survey of uk construction professional servicescic.org.uk/download.php?f=cicsurvey.pdf · survey of...

TRANSCRIPT

Survey ofUK Construction Professional Services

2005/06

This survey was led and project managed by:

Construction Industry Council (CIC), CIC is a partner in ConstructionSkills

And jointly undertaken by:

Davis Langdon Management Consulting and Experian BS

PROFESSIONAL SURVEY 23/11/07 16:21 Page 1

This research was funded by ConstructionSkills, the Sector Skills Council for Construction,

and carried out by the Construction Industry Council (CIC) as lead partner.

Survey of UK Construction Professionals 2005/06 - REPORT

Davis Langdon Management Consulting July 2007

Contents

1 Executive Summary .................................................................. i

1.1 Headline findings......................................................................... i

1.2 Structure and earnings (see Section 3, page 6)........................... i1.3 Key changes since 1995/96 (see Section 8, page 26) .................ii

1.4 Profile and type of work (see Sections 4 & 5, pages 12 and 17) ..ii

1.5 Regional and overseas profile (see Section 6, page 20)..............ii1.6 Employment (see Section 7, page 23).........................................ii

2 Introduction .............................................................................. 1

2.1 Survey aims and scope .............................................................. 1

2.2 Scope of the report..................................................................... 12.3 Summary of survey sample and response.................................. 2

2.4 Classification of Firms ................................................................ 3

2.5 Analysis of Responses ............................................................... 33 Structure of the CPS sector and fee income .......................... 5

3.1 Headline findings........................................................................ 5

3.2 Structure of the CPS sector........................................................ 53.3 Gross Fee income by type of business (2005/06)....................... 7

3.4 UK Fee income by size of business............................................ 8

3.5 Fee income by type of business ................................................. 9

4 Profile of work by sector and discipline ............................... 114.1 Headline findings...................................................................... 11

4.2 Main services provided by type of firm...................................... 11

4.3 Breakdown of services ............................................................. 125 Type of work ........................................................................... 16

5.1 Headline findings...................................................................... 16

5.2 Overall breakdown ................................................................... 165.3 Sector of work (DTI Classifications).......................................... 17

5.4 Type of project ......................................................................... 17

6 Regional and overseas profile of work ................................. 19

6.1 Headline findings...................................................................... 196.2 UK Regions .............................................................................. 19

6.3 Overseas Fee Income .............................................................. 20

7 Employment............................................................................ 227.1 Headline findings...................................................................... 22

7.2 Employment profile................................................................... 22

7.3 Breakdown by type and size of business.................................. 23

7.4 Per capita fee income............................................................... 248 Headline changes since 2002 ................................................ 25

8.1 Headline findings...................................................................... 25

8.2 Fee income .............................................................................. 258.3 Trends in construction and professional activity ....................... 26

8.4 Improvements in the performance and productivity of the CPS

sector ....................................................................................... 298.5 Services provided..................................................................... 30

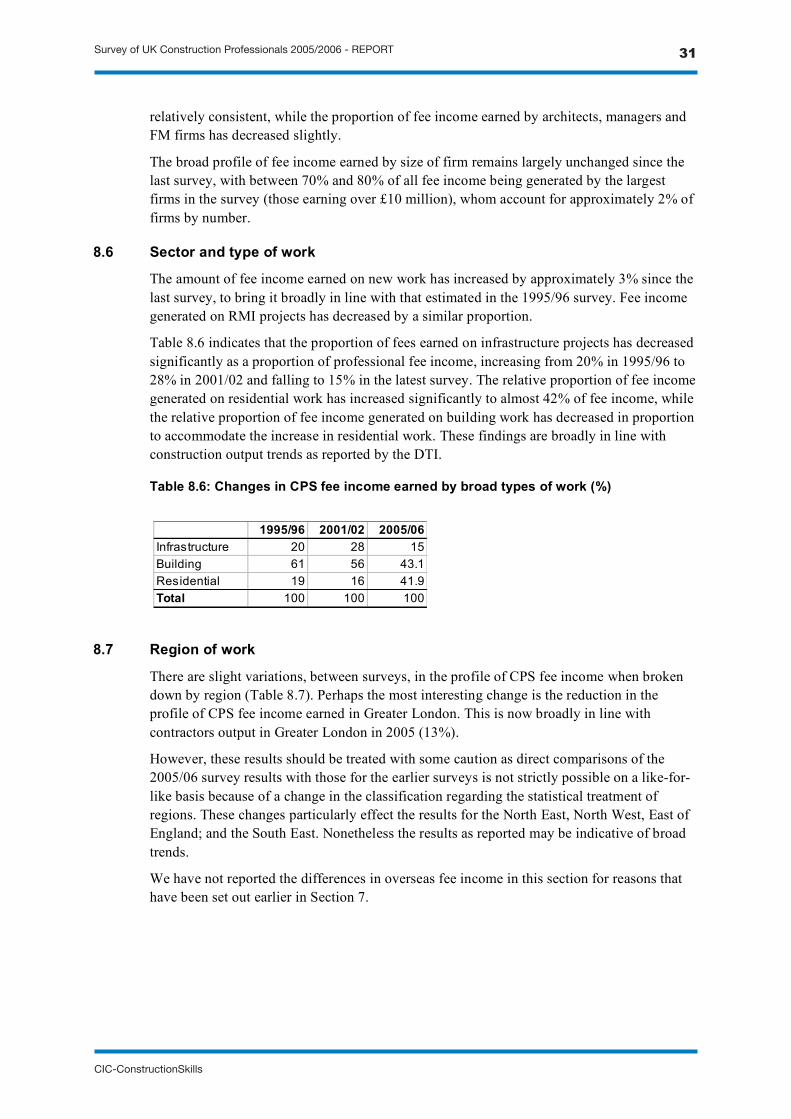

8.6 Sector and type of work............................................................ 31

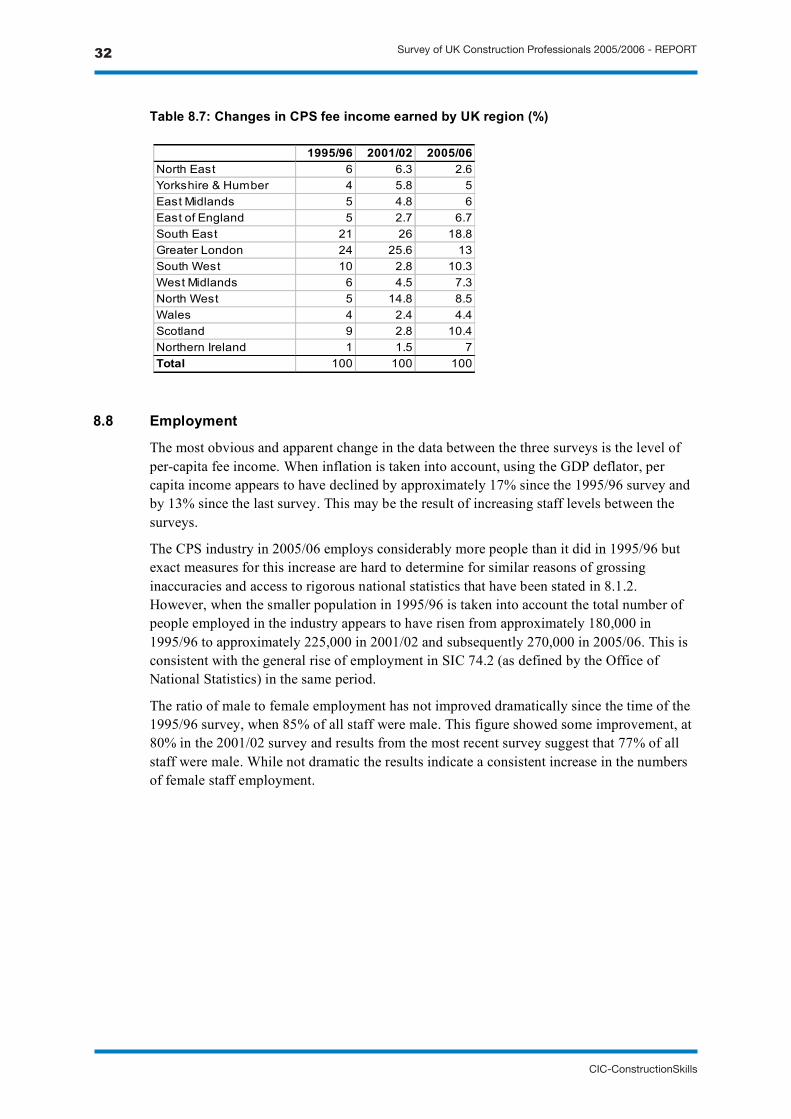

8.7 Region of work ......................................................................... 31

8.8 Employment ............................................................................. 32

Annex 1 ................................................................................... 33

Survey of UK Construction Professionals 2005/2006 - RePoRt

CIC-ConstructionSkills

19)22)

Survey of UK Construction Professionals 2005/06 - REPORT i

Davis Langdon Management Consulting July 2007

1 Executive Summary

1.1 Headline findings

This is the third comprehensive survey of the Construction Professional Services (CPS)

sector in the UK. Its aim has been to assess the size of the UK market for construction

professional services. The results have been based on detailed information of fee income and

the services provided by construction professional services firms in the financial year

2005/06. They represent the responses of a representative sample of over 800 construction

professional firms of all types and sizes.

Size of market 2005/06

UK professional services firms earned a total of £13.9 billion on projects in the UK

There were approximately 27,950 professional firms in the UK.

UK Market shares (% of UK fee income)

Engineering services accounted for 28% of all work, £3.9 billion

Architecture services accounted for 24% of all work, £3.3 billion

Surveying services accounted for 17% of all work, £2.3 billion

Management accounted for 12% of all work, £1.7 billion.

Income by type of firm

Per capita fee income for professionals increased steadily by size of firm and mean per

capita fee income for the smallest firms (<£200k fee income pa) is £65K per annum.

Income by size of firm

A small number of large firms (2%) generated almost 80% of UK fee income.

Regional and Overseas Markets

A third of UK fee income is earned on projects in the South East and Greater London

£2.5 billion of fee income is earned by UK firms on work overseas.

Employment

Approximately 270,000 people were employed by construction professional firms

77% of this total were male.

1.2 Structure and earnings

Approximately 27,950 professional services firms earn a total of £13.9 billion on UK

construction projects. The size of the overseas market for UK CPS firms is estimated to be

approximately £2.5 billion – 15% of total fee income.

79% of all CPS firms operate from a single office and 84% employ less than 10 people -

28% of all firms are single person practices. 2% of firms earn over £10 million per annum

and employ more than 50 people – yet this small group of firms are responsible for

generating 78% of all UK fee income.

Survey of UK Construction Professionals 2005/06 - REPORT i

Davis Langdon Management Consulting July 2007

1 Executive Summary

1.1 Headline findings

This is the third comprehensive survey of the Construction Professional Services (CPS)

sector in the UK. Its aim has been to assess the size of the UK market for construction

professional services. The results have been based on detailed information of fee income and

the services provided by construction professional services firms in the financial year

2005/06. They represent the responses of a representative sample of over 800 construction

professional firms of all types and sizes.

Size of market 2005/06

UK professional services firms earned a total of £13.9 billion on projects in the UK

There were approximately 27,950 professional firms in the UK.

UK Market shares (% of UK fee income)

Engineering services accounted for 28% of all work, £3.9 billion

Architecture services accounted for 24% of all work, £3.3 billion

Surveying services accounted for 17% of all work, £2.3 billion

Management accounted for 12% of all work, £1.7 billion.

Income by type of firm

Per capita fee income for professionals increased steadily by size of firm and mean per

capita fee income for the smallest firms (<£200k fee income pa) is £65K per annum.

Income by size of firm

A small number of large firms (2%) generated almost 80% of UK fee income.

Regional and Overseas Markets

A third of UK fee income is earned on projects in the South East and Greater London

£2.5 billion of fee income is earned by UK firms on work overseas.

Employment

Approximately 270,000 people were employed by construction professional firms

77% of this total were male.

1.2 Structure and earnings

Approximately 27,950 professional services firms earn a total of £13.9 billion on UK

construction projects. The size of the overseas market for UK CPS firms is estimated to be

approximately £2.5 billion – 15% of total fee income.

79% of all CPS firms operate from a single office and 84% employ less than 10 people -

28% of all firms are single person practices. 2% of firms earn over £10 million per annum

and employ more than 50 people – yet this small group of firms are responsible for

generating 78% of all UK fee income.

CIC-ConstructionSkills

Survey of UK Construction Professionals 2005/2006 - RePoRt i

This is the third comprehensive survey of the Construction Professional Services (CPS) sector in the UK carried out by the Construction Industry Council (CIC). The project follows earlier surveys that were conducted in 1996 and 2002. Its aim has been to assess the size of the UK market for construction professional services. The results have been based on detailed information of fee income and the services provided by construction professional services firms in the financial year 2005/06. They represent the responses of a representative sample of over 800 construction professional firms of all types and sizes.

Survey of UK Construction Professionals 2005/06 - REPORT ii

Davis Langdon Management Consulting July 2007

Firms that describe themselves as being multidisciplinary earn almost 50% of all UK fee

income and 50% of all CPS output is generated in the provision of architecture and

engineering services.

1.3 Key changes since previous surveys

Output of CPS firms has risen by approximately 4% (in real terms) in the four years since the

last survey, which is slightly below contractors output for the same period.

There has been very little change in the proportion of core services that are provided by the

sector but there have been significant changes in the type and profile of firms that deliver

these services – with growth in the proportion of outputs from multidisciplinary firms.

Residential projects have experienced the largest rise as a proportion of all work since

2001/02, accounting for 42% of all fee income – an increase of 26% in the overall proportion

since the last survey.

Per capita fee income per professional has decreased since the time of the last survey, with a

fall of 13% in real terms. This is likely to be the result of increasing staff levels. The

proportion of male to female staff within each type of CPS firm has not improved

significantly, 77% of all employment in the sector is male.

1.4 Profile and type of work

Almost two-thirds of fee income is earned on new work (62%) with 32% being earned on

refurbishment projects and the balance – 6% being earned on repair and maintenance work.

Fees earned on building projects (in particular offices) account for the largest proportion

(43%) of fee income closely followed by fees earned on residential projects (42%). The

proportion of fees earned on infrastructure projects is considerably smaller (15%).

In terms of clients, 75% of fee income was generated from private sector clients (including

PFI/PPP projects) with the remaining 25% coming from public sector clients.

1.5 Regional and overseas profile

A third of all fee income was generated on projects in the South East of England and Greater

London. Other regions with relatively large CPS inputs are the South West and Scotland.

Approximately £2.5 billion of fee income was received by practices in the UK for

professional services provided on overseas projects.

1.6 Employment

The CPS sector employs approximately 270,000 permanent employees. On average, 77% of

all employment in the sector is male.

When fee income and employment are compared, engineering firms employ 17% of all staff

and are responsible for 15% of all income. Architects employ 14% of the total workforce and

generate 11% of fee income. Surveying practices employ 16% of staff and are responsible

for 15% of all fee income.

CIC-ConstructionSkills

ii Survey of UK Construction Professionals 2005/2006 - RePoRt

Survey of UK Construction Professionals 2005/06 - REPORT

Davis Langdon Management Consulting July 2007

1

2 Introduction

This report contains the findings of the first major survey of the UK Construction

Professional Services Sector to have taken place in the last four years. It is a survey of

professional services practices and firms, their outputs and activity, for the financial year

2005/06.

The organisations that responded to this survey form a broad and representative cross section

of the professional services sector. The results detail the findings from over 800 companies,

who between them employ over 45,000 full time members of staff and generate a fee income

of over £2.5 billion.

The results have been used in conjunction with available population data to provide

estimates on the size and output of construction professional services firms. This is a survey

of firms that are in private practice and does not therefore represent the totality of

professional services that contribute towards UK construction. Many construction

professionals work within large contracting or client organisations and this survey does not

include the inputs that such individuals contribute to UK construction activity.

This is a cross sectional, ‘snap shot’, study and therefore it has not been possible to provide a

longitudinal analysis of the intervening years between this and the previous survey.

However, a section of this report is devoted to highlighting the key differences between the

comparable results for the surveys of 1996, 2002 and those of 2006.

2.1 Survey aims and scope

This survey is a collaborative project involving the Construction Industry Council, their

principal professional members and ConstructionSkills. The principal investigators for the

research have been Davis Langdon Management Consulting (DLMC) and Experian, both

consultancy practices carried out the previous research.

The study’s key objectives have been to:

quantify the volume of outputs of the construction professional services sector in the UK

provide various breakdowns of professional services output, which include:

o the type of services traded by UK construction professional practices

o the type of service providers and suppliers

o the main elements of construction work for which professional services are traded

o regional variations in the survey results

identify the various service functions undertaken within each of the major professional

disciplines

provide data and information that is of interest to all of the major stakeholders in the

project, including the CIC, its member organisations, ConstructionSkills and professional

services firms themselves

maximise the response rate to the survey to provide the most statistically robust results

within a sampling frame of 12,924 firms.

2.2 Scope of the report

Part 1 (this report) provides the analysis of responses in the main survey and highlights the

main issues that arise from it. There is a summary of key findings at the start of each section

CIC-ConstructionSkills

Survey of UK Construction Professionals 2005/2006 - RePoRt 1

Survey of UK Construction Professionals 2005/06 - REPORT

Davis Langdon Management Consulting July 2007

2

of the report, which is followed by a more detailed commentary of survey responses. Part 2

of the report documents the methodology that has been adopted for the survey. Brief

explanations of the key issues that have affected the analysis have been included in this

document but please refer to Part 2 for a detailed explanation of the key issues that have

affected the overall analysis.

2.3 Summary of survey sample and response

The results that are presented in this report are based on 801 completed questionnaires, from

an original sample of 12,924 firms (a response rate of 6.2%). The research team originally

set a target of 1,000 responses in order to achieve an acceptable level of accuracy when

presenting the findings. While the response rate was not as high as had been sought at the

outset, it falls somewhere between the response rates obtained on previous surveys, as such

we believe the results as presented are statistically valid.

The 2002 survey achieved 927 valid responses, from an original sample of 10,000 firms (a

response rate of 9.3%). The 1996 survey achieved 824 valid responses from a sample of

15,000 firms (a response rate of 5.4%), both proved to be statistically robust for the headline

issues that were covered by those studies.

We believe that respondent fatigue may be a factor in the decline in response rate evident

between the second and third surveys. Since the last survey there has been increasing interest

in the CPS sector generally, and we are aware of a growing number of survey requests made

on Construction professional service firms.

Given the highly sensitive and complex levels of financial information that each respondent

has had to supply, the research team are extremely thankful to all those that took part and are

pleased with the overall response.

One sampling source has been used for the survey, which has been provided by Experian. In

carrying out initial research for the survey it was found that no comprehensive data is kept by

institutional or government sources that provides a sound basis for the sampling and grossing

of the CPS sector – a situation that is essentially unchanged since previous surveys. The need

to look outside institutional and government records therefore became an important element

of our work in developing the sampling frame.

In seeking a suitable source of data, the research team carried out a review of other sources.

In particular the Inter Departmental Business Register (IDBR), which was used in the 1996

survey.

Significant problems exist with the IDBR. These include:

the lack of any personal contacts to whom the questionnaire could have been sent,

risking an adverse affect on the overall response rate

a classification based on high level SIC (Standard industrial classification) codes, which

introduces a high risk of questionnaire redundancy because of the inability to identify

‘true’ construction organisations within the sample

restrictions on the data’s use, when used by third parties, which would have created

severe time constraints for the survey.

CIC-ConstructionSkills

2 Survey of UK Construction Professionals 2005/2006 - RePoRt

Survey of UK Construction Professionals 2005/06 - REPORT

Davis Langdon Management Consulting July 2007

3

Our research showed that Experian’s National Business Database provided the most useful,

practical and cost effective source of data in developing the sample framework, especially in

relation to smaller firms, for which there was extensive coverage.

The Experian National Business Database

The sampling source for the survey was Experian’s National Business Database, which is an

amalgam of the Thomson, Yellow Pages and Companies House data covering approximately

4.2 million businesses in the UK.

Our sample has been chosen from a population of approximately 28,000 organisations in 24

construction related categories in the Experian dataset. The majority of firms within the

sample have been drawn from the traditional disciplines of architecture, engineering and

surveying. A full breakdown of the sample structure can be found in Part 2 of this report.

Selection for the sampling frame by type of firm and region was in relation to the proportion

of firms in the global population, with the exception of Northern Ireland. For Northern

Ireland, the size of the survey sample was boosted to the total population of firms to ensure

that the minimum of 50 responses required to provide a robust analysis of the sector in

Northern Ireland was received. For size of firm, the sample was biased in the direction of

large firms to ensure the greatest coverage of the sector in terms of fee income and

employment.

2.4 Classification of Firms

The stratification of the survey sample has been based upon the type of firm, size of firm and

region. This has been based on classifications, which are loosely based on SIC Minor Codes

(Standard Industrial Classifications), which have been adapted, extended, or condensed to

suit the format of the sampling frame. The questionnaire used fewer categories than the 24

that were used to develop the sample. For the purposes of simplicity and interpretation, the

classifications have been recoded into:

Architects

Quantity surveyors

Surveyors (other)

Building services engineers

Civil and structural engineers

Planners (town planners)

Project managers

Multidisciplinary practices

2.5 Analysis of Responses

Response by type of firm

The survey was sent out at the beginning of November 2006, with responses requested by the

end of that month. Of the 891 questionnaires that were returned by responding companies,

801 contained sufficient data to be considered valid, representing an overall response rate of

6.2%. Over 90% of those that responded provided answers for their practice as a whole with

the remainder providing responses in terms of a local office. Responding firms employed

some 45,432 members of staff and generated over £2.56 billion of UK fee income.

CIC-ConstructionSkills

Survey of UK Construction Professionals 2005/2006 - RePoRt 3

Survey of UK Construction Professionals 2005/06 - REPORT

Davis Langdon Management Consulting July 2007

4

The response to the survey largely reflected the structure of the overall population by type of

firm, size band of firm and region. Figure 2.1 shows the distribution of respondents by size

of firm and Part 2 of this report provides a breakdown of responses, against the structure of

the original population.

Figure 2.1: Survey responses – distribution of respondents by size of firm (DTI

classifications)

Note: Size bands relate to those used in DTI’s Construction Statistics Annual, 2007

When viewed in terms of firm size, the sample displays typically, negatively skewed

characteristics. The shape and relative proportions of this distribution are very similar to that

for construction contracting organisations.

Companies that employ less than 4 employees within the sample represent approximately

45% of all firms by number. These companies employ 1.4% of all of the employees within

the sample and generate 1.2% of the fee income. While firms that employ over 300 members

of staff represent approximately 2% of all firms in the sample (by number), are responsible

for 75% of employment and 76% of total fee income within the sample.

The unadjusted fee income data is heavily skewed towards the largest firms, with 60% of the

fee income being generated by 1% of the firms. The sample has therefore been normalised

with respect to fee income, to ensure that the largest firms have not unduly influenced the

results. The overall fee income generated by the unadjusted sample is £2.6 billion. The

adjusted, normalised sample, which forms the basis of the various fee income estimates

presented in this report, accounts for some £1.5 billion of fee income.

To provide a robust estimate of the actual number of firms in the sector we have de-

duplicated all of the records in the original population dataset, both within and between the

various corporate classifications. Where the same companies have appeared in more than one

of the dataset classifications (for example, as both Acoustic Engineers and Building Services

Consultants) we have included them within the larger, core discipline.

0

5

10

15

20

25

30

35

40

45

50

1-3 4-7 8-13 14-24 25-34 35-59 60-79 80-114 115-299 300-599 300-1199 >1200

No. employees in UK

Pe

rce

nt

CIC-ConstructionSkills

4 Survey of UK Construction Professionals 2005/2006 - RePoRt

Survey of UK Construction Professionals 2005/06 - REPORT

Davis Langdon Management Consulting July 2007

5

3 Structure of the CPS sector and fee income

3.1 Headline findings

Firms

There are approximately 27,950 firms in the CPS sector

79% of CPS firms operate from a single office

28% of CPS firms are single person practices

84% of CPS firms employ less than 10 people

45% of CPS firms earn up to £200,000 per year

Only 2% of all firms earn more than £10 million per year

2% of CPS firms employ over 50 people

Fee income

The sector generated approximately £13.9 billion in fee income during 2005/06

Architecture and engineering services account for 52% of fee income

Nearly 50% of fee income is earned by multidisciplinary firms

3.2 Structure of the CPS sector

We estimate that there are now approximately 28,000 CPS firms in the UK, compared to our

estimates of 23,500 firms in 2002. Our commentary relating to this change can be found in

Section 8. Breakdowns of the sector by size of firm and turnover are presented in Tables 3.1

and 3.2.

Table 3.1: Estimated number of CPS firms by main type and number of employees (%

and no.)

No. of employees 1 2-5 6-10 11-50 >50 Total

Architects 4062 4857 1339 1071 126 11455

35 43 12 9 1 100

Civil & structural engineers 1189 2181 994 1423 321 6108

20 36 16 23 5 100

Building services engineers 780 1688 672 751 110 4001

19 42 17 19 3 100

Other surveyors 619 981 273 205 29 2107

29 47 13 10 1 100

Quantity surveyors 550 845 298 242 16 1951

28 44 15 12 1 100

Managers 255 545 197 147 34 1178

22 46 17 12 3 100

Others (including planners) 366 464 166 124 27 1147

32 40 15 11 2 100

Total 7821 11561 3939 3963 663 27947

Note: Figures in italics are proportions

CIC-ConstructionSkills

Survey of UK Construction Professionals 2005/2006 - RePoRt 5

Survey of UK Construction Professionals 2005/06 - REPORT

Davis Langdon Management Consulting July 2007

6

79% of the respondents within the survey operate from a single office. The proportion of

single office practices is highest amongst planners, at 95%, followed by architects at 90%,

which compares to 50% of multi-disciplinary firms, the group exhibiting the lowest

proportion of single office practices.

Of the 20% of CPS firms that operate from multiple offices, 78% of these operate from four

offices or less. Only 6% of these practices operate from 10 offices or more.

Table 3.2: Estimated number of CPS firms by main type and fee income (% and no.)

Fee incomeSmall

<£200k

Medium

£200k-£1m

Large

>£1m-£10m

Largest

>£10m Total

Architects 6071 3895 1375 114 11455

53 34 12 1 100

Civil & structural engineers 2321 2382 1222 183 6108

38 39 20 3 100

Building services engineers 1321 1520 1080 80 4001

33 38 27 2 100

Other surveyors 948 822 316 21 2107

45 39 15 1 100

Quantity surveyors 1034 663 234 20 1951

53 34 12 1 100

Managers 553 425 188 12 1178

47 36 16 1 100

Others (including planners) 390 471 275 11 1147

34 41 24 1 100

Total 12638 10178 4690 441 27947

Note: Figures in italics are proportions

Table 3.3 below highlights the operating structure and fee income of CPS firms. The

majority operate as private Limited companies, followed by sole practitioners. In terms of

fee income Limited companies both public and private account for the vast majority of fee

income. Indeed, while PLCs only account for 1% of firms they account for 42% of fee

income as would be expected given that these are the largest firms in the sector. Also of

interest is the number of sole practitioners providing construction professional services,

although the fee income they generate is relatively small.

Table 3.3: Operating structure of CPS firms (%)

No of firms % Fee income %

Partnership 14.2 5.3

LLP 4.7 10.5

Ltd Co 52.1 40.9

PLC 1.1 42.3

Sole practitioner 27.9 1

Total 100 100

CIC-ConstructionSkills

6 Survey of UK Construction Professionals 2005/2006 - RePoRt

Survey of UK Construction Professionals 2005/06 - REPORT

Davis Langdon Management Consulting July 2007

7

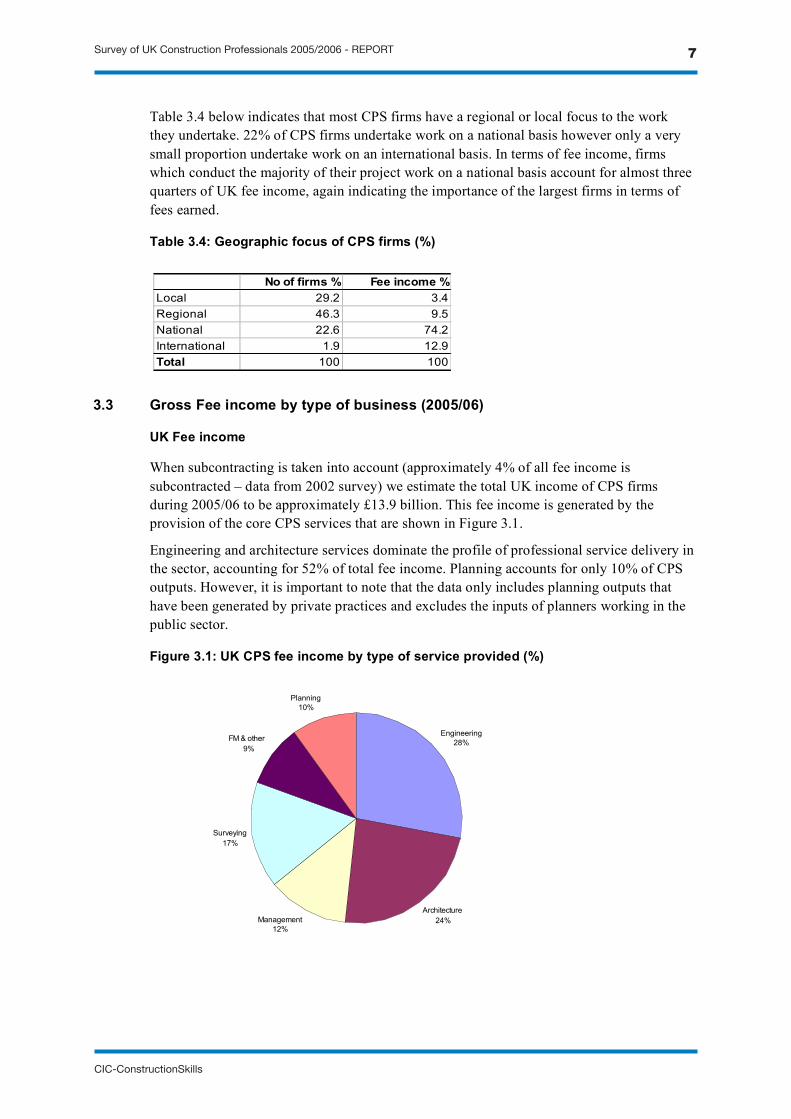

Table 3.4 below indicates that most CPS firms have a regional or local focus to the work

they undertake. 22% of CPS firms undertake work on a national basis however only a very

small proportion undertake work on an international basis. In terms of fee income, firms

which conduct the majority of their project work on a national basis account for almost three

quarters of UK fee income, again indicating the importance of the largest firms in terms of

fees earned.

Table 3.4: Geographic focus of CPS firms (%)

3.3 Gross Fee income by type of business (2005/06)

UK Fee income

When subcontracting is taken into account (approximately 4% of all fee income is

subcontracted – data from 2002 survey) we estimate the total UK income of CPS firms

during 2005/06 to be approximately £13.9 billion. This fee income is generated by the

provision of the core CPS services that are shown in Figure 3.1.

Engineering and architecture services dominate the profile of professional service delivery in

the sector, accounting for 52% of total fee income. Planning accounts for only 10% of CPS

outputs. However, it is important to note that the data only includes planning outputs that

have been generated by private practices and excludes the inputs of planners working in the

public sector.

Figure 3.1: UK CPS fee income by type of service provided (%)

Engineering

28%

Architecture

24%Management

12%

Surveying

17%

FM & other

9%

Planning

10%

No of firms % Fee income %

Local 29.2 3.4

Regional 46.3 9.5

National 22.6 74.2

International 1.9 12.9

Total 100 100

CIC-ConstructionSkills

Survey of UK Construction Professionals 2005/2006 - RePoRt 7

Survey of UK Construction Professionals 2005/06 - REPORT

Davis Langdon Management Consulting July 2007

8

The amount of fee income generated in the provision of each of these services is estimated to

be:

Engineering £3.9 billion

Architecture £3.3 billion

Management £1.7 billion

Surveying £2.3 billion

FM and other £1.3 billion

Planning £1.4 billion

Total £13.9 billion

A thorough breakdown of this fee income is included in the following sections.

3.4 UK Fee income by size of business

For reporting purposes we have classified firms as being ‘small’, ‘medium’, ‘large’ and

‘largest’, based upon four turnover bands. These bands are based on those that were used in

the previous survey and have been adjusted to allow for inflation of fee income since 2002.

The four size band groups are:

Small - earning less than £200k per year

Medium - earning between £200k and £1 million per year

Large - earning over £1 million but less than £10 million per year

Largest – earning equal to or more than £10 million per year

Figure 3.2 details CPS fee income by size of firm. Not surprisingly, the largest firms

generate the majority of all fee income.

CPS firms in this category generate approximately 78% of all fee income (£10.8 billion) and

yet they account for only 2% of all firms by number (approximately 550 organisations). As

the size of CPS firms increases, the geographical profile of their work widens. Firms earning

less than £1 million generate the majority of their fee income on local projects or regionally

(accounting for approximately 85% of all work). The data shows that the majority of the

largest firms tend to operate nationally, with over 82% of their work being generated on a

national portfolio of projects (refer to Section 6).

Figure 3.2: UK CPS Fee income by size of business (£ billion)

0 2 4 6 8 10 12

<£200k

£200k-£1m

>£1m-£10m

>£10m

Siz

e o

f fi

rm

UK fee income (£bn)

CIC-ConstructionSkills

8 Survey of UK Construction Professionals 2005/2006 - RePoRt

Survey of UK Construction Professionals 2005/06 - REPORT

Davis Langdon Management Consulting July 2007

9

3.5 Fee income by type of business

3.5.1 Estimates of fee income by type of firm

Our data suggest that over 48%, or £6.6 billion, of all fee income is earned by organisations

that describe themselves as being ‘Multidisciplinary’. These firms account for only 8% of all

CPS organisations (by number).

Other types of CPS firm account for the remaining 52% of fee income (£7.2 billion).

Engineering firms generate 15% of all fee income (£2.1 billion) and account for 21% of all

CPS organisations by number. Architectural practices account for 11% of total fee income

(£1.5 billion) whilst surveying firms account for 16% of overall output.

Multidisciplinary firms do provide a broad range of services. However, in many cases one

service tends to dominate the profile of firms who choose to describe themselves as

multidisciplinary. The provision of any one service by such firms often exceeds 50% of total

fee income but is rarely above 70%.

Figure 3.3: Proportion of UK CPS fee income earned by type of firm (%)

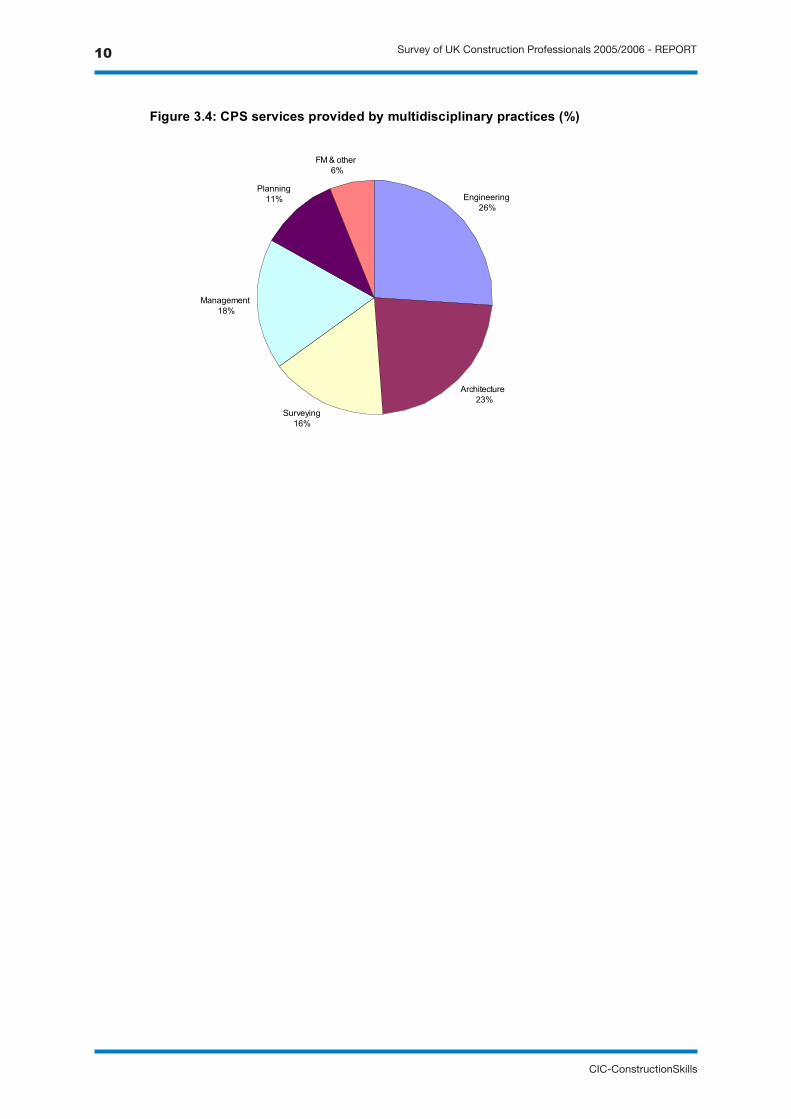

3.5.2 Multidisciplinary practices

The data support the fact that these firms do offer a wide range of services, from more than

one core discipline (Figure 3.4). The dominant service offered by such firms, in terms of fee

income, is engineering, which accounts for 26% of the outputs from multidisciplinary firms

(approximately £1.7 billion) followed by architecture services which account for 23%

(approximately £1.5 billion). The core disciplines of surveying and management generate

roughly equal proportions of outputs for multidisciplinary CPS firms (between 16% and 18%

each), whilst FM services and planning account for 17% of the total fee income from these

firms.

Architecture

11%

Building services

engineering

7%

Civil and structural

engineering

8%Management consultancy

0%

Multi-disciplinary

49%

Planning

1%

Project management

6%

Quantity surveying

14%

Surveying

1%

Other

3%

CIC-ConstructionSkills

Survey of UK Construction Professionals 2005/2006 - RePoRt 9

Survey of UK Construction Professionals 2005/06 - REPORT

Davis Langdon Management Consulting July 2007

10

Figure 3.4: CPS services provided by multidisciplinary practices (%)

Engineering

26%

Architecture

23%

Surveying

16%

Management

18%

Planning

11%

FM & other

6%

CIC-ConstructionSkills

10 Survey of UK Construction Professionals 2005/2006 - RePoRt

Survey of UK Construction Professionals 2005/06 - REPORT

Davis Langdon Management Consulting July 2007

11

4 Profile of work by sector and discipline

4.1 Headline findings

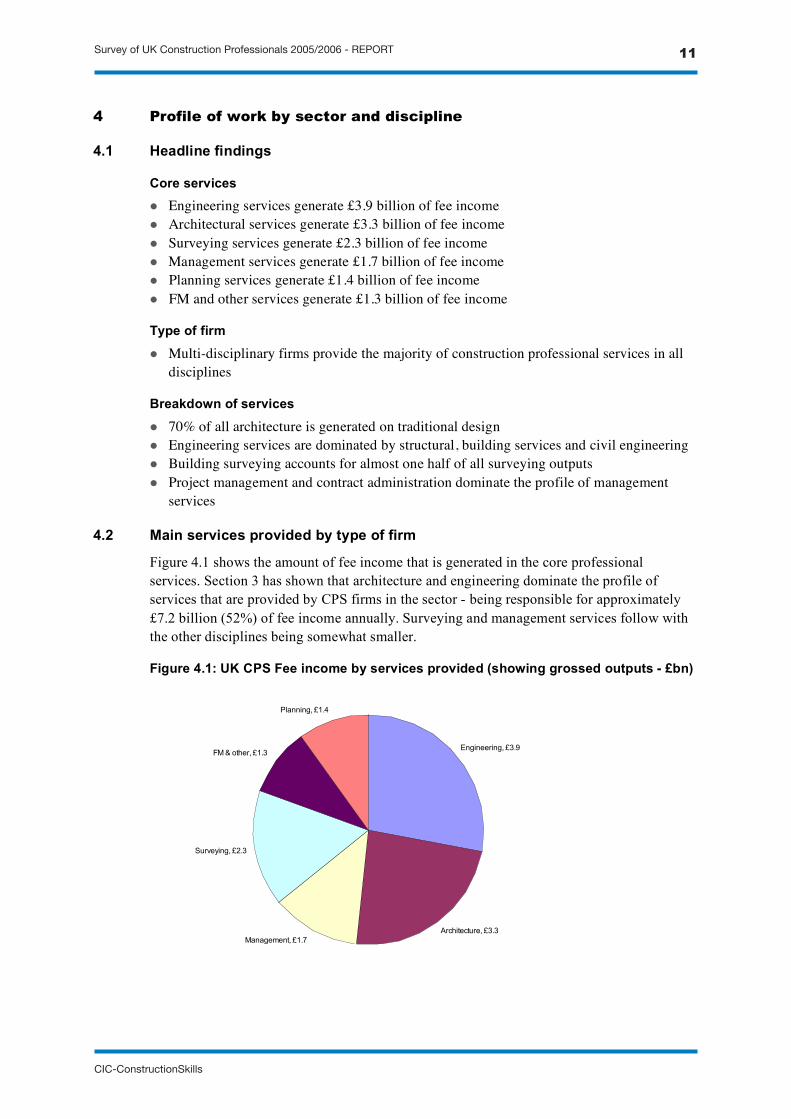

Core services

Engineering services generate £3.9 billion of fee income

Architectural services generate £3.3 billion of fee income

Surveying services generate £2.3 billion of fee income

Management services generate £1.7 billion of fee income

Planning services generate £1.4 billion of fee income

FM and other services generate £1.3 billion of fee income

Type of firm

Multi-disciplinary firms provide the majority of construction professional services in all

disciplines

Breakdown of services

70% of all architecture is generated on traditional design

Engineering services are dominated by structural, building services and civil engineering

Building surveying accounts for almost one half of all surveying outputs

Project management and contract administration dominate the profile of management

services

4.2 Main services provided by type of firm

Figure 4.1 shows the amount of fee income that is generated in the core professional

services. Section 3 has shown that architecture and engineering dominate the profile of

services that are provided by CPS firms in the sector - being responsible for approximately

£7.2 billion (52%) of fee income annually. Surveying and management services follow with

the other disciplines being somewhat smaller.

Figure 4.1: UK CPS Fee income by services provided (showing grossed outputs - £bn)

Engineering, £3.9

Architecture, £3.3

Management, £1.7

Surveying, £2.3

FM & other, £1.3

Planning, £1.4

CIC-ConstructionSkills

Survey of UK Construction Professionals 2005/2006 - RePoRt 11

Survey of UK Construction Professionals 2005/06 - REPORT

Davis Langdon Management Consulting July 2007

12

Table 4.1 below details UK fee income earned by type of CPS firm and the services that they

provide.

Table 4.1: Breakdown of core services provided by type of CPS business

Percent

Planningservices

Architectureservices

Engineeringservices

Surveyingservices

Managementservices

FM & otherservices

Architects 14.6 29.2 2.2 3.3 4.5 15.3

Building services engineers 3.8 3.8 18.8 1.3 6.5 5.9

Civil and structural engineers 5.4 3.2 22.1 2.3 6.9 6.2

Multi-disciplinary 48.3 52.3 50.5 41.3 40.9 54.3

Planning 21.0 3.4 0.0 1.4 1.9 1.8

Project management 2.0 2.9 0.5 3.9 22.2 3.5

Quantity surveyors 3.4 3.6 4.1 29.6 14.8 10.1

Surveyors 1.5 1.6 1.8 16.9 2.3 2.9

Total 100.0 100.0 100.0 100.0 100.0 100.0

4.2.1 Breakdown by type of firm

Table 4.1 shows that multi-disciplinary firms provide the majority of CPS services in all

disciplines. Indeed, multi-disciplinary firms provide over one half of the total of architecture,

engineering and FM services. This is not surprising, as the multi-disciplinary practices tend

to be the largest firms, who in turn generate the majority of fees in the CPS sector as a

whole.

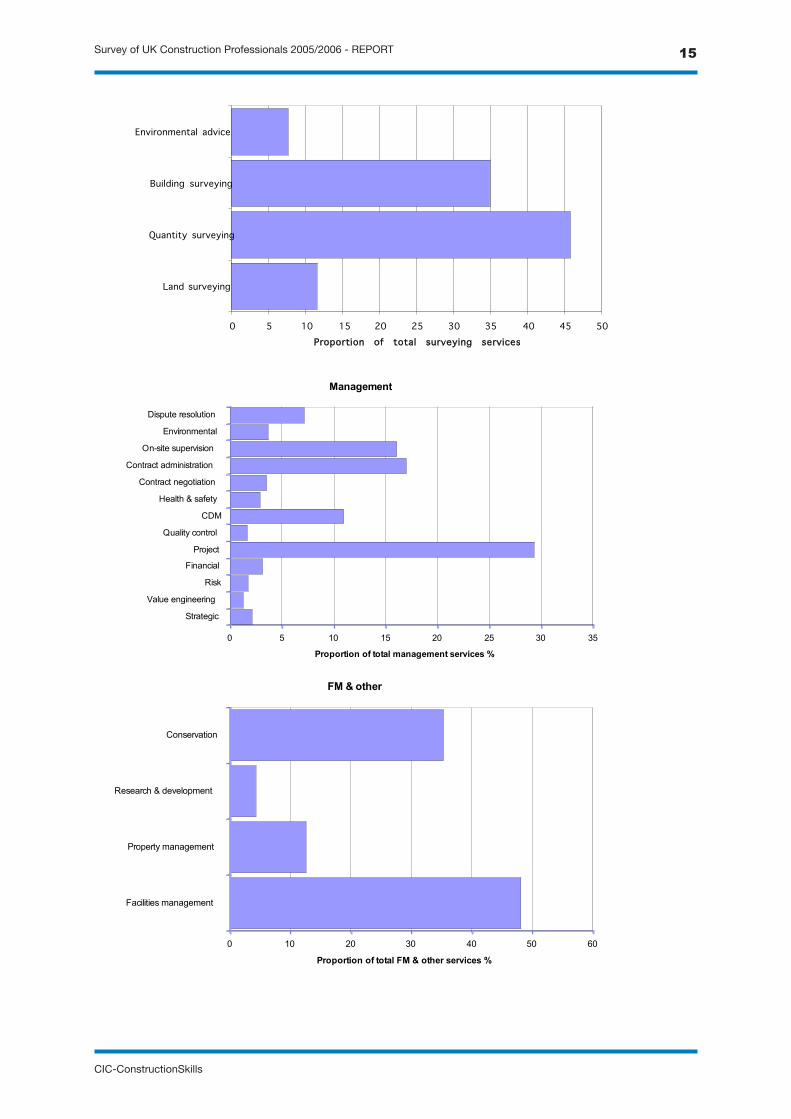

4.3 Breakdown of services

Figure 4.2 shows the proportions of individual services that fall within the core service

headings, irrespective of the type of firm. These display the following main characteristics.

4.3.1 Architecture

The field of architecture is dominated by the architectural design of buildings. This may not

seem surprising and architecture shows the least amount of ‘spread’ between its various sub-

disciplines. Approximately 70% of all architecture outputs are in the architecture and design

category, accounting for approximately £2.31 billion of fee income annually. 11% of

architectural fee income is generated by the provision of architectural technology services

(approximately £360 million) with other services being somewhat smaller.

4.3.2 Engineering

Engineering displays a relatively even spread of outputs between the various sub-disciplines

that make up this service category. The three largest fee-earning categories are structural

engineering (34% / £1.33 billion), building services (26% / £1.01 billion) and civil

engineering (18% / £700 million). Fire engineering and waste management engineering are

responsible for the smallest proportions of engineering related income, at 1.2% and 1.6%

respectively. Dedicated environmental and sustainability projects account for approximately

6% of engineering fee income (£230 million).

CIC-ConstructionSkills

12 Survey of UK Construction Professionals 2005/2006 - RePoRt

Survey of UK Construction Professionals 2005/06 - REPORT

Davis Langdon Management Consulting July 2007

13

4.3.3 Surveying

Quantity surveying accounts for almost half (46%) of all surveying outputs (approximately

£1.06 billion), followed by building surveying which accounts for over a third of all

surveying outputs, equating to £805 million of fee income. Other surveying service are

considerably smaller although surveying outputs dedicated to environmental or sustainability

projects exhibit the highest proportion amongst all of the core service categories.

4.3.4 Management and legal services

This is the broadest category, containing 13 sub-categories of management service. Eight of

these sub categories (which include risk, financial, quality control and environmental

management) do not exceed 4% of total fee income generated within this core service.

Project management (29%), contract administration (17%) and on site supervision (16%)

dominate the profile – being responsible for 63% of all management outputs (£1.05 billion).

4.3.5 Planning services

Planning services are dominated by the provision of planning applications, appeals and

inquiries output. These services account for 62% of planning fee income (approximately

£868 million). In addition, a significant proportion of planning income (15% / £210 million)

is generated in project feasibility.

4.3.6 Facilities management and other services

Overall, facilities management and related services generate the lowest proportion of fee

income in the CPS sector, accounting for £1.3 billion. Within this classification facilities

management (48%) and conservation (35%) provide the largest share of output.

CIC-ConstructionSkills

Survey of UK Construction Professionals 2005/2006 - RePoRt 13

Survey of UK Construction Professionals 2005/06 - REPORT

Davis Langdon Management Consulting July 2007

14

Figure 4.2: Breakdown of professional services provided by sub-discipline (%)

Engineering

0 5 10 15 20 25 30 35 40

Geotechnical

Structural

Fire

Highways

Civi l

Building services

Water management

Environmental

Waste management

Proportion of total engineering services %

Architecture

0 10 20 30 40 50 60 70 80

Urban design

Landscape

Architectural design

Space planning

Interior design

Environmental

Technology

Proportion of total architecture services %

Planning

0 10 20 30 40 50 60 70

Environmental studies

Urban/regional studies

Planning applications

Transport planning

Site appraisal

Project feasibility

Proportion of total planning services %

CIC-ConstructionSkills

14 Survey of UK Construction Professionals 2005/2006 - RePoRt

Survey of UK Construction Professionals 2005/06 - REPORT

Davis Langdon Management Consulting July 2007

15

Management

0 5 10 15 20 25 30 35

Strategic

Value engineering

Risk

Financial

Project

Quality control

CDM

Health & safety

Contract negotiation

Contract administration

On-site supervision

Environmental

Dispute resolution

Proportion of total management services %

FM & other

0 10 20 30 40 50 60

Facilities management

Property management

Research & development

Conservation

Proportion of total FM & other services %

Surveying

0 5 10 15 20 25 30 35 40 45 50

Land surveying

Quantity surveying

Building surveying

Environmental advice

Proportion of total surveying services %

CIC-ConstructionSkills

Survey of UK Construction Professionals 2005/2006 - RePoRt 15

Survey of UK Construction Professionals 2005/06 - REPORT

Davis Langdon Management Consulting July 2007

16

5 Type of work

5.1 Headline findings

Type of work

New work accounts for 62% of fee income - £8.7 billion

Refurbishment accounts for 32% of fee income - £4.4 billion

Repair and Maintenance (RMI) accounts for 6% of fee income - £0.8 billion

Residential accounts for 42% of CPS fee income - £5.8 billion

Building accounts for 43% of CPS fee income - £6.0 billion

Infrastructure accounts for 15% of CPS fee income - £2.1 billion

Private work accounts for 75% of CPS fee income - £10.5 billion

Public work accounts for 25% of CPS fee income - £3.4 billion

5.2 Overall breakdown

There are various ways in which the actual types of project on which CPS firms become

engaged can be broken down.

Typically these include:

breakdowns by new work, repair and refurbishment

breakdowns by public or private modes of procurement

broad classifications of work (such as those used in the DTI Housing and Construction

Statistics)

breakdowns by type of project.

All four of these classification types have been addressed in this survey and are described in

this section.

5.2.1 New work, repair and refurbishment

Figure 5.1: UK CPS Fee income by type of work (%)

New construction

62%

Refurbishment

32%

Repair & maintenance

6%

CIC-ConstructionSkills

16 Survey of UK Construction Professionals 2005/2006 - RePoRt

Survey of UK Construction Professionals 2005/06 - REPORT

Davis Langdon Management Consulting July 2007

17

Figure 5.1 shows that the profile of CPS firms is dominated by their inputs to new

construction, with approximately £8.7 billion (approximately 62%) being devoted to this

category. Repair, maintenance and improvement (RMI) accounts for only 6% of CPS fee

income, whilst refurbishment projects account for the remainder (32%). Collectively these

two categories generate just over £5 billion of income for the sector.

5.3 Sector of work (DTI Classifications)

When broken down by broad categories of work, the majority of CPS fee income is

generated in the following proportions.

Residential – 42%, or £5.8 billion

Building – 43%, or £6.0 billion

Infrastructure – 15%, or £2.1 billion

The classifications of work by type can also be considered in terms of their broad

procurement category. The breakdown of CPS inputs to Private or Public projects is as

follows:

Private – 75%, or £10.5 billion

Public – 25%, or £3.4 billion

5.4 Type of project

Within each broad type of work there are specific building or project types on which

professional services are employed. In residential projects this includes conventional housing

units (terraced, semi-detached and detached), refurbishments and the construction of purpose

built apartment blocks. The 2006 CPS survey asked respondents to provide details on the

specific types of building to which they provide services. The numbers of respondents in

each element of the analysis are not as high as in other areas of the survey. The results are

therefore not as statistically robust as those that have been presented elsewhere in this report

but we include them here, as we believe that they provide a useful indication as to the inputs

that the CPS sector provides to specific types of work.

5.4.1 CPS inputs to building projects

The data suggests that CPS firms provide the following inputs to various types of building

projects (as a proportion of all building work):

Offices 24%, or £1.45 billion

Retail outlets 12%, or £0.75 billion

Leisure facilities 11%, or £0.64 billion

Educational buildings 16%, or £0.96 billion

Healthcare facilities 9%, or £0.53 billion

Factories and warehouses 14%, or £0.82 billion

Other buildings 14%, or £0.85 billion

The majority of CPS fee income earned on building projects comes from services provided

in office construction, followed closely by fees earned on educational buildings and factories

and warehouses. The proportion of fees earned on other building projects is somewhat

smaller.

CIC-ConstructionSkills

Survey of UK Construction Professionals 2005/2006 - RePoRt 17

Survey of UK Construction Professionals 2005/06 - REPORT

Davis Langdon Management Consulting July 2007

18

5.4.2 CPS inputs to infrastructure projects

The professional inputs to infrastructure projects, as a proportion of all infrastructure work,

is described below:

Rail projects 10%, or £0.20 billion

Road projects 30%, or £0.64 billion

Port projects 2.1%, or £0.04 billion

Airports 6% or £0.13 billion

Energy projects 11% or £0.22 billion

Cable projects 5% or £0.11 billion

Water projects 22% or £0.46 billion

Other infrastructure 14% or £0.30 billion

The majority of CPS fee income earned on infrastructure projects comes from services

provided in road construction, followed by fees earned on water and sewerage projects. The

proportion of fees earned on other infrastructure projects is somewhat smaller.

CIC-ConstructionSkills

18 Survey of UK Construction Professionals 2005/2006 - RePoRt

Survey of UK Construction Professionals 2005/06 - REPORT

Davis Langdon Management Consulting July 2007

19

6 Regional and overseas profile of work

6.1 Headline findings

Level of fee income

A third of all CPS fee income is generated on projects in the South East and

Greater London

Other regions of note are the South West and Scotland

A greater proportion of fee income is earned on new build projects in the South East

and Greater London than any other regions in the UK

Overseas fee income

Overseas fee income of UK CPS firms (remitted back to offices in the UK) is

approximately £2.5 billion

6.2 UK Regions

Figure 6.1: UK CPS fee income by Government Office Region (%)

Firms have been asked to allocate their fee income to the regions where their relevant

projects were located, as opposed to the location of their corporate offices. The distribution

of this fee income is shown in Figure 6.1.

The largest proportion of UK professional fee income is earned on projects in the South East

and Greater London. We estimate the gross levels of fee income generated in each region of

the UK to be:

North East – £0.36 billion

Yorkshire & Humber - £0.69 billion

East Midlands - £0.83 billion

East of England - £0.33 billion

South East - £2.61 billion

North East

3% Yorkshire & Humber

5%

East Midlands

6%

East of England

7%

South East

20%

Greater London

13%

South West

10%

West Midlands

7%

North West

8%

Wales

4%

Scotland

10%

Northern Ireland

7%

CIC-ConstructionSkills

Survey of UK Construction Professionals 2005/2006 - RePoRt 19

Survey of UK Construction Professionals 2005/06 - REPORT

Davis Langdon Management Consulting July 2007

20

Greater London - £1.82 billion

South West - £1.43 billion

West Midlands - £1.02 billion

North West - £1.18 billion

Wales - £0.61 billion

Scotland - £1.45 billion

Northern Ireland – £0.97 billion

6.2.1 Breakdowns by region

Projects in Greater London and the rest of the South East are responsible for 33% of CPS fee

income. This is no surprise given that these two regions account for the bulk of the UK’s

population and in turn construction spending.

The regional pattern of fee income is broadly in line with contractor’s output in the same

period, in that a large proportion of all income is generated in Greater London and the South

East. Indeed, contractors output in these regions accounted for 33% of all work in 2005.

Other regions of note, where CPS output exceeds £1 billion, are Scotland, the South West

and the North West of England.

6.3 Overseas Fee Income

6.3.1 Profile of overseas fee income

When the figures are grossed up, using a similar methodology to that used in the estimate of

UK fee income, overseas fee income is estimated to be approximately £2.5 billion. This

represents approximately 15% of total fee income of UK CPS firms, a similar proportion to

that reported in the 1995/96 survey but significantly higher than that reported in the 2001/02

survey.

However, the data presented above has to be interpreted carefully, as the survey returns only

reflect fee income that has been remitted back to offices in the UK. Furthermore, we believe

that:

information on overseas fee income could have been very difficult to obtain for many

respondents.

there are significant problems in finding a suitable coefficient for fee income inflation

when comparing 2005, 2002 and 1996 overseas fee income levels.

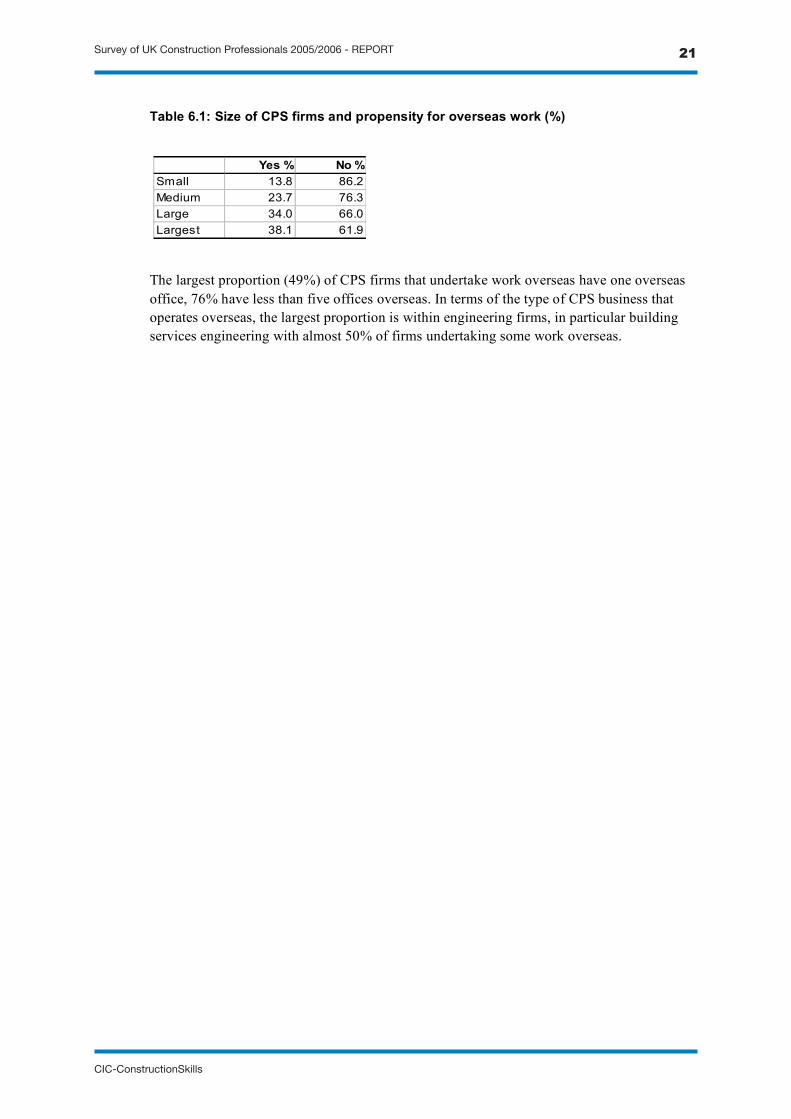

6.3.2 Profile of overseas fee income by type of firm and service

Table 6.1 below indicates that even the smallest CPS firms undertake some work overseas,

as would be expected there appears to be a very strong relationship between the size of firm

and the propensity to work overseas.

CIC-ConstructionSkills

20 Survey of UK Construction Professionals 2005/2006 - RePoRt

Survey of UK Construction Professionals 2005/06 - REPORT

Davis Langdon Management Consulting July 2007

21

Table 6.1: Size of CPS firms and propensity for overseas work (%)

The largest proportion (49%) of CPS firms that undertake work overseas have one overseas

office, 76% have less than five offices overseas. In terms of the type of CPS business that

operates overseas, the largest proportion is within engineering firms, in particular building

services engineering with almost 50% of firms undertaking some work overseas.

Yes % No %

Small 13.8 86.2

Medium 23.7 76.3

Large 34.0 66.0

Largest 38.1 61.9

CIC-ConstructionSkills

Survey of UK Construction Professionals 2005/2006 - RePoRt 21

Survey of UK Construction Professionals 2005/06 - REPORT

Davis Langdon Management Consulting July 2007

22

7 Employment

7.1 Headline findings

Profile of employment

The CPS sector employs approximately 270,000 employees

77% of all employment in the sector is male

Engineering firms generate 15% of income and employ 17% of all staff

Architectural firms generate 11% of income and employ 14% of all staff

Surveying firms generate 15% of income and employ 16% of all staff

Multi-disciplinary firms generate 48% of income and employ 41 % of all staff

Professional per capita fee income rises steadily by size of firm

7.2 Employment profile

The total number of staff permanently employed by UK CPS firms in the UK, excluding sub-

contractors is estimated at approximately 270,000.

Figure 7.1: Profile of professional employment by CPS discipline (%)

Architects

7% Architectural technologists

4%

Building services engineers

9%

Civil engineers

17%

Other engineers

12%

Technicians

7%

Building surveyors

2%

Quantity surveyors

7%

Scientists

2%

Business managers

6%

Contract & project managers

6%

Administrators

12%

Legal/business professionals

1%

Other construction

professionals

6%

Tow n planning professionals

2%

CIC-ConstructionSkills

22 Survey of UK Construction Professionals 2005/2006 - RePoRt

Survey of UK Construction Professionals 2005/06 - REPORT

Davis Langdon Management Consulting July 2007

23

Figure 7.1 above indicates the professional staff profile of CPS firms in the UK. Engineering

staff dominate CPS employment in the UK and account for 38% of professional

employment. Civil engineers exhibit the largest proportion (17%) which represents

approximately 45,000 fully qualified professional members of staff. Other engineers (i.e.

structural) are the next largest category representing almost 30,000 members of staff.

7.3 Breakdown by type and size of business

7.3.1 Male and female employment

We estimate that of the total number of UK staff employed by CPS firms in the 2005/06

survey 77% are male. The dominance of males within each profession means that the

proportion of male/female employment is relatively constant within each of the professions.

The data show an exceptionally high proportion of male employment generally, which in

most types of firm and discipline is not dissimilar to the rest of the construction sector.

Employment in contracting is currently approximately 90% male (according to the most

recent Labour Force Survey estimates) and within the construction operative trades male

employment is currently above 95%.

7.3.2 Profile of employment by type and size of firm

The profile of total employment, by firm’s main activity, is estimated to be in the proportions

indicated in Figure 7.2.

Figure 7.2: Profile of employment by CPS firms main activity (%)

Architecture

14%

Engineering

17%

Surveying

16%

Multi-disciplinary

41%

Management

5%

Planning

3%

FM & other

4%

CIC-ConstructionSkills

Survey of UK Construction Professionals 2005/2006 - RePoRt 23

Survey of UK Construction Professionals 2005/06 - REPORT

Davis Langdon Management Consulting July 2007

24

Figure 7.2 indicates that multi-disciplinary firms employ the highest proportion of

professional staff as would be expected given their share of total output. 80% of all

professional employment is in the largest firms, which earn more than £10 million per

annum.

7.4 Per capita fee income

Overall, we estimate that the average per-capita fee income of the CPS industry in 2005/06 is

in the region of £51,500. However, as would be expected this measure varies with the size

and type of firm. Data in Figure 7.3 indicates that the mean per capita fee income in the

smallest firms (fee income less than £200,000 pa), is some £65,411. Generally fee income

per capita increases with the size of firm measured in terms of fee income.

The overall profile of per capita fee income per professional is at its highest in engineering

and multi-disciplinary practices. There is a level of consistency in the per capita fee income

profile of these main types of firm, with the exception of architects and surveying practices,

who appear to earn significantly less than the other disciplines, per member of staff, in the

larger firms and practices.

Figure 7.3: CPS Per-capita fee income by type and size of firm (£)

0

200000

400000

600000

800000

1000000

1200000

1400000

Small Medium Large Largest

Pe

rc

ap

ita

fee

inc

om

e-

pe

rma

ne

nt

sta

ff(£

)

Architecture

Engineering

Surveying

Multi-disciplinary

CIC-ConstructionSkills

24 Survey of UK Construction Professionals 2005/2006 - RePoRt

Survey of UK Construction Professionals 2005/06 - REPORT

Davis Langdon Management Consulting July 2007

25

8 Headline changes since 2002

8.1 Headline findings

Fee income, growth and performance

CPS fee income has risen by 4% in real terms since 2001/02

Rate of income growth is below that of contractors output for the same period

Growth in the professional services has been consistent since 2002

Services provided

There has been very little change in the overall proportion of services provided by the

CPS sector

The proportion of work undertaken by multi-disciplinary firms has increased and now

accounts for almost one half of total CPS output

The overall profile of output by broad size of firm has changed little but there has been a

substantial rise in the amount of output generated by the largest firms

Type of work

Fee income on new work has increased by 3%, whilst fee income earned on RMI work

has decreased by the same amount as a proportion of all work

Residential projects have seen the largest rise and now account for 42% of all fee income

Offices have seen substantial growth in non-residential building projects

Roads have seen substantial growth in infrastructure projects

Employment

Per capita fee income has decreased by approximately 13% in real terms since the last

survey

The proportion of male to female staff has not improved significantly since the

2001/02 survey, although the results indicate a consistent increase in the numbers of

female staff in the CPS sector

8.2 Fee income

8.2.1 Headline changes

We estimate that output of the construction professional sector has risen by approximately

4% in real terms since 2001/02, from £13.4 billion to £13.9 billion.

Our estimates of fee income are based on a total population of 27,950 CPS firms, compared

to our estimate of approximately 23,500 firms in the 2001/02 survey (refer to notes on

population size below). At the time of the last survey we estimated CPS output to be 18% of

UK contractors output. This proportion has remained constant at 18% in 2005/06. The level

of growth in fee income (+4%) is below growth in contractors output, as reported in the

DTI’s Construction Statistics Annual (2007). This has increased by approximately 13% in

the same period.

However, it is consistent with the overall growth in output from firms that are in the same

peer group and whose output is measured by the ONS (Office of National Statistics) as part

CIC-ConstructionSkills

Survey of UK Construction Professionals 2005/2006 - RePoRt 25

Survey of UK Construction Professionals 2005/06 - REPORT

Davis Langdon Management Consulting July 2007

26

of the Real Estate and Associated Business Services sector - Section K of the Annual

Business Inquiry (ABI).

8.2.2 Key factors in the interpretation of results

Estimates of the change in absolute levels of fee income in the CPS sector are inherently

difficult to make and caution should be taken when interpreting the results. For example,

such estimates are not as reliable as measuring the relative changes between specific

variables in the surveys, such as breakdowns of service provision or employment.

However, we are confident that the overall magnitude of the increase is correct and that it

represents some improvement in the growth of fee income since the time of the last survey.

Difficulties in making such comparisons arise because of:

the lack of reliable and longitudinal data on the performance of the CPS sector in the

intervening period

the different populations that have been used as a basis for the surveys

difficulties in finding and applying an appropriate measure of fee income inflation.

In addressing these three fundamental issues we have firstly used the ‘All industries implied

deflator for Gross Domestic Product’ at market prices to inflate the estimates of UK fee

income of CPS firms from the 1995/96 and 2001/02 surveys to 2005 prices. There are no

definitive statistics for the actual inflation of professional fees during this period, but we

believe that the all industries implied deflator is the most reliable when compared to other

available measures such as the Tender Price Index which is not wholly relevant to

professional services.

Secondly, we estimate that at least 10% of the firms who have been surveyed in 2006 would

not have been included in the 1995/96 population or sample because of the wider and more

selective sampling processes that have been employed since that survey. An adjustment has

therefore been made to further inflate the 1995/96 estimates to account for the output of

firms that would not have been included in that survey.

Finally, we have referenced data supplied by the ONS on the output and employment of

firms within Section K of the ABI to ensure that our methodology does not produce results

that could not possibly be supported in robust observations of the wider economy.

8.3 Trends in construction and professional activity

There is no specific data on the output of the CPS sector since the time of the last survey.

However, it is useful to review the trend in outputs and employment for the wider

construction sector, as it may be assumed that trends in the development of the CPS sector

will have shared much in common with the wider construction economy.

Construction output has grown by 11% in real terms between 2001 and 2005, and by 43% in

current prices. After the recession of the early 1990s, when construction output reached it

lowest point in 1993, it rose in 1994, but fell back slightly in 1995. Thus the 1995/96 survey

took place at a point that is now considered to be the start of the last growth cycle in

construction which peaked in 2004. Indeed, 2005 saw the first decline in construction output

for a decade. Thus the 2001/02 survey took place during a period of sustained growth, while

the most recent survey has been undertaken during a period of a decline in construction

output. This trend can be seen in Figure 8.1 below.

CIC-ConstructionSkills

26 Survey of UK Construction Professionals 2005/2006 - RePoRt

Survey of UK Construction Professionals 2005/06 - REPORT

Davis Langdon Management Consulting July 2007

27

Whilst we have no data on the specific outputs of the CPS sector since the last survey it

would appear that these changes in the profile of construction output are reflected in the

results that have been presented earlier in Section 6 (and later in this section).

Figure 8.1: Construction output trends between the surveys (DTI, 2007)

Not surprisingly, the growth in construction output has led to increasing employment in the

industry, which has risen from 1.38 million in October 1996, to 1.63 million in July 2002

(+18%), to 1.81 million in December 2005, an increase of 11% between 2001 and 2005 (DTI

manpower series). Similar employment increases are evident in the CPS industry, from

approximately 180,000 in 1996 to an estimated 225,000 in 2002 (+25%) to 270,000 in 2005

(+20%).

Whilst it has not been possible to obtain specific data on the CPS sector in the intervening

year’s, data does exist on the trends associated with the wider sector of economic activity in

which CPS output is generally measured. Again this data can be found in Section K of the

ABI.

Growth in this sector of the UK economy has been consistently strong since the time of the

last survey and net output is estimated to have grown by approximately 31% (in current

prices) during the period. However, this figure is considerable lower than that recorded

between the 1996 and 2001 surveys where growth of 74% was evident. ‘Architecture,

engineering and associated technical consultancy’ (a sub set of Section K - SIC 74.2) has

seen similar growth (+30%) during the intervening years. It is assumed that the trends shown

in Figures 8.2 and 8.3 below are largely representative of those that will have taken place in

the CPS sector during the period between the three surveys.

20000

30000

40000

50000

60000

70000

80000

90000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

£m

illi

on

(co

ns

tan

t2

00

0p

ric

es

)

New orders

New work

Total output

CIC-ConstructionSkills

Survey of UK Construction Professionals 2005/2006 - RePoRt 27

Survey of UK Construction Professionals 2005/06 - REPORT

Davis Langdon Management Consulting July 2007

28

Figure 8.2 and Figure 8.3: SIC 74.2 - Trends in the value-added and no. of firms

between the surveys (ONS, 2007)

Approximate gross value added for this sector of the economy dipped in 2001, at a similar

time that construction orders for new buildings went into temporary decline. CPS firms’

income is likely to track orders (particularly for new build and major refurbishment) more

closely than construction output as this is the point in the cycle at which their inputs are

likely to be more intense. Interestingly, this was preceded by a decrease in the number of

firms within the sector in 2000.

However, it is impossible to determine how much of this growth was attributable to CPS

specific firms. Whilst the available ONS data ends at the end of 2005 we believe that the

6000

8000

10000

12000

14000

16000

18000

20000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Gro

ss

va

lue

-ad

de

d(£

mil

lio

n)

46000

48000

50000

52000

54000

56000

58000

60000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

No

.o

ffi

rms

CIC-ConstructionSkills

28 Survey of UK Construction Professionals 2005/2006 - RePoRt

Survey of UK Construction Professionals 2005/06 - REPORT

Davis Langdon Management Consulting July 2007

29

trend in output growth and number of firms has continued to exhibit modest growth up to the

end of the current survey. We also believe that the trends shown in Figures 8.1 (particularly

for new orders), 8.2 and 8.3 have been partially mirrored in the CPS sector itself.

Looking to the future, growth in construction output during 2006 is expected to have

increased slightly over 2005, but we expect 2007 to be slightly more upbeat as some of the

work on major projects in the pipeline, such as the Olympics, begins to come on stream.

Infrastructure output fell steeply for the third year running in 2006 and the sector has shrunk

by nearly 30% since 2002 largely as a result of investment in other sectors, mainly health

and education construction. All the indications are, however, that the sector is likely to turn

around over the next few years, with growth across the sub-sectors expected. Indeed work

directly related to the Olympics is already beginning to build up.

In terms of public construction, there is evidence that public spending is being reigned in,

particularly in the health sector where significant overspend at a number of Health Trusts

may mean that capital expenditure on health facilities could be particularly vulnerable.

The residential sector continues to perform reasonably well and until supply matches demand

the sector is expected to continue growing at a healthy rate. Activity is likely to be driven by

the provision of more affordable and key worker housing. Industrial construction continues

to perform surprisingly well considering the relative weakness of the manufacturing sector.

The primary growth in recent years has been in the provision of distribution warehouses

rather than factories.

8.4 Improvements in the performance and productivity of the CPS sector

Measuring the productivity improvement of an industrial sector, or making comparison with

similar sectors in other countries is a complex issue and this survey is limited in what can be

said directly in relation to the overall productivity of the sector. The only measures that have

been collected within the survey are fee income and employment data (which have been

presented earlier in Section 7). Productivity can only be sensibly considered when quality of

outcomes, utilisation of time and other factors are also taken into account.

Whilst this survey is not therefore a suitable vehicle for making accurate statements about

productivity in the CPS sector, there are some limited indications that the sector has

witnessed some decline and change since the last survey. Some of these are contained in

Section 8.2 above, with limited growth being seen in the overall construction economy and

the professional services sector more generally. The data also suggests that there has been a

significant decline in per capita fee income between the three surveys (approximately 13% in

real terms between the 2005 and 2002 surveys and 16% in the ten years since the original

survey in 1996).

There are obviously problems of interpretation when data is only considered at three

particular points in time, as the points at which measurements are taken within the

construction cycle, or the general economic cycle, is an important consideration. This is

particularly important in construction, where the domestic market in the UK can vary

considerably from times of high demand to times when the market suffers from a widespread

lack of work.

CIC-ConstructionSkills

Survey of UK Construction Professionals 2005/2006 - RePoRt 29

Survey of UK Construction Professionals 2005/06 - REPORT

Davis Langdon Management Consulting July 2007

30

However, the data suggests that average per capita fee income in the CPS sector stood at

£51,500 in 2005/06. This compares favourably with the productivity measures available in

the ABI, where output per employee (i.e Gross value-added per person employed) in SIC

74.2 was some £50,600 in 2005.

8.5 Services provided

Table 8.4 shows that there has been some change in the proportions of the core services that

are delivered by CPS firms in 2005/06, when compared to 2001/02 and 1995/96. A summary

of the changes suggests that engineering services account for a slightly smaller share than in

1995/96, while architecture services account for a slightly larger share. Surveying and

planning services remain relatively consistent, while management services have seen some

decline and FM and other services have increased their share throughout the period.

However, there have been some significant changes in the types of firm that deliver these

services and an indication of this is shown in Table 8.5. Unfortunately we did not ask firms

to describe the nature of their own business in the 1995/96 survey, therefore the results

presented are for the most recent results and the survey conducted in 2001/02.

Table 8.4: Changes in CPS fee income earned by services provided (%)

Table 8.5: Changes in CPS fee income earned by types of firm (%)

A key finding of this survey is that the proportion of work that is being undertaken by firms

that describe themselves as multi-disciplinary has increased and now accounts for almost one

half of total fee income.

However, the largest increase in fee income has arisen in firms that describe themselves as

surveyors which have seen the proportion of fee income earned double since the time of the

last survey. The proportion of fee income earned by engineers and planners has remained

1995/96 2001/02 2005/06

Surveying 18 16 17

Planning 8 6 10

Management 16 19 12

FM & other 5 7 9

Architecture 21 22 24

Engineering 32 30 28

Total 100 100 100

2001/02 2005/06

Surveyors 7.0 14.5