “satisfied” rather than, as is often thecase, at best “not dissatisfied.” In general, when it comes tohealth care plans, consumers want value (ie, economicalplans that provide an optimal number of quality health careservices). How those services are organized and how theservices must be consumed may or may not be satisfactoryto the consumer. Typically, consumers want freedom ofchoice and a sense of satisfaction derived from feeling theyare in control.

To evaluate how employers motivate employees, Fred-

erick Herzberg developed a theory, involving two sets ofmotivating factors: (1) satisfiers or motivators, which whenadequate result in satisfaction; and (2) dissatisfiers or hy-giene (ie, maintenance) factors, which when deficient causedissatisfaction [9]. If satisfiers are present, then an individ-ual is “satisfied.” However, if satisfiers are not present, itdoes not mean an individual is “dissatisfied;” it may simplymean he or she is “not dissatisfied” or “not satisfied.”“Satisfied” and “dissatisfied” as described by Herzberg’s“two-factor” theory of motivation can be viewed on a con-tinuum (Fig. 6).

Herzberg’s model can be used to explain the reaction byemployees involved in third-party health beneficiary con-tracts in relation to the payment systems described above.Under the fee-for-service system, employees had choice ofaccess, low out-of-pocket-expense, and a perception ofquality. The employee was “not dissatisfied.” The employerwas “dissatisfied” because costs escalated faster than thecost of general inflation in the economy. During the earlyphases of managed care, employees remained generallysatisfied with their health care benefits. Over time, as morestringent measures were introduced to control costs, em-ployees moved from “not dissatisfied” to “dissatisfied.” Wepostulate that this state of dissatisfaction reflects the currentfeelings of consumers with health care benefits in the UnitedStates, complicated by the fact that health care costs areescalating at a rate several times that of general inflation.The possibility of a rollover for unused health benefits inconsumer-driven health care plans may provide a means toreward participants and reinforce a value-conscious behav-ior (in the economy at large, customers typically seek value,which is defined as a balance between quality and cost). Toan extent, they may actually become “satisfied” rather thanjust “not dissatisfied” with health benefits provided by em-ployers.

Alignment of parties

Ideally, an employer-provided health plan would alignthe interests of all three parties. Unfortunately, the healthcare system still awaits such a health benefit model. Somewould argue that the best approach to health care would be

Fig. 6. Herzberg’s theory of employee motivation.

122 T. W. Samuel et al. / The American Journal of Surgery 186 (2003) 117–124

to eliminate the employer-sponsored plans entirely, andpermit employees to purchase health benefits from the mar-ket like any other good or service [10]. However, just as thebenefits from removing the employer from the transactionare many, so are the problems. The overriding problemintroduced by removing the employer from the health caretransaction is a loss of equitable access to health care. Withrising health care costs, an aging population, changes intechnology, and broadening definitions of health-relatedconditions, a method is needed for subsidizing the purchaseof health benefit plans by low-income persons. Conceiv-ably, this could be accomplished through direct governmentsubsidy or tax credits to, in effect, increase the salary oflow-income workers for the express purpose of purchasinghealth benefit plans. Such a subsidy program is a complexundertaking. For now, the system of employer-providedhealth benefit plans remains appealing because of its rela-tive simplicity. This method permits the employer to incor-porate the cost of health care into the cost of doing businessand to make employer-by-employer or union-by-employerdecisions about which individuals are covered by healthbenefit plans.

Presumably, today’s employees consider health benefitplans in their employment decisions. Most employers rec-ognize that health benefit plans are more likely to dissatisfyemployees and less likely to motivate employees and, sub-sequently, less likely to improve job performance [9]. Nev-ertheless, health benefit plans do permit employers to ex-press interest in the entire work force and emphasize theimportance of the organization in providing for employees’basic needs.

When it comes to health care, Americans have come toexpect outstanding quality and immediate access. Unfortu-nately, they often equate the quality of care with the amountof care consumed. Because of this assumption, and thequantity issues discussed above, the cost of health care hasrisen dramatically. Ultimately, creating a system that solvesthese alignment issues may not be possible.

National health insurance

Finally, this discussion would be incomplete withoutreference to the debate over national health insurance. Al-though such a system would ensure all Americans access tohealth care, many issues present in the current system wouldremain. In fact, many contend the benefits of universalcoverage would not outweigh the associated sacrifices.

Overall, universal health coverage has a number of ad-vantages. Currently, one of the most important unresolvedhealth care issues is the large number of persons withouthealth care benefits. Approximately 40 million Americansare not covered under any form of health care plan [11].Because uninsured families must pay for their medical ex-penses out of pocket, it is common for families to spend10% to 15% of their income on payments for health care

services. This often results in medical bankruptcy, whichaccounts for approximately 40% of the bankruptcies in theUnited States [12].

Universal health coverage could resolve this crisis byproviding health benefits for all U.S. citizens without regardfor socioeconomic status. When people are uninsured, theyoften do not have a primary care physician, and thus theytend to delay treatment until their medical condition be-comes unmanageable. At that point, they often seek treat-ment at emergency rooms because emergency rooms, bylaw and regulation, must treat people regardless of theirability to pay. Universal coverage could stop this pattern ofsystem misuse [13]. Individuals who currently are insuredwould also benefit from universal coverage in that employ-ees would be freer to change jobs if health care benefitswere no longer linked to one’s employer.

However, not everything about national health insuranceis positive. Under most universal coverage systems, onedoes not have the privilege of accessing medical services atwill. Universal coverage systems create priority listswhereby the critically ill receive services first, and patientswho have nonlife-threatening conditions or who desire elec-tive procedures may have to wait a long time to receive care.To most Americans, especially those with existing cover-age, such change represents undesirable sacrifice and loss ofcontrol. This loss of control could be overcome by some ifthe purchase of individual health benefits were allowable.However, it follows that such an allowance would introduceinequities in service access to the overall universal coveragesystem.

Except for the United States, every industrialized countryin the world has some form of national health coverage.Most of these countries have managed to make their sys-tems work, but not without consumer dissatisfaction. Forexample, Canada’s national health care system has createda shortage of physicians, whereby not all citizens haveaccess to a primary care physician. This shortage also pre-vents some patients from being referred to provider special-ists. Even after a diagnosis has been made, a patient maystill have to wait months before surgery can be performed.As a result, many Canadians are traveling to the UnitedStates to have their medical procedures performed. Like-wise, the government formulary is limited, thus forcingsome Canadians to travel to the United States to obtainmedications [5].

Yet another major concern with universal coverage isconsumption. If a person is not responsible for paying themedical bills, no economic incentive exists to restrict con-sumption—“who cares, the government is paying.” Thementality that quality equals quantity could grow uncheckedif no counteracting financial incentives were in place [14].

Providers also have reason for serious concern about theinstitution of government-sponsored health care. Govern-ment sponsorship could result in reimbursement rates beingset based on the availability of government funds rather thanon the cost of service provision. In addition, the government

123T. W. Samuel et al. / The American Journal of Surgery 186 (2003) 117–124

could impose restrictions that could limit the discretion ofthe provider and could require providers to meet outcomestandards to qualify for payment. For these reasons, al-though universal coverage is a future possibility, it is un-likely to materialize anytime soon. We would argue, how-ever, that the universal coverage solution is as likely, andmaybe even more likely, to occur as is removing the em-ployer from the scenario while retaining a private healthbenefit market.

Conclusion

Underlying this entire discussion, health plan decision-making is strongly affected by the overall condition of theeconomy. During the growth period of the 1990s, employerswere more concerned about retaining employees than aboutthe cost of health plans. Now with the current economicslowdown, profit margins are tight and employers are moreconcerned about costs and somewhat less concerned withemployee satisfaction. Likewise, in the current economicclimate, employees are becoming less concerned with opti-mal health plans and becoming increasingly concernedabout job security.

Although the overall societal movement toward consum-erism is now being played out in the consumer-driven healthcare plans that are unfolding, we are not proposing that theconsumer-driven health care model is the ideal model andthe end stage of a long quest to align the interest of theemployee/patient, employer/payer (insurer), and the pro-vider. In fact, we are postulating that almost out of desper-ation employers will select to use the consumer-drivenhealth care benefit model in order to both control health carecosts and improve employee satisfaction. The model differsfrom the fee-for-service and managed care models in thatthe alignment of the parties differs. The employer’s eco-nomic interest in this model is aligned with the employee/patient. The employer’s method for reducing health benefitcosts entails providing information, tools, and direct eco-nomic incentives to the employee/patient. The assumptionis that this approach will result in more responsible, rationalconsumption of health care services, and, in turn, providebetter control over the costs of health care, and thus morecontrol over the employer’s costs of health benefits. The

added employee incentive to roll forward unused benefits tothe next plan year, may help consumer-driven plans be“satisfiers” for the employees, as opposed to “not dissatis-fiers.” Will this model be successful in controlling cost andimproving access and quality? Perhaps not, maybe evenlikely not. Nevertheless, it may be the only option foremployers who are currently faced with dissatisfied employ-ees and uncontrollable increases in the cost of health ben-efits.

References

[1] Bipartisan patient protection acts. HR 2563 (August 2, 2001); S 1052(June 29, 2001).

[2] Gunsauley C. HMO quotes show 22% average increase. EmployeeBenefit News 2002;16(9). Available at: http://www.BenefitNews.com, accessed August 22, 2002.

[3] National Center for Health Statistics. National health expenditures,Health United States 2002. Available at: http://www.cdc.gov/nchs/products/pubs/pudh/hus/02hustop.htm. Accessed June 23, 2003.

[4] Landers P. Industrial giants urge action on ballooning health ex-penses. The Wall Street Journal, June 11, 2002, p A2.

[5] Wysocki B. U.S. exports medical advances, and high costs, to rest ofglobe. The Wall Street Journal, June 10, 2002, p A3.

[6] NCPA policy report no. 222—survey medicare. Washington, DC:National Center for Policy Analysis, 1999.

[7] Bradford SL. Health on the horizon. Smart Money, January 27, 2002.Available at: http://online.wsj.com/article/o,sb10120720887178, ac-cessed August 22, 2002.

[8] Craver, ML. Employers cautious about new health plans. TheKiplinger Letter 2002;19(42). Available at: http://special.kiplinger.com/health/stories/employers_step_gingerly_br_toward_new_health_plans.html, accessed August 22, 2002.

[9] Longest BB, Rakich S, Darr K. Managing health services organiza-tions and systems. Baltimore: Health Professions Press, 2000.

[10] Kleinke JD. Editorial commentary: how to revive health care. Bar-ron’s Online, June 17, 2002, p 38.

[11] Tuffnel S, Kirby J. Brief analysis 119: is universal coverage neces-sary to control health care costs? Washington DC: National Center forPolicy Analysis, 2002. Available at: http://www.Nepa.org/ba/ba119.html, accessed August 22, 2002.

[12] Light DW. A conservative call for universal access to health care.PennBioethics 2002;9(4):4–6.

[13] The National Coalition for the Homeless. Universal health care:summary of recommendations. Available at: http://www.nationalhomeless.org/universalhealth.html, 2001, accessed August 22, 2002.

[14] Cleveland P. Universal health coverage: the cure or the disease?Critical Issues 2002;1(4). Available at: http://www.campus.leaderu.com/critical.health.html, accessed August 22, 2002.

124 T. W. Samuel et al. / The American Journal of Surgery 186 (2003) 117–124