the forward exchange rate for sterling and the efficiency of expectations

TRANSCRIPT

The Forward Exchange Rate for Sterling and the Efficiency of Expectations

By

Paul A. Ormerod

T his paper investigates the determination of the forward exchange rate for sterling against the U.S. and Canadian dollars, the Belgian and French francs, and the West German mark over the period

August 1972 through March 1978. The first part of the paper sets out the theoretical background to the equations which are used in the estimation work. These equations are in the tradition of recent empirical work on forward rates, which has obtained estimates of the equilibrium condition that expresses the forward rate as a weighted average of the interest- parity forward rate and the expected spot rate [e.g. Stoll, 1968; Kessel- man, 1971; Haas, 1974]. In this paper we first estimate an equation assuming that the expected spot rate is the only determinant of the for- ward rate, and that expectations are formed rationally in the sense of Muth [1961 ]. We then follow the approach of McCallum [I977] , relaxing the assumption that the coefficient on the interest-parity forward rate is zero, but still retaining the assumption that expectations are formed ration- ally. Finally, we examine a more general specification which allows the expectations generating mechanism to be determined endogenously by the data, and test the hypothesis that the expectations so formed are efficient, conditional upon the estimated model of the forward rate being correct.

The basic theory underlying the determination of the forward rate is very similar to the model described by Hodjera [1973]. There are postu- lated to be essentially four types of traders in the forward market, arbi- tragers, speculators, traders, and the monetary authorities. Considering the 9o-day forward market, the net demand function for 9o-day forward exchange by an individual arbitrager is given by

t---89

(i) Dat = g~ [(F* -- Ft), Vdt, Vft, Aat, Z Da~] i ~ t - - I

where F t is the 9D-day forward exchange rate, Ft* is the corresponding interest-parity forward rate given by Ft* = St Rt, where St is the current

Renu~rk: This paper was presented to the Econometric Society European Summer Work- shop, University of Warwick, July x979. The author is grateful to Leigh Roberts for research assistance, and to colleagues at the National Institute of Economic and Social Re- search and Professor Patrick Minford of Livertmol University for comments on a previous draft.

Wettwlrtschaftliches Archiv Bd. CXVI. x4

206 P a u l A. O r m e r o d

spot rate and R t = (1 + if) / (1 + rd) , with rf and r d denoting foreign and domestic interest rates, respectively. We expect the partial derivative of gl with respect to (F* -- Ft) to be positive. It might be expected that this schedule would in fact be infinitely elastic with respect to (F* -- F), but there are a number of reasons why this might not be the case. The existence of transactions costs for example will limit changes in arbitrag- ers' net demand for forward foreign exchange with respect to small changes in (F*--F). Moreover, although the pure foreign exchange risk is by definition covered in the arbitrage operation, other types of risk do exist which might influence the demand of arbitragers for forward foreign exchange. For example, each arbitrager will have a subjective assessment of the risk of intervention by domestic or foreign governments in the freedom of short-term capital transactions. The terms Vd and Vf in equation (i) represent the arbitrager's estimate of this type of risk in domestic and foreign exchange markets, with the partial derivative of gl with respect to Vd being greater than zero, and less than zero with respect to Vf. Two further factors which limit the elasticity of the schedule with respect to (F*--F) are the budget constraint implied by the total asset position of the arbitrager, and the portfolio balance constraint imposed by his existing unexpired commitments. These two factors are represented

t-~89

in (I) by Aa, the arbitrager's total liquid assets, and by Z Dai, where i = t - - 1

the partial derivative of gl with respect to the former variable is positive, and is negative with respect to the latter variable.

The net demand function for forward foreign exchange by a speculator, again limited to 9o-day contracts, is given by

t---89

(2) Dst ---- g~ [(SE~ +9~ -- Ft), RIt, Ast, Z Dsj] j=t--X

where SE~ +9~ is the expected value of the spot rate in 9 ~ days' time formed at time t, RI t is the speculator's subjective risk in undertaking forward contracts, and As t is his total liquid assets. We expect that the partial derivatives of g, with respect to (SE -- F) and As to be greater than zero, and less than zero with respect to RI and Y~Dsj.

Credit arising from trade transactions contracted for future payments is an important proportion of short-term capital movements. However, in terms of the underlying theory, traders can be regarded as operating from a mixture of arbitrage and speculative motives. For example, traders will try to obtain finance from the sources where interest rates, after allowing for the forward premium, are lowest, and in this respect behave as arbitragers. Traders also behave as speculators, either through leaving trade credit contracts uncovered or through leads and lags. The fourth

The Forward Exchange Rate 207

group of agents operating in the forward exchange market, the monetary authorities, will enter the market for a var ie ty of reasons, sometimes to prevent a currency from falling in value, as the U.K. authorities did at the end of 1967, sometimes to prevent a currency from rising in value, as the West German authorities have done in recent years, and sometimes no doubt to engineer for a mixture of reasons falls or rises in currencies. For convenience we assume that the net demand for forward foreign exchange by the authorities is exogenously determined.

Equilibrium in the forward exchange market requires tha t net demand for forward exchange equals zero

(3) DA t - (DS t + D M t - S x t + G t ) = 0

where DA, is the net market demand for forward foreign exchange by arbitragers, DSt is the net market demand by speculators, DMt is the net market demand by trade importers, SX t the net market supply by trade exporters, and G t the net market demand by the authorities.

Equation (3) is part of a system which includes the spot market. Arbitrage creates the link between the spot and forward exchange markets, since arbitragers always cover their forward commitments by reverse spot transactions. For equilibrium in the system, the net supply of foreign exchange on the spot exchange market, resulting from transactions which are independent of the current ac t iv i ty on the forward market, is equal to the demand for spot currency by arbitragers to cover forward commit- ments.

The equation for the forward rate which has been used in recent em- pirical work can be derived by applying a number of simplifying assump- tions to the above model. Data on intervention in the forward market by the authorities is in general treated as confidential and is not made avail- able, so this aspect of forward market activity has had to be excluded from the work of empirical investigators. In estimation work there will therefore be the possibility of bias in the coefficients due to the omission of variables, although the recent results by Beenstock [1979] and Been- stock and Bell [i979], who as civil servants were allowed to use data on forward intervention by the U.K. authorities, suggest that this potential bias is in practice very small.

The activities of traders in the forward exchange market can be effec- tively regarded as a mixture of arbitrage and speculation, so that explicit account need not be taken of these agents in formulating the equation for estimation. Further, with the exceptions of (F*--F) and (SE--F), it is not obvious how to construct suitable expressions for the other explanatory variables contained in equations (i) and (2), so as an initial assumption

X4*

208 Paul A. Ormerod

these terms are excluded from the equation to be estimated. This is derived more conventionally by re-writing (I) and (2) in terms of the excess de- mand of arbitragers and speculators for forward claims

(4) Xat = a (F* -- Ft) ~ > 0

(5) K s t = ~ (GEl +k - - Ft) ~ > 0

using the market clearing condition

(6) Xa + Xs = 0

to give the equation

(7) F t = (1 -- x) F~ + xSE[ +k where x = ~/(~ + ~)

One point to note is that in equation (7) a and f~, which are the absolute slopes of, respectively, the arbitrage and speculation schedules, are not identified, since an infinite number of ~s and ~s can be derived from any given value of x. In other words, the volume of capital flows which results from increasing domestic interest rates by a given amount, for example, is not identified.

The basic equation which we use in estimation is

(8) F t = Y0 + Y1 Ft* + Y2 SE~ +k

where the theory suggests that 71 + 72 = 1. Although the theory suggests that there should not be a constant term in the equation, 70 is included in order to allow a further test of the validity of the theory, i.e. 7o = 0.

Equation (8) was estimated over the period August 1972 through March 1978 using a variety of proxies for the expected spot rate, and using monthly data on the three-month forward rate for sterling against the five currencies mentioned above. The spot and forward rate data was obtained from Financial Statistics of the Central Statistical Office. The interest rates used are the three-month treasury bill rates for the United Kingdom and the United States, taken from the Bank of England, Quar- terly Bulletin. The interest rates for Belgium, Canada, France and Germany were obtained from the summary money market rates table in International Financial Statistics (IFS) of the IMF, which also presents the United Kingdom and United States three-month treasury bill rates. The Cana- dian interest rate is also the three-month treasury bill rate, and although the interest rates used for Belgium, France and Germany are not identical in definition, they are probably the most relevant ones for our purpose 1.

t They are in fact call money rates.

The Forward Exchange Rate 209

There is a potential problem in that the exchange rate data refers to the end of the month, whereas the IFS interest rate data is a monthly average. End-of-month interest rates are, however, readily available for the United Kingdom and the United States. And instrumental variable estimates of equation (8) for the sterling/U.S, dollar forward rate using both end-of- month and monthly average interest rate data to define F* yielded results which were almost identical. The results presented below all use monthly average interest rates.

Under the assumption that expectations are formed rationally in the sense of Muth, we have

(9) SE~ +k = E (St+k] Zt)

where E is the expectations operator and refers to the actual distribution, given the information Z available at time t, of the random variable St+ k. Further, the stochastic term e t defined by

(IO) St+k = E (S[+klZt) + e t

has mean zero and is uncorrelated with the variables comprising Z t, so we can write

( I I ) SE~ +k = S t+ k - - e t

Combining (8) and (II) gives us

(12) Ft = "f0 "]- "I'l F* + "rz St+k + ut

Our first step was to estimate equation (12) on the assumption that ~'1 = 0, i.e. that the forward rate is determined by the expected spot rate. This is similar to the approach used by Frenkel [1977; 1978] to test the hypothesis of the efficient working of the foreign exchange market although the causal interpretation of the two approaches is different. Frenkel esti- mated the equation

( I3) St = 0 0 AV 01 F t _ k -[- V t

arguing that if the foreign exchange market is efficient, then the forward rate should reflect all available information, so that in (13) the constant term should not differ significantly from zero, the slope coefficient should not differ from unity, and the error term should be serially uncorrelated. Using data on the German mark, U.S. dollar, pound sterling and French franc from the early I92OS, Frenkel obtained empirical support for the above conditions.

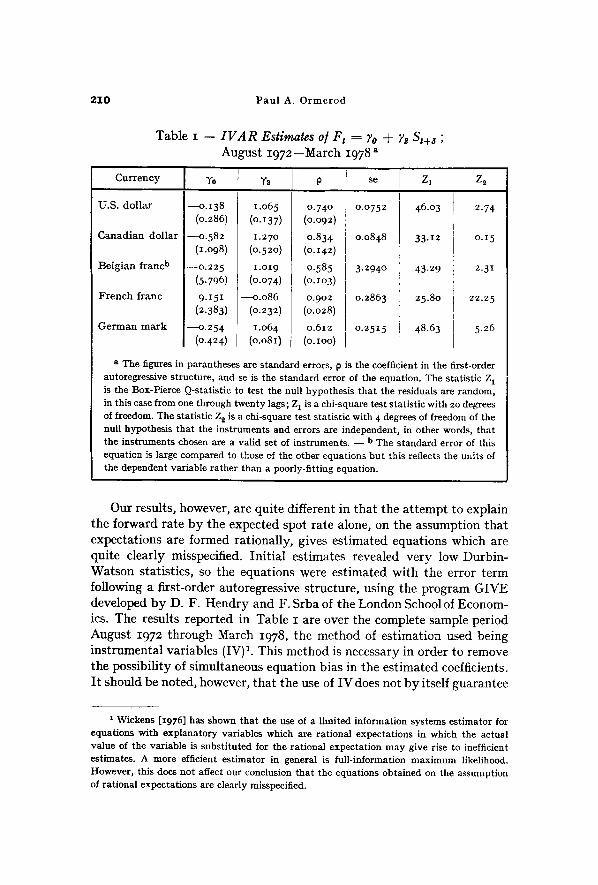

2 1 0 Pau l A. O r m e r o d

Table i -- I V A R Estimates o/ F t = Yo + Y~ St+s ; August I972--March 1978 a

Currency Y0

U.S. dollar ---o.138 (0.286)

Canadian dollar ---0.582 (1.098)

Belgian franc b - -o .225

(5.796)

French franc 9.15 I

(2.383)

German mark ---o.254

(0.424)

Y2 0

I .o65 (o.137)

1.27o (0.520) i.Ol 9

l (o.o74)

'----o.086 (0.232)

I.O64 (o.o81)

0.740 (0.092)

o.834 (o.142)

0.585 (O.lO3)

0.902 (0.028) o.612

(o.ioo)

se Z 1

0.0752

i

0.0848

I 3.294o

o.2863

o.2515

46.03

33.12

43,29

25.80

i 48.63

Z2

I 2.74

i i i o.15

2.31

r 22.25 I i ] 5.26

a The figures in parantheses are standard errors, p is the coefficient in the first-order autoregressive structure, and se is the standard error of the equation. The statistic Z 1 is the Box-Pierce Q-statistic to test the null hypothesis that the residuals are random, in this case from one through twenty lags; Z 1 is a chi-square test statistic with 20 degrees of freedom. The statistic Z 2 is a chi-square test statistic with 4 degrees of freedom of the null hypothesis that the instruments and errors are independent, in other words, that the instruments chosen are a valid set of instruments. - - b The standard error of this equation is large compared to those of the other equations but this reflects the units of the dependent variable rather than a poorly-fitting equation.

Our results, however, are quite different in that the at tempt to explain the forward rate by the expected spot rate alone, on the assumption that expectations are formed rationally, gives estimated equations which are quite clearly misspecified. Initial estimates revealed very low Durbin- Watson statistics, so the equations were estimated with the error term following a first-order autoregressive structure, using the program GIVE developed by D. F. Hendry and F. Srba of the London School of Econom- ics. The results reported in Table I are over the complete sample period August 1972 through March I978, the method of estimation used being instrumental variables (IV) 1. This method is necessary in order to remove the possibility of simultaneous equation bias in the estimated coefficients. I t should be noted, however, that the use of IV does not by itself guarantee

1 Wickens [1976 ] has shown that the use of a limited information systems estimator for equations with explanatory variables which are rational expectations in which the actual value of the variable is substituted for the rational expectation may give rise to inefficient estimates. A more efficient estimator in general is full-information maximum likelihood. However, this does not affect our conclusion that the equations obtained on the assumption of rational expectations are clearly misspecified.

The Forward Exchange Rate 2 1 1

this. I t is necessary to test whether the instruments are independent of the error term, and an appropriate test statistic is reported in Table I.

The equations have a high degree of explanatory power, and for all countries except France the constant term and slope coefficient are not significantly different at the 5 per cent level from zero and unity, respec- tively. However, even when estimated with a first-order autoregressive error structure, the equations show marked signs of misspecification. For all except France the null hypothesis of random residuals is rejected at the 5 per cent level, and in the case of France the null hypothesis of the independence of the instruments and the errors is rejected. The high values of the Q-statistic are clear indications of considerable misspecifi- cation, since this statistic is known to have a low power 1. The calculated value of the statistic only infrequently exceeds the critical value at the conventional level of significance (5 per cent).

Results obtained adding the term F* , again on the assumption that expectations on the future spot rate are formed rationally, show an in- crease in explanatory power and less signs of misspecification, although a first-order autoregressive scheme is again indicated by the data. Because of the high degree of collinearity between F* and St+3, we did not estimate equation (12) directly, but rather

(14) Ft = 70 + 7~ F* + 7z (St+3 -- F*) + ut

Equations (12) and (14) are equivalent, but the specification in (14) should overcome any problem which might arise through multicollinearity.

Table 2 -- I V A R Estimates o[ Ft = Yo + Y'I F * + Ye (S~+3 -- F*); August I972--March 1978a

Currency

U.S. dol lar

Canadian dollar

Belgian f ranc

F r e nc h f ranc

German m a r k

0.006 (o.o15) 0.004

(0-014)

0.903 (0.556)

0.o84 (o.Io9)

0.090 (0.046)

0.993 ---o.o19 (0.007) (0.039)

0.994 -----0.o22 (0.006) (0.023)

0.987 -----o.o71 (0.007) (0.067)

! 0.990 o.o14 ](o.o11) (0.038)

] 0.974 0.o02 i(o.oo9) (o.o21)

a For the symbols of the statistics see Table x.

0.567 (0.409)

0.448 (o.12o)

o.417 (o.II9)

0.585 (o.131) 0.486 (O.llI)

se

0.0072

0.0073

0.4520

o.o412

0 .0386

Z t Z~

I 7 . 3 9 2.32

14.1o 2.47

13"87 [ 0'73

16.5 S ' ~.40

I 8 . 5 6 8.34 l

t See, for example, Davies et al. [x977]-

2 1 2 P a u l A. O r m e r o d

We estimated (14) for each of the currencies measured against sterling over the sample periods August 1972 through March 1978, and August 1972 through July 1974, carrying out a test of post-sample parameter stability in the case of the shorter sample.

The equations are bet ter specified than those in Table I. The null hypotheses of random residuals and independence of instruments and er- rors are not rejected for any equation at the 5 per cent level. The results are strikingly similar to those obtained by McCallum for the Canadian/ U.S. dollar rate over the period of Canadian floating 1953--1962. The 7o = 0 and Y1 + Y~ = 1 conditions of equation (8) are virtually met. Indeed, both the constant and the coefficient on St+3 are not significantly different from zero at the 5 per cent level in any equation. And only in the case of the sterling/mark rate is the coefficient on F* significantly different from unify at the 5 per cent level.

However, as was the case with McCallum's results, the data indicates that the equations need to be estimated with the error term following a first-order autoregressive process, which we interpret as indicating that the equation is still misspecified.

Results obtained using the short sample period August 1972 through July 1974 suggest that the above result also held in the period immedia- tely after the introduction of floating.

Table 3 - - I V A R Estimates o~ Ft = 7o + 7~ F* + 72 (St+3 - - F ~ ) ; August I 9 7 2 - J u l y 1974 ~

Cur rency

U.S. dol lar 0.073 (O.202)

C a n a d i a n dol lar ---o.o41 (0.092)

Belgian f ranc 2.259 (Io.96)

F r e n c h f ranc - - 1 . o 3 o (0.382)

G e r m a n m a r k - -o .271 (o.I77)

o.966 0.727 (o.193)

0.405 (0.229)

0.525 (0.256)

o.129 (o.244)

o.284 (0.232)

se Zl b Z2C Y~ I ---o.042

(o.084) (0.002)

I .Ol 3 o.ooi (0.034) (0.042)

o.971 - -o .133 (o.II9) (o.315)

I.O87 o.o34 (o.o34) (o.o33)

1.o29 O.lO6 (0.028) (o.o5I)

0.0085 25"62 i 0.28

0.0085 12.o8 ] 1.45

0.654 ~ 6.29 I 0"39

~176 1 7 " 8 5 i o.69

o.o443 9.22 7.23

zad

12.4o

16.64

7.85

204.30

86.22

a For the symbols of the statistics see Table i. - - b xo degrees of freedom. - - c 4 degrees of freedom. - - d Zs is a chi-square test statistic with 20 degrees of freedom of the joint null hypothesis of post-sample parameter stability and of constant error variance of the equation on the assumption tha t the parameters are known with certainty, when 20 further observations are added to the sample period.

The Forward Exchange Rate 213

Apart from the problem of misspecification indicated by the existence of autocorrelation of the residuals of the equations set out in Tables 2 and 3, there is an additional query about the validity of these results. Namely, that although the theoretical priors of Y0 = 0 and "r + ~'2 = 1 are met, the expected spot rate has had very little effect in the determi- nation of the forward rate, and that the forward rate of sterling during the recent period of floating appears to have been determined almost entirely by arbitrage and not by speculation on the basis of rational expectations. This is an unusual result, although other studies have obtained similar weights on the interest-parity forward rate and expected spot variables. The results of McCallum [1977] have already been mentioned, and Been- stock [1977; 1979] obtained a similar conclusion for the German mark] U.S. dollar forward rate and the Canadian dollar and pound sterling for- ward rates. Lomax and Denham [i978], in a description of the financial sector in the model of HM Treasury, report weights of 0.943 on arbitrage activity and o.o57 on speculative expectations in an equation for the sterling/U.S, dollar forward rate. However, the above results contrast with those obtained by I-[utton [1977] using a similar approach to Been- stock for the sterling/U.S, dollar forward rate over the period 1963-I97o, using quarterly data. Hutton (p. 39)concluded that his "result indicates a dominant role for speculation in the determination of the forward rate, with speculators' holdings of forward currency more than twice as sensi- tive to the forward rate as arbitragers' holdings." Minford [1978 ] found that the weights of speculative expectations and of arbitrage were roughly equal, again using quarterly data on the stefling/U.S, dollar forward rate over the period 1963 --1971.

It is possible to reconcile these contrasting results within the theoreti- cal framework used. For example, considering the sterling]dollar results, although ~ and ~ cannot be identified in (7), a highly elastic supply of arbitrage funds seems to be implied. During the period of fixed rates 1963 --197o, however, the spot rate for sterling was often close to its lower value in the band, and sterling crises were frequent events. A much greater fear of possible action by the U.K. government to restrict short-term capital movements may therefore have existed and have limited the elasticity of supply of arbitrage funds. Moreover, when the spot rate was close to its floor value, which it frequently was, speculators were presented with the opportunity of transactions offering a reasonable prospect of very large capital gains if the spot rate could not be held at its existing parity, counterbalanced by the prospect of only limited capital losses if the authorities succeeded in raising the value of sterling within its fixed band. In these circumstances it would not be surprising if the elasticity of supply of speculative funds became very large, and if as a consequence the for-

2 I 4 P a u l A. O r m e r o d

ward premium was largely independent of movements in interest rate differentials.

There is also the theoretical point to which Kohlhagen [I978 ] has re- cently drawn attention. Namely, if expectations are formed in a Fisherian manner such that the relative interest differential equals the forward premium which equals the expected change in the exchange rate, then the variables F* and SE~ +k in equation (8) are identical. If expectations are formed in such a way, then the result that ~,, ---- 0 when equation (I4) is estimated tells us nothing about the relative weights of arbitragers and speculators in determining the forward rate. This is because, although arbitrage activity is a function of the interest-parity forward rate and speculative activity a function of the expected spot rate, under Fisherian expectations the expected spot rate is equal to the interest-parity forward rate, so that the term (SEt+ S -- F*) in (I4) is identically zero except for measurement error or other random factors.

However, noting that the results in the literature which obtained 71 approximately equal to unity and -f~. approximately equal to zero all indi- cated misspecification through residual autocorrelation, our next step was to estimate a more general equation for the forward rate to investigate whether other variables in the system were statistically significant. We used only contemporaneous and lagged variables in the system, and did not include forward values. Economic agents are forming expectations at time t on the spot rate at t ime tna3, conditional upon the information available to them at time t. The inclusion of future values of variables such as St+l and St+2 should not add any explanatory power to the equa- tion since the information used to form expectations at time t on these variables is identical to the information set used to form expectations on St+3. Forward values of variables appear in (I2) and (I4) because it is assumed there that the future spot rate is forecast in an efficient and un- biased manner, enabling the actual future spot rate to be substituted for the expected future spot rate. Our approach below enables us to allow the function generating the expected spot rate to be empirically determined by the data and, conditional upon the theoretical equation (8) being a correct representation of the determination of the forward rate, to test for the efficiency of expectations. The general equation used was

3 3

(I5) F t = s 0 + l~ (~i Ft*--i + Yi St-i + ~i Bt-i) -t- N 0i Ft - i -t- ut i = 0 i = l

where B t is the visible balance of payments. The variable Bt was included on the empirical grounds that a number of investigators [for example, Ball et al., I979; NIESR, I979] have found it significant in equations ex-

The Forward Exchange Rate 215

plaining the spot rate for sterling. The term does not have a rigorous theoretical justification, one interpretation being that it proxies the short- term "confidence" effects following the announcement of the trade figures.

We performed sequential F-tests on the exclusion of variables from the general equation until a preferred equation was obtained, following the methodology described, for example, by Anderson [1971 ] and by Hendry and Mizon [1978 ]. Given our underlying theoretical hypothesis (8) it might seem that the coefficient 8o on F* in (15) represents the weight of arbitrage activity in the determination of the forward rate, and that any other variables which are statistically significant in the preferred equation de- rived from (15) represent the term y, SE t+k in equation (8). We cannot, however, put such a strong interpretation on the results because of the possibility that the term Ft* also enters into the expectations generating function for SE[ +k. If no other variables are statistically significant, we have of course, Fisherian expectations as described above. This question is discussed below in the context of the results.

After carrying out sequential F-tests on the general equation, the following results were obtained for the sample period August 1972-Ju ly 1975-

Table 4 -- I V Estimates of F t = Yl F * + Y2 SE t ;

August 1972-Ju ly I975 a

Y1

U.S. dollar

Canadian dollar

Belgian franc

French franc

Y2

o.418 (0.225)

o.694 (o.11o) 0.592

(o.124)

0.456 (o.141)

se

o.58I (0.254) 0.305

(O.I 12)

o.411 (O. I25)

0.542 (o.142)

D W b

0.0067

o.oo75

o.525o

0.0460

2.3I

i i t 2.O1

1.94

1.9 2 18.58

Zxe

I6.91

14.68

8.60

Currency z2d Zae

IO.99 28.75 ]

9.23 I9.O2

5"31 i2~

8.30 7.34

a For the symbols of the statistics see Tables x and 3. - - b Durbin-Watson statistic. __ e I6 degrees of freedom. - - d 8 degrees of freedom for the United States, 9 for Canada, Belgium and France. - - e 20 degrees of freedom.

These equations are much better specified than those reported in Tables 2 and 3, in that there is no evidence of autocorrelation of the residuals. The weights on arbitrage and speculative activity, namely the coefficients Y1 and Y2, sum to almost exactly unity in each case in accord- ance with our theoretical priors, and indicate the weights of speculative

216 Pau l A. O r m e r o d

expectations and of arbitrage were roughly equal, at about o.5, except in the case of Canada where the weight on arbitrage is about twice that on speculative expectations. The constant term was insignificant in all equa- tions. The variables which the data indicated should be included in the SE variable were in general different between the markets. Table 5 sets out the variables used to generate SE t as indicated by the data in each case.

Table 5 -- SE Variables Used in Table 4

Currency

U.S. dollar

Canadian dollar

Belgian franc

French franc

St - - 1.28 (St--1 - - Ft--1) - - o.71 (Ft--3 - - F~--3)

F~ + Ft__ 1 - - St--1

F~ + Ft__ 1 - - S t - - 1

F~ + Ft--1 - - St--1 + St--2 - - F~--2

In the case of Canada, Belgium and France, the Fisherian expectations variable F~' appears to have been the main determinant of speculative expectations, although in each case this was modified by past values of other variables in the system. The existence of variables other than F* which are statistically significant indicates that expectations are not formed in a pure Fisherian manner. However, there is a problem in allocating the coefficient on F* into its arbitrage and speculative components. If, at one extreme, it is assumed that F* does not enter into the mechanism generating the expected future spot rate, and that the estimated coeffi- cient on F* simply represents the weight of arbitrage in determining the forward rate, then the other variables represent the expectations gener- ating mechanism on the future spot rate. This assumption, however, would give implied values for the expected spot rate which were absurd. Equally, there are problems with making the assumption at the other extreme, that the weight of arbitrage is zero and that the coefficient on Ft* simply enters into the mechanism generating the expected spot rate. The solution adopt- ed in practice was to allocate the coefficient on F* between arbitrage and speculative activity in such a way that the expectations generating mechanism for the future spot rate gave non-absurd, and indeed unbiased, predictions of the actual future spot rate. The constraint that the coeffi- cients on these variables were equal in absolute value was not rejected. In the United States case, expectations seem to have been based on the current spot rate, again modified by lagged values of other variables. This was also the case for Germany, where the results are otherwise completely

The Forward Exchange Rate 217

different from the other markets in that the variable F* was not statisti- cally significant at all, the preferred equation being

(16) Ft ---- 0.977 St + o.4ol (St-3 -- Ft-3) + o.119 (Bt -- Bt-2) (0.003) (o.157) (o.o51)

se = o.o34; DW -- 1.63; Za (16) ~-- 9.11; Zz (IO) -- 5.55; Z 3 (2o) = 33.86

In other words, over the sample period August I 9 7 2 - J u l y 1975 the sterling/German mark forward rate appears to have been determined by speculative activity alone.

We then carried out sequential testing of restrictions on equation (15), over the complete sample period August I972--March 1978.

Currency

U.S. dollar

Canadian dollar

Belgian franc

French franc

German mark

0.428 (o.115) o.589

(o.137)

o.493 (O.120)

o.4o2 (o .096)

o.185 (o.121)

0.572 (0.II4)

(o.143)

0.507 (o.121)

o.597 (0.096)

o.8o 7 (O. I2I)

i 0.470

0.040

0.035

1.79

2.10

1.86

1.95

2.o 7

15.12

17.76

9.48

13.27

30.78

Z~ c

8.23

4.7 ~

8.61

8.56

4.05

a For the symbols of the statistics see Tables z and 4. - - b 20 degrees of freedom. - - c 9 degrees of freedom for the United States, 8 for Canada, io for Belgium, France and Germany.

The equations are better specified than those reported in Table 2, the null hypothesis of independence of errors and instruments not being reject- ed for any equation, and the only equation to show signs of autocorrelated residuals being that for the German mark, where the null hypothesis of random residuals is just not rejected at the 5 per cent level.

The results are similar to those reported in Table 4, with the coeffi- cients summing to unity and the constant term being not significantly different from zero, which perhaps is not surprising given that the Za statistics in that table indicate that the null hypothesis of post-sample parameter stability over the next twenty quarters was not rejected at the

218 Pau l A. Ormerod

5 per cent level for any of the equations reported in the table. For Ger- many, however, this was rejected, as equation (16) indicates; the main reason for this is that arbitrage activity does seem to have had some weight in the determination of the forward rate over the longer sample period, although the coefficient of F* is relatively small and is signifi- cantly different from zero at the 2o per cent level only.

Although the weights on arbitrage and speculative activity are approxi- mately constant in each market over the shorter and longer sample peri- ods, the mechanism of expectation formation appears to have been chang- ing. The variables used to generate SE over the August 1972--March 1978 sample period as indicated by the data are set in Table 7.

Table 7 -- SE Variables Used in Table 6

Currency

U.S. dollar

Canadian dollar

Belgian franc

French franc

German mark

St + F t - - 1 - St--1

F~ + F t _ 1 - F~_ 1

St + F t - - 1 - St--1

F* F~ + F t _ 1 - S t _ 1 + S t _ 2 - t--2

St + 0.5 (Ft--1 - - St--l) + o.117 ( B t - - Bt--2)

Only in the case of France does the data indicate that the mechanism used to generate speculative expectations was the same over the two sample periods. Except in the case of Germany, the constraint that the coefficients on the variables used to generate SE were equal in absolute value was not rejected by the data.

Our next step was obviously to investigate whether the expected spot rate indicated by the data was an efficient and unbiased predictor of the actual future spot rate. In other words, we regressed the actual future spot rate against the series generated for the expected spot rate by the mecha- nisms set out in Tables 5 and 7.

(17) St+3 = 9o + ~x SEt t+3 + vt

If the expected spot rate is an efficient and unbiased predictor of the actual future spot rate, in (17) the constant term should not differ signif- icantly from zero, the slope coefficient should not differ from unity and the error term should be serially uncorrelated. I t should be emphasized that this test for the efficiency and unbiasedness of the expected future spot rate is a test which is conditional upon the theoretical equation (8) being a correct representation of the determination of the forward rate.

The Forward Exchange Rate 219

An alternative approach would have been to regress the actual future spot rate, St+3, on current and lagged values of variables in the system and to use the fitted values from this equation as the expected future value of the spot rate, S[ +k in equation (8).

Using the expectations formation mechanism of Table 7, OLS esti- mates of (17) over the period August 1972 through March I978 for all currencies typically have R~s greater than o. 9, with the constant term and slope coefficients apparently not significantly different from zero and unity, respectively. However, there are two problems with the validity of these results. Firstly, in each case the expected spot rate is a function of a current endogenous variable and so instrumental variables should be used in estimation. Secondly, the Z 1 statistics decisively rejected the null hypothesis of random residuals in each case; indeed, the DW statistics of the estimated equations are less than o.5 in each case 1. Estimation by instrumental variables with the error term following a first-order auto- regressive process gave values for the coefficient in the autoregressive pro-

Table 8 - - I V Estimates o/ASt+a = ~ + ~1 ASEt ; August I972--March 1978a

Currency

U.S. dollar

Canadian dollar

Belgian franc

French franc

German mark

- -~ .oo6 (0.007)

i----O.OO2

(o.oo7) ---o.634

(0.363)

- -o .o39 (0.040)

,.....-0.049

(0.029)

opt

o.zo 5

(0.333)

o.456 (0.295) O.OI8

(0.324)

o.3o5 (0.258)

O . I I I

(0.327)

s e

0.053

D W

1,46

z tb

27.71

0.059

2.26o

0-303

o.I74

1.6o

1.9I

1.8i

i .69

22.63

21.5o

36.94

22.48

ZzC

6.88

6.46

3.36

18.21

t4.o5

a For the symbols of the statistics see Tables x and 4- - - b I6 degrees of freedom. - - c 6 degrees of freedom for the United States and Belgium, 9 for Canada, and io for France and Germany.

a Further, inspection of the residual correlograms revealed correlation of the residuals at a number of lags. Using the Box-Jenkins approximation of 4- 2[]/n, where n is the number of observations, for the 95 per cent confidence interval around zero for each individual value in the correlogram, in the case of the United States 8 out of zo observations in the correlogram were greater than this value, of which 6 were third-order and above. For Canada the respec- tive figures were 9 and 7, for Belgium 6 and 5, for France 6 and 4, and for West Germany 5 and 4. Estimating the equations with the error term following a third-order autoregressive process gave values for the coefficient in the autoregressive process greater than 0.8 in all cases except West Germany.

220 Pau l A. O r m e r o d

cess greater than o.9, and so the results set out in Table 8 are for the differenced form of equation (17) ; a constant term is still included to check whether or not it is different from zero.

The null hypothesis of independence of instruments and errors is not rejected at the 5 per cent level in any case, and the null hypothesis of random residuals is not rejected at the 5 per cent level for all except the United States and France. However, given the limitations of the Q-sta- tistic, the calculated values are sufficiently close to the critical value of 26.29 to perhaps indicate that the residuals are in fact non-random. I t is not rejected at the 7-5 per cent level for the United States, but it is rejected even at the 0. 5 per cent level for France, where an examination of the residual correlogram reveals both third and thirteenth-order autocorre- lation. The equations have a very low degree of explanatory power. The constant terms are not significantly different from zero, and the slope coefficients are determined very poorly indeed.

We next ran the same equation over the period August 1972 through July 1975, using the SE variables in Table 5, to investigate whether there had been any sign of learning from the experience of floating in the for- mation of expectations on the spot rate. In other words, poor though the results of Table 8 are, the expectations generating mechanism appears to have changed as the sample period was extended 1, and it is possible that

Table 9 - - I V Estimates o~ ASt+s = 9~ + 91 ASEt ; August i 9 7 2 - J u l y 1975 a

Currency q~0 (Px ! se D W Zlb z2e z3d

U.S. dol lar ---o.o11 ---o. i43 0.054 1.56 21.19 8.05 15.42 (0.009) I (0.324)

Canadian dol lar - -0 .o06 I 0"350 0.050 1.3o 22.54 13.Ol 35.97 (0 .009) ] (0.302)

Belgian f ranc ----o'789 [ - - ~ 2"450 I 2.20 17.o 9 7.1o 14.21 (0.472) I (o.319) [

F r e n c h f ranc ---o.o6i [ o.319 0"337 I 2.02 20.82 17.54 11.7o (0.065) t (0.389) l

G e r m a n m a r k - - o . o 7 i 1----o.II 3 o .2ol i 1"79 16.24 16.27 9.11 (o.o39) 1 (o.311) L

a For the symbols of the statistics see Tables x, 3 and 4. - - b 16 degrees of freedom. - - c 8 degrees of freedom for Canada, 9 for Belgium, and io for the other countries. - - d 20 degrees of freedom.

x Kohlhagen [1977], using an endogenous exchange rate expectations function in a study of the German mark/U.S, dollar forward rate, also found that the parameters in this function tended not to be stable.

The Forward Exchange Rate 22I

over the shorter sample period the expected spot rate was an even less efficient predictor of the actual future rate. A comparison of Tables 8 and 9 shows that there seems to be a very gradual move to greater efficiency over the longer sample period, but that the movement is very slight. I t is worth noting that our conclusion that the expected spot rate is not suited as an efficient predictor for the future spot rate casts some doubt on the appropriateness of assumption (Ii), although again it should be empha- sized that this conclusion ig'conditional upon equation (8) being a correct representation of the forward rate.

In this paper, we have examined the determination of the forward exchange rate for sterling against the U.S. and Canadian dollars, the Belgian and French francs, and the West German mark over the period 1972--1978, postulating that the forward rate is determined by a combi- nation of arbitrage and speculative activity. The results of estimating a special case of this, in which the forward rate is postulated to be entirely determined by the expected spot rate, on the assumption that the expec- tations on the future spot rate formed by speculators are rational in the sense of Muth, show a marked degree of misspecification, in contrast to the results of Frenkel for the early I92OS. The results of a more general model which, again on the assumption of rational expectations, allows the for- ward rate to be determined by both the expected future spot rate and the interest-parity forward rate also show clear signs of misspecification. Our preferred results appear to be well-specified, and allow the expectations generating mechanism for the expected spot rate to be endogenously determined by the data. In these results, both over the period 1972--1978 and over 1972--1975, for all currencies except the German mark, the weights on arbitrage and speculative activity in the determination of the forward rate are approximately equal. The sterling/German mark forward rate has been determined almost entirely by speculative activity. The expected spot rate revealed by the data is not, however, an efficient pre- dictor of the actual future spot rate, although there are very tentative signs of an improvement in efficiency comparing the period 1972--1978 to the shorter period of 1972--1975.

References

Anderson, T. W., The Statistical A~alysis o/ Time Series. New York, 1971.

Ball, R. J., T. Burns, P. J. Warburton, "The London Business School Model of the UK Economy: An Exercise in International Monetarism". In: Paul A. Ormerod (Ed.), Economic Modelling. London, 1979, pp. 86--114.

Beenstock, Michael, "Monetary Independence under Fixed Exchange Rates: ' The Case of West Germany 1958--1972". In: S. F. Frowen, A. S. Courakis, M. H. Miller (Eds.), Monetary Policy and Economic Activity in West Germany. London, 1977, pp- 213--231.

Weltwirtsehaftlich~ Archly Bd. CXVI. z5

222 Paul A. Ormerod

Beenstock, Michael, "Arbitrage, Speculation, and Official Forward Intervention: The Case of Sterling and the Canadian Dollar". The Review of Economics and Statistics, Vol. 6I, Amsterdam, 1979, pp. 135--139.

- - , Steven Bell, "A Quarterly Econometric Model of the Capital Account of the U.K. Balance of Payments". The Manchester School o/ Economic and Social Studies, Vol. 47, Manchester, 1979, pp. 33 _(72.

Davies, N., C. M. Triggs, P. M. Newbold, "Significance Levels of the Box-Pierce Portmanteau Statistic in Finite Sample". Biometrika, Vol. 64, London, 1977, pp. 517--522.

Frenkel, Jacob A., "The Forward Exchange Rate, Expectations, and the Demand for Money: The German Hyperinflation". The American Economic Review, Vol. 67, Menasha, 1977, PP. 653--()7 o.

- - , "The Purchasing Power Parity: Doctrinal Perspective and Evidence from the I92O'S". Journal o[ h~ternational Economics, Vol. 8, Amsterdam, 1978, pp. 169 to 191.

Haas, Richard D., "More Evidence on the Role of Speculation in the Canadian Forward Exchange Market". The Canadian Journal o~ Economics, Vol. 7, Toronto, 1974, pP- 496--5Ol.

Hendry, David F., Grayham E. Mizon, "Serial Correlation as a Convenient Simpli- fication Not a Nuisance : A Comment on a Study of the Demand for Money by the Bank of England". The Economic Journal, Vol. 88, Cambridge, 1978, pp. 549--563 .

Hodjera, Zoran, "International Short-Term Capital Movements: A Survey of Theory and Empirical Analysis". IMF, Staff Papers, Vol. 20, Washington, 1973, pp. 683--740.

Hutton, John P., "A Model of Short-Term Capital Movements, the Foreign Exchange Market and Official Intervention in the UK, 1963--197 o''. The Review o/Economic Studies, Vol. 44, Edinburgh, 1977, pp. 31--41-

Kesselman, Jonathan, "The Role of Speculation in Forward-Rate Determination: The Canadian Flexible Dollar 1953--196o". The Canadian Journal o/Economics, Vol. 4, Toronto, I97 I, pp. 279--298.

Kohlhagen, Steven W., " 'Rat ional ' and 'Endogenous' Exchange Rate Expectations and Speculative Capital Flows in Germany". Weltwirtscha[tliches Archly, Vol. I I3, 1977, PP. 624--644.

- - , The Behaviour o/Foreign Exchange Markets - - A Critical Survey o/the Empirical Literature. New York, 1978 .

Lomax, R., M. Denham, The Model o[ External Capital Flows. GES Working Paper, No. 17 , Par t 2, London, 1978 .

McCallum, B. T., "The Role of Speculation in the Canadian Forward Exchange Market: Some Estimates Assuming Rational Expectations". The Review o t Econom- ics and Statistics, Vol. 59, Amsterdam, 1977, PP. 145--151.

Minford, A. P. L., Substitution El~ects, Speculation and Exchange Rate Stability. Amsterdam, 1978 .

The Forward Exchange Rate zz3

Muth, John It., "Rat iona l Expectat ions and the Theory of Price Movements" . Econometrica, Vol. 29, New Haven, I961, pp. 315--335.

National Institute of Economic and Social Research (NIESR), A Listing of National Institute Model IV. Discussion Paper, No. 28, London, 1979.

StoU, Haas R., "An Empirical S tudy of the Forward Exchange Market under Fixed and Flexible Exchange Rate Systems". The Canadian Journal o/ Economics, Vol. ~, Toronto, I968, pp. 55--78.

Wickens, M. R., Rational Expectations and the E/#cient Estimation o[ Econometric Models. Universi ty of Essex Working Paper, No. 35, Colchester, 1976 .

Z u s a m m e n f a s s u n g : Die Terminkurse fiir das Pfund Sterling und die Effizienz yon Erwartungen. - - Dieser Aufsatz untersucht die Effizienz yon Erwar tungen auf dem Terminmark t ffir das Pfund Sterling gegcnfiber fiinf bedeutenden W/~hrungen in den Jahren yon 1972 bis i978. Dabei wird unterstellt , dab der Terminkurs das gewogene Mittel aus dem sich aus der Zinsparit~t ergebenden Terminkurs und dem erwarteten Kassakurs ist. Unter der Annahme, dab die Erwartungen hinsichtl ich der zuktinftigen Kassakurse rational sind, zmgen die Gleichungen deutliche All- zeichen yon falscher Spezifizierung. Eine ailgemeinere Spezifizierung gestat te t es, den Mechanismus der Erwar tungsbi ldung endogen dutch die Daten best immen zu lassen. Diese Gleichungen sind gut spezifiziert und deuten darauf hin, dab die sich aus den Daten ergebenden Werte fur die erwarteten Kassakurse zwar unverzerrte, aber ineffiziente SchAtzungen ftlr die tatsgch]ichen Kassakurse sind.

R 6 s u m 6 : Le t aux de change ~ terme pour la livre sterling et l 'efficience des expectatives. - - Cet article analyse l'efficience des expeetatives sur le march6 de change ~ terme pour la livre sterling vis-a-vis cinq monnaies importantes pendan t la p6riode 1972--1978. I1 est postuM que le t aux ~t terme est une moyenne pond6r6e du t aux ~ terme d'int6r~t-parit6 et du taux au comptant a t tendu. Sous la supposi- tion que ies expectatives sur le t aux au comptan t fu tur soient rationelles, les 6qua- tions estim6es d6montrent des clairs signes de mis-sp~cification. Une specification plus g6u~rale permet de d6terminer endog~nement le m~canisme de formation des expectatives. Ces ~quations sont bien sp~cifi~es et sugg~rent que les t a ux au comp- rant a t tendus qui sont r6v6Ms par les donn~es sont des variables de pronostic sans biais mais pus efficientes du t aux au comptant actuel.

R e s u m e n : La tasa de cambio a futuro para la libra esterlina y la eficiencia de las expectativas. - - En este articulo se investiga la eficiencia de las expectat ivas en el mercado cambiario a futuro para la libra esterlina frente a cinco monedas importantes para el periodo entre 1972 y 1978. La tasa de canxbio a futuro se define como el promedio ponderado de la tasa de inter6s de paridad a futuro y la tasa *spot, esperada. Bajo el supuesto que las expectat ivas de la tasa spot fn tura son

I5"

224 P a u l A. Ormerod The Forward Exchange Rate

racionales, las ecuaciones es t imadas muest ran claros signos de mala especificaci6n. Una especificaci6n mhs general permite que el mecanismo de generaci6n de expectati- vas sea determinado end6genamente por los datos. Estas ecuaciones est~n bien especificadas y sugieren que las series de las tasas spot esperadas reveladas por los datos han sido predictores sin sesgo pero ineficientes de la tasa spot real.