taxpert professionals presentation by shreya on secretarial standards

TRANSCRIPT

TAXPERT PROFESSIONALS

An AnalySiS on

Secretarial Standards

&

Secretarial AuditBy Shreya Tiwari

on 28th August 2015

Companies Act , 2013

Two main inclusions:

=> Secretarial Audit

=> Secretarial Standards

Secretarial Audit

A process to check compliances made by the Company

under Corporate Law & other law, rules & regulations,

procedures, etc.

It helps to detect the instances of non-compliance and

facilitates taking corrective measures.

It is therefore an independent and objective assurance

intended to add value and improve operations of the

Company.

Secretarial Audit thus provides comfort to stakeholders,

management and regulators as to statutory compliance &

corporate governance.

Secretarial Audit

Secretarial Audit shall include compliances of following law:

i) The Companies Act, 2013 (the Act) and the rules made there-

under;

ii) The Securities Contracts (Regulation) Act, 1956 (‘SCRA’) and

the rules made there-under;

iii) The Depositories Act, 1996 and the Regulations and Bye-laws

framed there-under;

iv) Foreign Exchange Management Act, 1999 and the rules and

regulations made there-under to the extent of Foreign Direct

Investment, Overseas Direct Investment and External

Commercial Borrowings;

v) Various Regulations and Guidelines prescribed under the

Securities and Exchange Board of India Act, 1992 (‘SEBI Act’)

vi) Any other law as may be specifically applicable to Company.

Applicability

As per Section 204(1) of Companies Act, 2013 read with

rule 9 of the Companies (Appointment and Remuneration

of Managerial Personnel) Rules, 2014 the following

companies are required to obtain Secretarial Audit Report:

- Every listed company,

- Every public company having a paid-up share capital

of fifty crores or more, or;

- Every public company having a turnover of two

hundred and fifty crores rupees and more.

Beneficiaries

Assurance of Compliances to:

Companies - foundation for good governance, reduction

in penalties, public respect for brand. Recognition of

company as to good corporate citizen.

Directors – comforts directors as to compliances and

mitigating risk from regulatory or other governance.

Investors – helps in taking informed investment decisions.

Regulatory Authorities – reducing burden on regulators

in ensuring compliances.

Other Stakeholders

Secretarial Audit Report

Only a member of Institute of Company Secretaries of

India holding certificate of practice (Company Secretary in

practice) can conduct Secretarial Audit and furnish the

Secretarial Audit Report to the company.

Secretarial Audit Report is required to be provided in the

format prescribed in Form MR-3. (Rule 9 of the

Companies (Appointment and Remuneration of

Managerial Personnel) Rules, 2014).

Appointment of Secretarial Auditor

As per Rule 8 of the Companies (Meetings of Board and

its powers) Rules, 2014, Secretarial Auditor is required to

be appointed by means of resolution passed at a duly

convened Board meeting.

Resolution for appointment shall be filed with Registrar of

Companies within 30 days in E-form MGT-14. [Section

117]

Period of Office: The Act is silent – suggested to be similar

to Statutory Auditor appointed under Section 139 (10 years

whether Secretarial Auditor is a Proprietor or a firm)

Obtain consent of the Secretarial Auditor

Secretarial Auditor can be appointed by passing resolution

in Board Meeting.

Penal Provisions

As per Section 204(4) of the Companies Act 2014,

If a company or any officer of the company or the

Company Secretary in Practice contravenes the provisions

of this section, the company, every officer of the company

or the company secretary in practice, who is in default,

shall be punishable with fine which shall not be less than

one lakh rupees but which may extend to five lakh rupees.

Fine of not less than one lakh which may extend to

five lakh rupees.

Secretarial Standards

I Board Meeting (SS-1)

II General Meetings (SS-2)

Why SS ??

In India there are approximately 10 Lakhs companies

out of which 7000 + are Listed in Stock Exchange.

This number is the largest in the World.

With the advent of the secretarial standards, as issued

by the ICSI and approved and notified by the Central

Government, a uniform framework of procedures and

practices have been prescribed for adoption and

adherence by the companies which will function as a

facilitator of good corporate governance and

compliance management.

Provision

As per Section 118 (10) of The Companies Act, 2013:

Every company shall observe Secretarial Standards

with respect to General Meetings and Board Meetings

specified by the Institute of Company Secretaries of

India constituted under section 3 of the Company

Secretaries Act,1980, and approved as such by the

Central Government.

Every Company shall comply with SS-1 & SS-2

Applicability

MCA has notified the Secretarial Standard 1 (Meeting of

the Board of Directors) and Secretarial Standard 2

(General Meeting) vide Letter No. 1/3/2014/CL/I dated

10th Day of April 2015 which will be effective form 1st day

of July 2015.

Further, other Secretarial Standards issued by ICSI in

line with the provisions of the Companies Act, 1956 are

under revision to align with the provisions of the

Companies Act, 2013. Accordingly, such other

secretarial standards are not applicable presently.

Applicable Date: 1st July,2015

Definitions

“Invitee” means a person, other than Director and

Company Secretary, who attends a particular Meeting

by invitation.

“Maintenance” means keeping of registers and

records either in physical or electronic form, as may be

permitted under any law for the time being in force,

and includes the making of appropriate entries therein,

the authentication of such entries and the preservation

of such physical or electronic records.

“National Holiday” includes Republic Day i.e. 26th

January, Independence Day i.e. 15th August, Gandhi

Jayanti i.e. 2nd October and such other day as may be

declared as National Holiday by the Central

Government.

Definitions

“Original Director” means a Director in whose place

the Board has appointed any other individual as an

Alternate Director.

“Time stamp” means the current time of an event

that is recorded by a Secured Computer System and is

used to describe the time that is printed to a file or

other location to help keep track of when data is added,

removed, sent or received.

(SS-1) Steps involved in conducting

Board Meeting

Notice

Frequency of Meeting

Quorum

Convening

Attendance Register

Passing of resolution

Adjournment

Minutes

Disclosure

Board / Committee Meetings (SS-1)

1) Applicability:

Applicable to the Meetings of Board of Directors &

Meetings of Committee (s) of the Board of all

companies incorporated under the Act.

2) Exemptions:

One Person Company (OPC) in which there is only

one director on its Board. Kindly note that the OPC

having more than one director shall comply with SS-1.

Applicable to all Board meeting of all companies

except OPC.

Board / Committee Meetings (SS-1)

3) Convening:

a) Without requisition of Director: any director may

convene the meeting.

b) With requisition of Director: Company Secretary or

where there is no Company Secretary, any person

authorised by the Board in this behalf, on the

requisition of a director, shall convene the meeting of

the Board in consultation with the Chairman.

4) Adjournment:

Chairman having power to adjourn Board Meeting at

any stage unless dissented to or objected by majority of

Directors present at the meeting.

Board / Committee Meetings (SS-1)

5) Time, Place, Mode & Serial

Numbering:

a) Every Meeting shall have a serialnumber.

b) A meeting shall be convened at any

place, any time, on any day excludingNational Holiday.

c) Venue can be registered office or

otherwise. It may be held anywhere across

the globe.

d) No time limit for meeting of Board of

Directors.

6) Meeting through electronic mode:

a) Notice of the meeting shall specify

venue of the meeting.

Can be heldanywhere inthe globe

No meetingson NationalHolidays

No time barfor holdingmeeting

Board / Committee Meetings (SS-1)

b)Restricted agenda for e-participation in Board

Meeting:

Approval of Annual Financial Statements

Board’s Report

Prospectus

Matters relating to amalgamation, merger,

demerger, acquisition, takeover, etc.

7) Notice:

a) Notice, agenda and notes to agenda shall be given to

every Director by hand, or speed post or registered

post or by courier or e-mail or by any other electronic

means.

Board / Committee Meetings (SS-1)

b) Notice in writing shall be given to every

director.

c) In absence of / unavailability of address or e-

mail id, than it should be sent to address

appearing in Directors Identification Number

(DIN) registration of the Director.

d) Proof of sending the notice, Agenda and

notes to Agenda and its delivery shall be

maintained by the Company.

e) Notice shall specify day, date, time and full

address of venue of the meeting.

f) Notice shall be issued by Company

Secretary or where there is no Company

Secretary, any director or any other person

authorised by Board for this purpose.

Proof of sending tobe maintained

Shall specify date, day,full address, time &venue of the meeting

Given by hand, e-mail, speed post,registered post,courier, facsimile

Board / Committee Meetings (SS-1)

g) Notice shall be given at least seven days

before the date of meeting, unless the Articles

prescribes a longer period.

h) In case the notice is to be send by speed

post additional 2 days shall be added.

i) The notice of the meeting shall be give even

if Meetings are held at pre determined dates.

j) If majority of directors give their consent the

meeting can be held by giving shorter notice.

The fact that meeting is being held at shorter

notice shall be stated in the notice.

Atleast seven days

notice to be given.

In case of speed

post additional 2

days be added.

Board / Committee Meetings (SS-1)

8) Frequency:

a) Meeting of BOD:

Board shall meet atleast once in every

calendar quarter. (Maximum Interval of

120 days between two consecutive

meetings).

First Board Meeting shall be held within 30

days of incorporation.

9) Quorum:

Quorum shall be present through out the

meeting including commencement of

meeting and also while transacting meeting.

Directors shall not be counted in items in

which he/ she are interested.

Frequency

Quarter – 1Meeting

Yearly – 4Meetings

Maximuminterval of 120days

Board / Committee Meetings (SS-1)

Meeting of Board:

Quorum of Board Meeting shall be one

third of total strength or two whichever

is higher.

10) Attendance Register:

Every company shall maintain separate

attendance registers for the Meetings of

the Board.

The pages shall be consecutively

numbered.

If attendance register is maintained in

loose leaf form it shall be bound at

periodical intervals.

Quorum shall be

-One third of total

strength or

-Two

Whichever is higher

Attendance Register

-Consecutively Numbered

-Shall be maintained for

eight years

Board / Committee Meetings (SS-1)

The attendance register shall contain following

particulars: serial number and date of the Meeting,

names of directors and signature of each director

present, name and signature of Company Secretary who

is in attendance and also of persons attending the

Meeting by invitation.

In case directors participating through Electronic

Mode, the Chairman shall confirm attendance of such

directors.

For this purpose before commencement of the Meeting,

the Chairman shall take a roll call.

The Chairman or Company Secretary shall request the

director participating through electronic mode to state

his full name and location from where he is participating

and shall record the same in the Minutes.

Board / Committee Meetings (SS-1)

The Attendance register shall be

maintained at the Registered Office of

the Company or such other place as may

be approved by the Board.

The attendance register is open for

inspection by the Directors.

The attendance register shall be preserved

for a period of eight years and thereafter

be destroyed with the approval of the

Board.

11) Leave of absence:

It shall be communicated with the

chairman. The office of Director shall

become vacant if directors fails to attend

any of the board meeting for a period of

twelve months, with or without seeking

leave of absence.

Director shall vacate his

office if he fails to attend

any of the Board Meeting

for a period of 12 months

with or without seeking

leave of absence

Board / Committee Meetings (SS-1)

12) Chairman:

The chairman of the Company shall be

chairman of the Board (incase of no

chairman Board shall elect among

themselves to act as a chairman).

13) Passing of Resolution by Circulation:

Urgent decisions can be approved by

resolution passed by circulation.

It shall have equal authority as a duly

convened meeting.

Procedure:

a) Draft copy of resolution to be passed by

circulation.

b) Such draft shall be sent to all directors with

relevant documents on the same day by

hand delivery, speed post or registered post.

If chairman is

interested in any

matter to be

transacted / taken-up

during the meeting, he

should not be counted

for quorum for that

matter.

Board / Committee Meetings (SS-1)

c) Proof of sending and delivery thereof shall be

maintained by the Company.

d) Each business shall be explained by way of note.

Even a note shall indicate the way by which

director shall assent or dissent to the same.

e) At most seven days from the date of passing of

resolution by circulation of draft of resolution

shall be given to directors to respond.

Approval:

a) The resolution must be passed when it is

approved by majority of directors entitled to

vote.

b) The interested director shall not be entitled to

vote.

c) In case director doesn’t respond on or before

seven days, it shall be presumed that director is

abstained from voting.

Assent or dissent shall be

communicated by the

directors within seven

days.

Board / Committee Meetings (SS-1)

Recording:

The note of passing the resolution by resolution shall

be taken up at the next Board Meeting. The dissent or

abstention shall be recorded in minutes.

Validity:

The resolution passed by circulation shall be valid as if

resolution passed at duly convened meeting.

Note:

Resolution passed by circulation will not reduce

the frequency of meetings which are required to be

held.

Board / Committee Meetings (SS-1)

14) Minutes:

Every Company shall keep minutes of all meetings of

Board in Minute Book.

Maintenance

Minutes in Physical or Electronic form shall be

maintained with Time Stamp.

Minutes shall be serially numbered and pages of minute

book are left blank it should be scored out and initialed

by the Chairman.

Minutes shall not be pasted or attached to Minute

Book.

Recording:

The CS shall record proceedings of the meetings. If

there is no CS any person authorised by Board or

Chairman shall record the proceedings.

Board / Committee Meetings (SS-1)

Minutes shall be written in third person and past

tense; however resolution shall be in present

tense.

Time of commencement and closure of meeting

shall be recorded in minutes.

Finalisation of Minutes:

Draft minutes shall be circulated within 15

days from the date of conclusion of the

meeting of Board or Committee.

Proof of sending the draft minutes and its

delivery shall be maintained by the Company.

The Directors(whether present or not) shall

communicate their comments in writing on

the draft minutes within 7 days.

The minutes shall be finalised and entered into

minutes book within 30 days.

Draft of minutes to be

circulated within 15 days.

Comments on the same

shall be communicated

within 7 days.

Minutes shall be finalised

within 30 days of passing

of resolution.

Board / Committee Meetings (SS-1)

Signing of the Minutes:

Minutes shall be signed and dated by the

Chairman of the Meeting or Chairman of

the Next Meeting.

The Chairman shall initial each page of

the Minutes, sign the last page and

append to such signature the date on

which and the place where he has signed

the Minutes.

Minutes once signed shall not be altered.

A copy of the signed Minutes certified by

the Company Secretary or where there is

no Company Secretary, by any Director

authorised by the Board shall be

circulated to all Directors within fifteen

days after these are signed.

Each page of minutes

shall be initialled and last

page shall be signed by

the Chairman of the

Meeting.

Minutes Book once

signed shall be circulated

to directors within 15

after it is signed.

Board / Committee Meetings (SS-1)

15) Disclosure:

The Annual Report and Annual Return of a company

shall disclose the number and dates of Meetings of

the Board and Committees held during the financial

year indicating the number of Meetings attended by

each Director.

(SS-2) Steps involved in conducting

General Meeting Convening

Frequency

Quorum

Presence of Directors, Auditors

Proxies

Voting

Conduct of e-voting

Reading of Report

Passing of resolution

Adjournment

Minutes

General Meetings (SS-2)

1) Applicability:

This Standard is applicable to all types of

General Meetings of all companies

incorporated under the Act except One

Person Company (OPC) and class or classes

of companies which are exempted by the

Central Government through notification.

2) Convening:

A General Meeting shall be convened by or on

the authority of the Board. The Board shall,

every year, convene or authorise convening of

a Meeting of its Members called the Annual

General Meeting to transact items of Ordinary

Business specifically required to be transacted

at an Annual General Meeting as well as

Special Business, if any

Applicability of SS-2 to all

companies except OPC.

Convening of the meeting

shall be by authority of

board.

General Meetings (SS-2)

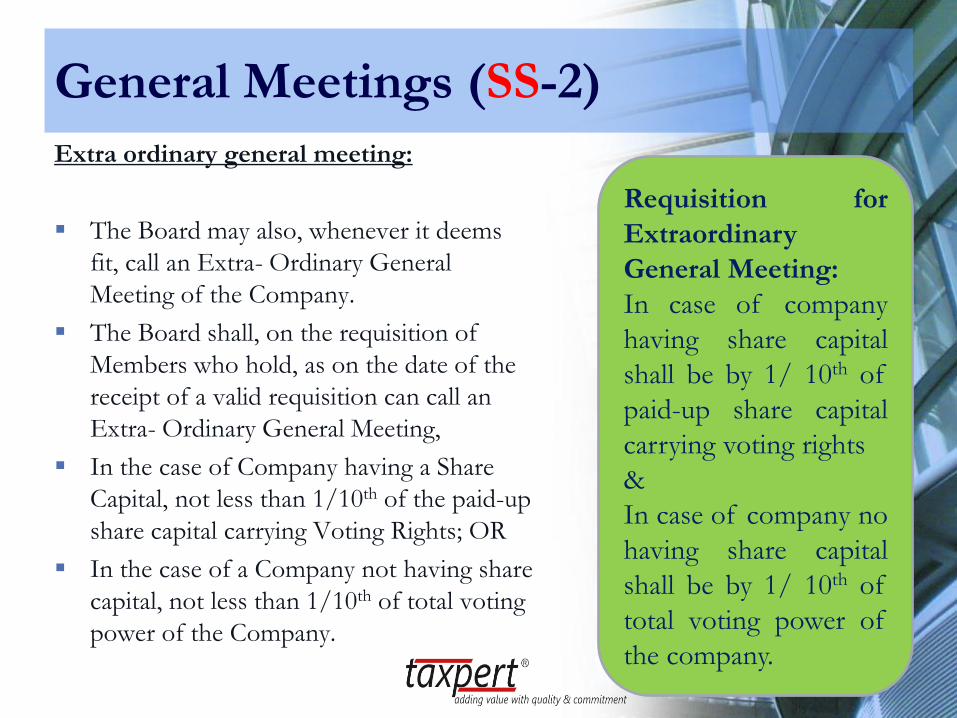

Extra ordinary general meeting:

The Board may also, whenever it deems

fit, call an Extra- Ordinary General

Meeting of the Company.

The Board shall, on the requisition of

Members who hold, as on the date of the

receipt of a valid requisition can call an

Extra- Ordinary General Meeting,

In the case of Company having a Share

Capital, not less than 1/10th of the paid-up

share capital carrying Voting Rights; OR

In the case of a Company not having share

capital, not less than 1/10th of total voting

power of the Company.

Requisition for

Extraordinary

General Meeting:

In case of company

having share capital

shall be by 1/ 10th of

paid-up share capital

carrying voting rights

&

In case of company no

having share capital

shall be by 1/ 10th of

total voting power of

the company.

General Meetings (SS-2)

3) Notice:

Notice in writing shall be given to every

member of the Company. Such notice

shall also be given to the Directors and

Auditors, Secretarial Auditor of the

company.

Notice shall be sent by hand or by

ordinary post or by speed post or by

registered post or by courier or by

facsimile or by e-mail or other electronic

means.

Proof of sending shall be maintained.

In case of companies having website, the

notice shall be hosted on website.

Modes of sending

notice:

hand or

Ordinary post or

Speed post

Registered post or

Courier or

Facsimile or

e-mail or

other electronic

means

General Meetings (SS-2)

Notice shall specify the day, date, time & full address of the

venue of the meeting.

Notice shall clearly specify the nature of the Meeting and the

business to be transacted thereat. Items of special business,

each business item shall be in form of resolution and shall e

accompanied by an explanatory statement.

21 clear days in advance the notice shall be given.

If consent in writing given by 95% of the members then

shorter notice can be given.

No items other than those specified in the notice shall be

taken up at the meeting.

Notice shall be hosted

on the website, if any

General Meetings (SS-2)

Frequency:

Every company shall, in each

Calendar Year, hold a General

Meeting called the Annual

General Meeting.

First AGM shall be within 9

months from the close of first

financial year.

Subsequent AGM shall be held

within 6 months from the end of

financial year or interval of not

more than 15 months between

two consecutive AGM’s.

Note: If company holds it’s AGM as

per aforesaid, it is not required to

hold any AGM in calendar year of

its incorporation.

Subsequent AGM shall be held-

Within 6 months from the end of

financial year or

Interval between two consecutive

AGM shall not be more than 15

months

If first AGM is held within 9

months from end of first financial

year it is not required to hold any

AGM in calendar year of its

incorporation.

General Meetings (SS-2)

4) QUORUM OF GENERAL MEETING:

Private Limited:

Minimum No. of Members required being present

“Two Members Personally Present”.

Public Limited:

In case of Public Company “Minimum Present of

Members required”

5 members personally present if the number of

Members as on the date of Meeting is not more than

1000.

15 members personally present if the number of

Members as on date of Meeting is more than 1000

but upto 5000

30 personally present if the number of members as

on date of the Meeting exceeds 5000

Quorum shall be present not only at the time of

commencement of the Meeting but also while

transacting business.

Private Company:

Two member personally

present.

Public Company:

5 members where number of

members is not more than

1000,

15 members where number of

members is more than 1000

but less than 5000,

30 members where number of

members is more than 5000.

General Meetings (SS-2)

5) PRESENCE OF DIRECTOR AND AUDITORS:

Director:

If any Director is unable to attend the Meeting, the Chairman shall

explain such absence at the Meeting.

The Director who attends the General Meeting shall seat with

Chairman.

Company Secretary:

The Company Secretary shall seat with Chairman.

The Company Secretary shall assist the Chairman in conduction the

Meeting.

Auditor:

It is mandatory for the Auditor to attend General Meeting,

Exemption: Auditor can absent himself by following two ways:

If it get exemption from the Company to attend General Meeting.

If his authorized representative attend the General Meeting.

[Condition: Authorized representative should also be qualified to be an

Auditor]

General Meetings (SS-2)

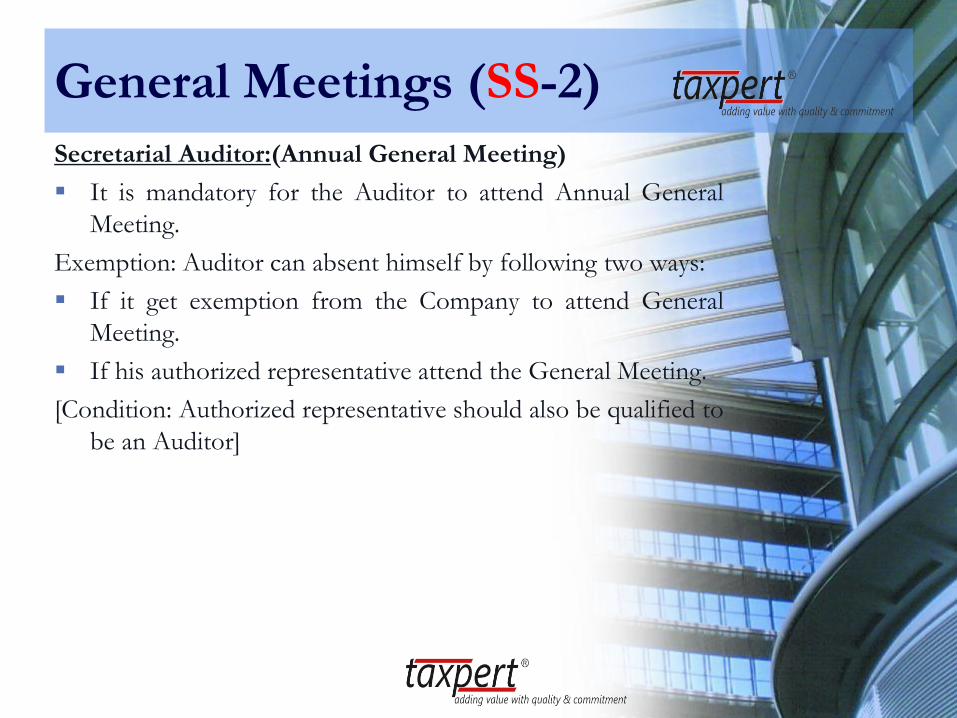

Secretarial Auditor:(Annual General Meeting)

It is mandatory for the Auditor to attend Annual General

Meeting.

Exemption: Auditor can absent himself by following two ways:

If it get exemption from the Company to attend General

Meeting.

If his authorized representative attend the General Meeting.

[Condition: Authorized representative should also be qualified to

be an Auditor]

General Meetings (SS-2)

6) CHAIRMAN:

The Chairman of the Board shall take the Chair and conduct

the Meeting.

If the Chairman is not present within 15 minutes after the

time appointed for holding of Meeting, or

If he is unwilling to act as Chairman of the Meeting, or

If no Director has been so designated.

(In above three situations) The Director present at the

Meeting shall elect one of them to be the Chairman of the

Meeting.

The chairman shall explain the objective and implication of

the Resolutions before they put to vote at the meeting.

General Meetings (SS-2)7) Proxy Form:

An Instrument appointing a proxy shall be either:

In the form set out in Act (MGT-11)

Validity of Proxy Form:

An instrument of Proxy duly filed, stamped and signed, is

valid only for the Meeting to which it relates including any

adjournment

Stamping of Proxy:

An instrument of proxy is valid only if it is properly stamped

as per the applicable law.

Unstamped or inadequately stamped Proxies or Proxies upon

which the stamps have not been cancelled are INVALID.

Execution of Proxy:

The proxy-holder shall prove his identity at the time of

attending the Meeting.

General Meetings (SS-2)

Deposit of Proxies:

Proxies shall be deposited with the company either in person

or through post within forty-eight hours before

commencement of the meeting.

If company receive multiple proxies for the same holdings of

the Member and they are not dated or bear the same date

without mention of time, all such multiple proxies shall be

treated as invalid.

Note:

If a company receives multiple proxies form the same

holding of a member, the Proxy which is dated last shall be

considered valid.

Proxy shall be deposited within 48 hours before commencement of

meeting.

General Meetings (SS-2)

Revocation of Proxy:

A proxy later in date can revoke the earlier dated proxies.

Proxy is valid until written notice of revocation has been

received by the Company before the commencement of the

Meeting or adjourned meeting.

When both the Member and Proxy attend the Meeting, the

proxy stand automatically revoked.

Inspection of Proxy:

Proxies shall made available for inspection:

Ending with the conclusion of the Meeting

Between 9 a.m. to 6 p.m.

Record of Proxy:

All the proxies shall be recorded chronologically in a register

kept for that purpose.

In case any proxy entered in the register is rejected, the reasons

there for shall be entered in the remarks column.

General Meetings (SS-2)

8) Voting:

a) Proposing a Resolution

Every resolution shall be proposed by a Member and

seconded by another Member.

b) Voting at the meeting:

Every company, which has provided e-voting facility to its

Members, shall also put every resolution to vote through a

ballot process at the Meeting.

c) Show of Hands:

Every company shall, at the Meeting, put every Resolution,

except a Resolution which has been put to Remote e-voting,

to vote on a show of hands at the first instance, unless a poll

is validity demanded.

d) Poll:

The Chairman shall order a poll upon receipt of a valid

demand for poll either before or on the declaration of the

results of the voting on any Resolution on show of hands.

Ballot process may

be carried out by

distributing

ballot/poll slips or

by making

arrangement for

voting through

computer or

secured electronic

systems.

A proxy can also

vote in the ballot

process.

General Meetings (SS-2)

e) Voting Rights:

A Member who is a related party is not entitled to vote on a

Resolution relating to approval of any contract or arrangement in

which such Member is a related party.

The voting period shall close at 5 p.m. on the day preceding the date

of General Meeting.

Notice of meeting, wherein facility of e-voting is provided, shall be

sent either by registered post or speed post or by courier or by e-

mail or by any other electronic means.

General Meetings (SS-2)

9) Declaration of Results:

The result of the voting, with details of the number of votes

cast for and against the Resolution, invalid votes and

whether the Resolution has been carried or not shall be

displayed on the Notice Board of the company at its

Registered Office and its Head Office as well as Corporate

Office, if any, if such office is situated elsewhere.

10) Reading of Report:

The qualifications, observations or comments or other

remarks on the financial transactions or matters which have

any adverse effect on the functioning of the company, if

any, mentioned in the Auditor’s Report shall be read at the

Annual General Meeting and attention of the Members

present shall be drawn to the explanations / comments

given by the Board of Directors in their report.

General Meetings (SS-2)

11) Distribution of Gifts:

No gifts, gift coupons, or cash in lieu of gifts shall be

distributed to Members at or in connection with the

Meeting.

12) Minutes:

a) Maintenance of Minutes

Minutes shall be recorded in books maintained for that

purpose.

A distinct Minutes Book shall be maintained for Meetings of

the Members of the company, creditors and others as may

be required under the Act.

Minutes may be maintained in electronic form with

Timestamp.

General Meetings (SS-2)

Minutes shall not be pasted or attached to the

Minutes Book, or tampered with in any

manner.

Minutes of Meetings, if maintained in loose-

leaf form, shall be bound periodically

depending on the size and volume.

Minutes Books shall be kept at the Registered

Office of the company or at such other place,

as may be approved by the Board.

The Chairman shall initial each page of the

Minutes, sign the last page and append to such

signature the date on which and the place

where he has signed the Minutes.

Minutes shall be entered in the Minutes Book

within thirty days from the date of conclusion

of the Meeting.

Minutes shall be

entered in Minutes

Book within thirty days

from the conclusion of

the Meeting.

General Meetings (SS-2)

13) Disclosure:

The Annual Return of a company shall disclose the date of

Annual General Meeting held during the financial year.

Secretarial Standards- Penal

ProvisionAs per the Companies Act, 2013, Section 118 (11) & (12)

If any default is made in complying with the provisions of

this section in respect of any meeting, the company shall be

liable to a penalty of twenty-five thousand rupees and every

officer of the company who is in default shall be liable to a

penalty of five thousand rupees.

If a person is found guilty of tampering with the minutes of

the proceedings of meeting, he shall be punishable with

imprisonment for a term which may extend to two years and

with fine which shall not be less than twenty-five thousand

rupees but which may extend to one lakh rupees.

Penalty for non compliance of SS – The company shall be liable to a penalty of

Twenty-five thousand and every officer in default with a penalty of rupees five

thousand.

Thank YouPlease feel free to call/mail us for further clarification.

Contact:

Taxpert Professionals Private Limited

Tel: +91 9769134554

E-mail us: [email protected]

Visit us at: www.taxpertpro.com