the geography of the scottish knowledge economy€¦ · the local futures group 3 queen square...

TRANSCRIPT

the local futures group 3 Queen Square London WC1N 3AU

T +44 020 75208120 F +44 020 7520 8150

The Geography of the Scottish Knowledge Economy

A report prepared for Scottish Enterprise

August 2004

Mark Hepworth

Lee Pickavance

Contents

the local futures group

Contents

Contents....................................................................................................................................................................... i Acknowledgements...................................................................................................................................................... I Executive Summary.................................................................................................................................................... II

Aims ........................................................................................................................................................................ II Research and Policy Contexts ............................................................................................................................... II The Analysis .......................................................................................................................................................... III Stakeholder Views..................................................................................................................................................V A Spatial Framework for Scotland’s Knowledge Economy...................................................................................VI

1 Introduction ......................................................................................................................................................... 7 1.1 Background to the Study............................................................................................................................ 7 1.2 This Report ................................................................................................................................................. 8

2 The Knowledge Economy: Research and Policy Contexts ............................................................................... 9 2.1 Introduction................................................................................................................................................. 9 2.2 Research Background................................................................................................................................ 9 2.3 Spatial Perspectives – Globalisation and City-Regions...........................................................................13 2.4 UK and EU Policy Background ................................................................................................................17 2.5 The Scotland Context...............................................................................................................................20 2.6 Conclusion................................................................................................................................................23

3 Benchmarking the Knowledge Economy – the Local Futures Approach ........................................................24 3.1 Introduction...............................................................................................................................................24 3.2 The Economic Architecture Analysis .......................................................................................................25 3.3 The Competitiveness Analysis .................................................................................................................28

4 The Geography of the Knowledge Economy in Scotland ................................................................................33 4.1 Introduction...............................................................................................................................................33 4.2 The Architecture Analysis ........................................................................................................................33 4.3 The Competitiveness Analysis .................................................................................................................41 4.4 The Relative Competitiveness of Scotland’s Urban and Rural Knowledge Economies .........................49 4.5 Scottish Cities as Drivers of Regional Growth in the Knowledge Economy............................................52 4.6 Conclusion................................................................................................................................................60

5 Stakeholder Views on Scotland’s Knowledge Economy .................................................................................61 5.1 Introduction...............................................................................................................................................61 5.2 Understanding of the Knowledge Economy Agenda ...............................................................................61 5.3 Geography................................................................................................................................................63 5.4 Policy Priorities .........................................................................................................................................64 5.5 Conclusion................................................................................................................................................65

6 A Spatial Framework for the Knowledge Economy in Scotland ......................................................................66 6.1 Task Force Number 3...............................................................................................................................66 6.2 Vision: The “Nation-Region” Knowledge Economy .................................................................................66 6.3 Scenarios Development ...........................................................................................................................67 6.4 A ‘Distributed Policy’ Model for the Knowledge Economy.......................................................................72 6.5 ‘Knowledge Economy Observatory’ for Scotland.....................................................................................73 6.6 A Publicity and Awareness Campaign for the Knowledge Economy ......................................................73

Annex........................................................................................................................................................................75 References................................................................................................................................................................87

Acknowledgements

the local futures group

I

Acknowledgements

We are extremely grateful to all of the individuals and organisations that contributed their time and expertise to this study. Special thanks to the Scottish Enterprise Steering Group for this project: Kenny Richmond, Kevin Kane, Veronica Noone, Jamie Bell and David Lippiatt.

Steve Inch Glasgow City Council Stephanie Young Scottish Enterprise Glasgow Caroline Sincock Targeting Innovation - Intellectual Assets, Scottish Enterprise Glasgow Prof. Andrew Hamnett University of Strathclyde Jim McIntyre Competitive Place Scottish Enterprise Gordon Kennedy Scottish Enterprise Glasgow Kevin Kane Scottish Enterprise Glasgow Prof Neil Hood Deputy Chairman of Scottish Enterprise and Strathclyde University George Boag Targeting Innovation, Scottish Enterprise Glasgow Paul Lewis Scottish Enterprise Edinburgh & Lothian Neil Francis Scottish Enterprise Edinburgh & Lothian Veronica Noone Scottish Enterprise Edinburgh & Lothian Robin Benn Scottish Executive Alistair Shaw West Lothian Economic Development Prof. Archer Heriot Watt University Andrew Holmes City Development, Edinburgh Shonagh McPherson McGrigor Donald & Scottish Enterprise and Edinburgh & Lothian Board Member Ashok Khindria CES Services & Scottish Enterprise and Edinburgh & Lothian Board Member Neil Gordon AVC Media Enterprises Tony Aldhous Competitive Business, Scottish Enterprise Grampian Jennifer Craw Scottish Enterprise Grampian Ian Heywood Skills & Learning, Scottish Enterprise Grampian Ian Gabriel Transportation and Infrastructure, Aberdeenshire Council Colin Turnbull AXEON Ltd. Aberdeen Bob Sinclair Banff and Buchan College of Further Education Allan Macaskill Talisman Energy, Aberdeen Shona Cormack Scottish Enterprise Tayside Ken Macdonald Economic Development, Perth & Kinross Prof. Nicholas Terry Dundee Business School University of Abertay Dundee David Valentine Economic Development, Angus Council Doug Grimmond Economic Development, Dundee City Council Jamie Bell Scottish Enterprise Grampian David Lippiat Scottish Enterprise Tayside Brendan Dick British Telecommunications Scotland Graeme Purves National Planning Framework, Scottish Executive Alan Denham National Planning Framework, Scottish Executive David Glass Scottish Enterprise Borders Joe Noble Scottish Enterprise Fife Allan Watt Scottish Enterprise Fife Alan Sinclair Skills and Learning, Scottish Enterprise Stephen Boyle Futureskills Scotland, Scottish Enterprise Charlie Woods Knowledge Management, Scottish Enterprise

Executive Summary

the local futures group

II

Executive Summary

Aims

In August 2003, Scottish Enterprise commissioned the Local Futures Group to carry out a geographical analysis of the knowledge economy in Scotland. This study supports the work of Scottish Enterprise and its network of Local Enterprise Companies in building a Scottish knowledge economy that delivers national prosperity and cohesion. The main aims of the research were:

To create a baseline picture of the geography of the knowledge economy in Scotland

To evaluate the case for a unified economic development and planning framework to enhance the performance of Scotland’s knowledge economy

To recommend ways forward on developing this strategic framework

Research and Policy Contexts

Research on the ‘knowledge economy’ dates back to the seminal work of Professors Fritz Machlup and Peter Drucker in the early 1960s. OECD studies of the knowledge economy in the 1990s advanced the ‘knowledge economy’ as a paradigm for policy making. Policy interest in the UK and the EU has intensified owing to the competitive pressures of the 21st

century global economy. Geographers believe that cities and city-regions will be the main players in the global knowledge economy.

The UK Government has made the knowledge economy its vision of Britain’s future. It is also committed, with other European governments, to delivering the Lisbon Summit (2000) goal of a successful knowledge economy across the EU by 2010. European regions are planned to help deliver this goal, and the knowledge economy is written into the future Structural Funds.

Clearly, Scotland will be influenced by UK Government knowledge economy policies, as set out most recently in the Innovation Report (2003). Of particular relevance to this study are two emerging dimensions in the Government’s approach to the knowledge economy:

The ‘horizontal’ dimension – across policy domains: enterprise and investment, competition, learning and skills and infrastructure for business, including planning (and housing), transport and broadband networks

The ‘vertical’ dimension – across geographies: national, regional, sub-regional and local layers of economic development policy and delivery

Strengthening these dimensions of knowledge economy policy involve partnerships and ‘joined up’ strategy – connecting policy domains and services, and connecting national, regional and local tiers of decision-making and delivery. What emerges in

Executive Summary

the local futures group

III

making both sets of connections is a “distributed model of knowledge economy policy”. At the same time, the ODPM-backed Core Cities Network is seeking to promote regional capitals in England as world-class knowledge economies.

The knowledge economy agenda in Scotland has evolved alongside that of the UK Government’s policy approach. In January 1999, the first knowledge economy task force focused on the commercialisation of university research, clusters and business innovation. A year later, the second knowledge economy task force focused on creating a more ‘joined up’ strategy.

Presently, Scotland’s national economic development strategy – and knowledge economy policies – is set out in the Framework for Economic Development in Scotland and Smart, Successful Scotland reports. Policy now favours a knowledge economy driven by ‘endogenous growth’ and aims to boost innovation, skills, and entrepreneurship in all sectors of the economy and in all regions of Scotland.

There is now policy interest in the role of cities and regions in Scotland’s economic development. This is being addressed through The Review of Scotland’s Cities and the National Planning Framework, the latter being directly citied in the UK Innovation Report as a potential building block for knowledge economy strategy.

The obvious question is: does Scotland need a third knowledge economy task force that explicitly introduces geography as the unifying framework for the knowledge economy?

The Analysis

For this study, we have carried out three types of analysis on Scotland’s knowledge economy:

Economic Architecture Analysis, based on skills and employment, provides an overview of the Scottish knowledge economy

Competitiveness Analysis – provides a benchmarking assessment of the knowledge economy at the sub-regional and local levels

A Stakeholder Analysis examines the evidence on some key issues raised by the local stakeholders

Results of the Architecture Analysis

For the regional level:

Scotland, along with the North and Midlands of England, lags behind Greater London and the South East and East of England on average earnings

Scotland’s employment rate is also disappointing by national standards – it is below the national average and very much lower than southern England

Scotland compares extremely favourably with the powerful South East on high knowledge-intensive sectors, depending more on the public sector; Scotland is far more competitive than the North and Midlands regions.

Less favourably, one in two private sector jobs in Scotland are concentrated in the relatively low

Executive Summary

the local futures group

IV

knowledge intensity K3 sector (where graduates account for between 15 and 25% of the workforce) – compared to a one in four figure for the North West, or one in seven figure for the South East. The bulk of Scotland’s K3 jobs are concentrated in retail and hotels and restaurant services, which are closely linked to tourism, and the construction industry.

Scotland’s skills profile resembles that of the South East and is far more favourable than the North West – it has a relatively large graduate labour pool and less serious ‘skills poverty’ problem

Thus, Scotland’s policy makers have to critically examine the nation-region’s business base in building a successful knowledge economy. Presently, Scotland’s problems appear not to lie with average skills or the public sector, but with its apparent dependence and growth bias towards consumer and tourism related services. This low value services bias combined with a large public services sector is not likely to produce a globally competitive knowledge economy in Scotland.

At the sub-regional and local levels:

South Western Scotland struggles with low employment rates and a large unskilled workforce

Highlands and Islands is marked by very low earnings levels and is dependency on ‘K3’ sectors

North Eastern Scotland has a very strong business knowledge economy

Eastern and South Western Scotland are highly dependent on the public knowledge economy for job generation

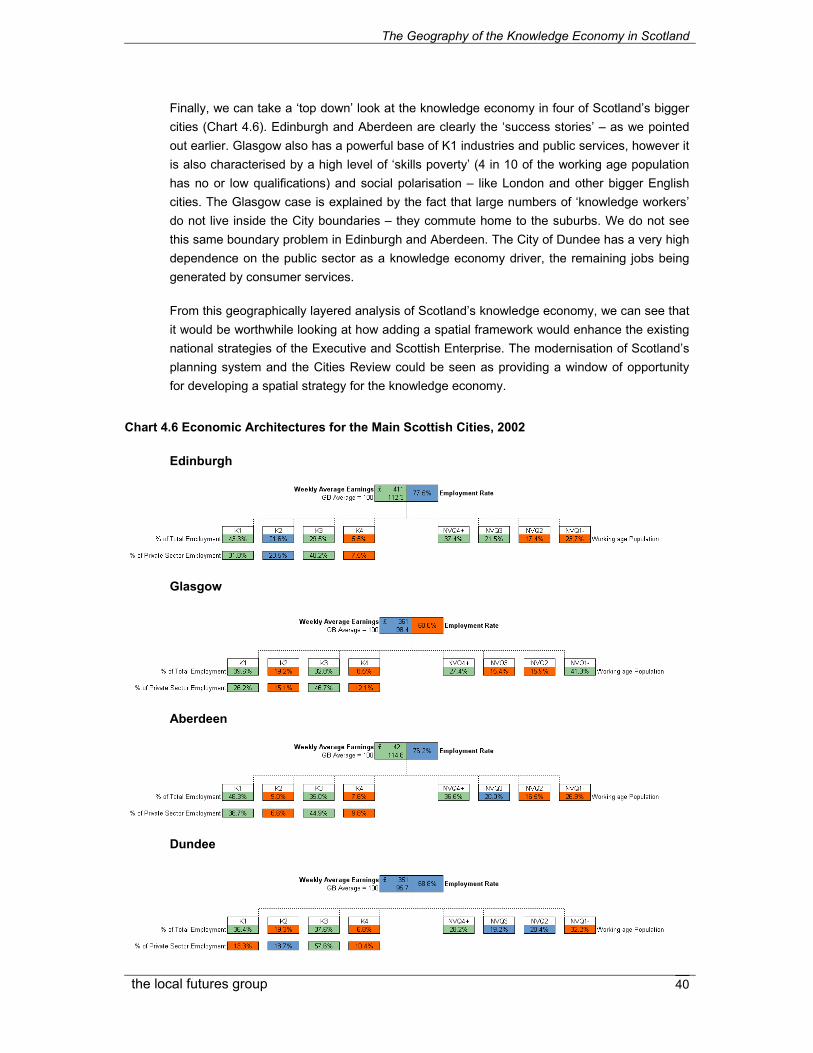

Edinburgh and Aberdeen are success stories and are highly competitive by national standards.

Glasgow also has a powerful base of knowledge-driven industries and public services, but is also characterised by a high level of ‘skills poverty’ and social polarisation.

The City of Dundee has a very high dependence on the public sector as a knowledge economy, the remaining jobs being generated by consumer services.

All English regions show a similar pattern of ‘metropolitan dominance’ in the knowledge economy. However, in the south of England, the knowledge economy is dynamic in accessible rural areas.

Results of the Competitiveness Analysis

We examine 5 dimensions of competitiveness: knowledge-intensive industries, skills & learning, enterprise, Infrastructure and Cultural Amenities.

With respect to knowledge-intensive industries:

In terms of city knowledge economies, Edinburgh and Glasgow outpaced Aberdeen and Dundee. There is a disappointing picture of economic change south of the ‘Central Belt’.

Executive Summary

the local futures group

V

In most parts of Scotland the public sector generates at least 40% of employment in knowledge-intensive sectors.

With respect to skills and learning:

Only Edinburgh appears to be a strong ‘magnet’ for migrants and the skills they potentially bring.

Both Edinburgh and Glasgow are in the top 10 local authorities in Great Britain when it comes to the retention of graduates in the local economy.

Areas in and around Glasgow and Edinburgh suffer skills poverty equal or greater than that seen in remote rural areas.

With respect to enterprise:

While recent start-up rates are comparable to the British average, the business dynamic of Scotland’s knowledge economy needs to be stronger – the glaring exception to this is Edinburgh’s phenomenal success on enterprise.

Edinburgh, followed by Aberdeen, performs well with greater access to knowledge creators and communications and business services firms. Glasgow trails behind on these measures.

With respect to infrastructure and cultural Amenities:

Scotland – with the exception of Glasgow – could benefit from higher levels of connectivity to international transport gateways within the UK and to London as

Britain’s global knowledge economy ‘hub’

Glasgow and Dundee score highly on ‘cultural amenities’ – although Edinburgh is also an international cultural destination.

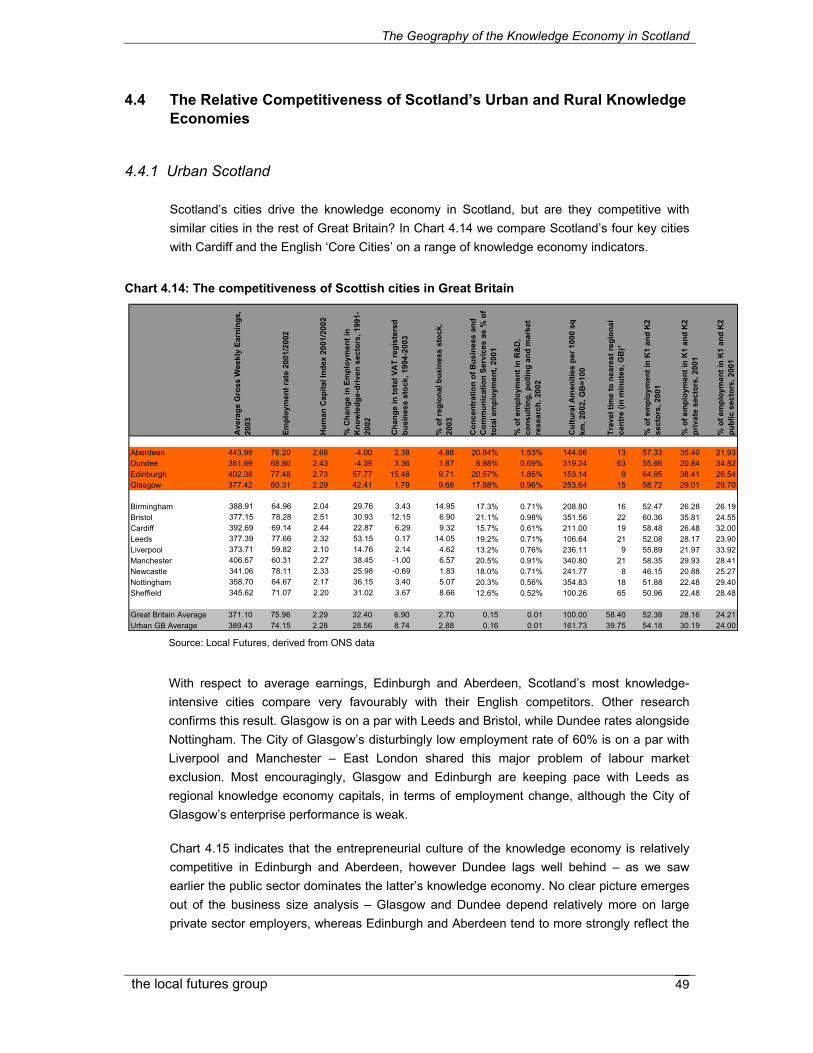

More detailed analysis of how Scotland’s urban and rural areas performed produced the following results:

With respect to average earnings, Edinburgh and Aberdeen, Scotland’s most knowledge-intensive cities compare very favourably with their English competitors.

Rural Scotland lags behind England on knowledge-driven business employment change – Scotland’s rural knowledge economy is more public sector-dependent.

We can infer three regional knowledge economy centres in Scotland based on travel-to-work-areas: Glasgow and Motherwell and Lanark, Aberdeen City and the areas of Aberdeenshire, and Edinburgh City, West Lothian, Falkirk and Fife.

Stakeholder Views

Our interviews and workshops with local stakeholders confirmed the need for:

A local-regional approach that uses geography to reinforce strategies for the knowledge economy and regional cooperation

Recasting the competitive cities agenda to ensure that growth and

Executive Summary

the local futures group

VI

prosperity is inclusive of rural Scotland

A strategic framework that brings together spatial and economic levers along with a set of strategic priorities and actionable next steps

A Spatial Framework for Scotland’s Knowledge Economy

We conclude by recommending the following agenda-setting framework for Scottish Enterprise and its partners.

It would be worthwhile for the Scottish Executive and Scottish Enterprise to thoroughly explore options for strengthening the regional and local dimensions to the country’s knowledge economy policies.

We recommend a 3rd Task Force on Scotland’s Knowledge Economy that introduces geography as the unifying framework for the knowledge economy.

Vision: The “Nation-Region” Knowledge Economy

Scotland’s vision of its future as a knowledge economy has to fully reflect the country’s status as a ‘nation region’. Because Scotland’s economic governance status is ‘new’ (though Scotland’s nationhood status is old), Scottish policy makers have to embark on a ‘nation-building’ exercise if its knowledge economy policies are to work.

Scenarios Development

As a further, reinforcing policy step, Scottish Enterprise needs to develop future scenarios for the knowledge economy that can be used to support not only its visioning work, but also to

help begin the process of benchmarking progress at all levels.

A ‘Distributed Policy’ Model for the Knowledge Economy

We recommend the use of a distributed policy model for the Scotland knowledge economy. This model should be used as an organising framework for developing ‘joined up’ strategy and weighing up options for greater regionalism and localism in knowledge economy policy – including the case for planning ‘city-regions’ and developing a rural knowledge economy strategy.

A ‘Knowledge Economy Observatory’

Scottish Enterprise needs to create a ‘knowledge infrastructure’ to support and guide knowledge economy policy-making across sectors and geographies. The ‘hub’ of this nationwide ‘joined up’ infrastructure should be a ‘smart observatory’ – an interactive, web-enabled database-driven knowledge management system. This should be a ‘zero option’ for Scotland’s knowledge economy community of policy makers.

A Publicity and Awareness Campaign

Scottish Enterprise should work with the LECs to develop a unified message for local economic partnerships, local and regional authorities, industry associations and business networks, the HE and FE sectors, skills and training providers and other stakeholder groups. Local Economic Forums should provide an initial platform to deliver this message.

Introduction

the local futures group

7

1 Introduction

1.1 Background to the Study

In August 2003, Scottish Enterprise commissioned the Local Futures Group to carry out a geographical analysis of the knowledge economy in Scotland and to suggest its broad implications for economic development policies. This research supports the work of Scottish Enterprise and its network of Local Enterprise Companies in building a Scottish knowledge economy that delivers national prosperity and cohesion.

This interest in the geography of Scotland’s knowledge economy is mirrored by parallel developments ‘south of the border’. The UK Government is steadily growing the local and regional dimensions of its economic policy-making, and its latest statement on the knowledge economy – the Innovation Report (DTI, 2003) – recognises that regional development agencies, sub-regional learning councils and local authorities have to partner up successfully in the interests of national prosperity. Interestingly, whereas previous Competitiveness White Papers on the knowledge economy covered innovation, enterprise and skills, the Innovation Report adds two more great building blocks – infrastructure and planning – that require a more decentralised and geography-based approach towards the knowledge economy.

Through this study, then, Scottish Enterprise wishes to explore the rationale for making geography and planning and infrastructure an integral part of its strategies to deliver a competitive and inclusive knowledge economy. In turn, how can the knowledge economy agenda be embedded in national planning and infrastructure policies? Of particular interest is the role of Scottish cities as engines of the knowledge economy – geographers, including Local Futures Academic Panel – believe that city regions (but not any city region) should be seen as national ‘flagships’ in the global economy. Will rural Scotland be left behind as backwaters of the knowledge economy – Local Futures is currently working with DEFRA and EMDA on this very issue and the policy responses needed to grow the knowledge economy in rural England.

This study builds upon the geographical analysis contained in Local Futures previous report on the knowledge economy in Scotland, under the ERKE research programme 2002-03. In that report, we raised a number of issues based on applying our Regional Economic Architecture model of the knowledge economy to Scotland and its sub-regions:

The weakness of the business drivers of the knowledge economy

The importance of the public sector as a major player in the knowledge economy

The metropolitan bias of the knowledge economy and regional and local disparities

Introduction

the local futures group

8

1.2 This Report

Basically, this report extends and refines the previous analysis of the geography of the knowledge economy. The main aims of the research were as follows:

To create a baseline picture of the geography of the knowledge economy in Scotland

To evaluate the case for a unified economic development and planning framework to enhance the performance of Scotland’s knowledge economy

To recommend ways forward on developing this strategic framework

The study involved a mapping and measuring analysis of the knowledge economy in Scotland, using Local Futures original models and benchmark indicators. In addition, we carried out a range of stakeholder interviews to develop a critical view of the policy environment – this included the Scottish Executive, Scottish Enterprise, the Local Enterprise Companies and local authorities – and a range of university representatives and private sector organisations.

The report is organised as follows:

Chapter 2 provides a selective review of the research literature on the knowledge economy, and then goes on to discuss the policy agenda that has evolved in the UK and Scotland

Chapter 3 explains the Local Futures methodology for benchmarking the knowledge economy using an original set of indicators derived from our ‘architecture’ and ‘competitiveness’ analysis

Chapter 4 presents the results of our geographical analysis of Scotland’s knowledge economy, with special attention being given to its ‘city-region’ and urban-rural structural characteristics

Chapter 5 reflects on the results from our stakeholder interviews and the degree to which the results of our data analysis are consistent with perceptions of major issues on Scotland’s knowledge economy

Chapter 6 presents our ideas on a geography-based knowledge economy agenda for Scotland

The Knowledge Economy: Research and Policy Contexts

the local futures group

9

2 The Knowledge Economy: Research and Policy Contexts

2.1 Introduction

The knowledge economy concept surfaced in the Government’s Competitiveness White Papers during the 1990s as a scenario or imperative for UK Plc – around the same time as the publication of the OECD Knowledge-Based Economy report (1996). In March 2000, the Lisbon European Council agreed on making Europe “the most competitive and dynamic knowledge-based economy in the world’ by 2010. Scotland, reflecting these wider policy directions, has been relatively advanced in its policy thinking on the knowledge economy as the route to sustainable economic growth.

In this chapter, we have drawn together a number of strands of Local Futures’ analysis of the knowledge economy research and policy literature, as circulated to sponsors of the ERKE programme – [see, for example: Understanding the Knowledge Economy (Local Futures, 2004), A Regional Perspective on the Knowledge Economy in Great Britain (DTI, 2003), and The Geography of the Knowledge Economy: Academic Panel Survey (Local Futures, 2003)]. In this literature review, we have highlighted research and policy that relates to urban and regional development in the knowledge economy.

The last part of the chapter discusses current directions in Scotland’s economic and spatial policies. The UK Government’s drive towards regionalism and now localism in economic policy (see HM Treasury reports: Productivity – The Regional/The Local Dimension, 2001 and 2003) is already leading to a geography-based approach to the knowledge economy. Is Scotland going down this same policy path?

2.2 Research Background

The ‘knowledge economy’ as a new perspective on capitalist economic development surfaced more than 40 years ago – as such it does not refer to a ‘new economy’ built around the notion of the Information Society (the ICT industries were embryonic at the start of the 1960s). Unfortunately, and to plagiarise George Stigler’s view on the status of information in economic theory, the knowledge economy has tended to ‘occupy a slum dwelling in the town’ of economic development strategy – it appears under an ICT or High Technology sub-heading in policy documents. To fully grasp the knowledge economy as a paradigm for contemporary policy and research, we have to go ‘back to the future’ and revisit the work of the great Princeton economist, Fritz Machlup.

The Knowledge Economy: Research and Policy Contexts

the local futures group

10

In his seminal work, The Production and Distribution of Knowledge in the United States (1962), Machlup examined long-term changes in the industrial and occupational structures of the US economy (1900 –1960) to show that:

Services and ‘white collar’ work had overtaken manufacturing and ‘blue collar’ work in terms of their respective shares of GDP and the workforce by 1960

‘Knowledge industries’, defined by the intrinsic nature of their final outputs, dominated wealth creation – technology, publishing and communications, finance and business services, R&D and education (including libraries), cultural and creative activities

‘Knowledge workers’ – professional, managerial, scientific and technical workers scattered across all sectors of the US economy – from agriculture through manufacturing to services – formed a growing majority of the workforce and held the key to growth, competitiveness and prosperity

Machlup’s work was highly significant for two reasons. Firstly, it put services, high technology and the knowledge economy on the US Government’s economic policy agenda, domestically and internationally. Second, as Boulding (1963) observed in reviewing Machlup’s book, “the very concept of a knowledge industry contains enough dynamite to blast traditional economics into orbit”. Neo-classical economics (the ‘text book’) relied on the axiomatic assumption that producers and consumers were perfectly informed about market conditions and choices – prices, technologies, the identities of suppliers, locations, job opportunities, etc. All the smoothly drawn demand and supply curves to be found in economics textbooks are only definable if this assumption holds. But, if knowledge was really freely available and costless – a ‘public good’ that was equally accessible to all producers and consumers - why were businesses, governments and consumers devoting the lion’s share of the nation’s resources to it?

This question was simple but profound in terms of its impact on economics as a discipline and hence economic models as policy tools. It paved the way for new areas of theoretical and policy development, for example:

What role did knowledge as human capital – the skills and competences of the workforce – play in national economic competitiveness? Were countries investing enough in universities and training?

What role did knowledge as innovation play in national economic performance (productivity)? Were countries spending enough on science and technology or R&D? How advanced or backward were a nation’s businesses when benchmarked internationally?

What role did knowledge as power play in the regulation of markets and industries? How were monopolies rooted in intellectual property – brands, patents, copyright, etc? How did knowledge inequalities influence relations between businesses (large and small firms), between employers and employees, producers and consumers and so on?

The Knowledge Economy: Research and Policy Contexts

the local futures group

11

These types of questions are, of course, highly relevant to present debates on the knowledge economy and its policy framework. For example, are we under or over investing in universities? Or, why are we lagging behind in the international productivity, innovation and skills ‘stakes’? Scotland’s policy makers are locked into these types of policy debates – raised by Machlup’s brilliant analysis of the knowledge economy, 40 years ago.

From a business school background, Peter Drucker also claims to have invented the knowledge economy concept. Rather than capital, labour or natural resources, Peter Drucker sees applications of knowledge to work – the creation of value by productivity and innovation – as central to wealth creation activity in the 21st century economy. In his recent book entitled Post Capitalist Society (1993), he identifies three historical (overlapping) phases of the ‘knowledge economy’:

The Industrial Revolution (1750-1900) – knowledge as applied to tools, processes and products

The Productivity Revolution (1880-1945) – knowledge as applied to work

The Managerial Revolution (1945 – now) – knowledge as applied to knowledge

According to Drucker, the term ‘productivity’ was unknown at the time Frederick Taylor (1856-1915) published his studies of work and training-driven business and economic growth. Similarly, management – a core discipline of the modern knowledge economy – was not discovered as an economic driver until after World War II. The types of issues raised by Drucker resonate with current policy debates on the knowledge economy. He points out that the quickest way to middle class income in Britain as late as 1960 was to work in unionised mass production industries – whereas today ‘there is practically no access to middle-class income without a formal degree’. The UK Government’s goal of widening access to higher education to reach 50 per cent of young people is consistent with Drucker’s views on the route to a more open and inclusive Knowledge Society – Scotland has already reached this target.

These challenges, according to Drucker, have to be addressed through technical and social innovation – the latter referring to changes in economic institutions and cultures. Continuous innovation in firms, public bodies and non-profit organisations is central to knowledge-driven economies. The implication of this is that knowledge economies have to be decentralised:

Its organisations must be able to make fast decisions, be based on closeness to performance,

closeness to the market, closeness to technology, closeness to changes in society, environment,

demographics, knowledge, which must be seen and utilised as opportunities for innovation’ (page 54).

Drucker argues that, while the knowledge economy may be decentralised and embedded in local communities, it is also inherently global in the sense that it transcends the boundaries of communities and nation states and administrative or planning regions and city regions. As LSE economist Danny Quah (1999) observes in his analysis of the ‘weightless’ knowledge economy, the future IS global “because the supply of knowledge products is bounded neither by geographical location nor by increasing marginal cost, their natural marketplace is

The Knowledge Economy: Research and Policy Contexts

the local futures group

12

immediately global”. The knowledge economy is a global-local phenomenon and has to be approached by policy-makers as such.

Machlup and Drucker worked on a ‘big canvas’ - the macro level. Most economists have focused attention on the micro level, the main themes being the roles of knowledge, innovation, technical change and learning in firms and industries. Relevant areas of work include: information economics (see, for example: Stiglitz, 2000), national innovation systems (Freeman and Louca, 2001), the ‘networked economy’ (Castells, 1996), institutions and evolutionary economics (Loasby, 1999) and the role of human capital (Lucas, 1988), or ‘talent’ (Florida, 2002). The so-called ‘new economy’ (Leadbetter, 1997) is essentially an extension to the ‘old knowledge economy’, a necessary update of its technological, market, industrial and geographical frameworks.

Reflecting the eclectic nature of knowledge economy research, the scope of the knowledge economy agenda is extremely wide and crosses over numerous policy fields – see Chart 2.1.

Chart 2.1 – The Scope of the Knowledge Economy Agenda (Research and Policy)

OECD – Macro-level Knowledge Economy

Strategic Management – Business Process

EC Immaterial Investments as Innovation

R&D Spend Knowledge about social/economic changes, demand articulation

Knowledge and education

Know How Hard technological knowledge Distribution and logistics

Industrial patterns/design Strategic choices about core competences (contracting out, co-development)

Image, design and quality

Patents & licences Strategic positioning of products and concepts

Premium brands and market differentiation

Artistic creations/copyright Product design, user friendliness and integrated electronic software

Innovative/active marketing/advertising

Royalty payment rights Integrated values, convenience, quality of life, self affirmation, fun

Ability to produce, re-package and market content

Training and Human Resource Development

Brand names, advertising and image-building

Organisational transformation

Market share Team and network building Re-training

Product certification Process design, learning organisation and ‘soul’

Distribution channels

Customer/subscriber lists Reputation in networks New communication patterns

Product/service brands External logistics Knowledge-intensive and high value added production

Software and similar products After-sales service and customer feedback

Consumer behaviour

Source: European Commission, Panorama of EU Industry, 1997

The Knowledge Economy: Research and Policy Contexts

the local futures group

13

2.3 Spatial Perspectives – Globalisation and City-Regions

Globalisation has raised the stakes of developing a better understanding of the knowledge economy and what it means for local to regional to national economic development. Announcing the launch of a Commons Treasury Committee inquiry into Britain’s regional productivity gap, Chancellor Gordon Brown emphasised the need to “meet the challenges of China growing at 8 per cent a year and the 1m graduates coming out of universities in India” (Financial Times, 16 December 2003, p.8). The 2003 Pre-Budget Report highlights the long-term jobs threat to the regions of call centre and other e-enabled information work migrating to India. Building a globally competitive knowledge economy around a new enterprise culture, a highly skilled workforce and greater innovation capacity is now a ‘zero option’ for the regions as well as UK Plc.

In his insightful book on the nature of markets and marketplaces entitled Reinventing the Bazaar, John McMillan (2002) argues that the competitive forces unleashed by globalisation combined with the e-business explosion could produce a ‘win-win’ future for rich and poor countries – and presumably for rich and poor regions within countries. However, radical reforms of market systems and institutions are needed for the knowledge economy to bring more balanced and equitable patterns of economic development between and within countries. The fundamental source of competitive advantage in the knowledge economy - intellectual property rights defined very broadly – lies with rich countries/regions and multinational corporations.

The challenge facing many regions and countries in an ideas-based knowledge economy characterised by the unequal distribution of intellectual property (patents, copyrights, brand names, trademarks, education, health care innovation, etc) is to somehow develop their own authentic base of comparative economic advantage. As Danny Quah puts it:

(In the knowledge economy) winners are superstars – they own the entire market, and there is only one

of them. Those who come second find no economic elbowroom. Rightly they need to seek out new

knowledge-products to make their own, not attempt me-too reproductions. And if this leads to faster

technical innovation economic growth might be higher as a result.

The most promising and liberating area of the Knowledge Economy for ‘home-grown’, authentic businesses and jobs appears to be the creative and cultural industries. In his thought-provoking book on cross-cultural trade, Creative Destruction (2002), Tyler Cowen argues that globalisation is leading to the homogenisation of cultural products across countries – through trade in music, arts, media, food, fashion, etc – but at the same time, also to greater heterogeneity of cultural production and experience within countries. The end result then is not the subversion of distinct local cultures but greater cultural diversity as a new asset for global trade and regional economic growth.

More globalised and diverse economies – with city-regions acting as international and national hubs – have the crucial advantage of being ‘magnets’ to those creative, entrepreneurial and professional classes that ultimately make the ‘wheels of the knowledge economy turn’. Richard Florida’s (2002) work in the US and Canada has been particularly influential in this area of Knowledge Economy policy development. Talent flows to where

The Knowledge Economy: Research and Policy Contexts

the local futures group

14

cultural diversity thrives – quality theatre and quality restaurants, rather than the standard fare that has made so many British high streets dull, boring and ultimately commercially unviable. Globalisation will, according to Cowen, increase the quality and sophistication of modern consumer tastes: “Ignorant consumers damage quality just as well-informed customers support it”. In other words, the Knowledge Economy extends to the consumption sphere, as much as it does to the production sphere. The virtuous circle is complete where knowledgeable consumers drive knowledgeable producers in rounds of innovation – whether this consists of new types of food, new fashion designs and so on.

Consumer knowledge as a driver of business innovation – is completely neglected in economic development strategies. Yet, as a recent DTI-sponsored study (DTI, 2003) of the drivers behind skills and workforce development clearly shows, dynamic SMEs and large firms are led by changes in markets – that is consumers of their products and services. In modern service economies – that is, local and regional economies throughout Britain – it is important to understand and harness the power of consumer knowledge as exercised in markets – not just the high street impacts, but how purchases and preferences ripple through the supply chains to original producers. The consumer-driven quality and diversity ‘revolution’ needed for knowledge economies to flourish locally and globally should be a major future theme of economic development strategies.

According to the University of Toronto’s Meric Gertler (2001), cities are the principal sites of innovation and the production of knowledge-intensive good and services. His explanation underlines the sharing of tacit as well as codified knowledge between individuals and institutions (economically meaningful ideas and intelligence are exchanged ‘over lunch’ or ‘over a drink’). Underlying relations of trust and reciprocity are encouraged by the parties concerned being located in the same city or city-region.

Given the interactive and social nature of innovation, city-regions provide the ideal space in which social

learning processes can unfold. The sheer density and concentration of economic players in large cities

offer multiple opportunities for contact, interaction and information circulation over time. Supporting this

interaction is a large concentration of specialised providers of services and goods operating within a

well-defined social division of labour in the city. Furthermore, while the simple geographical

concentration of economic players facilitates productive interaction, spatial clustering provides another

ingredient that is essential to the innovation process.

The most powerful treatment of ‘localised knowledge spillovers’ is Michael Porter’s (1990) work on clusters and competitive advantage. The knowledge economy of the Government’s Competitiveness White Papers and the Innovation Report is a cluster-based economy – from the biotechnology firms around Cambridge University to the City and London’s world-beating marketing and advertising industries concentrated around Soho. The DTI has identified ‘clusters’ in every region of Britain, as an organising framework for regional economic strategies, business support and skills training. Cluster-based economic strategies have their critics and their supporters. They are perceived to be too exclusive, favouring more knowledge and technology-based sectors over traditional manufacturing and service industries – the latter accounting for the great bulk of SMEs and start-up businesses. There is some scepticism about the genuine potential of officially designated clusters to compete globally and act as engines of local and regional growth.

The Knowledge Economy: Research and Policy Contexts

the local futures group

15

Cluster growth depends on being able to generate, attract and retain talent – the creative classes (Florida, 2002) and highly educated people (Lucas, 1988; Glaeser, 1998) who drive modern knowledge economies. These footloose ‘knowledge workers’, according to Gertler (2001) and Florida (2002), are attracted to city regions – and NOT ANY city region – that offer local social and cultural diversity (note Florida’s use of a Gay Index to reflect an environment that is open to diversity and newcomers), as well as a diversity of available opportunities for career advancement. The geography of ‘brain drains’ and ‘brain gains’ – internationally and within countries – is determined increasingly by the economic, social and cultural diversity of knowledge economies.

It is possible that globalisation could actually benefit Britain’s would-be city-regions outside London and the South East, through cross-cultural trade and linkages with other regions of Europe and the rest of the world. Building institutional links, including university alliances – together with traditional trade missions and export offensives – should be core global-local economic strategies.

To create an up-to-date picture of how academic researchers see the geography of the knowledge economy in Britain, Local Futures established an Academic Panel (LFAP) of leading UK university-based geographers and invited their views on trends and policies. There was a consensus among Panel members that London and the South East dominated the knowledge economy today, and in the absence of a radical national strategy that could produce a more balanced economic geography, these regions would continue to do so in future. Globalisation would work with a southern bias.

All of the panellists explained their responses with reference to the ‘pre-existing geography’ of economic development in Britain – London and the South had dominated historically, in different stages of capitalist development, and this had now translated into cumulative or first-mover advantages in the contemporary knowledge economy. In aggregate, the North and Midlands were effectively locked into a low-wage equilibrium trap and locked out of the business knowledge economy. This perspective can be traced back to the cumulative causation theory of regional growth first proposed by Gunnar Myrdal (1957) and then refined and applied to the UK by Nicolas Kaldor (1957, 1970). Basically, this theory challenged the neo-classical implication of equilibrating regional markets – factor price equalisation would guarantee an end to the ‘north-south divide’ in the long run. Instead, Myrdal and Kaldor identified the possibility of endogenous income divergence attributable to cumulatively reinforcing growth based on agglomeration economies and increasing returns to scale. The ‘trigger’ for cumulative growth in the UK regional context – with London and the South East benefiting – was certainly the ‘Big Bang’ in the financial markets, reinforced by and working in combination with the new economy (ICT), both inherently global in nature.

The Panel generally believed that successful re-balancing the knowledge economy in favour of the Regions, Scotland and Wales depended on the development of successful city-regions – backed by fast track rail services out of London, devolution and relocation of Whitehall offices, more R&D spending for universities other than Oxbridge/London and other radical big policy changes in economic development. Chart 2.2 highlights the Panel’s views on cities and city-regions in particular.

The Knowledge Economy: Research and Policy Contexts

the local futures group

16

Chart 2.2 Academic Viewpoints on the Geography of Britain’s Knowledge Economy

Support for City Regions

We need the pre-1986 governance structures that provided strategic metropolitan government like in London. We need this for the regional capitals and it is vital to get the knowledge economy going in the regions – the City-Region Future. This is the message from worldwide evidence and experience.

Metropolitan unitary authorities like Newcastle and Sunderland are important as drivers behind the city region scenario. Sub-regional partnerships have been set up as vehicles for devolving RDA budgets, however, their strategic roles as knowledge economy players are limited.

Big city authorities could become knowledge economy leaders. Birmingham Council, for example, provides leadership for the City, the West Midlands county and the Region, and provides a focus for visioning the future and more practically, a focus for integrated knowledge-driven economic development, including transport and planning.

Planning Ahead

A national approach to the geography of the knowledge economy should be high-tech specialisation in Manchester/Cheshire area, finance in Leeds, and medicine in Edinburgh (for example). It is utterly critical – so much policy is spatially discriminatory.

A national strategy for regional development should aim to establish a knowledge economy backbone of city regions. These city regions would need an excellent transport infrastructure, big knowledge economy projects (e.g. Nottingham’s planned Bio City), and high-level Government jobs capable of generating clusters (e.g. the NHS Executive in Leeds).

Elected regional assemblies should underpin regional knowledge economies with a massive redistribution of resources away from the South East. More autonomy for Scotland, Wales and Northern Ireland to recognise that the most successful European economies over recent decades have been small nations with genuine economic sovereignty.

RDAs have a critical role to play in the regional knowledge economy. However, in order to ‘interface’ more effectively with more global companies, the RDAs have to be backed up by national economic coordinators.

The Future

Major changes are unlikely. The trends are obdurate and will probably involve London growing even bigger, counter-urbanisation with the growth of e-work and e-business around the bigger cities, and a global shift of call centres, with the biggest impact being felt in the north.

It is possible that new technologies (for example in design) or cultures may allow some specific localities - not necessarily within the current main knowledge economy locations - to begin to bloom.

The current spatial structure will not change up to 2010. The spread effects are too weak. The more knowledge-intensive economic activities will stick to the major centres – and some accessible rural areas where there is growth are really like “halos” around these centres.

Source: Local Futures, Report of the Academic Panel Survey on the Geography of the Knowledge Economy, 2003

The Knowledge Economy: Research and Policy Contexts

the local futures group

17

2.4 UK and EU Policy Background

The Government’s approach to the knowledge economy is set out in a series of Competitiveness White Papers (1997-2001) and the Innovation Report (2003). The latter is most relevant to this study because it consolidates the Government’s policy thinking and progress on the knowledge economy. Before turning to the Innovation Report, it is worthwhile flagging up the EU policy context – vision and strategy for Europe’s knowledge economy matches closely with the UK agenda.

The ‘Lisbon Strategy’ (with extensions agreed at the Stockholm and Goteburg European Councils, 2001) mirrors the UK knowledge economy strategy (see below), with its initiatives designed to encourage competition and enterprises, innovation, employment, education and training and modernising the European Social Model. The European Council meets in March 2005 to assess progress with the delivery of the Lisbon Strategy targets – then, the Strategy will be reviewed and given fresh impetus in light of its application to the enlarged European Union.

The EU expects every nation and region to contribute towards the delivery of the Lisbon Strategy – with a successful knowledge economy at its heart. The UK Government is committed to the Strategy nationally and regionally, with the RDAs in England and the Devolved Administrations (DAs) in Scotland and Wales playing a key role in delivering a globally competitive knowledge economy across the whole of Europe. In England, the RDA Regional Economic Strategies, the Frameworks for Regional Employment and Skills Action (FRESAs, and now Regional Skills Partnerships) and Sustainable Development Frameworks together map closely into the Lisbon Strategy in terms of objectives. The Integrated Regional Strategies (IRS) of the English regions are gradually being rolled out by the Regional Assemblies and RDAs as ‘umbrella’ strategies that bring together the RES/FRESA and Regional Planning Guidance. The North West, North East and Yorkshire and Humber regions are obviously most advanced in this process of creating up regional ‘joined up’ strategies for the knowledge economy, given the impending referendums on devolution due in November 2004.

As set out in the Innovation Report, the UK is seeking to make the most of European innovation and economic initiatives – such as the knowledge economy R&D infrastructure work in Framework 6, the European Research Area for highly skilled workers and so on. Of equal relevance is the Third Cohesion Report outlining the latest proposals for 2007 to 2013, given the main three themes that will guide interventions backed by the Structural Funds: innovation and the knowledge economy, accessibility and services of general interest and environment and risk prevention. These themes, supplemented by the European Employment Strategy, will be integrated into the various EC plans and programmes, though exactly how is not clear at present. There will however be an emphasis on knowledge-driven businesses and industries, learning and skills, university and R&D drivers of regional economies and a general emphasis on knowledge economy infrastructure – such as ICT and e-government, business support and so on. Most of this coincides with the Innovation Report. There is also a strong urban-rural dimension to the European knowledge economy strategy, though beyond the accessibility and cohesion objectives it is not yet clear as to how this dimension will translate into policy and practice.

The Knowledge Economy: Research and Policy Contexts

the local futures group

18

From the Innovation Report, it is evident that the UK Government’s approach to the knowledge economy is mainly concerned with improving business innovation and the global competitiveness of UK Plc. For the ‘new economic localism’ to succeed, local authorities need to lead the creation of a local knowledge economy agenda – because the knowledge economy is the Government’s vision and main organising concept in economic policy. According to the Prime Minister in his introduction to the DTI Innovation Report (2003)

“We want the UK to be a key knowledge hub in the global economy, with a reputation not only for world

class scientific and technological discovery but also for turning that knowledge into new and profitable

products and services. This report sets out the next steps we are taking to turn that vision into a reality.”

Minister for Science and Innovation Lord Sainsbury is the main champion of the knowledge economy agenda, including its policies for developing knowledge-based ‘clusters’ in all regions of the UK. This global orientation and strong emphasis on high technology businesses, universities and ‘talent’ has led to a widespread view that the Government’s knowledge economy vision and policy agenda is not universally relevant or appropriate to all regions of the UK.

There are signs that the Government is seeking to widen out and create a more ‘joined up’ approach to the knowledge economy. The Ministerial team is one important step in this direction. Within the DTI itself, the Skills Unit works across departmental boundaries connecting policy analysts from skills, innovation, enterprise and economic development – this attempt to create a joined up approach to skills from a knowledge economy perspective is being pursued at the centre and in the regions.

There are two dimensions to the Government’s strategic approach that are particularly relevant to defining a knowledge economy agenda for local authorities:

First, the ‘horizontal’ structure of knowledge economy policy – stretching across policy domains where local authorities are already active players: enterprise and investment, competition and learning and skills; and infrastructure for business, including planning (and housing), transport and broadband networks

Second, the decentralised structure of knowledge economy policy – more policy and delivery responsibility shifting to the regional and local levels, where local authorities act in partnerships with sub-regional bodies, notably the LSC and SBS, and regional agencies, especially the RDAs

Importantly, both dimensions of knowledge economy policy necessarily involve partnerships and ‘joined up’ strategy – connecting policy domains and services, and, connecting national, regional and local tiers of decision-making and delivery. What emerges in making both sets of connections is a “distributed model of knowledge economy policy” – a matrix of partnership activity – see Chart 2.3.

The Knowledge Economy: Research and Policy Contexts

the local futures group

19

Chart 2.3 A Distributed Model of Knowledge Economy Policy

Skills Enterprise Innovation Infrastructure Competition

National

Regional

Sub-regional

Local

Between the idea and the reality of joined up knowledge economy policy we find the familiar obstacles posed by existing governance structures. Using the above matrix for our stakeholder analysis, Local Futures research at the regional, sub-regional and local levels in England has found that the main policy levers and players of the knowledge economy are not ‘joined up’ at present.

Time is bound to change this picture of regional economic governance. It is important to bear in mind that the RDAs are new and much could change should devolution in England become a reality, as it has in Scotland and Wales. The LFAP unanimously felt that without devolution and competitive city regions outside London, the knowledge economy is likely to continue to widen rather than close the productivity gap between and within regions - the Government’s central policy target and rationale for the new localism and regionalism in economic policy.

The Government’s knowledge economy agenda has reached the regional level, although as with the national level, the agenda is still fragmented rather than joined up in any real sense. The signs are, however, more encouraging and there is an observable tendency towards a distributed model of knowledge economy policy. A key aspect of this is the ODPM-backed Core Cities Working Group – a partnership between 8 UK Core Cities (Birmingham, Bristol, Leeds, Liverpool, Manchester, Newcastle, Nottingham and Sheffield), the 9 RDAs and central government departments, including the ODPM, the Treasury and the DTI, Transport and Culture, Media and Sport.

The recent Competitive European Cities report (ODPM, 2004) found that the English Core Cities lag behind the best continental cities in economic competitiveness. Only London (23rd) and Scotland’s ‘big two’, Edinburgh (25th) and Glasgow (29th), appear in the top half of the 61-city league table showing GDP per head performance in 2001. Generally UK cities score poorly on innovation and skills – the cornerstones of a modern knowledge economy. We see later in this report that our benchmarking analysis of the knowledge economy also shows Scotland’s cities as leaders outside London.

The ODPM report emphasises that urban competitiveness performance is sensitive to how city boundaries are drawn. This is one of the big missing links in the ‘core city’ analysis and also in city-region definition and measurement. In fundamental respects, city boundaries are historical constructs, and their geographical delineation reflects arguments about the efficiency of the public space economy (optimum service delivery) and its administration, as much as arguments about local democracy and community attachment (the local geography of social capital). But, and a big but, city boundaries – and rural boundaries – are certainly not designed in any genuine respect to meet the demands of city-region economies that the Government would like to act as ‘dynamos’ and global competitors’ in the contemporary or

The Knowledge Economy: Research and Policy Contexts

the local futures group

20

future global economy. In the Scottish context, interpretation of data analysis must be conscious of the local delineation of city boundaries - tight boundaries used for Glasgow and Dundee and the wider cast boundaries for Edinburgh and Aberdeen – to reflect the true characteristics on the ground. Travel to work areas are only one way of defining these new possible geographies – but they measure sprawl, rather than the market-based networks of industrial and cluster activity that a functional regional economy is based upon.

The best we can do is to adopt a pragmatic approach, using available data on the knowledge economy – the approach we use here. Importantly, in defining city-regions, one needs to have a more comprehensive geographical picture of the national or regional knowledge economy – that is what lies outside the ‘city walls’ and how urban and rural areas fit together as part of a greater economic and social formation. This is how we have approached Scotland’s knowledge economy geography.

2.5 The Scotland Context

The knowledge economy agenda in Scotland has evolved alongside that of the UK Government’s policy approach. The response to the DTI’s 1998 Competitiveness White Paper was the setting up of the first Knowledge Economy task force in January 1999, and the publication of its findings in the report Scotland: Towards the Knowledge Economy (the recommendations centred on the commercialisation of university research, clusters and business innovation). The second Knowledge Economy task force produced the report The Knowledge Economy Cross-cutting Initiative (2000), its emphasis being on creating a more joined up’ approach towards the knowledge economy:

“…We have in the Scottish Executive brought together the Digital Scotland and Knowledge Economy

agendas within the Enterprise and Lifelong Learning Department. This will I hope send a strong

message about the importance we place on these topics and on our commitment to a technologically

advanced and inclusive Scotland.” – Henry McLeish, First Minister.

Scotland’s policy thinking reflected the wider UK strategy and also the OECD work on the knowledge economy referred to earlier in the chapter. Local Futures research under ERKE and other projects also suggests that Scotland’s thinking on the knowledge economy as a Devolved Administration – with Scottish Enterprise pre-dating the English RDAs – has been well ahead of other regions in Britain, including London. In many senses, Scotland has had a head start on the knowledge economy agenda.

The DTI Innovation Report (2003) has refreshed the Government’s knowledge economy agenda – as discussed above, it is more ‘joined up’ and regional in terms of its overall policy directions. The DAs are ‘covered’ by the Report:

“The Government is committed to increasing the prosperity of all regions while narrowing inter- and

intra-regional disparities… significant aspects of the innovation policy agenda in Northern Ireland, Wales

and Scotland are the responsibility of the Devolved Administration

The Knowledge Economy: Research and Policy Contexts

the local futures group

21

Much of the thinking on innovation is consistent with Scotland’s core policy ideas – and perhaps most significantly, the Report makes special mention of Scotland’s planning system as an infrastructure building block of the knowledge economy (see page 27).

The Scottish Executive and Scottish Enterprise are the two main drivers behind economic development in Scotland. Within the Scottish Executive the Innovation Policy Unit (IPU) has broad responsibility for innovation working with a number of departments including the Development Department, Education Department and Enterprise, Transport and Lifelong Learning Department. As the lead regional economic development agency, Scottish Enterprise is charged with delivering a successful knowledge economy ‘on the ground’ through its nationwide network of Local Enterprise Companies (LECs). Scotland’s economic development policy is articulated in the report Framework for Economic Development in Scotland (FEDS), with the Smart, Successful Scotland (SSS) report setting out a national strategy for the knowledge economy.

Like the UK and EU strategies, the FEDS links the knowledge economy imperative for Scotland to the challenges of the 21st Century global economy. The central argument in the FEDS is that Scotland needs to develop a successful knowledge economy on the basis of ‘endogenous growth’, rather than relying on inward investment and the global competitiveness of a handful of sectors. The knowledge economy is seen as being universal in scope, with a ‘rising tide’ of innovation, skills and entrepreneurship evident in all sectors of the economy and in all urban and rural areas of the country.

Of paramount importance is how Scottish Enterprise realises the Executive’s vision and delivers it nationally, regionally and locally in partnership formats. Skills and learning have moved to the centre of Scotland’s economic development strategy – like in the UK and the regions. Reflecting this greater emphasis on developing the country’s human capital stock, Scottish Enterprise is pursuing a number of initiatives such as:

Demand-led learning support as part of the Scottish Executive’s strategy for lifelong learning

Developing Careers Scotland as an all-age career management service that responds to local economic development needs

“Futureskills Scotland” as a research and intelligence base for labour market policy and reform

Merger of the skills advisory services for businesses with Business Gateway to support investment in demand-led training

In addition to learning and skills, Scottish Enterprise has prioritised business and enterprise growth and global connections as organising themes of its knowledge-driven economic development strategy and its implementation through the LEC network – see the box below. The ‘Global Connections’ policy strand is concerned with improving digital connectivity and making Scotland a ‘hub’ of the global knowledge economy.

The Knowledge Economy: Research and Policy Contexts

the local futures group

22

Organising themes for the Local Enterprise Companies

As outlined by A Smart, Successful Scotland, 2001 Growing Businesses – productivity, skills, higher wages, employment growth, and higher growth rate

• Greater entrepreneurial dynamism and creativity • More e-business • Increased commercialisation of research and innovation • Global successes in key sectors

Global Connections – increase flow of products, technologies and ideas in and out of Scotland

• Digital connectivity • Increased involvement in global markets / export market, etc. • Scotland to be a globally attractive location – importance of place • More people choosing to live and work in Scotland (attraction and retention of talent)

Learning and Skills – high skill, high wage economy with high employment rate

• Improving the operation of the Scottish Labour market • The best start for all your young people • Narrowing the gap in unemployment • Improved demand for high quality in-work training

Like the UK and the English regions, Scotland is pursuing the ‘holy grail’ of joined up economic policy, based on the distributed policy model of the knowledge economy we outlined earlier. The SSS strategy demands higher levels of policy coordination between national and sub-national players - the Executive, Scottish Enterprise, the LECs, the HE and FE sectors, sub-regional economic partnerships and local authorities – as well as a strong global dimension to economic development strategy – such as Scottish Development International, Visit Scotland, British Trade International, Invest UK, etc. In our earlier literature review, we emphasised the need for a global-local approach to the knowledge economy agenda.

Like the rest of the UK and the English regions, Scotland has to give serious consideration to the issue of decentralisation in knowledge economy policy-making and delivery. Presently, and like the RDAs, Scottish Enterprise uses the LEC network to deliver national policies, however it lacks a strategic engagement with local and sub-regional economic partnerships that are proactively shaping the knowledge economy across the country – but ‘off the radar screen of top-down national policies’. Embedding geography into Scottish Enterprise strategy is becoming all the more necessary with the modernisation of Scotland’s national planning system – earlier we mentioned its citation in the UK Innovation Report as a building block of the knowledge economy in Scotland.

The Review of Scotland’s Cities and the National Planning Framework for Scotland have largely been responsible for addressing spatial planning. Sharing the basic thrust of the ODPM-backed ‘Core Cities’ network of English metropolitan centres (see above), the ‘Review’ examines the roles of Scotland’s six cities (Stirling has since gained city status) and their immediate hinterland. While cities are recognised as drivers of the knowledge economy the big strategic question for planning and economic development relates to the definition of geographical boundaries – the spatial parameters of the wider ‘city-region’ or inter-regional relationships. A recent paper by Begg and Docherty (2003) argues the case for city-regions as the preferred framework for planning and developing Scotland’s knowledge economy – we return to this issue in our mapping and measuring analysis.

The Knowledge Economy: Research and Policy Contexts

the local futures group

23

The patchwork of formal and informal arrangements since Local Government re-organisation in 1996

confirms the need for city-region governance arrangements.

Building Better Cities

The recently published National Planning Framework provides a broad overview for spatial development. It identifies the linkages between economic growth and spatial development (infrastructure planning, regeneration, core cities, etc.) and focuses attention on economic development zones as strategic areas for co-ordinated action - for example, the Edinburgh-Glasgow axis and West Edinburgh and the Clyde Corridor. The 21st Century modernisation of Scotland’s planning system does present opportunities for pursuing a geography-based approach to the knowledge economy. The emerging policy framework sets out urban development objectives that reflect local variations and priorities in the case of each city. Reinforcing this are strategic city-region agreements, which are basically regional planning frameworks for prioritising the allocation of City Growth Funds money.

2.6 Conclusion

The knowledge economy policy agenda is still evolving in Scotland, the UK and Europe. There are two clear trends that Scottish policy makers have to address: first, the need for a ‘joined up’ strategy and second, the need for a decentralised approach to the knowledge economy agenda. The former strategic imperative is, of course, the ‘holy grail’ of modern economic development policy, given the governance and political barriers to its implementation. The second imperative is about greater regionalism and localism in economic development.

Scotland is a ‘nation region’ in the same way that London is a ‘city region’. As such, while its strategic approach to building a successful knowledge economy is still influenced by UK and EU policies, Scotland has much greater scope – compared to the English regions – in setting its own priorities in making and delivering policies. A spatial planning framework for the knowledge economy in Scotland would help to create a ‘joined up’, centralised strategy, one that keeps pace with governance trends in the UK and the EU. Further, the Scottish economy is relatively small and largely concentrated in the ‘central belt’ - this could be one of Scotland’s biggest advantages if it can succeed in building synergies nationally, regionally and locally.

In the next chapter, we take the first step towards creating a spatial framework for Scotland’s knowledge economy – a baseline analysis of the geography of the knowledge economy. Our methodology and indicators for this analysis have been developed in the context of three years of research for Scottish Enterprise and other partners in Scotland (the previous ERKE project), and for the English regions and the DTI.

Benchmarking the Knowledge Economy – the Local futures Approach

the local futures group

24

3 Benchmarking the Knowledge Economy – the Local Futures Approach

3.1 Introduction

The knowledge economy is here, but the analytical tools and indicators for measuring its performance are missing. The OECD (1996) concluded in its major programme of work on The Knowledge-Based Economy that:

“At the heart of the knowledge-based economy, knowledge itself is particularly hard to quantify and also

to price. We have today only very indirect and partial indicators of growth in the knowledge base itself.

An unknown proportion of knowledge is implicit, uncodified and stored only in the minds of individuals.

Terrain such as knowledge stocks and flows, knowledge distribution and the relation between creation

and economic performance is still virtually mapped”.

A definitive list of indicators for mapping and measuring the knowledge economy does not yet exist. The OECD has tended to lean towards ‘harder’ technology, innovation and intellectual property; strategic management experts have tended to focus on various aspects of the business process (this is where the knowledge economy literature is mostly to be found in major bookshops).

This chapter explains our methodology for benchmarking national, regional and local economic development in Scotland from a knowledge economy perspective. Local Futures has developed this methodology – including an original set of benchmark indicators for mapping and measuring the knowledge economy – in the course of the ERKE research programme and consultancy projects. We have included a metadata supplement in the Annex (see Annex - A.5) given the strong interest Scottish Enterprise has in this project’s delivery of a knowledge economy methodology and indicator base.

The foundations of this benchmarking analysis were built in the context of a research collaboration with all of the English Regional Development Agencies, where Local Futures developed a regional model of the knowledge economy called “regional economic architecture”. We subsequently carried out this analysis for Scotland under year one of the ERKE programme. The results of this work were published by the DTI in a report entitled “A Regional Perspective on the Knowledge Economy in Britain”. The report influenced the Innovation Report (2003) and the 21st Century Skills White Paper.

The DTI has commissioned Local Futures to up-date and extend its analysis as part of a major project on skills, economic development and the knowledge economy. It is particularly interested in a benchmarking methodology that covers the planning, infrastructure, enterprise

Benchmarking the Knowledge Economy – the Local futures Approach

the local futures group

25

‘building blocks’ identified in the Innovation Report as key to a successful knowledge economy, as well as a local and sub-regional breakdown of the regional knowledge economy. This project is currently underway and is due to report in September 2004.

Under what we call the Knowledge Economy Audit, the Local Futures benchmarking approach consists of the following analyses

Economic architecture analysis – applying the REA model (see below) at different levels to obtain a geographical overview of the knowledge economy in Scotland

Competitiveness analysis – assessment of knowledge-intensive industries, skills and education, enterprise, connectivity and quality of life, again at different levels.