the global market - nanotech · pdf filethe global market forecast from 2010 ... companies 36...

TRANSCRIPT

APPLICATIONSSemiconductors and data storage,

materials research, nanotechnology and life sciences.

THE GLOBAL MARKETForecast from 2010 to 2020Revenues, future projections and end user markets for scanning probe and electron microscopes.

COMPANIESAll the leading

companies profiled.

MARKETSEnd user markets

including revenues.

PRODUCTSCurrent product

offerings.

EDITION 5FEBRUARY 2014£900

MICROSCOPESFUTURE MARKETS

www.futuremarketsinc.com

ADVANCED

MIC

ROSC

OPE

S • O

CTO

BER

2013

02

EDITOR’S LETTER

4 EXECUTIVE SUMMARYThe advanced microscopy market con-tinues to grow in developing markets.

9 ELECTRON MICROSCOPES (EM)Analysis of the transmission electron microscopy (TEM), scanning electron microscopy (SEM) and dual beam markets through 2018 including unit sales, and conservative and optimistic revenue estimates.

16 SCANNING PROBE MICROSCOPES (SPM)Analysis of the scanning probe mi-croscopy (SPM) market through 2018 including conservative and optimistic revenue estimates.

19 REGIONAL MARKETSAnalysis of regional markets for EM and SPM including conservative and optimistic revenue estimates in North America, Asia-Pacific, Europe and the Rest-of-the-World.

MARKETS24 SEMICONDUCTORS

AND DATA STORAGEAnalysis of the semiconductors and data storage market for EM and SPM including conservative and optimistic revenue estimates.

28 MATERIALS AND NANOMATERIALS RESEARCHAnalysis of the academic and industrial materials and nanomaterials research market for EM and SPM including conservative and optimistic revenue estimates.

32 LIFE SCIENCESAnalysis of the life sciences market for EM and SPM including conservative and optimistic revenue estimates.

COMPANIES36 MARKET STRUCTURE

Market structure summary for EM and SPM.

37 PROFILESOver 30 profiles of EM and SPM manu-facturers including product descrip-tions and contact details.

16

24

32

contentsADVANCED MICROSCOPES: THE GLOBAL MARKET TO 2018

Market focus : Semicon-

ductors

TABLESTable 1: Global Electron Microscopes Market Revenues 2010-2018, (US$)Table 2: Global Scanning Probe Microscopes Market Revenues 2010-2020, (US$)Table 3: Global Electron Microscopes Market Revenues 2010-2020, (US$)Table 4: Global Non-Analytical Scanning Electron Microscope Unit Sales, 2010-2020Table 5: Global Non-Analytical Scanning Electron Microscope Revenues, 2010-2020 (US$)Table 6: Global Analytical Scanning Electron Microscope Unit Sales, 2010-2020Table 7: Global Analytical Scanning Electron Microscope Revenues, 2010-2020 (US$)Table 8: Global Transmission Electron Micro-scope Unit Sales, 2010-2020 (US$)Table 9: Global Transmission Electron Micro-scope Revenues, 2010-2020 (US$)Table 10: Global Dual Beam (FIB-SEM) Unit Sales, 2010-2020Table 11: Global Dual Beam (FIB-SEM) Rev-enues, 2010-2020 (US$)Table 12: Global Scanning Probe Micro-scopes Market Revenues 2010-2020, (US$)Table 13: Global Atomic Force Microscopes Market Revenues 2010-2020, (US$)Table 14: Global R&D Expenditure 2012, Billion US$ Table 15: Global R&D Expenditure 2012 Top 10 countries, Billion US$Table 16: Market for electron microscopes, by region, 2010-2020, Conservative esti-mate, (US$)Table 17: Market for electron microscopes, by region, 2010-2020, Optimistic estimate, (US$)Table 18: Market for scanning probe microscopes, by region, 2010-2020 (US$), Conservative estimateTable 19: Market for scanning probe microscopes, by region, 2010-2020 (US$), Optimistic estimate

SUBSCRIBEto Nanotech Magazine today!www.futuremarketsinc.com

£100/year

Table 20: Global market for scanning electron microscopes, in semiconduc-tors and data storage, 2010-2020 (US$), Conservative estimateTable 21: Global market for scanning electron microscopes, in semiconduc-tors and data storage, 2010-2020 (US$), Optimistic estimateTable 22: Global market for transmission electron microscopes, in semiconduc-tors and data storage, 2010-2020 (US$), Conservative estimateTable 23: Global market for transmission electron microscopes, in semiconduc-tors and data storage, 2010-2020 (US$), Optimistic estimateTable 24: Global market for scanning probe microscopes, in semiconductors and data storage, 2010-2020 (US$), Conservative estimateTable 25: Global market for scanning probe probe microscopes, in semicon-ductors and data storage, 2010-2020 (US$), Optimistic estimateTable 26: Global market for scanning electron microscopes, in materials and nanomaterials research, 2010-2020 (US$), Conservative estimateTable 27: Global market for scanning electron microscopes, in materials and nanomaterials research, 2010-2020 (US$), Optimistic estimateTable 28: Global market for transmis-sion electron microscopes, in materials and nanomaterials research, 2010-2020 (US$), Conservative estimateTable 29: Global market for transmis-sion electron microscopes, in materials and nanomaterials research, 2010-2020 (US$), Optimistic estimateTable 30: Global market for scanning probe microscopes, in materials and nanomaterials research, 2010-2020 (US$), Conservative estimateTable 31: Global market for scanning

probe microscopes, in materials and nanomaterials re- search, 2010-2020 (US$), Optimistic estimateTable 32: Global market for scanning electron microscopes, in life sciences, 2010-2020 (US$), Con- servative esti-mateTable 33: Global market for scanning electron microscopes, in life sciences, 2010-2020 (US$), Opti- mistic estimateTable 34: Global market for transmission electron microscopes, in life sciences, 2010-2020 (US$), Conservative estimateTable 35: Global market for transmission electron microscopes, in life sciences, 2010-2020 (US$), Optimistic estimateTable 36: Global market for scanning probe microscopes, in materials and nanomaterials research, 2010-2020 (US$), Conservative estimateTable 37: Global market for scanning probe microscopes, in materials and nanomaterials research, 2010-2020 (US$), Optimistic estimateTable 38: Scanning probe microscopy market structureTable 39: Electron microscopy market structure

Future Markets, Inc.Future Markets, Inc. (www.futuremarketsinc.com) is an advanced technology consul-tancy with a focus on the development and commercialisation of nanomaterials and nanotechnology.

Tel +44 (0) 131 478 0921Fax +44 (0) 872 115 4084 Email: [email protected].

© Future Markets, Inc. 2014

MIC

ROSC

OPE

S • O

CTO

BER

201

3

4

EXECUTIVE SUMMARY The advanced microscopes market contin-ues to grow in developing markets.

F uture research and devel-opment needs are depen-dent upon the capacity of

instrumentation to measure, sense, fabricate, and manipulate matter at the nanoscale. Advanced micros-copy has the advantage over other characterisation techniques (e.g., bulk spectroscopy or electrical test-ing) in that it is descriptive, pro-ducing images of objects that are directly related to their structure, morphology, and composition, and hence it directly uncovers spatial heterogeneities. This is crucial in semiconductors, nanomaterials science, industrial R&D and life sciences. The total global micros-copy market in 2012 was over $4 billion. Scanning probe (SPM) and electron microscopes (EM) make up a significant proportion of this market. Market drivers for advanced microscopy include the increase in the complexity and performance level of devices used in electronic products, reduction of manufac-turing costs, increased resolution, increasing device complexity and shrinking geometries in materials research.

T rends in the scanning probe and electron microscopes market in 2012 were:

Revenues and sales (Electron Micro-scopes)• The electron microscopes market

in 2012 generated approximately US$2.08 billion in revenues (conser-vative estimate)• Approximately 2, 700 analytical Scanning Electron Microscopes (SEM) were sold in 2012. This is up from approximately 2,000 in 2010 and 2, 500 in 2011.• Approximately 1,600 non-analyt-ical SEMs (Critical Dimension SEMs utilized in semiconductors and electronics) were sold in 2012.• Approximately 345 Transmission Electron Microscopes were sold in 2012. More than 300 units have been sold per annum since 2009. Biotechnology is the fastest grow-ing market for TEM.• Approximately 163 Dual Beams were sold in 2012.• The total global electron beam

imaging instruments market was approximately $3.1 billion in 2012, including SEMs, TEMs, Dual-beam, FIB and Defect-Review SEM (FIB and DR-SEM are not covered in this report). • The Electron Microscopes market is dominated by global companies such as FEI, Hitachi, Carl Zeiss and JEOL Ltd. These companies sell the majority of their products to semiconductor and FA labs, with medium-high growth markets in the nanomaterials research and biomedical and life sciences sec-tors. Hitachi High-Technologies are the market leader in the world SEM market. FEI is the market leader in TEM.• The total serviceable available market for analytical techniques

EXECUTIVE SUMMARY

MIC

ROSC

OPE

S • O

CTO

BER

201

3

5

in 2012 was approximately $7.7 billion.

Revenues and sales (Scanning Probe Microscopes)• The SPM market in 2013 generated between $375million (conservative estimate) and $476 million (Opti-mistic) in revenues. Atomic Force Microscopes (AFM) accounted for the majority of this market with Scanning tunneling microscope (STM) making up less than 10%. STM and NSOM are more or less exclusively used in industrial and materials research. Main players in the market are Agilent Technolo-gies, Bruker Nano, Hitachi High-Tech Science Corporation (buy-out of SII Nanotechnology), NT-MDT, Oxford Instruments (buy-out of Asylum Research and Omicron Nanotech-nology) and Park Systems.

Competition• The advanced microscopy industry is highly competitive and character-ized by rapid technological change. There has been a major shift in SPM and EM design away from generic stands toward systems more dedi-cated to specific application areas and incorporating 3D imaging. Biology and natural resources such as oil, gas, and minerals have both been major targets for these new designs. In targeting the natural resources industry companies are also seeking to address a need for on-site rather than laboratory-based analysis.• Significant competitive factors include technical capability and differentiation (performance, range of features, reliability), productivity and cost-effectiveness. • Competitors range from small companies that compete with a single product and/or in a single region, to global, diversified compa-

nies with a range of products.

The market in 2013• There was a ‘‘mixed’’ market envi-ronment in 2013. While industrial markets appear to be stabilizing and academic markets outside of the United States remain mostly solid, there are weaknesses in mar-kets such as the semiconductor and data storage industries, the applied markets, and continued uncertainty in U.S. academic markets. • The US research sector has been hit by $85.4 billion in sequestration-related budget cuts and negative growth has returned to several key European states in early 2013. • Developing regions are of increas-ing importance in advanced mi-croscopy, with growing science and technology markets in India, Latin America, China, and Singapore.• Growth in electron microscopes, in 2013 is likely to be modest overall, as expansion in demand from new energy, new materials and other cutting-edge fields ahead of the next-generation of products in these sectors will counter falling demand from semiconductor and LCD-related sectors.

Target markets• The semiconductor and LCD-related sectors are cyclical and have experienced significant economic downturns at various times in the last decade. Such downturns have been characterized by diminished product demand, accelerated ero-sion of average selling prices and production overcapacity. There is expected decline 2013-2014 in this market, offset by growth new en-ergy and new materials markets. • The materials science market segment is also affected by overall economic conditions, but is not as

cyclical as the electronics market segment. • A weakness in semiconductor equipment spending was witnessed in the early part of 2012 and is ex-pected to continue into mid 2013. Industry decline was estimated at 8% in this end user sector in 2012, although some companies expe-rienced modest growth. This was primarily due to increased demand for certain products as the industry shifts to smaller semiconductor manufacturing process nodes. Cus-tomers are migrating from SEM-based to more TEM-based lab analysis. As nodes shrink in the semiconductors industry advanced microscopy will continue to grow; as a corollary to this 3D imaging is also becoming extremely impor-tant.• The Life Sciences market seg-ment is a smaller and still emerging market for advanced microscopes, and the tools companies sell to this market have average selling prices ranging from $0.1 million to over $5.0 million. There is an increased penetration in electron microscopy in Life Sciences market. This market has good potential for long-term growth despite occasional short-term revenues shortfalls. The Life Sciences market is heavily depen-dent on government funding for re-search grant. Historically there has been volatility in the sale of high-end microscopes for Life Sciences.• A significant portion of Materials Science and Life Sciences revenue for advanced microscopes com-panies is dependent on govern-ment investments in research and development of new technology. To the extent that governments, especially in Europe or the U.S., reduce their spending in response to budget deficits and debt limita-tions, demand for products could

MIC

ROSC

OPE

S • O

CTO

BER

201

3

6

be affected. AFM has also become important in nanomedicine, which focuses on imaging, early diagnosis, pathological tissue analysis, and drug delivery. A number of SPMmanufacturers produce AFMs for biological research.• Companies witnessed growth in sales in the materials science sector in 2012. • Companies witnessed growth in sales in the mining, oil and gas industries with automated mineral-ogy solutions that help those com-panies improve yields and lower costs. These are new solutions for both laboratory and on-site applica-tions that are in the early stages of penetration in these markets.• Growth has primarily come from developing countries such as China as these economies continue to invest in education infrastructure, offsetting potential weakness in the United States due to political uncertainty and a mixed economic picture in Europe.

Main players financial results 2012Agilent• Revenues for electronic measure-ment were $3.3 billion in 2012. • Electronic measurement orders declined 1% in 2012. • Orders increased 13% in Ameri-cas but declined 3% in Japan, 7% in Europe and 11% in Asia-Pacific excluding Japan• Year-over-year changes in commu-nications test demand contributed to the order growth in the Americas and the decline in Asia Pacific ex-cluding Japan. Electronic measure-ment orders increased 10 percent in 2011 compared to 2010. • Order growth in wireless manufac-turing, industrial, and computers and semiconductor test • Electronic measurement revenue increased 19 percent in 2011 com-

pared to 2010 on strong demand from industrial, computers and semiconductor, and wireless com-munications test • General purpose test revenue, rep-resenting approximately 63 percent of electronic measurement revenue, reflected slight growth in comput-ers and semiconductor business, flat industrial test demand, and a slight decline in aerospace and defense. • Growth in the computers and semiconductor business reflected continuing demand for digital test driven in part by the proliferation of high speed data transmission and increased investments in new semi-conductor processes and technol-ogy partially offset by a decline in semiconductor manufacturing.

Bruker Corporation• The mix of products sold in the Scientific Instruments segment dur-ing 2012 reflects increased demand from academic, government and industrial customers. • Increased revenue in 2012 on a year-over-year basis, but a softening in demand, particularly in Europe. • Weakening in global industrial and applied markets, as well as in the semiconductor and data stor-age metrology markets. • Continued growth in Bruker Nano Analytics division.

Carl Zeiss• The Microscopy business group, in which the light and electron micros-copy businesses have been com-bined since the beginning of fiscal year 2011/12, ended the reporting period with revenue totaling EUR 650m.• Revenue in the Microscopy busi-ness group rose five percent to EUR 650m (prior year on a like-for-like basis: EUR 620m). This development

was attributable not only to organic growth, but also to the integration of the electron microscopy business – previously part of the Semicon-ductor Manufacturing Technology business group – and to positive currency effects. • The Microscopy business group was faced with a difficult market environment in the debt-ridden industrial nations: many states re-duced their research and education budgets, with the funding of basic biomedical research suffering most from the cuts. Investments into ap-plied research, on the other hand, were increased. • The business with systems for ma-terials analysis and quality inspec-tion in industry continued to show a positive trend.• The business group was able to compensate for the subdued business trend in the established markets through strong growth in Asia – and in China, above all. • With correlative microscopy – the combination of light and electron microscopy – Carl Zeiss is offering a supplement to super-resolution microscopes. Super-resolution systems enable resolution of down to 20 nanometers compared to 250 nanometers in traditional light microscopes, allowing researchers to advance into totally new dimen-sions.

FEI• Revenue for 2012 was $891.7 mil-lion, compared with $826.4 million in 2011. • The largest segment in 2012 was Materials Science, which recorded 8% revenue growth to $315.5 million, along with 24% bookings growth. The Materials Science seg-ment includes traditional research customers and the emerging Natu-ral Resources business.

MIC

ROSC

OPE

S • O

CTO

BER

201

3

7

• Electronics revenue grew 13% to $293.1 million based on increasing demand for solutions as node sizes continue to shrink for semiconduc-tor customers. • Life Sciences revenue was $82.9 million, down 19% from 2011 with essentially level bookings. • Revenue from Asia and Japan made up 40% of the total and grew 15%. • North American revenue made up 33% of the total• European revenue made up 27% of the total.

Hitachi High-Technologies• Japan accounted for 42.4% of international sales, North America 12.9%, Europe 13.8%, Asia 28.6%, Other 2.3%• Science & Medical Systems posted a significant year on year increase in both sales and operating profit, as sales of scientific instruments grew as a result of the strong sales of new equipment, particularly electron mi-croscopes, and the biotechnology products/clinical analyzers business posted a large increase in sales, especially to overseas markets.

• Sales of scientific instruments rose sharply in fiscal 2011, buoyed by brisk sales of electron microscopes and other new products, particu-larly to emerging markets.

JEOL Ltd. • Net sales up 10% on previous years• Main markets remain China and Asia• Solid-growth in China • Lack of growth in Europe and the US due to financial problems in sev-eral south European countries and the downgrading of the US credit

Table 1: Global Electron Microscopes Market Revenues 2010-2020, (US$)

Year Conservative estimate Optimistic estimate

2010 1,902,500,000 2,462,500,000

2011 2,099,350,000 2,728,850,000

2012 2,208,000,000 2,873,050,000

2013 2,264,320,500 2,947,029,700

2014 2,322,820,385 3,023,951,215

2015 2,387,214,139 3,108,926,131

2016 2,457,171,629 3,201,250,876

2017 2,524,715,188 3,300,455,078

2018 2,613,183,240 3,407,380,037

2019 2,696,855,529 4,529,920,605

2020 2,783,397,190 4,841,346,108

Table 2: Global Scanning Probe Microscopes Market Revenues 2010-2020, (US$)

Year Revenues (Conservative) Revenues (Optimistic)

2010 355,000,000 450,000,000

2011 375, 000, 000 465,000,000

2012 385, 000, 000 480,000,000

2013 375,000,000 476,000,000

2014 384,000,000 480,000,000

2015 391,680,000 494,400,000

2016 403,430,400 509,232,000

2017 415,533,312 529,601,280

2018 430,076,978 558,729,350

2019 445,129,672 592,253,111

2020 460,709,211 630,749,564

MIC

ROSC

OPE

S • O

CTO

BER

201

3

8

T he research methodology initially encompassed a comprehensive and exhaustive search of the literature on advanced (electron and scanning

probe) microscopes, including annual reports. Second-ary sources included journals and related books, trade literature, marketing literature, technology roadmaps, other product/promotional literature, annual reports, analyst reports, conference proceedings and other pub-lications. An extensive patent analysis was conducted to gauge technological innovation and to determine research activity as it applies to new product develop-ment.

A series of interviews were conducted via email and phone with electron and scanning probe microscope company representatives, aca-

demics, technology suppliers, technical experts, trade association officials, and consulting companies. In addi-tion, service providers and end users were contacted to evaluate current and future demands. The market was then quantified relevant application impact and the main prerequisites for commercial success were identi-fied including performance of the technology, supplier distribution, legislation, pricing of competing products, sale of complementary products, industry environment and demographics of the customer. Market estimates and projections were based on the following:• Annual sales figures extrapolated from annual reports

from 2008-2013 and subsequently verified with micro-scope company representatives• Percentage of regional markets sold to, based on interviews with company representatives and available market data• Number of Electron and Scanning Probe Microscopes sold per annum based on interviews with microscope company representatives• Percentage of end user markets sold to, based on interviews and available market data• Future market projections based on interviews with company executives and growth rates extrapolated from historical data and projected government and private funding for end user markets.

Report methodology

METHODOLOGY

MIC

ROSC

OPE

S • O

CTO

BER

201

3

9

Electron microscopes (EM) use a beam of highly energetic electrons to examine objects on a very fine scale. Information is gathered from electrons transmitted through the sample, and from the charge absorbed by the sample. It is used mainly for objects with dimensions smaller than the wavelengths of vis-ible light, with linear magnification, approaching or exceeding a million. The electron microscopes market covers the following segments: • Scanning electron microscope (SEM)• Transmission electron microscope (TEM)• DualBeam Instruments

Electron microscopes meet broad-ranging demand not only in re-

search and development in nano-technology but also for material verification, evaluation, fault analy-sis, and quality control. In the last few years there has been the devel-opment of dedicated designs and modifications to electron micro-scope columns and also significant improvement of auxiliary attach-ments such as dedicated holders, stages, and reaction cells for various in situ processes. Vendors focus on providing advanced systems with special sampling handling capabili-ties in order to enable analysis of living cells. There is a growing demand for such systems with special environmental chambers from the biological and life sciences industries. In addition, the market has witnessed signif-

icant demand for integrated systems and custom solutions that provide additional capabilities to suit the needs of specific end-user applications.

Scanning Electron Microscopes (SEM)FEI, JEOL Ltd., Carl Zeiss MST A.G, Hitachi High Technologies and Tescan, A.S. are the main vendors selling SEMs. SEM account for the majority of electron microscopes sold at present, comprising over 75% of units sold globally in 2012. There is a high demand for SEMs across all major end-user groups. SEMs are also cheaper than TEMs and DuelBeams. However, TEMs are starting to take market share from SEMs as customers migrate from

Electron Microscopes

ELECTRON MICROSCOPES

MIC

ROSC

OPE

S • O

CTO

BER

201

3

10

SEM-based to more TEM-based lab analysis in semi-conductors, materials research and life sciences as the demand to image on an increasingly small scale continues.

PricePrices in the electron microscopes market have been rather steady since 2004, as the higher image resolu-tion and performance of this technique have led to increased acceptance, prominence, and popularity. SEMs are priced in the range of $100,000 to $1.25 mil-lion. Non-analytical SEMs (typically Critical Dimension SEMS used in Semiconductors and failure analysis labo-ratories, such as Hitachi’s CD-SEM) sell for approximate-ly $700,000 (FEI and Zeiss sell in this range). Analytical SEMs (typically FE-SEMs) sell from $370,000 (Carl Zeiss EVO HD 25 LS) to $610,000 (FEI Quanta 650 FEG). Prices can fluctuate depending on specification and augmen-tation of the particular model and is also negotiable in most instances, and when tendering for contracts com-panies often offer their product below regular market price. Purchase prices for SEMs are primarily dictated by resolution. Other factors that determine the price are automation, chamber size, and optional SEM accesso-ries, such as an elemental dispersive spectroscopy (EDS) system. The price difference between new and used SEMs can approach 50 percent or more, depending on the circumstances.

Benchtop SEMsBenchtop SEMs are priced at a relatively lower price, ranging from $65,000 to $125,000, since they are mainly targeted at the educational and academic institutions end user markets. Main players in the benchtop SEM market are Hitachi (TM‐1000) and Nikon/JEOL (Neo-Scope Benchtop SEM) and FEI (Phenom Desktop SEM). Delong (LVEM5), Pemtron (PS-230 and PS-250) and Agi-lent (8500 SEM) also produce benchtop SEMs. Agilent sell their system for approximately $175,000. In 2012, FEI acquired Aspex Corporation, a producer of the pSEM and Agilent Technologies bought over Novelx (mySEM) in 2010. Main end user market for benchtops are the physical/biological/chemical science research market, automotive manufacturers and pharmaceutical com-panies. Although benchtop SEMs offer a magnification range that is ahead of the range of traditional optical microscopes, they are not expected to replace existing

SEMs due to relatively lower performance in terms of sample specimen size and image resolution. However, being comparatively less expensive than the existing SEMs, these can be used in a variety of applications such as academic and educational research that usually utilize optical microscopes. These SEMs are most likely to suit the analysis of micro- and nano-scale structures of specimens in fields such as pathology and biology, and opportunities are expected to be created in indus-trial applications as well.

Market shareHitachi High-Technologies dominate the world SEM market. In 2012, it was estimated that Hitachi’s share of the critical dimension scanning electron microscope (CD-SEM) market was over 66%. CD-SEMs may expe-rience problems in semiconductors in the next few years due to scaling problems, with critical dimensions shrinking to the low nanometer level but will continue to be widely used. The main market for SEMs and semi-conductor manufacturing and failure analysis is in Asia, a market Hitachi also dominates in CD-SEM.

Transmission Electron Microscopes (TEM)Transmission Electron Microscopes (TEM) are much more expensive than SEMs, and are mainly utilized in high-end research such as molecular research, biologi-cal research, cancer research, and semiconductor re-search. A typical commercial microscope TEM costs $4-5 for each electronvolt(eV) of energy in the beam and with accessories up to $10 per eV. Most research uses beam energies in the range from 100,000 to 400,000 eV, making the TEM an extremely expensive piece of equipment, with total costs ranging between $1.3mil-lion-$13million. However depending on the specific-tions and contract tendered for, prices can be as low as $400,000. As of 2011 typical prices for TEMs from the main suppliers are $2.2-$2.9 million from FEI (Titan ChemiSTEM) and $2.8 million from Carl Zeiss (Libra 200HR). FEI is the market leader in TEM. The com-pany’s TEMs sell for up to $4.5million, their SEMs from $125,000. The company’s Titan TEM prices range from $1.5million to $4million, with average selling price of around $2,750,000. Including SEM, the company has over 10, 000 systems installed worldwide and over 3, 500 customers and has grown quickly in the last 5 years.

MIC

ROSC

OPE

S • O

CTO

BER

201

3

11

Total bookings were approximately $700 million in 2010. Approximate prices of other models are:• JEOL JEM-ARM 200FT: $3.4 million• FEI TITAN KRIOS S/TEM: $5million• FEI TECNAI T12 TEM: $1million• JEOL JEM 3010: $1.2 million

TEMs are in demand from a variety of sectors, with the main markets in semiconductors and data stor-age, materials failure analysis, materials R&D, quality control and growing markets in life sciences and oil and gas (natural resources) exploration. Semiconduc-tor manufacturers use TEMs to monitor product yield and process control, analyze defects, and investigate interface layer morphology. Generally, the TEM resolu-tion is about an order of magnitude greater than the SEM resolution, however, because the SEM image relies on surface processes rather than transmission it is able to image bulk samples and has a much greater depth of view, and so can produce images that are a good repre-sentation of the 3D structure of the sample. The only companies currently operating in the TEM market are Hitachi HIgh-Technologies, FEI Company, JEOL, and Carl Zeiss. FEI is the current market leader in TEM. The main drawback is that despite the advanced tech-nological capabilities of TEMs, the number of organiza-tions performing such high-end research is relatively small, resulting in low unit shipments and demand.Most TEM equipment providers have sought to imple-ment DualBeam systems and automate this process with software, significantly improving the sample con-sistency and overall throughput.

Dual Beam instruments (FIB-SEM)All major producers of electron microscopes produce these systems that have SEM and focus ion beam (FIB) capabilities on a single platform. Main products are• Dual Beam (FEI)• CrossBeam (Carl Zeiss)• MultiBeam (JEOL).

FIB-SEM represent the smallest market in terms of revenues for advanced microscopy at present, but their unit sales have been increasing. The segment is rela-tively new, and also higher in cost than both SEMs and TEMs. The application base for these instruments is also

currently small and they are mainly used in material characterization, industrial failure analysis and process control applications. However, it is expected to expand significantly during the next four years, which will increase the market share for DualBeam instruments. There has been a growing interest in dual beams for different areas related to renewables, as well as oil and gas.Dual beam prices vary-Laboratory level DuelBeams are sold by FEI from $300k up to $3,000,000 for wafer-level models. The Carl Zeiss Auriga CrossBeam sells for ap-proximately $1million. FEI’s market share in DualBeam systems, a product that the company invented, is esti-mated at over 75% in 2012. They have a large installed base in companies globally.

Market outlookIn the Materials Science sector there has been steady growth in 2012, with increased demand in Asia-Pacific. In the Life Sciences sector, growth has been variable among TEM and SEM manufacturers, but the market remains one of the key medium-term end user seg-ments and growth has been higher in the last few years than in other sectors. In semiconductors, companies are witnessing cyclical industry recovery that they expect to continue through 2014. Increased demand is ex-pected medium-to-long term as companies continue to shrink the dimensions of their products, develop new structures and use new materials. The natural resources market which has grown significantly in the last few years has levelled off in 2013 as mining customers cut back on their capital spending due to lower commodity prices and global uncertainty. In oil and gas there has been a similar pattern.

MIC

ROSC

OPE

S • O

CTO

BER

201

3

12

Table 3: Global Electron Microscopes Market Revenues 2010-2020, (US$)

Year Conservative estimate Optimistic estimate

2010 1,902,500,000 2,462,500,000

2011 2,099,350,000 2,743,650,000

2012 2,208,000,000 2,845,000,000

2013 2,264,320,500 3,062,051,100

2014 2,322,820,385 3,340,142,765

2015 2,387,214,139 3,522,247,949

2016 2,457,171,629 3,725,766,974

2017 2,524,715,188 3,930,674,813

2018 2,613,183,240 4,239,506,285

2019 2,696,855,529 4,529,920,605

2020 2,783,397,190 4,841,346,108

Table 4: Global Non-Analytical Scanning Electron Microscope Unit Sales, 2010-2020

Year Units

2010 1,500

2011 1,550

2012 1, 600

2013 1,634

2014 1,668

2015 1,703

2016 1,740

2017 1,780

2018 1,823

2019 1,867

2020 1,912

Table 5: Global Non-Analytical Scanning Electron Microscope Revenues, 2010-2020 (US$)

Year Conservative estimate* Optimistic estimate**

2010 787,500,000 975,000,000

2011 813,750,000 1,007,500,000

2012 840,000,000 1,040,000,000

2013 857,640,000 1,154,400,000

2014 875,650,440 1,310,244,000

MIC

ROSC

OPE

S • O

CTO

BER

201

3

13

Table 5: Global Non-Analytical Scanning Electron Microscope Revenues, 2010-2020 (US$)

Year Conservative estimate* Optimistic estimate**

2015 894,039,099 1,349,551,320

2016 913,707,959 1,396,785,616

2017 934,723,242 1,466,624,897

2018 957,156,600 1,542,889,392

2019 980,128,359 1,623,119,640

2020 1,003,651,439 1,707,521,861* Based on average price of $525, 000** Based on average price of $650, 000

Table 6: Global Analytical Scanning Electron Microscope Unit Sales, 2010-2020

Year Units

2010 2,000

2011 2,500

2012 2,700

2013 2,786

2014 2,878

2015 2,988

2016 3,107

2017 3,238

2018 3,380

2019 3,529

2020 3,684

Table 7: Global Analytical Scanning Electron Microscope Revenues, 2010-2020 (US$)

Year Conservative estimate* Optimistic estimate**

2010 500,000,000 700,000,000

2011 625,000,000 875,000,000

2012 675,000,000 945,000,000

2013 696,600,000 1,000,755,000

2014 719,587,800 1,060,800,300

2015 746,932,136 1,124,448,318

2016 776,809,422 1,191,915,217* Based on average price of $250, 000** Based on average price of $350, 000es, 2010

MIC

ROSC

OPE

S • O

CTO

BER

201

3

14

Table 7: Global Analytical Scanning Electron Microscope Revenues, 2010-2020 (US$)

Year Conservative estimate* Optimistic estimate**

2017 809,435,418 1,263,430,130

2018 845,050,576 1,345,553,089

2019 882,232,801 1,433,014,039

2020 921,051,045 1,526,159,952-2018 (US$)

Table 8: Global Transmission Electron Microscope Unit Sales, 2010-2020 (US$)

Year Units

2010 300

2011 327

2012 345

2013 354

2014 362

2015 372

2016 382

2017 393

2018 404

2019 416

2020 428

Table 9: Global Transmission Electron Microscope Revenues, 2010-2020 (US$)

Year Conservative estimate* Optimistic estimate**

2010 390,000,000 510,000,000

2011 425,100,000 555,900,000

2012 448,500,000 527,000,000

2013 459,712,500 553,350,000

2014 471,205,313 590,203,110

2015 483,456,651 641,314,699

2016 496,509,980 698,391,708

2017 510,412,260 761,945,353

2018 525,214,215 832,501,493

2019 540,445,427 909,591,131

2020 556,118,345 993,819,270* Based on average price of $1, 300, 000** Based on average price of $1, 700, 000enue

MIC

ROSC

OPE

S • O

CTO

BER

201

3

15

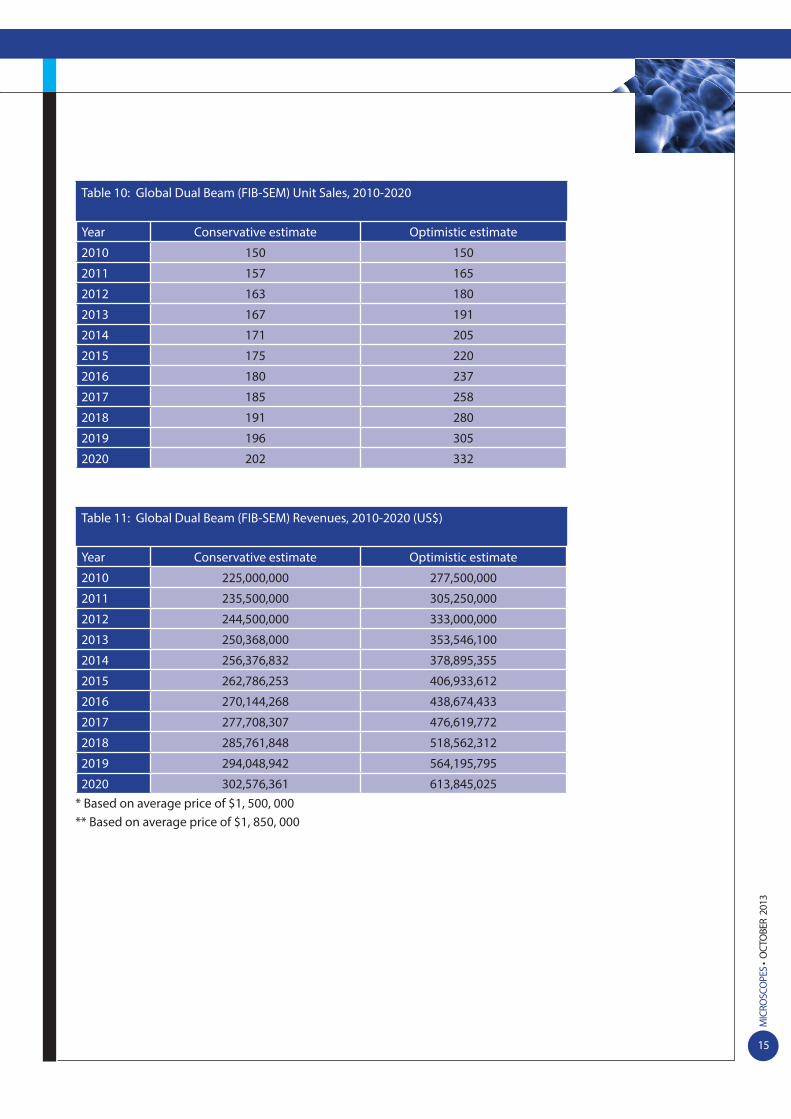

Table 10: Global Dual Beam (FIB-SEM) Unit Sales, 2010-2020

Year Conservative estimate Optimistic estimate

2010 150 150

2011 157 165

2012 163 180

2013 167 191

2014 171 205

2015 175 220

2016 180 237

2017 185 258

2018 191 280

2019 196 305

2020 202 332

Table 11: Global Dual Beam (FIB-SEM) Revenues, 2010-2020 (US$)

Year Conservative estimate Optimistic estimate

2010 225,000,000 277,500,000

2011 235,500,000 305,250,000

2012 244,500,000 333,000,000

2013 250,368,000 353,546,100

2014 256,376,832 378,895,355

2015 262,786,253 406,933,612

2016 270,144,268 438,674,433

2017 277,708,307 476,619,772

2018 285,761,848 518,562,312

2019 294,048,942 564,195,795

2020 302,576,361 613,845,025* Based on average price of $1, 500, 000** Based on average price of $1, 850, 000

MIC

ROSC

OPE

S • O

CTO

BER

201

3

16

The enormous and growing need to analyze three-dimensional topo-graphic images and resolve sur-face roughness on the nanometer scale has made AFMs essential in a wide range of end-user industries. AFM systems provide atomic or near-atomic resolution of material surface topography using a nano-scale probe that is brought into light contact with the sample being investigated. In addition to present-ing a surface image, AFM can also provide quantitative nanoscale measurements of feature sizes, ma-terial properties, electrical informa-tion, chemical properties and other sample characteristics. AFM systems are used for applications in mate-rials and biological research and semiconductor, data storage hard drive, LED, battery, solar cells, poly-mers and pharmaceutical product development and manufacturing.The scanning probe microscope market covers the following seg-

ments:• Atomic force microscopes (AFM)• Scanning tunneling microscopes (STM);• Near-field scanning optical micro-scopes (NSOM).

AFM is the most widely used sub-set of SPM, which can be used in ambient conditions with minimum sample preparation. The market share of AFMs/STMs is about 90% of all SPMs. Several tens of thou-sands of AFM instruments are in use worldwide. Prices for scanning probe micro-scopes range from under $100, 000 (AIST-NT SmartSPM-1000 Scanning Probe Microscope) to approxi-mately $290, 000 (Bruker Dimension Icon) for general purpose material science and device analysis instru-ments and around the same figure for SPMs for biological applica-tions. JPK Instruments AFMs sell for approximately $215, 000. THe JPK

Nanowizard 3 BioScience costs around $280,000 and the Oxford In-struments Atomic Force MFP 3D-Bio sells for around $305,000.

Market outlookThe majority of SPM users are in academia and government labora-tories. Nanotechnology measure-ment has boosted the market signif-icantly over the past decade. Academic customers in the typically rely on government agencies (e.g. in the United States the National Science Foundation, the National Institutes of Health, the Depart-ment of Energy and the Depart-ment of Defense) for funding. Most countries and the European Union have similar organizations that fund academic research. Materials research accounts for approximately 50% of SPM business globally with life sciences and semiconductors customers accounting for the rest of the market.

Scanning Probe Microscopes

SCANNING PROBE

MIC

ROSC

OPE

S • O

CTO

BER

201

3

17

In the research sector a significant trend is the in-creased requirement for instrumentation capable of measuring materials and their associated properties at the nanoscale. The ability to design and control material structures from the atomic to the micron scale is fun-damentally important to the creation of new materials and structures which have potential to reduce emis-sions, increase manufacturing yields and contribute to a longer and improved quality of life. Nanoscience continues to receive significant funding from the U.S. and other governments as well as from industry. Initia-tives in 2D nanomaterials will also contribute to growth. Government funding for science research in developing countries will also rise in the coming years. In 2012, demand from industrial and microelectronics/semiconductor customers in SPM was relatively flat. AFMs are used in the semiconductors to provide surface measurements on thin film magnetic heads and semiconductors. They are used to monitor the prod-ucts throughout the manufacturing process in order to improve product quality and reduce costs in industrial applications. Due to the ever increasing metrology re-quirements for 1X nm node fabrication, measurements of sub-10 nm defects are required and recognized as one of the challenges for blank and patterned wafers and masks. Scanning probe microscopy (SPM) has been

suggested as one of the technologies that can fulfil the future metrology and inspection requirements, because it has the distinct advantage of being able to discern in 3D the atomic structure of the substrate.AFMs are used in the manufacturing process to monitor product quality, process accuracy, and data repeatabil-ity. There is also a demand for SPM from polymer and metallurgy industries to determine characteristics such as molecular structure and polymer chains, corrosion resistance, defects, faults, cracks, and fatigue.The biomedical and life sciences sector is high growth market for SPM. With the development of sharper probe tips, there has been a huge improvement in resolu-tion and different imaging methods, due to which the technique has become highly suitable for the study and analysis of DNA structures.Main suppliers of vacuum STM/AFM are RHK-Technolo-gy, Omicron (Oxford Instruments), SPS-CreaTec GmbH, SPECS Surface Nano Analysis GmbH and Unisoku.

Table 12: Global Scanning Probe Microscopes Market Revenues 2010-2020, (US$)

Year Revenues (Conservative) Revenues (Optimistic)

2010 355,000,000 450,000,000

2011 375, 000, 000 465,000,000

2012 385, 000, 000 480,000,000

2013 375,000,000 476,000,000

2014 384,000,000 480,000,000

2015 391,680,000 494,400,000

2016 403,430,400 509,232,000

2017 415,533,312 529,601,280

2018 430,076,978 558,729,350

2019 445,129,672 592,253,111

2020 460,709,211 630,749,564* Due to fluctuations in prices of units sold, figures are based on total company revenues rather than number of units sold.

MIC

ROSC

OPE

S • O

CTO

BER

201

3

18

Table 13: Global Atomic Force Microscopes Market Revenues 2010-2020, (US$)

Year Revenues (Conservative) Revenues (Optimistic)

2010 323,050,000 409,500,000

2011 341,250,000 423,150,000

2012 350,350,000 436,800,000

2013 341,250,000 433,160,000

2014 349,440,000 436,800,000

2015 356,428,800 449,904,000

2016 367,121,664 463,401,120

2017 378,135,314 481,937,165

2018 419,245,382 508,443,709

2019 405,068,002 538,950,331

2020 419,245,382 573,982,103

MIC

ROSC

OPE

S • O

CTO

BER

201

3

19

Markets by region

T he North America advanced microscopy market is considered mature. Developing Asian markets such as China, Korea, India, and Taiwan are ex-

periencing good growth. The developments in nano-technology, material science and life sciences, heavily backed by government investment, drive interest in advanced microscopy, in addition to the improvements in software design and increased degrees of automa-tion in end-user industries. The main regional market for EM and SPM is Asia-Pacif-ic, and it is also the fastest growing market, with robust sales in Japan and China and an emerging market in India. Brazil and Russia are also emerging forces backed by increased budgets for scientific infrastructure and nanotechnology and nanomaterials research. The growth in the advanced microscopy sector has been aided by continued government R&D spending despite the fallout from the financial crisis. Most countries with significant R&D budgets will either increase or main-tain the same level of R&D spending in the coming years. Spending levels with only decrease in relatively insignificant markets for advanced microscopy. Global R&D spending increased in 2012 with continued strong growth in emerging economies and stable growth in established economies. The US market however will be affected by significant budget cuts for research.

Electron MicroscopesMost companies witnessed renewed growth in the North American market in 2010. The United States after Japan, is the second largest country market for elec-tron microscopes. In 2005, developed regions (North America, Western Europe and Japan) constituted 2/3rds of the the market for electron microscopes. In 2012, the ratio is around 50/50 with developing regions (Asia, Eastern Europe, Middle East, Latin America, Africa).Prior to the economic recession, Europe was the market most likely to experience reasonable growth to 2017. Nanotechnology and life sciences are key funding areas for the EU and countries such as Germany, the Nether-lands and the UK. Developing markets in Asia-Pacific for EM include Chi-na, India, South Korea. A number of EM suppliers have

expanded into BRICs (Brazil, Russia, India, and China) countries. The semiconductors market in Asia recovered remarkably quickly from the economic downturn. Asia-Pacific will remain the main market for the fore-seeable future. As result of the abundant material and manpower resources, countries such as China, South Korea, India, Taiwan, and Thailand have been growing in prominence in the industrial segment. With the need to develop and improve infrastructure in the region, demand for electron microscopes has been steadily increasing. The region is considered to be the manufac-turing hub of the world at present, offering significant opportunities for electron microscopes especially in the semiconductors market. Companies are witnessing increased revenues to smaller, developing countries where nanotechnology is being funded by govern-ments.Latin America is an emerging market for electron micro-scopes, although starting from a low base. Government towards development and promotion of nanotechnol-ogy research and growing interest of pharmaceutical and biotechnology companies towards expansion of their global clinical trials projects to the Latin American region are drivers for this market. Main markets are in Brazil, Mexico and Argentina. The Middle East is also a relatively new market for advanced microscopy prod-ucts with growing research, nanotechnology, education and industrial sectors. Companies are selling products in these regions for use in the mining and oil and gas exploration market. Oil and gas is a relatively small proportion of the advanced microscopes market, but is likely to grow in the coming years. 5% of FEI’s micros-copy sales are in this market (natural resources). More than $1 billion a year is now spent on analyzing par-ticles of rock brought up from the surface. Restructuring and consolidation has led to a new focus for the semiconductor manufacturers in Japan. As a re-sult, the semiconductor equipment market in Japan will experience double-digit growth in both 2013 and 2014, driven by higher spending for memory production and in spending increases planned for the manufacturing of power semiconductors and “More than Moore” semicon-ductor technologies .

REGIONS

MIC

ROSC

OPE

S • O

CTO

BER

201

3

20

Total equipment spending in Japan is estimated to reach $4.6 billion by 2014. Combining this with the $8 billion-plus spending on semiconductor materials, Japan represents a $12 billion market in 2014 for the suppliers of equipment and materials.

Scanning Probe MicroscopesThe United States is the second-largest market for scanning probe microscopes, behind Japan. There are numerous government, academic and industrial activi-ties in nanotechnology, material sciences research, and life sciences and bio in these countries. Asia-Pacific is the largest and fastest-growing market for SPM. China and Russia are growth markets backed by increased budgets for scientific infrastructure and nanotechnology/nanomaterials research. The govern-ment strategy in these countries is aimed at building an innovative economies that support IT-related industries and scientific institutions and academia. China is now

a significant world player in science and technology, the third largest R&D performer. Other growing mar-kets are in South Korea and of India with government’s providing larger R&D budgets year-on-year. Demand is increasing in these countries for easy to operate sys-tems in the sub-micron to nanometer range, for use in materials development and inspection applications. The main markets for SPM in Latin America and the Middle East are in universities and research centers. Improvement in economic conditions in the Latin American markets is a key driver for AFM demand in the region. Increased manufacturing and inspection activi-ties in Brazil, Mexico, South Africa, and the Middle East are other key factors driving growth.Asia-Pacific accounts for approximately 35-40% of SPM sales. North America and Europe make up approxi-mately 55%. Broad market share for SPM is 40% from applied/industrial customers and 60% from academic/government customers.

Table 14: Global R&D Expenditure 2012, Billion US$ (Source: Battelle)

Americas Total 505.6

U.S. 436.0

Asia 514.4

Japan 157.6

China 198.9

India 41.3

Europe 338.1

Rest of World 44.5

Table 15: Global R&D Expenditure 2012 Top 10 countries, Billion US$ (Source: Battelle)

1. United States 436.0

2. China 198.9

3. Japan 157.6 494,650,000

4. Germany 90.6

5. South Korea 56.4

6. France 51.1

7. UK 42.4

8. India 41.3

9. Brazil 30

10. Canada 28.6

MIC

ROSC

OPE

S • O

CTO

BER

201

3

21

Table 16: Market for electron microscopes, by region, 2010-2020, Conservative estimate, (US$)

YEAR North America Asia-Pacific Europe RoW

2010 494,650,000 951,250,000 418,550,000 38,050,000

2011 524,837,500 1,091,662,000 440,863,500 41,987,000

2012 511,011,997 1,174,137,314 470,485,329 52,365,360

2013 498,150,510 1,222,733,070 486,828,908 56,608,013

2014 511,020,485 1,277,551,211 464,564,077 69,684,612

2015 525,187,111 1,312,967,776 477,442,828 71,616,424

2016 540,577,758 1,351,444,396 491,434,326 73,715,149

2017 557,101,430 1,392,753,575 506,455,845 88,629,773

2018 574,900,313 1,424,184,866 522,636,648 91,461,413

2019 593,308,216 1,456,301,986 539,371,106 107,874,221

2020 612,347,382 1,503,034,483 556,679,438 111,335,888

Table 17: Market for electron microscopes, by region, 2010-2020, Optimistic estimate, (US$)

YEAR North America Asia-Pacific Europe RoW

2010 640,250,000 1,231,250,000 541,750,000 49,250,000

2011 685,912,500 1,426,698,000 573,058,500 54,873,000

2012 654,350,000 1,507,850,000 597,450,000 85,350,000

2013 673,651,242 1,653,507,594 658,340,987 76,551,278

2014 734,831,408 1,837,078,521 668,028,553 100,204,283

2015 774,894,549 1,937,236,372 704,449,590 105,667,438

2016 819,668,734 2,049,171,836 745,153,395 111,773,009

2017 873,096,433 2,182,741,084 793,724,030 119,058,605

2018 932,691,383 2,310,530,925 847,901,257 148,382,720

2019 996,582,533 2,446,157,127 905,984,121 181,196,824

2020 1,065,096,144 2,614,326,898 968,269,222 193,653,844

MIC

ROSC

OPE

S • O

CTO

BER

201

3

22

Scanning Probe MicroscopesThe United States is the second-largest market for scanning probe microscopes, behind Japan. There are numerous government, academic and industrial activi-ties in nanotechnology, material sciences research, and life sciences and bio in these countries. Asia-Pacific is the largest and fastest-growing market for SPM. China and Russia are growth markets backed by increased budgets for scientific infrastructure and nanotechnology/nanomaterials research. The govern-ment strategy in these countries is aimed at building an innovative economies that support IT-related industries and scientific institutions and academia. China is now a significant world player in science and technology, the third largest R&D performer. Other growing mar-kets are in South Korea and of India with government’s

providing larger R&D budgets year-on-year. Demand is increasing in these countries for for easy to operate systems in the sub-micron to nanometer range, for use in materials development and inspection applications. The main markets for SPM in Latin America and the Middle East are in universities and research centers. Improvement in economic conditions in the Latin American markets is ae key driver for AFM demand in the region. Increased manufacturing and inspection activities in Brazil, Mexico, South Africa, and the Middle East are other key factors driving growth.Asia-Pacific accounts for approximately 45% of SPM sales. North America and Europe make up approxi-mately 52%. Broad market share for SPM is 40% from applied/industrial customers and 60% from academic/government customers.

Table 18: Market for scanning probe microscopes, by region, 2010-2020 (US$), Conservative estimate

YEAR North America Asia-Pacific Europe RoW

2010 71,000,000 170,400,000 106,500,000 7,100,000

2011 75,000,000 180,000,000 112,500,000 7,500,000

2012 80,850,000 180,950,000 115,500,000 7,700,000

2013 85,900,000 172,400,000 108,050,000 8,650,000

2014 88,320,000 176,640,000 107,520,000 11,520,000

2015 90,539,095 181,078,191 106,285,025 13,777,688

2016 92,788,992 185,577,984 108,926,208 16,137,216

2017 95,572,662 191,145,324 108,038,661 20,776,666

2018 98,917,705 197,835,410 111,820,014 21,503,849

2019 97,928,528 204,759,649 120,185,011 22,256,484

2020 101,356,026 211,926,237 124,391,487 23,035,461

Table 19: Market for scanning probe microscopes, by region, 2010-2020 (US$), Optimistic estimate

YEAR North America Asia-Pacific Europe RoW

2010 90,000,000 216,000,000 135,000,000 9,000,000

2011 93,000,000 223,200,000 139,500,000 9,300,000

2012 100,800,000 225,600,000 144,000,000 9,600,000

2013 109,035,733 218,833,067 137,151,467 10,979,733

2014 110,400,000 220,800,000 134,400,000 14,400,000

2015 114,283,417 228,566,834 134,158,794 17,390,955

MIC

ROSC

OPE

S • O

CTO

BER

201

3

23

Table 19: Market for scanning probe microscopes, by region, 2010-2020 (US$), Optimistic estimate

2016 117,123,360 234,246,720 137,492,640 20,369,280

2017 121,808,294 243,616,589 137,696,333 26,480,064

2018 128,507,751 257,015,501 145,269,631 27,936,468

2019 130,295,685 272,436,431 159,908,340 29,612,656

2020 138,764,904 290,144,799 170,302,382 31,537,478

MIC

ROSC

OPE

S • O

CTO

BER

201

3

24

The semiconductor industry is the primary market for EM and a major market for SPM. Demand in the semiconductors industry is from customers in semiconductor inte-grated circuit manufacturing and related industries such as manufac-turers of data storage equipment and other technologies. The market is extremely volatile; recently year-to-year variation has been a factor of three.Growth is driven by shrinking line widths and process nodes of 32 nanometers and smaller, increasing complexity in their materials such as high-k metal gates and low-k dielectrics and increasing device complexity such as 3D transis-tor architectures. There is also an increased demand for TEM-FIB for sample preparation and analysis.Advanced microscopy products are used primarily in laboratories or near the fabrication line to speed new product development and in-crease yields by enabling 3D wafer metrology, defect analysis, root cause failure analysis and circuit edit for modifying device function-ality. Trends in semiconductors and data storage that impact EM and SPM include: • Need for defect free IC• Decreasing feature size (22 nm towards 10 nm Node)• Wafers are getting bigger• Equipment should be better de-signed to avoid contamination• Increase in complexity and perfor-mance level of devices

Global semiconductors marketTotal semiconductor revenue world-

wide will see improved growth this year of 6.9%, reaching $320 billion, according to the mid-year 2013 up-date from International Data Corp. IDC also forecasts that semiconduc-tor revenues will grow 2.9% year over year in 2014 to $329 billion and log a compound annual growth rate (CAGR) of 4.2% from 2012-2017, reaching $366 billion in 2017. The semiconductor equipment sector is between $3-$4billion. Gartner has predicted that semiconductor equipment spending is expected to fall by 6% in 2013, but will pick up by the end of the year and is ex-pected to increase by 14% in 2014. The advanced microscopy market will benefit from both the cyclical rebound in overall semiconduc-tor spending as well as the secular trend of increased capital intensity for process control in advanced semiconductor nodes.Although it is forecast in 2013 that overall semiconductor equipment spending will be down , most microscopy companies believe that the downturn has bottomed and that the industry is at or near the beginning of the next investment upswing.Process control has emerged as a secular trend within the overall cyclical semiconductor capital equipment industry, driven by com-plex chip architectures, geometry shrinks and wafer migration. Companies anticipate a recovery in the last quarter of 2013, driven by growth in mobile and an upsurge in consumer/enterprise spending. There will also be an increase in semiconductor spending in Ja-

pan which is expected to show double-digit growth in both 2013 and 2014, driven by higher spend-ing for memory production and in spending increases planned for the manufacturing of power semicon-ductors and “More than Moore” semiconductor technologies. Leading the investment activity in Japan is Flash Alliance, a joint-ven-ture between Toshiba and Sandisk. According to the SEMI World Fab Forecast database, equipment spending for Flash Alliance could approach $2 billion this year and even more in 2014 because of the overall strong market demand for NAND flash in mobile products. Toshiba has announced plans to spend up to $300 million (30B yen) to construct the Fab 5 phase 2 at the Yokkaichi plant location. This fab will ramp for production of sub-20 nm/3D flash memories, with building construction completed by 2014 summer.In the next ten years the semicon-ductor market has been predicted to grow by approximately 14% per year in the silicon area, while the complexity will keep increasing with a rapid pace. The number of process steps and use of diverse materials will increase, which will helped to continue the growth in the advanced microscopy markets. As a result of “more Moore”, me-trology and characterization of semiconductor products become more critical since the features to be observed are becoming so small that imaging requires advanced microscopy equipment. Although the semiconductor equip-

Semiconductors and data stor-age

SEMICONDUCTORS

MIC

ROSC

OPE

S • O

CTO

BER

201

3

25

ment industry is highly cyclical there is an overall growth trend (excluding the fallout from the 2008/2009 financial crisis)- succes-sive peak and trough are higher than the preceding peaks and troughs. The requirement for more sophisticated equipment for each successive node creates these growth cycles in semiconductor

capital equipment.Hitachi-High Technologies is the lead supplier in CD-SEM in semi-conductors with over 66% of the market in 2012; FEI has the largest market share in TEM and is aggres-sively expanding in this market with a number of new product launches in 2013; and Park Systems has a significant market share in AFM in

semiconductors and data storage. According to the company they dominate the AFM hard disc market with a 90% market share.

SEMICONDUCTORS

Table 20: Global market for scanning electron microscopes, in semiconductors and data storage, 2010-2020 (US$), Conservative estimate

YEAR Revenues (US$)

2010 912,500,000

2011 951,250,000

2012 988,500,000

2013 1,003,926,000

2014 1,026,763,878

2015 1,050,894,848

2016 1,069,069,844

2017 1,104,704,680

2018 1,134,617,221

2019 1,165,397,247

2020 1,197,072,159

Table 21: Global market for scanning electron microscopes, in semiconductors and data storage, 2010-2020 (US$), Optimistic estimate

YEAR Revenues (US$)

2010 1,150,000,000

2011 1,200,000,000

2012 1,247,900,000

2013 1,364,558,550

2014 1,533,012,063

2015 1,585,685,467

2016 1,635,168,660

2017 1,466,624,922

2018 1,825,455,540

2019 1,963,975,624

2020 2,028,015,451

MIC

ROSC

OPE

S • O

CTO

BER

201

3

26

SEMICONDUCTORS

Table 22: Global market for transmission electron microscopes, in semiconductors and data stor-age, 2010-2020 (US$), Conservative estimate

YEAR Revenues (US$)

2010 148,200,000

2011 161,538,000

2012 170,430,000

2013 165,496,500

2014 169,633,913

2015 169,209,828

2016 173,778,493

2017 178,644,291

2018 183,824,975

2019 189,155,900

2020 194,641,421

Table 23: Global market for transmission electron microscopes, in semiconductors and data stor-age, 2010-2020 (US$), Optimistic estimate

YEAR Revenues (US$)

2010 193,800,000

2011 211,242,000

2012 200,260,000

2013 199,206,000

2014 212,473,120

2015 224,460,145

2016 244,437,098

2017 266,680,874

2018 291,375,522

2019 318,356,896

2020 347,836,744

MIC

ROSC

OPE

S • O

CTO

BER

201

3

27

SEMICONDUCTORS

Table 24: Global market for scanning probe microscopes, in semiconductors and data storage, 2010-2020 (US$), Conservative estimate

YEAR Revenues (US$)

2010 99,400,000

2011 105,000,000

2012 107,800,000

2013 100,300,000

2014 96,000,000

2015 94,003,200

2016 96,823,296

2017 95,572,662

2018 98,917,705

2019 102,379,825

2020 105,963,118

Table 25: Global market for scanning probe probe microscopes, in semiconductors and data storage, 2010-2020 (US$), Optimistic estimate

YEAR Revenues (US$)

2010 112,500,000

2011 120,900,000

2012 116,250,000

2013 123,950,000

2014 120,000,000

2015 118,656,000

2016 122,215,680

2017 121,808,294

2018 128,507,751

2019 136,218,216

2020 145,072,400

MIC

ROSC

OPE

S • O

CTO

BER

201

3

28

The materials and nanomaterials cience market segment includes universities, public and private research laboratories and custom-ers in a wide range of industries, including natural resources (mining and oil and gas), petrochemicals, metals, automobiles, aerospace, fiber optics, polymers, ceramics, solar, thin films and forensics. Ad-vanced microscopy is fundamental for the exploitation and control of nanostructures and -systems.

DriversGrowth in the materials and nano-materials academic and industrial research segment is driven by a number of factors. In the academic research segment these include:• Worldwide government and pri-vate spending • The number of nanotech centers continues to grow and they have equipment requirements for char-acterization, prototyping and in-situ process development• Third world using tech to move to the first world• Increased global nanotechnology investment. Nanotech research is also linked to important govern-ment societal issues (energy, sus-tainability, environment)• Research institutes demanding leading-edge tools.Materials researchers seek to understand the structure-function relationships and chemical compo-sition down to the atomic level. Full characterization is more difficult due to decreasing feature sizes and increasingly complex architectures. Growth in these markets is driven

by global corporate and govern-ment funding for research and de-velopment in materials science and by development of new products and processes based on innovations in materials at the nanoscale. Ad-vanced microscopy enables scien-tific discovery and advancement for researchers and help manufacturers develop, analyze and produce ad-vanced products. Usage is growing mining for automated mineralogy and their are increased opportu-nities in oil and gas exploration and laboratory analysis. Advanced microscopy products are also used in root cause failure analysis and quality control applications across a range of industries.

NanotechnologyGrowth in nanotechnology and nanomaterials applications is having a significant impact on most high-tech industries, creat-ing opportunities for advanced microscopes. Nanostructured materials are becoming increas-ingly important in micromechanical, electronic, and magnetic devices. Low dimensional materials, such as nanotubes, nanowires, and other nanoparticles have properties that could provide solutions for emerg-ing research devices, lithography, front end process, interconnects, and assembly and packaging for the semiconductors. Nanotechnology requires removal and deposition to produce features of 100nm or less, which is within the range of most failure analysis technology. AFM, SEM and TEM are key instruments for the nanotechnology/nanomate-

rials market. The enormous need to analyze three-dimensional topo-graphic images and resolve surface roughness on the nanometer scale has made AFMs essential in a wide range of end-user industries. Trends in metrology that impact SPM include:• Throughput of current state-of-the-art SPMs are extremely low• Increased metrology requirements at the nanoscale• Amount of necessary metrology steps is increasing, it needs to be fast and simple.

Market outlookThe materials and nanomaterials research (academic and industrial) segment is a prime market for ad-vanced microscopy and will remain stable in the coming years with continued investment in develop-ing countries, stable funding in developed countries and new ap-plications in the coming years. The natural resources sector is viewed as a key medium-term growth mar-ket as the need for sophisticated analysis to improve yields becomes greater as resources deplete.

Materials and nanomaterials re-search

MATERIALS RESEARCH

MIC

ROSC

OPE

S • O

CTO

BER

201

3

29

MATERIALS RESEARCH

Table 26: Global market for scanning electron microscopes, in materials and nanomaterials research, 2010-2020 (US$), Conservative estimate

YEAR Revenues (US$)

2010 325,000,000

2011 406,250,000

2012 438,750,000

2013 459,756,000

2014 474,927,948

2015 485,505,889

2016 504,926,124

2017 518,038,667

2018 540,832,369

2019 564,628,993

2020 589,472,669

Table 27: Global market for scanning electron microscopes, in materials and nanomaterials research, 2010-2020 (US$) Optimistic estimate

YEAR Revenues (US$)

2010 455,000,000

2011 568,750,000

2012 614,250,000

2013 660,498,300

2014 700,128,198

2015 730,891,407

2016 774,744,891

2017 808,595,283

2018 861,153,977

2019 1,038,799,190

2020 976,742,369

Table 28: Global market for transmission electron microscopes, in materials and nanomaterials research, 2010-2020 (US$), Conservative estimate

YEAR Revenues (US$)

2010 195,000,000

2011 212,550,000

2012 224,250,000

2013 225,259,125

MIC

ROSC

OPE

S • O

CTO

BER

201

3

30

MATERIALS RESEARCH

Table 28: Global market for transmission electron microscopes, in materials and nanomaterials research, 2010-2020 (US$), Conservative estimate

2014 221,466,497

2015 227,224,626

2016 228,394,591

2017 234,789,639

2018 241,598,539

2019 248,604,897 9

2020 255,814,439

Table 29: Global market for transmission electron microscopes, in materials and nanomaterials research, 2010-2020 (US$), Optimistic estimate

YEAR Revenues (US$)

2010 255,000,000

2011 277,950,000

2012 263,500,000

2013 271,141,500

2014 277,395,462

2015 301,417,909

2016 321,260,185

2017 350,494,862

2018 382,950,687

2019 418,411,920

2020 457,156,864

Table 30: Global market for scanning probe microscopes, in materials and nanomaterials re-search, 2010-2020 (US$), Conservative estimate

YEAR Revenues (US$)

2010 191,700,000

2011 202,500,000

2012 200,200,000

2013 200,900,000

2014 211,200,000

2015 219,340,800

2016 225,921,024

2017 236,853,988

2018 245,143,877

2019 253,723,913

MIC

ROSC

OPE

S • O

CTO

BER

201

3

31

MATERIALS RESEARCH

Table 30: Global market for scanning probe microscopes, in materials and nanomaterials re-search, 2010-2020 (US$), Conservative estimate

2020 262,604,250

Table 31: Global market for scanning probe microscopes, in materials and nanomaterials re-search, 2010-2020 (US$), Optimistic estimate

YEAR Revenues (US$)

2010 256,500,000

2011 260,400,000

2012 264,000,000

2013 256,850,000

2014 264,000,000

2015 276,864,000

2016 285,169,920

2017 301,872,730

2018 318,475,730

2019 337,584,274

2020 359,527,251

MIC

ROSC

OPE

S • O

CTO

BER

201

3

32

The Life Sciences market segment includes universities, government laboratories and research institutes engaged in biotech and life sciences applications, as well as pharmaceu-tical, biotech and medical device companies and hospitals. The majority of the market is made up by research institutes and uni-versities; however there is a grow-ing market in pharma and biotech.Ultrahigh resolution imaging al-lows structural biologists to create detailed 3D reconstructions of complex biological structures such as proteins and viruses.

Electron microscopesCellular biologists use electron microscopes to correlate wide-field, lower resolution optical images with higher resolution electron microscope imaging. Products are also used by drug researchers and in particle analysis and a range of pathology and quality control ap-plications.TEM and SEM seek to simplify atomic level structural analyses in

biology, medicine, pharmaceuti-cals. The particle and size distribu-tion characteristics of a drug will often have an impact on the rate of delivery in the body. Regulatory bodies (e.g. FDA) have a stringent requirement of understanding the chemical and physical characteris-tics of drug particles and potential contaminants as part of the drug validation process. Historically, optical light microscopy has been sufficient, however in the last few years the regulatory authorities are increasingly insisting on character-izing finer particles and agglomer-ates unresolvable in transmission or reflection by optical microscopy. FEI, JEOL, Hitachi, and Carl Zeiss SMT all produce electron micro-scopes for life science research. There has been faster percentage growth in the life sciences market than any other in the past 4 years.

Scanning probe microscopesBiophysics is driving new interest in both the cell membrane and in measuring the cell’s nano-mechan-

ical properties, both at the cellular and molecular level. This shift is opening new life science opportuni-ties for atomic force microscopy (AFM). AFM is used widely with biological specimens and in drug discovery for the visualization, probing and manipulation of biological systems from living cells down to single molecules. AFM measurements can be carried out in buffer solution under physiological conditions, which is crucial to study the structure and function of bio-logical objects. AFM is used in cell biology, biochemistry, biomedicine, molecular biology, pharmaceutical industry, cancer research, virology, microbiology, etc. • AFM offers a number of advan-tages in life sciences:• it requires no dehydration, sample labelling or surface coating• operates well in liquids and on live cells• can detect at the single-molecule level• extends XY resolution to the na-noscale.

Life Sciences

LIFE SCIENCES

Table 32: Global market for scanning electron microscopes, in life sciences, 2010-2020 (US$), Con-servative estimate

YEAR Revenues (US$)

2010 50,000,000

2011 81,250,000

2012 87,750,000

2013 90,558,000

2014 93,546,414

2015 104,570,499

2016 116,521,413

2017 121,415,313

2018 126,757,586

MIC

ROSC

OPE

S • O

CTO

BER

201

3

33

LIFE SCIENCES

Table 32: Global market for scanning electron microscopes, in life sciences, 2010-2020 (US$), Con-servative estimate

2019 132,334,920

2020 138,157,657

Table 33: Global market for scanning electron microscopes, in life sciences, 2010-2020 (US$), Opti-mistic estimate

YEAR Revenues (US$)

2010 70,000,000

2011 113,750,000

2012 122,850,000

2013 130,098,150

2014 137,904,039

2015 157,422,765

2016 178,787,283

2017 189,514,520

2018 201,832,963

2019 243,468,560

2020 228,923,993

Table 34: Global market for transmission electron microscopes, in life sciences, 2010-2020 (US$), Conservative estimate

YEAR Revenues (US$)

2010 46,800,000

2011 51,012,000

2012 53,820,000

2013 68,956,875

2014 84,816,956

2015 87,022,197

2016 94,336,896

2017 96,978,329

2018 99,790,701

2019 102,684,631

2020 105,662,486

MIC

ROSC

OPE

S • O

CTO

BER

201

3

34

LIFE SCIENCES

Table 35: Global market for transmission electron microscopes, in life sciences, 2010-2020 (US$), Optimistic estimate

YEAR Revenues (US$)

2010 61,200,000

2011 66,708,000

2012 63,240,000

2013 83,002,500

2014 100,334,529

2015 115,436,646

2016 132,694,424

2017 144,769,617

2018 158,175,284

2019 172,822,315

2020 188,825,661

Table 36: Global market for scanning probe microscopes, in materials and nanomaterials re-search, 2010-2020 (US$), Conservative estimate

YEAR Revenues (US$)

2010 191,700,000

2011 202,500,000

2012 200,200,000

2013 200,900,000

2014 211,200,000

2015 219,340,800

2016 225,921,024

2017 236,853,988

2018 245,143,877

2019 253,723,913

2020 262,604,250

Table 37: Global market for scanning probe microscopes, in materials and nanomaterials re-search, 2010-2020 (US$), Optimistic estimate

YEAR Revenues (US$)

2010 256,500,000

2011 260,400,000

2012 264,000,000

2013 256,850,000

2014 264,000,000

MIC

ROSC

OPE

S • O

CTO

BER

201

3

35

LIFE SCIENCES

Table 37: Global market for scanning probe microscopes, in materials and nanomaterials re-search, 2010-2020 (US$), Optimistic estimate

2015 276,864,000

2016 285,169,920

2017 301,872,730

2018 318,475,730

2019 337,584,274

2020 359,527,251

MIC

ROSC

OPE

S • O

CTO

BER

201

3

36

Table 38: Scanning probe microscopy market structure

Category Description

Competitors Leading companies (alphabetical order)• Agilent Technologies• Bruker Nano• Hitachi High-Tech Science Corporation• NT-MDT• Oxford Instruments/Asylum Research• Park Systems

Other manufacturers• AIST-NT• Anasys Instruments• Anfatec• Angstrom Advanced Inc. • APE research srl• JPK Instruments• Kleindiek Nanotechnik• Multiprobe, Inc.• Nanonics Imaging• Nanoscan• Nanosurf• Nanotec Electronica• RHK Technology • Shimadzu• SPECS Surface Nano Analysis GmbH (Vacuum STM/AFM)• SPS-CreaTec (LT-STM)• Techscience Ltd.• Unisoku• Witec

Types of competitors • Large instrumentation companies marketing and selling products on a global basis and via distributors• Medium-sized and small private companies mainly selling on a regional basis or on a price competitive basis in niche microscope markets

Means of distribution • Direct sales by companies • Distribution through third parties usually on a regional basis

End user markets • Semiconductors and electronics• Biomedical research and life sciences• Nanotechnology and nanomaterials research• Industrial R&D• Research labs and academia • Failure analysis labs

Scanning Probe Microscopy mar-ket structure

MIC

ROSC

OPE

S • O

CTO

BER

201

3

37

Table 39: Electron microscopy market structure

Category Description

Competitors Leading companies (alphabetical order)• Carl Zeiss SMT• FEI Company• Hitachi High-Technologies• JEOL

Other manufacturers• Agilent (FE-SEM)• Tescan s.r.o.

Types of competitors • Large instrumentation companies marketing and selling products on a global basis and via distributors (Plus Tescan)