textiles and clothing presentation to parliament portfolio committee 18 may 2005

TRANSCRIPT

Global Context

• In 2003, global textiles and clothing exports were valued at US$395 billion, making it one of the world’s most traded manufactured products.

• The global textiles and clothing value chain is a buyer driven value chain, dominated by large retailers

• Retailers do not own their own factories, but rather organise and control production on a worldwide basis

• Retailers are driven by changing consumers preferences and demands in terms of quality and price.

• Consumers’ demands have lead to retailers sourcing production from the lowest cost locations around the world.

• While price is still the primary determinant in terms of sourcing, quota elimination means lead times, quality, reliability and flexibility will be important aspects of competitiveness within the international value chain.

Dynamics in SA Textiles and Clothing Sector

• South African economy was isolated and in recession - high levels of protection, inefficiencies and generally uncompetitive.

• Clothing and textiles sector was virtually completely closed.• SA decided to integrate into the global economy through the

Uruguay Round, becoming member of the WTO.• Uruguay round required economies to lower protection

(duties and quotas).• SA, in consultation with industry and labour (NEF), agreed to

a gradual phase-down in most sectors.• Clothing and Textiles largely exempted from opening to

competition. • Multi-fibre Agreement (MFA), allowing quotas on textiles and

clothing imports, extended till 31 December 2004 giving nearly decade of notice to industry.

• Longer Uruguay Round Phase down of 12 years negotiated.• SA maintains high tariffs in sector, when WTO sees tariffs

above 20% as high (40% on some products).• SA industry in sector enjoys double protection: tariffs and

subsidy (DCCS).• Tariff protection and DCCS extended several times to allow

industry to restructure.

Dynamics in SA Textiles and Clothing Sector

• South Africa has to operate as part of the global textiles and clothing value-chain.

• South Africa accounts for less than 1% of global exports of textiles and clothing.

• The current challenges facing the sector have to be viewed in the context of increased global competition and inefficiencies within the sector.

• Past protection and increased international exposure has highlighted inefficiencies in the industry – lack of capital investment, innovation and technology.

• The current challenge of the industry given the change in global dynamics is to improve efficiencies in terms of management practices, technological and product innovation, human resources and firm linkages.

• South Africa’s industry is dominated by a small number of large retailers who yield considerable power over the value chain.

• Price and quality is now a key issue in terms of both the local and export market.

Establishment of Technical Task Team (TTT)

• The TTT meetings commenced in May 2004.• It was established based on industry's approach to

government regarding the increase in imports from China.• The purpose of the Task Team has been to look into

factors that underlie industry's vulnerabilities to imports and explore short-term and long-term responses to challenges.

• Initial discussions included processes around safeguards, identifying other short term interventions and industry developing restructuring plans.

• Through the TTT short term measures have been identified and agreed to subject to Ministerial approval, these are:• Safeguards• An interim replacement scheme for the DCCS• Country of Origin Labeling• Addressing illegal imports and under-invoicing

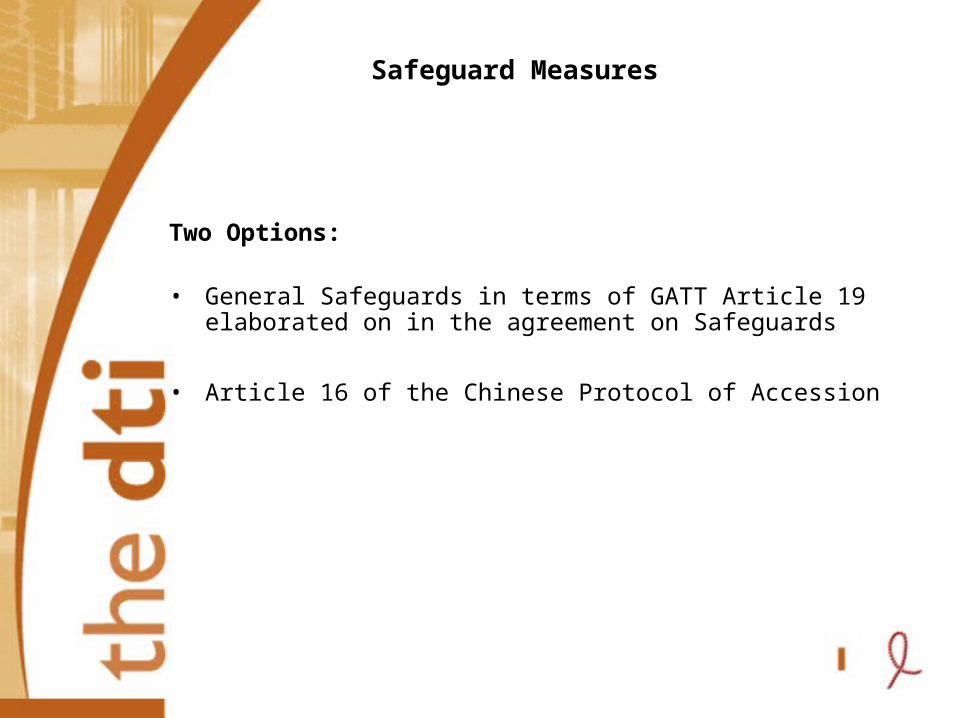

Safeguard Measures

Two Options:

• General Safeguards in terms of GATT Article 19 elaborated on in the agreement on Safeguards

• Article 16 of the Chinese Protocol of Accession

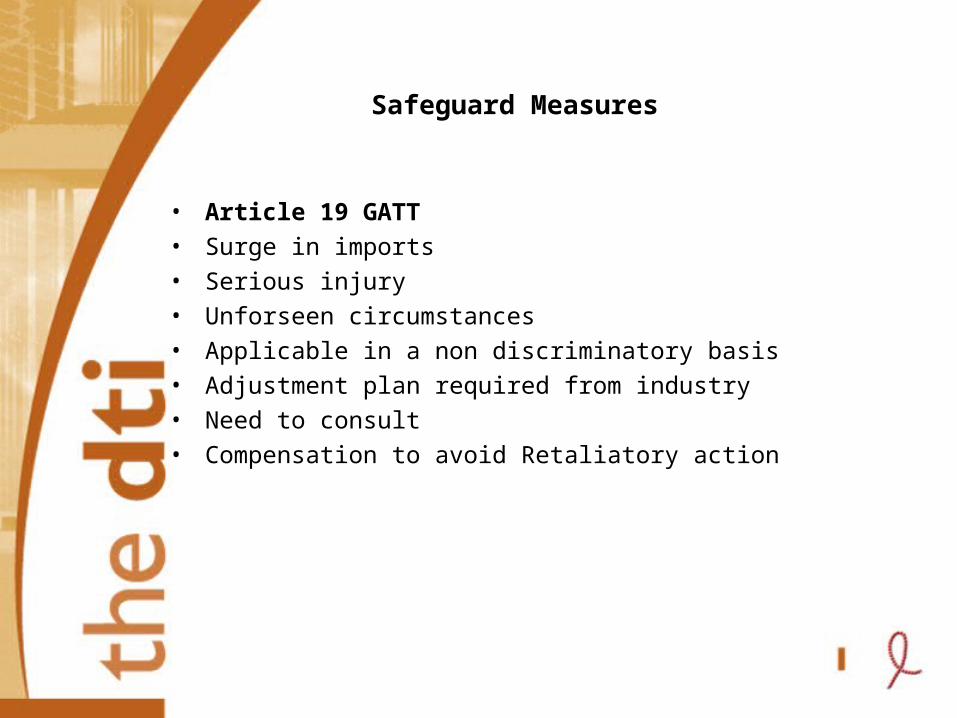

Safeguard Measures

• Article 19 GATT

• Surge in imports

• Serious injury

• Unforseen circumstances

• Applicable in a non discriminatory basis

• Adjustment plan required from industry

• Need to consult

• Compensation to avoid Retaliatory action

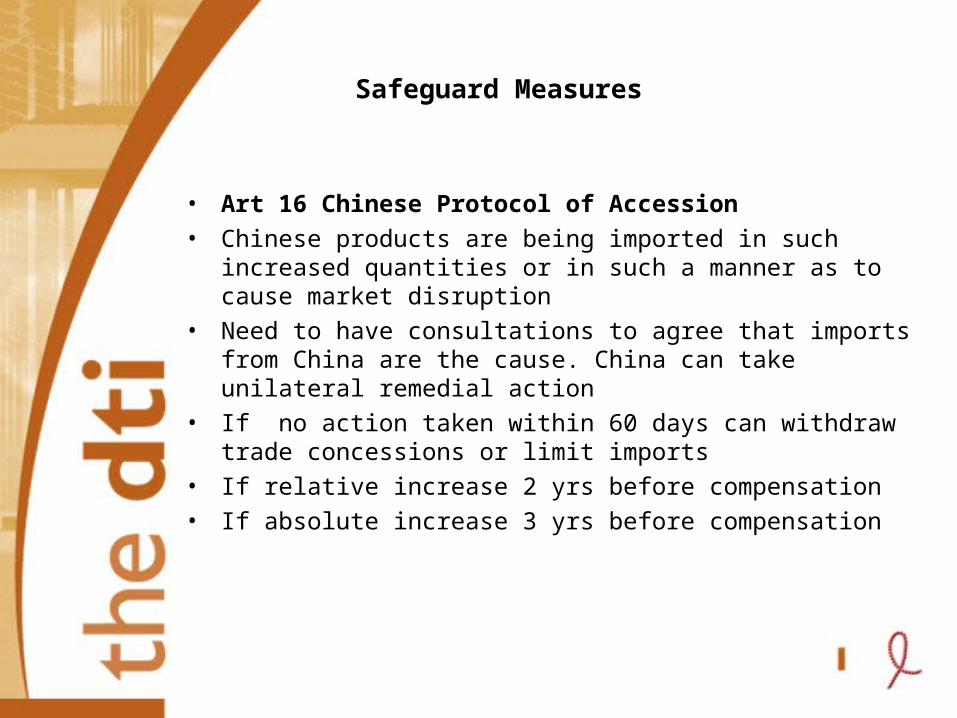

Safeguard Measures

• Art 16 Chinese Protocol of Accession

• Chinese products are being imported in such increased quantities or in such a manner as to cause market disruption

• Need to have consultations to agree that imports from China are the cause. China can take unilateral remedial action

• If no action taken within 60 days can withdraw trade concessions or limit imports

• If relative increase 2 yrs before compensation

• If absolute increase 3 yrs before compensation

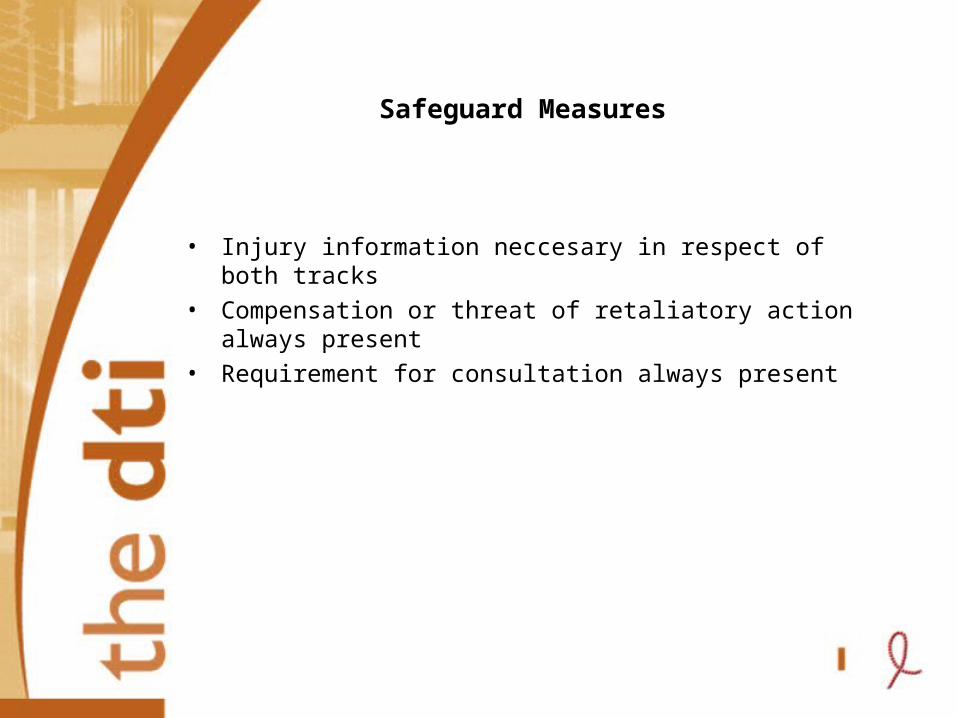

Safeguard Measures

• Injury information neccesary in respect of both tracks

• Compensation or threat of retaliatory action always present

• Requirement for consultation always present

Safeguard Measures

• Industry met ITAC officials for the first time in March 2005 to assist them in preparing an application.

• Six weeks later another meeting was held on the preparations and it became clear that although labor and federations were keen no actual manufacturer was prepared to submit an application

Establishment of Technical Task Team (TTT)

• The TTT meetings commenced in May 2004.• It was established based on industry's approach to

government regarding the increase in imports from China.• The purpose of the Task Team has been to look into

factors that underlie industry's vulnerabilities to imports and explore short-term and long-term responses to challenges.

• Initial discussions included processes around safeguards, identifying other short term interventions and industry developing restructuring plans.

• Through the TTT short term measures have been identified and agreed to subject to Ministerial approval, these are:• Safeguards• An interim replacement scheme for the DCCS• Country of Origin Labeling• Addressing illegal imports and under-invoicing

Long-term Interventions

The Textile and Clothing Development Council

• Forum for engagement between government (dti) and industry stakeholders on short and long-term competitiveness issues.

Restructuring by Industry

• Firm level restructuring in order to compete globally.

Customised Sector Programme (CSP)• Sector development strategy which employs a project-

based methodology to seek high impact and enduring action initiatives.