the effects of stock market rumors on stock prices: evidence from an emerging market

TRANSCRIPT

eJournal of Multinational Financial Management

11 (2001) 105–115

The effects of stock market rumors on stockprices: evidence from an emerging market

Halil Kiymaz *Finance and Economics-SBPA, Uni6ersity of Houston-Clear Lake, Houston, TX 77058, USA

Received 5 June 1999; accepted 18 February 2000

Abstract

The purpose of this study is to investigate the effects of stock market rumors on the pricesof stocks traded at the Istanbul Stock Exchange. The sample consists of 355 favorablerumors mentioned in the HOTS column of ‘Ekonomik Trend ’. While positive significantabnormal returns are observed in each of the 4 days prior to the publication date, negativeinsignificant abnormal returns are detected in the post-publication period. The findings in thepre-publication period refute the strong form of market efficiency while the findings in thepost-publication period suggest that investment decisions based on the published rumorswould not benefit investors. A further analysis based on the content of rumor shows thatearning expectations’ rumors, and purchases by foreign investors rumors generate greaterimpact on stock prices than other rumors. © 2001 Elsevier Science B.V. All rights reserved.

JEL classification: G14; G15

Keywords: Stock market rumors; Emerging market; Istanbul stock exchange

www.elsevier.com/locate/econbase

1. Introduction

Although the behavior of stock market prices has been investigated extensively,the question of whether trading based on a particular set of information can leadinvestors to obtain excess returns remains as an interesting topic to study. Studiesinvestigating effects of analysts’ recommendations or rumors on stock prices are

* Tel.: +1-281-2833208; fax: +1-181-2833951.E-mail address: [email protected] (H. Kiymaz).

1042-444X/01/$ - see front matter © 2001 Elsevier Science B.V. All rights reserved.

PII: S1042 -444X(00 )00045 -1

H. Kiymaz / J. of Multi. Fin. Manag. 11 (2001) 105–115106

mainly related to the market efficiency hypothesis. The strong form of the efficientmarket hypothesis assumes that all information, whether public or private, israpidly incorporated into security prices that no investor can use it to earn excessreturns. Although the initial studies (i.e. Diefenback, 1972; Logue and Tuttle, 1973)argue that information based on market rumors does not have any economic value,later studies report statistically significant stock price reactions to stock marketrumors. The majority of studies in literature seem to refute the market efficiencyhypothesis in its strongest form. These studies document the existence of significantabnormal returns following analysts’ recommendations or rumors. Among themLloyd-Davies and Canes (1978), Syed et al. (1989), Liu et al. (1990), Barber andLoeffler (1993) report abnormal stock price performance following recommenda-tions reported in the Dartboard column of the Wall Street Journal (WSJ).

The objective of this study is to investigate whether stock market rumors haveany impact on common stocks traded at the Istanbul Stock Exchange (ISE) byexamining the ‘Heard on the Street’ (HOTS) column of ‘Ekonomik Trend ’ (ET)weekly. Furthermore, the impact of the content of the rumors on stock prices isinvestigated. The results of this study provide additional international evidence oneffects of rumors on stock prices. The empirical findings show the existence ofpositive and significant abnormal returns in each of the 4 days prior to thepublication date, and negative insignificant abnormal returns in the post-publica-tion period. These results suggest that rumors and gossips contained in the HOTScolumn have been disseminated prior to their publication. A further analysis basedon the content of rumor reveals that the earning expectation rumors and purchasesby foreign investors rumors generate greater impact on stock prices than otherrumors.

2. Literature review

The question of whether trading based on recommendations and/or rumorspublished in newspaper or magazines would benefit investors has been investigatedextensively. The empirical studies in this subject report mixed results. Diefenback(1972) and Logue and Tuttle (1973) are two initial studies reporting that analysts’recommendations have no value for investors. Later studies, on the other hand,report that information provided by the Wall Street Journal Heard on the Streetcolumn or analysts contain valuable information to investors. Lloyd-Davies andCanes (1978) focus on financial analysts’ recommendations as discussed in theHOTS column of the WSJ. They report that buy recommendations providesignificant positive abnormal returns, while sell recommendations are associatedwith significant negative abnormal returns on the day of publication. They concludethat analysts and investment advisors provide valuable service to investors. Liu etal. (1990) extend the Lloyd-Davies and Canes (1978) study with more recent sampleand further analyze the effects of the single-company versus multi-company recom-mendations, and the trading volume around the publication day. Their findings arein the line with the Lloyd-Davies and Canes (1978) study. Moreover, the results

H. Kiymaz / J. of Multi. Fin. Manag. 11 (2001) 105–115 107

indicate that investors respond earlier to the information and single companyrecommendations have greater impact on the stock prices than those of multi-com-pany recommendations. Finally, they report higher trading volume around thepublication day.

There are also studies investigating the factors influencing the magnitude of stockmarket reaction to analysts’ information or recommendation provided by variouspublications. Beneish (1991) investigates explanations for the significant stock pricereaction to analysts’ information reported in the ‘HOTS’ column of the WSJ. Theresults indicate that market reaction persists after controlling for confoundingreleases. Furthermore, stock prices adjust prior to publication when recommenda-tions are reported on a single firm. Huth and Maris (1992) examine the same issuein terms of the usefulness of recommendations in short term trade decision makingand firm size. The findings indicate that information obtained from the HOTScolumn can produce statistically significant stock price movements. Firm size isfound to be important only for negative comments in the column. Barber andLoeffler (1993) analyze the stock price and volume behaviors using recommenda-tions published in the Dartboard column of the WSJ. They report average positiveabnormal returns of 4% in 2 days following the publication. Furthermore, averagevolume doubles normal volume level in the same period.

More recently, Mathur and Waheed (1995) investigate the stock price behavior offirms that are favorably mentioned in the ‘Inside Wall Street’ column of BusinessWeek. The results reveal the existence of positive significant abnormal returns onthe day before the publication date, the publication date, and 2 days after thepublication date. The study suggests that information provided by the column isvaluable to short term traders if transaction costs are low. Moreover, the resultsindicate that investors who invest long term based on the information obtain rateof returns below market returns.

In general, the studies on stock market rumors or analysts’ recommendationssupport the view that information provided to investors is valuable. This paperaims to investigate the effects of stock market rumors on stocks traded at the ISEto provide evidence from an emerging market.

3. Data and methodology

The study uses the stock market rumors published in the HOTS column of the‘ET ’ weekly magazine during the period of July 21, 1996 and August 17, 1997.1 TheHOTS page is published every week in ET. Topics covered in the page includeinformation about both single firms and a group of firms. The purpose of the pageis to inform investors about market developments influencing stock prices. Informa-tion provided by the HOTS, with rare exceptions, is favorable.

1 The study period of 1996–1997 is randomly selected.

H. Kiymaz / J. of Multi. Fin. Manag. 11 (2001) 105–115108

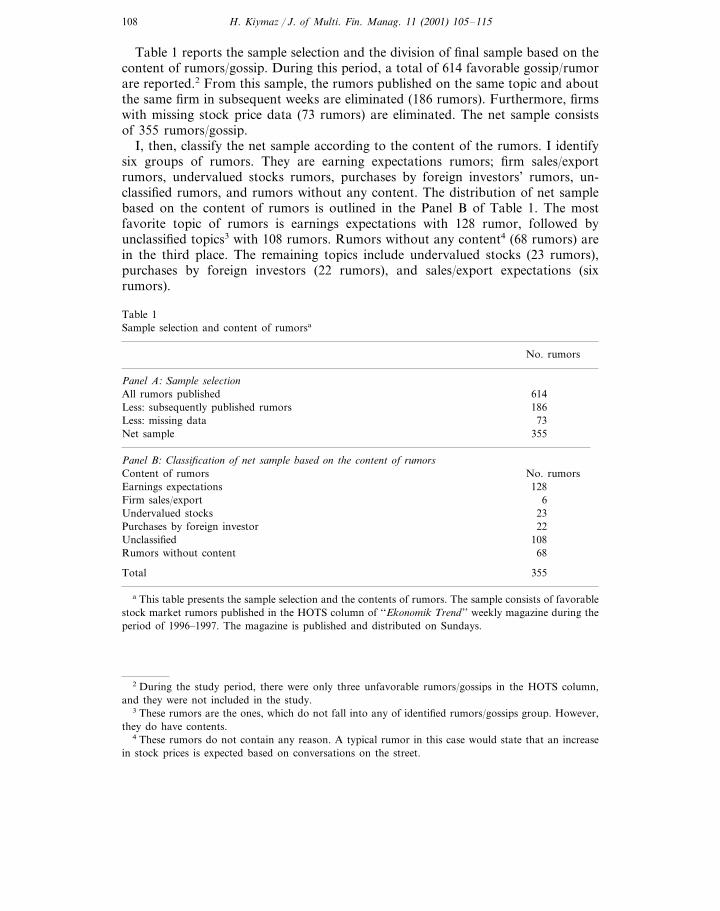

Table 1 reports the sample selection and the division of final sample based on thecontent of rumors/gossip. During this period, a total of 614 favorable gossip/rumorare reported.2 From this sample, the rumors published on the same topic and aboutthe same firm in subsequent weeks are eliminated (186 rumors). Furthermore, firmswith missing stock price data (73 rumors) are eliminated. The net sample consistsof 355 rumors/gossip.

I, then, classify the net sample according to the content of the rumors. I identifysix groups of rumors. They are earning expectations rumors; firm sales/exportrumors, undervalued stocks rumors, purchases by foreign investors’ rumors, un-classified rumors, and rumors without any content. The distribution of net samplebased on the content of rumors is outlined in the Panel B of Table 1. The mostfavorite topic of rumors is earnings expectations with 128 rumor, followed byunclassified topics3 with 108 rumors. Rumors without any content4 (68 rumors) arein the third place. The remaining topics include undervalued stocks (23 rumors),purchases by foreign investors (22 rumors), and sales/export expectations (sixrumors).

Table 1Sample selection and content of rumorsa

No. rumors

Panel A: Sample selectionAll rumors published 614

186Less: subsequently published rumorsLess: missing data 73Net sample 355

Panel B: Classification of net sample based on the content of rumorsContent of rumors No. rumors

128Earnings expectationsFirm sales/export 6Undervalued stocks 23

22Purchases by foreign investorUnclassified 108Rumors without content 68

355Total

a This table presents the sample selection and the contents of rumors. The sample consists of favorablestock market rumors published in the HOTS column of ‘‘Ekonomik Trend ’’ weekly magazine during theperiod of 1996–1997. The magazine is published and distributed on Sundays.

2 During the study period, there were only three unfavorable rumors/gossips in the HOTS column,and they were not included in the study.

3 These rumors are the ones, which do not fall into any of identified rumors/gossips group. However,they do have contents.

4 These rumors do not contain any reason. A typical rumor in this case would state that an increasein stock prices is expected based on conversations on the street.

H. Kiymaz / J. of Multi. Fin. Manag. 11 (2001) 105–115 109

Table 2Daily average abnormal returns (AARs) surrounding the publication of rumorsa

Event days t-valueAARs (%)

−0.99−10 −0.17−9 −0.03 −0.02−8 −0.26 −1.29−7 0.21 1.49−6 −0.05−0.08−5 −0.20 −0.21−4 3.29***0.52−3 0.29 2.14**−2 4.89***0.76−1 0.78 3.60***

0 – –+1 0.07 0.36+2 −2.65**−0.43+3 −0.04 −0.06+4 −1.12−0.37+5 −0.04 −0.44+6 −1.44−0.21+7 0.21 1.31+8 −0.01−0.04+9 −0.10 −0.09

+10 −1.42−0.42

a This table presents the abnormal returns surrounding the publication date t=0 in the EkonomikTrend. Abnormal return is calculated as the difference between the actual and expected return. Expectedreturn is generated from the market model parameters. The ISE Composite index used as a proxy formarket. The t-statistics tests the null hypothesis that the average abnormal returns are equal to zero.

*** Statistically significant at 1%.** Statistically significant at 5%.

The event study methodology is employed to analyze the effects of rumors/gos-sips on stock prices as surveyed by Brown and Warner (1985). The analysis periodextends from day −30 to +30 relative to publication date t=0.5

4. Empirical results

To determine how stock prices are influenced by rumors, I pose three periodanalyses. The first examines the effect of rumors around the publication date. The

5 Standard event methodology is used to measure the stock price reaction for N firms in each of thegroup of firms. The standard event study methodology is not spelled out here.

H. Kiymaz / J. of Multi. Fin. Manag. 11 (2001) 105–115110

second looks for unusual activity prior to publication of rumors. Finally, I analyzeprice movement after the publication date.

The empirical results are reported on Tables 2–4. The daily average abnormalreturns (AARs) for all rumors are calculated over −30 and +30 period relative tothe event day 0. Only AARs for −10 and +10 period are reported on Table 2.The results indicate that the sample experiences statistically significant positiveabnormal returns prior to publication of rumors. The AARs are 0.52, 0.29, 0.76and 0.78% for the days −4, −3, −2 and −1, respectively. These results arestatistically significant at 1% level. The AARs following the publication day aremostly negative and statistically insignificant. For example, AARs are 0.07% onday +1, −0.43% on day +2, −0.04% on day +3, and −0.37% on day +4.Only AARs on day +2 is statistically significant at 5% level.

The average cumulative abnormal returns (CARs) for all rumors are reported onTable 3. In the top part of table, the CARs around the publication of rumors arereported. The results indicate that firms experience positive abnormal returns justbefore and after publication date. For example, during (−1, +1), (−2, +2), and

Table 3Cumulative abnormal returns (CARs) surrounding the publication of rumorsa

t-valueCARs (%)Windows

Combined periods0.85 2.80***(−1, +1)

3.09***1.19(−2, +2)3.42***1.35(−5, +5)1.89*0.44(−10, +10)

−0.75(−20, +20) −0.28−1.22(−30, +30) −0.49

Prior to publication date2.16(−5, −1) 6.13***1.82 4.06***(−10, −1)1.48(−20, −1) 2.60**

After publication date−0.81(+1, +5) −1.31−1.38 −1.39(+1, +10)−1.78(+1, +20) −1.54

a This table presents the cumulative abnormal returns in combined, pre, and post publication periodrelative to publication date t=0 in the Ekonomik Trend. Abnormal return is calculated as the differencebetween the actual and expected return. Expected return is generated from the international marketmodel parameters. The t-statistics tests the null hypothesis that the cumulative abnormal returns areequal to zero.

*** Statistically significant at 1%.** Statistically significant at 5%.* Statistically significant at 10%.

H. Kiymaz / J. of Multi. Fin. Manag. 11 (2001) 105–115 111

Tab

le4

Dai

lyav

erag

eab

norm

alre

turn

s(A

AR

s)ba

sed

onth

eco

nten

tof

rum

orsa

Und

erva

lued

stoc

ksE

arni

ngs

expe

ctat

ions

Unc

lass

ified

rum

ors

Rum

ors

wit

hout

cont

ent

Day

sP

urch

ases

byfo

reig

nin

vest

orSa

les/

expo

rtex

pect

atio

ns(n

=68

)(n

=22

)(n

=23

)(n

=6)

(n=

108)

(n=

128)

t-va

lue

AA

Rs

AA

Rs

t-va

lue

AA

Rs

t-va

lue

AA

Rs

t-va

lue

t-va

lue

AA

Rs

t-va

lue

AA

Rs

0.15

−0.

62−

0.56

−0.

15−

0.35

0.81

0.36

−10

0.30

0.30

0.72

−1.

55−

0.52

−0.

40−

1.15

−1.

94**

0.10

0.27

0.24

0.82

0.46

0.66

−0.

791.

13−

91.

17−

0.37

−0.

11−

0.16

0.11

−0.

15−

0.32

−0.

36−

8−

0.58

−1.

490.

04−

0.31

−0.

300.

430.

381.

050.

581.

37−

0.09

0.23

0.04

−7

−0.

020.

130.

450.

02−

0.34

0.87

1.13

−0.

110.

29−

0.07

−6

0.21

−0.

29−

0.78

0.44

0.40

0.08

−0.

110.

751.

74*

−0.

33−

0.04

−1.

03−

0.14

−1.

93*

−5

0.50

0.57

0.19

0.13

0.75

0.65

1.13

0.09

−0.

410.

832.

94**

*−

0.02

−0.

192.

44**

−0.

51−

0.47

−4

0.71

0.97

1.97

*0.

301.

460.

470.

321.

350.

21−

3−

2.27

**−

2.58

0.51

0.21

0.67

0.35

−0.

55−

1.38

1.96

6.32

***

−0.

300.

112.

38**

0.15

0.15

−2

0.22

−0.

120.

371.

412.

17**

2.18

5.88

***

0.37

0.89

−0.

89−

0.46

−0.

56−

1–

––

––

––

––

0–

––

0.81

−1.

46−

2.40

**0.

200.

600.

210.

04+

10.

150.

84−

1.10

−1.

050.

40−

0.28

−0.

09−

0.51

−0.

35−

1.04

−0.

87−

0.11

−1.

60+

2−

0.35

−0.

68−

0.79

−2.

34**

0.24

0.10

0.13

−0.

24−

0.49

−0.

56−

1.07

0.40

0.56

−0.

98−

1.40

+3

−1.

160.

63−

0.60

−0.

99−

0.21

−0.

09−

0.20

0.24

0.42

−0.

62+

4−

1.29

−1.

74−

2.07

**0.

30−

0.07

0.50

1.04

1.65

−0.

13−

0.12

−0.

44−

0.80

−0.

221.

58−

1.36

+5

0.02

−0.

39−

0.95

−0.

20−

0.12

−0.

34−

0.74

−0.

21−

0.68

+6

−0.

74−

0.08

0.06

0.24

−0.

04−

0.10

0.08

0.79

0.64

0.12

1.37

0.00

0.21

+7

0.16

0.41

−0.

530.

21−

0.93

−0.

40−

0.74

−0.

08−

0.06

−0.

11−

0.17

1.05

−0.

57−

0.52

+8

−1.

051.

072.

01**

−0.

46+

9−

1.17

0.21

−0.

07−

0.06

1.16

−0.

22−

1.75

*−

0.80

0.68

0.39

0.68

−0.

34−

0.26

−1.

330.

31−

0.35

0.76

0.81

−1.

15+

10

−2.

08**

aT

his

tabl

epr

esen

tsth

eav

erag

eab

norm

alre

turn

sba

sed

onth

eco

nten

tof

rum

ors,

surr

ound

ing

the

publ

icat

ion

date

t=0

inth

eE

kono

mik

Tre

nd.

Abn

orm

alre

turn

isca

lcul

ated

asth

edi

ffer

ence

betw

een

the

actu

alan

dex

pect

edre

turn

.E

xpec

ted

retu

rnis

gene

rate

dfr

omth

em

arke

tm

odel

para

met

ers.

The

ISE

Com

posi

tein

dex

used

asa

prox

yfo

rm

arke

t.T

het-

stat

isti

cste

sts

the

null

hypo

thes

isth

atth

eav

erag

eab

norm

alre

turn

sar

eeq

ual

toze

ro.

Eve

ntda

y(0

)re

pres

ents

the

day

ofpu

blic

atio

nof

rum

ors/

goss

ips

and

corr

espo

nds

toSu

nday

s.**

*St

atis

tica

llysi

gnifi

cant

at1%

.**

Stat

isti

cally

sign

ifica

ntat

5%.

*St

atis

tica

llysi

gnifi

cant

at10

%.

H. Kiymaz / J. of Multi. Fin. Manag. 11 (2001) 105–115112

(−5, +5) periods, CARs are 0.85, 1.19 and 1.35%, respectively. All of them arestatistically significant at 1% level. In longer time periods firms experience negativeinsignificant abnormal returns. For example, during (−20, +20) and (−30, +30)periods, CARs are −0.28 and −1.22%, respectively. Based on these results, onewould conclude that stock market rumors provide valuable information to in-vestors. Trading based on rumors would provide statistically significant abnormalreturns.

I further analyze the behavior of stock prices in the period prior and after thepublication of rumors. In the middle part of Table 3, the CARs in the pre-publica-tion period for several windows are reported. The CARs in the pre-publicationperiods are positive and statistically significant. For example; during (−20, −1),(−10, −1) and (−5, −1) periods, the CARs are 1.48, 1.82 and 2.16%, respec-tively. While the results of (−20, −1) period is statistically significant at 5%,others are statistically significant at 1% level. The significant positive stock pricereaction in the pre-publications days may be explained by two interpretations. Thefirst one is related to the possible use of information by those who initially possesit. These may include insiders, who may use information for their trading, andstock analysts, who may supply information to their clients for trading. The secondinterpretation can be attributed to the nature of the HOTS column itself. Typically,the stocks mentioned in HOTS are those that recently have been performing well.This may be one of the reasons why almost all HOTS rumors/gossips are favorable.

Finally, in the bottom part of Table 3, CARs in the after-publication period areanalyzed. The CARs for (+1, +5), (+1, +10) and (+1, +20) windows are−0.81, −1.38 and−1.78%, respectively. None of these results is statisticallysignificant. The negative gains in the after publication period would support theview that trading based on the rumors would not benefit to investors and informa-tion does not have any value. These results are contrary to those of recent USstudies, which reports a positive price reaction after the publication date. Theresults of this study seem to suggest the possible dissemination of information priorto the publication date.

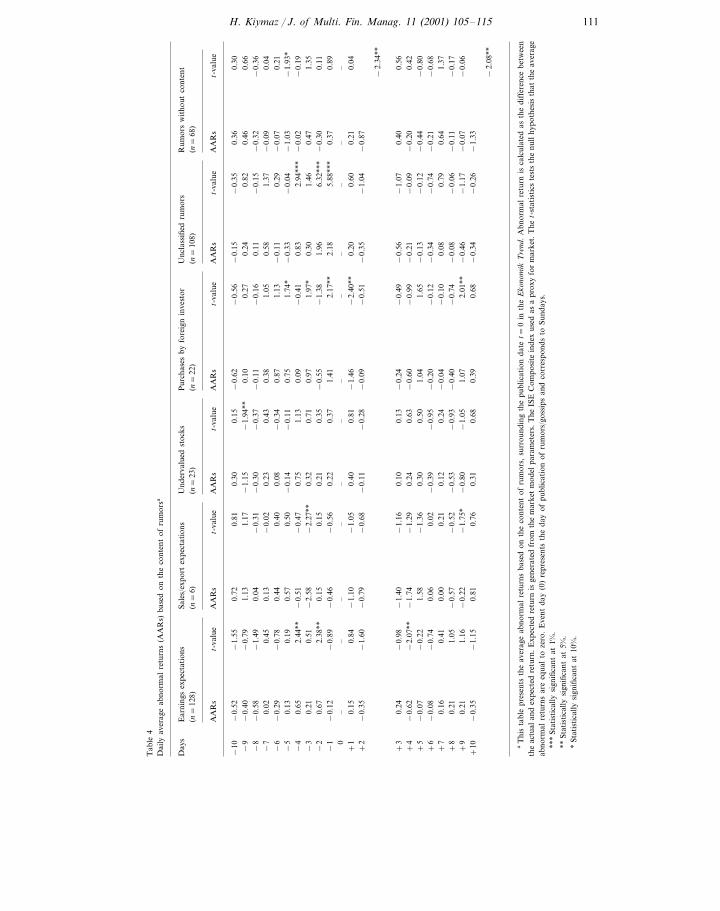

To further analyze the differences in stock price reaction with respect to thecontents of rumors, I classify gossips into six sub-groups. The results of AARs arereported on Table 4. When the pre-publication period is examined, earning expecta-tions rumors, purchases by foreign in6estor rumors, and unclassified rumors groupshave positive significant abnormal returns. For example; earning expectationsrumors group experiences abnormal returns of 0.65 and 0.67% on days −4 and−2. Both findings are statistically significant at 5% level. Unclassified rumors groupshows the highest abnormal returns in pre- publication period. The AARs are 2.18,1.96 and 0.83% for the days −1, −2, and −4, respectively. All of them arestatistically significant at 1% level. The rest of the groups do not show anystatistically significant specific patterns. In the period following the publication ofrumors, the AARs are mostly negative and some of them are statistically signifi-cant. For example; earning expectations group has a return of −0.62% on day+4, which is statistically significant at 5% level. Similarly, purchases by foreigninvestors group experiences a return of −1.46% on the day +1.

H. Kiymaz / J. of Multi. Fin. Manag. 11 (2001) 105–115 113

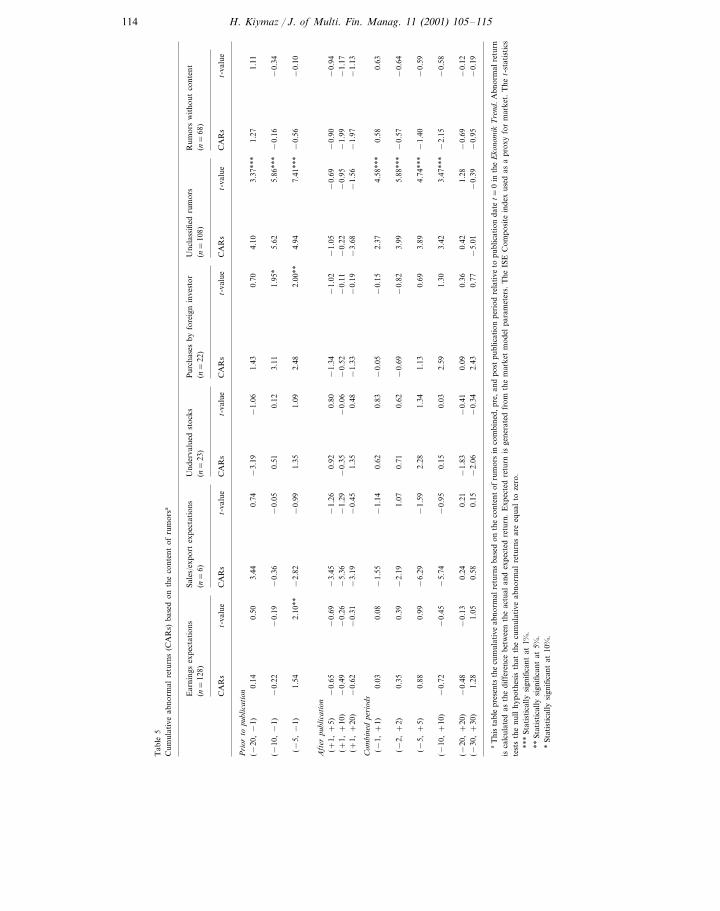

Table 5 reports for CARs for three periods based on the subjects of rumors. Inpre-publication period positive CARs are observed for earning expectations’ rumors,purchases by foreign in6estors rumors, and unclassified rumors groups. For example;earning expectations’ rumors group experience CARs of 1.54% during (−5, −1)windows, purchases by foreign in6estors rumors and unclassified rumors groups haveCARs of 2.48 and 4.94% in the same time period. While the first two results arestatistically significant at 5% level, the last one is highly significant at 1% level.

In the after publication period, all CARs are negative but none of them isstatistically significant. For combined periods, only CARs for other topics arestatistically significant. For example; CARs are 2.37, 3.99, 3.89% in the windows(−1, +1), (−2, +2) and (−5, +5) respectively. The analysis of content ofrumors reveals that there are differences in abnormal returns with respect to thecontent of stock market rumors. Clearly rumors related to earning expectations andpurchases by foreign in6estors have greatest impact on stock prices, while othershave statistically insignificant effects.

Overall, the empirical results indicate the existence of positive statistically signifi-cant abnormal returns in the pre-publication period of rumors. Such findings wouldrefute the strong form of market efficiency, and are in line with the existingliterature. The findings pertaining to the post-publication of rumors, on the otherhand, show that there are statistically insignificant negative abnormal returns. Thissuggests that investment strategies based on the published rumors would notgenerate any wealth gains to investors, implying that information provided bycolumn does not have any value at all. The results seem to suggest the possibledissemination of information prior to publication, and are contrary to those of USstudies.

5. Summary and conclusions

The question of whether the trading based on a particular set of information canlead investors to obtain abnormal returns continues to receive attention fromresearchers and investors. A vast majority of these studies on analysts’ recommen-dations and stock market rumors reports statistically significant stock price reactionto the publication of information and, hence, concludes that information has value.

This study investigates the effects of stock market rumors/gossips on the prices ofstocks traded at the ISE by using 355 favorable rumors mentioned on the HOTScolumn of ‘ET ’. The empirical findings suggest that there are statistically significantabnormal returns around the publication date. While positive, significant abnormalreturns are observed in each of the 4 days prior to the publication date, negativeinsignificant abnormal returns are detected in the post-publication period. Thesignificant stock price reaction in pre-publications days may be interpreted in twoways. The first one is related to the possible use of information by either insider,who may use information for their trading, or stock analysts, who may supplyinformation to their clients for trading. This interpretation suggests the dissemina-tion of information prior to publication. The second interpretation can be at-

H. Kiymaz / J. of Multi. Fin. Manag. 11 (2001) 105–115114

Tab

le5

Cum

ulat

ive

abno

rmal

retu

rns

(CA

Rs)

base

don

the

cont

ent

ofru

mor

sa

Und

erva

lued

stoc

ksP

urch

ases

byfo

reig

nin

vest

orU

ncla

ssifi

edru

mor

sR

umor

sw

itho

utco

nten

tSa

les/

expo

rtex

pect

atio

nsE

arni

ngs

expe

ctat

ions

(n=

68)

(n=

128)

(n=

22)

(n=

6)(n

=10

8)(n

=23

)

t-va

lue

CA

Rs

t-va

lue

CA

Rs

t-va

lue

CA

Rs

t-va

lue

CA

Rs

CA

Rs

t-va

lue

CA

Rs

t-va

lue

Pri

orto

publ

icat

ion

−1.

061.

430.

70(−

20,−

1)4.

100.

143.

37**

*0.

501.

271.

113.

440.

74−

3.19

0.12

3.11

1.95

*5.

625.

86**

*0.

51−

0.05

−0.

16−

0.36

−0.

34−

0.19

(−10

,−

1)−

0.22

1.09

2.48

2.00

**4.

947.

41**

*1.

54−

0.56

(−5,

−1)

−0.

102.

10**

−2.

82−

0.99

1.35

Aft

erpu

blic

atio

n0.

80−

1.34

−1.

02−

1.05

−0.

65−

0.69

−0.

69−

0.90

−0.

94(+

1,+

5)−

3.45

−1.

260.

92−

0.06

−0.

52−

0.11

−0.

22(+

1,+

10)

−0.

95−

0.49

−1.

99−

1.17

−0.

26−

5.36

−1.

29−

0.35

0.48

−1.

33−

0.19

−3.

68−

1.56

−1.

97−

1.13

1.35

−0.

62−

0.31

−3.

19−

0.45

(+1,

+20

)

Com

bine

dpe

riod

s−

1.14

0.62

0.83

−0.

05−

0.15

2.37

4.58

***

0.08

0.58

0.63

(−1,

+1)

−1.

550.

03

0.62

−0.

69−

0.82

3.99

5.88

***

0.35

0.71

−0.

57(−

2,+

2)−

0.64

1.07

−2.

190.

39

1.34

1.13

0.69

3.89

4.74

***

0.88

−1.

40−

0.59

(−5,

+5)

0.99

−6.

29−

1.59

2.28

0.03

2.59

1.30

3.42

3.47

***

0.15

−0.

95−

2.15

−0.

45−

0.58

−5.

74−

0.72

(−10

,+

10)

−0.

48−

1.83

−0.

410.

090.

360.

421.

28−

0.69

−0.

12−

0.13

0.24

(−20

,+

20)

0.21

0.15

−2.

06−

0.34

2.43

0.77

−5.

01−

0.39

−0.

95−

0.19

1.28

(−30

,+

30)

1.05

0.58

aT

his

tabl

epr

esen

tsth

ecu

mul

ativ

eab

norm

alre

turn

sba

sed

onth

eco

nten

tof

rum

ors

inco

mbi

ned,

pre,

and

post

publ

icat

ion

peri

odre

lati

veto

publ

icat

ion

date

t=0

inth

eE

kono

mik

Tre

nd.A

bnor

mal

retu

rnis

calc

ulat

edas

the

diff

eren

cebe

twee

nth

eac

tual

and

expe

cted

retu

rn.

Exp

ecte

dre

turn

isge

nera

ted

from

the

mar

ket

mod

elpa

ram

eter

s.T

heIS

EC

ompo

site

inde

xus

edas

apr

oxy

for

mar

ket.

The

t-st

atis

tics

test

sth

enu

llhy

poth

esis

that

the

cum

ulat

ive

abno

rmal

retu

rns

are

equa

lto

zero

.**

*St

atis

tica

llysi

gnifi

cant

at1%

.**

Stat

isti

cally

sign

ifica

ntat

5%.

*St

atis

tica

llysi

gnifi

cant

at10

%.

H. Kiymaz / J. of Multi. Fin. Manag. 11 (2001) 105–115 115

tributed to the nature of the HOTS column itself. Typically, the stocks mentionedin HOTS are those that recently have been performing well.

The negative insignificant abnormal returns in the post-publication period maysuggest that investment decisions based on the published rumors would not benefitinvestors. Hence, information provided by such columns may not have any value.A further analysis based on the content of rumors/gossips reveals that earningexpectations’ rumors, purchases by foreign investor rumors generate higher abnor-mal returns than other rumors.

Acknowledgements

I thank the participants at the 1999 meeting of Financial Management Associa-tion International, the editor, and an anonymous referee for helpful suggestions onan earlier draft.

References

Barber, B.M., Loeffler, D., 1993. The dartboard column: second-hand information and price pressure.Journal of Financial and Quantitative Analysis 28, 273–283.

Beneish, M.D., 1991. Stock prices and the dissemination of analysts’ recommendations. Journal ofBusiness 64, 393–416.

Brown, S.J., Warner, J.B., 1985. Using daily stock returns: the case of event studies. Journal of FinancialEconomics 14, 3–31.

Diefenback, R., 1972. How good is institutional brokerage research. Financial Analyst Journal 28,54–60.

Huth, W.L., Maris, B.A., 1992. Large and small firm stock price responses to heard on the streetrecommendations. Journal of Accounting and Auditing 7, 27–47.

Liu, P., Smith, D., Syed, A., 1990. Stock reaction to the Wall Street Journal’s securities recommenda-tions. Journal of Financial and Quantitative Analysis 25, 399–410.

Lloyd-Davies, P., Canes, M., 1978. Stock prices and publication of second-hand information. Journal ofBusiness 51, 43–56.

Logue, D., Tuttle, D., 1973. Brokerage houses investment advises. The Financial Review 8, 38–54.Mathur, I., Waheed, A., 1995. Stock price reactions to securities recommended in Business Week’s inside

Wall Street. The Financial Review 30, 583–604.Syed, A., Lui, P., Smith, S., 1989. The exploitation of inside information at the Wall Street Journal: a

test of strong form efficiency. The Financial Review 24, 567–759.

.