the adjusting process chapter 3 3-1. what is the difference between cash basis accounting &...

TRANSCRIPT

The Adjusting Process

Chapter 3

3-1

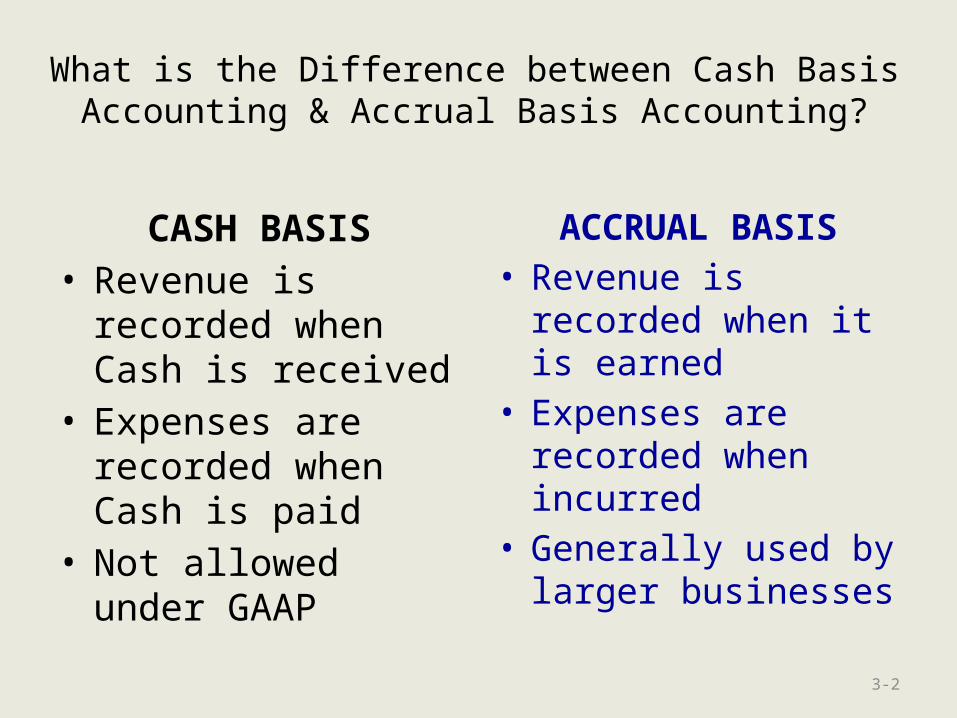

What is the Difference between Cash Basis Accounting & Accrual Basis Accounting?

CASH BASIS• Revenue is recorded

when Cash is received

• Expenses are recorded when Cash is paid

• Not allowed under GAAP

ACCRUAL BASIS• Revenue is recorded

when it is earned• Expenses are

recorded when incurred

• Generally used by larger businesses

3-2

The Time Period Concept

• Assumes that a business’s activities can be sliced into small segments and that financial statements can be prepared for specific time periods, such as a month, quarter, or year.

• Any twelve month period is referred to as a fiscal year.

3-3

Su Mo Tu We Th Fr Sa

1 2 3 4 5 6

7 8 9 10 11 12 13

14 15 16 17 18 19 20

21 22 23 24 25 26 27

28 29 30 31

OCTOBER 2012

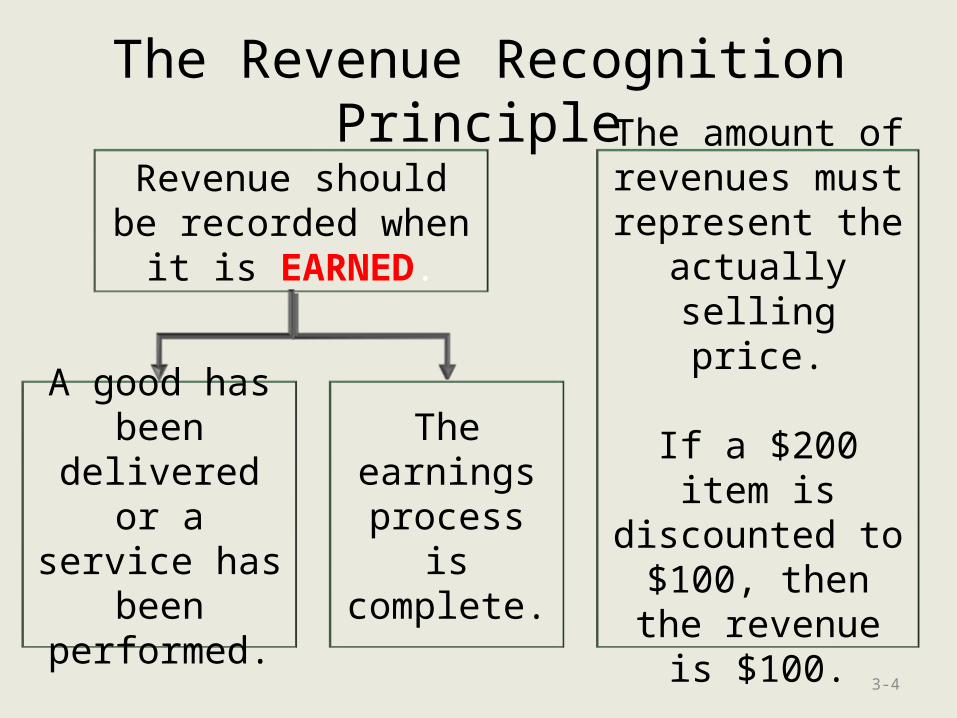

The Revenue Recognition Principle

3-4

Revenue should be recorded when it is

EARNED.

A good has been delivered

or a service has been

performed.

The earnings

process is complete.

The amount of revenues must represent the

actually selling price.

If a $200 item is discounted to $100, then the

revenue is $100.

The Matching Principle

3-5

Expenses are recorded when

they are incurred during

the period.

Expenses are matched at the end of the period

against the revenues for that period.

For example, rent expense for January should be

matched against January revenues, even if was

actually paid in December.

3-6

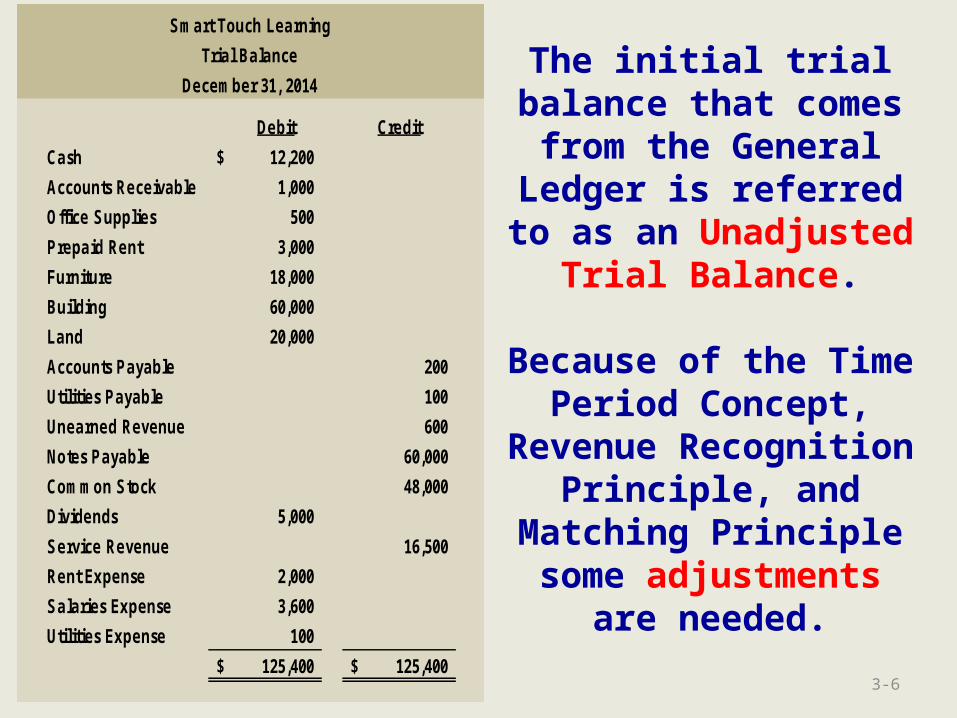

The initial trial balance that comes from the

General Ledger is referred to as an Unadjusted Trial

Balance.

Because of the Time Period Concept,

Revenue Recognition Principle, and Matching

Principle some adjustments are

needed.

Smart Touch Learning

Trial Balance

December 31, 2014

Debit Credit

Cash 12,200$

Accounts Receivable 1,000

Office Supplies 500

Prepaid Rent 3,000

Furniture 18,000

Building 60,000

Land 20,000

Accounts Payable 200

Utilities Payable 100

Unearned Revenue 600

Notes Payable 60,000

Common Stock 48,000

Dividends 5,000

Service Revenue 16,500

Rent Expense 2,000

Salaries Expense 3,600

Utilities Expense 100

125,400$ 125,400$

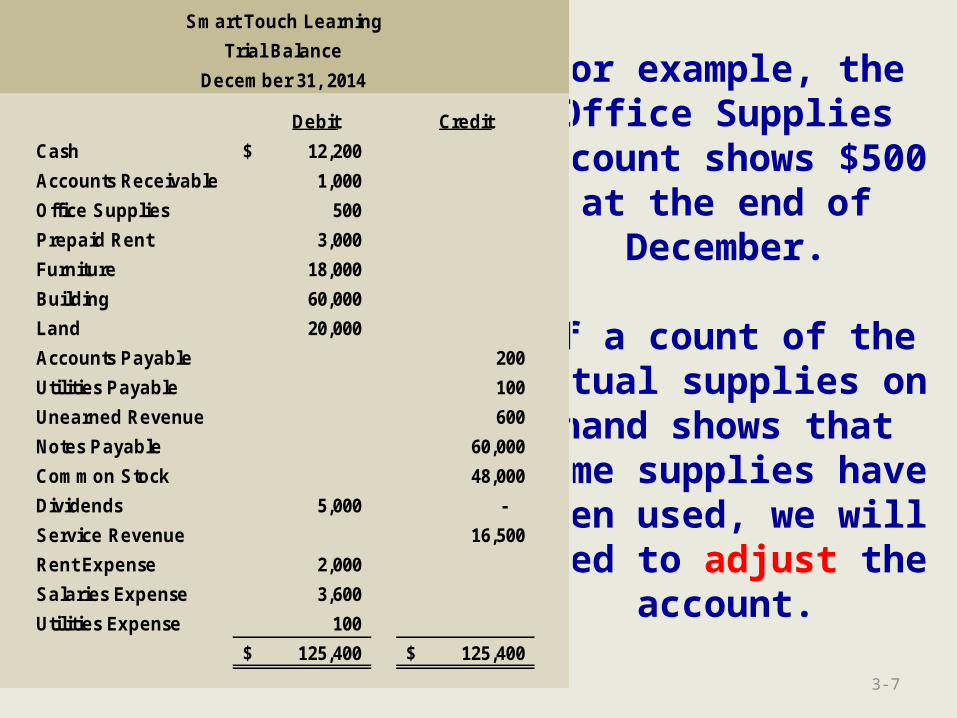

Smart Touch Learning

Trial Balance

December 31, 2014

Debit Credit

Cash 12,200$

Accounts Receivable 1,000

Office Supplies 500

Prepaid Rent 3,000

Furniture 18,000

Building 60,000

Land 20,000

Accounts Payable 200

Utilities Payable 100

Unearned Revenue 600

Notes Payable 60,000

Common Stock 48,000

Dividends 5,000 -

Service Revenue 16,500

Rent Expense 2,000

Salaries Expense 3,600

Utilities Expense 100

125,400$ 125,400$

3-7

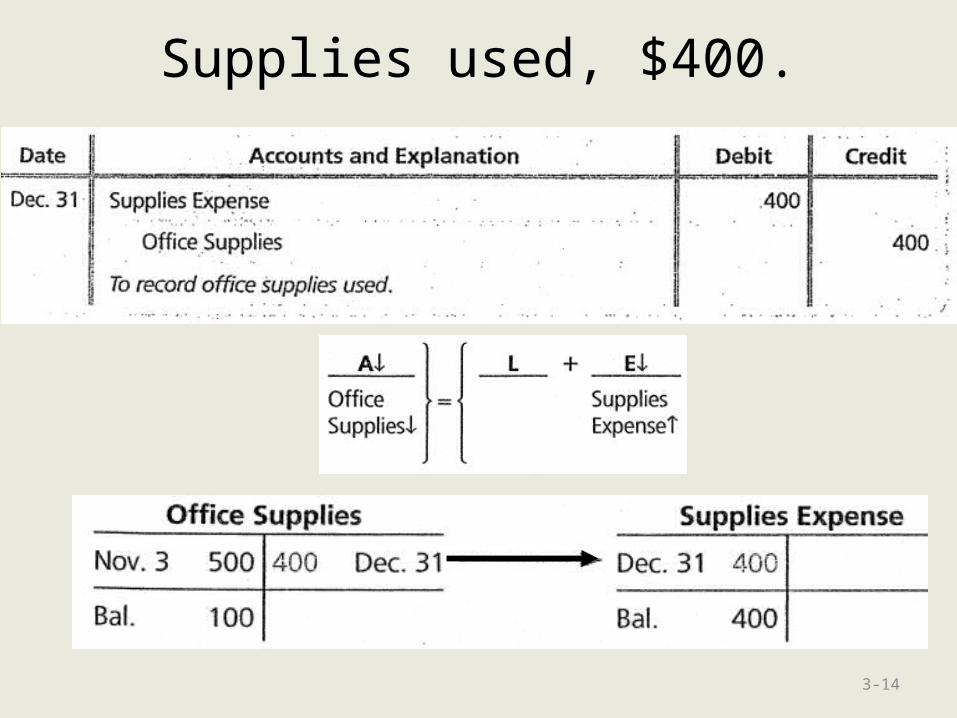

For example, the Office Supplies account

shows $500 at the end of December.

If a count of the actual supplies on hand shows that some

supplies have been used, we will need to adjust the account.

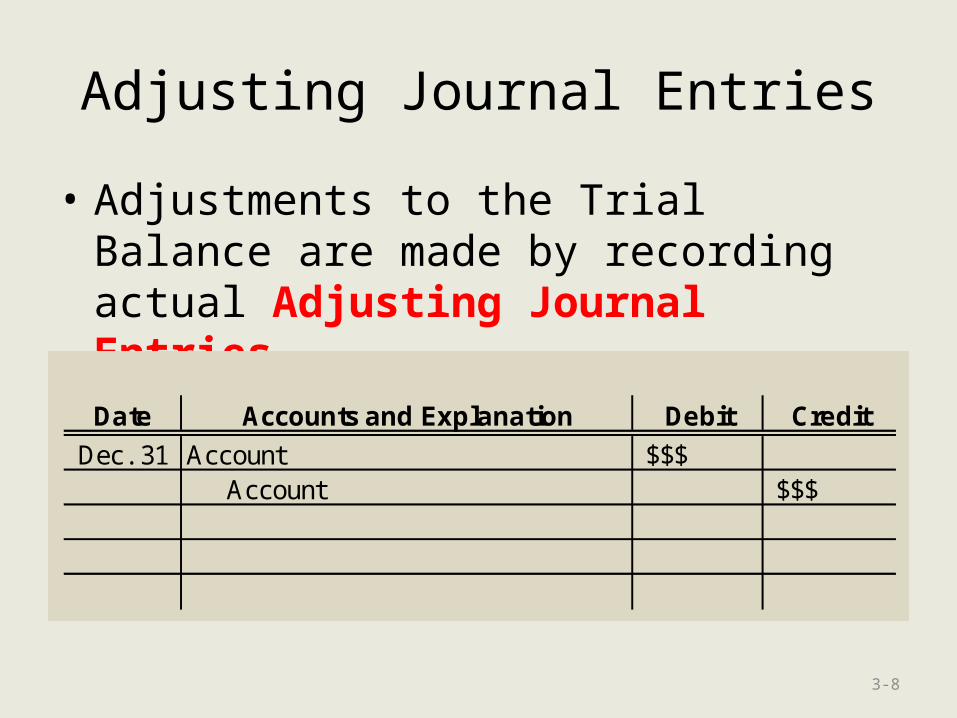

Adjusting Journal Entries

• Adjustments to the Trial Balance are made by recording actual Adjusting Journal Entries.

3-8

Date Accounts and Explanation Debit Credit

Dec. 31 Account $$$ Account $$$

Adjusting Journal Entries

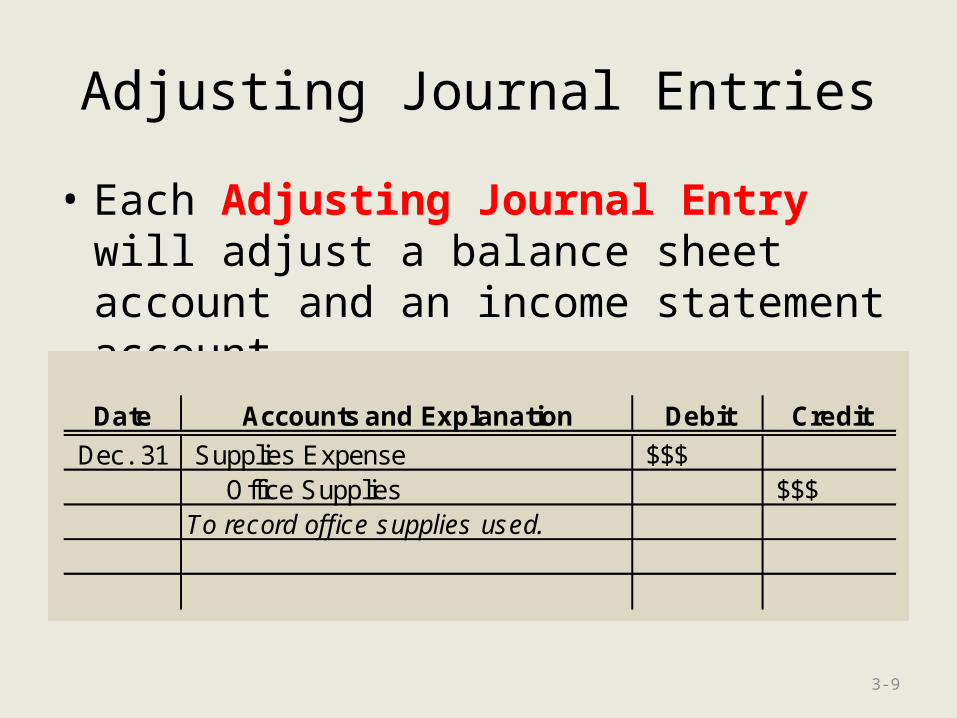

• Each Adjusting Journal Entry will adjust a balance sheet account and an income statement account.

3-9

Date Accounts and Explanation Debit Credit

Dec. 31 Supplies Expense $$$ Office Supplies $$$To record office supplies used.

Adjusting Journal Entries

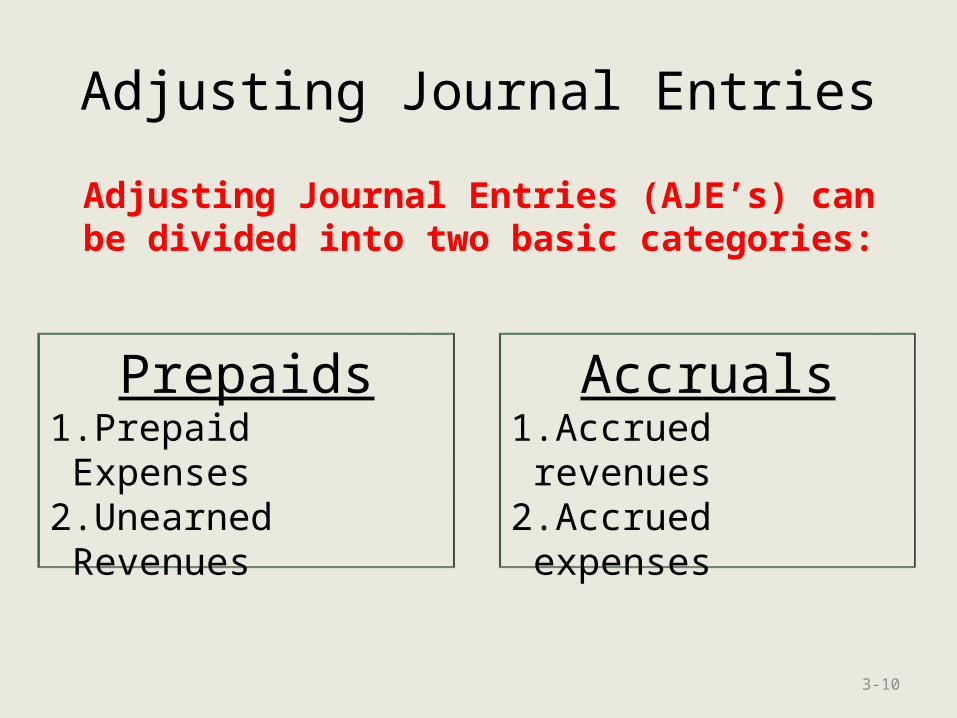

Adjusting Journal Entries (AJE’s) can be divided into two basic categories:

3-10

Prepaids1.Prepaid Expenses2.Unearned Revenues

Accruals1.Accrued revenues2.Accrued expenses

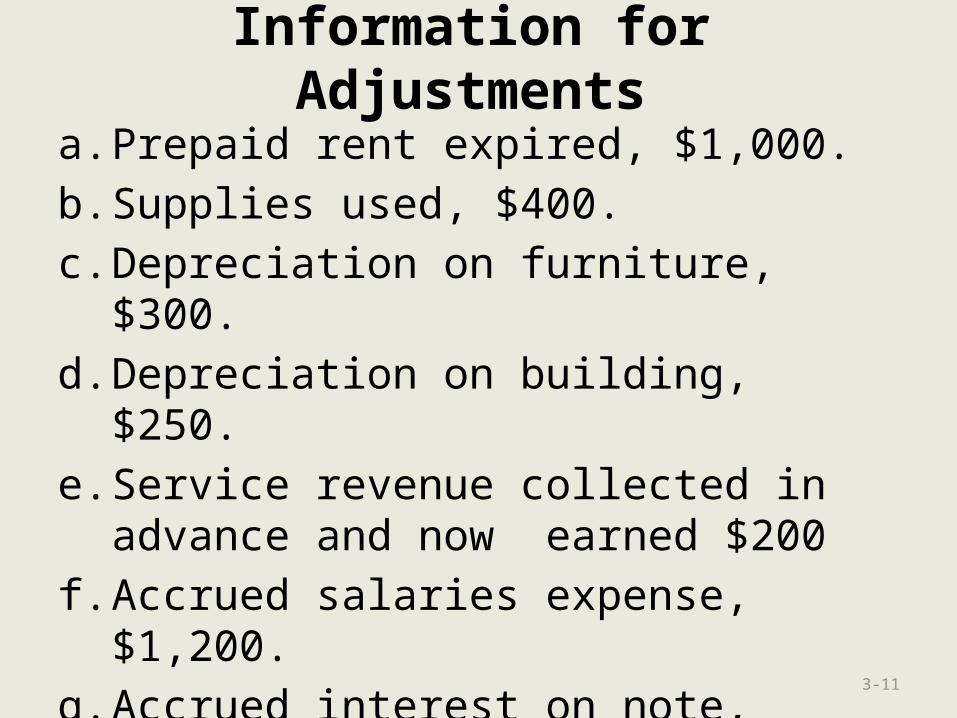

Information for Adjustments

a. Prepaid rent expired, $1,000.

b. Supplies used, $400.

c. Depreciation on furniture, $300.

d. Depreciation on building, $250.

e. Service revenue collected in advance and now earned $200

f. Accrued salaries expense, $1,200.

g. Accrued interest on note, $100.

h. Accrued service revenue, $800.

3-11

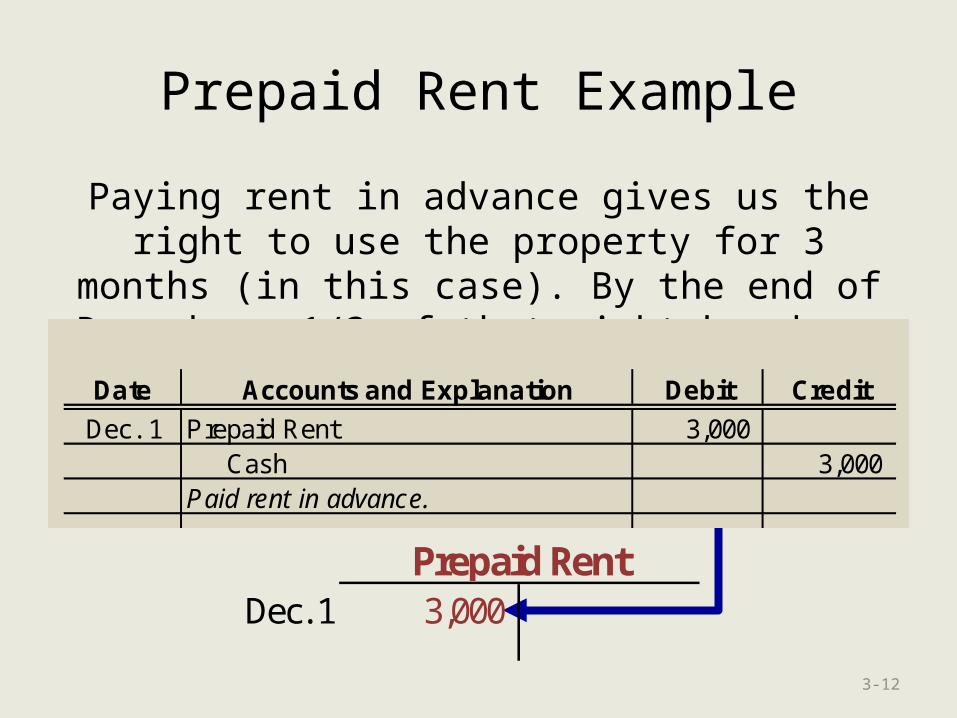

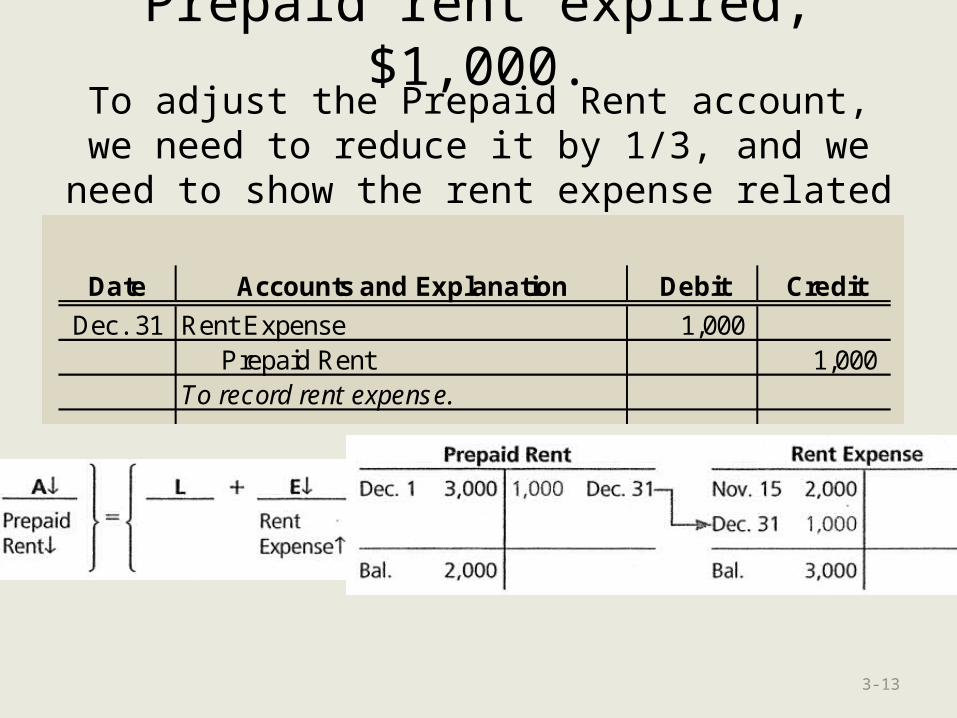

Prepaid Rent Example

Paying rent in advance gives us the right to use the property for 3 months (in this case). By the end

of December, 1/3 of that right has been used.

3-12

Date Accounts and Explanation Debit Credit

Dec. 1 Prepaid Rent 3,000 Cash 3,000 Paid rent in advance.

Dec. 1 3,000 Prepaid Rent

Prepaid rent expired, $1,000.To adjust the Prepaid Rent account, we need to reduce it by 1/3, and we need to show the rent expense related to the December revenues.

3-13

Date Accounts and Explanation Debit Credit

Dec. 31 Rent Expense 1,000 Prepaid Rent 1,000 To record rent expense.

Supplies used, $400.

3-14

Depreciation

• Long-lived, tangible assets used to generate revenue are referred to as plant assets.

• Plant assets act like Prepaid Expenses

3-15

Paid for when

acquiredUsed to produce revenues

Used up over time

Depreciation

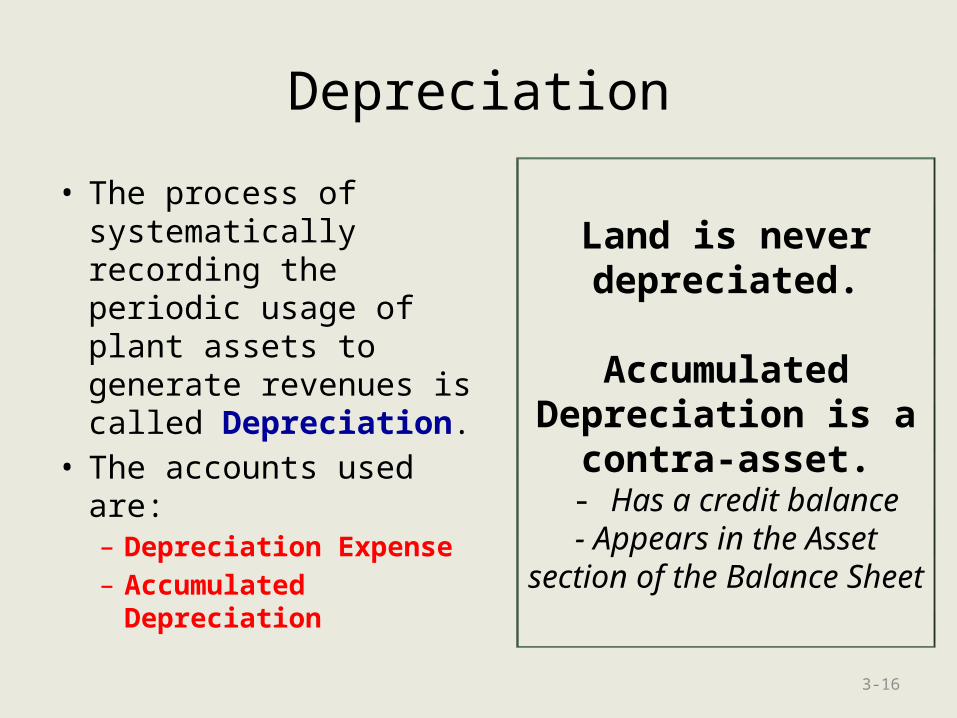

• The process of systematically recording the periodic usage of plant assets to generate revenues is called Depreciation.

• The accounts used are:– Depreciation Expense– Accumulated

Depreciation

3-16

Land is never depreciated.

Accumulated Depreciation is a

contra-asset. - Has a credit balance- Appears in the Asset section of the Balance

Sheet

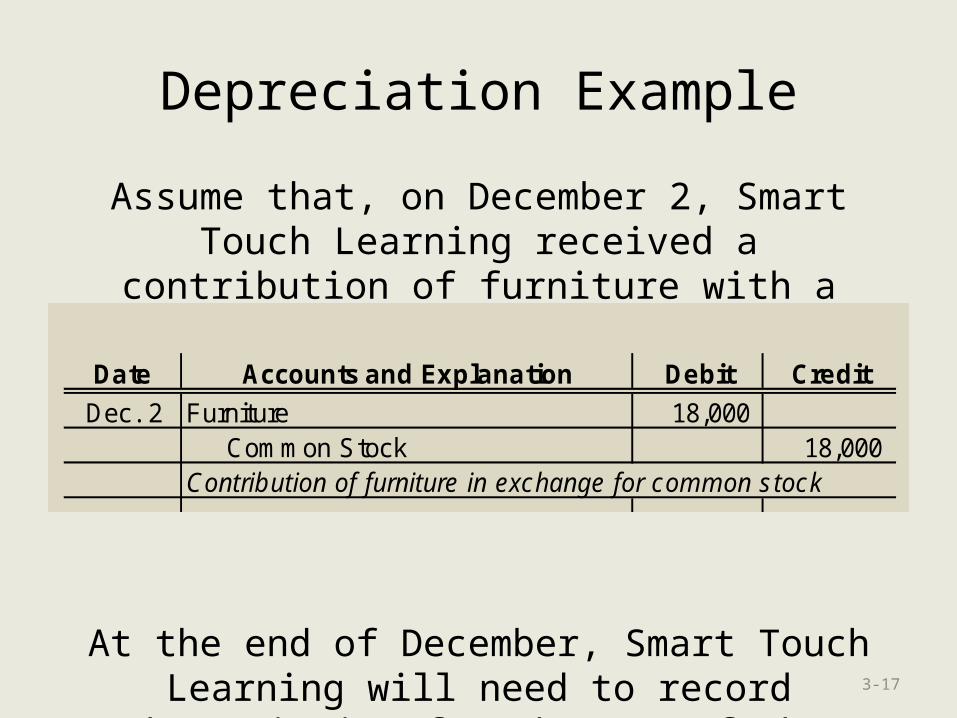

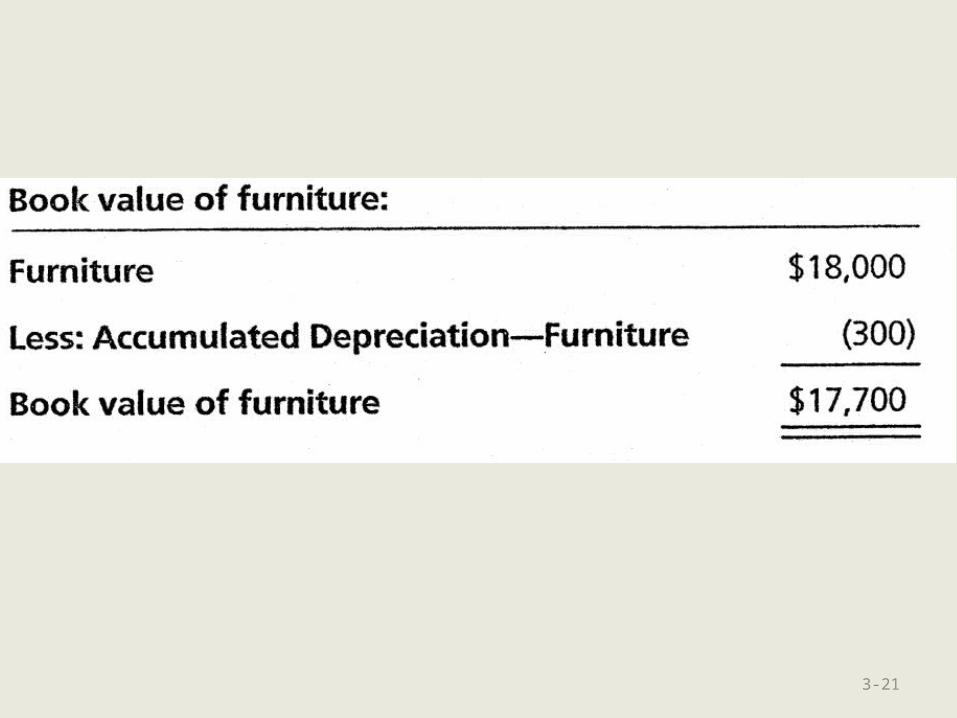

Depreciation Example

Assume that, on December 2, Smart Touch Learning received a contribution of furniture with a

market value of $18,000 from a stockholder.

At the end of December, Smart Touch Learning will need to record depreciation for the use of the furniture, assuming it has a 5 year useful life.

3-17

Date Accounts and Explanation Debit Credit

Dec. 2 Furniture 18,000 Common Stock 18,000 Contribution of furniture in exchange for common stock

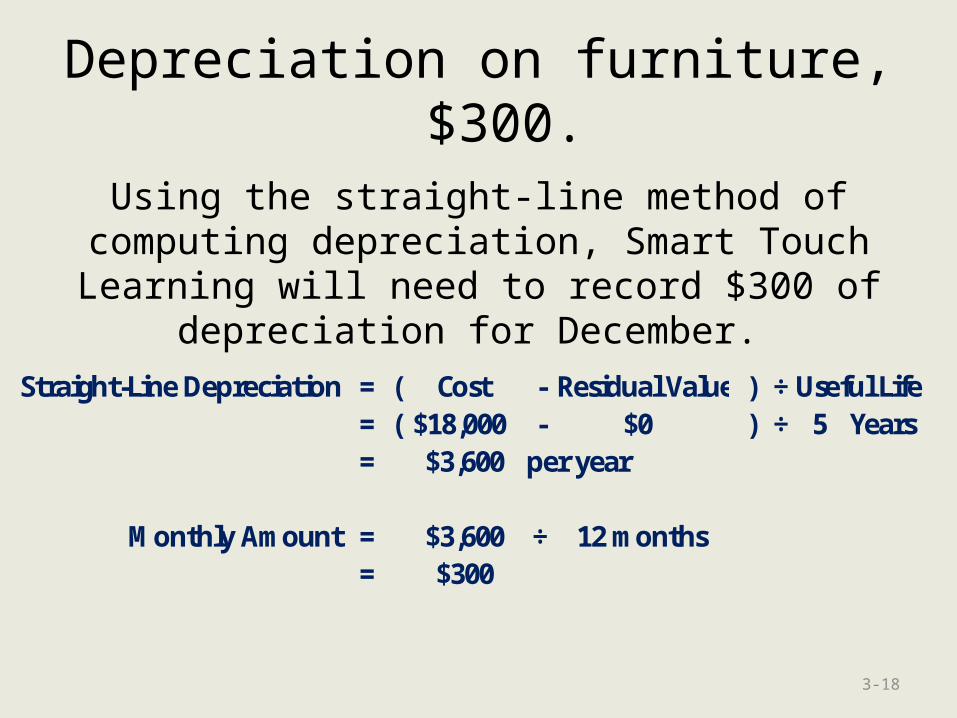

Depreciation on furniture, $300.

Using the straight-line method of computing depreciation, Smart Touch Learning will need to

record $300 of depreciation for December.

3-18

Straight-Line Depreciation = ( Cost - Residual Value ) ÷ Useful Life = ( $18,000 - $0 ) ÷ 5 Years = $3,600 per year

Monthly Amount = $3,600 ÷ 12 months = $300

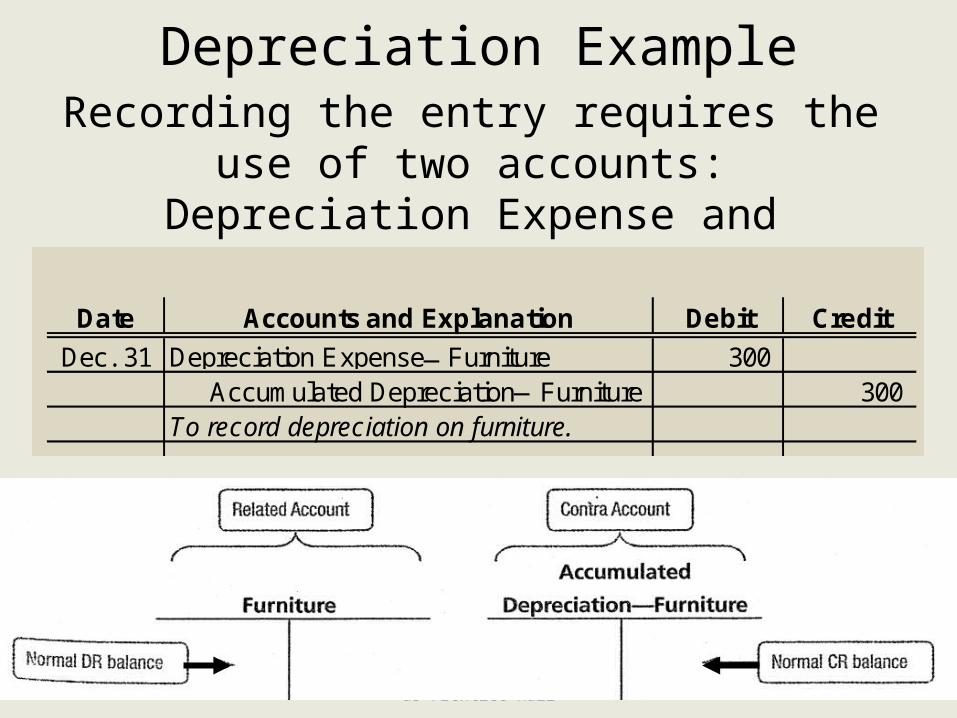

Depreciation ExampleRecording the entry requires the use of two

accounts: Depreciation Expense and Accumulated Depreciation.

3-19Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

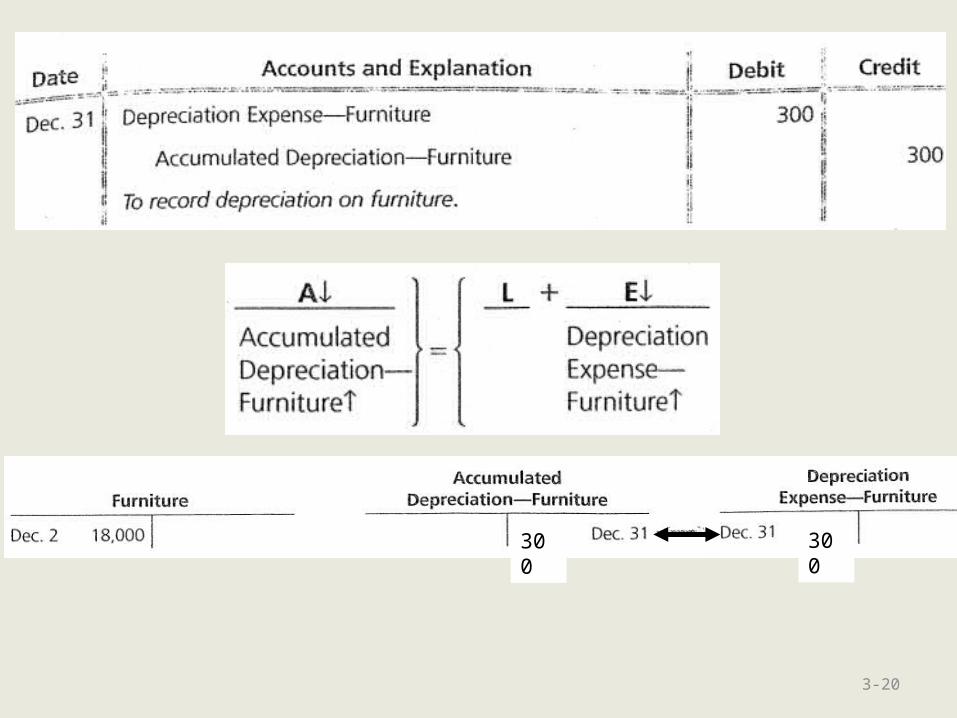

Date Accounts and Explanation Debit Credit

Dec. 31 Depreciation Expense—Furniture 300 Accumulated Depreciation—Furniture 300 To record depreciation on furniture.

3-20

300 300

3-21

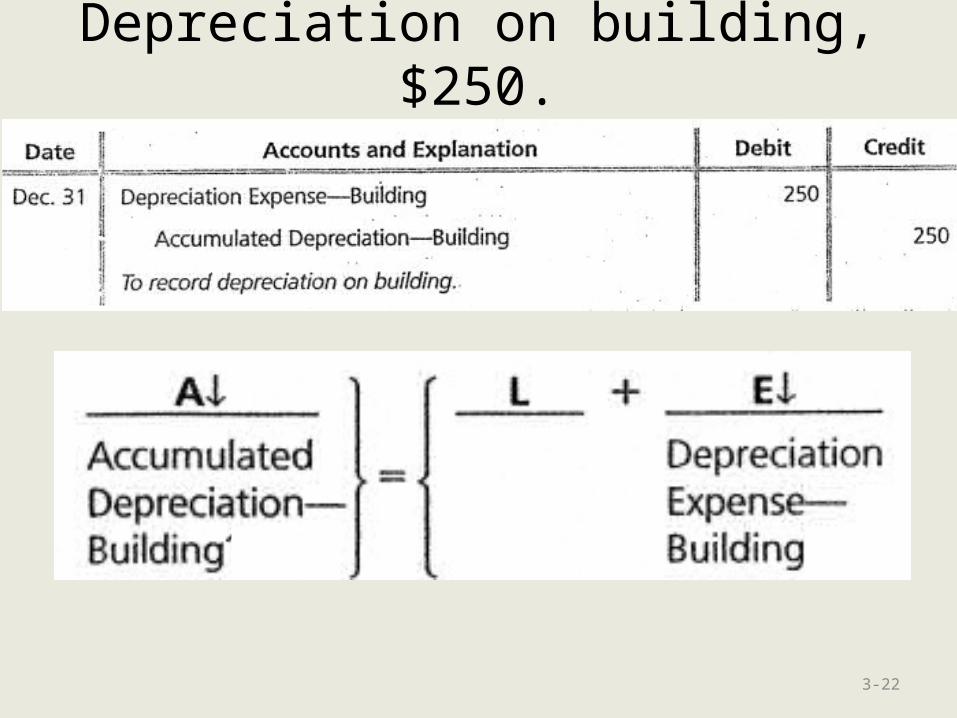

Depreciation on building, $250.

3-22

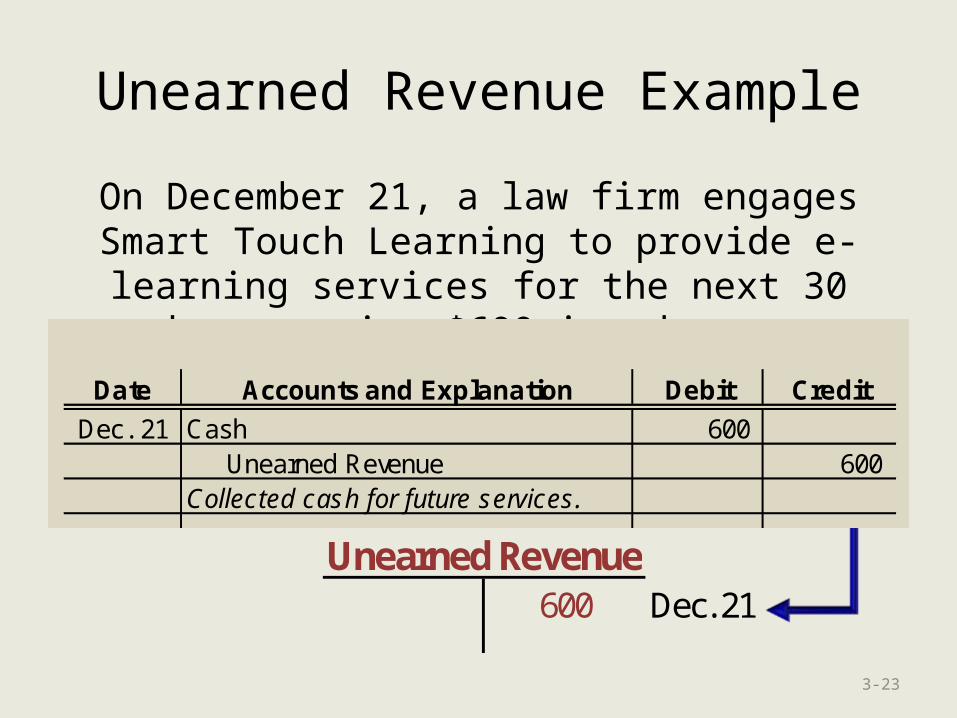

Unearned Revenue Example

On December 21, a law firm engages Smart Touch Learning to provide e-learning services for the next

30 days, paying $600 in advance.

3-23

Date Accounts and Explanation Debit Credit

Dec. 21 Cash 600 Unearned Revenue 600 Collected cash for future services.

600 Dec. 21Unearned Revenue

Date Accounts and Explanation Debit Credit

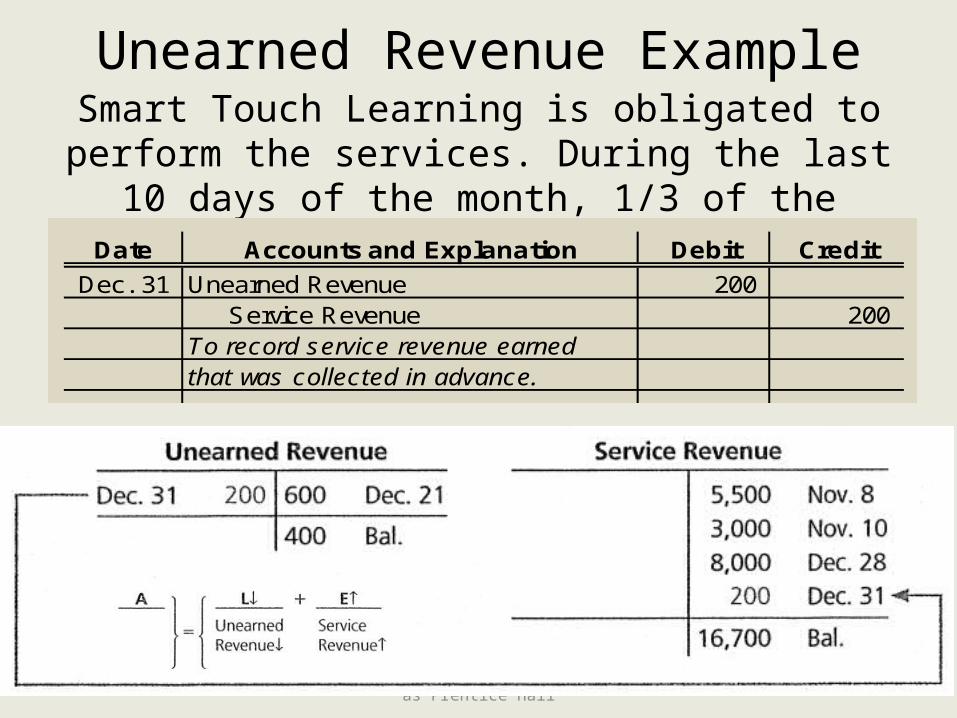

Dec. 31 Unearned Revenue 200 Service Revenue 200 To record service revenue earned that was collected in advance.

Unearned Revenue ExampleSmart Touch Learning is obligated to perform the

services. During the last 10 days of the month, 1/3 of the services are performed.

3-24Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

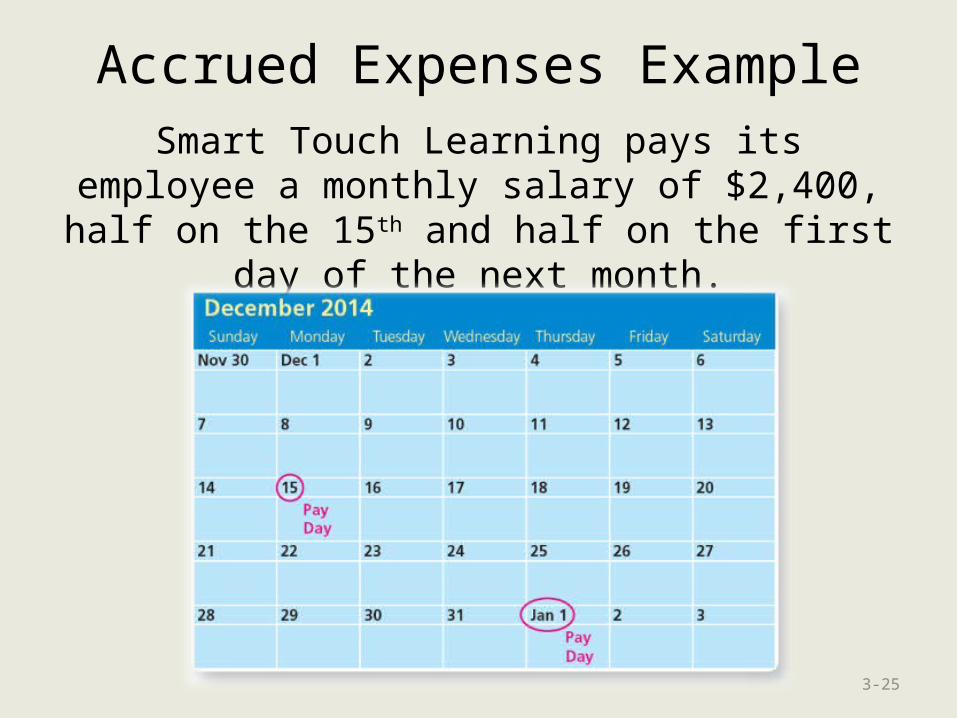

Accrued Expenses ExampleSmart Touch Learning pays its employee a

monthly salary of $2,400, half on the 15th and half on the first day of the next month.

3-25

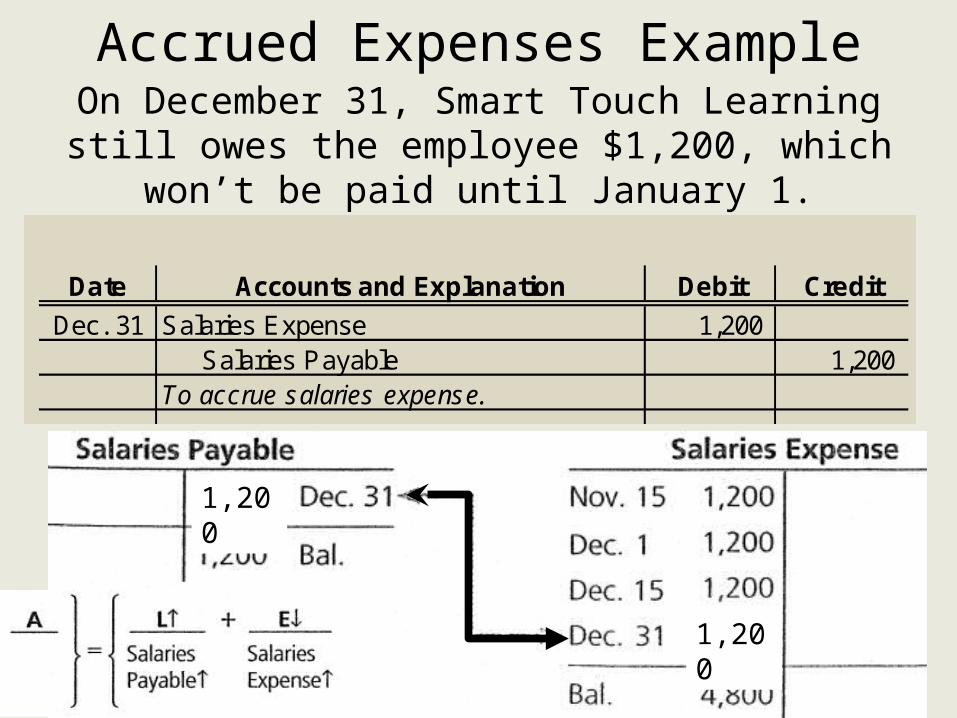

Accrued Expenses ExampleOn December 31, Smart Touch Learning still owes

the employee $1,200, which won’t be paid until January 1.

3-26Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

Date Accounts and Explanation Debit Credit

Dec. 31 Salaries Expense 1,200 Salaries Payable 1,200 To accrue salaries expense.

1,200

1,200

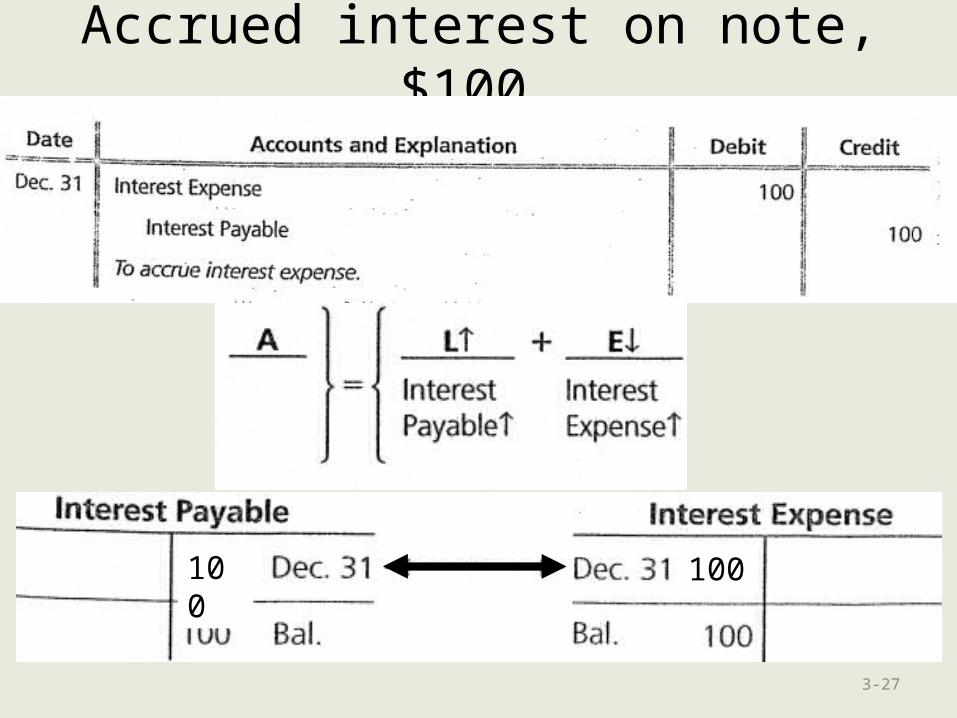

Accrued interest on note, $100.

3-27

100 100

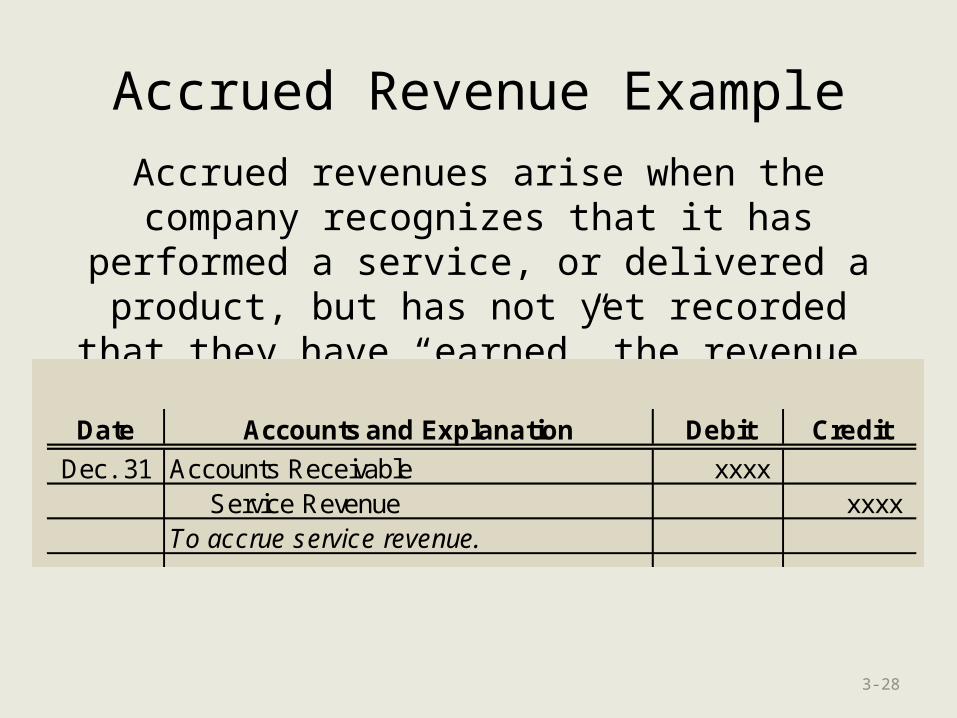

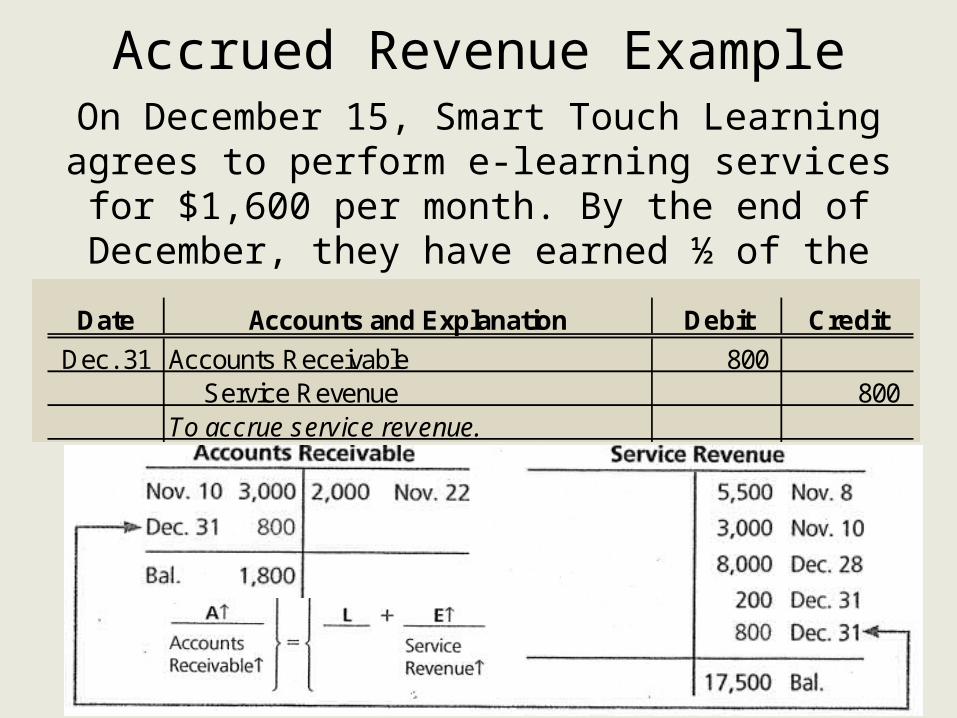

Accrued Revenue Example

Accrued revenues arise when the company recognizes that it has performed a service, or

delivered a product, but has not yet recorded that they have “earned” the revenue.

3-28

Date Accounts and Explanation Debit Credit

Dec. 31 Accounts Receivable xxxx Service Revenue xxxxTo accrue service revenue.

Accrued Revenue ExampleOn December 15, Smart Touch Learning agrees to perform e-learning services for $1,600 per month. By the end of December, they have earned ½ of

the monthly fee for December.

3-29Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

Date Accounts and Explanation Debit Credit

Dec. 31 Accounts Receivable 800 Service Revenue 800 To accrue service revenue.

3-30©2014 Pearson Education, Inc. Publishing as Prentice Hall

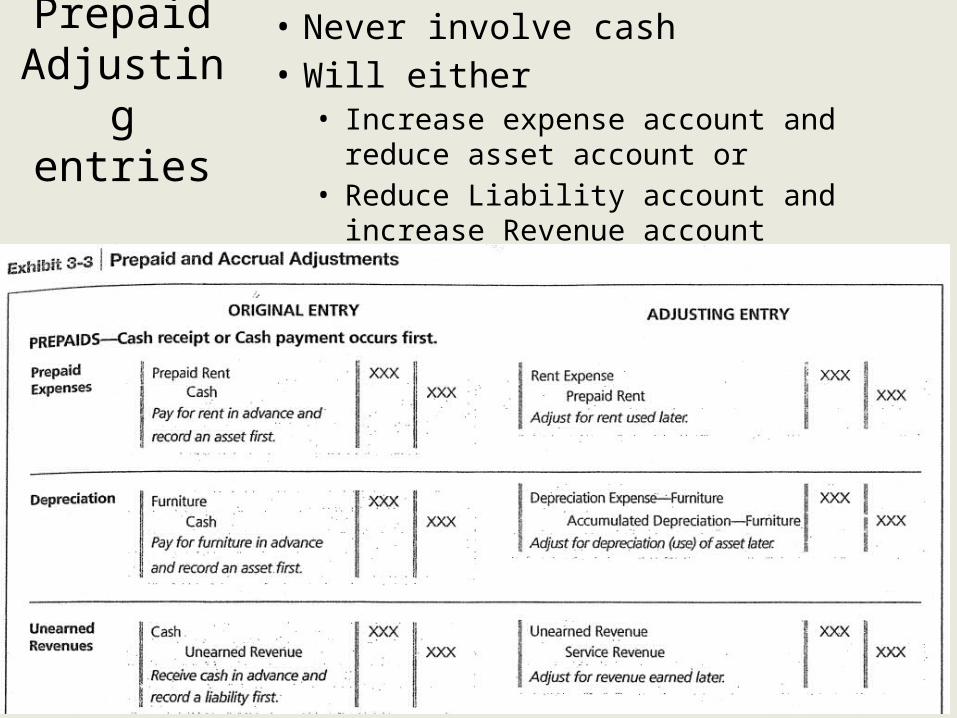

Prepaid Adjusting

entries

• Never involve cash• Will either

• Increase expense account and reduce asset account or

• Reduce Liability account and increase Revenue account

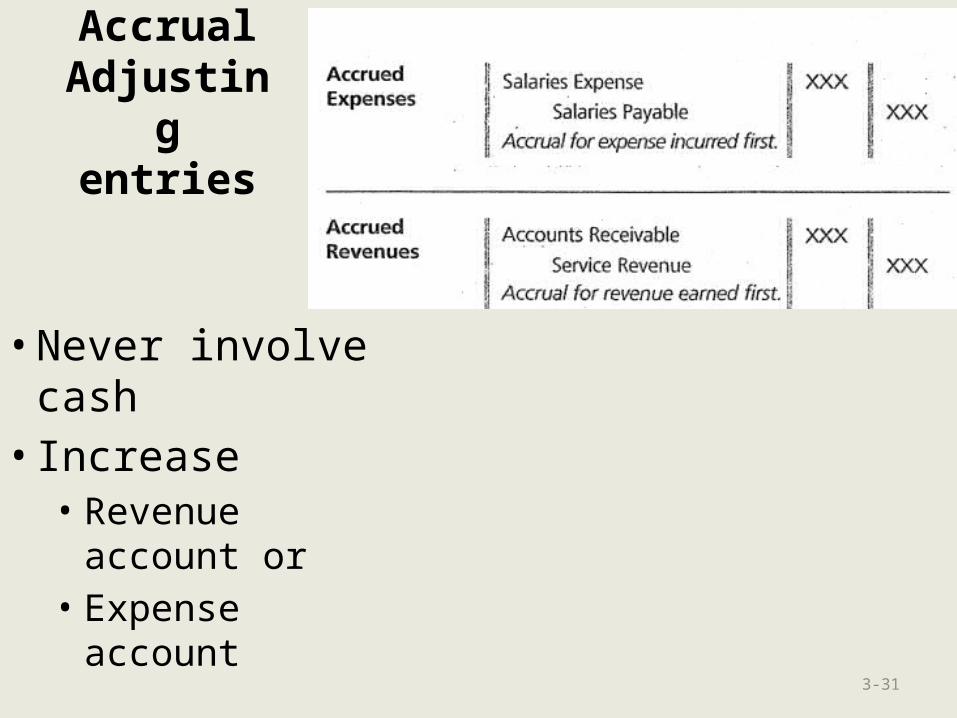

Accrual Adjusting

entries

• Never involve cash• Increase

• Revenue account or

• Expense account

3-31

3-32©2014 Pearson Education, Inc. Publishing as Prentice Hall

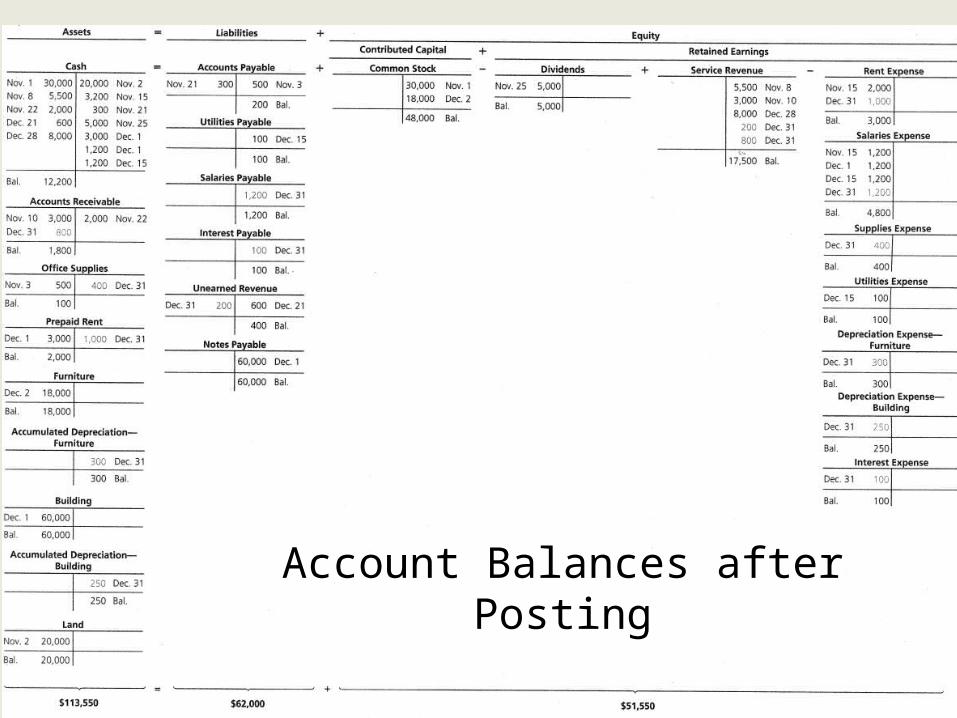

Account Balances after Posting

The Adjusted Trial Balance

• After journalizing and posting all the adjusting journal entries at the end of the fiscal period, a new adjusted trial balance is prepared.– List all accounts– List debit balances in the debit column– List credit balance in the credit column

• If it balances, financial statements can be prepared.

3-33Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

• The adjusted trial balance includes accounts that did not appear on the original unadjusted trial balance.

• The financial statements are prepared directly from the adjusted trial balance.

3-34Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

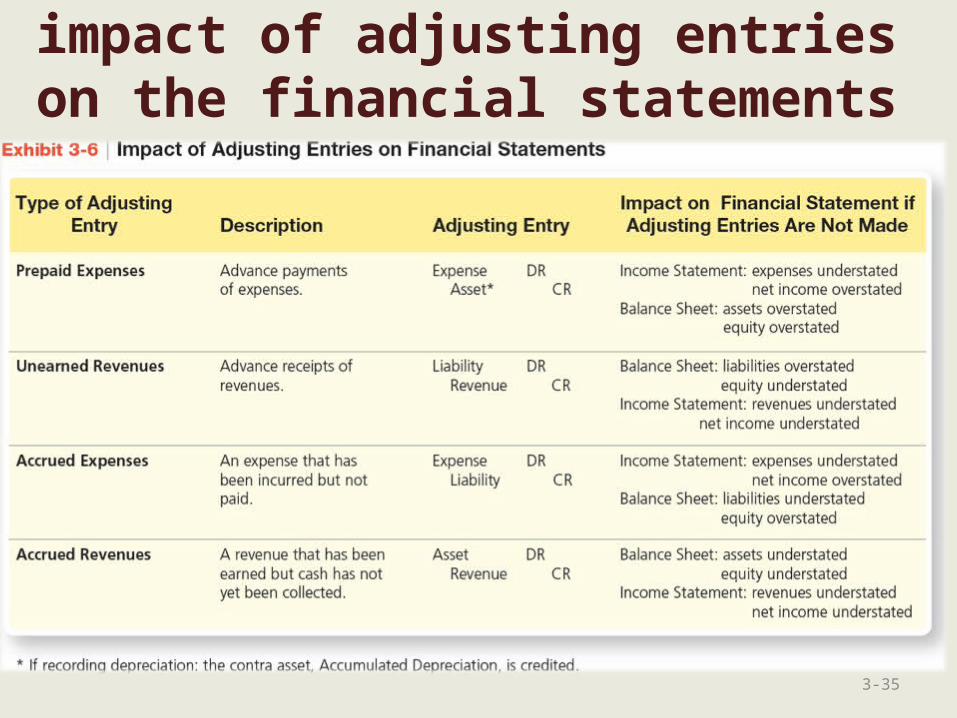

impact of adjusting entries on the financial statements

3-35

Purpose of a worksheet

3-36

• Useful tool for the adjusting process• Typically done on a spreadsheet• Lists

– Accounts– Unadjusted balances– Adjustments– Adjusted balance

3-37

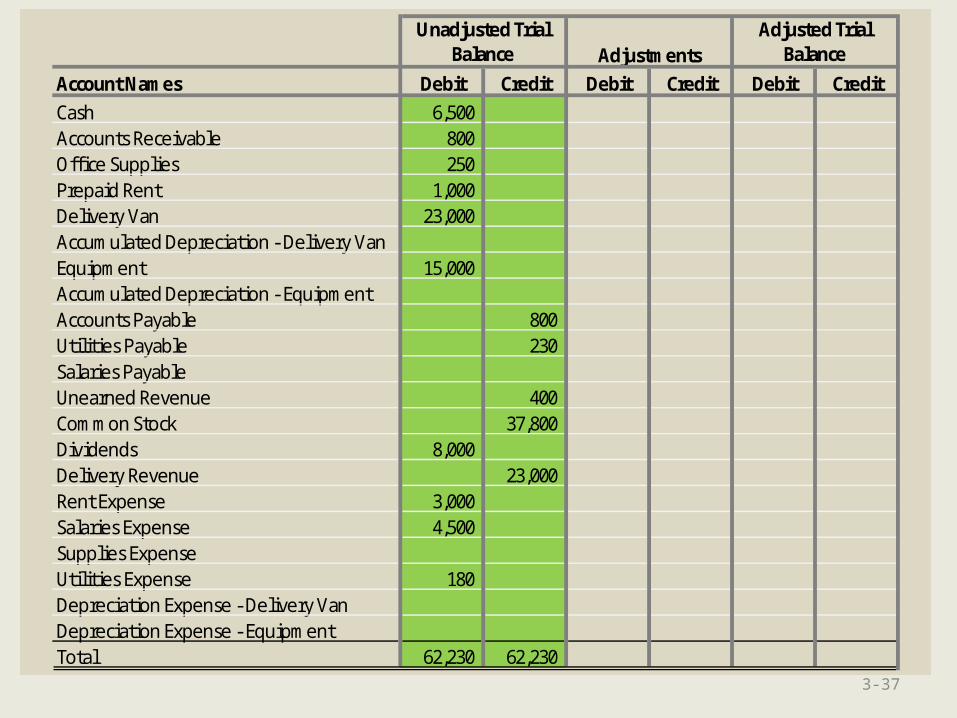

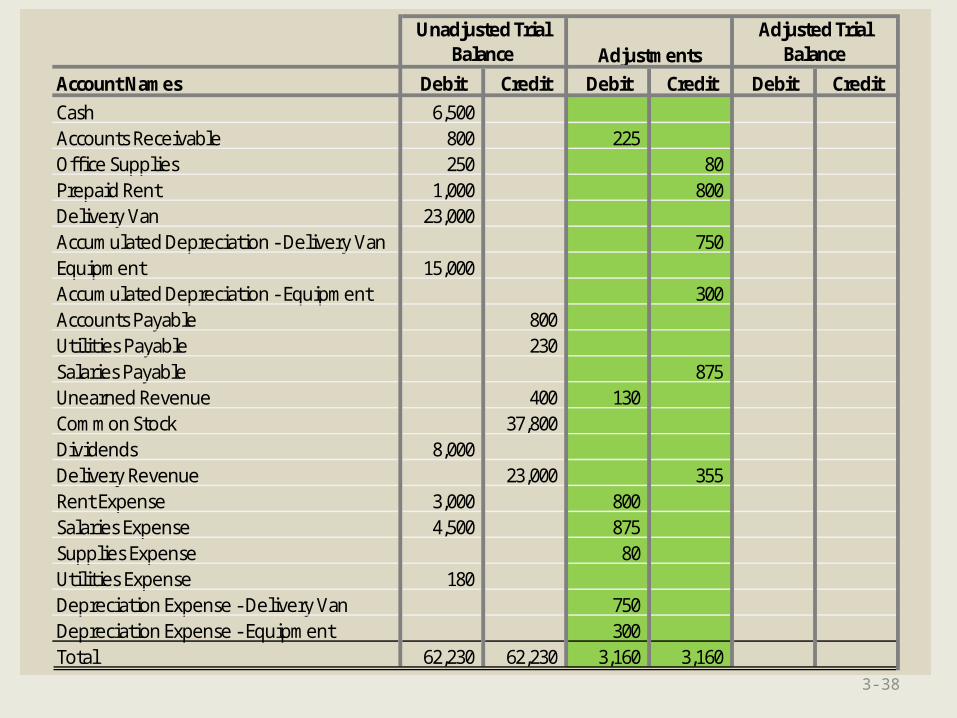

Account Names Debit Credit Debit Credit Debit CreditCash 6,500 Accounts Receivable 800 Offi ce Supplies 250 Prepaid Rent 1,000 Delivery Van 23,000 Accumulated Depreciation - Delivery VanEquipment 15,000 Accumulated Depreciation - EquipmentAccounts Payable 800 Utilities Payable 230 Salaries PayableUnearned Revenue 400 Common Stock 37,800 Dividends 8,000 Delivery Revenue 23,000 Rent Expense 3,000 Salaries Expense 4,500 Supplies ExpenseUtilities Expense 180 Depreciation Expense - Delivery VanDepreciation Expense - EquipmentTotal 62,230 62,230

Unadjusted Trial Balance Adjustments

Adjusted Trial Balance

First, enter the information from the unadjusted

trial balance into the first two

columns of the worksheet.

3-38

Account Names Debit Credit Debit Credit Debit CreditCash 6,500 Accounts Receivable 800 225 Offi ce Supplies 250 80 Prepaid Rent 1,000 800 Delivery Van 23,000 Accumulated Depreciation - Delivery Van 750 Equipment 15,000 Accumulated Depreciation - Equipment 300 Accounts Payable 800 Utilities Payable 230 Salaries Payable 875 Unearned Revenue 400 130 Common Stock 37,800 Dividends 8,000 Delivery Revenue 23,000 355 Rent Expense 3,000 800 Salaries Expense 4,500 875 Supplies Expense 80 Utilities Expense 180 Depreciation Expense - Delivery Van 750 Depreciation Expense - Equipment 300 Total 62,230 62,230 3,160 3,160

Unadjusted Trial Balance Adjustments

Adjusted Trial Balance

Second, enter the information

for the adjusting journal entries

into the Adjustments

columns.

3-39

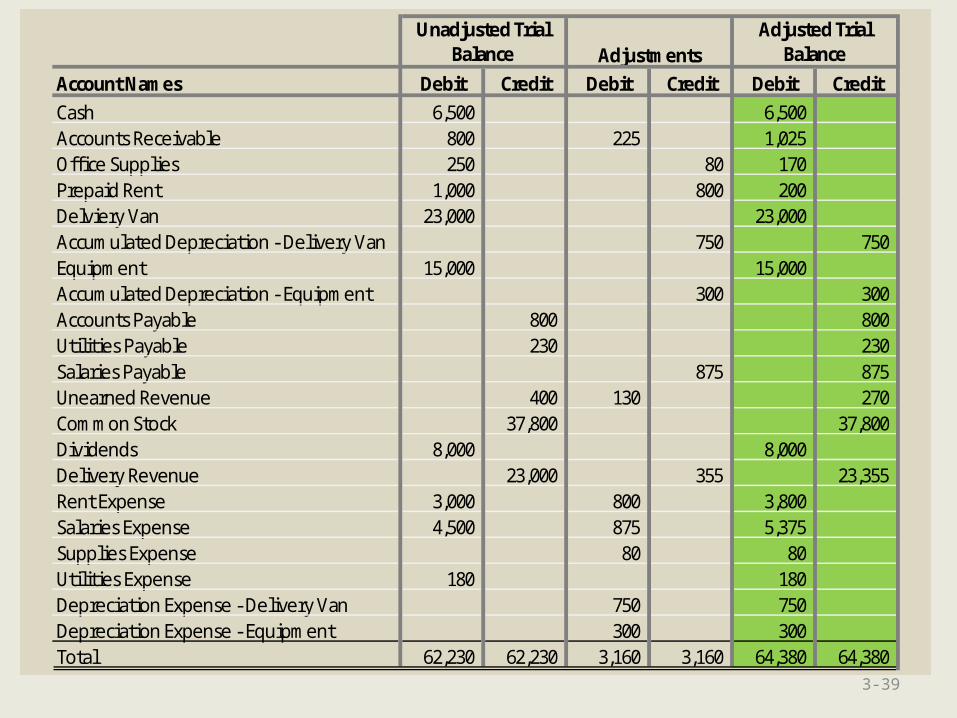

Account Names Debit Credit Debit Credit Debit CreditCash 6,500 6,500 Accounts Receivable 800 225 1,025 Offi ce Supplies 250 80 170 Prepaid Rent 1,000 800 200 Delviery Van 23,000 23,000 Accumulated Depreciation - Delivery Van 750 750 Equipment 15,000 15,000 Accumulated Depreciation - Equipment 300 300 Accounts Payable 800 800 Utilities Payable 230 230 Salaries Payable 875 875 Unearned Revenue 400 130 270 Common Stock 37,800 37,800 Dividends 8,000 8,000 Delivery Revenue 23,000 355 23,355 Rent Expense 3,000 800 3,800 Salaries Expense 4,500 875 5,375 Supplies Expense 80 80 Utilities Expense 180 180 Depreciation Expense - Delivery Van 750 750 Depreciation Expense - Equipment 300 300 Total 62,230 62,230 3,160 3,160 64,380 64,380

Unadjusted Trial Balance Adjustments

Adjusted Trial Balance

Third, cross-foot the numbers across the

spreadsheet to the Adjusted Trial Balance

columns.