the continuous mortality investigation bureau chris daykin, cmi executive committee

TRANSCRIPT

The Continuous Mortality Investigation Bureau

Chris Daykin,

CMI Executive Committee

The CMIB

• History

• Role

• Structure

• Funding

• Investigations

• Reporting results

NB “Office” = “company”

History• actuaries produced Mortality table - 1843

– “Seventeen Offices’ Table”– assured lives– experience up to 1837

• further tables during 19th century• investigation into annuitants 1900-20• continuous collection of data started in

1924 – emergence of the CMI Bureau

Features

• sponsored by the actuarial profession

• continuous investigations

• independent

• confidentiality is paramount

• production of standard mortality tables

• actuarial profession provides expertise

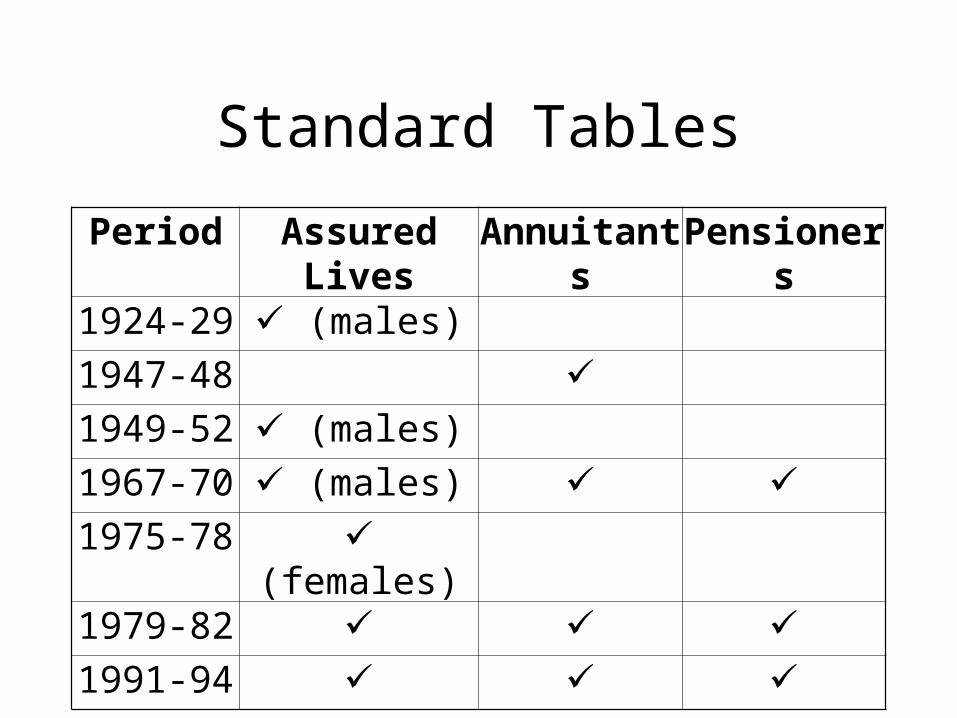

Standard Tables

Period Assured Lives Annuitants Pensioners

1924-29 (males)

1947-48 1949-52 (males)

1967-70 (males) 1975-78 (females)

1979-82 1991-94

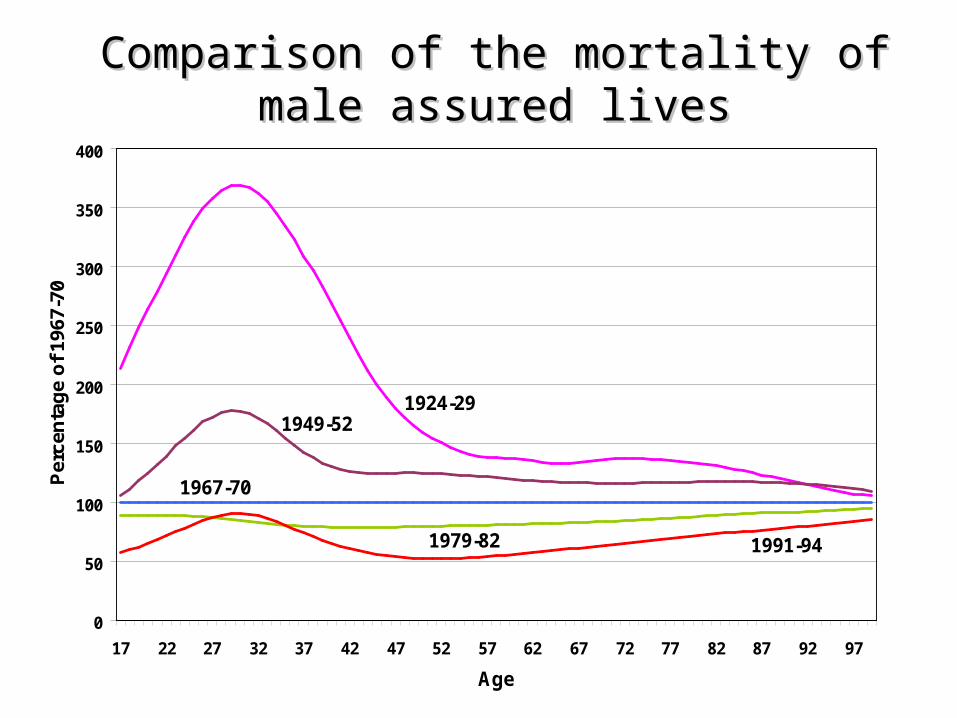

Comparison of the mortality of male assured livesComparison of the mortality of male assured lives

0

50

100

150

200

250

300

350

400

17 22 27 32 37 42 47 52 57 62 67 72 77 82 87 92 97

Age

Per

cen

tag

e o

f 19

67-7

0

1924-291949-52

1967-70

1991-941979-82

Role of CMI• Research – Mortality, IP and CI.

– Methodologies– Graduation– Models

• Data collection• Analysis & reporting

– Industry experience– Contributing offices

• Standard Tables• Projecting future experience

Structure

Life Companies and Profession

CMIB

Life Companies

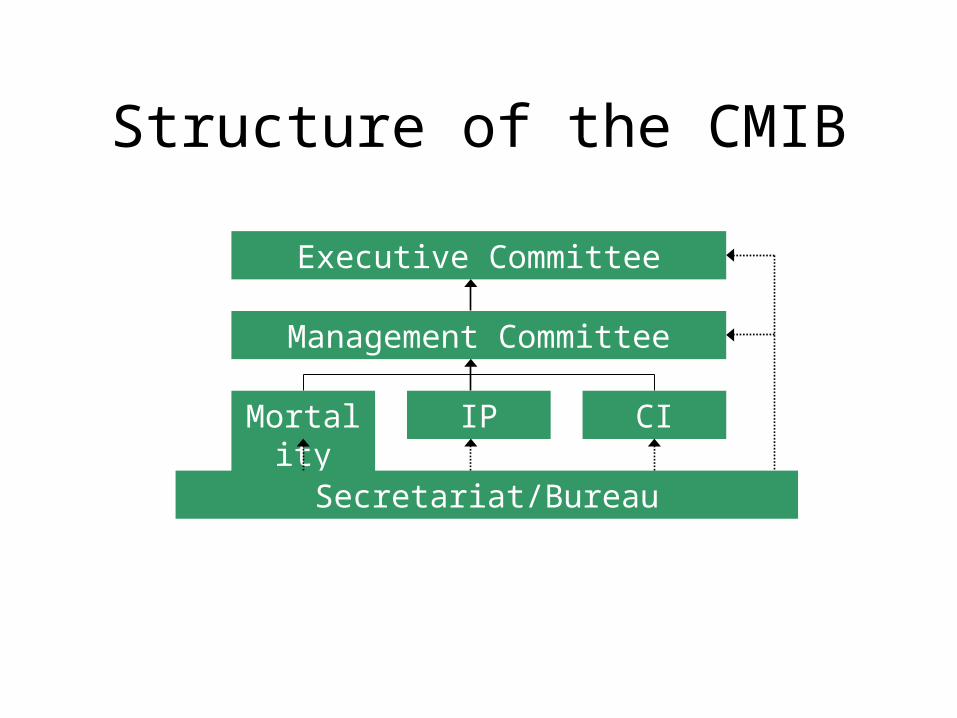

Structure of the CMIB

Executive Committee

Management Committee

Mortality IP CI

Secretariat/Bureau

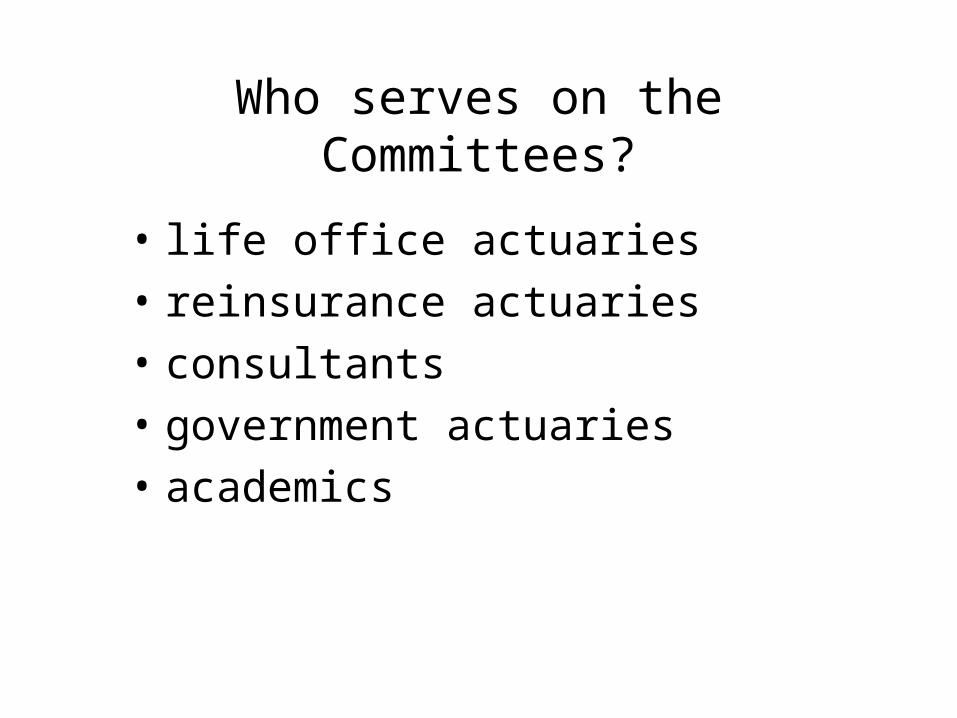

Who serves on the Committees?

• life office actuaries

• reinsurance actuaries

• consultants

• government actuaries

• academics

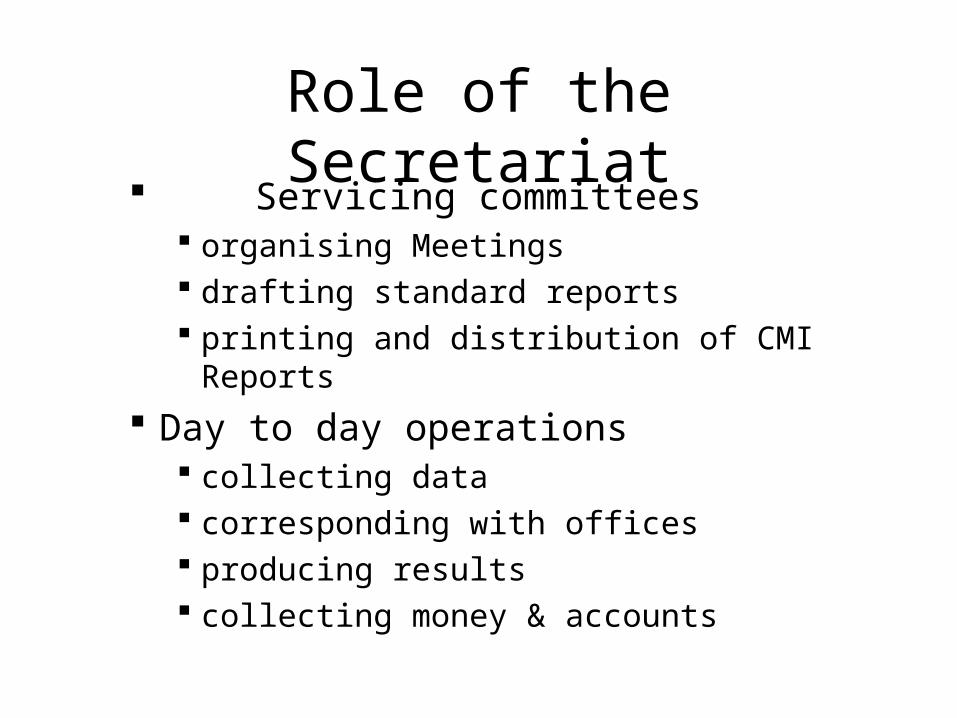

Role of the Secretariat Servicing committees

organising Meetings drafting standard reports printing and distribution of CMI Reports

Day to day operations collecting data corresponding with offices producing results collecting money & accounts

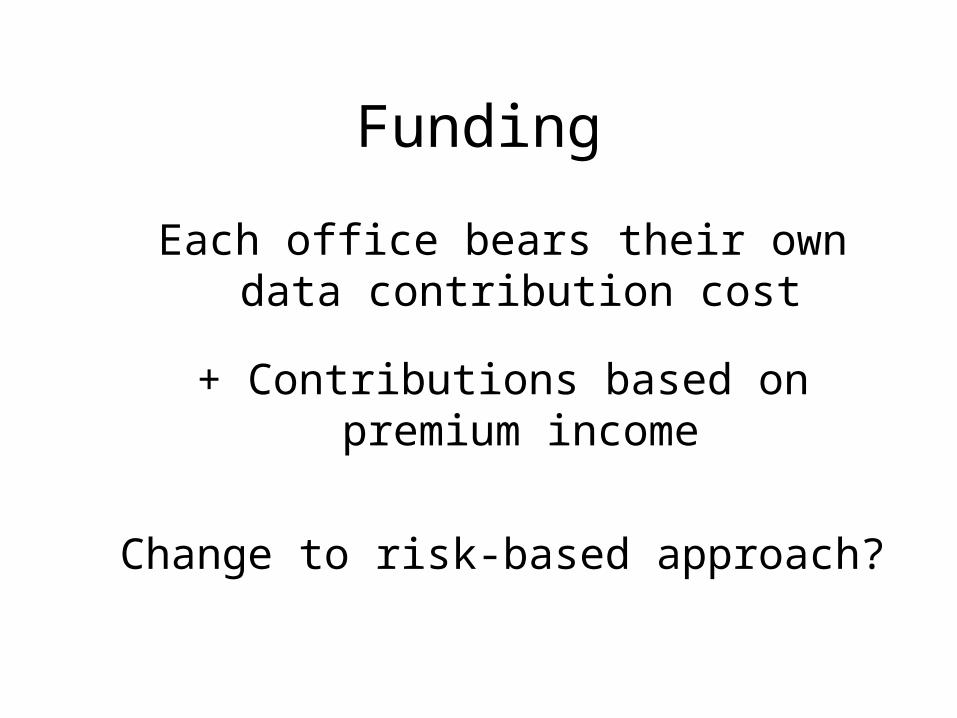

Funding

Each office bears their own data contribution cost

+ Contributions based on premium income

Change to risk-based approach?

Investigations

• Mortality– life contracts issued at standard rates– impaired lives– annuitants– individual pension arrangements– group pension arrangements

Investigations

• Income Protection– individual policies– group policies

• Critical Illness

Data Timetable

• Collect data as at each 31 December

• Wait until 30 June

• July October: collect and process data

• Nov Dec: final chasing & checking

• December: run & distribute “all office” results

Reporting results

Own Office Results– As soon as data is clean– Data summary– A/E comparison with standard tables– Special requests

Confidentiality

• taken extremely seriously

• only Secretariat & office sees results

• office numbers

• can be restrictive

Reporting results

All Office pooled results– annual– quadrennial– available to members first– interim results– available to all member offices

Reporting results

To the Actuarial Profession– CMI Reports (CMIRs)– the profession’s magazine & internet site– conferences– sessional meetings

Data Collection Methodologies

Main methods

• What are we doing?– What are we measuring?– Definitions

• Census

• Policy data

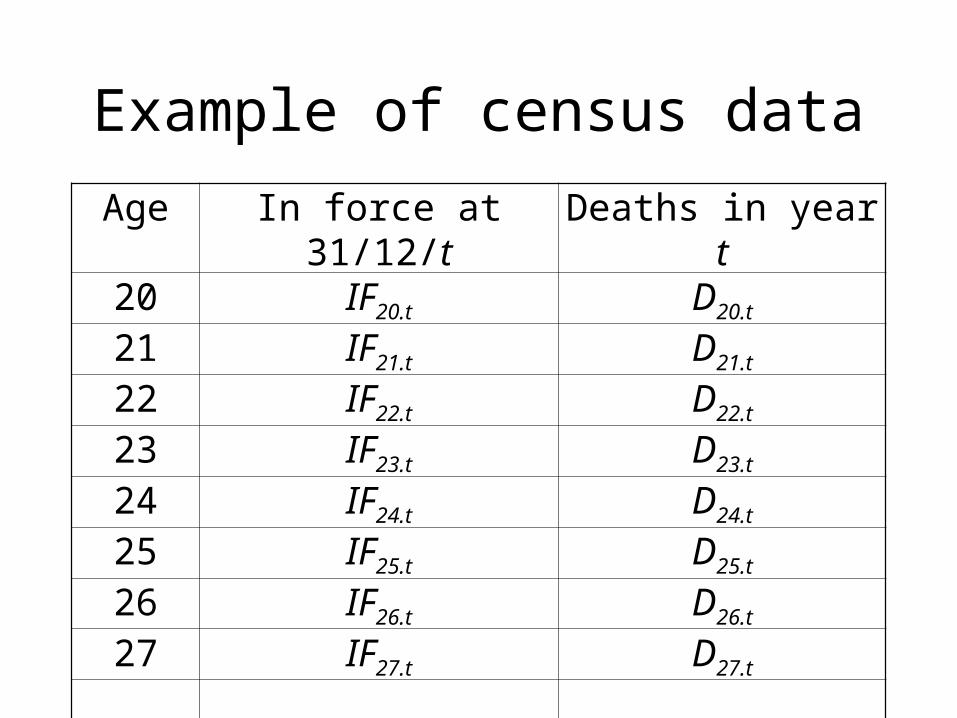

Example of census data

Age In force at 31/12/t Deaths in year t20 IF20.t D20.t

21 IF21.t D21.t

22 IF22.t D22.t

23 IF23.t D23.t

24 IF24.t D24.t

25 IF25.t D25.t

26 IF26.t D26.t

27 IF27.t D27.t

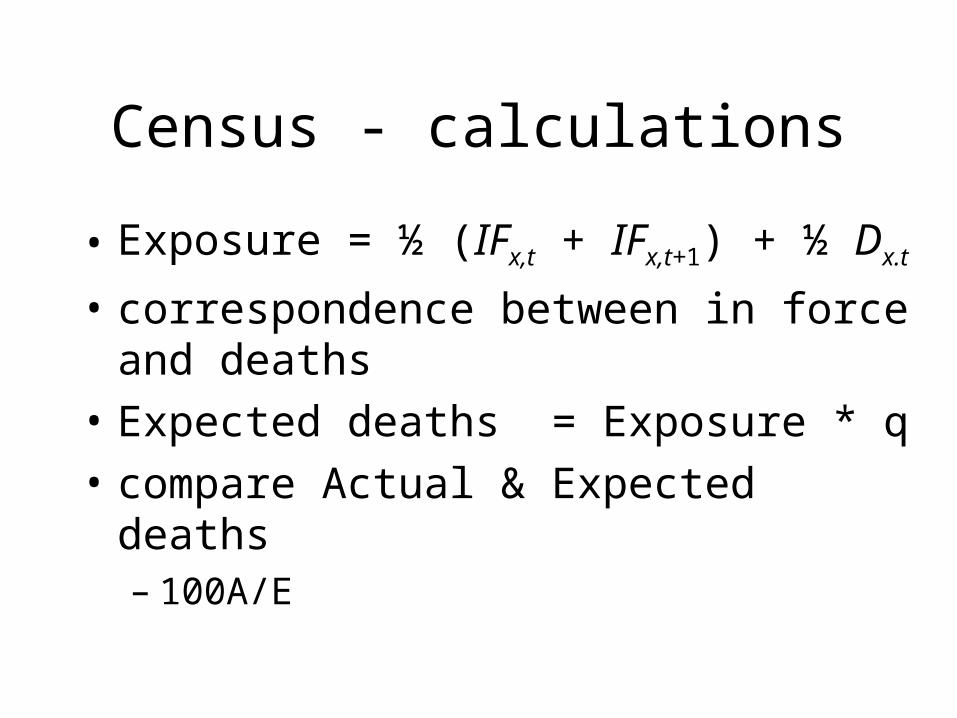

Census - calculations

• Exposure = ½ (IFx,t + IFx,t+1) + ½ Dx.t

• correspondence between in force and deaths

• Expected deaths = Exposure * q

• compare Actual & Expected deaths– 100A/E

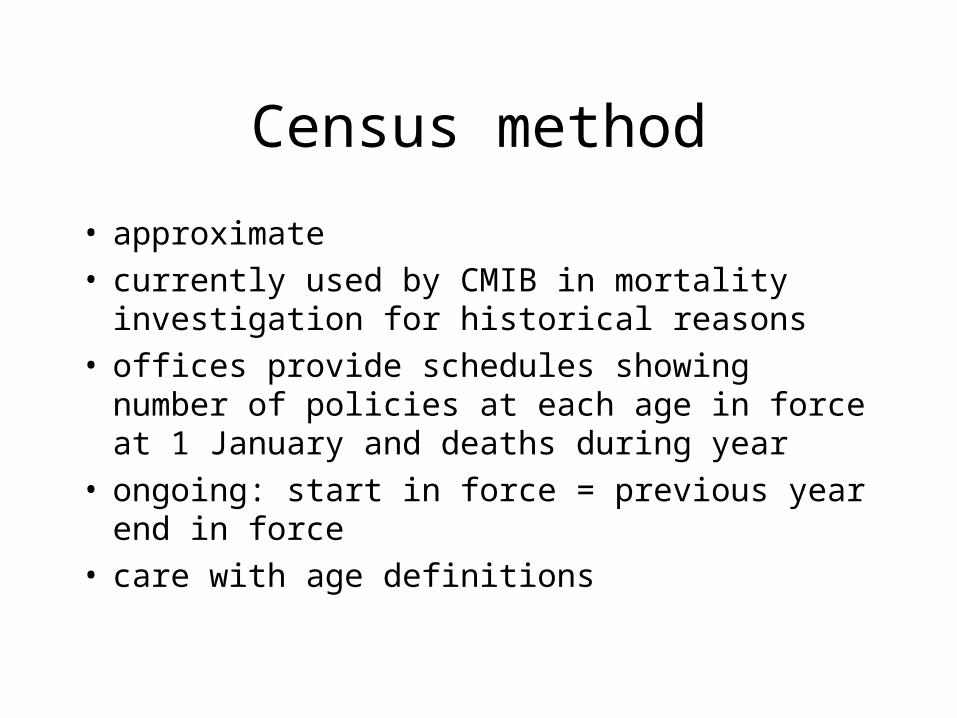

Census method

• approximate• currently used by CMIB in mortality investigation

for historical reasons• offices provide schedules showing number of

policies at each age in force at 1 January and deaths during year

• ongoing: start in force = previous year end in force• care with age definitions

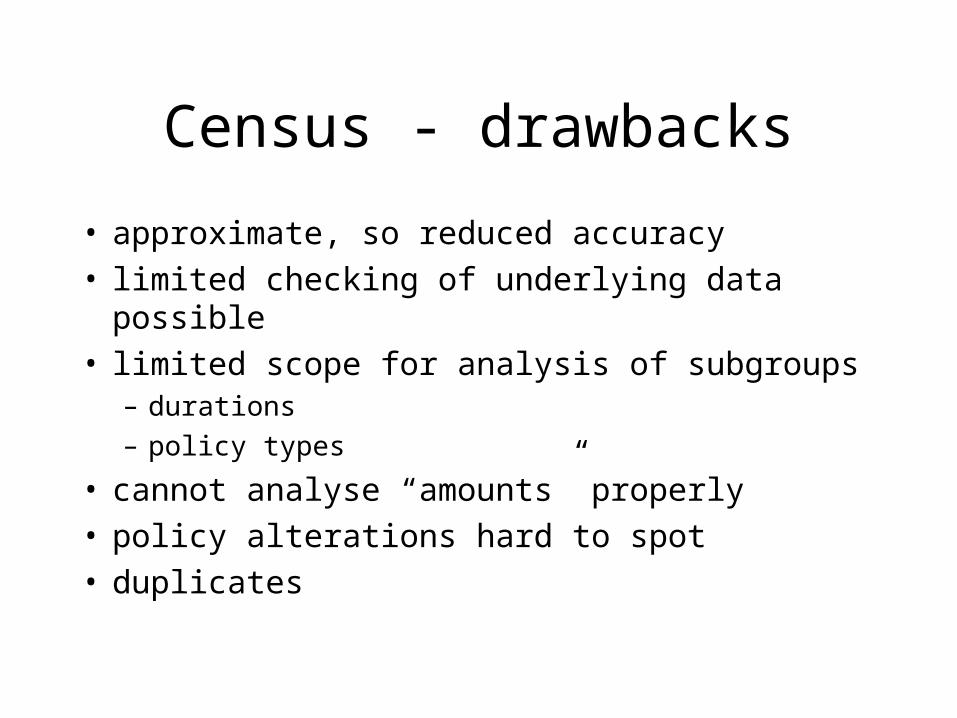

Census - drawbacks

• approximate, so reduced accuracy• limited checking of underlying data possible• limited scope for analysis of subgroups

– durations

– policy types

• cannot analyse “amounts” properly• policy alterations hard to spot• duplicates

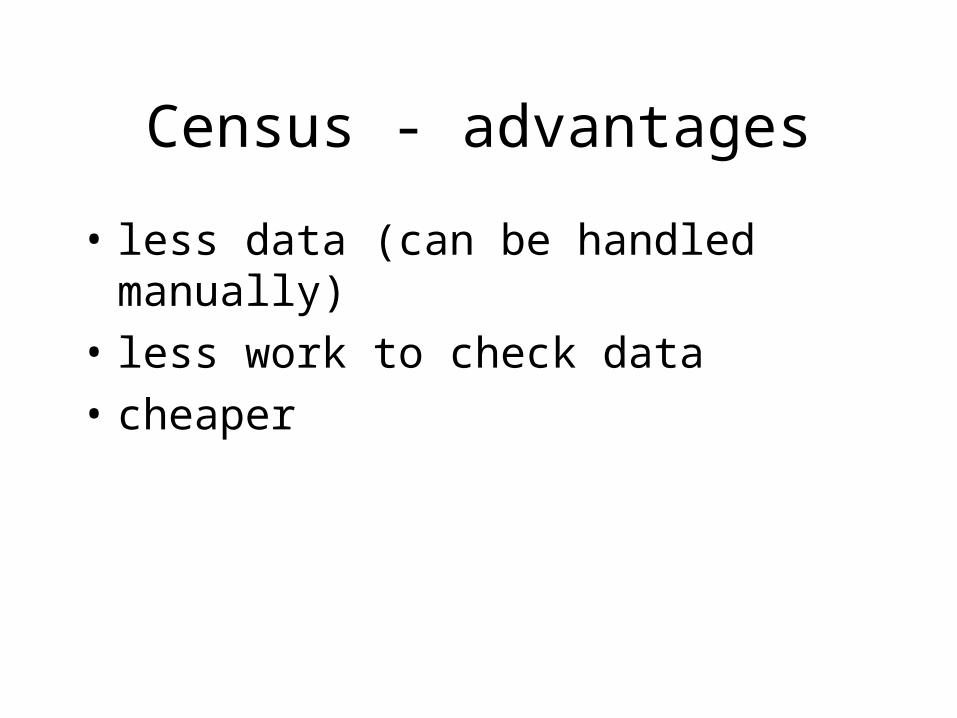

Census - advantages

• less data (can be handled manually)

• less work to check data

• cheaper

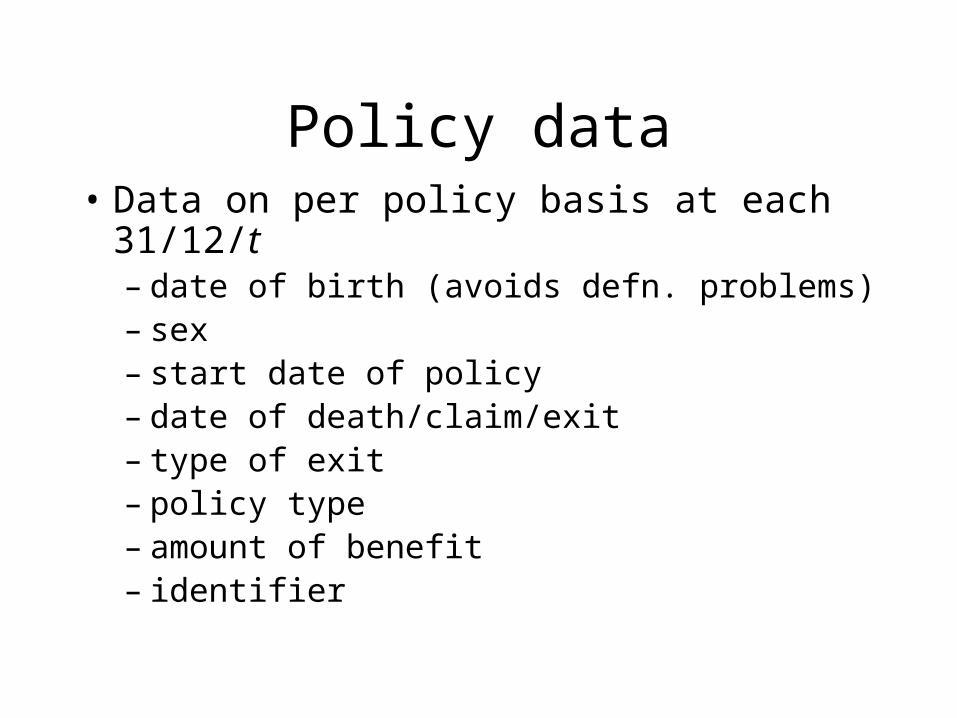

Policy data• Data on per policy basis at each 31/12/t

– date of birth (avoids defn. problems)– sex– start date of policy– date of death/claim/exit– type of exit– policy type– amount of benefit– identifier

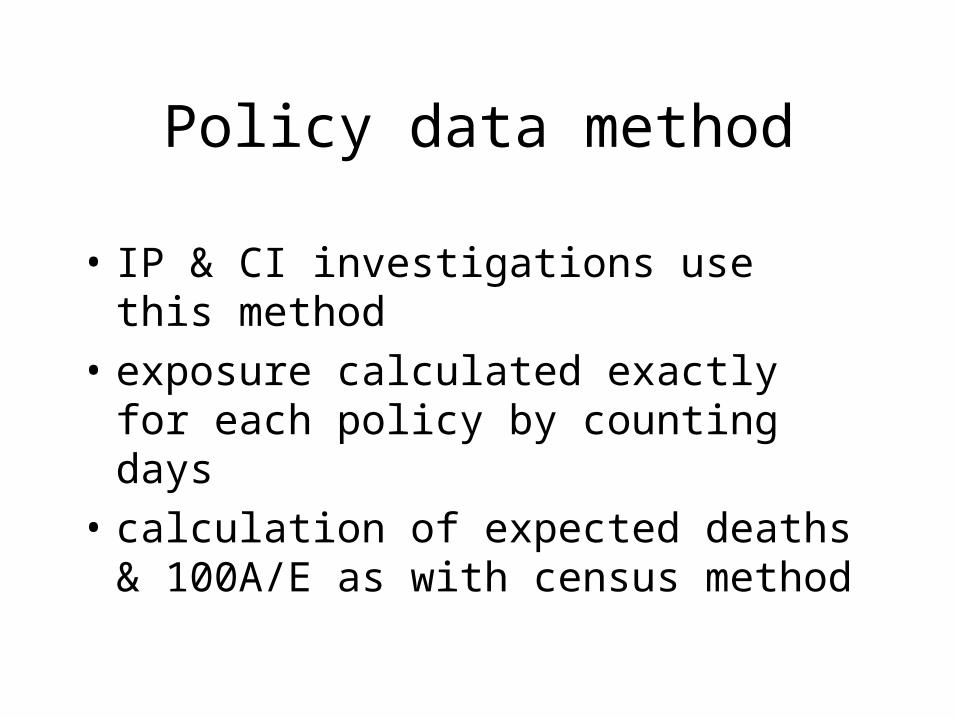

Policy data method

• IP & CI investigations use this method

• exposure calculated exactly for each policy by counting days

• calculation of expected deaths & 100A/E as with census method

Policy data – features

• advantages over census method– greater accuracy

– more checking possible better data quality

– more control over data included in investigations

– more detailed analyses possible

• should be easier for offices to supply

But• increased storage requirements• more complex to process - hence expensive

Observations (1)

• need for detailed rules

• consistent interpretation across offices

• must check to make sure data is sensible

• will have delays in data collection

• offices “come and go”

• office mergers

Observations (2)

• staff who produce data are not the same as staff who use the results

• sometimes difficult to get offices to pay attention

• speedy turn around helps data quality

• data audits

Common data problems

• policy alterations (e.g. amounts)

• duplicates

• What is a claim? (claim date in IP)

• multiple claims (IP)

• matching data across periods

• consistency - over time - between offices

Sub-population differences

Questions to be investigated

• Do differences justify a standard table?

• if not, how to adjust current table?– pricing– valuation

• trends in sub population

Categories investigatedMain categories• age• male / female• policy type• duration• smoker / non-smoker• impairmentOther possible ( but only have insurance data)• regional variation• social variation

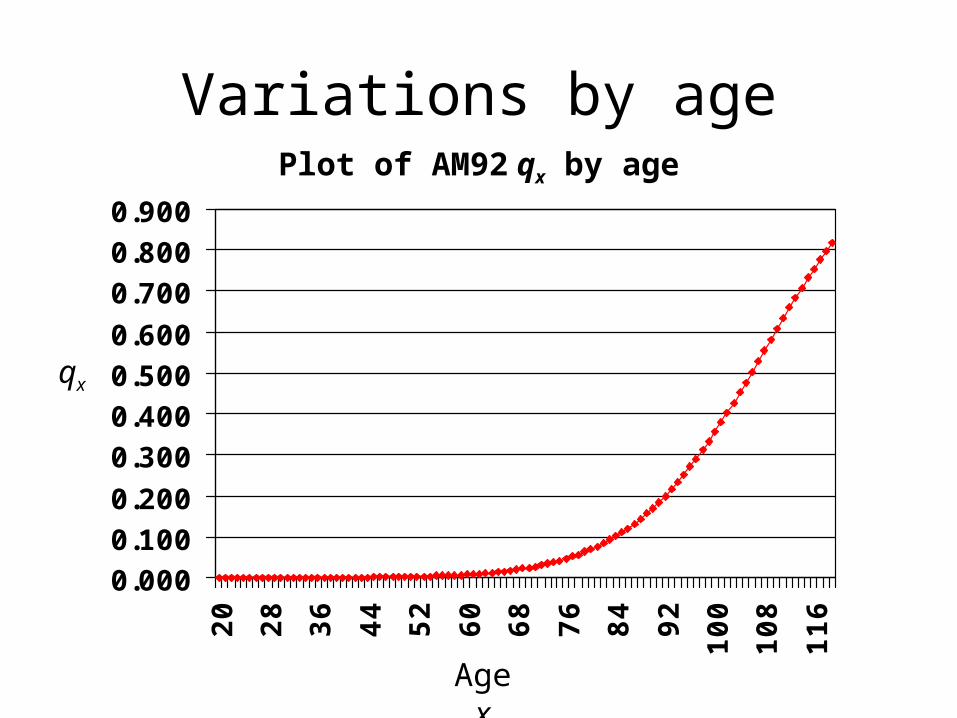

Variations by age

0.0000.1000.200

0.3000.4000.5000.600

0.7000.8000.900

20

28

36

44

52

60

68

76

84

92

100

108

116

Plot of AM92 qx by age

qx

Age x

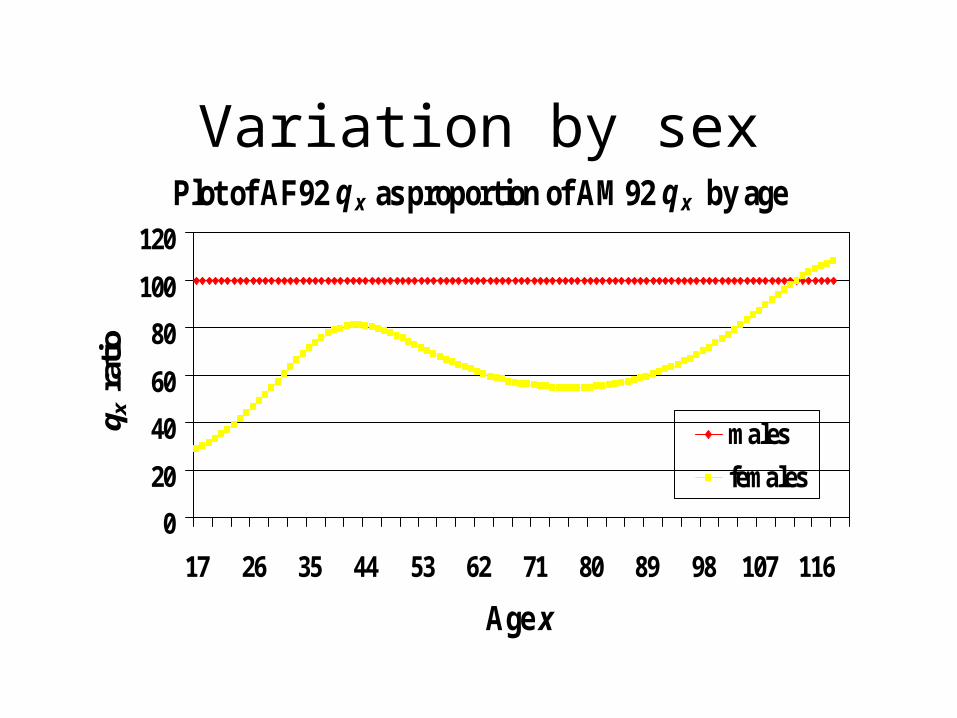

Variation by sexPlot of AF92 q x as proportion of AM92 q x by age

0

20

40

60

80

100

120

17 26 35 44 53 62 71 80 89 98 107 116

Age x

q x r

atio

males

females

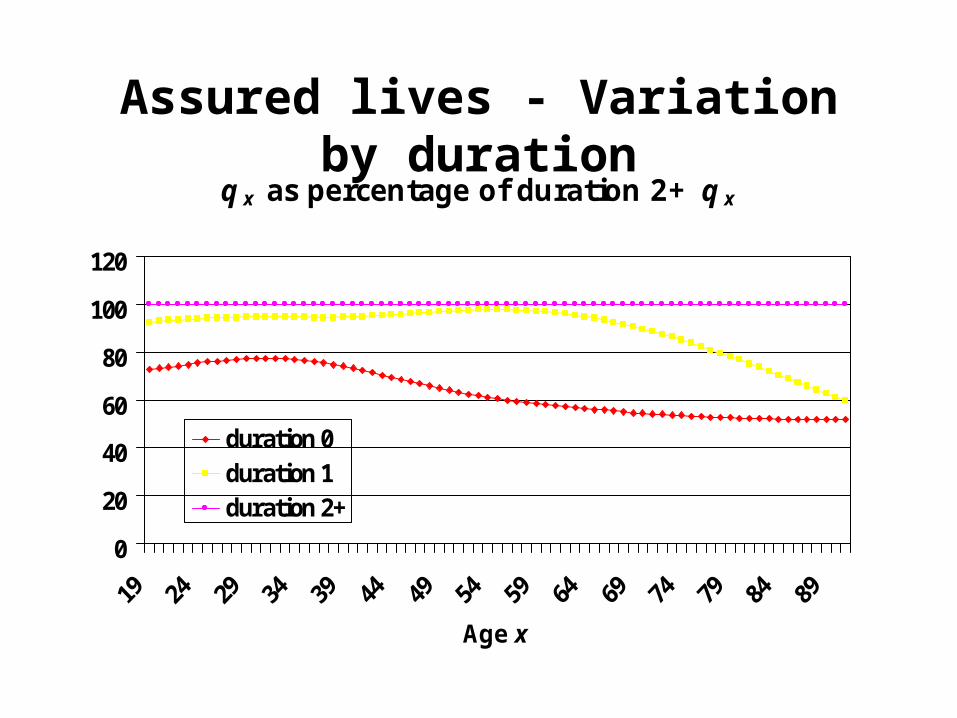

Assured lives - Variation by durationqx as percentage of duration 2+ qx

0

20

40

60

80

100

120

Age x

duration 0duration 1duration 2+

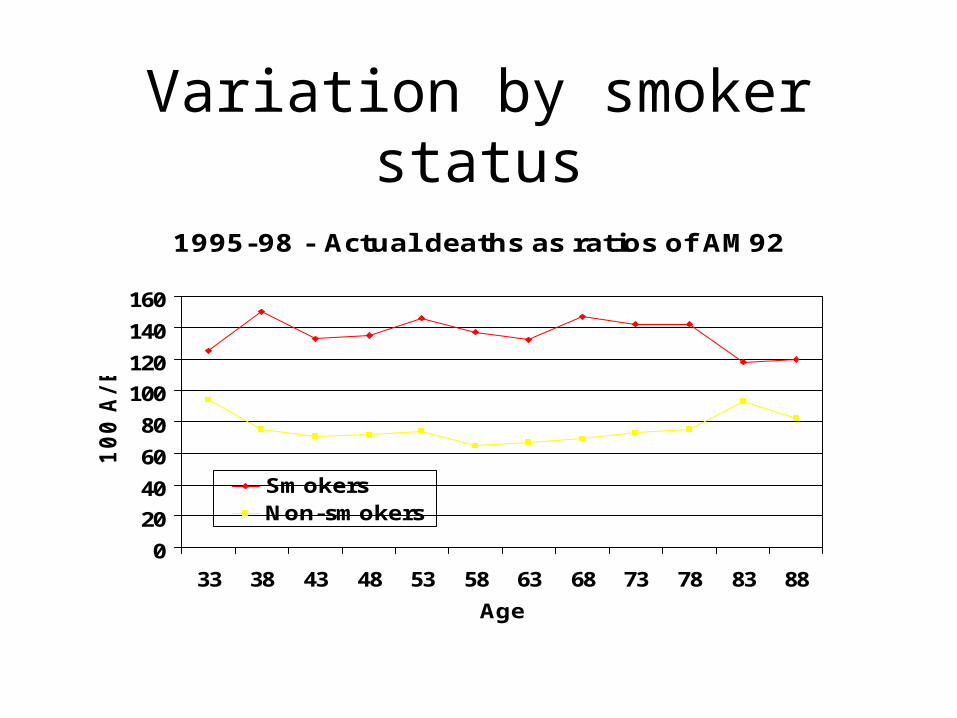

Variation by smoker status

1995-98 - Actual deaths as ratios of AM92

0

20

40

60

80

100

120

140

160

33 38 43 48 53 58 63 68 73 78 83 88

Age

100 A

/E

SmokersNon-smokers

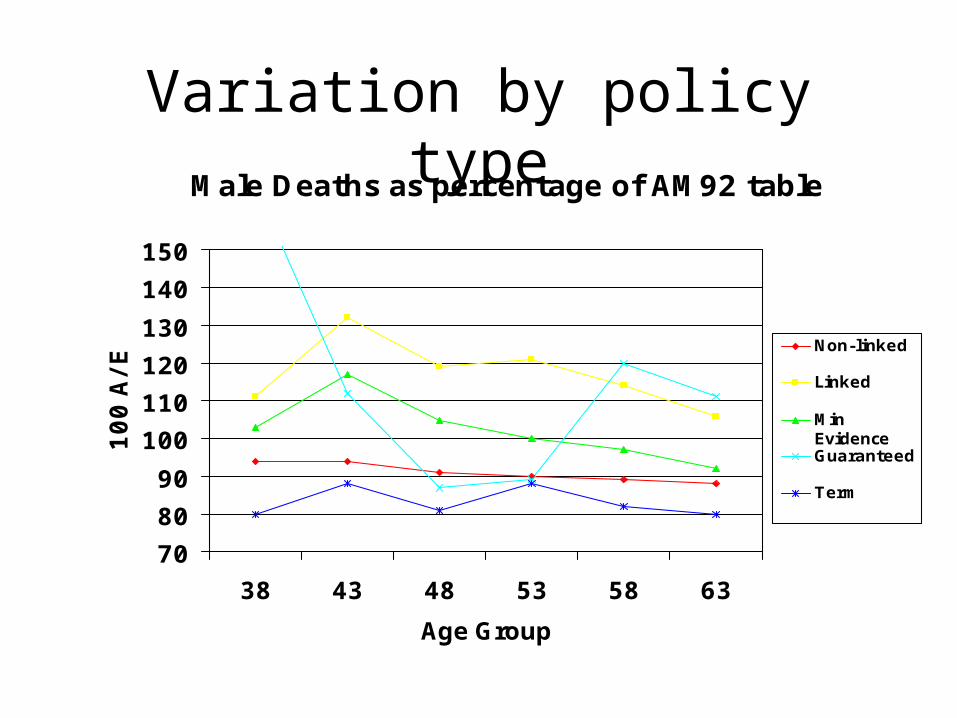

Variation by policy typeMale Deaths as percentage of AM92 table

70

80

90

100

110

120

130

140

150

38 43 48 53 58 63

Age Group

100 A

/E Non-linked

Linked

MinEvidenceGuaranteed

Term

Sub-population comments

• must collect data!

• data collection follows market

• companies that innovate via sub-population differences are exposed

• getting credible data sometimes difficult

• takes time for investigations to get established