*$tgl{ sla :rq - kvic.org.inkvic.org.in/kvicres/update/khadi/khadi isec report.pdf · irla road....

TRANSCRIPT

#-M* *$tgl"{ i e# Sla ls'{

Ilv Special MessengerF. No.6(2)tCACl2016Governnrent of IndiaMinistry o1'Finance

Departrrent of E-rpend itr-r re

O1'flce of Chief Aclviscr Cost,<x*>1<x

2"'l Floor. 'C' Wing. t.ok Na1,'ak Bharvan.Khan Market. Nerv Delhi-l 10003

Dated: 2"d February. 2018

To, /

Shri B. H. Anil Kumar,IASJoint Secretary,Ministry of Micro, Small & Medium Enterprises,Room No. 171, Udyog Bhawan,Nerv Delhi-110011.

) r o-\u!" '

Subject: Proposal for conducting a study to ascertain an appropriate working capitalformula for Interest Subsidy Eligibility Certificate (ISEC) Scheme for Khadi &Polyvastra programme of KVIC-reg.

Sir.

Ref'erence is invited to your D.O. No. G.-2701710112016-l(VI dateci 23"r June. 2016

reqLresting this Olfice to conduct a str"rdy regarding working capital formula lor Interest SubsidyEligibility Certillcate (ISEC) Scherne for Khadi & Poll,vastra Programme o1'KVIC. Enclosedplease frrld this OfTlce Report No. 8632 dated 2"d February,20l8 on the sLrbject fbr firrthernecessary action in the matter.

:rq

Encl. as above

, rrl)frS.l L@- >

^ azlJ I ---.'6\ 6tx*4-16W(.-rn *

t-

$E

t"\,*.."---$"l $t{ffi& urfrrcrfr /Cmef ExecdivA$sjgC h i e f A d v i s e r ( C o sr )

011-24618913

'n Cop)' to: Chief Executive Officer. Khadi and Village Industries Commission (KVIC).'Ciramodal'a' 3. IRLA Road. Vile Parle (West), Mumbai, Maharashtr"a - 400056, rvith a c,opy ofilrc leport lor rreccssarr actiorr.

Yours faithfull

-/ tr)

P.K. Aggarnal)

T fi {tilrir ,;,;ln,tltrrl"t

t:

s,'

$'t\'t

a;,Ir

5t

CONFIDENTIALF. No. 6(2)tCACl2016

Report No. 8632

${}

ss,

*,*

$$$oJi)nsn)

*:J

st

'a.

dde$*

'*dd*'.-

Study on Working Capital Formulaunder Interest Subsidy Eligibility certificate scheme of

Khadi and Village Industries Commission

Ministry of FinanceDepartment of ExpenditureOffice of Chief Adviser Cost

February 2018

t'

ut

-'t

ti

t; Contents

'#

s.sre

ssssBB

s*

ry

3

3

sry

q

h

?

E

3

tI

9

t,

l.

Cirapter'- I lntroductionI

111.1 Background1

i1.2 Ieuns of Refbrence

I .-1 Study Metlioclology I

Chapter- 2 Interest S u bsidy Eli gibility Certiflcate Schenie aJ

2.1 Overview of KVIC J2.2 Interest Subsidy Eligibility Certificate Sche,ne gtSfC;

Backgrouud-)

!..J KVIC',s guidelines regarding fixation tf tffia-sales

I

2.4 ;ireme"t "f

w".ilr,tCapital

6

2.5 Recommendations of Other Comniittees 7

82.6 Guidelines being observed t y t unt

unitsChapter- 3 Analysis of Working Capital Requirement t2

3.1 Assessment of Working Capitil by KVIC 12

Operating Cycle and Cash Cycle3.215

G18

r8

J.J Analysis of Profitability and Liquidity of KGChapter- 4 Methodology for Assessrnent of Wortiing Capital

4.1 Working Capital Assessment MethoclsA''.l.z- Actual operati,g cycle (based onffi 18

194.3 Comparison of Assessed Working @

Operating Cycle)Chapter- 5 Recommendations 21

215.1 Working Capital Assessment Method5.2

215.3 Inventory of Finished Goods anA CreAitors nu1,rr*r-,t 2t

n5.4 Market Devel.pment Assi stance /rnffiState Boards _

5.5 Others 22

lrI

i

:

I

tr ist of Table

List of Annexure

3/

,*r

ti{'i

{}

ur

-*

t

Y

'5

*ra

J

3€S

3s'

a.3

"a

3q

5353L,

j

3

5

'lJ

9

a

Iet

I*l

Table 1 working capital amouni approved by KVIC and finance sancti,r,rcdby the banks

4

Table2 Khadi Production and Saies during 2An-14 to 2015-i6 5

Table 3 KVIC's Method of Assessment of Requirement of working capr-tal 6Table 4 Banks' guidelines regarding working capital ugainri LSe- ittu.,i

by KVIC9

Table 5 consolidated Production and Sales values, working cupital ,r-,dBank Finance

12

Table 6 Assessment of Net wo'king capital for ISEC for udu,ralpetSarvodaya Sangh for 2013-14

13

TableT Opeiating Cycle for the period from 2013-t+ to ZOtS-iO i6Table 8 Profitability and Liquidity Ratio 17Table 9 Actual operating cycle (on an average) for trre period fi orl zo t :- i +

to 2016-1719

Terms of Reference

from 2013-14 to 2015-16

State wise Details of V/orking Capital Amount appr.oueA UyKVIC and Bank Finance sanctioned by the Ba,ks for the years

Statement of working capital *ss"ss.ffiAssessment of working capital cycle (in Nos. of oayg c,f rt*aiInstitutions for tle years from 2013-14 to 2015-l 6Statement of Position of profitability ancl Liq;i,lity

"f KIs 1.or-ri*

fiorn 201 3- 14 to 201 5-16.statemellt of Actual operating cycle for the vear' rrorl 2013-lato 2015-16"Statement of Comparison of Assessment of Working CapitatRequirement for the years from 2013-14 to 2015-16.

I

I

i

II

."1

Annexure-1 't.t

Annexure-2 26

Annexure-3 27

Annexure-4 28

Annexure-5 2q

Annexure-6 30

Annexure-731

t]a'

tii! Abbreviation

Ir A!VI'rT Artisan Wellare Fund TlustCIBC Consortiurn Bank Credit

\3 CtlA Core Current Assets

:"r CGTMSE Credit Guarantee Fund Tlust for Micro and Small Enterprises

;* CSPs Central Slivel Plants''l iSEC Inreresr Subsidy Eligibility Certificate

e KIs Khadi Institutions,:,* KRDP Khadi Reform and Development programme? r o -'-------

KVIBs State Khadi and Village Industries BoardsY KVIC Khacii and Village Industries Commission

S MBPF Maximum Pemrissible Bank Finance

,- MMDA Moditled Market Development Assistance5 MSE Micro and Small EnterprisesI MSME Mi,istry of Micro, Small and Mediurr Enterprises

S OCL Other Curent LiabilitiesPMEGP Flime Minister's Employment Generation Programme

'* RBI Reserve Bank of India.q REGP Rural Employment Generation programme

SFC Standing Finance CommitteeS SITURTI Scheme of Fr-urd fbr Regeneration of Traditional Industries-:1 SLBT State Level Budget Team

- TCA Total Current Assets, ,.... -: .' VIs Village Industries

*9

a.

I

1r

l

:

I

l

I

.,rl

I

II

1V

*9

,q

"5

i93335;)

sI933

\r*;

{itt1!,

rt3a;*17

's

3

:ry

53-l

.:)

€

1

5Iq9I55e335p

I5

3

3

3

Chapter - 1

lntroduction

I.1. Background

1.1'f i\{inistry of Micro, Smiill and Mediurn Enterprises (MSME) through Khadi a,cl VillageIndustries Clornrnission (KVIC) has been implenrerrting a Central Sector Schenre, namely, InterestSubsid"v Eligibility Cerlificate (ISEC) Scheme since lg77-78 for institutiolal financing of theKhadi ancl Village Industries programme. Under the ISEC Scheme, the woriiing capital creclit isprovided to the Khadi Institutions (KIs) as per their requirement assessed by the banks. Theinstitutit'rl'ts are to bear the interest liability only at the rate of 4 percerlt per aprlu* u,lrile thedifierence betr'r'een tlre actual Iending rate and 4 percent is borne and paid by ttre Ce,tralGovernment through KVIC to the lending banks and the funcls for this purpose are proviclecl unclerthe'Khadi Granr'Ilead of KVIC.

1.2. Terms of Reference

| .2.1 . KVIC vide their Ietter No. KVIC/Ec.R .lATN261-DRPSCI/Reporr/2o14- 15 clatecl18.03.2016 has requested this office for conducting a study to ascertain an appropriate rvorkipgcapital formula for Iuterest Subsidy Eligibility Certificate (ISEC) Scheme. Subsequenrly. Ministrl,of Micro, Srnalland Mediurn Enterprises has sent the study reference to this Office vide their D.0.letterNo. C.-27017104/2A16-KVI dated23.06.2016 (Annexure-l) on the same issue a,d appriseclthat KVIC has recently adopted flexible pricing policy by which Khadi Insritutions are fi-ee to addmargin over and above the production cost and therefore, they can sustain their activity to theextent of 10A% of their turnover under this scenario. KVIC's existing method of assessment ol.higher working capital than the production cost for which banks are reluctant to provicle workingcapital to Khadi Institutions as per ISEC issued. Banks normally aclopt Naik Conrmitteerecotnmendations for assesstnent of rvorking capital to provide financial suppofi to Igs.

1.3. Study Methodology

I'3.1. This Office has already conducted a study and subnritteci its repolt on the issue vicle ReportNo. 8349 of January, 201 3 vide this Office's letter No. F.No. 6(4)lCAC:2Ol I dated 24.01 .2013.During discussion with the ofllcials of KVIC, it has been informed that no action has bee, takerron the recommendations made in that report. However, ttris Office has accepted fi.esh referencesent by MSME vide their D.O. letter No.G.-270 1710412016-KVI dated 23.06.2016.

1.3.2. The methodology adopted for this str,rdy includes issuance of questionnaire for datacoliection lrom (i) KVIC, (ii) KIs, (iii) Reserve Bank of Inclia, and (iv) Bapl<s ipvol'ed i*disbursing the working capital loans to Khadi sector based on ISEC issuecl bv KVIC: visit and

,, 1i,

{;

{i

tltil

rk

\

E

3:*"\

$3"td.-f

*

3:AB

3s55"d?

5.{{

ssdU,

a3'*

5:3,3-{--.

'*1

discussion hetd by Officers of this Ofirce rvith few Kls around.laipur/ Daltsa (before issltance oi'

questiopnaire), study of literature, discussion rvith KVIC Officers, data analysis and interpt'etatiotr

anci firrally made recorlrnendations. In the instant case, questionnaire rvas issued on 31.10.2016

vide tiris Office letter No F.No. 6(2)/CAC/2016 dated 3 1 . 10.201 6.

1.3.3" KVIC subrnitted partial and incomplete data to this Office in response to the questiottttaire

vide their letrer No. DK (BF)/ISEC Study W.C./REC/Varanasi/2016-17 dated 1510312017.

Subsequently, this Office issued reminder seeking complete data/infbrmation alorrg rr ith

arjditional data/information pertaining to Cotton Khadi, Muslin Khadi, Silk Khadi, Woolen Khadi

and Polyvastra like (i) annual buclget guidelines of KVIC, (ii) calculation of rvorliing capital as

per KVIC's metlrod, (iii) Working Capital Cycle: (iv) cost of production/sale; (v) financial clata,

inrespectofatleast5l(lsofeachcategory('A+',A,B,C &'D' category)assamplefortheyear

2013-14,2014-15, 2015-16 r,vitli annual financial accounts vide this Office letter No F.No.

6(2)l C ACIZO 1 6 dated 1 6.06.2017 .

1.3.4. Again KVIC submitted partial data/inficrmation to this Offrce vide their letter: No.DK

(BFyISEC Study W.C./2017-181274 dared 04.08.2017 against this Olfrce reminder letter F.hio.

6(2)lCACl20l6 dated 16.06.2017. Subsequently this Office held discussions with the Officials ol'

KVIC during their visit to this office on 05.09.2017 and 06.09.2A I 7 on the issues pertaining to this

study and requested to submit complete information.

i.3.5. This Olfice also issued second and third reminder letters No.F.No.6 (z)lcA,Clz}l6 dated

07.A9.2A17 and 12.10.2017 respectively requesting KVIC to furnish complete data artd

information. KVIC submitted partial data vide their letter No.DK/(BFIISEC StLrdy W.C..lZAl7-

l8/339 dated 12.09.2A17 under intimation to MSME. KVIC has submitted balance data a'long r,vith

annual financial accounts in respect of 20 KIs vide their letter No.DK/(BFyISEC Str-rcl1,

W.C./2017-181418 dated 17.10.2017 (received on 24.10.2017) regarding 18 KIs locatecl in

Chennai Region (12 KIs) and Kolkata Regiorr (6 KIs) under category of 'A.|', A, B and C tbr the

year2Al3-14,2.014-15 and 2015-16. Data related to Jaipur: Region was subrnitted vide letter No.

DK(BFyISEC Study W.C.12017-181431 dated 25.10.2017 regarding 2 KIs. KVIC has aiso

infornred that there is no sucla KIs under "D" category f,or instant case and hence no data submitted

by them in this regard. Last set of information l-ras been received by this Office an 25.10.201 7 and

subsequerrt clarifications vide e-mail dated I 1 .12.2017.

1.3.6. Based on the data and intbrmation received from various stakeholders aud tlre cliscussions

held, this Report as brought out in the subsequent chapters has been prepared. This reporl consists

of five chapters. Chapter 1 provides terms of reference and study metliodology adopted in the

study. Chapter 2 relates to Interest Subsidy Etigibility Certificate Schen,e. Chapter 3 gives anall'sis

of working capital requirement. Chapter 4 deals with methodology fbr assessntetrt ol u,orkin.q

capital. ?$gj :.ojtull]:- t.:ommendations.I

l

I

I

i

I2

\*1

{;

{j

{},

i*

'\.$,

T

Tsr

q,

*

J

53a.lo

-*

353g*t

.at/

L'

L,

d*

d*a?,

ti,

333dl

Chapter - 2

Interest Subsidy Eligibility Certificate Scheme

2.1. Overview of KVIC

2"1.l. Khadi is natural, hand crafted. ecofl'iendl),. bio-degradable and non-exploitativr:. Kha<iiactivity provided employnrent to [1.07 L.akir persons during 2015-16. The h4inistrr, of Mierro"Srnall and Medium Enterprises (N{SME). Covernrnelrt of India is prornotirrg Khadi through varigusproBrammes and schenres. Khadi and Village Industries Conrmission (KVIC) is the nodal agenc),for irnplementation of these progranrmes. Presently, Khadi programme is implemented by KVICwith the sr-rpport of 33 Statell-..r.Ts, Khadi and Village lndustries Boards (KVIBs) ancl 2313irrstitutions (157A registered rvith KVIC at'td743 registereci with KVIB ciuring 20j5-16).

2.1.2. KVIC is a statutot'y body underthe Act of Parliarrrent,viz., 'Khadi and Village IndustriesComntission Act, 1956 and under the administrative control of the MSI\48, Government of Incliawith its Head Office at Murnbai and six Zonal Offices located at New Delhi; Bhopal; Ban_ealore;Kolkata; Murnbai and Guwaltati and 36 State/Divisional Offices spreacl all over the country tofacilitate speedy implementation of KVI programmes. KVIC underlakes training and marketingactivities through its departrnental and non-departmental training centres. Marketing is taken Lrp

through its 9 departmentally-run l(hadi Gramodyog Bharvans located in urban areas ancl 7.0-50institutionallretail saies outlets Iocated at different parts of the country. KVIC also makes availablequality rar'v materiai to Khadi Institutioris through its six Central Sliver Plants (CSps) Iocatecl ar(i) lJazipur (Bihar). (2) Chitradurga (Karnataka), (3) Trichr-rr (Kerala). (4) Setrore (lv{adh1,aPradesh), (5) Rai Bareilly (Uttar Pradesh) and (6) Etah (Urtar pradesh).

2.1.3. KVIC has been irnplernenting several new and innovative schemes approved by thcGovernment of India frotn tirrre to tir,re under Khadi segment, KVIC has also implementecl

'ari.Lrsschenres/programmes for the promotion of Khadi during the year 20t5-16 namely (l) N4oclifiedMarket Development Assistance (MMDA); (2) Interest Subsidy Eligibilit5, Certificate Schenre(ISEC); (3) Workshed Scheme fbr Khadi Artisans; (4) Strerrgthening of Weak Instirutions. (5)Aarn Admi Bima Yojana (erstwhile Jana Shree Bima Yojana),and (6) Artisan Welfare Fund Trust(AWFT).

2.2. rnterest subsidy Eligibility certificate schenre (rsEC)- Background

2.2.1. The Interest Subsidy Eligibility Certificate (ISEC) Scheme is an imporlant mechanism fbrfunding khadi progratlltlle,undertaken by Khadi Institutions. It was introduced in May 1977 tomobilize funds lrorn banl<ing institutions for filling the gap betr.veen the actual fund requirementsand availability of funds from budgetary sources. Under the ISEC Scheme, credit at a concessionalrate of interest of 4 %o per annum for capital expenditure as r,vell as rvorking capital. is rnacle

t

II

1i

{r

\\

:1

-1

.ii..\

.r

i1

5_-i

]

:1

avaiiable as per the requiremeltt of tlre l(hadi Irrstitutions. The cliffcrence betu,eerr the aclr-iitl

Ierrding rate and 4Yois paid by the Central Government through KVIC to the lending bani<s. FLrncls

lor this pllrpose are provicied under the Khadi Grant Head to KVIC. The Ilstitutiops r-egisterecJ

u,ith the KVIC/ KVIB can avail of financing under the ISEC Scheme. Initially, the enrire I1VIsector was covered under the Scherrre. However, with the inrroductior-t of Rural EntploymentGeneratiot-t Programme (REGP) for village industries (V.1.) in 1995 and Prime Minister.,sEmploynent Generation Progranlme (PMEGP) in 2008, the Sc|eme now supports onlv the Khacliand the Polyvastra sector. Florvever, all village industries units existing as olt Marclr 3 l. 1995. havebeen allorved to avail this facility lor the amount of bank finance availed as on that date or actlral.whichever is less provicled they are lul11,1unc1l.nai anrl lunds forthis purpose are proviclecl Lriiclerthe V.l. grant head.

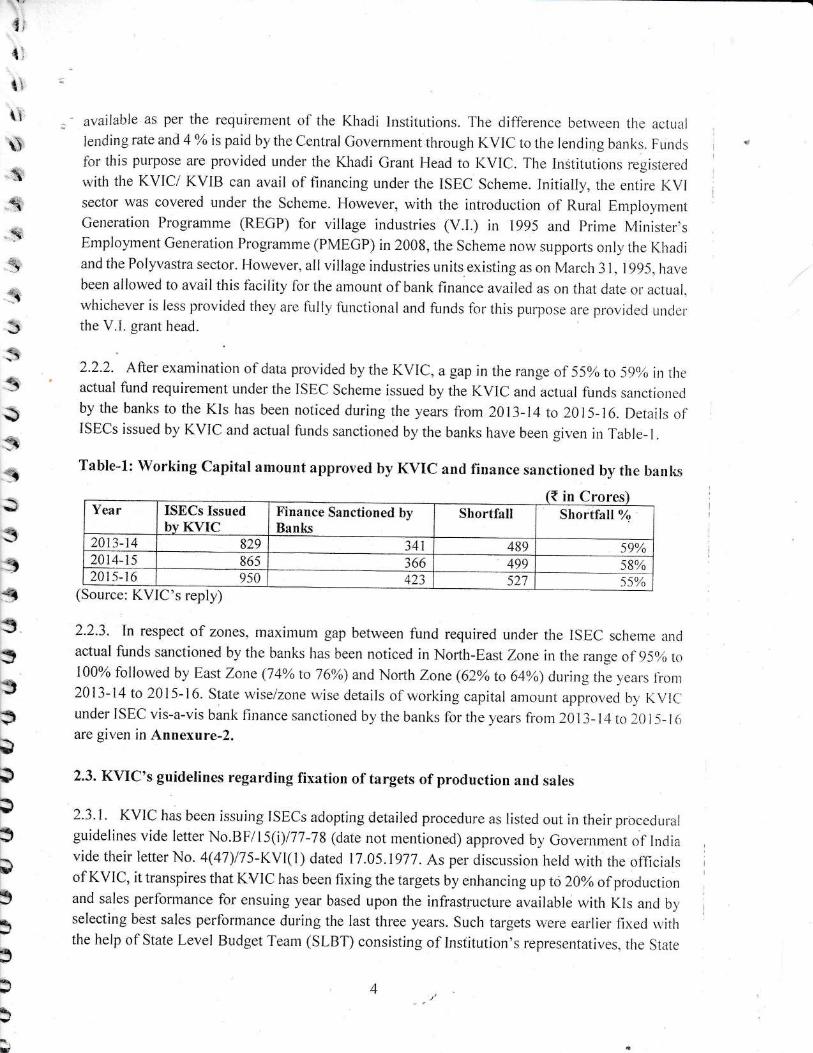

2.2.2. After examirtation of data prol'ided by the KVIC, a gap in the range of 55% to 599t, i, thcactual fund requirement utrder the ISEC Scheme issued by tlie KVIC and actual funds sancrioner-lby the banks to the KIs has been noticed during the vears fi'om 2013-14 to 2015-16. Details o1,

ISECs issued by KVIC attd actual funds sanctioned by,the banks have been gir,,en in Table-1.

Table-l: Working Capital amount approved by KVIC and finance sanctioned by the banks

{ in CroresYear ISECs Issued

bv KVICFinance Sanctioned byBanks

Shortfall Shortfall To

2013-14 829 7+t 489 59%2At4-15 865 366 499 58%20rs-16 9s0 123 527 55%

(Source: KVIC's reply)

2.2-3. In respect of zones. maximunr gap between fund required under the ISEC schenre arrcl

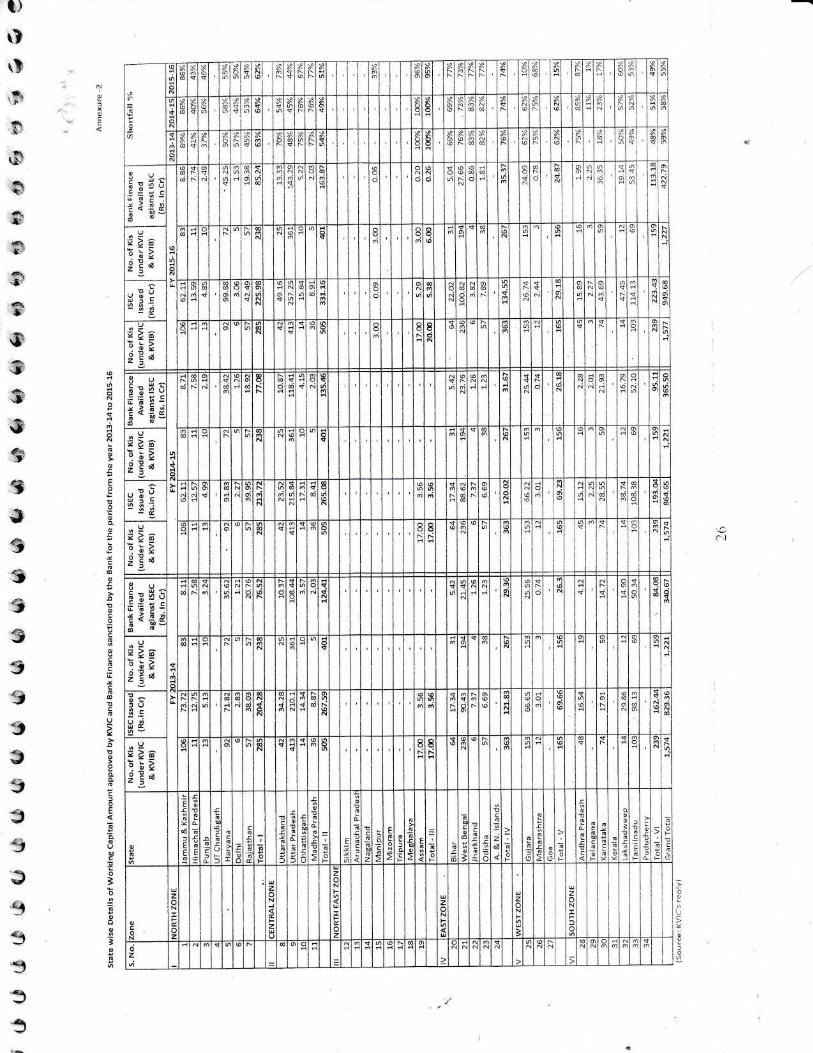

actual funds sanctioned by the banl<s has been noticed in North-East Zone i1 the range oig5ozo ro100% followed by East Zone (740/ota76%) and North Zone{620/oto 64on) clnripg t6e rears il-onr2013-14 to 2015-16. State rvise,'zoue u,ise details of rvorl<irrg capital amour.rt approved try l.,VI(under ISEC vis-a-vis bank flnance sanctiorred b,v the banks for the 1.,ears fi.gp.r 20l3-14 to l0i-\-16are given in Annexure-2.

2.3. KVIC's guidelines regarding fixation of targets of production and sales

2'3.1. KVIC has been issuilrg ISECs acloptingdetailecl procedure as Iisted out irr theirprocecluralguidelines vide letter No.BF/15(i)177-78 (date not mentionecl) approved b1, Goveltrne,t of l,cliavide tlreir letterNo. 4(47)17S-KVI(1) dated 17.05.1977. As per discussion helcl rvith the officialsof KVIC, it transpires that KVIC has been fixing the targets by enhancing up to Zloh of procjuctionand sales performance for ensuitlg year based upon the infrastructule available u,ith KIs ancl b1,

selecting best sales performance during the last three years. Such targets rvere earlier lrxecl g,it6the help of State Level Budget Team (SLBT) consisting of Institution's representatives. tlte State

.lj{;{i

r l,

ti\3,

e.

5

5:r

55a;ro

55,

I

5.3

I3333av

b,,"3

#3.€t

3

."t+J

Director ancl other firnctionaries suoh as Cliiel'E,xecutive Officer o1'State Khacli & VI Boarcl. etc.

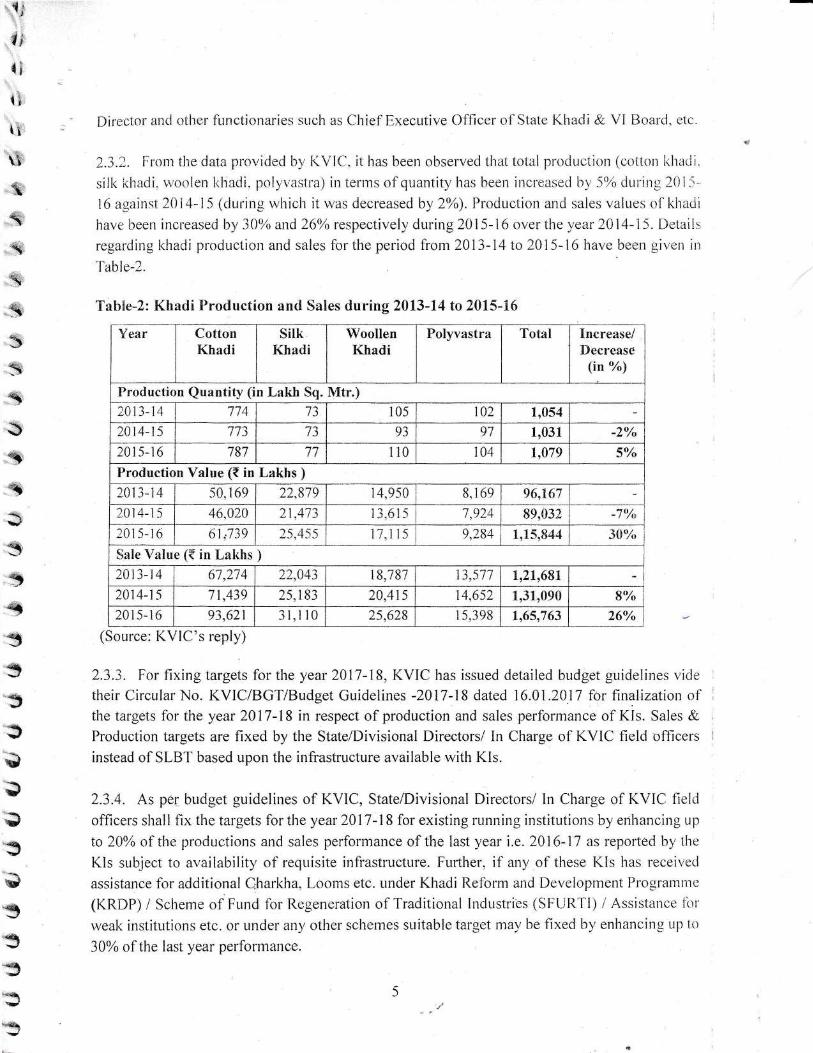

?.3.::. l'-rom the dala providr-:d by KVt[i. it has been observed that totaI proCuction (e'oilori liha,"ii.

silk riradi. rvoolerr khadi. polyvastra) in terrns of quantitv has been increaseci [rr,5-ozi, clLr-irrc 20]i'l6 againsf 2Ai4-1.5 (ciuring rvhich it r,vas decreased by 2%5. Prodr-rction and sales values of hharji

have been increaseci by 30% and260/o respectively during2015-16 overthe year 2014-15. Detail:,

regarding khadi prodLrclion and sales forthe period fi'om 2013-14 to 20i,5-16 have beerr given in

f irble-1.

Tabtre-2: Khadi Froduction anrl Sales during 2013-14 to 2015-16

Year CottonKhadi

sitkKhadi

WoollenKhadi

Polyvastra Total Increase/Decrease

{in "h)

Production Quantity ( n Lakh Sq. Mtr.)241-1-11 714 t) 105 102 1,054

2014-15 tJ-) 73 93 91 1,031 10/-L /O

20i5-16 787 11 1i0 104 1,079 5'1,

Production Value (t in Lakhs )2013-14 s0,169 22.819 14.950 8.1 69 96,167

2014-15 46.024 /"t.nt) I 3.61 -) 7.921 89,032 a(t/

201 5-16 6t;739 2.5.45-5 17.1 15 9.284 1,15,844 301',h

Sale Value {t in Lakhs2013-14 67.214 i) o_li 18,787 13.571 1,21,691

2011-15 71,439 25. I 83 20,41 5 11,652 1,31,090 8"/,20i5-16 93,621 3l ,l l0 25,628 15.398 1,65,763 260h

(Source: KVIC's reply)

2.3.3. For fixing targets for the year 2017-18. KVIC has issued detailed budget guidelines vide

tlreir Circular No. KVICiBGT/Budget Guidelines -2017-18 dated 16.01.2017 lor tlnalization ot'

the targets lor the year 2017-18 in respect of production and sales perfbrmance of KIs. Sales & l

Production targets are fixed by the State/Divisional Directors/ Irr Charge of KVIC field ofllcers

instead of SLBT based upon the infrastructure available with KIs.

2.3.4. As per bLrdget guidelines of KVIC, State/Divisional Directorsl In Charge of KVIC field

officers shall fix the targets forthe year20l7-18 for existing running instilr-rtions by enhancing up

to20% of the prodirctions and sales performance of the lastyear i.e.2016-17 as reportecl b1,'the

KIs subject to availability of requisite infrastructr-rre. Further" if any o1'these KIs has receivecl

assistance for additional Charl<ha. I-oorns etc. under Khadi Refbrm and Development Progratrttre

(KRDP) / Scheme ol'FLrrrd lirr Regerreration of Traditional lndustries (SFLiR-l'i) r Assistance iirt

rveal< institr-rtiorrs etc" or under au\, 011l.,' schemes suitable target tlal'be fixed bl,enhancing up 1o

30% ofthe last year perfonrrance.

q.aj:. I'dt{,el

{}

tB

\&

-*,.e,

",ffi

.s"s3,3

"ss:5

*<q

5:q:3q

3'qv

EU

2.3"4"1. Fixation of Targets for Nerv Institutions:- The limit of target production of all

varieties olKhadi & Polyvastra has been fixed not exceeding {15.00/- Lakh distributittg the tarset

proportionately as per available infi'astructure. Sales target has been distributed betn,eetr retail sales

of t10.00/- Lakh and ir,hole sale ot'{-5.00i- L.ahh if the KI has its ou,n sales outlets. othenvise.

maximum n,hole sales may be sarrctiorred. fhe State/ Divisionai Director and CEO. KViLI ccrtifi

that rhe KI has rvorking infi'astrLrctLlre and artisans to rult the prodr-rctittn activities. (Source:

detailed br-rdget gr-ridelines o1' KVIC).

2.3"4.2. Standing Finance Conrmittee (SFC) [Khadi] ciecided on 15.07.20i5 that retail sales

target to be fixed at the ntost upto two tlrnes of the procir-rction targets. Florveverr. the KIs iit'e frc.'

to execute retails sales beyond tlre above linrit but production target as fixed b1'K\zl(l n'ould lre

considered fcrr calculation of r.r,orkin-q capital eligibilitl'lbr bank flnance. (Source: detailed buclget

guidelines of KVIC).

2.4. KVIC's Method of Assessment of Requirement of Wor!<ing Capital

2.4.1. In financial terrns, working capital is determined by reducing the cLlrrent Iiabilities fionr

current assets. In case of assessment of working capital requirement under ISEC scheme. KVtC

determined net eligibility of u,orking capital i.e. gross eligibility of working capital so calculated

(based on certain fbrinr-ria) which is reduced by the funds available witli KI.

2.4.2. The detailed calcLrlations fbr the u,orking capital requirements of the units are ntade bv tht:

SLBTs, rvhich are based upon a set tbrmula n,hich in-turn is based on tlte productiott cycie lirr

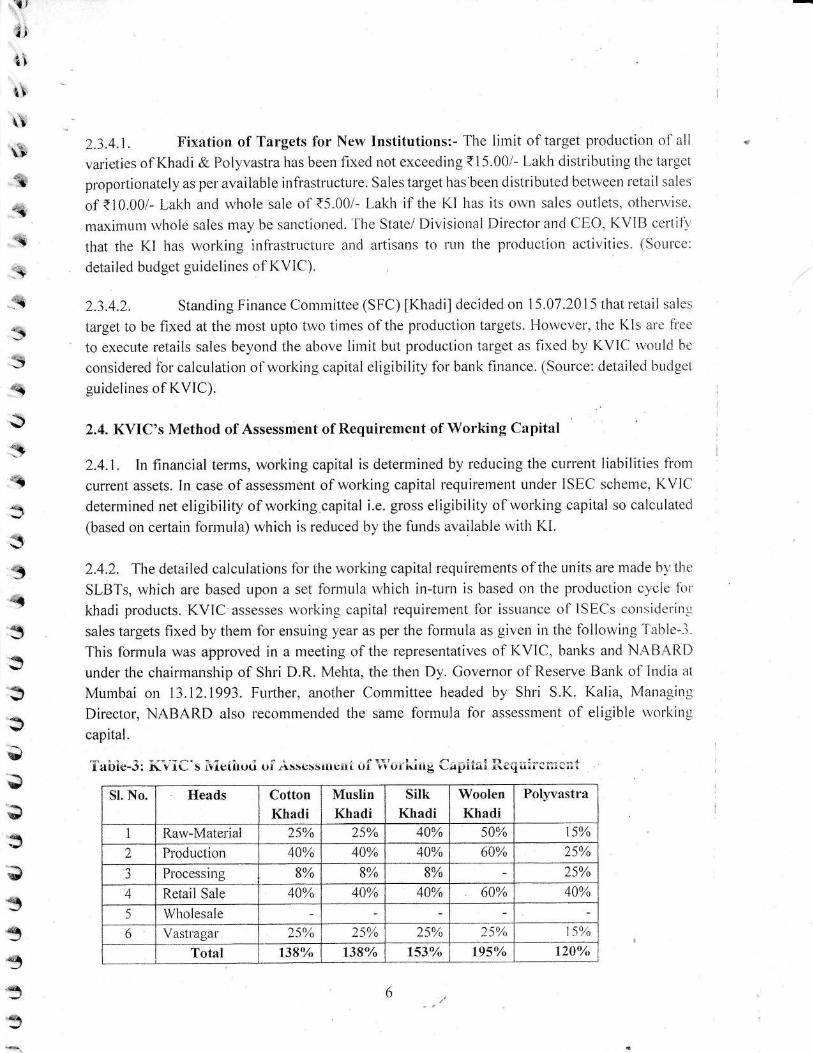

khadi products. KVIC assesses $'orkinc capital requirenrent lbr issuance of lSIlCs cotr:;idcrinr:

sales targets fixed by thern fbr ensuing vear as per the formula as givert in the fbllorving -[abie-.-l

This forrnula was approved in a rreeting of the represerttatives of KVIC. banks and NABARI-}

under the clrairmanship of Shri D.R. Mehta. the then Dy. Governor of Reserve Bank of lrtdia at

Mumbai on 13.12.1993. Further. another Committee headed by Shri S.K. Kalia. N4anaqinLt

Director, NABARD also recornmerrded the same formula lbr assessmeut of eligible norl<iltg

capital.

Tairie-3: Kv-iC's irleriruti oi,rsscs"nicut uf 'ri'uiliiu6 Capitalli.cqi;;;l;;;c;f

Sl. No. Heads CottonKhadi

MuslinKhadi

silkKhadi

WoolenKhadi

Pollwastra

1 Rar.v-Material 2s% z5% 40% 50% 15%

2 Production 40% 40% 40% 60% 25%

3 Processing 8% 8% 8% 25%AI Retail Sale 40% 4A% 4A% 60% 40%

5 Wholesale

6 Vastragar a<o.'-) /o 25% lao/

./_ J 70 1(02. l59zo

Total 138., 138o/" 153'/o l9sa tz{tot

EEI

*1

#533"e4

.r6tl

6

lY

lr-I

-i*.\"$r

!l

{r

di

\

s&

*

*

35*\

5:rq

1

3dt

{

a

{t

{

U

l''

J.t

v

'r!

't-3-::

"3

2.,1.3. lt nray be seerr lj'orl the above table thal for production ancl sale of t100,,- \\iortir of iiiriri;

cioth. the rn,orking capitai lecluiremcnt rvorks out Io {138/- fbr cotton kliadi, {195i- l'or u'rtoicl

khadi and t1-5-ii - lbr siil< khadi.

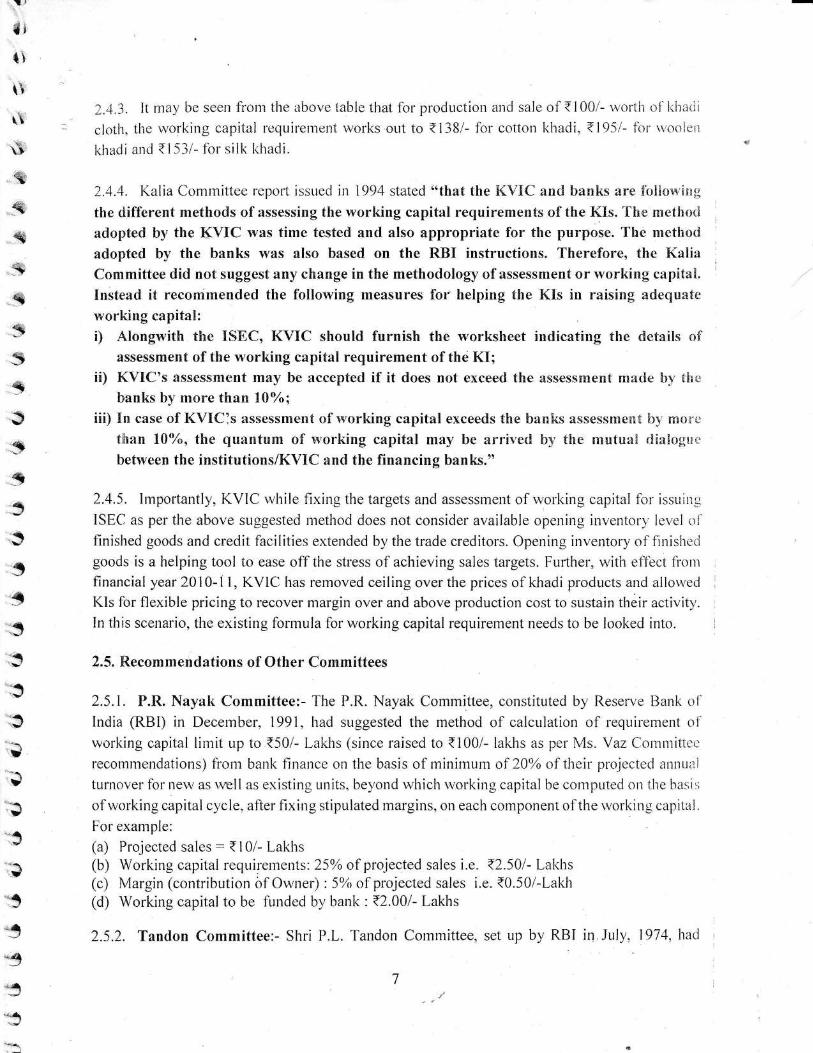

2.4.1. I(alia Committee report issuecl in 1994 stated'othat the KVIC ancl lranks trre f,olielw'ing

the diifferent methods of assessing the rvorking capital requirements of the KIs. 'fire ruethorl

adopted Lr), the KVIC lvas time tested and also appropriate for the purpose. The metlioct

adopterl by the banks was also based on the RBI instructions. Therefore, the KaliaCommittee did not suggest any change in the methoclology of, assessment or rvorking c:rpita["

Instead it recommended the fotrlorving measures for helping the KIs in raising adequate

working capital:i) Along.rvith the trSEC, KVIC should furnish the worksheet indicatirag the details of

assessment of the u,orhing capital requirement of the KI;ii) KVIC's assessrnent may be itccepted if it does nnt exceed the assessment nrade [rv til*

banks b1' more th:rn 10'lo;

iii) In case of KVICIs assessment of lvortrring capital exceeds the lran!<s assesslt]cr]t bt rnorir

fhan 10oZo, the quantum of l+'orliing capital may be arriverl bi' the rmartuaI r.ir*log;ur:

between the institutions/KVIC and the financing banks."

2.4.5. Iniportanfly. KVIC rvhile fixirrg the targets and assessrnent of rvorking capital lbr issuinir

ISEC as per the above suggested rrethod does not consider available opening inventorl level o1

finished goods and credit facilities extended bythetrade creditors. Opening inventor,v- o{'I'rnishedgoods is a helping tool to ease off the stress of achieving sales targets. Further, *'ith ellee t llrnrfinancial year 20[0-1 l, KVIC' has removed ceiling over the prices of khadi products and aliou,etl

Kls for flexible pricing to recover margin over and above production cost to sustain tlreir activitl'.In this scenario, the existing formula for working capital requirement needs to be looked into.

2.5. R.ecommendations of Other Committees

2.5.1. P.R. Nayak Committee:- The P.R. Nayak Committee, constituted by Resen,e llanlt of'

India (RBI) in Decernber. 1991. had sr"rggested the method of calculation of requirement o1'

working capital linrit up to {50r- L,akhs (since raised to t100/- lakhs as per N,Is. Vaz Comntittc,;

reconrmendations) fiom bank flnarrc,e on the basis of minimurn of 20'Yo of their pro.iected arrnull

turnover l'or neu,as nell as existing Lrnits. be-vond u,hich rvorking capital t-re cornputed on llre lrasi.;

of rvorking capital c1,cle. after fixing stipulated margins, on each component of the rvorking capitai.

For example:

(a) Projected sales : t l0i Laklrs(b) Working capital requirernents 25oro of proiected sales i.e. <2.501- Lakhs(c) Margin (contribution biOi.r,ner) :5oh of projected sales i.e. t0.50/-Lal<h(d) Working capital to Lre funded bv bank : t2.00/- Lakhs

2.5.2. Tandon Committee:- Shri P.L. Tandon Committee, set up by RBi in.July, l974,had I

1",*,".ll-rtl

3.11

ttta ,

th

{s*&

."#

s*ffi

"&."s

-ss.s-€

,,e

"s$s:s€-€:<r

.

sb,

*:l

b,

dq

?.*

q,

ss€

ssirq

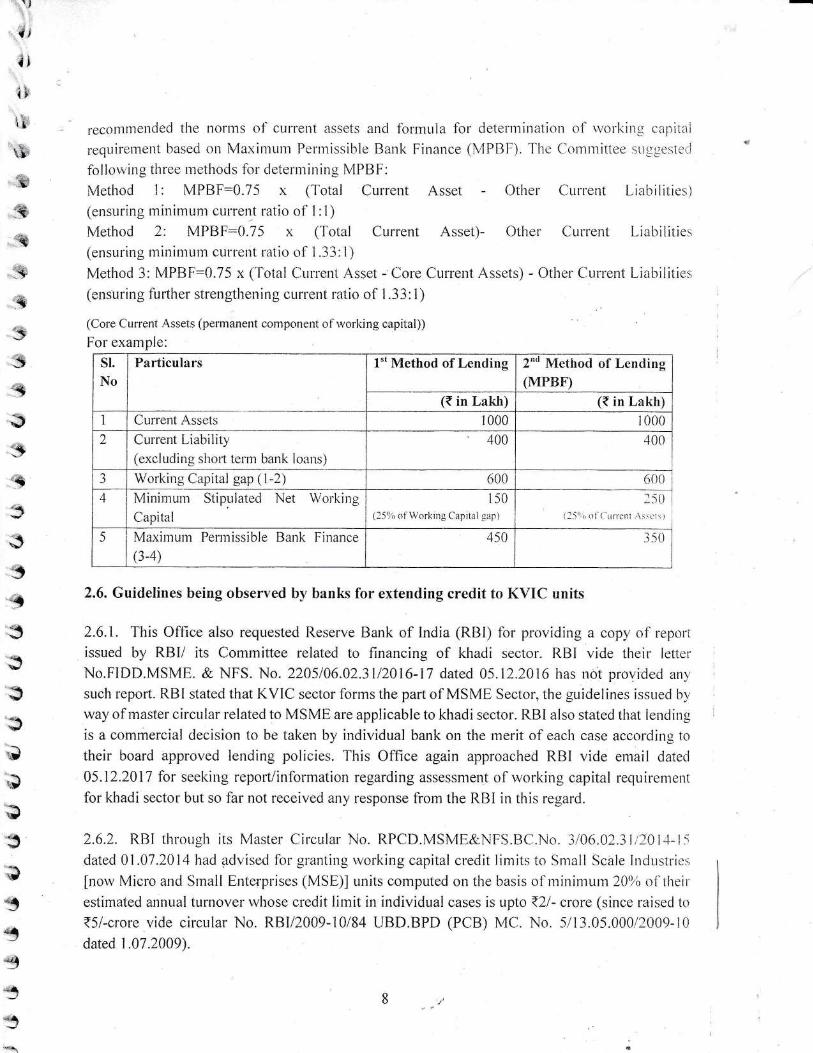

recon-unended the lromrs o1'current assets ancl iilrmula for determiltittion o1'rr'orl<irtg i:a1;iirri

requirernent based on Maximunr Pcrniissible Banl< Finance (MPBIT).'fh,; ['onrnrittee.,Li!::,csti:,-i

foIloir'ing titree Irethods fol determining MPBIr:

Method l: N4PBF:0.75 x (Total Current Asset - Other CLrrrent [.iabilities)(ensuring minimunr current ratio o1'' I :l)Method 2: MPIIF:0.75 x (Total Current Asset)- Otlrer Current Liabilities(ensuring rnininrurn clll'rellt raiio of 1.33:l)

Method 3: N4PBF;:0.75 x ('l-otal Current Asset - Core Current Assets) - Other flulrent Liabiiities(ensuring further strengthening clrrrent ratio o{' 1.33: 1)

(Core Current Assets (permanent component of u,orking capital))

For exampie:

SI.

No

Particulars l"t Method of Lending 2"d Method of Lending(MPBF)

(t in Lakh) (t in Lakh)1 Current Assets r 000 l0()0

2 Current Liability(excluding short ternr bank loans)

400 ,100

_1 Working Capital gap ( I -2 t (i00 600

4 Mininrurr Stipr-rlatecl Net Wor'liins

Capital

150

1i5'ri, oi\\rorliing Capital gapt

t-50t l-io r, rr l' (. LLrrcnl :\ s..ci s l

5 Maxirnuln Pelnrissible Bank Finance

(3-+1

4s0 l -50

2.6. Guidelines being observed b1' banks for extending credit to KVIC units

2.6.1. This Offlce also requested Reserve Bank of India (RBI) for providing a copr- of repori

issued by RBII its Committee related to financing of lchadi seotor. RBi vide their lettcr'

No.FIDD.MSME" & NFS. No.2205106.02.3112016-17 dated 05.12.2016 has rrot provided anr

such repoft. RBI stated that I(VIC sector forms the part of MSME Sector, the guidelines issued [r1,

way of master circular related to MSME are applicable to khadi sector. RBI also stated that lending

is a commercial decisiort to be taken by individual bank on the merit of each case according to

their board approved lendirrg policies. This Office again approached RBI vide email datecl

05.12.2011 for seekirrg report/information regarding assessment of rvorking capital requirenient

for khadi sector but so far not received any respouse fiorn the RBI in this regard.

2.6.2. RBI throLrgh its Mastel Circular No. RPCID.MSME&NFS.llCl.No. ir'06.02.i1,':0ll-15dated 01.07.2014 had acivised fbr granting rvorl<ing capital credit linrits to Small Scale Irrclustrie:,

fnorv Micro and Small Enterprises (MSE)] units computed on the basis olrnininrunt20'tt, of iheii

estimated annual turnovel rvhose credit lirnit in individual cases is upto t2l- crore (since raised to

{5/-crore vide circular No. RBI/2009-i0/84 UBD.BPD (PCB) N4C. No. -5/13.05.000.12009-10

dated I .07.2009).

1;

ai

ll

1l

\tr1

'3

4t,

3

2.b.-1,. Rl][ vidc its Circirlal No. I;iDD.MSN4E & r.,\[jS.L](1.No.60t06.02.31 2015-i(r ciaii--,

71.Uii.2{)l-5 had issued gLridelines on $treanilining flor,', of credit to N4icro and Srnall Lntcrprir,,,:;

(N,{Si-rs) lor facilitating tiniely ancl aderluate credit flou'dr-rring their'Lile Cr,'cle' and alloli,ctJ all

scheduied contmercial banks to derternrine r.vori<ing capital requirer-nents according to.borrorvei's

assessment and their credit needs. specifically for meeting the tenrporarv rise in rvorking capital

requirements arising mainll,' clue to unforeseen/seasonal increase in their demand for 1;roductsproduced by thenr.

2,6.4. Further. R.BI ltas issuecl clirections vide Master Direction FIDD.I\4SN4t1 t*-

NI-S.12106.A23112017-18 dated 24.A7.2017 regarding lending to lvlSME Sector. RBI has aclviser-l

to revierv and tune banl<s' existing lending policies to the N4SE, sector bl,incorporating thelein th':

iollorving provisiorrs so ils 1tl facilitate timell,and adeqr,rate availabilitl of'credit to viable \Jitiiborrorvers especially' rluring the need of firnds in unfbreseen circulnstauces:(i) To extenci stanclbt creclit iacilitr in case olterrr loans;(ii) Additional rvorlting capital to meet u,ith emergent needs of MSE urrits:(iii) Mid-temr revieu' o1'the regular rvorking capital limits, rvhere banks are convincecl that

changes in the denrand pattern of'MSE borrorvers require increasing the existing credit lirlir:;of the MSMEs. every'year based on the actual sales of the previous vear;

(iv) Timelines for credit dccisions

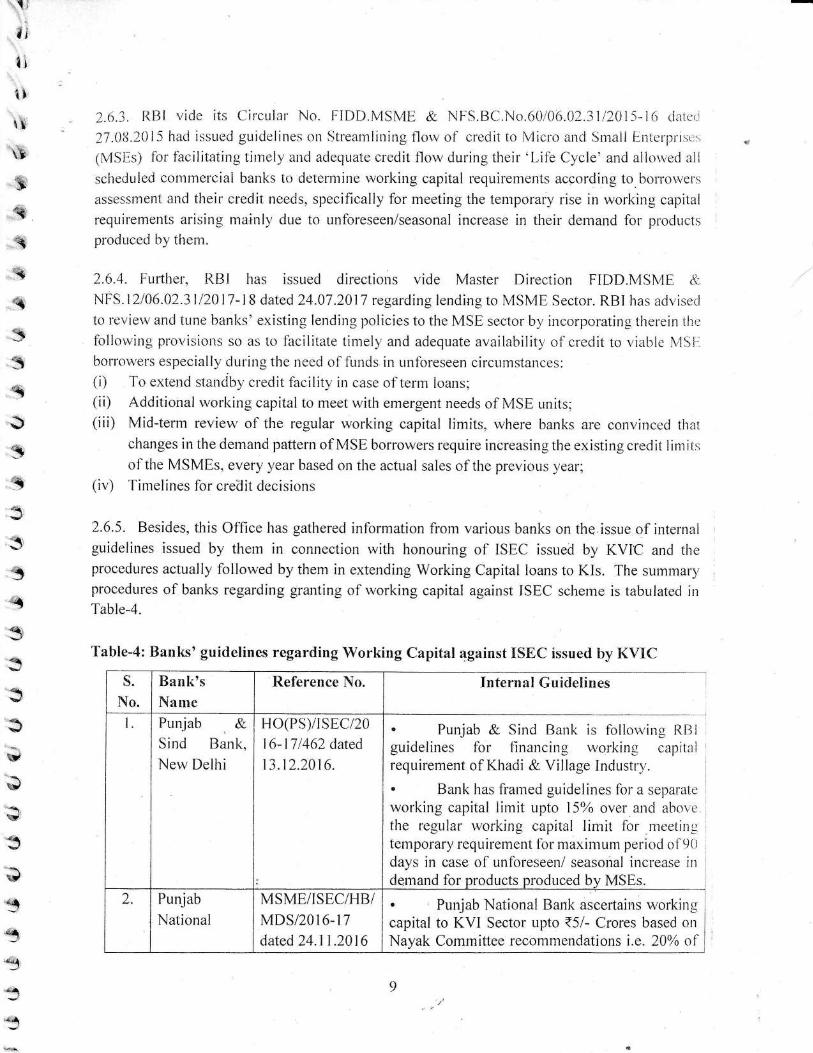

2.6.5. Besides, this Office ltas gatltered infbrmation frorn variours banks on the issue of internaigr-ridelines issued by thern in connection rvith honouring of ISEC issued by KVIC and theprocedures actually follou,ed by them in extending Working Capital loans to KIs. The sllrrmat'),procedures of banks regarding granting of u,orking capital against ISEC sclieme is tabulatecl inTable-4.

Table-4: Banl<s' guidelines regarding Working Capital against ISEC issued liy KVIC

S.

No.

Bank'sName

Reference 1Yo. Internal Guidelines

I Pr-rn.iab &Sind Bank,

Ne*,Delhi

rJo(PS)/tsEC/2nl6-17 462 dated

13. 12.20 r 6.

. Punjab & Sind Bank is fbllon,ing flltiguidelines fbr financing r,r,orking capitiiirequirement of Khadi & Village Industn,.

. Bank has framed guidelines fbr a separatcworking capital limit upto I5%o over and atroYe

thc regular working capital limit fbr nreetirigtemporart, requ iremeut fbr nraxim um peri ocl ol (){

}

days in case of unforeseen/ seasonal increase indemand fbr products produced bv MSEs.

2. Punjab

National

MSMEIISECftlBIMDS/2016-17

dated 24.11.2016

. Punjab National Bank asceftains r,r,orkingcapital to KVI Sector upto t5i- Crores based onNayak Committee recommendations i.e. 20% of

3,3

53"<l

\,

311

'{

3<"a

q

4r!

s?y

EJ

r#

*1

#59.'i3

d"

t3

L)

t'it{i.

:.-,

tl,-i3,

t:*Ewt

.=*

"*'*S

#,"s

"s-s

"s€:;s

,S{et

-q,

€,

€

€

s€"$=*a.d:,qts/rq\er

TJ

ssse€f

Bank, Netv

Delhi

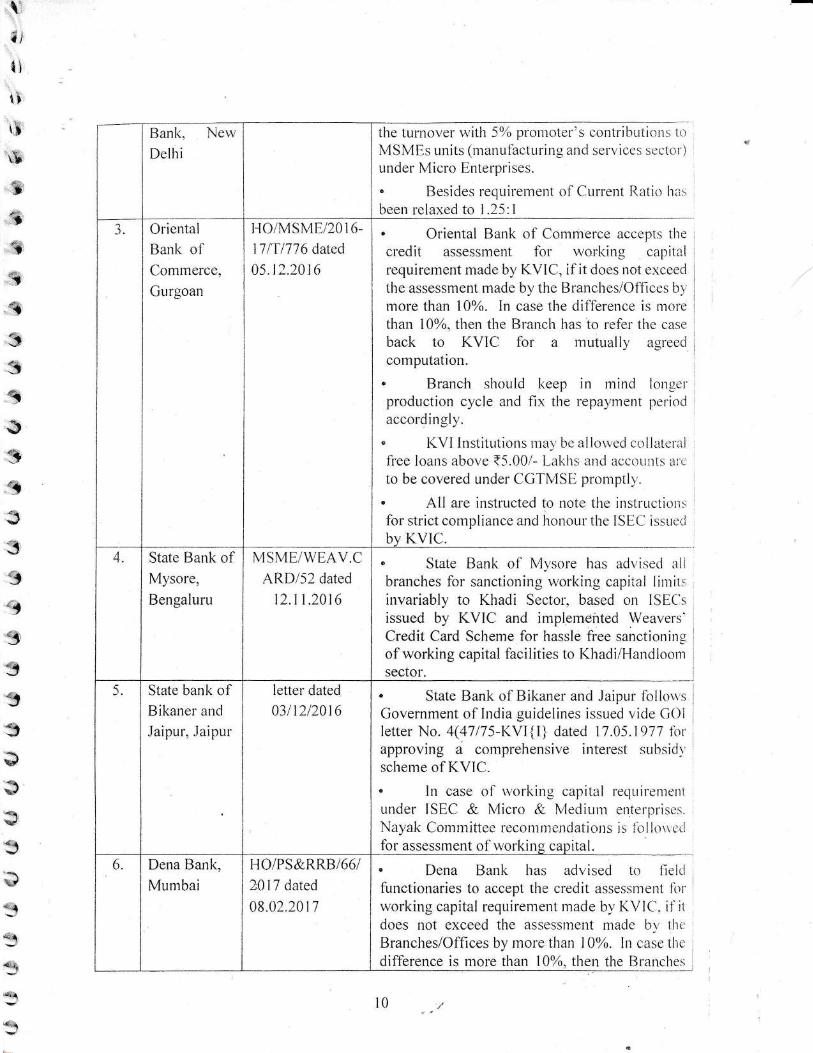

the tumover ivith 59/o prornoter's contrihLrlion:' 1,,

MSMEs units (manufar:turing ancl services Sr:'ctor')

uuder Micro Enterprises.

" Besides requirement of Currenl H.atio lui:treen rclaxed to 1.2-5:l

3. Oriental

Bank ofComrnerce.

Curgoan

Frc)i 1\4sMEl7A16-

17 l'f 177 6 clated

45.12.2016

Oriental Barrk of Commerce accepts the

credit assessment for u,orking capitalrequirenrent made b1, KVIC, if it does not exceed

the assessment rlade b1,the Branches/Offices b1

nrore than 107o. In case the dif'ference is rnorethan 10%, then the Branch lras to refer ttre case

back to KVIC for a rluluall1 agreeci

con-tputation.

, Brancir should keep in mincl ltlrncr'prodr-rctiot't cycle and fix the repaynrenl periodaccordingll,.

I(VI InstitLrtions nrai be alionecl collltcraiiree loarts above t5.00/- i-aiilrs rtncl accr;urrls ir","

to be covered under CGTN{SE promptll'.

All are irrstructed to note the instruction::for strict compliance and honr-rr-u'the ISE{- issu.:i.i

bv KVIC.4. State Bank ol

Mysore,

Bengaluru

\,IS\,{Ei \\/EAV.C'

ARD/-il dared

12.11.2016

. State Barrk of M1'sore has iidvised sltbranches for sanctioning ri,orking capital lirriiirinvariabil' to Khadi Sector, based on I5E('sissued by KVIC and irnplernented Weavers'Credit Card Scheme for hassle free sanctioningof working capital facilities to Khadi/Handk.ronrsector.

5 State banl< ofBikaner ar-rd

Jaipur, Jaipur

letter dated

0311212016

. State Bank o1'Bikaner and Jaipur follons ,

Government of India guidelines issued vide GOiletter No. 4(4717I-KYI{l} dated i7.05.1977 forapproving a comprehensive interest subsidlscheme of KVIC.

" Ir-r case ol rvorl<ins, capital reqrrir'.'rrrcnilunder ISECI & N4icro & N{ediLrnt enterpt'i\e\Na.v*alt Com m ittee recour nr Lrn(l a ti o n s i s ib I I oii cri

tbr assessnrent of uol'lciug capital.6. Dena Bank,

Mumbai

HO/PS&RRBI66I

201 7 dated

08.02.20 r 7

. Dena Bank has advised to lrelrifuuctionaries to accept the credit assessnrent firr'

rvorking capital requirement nrade b), KVIt'. if itdoes not exceed the assessrnent made' b1' thtr

BrancheslOffices by more than l0%. In casc' thc

diff-erence is more than 10%. then the Branchcs

r0

tlriri1l

1i

{}'}

}

1

at55353355II5535)

)

$5e99Y

3s

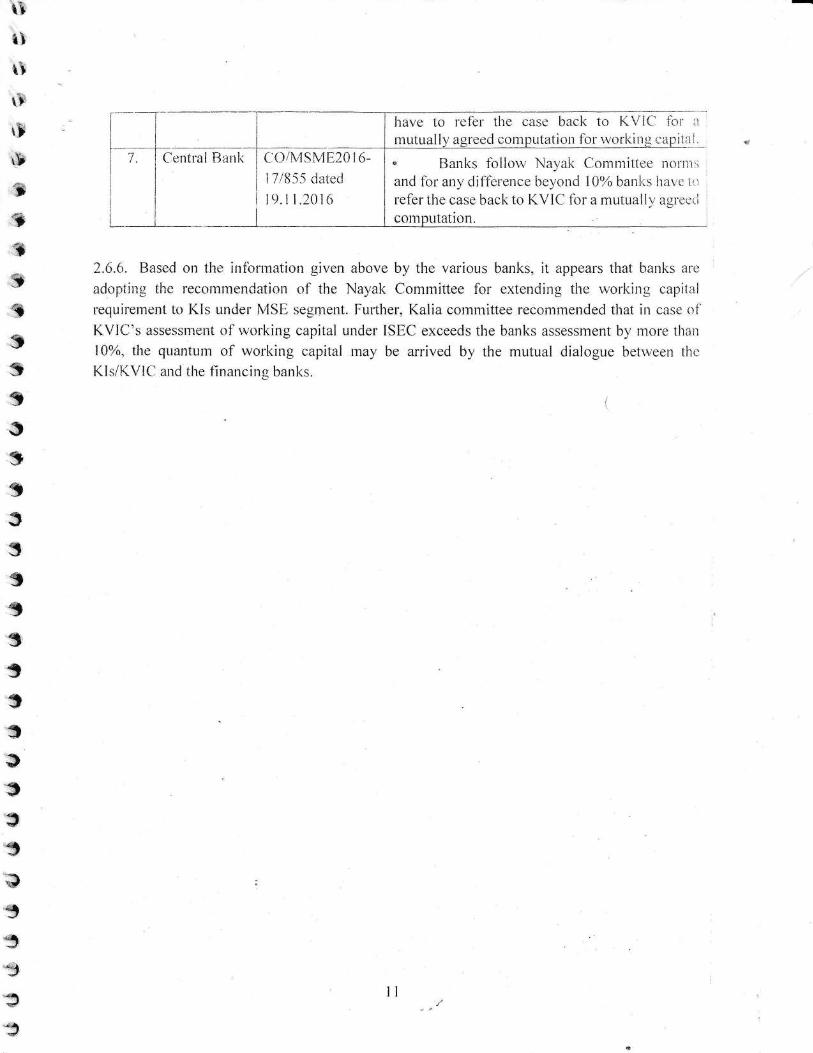

have to refer the case Lracl< to KVtrC lbl u

rnutuall c<,rmDutation ftrr u,orkitis crpiilt l.

u Bariks fbllorv nual,ak (-lomrlitlec nonlr:iand 1br any'' dil'ference bel,ourJ 10% banl;s ha',,,: ir,

refer the case back to KVIC fbr a mutualir,' asriiLl

2.6.6. Based ort the inlbrmation given above by the various banl<s, it appears that banlis arc

adopting thc recotnrnendation o{' the Nayal< Cornrnittee for extenditrg the rlorking capit:ii

requirenrent to KIs under i\4SE segn-rent. Fr"rrther, Kalia committee recomlnended that in case oi'

KVIC's ?sSessnrerrt of rvorking capital under ISEC exceeds the banks assessrnent b1'r'nore tharr

10%. the quanturn of u,orkiug capital may be arrived b),the mutual dialogr-re betn'cen thr:

KIs/KVIC and the flnancins banl<s.

c{li N4sN1u20l6-

1718-5.5 datecl

19.il.2016

t1

l.l

{r

{}

(i

rt

ri,t

1'\

1

CEaapter - 3

.4m a X-v s i s o fl \4/ o rfini m g C a p ita I Req'"1 i r e rm e m t

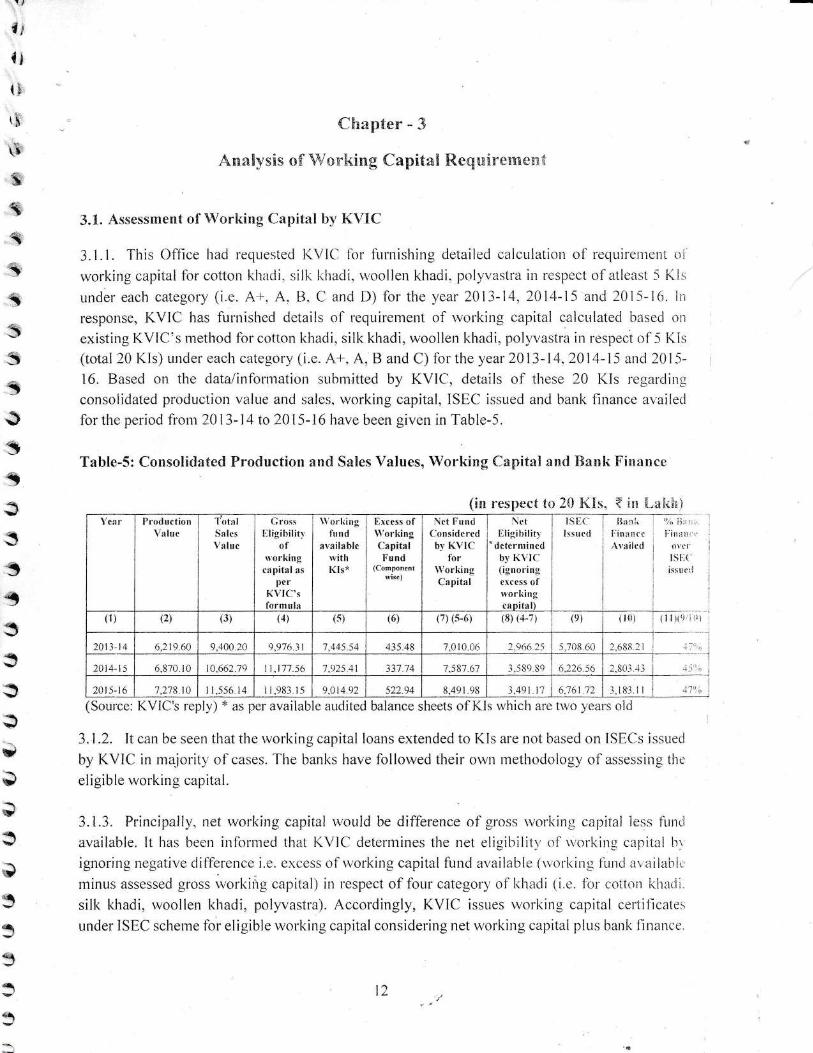

3.1. Assessment of \\/orking Cnpitatr by KVIC

3.1"1. This Office hacl recprested K\ilC firr firmishing detailed calculation o1'requirerrient oi

rv:orking capital lor cottorr iihirrli. s;ill.: ltiracli" r,r,oollen khadi. polyvastra irr respect of atlea-st 5 lc.i:r

uncler each category (i.e. Ar-. A. tl" C anci D) {br the year 2013-14. 2014-15 and 2015-16. in

response, KVIC has furnislrcd details of'requirement of wolking ca;rital calculatecl based or:

existirrg KVICI's method tbr cotton khadi, sitk khadi. woollen khadi, polyvastra in lespect ol5 Ki::

(total 20 KIs) under each category (i.c. A*. A, B and C) fbr the year20l3-14.2014-15 and 2015-

16. Based on the clata/inlornration submitteci by KVIC. details of these 20 I(ls rc'gar,Jirrg

consolidated prociuction value and salcs. working capital, ISECI issued and bank financc availed

for the period fronr 20 I 3- I 4 to 20 I 5- 16 have been given in Table-5.

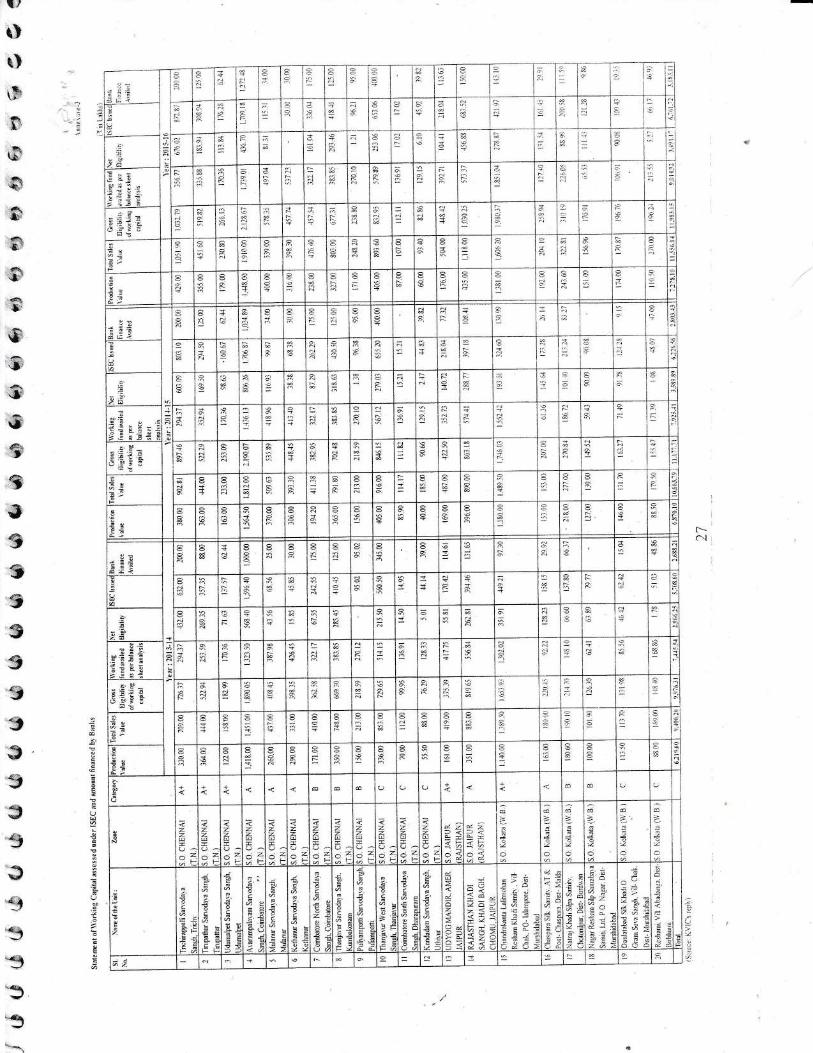

Table-S: Consolidated Pnoduction ancl Sales Values, Workilrg Capital and Eank Finanec

(Soulce: KVIC's reply) '' as per available ar,rdited balance sheets of KIs which are tu,o l,ears o1d

3"1.2. It can be seen thal the ivorl<ing capitaI loans extended to KIs are not based on ISECs issr-reci

try KVIC in nia.ioritv of cases. The banhs have follorved their orvn methcidology of assessin-u thc

eligib le rvorkin g capital.

3.1.3. Principallr,. rret norking capital nor.rid be difference olgross nr-rrliirrg capitai less iunri

available. [t has been infbrnretl that l(VIC determines the net eligiiiilitl,o1'u'ot'l<ing co]rital lr',ignoring negative clif-l'erence i.e. excess olu,orking capital lund avaiiable (riorking firncl a.,ailabl,,,

minus assessecl gross ivorkirig capitat; in respect o1'firur categor')'of thadi (i.e. 1il'coiton itirari;.

silk khadi, rvoollen khadi, polyvastra). Accordingly, KVIC issues rvorl<ing capitaI certillcaies

under ISEC schenle for eligible rvorking capital considering net norl<ing capital plus bani< f-inance.

\

_1

_a

a3"-1

tt

a

5Ida

<t

<r

U

t,**\

o53353

(in respecf to 2() Kis" { mr [.;-rtrlriYcar P rod uction

Valuc1'otrr I

S:r Ics

Yaluc

li rossiligibilitr

ofr orking

er pital asper

Ii\jlC'sfrtrrnultr

\\ orliing{ir rrd

availa hlctr ithl(ls*

lirrr:ss of\\'orl<ingCapitalFund

((lomponcntrvirc)

\ct Fund('on s idc rcriby KVIC

for\\'o rki ngCapital

Nrliiligi bilitr

'dcternrincdbl KVI('( ignori ngcrcess ofx orliingclnit:rll

iSI)(lrsurrl

Ii:i:t i.ljin:rrttAyailrd

'!u !ir'; .'

ljirrt:1..'o!.'iI$[,{'is:iutll

(1i (z) (3) (4) (s) (6) (7) (s-{r) (8) (a-7 t (e) 0{i) { I Ill(}r.:;l

2ilti-r4 6.2 t9 60 9,400 20 ,r.976 .1 I 7..14_5 -54 415 48 7.0l0.Urr " ai /-a. ri 5.7118 {rt) r n(R 'l -i.',,,

20t4-li (:,|i70. I0 l0 662 7Q I r,177 56 )) / t+ 7.581 67 i.-i89 sg 6.226 56 : s0r ,+l

20t5-t6 7.278 I 0 I I .556. t,1 1 i.983 r-s 9.0 14 92 522.94 8.491 .98 _1,;19 1 17 6.'161 72 l.i8,l 1l

12

trl

li(;

1l

t\capitai lrri"lihacli and consi(lered u'ot'kiug ftrnd ignoring excess o1'u,orking flnd lbr clclcrininrrlit, ,

\l o{'nct eligible lvorl<ing capilai lbr issuance of ISEC 1'or ilre l,ear 2013-14 as per detail giverr iri

\ T'eble 6.

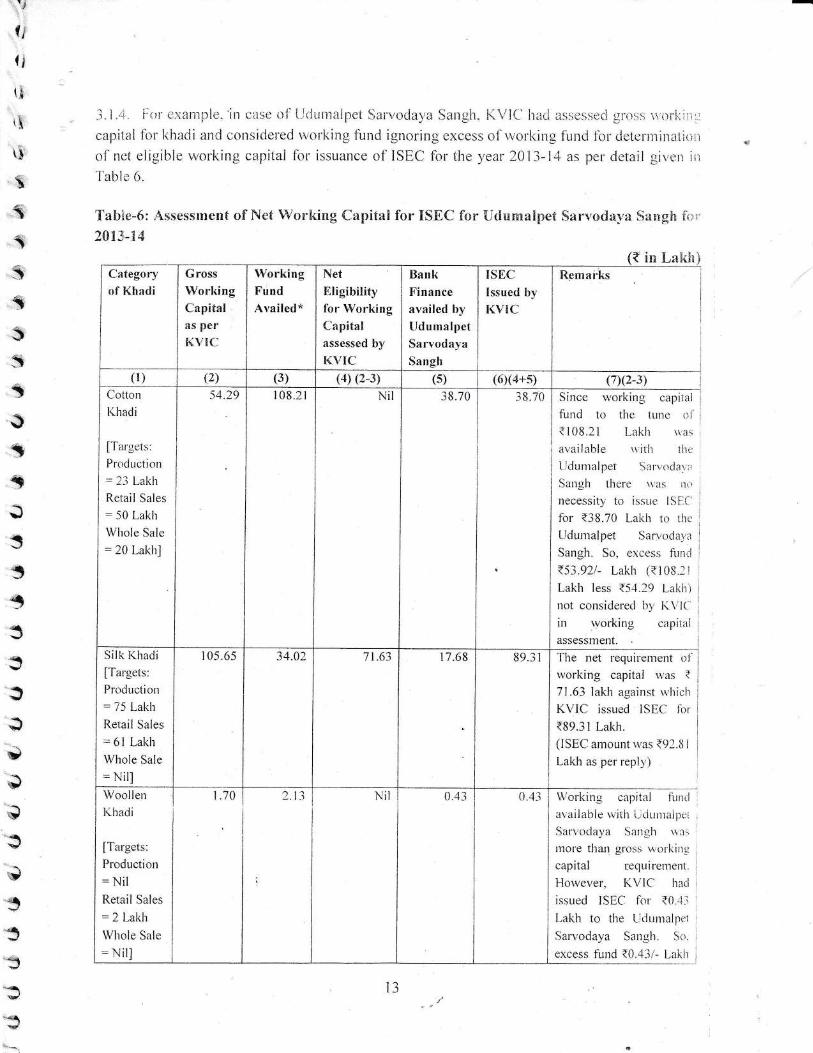

I Tabiie-6: Assessnlenf of'Net WorX<img Czrpitan for ISEC for {,tlumralpet San,od;15,p !i1p11g}f ii.,,'

\ 20tr3'-1"6

im n-alikCategoryof Khadi

Gross

WorkingCapitalas perK\/IC

WorkingFundAvailed*

Net

EligibiliQfor WorkingCapitalassessed byKVTC

BankFinance

availed byUdumalpetSarvodayaSangh

TSEC

lssued by

KVTC

Remaiks

(r) {z) (3) (4) Q-3j (s) (6)t4+s) (7)t2-3)(lotton

l(hacli

fTargets:Prociuction

- ll Lal<h

Retail Sales

= -50 Lalch

Whole Sale

= 20 Lakhl

s1.29 108.21 Nil 38.70 .18.70 Since r.i,orking capital ,

frirrd to tlrc lunc ,'r

{ 108.21 I-akir \\ a5

available .r ith 1h''

lrclurnalpi:t 5lt'r'i,clar;,

Satrllt llrulC \\ jti , t,

ttecessitl trr issrrr' ISI i

lor' ?i8.70 Lnlilr trr rlr,

I duirralpet SAI'r,,da. r:

Sarr,qlr. So.,-'rcc.. lir,,.i

i5:1.92i- Lalilt (T108 I t

Laklr less {51.19 I aliir,

rtot corrsidcretl lrr K \ It

in \yorkin-q capitrri :

assessll1ent.

Silk Khadi

ITargets:Producti on: 75 Laklr

Retail Sales

=61 Lakh

Whole Sale

= Nirl

r 05.65 34.02 71.63 17.68 89.3 r The net lequirenrent ol

ivorking capital u,irs {71.63 lakh aqainst *,hiclr

K\,'lC issued ISEC lor

{89.31 Lakh.(ISEC amourrt ri'as {9l.lj I

Lakh as per reply)

Woollen

l..had i

ITargets:Production

= NilRetail Sales

= 2 Lai.h

Whole Sale

= Nirl

1.70 2.1.1 n-il 0.43 0.43 \\rorkins capit;rl firrtrl

ar'ailable * ith i.-tiLrirtrli-rcr

San,odir),a Sartglr \\ ii:,

lllore than gtoss u orhinlcapital r:ecluirerncnt.

Hou,ever'. I{VIC haci ,

issued ISEC lor t0.-.1 I

I-akh to the L,duinalpcl

San,odaya Sangh. Si,.

cxcess turrcl ?0.1"1 - Liri\ir

l-1

I\

)3:i$:i*

L/

S

35i.l

*t

3;c\).:*\

.i5"1

-1

E'

{iiIt!r

ih

ri*Aii&

s*T

.a

$:i'<$

;)'*

*

3-lJ

'3,9

3333;

3<l

5-v

*

q

q

"l

3

(T2 ii Lakh less {1.7()I.alth) ntx c(lnsiLicre(l []\

I.,\'l(' i;r rrot.liing clpilllil SS CS S 1 l1 r)l it.

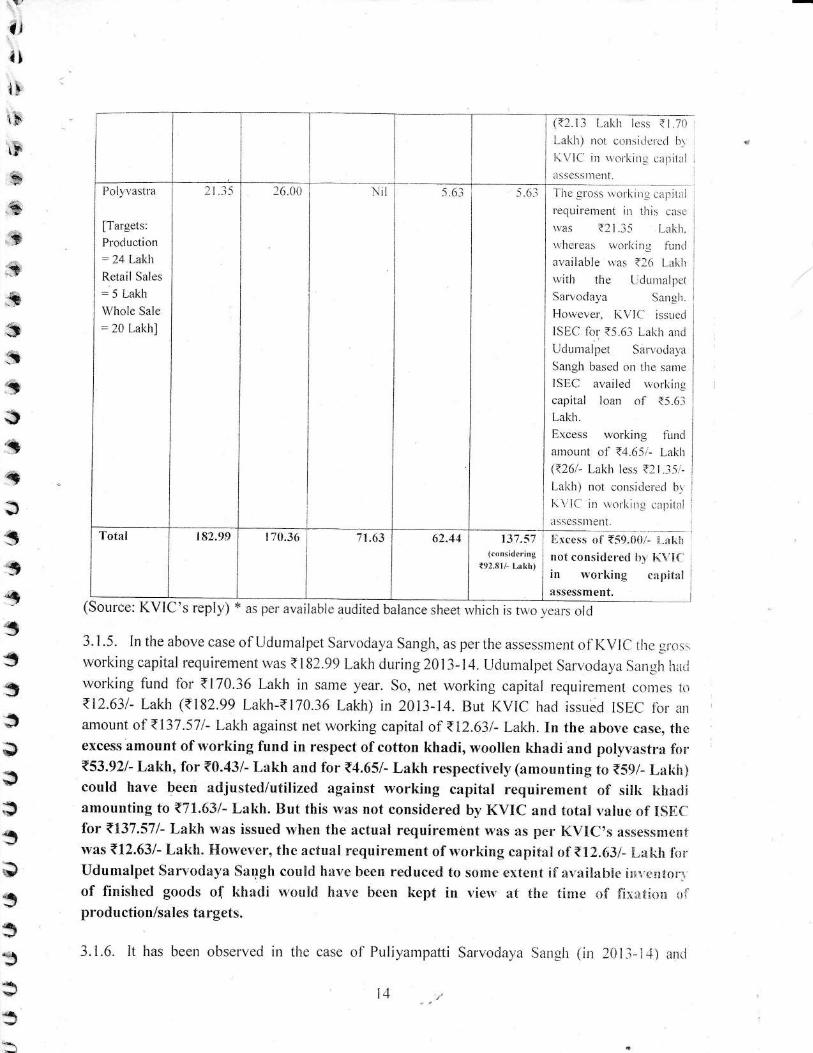

Pol-r vastla

ITargets:Productiorr

- 24 Lalih

Retail Sales

= 5 Lalih

\Vhole Sale:20 Lakhl

I I ..15 16.00 Nil 5.6-l -5.(rl-l-irc

!:i'oss ii r,,r'lir n t clrltitrri

tequirenteni in this ca:,--

\\'as t2l .i5 l-rlilr.u'lrcrelrs rvorkiltg hrrrtl

availablc- *'as {16 I alil:

rvitlt thcr L drrniaipcl

Sarvocla)'a Sarroh.

I'[on,ever. I(\''](' issrrcti

ISEC tor' {5.61 L.alih anrl

L,clLrnrallret SanrrtlalaSangh based on tlte satne

ISEC availed u,orliiugcapital loan ol {-s.(rlLakh.

E,xcess rvoll'ing lirndalroLrnt ol' {-1.65,- Lai<h

t {lO - Laklr less {l I l5 -

l-akh) not consider*i hr

ir\ lt itt'.r,,t l,irr'- , rr,it ,

nsscssrn *nt.Total 182.99 t 70.36 7 I .{t3 62-44 137.57

(consitlcrintt92.lil/- l-alih)

lrrcess ol {59.{}l,ii'- L-a[,ir

rrot consitlel'ecl hi !r\ X('

in n'orking capittlassessment.

(Source: KVIC's reply) + as per available audited balance sheer rvhich is tli,o venrs old

3.1.5. In the above case of [-iclurxa]pet Sarr,'odava Sarrsh. as pe. the assessnrent ol'KVIC ihc qi.ss.

working capital requirentent u,as t182.99 Lakh during 2013-14. L.lclunrnlpet Sanoclal,a Sarrgll hlr.i\'vorking f,Lrnd lor t170.36 I-al<h in sarre )/ear. So. nc't working capital requirement corncs Io<12.631- Lakh ({182.99 Lakh-{170.36 Lakh) in 2013-14. But KVIC hacl issuecl ISEC' lbl arr

amount o+;<137.571- l,al<h against net working capital of <12.631- Lal<h. In the abol,e case, thL]

excess amount of u'orl<ing fund in respect of cotton khadi, tvoollen khacli and polyvi'tstra I'on

<53.921- Lakh, for T0.431- Lakh and for t4.65/- Lakh respecti\/e11,(:rmounting to T59/- I-al<ii)could have beell adjusted/utilized against working capital requirement of silli l.rh*rliamouttting to {71.631- Lakh. Ilut tltis }r'as not considered by KVIC ancl total r.alue of ISECfor t137.57/- Lakh !y:rs issued rvhen the actual requirement vr,:rs irs per KVIC's ilssessmerrfwas t12.63/- Lal"le. Florvc'r'er, the actual requirement of n.orking capital atT12.63l- [-atriXr &ri"

Udumalpet Sarvoclal'a Sarrgh could have been reducecl to sonle <:xterlt iflnvaitrabie irrvr:irtor'.,of finished goods of khacli lvouitl ltitve lreen kept in vien'at the tirne *f fi:r:;ti3ri 1i'

production/sales targets.

3.i.6. It has been obset'ved in the case of Puliyanrpatti Sarvodava (an-h (in 20li-i-1) arrtl

itt+

Qr

{iiti5,

iF

*,.3,

tkr

a

s_a

533;}

!?

3$

\,

_3

-*I333

Iiethanirr Sarvodaya Sangh (irr 2015-21)16) where net eligible amoLrtrt of ri'orking capitai ivas niibirt l(VIC issLred ISEC firr t9-5.02/- i,akh ancl {30.00i- Lakh respectivell,. (Annexure-3 ref'en's,1.

In thcsc two oztses. tltcrre rvas no requirentent of additional rvorl<ing capital and. there[bre. therc\,vas no necessitv to issue of iSECs. lvloreover. these tu,o I(ls also availed banh finat-rce to the extcntof ISBC att.tot.tttt i.e. for t95.02,'- [.al<h in the case o1'Pulil,ampatti Sarvoday'a San-uh iind lirr130.00r- L,akh to Ketlranur Sarvodaya Sangh.

3.1.7. Sirrilariy. i1 may be observed fiorn tlre Tabie-5 that KVIC has not considered the exce:;s

amout.rt of ivorkins iLrrrcl to tlre tune of ?435.-18/- Laktr fbr 2013-14. ibr {337.74.1- Lalih 1br ).Al:,l5 artcl tbr {522.9,1/- I-akit 1or"20l-5-16 in tlte assessnrent olrvorl<ins capital in respc.ct o1'10 fils.i(VI':'had issued the ISCIL {br the hiqheL value tbr {5.708.60 L.al<}r against actual iir:i rioi'iiir.i::capital recluirerrrent 1or t2.5i0.621- Lalih ({9.976.161- Lakh less <7.145.54 - Lalth) in 2011-ti.Similaril,, the same can ber observed in next two years. Besides this. KVIC could have ad.justcr:l,

utilized the excess u,orking capital firnd for <435.481- L,akh for 2An-14. for <337.741- l-alil': fr:r.

2014-15 and for <522.941- Lakh for 2015-16 while issr-ring the tSEC to tlre 20 I(ls.

3. 1 .8. It rlay Lre observed fi'orn the above Table-5 that gross anrount o 1'u,orking capita l has bccirincreased rvith increasing trer-ld in sales and production but bank flnance has been availed in therange of 45%-47% over worlcing capital as assessed by KVIC. 'the details of assessed u'orl<ingcapital requirenrent as per the ISECs and the loan actually accessed by some of these 20 I(ls lravebeen siven in Annexure-3.

3.1.9. Earlier. KIs rtere not allo*,ed r.r,ith mark up tor.vards profits which left no cushion tou,ardsinternal generation of surplurs. Higher *,orking capital requirement shou,n by KVIC againstprojected production cost may be the reason for vvhich bank are rrot inclined to plovide r.r,orl<ing

capital to Kls based on ISEC issued by KVIC. Horvever, KVICI has recently adopted fleribi,:pricing policl' b5, rvhich KIs are {r'ee to add margin over and above production cost and tlierelirlc.they can sustain their activitl'to the extent o1'100% of their tul'llover under this chanced scenaiit,.

3.2. Operating Cycle and Cash Cycle

3.2.1. Operating cycle is the average period of time required fbr a business betweelt cash ourlarand cash realisation through sale olfinished goods & realisation of receivables. If average pavmenlperiod of payables is deducted fi'onr operating cycle. it gives net operating cycle (or cash c:r'clc or'

cash corrversion cycle). It consists of:a. Time taken to acquire and average storage period of raw rnaterial

b. Conversion process timec. Average peliod for which finished goods are in store

d. Average coliection period of receivables (Sundry Debtors)

e. Operating Cycle (a+b+c+d)

L Average payment period of payables (Sr"rndry Creditors)

g. Net Operating Cyclel Cash Cy'cie (e-t)

15

3'!,

',3

;"t

tq'-q

:-1

"a

.*\

Xr

(.t

ir

i!,

'.\

tS

5aessSS

!s*4$

L,

3ssa{a

3;)

*

)

ty

3rd

*3"rt

a'.t

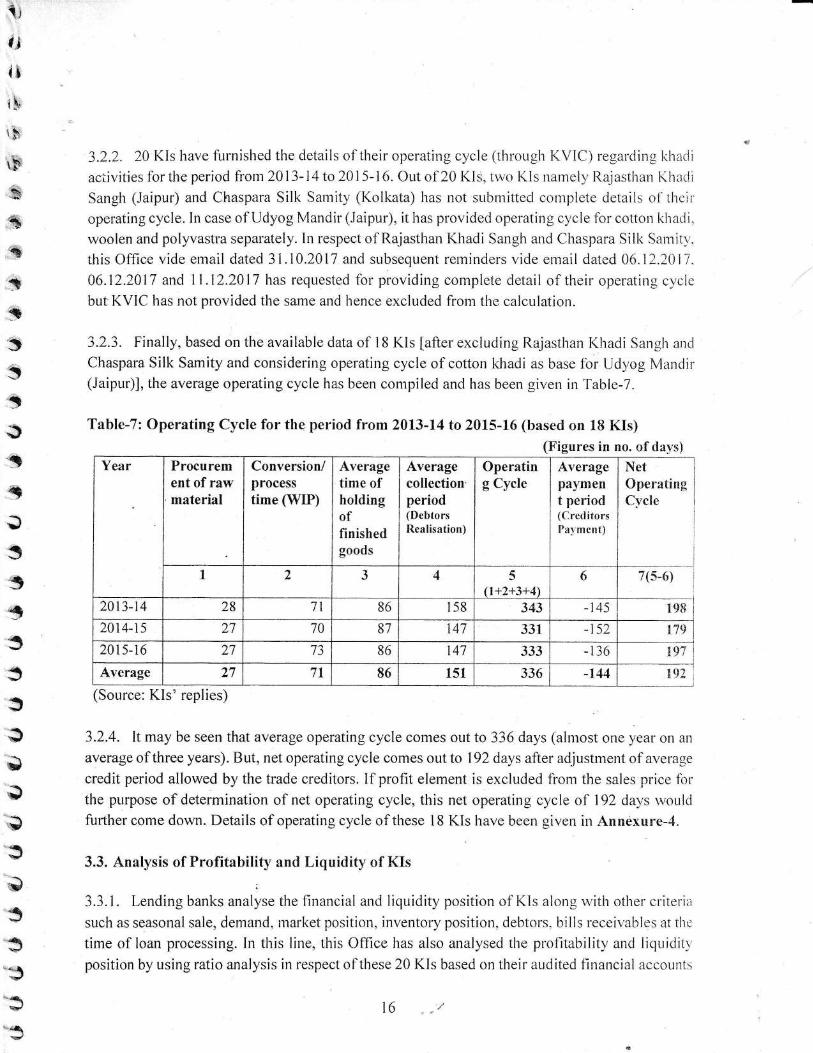

3.2.2. 20 KIs have furnished the details oitheir operating cycle (throLrgh KVIC) regarding khircli

aciivities for the period fi'orn 2013-14 to 2015-16. Out of 20 KIs, rno Kls narrelv Ilajasthan Kharii

Sangh (Jaipur) and Chaspara Silk Samity (Kolkata) has not sLrbmitted complete details oi'thciioperating cycle. ln case of Udyog Mandir (Jaipur), it has provided operating cycle fbr cotton lilratii.

r,voolen and polyvastra separately. In respect of Rajasthan Khadi Sangli arrd Cl.raspara Silk San-ritl'.

this Office vide emaiI dated 31.i0.2017 and subsequent reurinders vide errrail dated 06.i2.20i7.06.12.2017 and 11.12.2AI7 has requested ibr provicling conrplete detail of their operating cvcie

bul KVIC has not provided the same and hence excluded from lhe calculation.

3.2.3. Finally. based on the available data of 18 Kls [after excluding Rajasthan Khadi Sansh anil

Chaspara Silk Samity and considerirrg operating cycle of cotton Lhadi as base fbr udy'og l\,{andir(Jaipur)], the average operatir,g cycle has beerr compiled and lras beerr given in Table-7.

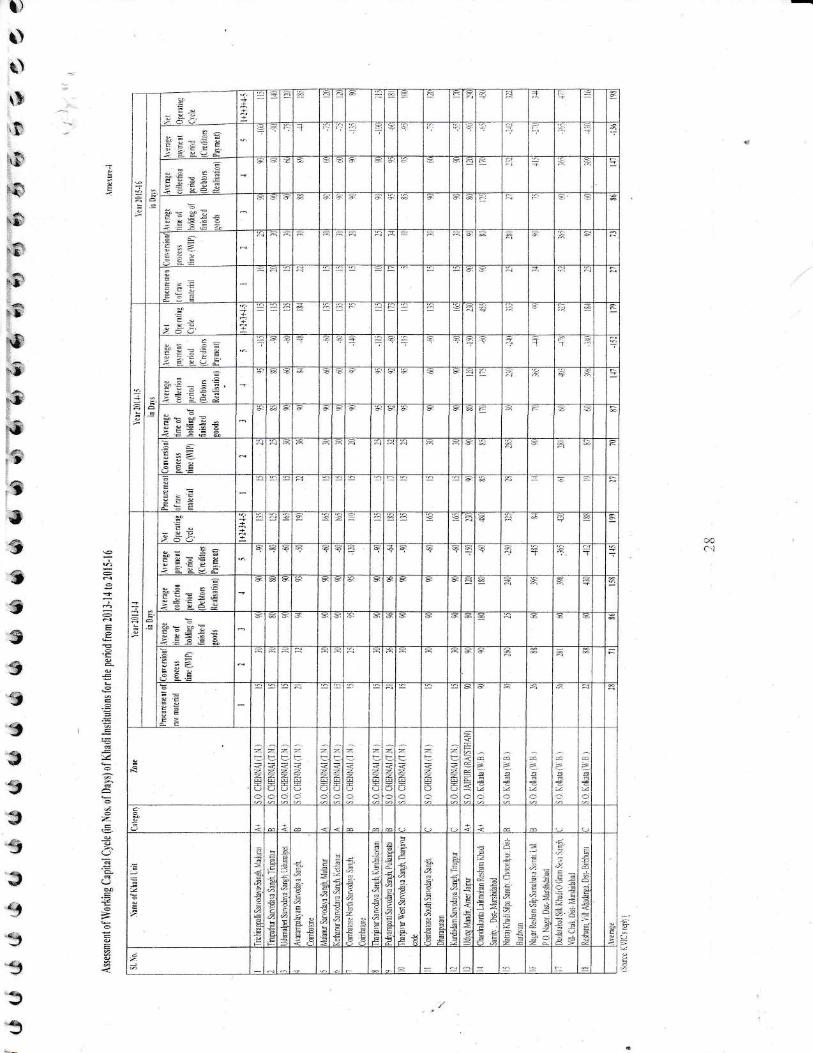

Table-7: Operating C1'cle for the period from 2013-14 to 2015-tr6 (based on 18 KIs)(Figures in no. of days)

Year Procurement of rawmaterial

Conversion/processtime (WIP)

Averagetinre ofholdingoffinishedgoods

Averagecollectionperiod(DcbtorsRealisation)

Operating Cycle

Averagepaymert period(CrcditorsPaynrcnt)

Net0peratingCvcle

1,,

J 4 5fi+2+3+4\

6 7(5-6) i

20r3-14 28 11 86 158 343 - 145 i982014-1 5 27 70 81 147 331 -152 l7L)

2015-16 2'7 13 86 147 133 136 19i

Average 27 7l 86 151 336 -144 Lq2

(Source: Kls'replies)

3.2.4. It may be seen that average operating cycle comes out to 336 days (alntost one )/ear olt atl

average of three years). Bt-tt, net operating cycle comes out to 192 da1,s after adjlrstment ol averase

credit period allowed by the trade creditors. If profrt element is excluded from the sales price fbrthe purpose of determination of net operating cycle, this net operating cycle of 192 dai,'s u,ould

further come down. Details of operating cycle of these l8 KIs have been given in Annexure--f.

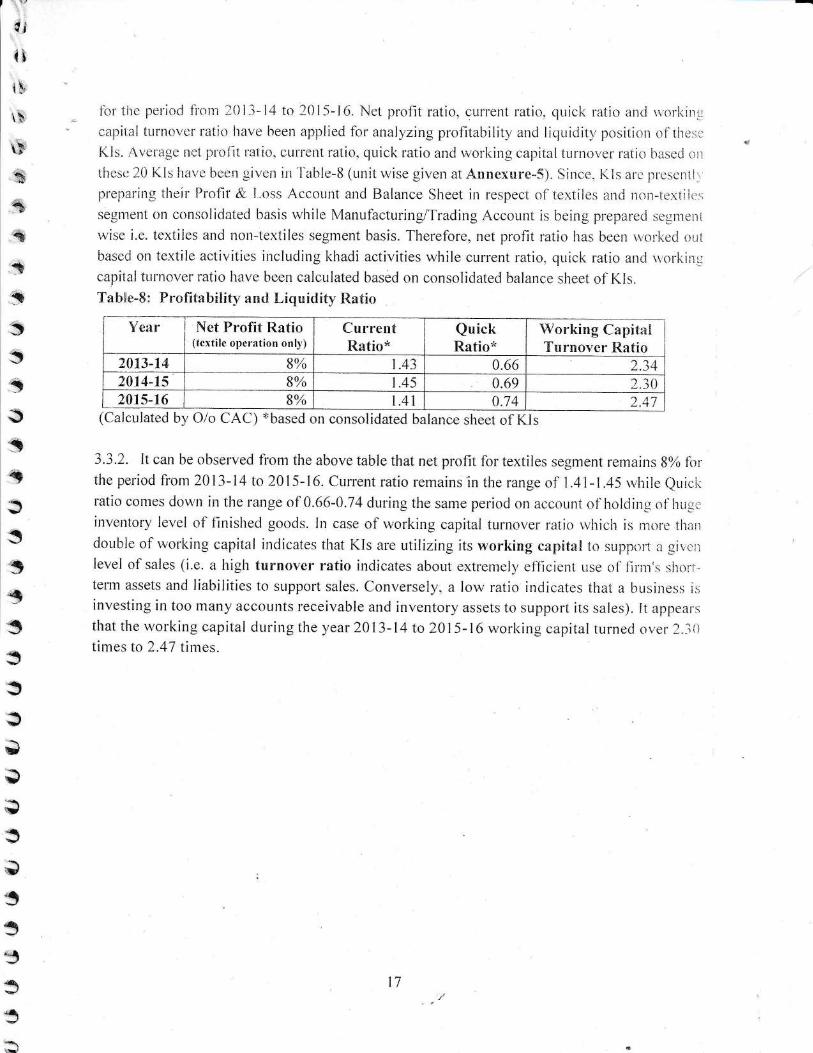

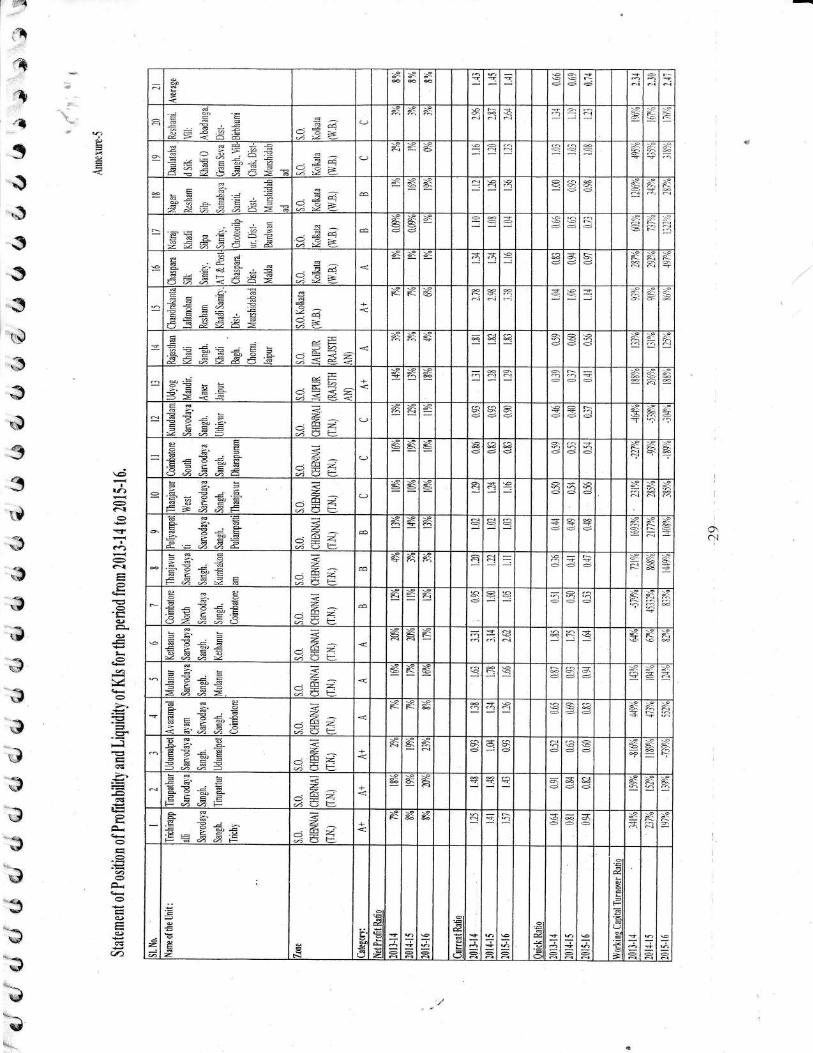

3.3. Analysis of Profitabilitl' and Liquidity of KIs:

3.3.1. Lending banks analyse the llnancial and liquidity position o1'KIs along riitir other criterir,

such as seasonal sale. demand" rrarket position. inventory position" clebtors. bills receivablr:s at tir':

time of loan processing. In this line, this Ofllce has also anall,sed the profitabilitl,ancl liqLriditr

position by using ratio analysis in respect of tlrese 20 KIs based on their auclited flr-rancial accor-urts

t6

{i

ir

i!.

i! iir tire perioci lL'oii-i lr{)i3-14 to 201-5-16. Net profit ratio. currenl ratio. quicl< ratio altci r,orliinirr:apital turnovcr l'atio itave heerr applieci fbr anal-vzing profitabilitl,and liLluitiitl,position oithc:;,,1

t3 KIs.Avcrage'netprolitt'ltiio"cut'retttratio.quickratioarrcl tl,orl<ingcapitaltun.loverratititlrsedrir

* tiresc 20 lils ita'.,e heerr given in 'l'able-8 (Lrnit rvise given at Annexure-S). Since. Ktrs arc prt:scrtl.

,, prepaiiitg ilteir Prolir & Loss Account and Balance Sheet irr rrspect o{'lcxliir:s anci licir-ti:rrtil:r4

segtttcnt on consclidated basis rvhile Manufacturing/I'rading Account is being prepared scrntcr,

% u,ise i.e. textiies and ttott-textiles segnrent basis. Therefore. net profit ratio has beeli u,olliccl oLil

based on textile activities including l<hadi activities while current ratio. c1r-rick ratio arrci riorliinr:<*' crpiial tLtrnorier ratio have been calculated based on consolidated balance sheet of Kls.

3 'fable-8: Prcfitatrilitl,antl l-iquidifv t{atio

Year Net Profit Ratio(textilc opcration onll,)

CurrentRatio*

QuickRatio*

Working CapitalTurnover Ratio

2073-14 8% 1.43 4.66 2.342474-1s 8% 1.45 0.69 2.302015-16 8a/,' t.4i 0.74 111

-,4 I

;) (Calculated by O/o CAC) *based o,', "o,.,solidat"a

Uit,i,t." rt.,""t of fls:i

3.3.2. It can be observed fl'ont the above table that net profit for textiles sesment renrains 8,/o for4$ the period from 2013-i4 to 2015-16. Current ratio remains in the range of 1.41-1.45 u,hile eLrici,

I ratiocomesdou,n intlterangeof 0.66-0,T4duringthesameperiodonaccountol'holciiirgul'hurr:invetttor.v leveI of f-inished goods. In case of rvorhin-e capital turrrover ratio rviriclr is ;troi'e tilin

S clouble of rvorking capital inclicates that KIs are utilizing its l,r,orking capitatr tt'i sr"rplrr-,r',, a srri;'r

3 level of sales (i.e. a high turnot,er ratio indicates about extrenrely efficienr use of liril's shor"r.

term assets and liabilities to support sales. Conversell,. a lou,ratio indicates that a business;r,S investing in too many accourtts receivable and inventory assets to support its sales). It appears3$ that the rvorking capital during the vear 2013-14 to 2015-16 rvorking capital turnecl svL,l' l.li)- tinres to 2.47 tirries.5

Ss:l

{f

1

vI/

va

a33-{

j

*

t7

'qi

il

{r

r:,

ii

rF

3rid',

" 4.1. Working Ctrpitatr Assessment Methocls

&4.1.1. Mainly barrlts adopt one or trvo nrethocl out the belorv rrethods fbr assessnient ot'rr,6riiilil.<ho capitai of any particr-rlarorigination lbllow,ing instructions/directions issued by RBI in this resar.ci.

* l) Pro.iected Balance Sheet l\4ethod (Current Assets rninus Current i.iabiiities)

- -l) Ctrslr Budget Mcthod

:i -+i Cpcraiirrg Clui. ivi,;iii..,i <ryl1! 5) Maxintum Penlissible Bank Finarrce (MPBF) (1-onclon Cominittee)

{) 4.1.2. Many banl<s have infbrrrrecl that thev aciopt the Projectecl Annual Tunrover lr4ethoci bascri

S on Nay'ak Contrttittee's recotrmendation lor assessmeltt ol rvorl<ing capital of KIs uncier N;lSl::

segment (Para 2.6.,{ refers).4*

f, 4.1.3. Orr the basis of anltual accolttrts o1'20 Kls. it has been obsen,ed that all I."ls ar"e 1'rr.:r.;riilr,nrenaring their Consolidated Profit & Loss Account and Balance Slieet in respect ollexiiles airLitL' ttolt-textiles segment. Whiie Manufacturing/Trading Accor-rr-rt is being prepared segment u,ise lirr

S textiles and non-textiles separately. Further. it has been observed in nran,v cases that the tbrrrat ol

q these balance sheet is such lil<e that it does not disclose the ilifbnration o1'cLrrrent ancl non-currerliassets and liabilities r.r'hich is '"'c'i'1, rnuch reciuired fbr deternrination o1'u,orliine capital. l-his ol'f rr:r:

3 has rvorked out rvorking capital based on consolidatecl balance sheet of these 20 KIs for the perigri

-.r of 2013-14 to 2015-16 biltrrcatittg assets and liabilities into current and non-current assiets and+' liabitities to the exteltt possible. The balance sheet method (current assets ntipr-rs currelt liabiiities)

5 will give results of requirentent of overall r.r,orking capital covering khacli arrd non-l<ltacii aclir,ities.

3 4J.4. For more specific to khacli operation, this Office has macle an attel-npt fbr assessple6t ()i

S worl<ing capital of 20 KIs Lrased orr'"Operating Cycle Methoci" for overall khadi operation basecJ

; on tl.reir audited financial accounts fbr three years fronr 2013-14 to 201 .-5- 1 6.

3 4.2. Actual Operating Cycle Perioctr (basecl orr Financial Accounts)

av 4.2.1. An atternpthas beelt ntade fbru,orkingoutactual operatirrgcl'cle (in c1ai,s) in rcsJrr--ri Lrl''Jt!

G KIs baseclon thedataavailable fionr theirfinancial accc'runts lorthe period fiorn l0l3-14;o.l(il:.t l6 considering 365 rvorl<ing days. In the absence of specific data rclated to u,ork-in-prourcss ii,v

financial accounts, u,ork-in-pr'()qress lrolding periocl has been consiclered based on KIs'replic:.3 exceptChaspara Silk Samity. Natra.j Khadi Silpa Sanrity and Daulatabacl Silli Khadi O (iranr Seiir

S Sangh. In these three cases. rr,orl<-in-progless holding period is abnctrrnallv ver\,,hish i.e. li5 cfuri,

t8

Chapter- 4

Methodonogy flor Assessment of Worfi<ireg Capi'raI

a

5

1t

{i

t!rl

\:q

*4,

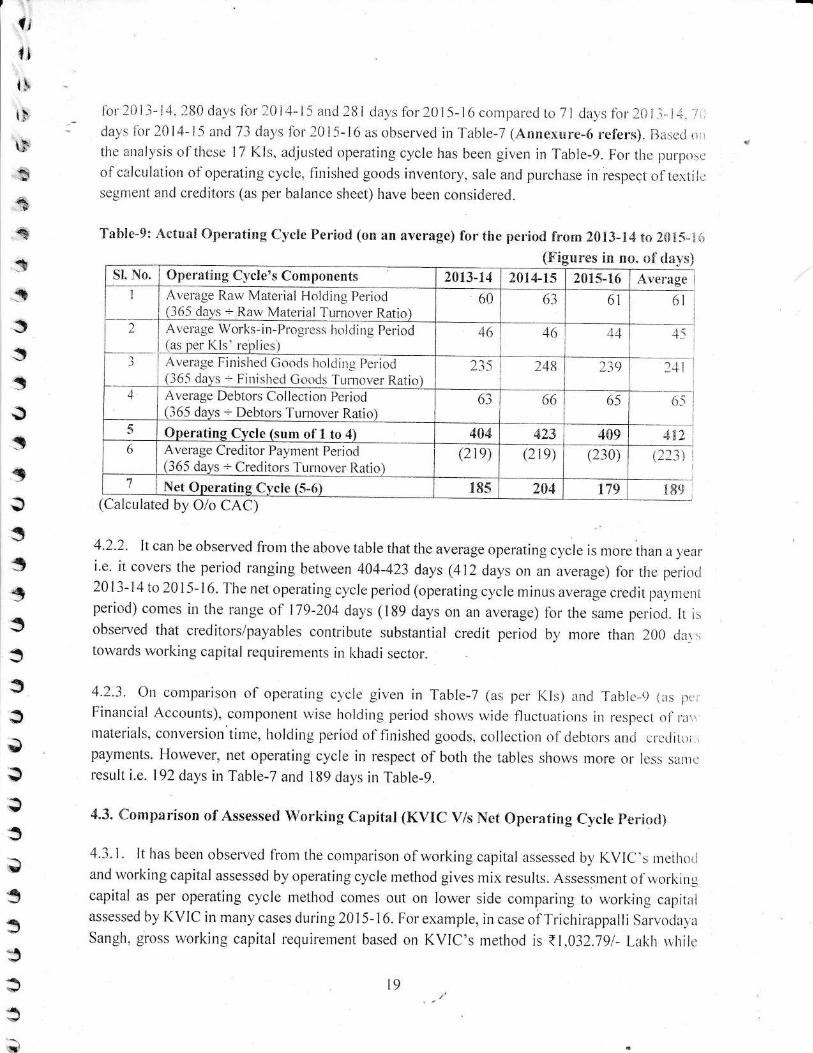

lbr'li)i-l-i-i.lti() da.vs li.rrll0i4-i5 i.rnci .l8i clals 1or2015-1(r coltrparecl io 7i ciar.s lirr-li)l r; l i.',Ca1's lbr 20lJ-15 anci 73 cJa-t's lbr 101-i-16 as obselvecJ in1'able-7 (Anne-xure-ir refers). il;.i.,,cti l,tire attalYsis cil'tltesc l7 KIs. acl.iirsted operatirrg cycle has been given in l"able-9. Fror tlic psr-p(.):iil

of calcLrlation oloperating cvcle, finislted goods inventorl,. sale and purchase iri r.espect o1.te.riii,.:sLrgnrelrl and creditors (as per balance sheet) have been considerecl.

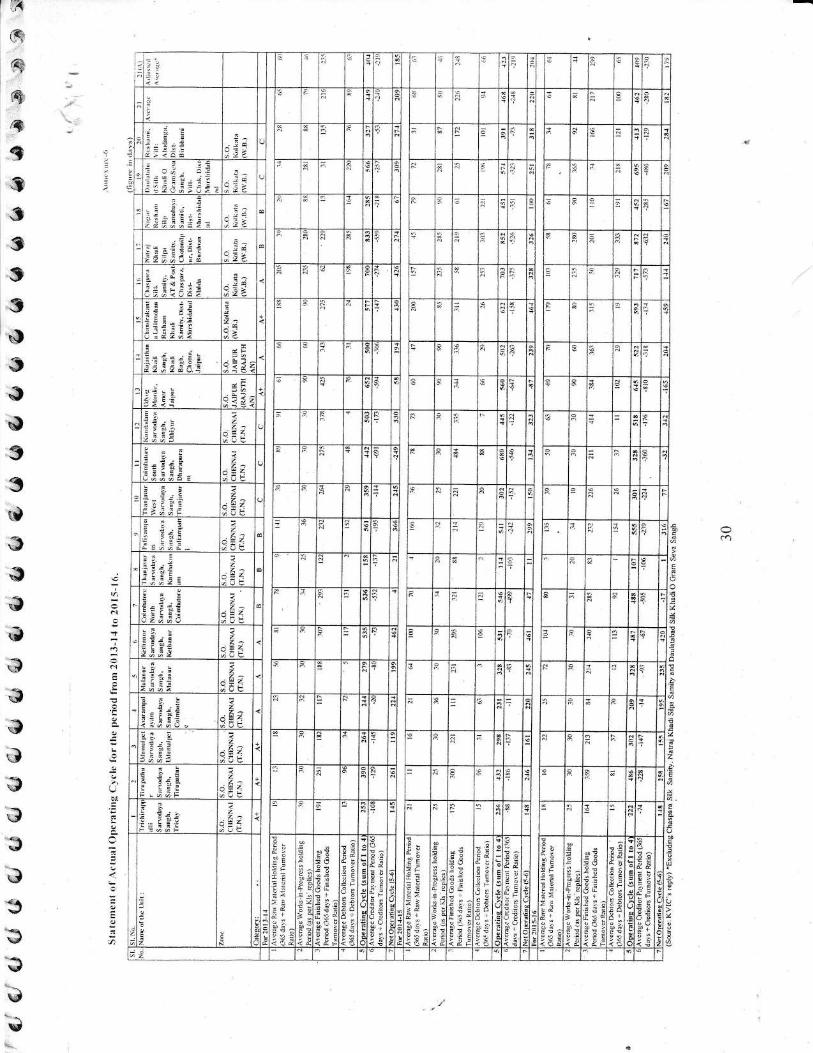

T'able-9: Actuai Oprerating Cl1,ctr* Period (on an average) forthe perioctr f'nom 201S-X4 to Zili5,l,r(Figures in no. of elavs)

st. t\o. 0perating Cycle's Components 2013-14 2014-15 2A1s-16 Averagel Ar,erage Rarv Material Holding Period

(365 davs - Itarv Materiai "l-urnover Ratio)60 63 61 6l

) Avelagc- Works-i n-Pr"ogrcss hol dine Period(as pe'r Kls' replies )

46 46 41, li

J Average Finished Coods holding Per.iocl(365 da1's - Firrished Coods 'Iuntovcr ltatio)

2.3,s-)10-?() li9 t"i 1

4 Average Debtors Collectiorr Pcriod(j65 days - Debtors Turnover Ratio)

6-i t)(-) 65 r.{

-l Operating Cycle (sum of 1 to 4) AAA+tr+ 423 /809 nn-o Avelage Creditor Pavlrent Period

(365 days -- Creditors -lulrrover

Ratio)(2 re) rllq) (230) /11:) i

1 Net Operating C3,cle (5-6) x85 204 179 l8{.}(Calculated by O/o CAC)

4.2.2. It can be observed fi'ortt the above table that the average operating cvcle is nrore than a I L..rr.

i.e' it covet's the periocl ranging between 4A4-423 days (412 days on an average) lbr the per.ic,ii2013-i4 to 2015-16. The net operating cvcle period (operating cvcle nrinus average cre,lit pillprcpipeLiod) comes in the ratlge of'179-2A4 da1,s (189 days on an average) fbr the same pei.ioct. Ir i:observed tlrat creditrlr5/payables contribute substantial credit period bl,nrore than 200 r.lar,tou,ards rvorking capital requirentents in ltltadi sector.

4.2.3' Ott compat'isotr o{'o;reralinu crcle sivot in Table-7 (as per I{ls) tnd 'l'al-rlc-9 iris pr,Financial Accounts). conrponeltt t,r,ise ltolcliug peliocl slron,s u,ide f'luctLratiolts ip respcc,L oi'1i..materials. conversiotr tirne. holciiltg periocl of finished goods. collection 6{'ciebt6rs anr,i ir.i.iilr,;paymettts. Horvever, net operating cycle in respect of both the tables shoq,s rrore or lcss sair,:result i.e. 192 days in Table-7 and 189 days in Tabte-9.

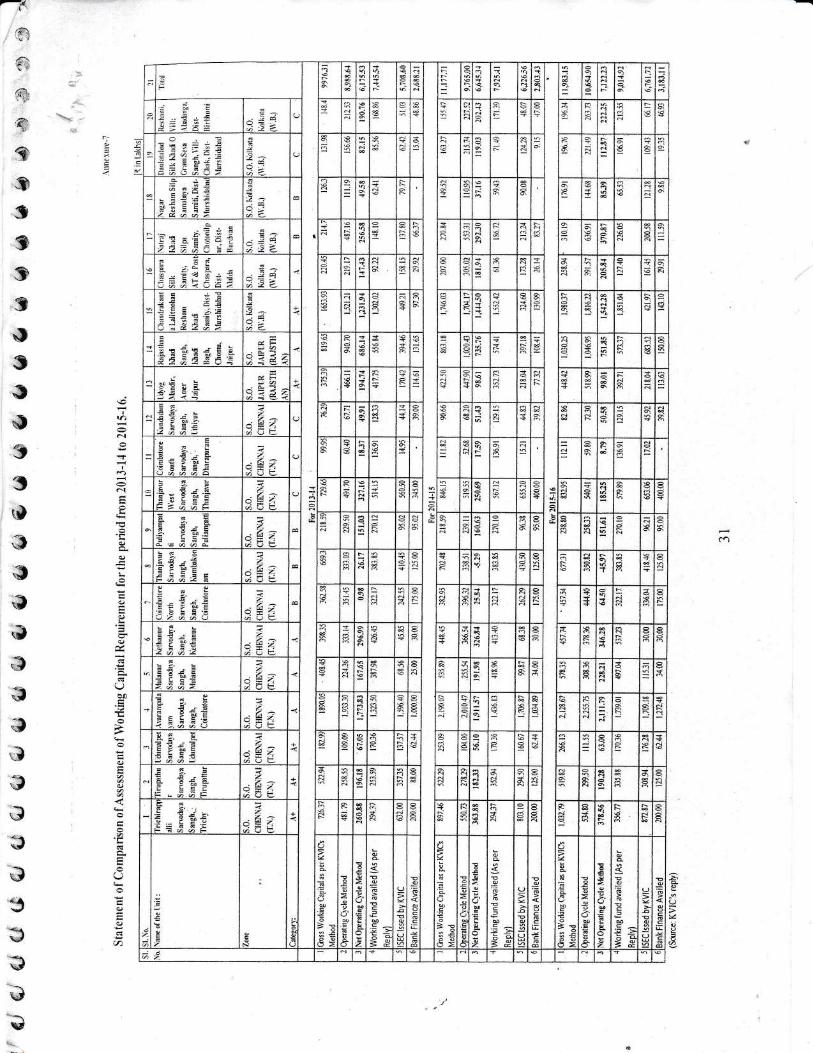

4.3. Conrparison of A.ssessed \4/orliing Capital (KVIC V/s Net Oper:rting C.vcle period)

1.3. I . It lias been observecl h'orrt lhe comparison of working capital assessec'l i:y KV IC "s rr rcti rrr, r

and rvorkitrg capital assessed by operating cycle rnethod gives rrrix results. Assessmeltt of g,orkilrlcapital as per operating c1,cle rnethod comes out on lorver side conrparing to work.ing capitr;assessed by KVIC in man,v cases during 2015- I 6. For example, in case of Tricltilap;ralli Sarl oclar a

Sangh,,eross norking capital requirement based on KVIC's nlethod is {1.032.79l- Lalth uhilc

$Q

3S3J:B

6$

\,

3353335o1\,

Y!

G

5j

It

j

'j

t'

19

!,

1t

It(1.

l!\"8

?t\

F

33%

333J:+

qJS

3sq

<t

3f+v

lrrosst'orkingcapital :lsperoperatil.lccvclemethridist534.S0/-[-aliitduliirg20l5-]{r. Iii,',ie',t:i'

of LidLrnraipet San,oda),a Salrgh" qloss rvorliing capital reclr:ireiitcnr as per I.,\'i(- is {l(r(;. i I - ,.ri.:,,rvirile;.rross wor[<irig capital .ts i]er opcraiinq c1,cle r-nethod is {lil.-5j-i,aliir (t(r-i,,- i-a},lit ,',.r:,i:ij ,;,,

net operating c1,cle) (Annexucn-7 refers).

4.3.2. KVIC assesses u'orliing capital fbr u'nsuirr6l year based on lrest higher sale/proclur:tion i a]ur:

anlong last three years b;- etiitrncius 209'i, ther'eon as targel.'fttis target is taken ils i',as;e lgr'detertrination ol u,orkitrg capital [rasr.:rl on the irrrnrula t'ecor-irr]tencled b1, Shri Il.R. )i,lclti.i

Contntittee and Slrri S.f.. Kalia Conrntiltee. fhis formula does not consirtrer fhe openatiug r:-r'ck.

of KI. As sales ligure inclucles profit element u,hich is not part of operationatr cost ulricir i:-

countecl in eristing mefhod. Most inrportantly, the existing KVIC's method does not consiclerthe available inr''entorv level of finishecl goods rvhich is readilS,available to nreet out tlte salcstargets amcX cnedit;reriod frrr trade pa1'ahles n'hich is one of tlte source of financing lr,eirkipgcapital.

1.3.3. Net operating cvclc rrretlrocl cr)vers the aspects of inrrentor),. creclit preriocl arrrl crl:lelemettt-s rvlrich eives fair results tou,irrcls irssesslrelrt oirvorking capitai ii hich reqLrire iir sper.aiirircycle. A colttparison olass;essecl u,orking capital under KVIC's metl'lod altri nr:l opeiuiinl r,r..,cll

method in respect of 20 KIs iras been gii,en in Annexure-7.

ea

G

'3

33

-:

20

rl

lt4t

rl.

rI

tite-.+

es*p

sS

$J*q

\J

S

5,E

5333J)<rY

5a53-|t

j

3].,

Chapter- 5

Itecommendations

5.1. Working Cailital Assessment &{ethod

5.1.1. As ex1:lair,er.l iit para 3.1. KVIC. determines the eligibilitl,'of norl<ine capitai b.t,iepor.iirrnegati\,'e clif-ference i.e. excess olu,orlting capital fund arrd issues norking capital cerlillcates L1t(irji.ISE('sohente aggregiiting o1'net rvorl<ing capital plus arnount of banl< fipalce rvhrch res,*its i6tr,superfltlotts assessment nf rvorl,iing capital requirement in iStrC scheme. The exces:l i].iil(!trlr:'of, rvorking funcl is parf of n'orking ca;lital anc! should he cossiriercd for irsse:,ilirlretrr{ i,flr ul'l;,irr g cre 6rii;r I rcr-tr u i rr.nr e-n t.

-5. 1.2. It is reconrntended lhol lhe producliorr torgets of cliffircnt l{Is mrt1, be .fi-ved ls.t, f{l.likeeping in view lhe soleoble invenlories of finished goorls o_f'khadi Tl.oducts olrectd-r ut,oilui;i,::witlt the fils. For assessitrg the w'orking copitot requirementfor procluc(iott largets s6.fi-ued, itctopero{ittg c.l,cle as cliscusset{ in Chapter-4, inv'entot"ies onfl others relet,utrt .fuctors skould h .

luken into considerotion. The net operating c1,cle mult be menlioner! in lhe ISEC issucriprominentllt.for the infornration of the banks.

5.2. Froforma of Financial Accou,ts of Khadi I.stitution

5.2.1. Preselttlr'. all KIs are preparing their Consolidatecl Protlt & L,oss Account ancl Llaia,c,:Sheet in respect o1'textiles ancl tton-textiles operational sesrnent rvhile Marrufacturipg/ Tradir;rAccount is being prepared separately for textiles and non-textiles segment. Since balanc:e slreet i:;being prepared by colrsolidating textiles rtnd non-textiles operational segnrents. / woulrf he ntot.,,opproprinte if the frinctnciul Acc'ourrts i.e. Manu,frtcturing/ Troding ,4cc6unt, pra./it o[ .f-r.,;,Accortnl und Bolonce Sheet is prepured.for texliles anrl non-texliles seguteNtts sef){tt.{ttr:{.r,,rt,!.0,tlte bi.furcafion of koltdi ond non*khutli operaliort ulong witlt t,ott:,^otidutod "fittoti(irtf ct'1euii,,.for assessnrent of working capitul uncler ISEC Scheme.

5.2.2. Fttrther,presetttformatofBalanceSheetol'KIs(olteratinginRa.jasthan) tJoesrrprrlisci.:r,:the infornlation about ctlrrent ancl non-current assets and tiabilities l,lriclr is rrr ir;it.rt,l,reclrtirenient for assesstnent of u'Orl<ing capital. T'herefore, it is also suggested thut Ki;!{ *uttdevise a new common formul o.f /inuncial occount, specifiatil.t,frtr bulance slteet spec.i.{.yirl:cLtrrant utrcl non-currenl ossets and lisbilitiesforfoir ossessment of working capital under.LtgaSchetne.

:

5.3. lnventor5, o1F-inished Goods and Creclitors Payment

5.3.1. KVIC detertltines tr'orl<itts capital fbr ensuing y'eal based on best hieirer sale/prciriuctiorr

21

l!

)

:

:.

,l

\

3*\}

3t

S

3J3J*il-<i

J3353II

.r,alue rlurirrg the last three l,eiirs b1,enhancirry20% thereon and lrxes targct trasecl oll thc iirl"ilrLll.,

recor.rrnencled by D.R. N{ehta Comnrittee at 1389; lbr cotton. 195% 1ir rioolen- l.',-19,n ii)| siii.

arrd ll11Zn 1br polyvastra. Sales ficul'e inclLrdes cost and prolit eienteitt. Ilrtlfii is tloi iriil.i ir:

operating cost br:t is consiclcred in this lirrntula. This lbrmula cloes Itol cousicler the lirrtiirll',i,''

irrvertorl,of fipishecJ goocis (at the beginning o1 the year) and holdrng creditors pa)'rrerlt pci'iori.

Therefore, it is suggested thal cost of goods so[d,.finished goods inverttor.r attd credit periori

allowed h),creclitors moy be consiclered.for proper ilssessntent o.f rttorking cupitul requirernenl.

S.4. 1V[arket Development .Assistance lluterest Subsidy/Rebate from State Eo*rds

5.4.l. Khacli Institirtiorr.c alsr:r shorv accrued lr,lDA/lnterest Sirbsiclvll{ebate fl'ont Siatc

Boarcls/KVIC in tfueil balance sheet. Due to the inherertt s)'stelll in the KVIC. rebate is paiti to tht:

institutiorrs orriv aftcr proper che,cl< br.the irrternal Audit N4echattistt-t. F{V{C mrt.l'crtrtsidcr r{

.follow, rqt the mofier *,itlt Stute Governrnettts.{or expeditittg releuse o.f 'R.ef;nte Dues".,{i'ottt l!tt'

concernerl Stata Goy'ernrnenr.s, tt,irich would e{{se oul the positittrt o.f avuilahIe ntarliiu{: fitnri:,

utith I'itrs.

5.5. Others

-i.5.1. Kalia Committee suggested that in case K\ilC's assessmeltt of rvoriiing capital exccei,is 1i..,-

banl<s assessmeut by more thau l0%. the quanilnrl o1'u'orlting capital nral bc: at'rived b1' 11.,. iriLitttrti

clialogLre between the Institutions/KVIC and the fitiattcing banks. l'his issue mat' be taltett Llll l-,''

KVIC witlr their lssociate bartlis.

5.5.2. In case assessment o1'rvorking capital bi,KVICl rraterially differs fi'onr the assesstrellt r-rl'

rvorl<ing capital nrade b1, the banks, the issue uray be taken r-rp by KVICI rvith Indiarl LJanli:i

Associatiol (lBA) as u,ellas n,itlr RBI. and the area of differences call be reconciled/resoli'ccl.

5.-5.3. Though various iltstrLrctiorrs have been issued to bauks regarding sanctity of I'"'i'l(assesslrept olrvorl<ing capitai requirerrent of Khadi units. the sante \\/as not llLtncl to bc billilirrg

on the banks. It r,r.,as suggested tliiLt irr ci]se an), dillicultf is faced bv tranlts itt sauctionitrg llli: lorrt',

as per ISECIs issnecj, banlis shttulci lefcr the matter to KVIC so thitt ihc tlill'ercnccs I'oLrlti i-"

resolyecl through discussions. This is ruore t'il less ignored b-r.- the banks ils Per tiic ittlirt'irlrtii,i:

gathered.

5.5.4. I(VIC issues ISECs tror net requirement of r,vorking capital atier settirlg o1l tir,: liitr,-i::

provicled by l(VIC ancl under Consorlium Banl< Credit (CBCI). In has beett obsen'ed itt stltlc cas,:,,

that I{VIC issuecl ISECs 111:5111111. Ils rr,here there rvas no lvorking capital reclitirenre-tlt liittl lli:il

ISECs tilr Irigher arlloLurt against thc assessed rvorking capital. trt is recorumenrled ttrat K\il('shoulrl assess the u,orking capital requil-enrent of I(Is properly'and restrict the alllotlrlt lcl-

issuance of ISEC on a case to case basis after proper analysis of rvorking ca;ritti

requirements.

5

-,3{fY

3!J

33-*

a3

r)(l

\1

\:,

\ i'

\F

3

3ee.\l;

{.-f

$$3s*q

J3353553J3{r

3a53333

:,i.:).-). l lrc:;toci<s ol'lr-hadi [-lrtits tniry be monitored at eaclt stagL'()f productioti to avoid erccssi', r:

blocl<iige o1'f irncjs. 1\u)' accunrulation ol'stocks at intermecliaie stages such as tt'crtiittu rrtl'i

vastragar etc. rra1,'L:e regLrlarl_"- urotritr--,red through proper MIS so as 1o avoid sttch blockauc'r,;

-rvorl..ing carriiai.

(8. lj i.i tr clffr:t I t:, a tiln ; t,/,ad', iscr' {( 6r,r ,

01.01.:01 ::

,/

,J

*$q_\J

.-,

'3&-}

''!r

3&,:t",.:,

s

r t!rl

Q.\.'

il'

L.'

G.;l

rf,'!I!.

e

\}qA

ui

?39

3I1'

533

&*Y"'^

h*""1""i""ttt\

S{udv Reference

8t.qq. :rrHuq'-r:"rtg. irr.j'''l'.' ai'"1

B H. ANlt- KtJMAR. r;rt,ia],*l Sectslal y

At il lr .\ <" e{ *"1*- l<5*{

-r.L--- r..-b\1\' i -\'\'' ,f \'fr

: t\**- O\, InC LPnIral tJOVt'rnmPllI Inr\ l.yt b' J ,Ut - a

je orovided undrr the scheme-y t**-'; '

Anneure-1

Fi: rd"r\lAi,rr.1tu-.ri.\':r. 1'u

IItr=IIIgrra. :_i ;'r i: i:r li,:

:l:.i:-'ir' l:'i " i:rrr' " j'

.{t:{il it {-.F;qq.eq, drg 3fit r{Lrrq r{flrl rI-Jt..lrl

srnq .raa -i-$ {}--d}- 1 10 6 j 1

GOVrRtaJtlE&lr cF tNDtn

MINJSTRY OT

MtcRo. st{tAtt. "qNat MEDtt,M Er.ll ERPRlsESuoYo{; BHAWAN. r*EW OELHl.lrf S11

1 ."i,

35

i Rmm No. 171, Udyog Bhswanrel .S'1 11 ?-3O€!543, fax +91-11-23OS2858, (-mari

New D6lhi-11OO11: ,[email protected]. Vdebsrte: ffi rrsrlle qov rn

E:r:1'r{k"fitr#Bdh';:ti

,:4J.!.d.:catl!.q:i-t: ..ri

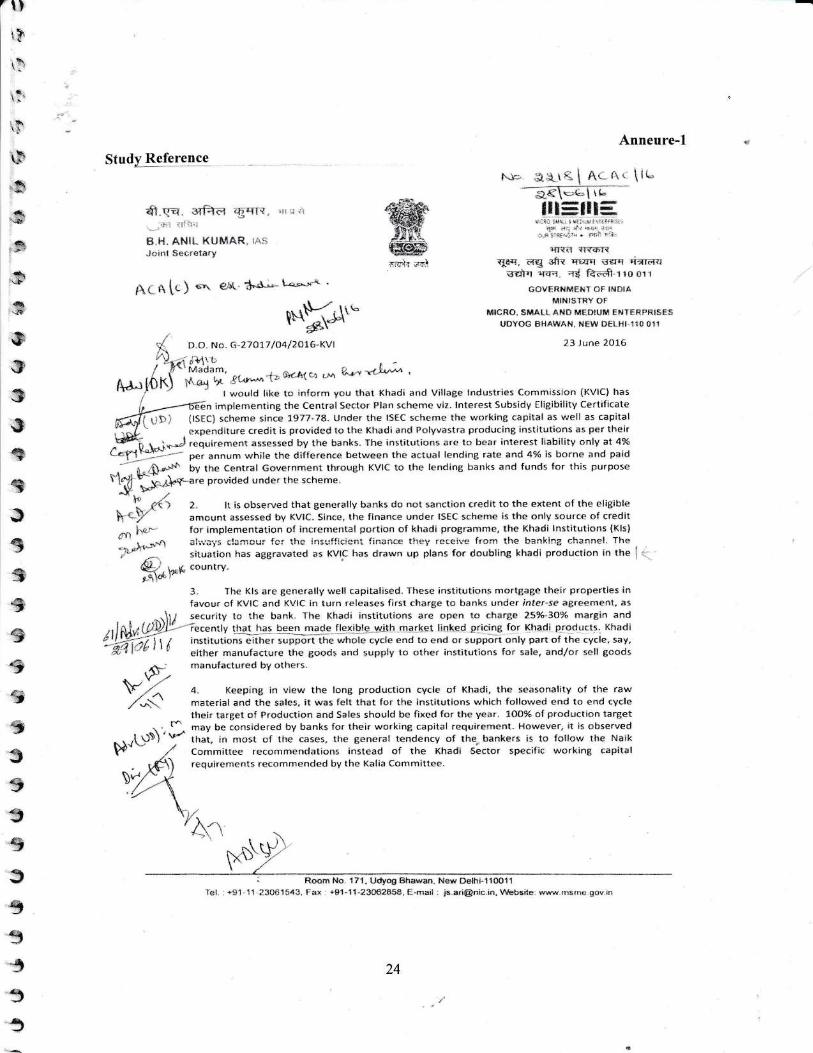

in imptemenring the Ccntral Sector pian schemc viz. lfiterest Subsidy EliCibilitY Certiflcate

i15ECi scheme since 1977.78, Under the ISEC scheme the vrorking capil.al as well a5 c.apital

cxpe .tditure credit is provided to the Khadi and Polyvastra producing institutions as per thL'i{

r-i*.J rcquiremeni :.::"::ll}li: iiT'. llilii':'::::::: :::i"-::::.1l':i'.:i'l:tj':::.:i:"-1IC_..l,1!)Al: o;;;,,"r; whiie the diifu.en " betvreen the actual lending rete and 47o't.o"ltl: and pa;cl-,L,i)..r+ by the central covernme,rt throuBh KVIC 10 rhe lending banks and funds {or lhis purpost

'. ii, 2. ltisobservedthatgerrr:rallybar-rksdonotsanciioncredittotheextertof th€Eligibteamounl as'e5sed by KVIC, Sifl(e , ttre finance under ISEC scheme is the only sourcr o{ creditfor inlplementation o{ incremental portion of khadi programme, the Khadi lnstitutions (Kls)

;iri';i': ll:;i:cur fc::hc i:rsuilicicni fina::e they rcleivc frr:n: tlre banki:rg ch:nnc!. Ths:

situation has aggrav:rtcd a5 KVIC has drawn up plans for doubling khadi production in the

&. ,,*,, ';;;;*t qr'r '

3, Th€ Kls are generally well capitalised. These institutions nrortgag€ th€ir protlerties infavour cf KVIC and KVIC in turn releases first charge to banks under inler-se agr€emenl. as

_,\i; serulty to the bank The Khad! institutions are open to .haree 25Yv3Oy" margin and

,,lli,.tllii)ll ' i-rccnrly that has been macle flcxible w-ith market llnked pricing for Klradi prod.r.ts. Khadii)ll-?l'i I t i inst;rurrons eirher suppbrt the whole cycle end to end or 5upporl only parr of thc cycle, say,' *'l'i /t t t t either manufacture the goods and supply to othe, insl:tutions for sale, andlor sell goods

r\ manufatturt'd bY others.\P,\ --

\Y- ,^ 4. Keeping in view the lonB production cycle of Khadi, the seasonality of lhe raw,

,r'*).' rnatErial 6nd the sales, it was felt that for the instatutions which followeC end to end cycletheir targ€t of Production and Sales should be fixed for the year. 1OO% of production target

. . f. *"y be considereri by banks for their working capital requirement However, r1 is observed

.,-,[5)}J'v- that, rn most of th{] cases, the general tend€ncy of t[re, bankers is to follor,,r thc Na,k

W - ,1 Committe€ reconlmendations instead of the Khadi Sector specific working capital

. lY{n) requirements recomn:ended by the Kalia Committee.

\r7'.r--,/ -,\'l-z' \ \'\ ,.

/ k -./,', , , \(\il\ $\'' /

24

;*11 r,$/iadarn.

*it,*' Xt**'t> e{*{ca ti'\iw,culd lrke to inforrn you that Khadi and Village lndustries Comrnission (t<Vlc:l has

D.O. No. 23 Jrrne 2016r

b

p

3

ll'

rq

c\

i6r;&;

.9

q+

*i*

q\r<tD.

*fe}.J

sa-t

sJIssJ

:,

353I3,5

.3

I55q

3

5. ttecently, KVla hn5 acjopted flexible prie!nB prlliLy by which khadi ir'istit!,tiont are {ree

to add margin over a,ld above production cosl and there'fore, they can sustain th€ir sctlvity

to the ex!enl o{ 1o0?i oi ttreir turncver under this scenario. Larlier a55e55rnnn1 had rvnrked i

out higher vvo.kinE capital thaa the production cost and because of vr'hich bank: are i

r€luctant to provide working capital to khadi institutions. The tendency o{ the bankers to

adop! Naik Comrnittee recommendalions needs to be restrained and justificatic'ns to b€

devised facililatinE extension o{ support to Kls, as suggested abave, if not lolallY on the

rrctur$rrlend3tion of Xalia Comar!ittee.

6. yoit are there{ore, rcquested to institute a stlrdy in the requirefilert of the r.vorking

capital by CAB.

\ryith regards,Yours sincerelY,

A

L ,. {"" .-I B.H" Anil (umar ]

Smt. Aruna SethiPrincipal AdviserDepartment of ExpenditureMinistry of FinanceNorth Block

New Delhi - 110 001.

25

'.t',

r.l

n

:o

o

:\

{

tr

c

*l'^1

lI

NIt I\a:+

xN r ;1 J x

oxrN N

rN

rN N

d *NI

I

I

mixl

d+oN

E :;l!^l

;.:+

> x x $ $ dc dxoc N

;( ; $ sN ili

i

ill i

II

od

* ;i sN o ;{

F V € o $$ t\N

;{ xN

>i N

uc o $l

*i.Ee

aqaN

d tr

^i

;;l

I

I

oi .ii

o c N

( No

N O,o"j ..i o o il

i

U

9E.a

c r r d o o oodi

Id

q@

oF€

6 rN

6 3'1-d

C

o@

a6oo

I o6i

oo N

ddi

od

@

.i Ici

oui

6 c N

I fioF

r r@

sni

oui 6:

oN

1N

@oio

YC6r;t!Eo

(c o r

N 8ri

IN

8CJ

d @ @ N o o

!lu

:{.9&

d

6tr

FN

oFN

rd

c6l

u

ri(F

stri

NCJ 6

N no6i j

or6

ao

U

tQ.4tbi!E.g

c rN

{ o oru o o

nn

.. ! uq A'.

6i

tr

6

o6

.io .ioo

nF s

ri NIui@

d N 6rN

o(( cA d

co( tri

i ^i qiN4i @o

qlol

I

@

Ya6:L>: OY9Eo

o o € r o EF

tF

( o € r ( g a F

o ,.!!oraI d-Y

E <';"d

d N tri ria,1

c G

F

c @o dio^i N

1(o6

Nci

( Nao

do$

F@o

UYC6rbe.9EoL)

6 c r N c c! or@

q o o o

Ecfu

8e

N

rF

d .iN

c od

6

e

qci

ts otru

c €di r io tr

oci d c

odi

q(oq ( N oi ^ic

(o

YC6t;;9E.l-a

o o € ts 6N IN

IF

€ c 6 @ N a oFt

ET

"daEE

!

!

d

ntE

=

I

!d

!

tgEUts)

c

If

zio

cT

'id

o

-I

Ic

o

:

I

iI

so!+

s!

or

Ej

n

oT

o'kI

!

!c

iz

a'iE

o

5a

F

iI

d

E

o&

!ct

I

t.9Eo

!c

zOJ

<

z'aoF

'l(,

f

Uots

!

o!

!c

c c

a

IfEf

;6o

io

!c

a

co

zN1F

cz

zNJdFz

trzcF

L

Fgcz

zoNF

zNF

I

zoNfF

oz

@ c ( tr c @N

;N

o o

t)$\?

,*i\}

.F

Bt-t '

R*'

;Ij

*'i

€q.r

$\J,

s\5Ga.,

s&3?3J

933s53Ie35333

6i

a

c

o

oNo

oN

oqTEo

oq

o

o

c6oE

EocoEcoqE

ciiq66!EoU

oooocloE

iou@c

t.L

o

q.9;a

rl : ,.) ./i;

-

== L ; |.. ; z

a.

27.

=

=-.) )" -

,.;a

tl9

l)

.iq

,: ;+ q ?:

;: .a 9

a>F

7?

q a *€ a

=a 9

=I :a$

a'.; B 1

a aI

a a