taxation of real estate some important aspects ... of real estate some important aspects including...

TRANSCRIPT

TAXATION OF REAL ESTATE

Some important aspects

including

Project Completion Method

Development & Redevelopment

s. 50C and 80IB(10)

Wednesday

20th October 2010

Walchand Hirachand Hall

IMC

Bombay Chartered Accountants Society

Pradip Kapasi & Co. 1

PROJECT COMPLETION METHOD

Pradip Kapasi & Co. 2

BILAHARI INVESTMENT, 299 ITR 1 (SC)

Case of a chit fund

CCM acceptable in tax laws

Possible for integrated scheme > 12 months

Objective assessment of income of contract

Revenue neutral

New AS not invoked

Method accepted in past

Onus on AO for change in method

Possible to invoke new AS – para 21

Pradip Kapasi & Co. 3

RECENT DEVELOPMENTS

Developments in Accountancy AS 7 Revised 1.04.2003

EAC, The CA Vol.52 pg.232

Exposure Draft AS I – The CA Vol. 54 April, 2005,

Guidance Note 23 The CA, Vol. 55 pg. 1764 June 06

IFRS on Real estate & Investment properties

Developments in Taxation Acceptance of Project Completion Method

Project completion NOT possible

Greater Ashoka LDC. (P) Ltd., 89 TTJ 281 (Del)

Growth Techno Projects Ltd., 29 SOT 59(Delhi)

New s. 145 and s. 145A

Pradip Kapasi & Co. 4

ROAD AHEAD IN ACCOUNTING

Guidance Note

Revenue from real estate sales Enterprise- Builders & Developers

Material Aspects Effect of flat sale agreement

Performance for buyer- contractor

Escalation and such claims

Percentage of completion method

Reference to AS 7

Examples in para 8

Retention of effective control

Disclosure of Accounting policy

IFRS Effect

Pradip Kapasi & Co. 5

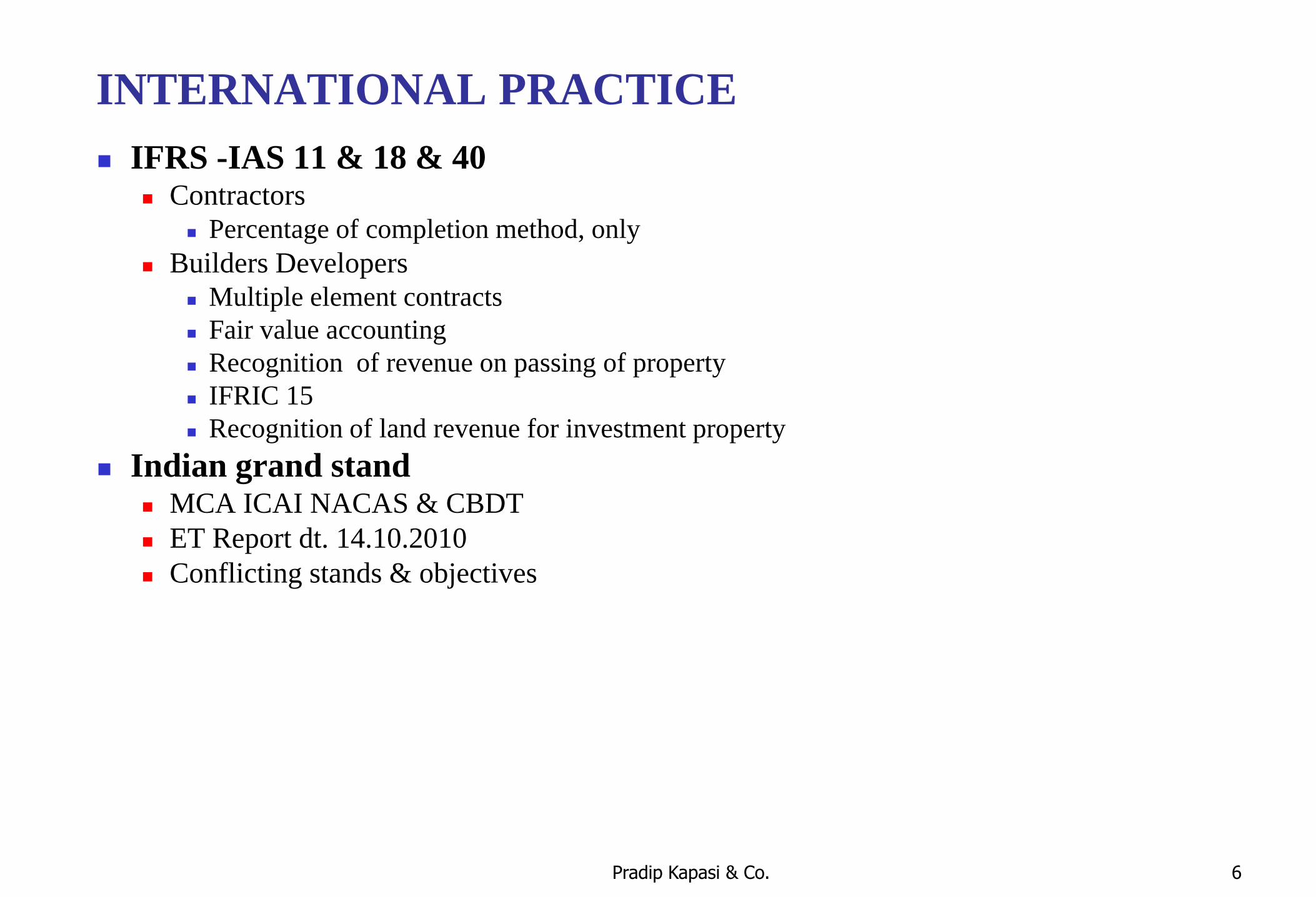

INTERNATIONAL PRACTICE

IFRS -IAS 11 & 18 & 40 Contractors

Percentage of completion method, only

Builders Developers

Multiple element contracts

Fair value accounting

Recognition of revenue on passing of property

IFRIC 15

Recognition of land revenue for investment property

Indian grand stand MCA ICAI NACAS & CBDT

ET Report dt. 14.10.2010

Conflicting stands & objectives

Pradip Kapasi & Co. 6

ROAD AHEAD IN TAXATION

New S. 145 & GN of ICAI

Relevance of PCM/CCM & deci. cases

Post 1.04.2003 and revised AS 7 Avadhesh Builders, 37 SOT 122 (Mum)

Prestige Estates Projects Ltd., 129 TTJ 680 (Bang)

Realest Builders Pvt. Ltd. 307 ITR 202(SC)

Matching concept, Rajgir Builders, 70 ITD 226 (Mum)

New scrutiny guidelines

Time for applying AS7 Lurgi India,114 ITD 1(Delhi)

Pradip Kapasi & Co. 7

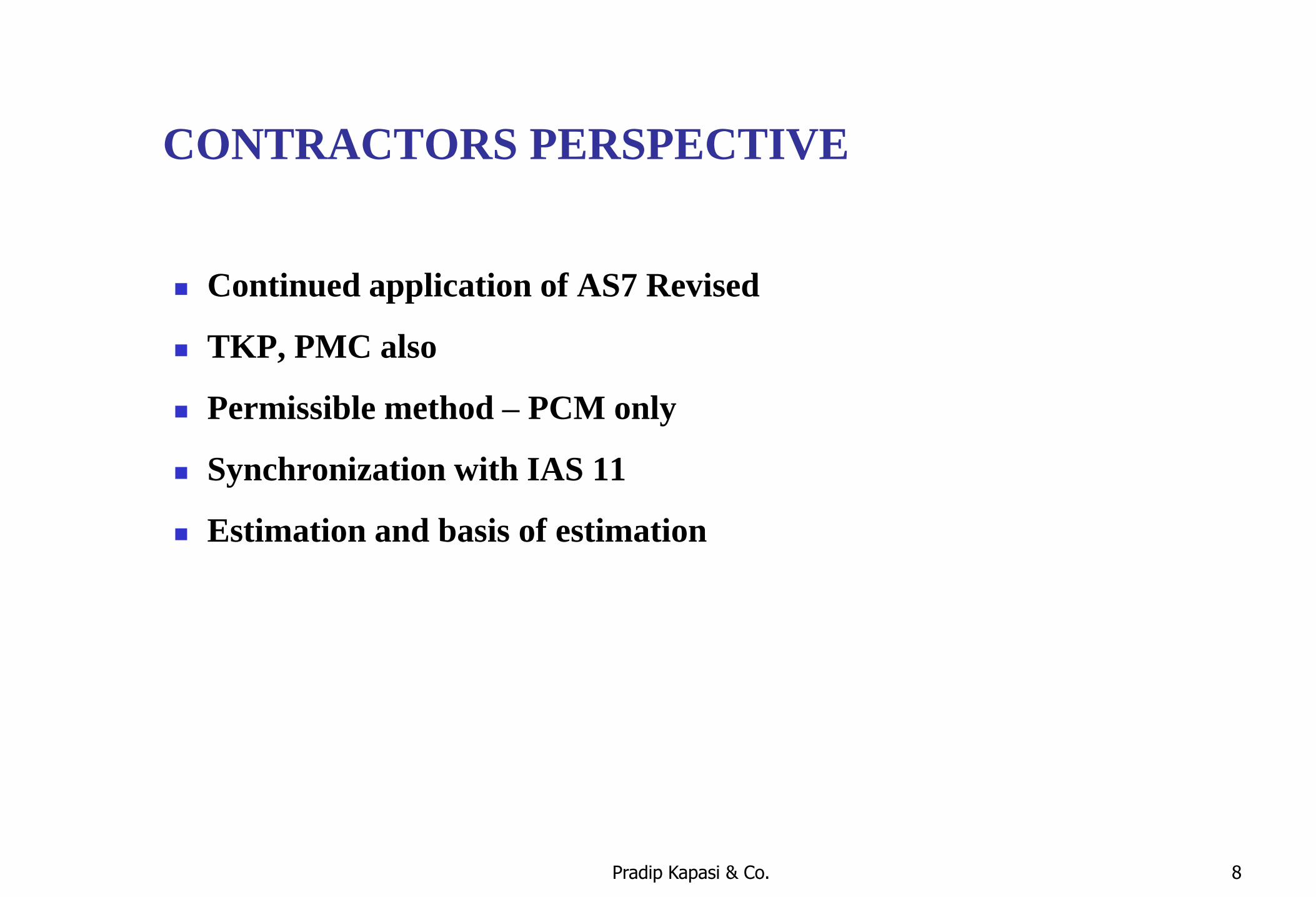

CONTRACTORS PERSPECTIVE

Continued application of AS7 Revised

TKP, PMC also

Permissible method – PCM only

Synchronization with IAS 11

Estimation and basis of estimation

Pradip Kapasi & Co. 8

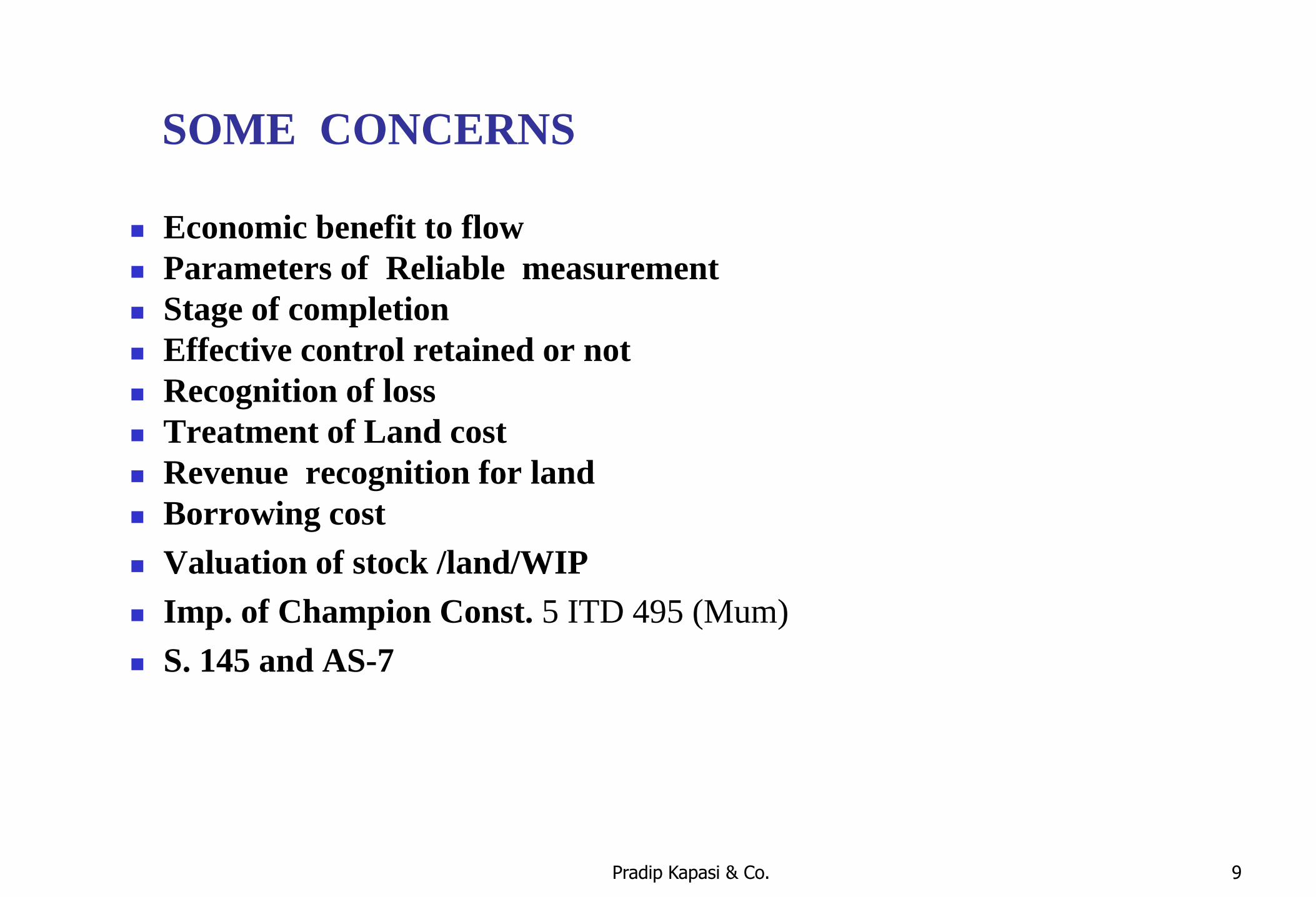

SOME CONCERNS

Economic benefit to flow

Parameters of Reliable measurement

Stage of completion

Effective control retained or not

Recognition of loss

Treatment of Land cost

Revenue recognition for land

Borrowing cost

Valuation of stock /land/WIP

Imp. of Champion Const. 5 ITD 495 (Mum)

S. 145 and AS-7

Pradip Kapasi & Co. 9

RELATED DEVELOPMENTS

Indirect & Finance cost Lokhandwala Construction, 260 ITR 579(Bom)

Wallstreet Constructions, 101 ITD 156 (Mum)(SB)

K.Raheja ,102 ITD 414 (Mum.)

Thakkar Developers, 115 TTJ 841(Pune)

Time sharing arrangements Club Mahindra (Chennai) (SB)

Change from PCM/WIP to CCM Satish H. Patel, 93 TTJ 458 (Pune)

Audit

Gopalkishan Builders, 92TTJ 215(Luck.)

Pradip Kapasi & Co. 10

JOINT VENTURE - AOP

Pradip Kapasi & Co. 11

STATUS OF JV

AOP or not

Van Ord , 248 ITR 399(AAR)

Geo Consult GmbH, 304 ITR 283(AAR)

Pradip Kapasi & Co. 12

INDIRECT TAXES

&

ALLIED LAWS

Pradip Kapasi & Co. 13

INDIRECT TAXATION Service Tax on sale of flats

Harekrishna Developers AIT- 2008-128 (AAR)

Magus Constructions P.Ltd. 2008-TIOL-321(Gau)

Controversy rested by circular dt. 29.01.2009

Amendment of 2010

Stay by Bombay high court

Consumer Protection Act Fakirchand Gulati v. Uppal,(SC), ITAT Online

VAT on sale of flats Review of K.Raheja’s decision by larger bench of SC in L&T ‘s case

Amendment of 2006 w.e.f. 20.06.2006 and stay for MCHI

Trade circular dt.07.02.2007

Amendment of 2010 and stay for MCHI

Completed flats

Stamp duty Development agreements and tenancy transfers

Pradip Kapasi & Co. 14

DEVELOPMENT AGREEMENTS

&

REDEVELOPMENT

Pradip Kapasi & Co. 15

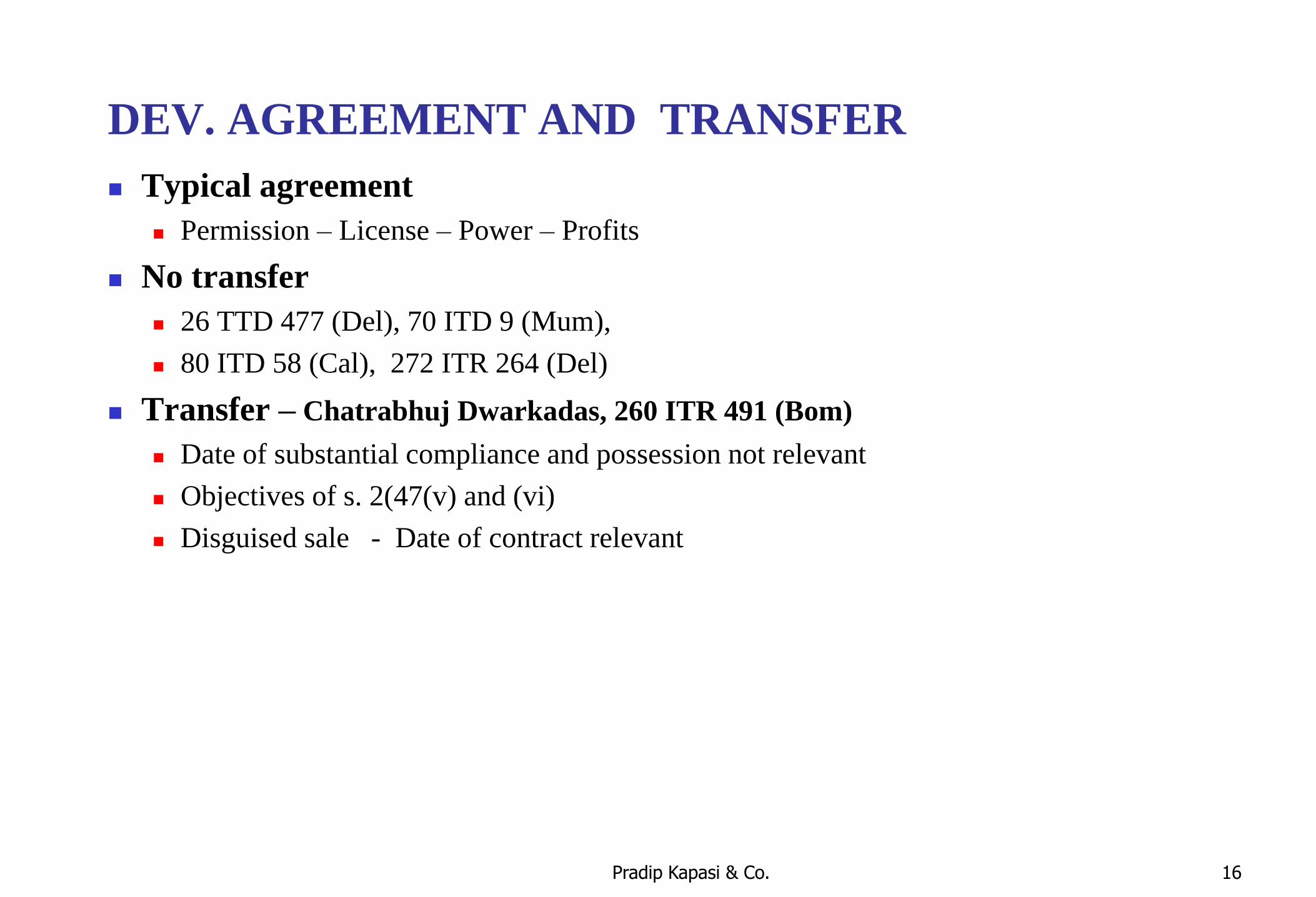

DEV. AGREEMENT AND TRANSFER

Typical agreement

Permission – License – Power – Profits

No transfer

26 TTD 477 (Del), 70 ITD 9 (Mum),

80 ITD 58 (Cal), 272 ITR 264 (Del)

Transfer – Chatrabhuj Dwarkadas, 260 ITR 491 (Bom)

Date of substantial compliance and possession not relevant

Objectives of s. 2(47(v) and (vi)

Disguised sale - Date of contract relevant

Pradip Kapasi & Co. 16

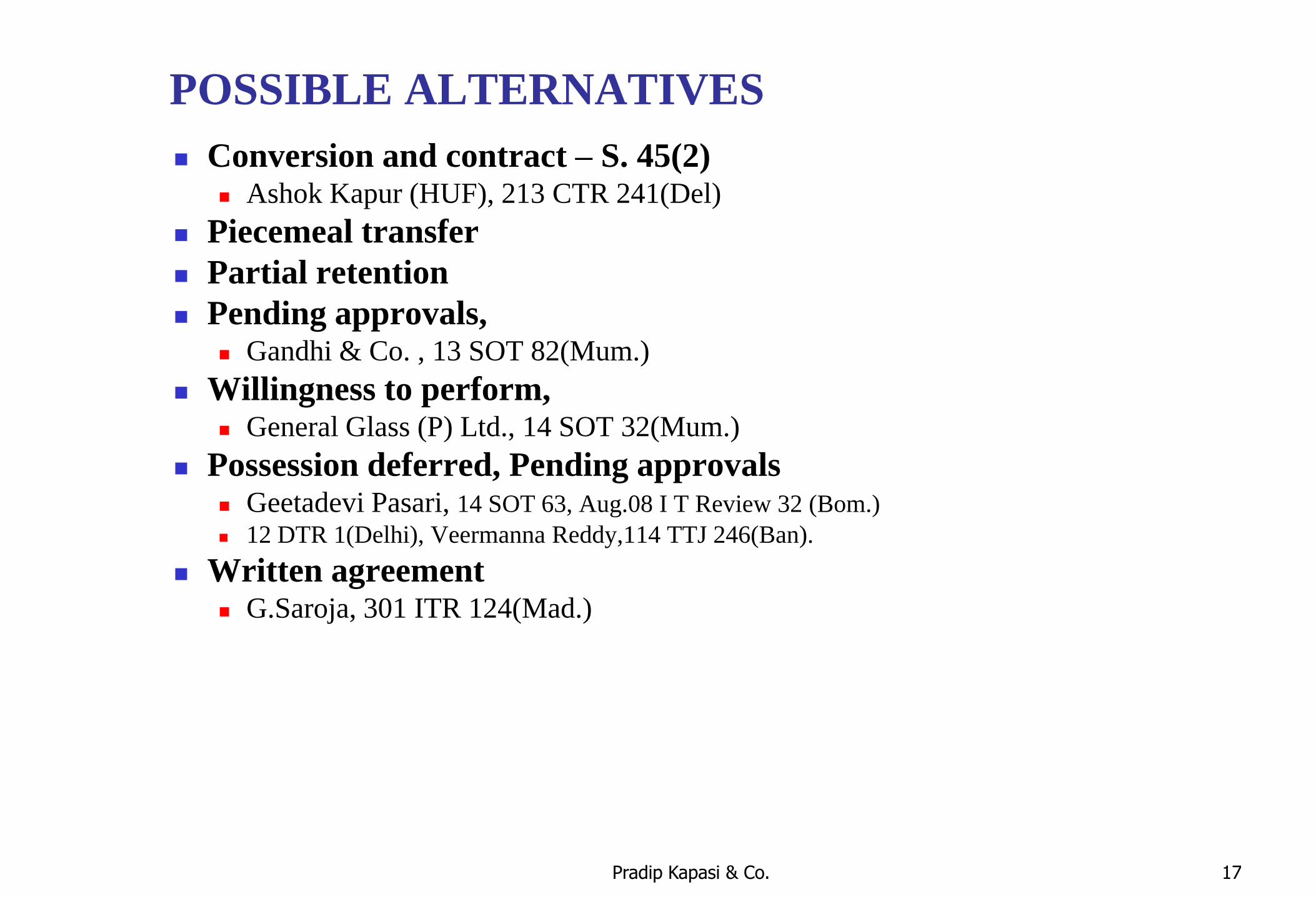

POSSIBLE ALTERNATIVES

Conversion and contract – S. 45(2) Ashok Kapur (HUF), 213 CTR 241(Del)

Piecemeal transfer

Partial retention

Pending approvals, Gandhi & Co. , 13 SOT 82(Mum.)

Willingness to perform, General Glass (P) Ltd., 14 SOT 32(Mum.)

Possession deferred, Pending approvals Geetadevi Pasari, 14 SOT 63, Aug.08 I T Review 32 (Bom.)

12 DTR 1(Delhi), Veermanna Reddy,114 TTJ 246(Ban).

Written agreement G.Saroja, 301 ITR 124(Mad.)

Pradip Kapasi & Co. 17

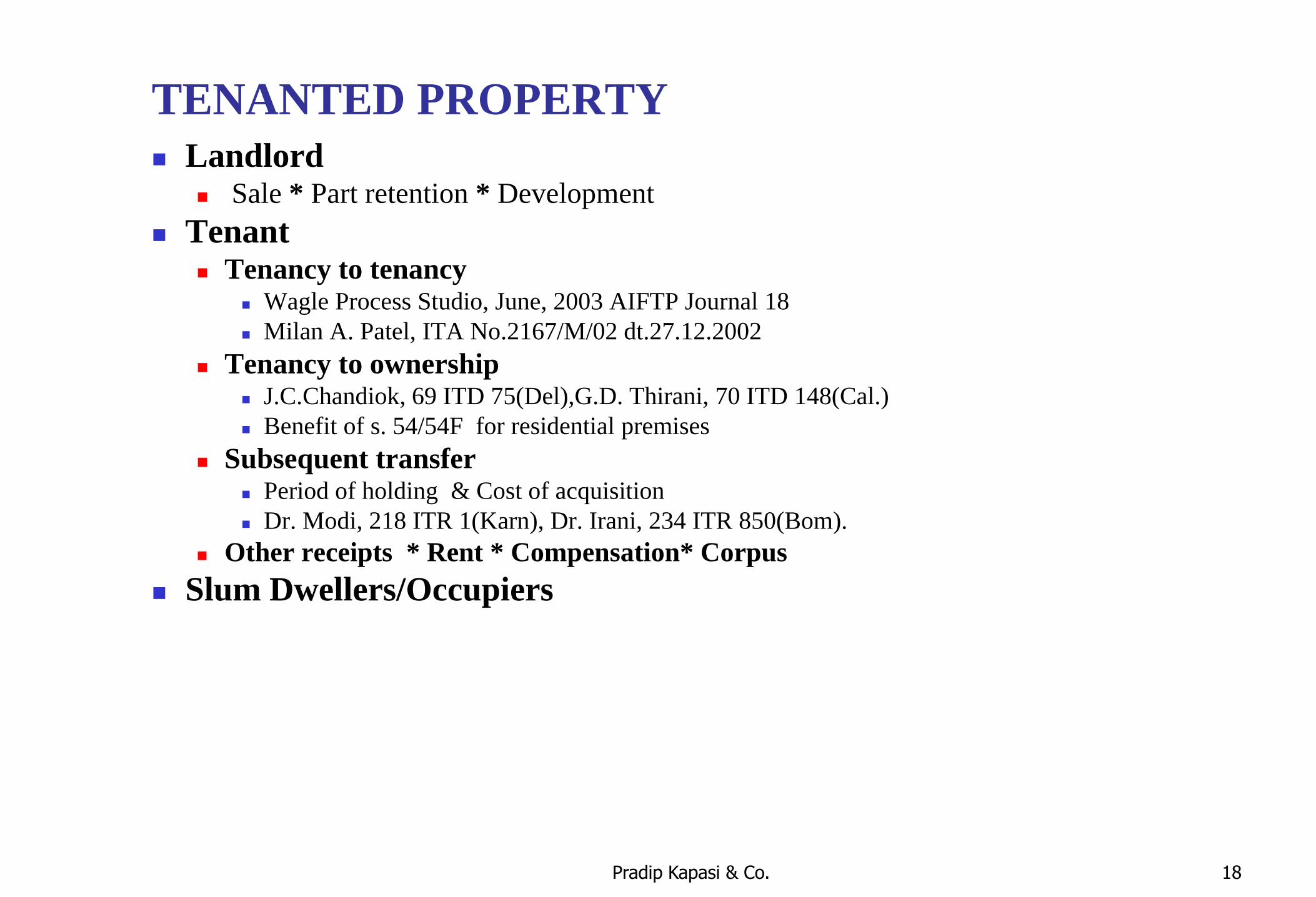

TENANTED PROPERTY

Landlord Sale * Part retention * Development

Tenant Tenancy to tenancy

Wagle Process Studio, June, 2003 AIFTP Journal 18

Milan A. Patel, ITA No.2167/M/02 dt.27.12.2002

Tenancy to ownership J.C.Chandiok, 69 ITD 75(Del),G.D. Thirani, 70 ITD 148(Cal.)

Benefit of s. 54/54F for residential premises

Subsequent transfer Period of holding & Cost of acquisition

Dr. Modi, 218 ITR 1(Karn), Dr. Irani, 234 ITR 850(Bom).

Other receipts * Rent * Compensation* Corpus

Slum Dwellers/Occupiers

Pradip Kapasi & Co. 18

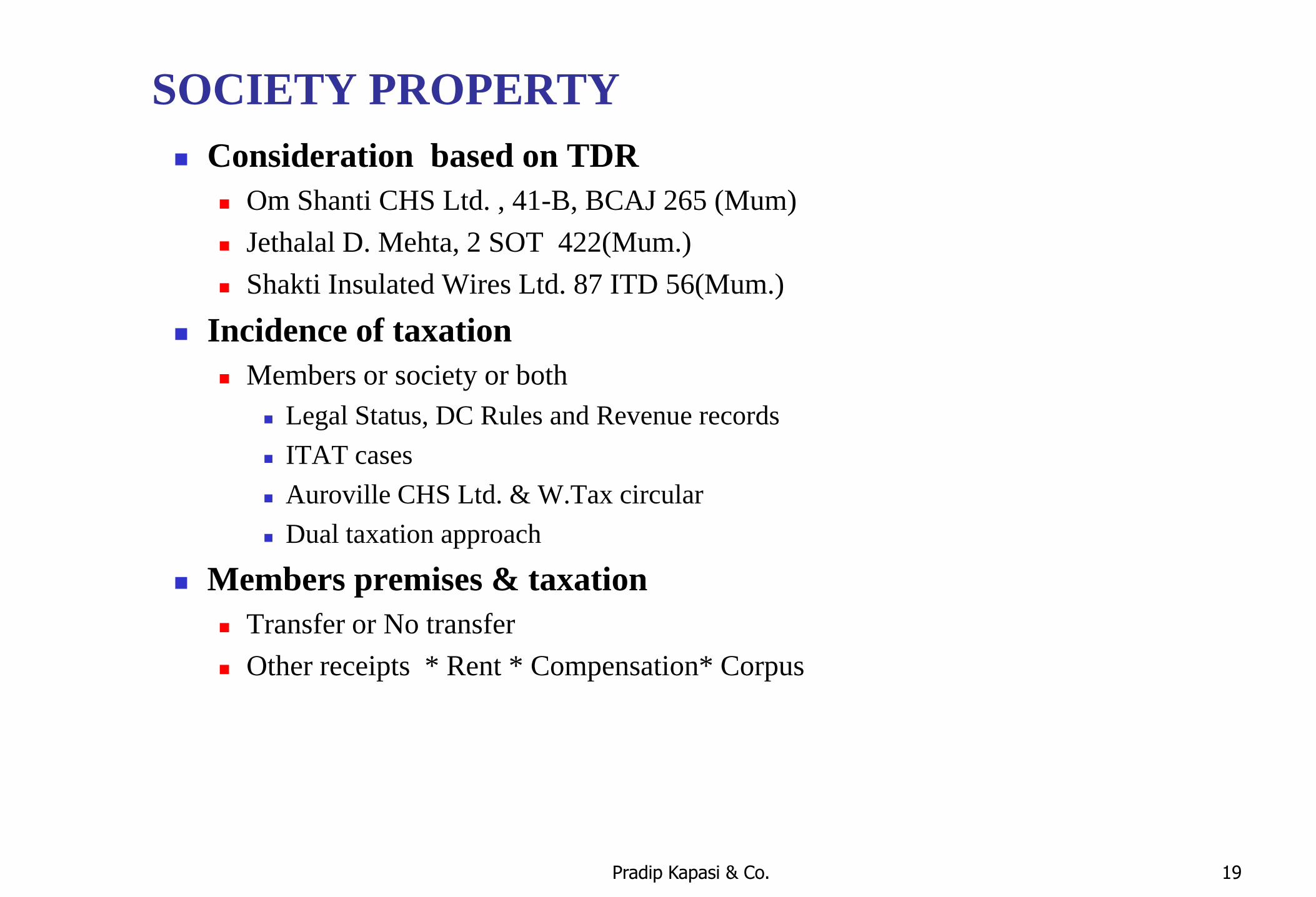

SOCIETY PROPERTY

Consideration based on TDR

Om Shanti CHS Ltd. , 41-B, BCAJ 265 (Mum)

Jethalal D. Mehta, 2 SOT 422(Mum.)

Shakti Insulated Wires Ltd. 87 ITD 56(Mum.)

Incidence of taxation

Members or society or both

Legal Status, DC Rules and Revenue records

ITAT cases

Auroville CHS Ltd. & W.Tax circular

Dual taxation approach

Members premises & taxation

Transfer or No transfer

Other receipts * Rent * Compensation* Corpus

Pradip Kapasi & Co. 19

S. 50 C

Pradip Kapasi & Co. 20

GENERAL

Constitutional K. Palanisamy, 306 ITR 61(Mad.) Bhatia Nagar Premises CHS Ltd. dt.19.08.2010 (Bom.)

Efficacy of Stamp duty valuation, Jai Marwar,79 TTJ 178(Jd), U.P.Jal Nigam, AIR 1996 SC 1170, Raja Narendra, 123 Taxation 63(Raj)

Acceptable margin – a break through Rahul Construction, 38 DTR 19 (Pune)

21

SCOPE

Assets Land & Bldg.

Immovable property

Whole or part

Purposive interpretation

Land & Building and right therein Kishori S. Gaitonde, 41-B, BCAJ 5321 (Mum)

Capital asset u/s 2(14) Thiruvengadam Investments, 320 ITR 346 (Mad)

Inderlok Hotels , 122 TTJ 145 (Mum)

Excellent Land Dev. (P) Ltd., 1 ITR (Trib) 563 (Delhi)

S. 50C and s. 69B Chandni Bhuchar , 323 ITR 510 (P&H)

Jayashankar S. Vaid, 35 SOT 46 (Ahd)

Optic Disc Mfg. , 11 DTR 264(Chd.)

22

VALUATION

Failure to apply Ambattur Clothing Co., 221 CTR 196 (Mad)

Need to refer to DVO Meghraj Baid, 114 TTJ 841(Jd.), Manju Rani Jain, 24 SOT 24(Delhi)

Effect of DVO’s valuation Less than SAV Ravi Kant, 110 TTJ 297(Del) Higher than SAV, Jitendra Saxena, 117 TTJ 974(Luck.)

Lower valuation by DVO R. V. Singh, 26 DTR 129 (Lucknow)

SVA value can not be challenged by AO Punjab Poly Jute, 120 ITD 233(Asr.)

Valuation of a let - out property Wakf Attar Aulad, 37 SOT 58 (Delhi)

Valaution of Tenant’s share Acceptable margin

Rahul Construction, 38 DTR 19 (Pune)

C. B. Gautam’s case 199 ITR 530 (SC)

23

REGISTRATION

Not applicable where registration not required

Navneet Kumar Thakkar,112 TTJ76(Jd)

Carlton Hotels,122TTJ 515 ,

Vijayalaxmi Dhadda, 20 DTR 365(Jp)

Morgardshammar India Ltd., 1999(1) SCC 108,

Effect of Amendments of 2009

S. 50 C and s. 56(2)

Effective date

24

REVISION & PENALTY

Possibility of revision where s. 50C ignored

AKG Consultants (P) Ltd. , 17 SOT 592(Luck.)

Penalty for concelment

N. Meenaxi, 125 TTJ 856 (Chennai)

Prakash Chand Nahar, 110 TTJ 886 (Jodhpur)

Balkrishna Waghere & Ors. July/Aug., 2010, PCAJ 3 (Pune)

25

EFFECTIVE DATE

Chapter XXC & Conveyance

Neville D Nooranha, 115 TTJ 390(Kol)

Agreement and conveyance

Mr. Sivaparvathi, 129 TTJ 463 (Visakha)

26

PARALLEL FICTIONS

Deeming Transfers& Fictions - FMV or SV S. 45(2)(3)(4), 47, 50 and 50B ,

Shahzada Nand & Sons, 60 ITR 392(SC)

Carlton Hotels, 122 TTJ 515( Luck.)

S. 50C and s. 50 Panchiram Nahata, 127 TTJ 128 (Kol)

Mrs. Munira S. Bootwala, ITA No. 7468/M/07 for A.Y.04-05 dt. 01.05.09

Overriding effect of s. 54F Mohammed Shoib, 29 DTR 306 (Luck.)

27

ASSESSMENT

Assessment not stayed for indefinite period

Rajni Venugopal, 16 DTR 319 (Mad)

Assessment order pending DVO’s report

N. Meenaxi, 30 DTR 1 (Mad)

Effect of s. 155(3)(ii)

Seller’s power under Stamp duty laws

28

PARTNERSHIP & REAL ESTATE

Introduction of Stock-in-trade

DLF Universal Ltd., 128 TTJ 121 (Delhi)

Introduction and revaluation

D. B. Shah, 1 UTR (Trib) 536 (Ahd)

‘Transfer’ of converted asset

Wipro Ltd., 34 DTR 493 (Bang)

Reorganisation and s.45(4)

Gurunath Talkies. 214 Taxation 729 (Karn)

Retirement and distribution

Puryyankar Ind., 188 Taxman 34 (Karn)

R

HOUSING PROJECTS

Pradip Kapasi & Co. 30

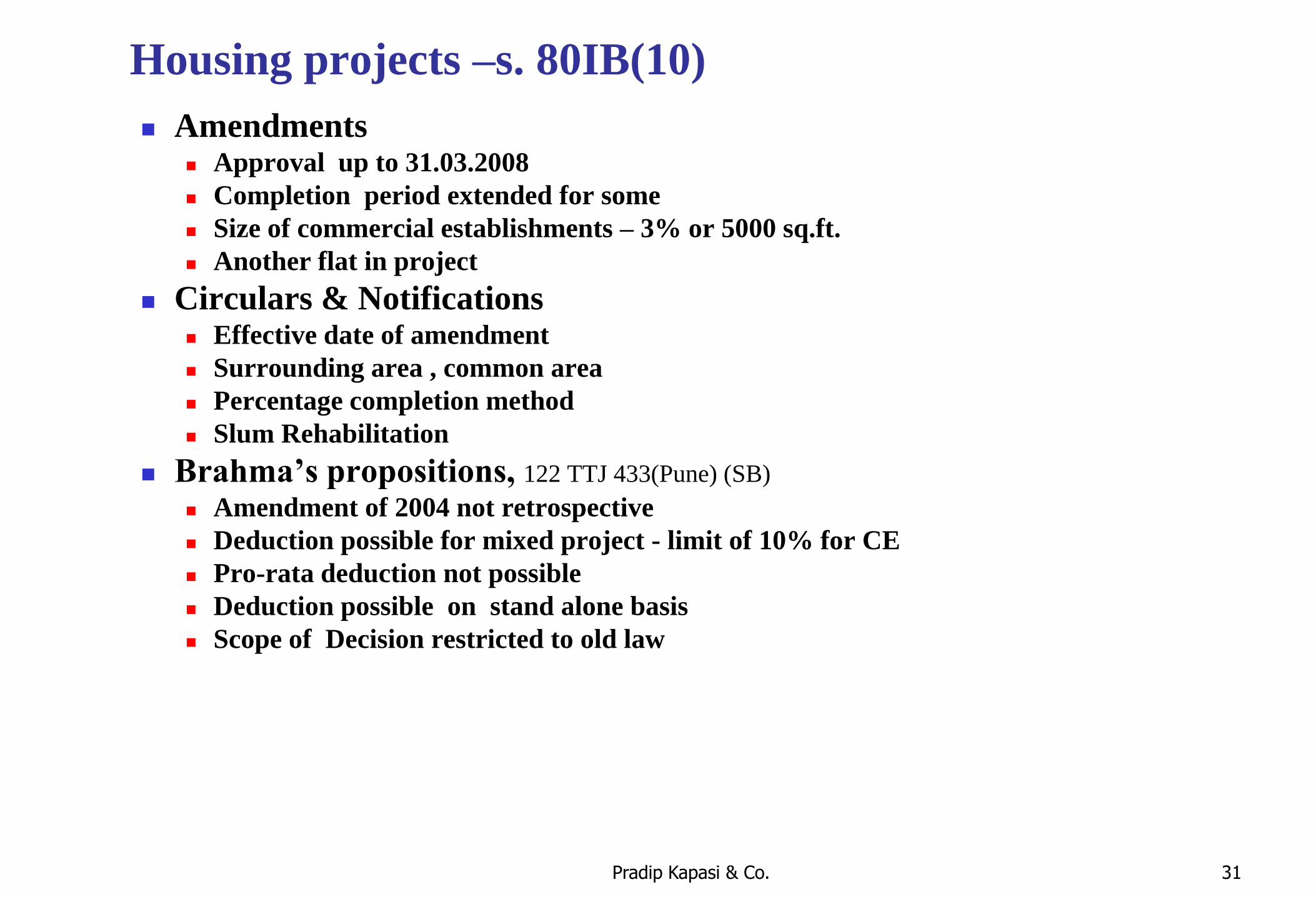

Housing projects –s. 80IB(10)

Amendments Approval up to 31.03.2008

Completion period extended for some

Size of commercial establishments – 3% or 5000 sq.ft.

Another flat in project

Circulars & Notifications Effective date of amendment

Surrounding area , common area

Percentage completion method

Slum Rehabilitation

Brahma’s propositions, 122 TTJ 433(Pune) (SB)

Amendment of 2004 not retrospective

Deduction possible for mixed project - limit of 10% for CE

Pro-rata deduction not possible

Deduction possible on stand alone basis

Scope of Decision restricted to old law

Pradip Kapasi & Co. 31

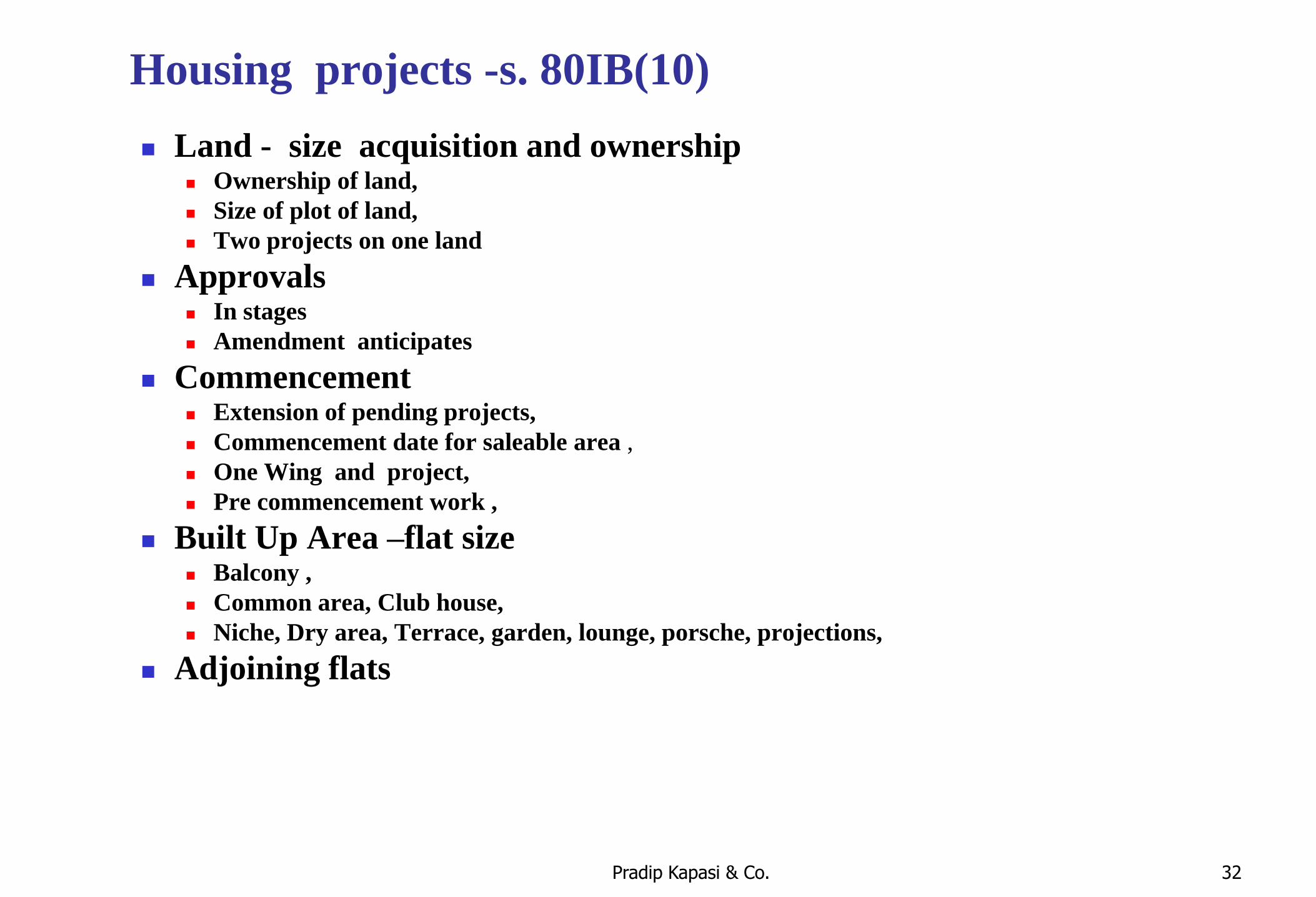

Housing projects -s. 80IB(10)

Land - size acquisition and ownership Ownership of land,

Size of plot of land,

Two projects on one land

Approvals In stages

Amendment anticipates

Commencement Extension of pending projects,

Commencement date for saleable area ,

One Wing and project,

Pre commencement work ,

Built Up Area –flat size Balcony ,

Common area, Club house,

Niche, Dry area, Terrace, garden, lounge, porsche, projections,

Adjoining flats

Pradip Kapasi & Co. 32

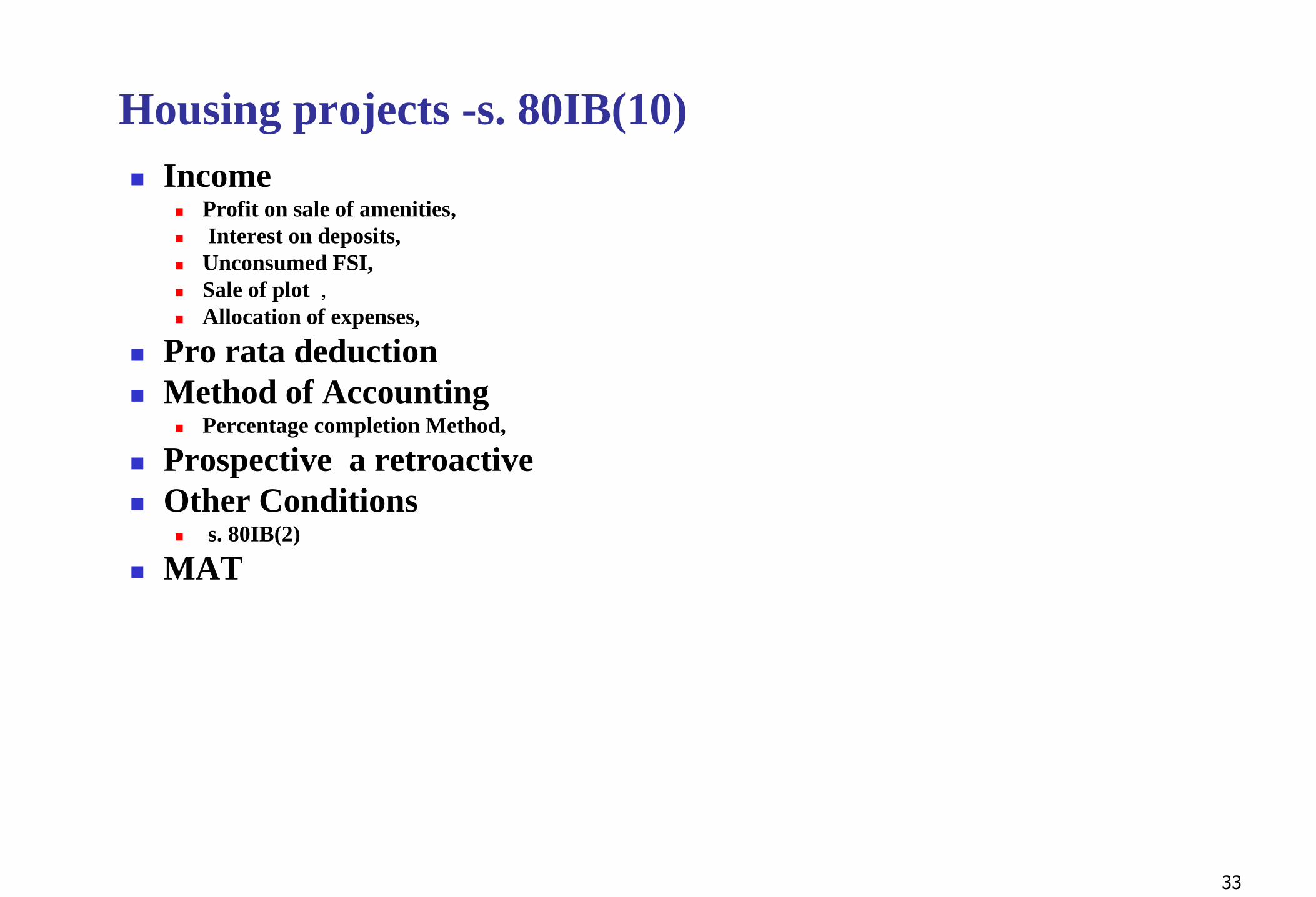

Housing projects -s. 80IB(10)

Income Profit on sale of amenities,

Interest on deposits,

Unconsumed FSI,

Sale of plot ,

Allocation of expenses,

Pro rata deduction

Method of Accounting Percentage completion Method,

Prospective a retroactive

Other Conditions s. 80IB(2)

MAT

33

Housing projects – s. 80IB(10) Brahma Associates, 122 TTJ 433(Pune) (SB)

AIR Developers, 123 TTJ 959(Nag.)

Saroj Sales, 3 DTR 494(Mum)

Radhe Developers, 113 TTJ 300(Ahd) ,

Shakti Corporation, 32 SOT 438 (Hyd),

Smt. Saroj Kapoor, 38 DTR 475(Indore)

Om Engg. & Builders, 109 ITD 235(Pune)

Ansals Property & Ind.22 SOT 45(Delhi)

Sheth Developers 33 SOT 277(Mum),

SJR Builders, 3 ITR (Trib) 569 (Bang)

Vandana Properties, 31 SOT 392(Mum.)

Vimal Builders, 41 A BCAJ 45(Mum)

Lok Holdings, 189 Taxman 452 (Mum)

B. Nagi Reddy, 2 ITR (Trib) 730 (Chennai)

Brigade Enterprises, 119 TTJ 269(Bang.)

G.V. Corporation, 38 SOT 173(Mum.)

Bengal Ambuja(Cal. HC)

B. T. Pate Ent. 28 DTR 451(Pune),

Paarth Corporation, 23 SOT 368 (Mum)

Ganesh Housing Corporation Ltd. 32 SOT 207(Ahd.)

34

THANK YOU

&

GOOD LUCK

Pradip Kapasi & Co. 35