the comscore 2010 europe digital year in review comscore 2010 europe digital year in review february...

TRANSCRIPT

The comScore 2010 Europe Digital Year in Review February 2011

2

TThhee 22001100 EEuurrooppee DDiiggiittaall YYeeaarr iinn RReevviieeww

The European Digital Landscape continues to evolve, with 2010 proving to be yet another exciting

year of change. The rise of social networking, availability of video content and growing mobile media

consumption is changing the marketer’s toolkit and creating new and unique opportunities to engage

with the European consumer.

In order to understand this opportunity more clearly we are pleased to launch our analysis of digital

trends for the European market. This report follows our Digital Year in Review for the US market,

http://www.comscore.com/Press_Events/Presentations_Whitepapers/2011/2010_US_Digital_Year_in_Review

and our Mobile Year in Review for US, EU5 (UK, France, Germany, Italy and Spain) and Japan.

http://www.comscore.com/Press_Events/Presentations_Whitepapers/2011/2010_Mobile_Year_in_Review

The many issues that will be addressed in this report include:

How does the European digital consumer compare to the rest of the world?

What European markets have the highest engagement online and how does that compare

across age groups?

Which site content categories are growing in popularity?

What trends are we seeing in the social networking space and what impact does that have on

email and instant messaging activity?

How has the consumption of online TV content changed over time?

What European smartphone operating system is growing the fastest?

Which search providers are starting to make headway against Google in Europe?

The comScore 2010 European Digital Year in Review offers a comprehensive overview of the

digital landscape in Europe. This report will examine the trends in European internet usage, social

networking trends, online video consumption, mobile and search, and includes individual scorecards

highlighting demographic data and top 20 sites for Austria, Belgium, Denmark, Finland, France,

Germany, Ireland, Italy, Netherlands, Norway, Poland, Portugal, Russia, Spain, Sweden, Switzerland,

Turkey and the United Kingdom.

The comScore 2010 Europe Digital Year in Review February 2011

3

TTaabbllee ooff CCoonntteennttss:: 22001100 EEuurrooppee DDiiggiittaall YYeeaarr iinn RReevviieeww

Europe Overview .................................................................................................................................. 4

Includes: Individual Market Penetration and Engagement, Demographic Comparison

Top Web Properties and Category Trends 2010 ............................................................................... 5

Includes: Top Properties and Categories, Trends in Instant Messaging, Email and Portals

Social Networking Trends 2010 .......................................................................................................... 7

Includes: Top Social Network Trends, Facebook Statistics, Demographic Analysis

Online Advertising Trends 2010 ....................................................................................................... 12

Includes: Ad Impressions, Advertising Exposed Reach, Top Publisher Categories

Category Spotlight: Couponing ........................................................................................................ 14

Includes: Region and Market Comparisons, Impact of Groupon

TV and Video Trends 2010 ................................................................................................................. 16

Includes: TV Category Viewing, Time Spent Watching Videos, Average Video Length,

Demographics of the Typical Video Consumer

European Mobile Market 2010 .......................................................................................................... 20

Includes: Smartphone Penetration, Comparison of Smartphone Operating Systems, Market

Enablers

European Search Market 2010 .......................................................................................................... 22

Includes: Market Comparisons, Top and Emerging Search Providers

Looking Ahead to 2011 ...................................................................................................................... 24

European Market Scorecards ........................................................................................................... 26

Includes: Demographics, Engagement, Top 20 sites for Austria, Belgium, Denmark, Finland,

France, Germany, Ireland, Italy, Netherlands, Norway, Poland, Portugal, Russia, Spain, Sweden,

Switzerland, Turkey and United Kingdom.

About comScore and Our Methodology ........................................................................................... 35

The comScore 2010 Europe Digital Year in Review February 2011

4

EEuurrooppee OOvveerrvviieeww

The Netherlands and UK Lead in Engagement

Europeans spend the equivalent of one day a month online (24:20 hours) with the Netherlands (31:39

hours) and United Kingdom (30:38 hours) far exceeding this trend. Consumers in Italy (16:02 hours)

and Austria (13:11 hours), however, spend nearly half as much time online as users in Holland and

the UK. Austria’s low engagement is not surprising as it has the lowest penetration of Social

Networking sites among all countries in Europe.

European Demographics Skew Older than Emerging Markets

Relative to the emerging markets of Asia Pacific and Latin America, Europe’s typical digital user is

markedly older, with more than half above the age of 35. Of the more than 360 million online

consumers in Europe, females represent a slightly larger percentage (48 percent) as compared to the

worldwide average (46 percent). A comparison of individual market demographics can be found later

in this report in the European Market Scorecard section.

28%

32%

24%

23%

32%

25%

25%

23%

23%

30%

26%

25%

28%

27%

19%

22%

18%

25%

28%

19%

World-Wide

Asia Pacific

Europe

North America

Latin America

Distribution of Internet Users, Age 15+Source: comScore Media Metrix, December2010

M 15-34 F 15-34 M 35+ F 35+

UV (MM)

1,323.5

111.4

534.0

361.7

204.0

0:00

4:48

9:36

14:24

19:12

24:00

28:48

33:36

0

10,000

20,000

30,000

40,000

50,000

60,000

Ave

rage H

ou

rs pe

r Visito

r (hh

:mm

)U

niq

ue

Vis

ito

rs (

00

0)

Unique Visitors (000) and Average Time Online in EuropeSource: comScore Media Metrix, Dec-2010

Total Unique Visitors (000) Average Hours per Visitor

The comScore 2010 Europe Digital Year in Review February 2011

5

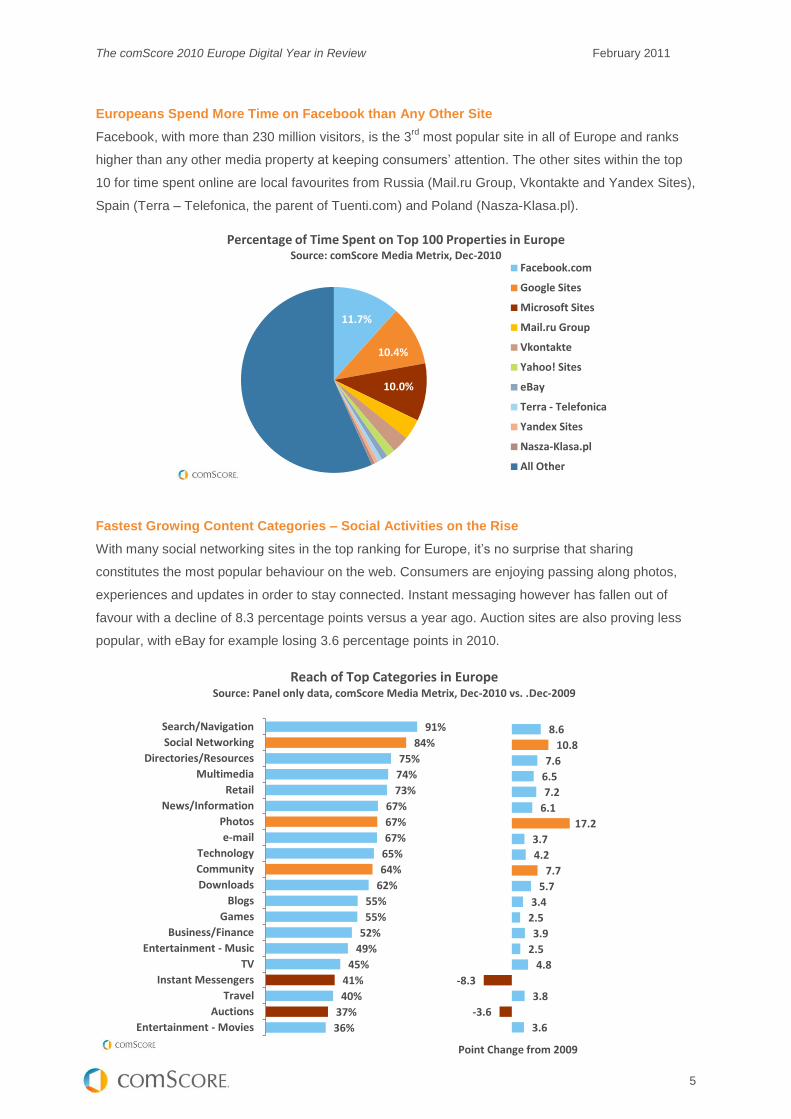

Europeans Spend More Time on Facebook than Any Other Site

Facebook, with more than 230 million visitors, is the 3rd

most popular site in all of Europe and ranks

higher than any other media property at keeping consumers’ attention. The other sites within the top

10 for time spent online are local favourites from Russia (Mail.ru Group, Vkontakte and Yandex Sites),

Spain (Terra – Telefonica, the parent of Tuenti.com) and Poland (Nasza-Klasa.pl).

Fastest Growing Content Categories – Social Activities on the Rise

With many social networking sites in the top ranking for Europe, it’s no surprise that sharing

constitutes the most popular behaviour on the web. Consumers are enjoying passing along photos,

experiences and updates in order to stay connected. Instant messaging however has fallen out of

favour with a decline of 8.3 percentage points versus a year ago. Auction sites are also proving less

popular, with eBay for example losing 3.6 percentage points in 2010.

11.7%

10.4%

10.0%

Percentage of Time Spent on Top 100 Properties in EuropeSource: comScore Media Metrix, Dec-2010

Facebook.com

Google Sites

Microsoft Sites

Mail.ru Group

Vkontakte

Yahoo! Sites

eBay

Terra - Telefonica

Yandex Sites

Nasza-Klasa.pl

All Other

Reach of Top Categories in Europe Source: Panel only data, comScore Media Metrix, Dec-2010 vs. .Dec-2009

91%

84%

75%

74%

73%

67%

67%

67%

65%

64%

62%

55%

55%

52%

49%

45%

41%

40%

37%

36%

Search/Navigation

Social Networking

Directories/Resources

Multimedia

Retail

News/Information

Photos

Technology

Community

Downloads

Blogs

Games

Business/Finance

Entertainment - Music

TV

Instant Messengers

Travel

Auctions

Entertainment - Movies

8.6

10.8

7.6

6.5

7.2

6.1

17.2

3.7

4.2

7.7

5.7

3.4

2.5

3.9

2.5

4.8

-8.3

3.8

-3.6

3.6

Point Change from 2009

The comScore 2010 Europe Digital Year in Review February 2011

6

Instant Messaging Experiences Rapid Declines

Instant Messengers were once one of the most popular pastimes online but times have changed with

consumers spending 39 percent less time using IM. In their place, Social Networking sites have

eclipsed most other activities and are a magnet for consumers to while away their day with 34 percent

more time spent social networking versus last year. Contrary to the US market, web-based email has

remained a small but stable activity throughout 2010.

Email Still Popular Among the Older Generation

A further analysis of the trends for web email, Instant Messengers, Portals and Social Networking

sites show that there are slight differences between age groups. The younger generation aged 15-34

are increasingly shifting their online activity to social networking (+32 percent) whereas the older

population, above the age of 35, are experimenting with social networking but also embracing the

comfort of traditional email (+6 percent).

0%

5%

10%

15%

20%

25%

Percent (%) Share of Time Spent Online in Europe Source: Panel only data, comScore Media Metrix, Dec-2009 to Dec-2010

Social Networking Portals

Instant Messengers e-mail

-11%

6%

-38%-42%

-28%

-18%

32%38%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

Year-over-Year Change in Time Spent Online in Europe Source: comScore Media Metrix, Dec-2010 vs .Dec-2009

Email Instant Messengers Portals Social Networking

Ages 15-34 Ages 35+

The comScore 2010 Europe Digital Year in Review February 2011

7

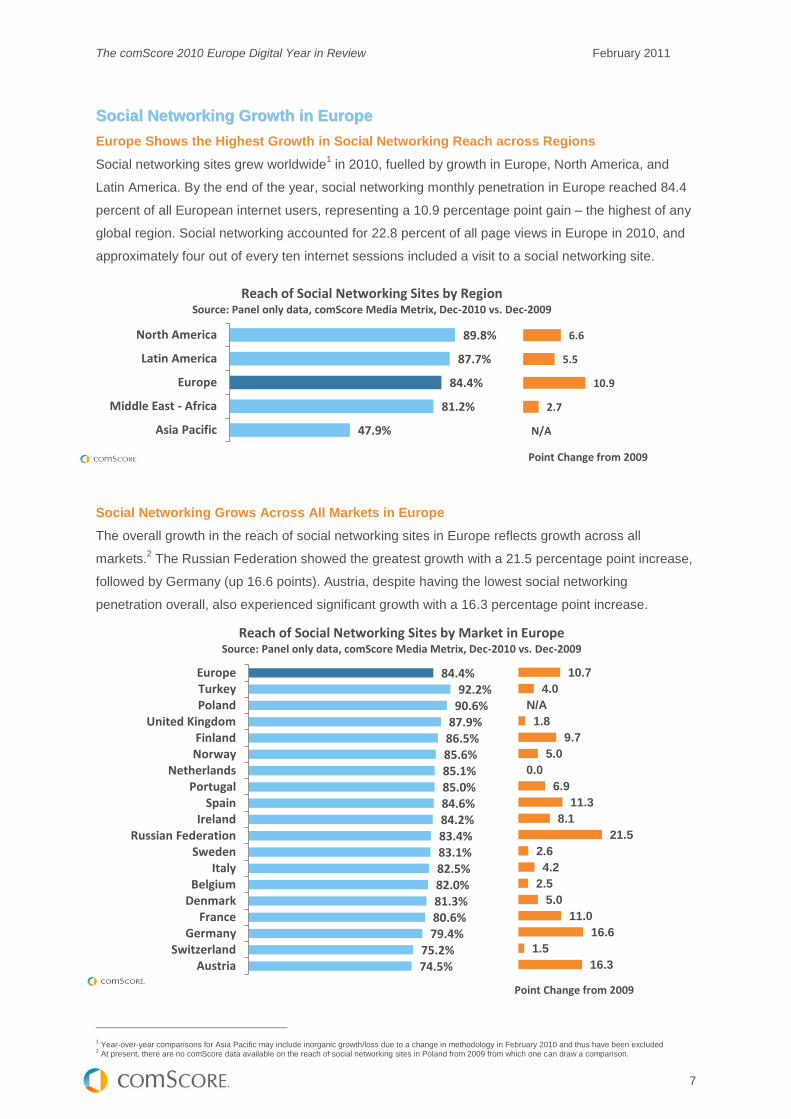

SSoocciiaall NNeettwwoorrkkiinngg GGrroowwtthh iinn EEuurrooppee

Europe Shows the Highest Growth in Social Networking Reach across Regions

Social networking sites grew worldwide1 in 2010, fuelled by growth in Europe, North America, and

Latin America. By the end of the year, social networking monthly penetration in Europe reached 84.4

percent of all European internet users, representing a 10.9 percentage point gain – the highest of any

global region. Social networking accounted for 22.8 percent of all page views in Europe in 2010, and

approximately four out of every ten internet sessions included a visit to a social networking site.

Social Networking Grows Across All Markets in Europe

The overall growth in the reach of social networking sites in Europe reflects growth across all

markets.2 The Russian Federation showed the greatest growth with a 21.5 percentage point increase,

followed by Germany (up 16.6 points). Austria, despite having the lowest social networking

penetration overall, also experienced significant growth with a 16.3 percentage point increase.

1 Year-over-year comparisons for Asia Pacific may include inorganic growth/loss due to a change in methodology in February 2010 and thus have been excluded

2 At present, there are no comScore data available on the reach of social networking sites in Poland from 2009 from which one can draw a comparison.

Reach of Social Networking Sites by Market in Europe

Source: Panel only data, comScore Media Metrix, Dec-2010 vs. Dec-2009

47.9%

81.2%

84.4%

87.7%

89.8%

Asia Pacific

Middle East - Africa

Europe

Latin America

North America

Reach of Social Networking Sites by RegionSource: Panel only data, comScore Media Metrix, Dec-2010 vs. Dec-2009

N/A

2.7

10.9

5.5

6.6

Point Change from 2009

84.4%92.2%

90.6%87.9%

86.5%85.6%85.1%85.0%84.6%84.2%83.4%83.1%82.5%82.0%81.3%80.6%79.4%

75.2%74.5%

EuropeTurkeyPoland

United KingdomFinlandNorway

NetherlandsPortugal

SpainIreland

Russian FederationSweden

ItalyBelgium

DenmarkFrance

GermanySwitzerland

Austria

10.7

4.0

N/A

1.8

9.7

5.0

0.0

6.9

11.3

8.1

21.5

2.6

4.2

2.5

5.0

11.0

16.6

1.5

16.3

Point Change from 2009

The comScore 2010 Europe Digital Year in Review February 2011

8

Demographic Profile of Social Networking Users in Europe

A demographic analysis of social networking users in Europe reveals women leading in terms of

engagement. In December 2010, women spent 24.3 percent of their online time on social networking

sites, up 5.6 percentage points from a year earlier. By contrast, men spent only 16.8 percent of their

time on these sites, showing only a 3.1 percentage-point increase from 2009. These figures are well

above the worldwide average, which shows women across the globe spending18.3 percent of their

online time on social networking sites. Compared to Europe, women worldwide spent less than a fifth

of their time online on social networking, and men spent even less, with only 13.1 percent of their time

on social networks.

The profile of social networking users in Europe also reveals an audience that generally skews

younger, with 15-24 year olds representing 25.3 percent of users, followed closely by 25-34 year olds

at 24.3 percent. While the breakdown of European visitors to Facebook and Twitter mirrors that of

social networking site users in general, LinkedIn has an older age profile. Only 10.4 percent of its

visitors are under 25 years old, while half of the site’s audience is between the ages of 35-54. This

older age profile is understandable given the site’s orientation toward professional networking.

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

Percentage of Time Spent on Social Networking Sites by Gender in EuropeSource: comScore Media Metrix, Dec-2009 to Dec-2010

Females Males

+5.6

+3.1

25.3% 27.1% 28.1%10.4%

24.3% 24.6% 22.5%

25.2%

20.9% 20.4% 19.9%

27.9%

16.4% 15.6% 15.9%20.9%

13.1% 12.4% 13.5% 15.6%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

All Social Networking Facebook Twitter LinkedIn

% o

f M

arke

t

Demographic Profile: Share of European Visitors to Facebook, Twitter, and LinkedIn Source: comScore Media Metrix, Dec-2010

Persons: 15-24 Persons: 25-34 Persons: 35-44 Persons: 45-54 Persons: 55+

The comScore 2010 Europe Digital Year in Review February 2011

9

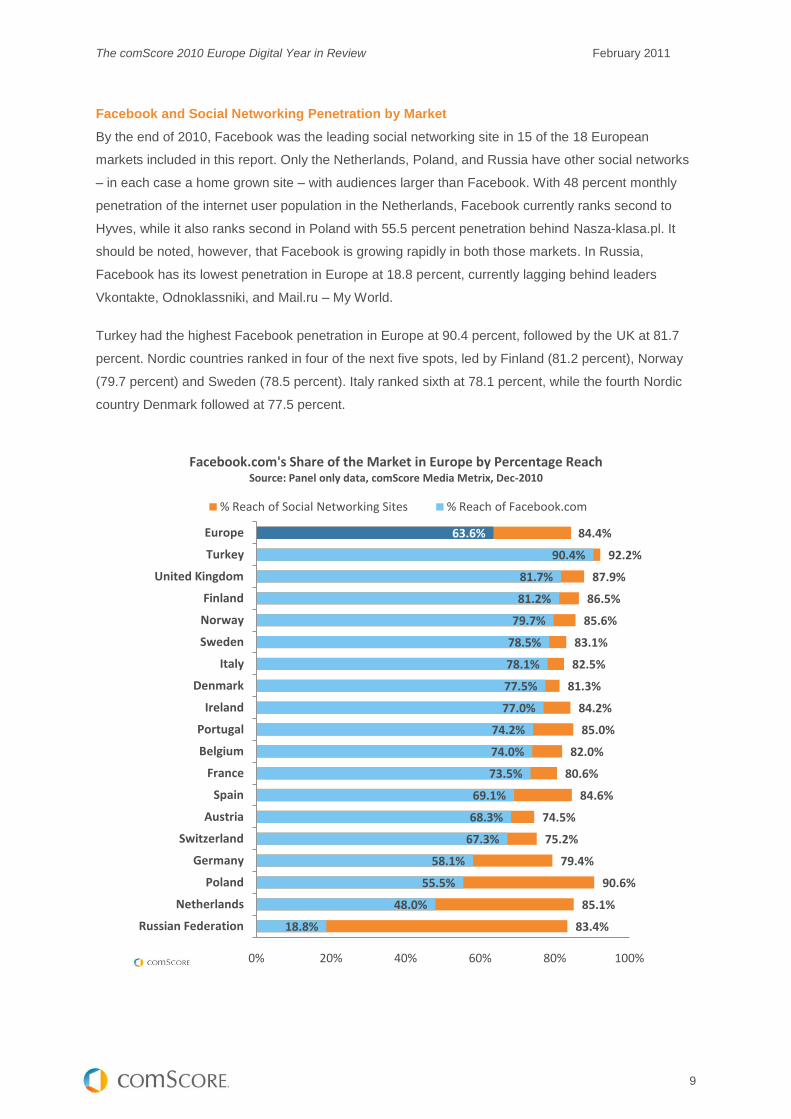

Facebook and Social Networking Penetration by Market

By the end of 2010, Facebook was the leading social networking site in 15 of the 18 European

markets included in this report. Only the Netherlands, Poland, and Russia have other social networks

– in each case a home grown site – with audiences larger than Facebook. With 48 percent monthly

penetration of the internet user population in the Netherlands, Facebook currently ranks second to

Hyves, while it also ranks second in Poland with 55.5 percent penetration behind Nasza-klasa.pl. It

should be noted, however, that Facebook is growing rapidly in both those markets. In Russia,

Facebook has its lowest penetration in Europe at 18.8 percent, currently lagging behind leaders

Vkontakte, Odnoklassniki, and Mail.ru – My World.

Turkey had the highest Facebook penetration in Europe at 90.4 percent, followed by the UK at 81.7

percent. Nordic countries ranked in four of the next five spots, led by Finland (81.2 percent), Norway

(79.7 percent) and Sweden (78.5 percent). Italy ranked sixth at 78.1 percent, while the fourth Nordic

country Denmark followed at 77.5 percent.

84.4%

92.2%

87.9%

86.5%

85.6%

83.1%

82.5%

81.3%

84.2%

85.0%

82.0%

80.6%

84.6%

74.5%

75.2%

79.4%

90.6%

85.1%

83.4%

63.6%

90.4%

81.7%

81.2%

79.7%

78.5%

78.1%

77.5%

77.0%

74.2%

74.0%

73.5%

69.1%

68.3%

67.3%

58.1%

55.5%

48.0%

18.8%

0% 20% 40% 60% 80% 100%

Europe

Turkey

United Kingdom

Finland

Norway

Sweden

Italy

Denmark

Ireland

Portugal

Belgium

France

Spain

Austria

Switzerland

Germany

Poland

Netherlands

Russian Federation

Facebook.com's Share of the Market in Europe by Percentage ReachSource: Panel only data, comScore Media Metrix, Dec-2010

% Reach of Social Networking Sites % Reach of Facebook.com

The comScore 2010 Europe Digital Year in Review February 2011

10

Markets Showing Greatest Facebook Growth

Although Facebook is not currently the leading social network in the Netherlands, it experienced

significant growth in 2010 in that country and in several other European markets. In addition to the

Netherlands, Facebook achieved its most significant gains in Portugal (up 48.2 percentage points),

Germany (up 35.7 points), Austria (up 27.2 points) and Spain (up 18.5 points). In April 2010,

Facebook eclipsed the leading social networks in Portugal (Hi5) and Germany (StudiVZ/VZ-

Netzwerke) to assume the #1 position among social networking sites in both those markets. The

previous year, Facebook grabbed the #1 position in Spain (from Tuenti.com) and in Austria (from

Netlog.com).

0%

10%

20%

30%

40%

50%

60%

70%

80%

% o

fM

arke

t

Top Five European Markets for Facebook Growth by Increase in Percentage Reach

Source: comScore Media Metrix, Dec-2009 to Dec-2010

Portugal Spain Austria Germany Netherlands

+48.2+18.5+27.2+35.7+23.6

Point Change from 2009

0%

10%

20%

30%

40%

50%

60%

70%

80%

Dec-2009

Mar-2010

Jun-2010

Sep-2010

Dec-2010

% o

f M

arke

t

Facebook.com Hi5.com

Facebook's Growth in PortugalSource: comScore Media Metrix, Dec-2009 to Dec-2010

+48.2

Facebook overtakes Hi5 in Portugal

0%

10%

20%

30%

40%

50%

60%

70%

Dec-2009

Mar-2010

Jun-2010

Sep-2010

Dec-2010

% o

f M

arke

t

Facebook.com StudiVZ Sites

Facebook's Growth in GermanySource: comScore Media Metrix, Dec-2009 to Dec-2010

+35.7

Facebook overtakes StudiVZ in Germany

The comScore 2010 Europe Digital Year in Review February 2011

11

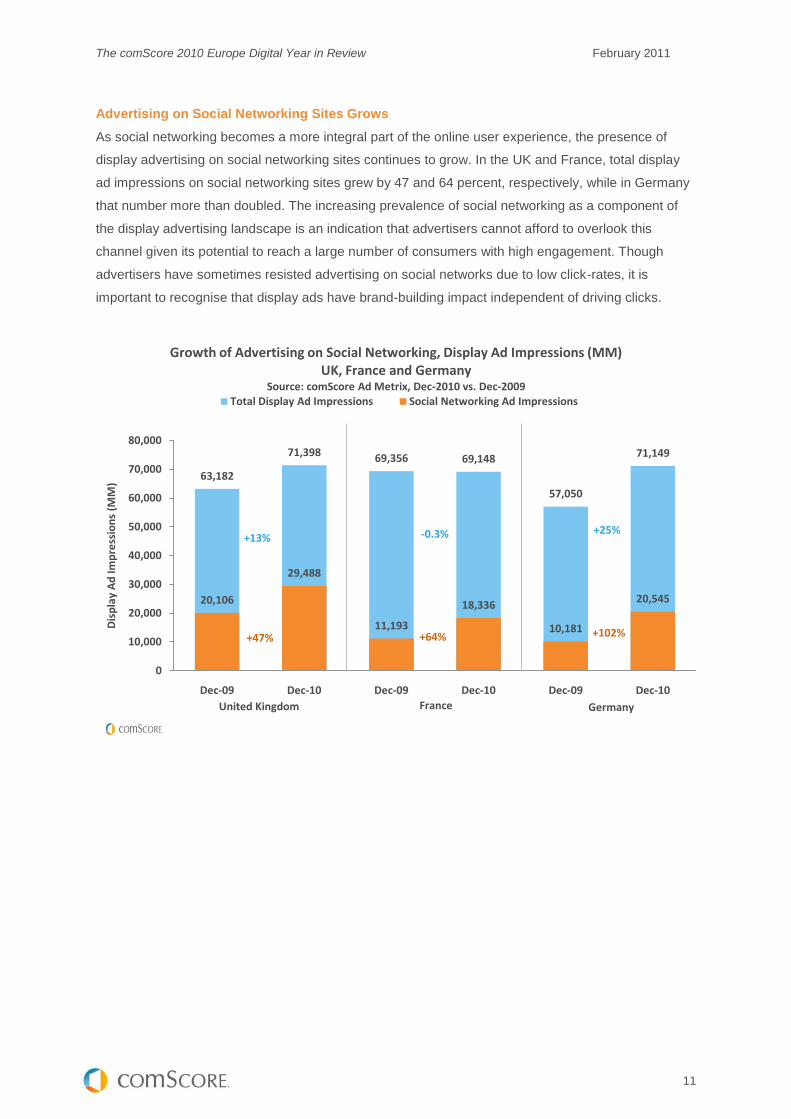

Advertising on Social Networking Sites Grows

As social networking becomes a more integral part of the online user experience, the presence of

display advertising on social networking sites continues to grow. In the UK and France, total display

ad impressions on social networking sites grew by 47 and 64 percent, respectively, while in Germany

that number more than doubled. The increasing prevalence of social networking as a component of

the display advertising landscape is an indication that advertisers cannot afford to overlook this

channel given its potential to reach a large number of consumers with high engagement. Though

advertisers have sometimes resisted advertising on social networks due to low click-rates, it is

important to recognise that display ads have brand-building impact independent of driving clicks.

63,182

71,398 69,356 69,148

57,050

71,149

20,106

29,488

11,193

18,336

10,181

20,545

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

Dec-09 Dec-10 Dec-09 Dec-10 Dec-09 Dec-10

Dis

pla

y A

d Im

pre

ssio

ns

(MM

)

Growth of Advertising on Social Networking, Display Ad Impressions (MM) UK, France and Germany

Source: comScore Ad Metrix, Dec-2010 vs. Dec-2009Total Display Ad Impressions Social Networking Ad Impressions

United Kingdom France Germany

+47% +64% +102%

+13% -0.3% +25%

The comScore 2010 Europe Digital Year in Review February 2011

12

OOnnlliinnee AAddvveerrttiissiinngg iinn EEuurrooppee

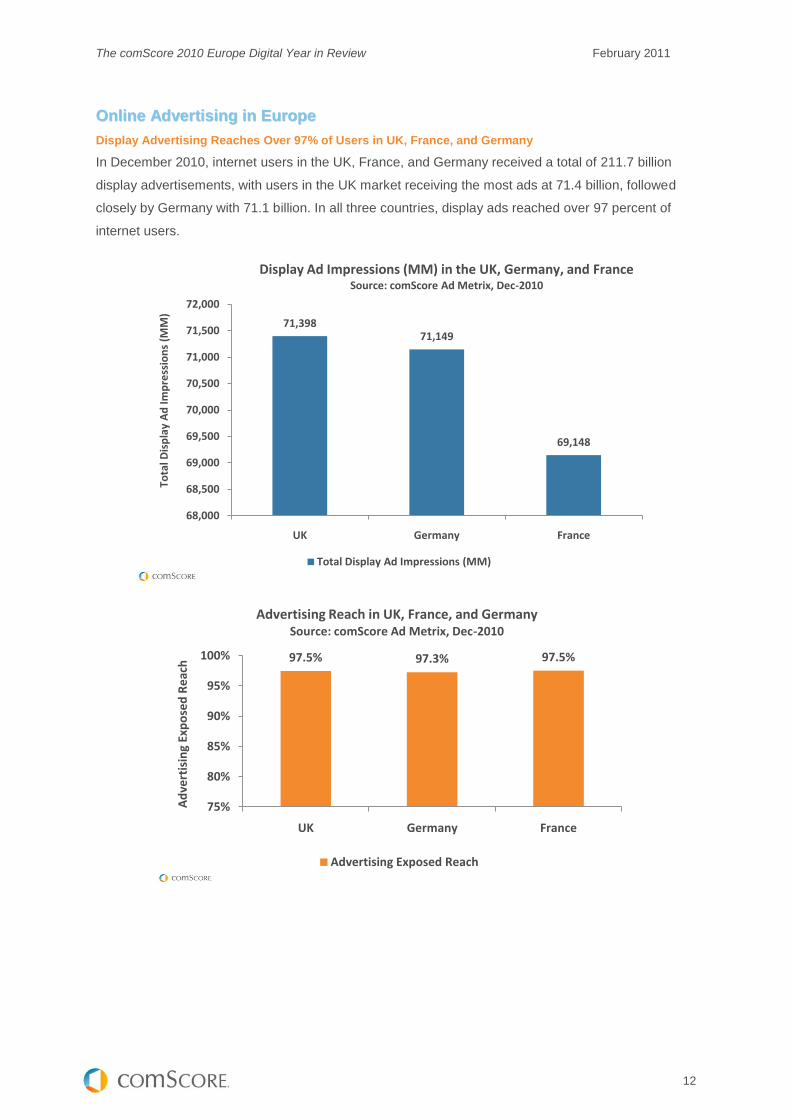

Display Advertising Reaches Over 97% of Users in UK, France, and Germany

In December 2010, internet users in the UK, France, and Germany received a total of 211.7 billion

display advertisements, with users in the UK market receiving the most ads at 71.4 billion, followed

closely by Germany with 71.1 billion. In all three countries, display ads reached over 97 percent of

internet users.

71,39871,149

69,148

68,000

68,500

69,000

69,500

70,000

70,500

71,000

71,500

72,000

UK Germany France

Tota

l Dis

pla

y A

d Im

pre

ssio

ns

(MM

)

Display Ad Impressions (MM) in the UK, Germany, and FranceSource: comScore Ad Metrix, Dec-2010

Total Display Ad Impressions (MM)

97.5% 97.3% 97.5%

75%

80%

85%

90%

95%

100%

UK Germany France

Ad

vert

isin

g Ex

po

sed

Re

ach

Advertising Reach in UK, France, and GermanySource: comScore Ad Metrix, Dec-2010

Advertising Exposed Reach

The comScore 2010 Europe Digital Year in Review February 2011

13

Social Networking Drives Advertising Market

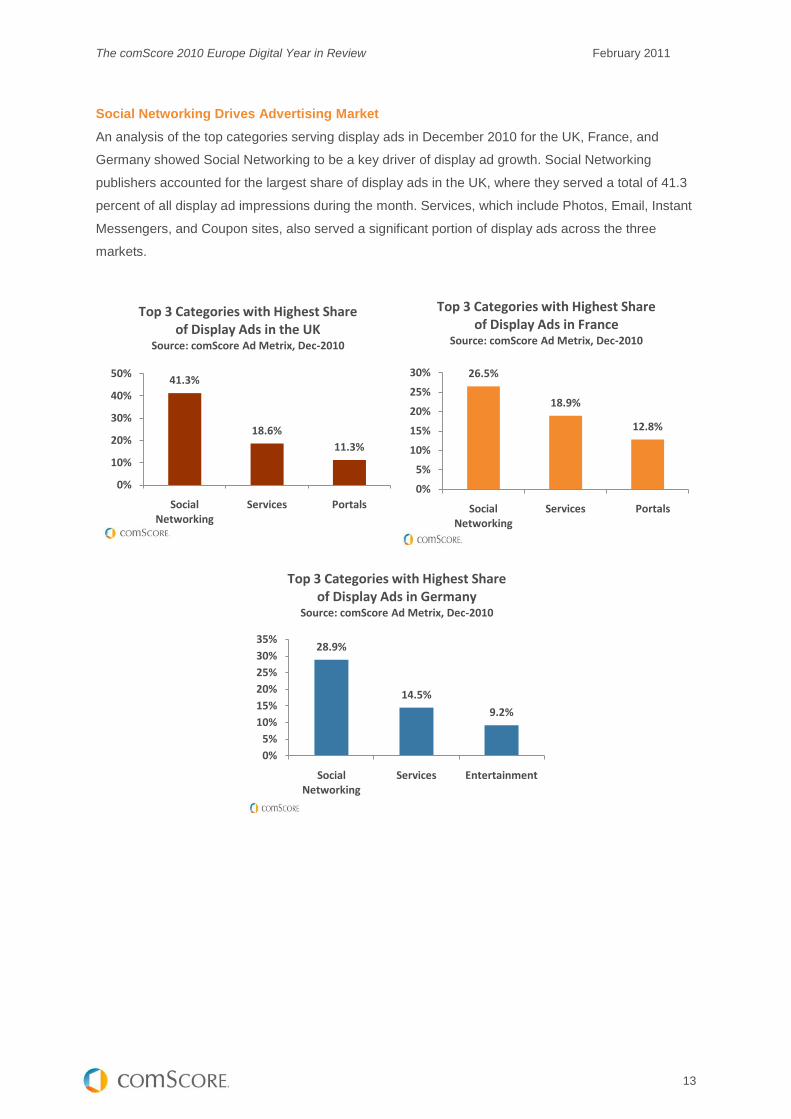

An analysis of the top categories serving display ads in December 2010 for the UK, France, and

Germany showed Social Networking to be a key driver of display ad growth. Social Networking

publishers accounted for the largest share of display ads in the UK, where they served a total of 41.3

percent of all display ad impressions during the month. Services, which include Photos, Email, Instant

Messengers, and Coupon sites, also served a significant portion of display ads across the three

markets.

41.3%

18.6%

11.3%

0%

10%

20%

30%

40%

50%

Social Networking

Services Portals

Top 3 Categories with Highest Share of Display Ads in the UK

Source: comScore Ad Metrix, Dec-2010

26.5%

18.9%

12.8%

0%

5%

10%

15%

20%

25%

30%

Social Networking

Services Portals

Top 3 Categories with Highest Share of Display Ads in France

Source: comScore Ad Metrix, Dec-2010

28.9%

14.5%

9.2%

0%

5%

10%

15%

20%

25%

30%

35%

Social Networking

Services Entertainment

Top 3 Categories with Highest Share of Display Ads in Germany

Source: comScore Ad Metrix, Dec-2010

The comScore 2010 Europe Digital Year in Review February 2011

14

TThhee RRiissee ooff CCoouuppoonn SSiitteess iinn EEuurrooppee

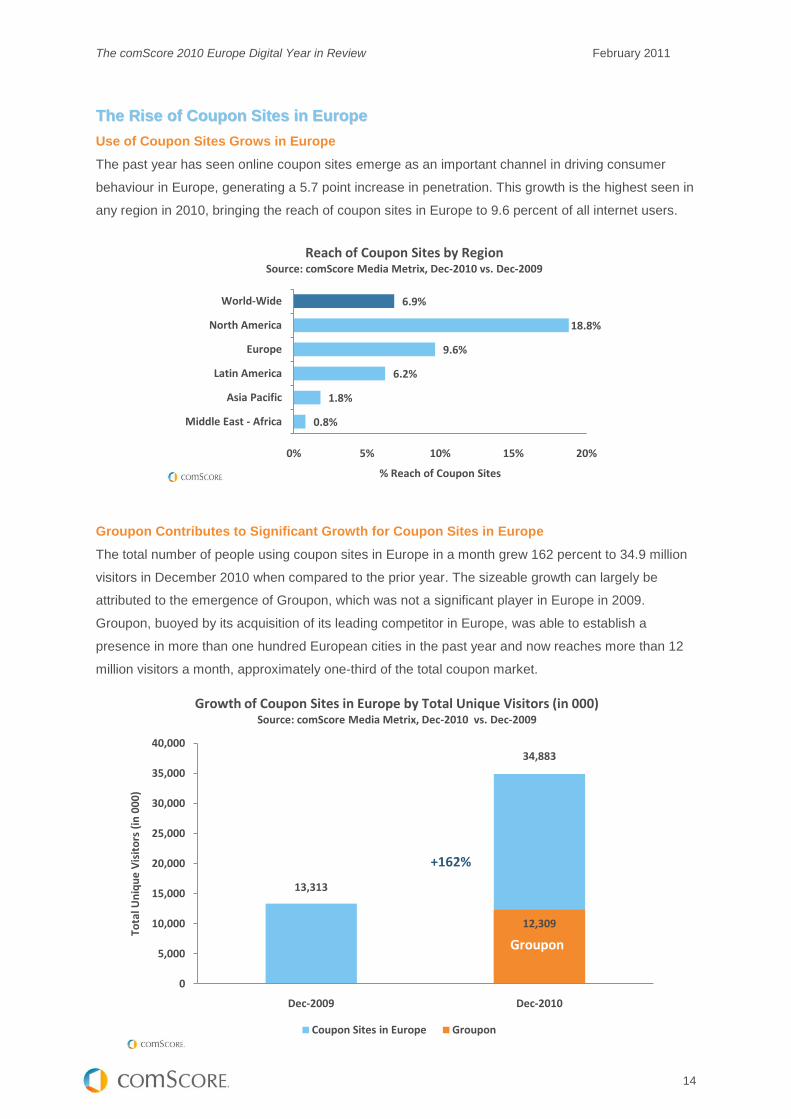

Use of Coupon Sites Grows in Europe

The past year has seen online coupon sites emerge as an important channel in driving consumer

behaviour in Europe, generating a 5.7 point increase in penetration. This growth is the highest seen in

any region in 2010, bringing the reach of coupon sites in Europe to 9.6 percent of all internet users.

Groupon Contributes to Significant Growth for Coupon Sites in Europe

The total number of people using coupon sites in Europe in a month grew 162 percent to 34.9 million

visitors in December 2010 when compared to the prior year. The sizeable growth can largely be

attributed to the emergence of Groupon, which was not a significant player in Europe in 2009.

Groupon, buoyed by its acquisition of its leading competitor in Europe, was able to establish a

presence in more than one hundred European cities in the past year and now reaches more than 12

million visitors a month, approximately one-third of the total coupon market.

13,313

34,883

12,309

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Dec-2009 Dec-2010

Tota

l Un

iqu

e V

isit

ors

(in

00

0)

Growth of Coupon Sites in Europe by Total Unique Visitors (in 000)Source: comScore Media Metrix, Dec-2010 vs. Dec-2009

Coupon Sites in Europe Groupon

Groupon

+162%

0.8%

1.8%

6.2%

9.6%

18.8%

6.9%

0% 5% 10% 15% 20%

Middle East - Africa

Asia Pacific

Latin America

Europe

North America

World-Wide

% Reach of Coupon Sites

Reach of Coupon Sites by RegionSource: comScore Media Metrix, Dec-2010 vs. Dec-2009

The comScore 2010 Europe Digital Year in Review February 2011

15

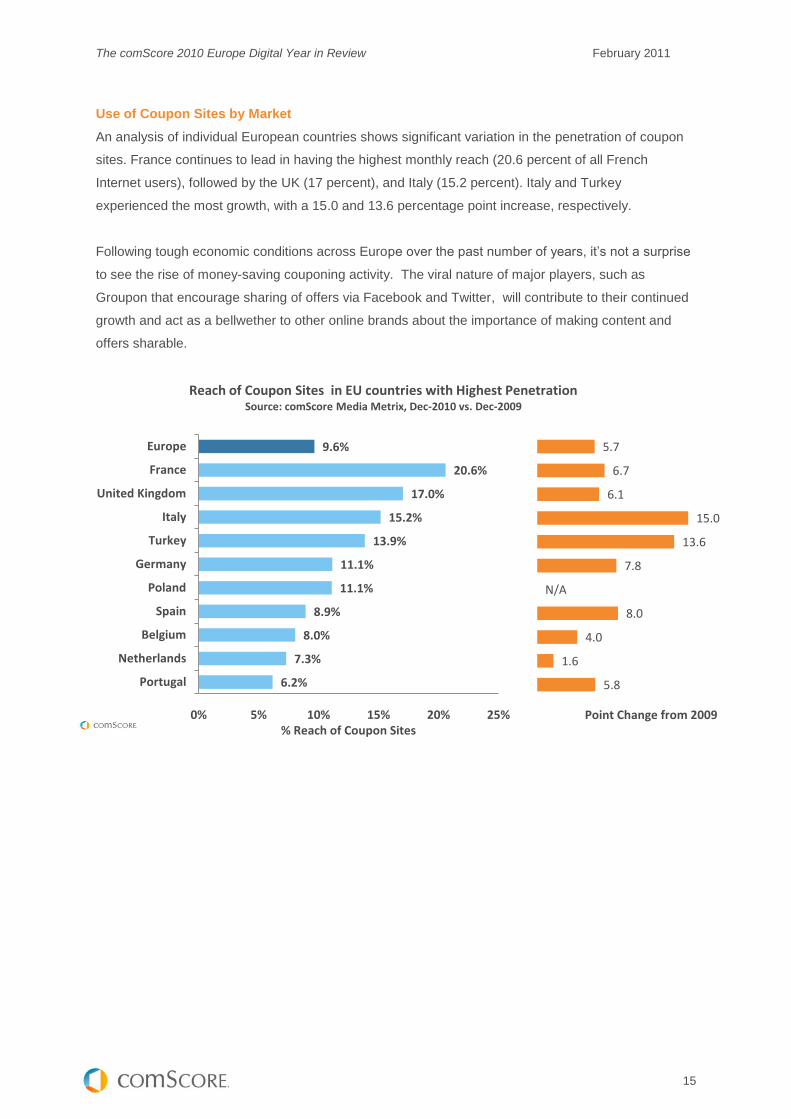

Use of Coupon Sites by Market

An analysis of individual European countries shows significant variation in the penetration of coupon

sites. France continues to lead in having the highest monthly reach (20.6 percent of all French

Internet users), followed by the UK (17 percent), and Italy (15.2 percent). Italy and Turkey

experienced the most growth, with a 15.0 and 13.6 percentage point increase, respectively.

Following tough economic conditions across Europe over the past number of years, it’s not a surprise

to see the rise of money-saving couponing activity. The viral nature of major players, such as

Groupon that encourage sharing of offers via Facebook and Twitter, will contribute to their continued

growth and act as a bellwether to other online brands about the importance of making content and

offers sharable.

6.2%

7.3%

8.0%

8.9%

11.1%

11.1%

13.9%

15.2%

17.0%

20.6%

9.6%

0% 5% 10% 15% 20% 25%

Portugal

Netherlands

Belgium

Spain

Poland

Germany

Turkey

Italy

United Kingdom

France

Europe

% Reach of Coupon Sites

Reach of Coupon Sites in EU countries with Highest PenetrationSource: comScore Media Metrix, Dec-2010 vs. Dec-2009

5.8

1.6

4.0

8.0

N/A

7.8

13.6

15.0

6.1

6.7

5.7

Point Change from 2009

The comScore 2010 Europe Digital Year in Review February 2011

16

VViiddeeoo GGrroowwtthh iinn EEuurrooppee

TV Sites Set for Continued Expansion in Europe

2010 was a strong year for TV web sites in Europe, with TV site penetration in the region increasing

by 7.5 percentage points to 47.4 percent of all European internet users in December 2010 – second

only to North America. Europe also leads in engagement with TV sites, as the average visitor spends

28 minutes visiting sites in this category each month.

German media giant ProSieben currently leads the European TV market with 32.5 million unique

visitors in December – nearly twice the audience of the second-ranking French property Groupe TF1

at 16.5 million. The German broadcaster ARD, the Italian Gruppo Mediaset, and the UK market leader

BBC round off the list of top five TV properties for the region.

3

The increase in the regional penetration of TV sites in Europe is similarly reflected in the growth of

visitors watching online video within the TV category across individual markets. In Germany, France

and the UK, the number of unique viewers on TV sites has shown significant increases from 2009 to

2010. In December 2010, TV sites in Germany reached 16.3 million viewers, up 14 percent. France

followed with the highest rate of change at 22 percent, with 15.0 million viewers. The UK also showed

strong growth at 19 percent, with 11.0 million viewers.

3 Year-over-year comparisons for Asia Pacific may include inorganic growth/loss due to a change in methodology in February 2010 and thus have been excluded

0%

10%

20%

30%

40%

50%

60%

70%

North America Europe Latin America Asia Pacific Middle East -Africa

Reach of Television Sites WorldwideSource: comScore Media Metrix, Dec-2010 vs. Dec-2009

Dec-09 Dec-10

+14.2

+7.5

+3.6

N / A3

+0.3

The comScore 2010 Europe Digital Year in Review February 2011

17

This growth in TV site video viewership proved to be more significant than growth in online video

viewership for the overall internet market, which held steady in Europe over the past year.

Viewers in Germany, the UK, and Spain Spend the Most Time Watching Online Videos

While all countries in the EU5 (France, Germany, Italy, Spain, UK) show similar rates of penetration

for the video market on the web, averaging 83.7 percent, the levels of engagement of users in these

markets differ. In December 2010, viewers from Germany, the UK, and Spain spent more time

watching online videos than those in the US, averaging 18.0, 17.0, and 16.2 hours respectively.

Viewers in France watched 12.2 hours of video and viewers in Italy watched the least with only 10.4

hours. On average, the time EU5 video viewers spent watching online videos in December 2010 (14.8

hours) was just an hour short of how many hours the average viewer in the US spent watching videos

in a month (15.8 hours).

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

Germany France UK

Tota

l Un

iqu

e V

iew

ers

(0

00

)Growth in Unique Video Viewers for TV Sites in Germany,

France, and the UKSource: comScore Video Metrix, Dec-2010 vs. Dec-2009

Dec-2009 Dec-2010

+14%+22%

+19%

0

2

4

6

8

10

12

14

16

18

20

Germany UK Spain US France Italy

Ho

urs

Pe

r V

iew

er

Time Spent Watching Online Videos in EU5 and US During the Month

Source: comScore Video Metrix, Dec-2010

Hours Per Viewer

The comScore 2010 Europe Digital Year in Review February 2011

18

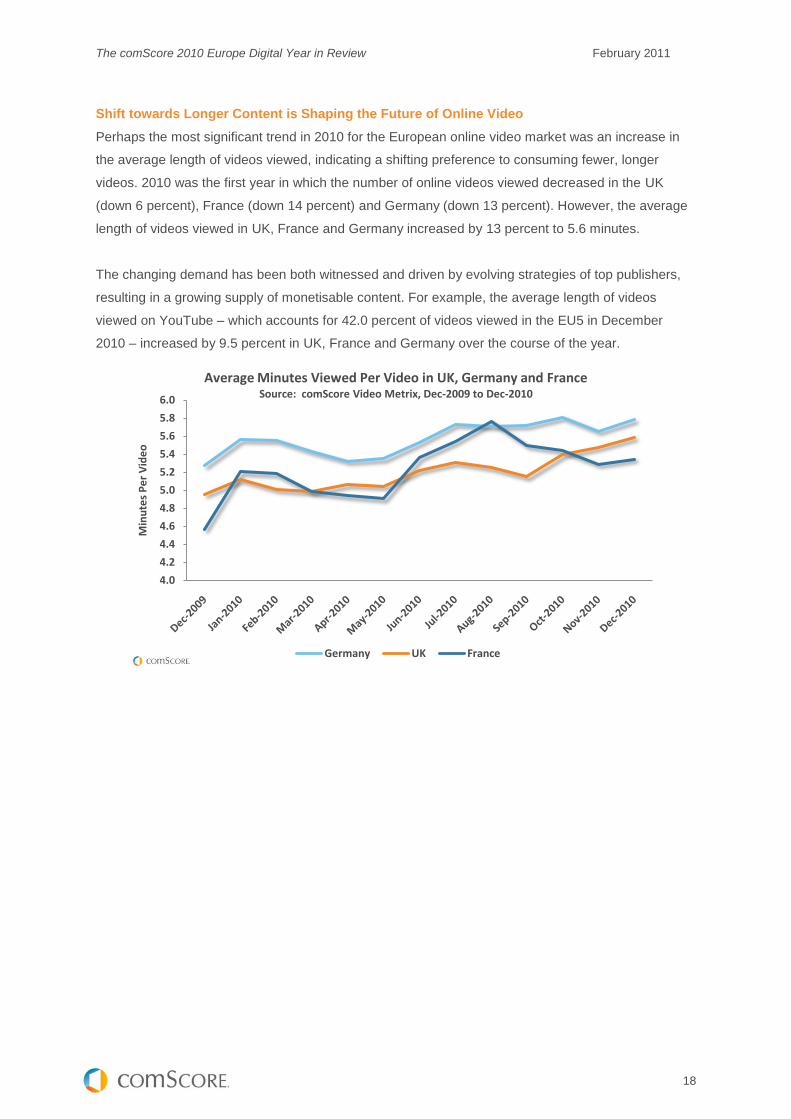

Shift towards Longer Content is Shaping the Future of Online Video

Perhaps the most significant trend in 2010 for the European online video market was an increase in

the average length of videos viewed, indicating a shifting preference to consuming fewer, longer

videos. 2010 was the first year in which the number of online videos viewed decreased in the UK

(down 6 percent), France (down 14 percent) and Germany (down 13 percent). However, the average

length of videos viewed in UK, France and Germany increased by 13 percent to 5.6 minutes.

The changing demand has been both witnessed and driven by evolving strategies of top publishers,

resulting in a growing supply of monetisable content. For example, the average length of videos

viewed on YouTube – which accounts for 42.0 percent of videos viewed in the EU5 in December

2010 – increased by 9.5 percent in UK, France and Germany over the course of the year.

4.0

4.2

4.4

4.6

4.8

5.0

5.2

5.4

5.6

5.8

6.0

Min

ute

s P

er

Vid

eo

Average Minutes Viewed Per Video in UK, Germany and FranceSource: comScore Video Metrix, Dec-2009 to Dec-2010

Germany UK France

The comScore 2010 Europe Digital Year in Review February 2011

19

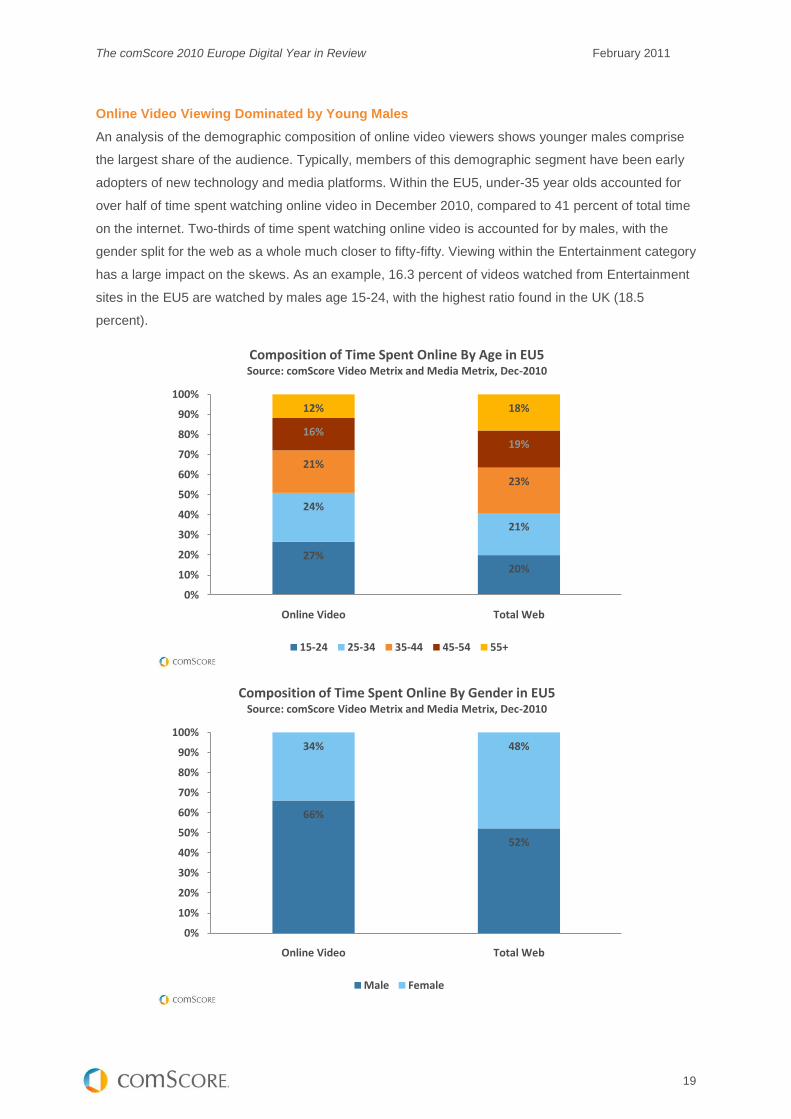

Online Video Viewing Dominated by Young Males

An analysis of the demographic composition of online video viewers shows younger males comprise

the largest share of the audience. Typically, members of this demographic segment have been early

adopters of new technology and media platforms. Within the EU5, under-35 year olds accounted for

over half of time spent watching online video in December 2010, compared to 41 percent of total time

on the internet. Two-thirds of time spent watching online video is accounted for by males, with the

gender split for the web as a whole much closer to fifty-fifty. Viewing within the Entertainment category

has a large impact on the skews. As an example, 16.3 percent of videos watched from Entertainment

sites in the EU5 are watched by males age 15-24, with the highest ratio found in the UK (18.5

percent).

27%20%

24%

21%

21%

23%

16%19%

12% 18%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Online Video Total Web

Composition of Time Spent Online By Age in EU5Source: comScore Video Metrix and Media Metrix, Dec-2010

15-24 25-34 35-44 45-54 55+

66%

52%

34% 48%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Online Video Total Web

Composition of Time Spent Online By Gender in EU5Source: comScore Video Metrix and Media Metrix, Dec-2010

Male Female

The comScore 2010 Europe Digital Year in Review February 2011

20

EEuurrooppeeaann MMoobbiillee UUssaaggee 22001100

Smartphone Penetration in EU5 Continues to Increase

Smartphones continue to become an increasingly important segment of the European mobile phone

landscape in 2010. Smartphone penetration in the EU5 (United Kingdom, France, Germany, Spain,

and Italy) increased by 9.5 percentage points to 31.1 percent, placing it higher than the US (which

saw smartphone penetration increase 10.2 percentage points to 27.0 percent).

An analysis of the growth in smartphone reach in the EU5 reveals a dramatic increase in the adoption

of Google and Apple smartphone operating systems (OS). Google Android, which experienced a 951-

percent gain in the use of its OS, now boasts an audience of 8.7 million subscribers in these five

European markets. Meanwhile, Apple experienced a 115-percent increase to 14.5 million subscribers.

While Symbian continues to lead the smartphone OS market, the growth in Google and Apple OS

usage reflects an increasing popularity for both platforms that appears positioned for continued

growth in 2011.

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Google Apple RIM Palm Symbian Microsoft

Use

rs (

00

0)

Year-over-Year Change in EU5 Smartphone OS Users (in 000)Source: comScore MobiLens, Dec-2010 vs. Dec-2009 (3 Month Average)

Dec-2009 Dec-2010

+951%

+115%

+65%

+34%

+12%

-2%

Note: The total audience for comScore MobiLens includes persons age 13+.

0%

5%

10%

15%

20%

25%

30%

35%

Europe U.S.

% o

f M

arke

t

Smartphone Penetration in EU5 and US by Market ReachSource: comScore MobiLens, Dec-2010 vs. Dec-2010 (3 Month Average)

% Reach of Smartphones in Dec-2009 % Reach of Smartphones in Dec-2010

+10.2+9.5

Note: The total audience for comScore MobiLens includes persons age 13+.

The comScore 2010 Europe Digital Year in Review February 2011

21

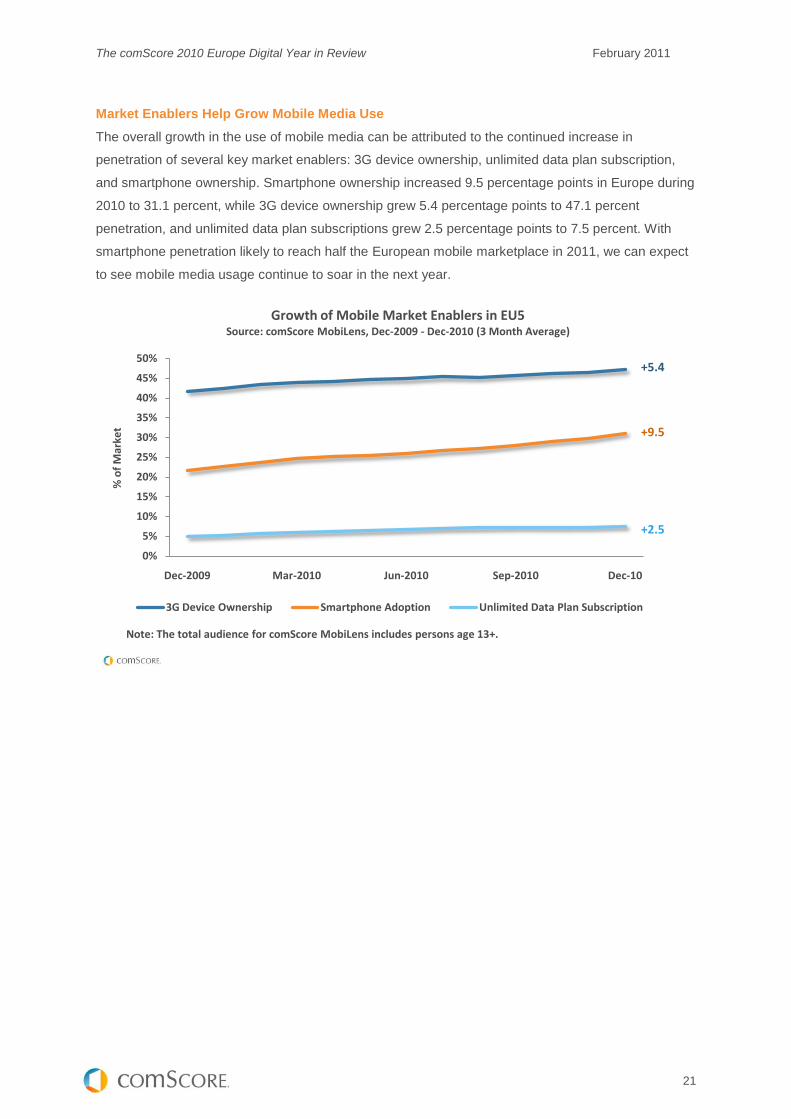

Market Enablers Help Grow Mobile Media Use

The overall growth in the use of mobile media can be attributed to the continued increase in

penetration of several key market enablers: 3G device ownership, unlimited data plan subscription,

and smartphone ownership. Smartphone ownership increased 9.5 percentage points in Europe during

2010 to 31.1 percent, while 3G device ownership grew 5.4 percentage points to 47.1 percent

penetration, and unlimited data plan subscriptions grew 2.5 percentage points to 7.5 percent. With

smartphone penetration likely to reach half the European mobile marketplace in 2011, we can expect

to see mobile media usage continue to soar in the next year.

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Dec-2009 Mar-2010 Jun-2010 Sep-2010 Dec-10

3G Device Ownership Smartphone Adoption Unlimited Data Plan Subscription

% o

f M

arke

t

Growth of Mobile Market Enablers in EU5Source: comScore MobiLens, Dec-2009 - Dec-2010 (3 Month Average)

+5.4

+9.5

+2.5

Note: The total audience for comScore MobiLens includes persons age 13+.

The comScore 2010 Europe Digital Year in Review February 2011

22

EEuurrooppeeaann SSeeaarrcchh MMaarrkkeett 22001100

European Search Intensity Varies by Market

An analysis of individual search markets in Europe reveals differing levels of search intensity in these markets.

Searchers in Poland, who make up a modest share of unique searchers in Europe, exhibit the heaviest search

intensity, with the highest number of searches per searcher across all markets. In contrast, Germany and Russia,

which have significant shares of European searchers, show lower search intensity than in most markets, indexing

below the European regional average.

0

20

40

60

80

100

120

140

160

180

200

0%

2%

4%

6%

8%

10%

12%

14%

16%

Sear

che

s P

er

Sear

che

r

Shar

e o

f U

niq

ue

Se

arch

ers

in E

uro

pe

Search Intensity in European MarketsSource: comScore qSearch, Dec-2010

Share of Europe's Unique Searchers Searches Per Searcher

The comScore 2010 Europe Digital Year in Review February 2011

23

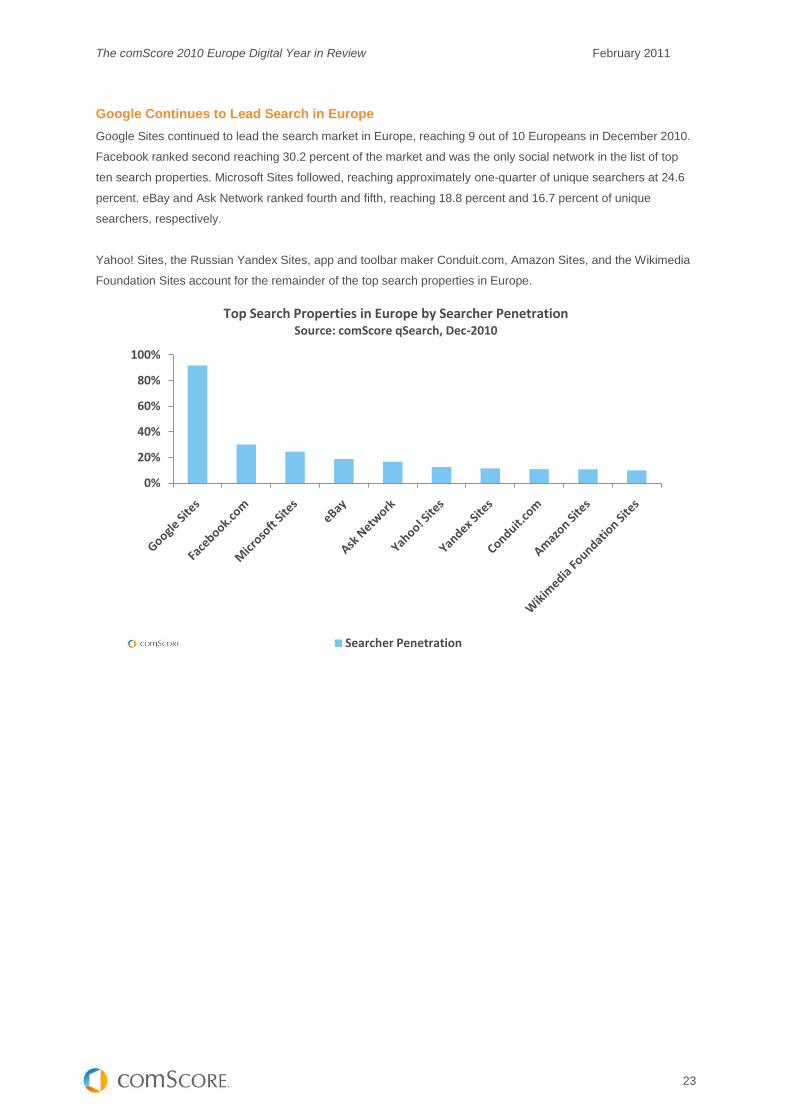

Google Continues to Lead Search in Europe

Google Sites continued to lead the search market in Europe, reaching 9 out of 10 Europeans in December 2010.

Facebook ranked second reaching 30.2 percent of the market and was the only social network in the list of top

ten search properties. Microsoft Sites followed, reaching approximately one-quarter of unique searchers at 24.6

percent. eBay and Ask Network ranked fourth and fifth, reaching 18.8 percent and 16.7 percent of unique

searchers, respectively.

Yahoo! Sites, the Russian Yandex Sites, app and toolbar maker Conduit.com, Amazon Sites, and the Wikimedia

Foundation Sites account for the remainder of the top search properties in Europe.

0%

20%

40%

60%

80%

100%

Top Search Properties in Europe by Searcher PenetrationSource: comScore qSearch, Dec-2010

Searcher Penetration

The comScore 2010 Europe Digital Year in Review February 2011

24

LLooookkiinngg AAhheeaadd ttoo 22001111

Europe is Ripe for Continued Growth and Innovation

IAB Europe reports that internet advertising is approaching a 20-percent share of total advertising

spend, almost doubling its share over the last two years. While the immediately previous years saw a

contraction in marketing budgets, the digital marketplace in Europe continues to grow. With growth

comes innovation -- from advanced planning tools to sophisticated targeting techniques. Creativity is

also beginning to take centre stage as marketers realise the previously unseen brand building

benefits that digital can deliver. Most importantly, as consumers continue to expand their media

consumption across a variety of devices and platforms, a rethinking of measurement approaches and

marketing strategies becomes necessary.

With that in mind, the following is a summary of the key digital media trends we’re seeing in Europe

that will have an impact on the year to come:

Social Networking: Social media grew immensely in 2010 and saturated at least three

quarters of individual European markets. 2011 will likely see a continued growth in the use of

such sites, as social networking continues to be an integral part of online life. Marketing on

these platforms will likely grow as well, as social networking becomes more heavily integrated

with publisher and advertiser sites. Notably, despite earlier concerns about low click-through

rates on social media advertising, advertising rates in social networks in European markets

increased in 2010, reflecting increased confidence in the value of such platforms in reaching

highly-targeted audiences. New trends such as location-based social networking will also

likely contribute to the evolution of marketing on social media.

Advertising: The display advertising market continued to grow in 2010, with the Social

Networking category accounting for a rapidly increasing share of impressions. The online ad

market continues to evolve, with more advanced ad units, improved targeting capabilities, and

higher quality creative.

Video: In 2010, a noticeable trend in video viewership in Europe was an increase in the

average length of time spent watching individual videos. With more viewers watching longer-

form content comes a more meaningful opportunity for video advertising online. It is

significant to note that although overall video viewership in Europe grew by only a few

percentage points in 2010, viewership on TV sites experienced much higher growth. As

viewers increasingly look to online video for longer, quality content traditionally found on

television, it is very likely that online video advertising will continue to experience exceptional

growth.

Mobile: As evidenced in comScore’s Mobile Year in Review report, we believe 2011 will be a

transformative year for Mobile. We predict more than half of all mobile consumers will have

access to mobile media, largely driven by growing adoption of smartphones. Identifying the

synergies that exist between all consumer touch points – traditional PC internet, mobile media

(via app and browser), tablets, etc. – and understanding how consumers use these devices to

fulfill different needs and convenience levels will be of critical importance to marketers.

The comScore 2010 Europe Digital Year in Review February 2011

25

Search: Search marketing continues to be an important component of an effective business-

building strategy. Local players are growing in popularity, particularly in Russia, which creates

more options for both consumers and marketers.

2011 will undoubtedly be an exciting year for the European digital marketplace, and a strong

understanding of both the similarities and differences across countries will be critical to the success of

the modern marketer.

The comScore 2010 Europe Digital Year in Review February 2011

26

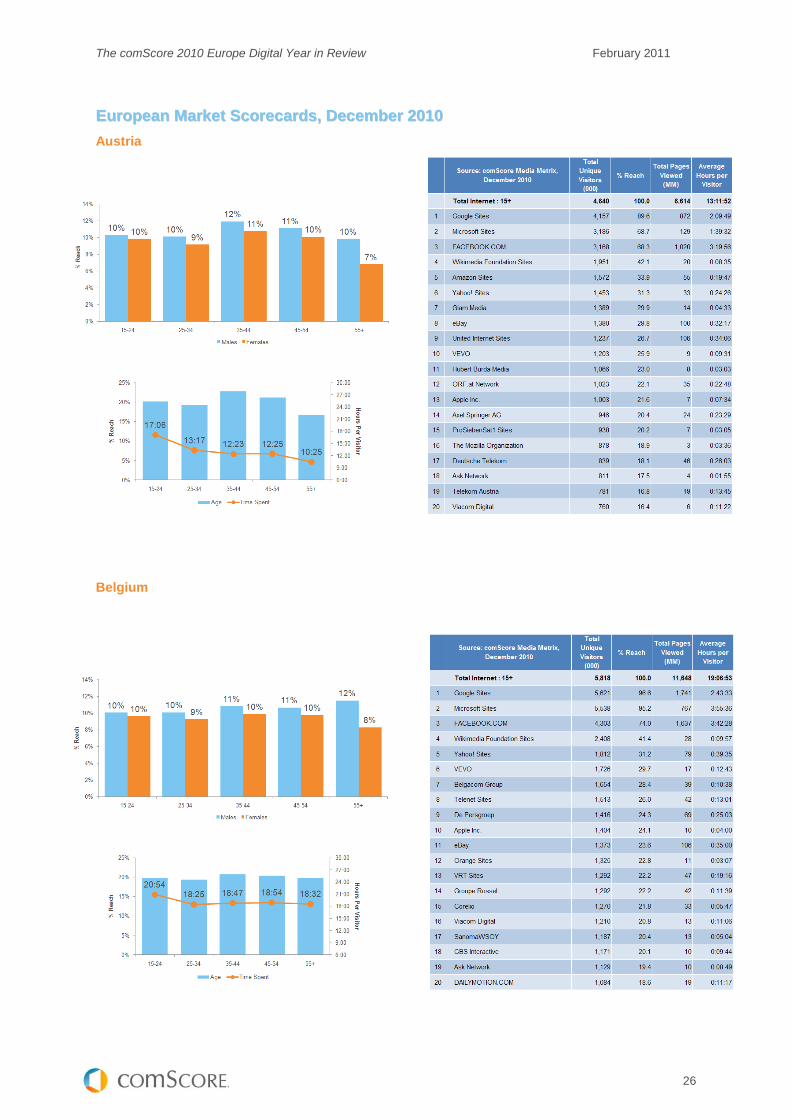

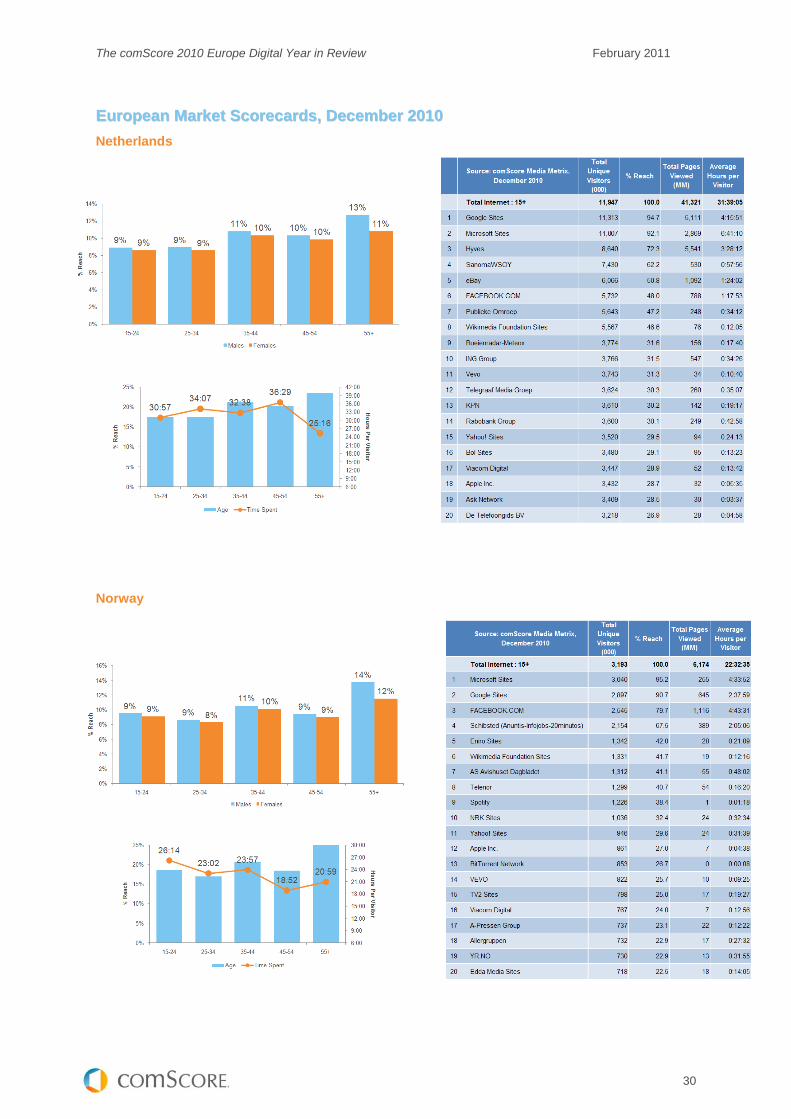

EEuurrooppeeaann MMaarrkkeett SSccoorreeccaarrddss,, DDeecceemmbbeerr 22001100

Austria

Belgium

The comScore 2010 Europe Digital Year in Review February 2011

27

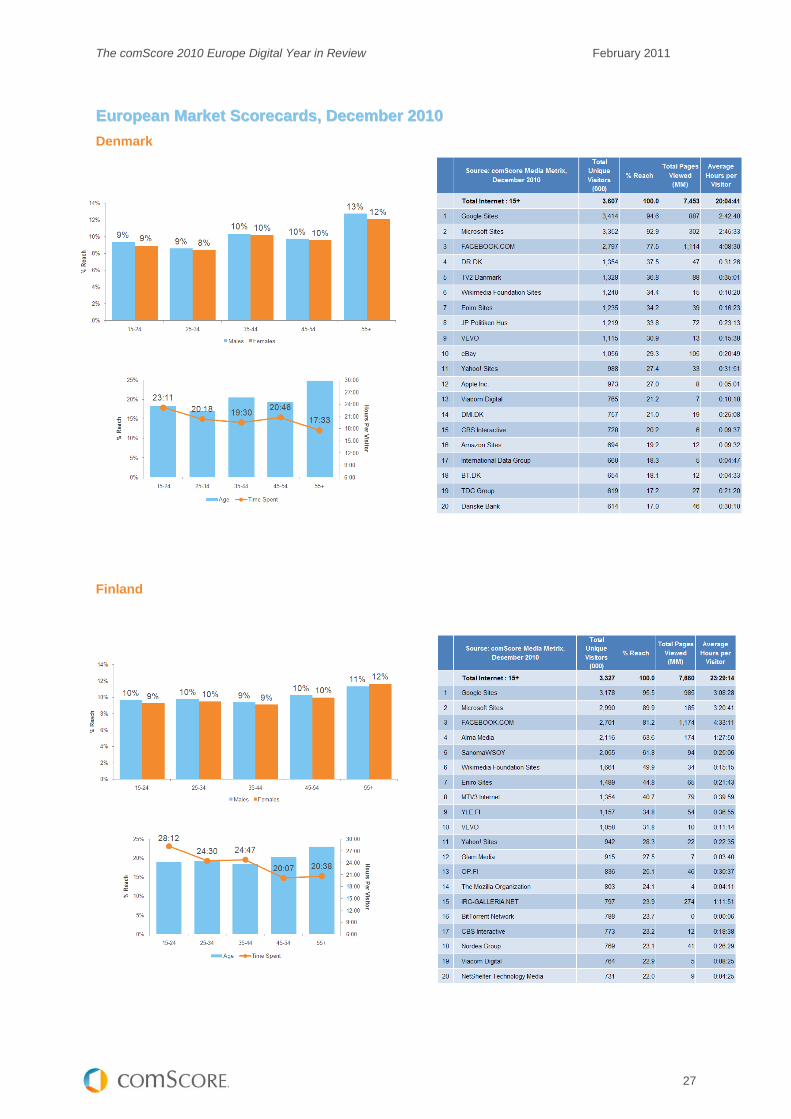

EEuurrooppeeaann MMaarrkkeett SSccoorreeccaarrddss,, DDeecceemmbbeerr 22001100

Denmark

Finland

The comScore 2010 Europe Digital Year in Review February 2011

28

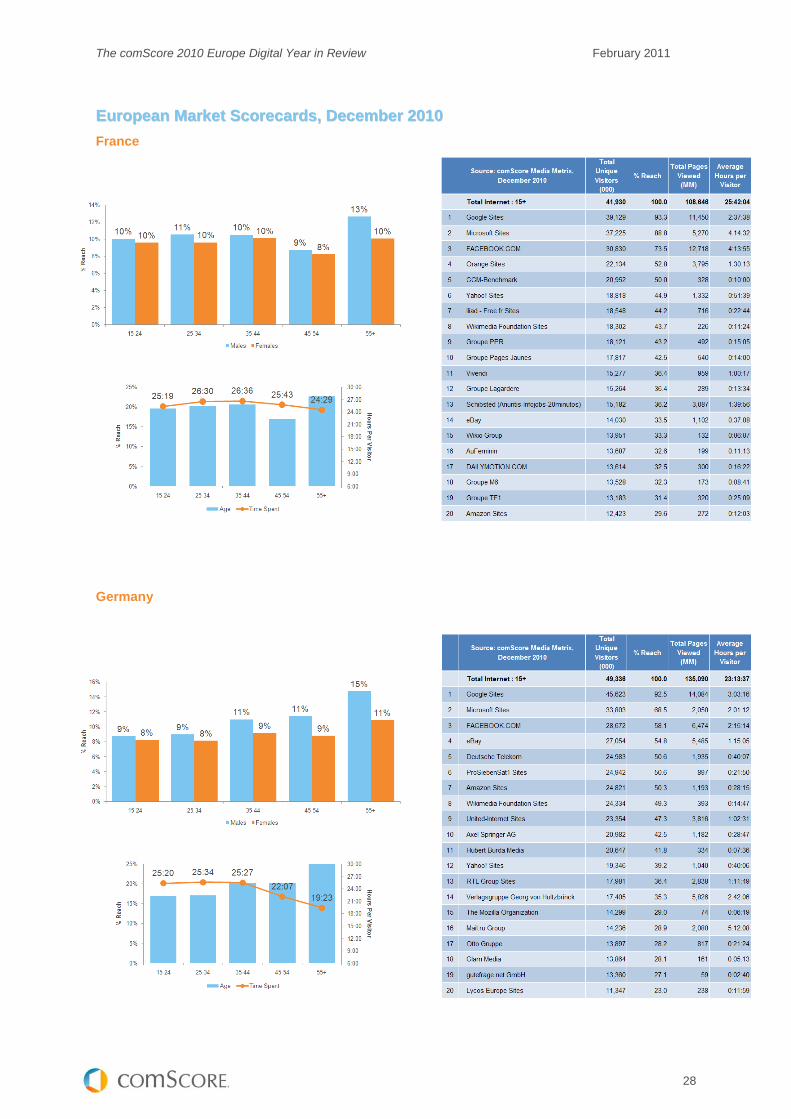

EEuurrooppeeaann MMaarrkkeett SSccoorreeccaarrddss,, DDeecceemmbbeerr 22001100

France

Germany

The comScore 2010 Europe Digital Year in Review February 2011

29

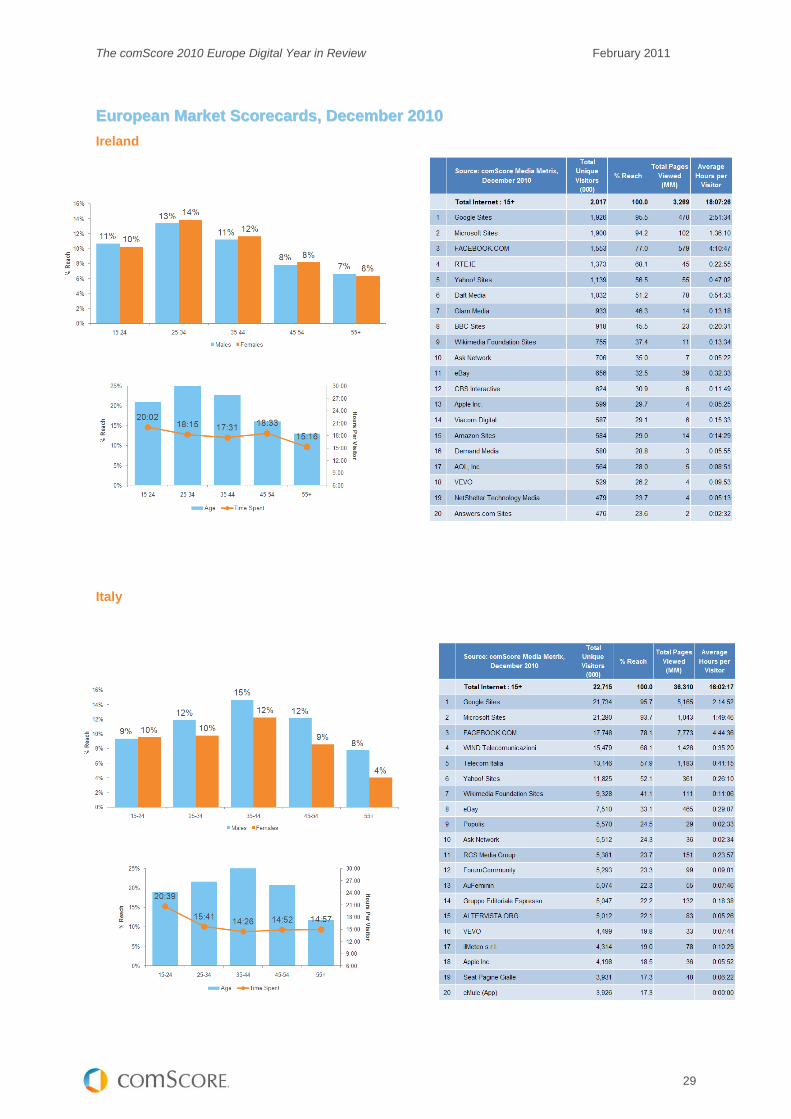

EEuurrooppeeaann MMaarrkkeett SSccoorreeccaarrddss,, DDeecceemmbbeerr 22001100

Ireland

Italy

The comScore 2010 Europe Digital Year in Review February 2011

30

EEuurrooppeeaann MMaarrkkeett SSccoorreeccaarrddss,, DDeecceemmbbeerr 22001100

Netherlands

Norway

The comScore 2010 Europe Digital Year in Review February 2011

31

EEuurrooppeeaann MMaarrkkeett SSccoorreeccaarrddss,, DDeecceemmbbeerr 22001100

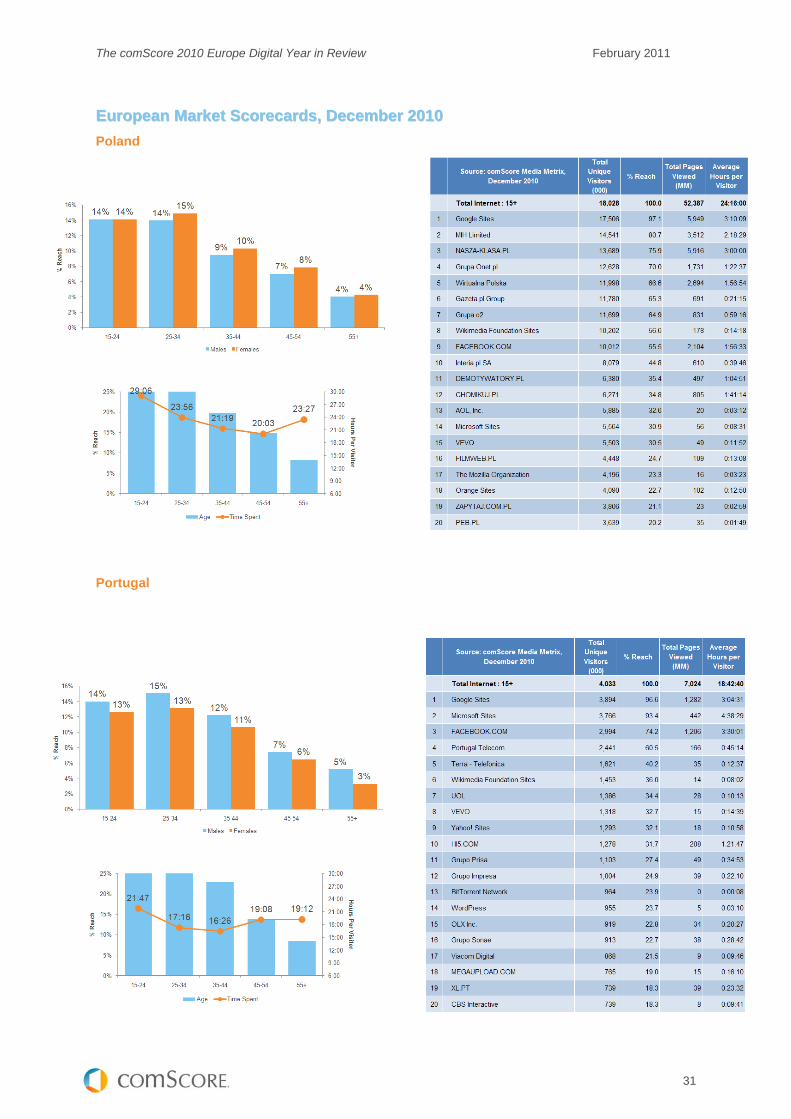

Poland

Portugal

The comScore 2010 Europe Digital Year in Review February 2011

32

EEuurrooppeeaann MMaarrkkeett SSccoorreeccaarrddss,, DDeecceemmbbeerr 22001100

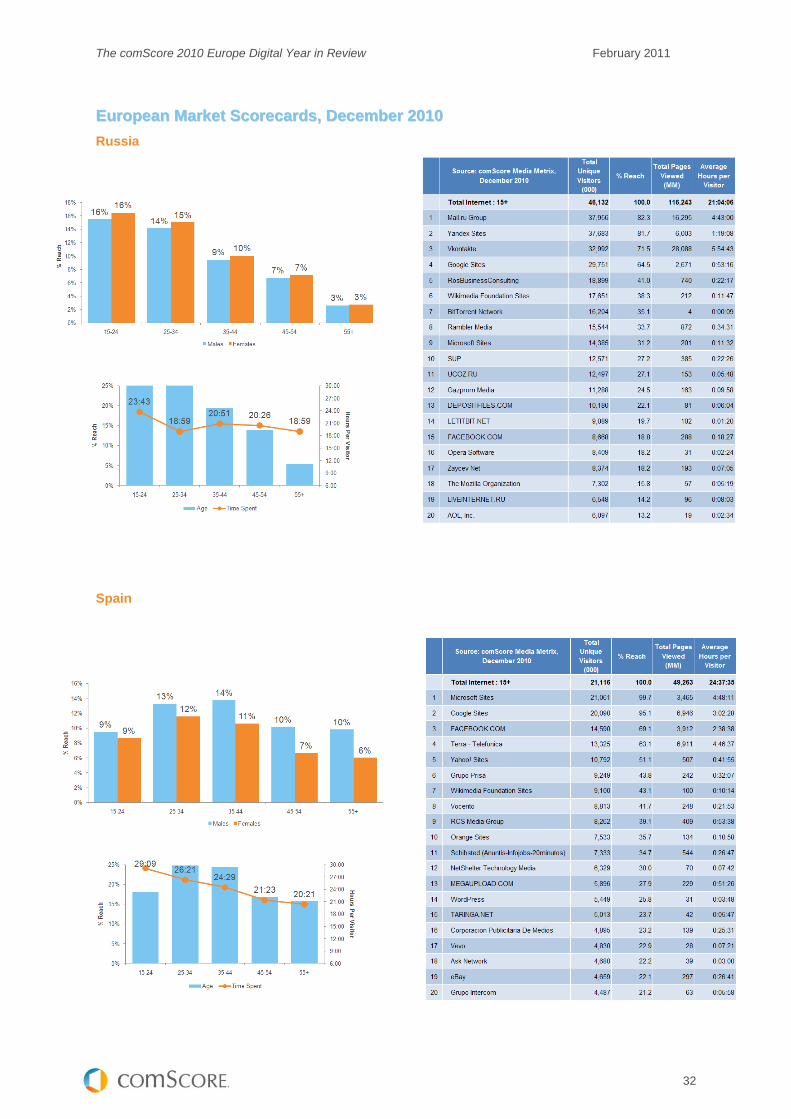

Russia

Spain

The comScore 2010 Europe Digital Year in Review February 2011

33

EEuurrooppeeaann MMaarrkkeett SSccoorreeccaarrddss,, DDeecceemmbbeerr 22001100

Sweden

Switzerland

The comScore 2010 Europe Digital Year in Review February 2011

34

EEuurrooppeeaann MMaarrkkeett SSccoorreeccaarrddss,, DDeecceemmbbeerr 22001100

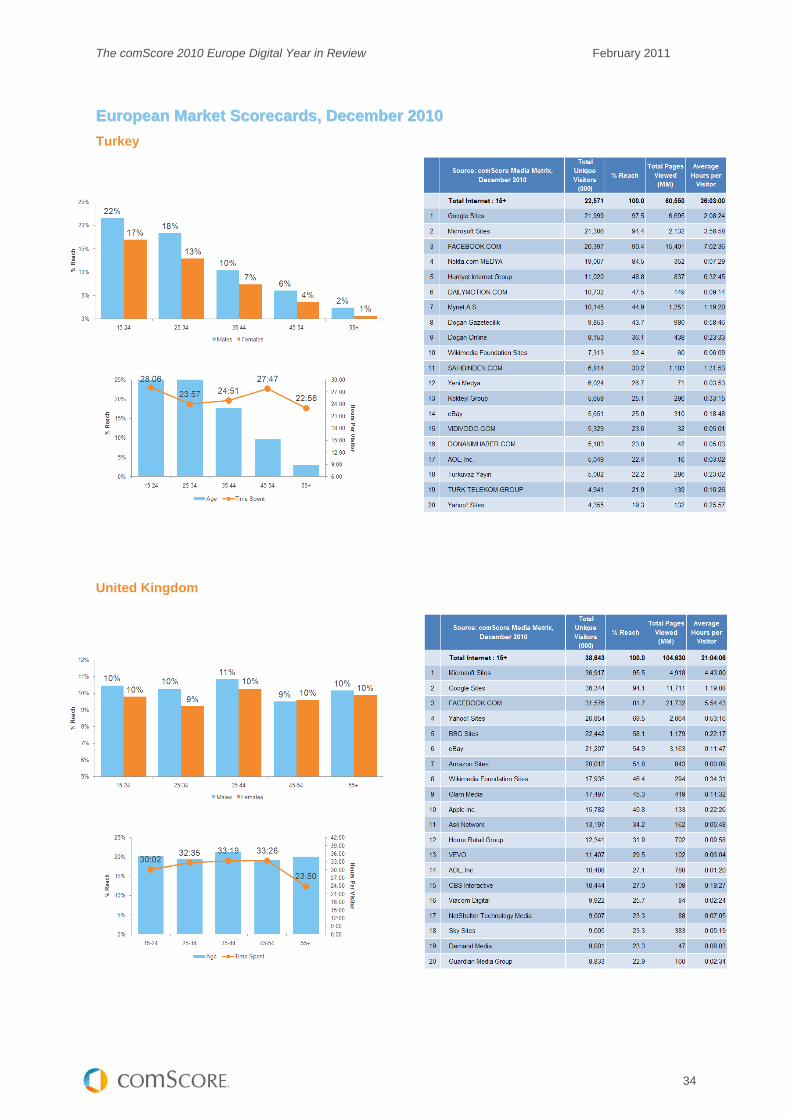

Turkey

United Kingdom

The comScore 2010 Europe Digital Year in Review February 2011

35

AAbboouutt ccoommSSccoorree

comScore, Inc. (NASDAQ: SCOR) is a global leader in measuring the digital world and preferred

source of digital business analytics. comScore helps its clients better understand, leverage and profit

from the rapidly evolving digital marketing landscape by providing data, analytics and on-demand

software solutions for the measurement of online ads and audiences, media planning, website

analytics, advertising effectiveness, copy-testing, social media, search, video, mobile, cross-media, e-

commerce, and a broad variety of emerging forms of digital consumer behaviour. comScore services,

which now include the product suites of recent acquisitions Nedstat, Nexius XPlore, ARSGroup and

Certifica, are used by more than 1,600 clients around the world, including global leaders such as

AOL, Baidu, BBC, Best Buy, Carat, Deutsche Bank, ESPN, Facebook, France Telecom, Financial

Times, Fox, Microsoft, MediaCorp, Nestle, Starcom, Terra Networks, Universal McCann, Verizon

Services Group, ViaMichelin and Yahoo!. For more information, please visit www.comScore.com.

OOuurr MMeetthhooddoollooggyy

Central to most comScore services is the comScore panel, the largest continuously measured

consumer panel of its kind. With approximately 2 million worldwide consumers under continuous

measurement, comScore delivers one of the highest quality, most comprehensive views of internet

browsing, buying and other activity, in the digital environment. Complementing the panel is a unique

census-level data collection method, which allows for the integration of consumers’ internet behaviour

with powerful audience-measurement insights. The methodology that comScore utilises to thread

census-level collected data with the comScore panel is called Unified Digital Measurement. For more

information, please visit: http://www.comscore.com/About_comScore/Methodology

The foundation of our MobiLens service is the continuous collection of consumer behaviour

information. Using proprietary data collection methods, we survey nationally representative samples

of mobile subscribers aged 13+. Survey fieldwork is conducted monthly and to ensure demographic

representation, recruitment quotas are set based on each country’s census demographic and

geographic profiles for age and gender. The resulting MobiLens survey panels are nationally

representative samples of mobile subscribers substantial enough to provide projected data for sub-

segments as small as 1% of mobile subscribers aged 13 years of age and higher. The MobiLens’

sampling and survey methods undergo extensive analysis and market validation including

comparisons to known network operator market shares, leading handset model shares, downloading

activity, and other usage metrics. For more information, please visit:

http://www.comscore.com/Products_Services/Product_Index/MobiLens

FOR MORE INFORMATION, PLEASE CONTACT:

Carmela Aquino, comScore, Inc.

+1 703 438 2024

Cathy McCarthy, comScore, Inc.

+44 203 111 1746