the effects of globalization on the accounting academic marlene plumlee university of utah western...

TRANSCRIPT

1

The Effects of Globalization on the Accounting Academic

MARLENE PLUMLEE

UNIVERSITY OF UTAH

Western AAA – April 2012

2

Using a Global perspective to enhanceTEACHING

RESEARCH

Disclaimer! These are my perspectives, a function of my experiences and preferences. Proceed with caution!

3

Teaching – use IFRS to your advantage. Consider IFRS a tool to teach financial reporting and other

things =>> Within your classroom.Concrete examples of the uncertainty and ambiguity

inherent in financial reporting.Helps tie financial reporting to the underlying economics

and the conceptual framework.

4

My class.

Focus on commonalities in the accounting differences to highlight both the similarities and differences in the recording and reporting.

Categorize differences across the standards into SUBSTANTIVE (REAL) and COSMETIC (visual) differences.

Within SUBSTANTIVE differences, consider three PROCESSING differences.

5

Processing differences.

Classification – Location within a given statement.Discuss ratios and the importance of subtotals.Emphasize substance versus form.Highlight the association between classification and how

it affects related transactions.

Easy example: Deferred taxes. More complicated: Debt/equity.

6

Processing differences.

Recognition threshold – location across statements.Review asset, liability, other definitions.Emphasize judgment involved.

Easy example: Provisions. More complicated: Development costs; Impairments.

7

Processing differences.

Measurement – which attribute is employed.Review various ways to measure value.Emphasize when issues arise.Discuss relevance and reliability.Cover Level 1, 2, and 3 fair values.

Easy example: Provisions More complicated: Inventory

8

Teaching – use IFRS to your advantage.

Consider IFRS a tool to reach students =>>across your department and school.

Teach across (all) levels.Opportunity to ‘refresh’ more advanced students’

understanding and focus on usefulness of information to all students.

Highlight use of ratios and other tools and the role that classification, measurement, and recognition threshold play.

9

My class.Discussion of measurement highlights the “Mixed

attribute model” within all reporting systems.Use paired sets of financials (US GAAP and IFRS filers) to

highlight how different firms can “look”.In class exercise #1.Importance of understanding how information is

prepared. GIGO.

10

Teaching – use IFRS to your advantage.

Consider IFRS a tool to broaden how we define accounting education=>>across the (academic) profession.Focus on understanding the association between financial reports

and economics.Nice place to consider ‘other issues’ that might be overlooked.

the role of regulators/standard setters/auditors in financial reporting.

Understanding the process of standard setting and inherent political issues.

11

My classPractical approach to roles ‘players’ have.

Highlight the roles the SEC, monitoring board, European Commission, FSA.And define them!

Consider the political and practical issues of operating in a global world.

Discuss accounting issues related to the 2008 financial crisis.

12

– but don’t over-invest!

Focus on the concepts.

Remember/recognize what you know already.

Details are changing, so take this into account when you are learning and incorporating content in your class.

Still lack good resources!!

13

Research – broaden your horizons!IFRS-related research has increased.

More data (in general).More ‘common’ data.More interest.

14

Some practicalitiesInteresting and sometimes new questions/places to ask

old questions.

Many more studies being published in top tier journals.Good news – more interested, engaged reviewers.Bad news – more competition!

15

“New” questions….Somewhat specific to the setting =>>Costs and

benefits of IFRS.Basic &broad question with lots of places to look

for/at this!Equity markets.Debt markets.Regulatory process.Role of institutions.

16

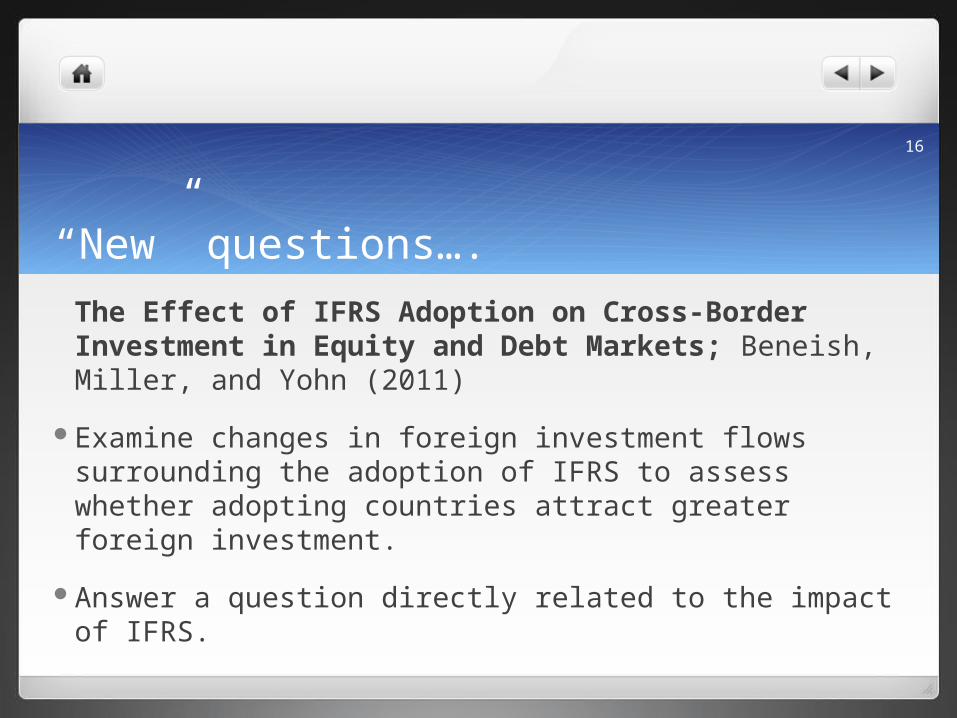

“New” questions….

The Effect of IFRS Adoption on Cross-Border Investment in Equity and Debt Markets; Beneish, Miller, and Yohn (2011)

Examine changes in foreign investment flows surrounding the adoption of IFRS to assess whether adopting countries attract greater foreign investment.

Answer a question directly related to the impact of IFRS.

17

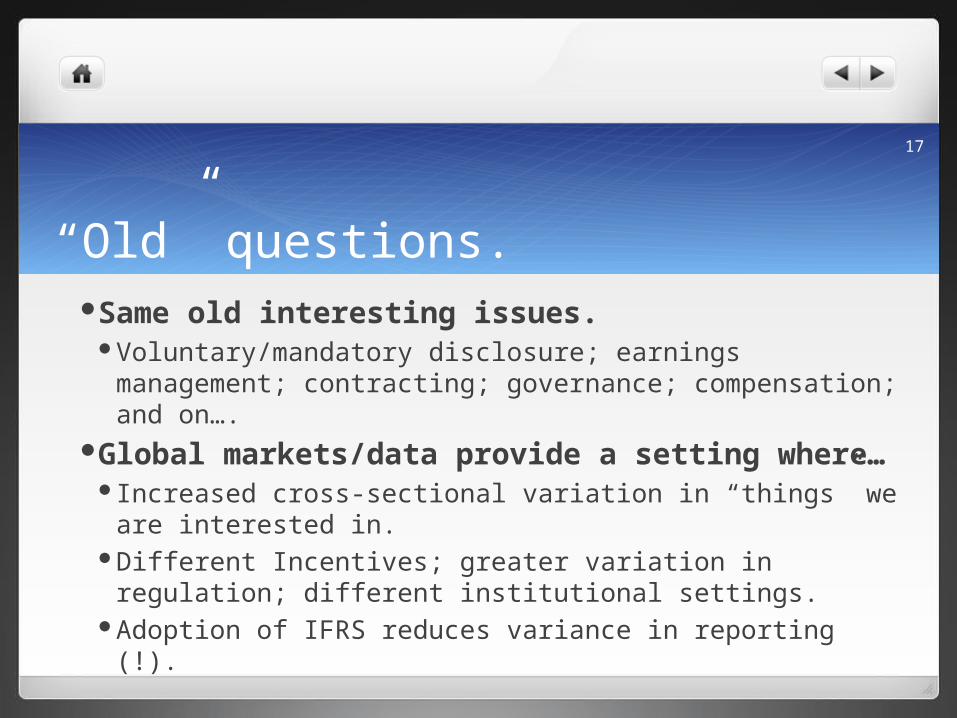

“Old” questions.Same old interesting issues.

Voluntary/mandatory disclosure; earnings management; contracting; governance; compensation; and on….

Global markets/data provide a setting where…Increased cross-sectional variation in “things” we are

interested in.Different Incentives; greater variation in regulation;

different institutional settings.Adoption of IFRS reduces variance in reporting (!).

18

Old question – new setting.International Differences in the Cost of Equity Capital: Do Legal

Institutions and Securities Regulation Matter? Hail and Leuz; JAR 2006 Examine cross-country differences in COEC => explained by variation in

disclosure, regulation, and enforcement. More variation in legal institutions and regulation than found within

the US. Adoption of IFRS allows for the estimation of cost of capital across

countries, which was more difficult when firms used different standards.

19

However, beware the “in bed” approach.Consider how, why, where we would expect the findings to be

different.

Framing the question Does cost of capital vary by country?Analysis of the effectiveness of legal institutions and

securities regulation.

20

ANY QUESTIONS?